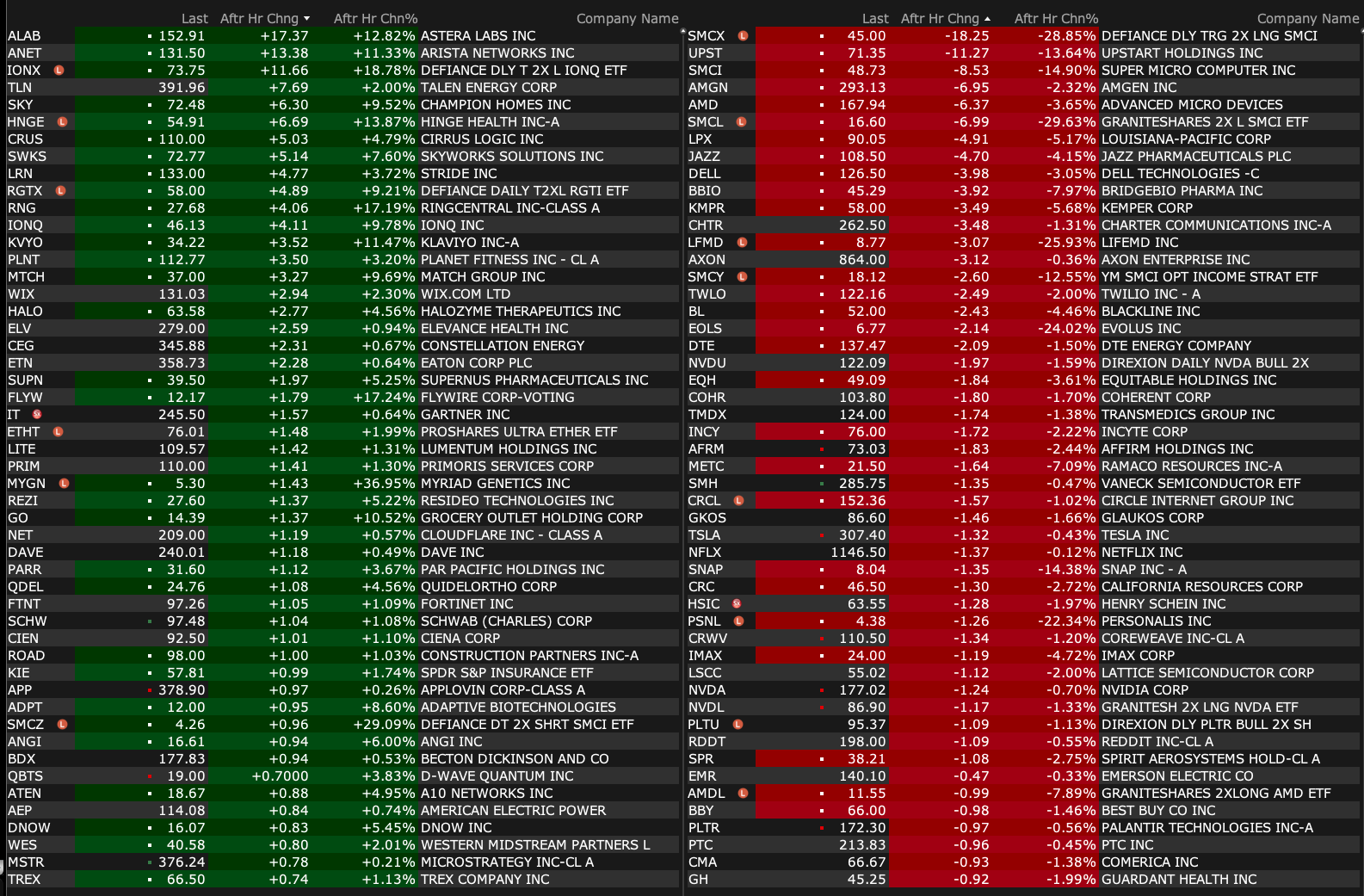

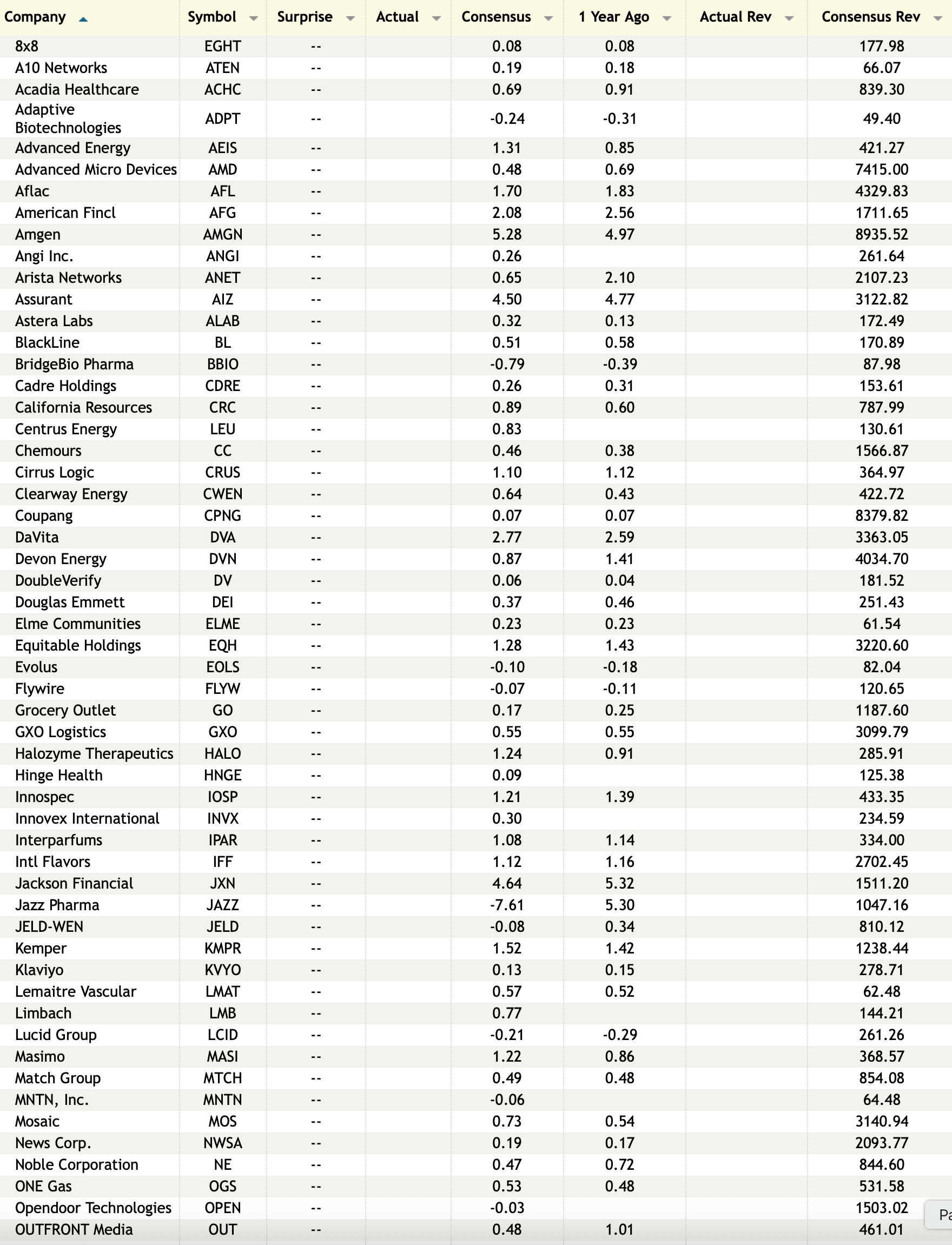

Tuesday's After-Hours Movers

As of 4:28:

BY Doug Kass · Aug 5, 2025, 4:45 PM EDT

As of 4:28:

BY Doug Kass · Aug 5, 2025, 4:45 PM EDT

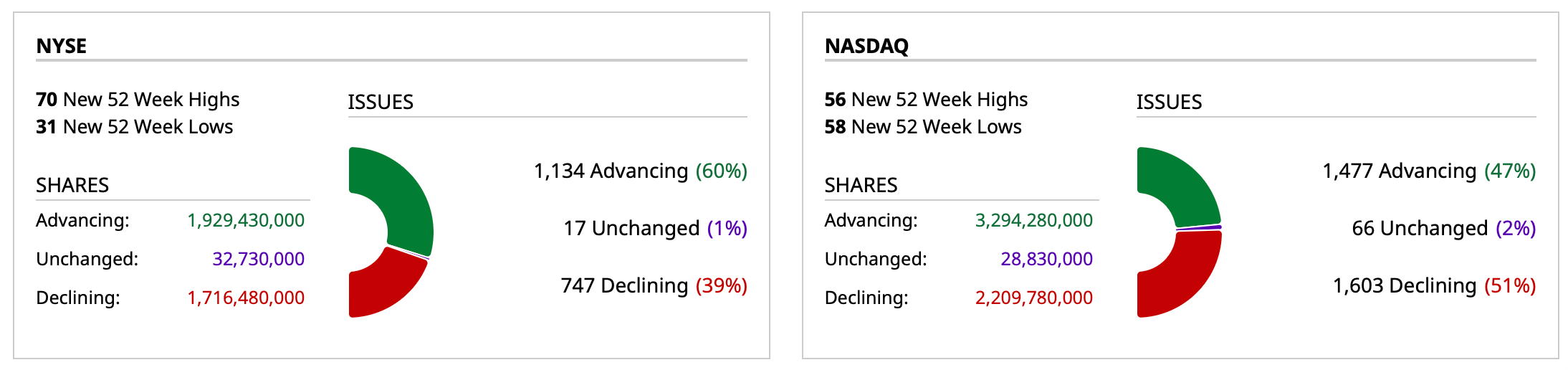

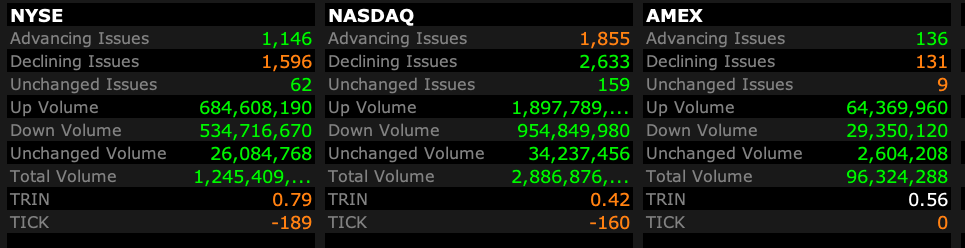

- NYSE volume 5% above its one-month average;

- NASDAQ volume 21% below its one-month average;

- VIX index: up 1.88% to 17.85

BY Doug Kass · Aug 5, 2025, 4:38 PM EDT

Thanks for reading my Diary today.

I hope it was useful in your investment process.

I have to address continued family issues so I am leaving early.

I will see you bright and early tomorrow morning.

Enjoy your evening.

Be safe.

BY Doug Kass · Aug 5, 2025, 3:45 PM EDT

BY Doug Kass · Aug 5, 2025, 3:15 PM EDT

With S&P cash -28 handles I have covered all of today's short common and calls in the Indices.

This takes me to small-sized (from medium) in my SPY/QQQ common short:

* SPY $628.29

* QQQ $560.26

I plan to reshort strength.

BY Doug Kass · Aug 5, 2025, 2:58 PM EDT

With S&P cash -8 handles, I have added to index shorts:

* SPY $630.20

* QQQ $562.61

BY Doug Kass · Aug 5, 2025, 2:07 PM EDT

* From my perch, equities are more overvalued than at any time this year.

* Current valuations are a poor launching pad for future investment returns.

* "Slugflation" likely lies ahead — as domestic economic growth is moderating and inflation is sticky.

* We see numerous cracks in forward-looking global economic fundamentals, an unclear path of U.S. corporate profit.

* Speculation has run amok with the proliferation of 0DTE options, meme stocks, Palantir (100x revenues), dip buying, etc. have led to a suspension of fear, doubt and skepticism.

* Everyone (especially "The Kids Today"), it seems, now worship at the altar of price momentum — a condition previously seen in the Winter of 1999, the Summer of 2007 and in late 2021.

What follows is a summary of some of my recent Daily Diary contributions on TheStreet Pro and selected correspondences with my hedge fund investors at Seabreeze Partners.

Skepticism and doubt have left Wall Street.

To learn from history it is helpful to go back in history.

“Once a bull market gets underway and once you reach the point where everybody has made money no matter what system he or she followed, a crowd is attracted into the game that is responding not to interest rates and profits but simply to the fact that it seems a mistake to be out of stocks. In effect, these people superimpose an I-can't-miss-the-party factor on top of the fundamental factors that drive the market. Like Pavlov's dog, these "investors" learn that when the bell rings - in this case, the one that opens the New York Stock Exchange at 9:30 a.m. - they get fed. Through this daily reinforcement, they become convinced that there is a God and that He wants them to get rich.”

- Warren Buffett, “God’s Plan” (November 1999)

The Oracle of Omaha delivered the above quote only a few months before the end of the dot-com boom. Arguably, it may apply to today’s markets.

Buffett’s warnings should have been heeded, as, by March, 2000, the Nasdaq made a seminal top and commenced on a sutherly route that would result in a -80% drawdown in that index.

Twenty eight years ago I wrote an editorial in Barron's, Kids Today — the zeitgeist today is similar to that 26 years ago near the end of the dot-com boom:

"Being over 40 years old has been a liability in the Bull Market of the 1990s. ... I want to be like Sheldon The Kid and the rest of the kids in the 1960s and 1990s — trading in and out and relentless buying all dips, paying 15x revenues for tech stocks, disregarding value and common sense — but I can't."

- Doug Kass, "Kids Today" editorial in Barron's, July 7, 1997

A decade later another vivid illustration of the acceptance of "God's Plan" was made in an infamous quote by Citigroup's former CEO Chuck Prince in July, 2007 — a few months before the Great Financial Crisis, which also led to an unprecedented market decline in percentage terms and in time:

"When the music stops, in terms of liquidity, things will be complicated. But as long as the music is playing, you've got to get up and dance. We're still dancing."

Voltaire said that “History never repeats itself. Man always does.”

I am blinded by a sense of history.

In both the Winter of 1999 and in the Summer of 2007 day traders and speculation ran amok and a rising market was an almost accepted part of the zeitgeist.

Conditions today are clearly much different than in 1999 and 2007 — today's market leaders are healthy/profitable companies with deep moats (and not companies with no or limited futures).

We don’t expect anywhere near the declines of 2000-03 or 2007-09. However, we do expect an extended period of substandard to negative returns — an ideal backdrop for a long/short hedge fund, like Seabreeze, that is comfortable with a short book.

Investors face a host of secular headwinds that could be more long lasting than even at prior market peaks — the most important of which are:

* A rising probability of "slugflation" (prickly inflation, disappointing economic growth).

Prickly Inflation: Despite the slowdown in the domestic economy, recent reports suggest a possible reacceleration in the rate of growth of inflation. Tariffs will not help in the time ahead. (See my comment on tariffs later on in today’s commentary)

An acquaintance made some good points to me over the weekend (edited):

To put Fed 2.0% inflation target in proper perspective, to reach 2.0% inflation is not reality.

From 1965 to 2024 inflation averaged 3.9%. The last time inflation was generally low and not due to a crisis of some kind was the sixties. It was 1.6% in 1965 when the economy was booming at 6.5% GDP growth. Then again in 1986 as Fed Chair Volcker was coming to the end of his inflation crushing interest rate program, so not a normal period. In 1998 it was 1.6% when the economy was doing well and there was a trove of new technology being introduced which helped improve productivity. GDP grew at 4.2% real growth. Then from the period of the GFC 2009-2016 it was under 2.0%. But again, that was a very unusual period of financial market meltdown and grave financial crisis when the banks and Wall Street were essentially out of the market. Then in 2002, right after 9-11, so again, not a normal period. If we look for periods comparable to today when inflation was 2.0%, there are almost zero. We must ask where did this 2.0% target for the Fed come from and how did that number become the gospel. Achieving it based on history is not realistic. Perhaps the entire premise the Fed is operating under of needing to reach 2.0% is a fantasy that is unlikely to be achievable so long as the economy is growing. It would only be achievable if there is a deep recession or another financial crisis like 2009. 3.0% is a realistic target and we are there now with PCE at 2.6%, so rates should come down.

Possibly we can have 2.0% inflation someday once AI is much more widespread and productivity is even higher than today and GDP is growing at 4.0%. But we are not there now and with tariffs we are not going there anytime soon.

Many recall the Humphrey-Hawkins Full Employment and Balanced Growth Act of 1978 – a landmark legislation designed to address unemployment and promote economic stability. That bill set the goal for inflation to be at 4% by 1988. The lesson was that Congress cannot set inflation rates just as these rates cannot be legislated today.

