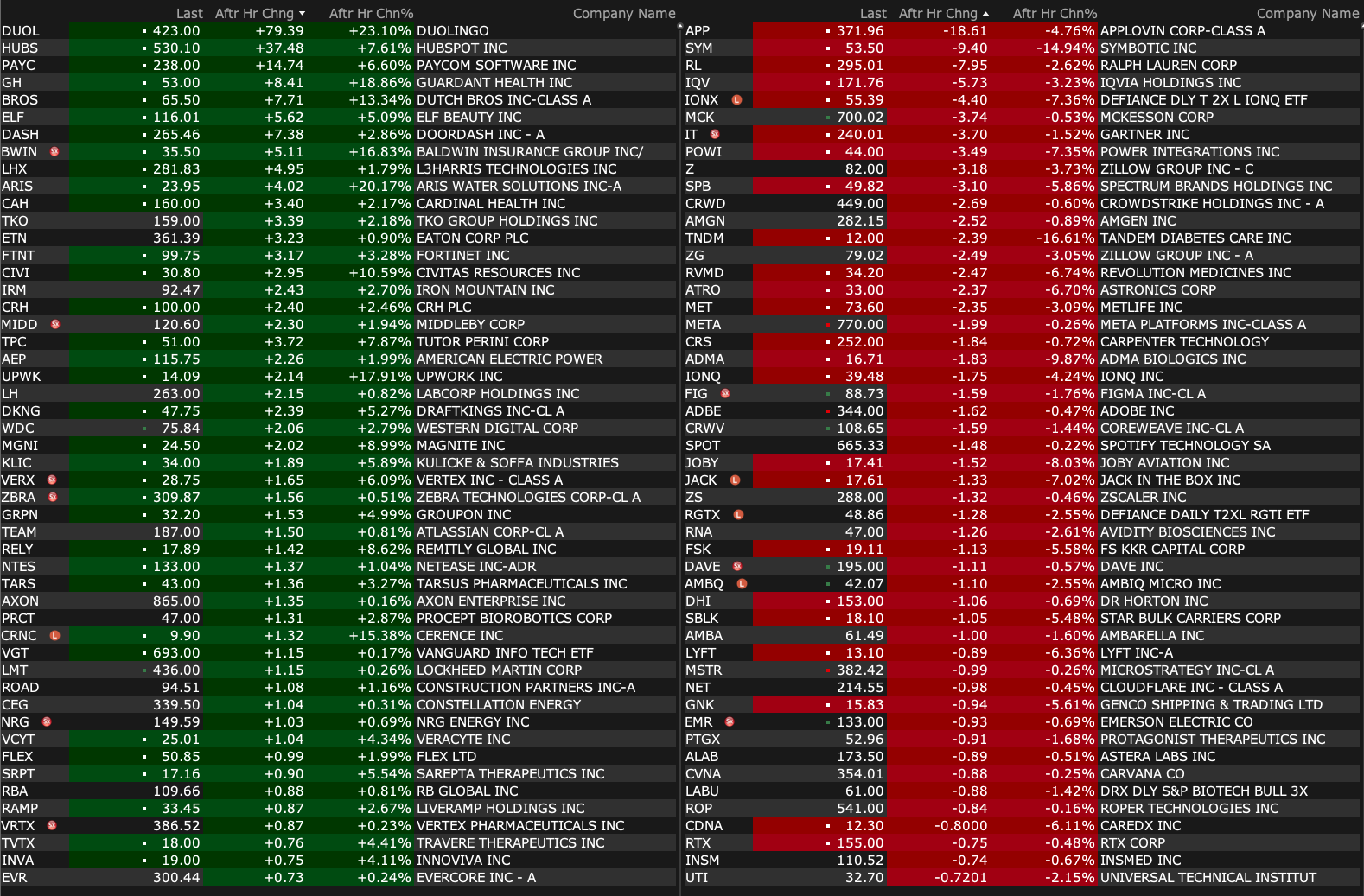

Wednesday's After-Market Movers

As of 4:17 p.m.:

BY Doug Kass · Aug 6, 2025, 4:45 PM EDT

As of 4:17 p.m.:

BY Doug Kass · Aug 6, 2025, 4:45 PM EDT

BY Doug Kass · Aug 6, 2025, 4:30 PM EDT

* Color me frustrated...

