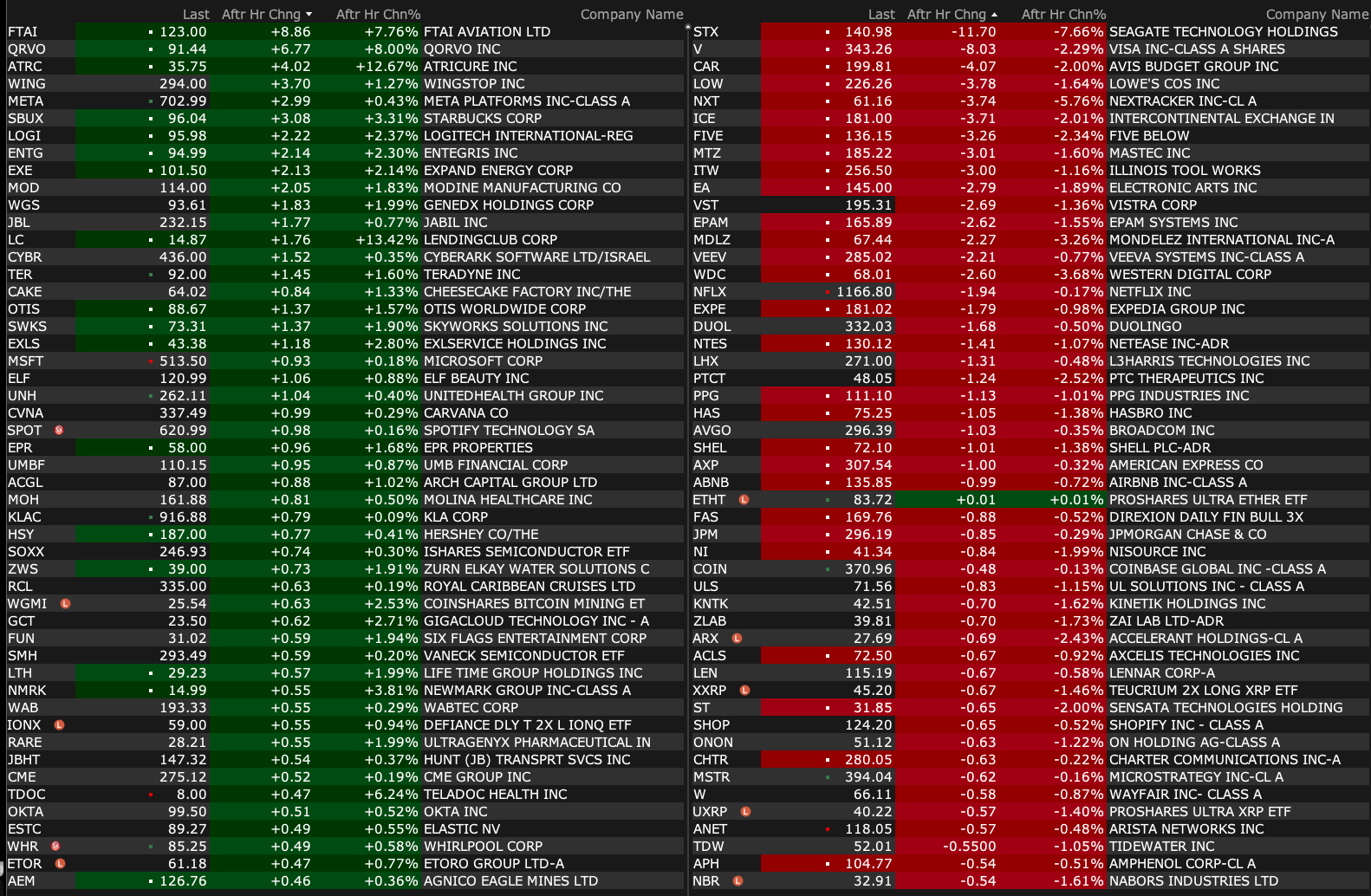

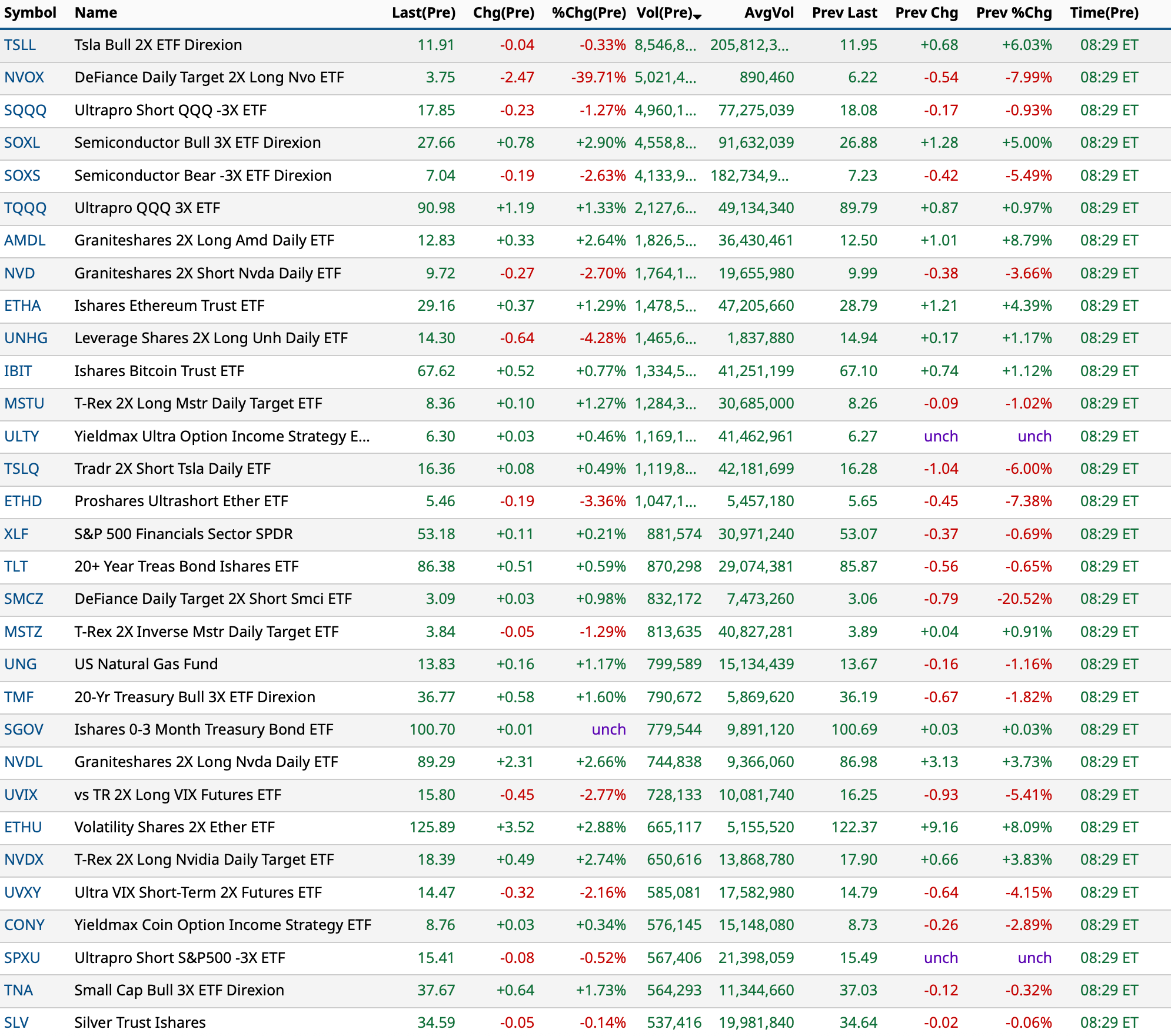

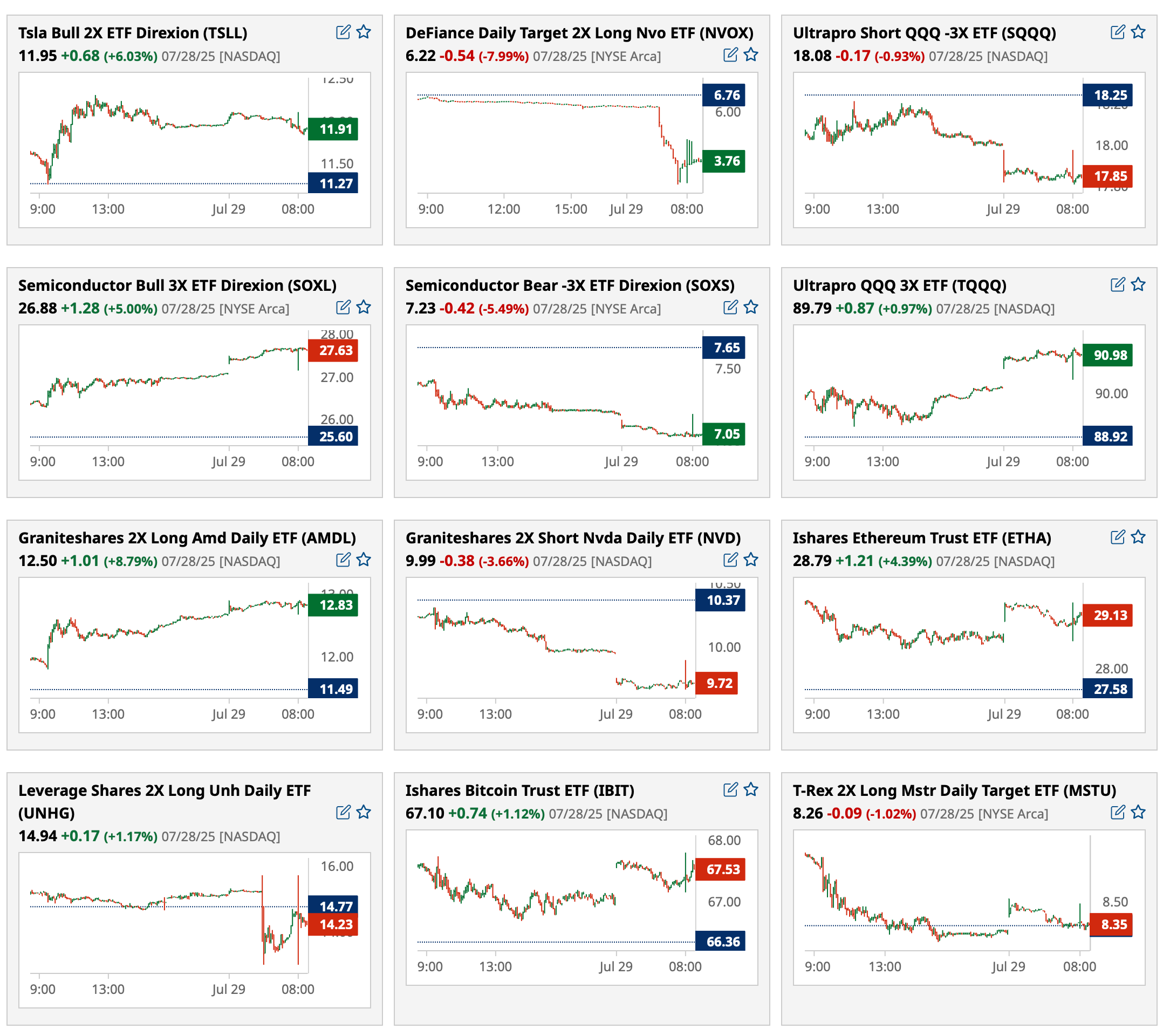

Tuesday's After-Hours Movers

As of 4:21 p.m.:

BY Doug Kass · Jul 29, 2025, 4:55 PM EDT

As of 4:21 p.m.:

BY Doug Kass · Jul 29, 2025, 4:55 PM EDT

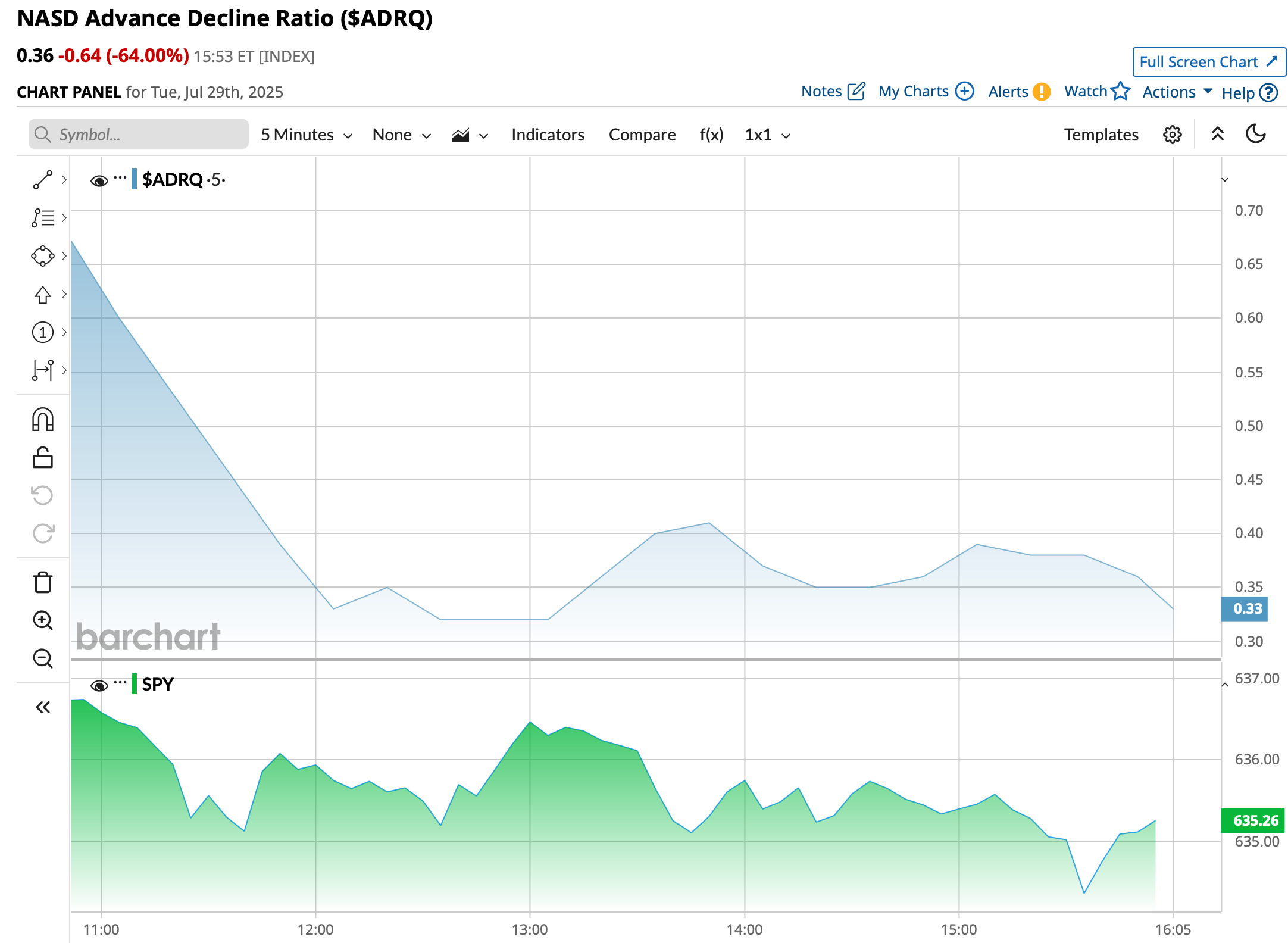

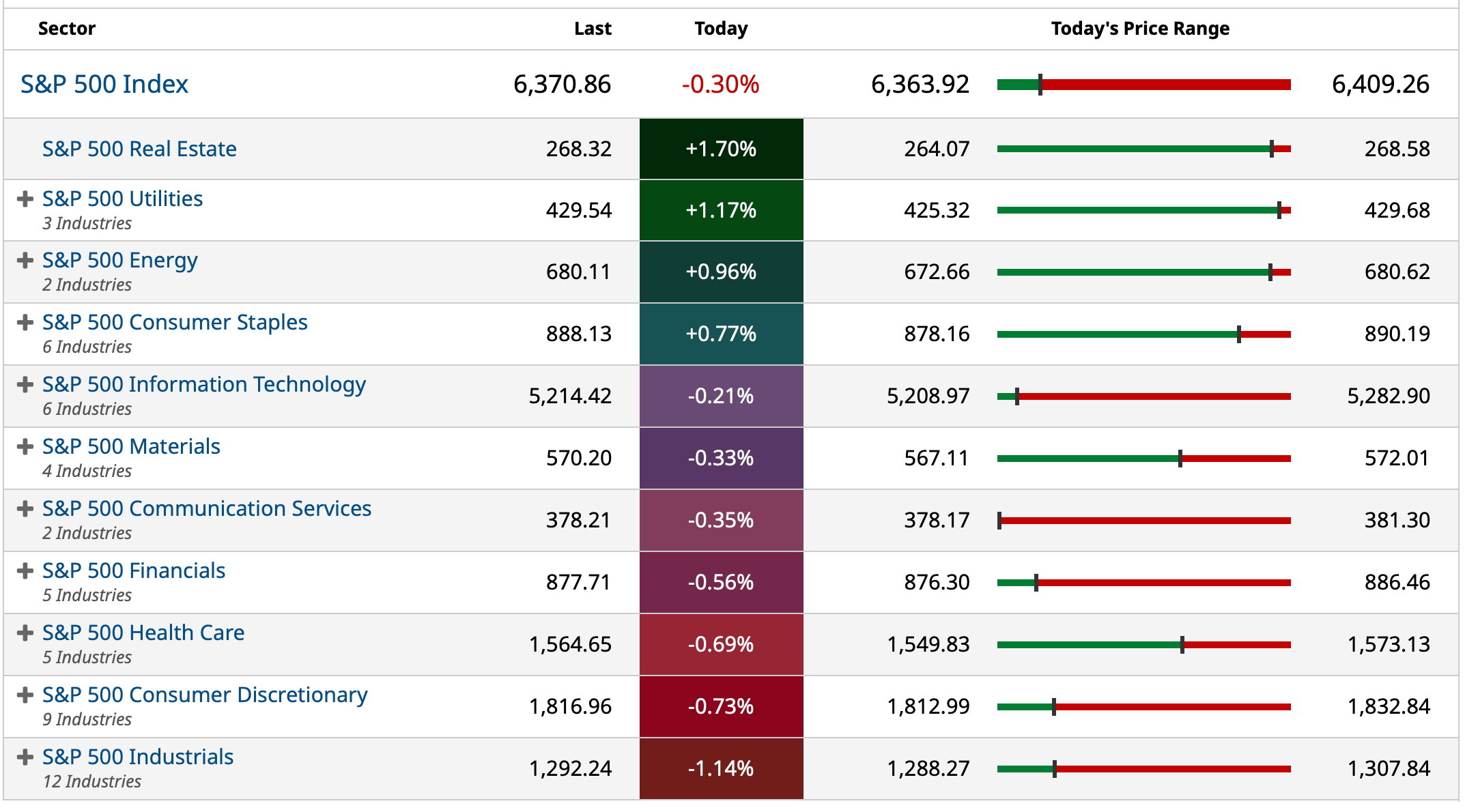

Through 4 p.m.:

BY Doug Kass · Jul 29, 2025, 4:45 PM EDT

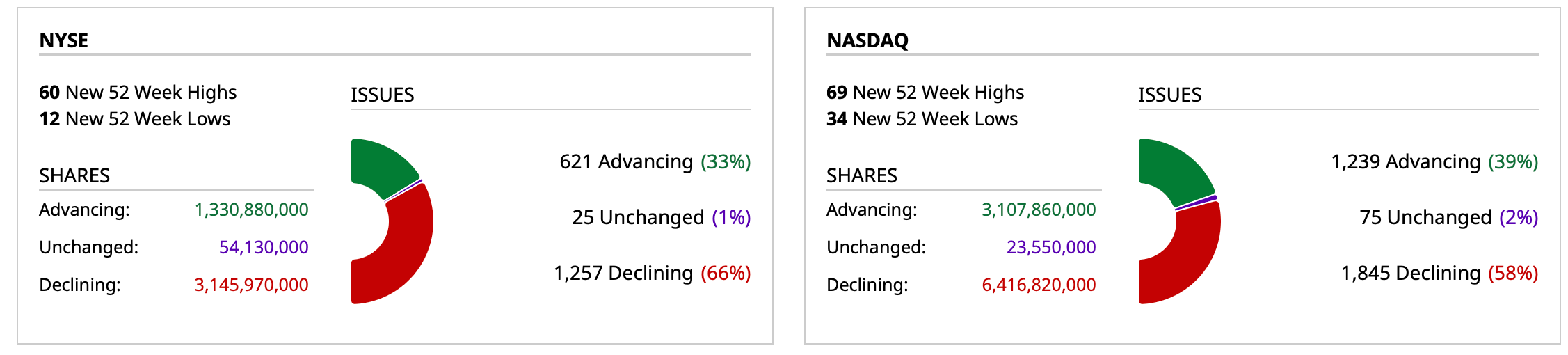

- NYSE volume 6% below its one-month average;

- NASDAQ volume 6% above its one-month average;

- VIX index: up 6.32% to 15.98

BY Doug Kass · Jul 29, 2025, 4:40 PM EDT

Randy

Trump gets tariffs; Americans get price hikes

BY Doug Kass · Jul 29, 2025, 3:56 PM EDT

* As the market accentuates the positives...

BY Doug Kass · Jul 29, 2025, 3:39 PM EDT

BY Doug Kass · Jul 29, 2025, 3:25 PM EDT

The portion of the EU deal where constituent governments would buy U.S. energy was a bunch of BS.

It is the private sector that purchases energy and the respective EU governments can not mandate the private sector to make such purchases.

When asked about this Secretary of the Treasury Bessent hemmed and hawed — stating it would be fine with President Trump if he continued to get high tariffs contributed into the U.S. Treasury.

May of the country tariff agreements are BS and have not been formalized.

But we are in a momentum-based global equity markets where facts are secondary.

