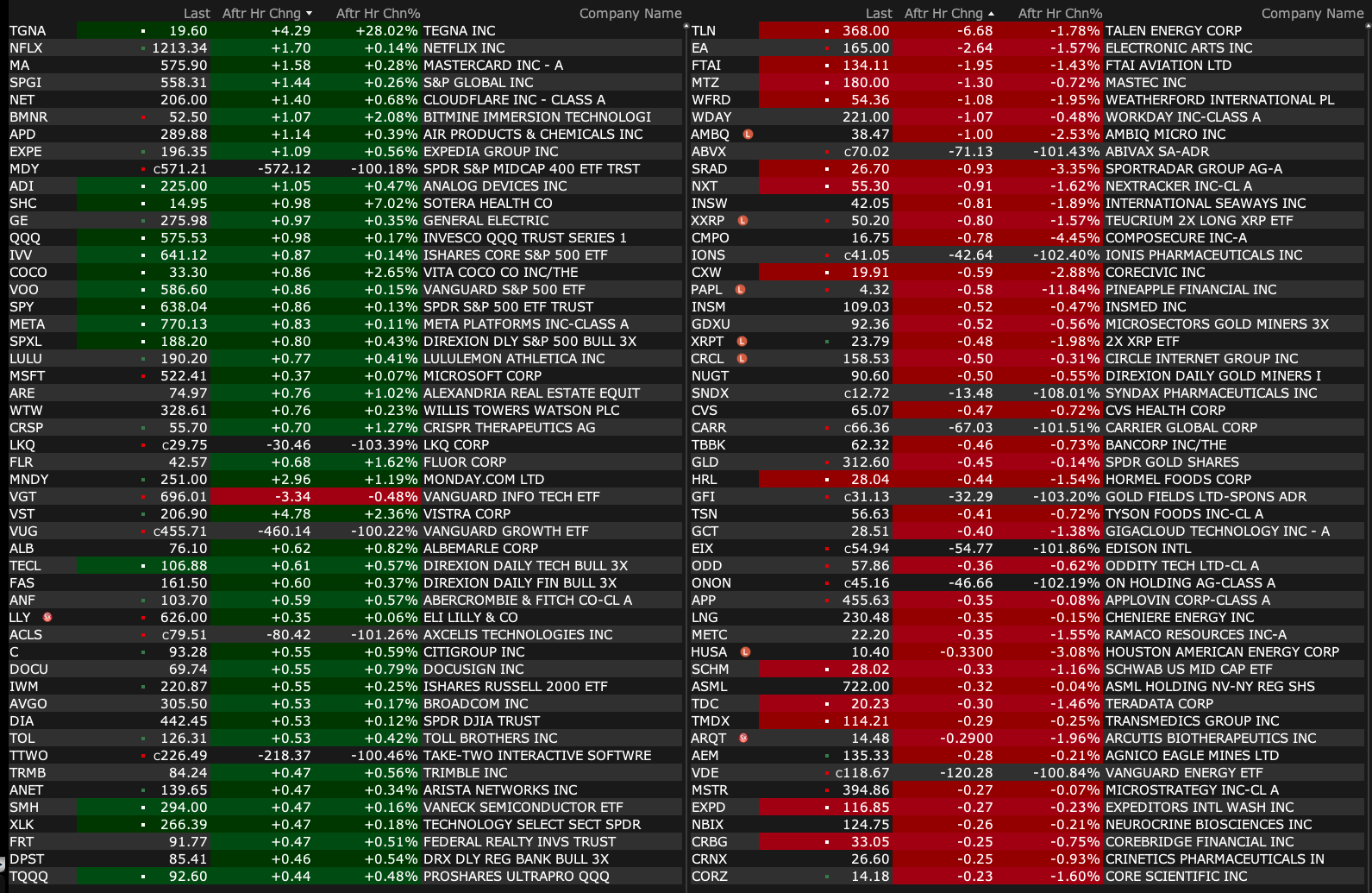

Friday's After-Hours Movers

As of 4:18 p.m.:

BY Doug Kass · Aug 8, 2025, 4:45 PM EDT

As of 4:18 p.m.:

BY Doug Kass · Aug 8, 2025, 4:45 PM EDT

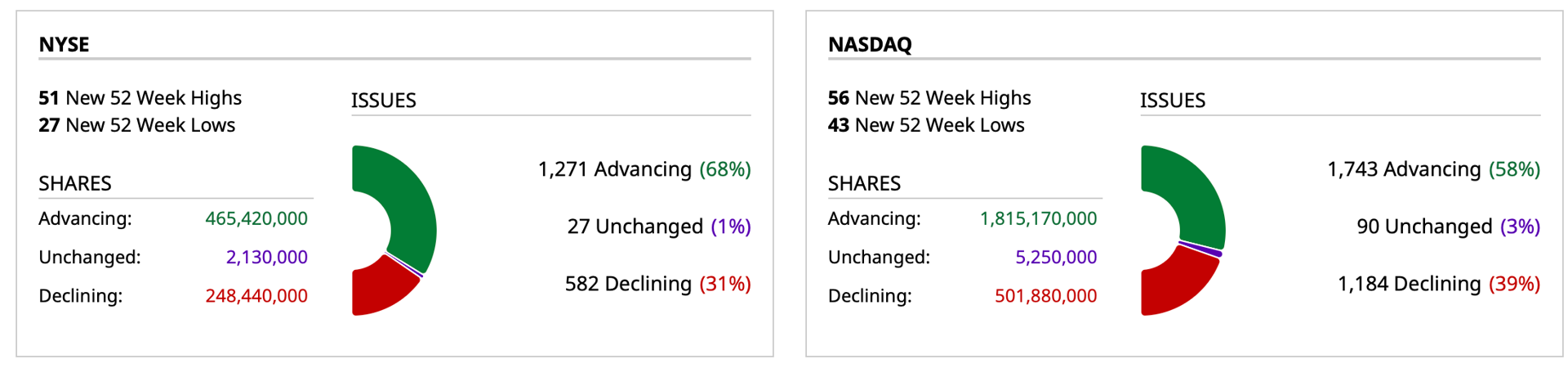

- NYSE volume 8% below its one-month average;

- NASDAQ volume 11% below its one-month average;

- VIX index: down 7.91% to 15.26

BY Doug Kass · Aug 8, 2025, 4:30 PM EDT

Thanks for reading my Diary today and all week.

I hope my output was of value.

Enjoy your weekend.