BY Doug Kass · Aug 6, 2025, 3:26 PM EDT

BY Doug Kass · Aug 6, 2025, 3:19 PM EDT

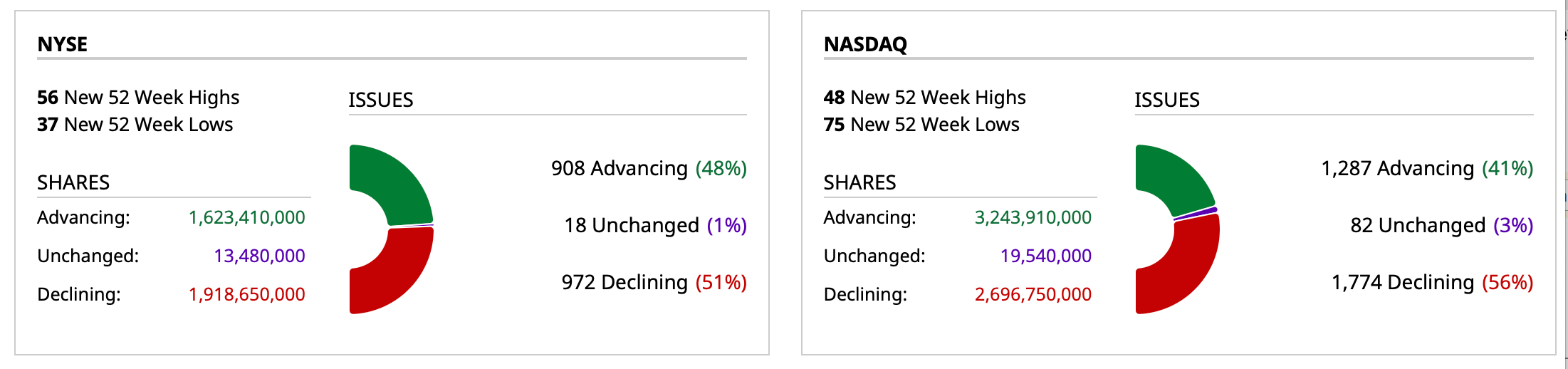

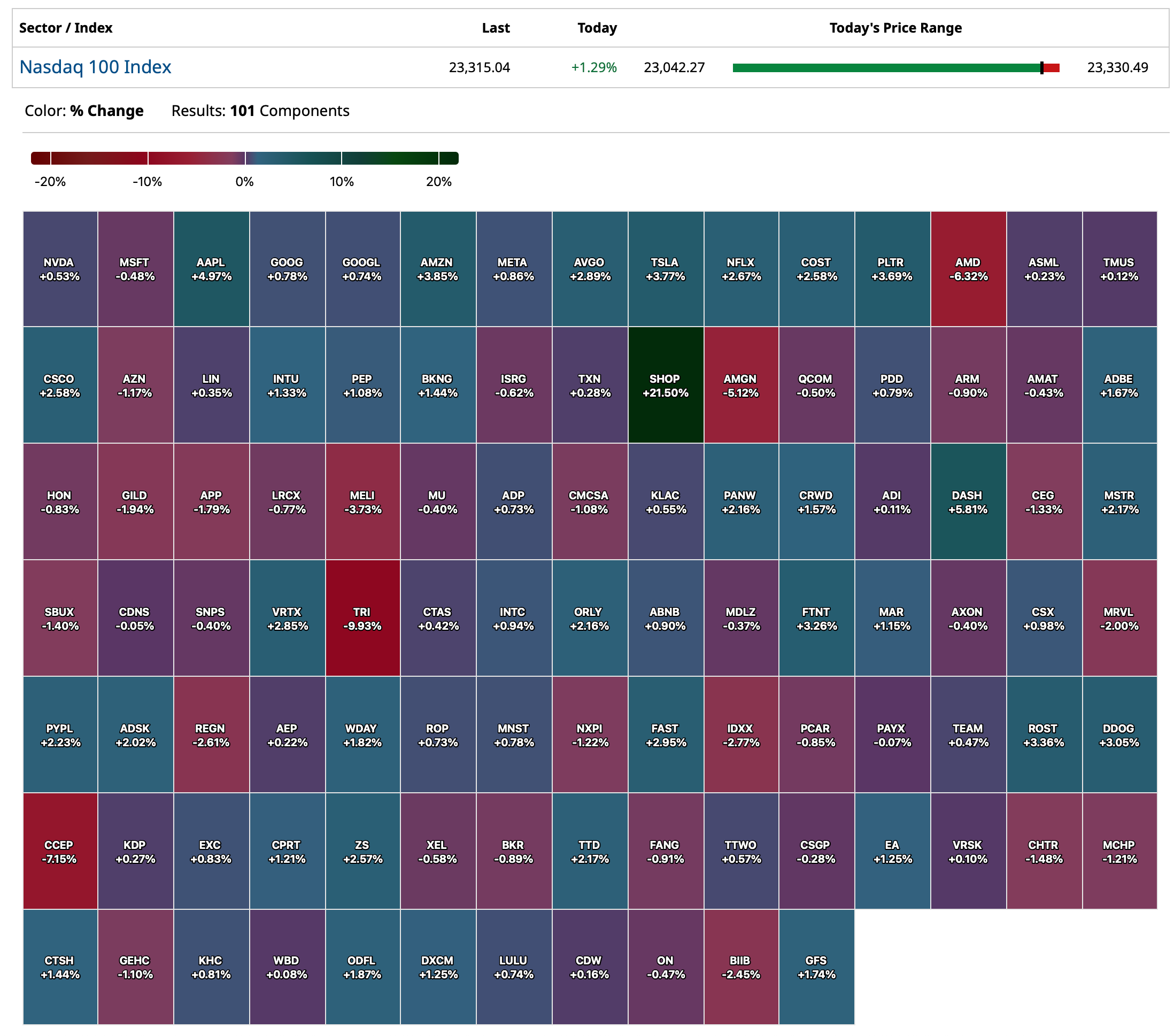

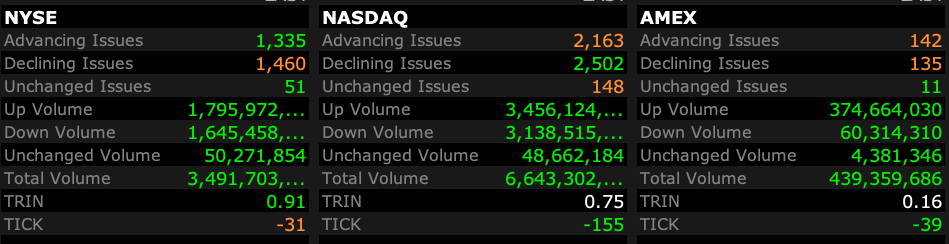

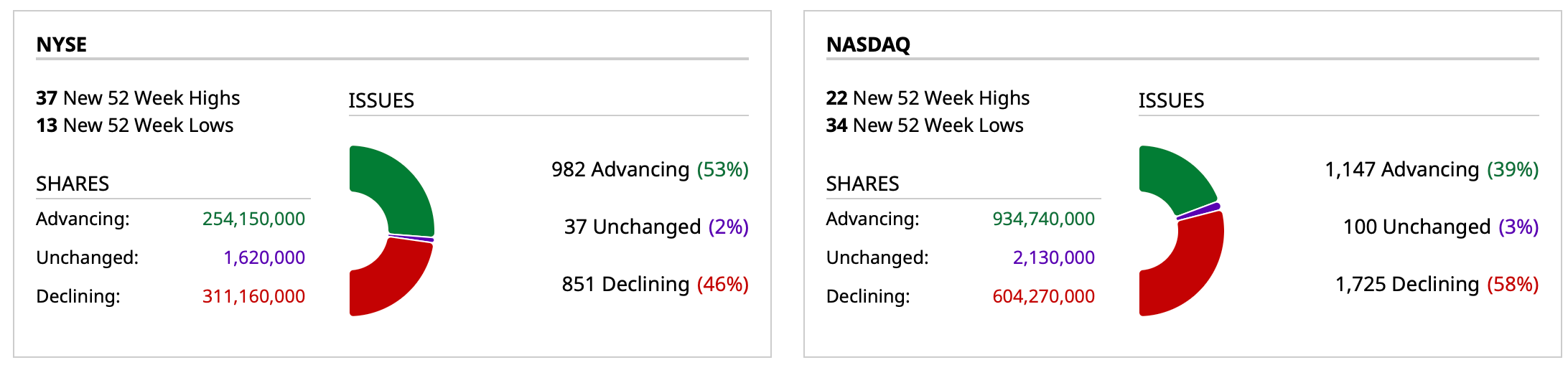

Another day, another advance in the indices while market breadth (on both the NYSE and Nasdaq) are negative:

Normally, I would consider buying a value stock like Disney DIS (-$3), but why bother? (Not a rhetorical question!)

Market participants are focused on a narrow sector of the market (technology) at the expense of everything else.

As a I mentioned earlier in my Diary, panelists on the FIN TV shows no longer bother discussing fundamentals.

They are not even faking it anymore.

This will end horribly, but I don't know the timing.