BY Doug Kass · Jul 29, 2025, 3:15 PM EDT

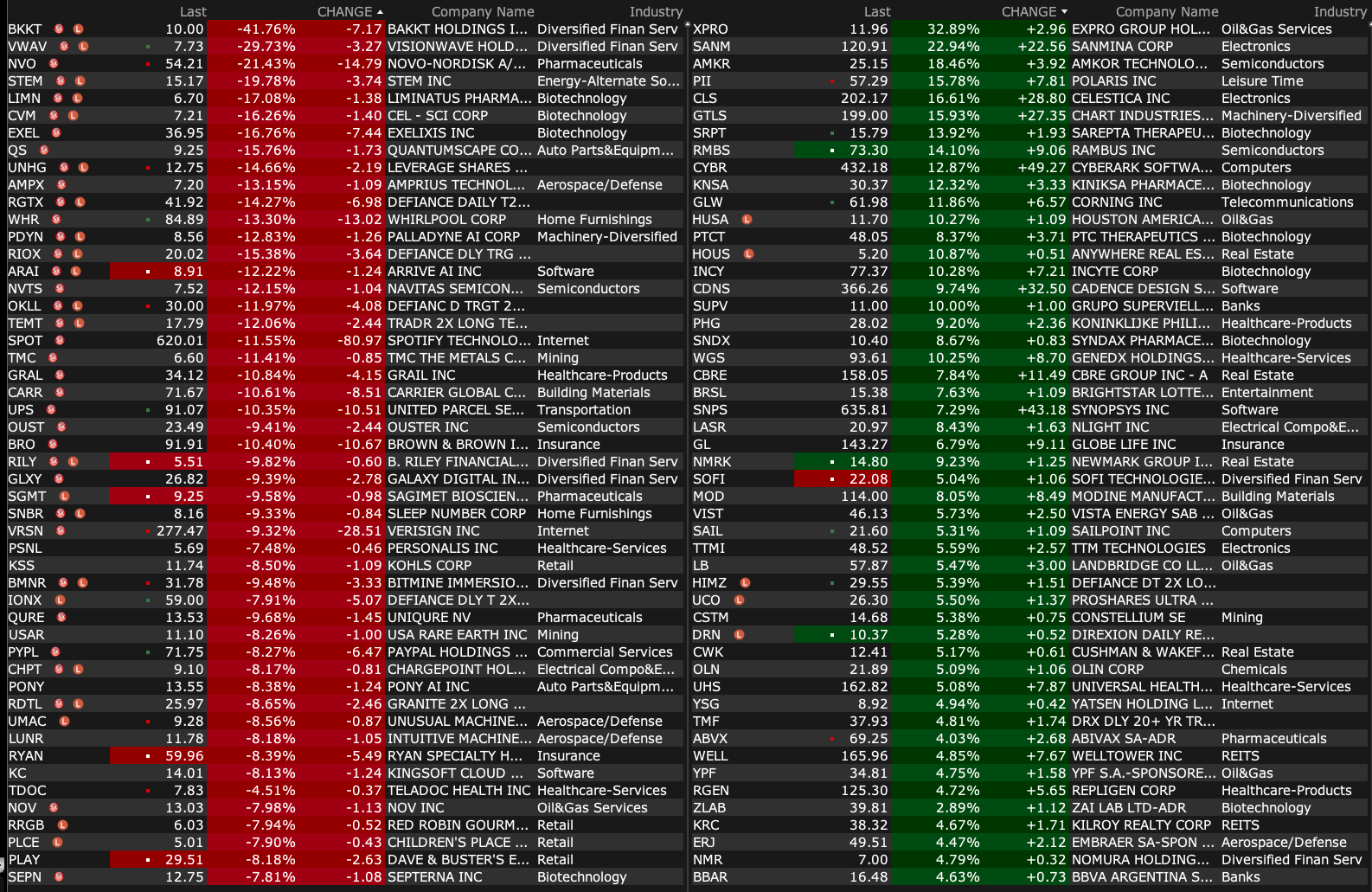

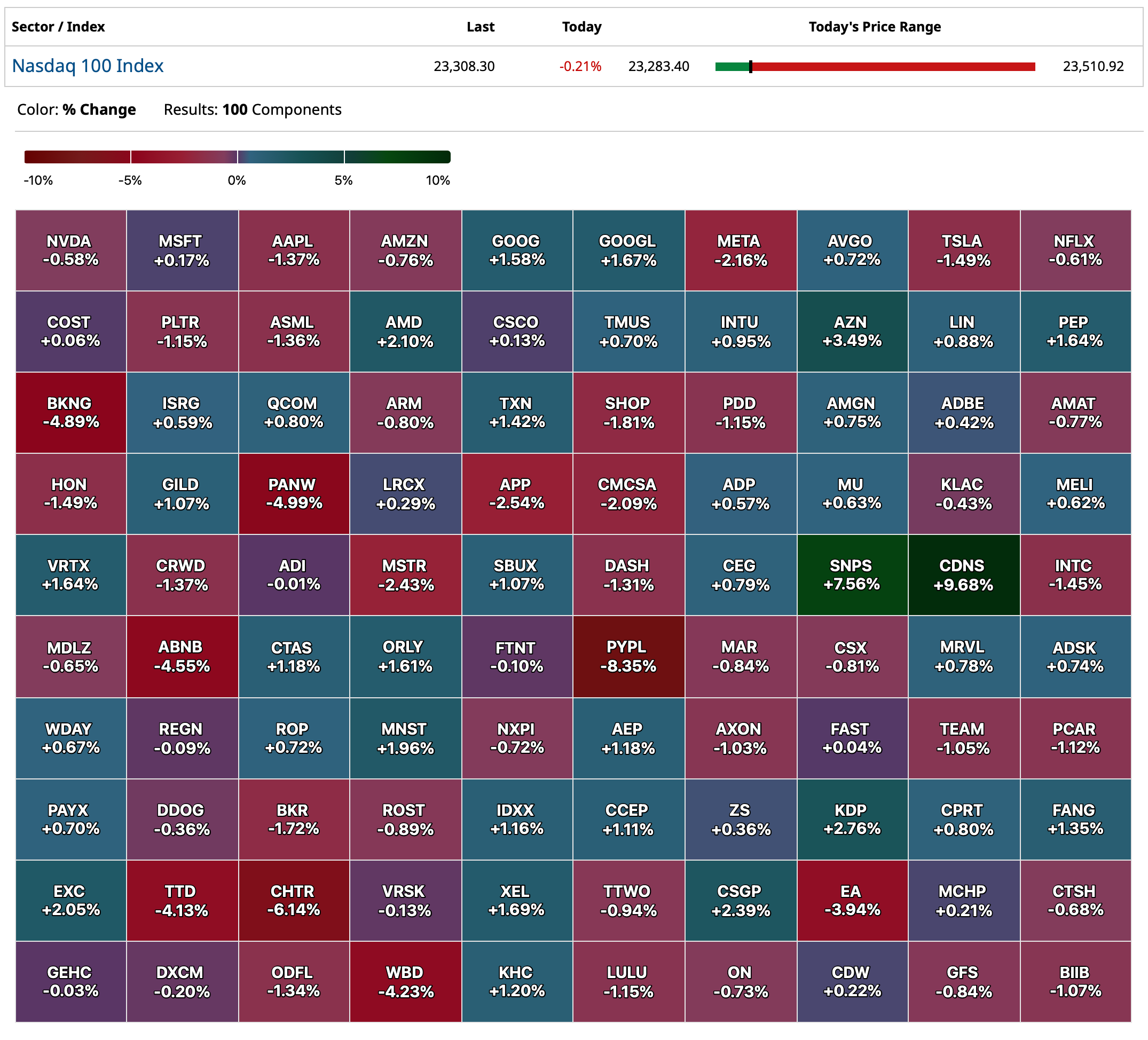

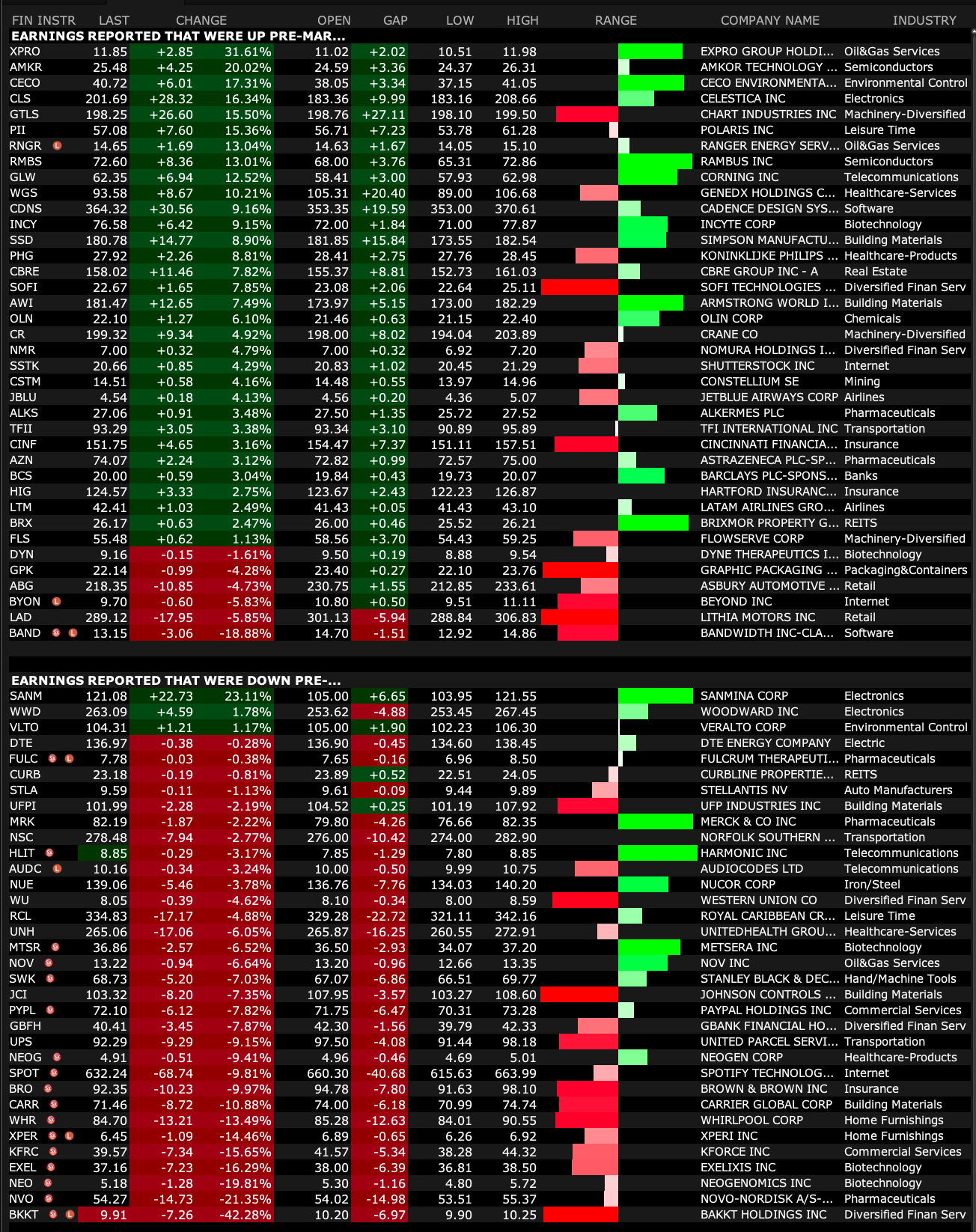

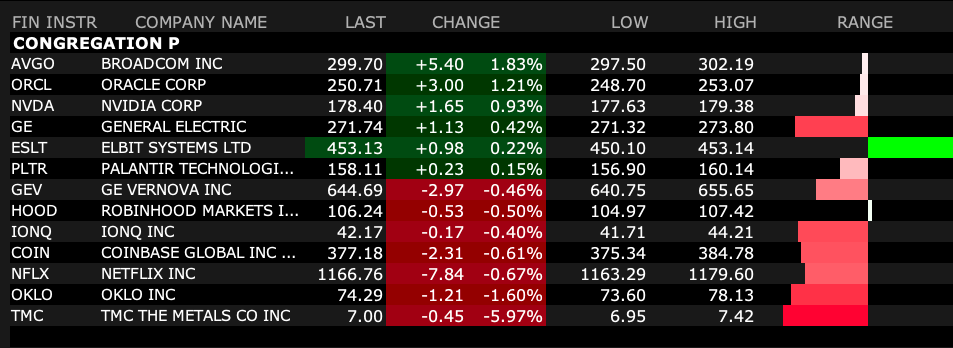

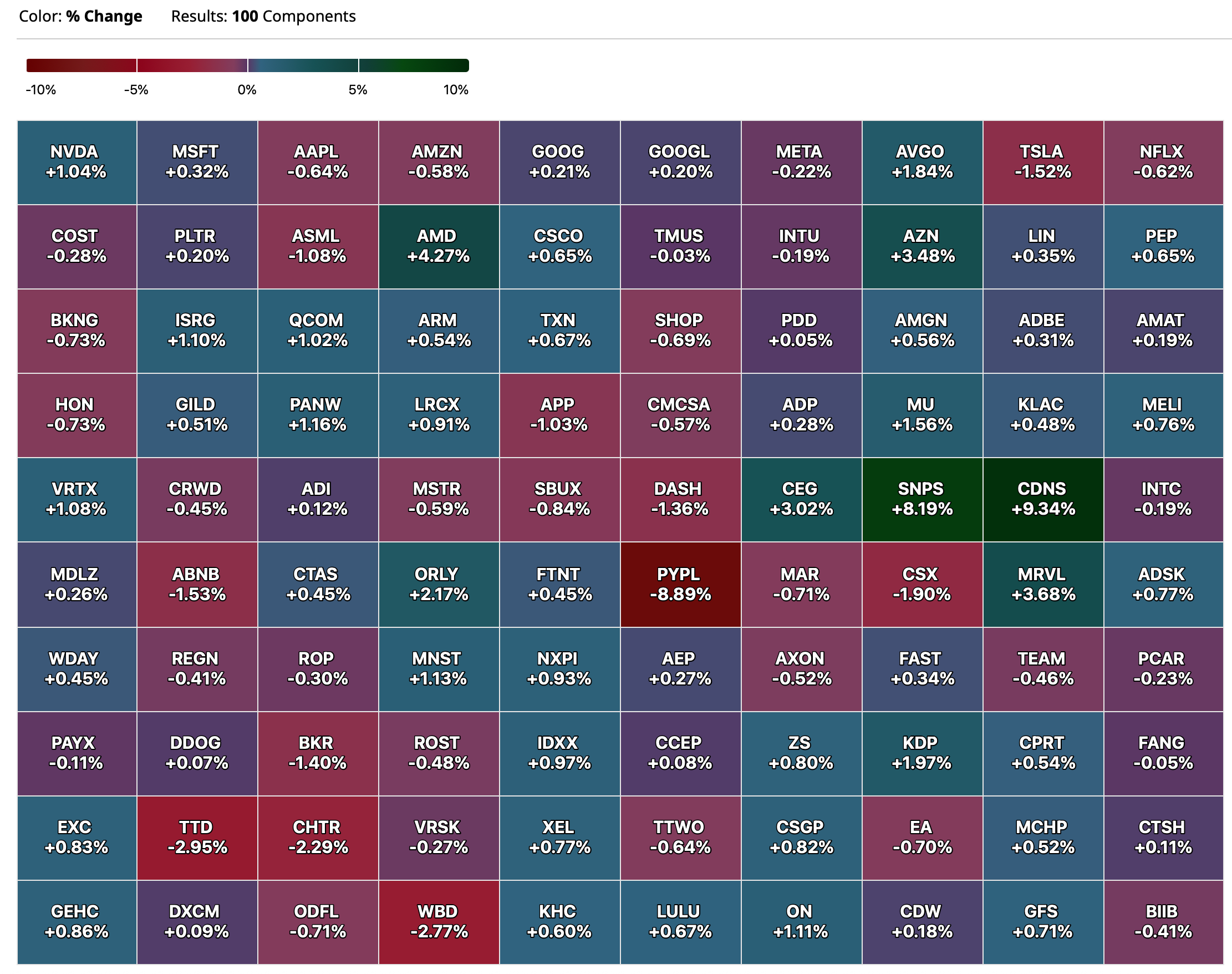

Earnings stocks grouped by those that were up/down pre-open Tuesday July 29:

BY Doug Kass · Jul 29, 2025, 3:09 PM EDT

BY Doug Kass · Jul 29, 2025, 3:00 PM EDT

Wolf Street on labor turnover.

BY Doug Kass · Jul 29, 2025, 2:40 PM EDT

BY Doug Kass · Jul 29, 2025, 2:30 PM EDT

With S&P cash -5 handles I am shorting more index calls.

BY Doug Kass · Jul 29, 2025, 1:14 PM EDT

I have a research call at 12:45 PM.

Radio silence for an hour or so.

BY Doug Kass · Jul 29, 2025, 12:50 PM EDT

My pals, Dan and Guy on MRKT CALL —with some nice references to Rosie and myself!

Let's go to the tape:

BY Doug Kass · Jul 29, 2025, 11:55 AM EDT

* Upbeat Consensus Profits Expectations Are Unrealistic 2025-26 S&P EPS expectations are too high (WHR, UPS, SWK, etc.). In particular, the second half of this year is likely to result in year over year disappointments given the deceleration of domestic economic growth and the uncertainties of rising costs and higher tariffs.

* Too Much "First Level Thinking" and Not Enough "Second Level Thinking" Increasingly, solid company EPS reports (BA, NFLX, etc.) have already been discounted by the markets.

BY Doug Kass · Jul 29, 2025, 11:45 AM EDT

From Peter Boockvar:

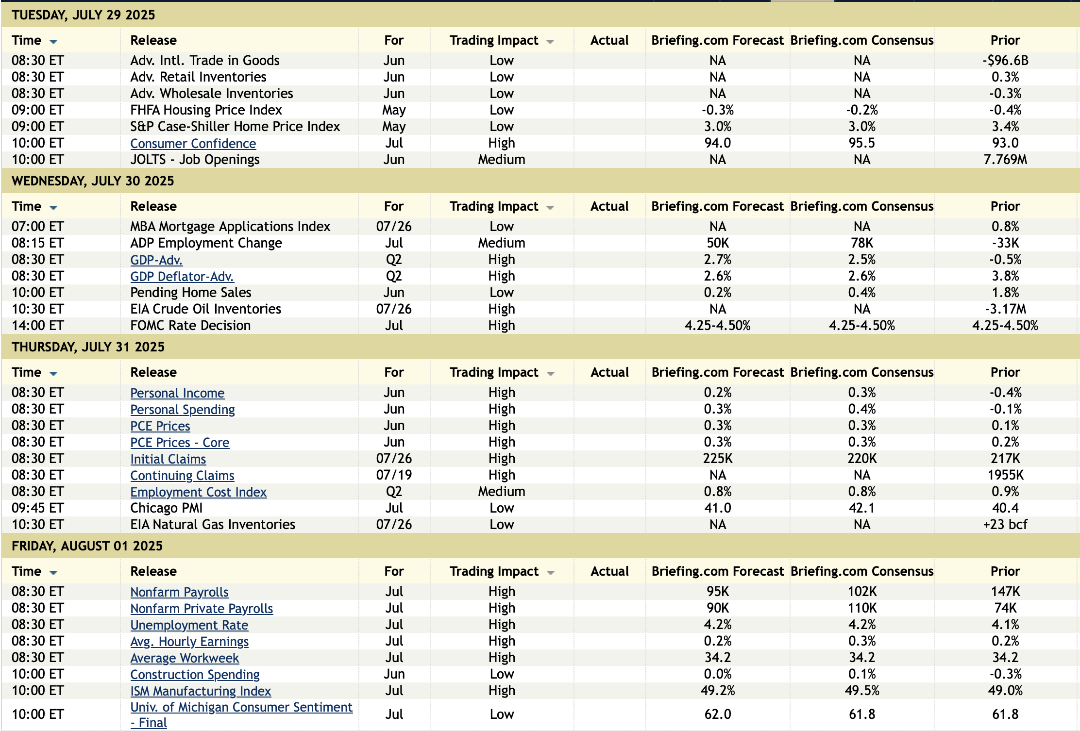

Quick rundown on goods deficit, inventories, home prices, job openings and consumer confidence

Moving closer away from the massive trade front running distortions around on and off tariffs in April and May, the exports of goods fell .6% m/o/m in June while imports were down by 4.2%. It will be key to watch imports from here as they’ve now gotten more expensive and after going through countless conference calls, US business is eating a lot of them and trying to pass on what they can while also pushing back on exporters to us where they can as well. The overall deficit of $86b was about $10b less than expected and vs $96b in May.

With June wholesale inventories rising .2% m/o/m vs the estimate of down one tenth, more inventory building seems to be taking place in response to trade uncertainties.

As seen with the existing home sales data last week, the pace of home price increases as measured by the S&P CoreLogic report continues to moderate. They rose 2.25% y/o/y in May for their home price index, though still up about 50% over the last 5 years. In order to unfreeze the housing market, home prices must stop going up for now and at least in some markets they need to go down in order to encourage more transactions.

I’ll argue again that those who think lower interest rates are the magic elixir for the housing market seem to have forgotten the lessons of the last 20 years of boom and busts in the industry. All lower mortgage rates do is stimulate demand and unless we get more housing supply to meet that demand, the benefit of lower financing rates is offset by having to pay a higher price for the home. We need BOTH lower mortgage rates and more home supply at the same time in order to unlock activity.