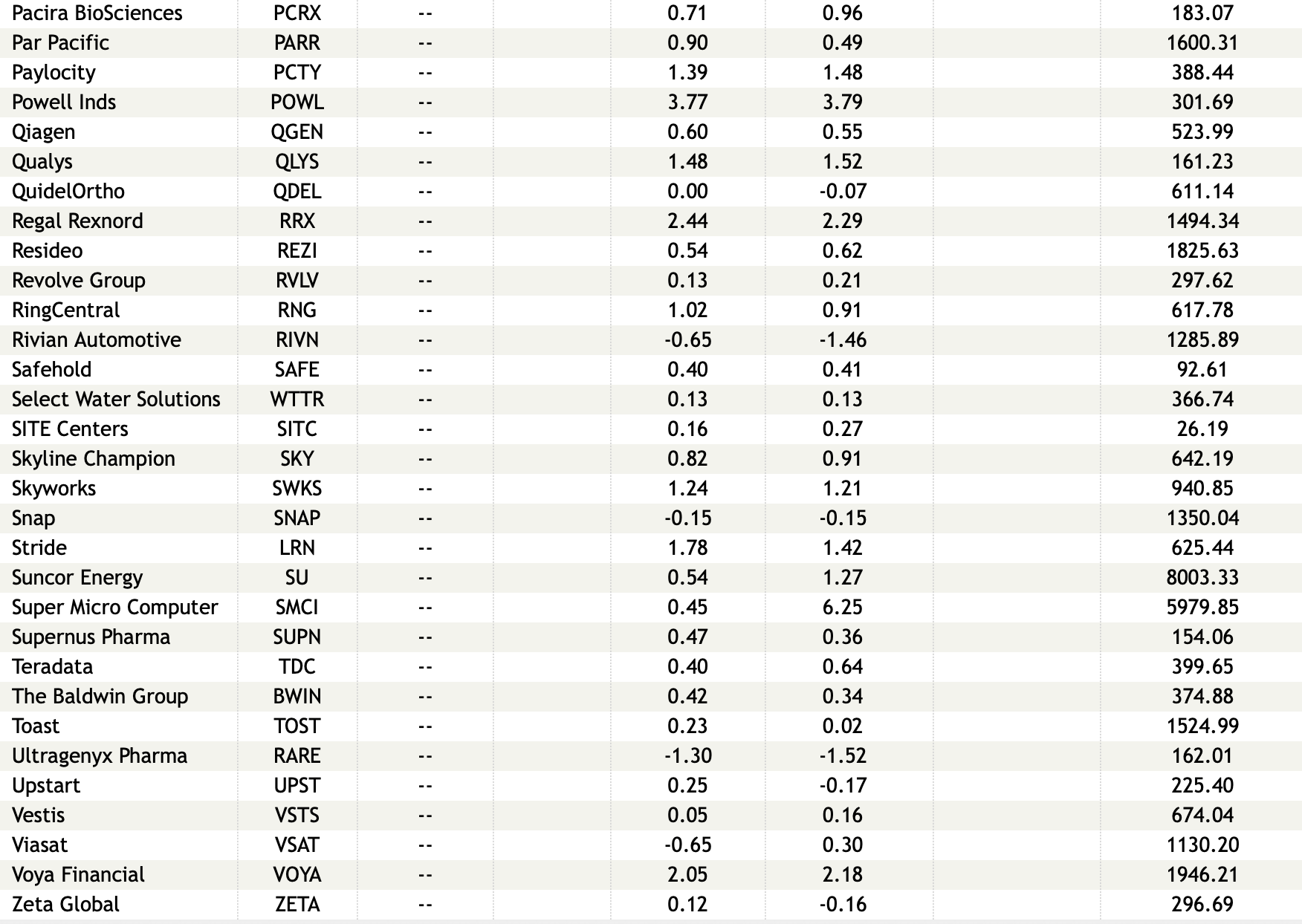

Disappointing Economic Growth: All traditional signposts (labor reports, ISMs, etc.) point to a slowing U.S. economy and a challenge to the wrong-sided bullish notions that macro-U.S. data is resilient, S&P EPS growth will be robust and the trade war rhetoric is improving.

I won’t repeat the multiple macroeconomic and company/sector examples of a growing slowdown but I would add something that I have found to be one of the best predictors of growth — Las Vegas tourism. And, on that score, we should also be cautious on a consumer-based economy.

The consumer is spent up, not pent up.

(We have numerous consumer sector shorts in our Seabreeze portfolio).

Representatively, this is from Colgate-Palmolive’s CL 3Q2025 EPS release (hat tip Peter Boockvar). Colgate makes things we use every day like toothpaste, deodorant, soap, and shampoo.

"There is a persistently cautious consumer in North America right now. We saw some rebound in April, May. The categories took a little step back in June, which we weren't expecting."

"Many of our markets and categories around the world remained challenging in the second quarter and we expect this to continue through the second half of the year."

"The cost environment is difficult as we're dealing with tariff increases, higher raw and packaging material costs, and less underlying category inflation. This means that our revenue growth management strategies need to drive additional pricing and mix with lower levels of elasticity as we look to improve organic sales growth in the second half of the year."

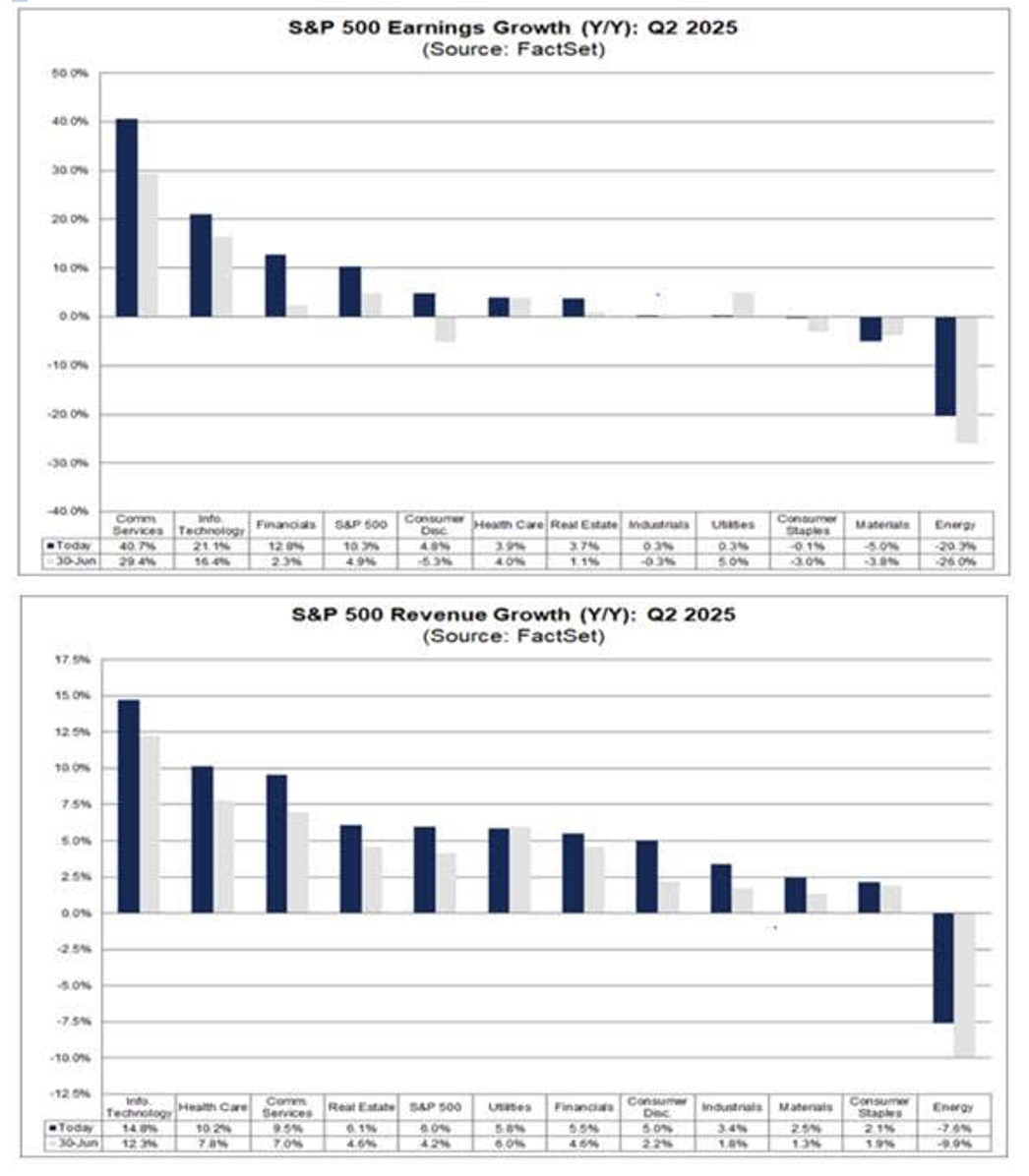

* The rate of corporate profit growth will markedly decelerate in this year’s second half

* Undisciplined fiscal policy by both parties that will likely lead to a continued and large deficit, adding to our nation's debt load

* Political and geopolitical polarization and competition will probably translate into less political centrism and a reduced concern for deficits — creating structural uncertainties, limited fiscal discipline and imprudence around the globe ... and for the possibility of bond markets to "disanchor"

* Equities are overpriced against interest rates: The equity risk premium is at a two-decade low — typically consistent with a slide in equities. (Given the plethora of uncertainties (many of them adverse), risk premiums should be rising, not falling!) The S&P dividend yield is at a near record low of 1.27% — and the spread between the dividend yield and the 10-year U.S. Treasury note yield has rarely been as wide.

* Valuations that are in the 98%-tile, a poor launching pad for future investment returns: The S&P Index’s trailing P/E multiple now stands at 26x — taking out the 23x peak of late 2021 and similar to the valuation reached in August 2000 (right before a two-year bear market commenced). The current multiple is more than +30% above the long-run norm. This is even more disquieting in that the real risk-free interest rate (at more than two percent) is double the historical average.

Over the last few weeks the markets have been buoyed by, among other factors, the Trump administration's "tariff" agreements which have been viewed by market participants as a big net investment positive.

We strongly are of the view that tariffs represent a bonafide threat to economic growth.

Most recently, the energetic reaction to a series of economically unfriendly tariff announcements and "agreements" are an exclamation point of unbridled and, arguably, poorly analyzed blind political and market enthusiasm. Moreover, the goal posts have been constantly been moved (in attempts to represent tariff policy success).