BY Doug Kass · Aug 6, 2025, 3:11 PM EDT

BY Doug Kass · Aug 6, 2025, 2:51 PM EDT

From Peter Boockvar:

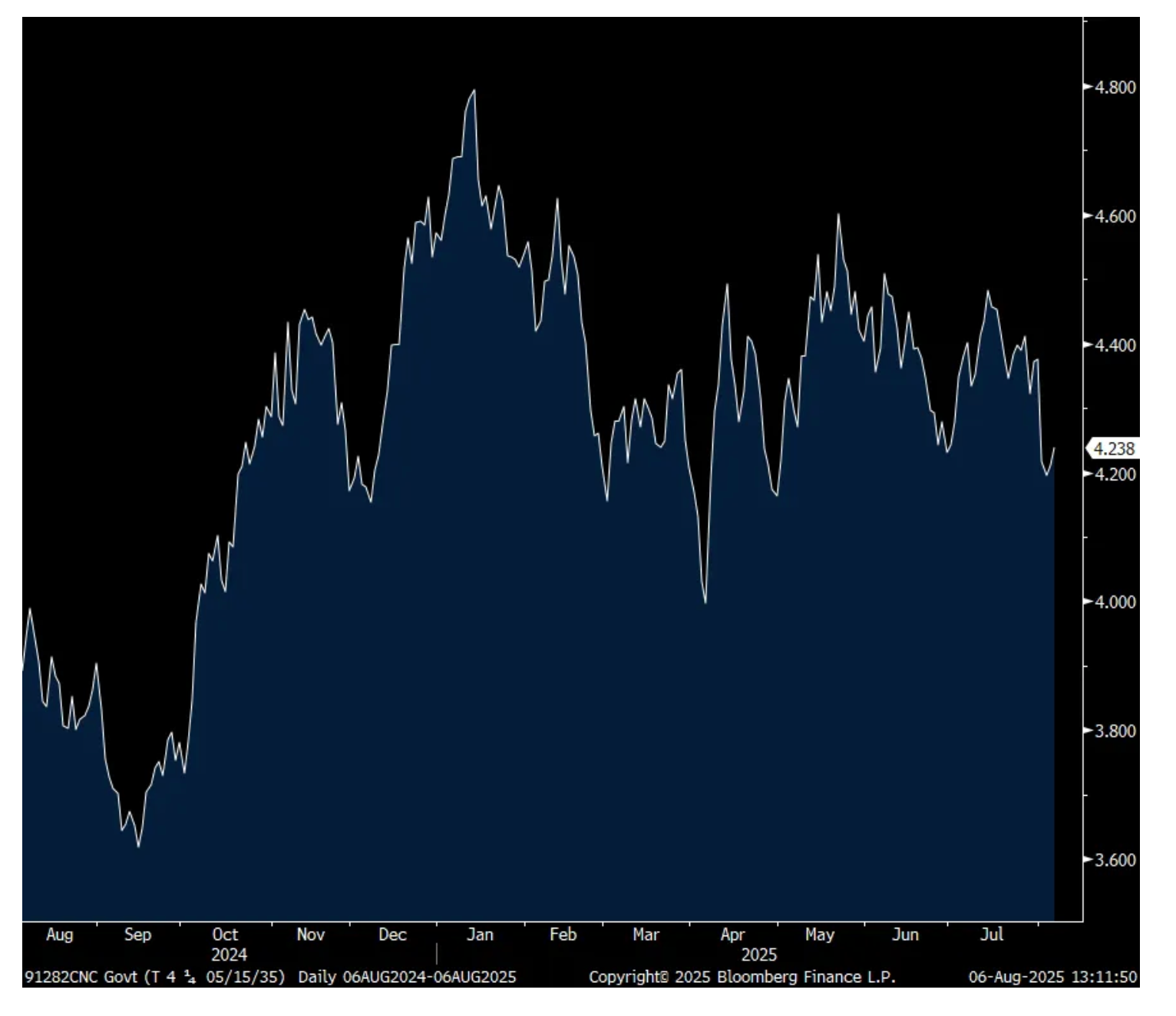

Questions about the integrity of the economic data, who will replace Fed Governor Adriana Kugler, what’s the state of the US economy, is the Fed going to cut in September, will tariffs make it thru judiciary review at the Federal appeals court, etc…all thoughts swirling in our heads and the precursor to the 10 yr note auction today. That auction, with the context too of a notable drop in yields on Friday, was pretty weak. The yield of 4.255% was about 1 bp above the when issued. The bid to cover of 2.35 was well below the previous one year average of 2.56 and the lowest since August 2024. Also, dealers were left with 16% of the auction, the most since August 2024.

Bottom line, I really only write about the 10 yr auction now because of its benchmark nature and today’s results were poor. If only we can ask the participants the reasoning for their lack of participation. Yields are at the highs of the day in response but still off last week’s highs. Key levels remain 4.5% in the 10 yr yield and 5% in the 30 yr.

10 yr Yield

BY Doug Kass · Aug 6, 2025, 2:45 PM EDT

From Oaktree: "Still Special?"

BY Doug Kass · Aug 6, 2025, 2:25 PM EDT

As of 1:48 p.m.:

BY Doug Kass · Aug 6, 2025, 2:10 PM EDT

* As I venture into the belly of the beast...

I am pressing my PLTR short — as well as some other speculative beauts (including GRNY).

BY Doug Kass · Aug 6, 2025, 1:56 PM EDT

BY Doug Kass · Aug 6, 2025, 1:16 PM EDT

On the climb higher to +47 handles we expanded our index shorts:

* SPY $632.68

* QQQ $566.04

P.S.: It's funny on the shows that panelists no longer discuss fundamentals and don't care about fundamentals — as they almost all worship at the altar of price.

This was my theme in yesterday's opener.

History shows this ends poorly.

BY Doug Kass · Aug 6, 2025, 1:00 PM EDT

Dougie Kass

Reshorting AAPL $214.46

BY Doug Kass · Aug 6, 2025, 11:55 AM EDT

* Some curious math...

Open AI is selling more stock.

It is just amazing the valuation keeps going up, from $300 billion last round to $500 billion this round, even when the round is entirely sales of equity from the insiders at Open AI. Wonder why they would want to do that? No capital even going back into the business. Yet I am sure the whole round will be hoovered right up. Never seen anything like this.

Not to mention, Open AI is a theoretical non profit. So investors are paying $500 billion for what, exactly? Hmmmm.

It also claims to have 700 million daily active users. The population of the U.S. is 350 million. The population of the EU is 450 million. That is 800 million total people. If you got rid of people under 10 and over 65, probably brings the number down to 650 million. If you went between 25-54 (the hot demographic) you get 320 million people. Good to know they have more daily active users than the entire available market in the U.S. and the EU – and about two-times the active daily users as the hot demographic that advertisers care about.

Of course the 20 other large language models will also probably tell you they too have 700 million daily active users. So we are up to two-times the population of the whole world in daily active users, and five-times the total population in the world of people between 25-54.

OpenAI eyes $500 billion valuation in potential employee share sale, source says

BY Doug Kass · Aug 6, 2025, 11:30 AM EDT

When I see this sort of speculative fever (coupled with divergences in the averages, Nasdaq up and IWM, RSP down), I become interested in expanding my short book.

