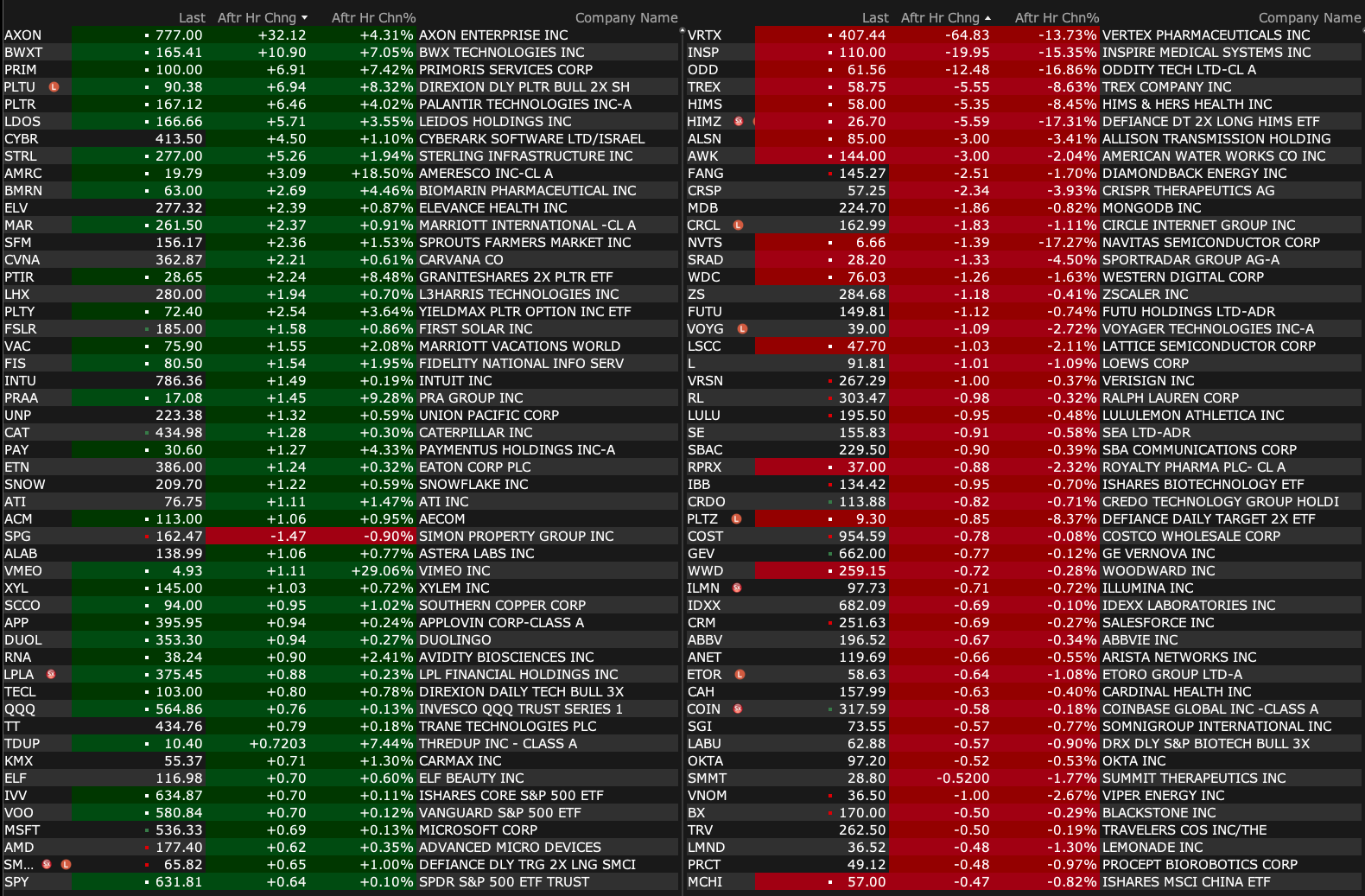

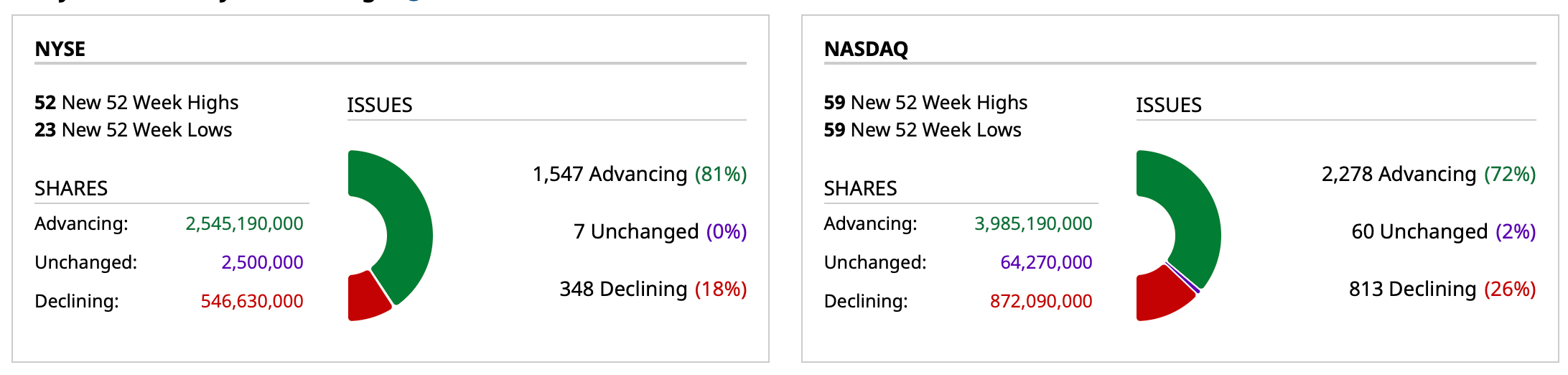

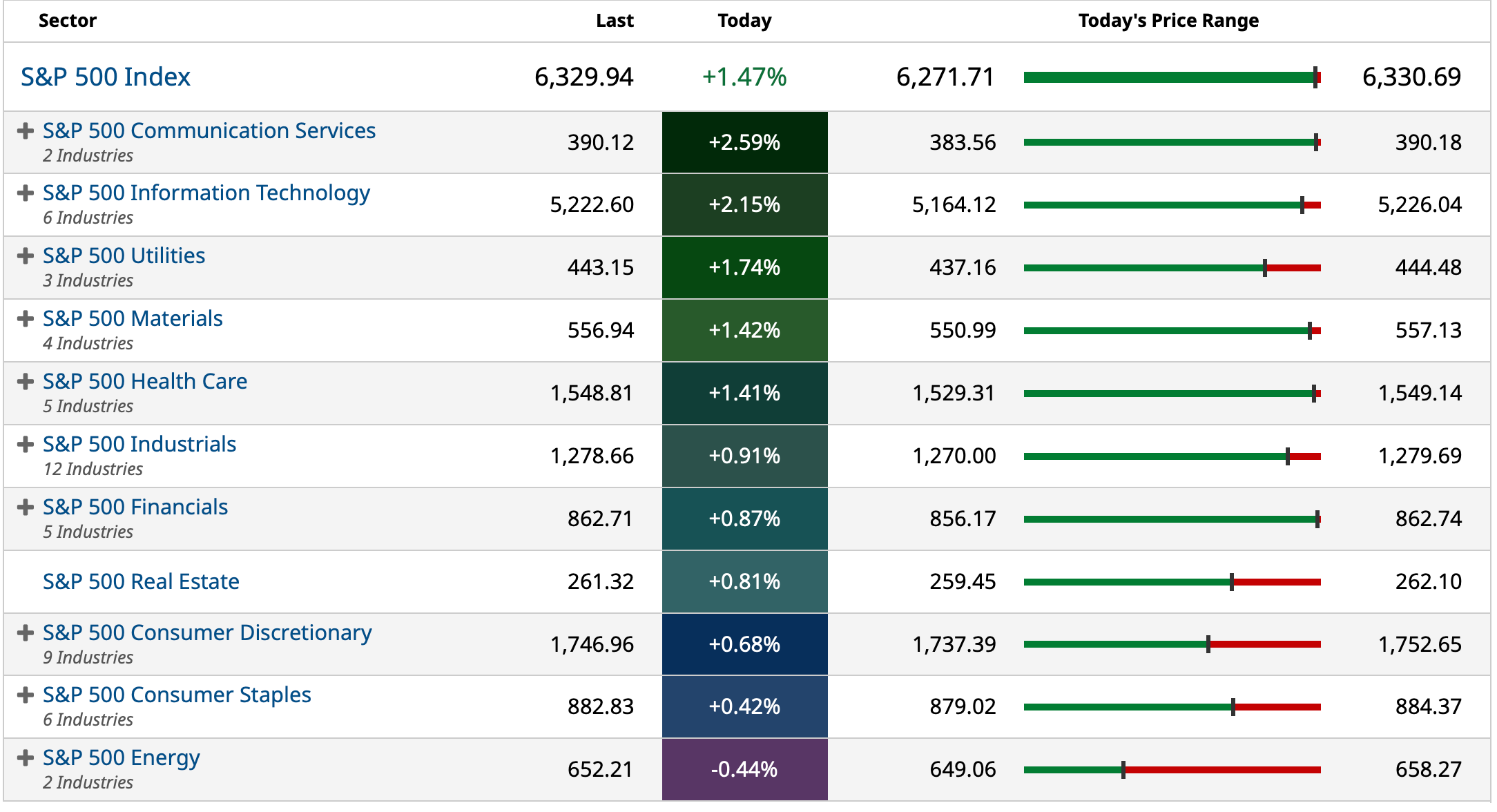