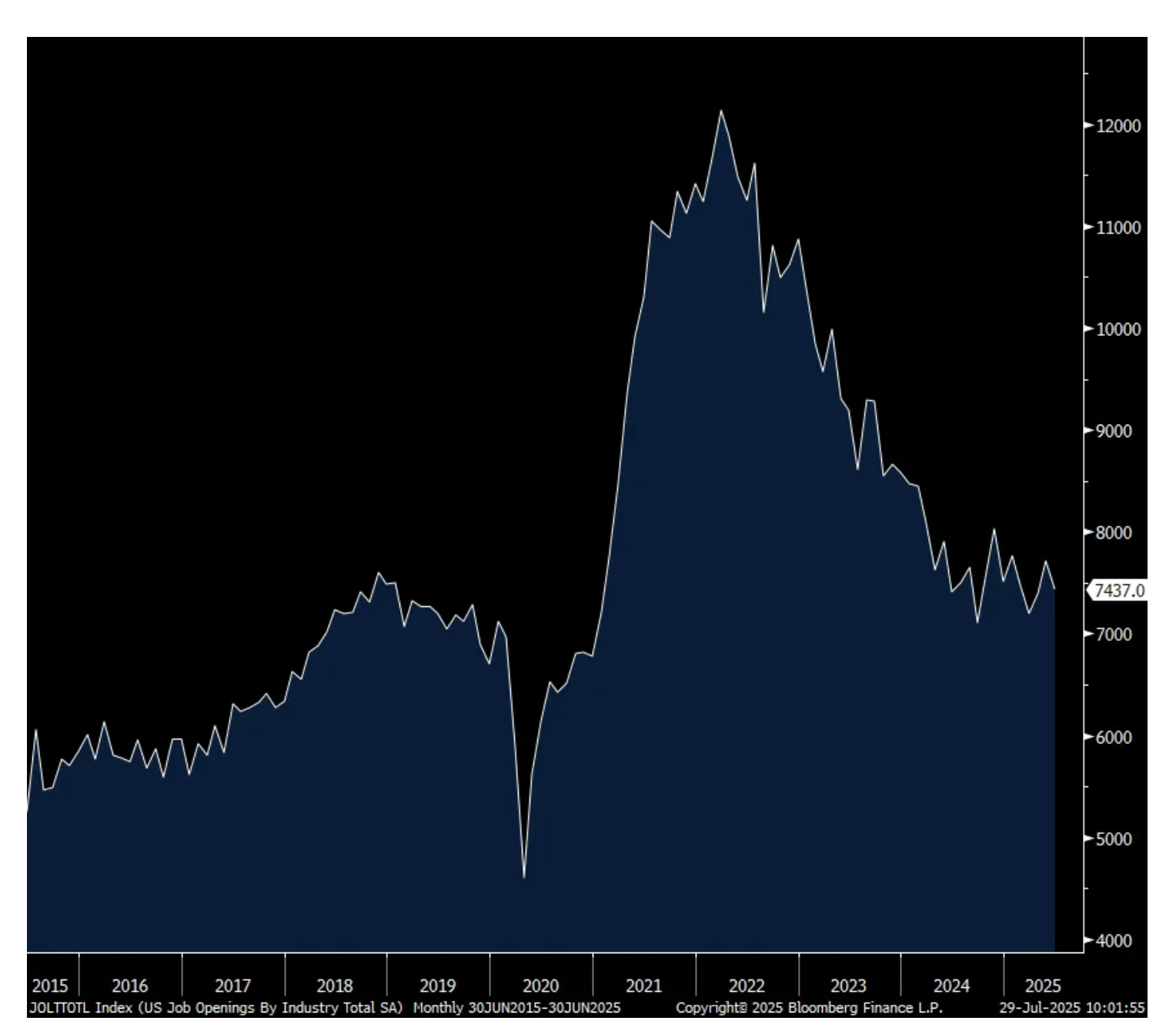

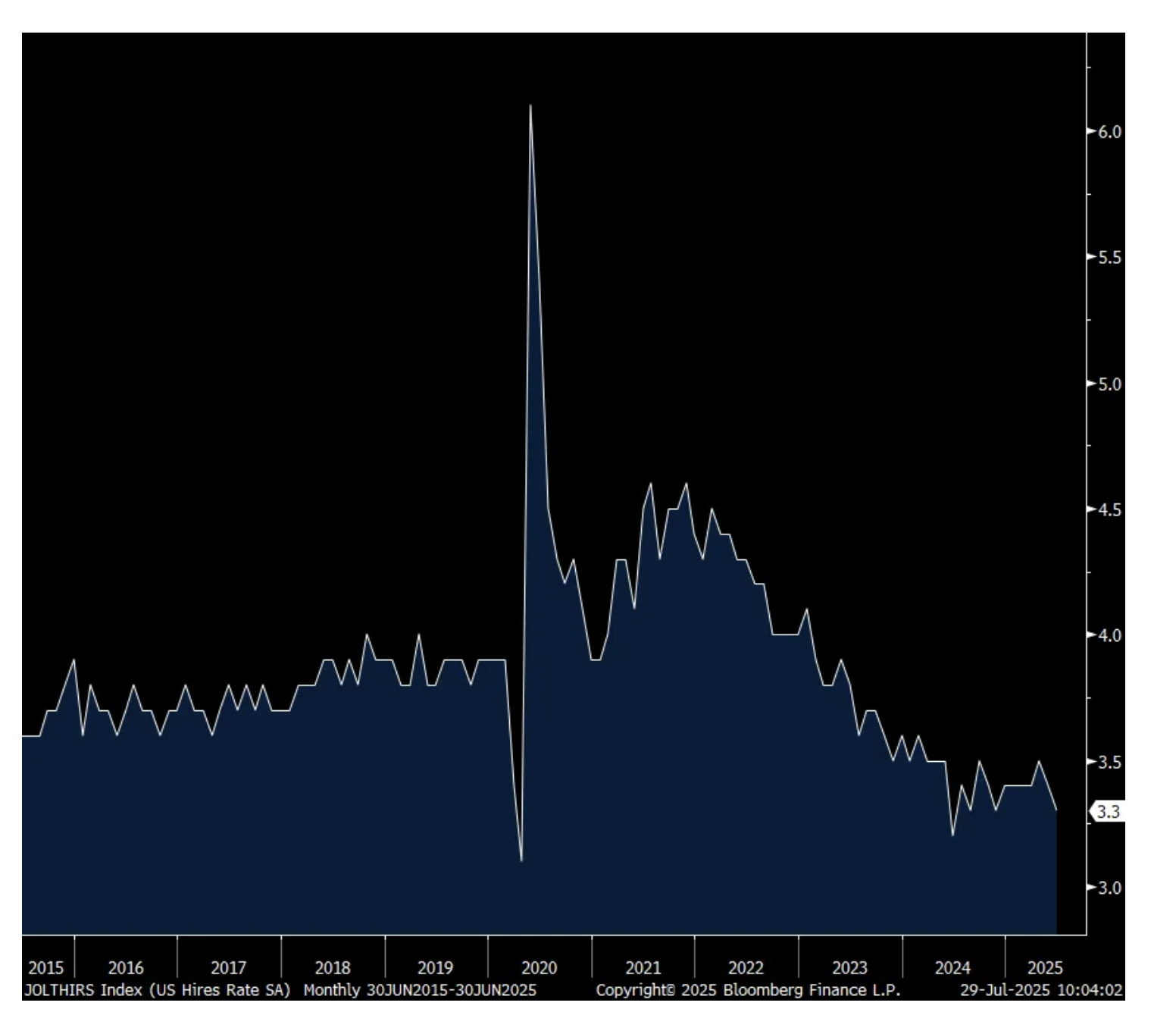

Job openings in June totaled 7.437mm, down by 275k m/o/m and just below the estimate of 7.5mm. With the 2nd straight month of declines in hiring’s, the hiring rate fell to 3.3% which matches the lowest since June 2024 and is just one tenth from matching the least since 2013 not including Covid. The quit rate was at 2% for a 3rd straight month.

While dated data, the hiring rate softness confirms many other data points evidencing the slowdown in the pace of hiring’s.

Job Openings

Hiring rate

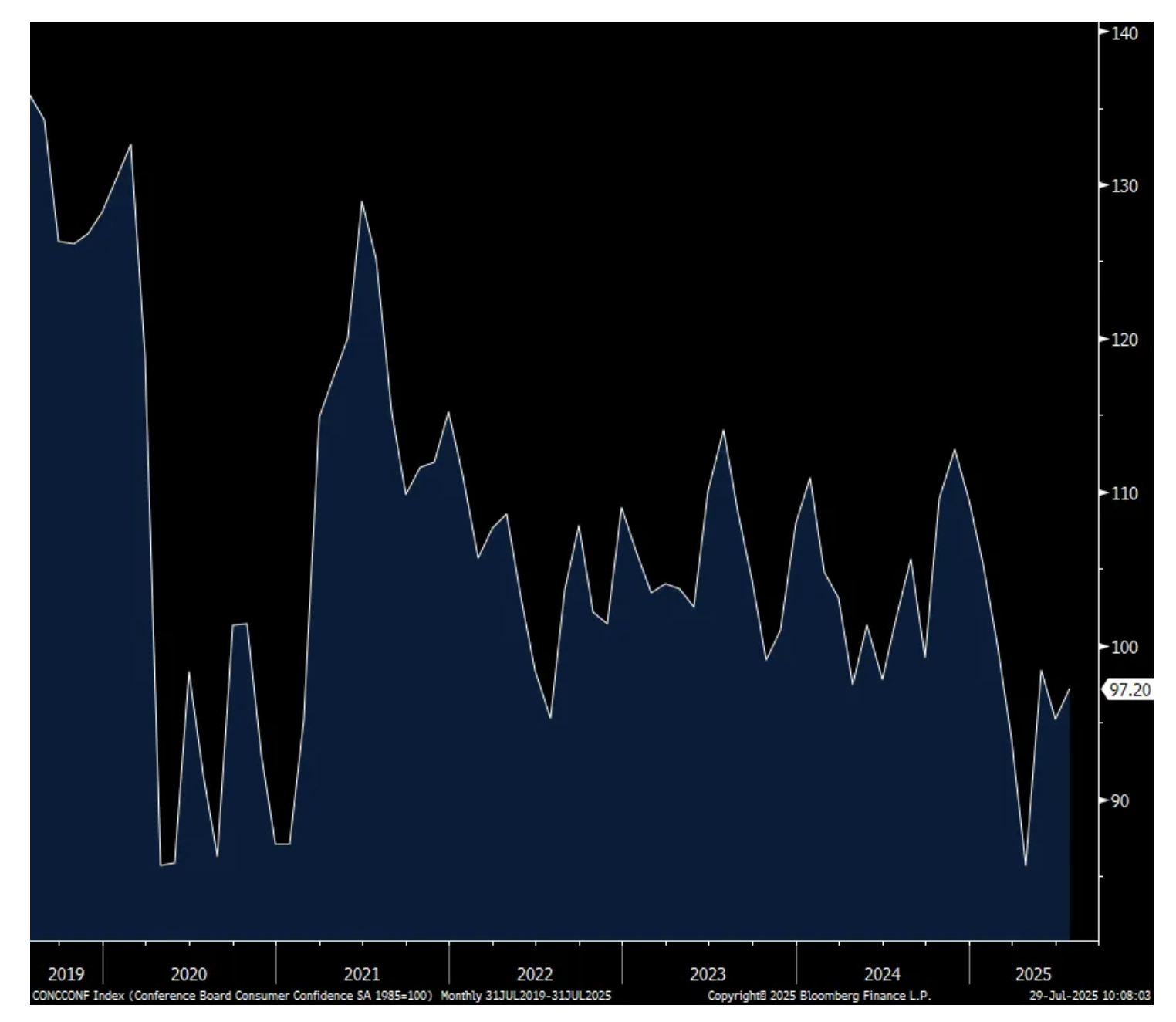

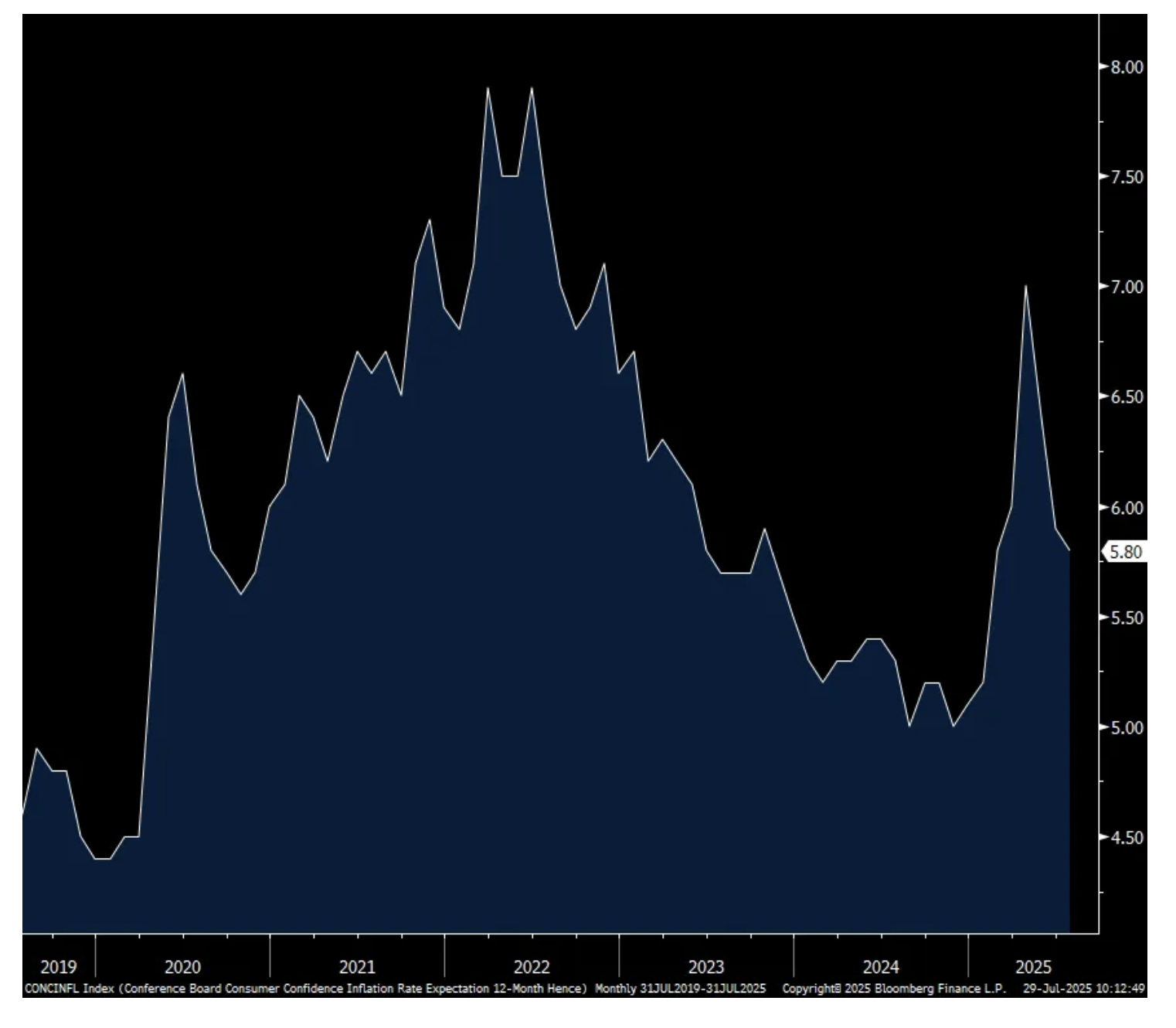

The July Conference Board’s Consumer Confidence index rose 2 pts m/o/m to 97.2 and that was 1.2 pts above the forecast. For perspective, this index was at 132.6 in February 2020. The Present Situation slipped 1.5 pts, offset by a 4.5 pt rise in Expectations. One yr inflation expectations were 5.8%, down one tenth from June. It’s ranged from 5.2 to 7% this year with the influences of the tariffs on the responses, of course.

