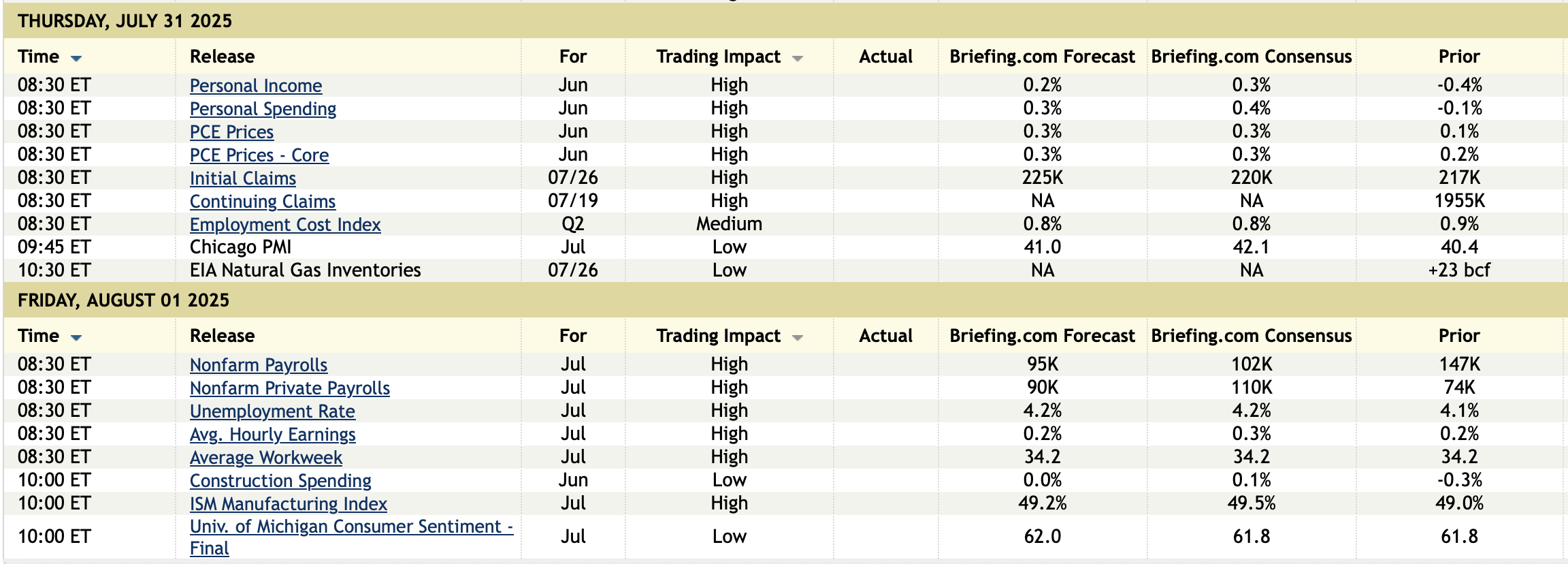

From Peter Boockvar:

Just when I thought Governor Ueda in Japan would get more hawkish in light of the upper house election results where the Prime Minister lost his support due to a voter pushback against inflation, he wasn't. While keeping rates unchanged at just .50% as expected he said "Right now I don't see us being behind the curve. Neither do I think there's a high risk we'll fall behind." He seems to be most concerned about the global trade war and "We don't see the fog suddenly lifting" though he did acknowledge that some trade uncertainty has receded.

He certainly didn't rule out more rate hikes and we're still likely to get some more. "If the economy and prices move in line with our forecast, we expect to continue raising interest rates and adjust the degree of monetary support in accordance to improvements in economic and price developments...It's not as if we will wait until underlying inflation is firmly at 2%. Our decision is dependent on how likely underlying inflation will reach that level." The BoJ is somehow defining an 'underlying inflation' metric that according to them is still below 2% even though all metrics the rest of us see are above 3%.