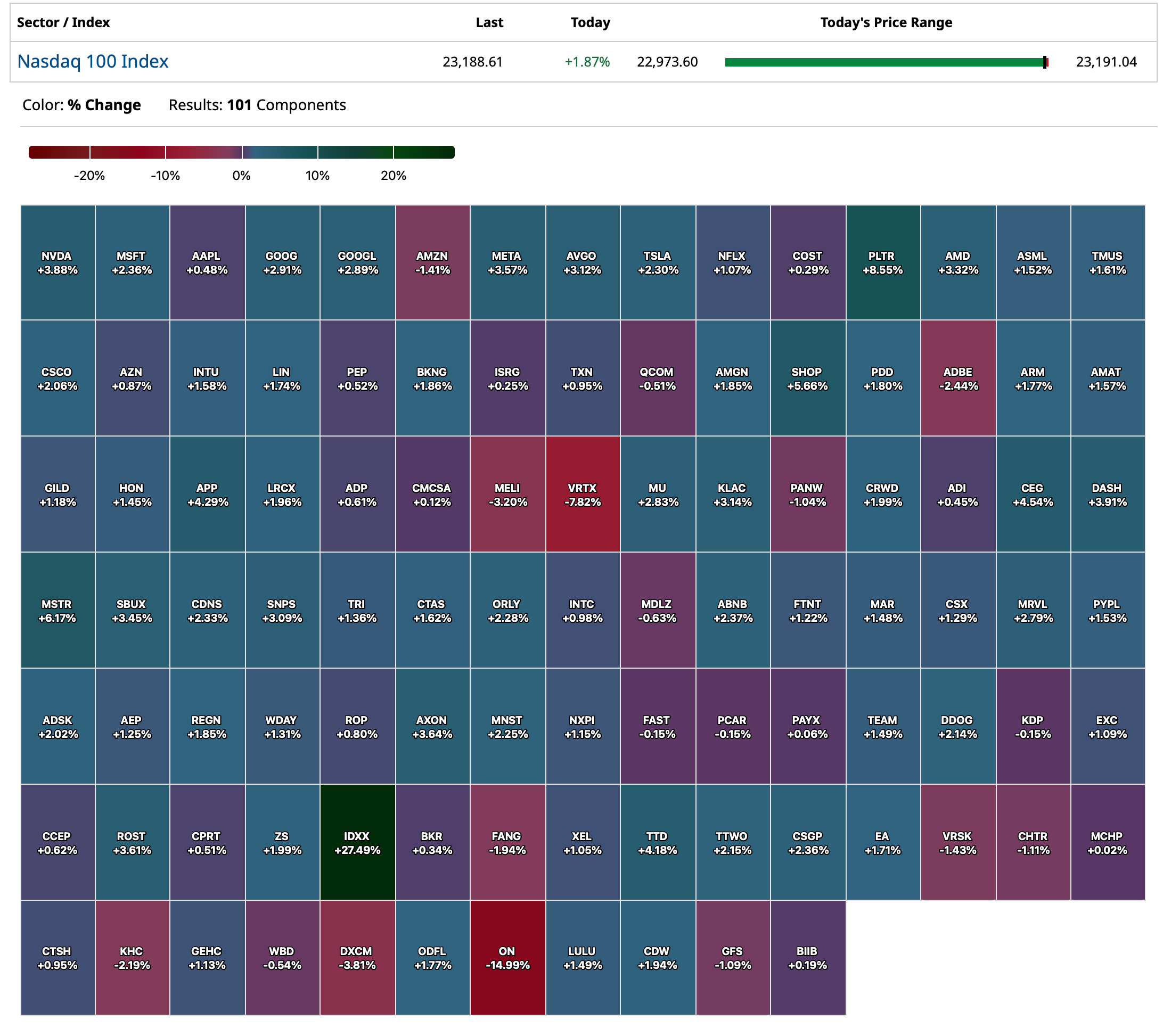

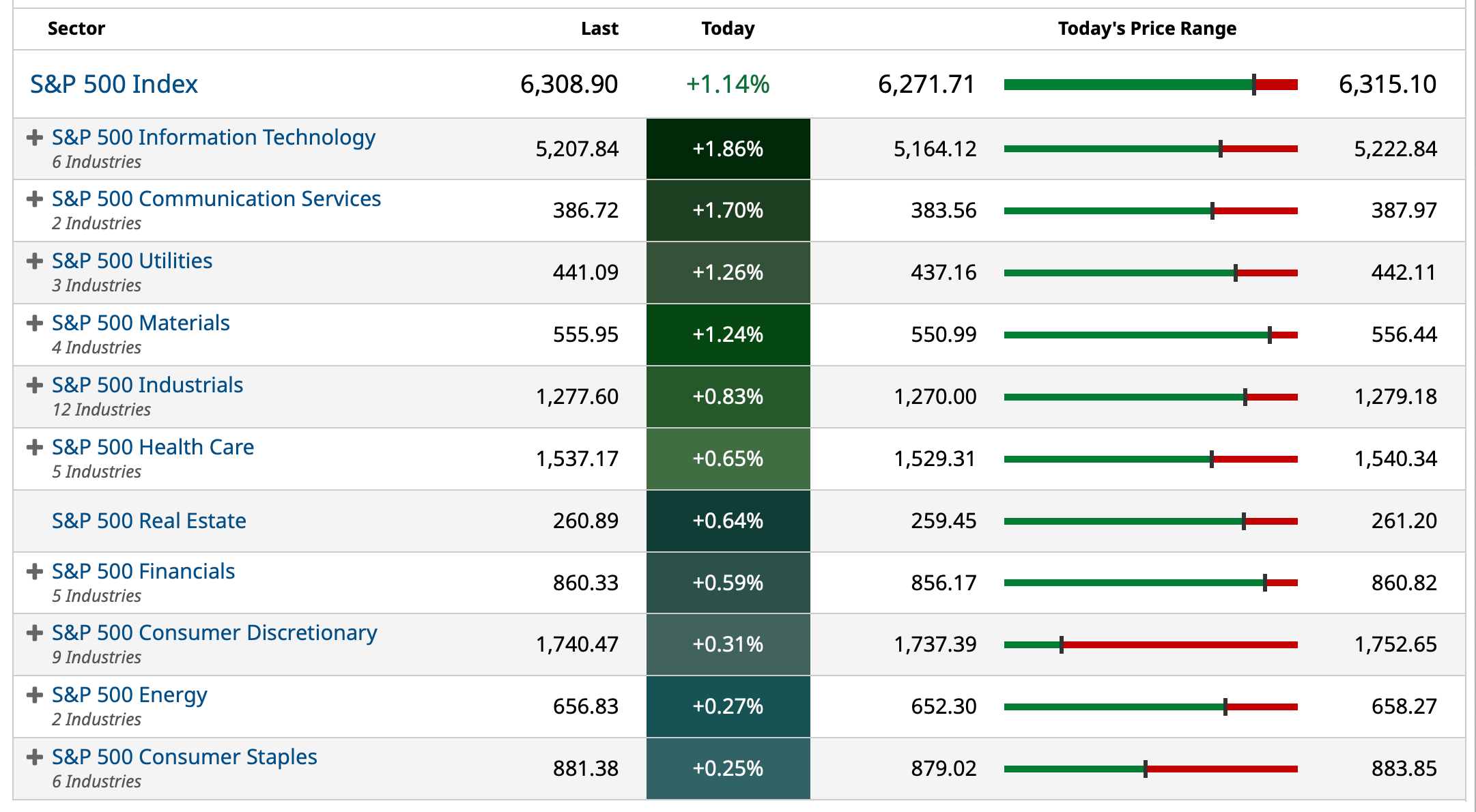

Monday's After-Hours Movers

As of 4:20 p.m.

