Thanks for Reading

Thanks for reading today and all week.

I hope my body of work has been helpful.

I have a date with a two-year-old and Peppa the pig.

Enjoy the weekend.

Be safe.

BY Doug Kass · Aug 15, 2025, 3:47 PM EDT

Thanks for reading today and all week.

I hope my body of work has been helpful.

I have a date with a two-year-old and Peppa the pig.

Enjoy the weekend.

Be safe.

BY Doug Kass · Aug 15, 2025, 3:47 PM EDT

From Peter Boockvar:

Succinct Summation of the Week's Events:

Positives,

1) Initial jobless claims totaled 224k vs 227k in the week before and about as expected. The 4 week average was little changed at 222k vs 221k in the week before. Off the cycle high, continuing claims fell to 1.953mm from 1.968mm.

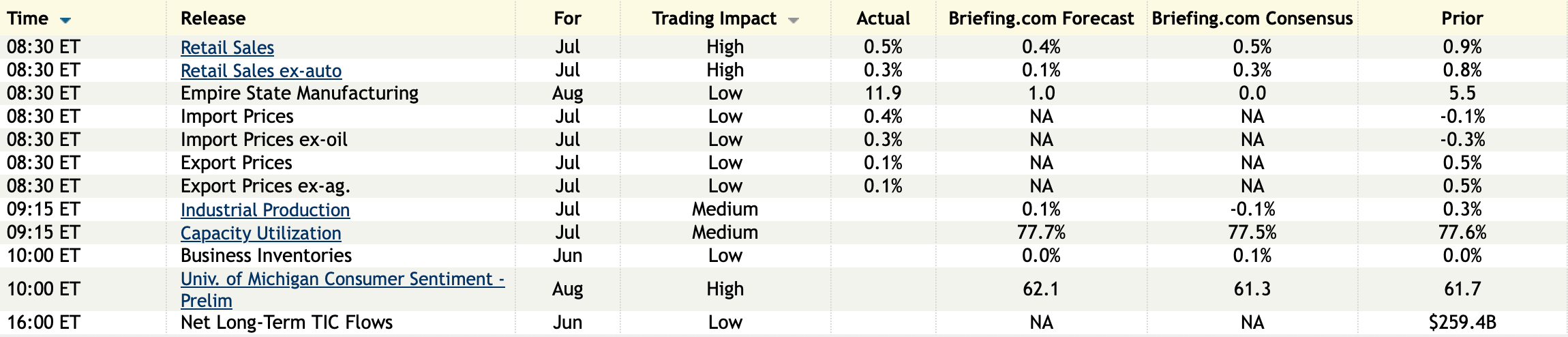

2) Core retail sales in July rose .5% m/o/m, one tenth more than expected and June was revised up by 3 tenths to an .8% gain. Above the core, auto sales rose 1.6% m/o/m while building materials fell by 1.3%.

3) July import prices which DO NOT include the tariffs, were about as expected when we include the June revisions. Headline import prices rose .4% m/o/m after two months of declines and are flattish y/o/y. Ex food and fuels saw import prices higher by .3% m/o/m after a one tenth drop in June, no change in May and a .4% rise in April. They are up .8% y/o/y.

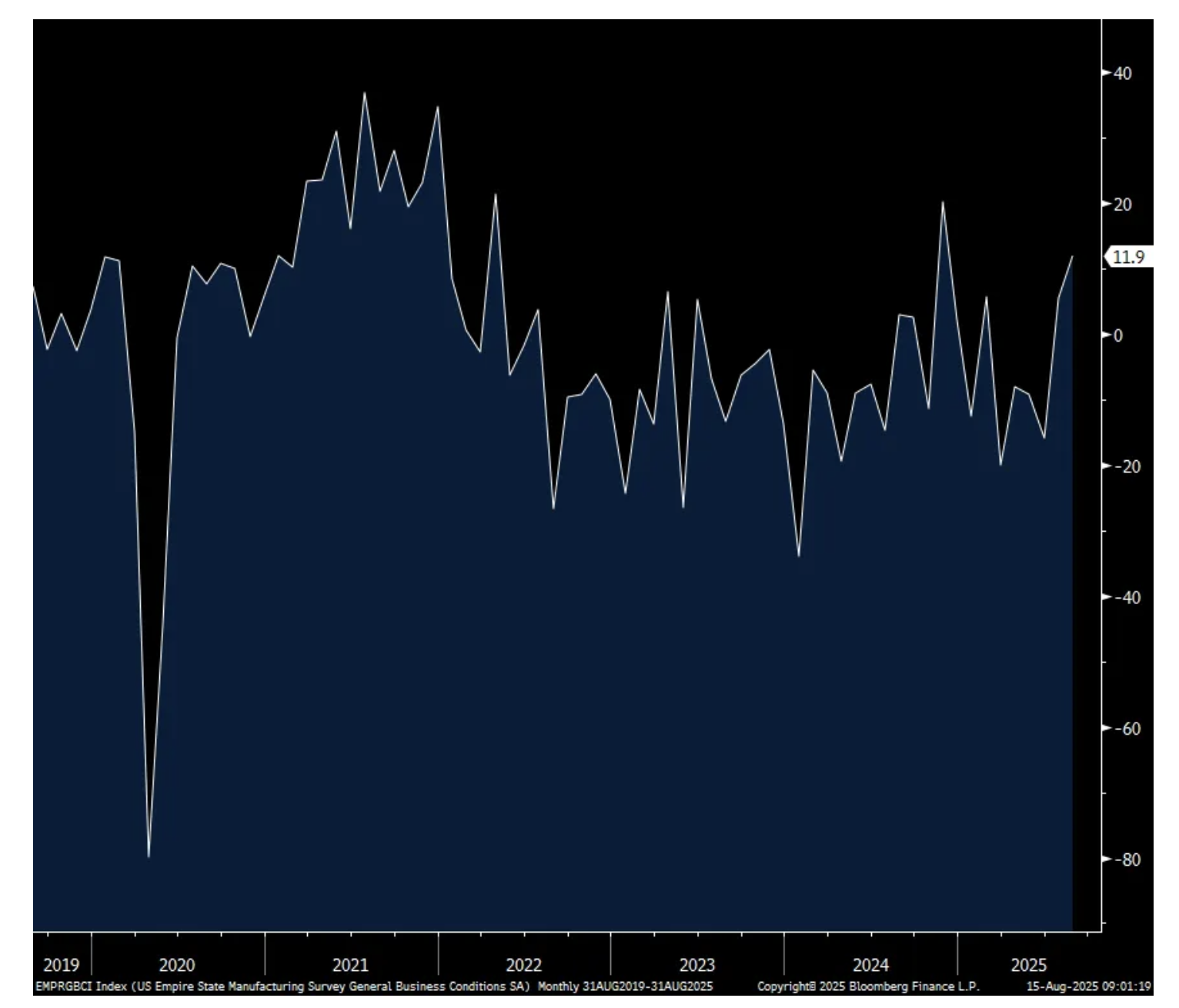

4) The August NY manufacturing index was above zero for a 2nd month at 11.9 vs the estimate of zero.