Be safe.

BY Doug Kass · Aug 8, 2025, 3:45 PM EDT

Wolf Street howls about the growing inventory of existing homes for sale.

BY Doug Kass · Aug 8, 2025, 3:22 PM EDT

Dougie Kass

GRNY falling off its high BEFORE the Indices drop.

Could this be the start of something big or am I just wishin' and hopin?'

Cue Dusty Springfield.

BY Doug Kass · Aug 8, 2025, 1:50 PM EDT

Professor Scott Galloway's No Mercy No Malice: "The Attention Economy and Young People"

BY Doug Kass · Aug 8, 2025, 1:35 PM EDT

Here are today's things:

* Back reshorting the indices:

1. SPY $635.01

2. QQQ $571.84

* Shorted more JOET at $41.29 and GRNY at $23.84

* Added to shorts PLTR at $185.27 and NVDA at $181.76

* Initiated a short in HOOD at $115.12

* Initiated a long in DIS at $112.95 and UNH at $246.83

* Added to TSLA short at $330.98

* Added to LLY at $633.79

BY Doug Kass · Aug 8, 2025, 1:15 PM EDT

BY Doug Kass · Aug 8, 2025, 1:05 PM EDT

BY Doug Kass · Aug 8, 2025, 12:20 PM EDT

"History never repeats itself. Man always does."

- Voltaire

I receive daily selling alerts (and not small-sized) of large insider sales — AMZN, NVDA, AVGO, HOOD, SCHW (to name a few!)

BY Doug Kass · Aug 8, 2025, 12:05 PM EDT

Dougie Kass

you took alot of risk 7iron for a small gain, imho.

this strategy will work and work and then... boom!

7iron

Thanks and I humbly agree. Yeah, it's the boom that wipes me out.

Dougie Kass

please dont do again 7

this is a recipe for disaster

it is what lee cooperman calls picking up nickels in front of a steamroller

BY Doug Kass · Aug 8, 2025, 11:56 AM EDT

- NYSE volume 9% below its one-month average;

- NASDAQ volume 5% below its one-month average;

- VIX index: down 4.35% to 15.85

BY Doug Kass · Aug 8, 2025, 11:45 AM EDT

BY Doug Kass · Aug 8, 2025, 11:30 AM EDT

* Shorted HOOD at $115.12 (like many of my shorts of high-octane stocks, this is not advised!)

* Purchased more DIS under $113

* Initiated buy in UNH at $246.83

* Added to LLY at $633.79

BY Doug Kass · Aug 8, 2025, 11:20 AM EDT

* Some additional capital spending concerns...

This is interesting on the CAPEX issue – both the tweet and the subtweet regarding how much debt will be required to fund the theoretical AI buildout:

When cash-rich and high-cash-flow companies like Meta META are turning to third-party sources to finance their initiatives (with interest rates where they are now too), you know their spending is stretched as much as it can be.

The buildout was somewhat de-risked when it was funded by the cash and cash flows from large companies, but when you start relying on the markets for it, well what the markets giveth, they can also take away. Just like post the year 2000.

Then related, the wildly hyped GPT 5.0 is another dud. (See previous post) Gen AI is not scaling at nearly the rate they thought it would, which has already been shown. In fact, the incremental return on all the extra money being spent is getting worse (lower rate of improvement per extra dollar spent). Ergo diminishing marginal returns. Which is one more reason all of the borrowing needs to happen. More and more $ (and power and water and cooling) are being required for less and less in the way of incremental gains.

More!

And what the heck, but boy is this a long one: AI Is A Money Trap

None

BY Doug Kass · Aug 8, 2025, 10:55 AM EDT

We are, in my judgment, moving to a fever pitch in U.S. equities.

I am dispassionately adding to my short book.

BY Doug Kass · Aug 8, 2025, 10:45 AM EDT

From Peter Boockvar:

Positives,

1) The MBA said that the average 30 yr mortgage rate dipped by 6 bps to 6.77% which is back to a one month low and that helped to lift refi's by 5.2% w/o/w after 3 weeks of declines. Purchases rose 1.5% w/o/w after some volatile weeks over the past month.

2) From Doordash: "In our US marketplace in Q2 2025, y/o/y growth in Total Orders accelerated, with notable strength in the US restaurant category. Strong growth in DashPass membership contributed to a y/o/y increase in average order frequency, which reached an all-time high in Q2 2025. We believe we have been a pioneer in membership programs for local commerce and have continued working to improve the value proposition we offer...High levels of consumer engagement in the US were evident across many metrics and widespread throughout our consumer cohorts...We believe this highlights the broadening attraction of our marketplace and the opportunity we have to continue attracting new consumers."

3) From Disney: Focusing on the parks/cruise business for clues on the consumer, “Results reflect higher guest spending at our theme parks, an increase in passenger cruise days due to the launch of the Disney Treasure, and higher occupied room nights, partially offset by higher costs reflecting new guest offerings including the expansion of our Disney Cruise Line fleet...In light of the fact that there’s a competitive offering in the marketplace (Universal’s park expansion in Orlando) , the fact that attendance came in as well as it did is something that we feel terrific about.”

4) From Airbnb: "We exceeded expectations across key metrics, including bookings, revenue, and margins. And while the quarter started with some global economic uncertainty, travel demand picked up, and nights booked at Airbnb accelerated from April to July."

5) From Yum Brands: On the overall consumer, "The data that we look at about the consumer behavior shows clear trade in from consumers in fast casual into the Taco Bell brand. And when you even pull apart the income bands, although I know that the lower income consumers are pulling back, that's been well documented by our competitors, we aren't seeing that at Taco Bell. In fact, if you pull all the income bands in Q2, we've had sales and transaction growth across all income bands at Taco Bell very consistently, very little difference from one income band to another."

6) From Gartner: "Clients see large potential in AI and they need help in determining the best way to capture that potential." Cybersecurity too among some other areas.

7) From Eaton: "Demand in our aerospace business remains very strong." And also in their electrical business as "Organic sales growth of 12% was driven primarily by strength in data centers, up about 50%, along with strength in commercial and institutional end markets."

8) From Cummins: With power generation in particular, the 25% revenue growth was "driven primarily by continued strong demand in data centers and mission critical applications."

9) From Camden Property Trust: "Rental rates for the second quarter had effective new leases down 2.1% and renewals up 3.7% for a blended rate of .7%. This was in line with our expectations for the quarter and reflected an 80 bps improvement from the negative .1% blended rate we reported in the first quarter of '25 and a 60 bps improvement from the .1% reported in the second quarter of 2024."