BY Doug Kass · Aug 4, 2025, 4:46 PM EDT

As of 4:20 p.m.

BY Doug Kass · Aug 4, 2025, 4:46 PM EDT

- NYSE volume 11% below its one-month average;

- NASDAQ volume 29% below its one-month average;

- VIX index: down 14.03% to 17.42

BY Doug Kass · Aug 4, 2025, 4:33 PM EDT

I have a family emergency to attend to.

I will be back tomorrow morning.

BY Doug Kass · Aug 4, 2025, 3:15 PM EDT

* Post Script to "More Tales From Nvidia."

I saw a recent analysis that showed any benefit from using AI to write code up front is wiped out by the extra debugging cost on the back end. It is not dissimilar that the benefit of using an LLM for search is partially wiped out by double checking all the source material. It seems, though, that the system costs of writing code are actually worse.

I couldn’t find the analysis, so I decided to ask the AI (Perplexity), and the chart in my previous More Tales is what the AI returned as an answer.

Imagine if the user of the AI to write the code was actually paying enough to the service provider such that the service provider was actually making a profit. The answer would be much worse. Thusly, on a full system basis, the answer is much worse than the AI suggests. The AI, of course, cannot think, and therefore cannot make this simple logical leap.

I asked: Is the savings from AI writing code lost from the extra debugging cost?

Here was the response:

The cost savings from AI writing code are often partially or even fully offset by increased debugging and maintenance expenses, especially when AI-generated code is used without careful oversight.

Key Findings

What This Means in Practice

Bottom Line

In summary, AI can deliver impressive savings in code writing speed, but these are often eaten up by greater debugging and maintenance costs unless mitigated by strong team practices and the use of AI-powered code analysis/debugging tools. Ignoring long-term quality management will likely result in higher overall costs, not lower

BY Doug Kass · Aug 4, 2025, 3:10 PM EDT

BY Doug Kass · Aug 4, 2025, 1:46 PM EDT

With the JOET ETF looking more like a momentum stock fund (like GRNY) I am adding to my short as the constituent holdings of both (the tip of market leadership) seem vulnerable to this observor in the weeks and months ahead.

BY Doug Kass · Aug 4, 2025, 1:30 PM EDT

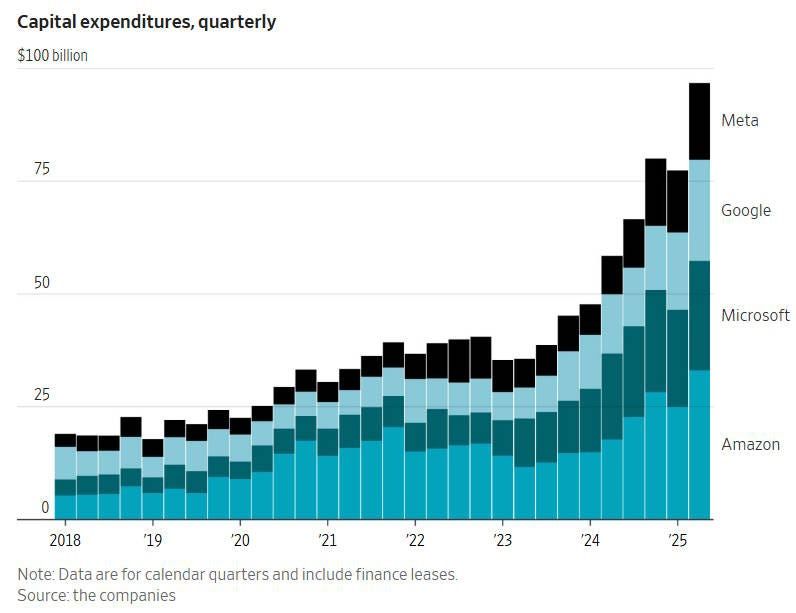

The chart below is on "Big 4" (MSFT, META, GOOGL, AMZN) capital expenditures. Infrastructure capex is already 20% higher as a % of GDP than what was spent on telecom and internet infrastructure at the peak of the dot-com boom.

For Microsoft and Meta, capex is now more than a third of their total sales. Capex also ignores the absurd sums of money being paid to the software designers, which are a much bigger part of the equation than what occurred in the dot-com era, so who knows how much higher the all-in spending is when you account for the soft costs.

Then, I also think this is more of a global phenomena with regard to it all happening at once, than the dot-com boom as well, so if the global spending data were accumulated the global spend rate would be substantially higher than it was then. "Capex spending for AI contributed more to growth in the U.S. economy in the past two quarters than all of consumer spending," says Neil Dutta, head of economic research at Renaissance Macro Research, citing data from the Bureau of Economic Analysis.

I reiterate once again, the depreciation schedules being used for this capital are absurd, as is CoreWeave CRWV reporting earnings before capital expenses! If accounting practices were tied to economic reality, which they should be, they would be an important governor on spending behavior. It is too bad general principles are not more strictly adhered to, because they exist for a reason and do have real value. Just like laws exist for a reason.

Also, overnight Microsoft pushed out a software update, that completely destroyed my computer, which is also pretty new. This has never happened to me before. Thankfully, I was able to get it resolved by wiping out the update. I am wondering if they used AI to help write the code, and I am not kidding.

Writing code was one thing I thought AI would be quite good at, because unlike language and thought, code is bound by much stricter rules and logic. But even that has not turned out to be the case. I saw a recent analysis that showed any benefit from using AI to write code up front is wiped out by the extra debugging cost on the back end. It is not dis-similar that the benefit of using an LLM for search is partially wiped out by double checking all the source material. It seems though that the system cost of writing code are actually worse.

I couldn’t find the analysis, so I decided to ask the AI (Perplexity), and below the chart, interestingly, is what the AI returned as an answer. Imagine if the user of the AI to write the code was actually paying enough to the service provider such that the service provider was actually making a profit. The answer would be much worse. Thusly, on a full system basis, the answer is much worse than the AI suggests. The AI, of course, cannot think, and therefore cannot make this simple logical leap.

BY Doug Kass · Aug 4, 2025, 1:05 PM EDT

BY Doug Kass · Aug 4, 2025, 12:50 PM EDT

BY Doug Kass · Aug 4, 2025, 12:35 PM EDT

BY Doug Kass · Aug 4, 2025, 12:10 PM EDT

- NYSE volume 10% below its one-month average;

- NASDAQ volume 33% below its one-month average;

- VIX index: down 10.84% to 18.17

BY Doug Kass · Aug 4, 2025, 11:50 AM EDT

The Federal Reserve has two jobs, in theory. Price stability and employment.

