From Peter Boockvar:

Positives,

1) Within the jobs report, average hourly earnings grew by .3% m/o/m and 3.9% y/o/y about in line while the average workweek moved up to 34.3 from 34.2 and vs 34.3 in the month before. Combine the two and weekly earnings rose .6% m/o/m and 4.2% y/o/y still reflecting good income growth.

2) The level of initial jobless claims was at just 218k, little changed with the 217k seen last week and below the estimate of 224k. The 4 week average fell to 221k from 225k and that’s the least since mid April. Continuing claims were unchanged w/o/w at 1.946mm and just off the cycle highs.

3) The June PCE inflation stats were up .3% m/o/m for both headline and core as expected and the headline figure for May was revised up by one tenth. The y/o/y gains were 2.6% and 2.8%, both one tenth above the consensus due to rounding.

4) Personal spending in June was as expected when we include a modest revision to May so no change to GDP estimates for Q2. Spending on big ticket durable goods fell for a 2nd month while rising for nondurable goods. Service spending rose again as it typically does. Income was also about as expected. Specifically looking at the private sector, wages and salaries rose 4.7%, the quickest pace since December.

5) The Q2 Employment Cost Index rose .9% q/o/q, the same pace seen in Q1 but one tenth above the estimate. Private sector wages and salaries rose 3.6% y/o/y vs 3.5% in Q1 and 3.8% in Q4 ’24 (measuring wages/salaries at individual level as opposed to above where it aggregates private sector pay) .

6) The Apartment List rental report for July said new rents were flat m/o/m and down .8% y/o/y. Of note, "The national multifamily vacancy rate ticked up to 7.1% this month, setting a new record for our index. We're past the peak of a multifamily construction surge, but the market is still absorbing all of the new units, and vacancies are still trending up."

7) The July Conference Board’s Consumer Confidence index rose 2 pts m/o/m to 97.2 and that was 1.2 pts above the forecast. For perspective, this index was at 132.6 in February 2020. The Present Situation slipped 1.5 pts, offset by a 4.5 pt rise in Expectations. One yr inflation expectations were 5.8%, down one tenth from June. The Conference Board said “Consumers’ write-in response showed that tariffs remained top of mind and were mostly associated with concerns that they would lead to higher prices. In addition, references to high prices and inflation rose in July, even though consumers’ average 12 month inflation expectations eased slightly.” The answers to the labor market questions were mixed.

8) The final July UoM consumer confidence index rose 1 pt to 61.7 and that is the highest since February though still remains well below the 101 in February 2020. The UoM said, "A rise in sentiment among stock holders was partially offset by a decline among consumers who do not own stocks."

9) From the view of the first time home buyer, S&P CoreLogic said home price growth continued to slow, iup 2.25% y/o/y in May.

10) From Amazon: "There continues to be a lot of noise about the impact that tariffs will have on retail prices and consumption. Much of it thus far has been wrong and misreported. As we said before, it's impossible to know what will happen. Where will tariffs finally settle, especially China? What happens when we deplete the inventory we forward bought or that our selling partners forward deployed in advance of the tariffs going into effect? If costs end up being higher, who will absorb them? But what we can share is what we've seen thus far, which is that through the first half of the year, we haven't yet seen diminishing demand nor prices meaningfully appreciating."

11) From Apple: While there definitely was US pull forward buying of iPhones ahead of tariffs (my wife was one of them) , "We saw an acceleration of growth around the world in the vast majority of markets we track, including Greater China and many emerging markets."

12) From Microsoft: "All up, Microsoft Cloud surpassed $168 billion in annual revenue, up 23%. The rate of innovation and the speed of diffusion is unlike anything we've seen. To that end, we are building the most comprehensive suite of AI products and tech stack at massive scale." Azure revenue growth was 34%, "driven by growth across all workloads." Their Q1 guidance for CapEx is $30b. Annualize that and it's an unbelievable 38% of their expected fiscal '26 revenue of about $318b. It was 13% in their 6/23 fiscal yr ended and 18% in 6/24 fiscal yr.

