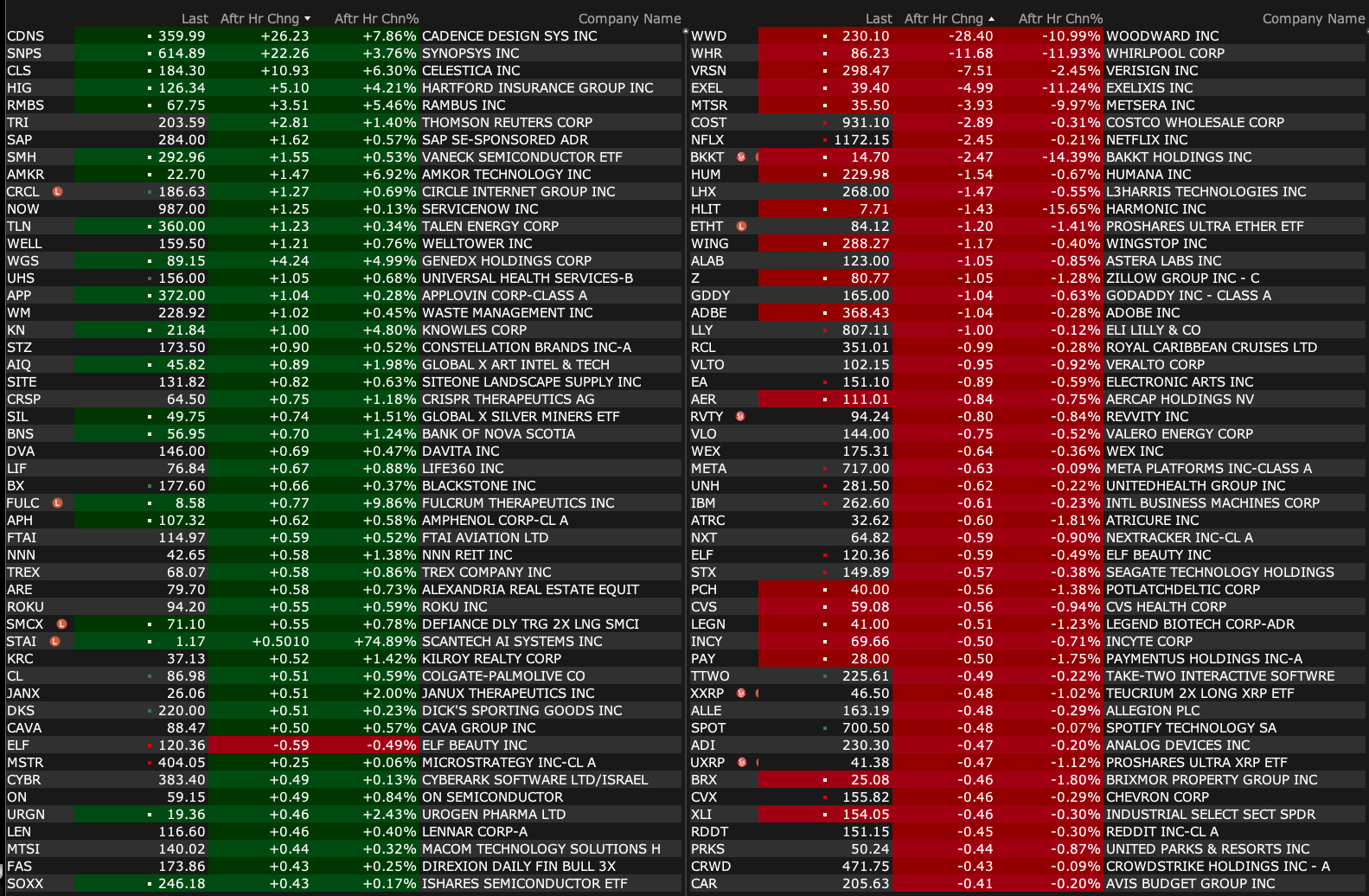

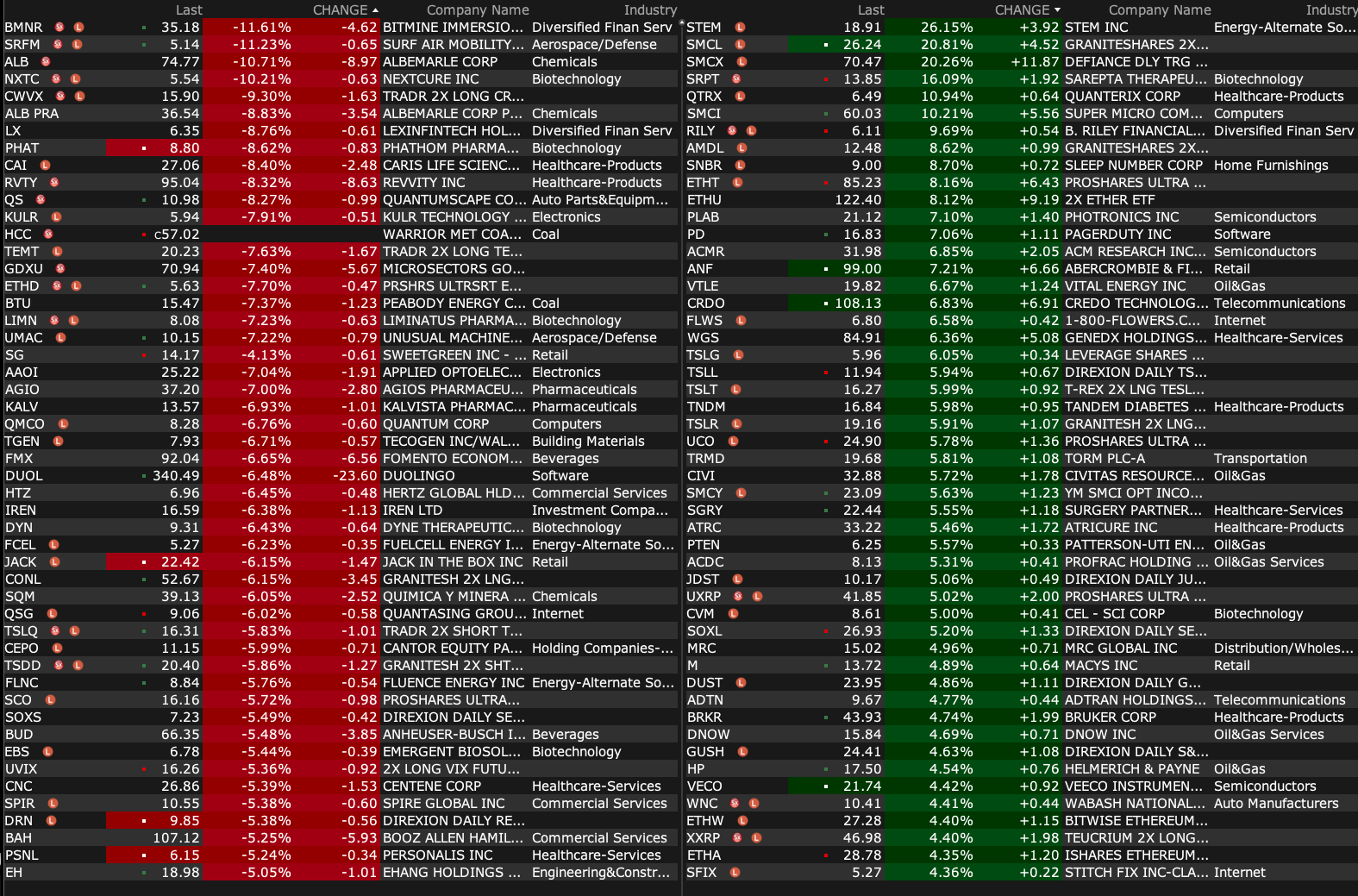

Monday's After-Hours Movers

As of 4:22 p.m.:

BY Doug Kass · Jul 28, 2025, 4:50 PM EDT

As of 4:22 p.m.:

BY Doug Kass · Jul 28, 2025, 4:50 PM EDT

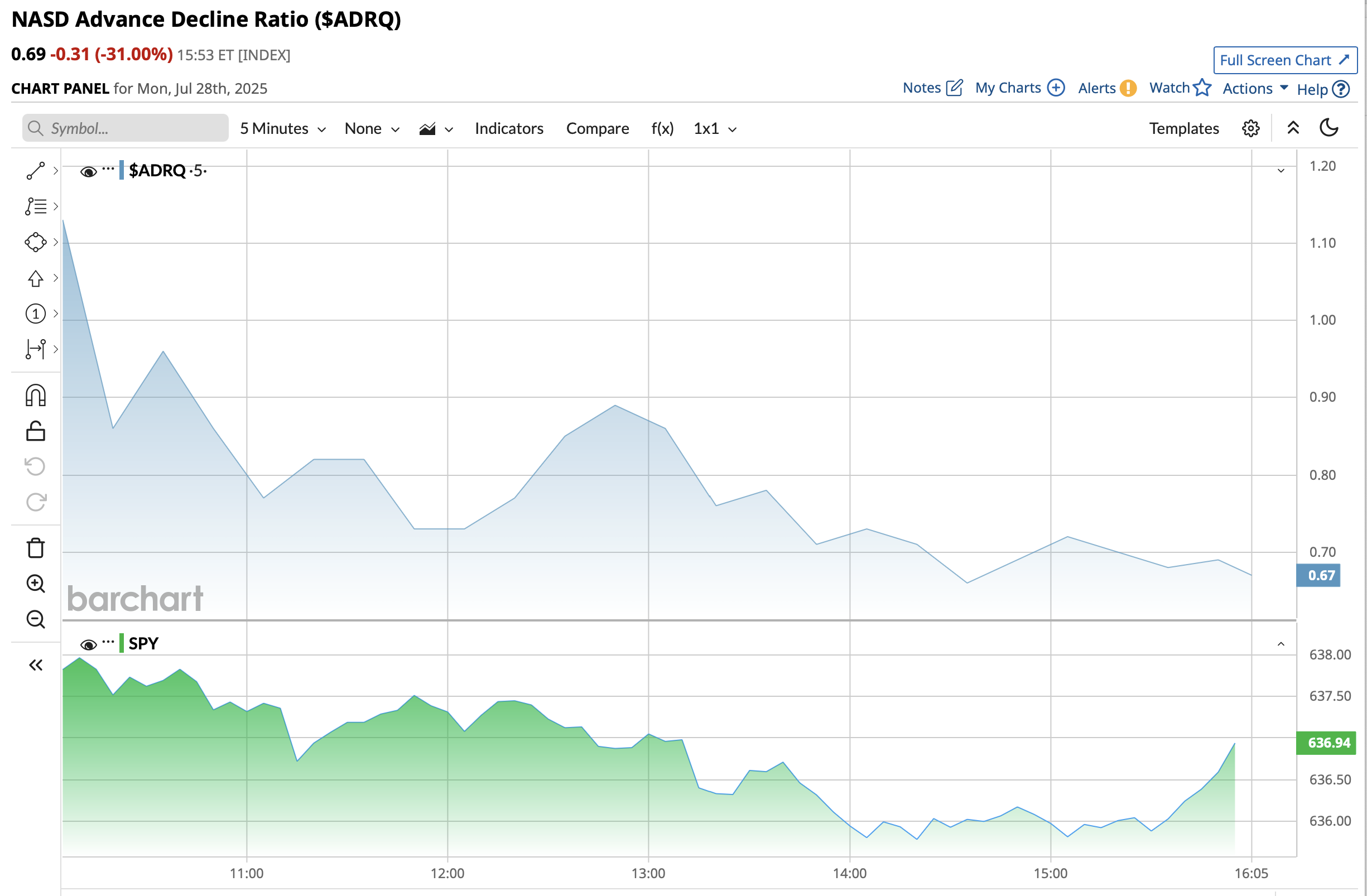

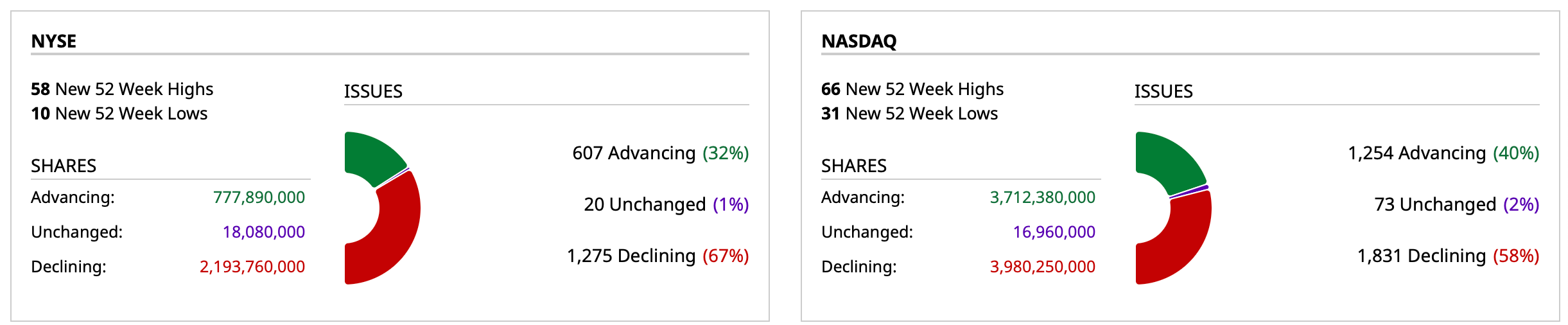

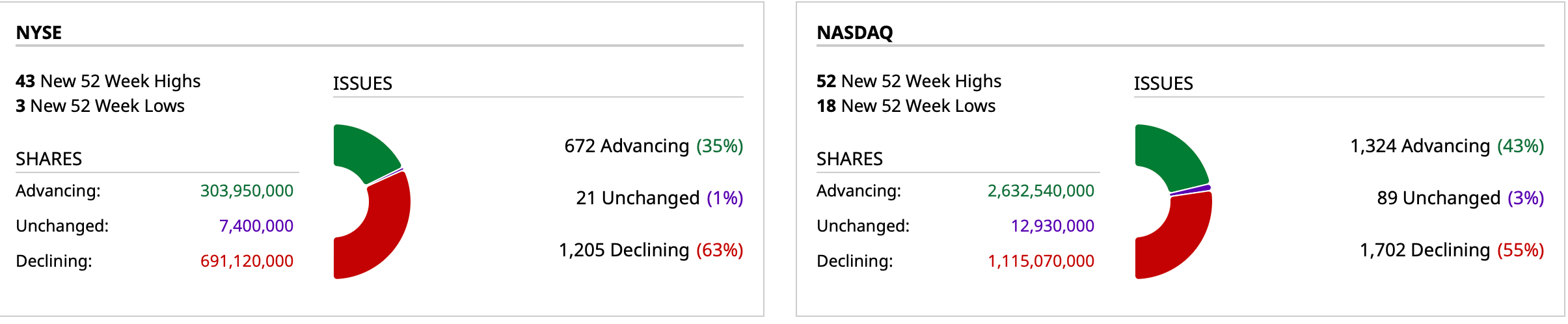

Intraday breadth (blue) declines at close despite SPY (green) advancing:

BY Doug Kass · Jul 28, 2025, 4:41 PM EDT

- NYSE volume 17% below its one-month average;

- NASDAQ volume 14% above its one-month average;