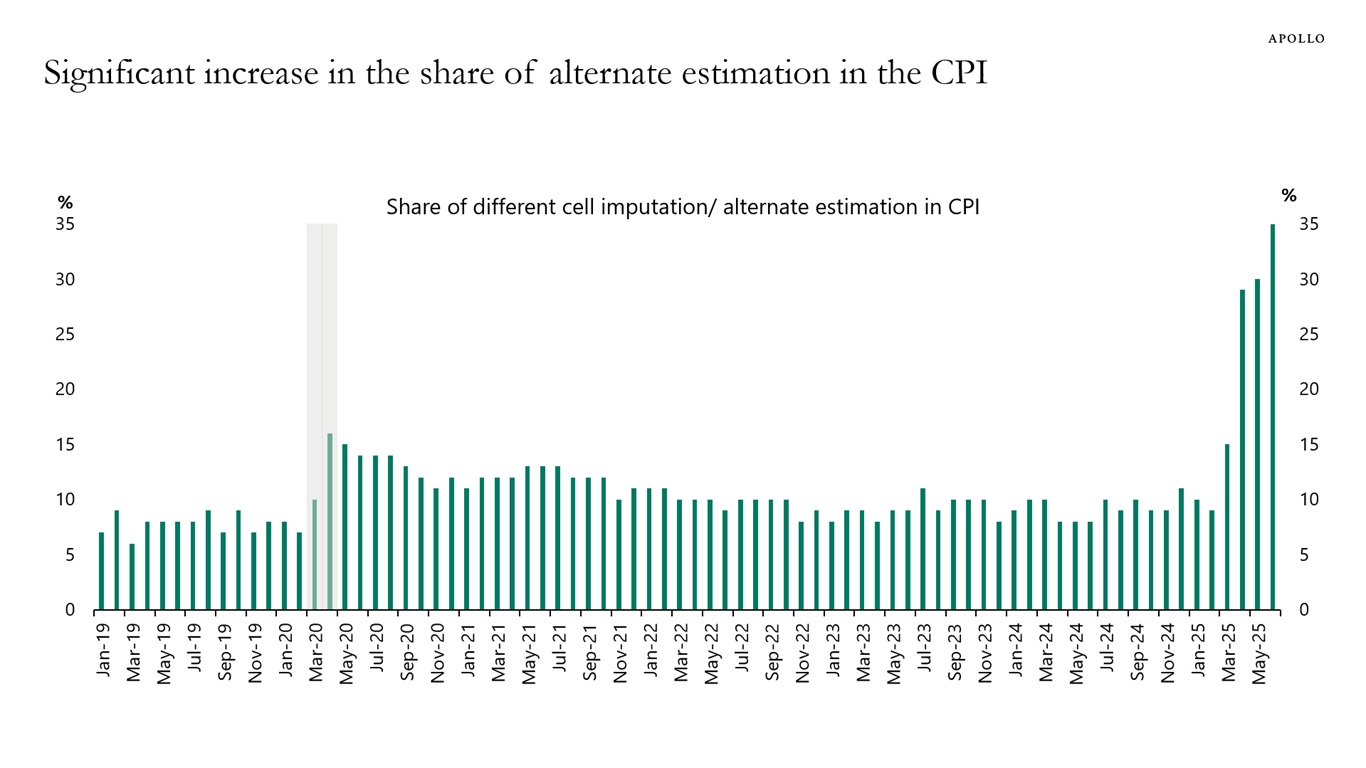

Most are aware of the recent controversies regarding employment data. I recently saw the chart below on the quality of data in the CPI. Notwithstanding all of the issues relative to the terrible judgement at times the Fed seems to have had, on top of it all, the data being used to form their views around the two most important issues in their mandate, is all garbage. How is this supposed to work? The CPI data may be even worse than this chart indicates, because the calculus of Owners Equivalent Rent, which is also an estimate, is absurdly done and that is roughly another 26% of the CPI. Then of course all the other garbage like hedonics, substitution, and who knows what else.

As to how much of what is going on is political or incompetence, my guess is both. It is certainly incompetent the money they have spent on the Eccles building, and themselves, and the whole institution seemingly is UBI for a bunch of academic incompetents that have aided and abetted the government in running the country into the ground.

Powell is not cutting now. In the prior administration he was very very very late to increase rates, and then he cut them going right into an election, which is a no no. Under the prior administration, the fake jobs data kept showing massive unexplainable upside, which is what drives the markets and a president's and parties' approval rating, then interestingly, the massive downward revisions (that nobody cares about and they don’t hit the news cycle and damage election chances) came at exactly the time needed to encourage the Fed to cut leading up to the election.

On the other side of the coin, these guys are jawboning the Fed to cut in part because interest expense on the national debt is too high. That is decidedly not the job of the Fed. It is the job of the government to get the fiscal house in order, such that there is less pressure on rates. Rates and interest expense should be an important governor on government spending.

Then, these guys now also seemingly want to take the revenue generated from tariffs and spit out checks to everyone in the country. This is just absurd, especially with debt levels where they are. This is just a crafty form of vote buying leading into mid-terms, and no different than what the other guys were trying to do with student debt relief and other forms of stimmies. And we know what that caused.

Lastly of course it is quite odd to claim that the jobs market is substantially better than what is being reported, and then asking the Fed to cut substantially at the same time, with inflation still running above targeted levels.

From Apollo Academy:

The Quality of CPI Data Continues to Deteriorate

To calculate CPI inflation, BLS teams collect approximately 90,000 price quotes every month covering 200 different item categories, and there are several hundred field collectors active across 75 urban areas.

When data is not available, BLS staff typically develop estimates for approximately 10% of the cells in the CPI calculation. However, the share of data in the CPI that is estimated has increased significantly in recent months and is now above 30%, see chart below.

In other words, almost a third of the prices going into the CPI at the moment are guesses based on other data collections in the CPI.

BY Doug Kass · Aug 4, 2025, 11:30 AM EDT

Below is a short video with Dr. Jeremy Siegel (never thought I would ever send out something from him!) being interviewed on CNBC. Apparently, the employment report is done by survey, and there is only a 60% response rate. Later, he mentions the JOLTS are done the same way, and there is only a 20% response rate.

This is the year 2025, and this is how we are still doing things? This is embarrassing. It is the same thing w/regard to the CPI.

It is hard enough getting monetary policy right with good data, and probably impossible with bad data. At least those setting policy should realize the data they are using is bad, and make decisions accordingly, but they don’t. They seem to proceed on the basis that the data they have is both good, and relevant. This is not just a current issue, it has happened over many cycles. In 2008, they missed the fact that housing prices were obviously exploding north, because they were staring at the OER number which was badly lagging, and that overwhelmed the consumer price index. All it would have taken was a little common sense (and less politics). Same goes for this prior cycle, where they were way behind and let inflation get out of control before they tightened. Those in the real world saw it, while somehow those in the Fed relied on bad numbers, and did not see it.

Even if the BLS is completely apolitical, it does not absolve them, or anyone else, from the fact that they are terrible at their jobs. They should be fired for being incompetent, and the CPI and employment reports really need to be cleaned up ASAP.

The whole system – the Fed and the Bureau of Labor Statistics needs a COO (a business person) to come in and oversee it. Instead of renovating buildings and having a giant staff of people that write meaningless white papers, these institutions need to be completely restructured. Granted, sadly, anyone who comes in would in theory be a political appointee. But that might be the best we can do, but someone with common sense needs to clean up the mess. The institutions need to stay independent, but the way they are run needs to be reformed, especially the data collection and how much resources they have and what they are spent on. Tax dollars should not be spent on building monuments and bureaucratic staff, like the universities do with their endowments, expanding the size of their kingdom at the expense of those they are meant to serve. The people running these institutions have not had the common sense to invest resources into doing things better. Instead they have been invested in the aforementioned buildings and white papers. In 2025, chunks of the CPI data should be automatically collected electronically, using real world prices that are easily available. Jobs data should be done in a similar fashion. It should all be real time. None of this is hard.