And that is exactly what I am doing with S&P cash +29 handles.

BY Doug Kass · Aug 6, 2025, 11:15 AM EDT

- NYSE volume 2% above its one-month average;

- Nasdaq volume 19% below its one-month average;

- VIX index: down 4.82% to 16.99

BY Doug Kass · Aug 6, 2025, 11:05 AM EDT

* In the early going...

Here are today's early morning things:

With S&P cash +25 handles I am back reestablishing or adding to shorts:

* Shorting SPY $630.45 (and calls)

* Shorting QQQ $563.61 (and calls)

* Adding to GRNY short at $23.45

* Adding to JOET short at $41.00

* Adding to NVDA short at $178.89

* Adding to PLTR short at $175.13

BY Doug Kass · Aug 6, 2025, 10:24 AM EDT

From Peter Boockvar:

You've read me for many weeks now talking about the continued drop in the US crude oil rig count as a possible offset to the continued OPEC oil production quota increases. Reuters published a story yesterday titled "Sliding US rig count outpaces efficiency gains, threatening onshore oil output." In it the piece said, "The falling number of oil and gas rigs deployed across the United States is reaching a level that would indicate onshore crude output from the world's top producer could fall in early 2026." They do go on to talk about the greater productivity of existing wells and with new technologies "But the number of rigs working in US shale fields has almost fallen so low - and is projected to keep falling - that those improvements will not be enough to keep onshore US production rising, or even steady in some basins, analysts say."

Finally, a quote from Brandon Myers in the article, head of research at Novi Labs, "We have seen a 25% improvement over the last few years in rig efficiency, but the rig count has fallen over 30% over that same period. Put simply, the rig count declines have begun to outpace drilling efficiency gains."

Food for more thought and we remain bullish and long oil and gas stocks.

Now on to some earnings calls because there were a bunch of note and the economic story remains the muddied same.

From Gartner, the IT research and analytics firm and whose stock plunged by 28% yesterday:

They first highlighted on their call the increase in AI related consulting that they're doing. "Clients see large potential in AI and they need help in determining the best way to capture that potential." Cybersecurity too among some other areas.

However, "We also experienced some headwinds during Q2. Measures of CEO confidence fell to recessionary levels, among the fastest drops ever recorded. In a Gartner survey, 78% of CEOs indicated they're implementing cost cutting measures to safeguard performance...The largest headwind in Q2 was the US federal government. Initiatives from the DOGE made it more challenging for clients to purchase or renew many of our products. In addition, there were impacts from tariff policies. With the prospect of higher tariffs, many companies implemented strong cost saving measures. Even companies not directly impacted by tariffs began implementing these measures."

Also, "Purchase decisions that were previously made by functional leaders are now being escalated to the CFO or even the CEO. These changes occurred at a record pace, impacting our performance during Q2."

From Marriott:

The numbers in Europe, APAC and the Middle East seemed solid but in the US and Canada regions, RevPAR was flat y/o/y and "grew nearly 1% when adjusting for the Easter shift. RevPAR growth was again strongest at the high-end, with luxury RevPAR up 4% and it weakened going down the chain scales, where results came in below our prior expectations." Highlighting again the bifurcated US consumer.

Also, "Second quarter US and Canada select service and extended stay RevPAR declined around 1.5% y/o/y, primarily due to a decline in government demand as two-thirds of government revenues are in the select service segment, as well as weaker demand from smaller business customers."

"Looking at RevPAR by customer segment, leisure transient grew the fastest this quarter, with leisure transient RevPAR rising 3% globally and 1% in the US and Canada. Group RevPAR rose 2% globally and 1% in the US and Canada. Second quarter business transient RevPAR declined 2% globally and in the US and Canada, in part because of a shift in Easter timing."

"With ongoing economic uncertainty, we now estimate full year RevPAR growth to be in the lower end of our prior range and increase between 1.5% and 2.5% over last year."

From Yum Brands, the owner of KFC, Taco Bell (drives 80% of their profit), Pizza Hut and Habit Burger & Grill:

With KFC, international comps did the best, "driven by strong performance in key markets, including South Africa, Spain, Canada, Japan, and the UK."

Also with KFC, "Even with solid overall top line performance, we have opportunities to improve performance in underperforming regions such as the US and parts of Europe, where challenges stem from gaps in value perception, inconsistent consumer experience, and innovation that has not fully resonated with consumers."

"Taco Bell delivered 4% same store sales growth, outpacing the limited service category in the US by 4 percentage points."

With Pizza Hut, "an insufficient value message amid a competitive value landscape resulted in transaction softness." International outperformed the US.

Comps fell at Habit Burger and "The decline reflects continued softness in consumer demand with some impacts associated with the recent events in the LA area."

On the overall consumer, "The data that we look at about the consumer behavior shows clear trade in from consumers in fast casual into the Taco Bell brand. And when you even pull apart the income bands, although I know that the lower income consumers are pulling back, that's been well documented by our competitors, we aren't seeing that at Taco Bell. In fact, if you pull all the income bands in Q2, we've had sales and transaction growth across all income bands at Taco Bell very consistently, very little difference from one income band to another."

From the McDonald's earnings release and whose comps were above expectations and stock is up pre-market:

"Our 6% global Systemwide sales growth this quarter is a testament to the power of compelling value, standout marketing, and menu innovation."

Specifically in the US, "comp sales results were primarily driven by positive check growth."

From Upstart, the online lending marketplace:

Broadly on the consumer, "I think we've been consistent in saying that the American consumer in aggregate is probably overspending relative to the income levels that they're earning, and that's been true for a while now."

From Caterpillar and whose revenue fell 1% y/o/y:

"We continue to see strong orders across our segments as demand remains resilient, supported by infrastructure spending and growing energy needs."

"The net incremental impact from tariffs was around the top end of our estimated $250 million to $350 million range for the quarter." For all of 2025, "we expect the net impact from incremental tariffs for 2025 will be around $1.3 billion to $1.5 billion, net of some mitigating actions and cost controls."

These are big numbers US companies are eating.

From Eaton, whose stock has become an AI infrastructure play but their guidance was more muted than expected and why it fell 7% yesterday:

"Demand in our aerospace business remains very strong." And also in their electrical business as "Organic sales growth of 12% was driven primarily by strength in data centers, up about 50%, along with strength in commercial and institutional end markets."

Their vehicle business saw a drop in sales, "primarily driven by weaknesses in the North American truck market."

From Dupont, the specialty chemicals giant:

Sales grew 2% y/o/y organically and "saw continued strength in electronics driven by AI technology demand in both Interconnect Solutions and Semi, and strong volume growth in healthcare and water. This momentum is continuing into the third quarter with order patterns remaining strong through July."

"Weakness in construction continued to impact our Diversified Industrials business during the quarter."