5) With the 10 bps w/o/w drop in mortgage rates to 6.67% on average for a 30 yr, the benefit mostly accrued to those looking to refi as refi's jumped 23% w/o/w while purchases were higher by just 1.4%.

6) The July NFIB Small Business Optimism Index did improve to 100.3 from 98.6 and that is the best since February. The NFIB's bottom line was this, "Optimism rose slightly in July with owners reporting more positive expectations on business conditions and expansion opportunities. While uncertainty is still high, the next six months will hopefully offer business owners more clarity, especially as owners see the results of Congress making the 20% Small Business Deduction permanent and the final shape of trade policy. Meanwhile, the labor quality has become the top issue on Main Street again."

7) July US industrial production was as expected with the June revision. The manufacturing component was a bit better.

8) From ZipRecruiter: "While the broader labor market remains soft, ZipRecruiter continues to see early signs of momentum." They've seen quarterly paid employers or QPEs rise sequentially since Q4 2024.” But the caveat, "That is not to say that the labor market is rebounding. That is to say that it is stabilizing." And what's the impact on the jobs market from AI? "If you look at the category that would be most likely impacted by AI, you'd look at technology. It's the one that's had the most headlines. It's the one that's had the most discussion. And that was down 5% y/o/y on a job posting basis... And if you look at that down 5% that puts it squarely in the category of ordinary, meaning that if you look at the broad spectrum of job categories, what you see is that makes it a very average decline, putting it nearly effectively the median, which means so far both quantitatively and qualitatively, we're not seeing significant disruption and/or impact from AI in terms of the number of jobs being posted."

9) From Birkenstock: "Our demand is strong across all product categories and target groups… In the Americas, revenue was up 16% in constant currency, with both the B2B and D2C channels growing double digits... Importantly, we saw no pushback or cancellations following the July 1st price increases implemented in response to tariffs.” As their shoes are in high demand, "we don't see any slowdown in consumer demand or anything. We are at the moment struggling with capacity. That's our biggest issue."

10) From Ralph Lauren: "Our strong first quarter results were once again broad based, driven by every geography and channel. We delivered double digit top line growth in both Asia and Europe and high single digit growth in North America with global comps up 13%."

11) From Advance Auto Parts: Comps were flat for the quarter "and our performance was driven by strength in the Pro business, which continued to deliver positive comp growth. In our DIY business, we are encouraged by emerging signs of stabilization as comparable sales were consistent with Q1 and improved on a two year basis. Notably, we concluded the quarter on a strong note with both Pro and DIY delivering positive results, and this momentum has continued into the first four weeks of Q3."

12) From Madison Square Garden Entertainment: "While we're certainly keeping an eye on the macro environment, we continue to see strong consumer demand. A number of factors that support this view is we are seeing strong demands for the Christmas Spectacular 2025 holiday run. And our advanced tickets are pacing well ahead of last year at this time."

13) From Madison Square Garden Sports: "Driven by sustained consumer and corporate demand for the Knicks and Rangers, we saw increases in key in-game revenue categories, including ticketing, sponsorship and suites… This past regular season, both combined average ticket yield and average paid attendance were up, which helped drive growth in ticketing revenue. And the upcoming 2025-'26 seasons, the average combined season ticket renewal rate is currently at approximately 90%."

14) From Sphere Entertainment: Coming soon is The Wizard of Oz at Sphere and "we have sold over 120,000 tickets to date and expect to reach 200,000 by the opening later this month… We're also seeing increasing demand from artists across a variety of genres, which are driving renewed interest in their music by playing Sphere in Las Vegas. We have continued to add shows to our calendar and now expect to host more than 100 concerts this year, up from 70 in 2024."

15) From Live Nation: "Global expansion continues to drive touring growth, with fan attendance hitting new highs and ticket buying strong at every price point from VIP to the back row… Over 130 million tickets sold for Live Nation concerts, up 6%, led by the strength of our international markets with double digit attendance increases across stadiums, arenas, and theaters and clubs.” Also, "Strong ticket sales at every price point from premium to budget friendly seats: Over 40% of global stadium shows sold out 95% of tickets in the first week, up double digits. Over 10% of seats across stadiums, arenas, and amphitheaters in the US priced closer to market value. Ticket to Summer promotion sold 1.5 million $30 lawn seats, consistent with historical levels… Continued growth in onsite spending across all venue types, including concession spending at large amphitheaters up double-digits."

16) From Brinker: Chili’s continues to be a casual dining standout. Their comps jumped 24% y/o/y, "outperforming a stronger casual dining industry by 1,890 bps… So we're still growing all income levels, so that's the good news. We saw growth in low, medium, and high, especially when we have traffic numbers like we've had... And so far as frequency goes, what I will tell you is we've had a huge influx, obviously, of new and lapsed users, and our frequency is actually staying flat." Their Maggiano's brand saw just a mediocre quarter with comps down .4% y/o/y.

17) From Restaurant Brands: "While the consumer environment remains dynamic, we've seen encouraging signs of improvement across many of our largest businesses." But, "Beef is about 25% of our cost basket and we're seeing around 15% inflation on the year to date."

18) From Texas Roadhouse: "Strong traffic growth throughout the quarter drove a 5.8% increase in same store sales.... driven by 4% traffic growth and a 1.8% increase in average check."

19) From Hapag-Lloyd: "Looking at the market, I'd say that the US trade policies have certainly caused a fair bit of volatility, both in demand and also in short term pricing... What I would say though that in the end, the first half was probably a bit better than many people feared."

20) From ON Holdings: "We saw strength across every region, channel and product category."

21) From CDW: "In a dynamic and complex environment, the team delivered double digit top line growth, even as federal and education markets faced evolving headwinds… Once again, healthcare was a standout performer with net sales up 24% as we continue to help our customers address clinical continuity… Consistent with recent trends, commercial customers prioritized mission critical hardware investments that could not be postponed, and public customers dealt with shifts in government priorities and funding."

22) From Expedia: "The US travel market was muted in the second quarter. Consumers at the higher end of the market remained resilient with those at the lower end taking a more cautious approach to discretionary spending. That said, since the beginning of July, we've seen an uptick in overall travel demand, particularly in the US."

23) The UK economy in Q2 grew by .3% q/o/q and 1.2% y/o/y which were both 2 tenths above expectations. More government spending helped as did trade. Consumer spending was about as expected.