- VIX index: up 0.67% to 15.03

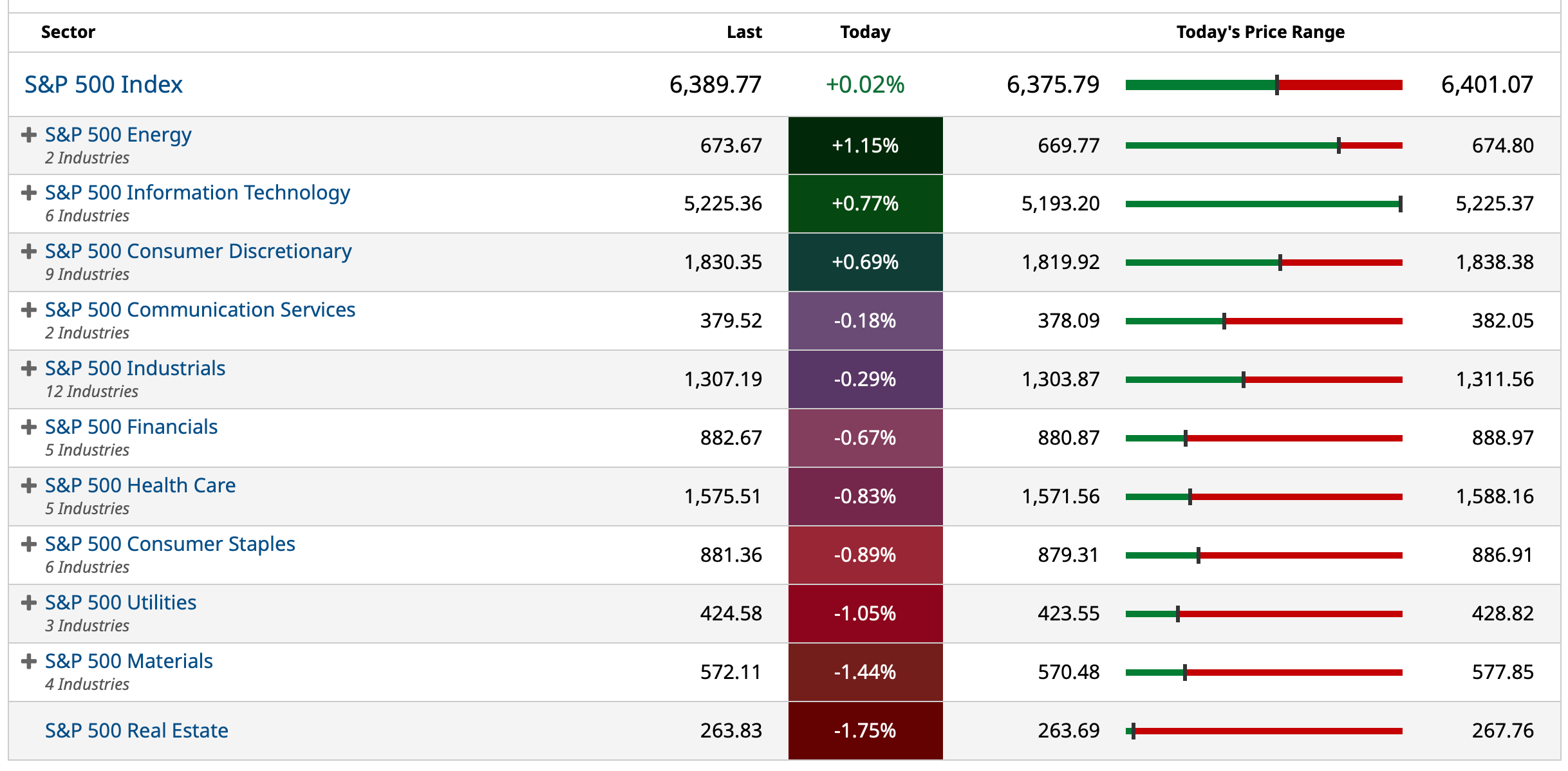

BY Doug Kass · Jul 28, 2025, 4:35 PM EDT

BY Doug Kass · Jul 28, 2025, 3:39 PM EDT

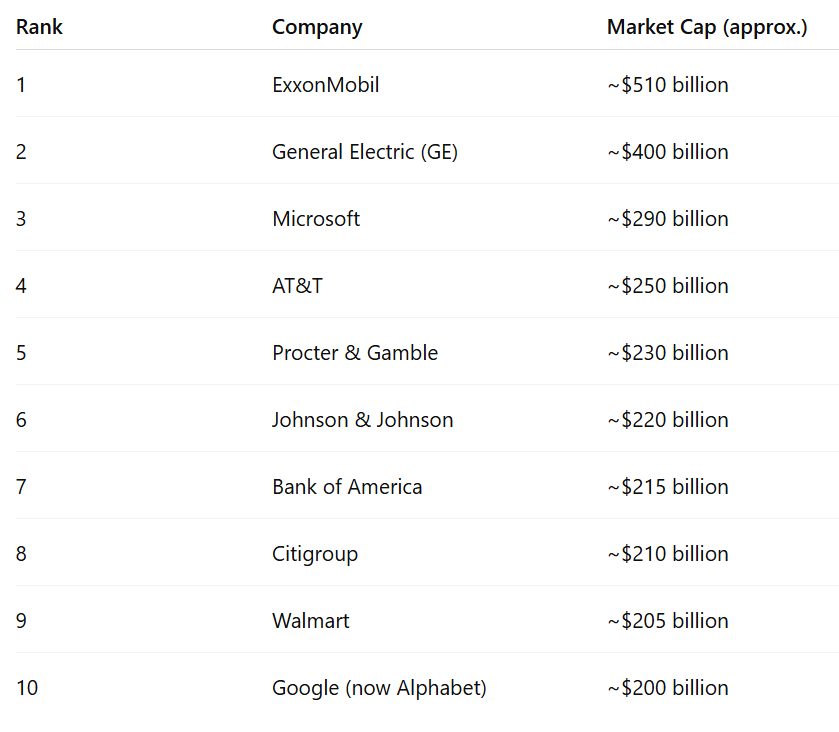

There is a consensus view that many of the Mag 7 companies will be immune to an economic or market downturn.

Let me remind everyone that the 10 biggest companies just before the 2000 crash were ALL "real" companies — so even in that regard there's nothing all that different from today:

And the same held for September 2007:

BY Doug Kass · Jul 28, 2025, 2:35 PM EDT

Addisonst

So far, the market seems to think the eu deal is a nothing burger.

Dougie Kass

what deal?

few of the constituent countries are in favor of it

no different than the tariff deal with japan.

basically undocumented.

TechNova

Perhaps because like the Japan "deal" it is not yet a "deal" ?

BY Doug Kass · Jul 28, 2025, 1:55 PM EDT

In the last week I sold out all of my remaining financial long positions (BAC, C, JPM, WFC, AXP, MS, GS etc.)

Today could be the start of a rollover in the sector, stay tuned.

I have been shorting JOET, which has a large financial component to its top holdings.

BY Doug Kass · Jul 28, 2025, 1:40 PM EDT

I am at my largest net short exposure since January 2025.

BY Doug Kass · Jul 28, 2025, 1:23 PM EDT

At 11:50 AM.

BY Doug Kass · Jul 28, 2025, 12:25 PM EDT

BY Doug Kass · Jul 28, 2025, 12:05 PM EDT

* Is AI so bad, it is good?

This has played out differently than I expected.

It is not working, in exactly the way I suspected it wouldn’t work. Not scaling, with the same flaws and making the same errors, and not advancing towards AGI.

HOWEVER, the reaction to the not working has been much different than I expected.

Normally, the rational thing to do when something is not working is to slow down, and re-evaluate. In this case, the opposite has happened. The big players (now including the U.S. government who wants to keep the hype train going) have all decided to do more of what is not working. Throw more money at the problem. And keep doing so. This is not unheard of either. It does happen in rare cases, and not just in business, although businesses are generally more rational.