10) From Equity Residential: Blended rents grew by 3% in Q2 with new leases down .1% more than offset by renewal rates up by 5.2% y/o/y. For Q3, "Blended rate is expected to be between 2.2% and 2.8%."

11) From Wayfair: "If you just look broadly at the market, what I would say is that the market this year is definitely better than the last three years, where it was down substantially each year. But I think the market is still flat to down low single digits. And I would describe the market not as having strength, but as sort of feeling like it's bottomed out, like bumping along the bottom...There's no question the higher end market is stronger than mass. That's definitely the case...But that's not really surprising if you just think about the category being discretionary."

12) From Simon Property: "And the physical shopping environment continues to be the place to be. So, we're quite bullish about what we've done, what we are doing, where we are going, despite all of the headlines that are out there." For smaller tenants, those more negatively impacted by tariffs, "I think they're managing it as best they can. I still think the full story, obviously, given the volatility, has not been written. But we're not seeing it in demand and that particular business that is sensitive to moms and pops continues to perform well. So, we're more optimistic about that segment than I was last quarter. But, like I said, it is something that we're watching closely."

13) From Trex: "The Trex team delivered strong second quarter results, highlighted by 3% net sales growth, achieving a record level of quarterly sales despite adverse weather conditions in many parts of the country and despite a declining repair and remodel market...New products are once again a key contributor to the past quarter's sales performance."

14) From On Semiconductor: "Turning to the demand environment, we are seeing signs of stabilization across our end markets. We have not seen any pull-ins to date due to tariffs and our diversified manufacturing footprint remains a competitive advantage, providing sourcing options to our customers as they work on optimizing their supply chains." Automotive revenue fell 4% but "performing better than anticipated and is expected to grow in the third quarter with continued EV ramps" particularly in China, offsetting "weakness in America and Europe." The strength, "Revenue for AI data center nearly doubled again in Q2 over the same quarter last year."

15) From Kimberly Clark: "I do see purchasing power under pressure for consumers. And frankly, we don't really see a catalyst for that dynamic to change in the near to medium term. So for us that does affect some of the categories. However...our categories are essential. There's not a whole lot of substitutes for our products. And so because of that, demand remains resilient and the categories continue to demonstrate durable growth."

16) The Bank of England cut its bank rate by 25 bps as expected to 4% but the vote was tight at 5-4 with 3 wanting no change while one voted for a cut of 50 bps.

17) UK's July services PMI was revised up to 51.8 from 51.2 initially, though down 1 pt m/o/m.

18) The Eurozone final services PMI was left little changed at 51 vs 50.5 in June. S&P Global said, "This could turn out to be a good summer for service providers. In Italy and Spain, business activity rose more sharply in July than in the previous month, while Germany, after several challenging months, has clawed its way back into growth territory...France, by contrast, is the only one of the four major Eurozone economies where the private services sector is contracting. Worse still, the downturn deepened."

19) Chinese exports grew by 7.2% y/o/y, above the estimate of 5.6% growth. But, the changing trade world was reflected here as exports to the US were down by 22% but rose to the EU, Southeast Asia and Australia. Imports were higher by 4.1% y/o/y vs the forecast of a drop of 1% driven by higher commodity and semi imports.

20) China's July private sector Caixin services PMI rose 2 pts to 52.6 and that is the best since May 2024.

21) Singapore's PMI rose to 52.7 from 51 while Hong Kong's went to 49.2 from 47.8.

22) The BoJ was given another reason to hike rates as base pay in June in Japan rose 2.1% y/o/y, just off the best levels since the mid 1990's. That though still remains below the rate of inflation.

Negatives,

1) Initial jobless claims totaled 226k, 4k more than expected and up from 219k in the week before. The 4 week average was unchanged at 221k. Continuing claims lifted to 1.974mm from 1.936mm and that is a new cycle high at the highest since November 2021.

2) The July ISM services index fell to 50.1 from 50.8 and that was below the estimate of 51.5. With many eyes on the labor market, the employment component fell to 46.4 from 47.2 and that is the 2nd lowest print since December 2023 and below 50 for the 4th month in the past 5. Prices paid rose to 69.9 from 67.5 and that is the highest since October 2022. The bottom line from the ISM was this, “July’s PMI level continues to reflect slow growth, and survey respondents indicated that seasonal and weather factors had negative impacts on business…The most common topic among survey panelists remained tariff-related impacts, with a noticeable increase in commodities listed as up in price.”

3) Productivity in Q2 was as expected when we include the downward revision to Q1. On a y/o/y basis, it grew by 1.3% following a 1.2% gain in Q1. The average in 2024 was about 2.7%. Unit labor costs grew by 2.6% y/o/y and that is most since Q1 2024. Averaging Q1 and Q2 gives us an average annualized first half 2025 productivity gain of just .3% with unit labor costs up by 4.25%.

4) From McDonald's: US comps were up 2.5% y/o/y, “But I would say we saw sales moderate through Q2 as I think those headwinds kind of persisted.” Also, “We outperformed nearing competitors on both comp sales and comp guest counts. Certainly, overall QSR traffic in the US remained challenging as visits across the industry by low income consumers once again declined by double digits versus the prior year ahead. Reengaging the low income consumer is critical as they typically visit our restaurants more frequently than middle and high income consumers. This bifurcated consumer base is why we remain cautious about the overall near term health of the US consumer.” And this was interesting as to how lower income consumers are behaving with the pressure they are feeling, “And the result of that is you’re seeing people either skip occasion, so they’re skipping a daypart like breakfast or they’re trading down either within our menu or they’re trading down to eating at home.”

5) From Jack in the Box: "As many in the QSR industry have already called out, the macro environment is very difficult and consumers remain cautious. Jack in the Box significantly over indexes with Hispanic guests, to especially in our core markets that face uncertainty and have pulled back their spending. This issue is having an outsized impact on our sales. In addition, we have seen lower income cohorts pull back as well in line with industry trends."

6) From Dine Brands: "Overall, we continue to operate in a competitive environment. Consumers are still feeling macroeconomic pressure, and as a result, guests continue to manage their check by ordering fewer beverages and appetizers as well as trading down to lower price items on our menus."