24) The UK saw another drop in July payrolls but not as much as expected and June was revised up to less of a negative. Also, jobless claims were down in July. Through June, their unemployment rate held at 4.7% which is the highest since 2021. Wage growth continued to be solid, rising 5% y/o/y ex bonus, as expected and above the rate of inflation.

25) Both the BoT and RBA cut rates as expected.

Negatives,

1) The July CPI rose .2% headline and .3% core m/o/m as expected. Versus last year the y/o/y gains were 2.7% and 3.1% (estimate was 3%) respectively vs 2.7% and 2.9% in the month before. Services inflation ex energy were up .4% m/o/m and 3.6% y/o/y. Core goods prices rose .2% m/o/m for the 2nd month and are now up 1.2%, the highest since June 2023.

2) The July PPI jumped by .9% m/o/m, well above the estimate of up .2%. The core rate was higher by .9% too vs the forecast of up .2%. The y/o/y increases are now 3.3% and 3.7% respectively and vs 2.3% and 2.6% in the month before. Headline goods prices were up .7% m/o/m and core goods prices rose .4% m/o/m vs a .2% gain in June and .3% increases in the 3 months prior and is now up 2.8% y/o/y. Services prices accelerated to a 1.1% increase in the month from June with trade jumping by 2% and transportation/warehousing costs higher by 1%. Services wholesale prices are now up 4% y/o/y. The BLS said “30% of the July rise in prices for final demand services can be traced to margins for machinery and equipment wholesaling, which jumped 3.8%.”

3)The preliminary July UoM consumer confidence index fell to 58.6 from 61.7 and that was below the estimate of a slight gain to 62. For reference, this was at 102 in February 2020. Almost all of the drop was in the Current Conditions component which dropped 7 pts while Expectations were lower by .5 pt. One year inflation expectations jumped to 4.9% from 4.5% while those guessing on the 5-10 view rose to 3.9% from 3.4%. This even though less people think that gas prices are going higher. Also, “The increase was seen across multiple demographic groups and all three political affiliations.” In addition to inflation, also weighing on confidence are concerns about the labor market as those expecting ‘more’ unemployment rose 5 pts to a 3 month high. The net income component was zero with the same amount of people seeing a rise in income vs those seeing lower income. Spending intentions worsened with plans to buy a home, a vehicle and a major household item all declining. The bottom line from the UoM, “This deterioration largely stems from rising worries about inflation… Overall, consumers are no longer bracing for the worst-case scenario for the economy feared in April when reciprocal tariffs were announced and then paused. However, consumers continue to expect both inflation and unemployment to deteriorate in the future.”

BY Doug Kass · Aug 15, 2025, 3:32 PM EDT

Back short PLTR, ARKK, HOOD and NVDA.

BY Doug Kass · Aug 15, 2025, 3:05 PM EDT

Recommended Reading

"Decoding Palantir, the Most Mysterious Company in Silicon Valley," WIRED

BY Doug Kass · Aug 15, 2025, 2:59 PM EDT

As of 2:30 p.m. ET:

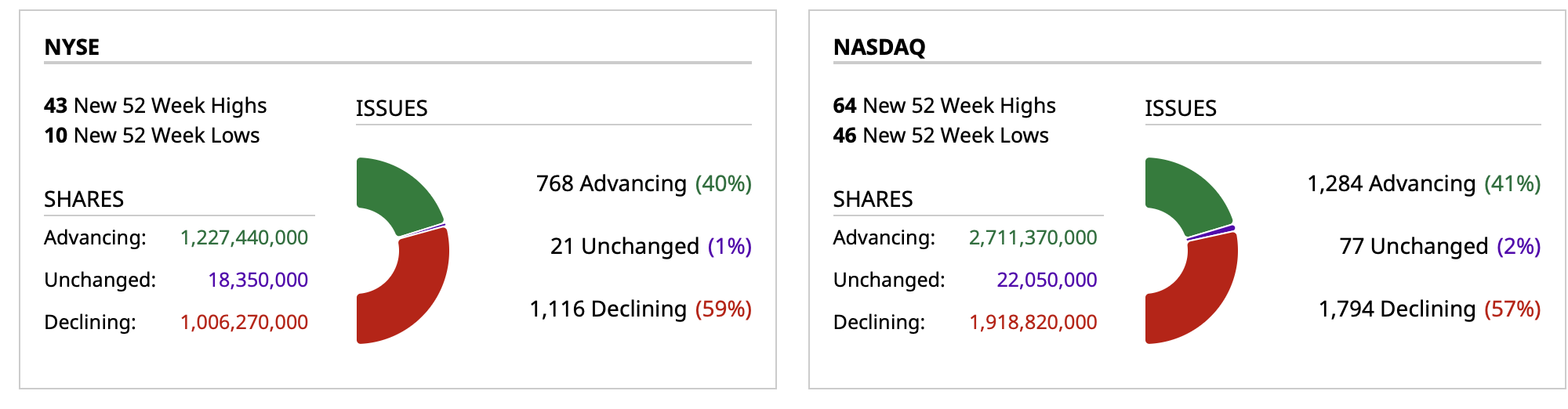

Breadth

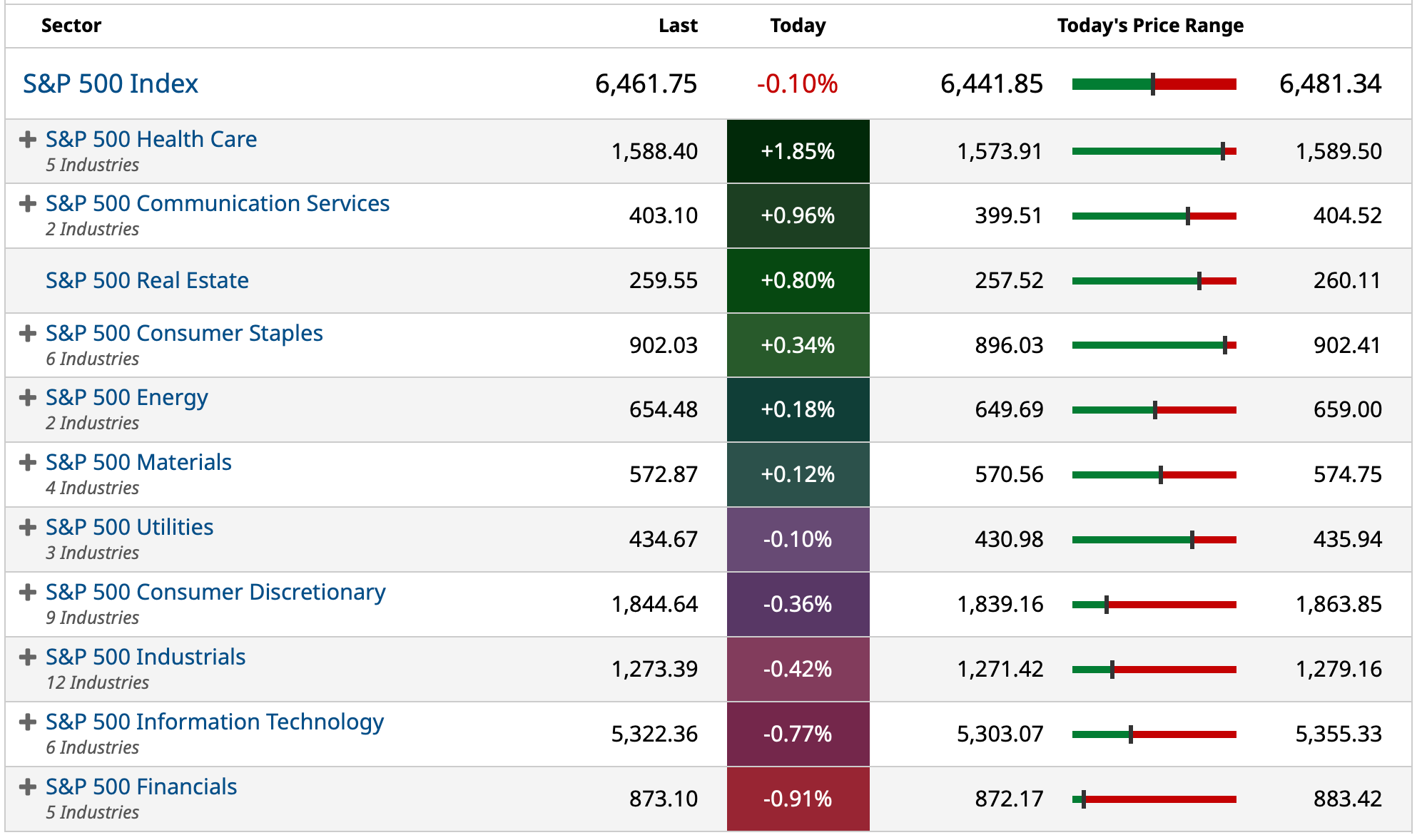

Sectors

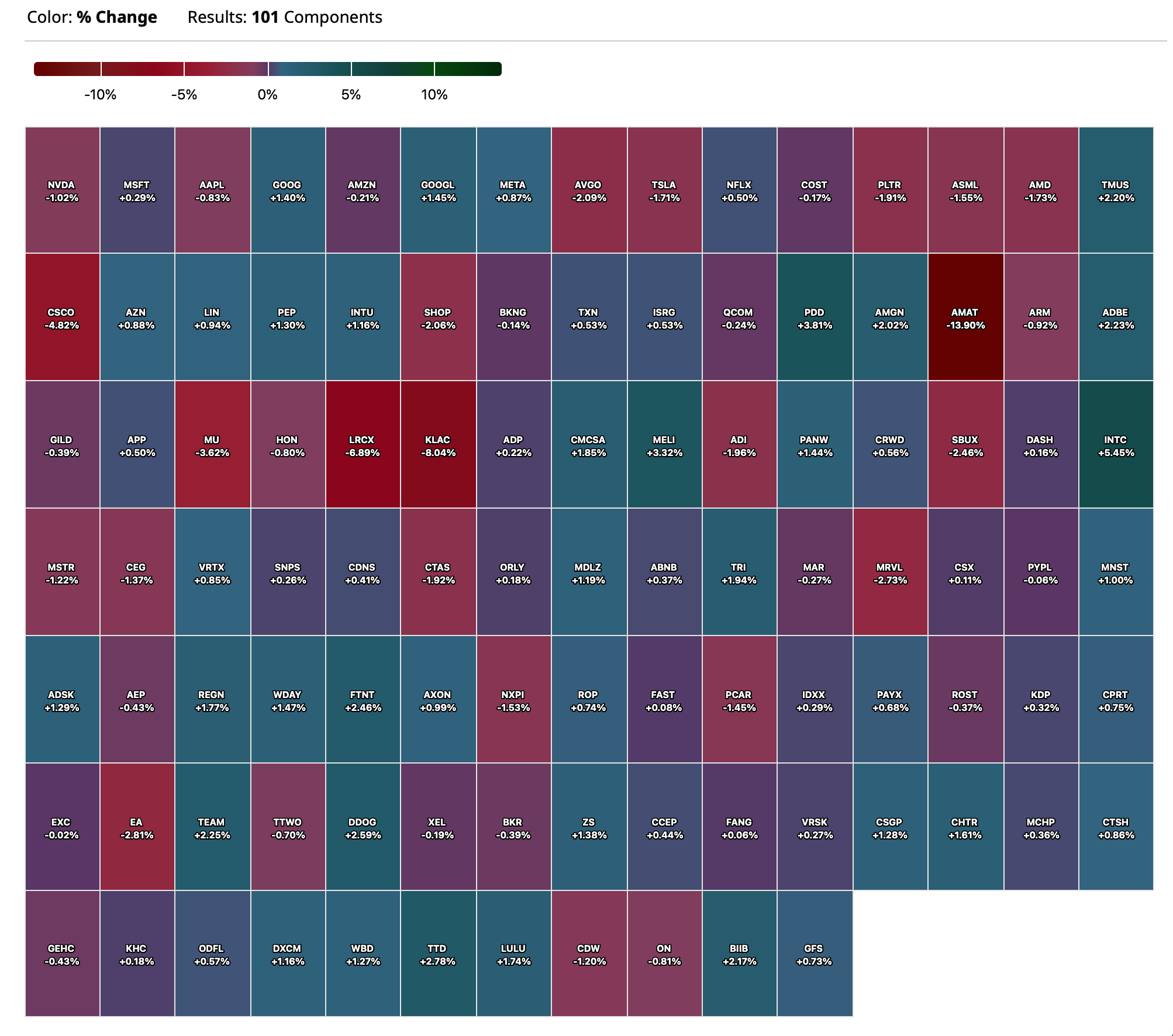

Nasdaq 100 Heat Map

BY Doug Kass · Aug 15, 2025, 2:36 PM EDT

I have moved to VS long UNH at $309.

With S&P cash rallying from the lows and now -7 handles I am adding to my Index shorts:

* SPY $644.50

* QQQ $577.88

BY Doug Kass · Aug 15, 2025, 2:16 PM EDT

To put how unimportant the UnitedHealth UNH purchase was for Berkshire Hathaway — at $1.5 billion the UNH holdings represent the conglomerate's nineteenth largest position!

BY Doug Kass · Aug 15, 2025, 1:28 PM EDT

From Charlie!

BY Doug Kass · Aug 15, 2025, 1:00 PM EDT

BY Doug Kass · Aug 15, 2025, 12:24 PM EDT

* But I will only "criticize by category and praise by individual" (h/t Warren Buffett)

* An appearance on FinTV may have already top ticked the momentum stocks...