From John Mauldin ( "Thoughts From The Front Line) over the weekend in "Uncertainties Squared" Uncertainty Squared - Mauldin Economics:

“I know very few bullish investors who think tariffs are good. Mostly, they see tariffs as the “least bad” response to an intolerable situation. They recognize the ill effects but believe the tariff pain will end soon. (More on that below.) In this view, the current confusion and chaos will lead to a new equilibrium that is manageable and maybe even positive. They don’t think it will be bad enough to derail the other bullish factors like AI technology. If that’s what you believe, then it makes sense to take advantage of current bearishness to buy more. I’m not in that group but I understand their thinking. What I don’t see is reason to think the tariffs lead to even a neutral outcome, much less a good one. I’ve gone over the reasons before and won’t repeat them now. (Read this if you’re interested. It is my letter from April 25 and realize how much change there has been since then. Rather astonishing, really.)The best case I can imagine is that tariffs will raise import prices for American consumers enough to show up as higher inflation but not enough to trigger a recession. Because I think even 2% inflation is too high and robs all of us, I don’t see that as a good trade-off. Further, the way all this is being done makes the hoped-for manufacturing revival more difficult in reality than it is in the theory that some political types believe. I would also note that bulls keep moving the goal posts. Stocks rallied back from their April crash because Trump postponed the highest tariff rates for 90 days, during which he was going to negotiate a bunch of great deals with our top trading partners. The 90 days passed with no significant deals. Now we are told higher rates are coming in August, but traders seem to think those rates won’t happen, either. Maybe they’re right. But other governments are planning their retaliatory moves, and this could easily spiral into a broader trade war. Hopefully cooler heads will prevail, and we won’t end up with a repeat of the spiraling Smoot-Hawley tariffs. I get the idea of “seeing through” short-term volatility. My problem is with the “short-term” part. I just don’t see the finish line. I assume one is out there. I don’t think it is near.”

The unjustified bows taken by the current administration were recently outlined in The Financial Times:

“Anyone surprised by this? Thinking equities will keep going up once the great negotiator finishes the most amazing beautiful deals with Europe and others might be in for a rude awakening.

“I just signed the largest trade deal in history, I think maybe the largest deal in history, with Japan,” Trump boasted Tuesday. But a new report from The Financial Times demonstrates that U.S. and Japanese officials don’t see eye to eye on what exactly the countries agreed upon.

According to Trump and his administration, in return for a reduction in tariffs, Japan would invest $550 billion in certain U.S. sectors and give the United States 90% of the profits.

Japanese officials, however, say the profit sharing isn’t so set in stone: A Friday slideshow presentation in Japan’s Cabinet Office, contra the White House, said profit distribution would be “based on the degree of contribution and risk taken by each party,” according to The Financial Times.

The FT also reports conflicting messages between Washington and Tokyo as to whether that $550 billion commitment is, as team Trump sees it, a guarantee or, as Japan’s negotiator Ryosei Akazawa sees it, an upper limit and not “a target or commitment.”

Mireya Solís, a senior fellow at the Brookings Institution, told The Financial Times that the deal contains “nothing inspiring,” and that “both sides made promises that we can’t be sure will be kept” and “there are no guarantees on what the actual level of investments from Japan will be.”

The inconsistent interpretations of the deal could be because it was hastily pulled together over the course of an hour and 10 minutes between Trump and Akazawa on Tuesday, according to the FT, which cited “officials familiar with the U.S.-Japan talks.” And, moreover, “Japanese officials said there was no written agreement with Washington—and no legally binding one would be drawn up.”

Does Trump’s so-called “largest deal in history” even count as a deal at all? Brad Setser, senior fellow at the Council on Foreign Relations,

“Well-nigh two thousand years and not a single new god!”

- Fredrich Nietzsche, The Antichrist (1888)

Another possible threat has emerged — the investing world almost universally believes it has discovered a new god in artificial intelligence and machine learning.

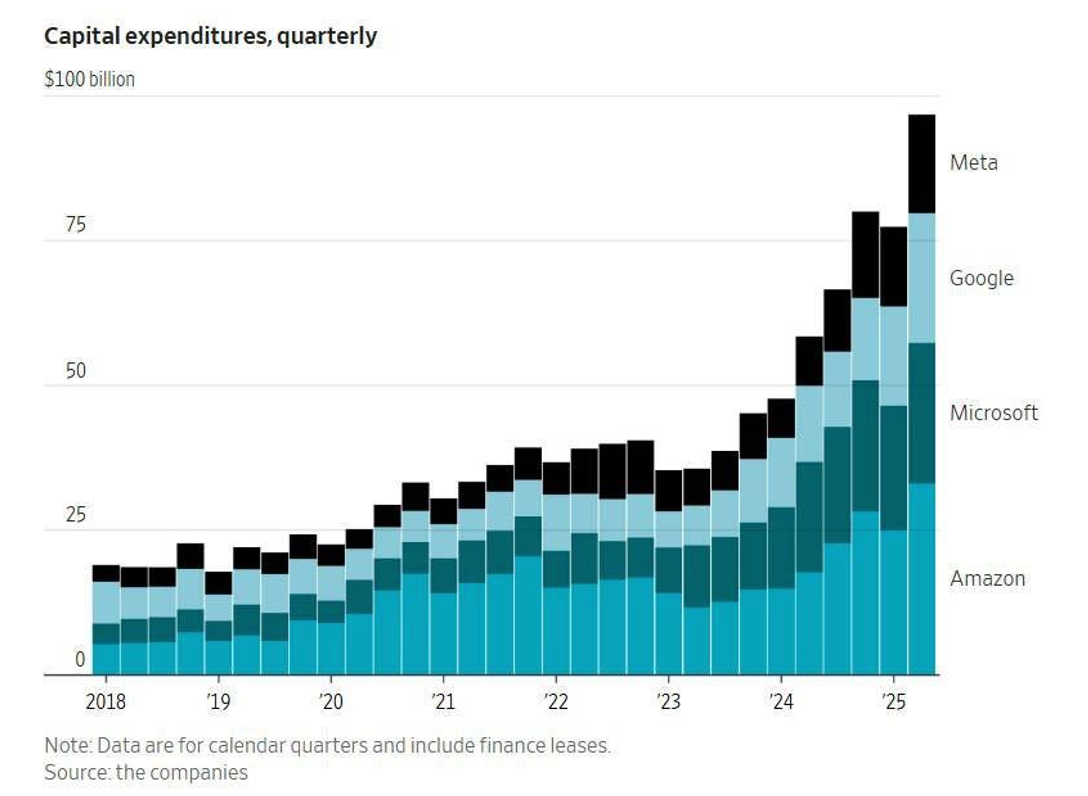

In dollar terms the AI outlays eclipse anything in history — with the four hyperscalers (Google GOOGL, Meta META, Amazon AMZN and Microsoft MSFT) undertaking a spending orgy by committing almost 60% of their 2025 cash flows (approximately $300 billion in 2025) on AI capital spending.

Putting this into perspective, AI infrastructure CAPEX is already 20% higher as a % of GDP than what was spent on telecom and internet infrastructure at the peak of the dot com boom. For Microsoft and Meta, CAPEX is now more than a third of their total sales. Astonishingly and according to Neil Dutta (head of economic research at Renaissance Macro Research), capital spending for AI contributed more to growth in the U.S. economy in the past two quarters than all of consumer spending.

The depreciation schedules being used for this AI spend is somewhere between aggressive and absurd. One company, CoreWeave CRWV, is reporting earnings before capital expenses!

I share the following concerns expressed over the weekend by The Credit Strategist:

“Anyone who questions AI faces the challenge of answering technology experts (genuine and self-proclaimed) who claim superior knowledge of the topic. But the projections on which future AI revenues and profits are based remain highly speculative because they are based on events that have yet to happen; put bluntly, they are based on predictions about the future that is always unknowable. But one characteristic of the future that is knowable is that it is reflexive, meaning human beings and organizations react and adjust to changes rather than remain static. As such, arguments that AI will eliminate jobs without creating new ones or arbitrage away margins without creating new margin opportunities are questionable. Further, it is unlikely that multiple LLM models addressing the same market will all prove successful; more likely, ruthless competition will create a small group of winners and many losers with a great deal of capital consumed in the process.

The quantum of AI spending dwarfs anything previously applied to a specific product or sector in such a concentrated period of time. All of this spending has yet to produce a commensurate amount of revenue or profit but we are still in early days and investors are convinced that it will. Whether the world needs numerous LLMs that perform similar tasks remains to be seen; it’s not clear that these models can meaningfully differentiate themselves despite spending hundreds of billions of dollars attempting to do so. As Fred Hickey writes in The High Tech Strategist (highly recommended): “revenue generation for the LLM builders is limited (they’ve not found killer apps for the masses) and the losses are unlimited. The capex would be destroying their company P&Ls – except for the fact that the chips and equipment costs are spread out over several years via depreciation expensing.” The fight for dominance and first-user advantage will continue to the bitter end. Some are projecting that annual AI spending could increase even further but I suspect it may end up tapering off if it doesn’t generate promised returns before long.”

To summarize, while Mag 7 and AI-related equities have dominated the market’s advance and participants’ attention over the last two years, AI has yet to demonstrate it will save the world. Any change in attitude towards these companies could send markets reeling lower.

S&P 500 Index over past 4 years

We see numerous cracks in forward-looking global economic fundamentals, an unclear path of U.S. corporate profits, coupled with extended valuations (both absolutely and relative to interest rates).