For example, if the government or the Federal Reserve has a bad policy that doesn’t work, rather than admit they are wrong, they just do more of what isn’t working. It happens in medicine too. Instead of trying to do something differently, the human tendency is sometimes to not admit you are wrong, and just do more, if one is able to do more of what isn’t working.

In this case, they are able to do more of what is not working. There seems to be an unlimited amount of money and egos, nobody who wants to admit they are wrong and this isn’t working exactly right (besides maybe MSFT who has decided to let others burn money while MSFT hosts their ability to do it), and still a lot of buy in to the hype, so more dollars continue to be spent. This whole thing seems to be somewhat reflexive with the stock market as well. The spending feeds on the stock market, and the stock market feeds on the spending. And around and around we go. Arguably, retail is driving equities now too. Therefore, the guys buying ODTEs are the ones determining massive allocations of capital in the U.S. economy. Therefore, the guys buying meme stocks and ODTEs are the ones determining massive allocations of capital in the U.S. economy. Swell!

The results have been so bad, it is driving more spending than I thought was even possible. Quickly on to the next model, and an even bigger data center, but neither Musk’s nor Zuckerberg’s nor Altman’s ... ah hem, abilities ... actually grow, so spend more again. In fact, the incremental return on additional dollars spent keeps getting worse. Which oddly, is causing more dollars to be spent. This is a worse return than the U.S. economy, where we have seen now that incremental debt no longer drives GDP and is in fact probably counterproductive.

But, finally, on the margin, the public markets seem to be punishing the spenders for all the $ going out the door. The market did not react well to Googles forecast of increased spend, for example. Granted, the stock still went slightly up because the markets are on fire and their actual results were pretty good. But the initial reaction to Google's increased spending was not positive. Even with the elongated depreciation schedules, the spend will start hitting bottom lines soon.

At any rate, after this current bolus of spend, when we are still in roughly the same place, it is going to be really interesting. What do you do if there is no substantial advancement? Further, it is not going to be easy to keep adding new DCs. Besides the expense, there is neither the power or grid capacity, and water for the liquid cooling is also an issue. It is becoming a bit dystopian. If this batch of spending does not cause a sea change, that is when the air comes out of the bubble.