"The whole problem with the world is that fools and fanatics are always so certain of themselves and wiser people so full of doubts."

-Bertrand Russell

I am often wrong and always in doubt.

My mantra is that we should not be overly confident as we still have to count the votes!

As I have consistently written over the years, this is too often not the case for uber confident "talking heads" in the business media who are trying to improve their brands, sell a service or gain money management assets.

That said, I am increasingly convinced that my observations in "Watching In Amazement" (Parts One and Two) will prove insightful:

Aug 13, 2025 1:10 PM EDT

The panelist I mentioned this week might have top ticked the momentum index with his buys yesterday

Long UNH (S)

Aug 12, 2025 2:43 PM EDT

I had CNBC's "Halftime Report" on today and I listened to a panelist (praise by individual, criticize by category — so no names!) who confidently added AVGO, NVDA and GS to his portfolio this afternoon.

Please look at the price charts of those companies before you read further!

While I recognize that my market view has been half baked for quite a while and having been mentored at Putnam by one of the great momentum traders in history ("The Chief") — I simply can't fathom the downside versus upside (and the absence of a margin of safety) in these buys.

While my general concerns continue to be realized — most notably: slowing economic growth, prickly inflation (seen in this morning's CPI report) and ever higher valuations — this has obviously not translated into a lower market.

Every day it grows clearer that momentum is a force unto itself.

It is terribly frustrating as I try to operate within the framework of a market that is disinterested in negatives and is continuing to be bought on every dip.

Despite that frustration I will not chase under any condition and compromise my investment process.

I will buy value (as I recently did with UNH and (PSKY) but I will never abandon the notion of risk/reward.

Position: Long UNH (S)

BY Doug Kass · Aug 15, 2025, 11:30 AM EDT

This seems like good news to me. Bad news is good news, right? So bad, it is good. Not sure why these guys are only asking for a $500 billion valuation, I think this should get them to $1 trillion, easy!

"The latest ChatGPT is supped to be 'PhD level' smart. It can't even label a map," CNN

On a more serious note, it is now starting to get into the common lexicon that there are all sorts of issues with generative AI and that something isn’t right — The New Yorker (prior email below), CNN and a general roasting of OpenAI and generative AI on Twitter and other places.

But, the equities do not seem to care, which is interesting. Of course, the U.S. government picked the biggest loser company (in my view) to team up with as well. Track record of the U.S. government investing in things continues to be quite Costanza-like. Do the opposite.

BY Doug Kass · Aug 15, 2025, 11:15 AM EDT

From Peter Boockvar:

Core retail sales in July rose .5% m/o/m, one tenth more than expected and June was revised up by 3 tenths to an .8% gain. Above the core, auto sales rose 1.6% m/o/m while building materials fell by 1.3%.

Elsewhere, sales gains were seen in furniture, clothing, sporting goods and at online retailers. They fell at restaurants/bars for the 2nd month in the past 3 (sort of mimics the traffic/transaction trends heard from a variety of restaurant earnings calls) and were down too for electronics and miscellaneous stores which include dollar stores, convenience stores, pet shops, flower shops, etc… The necessity pieces of the data, food/beverage and health/personal care each saw sales gains.

Bottom line, it’s tough to say how much of this is tariff buying pull forwards and what was organic. Also, these are nominal changes and to highlight, the average price of sporting goods In CPI was up .9% each of the past two months and today’s report said sporting goods sales were up .8% in July.

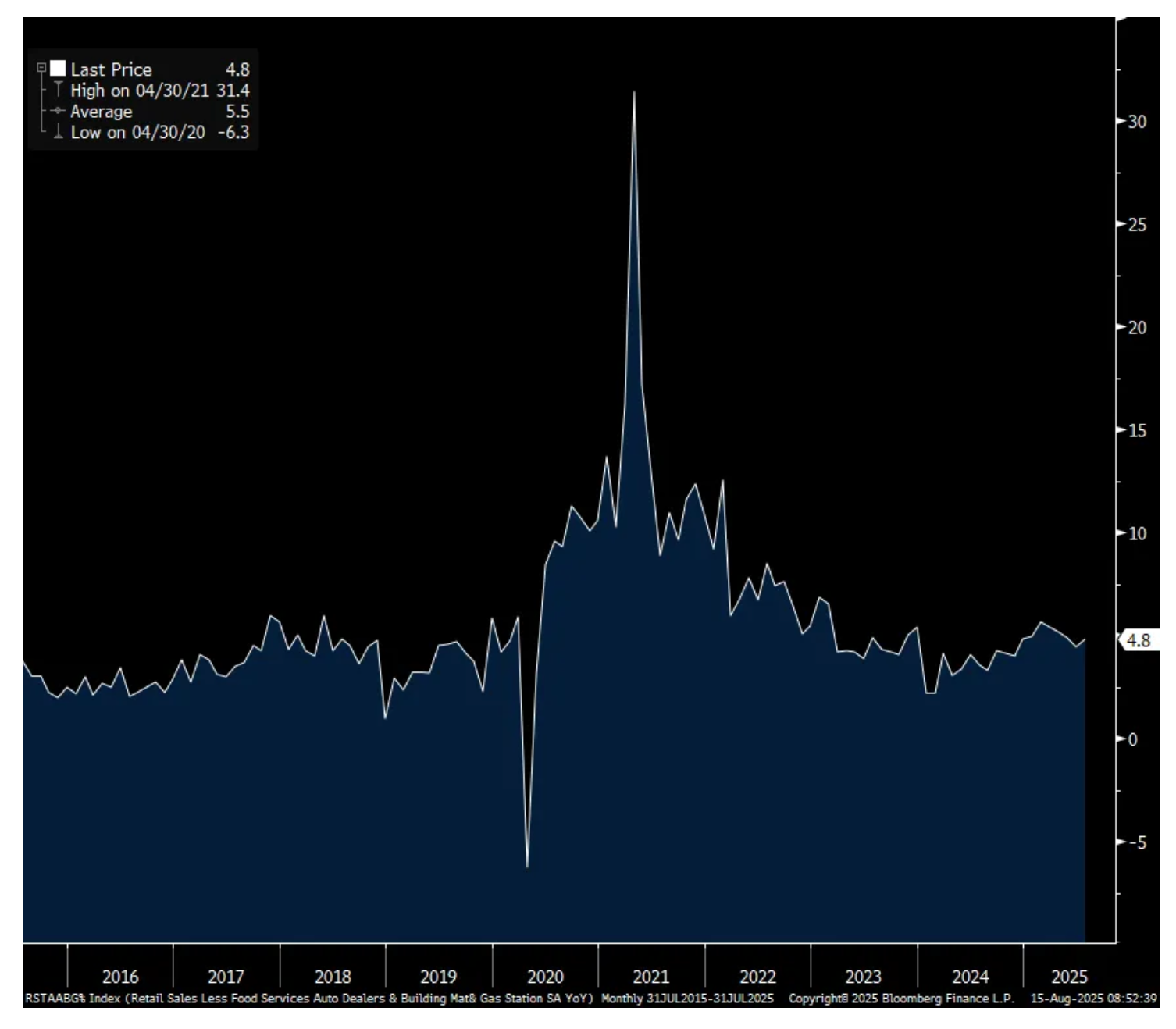

Core retail sales y/o/y

July import prices which DO NOT include the tariffs, were about as expected when we include the June revisions. Headline import prices rose .4% m/o/m after two months of declines and are flattish y/o/y. Ex food and fuels saw import prices higher by .3% m/o/m after a one tenth drop in June, no change in May and a .4% rise in April. They are up .8% y/o/y. While still benign, no signs of notable declines which would imply exporters to us are discounting product to absorb the tariffs.