13) From Meta: With context that there are about 8 million people in the world, "We had another strong quarter, with more than 3.4 billion people using at least one of our apps each day and strong engagement across the board." Also, "On advertising, the strong performance this quarter is largely thanks to AI unlocking greater efficiency and gains across our ad system." On spending, "Capital expenditures, including principal payments on finance leases, were $17 billion, driven by investments in servers, data centers and network infrastructure." On the full year outlook, they expect CapEx "to be in the range of $66 billion to $72 billion, narrowed from our prior outlook of $64 billion to $72 billion, and up approximately $30 billion y/o/y at the midpoint...as we continue aggressively pursuing opportunities to bring additional capacity online to meet the needs of our AI efforts and business operations."

14) From Shake Shack: Comps grew by 1.8% y/o/y and "Trends improved throughout the period and into July." This was helped by "successful marketing activations, operational improvements, compelling menu innovations, and further improving the guest experience."

15) From Mastercard: "Consumer spending remains healthy, supported by low unemployment in wage growth that continues to outpace inflation. This is true across affluent as well as mass market consumers. While macro uncertainty remains due to government actions and geopolitical tensions, overall, we remain positive about our growth outlook as the fundamentals that support consumer spending have been strong...our overall cross border volumes continue to grow well in the mid teens range. This is supported by strong underlying consumer spending and a diversified portfolio across geographies and travel and non-travel spend."

16) From Visa: "Within spend categories in the US, we saw relative stability to Q2 when adjusted for leap year impacts. Both US discretionary and non-discretionary spend growth remained strong and we see no meaningful impact from tariffs...For cross border, total volume growth excluding intra-Europe remains strong and above pre-Covid levels, even with continued impacts from currency weakness and travel to specific countries. While we're not immune to macroeconomic impacts, our business has proven to be diverse, resilient and well positioned to capture the significant opportunities ahead."

17) From Hershey: “Consumption was strong across our top chocolate franchises, with Reese growth of 4%, Hershey up nearly 8% and Kit Kat up 3% in the quarter, behind our summer limited edition programs and media campaigns…Our portfolio led in share gains among the top ten Salty Snack manufacturers this quarter as our brands continue to resonate with consumers for permissible and better for you brands.”

18) From Mondelez: “If I go a little bit around the world, maybe starting in Europe, a good quarter in Europe with good numbers, strong share gains. Clearly the business is very resilient. The consumer is more confident in Europe, still quite fragile and frugal spending, but snacking continues to outpace food. And overall, I would say we feel pretty good about our European business. Consumers are not exactly bullish, and they’re focused on essentials, but they keep buying our category even despite the significant price increases that we had to do in chocolate.”

19) From Camping World: “We set a record selling more RVs than we ever have in an entire quarter, 45,000 units. We set a record in our finance and insurance department, highest amount of revenue we’ve ever generated, $200 million. And we set a revenue record for Good Sam.”

20) From Avis Budget: “So, kind of what we’re seeing in terms of RPD (revenue per day) isn’t all that different from what other participants in the travel industry are seeing. I think demand is firming up post the passage of the Big Beautiful Bill. For us, leisure is stronger than commercial right now. And pricing is more challenged than volume…But we do think that there are signs that things are firming up for the summer and I think summer is off to a good start.”

21) From EBAY: Gross merchandise volume rose 4% y/o/y, "accelerating by over 2 points sequentially. Revenue grew by more than 4%...our marketplace has proven resilient to recent uncertainty brought on by tariffs and trade policy changes...Collectibles was once again the largest contributor to growth as y/o/y growth in trading cards GMV accelerated for the 10th straight quarter on the back of continued momentum in both collectible card games and sports trading cards. Interest in Pokemon cards has surged recently, with GMV growth in the triple digits for the second straight quarter amid renewed interest from collectors and a particularly strong slate of product releases."

22) From MGM Resorts: "During the second quarter and now into July, performance on the weekends has been solid as we've been operating near capacity in our hotels across the spectrum. Our luxury offerings in Vegas maintained rate integrity with slot and table volume increasing about 4% and several properties reporting second quarter records for net revenue." Macau numbers were a record and their regional casinos did well.