The Conference Board said “Consumers’ write-in response showed that tariffs remained top of mind and were mostly associated with concerns that they would lead to higher prices. In addition, references to high prices and inflation rose in July, even though consumers’ average 12 month inflation expectations eased slightly.”

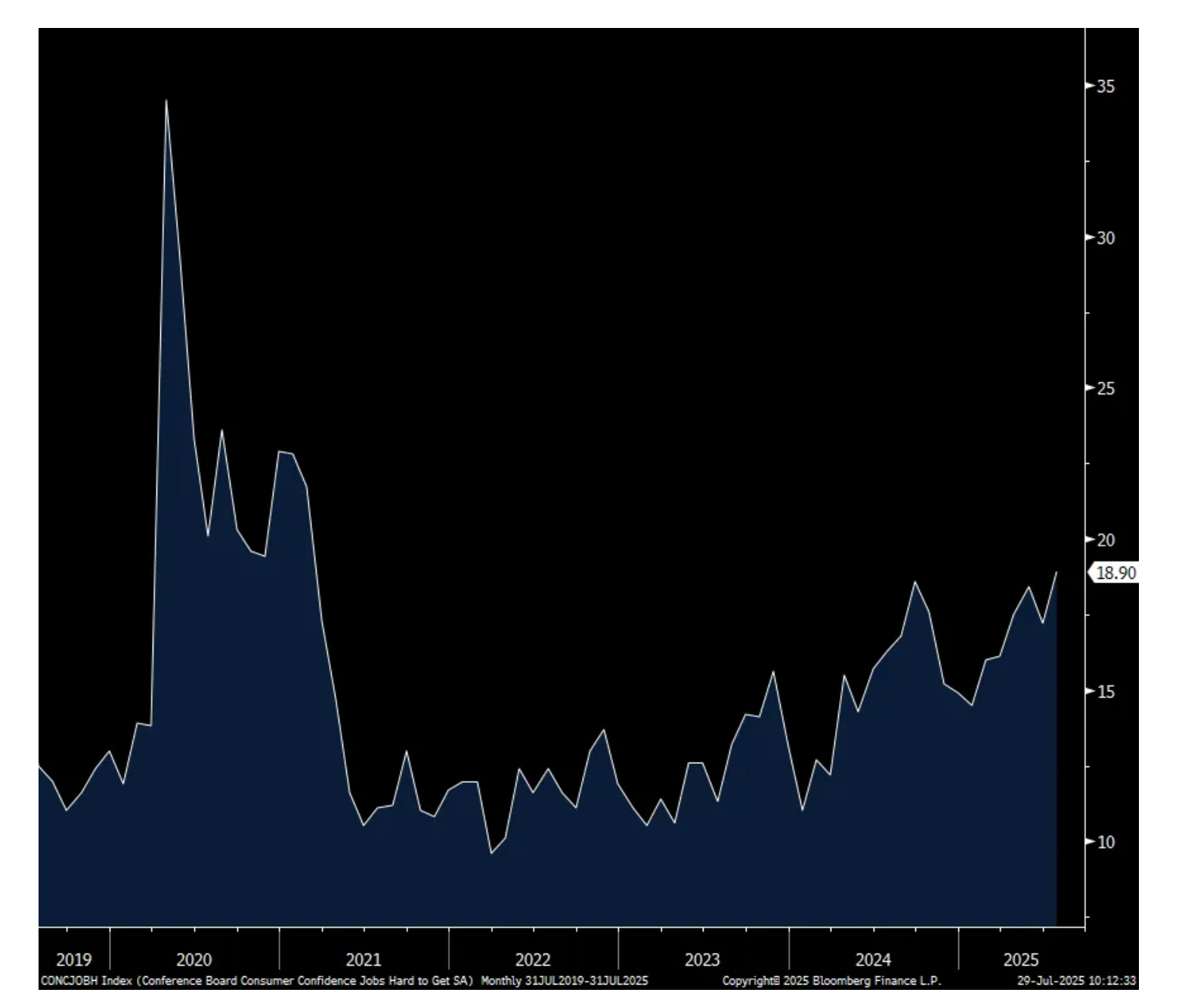

The answers to the labor market questions were mixed. Those that said jobs were Plentiful rose .8 pts but fell by 1.7 pts last month to the lowest level since March 2021. Jobs Hard to Get rose 1.7 pts to 18.9 and that is the highest print since February 2021. In looking out to the next 6 months, there was a 1.6 pt increase in those expecting ‘more jobs’ but this fell by 2.7 pts last month. Income expectations got back almost all of what it lost in June.

Spending intentions for ticket items softened for vehicles, homes and major appliances.

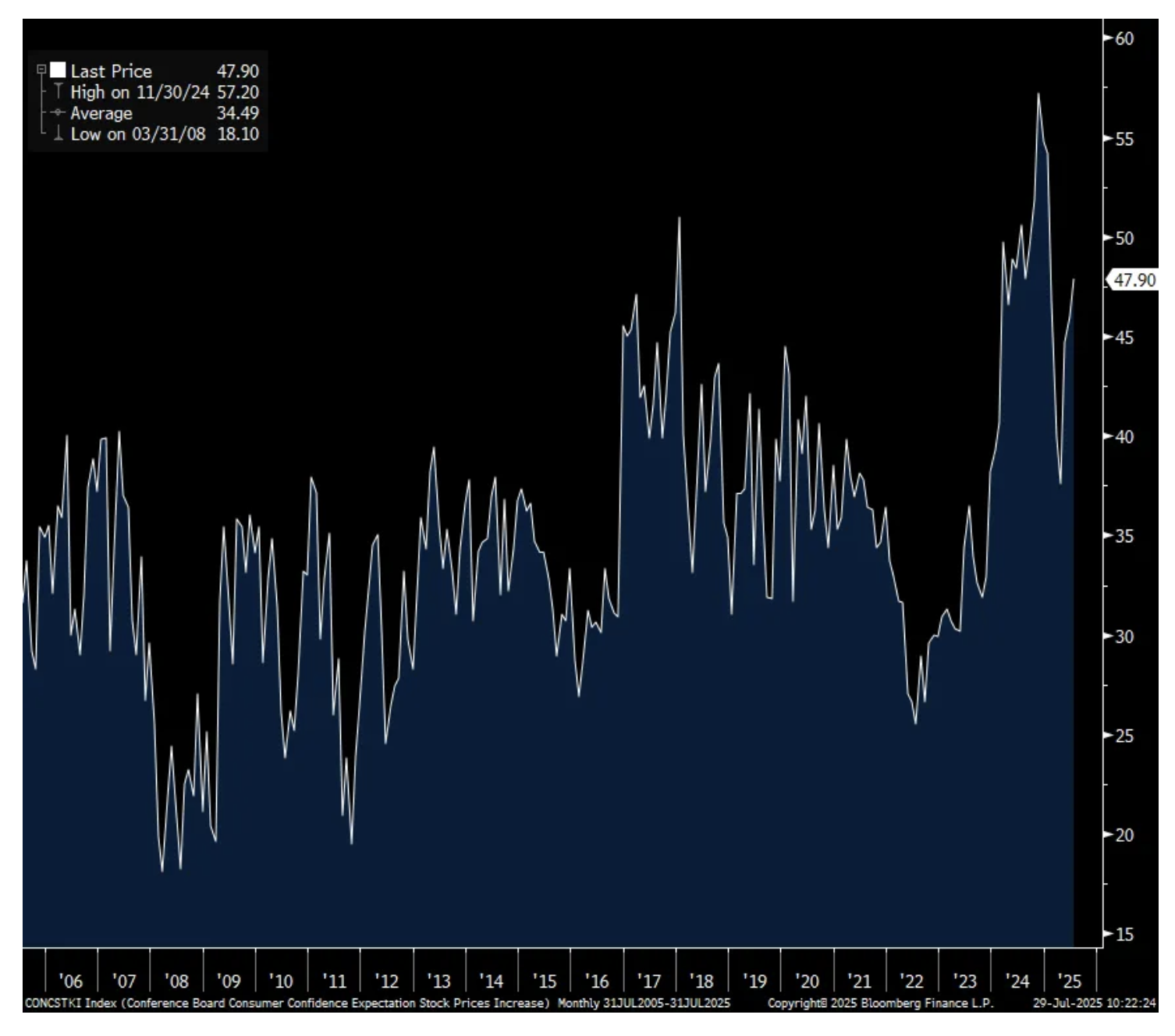

“The share of consumers expecting a recession over the next 12 months declined slightly in July but was still above the levels seen in 2024” said the press release. Also, those expecting higher stock prices in the coming 12 months rose to 47.9% from 46% as it recovers off the April bottom when it fell to 37.6%. It did get as high as 57.2% in November 2024.

The bottom line from the Conference Board, “Consumer confidence has stabilized since May, rebounding from April’s plunge, but remains below last year’s heady levels. In July, pessimism about the future receded somewhat, leading to a slight improvement in overall confidence.”

Adding color to the figures on the labor market answers, consumers “appraisal of current job availability weakened for the 7th consecutive month, reaching its lowest level since March 2021.”

Nothing market moving here but still notable that there remains a consumer angst with their level of confidence with this index still about 35 pts below its February 2020 level.

Consumer Confidence

One yr Inflation Expectations

Jobs Plentiful

Jobs Hard to Get

Percent expecting higher stock prices in coming 12 months

BY Doug Kass · Jul 29, 2025, 11:25 AM EDT

BY Doug Kass · Jul 29, 2025, 11:00 AM EDT

BY Doug Kass · Jul 29, 2025, 10:50 AM EDT

Occasionally I call for a market reversal (from high to lower).

I usually embarrass myself in this process.

But, once again, I am calling for a Ludacris Forecast today.

BY Doug Kass · Jul 29, 2025, 10:18 AM EDT

Some interesting items on popular equities:

Alphabet price target raised to $187 from $184 at Wells Fargo Wells Fargo raised the firm's price target on Alphabet GOOGL to $187 from $184 and keeps an Equal Weight rating on the shares. The firm expects Google Cloud to see meaningful tailwind in FY26 from OpenAI and Anthropic compute workloads with revenue contribution accelerating to +6pts from neutral in 2025. Wells estimates Anthropic was headwind to Google Cloud growth in the first half of 2025, as training workload mix shifted to AWS AMZN from GCP in 2025. This reinforces the firm's view that Google Cloud's Q2 outperformance was driven by core strength, supportive of industry growth. It expects Anthropic headwinds to yield to OpenAI tailwinds in the second half of 2025 and continue into 202

Whirlpool downgraded to Underperform at BofA on weak 2025 outlook As previously reported, BofA downgraded Whirlpool to Underperform from Neutral with a price target of $70, down from $100, following "disappointing" Q2 earnings and guidance as well as a dividend cut. After the company lowered its 2025 ongoing EPS guidance to $6-$8 from $10, the firm lowered its own 2025 and 2026 EPS estimates by (22%) and (23%), respectively.

Disney price target raised to $138 from $130 at JPMorgan JPMorgan analyst David Karnovsky raised the firm's price target on Disney to $138 from $130 and keeps an Overweight rating on the shares. The firm updated the company's estimates ahead of the fiscal Q3 report. The analyst believes investors want to see volume and pricing led operating income increases at Disney's direct to consumer assets and sustained growth at parks.