Product line wise, the import of industrial supplies saw a price gain of 1.6% in the month after declines seen in the four prior months. Capital goods prices were up .1% m/o/m while falling by .2% m/o/m in autos/parts and by a similar amount y/o/y. Consumer goods prices were higher by .4%, though flattish y/o/y

Bottom line, this data point is where you would find if foreign exporters are discounting product prices to any great extent to absorb the tariffs and you need a microscope to find it. On the other hand, the weakness in the US dollar hasn’t led to any notably rise in import prices, yet.

The August NY manufacturing index was above zero for a 2nd month at 11.9 vs the estimate of zero. One of the reasons was not a good reason, a 9 pt rise in ‘Delivery Time’ which implies slower supply chains. On the other hand, new orders jumped to 15.4 from 2. Backlogs remained below zero at -5.5 and inventories went negative too. Employment fell almost 5 pts m/o/m after rising by a similar amount in June. Prices paid slipped by 2 pts to 54.1 and those received fell by almost 3 pts but both are around the six month averages.

The 6 month business activity outlook fell by 8 pts to 16. Of note and surprisingly in light of the BBB tax incentives meant to goose capital spending, capital expenditure plans fell to -.9 from +9.2 and vs -7.3 in the month before.

Bottom line, the NY Fed referred to the headline number as reflecting ‘modest’ growth but after a more than 2 yr manufacturing recession, ‘modest’ is certainly an improvement. We’ll get the Philly release next week.

Treasury yields are little changed post all of this data.

NY Mfr’g

BY Doug Kass · Aug 15, 2025, 11:00 AM EDT

BY Doug Kass · Aug 15, 2025, 10:45 AM EDT

From Peter Boockvar:

While many are just focused on the services component of PPI and think higher 'portfolio management' prices were the main driver (it was not), I want to remind that goods prices jumped .7% m/o/m with core goods prices higher by .4% and are rising at an annualized pace of 3.6% year to date.

As we all debate the extent of rate cuts coming our way I want to remind people that currently the terminal REAL rate the Federal Reserve has had in their dot plot for the past few years is 1%. Call that the current 'neutral rate', aka, R* even though R* doesn't really exist, Powell has said we don't know what it is until we see it and is an econometric model construct but I'm playing along here with the Fed. So, with core CPI around 3% and core PCE slightly below that, about 50 bps of cuts gets us to a 1% REAL rate.

I also want to say, the 3% terminal dot plot rate is ONLY if inflation is sustainably at 2%. To say another way, 3% is NOT the 'neutral rate' UNLESS inflation is sustainably at 2% which it clearly isn't.

In trying to quantify the impact of tariffs on the shipment of goods, Cass Freight released its July shipments index yesterday and said they fell 1.8% in seasonally adjusted terms and are lower by 6.9% y/o/y. They said, "Tariffs hit shipments harder in the most recent data, as paybacks began from demand pull-forwards earlier in the year, though goods prices are still relatively steady."

Also, "Freight volumes are experiencing one of the air pockets we've warned about in recent months. We expect more to come after a reprieve in Q3. However, tariffs are also raising vehicle prices, and heavy truck makers are reducing production. In 2H '25, NA Class 8 production is set to fall more than 25% from 1H' 25."

What less truck production will eventually mean is less capacity.

Speaking of less capacity, you've heard me say many times that we have to enjoy the slowdown in rental gains while we can because it's not going to last. Redfin yesterday reported that "Permits to build US apartments have fallen 23% since the pandemic construction boom." This is "according to a Redfin analysis of US Census Bureau data covering building permits for multifamily units in buildings with five or more units." Not new news to us but Redfin finally mentioning it. https://www.redfin.com/news/press-releases/permits-to-build-u-s-apartments-have-fallen-23-since-the-pandemic-construction-boom/

So, as the huge amount of multi-family supply gets absorbed this year, and it will with still unaffordability challenges for the first time buyer, expect rents to start moving higher again next year. Inflation volatility is still what I expect in coming years and no easy trip back to 2% sustainably.

I heard someone notable on tv yesterday saying that the Fed is fighting the last war on inflation and I'll push back and say the war is not won yet and just look at the 1970's again to show that backing off from the fight prematurely can be a big mistake.