Here is his main reasoning for not raising rates now, "Tightening monetary policy to deal with too-high inflation works nicely when inflation is driven by strong demand. You can cool over-heated demand and moderate price pressure. But what's happening in Japan now is price rises driven by supply factors. When you try to deal with such price pressure with monetary tightening, it would hurt the economy, reduce households' income and weigh on consumption. I'm not sure that's what people would desire."

The 2 yr yield sensitive to the overnight rate was unchanged in response as were rates across their yield curve. The yen though is weaker while the Nikkei rallied 1%.

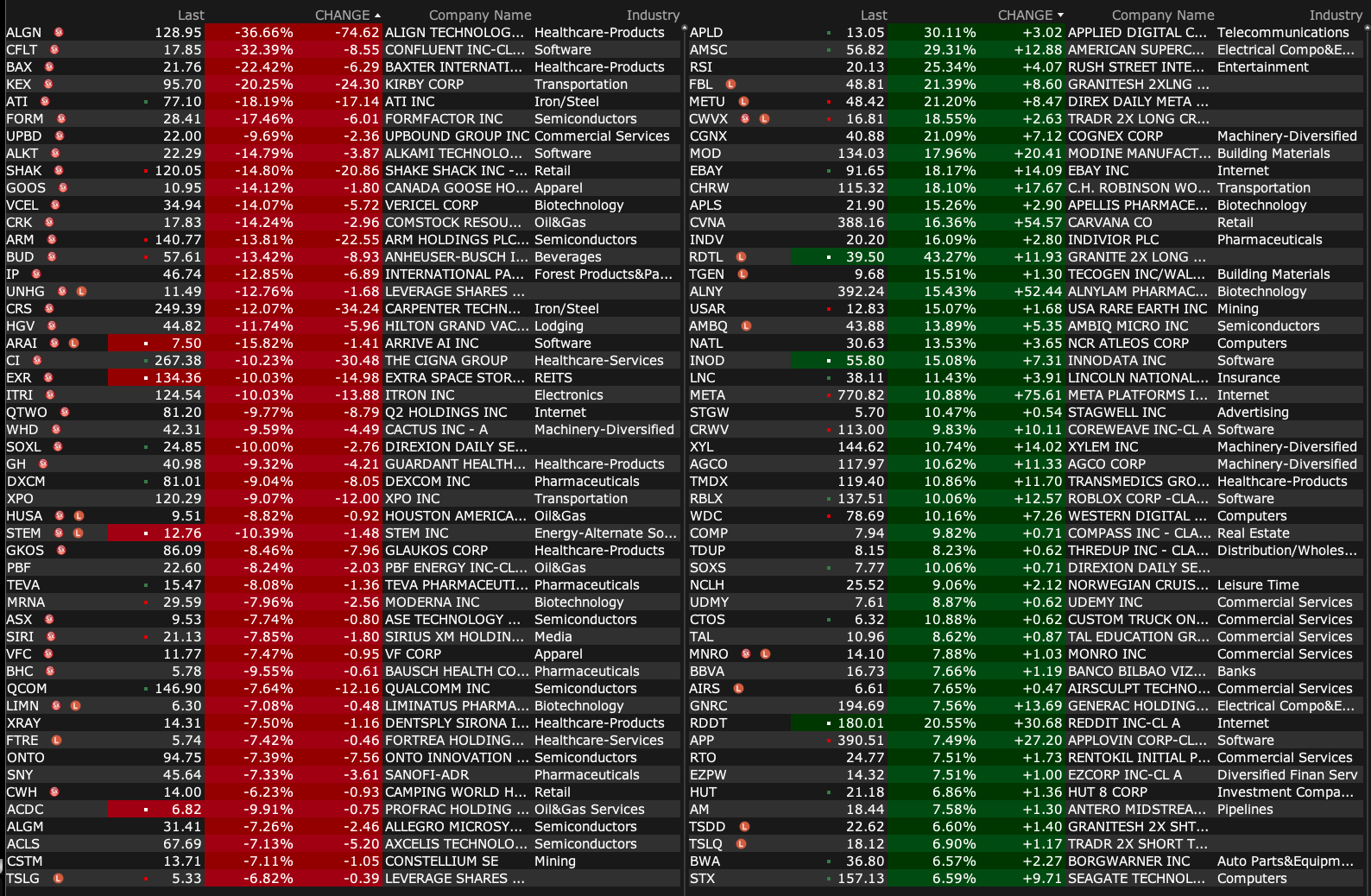

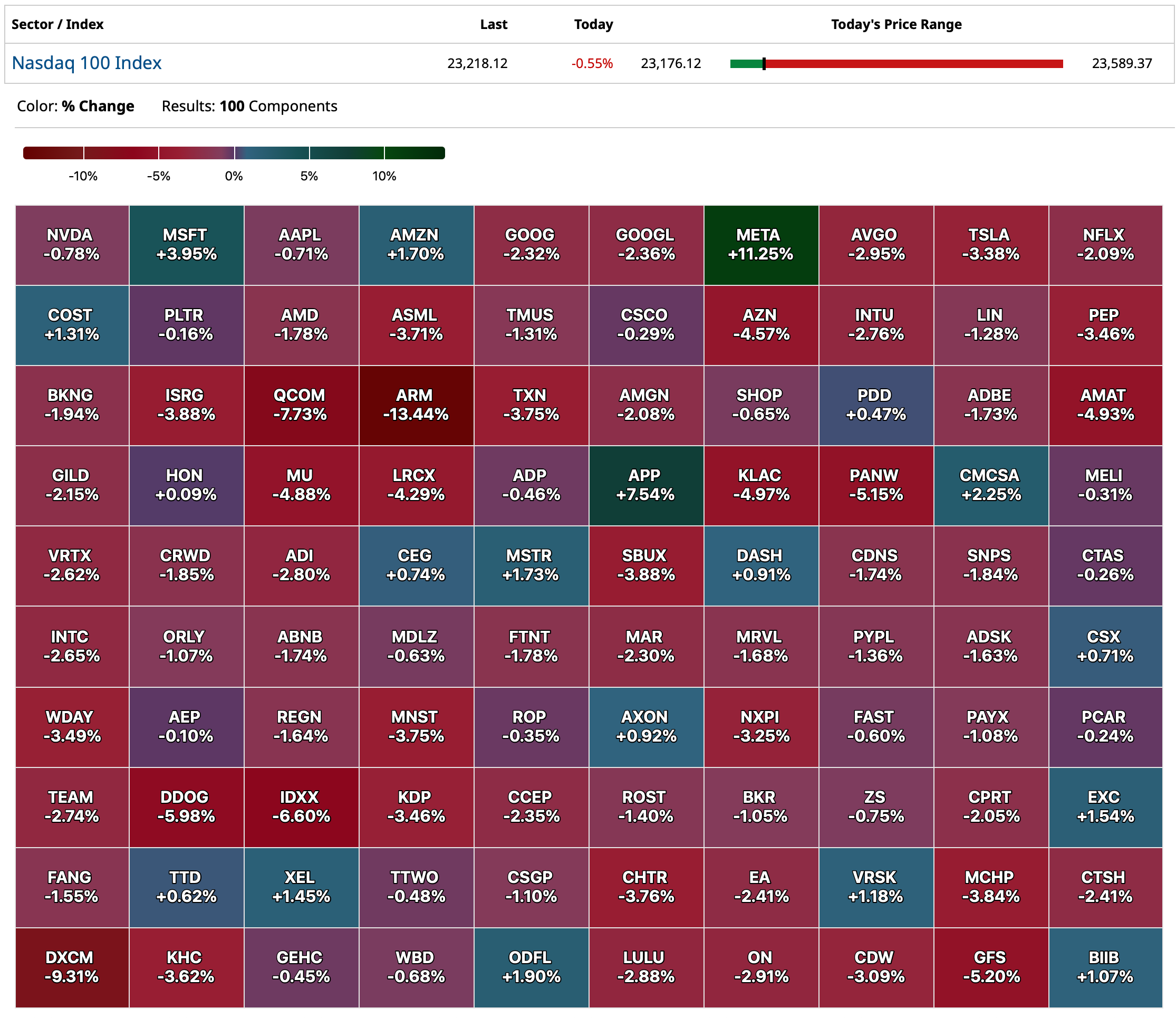

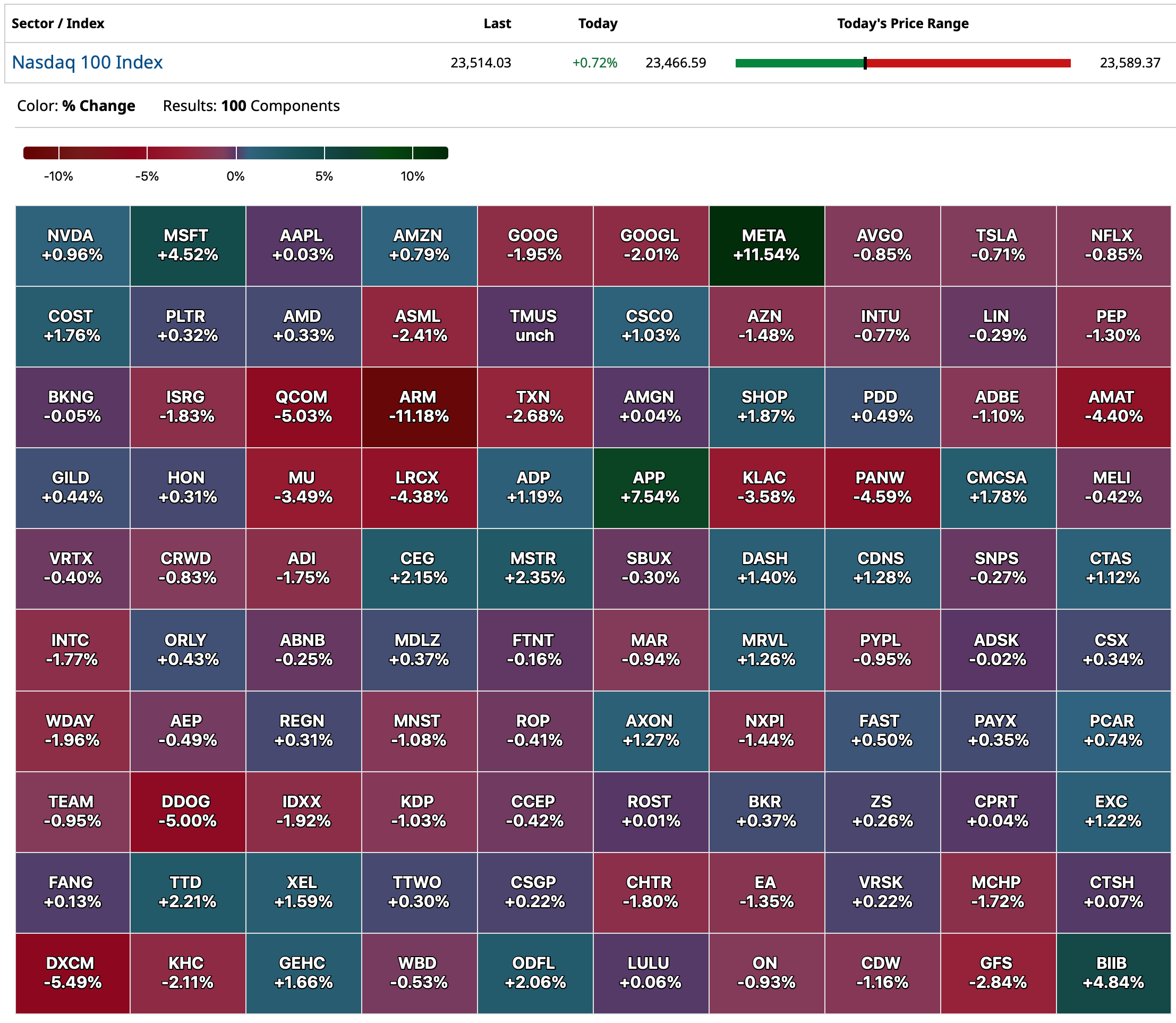

The results from Meta and Microsoft were just incredible and astonishing to see still solid earnings growth for companies as big as them. And, their CapEx numbers continue to be quite a sight too and this GenAI build out remains a major economic growth driver, as we know.

From Microsoft, and whose revenue grew by 18% y/o/y and by 17% in constant currency:

"All up, Microsoft Cloud surpassed $168 billion in annual revenue, up 23%. The rate of innovation and the speed of diffusion is unlike anything we've seen. To that end, we are building the most comprehensive suite of AI products and tech stack at massive scale."

Azure revenue growth was 34%, "driven by growth across all workloads."

"Our family of Copilot apps has surpassed 100 million monthly active users across commercial and consumer. And when you take a broader look at the engagement of AI features across our products, we have over 800 million monthly active users...Customers continue to adopt Copilot at a faster rate than any other new Microsoft 365 suite, with strong usage intensity as shown by our w/o/w retention. And we saw the largest quarter of seat add since launch, with a record number of customers returning to buy more seats."

One snippet of note on LinkedIn, "revenue increased 9% and 8% in constant currency with growth across all businesses, though talent solutions continues to be impacted by weakness in the hiring market."

Their Q1 guidance for CapEx is $30b. Annualize that and it's an unbelievable 38% of their expected fiscal '26 revenue of about $318b. It was 13% in their 6/23 fiscal yr ended and 18% in 6/24 fiscal yr.

From Meta and whose revenue growth was 22% y/o/y in the quarter:

With context that there are about 8 million people in the world, "We had another strong quarter, with more than 3.4 billion people using at least one of our apps each day and strong engagement across the board."

"On advertising, the strong performance this quarter is largely thanks to AI unlocking greater efficiency and gains across our ad system."

"Capital expenditures, including principal payments on finance leases, were $17 billion, driven by investments in servers, data centers and network infrastructure." On the full year outlook, they expect CapEx "to be in the range of $66 billion to $72 billion, narrowed from our prior outlook of $64 billion to $72 billion, and up approximately $30 billion y/o/y at the midpoint...as we continue aggressively pursuing opportunities to bring additional capacity online to meet the needs of our AI efforts and business operations."

For perspective, that CapEx guide is 36% of expected revenue this year. In 2023, it was 20%.

From Hershey:

“Consumption was strong across our top chocolate franchises, with Reese growth of 4%, Hershey up nearly 8% and Kit Kat up 3% in the quarter, behind our summer limited edition programs and media campaigns…Our portfolio led in share gains among the top ten Salty Snack manufacturers this quarter as our brands continue to resonate with consumers for permissible and better for you brands.”

While cocoa prices are up sharply, they seemed to have done a nice job with their hedging program, locking in 2025 prices “well below the market.”

“This month Hershey announced a new price action on the entirety of our U.S. confection portfolio. These products represent roughly 80% of total net sales and through a combination of list price and price pack architecture, we will deliver an estimated 16 points of pricing contribution to the overall Company… This pricing announcement reinforces our commitment to covering commodity inflation with pricing over time.”

“Regarding tariffs, the global business environment remains dynamic as trade negotiations continue. For the full year, we are now modeling tariff expense in the range of $170 million to $180 million, below our prior expectations, due to inventory on hand, fluctuations in country specific rates, and sourcing optimization. Given the unique circumstances surrounding cocoa, which cannot be grown in the United States, we remain hopeful that tariffs on our largest exposure will improve as trade negotiations continue, though this will likely take time. We are not planning for relief in 2025 and have fully embedded these incremental costs in our full year outlook.”