BY Doug Kass · Aug 5, 2025, 1:00 PM EDT

BY Doug Kass · Aug 5, 2025, 12:15 PM EDT

For point of reference: SPY is back to yesterday's opening levels:

BY Doug Kass · Aug 5, 2025, 11:50 AM EDT

BY Doug Kass · Aug 5, 2025, 11:35 AM EDT

From Peter Boockvar:

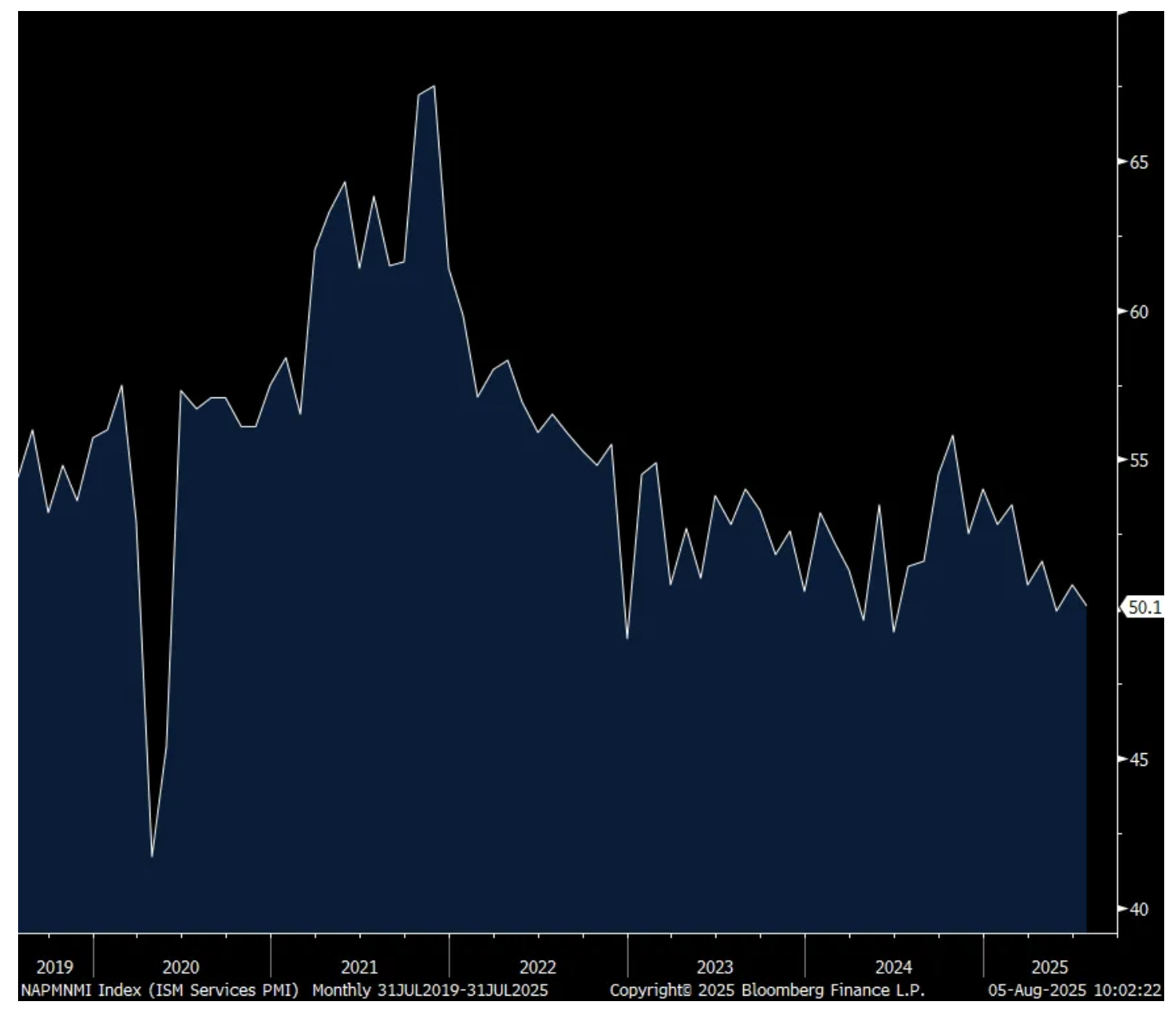

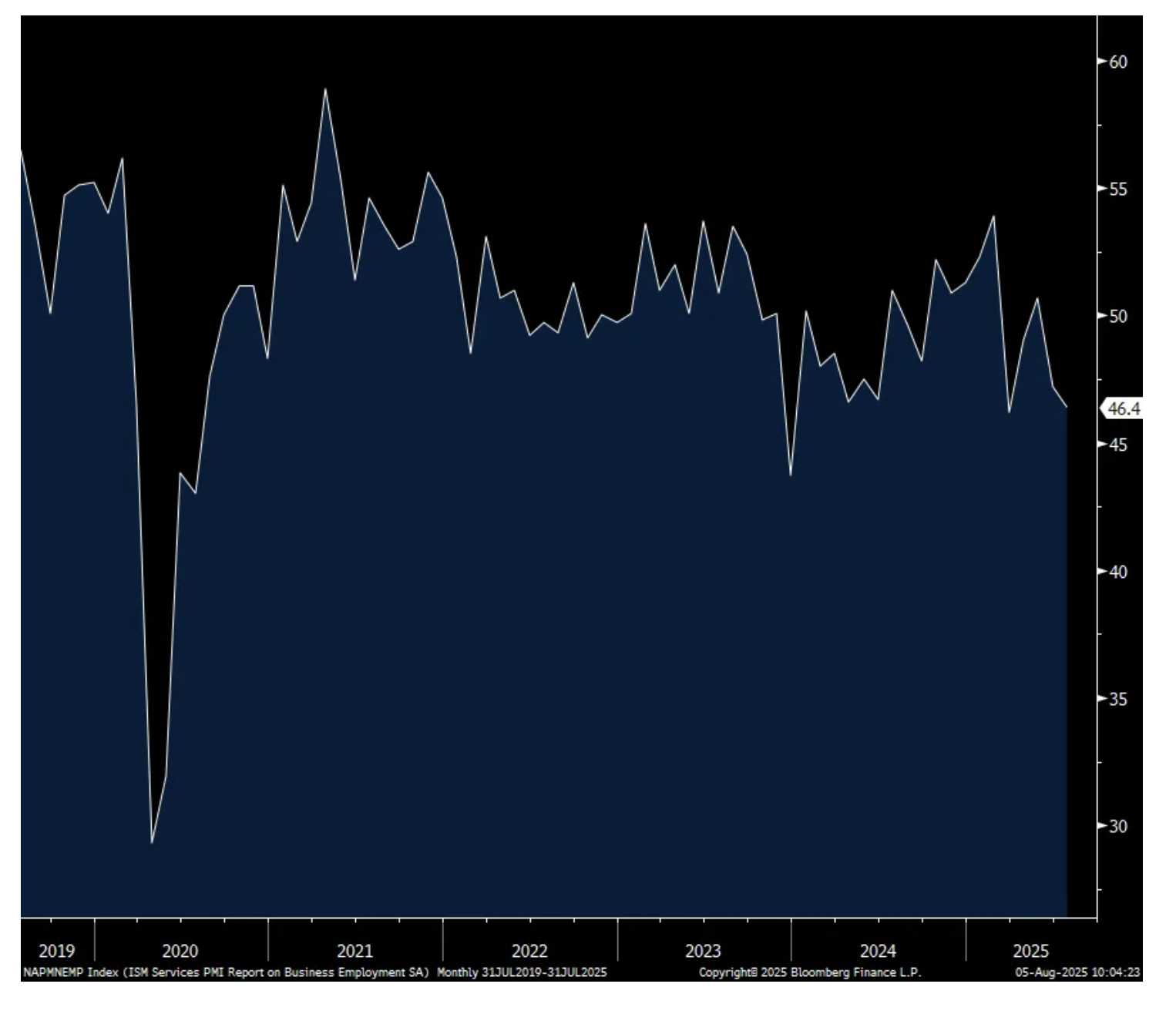

The July ISM services index fell to 50.1 from 50.8 and that was below the estimate of 51.5. With many eyes on the labor market, the employment component fell to 46.4 from 47.2 and that is the 2nd lowest print since December 2023 and below 50 for the 4th month in the past 5. New orders slipped by 1 pt to 50.3 while backlogs remained well below 50 but a bit less so at 44.3. Inventories fell about 1 pt to 51.8. Supplier deliveries rose a touch and remained above 50 but at 51 reflects no real supply chain issues in terms of timing of deliveries post the tariff influences in the first half of 2025.

Prices paid rose to 69.9 from 67.5 and that is the highest since October 2022. And I want to point out this, imports fell to just 45.9 from 51.7 and that is the lowest since June 2024, though 75% of service provider respondents don’t use/track imported materials directly. One comment from someone who does, “Imports have increased in price, to be less competitive than domestic vendors.”

With regards to breadth of growth (but not degree), 11 saw expansion vs 10 in June but there was a one industry pick up in those experiencing a contraction at 7.

Highlighting still where most of US economic growth is coming from, this was said by a few respondents: “We continue to see strong demand driven by the build-out of artificial intelligence-related data center capacity, semiconductor industry expansion fueled by national policy, and large-scale grid modernization projects” and “New orders for defense equipment surged; non-defense orders dropped.”