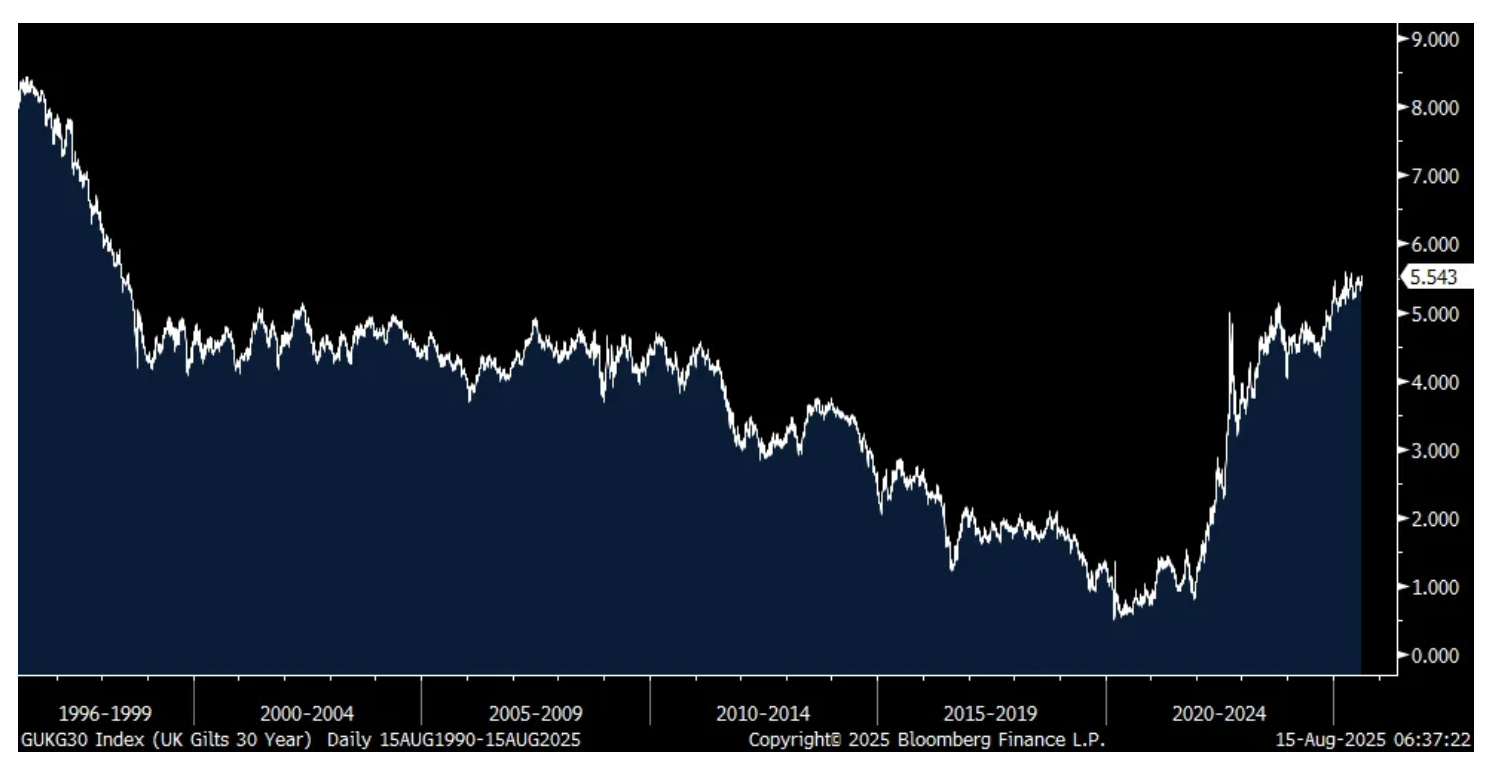

Long term yields in Europe are breaking out today and as I said yesterday, this kerfuffle in long term interest rates globally is not over yet. The German 30 yr bund yield is at the highest level since July 2011 at 3.31%. The French 30 yr oat yield is higher by 5 bps to 4.28%, last seen in November 2011. The 30 yr Gilt yield is just 3 bps from the highest level since 1998. Yes, 1998. This follows the US Treasury selloff yesterday and the rise in JGB yields after Japan's Q2 GDP figure was above expectations (1% growth vs the estimate of up .4%).

I'll argue again, the global bear market in longer duration sovereign bonds continues on and at some point it will matter.

German 30 yr yield

French 30 yr yield

UK 30 yr yield

To some earnings calls of note.

From Tapestry, the owner of Coach and Kate Spade brands and whose stock fell 16% yesterday:

Sales grew 8% with particular strength at Coach which saw sales up 16% and thus the weakness was at Kate Spade. They saw good overall sales growth in Europe and China while sales declined in Japan "amid a challenging consumer backdrop, and in other Asia, revenue decreased 1% as growth in Australia, New Zealand, and South Korea was offset primarily by a decline in Malaysia."

Notwithstanding the sales strength in Coach, "we are facing greater than previously expected profit headwinds from tariffs and duties with the earlier than expected ending of de-minimis exemptions being a meaningful factor. In aggregate, the total expected impact on profitability this year from tariffs is $160 million, representing approximately 230 bps of margin headwind." They are taking "thoughtful actions to mitigate these impacts."

From Birkenstock and whose stock fell 4%:

"Our demand is strong across all product categories and target groups."

"In the Americas, revenue was up 16% in constant currency, with both the B2B and D2C channels growing double digits...Importantly, we saw no pushback or cancellations following the July 1st price increases implemented in response to tariffs." They have some pricing power.

As their shoes are in high demand, "we don't see any slowdown in consumer demand or anything. We are at the moment struggling with capacity. That's our biggest issue."

From Advance Auto Parts and whose stock fell 8% yesterday:

Comps were flat for the quarter "and our performance was driven by strength in the Pro business, which continued to deliver positive comp growth. In our DIY business, we are encouraged by emerging signs of stabilization as comparable sales were consistent with Q1 and improved on a two year basis. Notably, we concluded the quarter on a strong note with both Pro and DIY delivering positive results, and this momentum has continued into the first four weeks of Q3."

"We are working with our vendor partners to effectively manage tariff related cost increases while thoughtfully adjusting retail prices in response to market dynamics. We anticipate that tariffs will have a more pronounced impact in the second half of this year."

"From our perspective, the market is in a transition phase, and while recent trade deals are expected to provide further clarity in vendor negotiations, consumers are still adapting to an evolving landscape of higher prices. We are closely monitoring consumer behavior and the potential for recalibration in purchasing habits, especially within our DIY business. While we have not observed any significant shifts to date and remain encouraged with our recent DIY trajectory, we believe it is prudent to take a cautious approach in planning for the remainder of the year."

From Applied Materials which is down sharply pre-market:

"we expect revenue and earnings to be sequentially lower in our fourth quarter, primarily due to uncertainties in our China business."

"The dynamic macroeconomic and policy environment, including trade and tariffs, has wide ranging implications for the semiconductor industry, increasing uncertainty and lowering visibility in the near term."

"For Applied's business, there are three main factors that mute our outlook for the quarter ahead. First is digestion of capacity in China. Second is our large backlog of pending export license applications, where we have taken a conservative position and assumed none of these licenses will be issued in the next quarter. And third is non-linear demand from leading edge customers, which is primarily linked to market concentration and fab timing."

China's July economic data was softer than expected across the board with retail sales, industrial production, fixed asset investment and home prices which keep falling. The retail sales figure in particular is noisy because of the 'cash for clunkers' type incentives they've implemented which I'm never a fan of as all it does is alter the timing of purchases rather than grow them overall and there is always a hangover after. The Hang Seng has had quite a year, up 26% but it fell 1% overnight in response.

BY Doug Kass · Aug 15, 2025, 10:35 AM EDT

I just covered my trading short rental in DHI at $165.71 for a $5 gain in about 60 minutes.

From comments section:

Dougie Kass

STAFF

1 hour ago

I took a trading short rental in DHI at $170.63.+$7 on the Berkshire buy.

BY Doug Kass · Aug 15, 2025, 10:15 AM EDT

JSR1111

35 minutes ago

Doug do you think you let your winners run enough? You’ve made some really good calls buying good companies after material drawdowns in recent years but even when they’re deemed investments and not trades, you’re often pretty quick to sell them after modest rallies. Not sure how much you made in LLY recently but don’t think it was substantial. If you believe in this rotation to value I’d think you’d be more patient on the long side. Thanks and have a great weekend.