On the overall macro, "What I would say is that we continue to be in a fairly mixed environment. Really, all of the growth so far for the last several quarters is really coming from AI driven applications across advanced nodes, advanced packaging and data center."

"Most of the rest of the electronics economy kind of remains relatively weak. I think we're starting to see the green shoots of stabilization and recovery on the lagging edge parts of the market, and we expect kind of slow improvement as we move through the back half of the year for the more industrial focused, lagging edge semiconductor nodes."

"And then, we still have a relatively weak consumer environment where consumer devices are expected to be up kind of low single digit."

From Cummins:

"We see a marked contrast in demand between longer cycle sectors such as power generation, which also continues to benefit from some well established secular themes and declining confidence in some of our more economically sensitive shorter cycle markets in North America, particularly truck, pickup and consumer related markets. We anticipate this contrast will become more pronounced in the second half of the year."

With power generation in particular, the 25% revenue growth was "driven primarily by continued strong demand in data centers and mission critical applications."

On the flip side, "we expect North America heavy and medium duty truck volumes to decline 25% to 30% from second quarter levels. As we have seen truck orders recently reach multi year lows and OEMs have initiated reduced work weeks through the next three months."

"Tariffs are undoubtedly having an impact on Cummins, our suppliers, customers and end users, creating uncertainty over freight activity linked to the movement of goods and increasing costs. We did experience increasing tariff costs in the second quarter. However, as anticipated, we did not see the full impact of the current policies as supply chains work through existing inventory."

They are not giving full year guidance as "Persistent economic and regulatory uncertainty continues to impact a number of our key markets and cloud our near-term outlook for both business and market performance."

The MBA said that the average 30 yr mortgage rate dipped by 6 bps to 6.77% which is back to a one month low and that helped to lift refi's by 5.2% w/o/w after 3 weeks of declines. Purchases rose 1.5% w/o/w after some volatile weeks over the past month.

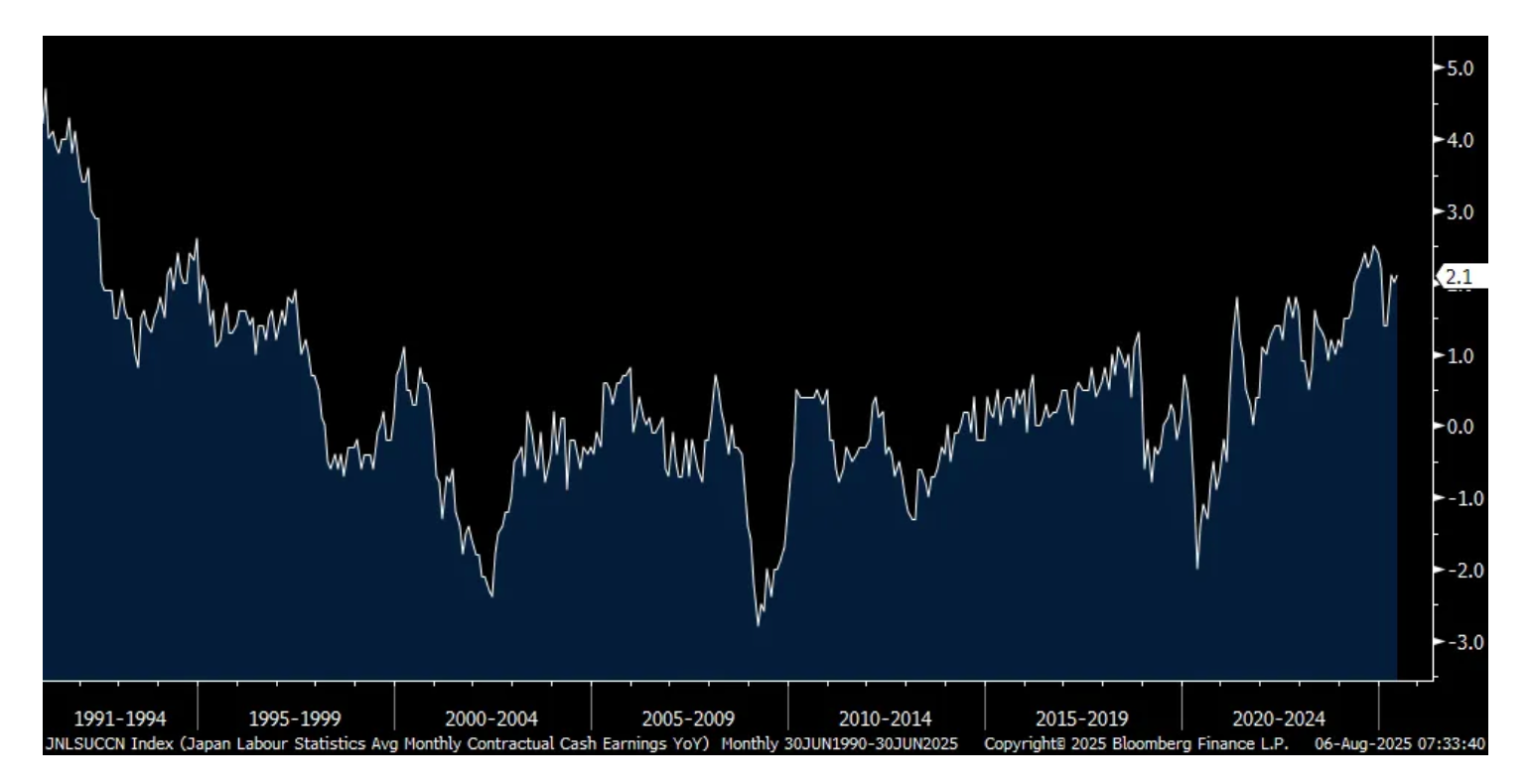

The BoJ was given another reason to hike rates as base pay in June in Japan rose 2.1% y/o/y, just off the best levels since the mid 1990's. That though still remains below the rate of inflation and why the populace is upset and voted their frustration a few weeks ago. JGB yields lifted in response.

Base Pay in Japan y/o/y

German factory orders were weak in June, down 1% m/o/m vs the estimate of up 1.1% (and partly offset by a 6 tenths upward revision to May) with particular softness in the orders from foreign countries outside of the Eurozone where orders declined by 7.8%, though follows a 7.6% rise in May. All tariff distorted figures but the economy ministry said "In light of the now likely permanent increase in tariffs on exports to the US, the industrial sector is likely to be characterized by subdued foreign demand in the future."