7) From Trulieve Cannabis: “Several months ago, we recognized a shift in consumer preferences towards value and mid-tier products, broadly in line with national economic conditions.” They met this with value products which helped them gain market share. And, “what we are seeing is we are seeing frequency increase fairly dramatically (in terms of traffic) candidly with customers coming back more often. But again, that basket and that spend per visit lowering and then looking for additional value in their purchase.”

8) Fron Elf Beauty: "As we spoke about last quarter, we are planning to provide a full year fiscal '26 outlook once we have greater certainty on tariffs. Unfortunately, there continues to be a broad range of potential outcomes. To set the foundation, about 75% of our global production today comes from China." And on pulling the pricing lever, "Overall retailer acceptance has been good for our price increases...The other thing I will tell you is we are hearing of a number of brands that are going to be taking pricing. So I think we're just in that environment right now with the uncertainty of tariffs and the tariff impact that you will probably see more companies take pricing."

9) From Gartner: "We also experienced some headwinds during Q2. Measures of CEO confidence fell to recessionary levels, among the fastest drops ever recorded. In a Gartner survey, 78% of CEOs indicated they're implementing cost cutting measures to safeguard performance...The largest headwind in Q2 was the US federal government. Initiatives from the DOGE made it more challenging for clients to purchase or renew many of our products. In addition, there were impacts from tariff policies. With the prospect of higher tariffs, many companies implemented strong cost saving measures. Even companies not directly impacted by tariffs began implementing these measures." Also, "Purchase decisions that were previously made by functional leaders are now being escalated to the CFO or even the CEO. These changes occurred at a record pace, impacting our performance during Q2."

10) From Marriott: "With ongoing economic uncertainty, we now estimate full year RevPAR growth to be in the lower end of our prior range and increase between 1.5% and 2.5% over last year."

11) From Caterpillar: "The net incremental impact from tariffs was around the top end of our estimated $250 million to $350 million range for the quarter." For all of 2025, "we expect the net impact from incremental tariffs for 2025 will be around $1.3 billion to $1.5 billion, net of some mitigating actions and cost controls."

12) From Eaton: Their vehicle business saw a drop in sales, "primarily driven by weaknesses in the North American truck market."

13) From Dupont: On the overall macro, "What I would say is that we continue to be in a fairly mixed environment. Really, all of the growth so far for the last several quarters is really coming from AI driven applications across advanced nodes, advanced packaging and data center...Most of the rest of the electronics economy kind of remains relatively weak. I think we're starting to see the green shoots of stabilization and recovery on the lagging edge parts of the market, and we expect kind of slow improvement as we move through the back half of the year for the more industrial focused, lagging edge semiconductor nodes...And then, we still have a relatively weak consumer environment where consumer devices are expected to be up kind of low single digit."

14) From Cummins: "we expect North America heavy and medium duty truck volumes to decline 25% to 30% from second quarter levels. As we have seen truck orders recently reach multi year lows and OEMs have initiated reduced work weeks through the next three months." Also, "Tariffs are undoubtedly having an impact on Cummins, our suppliers, customers and end users, creating uncertainty over freight activity linked to the movement of goods and increasing costs. We did experience increasing tariff costs in the second quarter. However, as anticipated, we did not see the full impact of the current policies as supply chains work through existing inventory."

15) From Camden Property Trust: On why rent growth will accelerate again in the coming years, on the supply side, "So, what's happening now, and if you look at the starts, starts are down 76% in Charlotte, Denver, Austin, Atlanta, and DC. They're down 60-76% in Tampa, Orlando, Phoenix and Nashville. They're down 45% to 65% in Dallas, Houston, West Palm Beach, and Fort Worth. So, when you look at those numbers, clearly the supply is down significantly. It's going to be down significantly."

16) From Colgate: "There is a persistently cautious consumer in North America right now. We saw some rebound in April, May. The categories took a little step back in June, which we weren't expecting...Many of our markets and categories around the world remained challenging in the second quarter and we expect this to continue through the second half of the year." And, "The cost environment is difficult as we're dealing with tariff increases, higher raw and packaging material costs, and less underlying category inflation. This means that our revenue growth management strategies need to drive additional pricing and mix with lower levels of elasticity as we look to improve organic sales growth in the second half of the year."

17) From WW Grainger: "It feels like the demand environment is still relatively muted. But we do feel like we're doing reasonably well in that environment." Also, "Looking ahead to the third quarter, we expect to adhere to our regular cycle with our next pricing actions slated to go live in early September. This round will include some further increases on products directly imported by Grainger to reflect current tariff rates, which are higher than what we passed in May. The September cycle will also include initial pricing actions on supplier imported products where we have finalized negotiations. The past price from this round is expected to result in net annualized incremental price of 2% to 2.5% on a run rate basis for the High Touch business."

18) German industrial production in June was weak, falling by 1.9% m/o/m, more than the expected fall of .5% and May was revised down by 110 bps.

19) German factory orders in June were down 1% m/o/m vs the estimate of up 1.1% (and partly offset by a 6 tenths upward revision to May) with particular softness in the orders from foreign countries outside of the Eurozone where orders declined by 7.8%, though follows a 7.6% rise in May. All tariff distorted figures but the economy ministry said "In light of the now likely permanent increase in tariffs on exports to the US, the industrial sector is likely to be characterized by subdued foreign demand in the future."

20) The August Sentix Investor Confidence index fell to -3.7 from +4.5 and worse than the estimate of +6.9. Sentix said, "Investors are not impressed by the EU's latest tariff deal with the US...The negative factors clearly out weigh the positive ones for the global economy. The EU and Switzerland are being punished severely. The US and Donald Trump may feel like winners in the short term, but falling expectations here too indicate that this type of trade policy will mainly produce losers." Some more, "The wrinkles of concern in the economy are deepening again." The Germany index fell to -12.8, down by 12 pts.

BY Doug Kass · Aug 8, 2025, 10:30 AM EDT

Bought (small) Disney DIS at $113.07.

BY Doug Kass · Aug 8, 2025, 10:25 AM EDT

Adding to Index shorts with S&P cash +43 handles:

* SPY $636.38

* QQQ $573.20

BY Doug Kass · Aug 8, 2025, 10:24 AM EDT

From JPMorgan:

US: Futs are higher. Headlines were quiet since yesterday’s close with no major macro data reporting today. The next key catalyst will be August 12 CPI release. Trump nominated CEA Chair Stephen Miran to fill Kugler’s expiring term; Feroli now see 25bp cut in September (vs. his previous December call), following by three 25bp cut in the next three meetings. Pre-market, MegaCap Tech sees NVDA leading gains (+0.7%); sectors like Utilities and Consumer Staples are outperforming. Yields are flat and USD is lower. Commodities are mixed with oil and precious metals higher, while base metals are flat.

and...