“relative to GLP-1s, we continue to see no material impact in ’25. Certainly we are always monitoring very closely, but at this point, we’re not expecting it to be significant in ’26. We broadly look at the consumer trend as it relates to health and wellness.”

From Mondelez:

“If I go a little bit around the world, maybe starting in Europe, a good quarter in Europe with good numbers, strong share gains. Clearly the business is very resilient. The consumer is more confident in Europe, still quite fragile and frugal spending, but snacking continues to outpace food. And overall, I would say we feel pretty good about our European business. Consumers are not exactly bullish, and they’re focused on essentials, but they keep buying our category even despite the significant price increases that we had to do in chocolate.”

“If I go to the US, a little bit more of a difficult situation there. There’s a lot of consumer anxiety. They look at quite an uncertain outlook as it relates to their personal finances, job expectations, inflation. So they tend to focus more on essential items. The size of the basket is getting very important. Absolute price point. There’s channel shifting going on. There’s more promotions and some pack shifting too.”

“Switching to the emerging markets, we feel very good. Double digit growth.” But, with some mixed markets.

From Wingstop and whose stock ripped higher by 27% as they plan to increase store count a bit quicker than the street expected even though comps fell by 1.9% y/o/y:

They expect full year comps up 1%.

“I think you’ve heard a lot of others mention some weakening with the consumer demand to start third quarter and some industry signals have signaled some softness to the start, and I don’t think that’s any different for Wingstop. What we’ve referenced in some of our prior calls about seeing some softness in a few pockets over indexed to lower income or Hispanic consumers. I would say we really haven’t seen those pockets improve.

From Camping World and whose stock fell 15% yesterday on weaker than expected RV average selling prices:

“When the quarter started, it was obviously a nerve racking situation for all of us. Liberation Day had started. Tariffs had set in. The general market was in a freefall and a volatile situation. And people were obviously concerned about what was going to happen to a discretionary item like RVs. I’m proud to tell you that our 12,000 team members purely simply delivered for the quarter.”

“We set a record selling more RVs than we ever have in an entire quarter, 45,000 units. We set a record in our finance and insurance department, highest amount of revenue we’ve ever generated, $200 million. And we set a revenue record for Good Sam.”

“On the new side, we were just slightly over $40,000 on a new ASP in 2024, and we’re operating today far below that, but we’ve already started to see that number tick up.” That means, "when margins remain constant, the amount of gross profit generated per transaction is just simply lower.”

From Avis Budget and whose stock fell 15% yesterday because of mixed guidance:

“So, kind of what we’re seeing in terms of RPD (revenue per day) isn’t all that different from what other participants in the travel industry are seeing. I think demand is firming up post the passage of the Big Beautiful Bill. For us, leisure is stronger than commercial right now. And pricing is more challenged than volume…But we do think that there are signs that things are firming up for the summer and I think summer is off to a good start.”

From Old Dominion Freight and whose stock fell 10% yesterday as revenue fell 6% y/o/y:

“Old Dominion’s second quarter financial results reflect continued softness in the domestic economy…Although the challenging economic environment has persisted for longer than we anticipated, we have remained focused on what we can control.”

From CH Robinson, the freight/logistics broker:

"From a macro standpoint, fluid trade policies continue to create uncertainty, making planning activities more difficult for our over 83,000 customers around the world. For some of them, tariffs caused them to reduce their import volumes. For instance, when US tariffs on Chinese goods increased to 145% in April, numerous retailers limited imports to only essentials needed for fall, like back-to-school products. Others accelerated shipments to beat tariff deadlines from Southeast Asia, and some stuck to their standard peak season schedules, taking a more wait and see approach."