23) From Sysco: “Traffic to restaurants improved throughout the quarter and Sysco specific initiatives delivered improved financial outcomes, top to bottom...All considered, Q4 was a relatively steady quarter from the perspective of restaurant foot traffic.”

24) From Royal Caribbean: “Bookings have accelerated since the last earnings call, particularly for close-in sailings. We continue to see engaged and excited consumers with roughly 75% intending to spend the same or more on leisure travel over the next 12 months. At the same time, more than half of consumers tell us they are booking closer to their departure date than they used to and for the people who intend to travel over the next 12 months, the majority have not yet booked.”

25) From Starbucks: "North America, Canada led the way with its second consecutive quarter of positive comparable sales. While in the US, comparable sales declined 2%. We are clearly in the early stages of our turnaround in the US, but our work is gaining momentum." Comps in China turned positive.

26) From Booking Holdings: They saw particular room night strength in Europe and Asia. "Asia in particular saw healthy growth, up low double digits, and we remain optimistic about our long term outlook for the region. The US continued to be our slowest growing region, but growth in the second quarter improved slightly from the first quarter and likely outpaced the broader US accommodations industry."

27) From AutoNation: "As was the case with the industry, our unit sales growth was strongest at the start of the quarter and moderated in May and June. And clearly there was a pull ahead of sales in late March and April in reaction to the tariff announcement, and it stands to reason that some portion of that demand was pulled ahead from the latter part of the second quarter."

28) Overseas manufacturing PMIs: Vietnam 52.4 vs 48.9, Thailand 51.9 vs 51.7, Malaysia 49.7 vs 49.3, Philippines 50.9 vs 50.7, Indonesia 49.2 vs 46.9. India was solid at 59.1 and Australia held above 50 at 51.3.

29) Germany said that unemployment in July rose by 2k people, below the estimate of up 15k.

30) The French economy grew faster than expected in Q2, up .3% q/o/q vs the estimate of up .1%. Consumer spending was a main factor.

31) Economic confidence in the Eurozone in July improved to 95.8 from 94.2, the best since February. Manufacturing confidence, along with services, consumer and retail all gained m/o/m while construction was down slightly.