JPM MARKET INTEL EQUITY & MACRO NARRATIVE

FEROLI NOW SEES SEP CUT – his full note is here

· So, in the off chance Miran is governor by the time of the next meeting, that could imply three dissents. That’s a lot of dissents. For Powell the risk management considerations at the next meeting may go beyond balancing employment and inflation risks, and we now see the path of least resistance is to pull forward the next 25bp cut to the September meeting. We continue to look for three like-sized cuts at the subsequent three meetings before pausing indefinitely.

· It's not unprecedented for the Fed to ease when stocks are at or near all-time highs. It’s rarer when stocks are at the highs and inflation is above target and inflecting higher. So, an ease next meeting isn't likely to be broadly welcomed by the Committee. At the last FOMC meeting, Powell framed the labor market risks in the context of the unemployment rate. Simplifying to that one dimension, a rate of 4.4% or higher could get a larger-sized cut at the next meeting, while a rate of 4.1% or lower could prompt a few dissents for a full employment, above-target inflation cut.

BY Doug Kass · Aug 8, 2025, 9:50 AM EDT

Moved to very large on my GRNY short.

BY Doug Kass · Aug 8, 2025, 9:35 AM EDT

A few on LLY (long) and AAPL (short)

Eli Lilly price target lowered to $895 from $1,050 at UBS UBS lowered the firm's price target on Eli Lilly to $895 from $1,050 and keeps a Buy rating on the shares. The beat and raise quarter was overshadowed by the weaker than expected ATTAIN-1 topline, the analyst tells investors in a research note.

Eli Lilly selloff brings 'compelling' entry point, says JPMorgan JPMorgan views the post-earnings selloff in shares of Eli Lilly as providing a "compelling" entry point. The Q2 report came in well ahead of consensus estimated and Lilly is raised guidance, which should dispel some weight loss market concerns, the analyst tells investors in a research note. However, the firm says the bigger focus was on orforglipron's Phase 3 obesity data where weight loss came in slightly below expectations. JPMorgan does not see 1-2 percentage points lower weight loss as meaningfully changing the use case for orforglipron. It keeps an Overweight rating on Lilly shares with a $1,100 price target.

Morgan Stanley trims Eli Lilly price target, calls selloff 'overdone' Morgan Stanley lowered the firm's price target on Eli Lilly to $1,028 from $1,135 and keeps an Overweight rating on the shares. Debates on the competitive profile of oral orforglipron in obesity drove the weakness in shares yesterday, notes the analyst, who says these concerns overshadowed a "solid" Q2 EPS report. While the firm notes that it lowered estimates for its oral weight loss pill bull case, its base case estimates for the drug are unchanged and it views the selloff as "overdone."

Apple has lost 'around a dozen' AI staff to rivals, FT reports Apple (AAPL) has lost around a dozen of its AI staff, including top researchers, to rivals in recent months, The Financial Times' Michael Acton reports. Apple has lost AI staff members to Meta (META), OpenAI, xAI, and Cohere, according to the report. OpenAI has poached Brandon McKinzie and Dian Ang Yap, two Apple foundation models research engineers, while Cohere hired machine learning scientist Liutong Zhou in June, and Ruoming Pang, head of Apple's foundational models team, departed for Meta last month. Several of the individuals who have left had previously contributed to research papers on AI models that Apple released last year, according to the report.

BY Doug Kass · Aug 8, 2025, 9:30 AM EDT

Adding to PLTR $184.03 and NVDA $182.02 shorts.

BY Doug Kass · Aug 8, 2025, 9:25 AM EDT

-LZ +35% (earnings, guidance)

-LASR +26% (earnings, guidance)

-SOUN +26% (earnings, guidance)

-OPRX +25% (earnings, guidance)

-PSIX +23% (earnings, guidance)

-OUST +20% (earnings, guidance)

-VIAV +19% (earnings, guidance)

-JAMF +18% (earnings, guidance)

-ABCL +15% (earnings)

-EXPE +15% (earnings, guidance)

-ANIP +13% (earnings, guidance)

-NTRA +13% (earnings, guidance)

-NTRB +11% (US FDA Grants Nutriband Meeting Request for Aversa Fentanyl Abuse Deterrent Fentanyl Patch)

-CART +8.8% (earnings, guidance)

-DOCS +8.7% (earnings, guidance)

-TEM +8.5% (earnings, guidance; files mixed shelf of indetermined amount)

-AMR +8.4% (earnings, guidance)

-XYZ +8.4% (earnings, guidance)

-FIGS +8.3% (earnings, guidance)

-AMCX +8.0% (earnings)

-SHCO +6.9% (earnings)

-GSAT +6.0% (earnings, guidance)

-RKLB +5.1% (earnings, guidance)

-PTON +4.8% (Goldman Sachs Raised PTON to Buy from Neutral, price target: $11.50 from $7)

-TTWO +4.6% (earnings, guidance)

-GILD +4.3% (earnings, guidance)

-SOLV +3.8% (earnings, guidance)

-FUBO +2.8% (earnings)

-PAR +2.7% (earnings)

-TTD -32% (earnings, guidance)

-SG -30% (earnings, guidance)

-VTEX -23% (earnings, guidance)

-SEZL -22% (earnings, guidance)

-SLVM -17% (earnings, guidance)

-UA -15% (earnings, guidance)

-PINS -13% (earnings, guidance)

-GRND -11% (earnings, guidance)

-FLY -9.4% (weakness following IPO)

-YELP -6.6% (earnings, guidance)

-VVX -5.7% (announces sale of 2.0M shares of its common stock on an underwritten basis by Vertex Aerospace Holdco LLC)

-BHF -5.3% (earnings)

BY Doug Kass · Aug 8, 2025, 9:16 AM EDT

BY Doug Kass · Aug 8, 2025, 9:05 AM EDT

BY Doug Kass · Aug 8, 2025, 8:55 AM EDT

I am adding to my Index shorts:

* SPY $634.64

* QQQ $571.40

BY Doug Kass · Aug 8, 2025, 8:35 AM EDT

* Is GPT 5.0 another dud?

No surprise.