The bottom line from the ISM was this, “July’s PMI level continues to reflect slow growth, and survey respondents indicated that seasonal and weather factors had negative impacts on business…The most common topic among survey panelists remained tariff-related impacts, with a noticeable increase in commodities listed as up in price.”

My bottom line, this index which covers the biggest chunk of the US economy, that being services, has essentially flat lined over the past three months with a 49.9 print for May, 50.8 for June and the July figure of 50.1.

Treasury yields fell post release after being initially up after Friday’s big drop.

Plenty of tariff talk in the company/industry comments:

“Anticipation of the final tariff impacts is resulting in delayed planning for next fiscal year purchases.” [Accommodation & Food Services]

“Higher tariffs are increasing the cost of imported feed ingredients and trace minerals for livestock and poultry feeds. Business and customer concerns over additional cost risk due to additional tariffs.” [Agriculture, Forestry, Fishing & Hunting]

“Trade uncertainty causing client reevaluation of feasibility for projects in certain sectors, resulting in some delays or cancellations. Public-funded jobs experiencing pullbacks.” [Construction]

“Summer break for students greatly reduces demand on campus.” [Educational Services]

“Steady business activity.” [Finance & Insurance]

“Tariffs are causing additional costs as we continue to purchase equipment and supplies. Though we need to continue with these purchases, the cost is significant enough that we are postponing other projects to accommodate these cost changes.” [Health Care & Social Assistance]

“Extra purchasing to head off tariffs has leveled off. Expecting decreases in activity in the second half of 2025.” [Mining]

“Economic uncertainty remains the dominant theme. However, the tariff talk has turned out to be much more bluster than actual policy, and businesses have seemed to tune out the noise. The outlook continues to look incrementally positive.” [Real Estate, Rental & Leasing]

“Retail results are solid — a little soft before and during Fourth of July week, but then a rebound. We see no reason to believe this won’t continue for the near term.” [Retail Trade]

“Our business activity is flat. We are not trending up or down. Tariffs are now starting to show up in pricing, and we are seeing increases across the board.” [Transportation & Warehousing]

ISM Services Index

ISM Employment

Prices Paid

BY Doug Kass · Aug 5, 2025, 11:20 AM EDT

My pals Guy and Dan on MRKT Call:

Now and free!

Let's go to the tape. MRKT Call - Tuesday, August 5th

BY Doug Kass · Aug 5, 2025, 11:11 AM EDT

Jim F

10 minutes ago

Hey Dougie, here is another thought I had about AI Capex.

I've heard arguments in the past that tech companies should have higher PE ratio's because they are capital light businesses. meaning their Capex scales with revenues. this eliminates the need to properly predict future demand. therefore resulting in lower risk expansion versus capital intensive businesses. this lower risk should be rewarded with higher multiples.

with capital intensive businesses like a widget manufacture. the C suite has to decide if the big upfront expense of building a factory will pay off based on future demand. if demand doesn't grow enough to get the factory utilization rate high enough. then they just spent a ton on a new factory that isn't profitable on a per unit basis. if they don't build the factory and the demand grows they just capacity constrained their growth. as well as opened the door to competitors who better anticipated the future demand. since you won't always get this decision right combined with the ramifications being so high. the idea is those companies should trade at a lower valuation to reflect this.

I thought this thesis makes some real sense. however, to me AI looks more like the capital intensive industrial business model. they certainly don't look like the capital light businesses they have been in the past. therefore, in theory, they should be trading at much lower multiples to reflect the risk of building overcapacity relative to future demand. I think you've talked about this from an angle of where is the future demand to justify all the money being spent. this is a slightly different way of looking at that issue from a multiple standpoint.

BY Doug Kass · Aug 5, 2025, 10:55 AM EDT

Dougie Kass

STAFF

6 minutes ago

Back to my largest net short exposure since January

Dougie Kass

STAFF

19 minutes ago

Trading short rental in NVDA $180.02

BY Doug Kass · Aug 5, 2025, 10:35 AM EDT

I have a continuing family health issue to deal with - so I will be in and out today.

A heads up.

BY Doug Kass · Aug 5, 2025, 10:25 AM EDT

From Peter Boockvar

The messaging behind yesterday's stock market rebound was clear to me. As seen many, many times over the past few decades, the stock market cares more about Fed rate cuts than it does about the reasons for it, rarely ever losing faith in the belief that Fed rate cuts are the cure to all ills.

Mary Daly, the SF president, doesn't vote but if she could she told us that she would by 2-3 times this year. Her waiting is over she told us.

We know rents are the key variable to CPI and we've heard from some multi family REITS over the past few days. Rent growth is continuing to decelerate but I'll say again, let's enjoy the moderation in rental growth because it won't last next year.

From Camden Property Trust, who mostly has a sunbelt presence and a stock we own run by one of my favorite management teams:

"Rental rates for the second quarter had effective new leases down 2.1% and renewals up 3.7% for a blended rate of .7%. This was in line with our expectations for the quarter and reflected an 80 bps improvement from the negative .1% blended rate we reported in the first quarter of '25 and a 60 bps improvement from the .1% reported in the second quarter of 2024."

They expect the back half of 2025 to see blended lease rate growth also just below 1%.

Occupancy remained steady at 95.6% vs 95.4% in Q1 and "Renewal offers for August and September were sent out with an average increase of 3.6%. Turnover rates across our portfolio remain very low with the second quarter of 2025 annualized net turnover of only 39%...with continued low levels of move-outs for home purchases, which were 9.8% this quarter."

As for why rents will be reaccelerating next year, "And so what's happening now...is we haven't had a demand falloff. Our demand in the last two years has been the highest it's been in 20 years. And so, you have this interesting issue where we have big time supply, and then we have big time demand."

And on the supply side, "So, what's happening now, and if you look at the starts, starts are down 76% in Charlotte, Denver, Austin, Atlanta, and DC. They're down 60-76% in Tampa, Orlando, Phoenix and Nashville. They're down 45% to 65% in Dallas, Houston, West Palm Beach, and Fort Worth. So, when you look at those numbers, clearly the supply is down significantly. It's going to be down significantly."

Finally in terms of rent forecasts, "Witten Advisors has kind of an average 4% growth in 2026 for Camden markets, and 5% plus in 2027, and them more beyond. And some of the markets are going 6%, 7% up."

Equity Residential, who has apartments mostly in coastal regions and where supply has been more muted relative to the sunbelt:

Blended rents grew by 3% in Q2 with new leases down .1% more than offset by renewal rates up by 5.2% y/o/y. For Q3, "Blended rate is expected to be between 2.2% and 2.8%." Their earnings call is this morning.

From Wayfair and whose stock popped by 13% yesterday:

"The second quarter was a resounding success, defined by accelerating sales and share gain in tandem with expanding profitability."

"If you just look broadly at the market, what I would say is that the market this year is definitely better than the last three years, where it was down substantially each year. But I think the market is still flat to down low single digits. And I would describe the market not as having strength, but as sort of feeling like it's bottomed out, like bumping along the bottom."

"There's no question the higher end market is stronger than mass. That's definitely the case...But that's not really surprising if you just think about the category being discretionary."

On how their suppliers are managing tariffs, "As we spoke about in the spring, suppliers take different approaches to managing cost increases. While some may pass through price increases, others who want to win share in a demand constrained environment will choose to keep their prices more competitive, and will use all the methods at their disposal to do so."

From Simon Property, the big Class A mall operator:

"In the sense that the whole world is uncertain. A lot of geopolitical stuff going on, obviously. A lot of domestic political stuff going on. New York City, thankfully we're not an investor in New York City, but obviously a lot of political uncertainty in New York City. Tariff swings back and forth, interest rate uncertainty you can name it. However, you have unbelievable stores that are us in particular, that are able to manage that. And in addition, retail demand is really unabated."

"And the physical shopping environment continues to be the place to be. So, we're quite bullish about what we've done, what we are doing, where we are going, despite all of the headlines that are out there."

For smaller tenants, those more negatively impacted by tariffs, "I think they're managing it as best they can. I still think the full story, obviously, given the volatility, has not been written. But we're not seeing it in demand and that particular business that is sensitive to moms and pops continues to perform well. So, we're more optimistic about that segment than I was last quarter. But, like I said, it is something that we're watching closely."

That all said, "we're still very cautious about the economic environment. We have to be right? I mean, tariffs are a real cost to doing business and they're changing consistently, right? The only consistent thing about tariffs is that they've been consistently changing, right? So, and it's a cost to do business now, ultimately who pays that cost, is it the consumer? No, it's the domestic company that imports right? So, they start with the cost pain and you can see it by Ford and a number of other companies, and so, it's going to cost me $800 million or $1 billion" referring to Ford.

"And then the next question is can the suppliers chip in, then ultimately the consumer. And I think most companies are kind of working that next step or two through. So, in that scenario it is hard for us not to be cautious and obviously from just pure retail are they going to be more cautious on buying then they might not otherwise be for tariffs."

From Trex, the faux, alternative wood decking company:

"The Trex team delivered strong second quarter results, highlighted by 3% net sales growth, achieving a record level of quarterly sales despite adverse weather conditions in many parts of the country and despite a declining repair and remodel market...New products are once again a key contributor to the past quarter's sales performance."