Negatives,

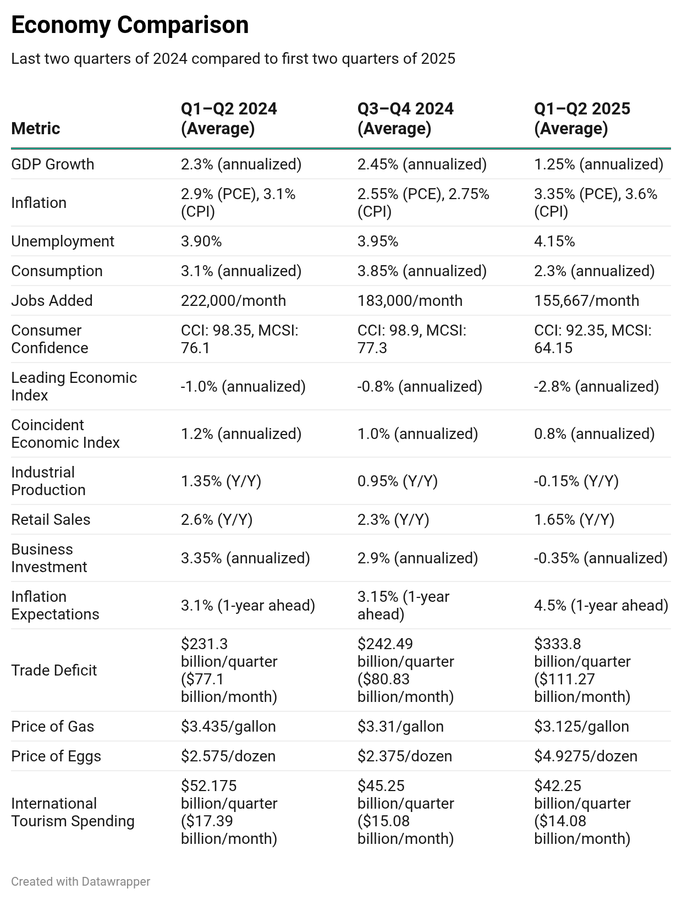

1) July payrolls rose by 73k, below the estimate of 104k and there were big downward revisions to the two prior months of 258k combined. June saw job growth of just 14k with the private sector contributing just 3k vs a rebound of 83k in July. The unemployment rate ticked up by one tenth to 4.2% as expected as the household survey saw a drop of 260k, more than the drop in the labor force of 38k. The all in U6 rate rose to 7.9% from 7.7% and that matches a 5 month high and is just one tenth from matching the most since October 2021. The participation rate continued to shrink at 62.2% from 62.3% and that is the lowest since November 2022. The key 25-54 yr old cohort saw its participation rate fall by one tenth too to 83.4% but still near the recent highs. Of note too, the average duration of unemployment rose to 24.1 weeks, the longest since April 2022, a consequence of the slowdown in hiring. The 3 month average job gain is now just 35k vs the 6 month average of 81k and the 12 month average of 128k.

2) The July Challenger jobs report reflected a 29% rise in layoffs from June and up 140% y/o/y. They said “July’s job cuts are well above average for this month since the pandemic.” Over the past 10 years, July averaged layoffs of 60,398 and this July it was slightly above 62,075. They also said “We are seeing the Federal budget cuts implemented by DOGE impact non-profits and healthcare in addition to the government. AI was cited for over 10,000 cuts last month, and tariff concerns have impacted nearly 6,000 jobs this year.” Also, hiring's slowed to just around 3k, a multi year low.

3) Job openings in June totaled 7.437mm, down by 275k m/o/m and just below the estimate of 7.5mm. With the 2nd straight month of declines in hiring’s, the hiring rate fell to 3.3% which matches the lowest since June 2024 and is just one tenth from matching the least since 2013 not including Covid. The quit rate was at 2% for a 3rd straight month.

4) US GDP growth averaged 1.25% in the first half of 2025.

5) The July ISM manufacturing index fell to 48 from 49 and thus remains in contraction. The employment component fell to just 43.4 from 45. New orders were 47.1 vs 46.4 in the month before while prices paid fell to 64.8 from 69.7, still remaining well above 50. New export orders slipped to 46.1 from 46.3. Inventories fell a touch and remaining below 50. Just 7 industries saw growth vs 10 that are in contraction.

6) Bottom line from Apartment List in their July rent report, "The late spring and summer are normally the peak season for moving activity, and rent growth tends to ramp up at this time of year in tandem with demand. The fact that we've instead seen rent growth get increasingly sluggish indicates softness in the market, possibly reflecting declining consumer confidence amid a more uncertain macroeconomic outlook."

7) The MBA said purchase applications fell by 5.8% w/o/w after rising by 3.4% last week. Refi's fell for a 3rd straight week, down a modest 1.1%.

8) Pending home sales in June fell .8% m/o/m instead of rising by .2% as expected.

9) From Amazon: While AWS revenue growth has slowed to 17% y/o/y, "we have more demand than we have capacity at this point...The single biggest constraint is power. But you also see constraints off and on with chips and then some of the components that once you have the chips to actually make the servers."

10) From Apple: Tariffs will cost them $1.1 billion in the September quarter they estimate.

11) From Microsoft: One snippet of note on LinkedIn, "revenue increased 9% and 8% in constant currency with growth across all businesses, though talent solutions continues to be impacted by weakness in the hiring market."

12) From International Paper: "Industry demand in North America has been relatively stable, but softer than last year as economic uncertainty from tariffs continues to impact industrial production and box demand across the manufacturing sector."

13) From Schneider National: "We expect the economic uncertainty that characterized the second quarter to persist into the back half of the year, with trade policy continuing to evolve. In addition, the timing and impact of regulatory enforcement, such as requirements around English language proficiency and the use of B1 drivers, along with the recent legislative developments, remain unclear. Even so, we believe the most likely path forward is for the freight environment to continue its movement toward recovery, with capacity continuing to exit the market at a slow but steady drumbeat."

14) From Shake Shack: Their guidance includes the "degree of pressure on the consumer spending landscape and ongoing inflationary headwinds."