The wildly hyped GPT 5.0 is another dud. Gen AI is not scaling at nearly the rate they thought it would, which has already been shown. In fact, the incremental return on all the extra money being spent is getting worse (lower rate of improvement per extra dollar spent). Ergo diminishing marginal returns. It’s here, finally, but not everything people dreamed it would be:

Here's Gary Marcus' GPT-5 Hot Take:

OpenAI just announced GPT-5. I stand by my predictions from a couple weeks ago; none of the problems I said would not be solved appear to have been solved..

Here’s my hot take:

• Took almost 3 years, many billions of dollars (over a half-trillion fieldwide).

• Good progress on many fronts.

• But still part of the pack, not a giant leap forward (e.g. Grok 4 beats it on ARC-AGI-2 results)

Also from Adam Clark:

Relax everyone—artificial intelligence isn’t about to take over yet, but the boom isn’t over. While OpenAI’s GPT-5 launch suggests progress is coming at a slower pace, that doesn’t spell disaster for the AI trade—far from it.The debut of the latest AI model from the ChatGPT developer on Thursday was eagerly awaited, coming more than two years after its official predecessor. However, the proliferation of so-called reasoning models in the meantime has raised the bar for performance. Early benchmarking tests suggest GPT-5 is only mildly better than rivals from Google and Elon Musk’s xAI.For investors, rather than trying to back the best AI model, the safer choice is still likely to be stocks powering the technology such as chip maker Nvidia. Its hardware will continue to be in demand as companies look to eke out improvements. Additionally, its CEO Jensen Huang is in President Donald Trump’s good graces, visiting the White House this week ahead of the announcement of chip tariffs, according to Bloomberg.And having Trump’s favor is very important for tech CEOs—a lesson Intel’s Lip-Bu Tan is learning the hard way after the president called for him to resign over his past ties to China. It’s the last thing the chief executive needs as he seeks to revive the beleaguered chip company, which is missing out on the AI boom.The fundamentals of the AI trade remain intact, with big cloud companies set to spend $340 billion this year in building data centers and chip tariffs being less burdensome than feared. It doesn’t require superintelligence to think the trend will continue.—Adam Clark

BY Doug Kass · Aug 8, 2025, 8:05 AM EDT

JPMorgan reduces its Eli Lilly LLY price target from $1,135 to $1,028.

That is a far cry from $641 close yesterday!

I initiated a long position in LLY yesterday (at around the closing price) and, despite the adverse drug news and that Big Pharma is out of favor, I am now planning to stick with this investment.

More next week.

BY Doug Kass · Aug 8, 2025, 7:30 AM EDT

In case you missed it:

Dougie Kass

Shorting TSLA $320.80 on the news that the company has disbanded its DOJO Supercomputer team. It could be viewed as a negative regarding their AI ambitions.

BY Doug Kass · Aug 8, 2025, 7:22 AM EDT

Bonus — Here are some great links:

Bull/Bear Spread Turns Negative

BY Doug Kass · Aug 8, 2025, 7:10 AM EDT

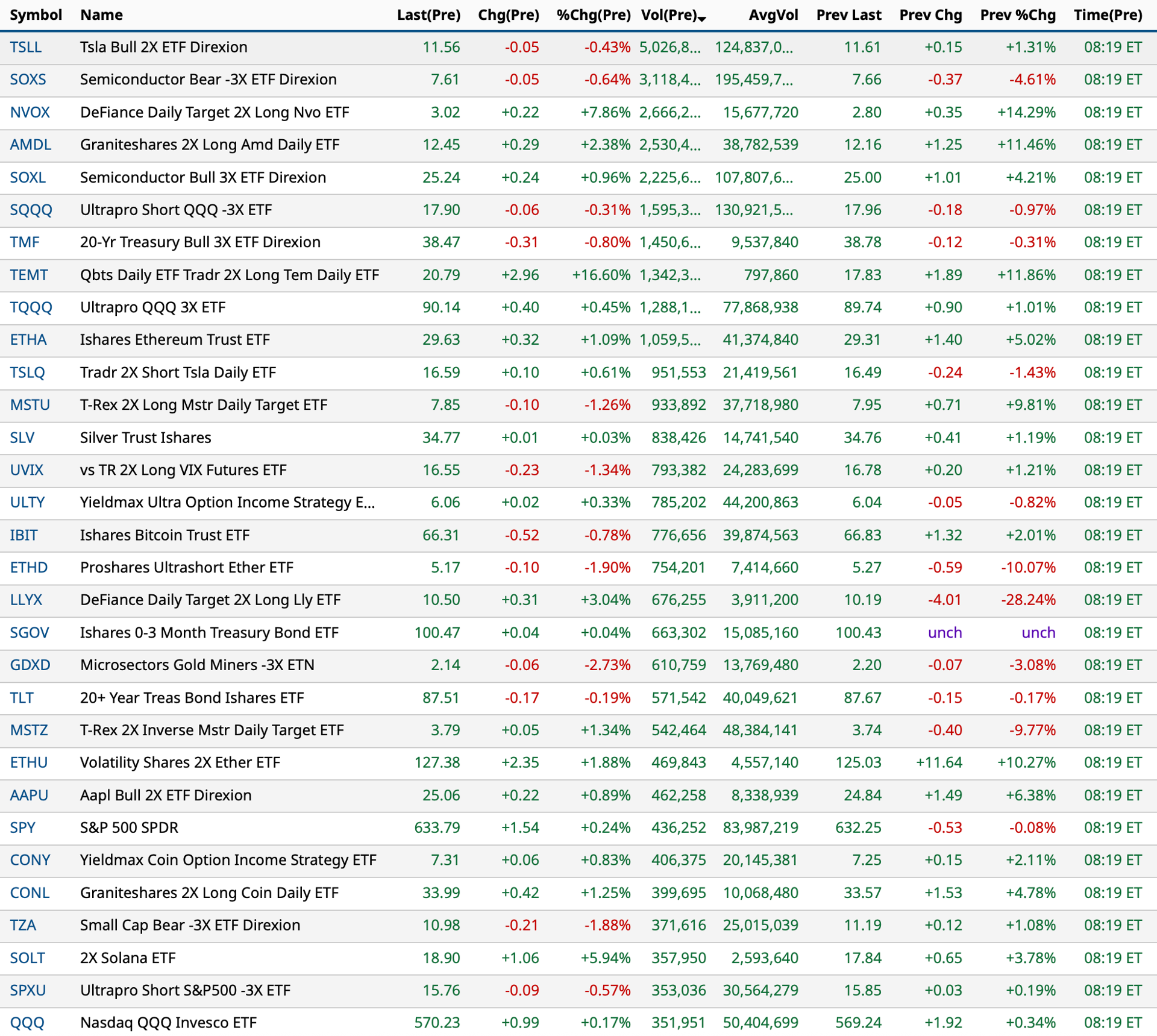

Coiling:

BY Doug Kass · Aug 8, 2025, 6:55 AM EDT

Let me start by writing that the sort of rapid-fire index trading (on the short side, in common and calls) is not for most.