Here's the video: https://youtu.be/O-LtsTnXg-Y?feature=shared

BY Doug Kass · Aug 4, 2025, 11:10 AM EDT

BY Doug Kass · Aug 4, 2025, 9:45 AM EDT

With S&P cash +55 handles I am back to medium sized short the indexes - here are the adds:

* SPY $627.07

* QQQ $560.62

BY Doug Kass · Aug 4, 2025, 9:37 AM EDT

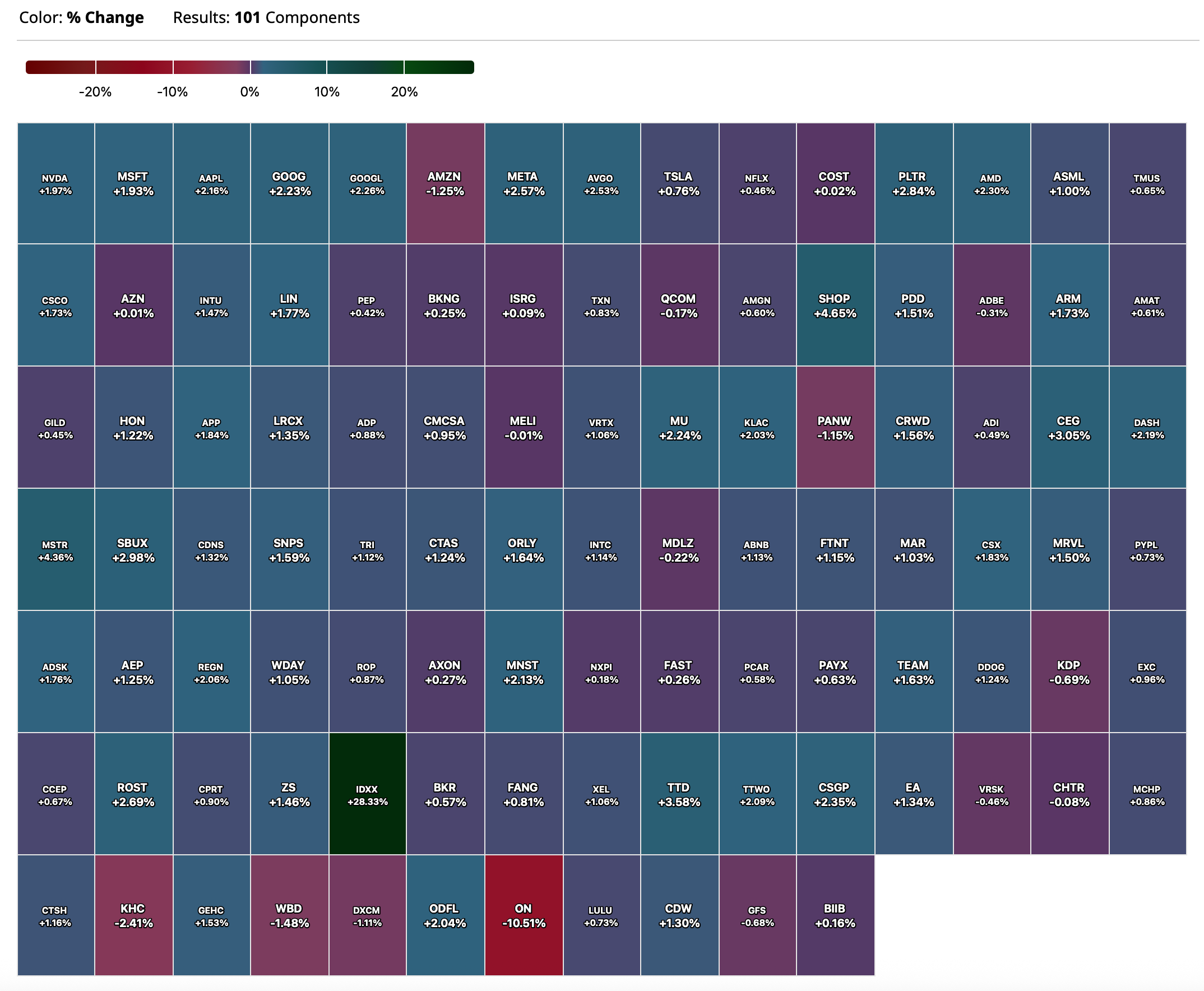

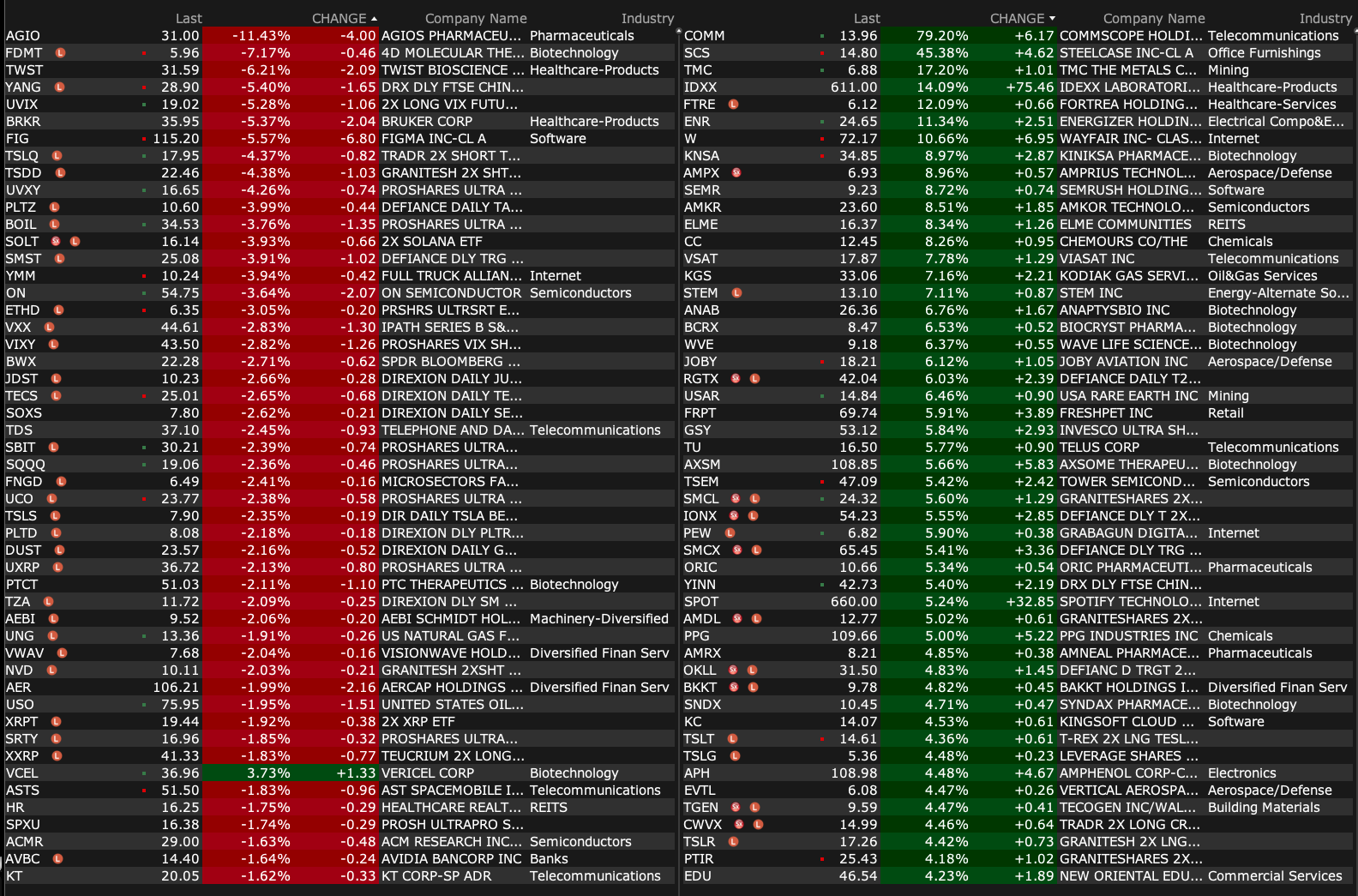

-VERB +99% (announces ~$558M Private Placement of 58.7M shares at $9.51/shr to establish first publicly listed TON Treasury Strategy Company, in partnership with Kingsway Capital)

-COMM +75% (confirms Amphenol Corporation to acquire connectivity and cable solutions business from CommScope for $10.5B cash; reports Q2 earnings)

-SCS +45% (to be acquired by HNI Corporation at $18.30/shr in $2.2B stock-cash deal)

-BLDE +27% (confirms sale of Passenger Division to Joby for stock or cash, at Joby’s election, up to $125M)

-TMC +18% (Tonga and TMC renew sponsorship agreement for seafloor mining; study shows $23.6B combined project value for deep-sea metals)

-OPEN +17% (regains compliance with NASDAQ)