"From a geographic standpoint, we see strong demand in markets across the US."

"Overall, we were pleased with the behavior of our consumers, seeing our contractor backlogs in the 6-8 week range. We're seeing that in the third quarter as well. We've seen us outperform against repair and remodel really for a couple of years now. That continues. It is a low cost way for people to be able to add square footage to their home. I mentioned about the large number of 50 million wood decks in existence in North America, most of which are at the point where they need to be replaced."

From On Semiconductor, whose stock fell 16% yesterday on margin pressures:

"Turning to the demand environment, we are seeing signs of stabilization across our end markets. We have not seen any pull-ins to date due to tariffs and our diversified manufacturing footprint remains a competitive advantage, providing sourcing options to our customers as they work on optimizing their supply chains."

Automotive revenue fell 4% but "performing better than anticipated and is expected to grow in the third quarter with continued EV ramps" particularly in China, offsetting "weakness in America and Europe."

More on auto, "So you're starting to see that stabilization. I'm not there calling the recovery, there's still a lot of uncertainty, and customers are being cautious."

"Revenue for AI data center nearly doubled again in Q2 over the same quarter last year."

"While our medical and aerospace and defense businesses continue to grow, traditional industrial declined slightly in Q2 vs Q1."

Lattice Semiconductor is looking up pre market after earnings:

Revenue was flat y/o/y and "We achieved these impressive results in an uncertain market...We exited Q2 with increased optimism about the market environment vs Q1."

On their industrial and automotive business, "We believe we've passed the bottom with channel inventory levels decreasing."

Ahead of the US ISM services report today, China's July private sector Caixin services PMI rose 2 pts to 52.6 and that is the best since May 2024. I'll add in particular, the Macau casino and visitation numbers continue to improve and we're still long Las Vegas Sands and Melco as a play on this. Within the PMI too, "Business sentiment also improved to the highest level since March."

Singapore's PMI rose to 52.7 from 51 while Hong Kong's went to 49.2 from 47.8.

The Eurozone final services PMI was left little changed at 51 vs 50.5 in June while the UK's was revised up to 51.8 from 51.2 initially, though down 1 pt m/o/m.

S&P Global said, "This could turn out to be a good summer for service providers. In Italy and Spain, business activity rose more sharply in July than in the previous month, while Germany, after several challenging months, has clawed its way back into growth territory...France, by contrast, is the only one of the four major Eurozone economies where the private services sector is contracting. Worse still, the downturn deepened."

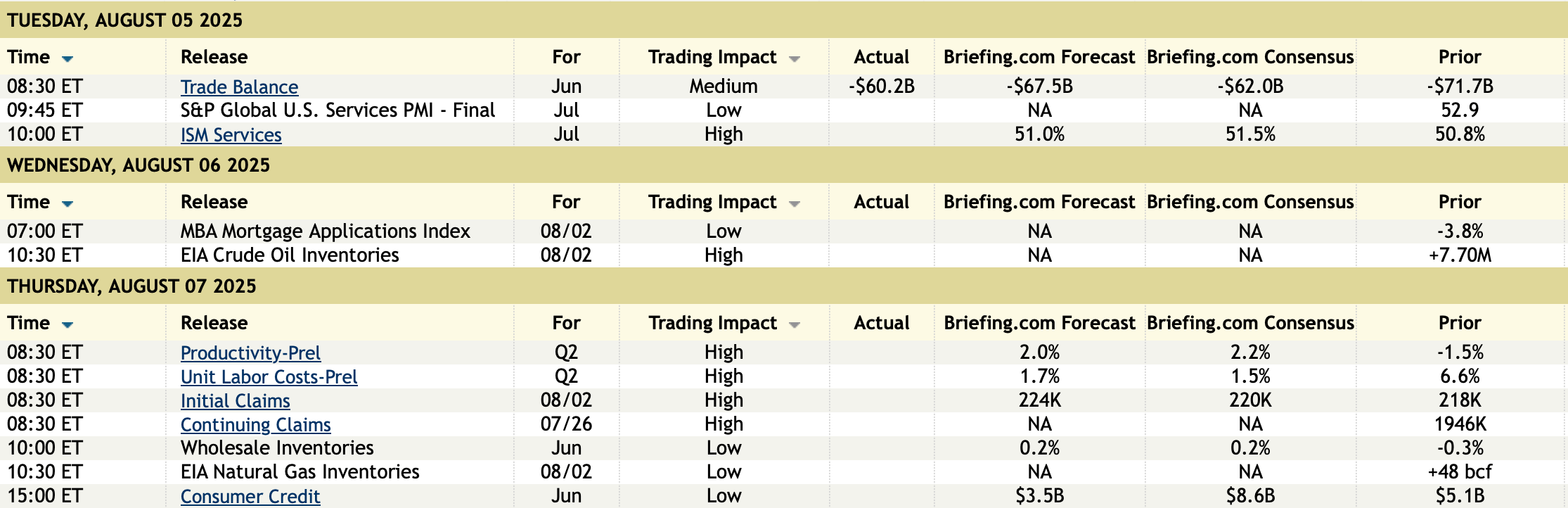

BY Doug Kass · Aug 5, 2025, 10:15 AM EDT

Today's Auctions

11:00 a.m.: Treasury Announces a 4 and 8 Week Bill Auction;

11:30 a.m.: Treasuy hosts a $50B 52-Week Bill Auction

Economic Calendar for Remainder of Week

BY Doug Kass · Aug 5, 2025, 9:59 AM EDT

I am adding to my GRNY and JOET shorts.