Not only shouldn't most short ANYTHING but I am shorting indices to position myself for what I expect to be a market inflection point and (tradeable) correction (something that many are not in agreement with).

When I am implementing these short-term index trades and a piece of negative news comes out (causing a quick market drop and maybe not yet a renewed or established trend lower occurs) or the market leaders (MAG 7) remain strong, I tend to cover rather quickly — as I have done recently.

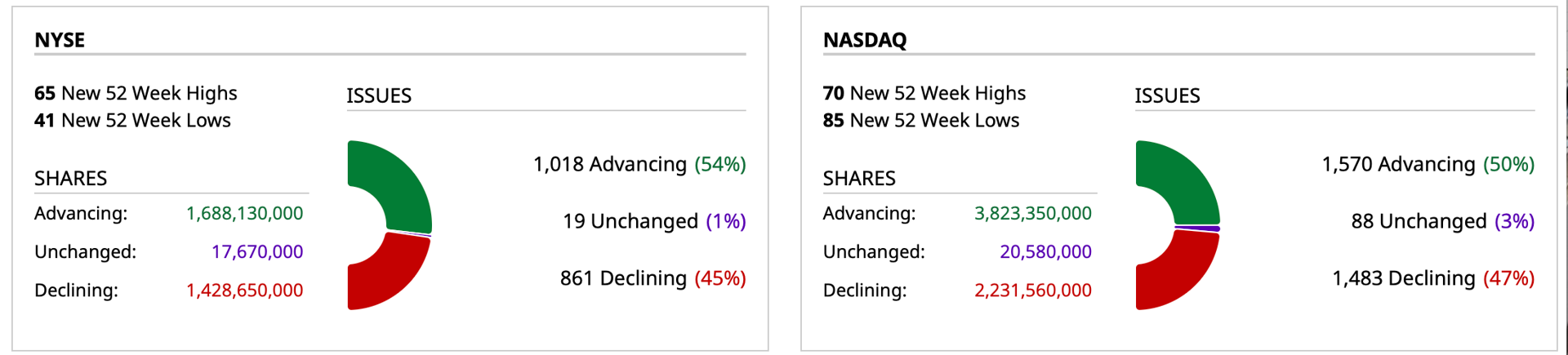

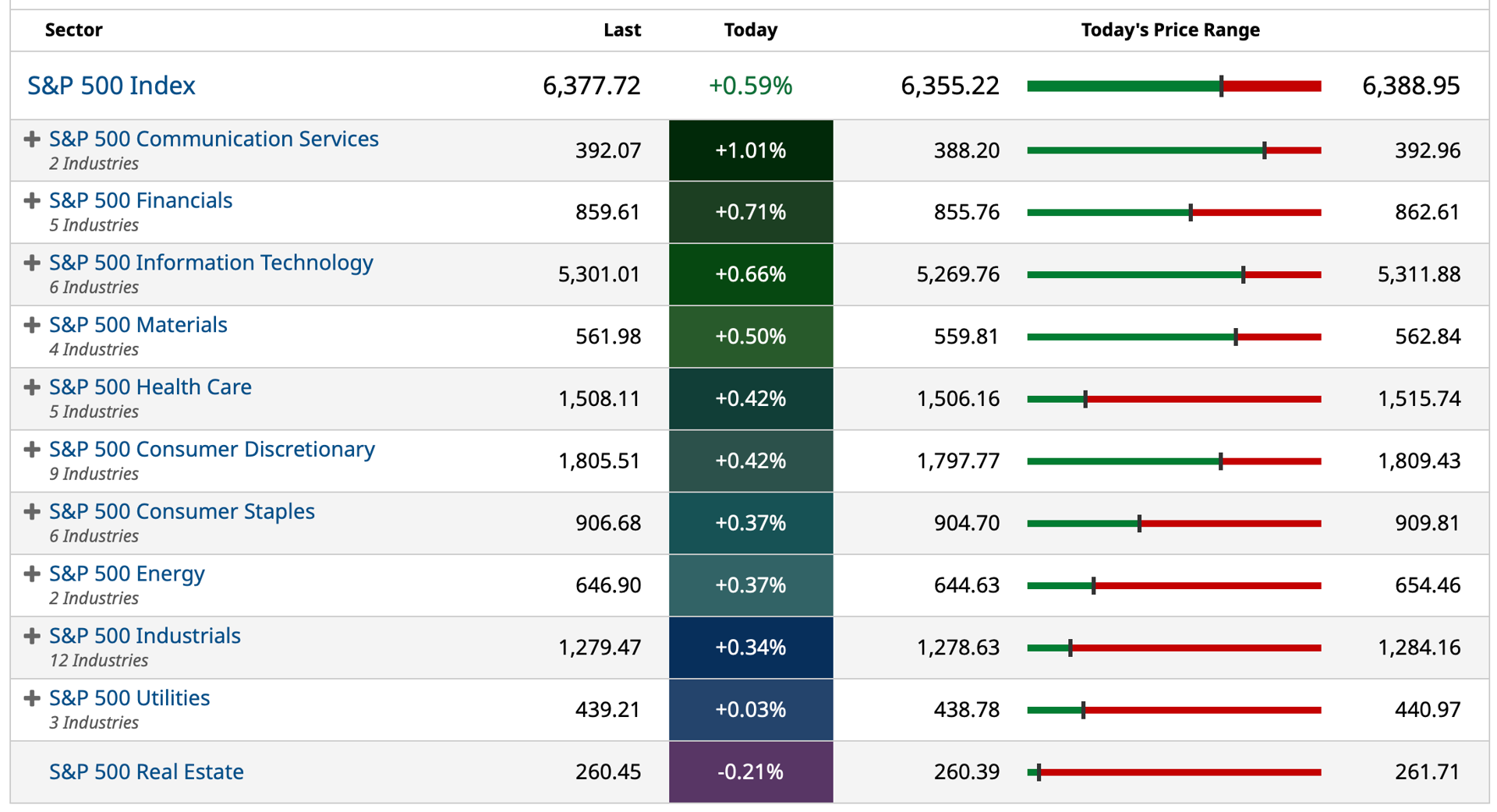

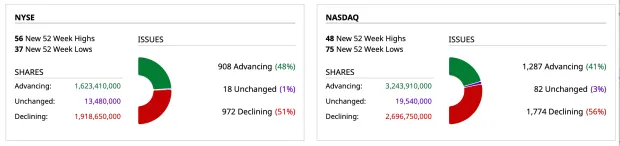

Besides my fundamental concerns, the primary and unhealthy divergence I am seeing is poor breadth, which has occurred repeatedly in the last 1-2 weeks and did again Wednesday and Thursday.