-IDXX +13% (earnings, guidance)

-PRAX +13% (earnings, guidance)

-W +10% (earnings, guidance)

-ENR +9.4% (earnings, guidance)

-SONN +9.3% (expands Clinical Evaluation of SON-1010 Dose Escalation with Atezolizumab in Ovarian Cancer)

-KGS +7.2% (to be added to S&P 600 Index)

-BCRX +6.5% (earnings, guidance)

-ELME +6.1% (concludes Strategic Alternatives Review Process; executes agreement to sell 19 properties to Cortland for $1.6B cash, remaining assets to be marketed for sale)

-JOBY +6.0% (BLDE confirms sale of Passenger Division to Joby for stock or cash, at Joby’s election, up to $125M)

-FRPT +5.9% (earnings, guidance)

-SPOT +5.3% (said to raise premium subscription price in select markets by ~9% from September)

-DYN +4.5% (announces FDA Breakthrough Therapy Designation for DYNE-251 in Duchenne Muscular Dystrophy (DMD))

-APH +4.3% (to acquire connectivity and cable solutions business from CommScope for $10.5B cash)

-LOGI +4.2% (momentum)

-AEO +4.0% (President Trump praises company’s Sidney Sweeney ad)

-LYFT +4.0% (to partner with Baidu to deploy autonomous rides across Europe)

-TSN +4.0% (earnings, guidance)

-CC +3.0% (Chemours, DuPont, and Corteva settle New Jersey PFAS claims; Total payments of $875M over 25 years starting early 2026)

-BNTX +2.9% (earnings, guidance)

-AXSM +2.2% (earnings)

-TSLA +2.2% (discloses 2025 CEO Musk Interim Award of 96M shares of common stock; reports prelim Jul China deliveries)

-REPL -38% (weakness following report Vinay Prasad did not play a major role in FDA’s decision not to approve company’s RP1 drug)

-HNI -19% (acquiring SCS at $18.30/shr in $2.2B stock-cash deal)

-BRKR -5.4% (earnings, guidance)

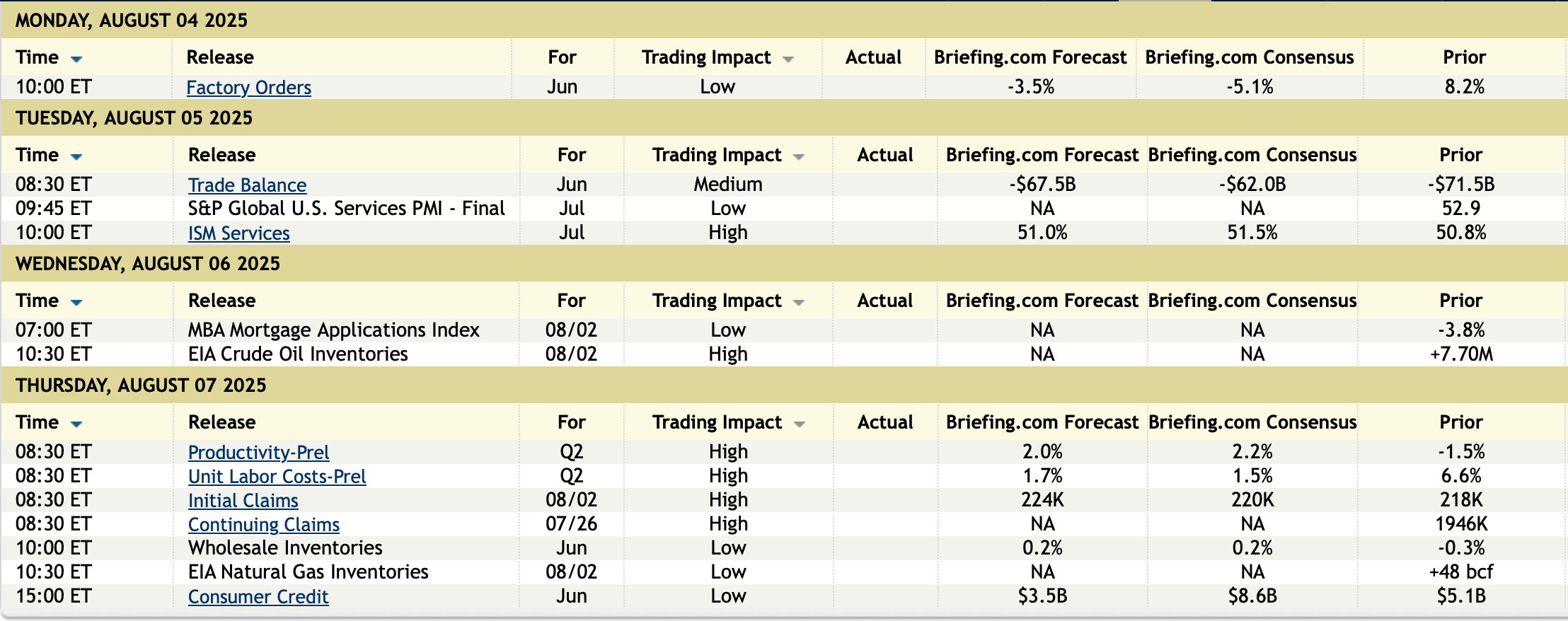

BY Doug Kass · Aug 4, 2025, 9:15 AM EDT

TREASURY AUCTION FOR TODAY:

11:30 a.m.: Treasury hosts a $82B 3- and $73B 6-Month Bill Auction

ECONOMIC CALENDAR FOR THE WEEK

BY Doug Kass · Aug 4, 2025, 9:05 AM EDT

BY Doug Kass · Aug 4, 2025, 8:55 AM EDT

BY Doug Kass · Aug 4, 2025, 8:40 AM EDT

From Peter Boockvar:

For those who don't want to rely on the BLS for their employment information luckily we have ADP who has millions of actual payroll slips. In their report last Wednesday, the 3 month job growth average in the private sector was 37k vs the 6 month average of 67k and the 12 month average of 130k.

I guess the main question of who will replace outgoing Fed Governor Adriana Kugler is whether that person will be the eventual Fed Chair in a sort of training run or will it be someone who will serve out the full 14 year term.