BY Doug Kass · Aug 6, 2025, 10:15 AM EDT

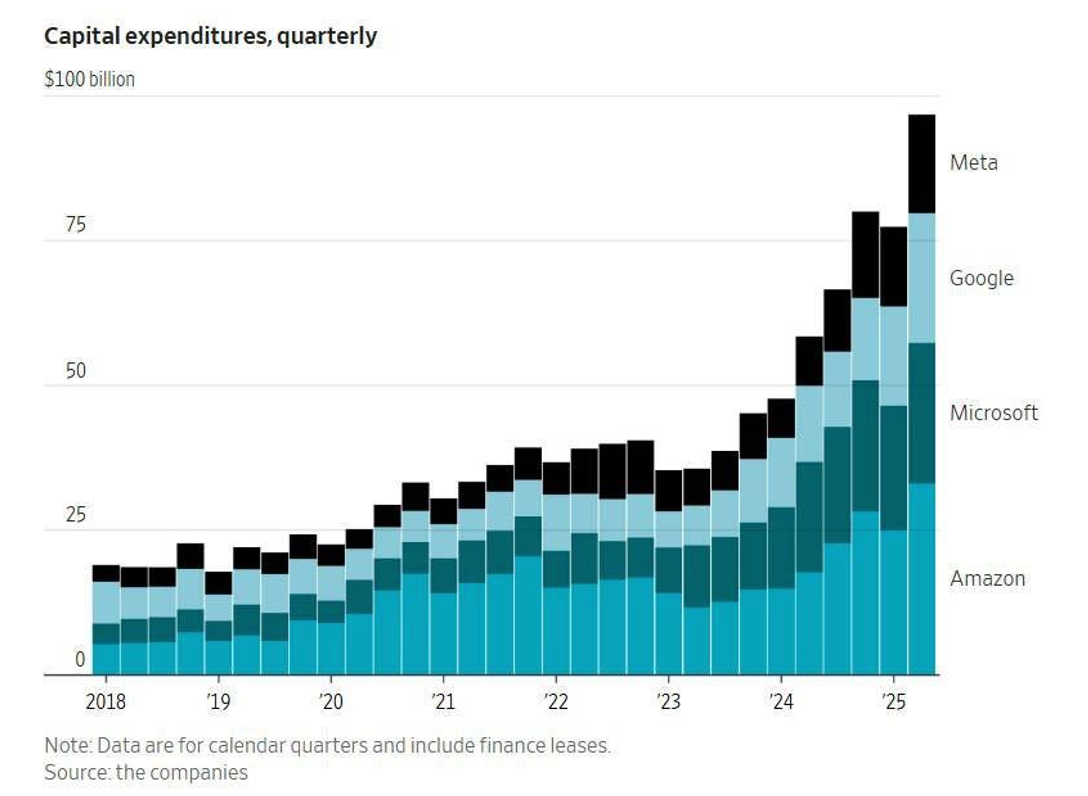

* As the hyperscalers morph from capital-light to capital-intensive businesses, shouldn't their valuations suffer?

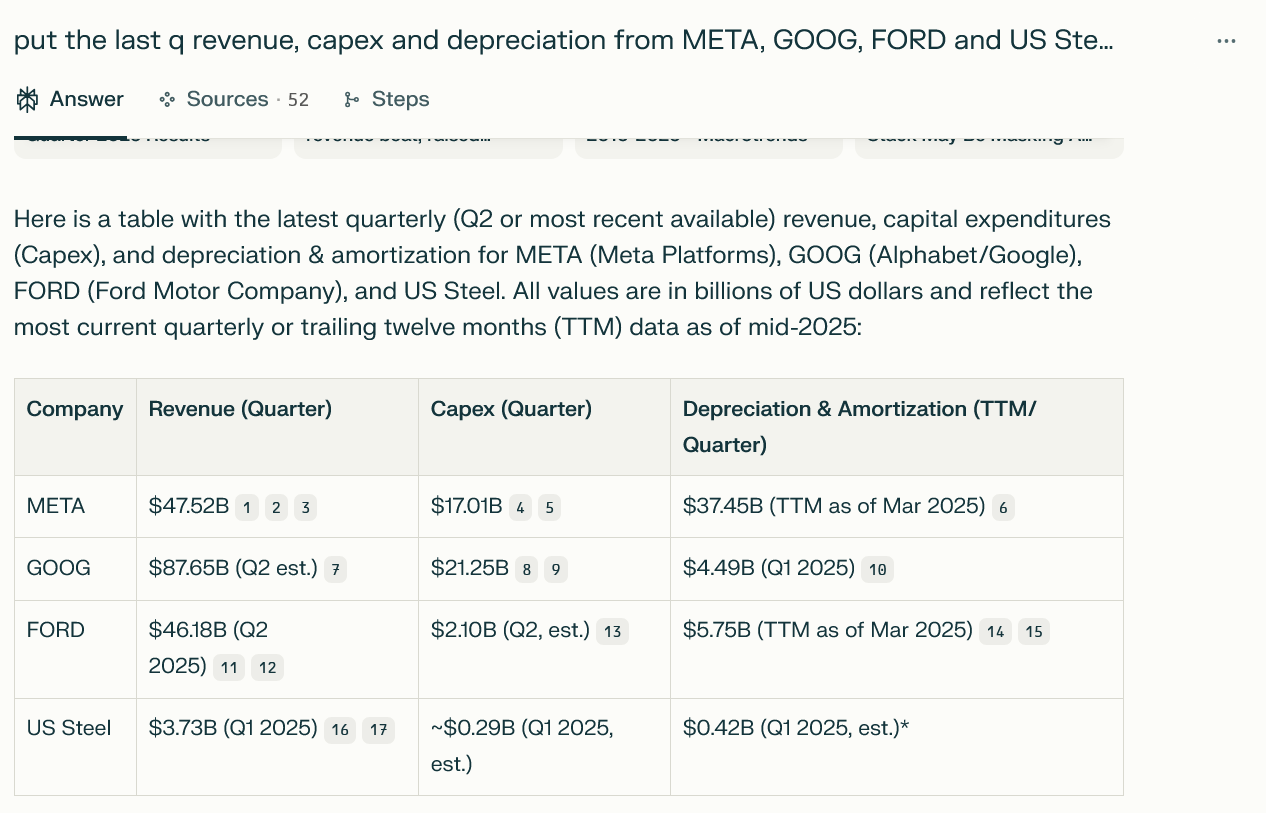

Per my prior "More Tales From Nvidia" on the huge CAPEX outlays from the hyperscalers, I did the following analysis.

I did not ask the AI to help, because I have tried before, and it can’t do this simple stuff.

Following my (first) table is the muddled mess the AI returned, some right, some wrong. Net time loss, because I still need to check everything independently, which I knew, so just did it myself the old-fashioned way looking at the earnings reports. The data is all out there, so it is interesting the AI still screwed it up.

At any rate I compared the metrics from the most recent reported quarters of Meta META, Google GOOGL, Ford F and U.S. Steel X. Ford and U.S. Steel are obviously thought of as not only cyclical businesses, but also un-differentiated capital-intensive commodity businesses, and trade at low multiples in part because of their non-differentiated commodity like capital-intensive business models.