On Wednesday when the averages climbed briskly breadth was conspicuously weak:

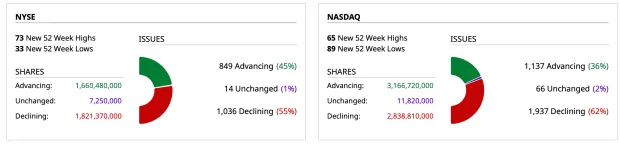

Same held for yesterday — though the averages were not as strong as the prior day:

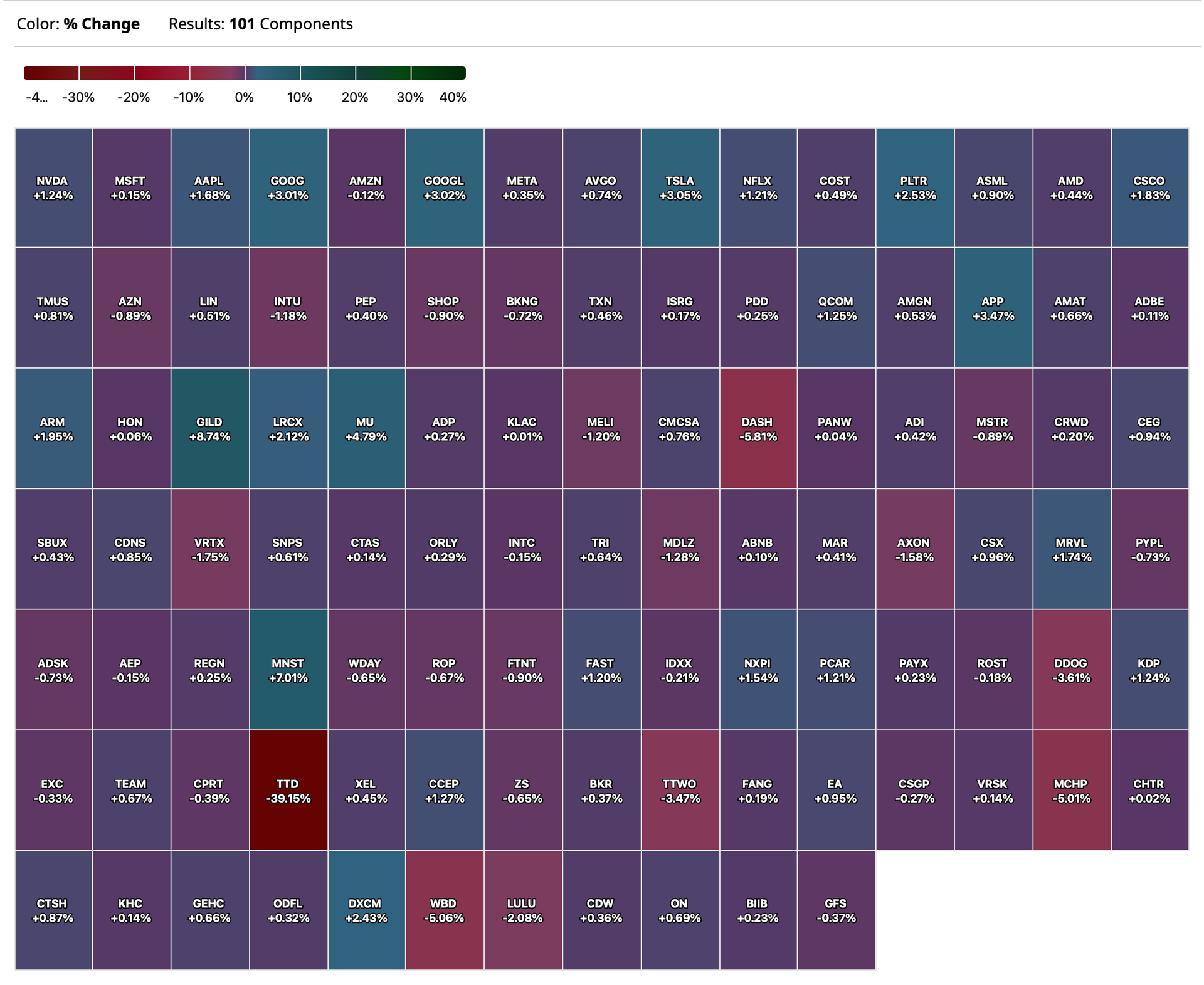

Late yesterday, when S&P cash was -30 handles (after being +50 handles in the early going, when I was shorting) I covered all my short index hedges (see below). My key take and why I covered was the continued strength of the annointed (Congregation P) — particularly Nvidia NVDA and Palantir PLTR (which dropped $3-$4/share each but were still hanging in positively).

Since then (at around 3:15 PM Thursday afternoon) stock futures commenced a rally of +35 handles by the close and have rallied by another 17 handles since then.

I have begun to reestablish my index shorts (on a scale — at around 5:30 AM):

* SPY $634.07

* QQQ $571.02

From yesterday:

With S&P cash -30 handles, I am now out of all of my Index (short positions) - common and calls:

* (SPY) $629.57

* (QQQ) $565.57

I plan to re-short on strength.

Position: None

BY Doug Kass · Aug 8, 2025, 6:42 AM EDT

Wolf Street howls about the Fed's balance sheet.

BY Doug Kass · Aug 8, 2025, 6:32 AM EDT

Doomberg on "energy-rich Australia hurtling toward grid collapse."

BY Doug Kass · Aug 8, 2025, 6:25 AM EDT

BY Doug Kass · Aug 8, 2025, 6:16 AM EDT

The S&P Short Range Oscillator is at -1.38% vs. -1.98%.

BY Doug Kass · Aug 8, 2025, 6:11 AM EDT