15) From Clorox: "While we delivered strong margin expansion and adjusted EPS growth for the year, we did not meet our topline expectations in the back half. We continued to see rapidly shifting consumer behaviors and broader market volatility which we expect to continue."

16) From Hershey: “This month Hershey announced a new price action on the entirety of our U.S. confection portfolio. These products represent roughly 80% of total net sales and through a combination of list price and price pack architecture, we will deliver an estimated 16 points of pricing contribution to the overall Company… This pricing announcement reinforces our commitment to covering commodity inflation with pricing over time.” Further, “Regarding tariffs, the global business environment remains dynamic as trade negotiations continue. For the full year, we are now modeling tariff expense in the range of $170 million to $180 million, below our prior expectations, due to inventory on hand, fluctuations in country specific rates, and sourcing optimization. Given the unique circumstances surrounding cocoa, which cannot be grown in the United States, we remain hopeful that tariffs on our largest exposure will improve as trade negotiations continue, though this will likely take time. We are not planning for relief in 2025 and have fully embedded these incremental costs in our full year outlook.”

17) From Mondelez: “If I go to the US, a little bit more of a difficult situation there. There’s a lot of consumer anxiety. They look at quite an uncertain outlook as it relates to their personal finances, job expectations, inflation. So they tend to focus more on essential items. The size of the basket is getting very important. Absolute price point. There’s channel shifting going on. There’s more promotions and some pack shifting too.”

18) From Wingstop: “I think you’ve heard a lot of others mention some weakening with the consumer demand to start third quarter and some industry signals have signaled some softness to the start, and I don’t think that’s any different for Wingstop. What we’ve referenced in some of our prior calls about seeing some softness in a few pockets over indexed to lower income or Hispanic consumers. I would say we really haven’t seen those pockets improve."

19) From Camping World: “On the new side, we were just slightly over $40,000 on a new ASP in 2024, and we’re operating today far below that, but we’ve already started to see that number tick up.” That means, "when margins remain constant, the amount of gross profit generated per transaction is just simply lower.”

20) From Old Dominion Freight: “Old Dominion’s second quarter financial results reflect continued softness in the domestic economy…Although the challenging economic environment has persisted for longer than we anticipated, we have remained focused on what we can control.”

21) From CH Robinson: "Although we're approaching the traditional retail peak season for ocean, the industry may not see traditional peak volumes as some retail customers are working through inventories and being highly selective and strategic about bringing in only the essential products they must import. We saw this dynamic with back-to-school ordering, and that trend is continuing as uncertainty about trade deals continues to shape customer behavior."

22) From Reynolds Consumer Products: They plan on taking price to make up for their higher costs. "So, as we said on the April call, we're expecting roughly 2 to 4 points of cost headwinds from commodities and tariffs through the year. That remains true. And similarly, as the guide contemplates full recovery of that, we're similarly anticipating 2 to 4 points of pricing."

23) From Ford: "We expect tariffs to be a net headwind of about $2 billion this year, and we'll continue to monitor the developments closely and engage with policymakers to ensure US auto workers and customers are not disadvantaged by policy change." That is a net number post their mitigation efforts.

24) From MGM Resorts: They referred to their Vegas business as "choppy." Remodeling and lower hold hurt MGM Grand "and to a much lesser degree, midweek performance at the Luxor and Excalibur" which caters to a lower income household compared to their other properties. "The lower midweek visitation in our more value oriented properties have continued in July, though we're taking advantage of this dynamic by pulling forward the MGM Grand room remodel timeline."

25) From Paypal: “the macro and consumer spending environment has been uneven. As we moved through the quarter, we observed a slight softening in retail spending in the US, most apparent in areas likely impacted by tariffs, such as Asia based marketplaces with higher exposure to goods sourced from China.”