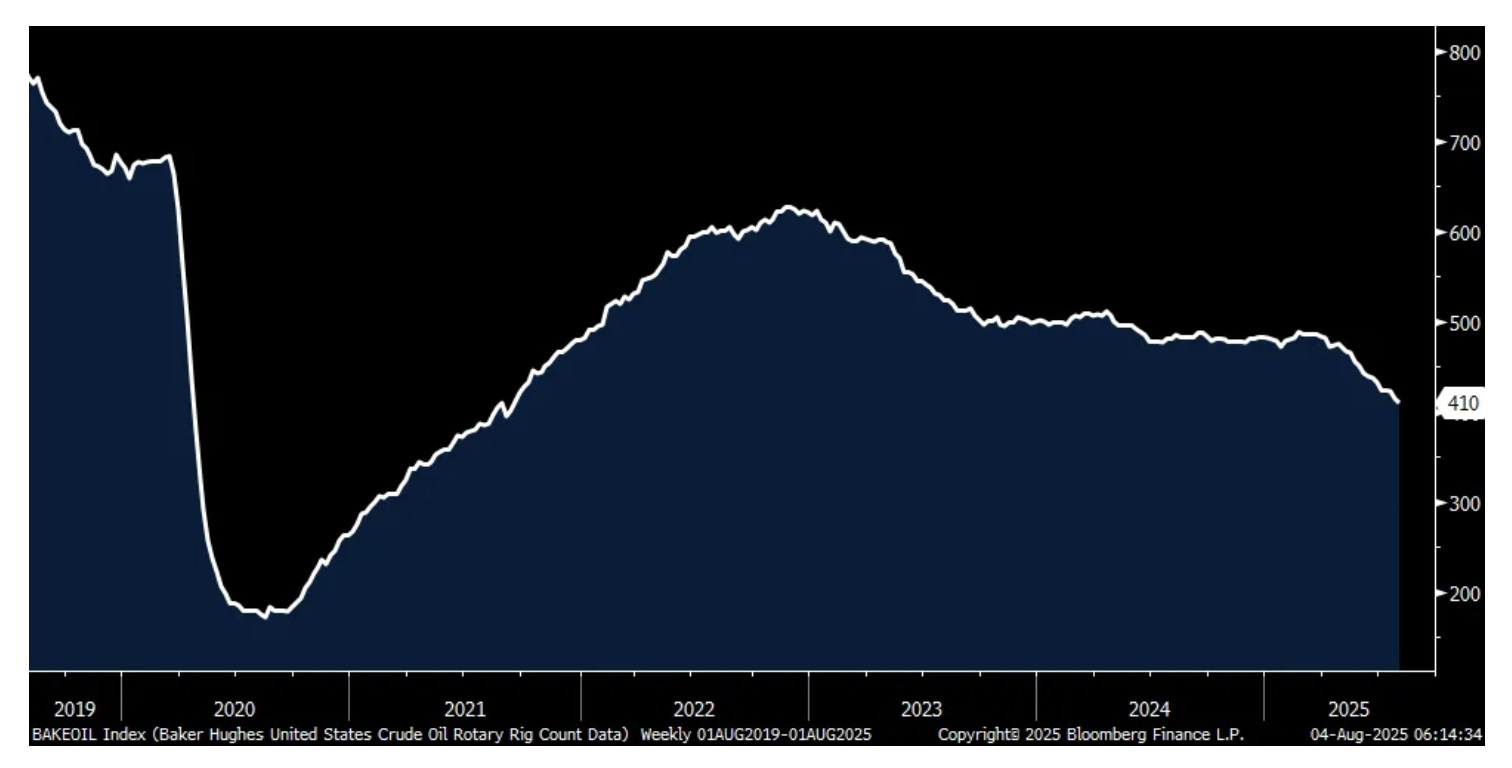

While OPEC has now fully reversed the quota on all of their post Covid response of 2.2mm barrels of production cuts, US oil companies/shale continues to do their best to offset that. The Baker Hughes crude oil rig count fell for a 14th straight week and by another 5 barrels and by 65 during this time frame to 410. That's the least since mid September 2021. It's growing more likely that US oil production will be down in 2025 y/o/y. Keep in mind too that over the past 20 years, about 85% of non-OPEC oil supply came from US shale.

Crude Oil Rig Count

To some Friday earnings calls and reflecting the choppy macro environment.

From Colgate Palmolive, who makes things we use every day like toothpaste, deodorant, soap, and shampoo.

"There is a persistently cautious consumer in North America right now. We saw some rebound in April, May. The categories took a little step back in June, which we weren't expecting."

"Many of our markets and categories around the world remained challenging in the second quarter and we expect this to continue through the second half of the year."

"The cost environment is difficult as we're dealing with tariff increases, higher raw and packaging material costs, and less underlying category inflation. This means that our revenue growth management strategies need to drive additional pricing and mix with lower levels of elasticity as we look to improve organic sales growth in the second half of the year."

"Pricing growth was 2% in the quarter...We have additional pricing and revenue growth management opportunities planned for the balance of the year."

"The overall promotional environment is still quite constructive."

Their tariff cost hit will be $75 million for 2025, though down from their previous guidance of $200 million.

From Kimberly Clark, the maker of tissues, toilet paper and diapers (both for babies and adults) and a stock we own:

"In an environment where the consumer wallet is stretched, we are focused on cascading innovation across the value spectrum ensuring the varying needs of our consumers are addressed within our portfolio."

"I do see purchasing power under pressure for consumers. And frankly, we don't really see a catalyst for that dynamic to change in the near to medium term. So for us that does affect some of the categories. However...our categories are essential. There's not a whole lot of substitutes for our products. And so because of that, demand remains resilient and the categories continue to demonstrate durable growth."

Tariffs are going to cost them $170 million with mitigation of $50 million, leaving them still with a $120 million hit.

From WW Grainger, the distributor of so many things into the industrial/manufacturing world and whose stock fell 10% Friday:

"It feels like the demand environment is still relatively muted. But we do feel like we're doing reasonably well in that environment."

On how they are dealing with tariffs, "As we shared during our first quarter earnings call, we took initial pricing actions in May, primarily related to Section 232 and the first wave of announced tariffs on China. These initial pricing actions only apply to a small portion of our products, largely those where Grainger is importing the product directly. As part of this initial wave, we did not take any pricing action on the reciprocal escalations. Consequently, we expect our initial pricing actions to hold as they relate to tariff levels that remain in place today."

They see these May actions "will approach the previously discussed 1% to 1.5% net annualized price inflation run rate for the High Touch business."

But, there is more. "Looking ahead to the third quarter, we expect to adhere to our regular cycle with our next pricing actions slated to go live in early September. This round will include some further increases on products directly imported by Grainger to reflect current tariff rates, which are higher than what we passed in May. The September cycle will also include initial pricing actions on supplier imported products where we have finalized negotiations. The past price from this round is expected to result in net annualized incremental price of 2% to 2.5% on a run rate basis for the High Touch business."

To a question on whether price increases would impact demand, "I guess what we would say is we think that price increases in general and inflation in general is going to have an impact on market demand. So, we have the market demand not doing so well in the back half as we had in the first half. So that's where you see that impact. We don't think we are uniquely exposed. We think everybody's doing the same thing, and so we feel confident in our ability to realize prices with that lower market demand."

How do European investors feel about the trade deal with the US? The August Sentix Investor Confidence index fell to -3.7 from +4.5 and worse than the estimate of +6.9. Sentix said, "Investors are not impressed by the EU's latest tariff deal with the US...The negative factors clearly out weigh the positive ones for the global economy. The EU and Switzerland are being punished severely. The US and Donald Trump may feel like winners in the short term, but falling expectations here too indicate that this type of trade policy will mainly produce losers."

Some more, "The wrinkles of concern in the economy are deepening again." The Germany index fell to -12.8, down by 12 pts.

Sentix European Investor Confidence index

BY Doug Kass · Aug 4, 2025, 8:19 AM EDT

marvinleftwich

When buying a put on the SPY to hedge your portfolio, how much time do you allow till expiration?

Dougie Kass

As you can see in my Diary I rarely buy puts (and pay premium).

More often I sell in the money calls (and take in premium).

BY Doug Kass · Aug 4, 2025, 8:00 AM EDT

BY Doug Kass · Aug 4, 2025, 7:50 AM EDT

* Freshpet lowers short-term and intermediate-term guidance.

* I would still avoid being long the sector (which I am net short of).

I had sold out of FRPT a while ago and remain short the space.

An excerpt from Freshpet's EPS release just now:

For full year 2025, the Company is updating its guidance and now expects the following:

The Company is also updating its long-term guidance. For full year 2027, the Company is removing the $1.8 billion net sales target to adjust for the recent slower growth; however, the Company expects to continue to deliver growth significantly in excess of the dog food category. The Company is reiterating its Adjusted Gross Margin target of 48% and Adjusted EBITDA Margin target of 22% for full year 2027.

The Company does not provide guidance for net income (loss), the U.S. GAAP measure most directly comparable to Adjusted EBITDA, and similarly cannot provide a reconciliation between its forecasted Adjusted EBITDA and net income (loss) metrics without unreasonable effort due to the unavailability of reliable estimates for certain components of net income (loss) and the respective reconciliations, including the timing of and amount of costs of goods sold and selling, general and administrative expenses. These items are not within the Company's control and may vary greatly between periods and could significantly impact future results.

Freshpet, Inc. Reports Second Quarter 2025 Financial Results

BY Doug Kass · Aug 4, 2025, 7:40 AM EDT

From JPMorgan (who steps back from bullish short term call)...

US: Futs are higher as markets look to rebound from last week’s sell-off amid increased expectations for rate cuts. Pre-mkt, Mag7 and Semis are outperforming with Cyclicals over Defensives. Bond yields are 2-3bp higher as USD falls. Cmdtys are weaker with Energy underperforming as OPEC+ approves another supply hike. This is a catalyst-light week with tmrw’s ISM the most important and heightened focus on weekly claims with the Fed spotlighting the unemployment rate.

and...