Well, I wonder who really are the capital-intensive non-differentiated commodity businesses now? Meta, Google, et al are monopolies in their core businesses, but they are not when it comes to generative AI. All of them, including the privates, are doing the same thing. Generative AI is a non-differentiated commodity. When seven or eight players are well funded and at scale doing the same thing, this is what you get. I cannot tell the difference in the output from any of them.

Heck, it is worse, throw in all the Chinese doing it too — and those guys are the low-cost providers. The low-cost providers win in a commodity business. This is why Open AI loses money hand over fist. They are a pure play on the economics of generative AI. And they get the benefit of CoreWeave CRWV losing money on whatever those guys provide to them too, so it is even worse than it looks.

Here are some observations:

-CAPEX as a % of revenue is now ~30% of revenue for the hyperscalers, compared to 7% of revenue for the crappy old economy businesses.

-CAPEX for the hyperscalers is now running at over 4x their reported D&A (and the depreciation schedules are a joke). CAPEX for the crappy old economy businesses is roughly consistent with their D&A.

With all of massive amounts of CAPEX, it is amazing Advanced Micro Devices AMD could miss earnings, with revenue upside. This is a business where revenue upside should have a massive impact to the bottom line. I have some suspicions, but I guess time will tell.

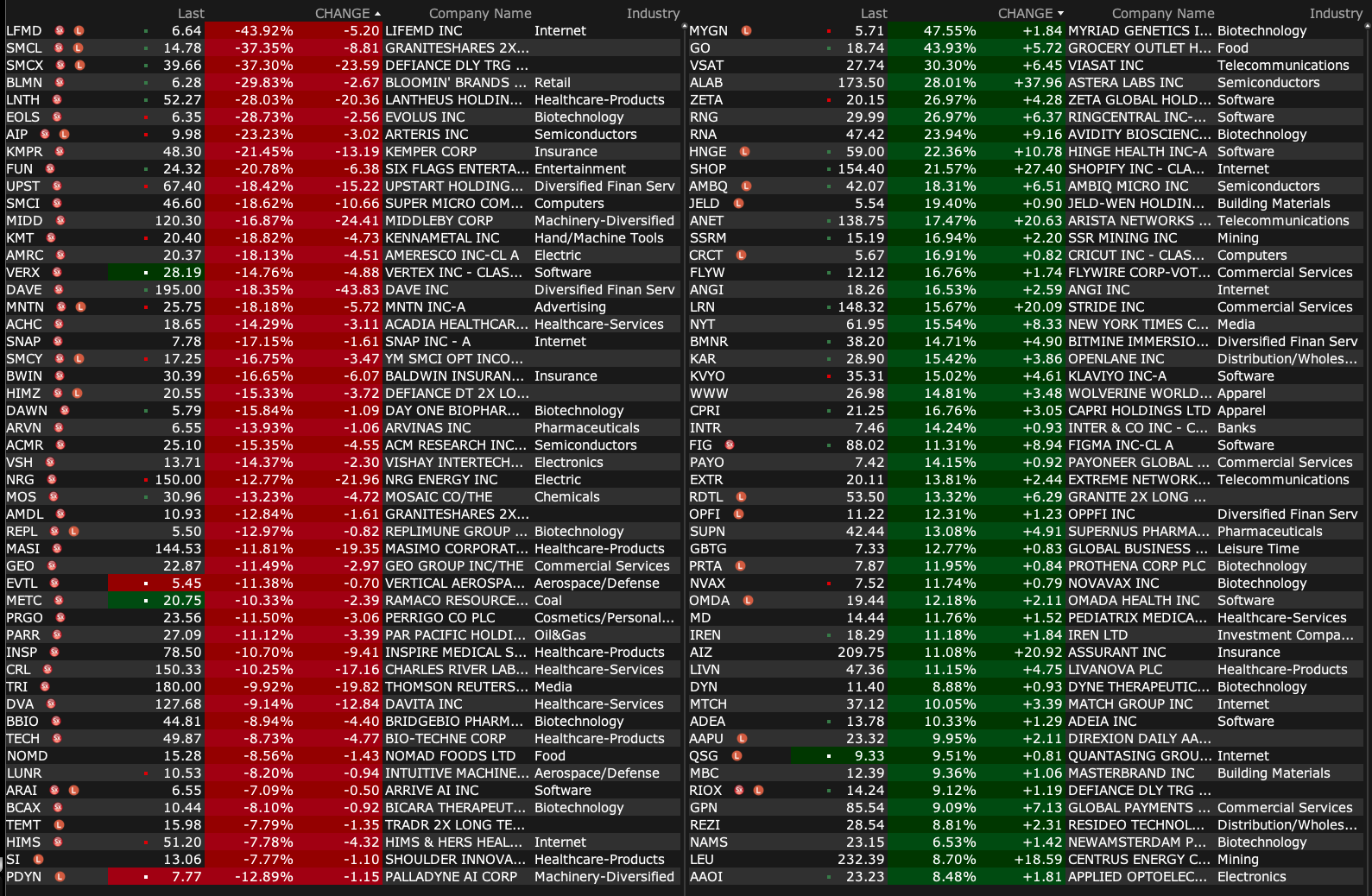

BY Doug Kass · Aug 6, 2025, 9:30 AM EDT

-GO +24% (earnings, guidance)

-ALAB +20% (earnings, guidance)

-PRCH +19% (earnings, guidance)

-CRCT +18% (earnings)

-PAYO +18% (earnings, guidance)

-KVYO +14% (earnings, guidance)

-SHOP +14% (earnings, guidance)

-CPRI +11% (earnings, guidance)

-HNGE +10% (earnings, guidance)

-EXTR +7.5% (earnings, guidance)

-TBLA +6.6% (earnings, guidance; announces $200M share repurchase expansion)

-TRMB +6.5% (earnings, guidance)

-GPN +5.8% (earnings, guidance)

-NYT +5.0% (earnings, guidance)

-ACTU +4.7% (to collaborate with Incyte Corporation and the University of Pittsburgh on Clinical Trial of Elraglusib in Combination with Retifanlimab and mFOLFIRINOX in Patients with Advanced Pancreatic Cancer)

-GEO +4.5% (earnings, guidance)

-RVLV +4.1% (earnings, guidance)

-DT +3.9% (earnings, guidance)

-MCD +3.8% (earnings, guidance)

-OC +3.7% (earnings, guidance)

-TKO +3.4% (ESPN, WWE Reach Landmark Rights Agreement as ESPN Platforms Become Exclusive U.S. Domestic Home of All WWE Premium Live Events, Including WrestleMania, Starting in 2026)

-AMWD +3.2% (MasterBrand and American Woodmark to Combine in an All-Stock Transaction' Combined company would have a pro forma equity value of $2.4B and an EV of $3.6B)

-CG +3.2% (earnings)

-HMC +2.8% (earnings, guidance)

-BCO +2.2% (earnings, guidance)