Dougie Kass

STAFF

11 minutes ago

I just made $60 in UNH. Thanks for your concerns.

BY Doug Kass · Aug 15, 2025, 10:00 AM EDT

Jaw4860

11 minutes ago

Waiting for his long investment and short list .Hedge funds are now posting their positions .Waiting for performance numbers ,which do get revealed to the public at sometime contrary to Doug 's comment .

Dougie Kass

STAFF

Just Now

BY Doug Kass · Aug 15, 2025, 9:45 AM EDT

* As the housing correction unfolds...

BY Doug Kass · Aug 15, 2025, 9:30 AM EDT

-PMNT +136% (earnings)

-PGEN +59% (confirms Full FDA Approval of PAPZIMEOS (zopapogene imadenovec-drba), the First and Only Approved Therapy for the Treatment of Adults with Recurrent Respiratory Papillomatosis)

-KULR +17% (earnings)

-FUFU +16% (earnings)

-NU +10% (earnings)

-UNH +10% (Berkshire Hathaway takes new stake)

-TE +9.2% (T1 Energy and Corning sign strategic commercial agreement that boosts the U.S. solar supply chain and advanced manufacturing of affordable, fast-to-deploy energy)

-ENLV +7.9% (to Present 3-Month Topline Data from Phase IIa Moderate/Severe Knee Osteoarthritis Trial on August 18 Webinar)

-JOBY +7.7% (achieves the First Piloted eVTOL Air Taxi Flight between Two Public California Airports)

-NUE +5.0% (Berkshire Hathaway takes new stake)

-TWLO +4.8% (to replace AMED in the S&P MidCap 400 Index, effective Aug 19th)

-CNC +3.8% (higher in sympathy with UNH)

-BRKR +3.4% (recent notable strength being attributed to Michael Burry's Scion Asset Management disclosed 250K stake)

-LEN +3.3% (Berkshire Hathaway takes new stake)

-DHI +2.9% (Berkshire Hathaway takes new stake)

-INTC +2.4% (reportedly US government discussing taking stake)

-ORGN -36% (earnings, guidance)

-GLOB -15% (earnings, guidance)

-AMAT -13% (earnings, guidance)

-TNXP -9.7% (weakness ahead of FDA decision for TNX-102 SL)

-SNDK -9.4% (earnings, guidance)

-CRWV -5.0% (GLXY.CA secures $1.4B financing for Helios AI datacenter expansion with CoreWeave)

-FLO -3.5% (earnings, guidance)

-CORZ -3.1% (downside momentum)

-HIMS -2.6% (FTC has opened probe of Hims' cancellation practices)

BY Doug Kass · Aug 15, 2025, 9:20 AM EDT

BY Doug Kass · Aug 15, 2025, 9:10 AM EDT

BY Doug Kass · Aug 15, 2025, 9:00 AM EDT

BY Doug Kass · Aug 15, 2025, 8:52 AM EDT

BY Doug Kass · Aug 15, 2025, 8:45 AM EDT

BY Doug Kass · Aug 15, 2025, 8:35 AM EDT

The test of a first-rate intelligence is the ability to hold two opposed ideas in the mind at the same time, and still retain the ability to function.

- F. Scott Fitzgerald

Small Caps, Where Hated Stocks Go To Rip Small-Caps: Where Hated Stocks Go To Rip - TrendLabs

Sentiment and Price Action Diverge Bespoke | My Research

Clusters Of Strength BRK.B & Clusters of Strong Breadth - by Frank Cappelleri

Breadth Isnt Broken, Its Building Breadth Isn’t Broken — It’s Building 🚀

BY Doug Kass · Aug 15, 2025, 8:25 AM EDT

I took a trading short rental in DHI at $170.63.

+$7 on the Berkshire buy.

BY Doug Kass · Aug 15, 2025, 8:21 AM EDT

Adding to Index shorts in premarket trading:

* SPY $646.35

* QQQ $580.15

Short SPY M QQQ M

BY Doug Kass · Aug 15, 2025, 8:17 AM EDT

The S&P Short Range Oscillator stands at 2.577% v 3.02% - well into the overbought area.

BY Doug Kass · Aug 15, 2025, 8:10 AM EDT

BY Doug Kass · Aug 15, 2025, 8:00 AM EDT

* I am making some sales in the premarket at $307

After the market closed on Thursday, Berkshire Hathaway BRK.A BRK.B revealed that it had purchased five million shares of United Healthcare UNH last quarter. (See: Warren Buffett's Berkshire Hathaway reveals new stake UnitedHealth)

The shares are trading at $307 at around 4:15 a.m. this morning, a gain of $37. I am reducing my long exposure in this name as investors grow very giddy about Berkshire's purchase.

I always find it odd how the markets overact to Berkshire's buy. (But these days, it is the state of the markets!)

This is especially the case with UNH -- a stock that mostly traded above the current share price during the quarter in which Berkshire initiated the purchase -- ergo, Berkshire, despite this morning's dramatic rally likely has a loss in the shares.

Like all of us, Warren Buffett is only human. He makes mistakes, a lot of them.

He has been bearish for as long as I have been bearish -- with few long purchases and net reductions in his long exposure in his stock portfolio for nearly two years. That has been wrong-footed.

So, he purchases United Health at higher prices than the shares currently trade at (perhaps much higher in the past quarter!) and investors reward him with a $37 boost in the share price this morning. This tells me more about the euphoric and unquestioning state of the market than anything else.

I recently purchased United Health at $247 on Aug. 8:

More Trading

* Shorted HOOD at $115.12 (like many of my shorts of high-octane stocks, this is not advised!)

* Purchased more DIS under $113

* Initiated buy in UNH at $246.83

* Added to LLY at $633.79

Aug 8, 2025 11:20 AM EDT

Buying Value, Shorting Momentum

I initiated three new investment longs (deep value) late last week - (UNH) , (LLY) and (DIS) . I plan to add on weakness.More later in the week.I initiated several trading short rentals of momentum stocks recently - (HOOD) NVDA , PLTR (see my Barron's comments) and added to the mother ship of momentum GRNY

Position: Long UNH VS LLY VS DIS S; Short GRNY VL NVDA VS PLTR VS HOOD VS

By Doug Kass

Aug 11, 2025 7:40 AM EDT

BY Doug Kass · Aug 15, 2025, 7:15 AM EDT

BY Doug Kass · Aug 15, 2025, 6:53 AM EDT

Adding to Index shorts at 7:35 p.m. Thursday night:

SPY $645.34

QQQ $579.37

BY Doug Kass · Aug 15, 2025, 6:37 AM EDT