While we remain Tactically Bullish, conviction is waning and think it prudent to move away from being maximally long. Last week’s data and tariff releases are reducing support for our investment hypothesis of (i) resilient macro data; (ii) positive EPS growth; and (iii) improving Trade War rhetoric / lower tariffs. Cracks in the economy continue to form as we approach negative seasonality but think there is an opportunity for stocks to continue to rise with the aid of macro data points, ISM-Srvcs (Aug 5) and CPI (Aug 12). Masked in the macro turmoil was a strong week for earnings; the SPX is on track to deliver its third consecutive double-digit earnings growth quarter. More color on our thinking follows in the subsequent sections.

· NEW MONETIZATION MENU – We still like most of the previous Monetization Menu but would flag the Cyclicals may struggle if ISM-Srvcs disappoints; the same argument applies to RTY. We like being Tactically Short Europe as both macro and micro environments are challenged.

· OLD MONETIZATON MENU – For Longs, we like Tech (includes a tactical preference for Software over Semis but would not short Semis), Mag7, AI Theme (including Chinese Tech), Cyclicals (esp. Fins and Industrials), and the Quality factor. Keep an eye on the USD rally. For International plays, Japan appears the most attractive, but tariff announcements are driving short-term plays (e.g., Brazil, India). For Shorts or Hedges, consider RTY (higher-for-longer), Beta Factor (overly crowded), Metals / Miners (copper tariff exemptions), some Discretionary plays (e.g., Autos, Homebuilders, parts of Transports). Further, consider using derivative plays to hedge such as SPX puts / put spreads or long VIX plays.

Last week, the SPX fell 2.4%, ending the week on a 4-day losing streak after an ATH on Monday. The initial angst began with Powell’s press conference on Wednesday where he failed to eliminate the possibility of a rate hike, triggering a sell-off in stocks. While META / MSFT earnings were impressive the market failed to hold gains on Thursday. AAPL / AMZN had solid prints but saw significant selling pressure leading to futures being lower, when combined with the ‘Liberation Day 2.0’ with Trump sending tariff letters to 60+ countries, on Friday where a weaker NFP report, spot missed expectations and then the prior two months revised lower by 258k jobs, dragged the market even lower. CTAs, dealer gamma, and rebalancing may have played a role in what many thought was an overbought market.

As we assess the health of the economy, recall Powell’s comments on watching the unemployment rate, which increased from 4.1% to 4.2% (4.248% unrounded), as he sees both labor supply and demand decreasing in tandem. The labor market is not hiring but we are not seeing mass layoffs, though that may change. The Challenger Job Cuts report (here) gives some additional insights for the 806k YTD . The top reasons for why companies are cutting jobs are (i) DOGE – inducing 290k layoffs; (ii) Market & Econ Conditions –171k layoffs; (iii) Closing of Stores – 120k layoffs; (iv) Restructuring – 67k layoffs; (v) Bankruptcy – 36k layoffs; (vi) AI Related – 30k cuts. When looking at hiring plans, there are 86,132k hiring announcements YTD, +17% YoY. This equates to 12,305 hiring announcements per month which compares to 64,163 for FY24 and 87,407 average from 2016 - 2019. The picture is one of slowing growth but not a recession as Feroli sees real GDP slowing to 0.75% for 25H2 (full note is here).

BY Doug Kass · Aug 4, 2025, 7:30 AM EDT

Bonus — Here are some great links:

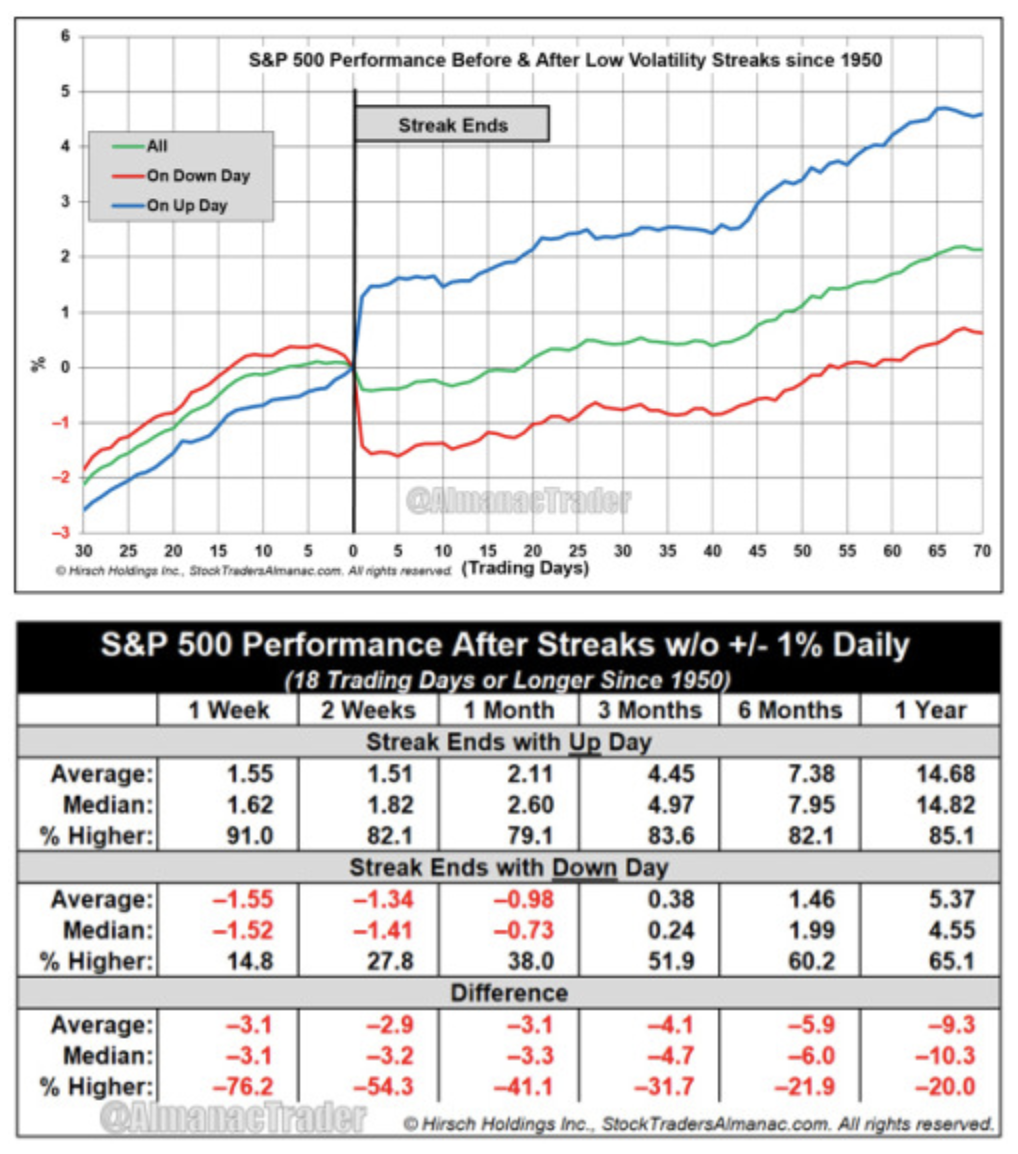

How Low Volatility Streaks End Matter

BY Doug Kass · Aug 4, 2025, 7:15 AM EDT

Back reshorting the indices:

* SPY $625.65

* QQQ $558.45

BY Doug Kass · Aug 4, 2025, 7:05 AM EDT

BY Doug Kass · Aug 4, 2025, 7:00 AM EDT

BY Doug Kass · Aug 4, 2025, 6:50 AM EDT

BY Doug Kass · Aug 4, 2025, 6:40 AM EDT

Wolf Street howls about the demand/supply imbalance in the U.S. residential real estate markets.

BY Doug Kass · Aug 4, 2025, 6:30 AM EDT

* Friday was likely the first shot across the bow...

The S&P Short Range Oscillator moved to -1.59% vs. -0.7, moving more into an oversold.

I am out of all of my index short hedges (not a permanent position, for sure!), having covered into Friday afternoon's swoon.

Bull Markets Die Hard so I don't anticipate a straight-down correction.

Rather, I am expecting a jagged move lower in the weeks and months ahead.

I will be reshorting strength.

Friday was likely the first shot across the bow.

BY Doug Kass · Aug 4, 2025, 6:23 AM EDT