UPS says seeing a 'complex macro environment' Says U.S. consumer sentiment "near historic lows" which unfavorably impacted small package market. Says manufacturing activity in U.S. "remains soft." Says Amazon glide down initiative "proceeding as planned." Says plans to close more buildings and sort centers in 2H25 in concert with Amazon volume decline. Says impact of trade policy "unknown." Says company, dividend "rock solid strong." Comments taken from Q2 earnings conference call.

BY Doug Kass · Jul 29, 2025, 10:00 AM EDT

From Peter Boockvar:

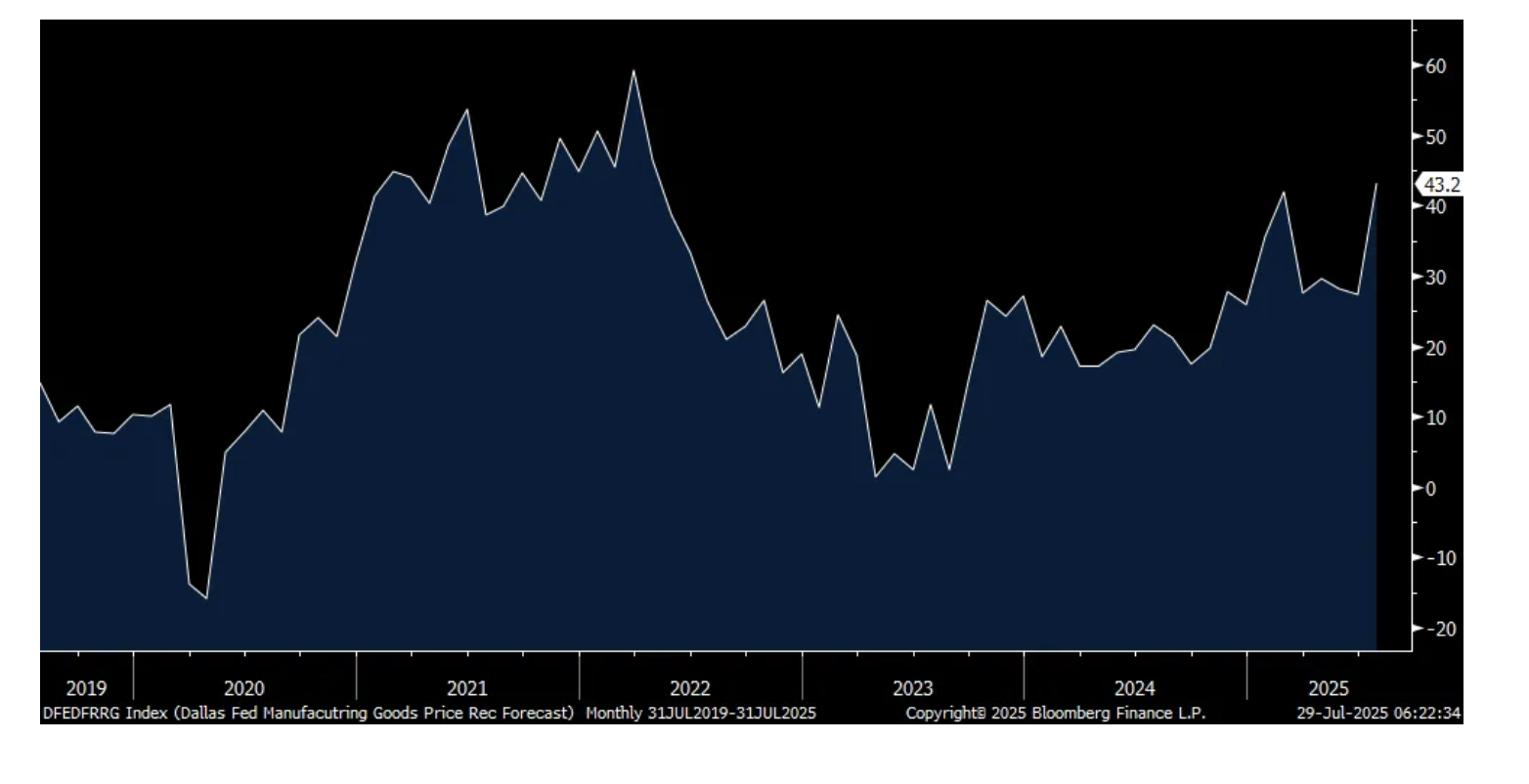

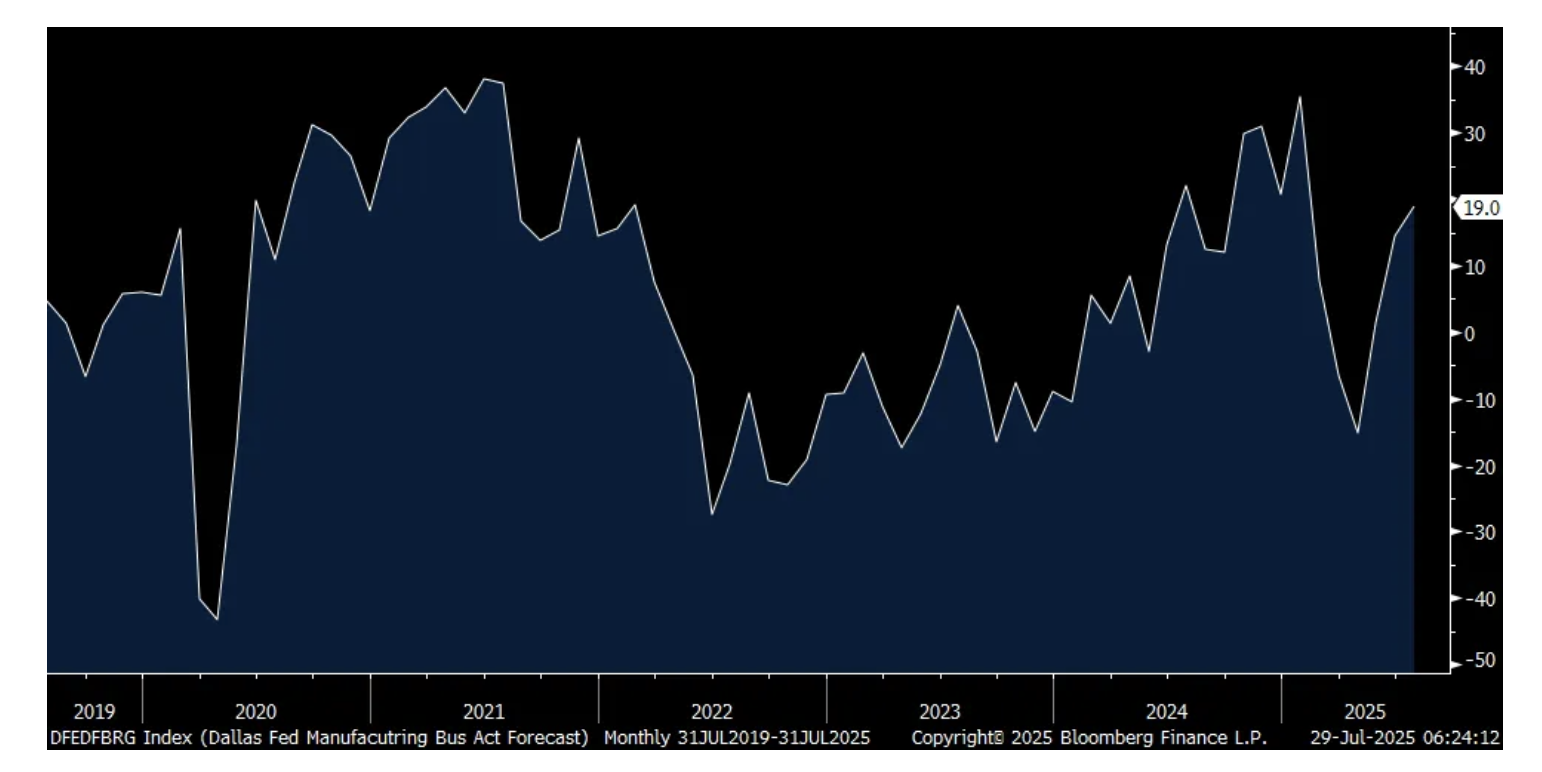

Seen yesterday, the July Dallas manufacturing index got back to around the flatline at +.9 vs -12.7 in June and vs the estimate of -9. This index has had a plus side in front of it just 3 times since Q1 2022. The internals were pretty mixed as new orders, backlogs, and inventories were negative. The lift in the headline looks like it was due to the big jump in production to 21.3 from 1.3. Employment was positive for a 3rd month while capital spending plans slipped m/o/m but was still above zero.

On costs/inflation, prices paid and received both fell m/o/m BUT the 6 month outlook for prices received rose to the highest level since April 2022 so companies are going to try to pass on their higher costs of tariffs, that they are mostly eating. The overall 6 month business outlook improved by another 4.6 pts m/o/m to 19 and that is the highest since January.

Anecdotally, the Dallas index is always a go-to for the company comments and here is what was said of note which continues to reflect the challenges of manufacturers, particularly with tariffs which just throws mud in the gears of business, but with a few pockets of hope. One quote was this, "Tariffs. Tariffs. Tariffs. Did I mention Tariffs?" :

Chemical manufacturing

Construction and automotive continue to have severe declines, leading to major impacts on the basic materials markets.

Computer and electronic product manufacturing

Please lower interest rates now, like other countries are doing.

The impact of DOGE [Department of Government Efficiency], early retirements and tariff uncertainty have caused consumers to be cautious and delay purchasing.

Fabricated metal product manufacturing

There is a significant slowdown in the progression status of new projects. Pricing competition has seemed to decrease.

We expect steady demand and production through September, then declining in the fourth quarter. Tariff costs are expected to continue increasing production material costs.

Food manufacturing

Recent tariff announcements to countries where we purchase raw materials and packaging supplies will strain our operations and result in price increases, potentially leading to decreased demand.

Demand has been soft all summer. Our outlook has dimmed recently, with the volume of new orders declining. New business has been tougher to convert.

I feel a little better now regarding geopolitical issues than in June. I am still a little concerned and worried but not as much as in June.

DOGE, opaque government policy and stagflation [are issues of concern].

Furniture and related product manufacturing

Tariff changes require a sit back and watch attitude. There is no way to forecast.

Machinery manufacturing

We are starting to see orders roll in at a much higher rate than we have in previous months.

In many respects, we seem to be kicking the same can down the same proverbial road, but I, personally, feel like I see the light at the end of the tunnel. My team disagrees with me in some respects, but we're all hopeful that the fourth quarter and into 2026 will bring to fruition what we had expected to occur already by now.

We build machines (capital equipment) in five segments: oil and gas, defense, marine, hydropower and nuclear power. All of these segments are spending money, and the vibe is positive.

Miscellaneous manufacturing

Tariffs [are an issue of concern].

Tariff impacts continue to hurt our overall business and profitability.

Nonmetallic mineral product manufacturing

Tariffs. Tariffs. Tariffs. Did I mention Tariffs?

Paper manufacturing

Business is maintained at a reduced level that has our outlook somewhat negative.

Primary metal manufacturing

Our industry is closely tied to the building and construction market, which remains softer than in previous years. The transportation industry, particularly for trailer manufacturing, is down significantly. Building and construction and transportation are the two largest markets for our products. However, that downturn is being partially offset by the ongoing trend of onshoring manufactured goods, driven largely by tariffs. One major challenge in recent years has been Mexico’s exemption from Section 232 tariffs, which created a significant disadvantage for U.S. manufacturers in our markets. With that exemption now lifted, we’re seeing a more level playing field. This change should benefit our industry, particularly as China had been setting up operations in Mexico to bypass tariffs and enter the U.S. market tariff-free. Fair trade is critical, and the enforcement of tariffs like Section 232 is a step in the right direction for protecting and strengthening U.S. manufacturing.