BY Doug Kass · Aug 5, 2025, 9:57 AM EDT

BY Doug Kass · Aug 5, 2025, 9:50 AM EDT

BY Doug Kass · Aug 5, 2025, 9:34 AM EDT

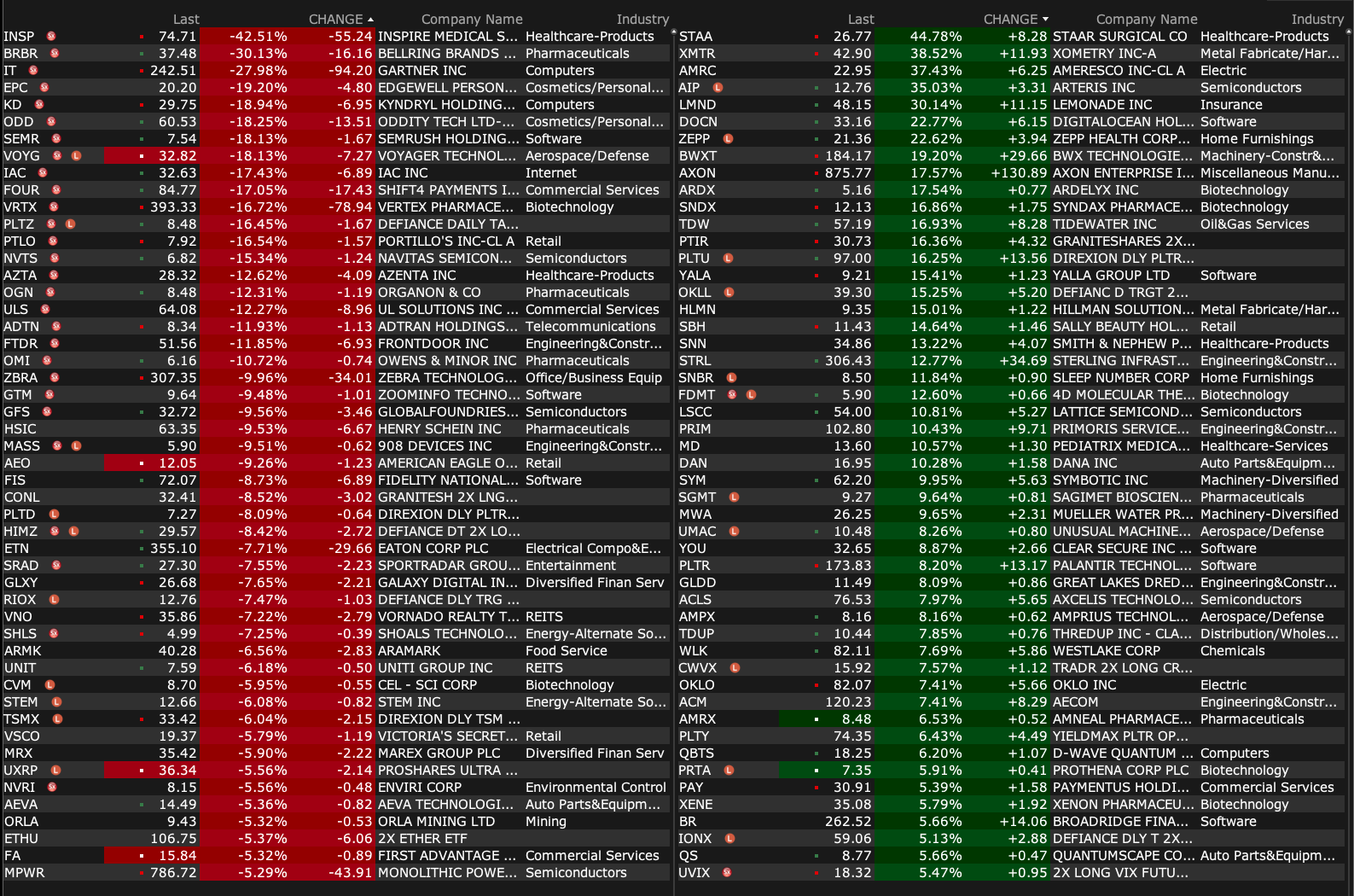

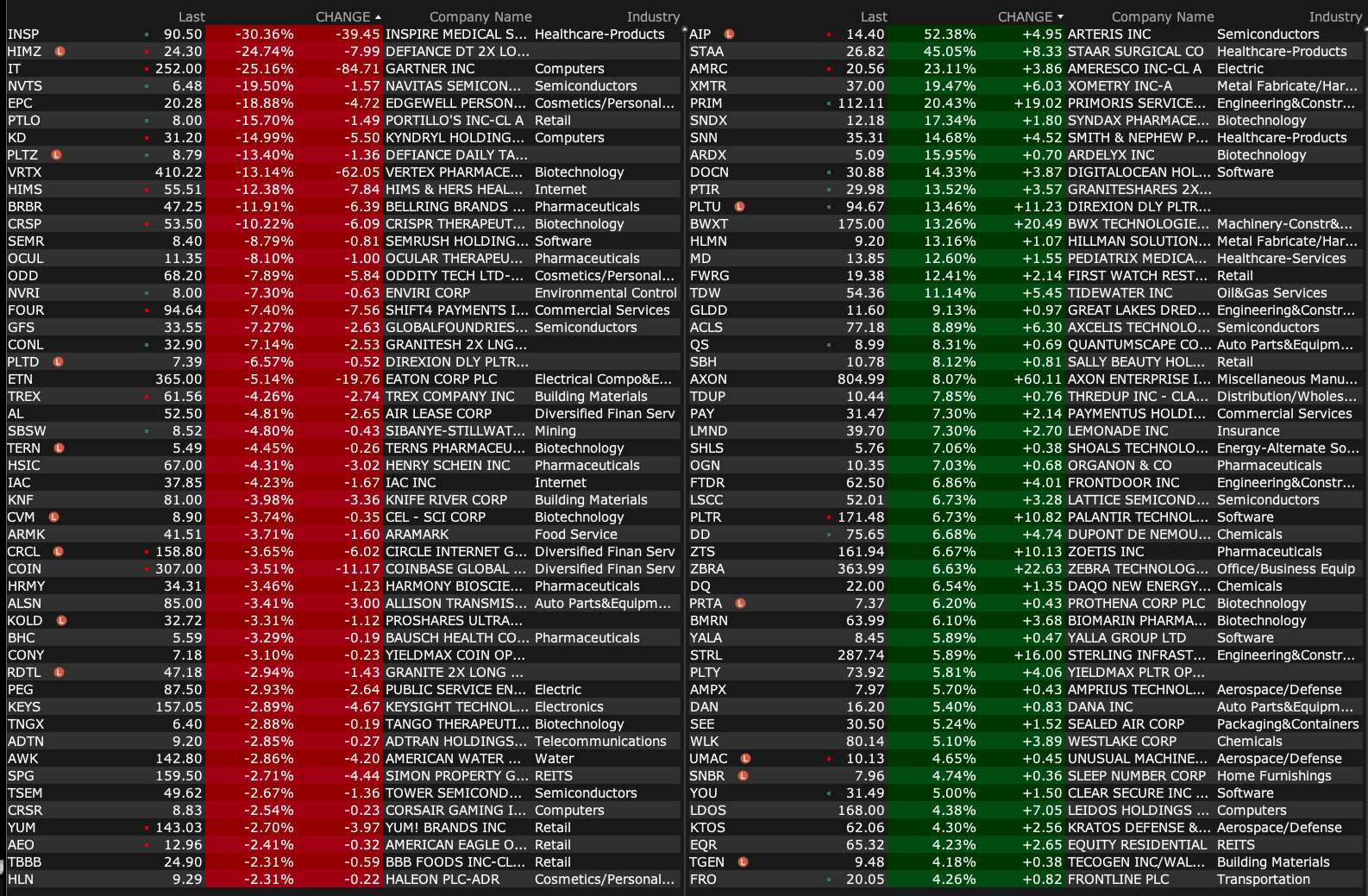

-AIP +59% (to Provide FlexGen Smart NoC IP In Next-Generation AMD AI Chiplet Designs)

-STAA +45% (to be acquired by Alcon at $28/shr in cash)

-AXGN +20% (earnings, guidance)

-ARDX +14% (earnings, guidance; CFO to step down)

-BWXT +13% (earnings, guidance)

-MDGL +13% (earnings)

-EVGO +12% (earnings, guidance)

-TDUP +12% (earnings, guidance)

-ACLS +11% (earnings, guidance)

-XMTR +9.8% (earnings, guidance)

-LMND +9.7% (earnings, guidance)

-FTDR +9.4% (earnings, guidance)

-ZTS +8.0% (earnings, guidance)

-NSPR +7.8% (earnings)

-AXON +7.4% (earnings, guidance)

-ZBRA +7.2% (earnings, guidance)

-PLTR +6.8% (earnings, guidance)

-QUBT +6.4% (awarded TFLN Photonic Chip Contract by U.S. Department of Commerce's National Institute of Standards and Technology)

-DD +5.9% (earnings, guidance)

-LDOS +5.5% (earnings, guidance)

-SEE +5.2% (earnings, guidance)

-YOU +5.0% (earnings, guidance)

-ALIT +4.9% (earnings, guidance)

-STRL +4.3% (earnings, guidance)

-APO +3.1% (earnings, guidance)

-PFE +2.1% (earnings, guidance)

-INSP -31% (earnings, guidance)

-ICHR -26% (earnings, guidance)

-NVTS -21% (earnings, guidance)

-IT -20% (earnings, guidance)

-PTLO -19% (earnings, guidance)

-VRTX -14% (earnings, guidance)

-KD -13% (earnings, guidance)

-BRBR -12% (earnings, guidance)

-HIMS -11% (earnings, guidance)

-TREX -6.5% (earnings, guidance)

-FOUR -5.3% (earnings, guidance)

-ETN -4.9% (earnings, guidance)

-HSIC -4.7% (earnings, guidance)

-COIN -3.9% (files to sell $2.0B of Convertible Senior Notes)

-YUM -2.6% (earnings)

-GLXY -2.4% (earnings, guidance)

-IAC -2.1% (earnings, guidance)

BY Doug Kass · Aug 5, 2025, 9:30 AM EDT

BY Doug Kass · Aug 5, 2025, 9:28 AM EDT

I have added to my trading short rental in PLTR at $172.26.

BY Doug Kass · Aug 5, 2025, 8:25 AM EDT

BY Doug Kass · Aug 5, 2025, 7:31 AM EDT

BY Doug Kass · Aug 5, 2025, 7:15 AM EDT

* An important observation....

BY Doug Kass · Aug 5, 2025, 7:05 AM EDT

Pay for play has become the standard today:

BY Doug Kass · Aug 5, 2025, 6:55 AM EDT

Bonus — Here are some great links:

BY Doug Kass · Aug 5, 2025, 6:40 AM EDT

BY Doug Kass · Aug 5, 2025, 6:30 AM EDT

From JPMorgan:

US: Futs are higher, led by small caps, potentially pointing to a further squeeze potential from shorts put on as recent as Friday. Pre-mkt, Semis are standing out with Mag7 names higher; Industrials are leading Cyclicals over Defensives. Staples are in the red. The yield curve is bear flattening as USD catches a bid. Today’s macro data focus is on ISM-Srvcs while we get an update on the trade balance. Trade tensions ratchet higher as geopolitics enter the debate.

and...

JPM MARKET INTEL EQUITY & MACRO NARRATIVE

Yesterday, we saw a significant reversal of Friday’s moves, which look increasingly technical / mechanical in nature, potentially from a combination of month-end rebalancing across mutual funds and ETFs plus CTAs exacerbating moves. Digging deeper, under the hood, we did not see a reversal of Friday’s biggest laggards (charts below). Regardless, there was a certain degree of squeeziness in yesterday’s session which increased late in the day. Where does this leave us? About 1% from all-time highs. Okay, a less flippant response is that we have not see a material change in the macro environment, but we likely are at the beginning of feeling the impact of the trade war. From here, inflation data is more important than growth data because the Fed could find itself in a situation where growth deteriorates (Powell’s proxy is the unemployment rate, per his own comments) but inflation has increased to an uncomfortable level, leaving the Fed paralyzing until we see a more significant change in the data. That said, the growth-related macro data can still affect the shape of the yield curve, Equity sector / factor selection, and overall index levels. Today, we receive ISM-Srvcs and Bulls will want to see a beat. Feroli forecasts a 51.0 print vs. 51.5 survey; 50.8 prior. Among the earnings, keep an eye on CAT for the macro read-through.

BY Doug Kass · Aug 5, 2025, 6:20 AM EDT

BY Doug Kass · Aug 5, 2025, 6:10 AM EDT

BY Doug Kass · Aug 5, 2025, 6:02 AM EDT

The S&P Short Range Oscillator moved to -0.15% vs. -1.59%.

BY Doug Kass · Aug 5, 2025, 5:54 AM EDT

If something like this is not "papered" it isn't really a deal. My two cents 3/3 ft.com/content/c1183b…