"Although we're approaching the traditional retail peak season for ocean, the industry may not see traditional peak volumes as some retail customers are working through inventories and being highly selective and strategic about bringing in only the essential products they must import. We saw this dynamic with back-to-school ordering, and that trend is continuing as uncertainty about trade deals continues to shape customer behavior."

From Illinois Tool Works, it fell 2% yesterday:

Revenue rose 1% y/o/y helped by FX. “Geographically, while North America posted a 2% organic revenue decline and Europe was down 3%, Asia Pacific stood out with a 9% increase, with impressive growth of 15% in China.”

“We experienced encouraging sequential revenue growth of 6% from Q1, along with some positive signs in end markets such as semiconductors, electronics, welding, specialty products, equipment and an improved outlook for auto builds. On the other hand, more consumer oriented end markets, notably construction products, remained challenging.”

“Although our decisive pricing actions more than cover tariff costs and positively impacted EPS in Q2, the overall price-cost dynamic was modestly dilutive to our margin.”

Specifically with their auto business, “Worldwide order builds are now projected to be about flat, with North America builds down mid single digits and Europe down low single digits, partially offset by mid single digit growth in China builds. Overall, our relevant markets are expected to be down in the low single digits in 2025, which is an improvement from the down mid single digit production in our prior guide.”

From Reynolds Consumer Products, the maker of Reynolds wrap and Hefty trash bags and a stock we own:

They plan on taking price to make up for their higher costs. So, as we said on the April call, we're expecting roughly 2 to 4 points of cost headwinds from commodities and tariffs through the year. That remains true. And similarly, as the guide contemplates full recovery of that, we're similarly anticipating 2 to 4 points of pricing."

From Ford:

"We expect tariffs to be a net headwind of about $2 billion this year, and we'll continue to monitor the developments closely and engage with policymakers to ensure US auto workers and customers are not disadvantaged by policy change." That is a net number post their mitigation efforts.

From EBAY, and whose stock is up sharply pre-market:

Gross merchandise volume rose 4% y/o/y, "accelerating by over 2 points sequentially. Revenue grew by more than 4%."

"our marketplace has proven resilient to recent uncertainty brought on by tariffs and trade policy changes."

"Collectibles was once again the largest contributor to growth as y/o/y growth in trading cards GMV accelerated for the 10th straight quarter on the back of continued momentum in both collectible card games and sports trading cards. Interest in Pokemon cards has surged recently, with GMV growth in the triple digits for the second straight quarter amid renewed interest from collectors and a particularly strong slate of product releases."

From MGM Resorts:

They referred to their Vegas business as "choppy" while they saw record results in Macau. Of note too, "We are also benefiting from the continued momentum of our domestic regional operations. Their stability is highly valued during times of volatility and we achieved our best second quarter results in both net revenue and slot win."

More on Vegas, "During the second quarter and now into July, performance on the weekends has been solid as we've been operating near capacity in our hotels across the spectrum. Our luxury offerings in Vegas maintained rate integrity with slot and table volume increasing about 4% and several properties reporting second quarter records for net revenue."

Remodeling and lower hold hurt MGM Grand "and to a much lesser degree, midweek performance at the Luxor and Excalibur" which caters to a lower income household compared to their other properties. "The lower midweek visitation in our more value oriented properties have continued in July, though we're taking advantage of this dynamic by pulling forward the MGM Grand room remodel timeline."

They still see "solid bookings of groups and conventions that are in place for later in the year."

China's July state sector focused manufacturing PMI slipped to 49.3 from 49.7 where no change was expected. The non-manufacturing side also fell to 50.1 from 50.5. The estimate was 50.2. All around the flat line in the aggregate.

French and Italian July CPI were each one tenth above expectations but benign at up .9% for the former y/o/y and by 1.7% for the latter. German CPI today is expected to be up 1.9% y/o/y.

German also said that unemployment in July rose by 2k people, below the estimate of up 15k as their economy tries to be putting in a bottom, helped by a lot of fiscal spend.