Capital is being spent to add product offerings to increase business activity

Printing and related support activities

The tariff matters continue to cause major uncertainty. It is impossible to plan. It is causing uncertainty throughout the supply chain.

If not for a few large jobs, we would be very slow and laying off workers. Things, however, have picked up the last few weeks with lots more quote activity and orders being entered. I still feel all the chaos and uncertainty over tariffs are having a very negative effect on demand in our market. I am hopeful it will improve six months from now.

Textile product mills

We are starting to see vendors and suppliers pass on more price increases, with "tariffs" being the explanation. We are weighing our options for passing this price increase on to our buyers, eating the additional cost/reducing our margin, or a combination of the two.

Transportation equipment manufacturing

We are implementing layoffs and reduced working hours in August.

6 month outlook for Prices Received

6 month outlook Business Activity

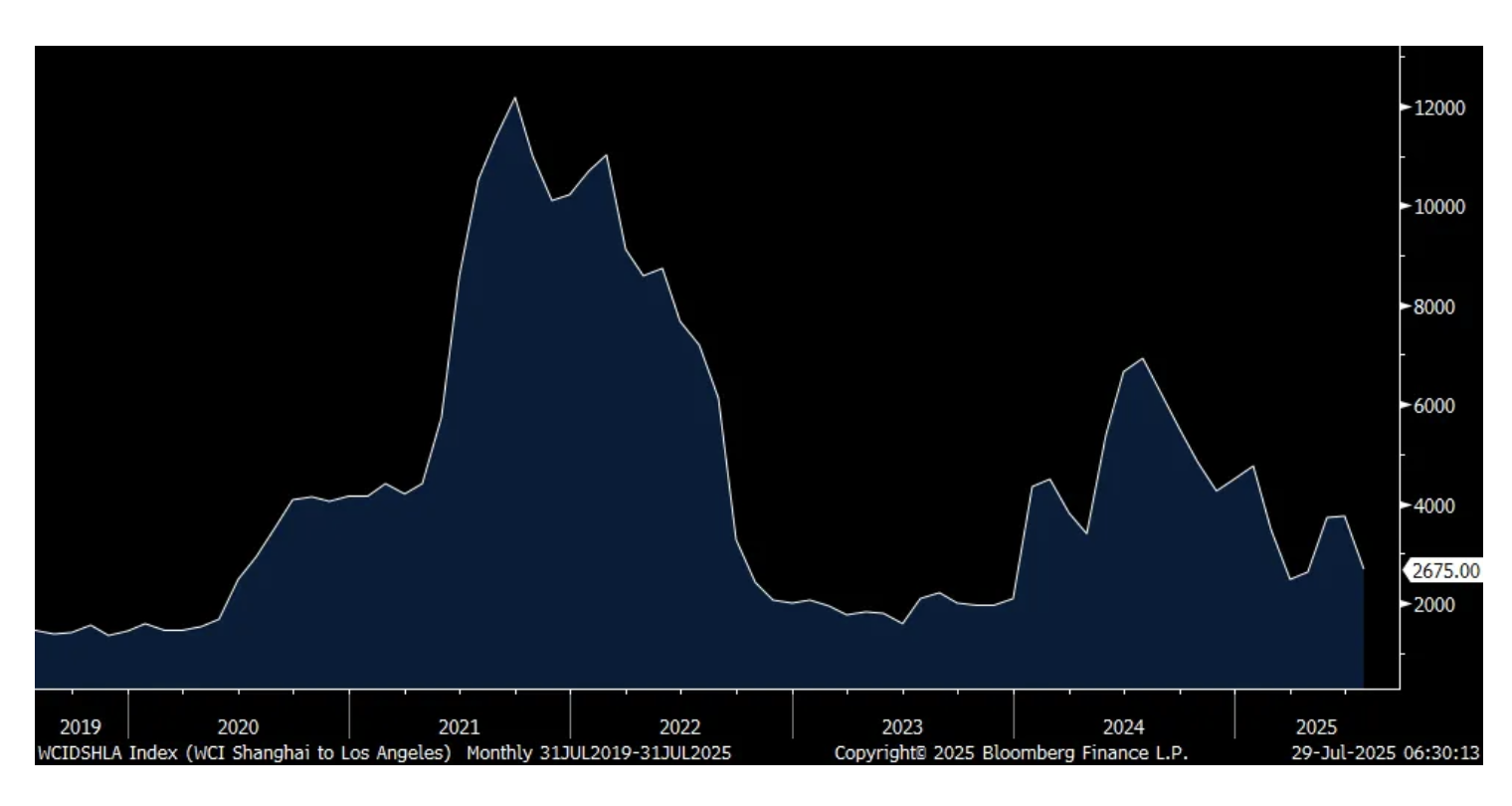

After the rush to order goods to front run tariffs, the cost of procuring containers has cooled as of Friday. The Shanghai to LA trip now cost $2,675, down $142 w/o/w and almost back to where it was in late March before the April 2nd tariff day. The Shanghai to NY has had a similar trajectory and with its cost at $4,210, down $329 w/o/w.

Shanghai to LA

Shanghai to NY

Revenue and earnings were mixed from UPS and they said "Given the current macro-economic uncertainty, the company is not providing revenue or operating profit guidance." We await their earnings call this morning.

From Whirlpool who badly missed numbers and whose stock is down sharply pre-market:

"As expected, the second quarter continued to be impacted by competitors stockpiling Asian imports into the US."

Sales fell 4.6% y/o/y specifically in North America "as negative consumer sentiment impacted demand and product mix; promotional intensity remains elevated amid continued 'pre-loading' of Asian imports by foreign competitors ahead of tariffs."

From Royal Caribbean who could not meet high expectations and whose stock is down pre-market but still reported a good quarter as we know travel/experiences has been an economic bright spot:

"Booked load factors remain in line with prior years and at higher rates for both 2025 and 2026. Bookings have accelerated since the last earnings call, particularly for close-in sailings, leading to second quarter outperformance. The company continues to experience strong demand across all key products and source markets. Commercial channels, particularly digital channels, are performing exceptionally well for both bookings and pre-cruise purchases. Guest spending onboard and pre-cruise purchases continue to exceed prior years, driven by participation at higher prices."

From the Proctor & Gamble earnings release, "We grew sales and profit in fiscal 2025 and returned high levels of cash to shareowners in a dynamic, difficult and volatile environment."

Spain continues to be an economic standout in Europe as its economy grew by 2.8% y/o/y in Q2, above the estimate of 2.5% and the same pace seen in Q1. This is more than double total growth for the Eurozone. Helping is that the economy is not that reliant on global trade and manufacturing compared with some of its regional peers and is benefiting from tourism and its service sector. The Spanish IBEX is up 1% today and by 24% ytd and by 38% in dollar terms. Amazingly though, it's still trading below its 2007 peak.

Spanish IBEX

BY Doug Kass · Jul 29, 2025, 9:37 AM EDT

BY Doug Kass · Jul 29, 2025, 9:23 AM EDT

BY Doug Kass · Jul 29, 2025, 9:10 AM EDT

-DRRX +264% (BHC to acquire DRRX for upfront consideration of ~$63M at closing, with the potential for two additional net sales milestone payments of up to $350M)

-CLDI +43% (receives FDA Fast Track Designation for CLD-201 (SuperNova), a First-In-Class Stem-Cell Loaded Viral Therapy for treatment of Patients with Soft Tissue Sarcoma)

-SRPT +36% (confirms FDA Informs Sarepta That It Recommends That Sarepta Remove Its Pause and Resume Shipments of ELEVIDYS for Ambulatory Individuals With Duchenne Muscular Dystrophy; Shipments to sites of care will resume imminently; FDA concluded the death of 8-yr-old in Brazil was unrelated to treatment with ELEVIDYS)

-WGS +28% (earnings, guidance)

-GTLS +16% (Baker Hughes to buy company for $210/shr cash at EV $13.6B)

-ATOS +14% (US FDA backs Atossa’s dose study for breast cancer drug (Z)-endoxifenancer)

-XPRO +13% (earnings, guidance)

-CECO +11% (earnings, guidance)

-SOFI +11% (earnings, guidance)

-AMKR +9.7% (earnings, guidance)

-PII +9.1% (earnings, guidance)

-CDNS +8.2% (earnings, guidance)

-CVLT +8.2% (earnings, guidance)

-TRS +7.7% (earnings, guidance)

-RMBS +5.3% (earnings, guidance)

-GLW +5.2% (earnings, guidance)

-CING +4.8% (receives $4.3M Waiver from FDA Ahead of Imminent Filing for Marketing Approval of Lead ADHD Asset CTx-1301)

-ON +3.9% (collaborates with NVIDIA to accelerate transition to 800 VDC Power Solutions for Next-Generation AI Data Centers)

-JBLU +3.7% (earnings, guidance)

-CBRE +2.7% (earnings, guidance)

-BKKT -40% (guidance; prices 6.75M shares at $10/share; the offering includes warrants)

-NVO -20% (cuts guidance; appoints new CEO)

-LESL -19% (prelim Q3 earnings; cuts guidance)

-WHR -17% (earnings, guidance)

-NEO -15% (earnings, guidance)

-TLRY -12% (earnings, guidance)

-SWK -7.8% (earnings, guidance)

-NOV -7.5% (earnings, guidance)

-VRSN -7.0% (prices 4.3M shares at $285/share for selling stockholder Berkshire Hathaway)

-SPOT -5.4% (earnings, guidance)

-RCL -5.2% (earnings, guidance)

-MRK -4.5% (earnings, guidance)

-NUE -3.9% (earnings, guidance)

-UPS -2.9% (earnings, guidance)

-BKR -2.8% (to buy GTLS for $210/shr cash at EV $13.6B)

-NSC -2.3% (Union Pacific confirms to acquire Norfolk Southern at $320/shr in $85B deal, mostly in stock with cash part; earnings, guidance)

-PYPL -2.3% (earnings, guidance)

BY Doug Kass · Jul 29, 2025, 9:00 AM EDT

BY Doug Kass · Jul 29, 2025, 8:48 AM EDT

BY Doug Kass · Jul 29, 2025, 8:25 AM EDT

BY Doug Kass · Jul 29, 2025, 8:16 AM EDT

BY Doug Kass · Jul 29, 2025, 7:10 AM EDT

From JPMorgan:

US: Futs are higher into a heavy earnings day and ahead of tmrw’s Fed decision. Pre-mkt, Mag7, Semis, and Cyclicals are outperforming. Bond yields are lower as the USD rally is poised to continue. Cmdtys are mixed with Energy leading on US / RU geopolitics. The macro data focus today includes JOLTS, Housing Prices, regional Fed activity indicators, trade data, inventories, and consumer confidence.

and...

JPM MARKET INTEL EQUITY & MACRO NARRATIVE

Yesterday, the euphoria surrounding the US / EU faded quickly with the EU session closing almost wholly in the red. There is pushback from EU-based businesses and what was thought to be the ‘least bad option’ looks to be a wholly one-sided deal, in favor of the US, and awaits broader approval. Further, this deal is likely to create a growth headwind for the EU with the potential to push the region into a mild recession.

In the US, Tech was able to keep NDX afloat with Semis driving the group higher which is more about the TSLA / Samsung deal than it is the US / EU trade agreement. The EUR / USD had its worst day since mid-May and now begs the question of whether this could be the early stages of a return to the US Exceptionalism trade.

BY Doug Kass · Jul 29, 2025, 6:52 AM EDT

BY Doug Kass · Jul 29, 2025, 6:40 AM EDT

BY Doug Kass · Jul 29, 2025, 6:30 AM EDT

BY Doug Kass · Jul 29, 2025, 6:15 AM EDT

The S&P Short Range Oscillator stands at 1.08% vs. 1.90%.

BY Doug Kass · Jul 29, 2025, 5:50 AM EDT