-LFMD -32% (earnings, guidance)

-LNTH -28% (earnings, guidance)

-KMT -22% (earnings, guidance)

-SNAP -19% (earnings, guidance)

-SMCI -17% (earnings, guidance)

-METC -16% (prices 10.7M shares at $18.75/share [upsized to $200M from $150M])

-FUN -15% (earnings, guidance; CEO to step down)

-ACMR -12% (earnings, guidance)

-POWL -11% (earnings)

-PSN -10% (earnings, guidance)

-VLN -9.9% (earnings, guidance)

-VERX -9.3% (earnings, guidance)

-CCEP -8.6% (earnings, guidance)

-EMR -7.2% (earnings, guidance)

-LCID -7.0% (earnings, guidance)

-MOS -5.7% (earnings, guidance)

-AMD -5.6% (earnings, guidance)

-NRG -4.6% (earnings, guidance)

-U -4.4% (earnings, guidance)

-PRGO -4.3% (earnings, guidance)

-UPST -2.8% (earnings, guidance)

-VSAT -2.8% (earnings, guidance)

-DIS -2.5% (earnings, guidance; confirms ESPN and the NFL reach new licensing agreements, extending ESPN’s NFL Draft rights and, separately, adding NFL programming and content to ESPN’s upcoming Direct-to-Consumer (DTC) service, as well as to Disney+)

-CPNG -2.4% (earnings)

-NVO -2.1% (earnings, guidance)

-OSCR -2.0% (earnings, guidance)

BY Doug Kass · Aug 6, 2025, 9:15 AM EDT

3:10 p.m. Fed Bank of San Francisco President Daly (Non-Voter) speaks and participates in a moderated conversation before the 2025 Anchorage Economic Summit hosted by the Anchorage Economic Development Corporation (AEDC), Anchoarage, Alaska (embargoed text expected.

Livestream is available here.

BY Doug Kass · Aug 6, 2025, 9:01 AM EDT

BY Doug Kass · Aug 6, 2025, 8:51 AM EDT

From JPMorgan:

US: Futs are higher as the market shakes off economic concerns raised by NFP/ISM. Pre-mkt, Mag7 names are mostly higher while Semis are dragged with AMD/SMCI earnings. DIS/UBER highlight pre-mkt earnings releases; both stocks up more than 2%. Energy, Indu, HC, and Utils stronger, too. Yields are bear steepening as USD is flat for the second day. The Swiss President arrived in DC yesterday to meet with Trump. Trump preps new sanctions against Russia’s shadow tanker fleet unless Putin agrees to a cease-fire by Friday; WTI did not react to this news. Witkoff to meet with Russian officials today. Macro data releases are light with only mtge apps but keep an eye on 10Y bond auction today to see if there is any fear premium ahead of BLS / Fed replacements.

and...

JPM MARKET INTEL EQUITY & MACRO NARRATIVE

After misses in NFP and yesterday’s ISM-Srvcs, we saw the yield curve bear flatten with RTY outperform in what can be characterized as an ‘unwindy’ session. As the market prepares for next week’s CPI, we wanted to update on some topics that have arisen in recent conversations:

· EARNINGS UPDATE (FactSet here and here) – Revenue growth is printing 6.0%, earnings growth at 10.3%, with margins exceeding 12%. This compares to expectations of about 4.0% top-line growth, 4.9% bottom-line growth, with margins around 12%. Mag7 printed 25.7% vs. 13.9% expected; SPX493 printed 6.3% vs. 2.5% expected. The QTD earnings performance has increased expectations over the next three quarters: 25Q3 from 7.3% to 7.6%, 25Q4 from 6.4% to 7.0%, and 26Q1 from 10.5% to 11.0%. That said, misses are being punished more than is typical with beats being rewarded with similar magnitude as the last 10 years.

none

BY Doug Kass · Aug 6, 2025, 8:41 AM EDT

BY Doug Kass · Aug 6, 2025, 8:17 AM EDT

The "other Dougie" responds with clarity to my opener:

douglas cassel

In regards to Doug K's article about "sunlight as a disinfectant". The bad numbers used by the Fed are not an isolated phenomena. These problems are neither new nor confined to government data. My time on boards convinced me that companies had wide leeway in the manner that they present financial data to the point that trust becomes a major issue. Doug K and others have pointed out that many companies have fudged numbers, often very skillfully, to the extent that they are often useless. The erosion of trust in accounting and management is an under appreciated factor we rarely speak of.

I studied just enough statistics to understand that even bad data can be useful if systems are stable and the sampling is consistent. In fact, with things like immigration and tariffs changing things rapidly, even this simplification cannot be used.

I came to these conclusions a long time ago. IMHO these considerations must lead one to rely less, or even reject "fundamentals", as the data is bad or manipulated.

One of the reasons I am more reliant upon price is that I simply don't trust the numbers.

BY Doug Kass · Aug 6, 2025, 8:00 AM EDT

* Why be myopic about the flawed calculus of jobs... how about the absurd calculation of the phony CPI numbers?

One more little bit on the data issue, which I touched on multiple times yesterday.

I was forwarded the article below. I do not understand the myopic focus on the jobs numbers alone.

All the data matter.

That includes, of course, the CPI, which the BLS also calculates. The Mises guys, of all people, should be the first ones to realize this issue, although the author of this article seems to ignore it. More importantly, so is everyone else, including the guy squawking about the jobs data.

I understand why the current administration is not offering a peep about the CPI because they know which way the CPI is biased.

At any rate, if one data series is addressed in a vacuum, that leaves you in a place where the consequences could be worse.

This is the year 2025. There needs to be a better job done with regard to all the economic data, equally. I would start with inflation and the CPI, equally, because they are the two biggest buckets with the greatest consequences.

Whoever gets the job better be equally focused on all the data, and how it is collected and calculated. Whatever they do with regard to any changes in collection and methodologies, needs to be made fully transparent, to everyone. You let the politicians become further involved in this process, with no oversight, you know where it ends up. As it stands now China might have more realistic numbers than we do.

As to the decision making, that is a different issue. It has also been terribly flawed. It will never be perfect, but it should be better. The starting point that helps with better decision making is better data.

Sunlight is the best disinfectant.

The Fed Says It Is "Data-Driven." But the Data Isn't Any Good.

BY Doug Kass · Aug 6, 2025, 7:30 AM EDT

* A good one...

BY Doug Kass · Aug 6, 2025, 6:55 AM EDT

Bonus — Here are some great links:

Some Bad News and Some Good News

The Trend Is Still In Place, Just Catching Breath

BY Doug Kass · Aug 6, 2025, 6:30 AM EDT

The S&P Short Range Oscillator reached -0.95% vs. -0.15% — that is modestly oversold.

BY Doug Kass · Aug 6, 2025, 6:10 AM EDT

BY Doug Kass · Aug 6, 2025, 6:01 AM EDT