26) From Proctor & Gamble: “What we are observing is that the consumer on both ends of the spectrum, the lower income consumer and the higher income consumer, they are reacting to the current volatility they are seeing and they are observing. And we see consumption trends consistently decelerating, not significantly, but we see a deceleration in the US. We see a deceleration in Europe and those are the biggest regions that have an immediate impact on the global category growth numbers. The volatility the consumer is seeing, I think is not necessarily grounded in their current reality, but more on what to expect for the future. So consumers are a bit more careful in terms of consumption. They are using up pantry inventory and they are looking for value either in smaller packs and promotions or in larger pack sizes in the club channel and online. That’s a behavior we’ve outlined before, but it’s not stopped. It’s continued.” And the cost of tariffs? “our outlook includes $1 billion before tax in higher costs from tariffs in fiscal ’26. This is based on tariff rates announced since July 9 and assumes USMCA exceptions…You can think about the tariff impacts in three buckets, about $200 million from materials and products imported from China to the US. Another $200 million from Canada’s tariffs on goods shipped from the US and the remaining $600 million from tariffs on goods coming to the US from the rest of the world.”

27) From Kering: “Overall, worldwide retail trends were similar in Q1 and Q2, but by region, notable changes occurred. The main feature was tourism spending, which clearly slowed down in Q2, impacted by currency moves and growing uncertainty depending on brands and regions."

28) From Whirlpool: “As expected, we navigated the challenging second quarter and continued to operate in an increasingly complex external environment. The macroeconomic uncertainty marked by elevated interest rates and evolving trade policies negatively impacted consumer sentiment. In particular, the weakness of consumer sentiment not only suppressed demand but also impacted itself as we continue to see consumers choosing to mix into lower end products. Furthermore, with the recent delays in tariff implementation, Asian competitors are not yet experiencing the full cost of tariffs and have continued to increase their imports ahead of our tariffs. In fact, we estimate that during the first half of this year, the amount of Asian appliance imports will approach the highest level on record. Needless to say that this pre-loading has created significant short term disruption, adding to the promotional intensity throughout the second quarter…it has become clear that they will extend well into the third quarter.”

29) From UPS: “Our second quarter financial results reflect the impact of a complex macro environment driven by ever evolving trade policies, as well as the significant actions we are taking to strengthen UPS’s competitive and financial positioning...Despite uncertainties around trade policies, in the second quarter the overall US economy demonstrated continued resilience. But our sector, specifically the US small package market, was unfavorably impacted by US consumer sentiment that was near historic lows. A recent research report from McKinsey showed that in the face of tariffs and other uncertainties, consumers are trading down, while at the same time splurging. For the first time in three years, consumer spending on discretionary categories like restaurants and automobiles outpaced growth in essential items.”

30) From Booking Holdings: "Inbound travel to the US was down y/o/y in the second quarter, particularly from bookers in Canada and to a lesser extent from bookers in Europe. That said, we also saw strong growth in other travel corridors, including Canada to Mexico and Europe to Asia, contributing to accelerating room night growth overall."

31) From Weyerhauser: "After a reasonably solid first quarter, housing starts have softened over the last few months, total starts averaging 1.3 million units on a seasonally adjusted basis in the second quarter. And single family starts below 1 million units. While the broader economy appears to be holding up reasonably well, the combination of weaker consumer confidence and elevated mortgage rates has been a headwind for housing activity. As a result, the spring building season was softer than we were expecting at the outset of the year, and I suspect we'll continue to see some choppiness in the housing market in the near term."

32) From Mohawk Industries: "A dominant trend across our geography is consumers' deferral of large discretionary purchases, which has reduced demand in our industry for almost three years. Geopolitical events, inflation, and low housing turnover are contributing to market uncertainty that is limiting residential remodeling and new construction. The commercial channel continues to outperform residential. However, the architectural billings index in the US is forecasting slowing conditions." In dealing with tariffs, "We have begun to address the implemented tariffs through price adjustments and supply chain optimization." By how much? They said 8% price increases are being implemented.

33) Overseas manufacturing PMIs: China 49.5 vs 50.4, Taiwan 46.2 vs 47.2, South Korea 48 vs 48.7, and Japan at 48.9.

34) BoJ Governor Ueda continues to drag his feet on raising interest rates in response to still high inflation and the clear displeasure with a higher cost of living on the part of the Japanese citizenry.

35) Germany's economy remained soft in Q2, contracting by one tenth q/o/q as expected.

36) Eurozone July CPI rose 2%, one tenth more than expected with a core rate up by 2.3% as forecasted. 2% is where the ECB currently has their deposit rate so REAL rates are zero.