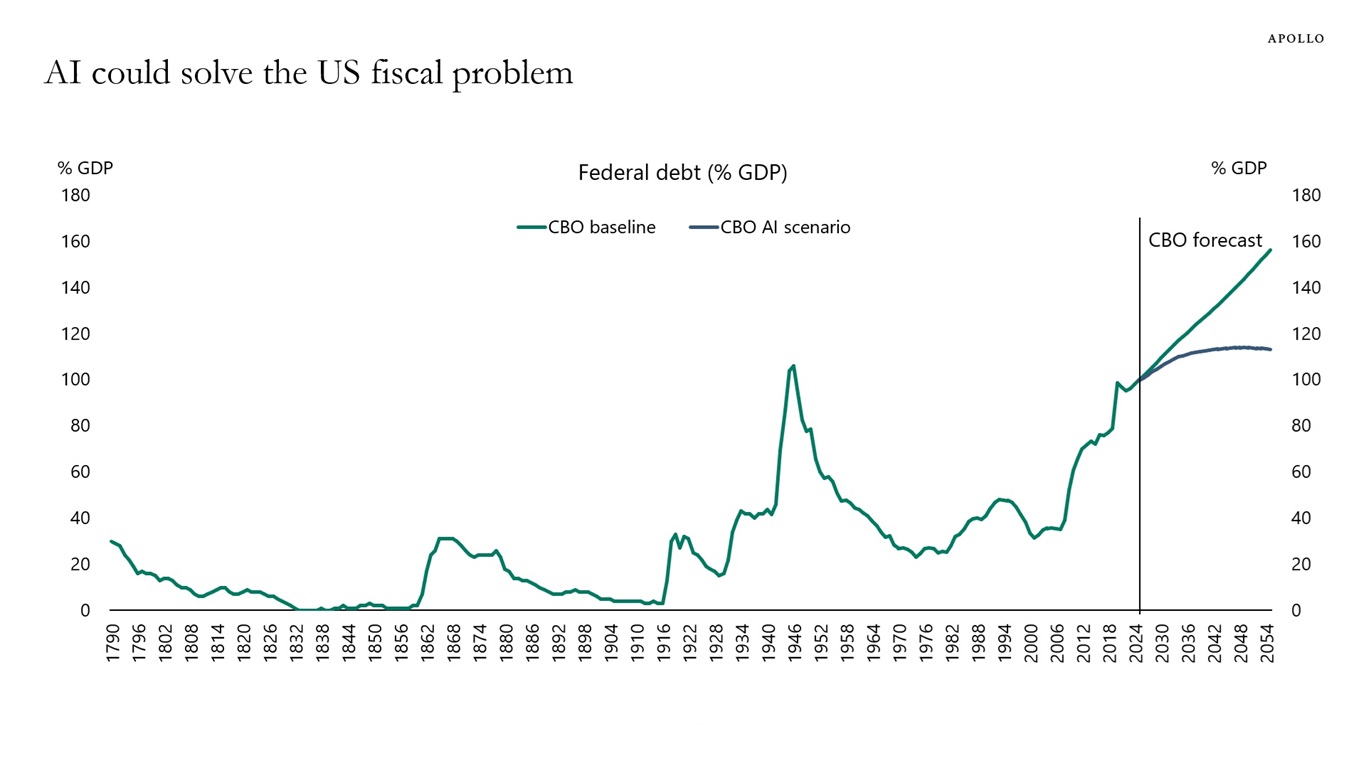

Related to all of this, I saw below chart from the Congressional Budget Office on the potential impact of AI on Federal debt as a pct of GDP. What a joke. I am not sure why we have a CBO, they are wrong about everything. What a waste of time to do this. I could close my eyes and draw 100 forecast lines, and each one of them would have an equal chance of being right as the CBOs single point forecast. The arrogance as well to produce a single point forecast, utterly absurd. What a bunch of dopes. Can I get my tax dollars back?

At any rate, what is always forgotten in this analysis, which relates to the point about all the spending and the diminished marginal returns, is the system cost of the whole thing. You cannot ignore all the losses on the other side. If a customer saves $5 by using something, but the provider loses $7 selling it, there is actually a $2 loss to productivity. That is what is going on now. Everyone is ignoring all of the losses on the provider side, which are massive. Customers may be getting some marginal productivity gains, but they wouldn’t be if what they purchased was being priced where the provider can profit. If it was priced at that point, there would be no revenue, because it doesn’t cover its cost.

This cannot go on forever. For AI to have value, it must deliver more $ than it loses. Right now, we are not even close. Oddly again, the more money being spent on infrastructure and services, the worse the math gets, because as opposed to the exponential improvement from scaling that was expected, you are getting as much improvement from the additional spend as the US economy is now getting from each additional $ of debt.

BY Doug Kass · Jul 28, 2025, 11:20 AM EDT

BY Doug Kass · Jul 28, 2025, 11:15 AM EDT

From JPMorgan:

US: Futs are higher on a trade-induced, global risk-on rally. US/EU did a deal for 15% tariffs. US/China are said to extend the trade truce by 90-days. Pre-mkt, all Mag7 names are higher with Semis outperforming. Cyclicals are poised to outperform, led by Fins/Indu. Bond yields are down 2bp as the curve shifts lower as USD appreciates. Cmdtys are mixed with crude higher, natgas lower, precious flat, base down, and Ags mixed. Today’s macro data is light with on Dallas Fed Mfg Activity.

and...

JPM MARKET INTEL EQUITY & MACRO NARRATIVE

As we enter what may be the last active week of the summer, let’s begin with color from my colleague Craig Cohen, “The S&P 500 ended modestly flat yesterday [July 24] but still marked an impressive milestone. The S&P 500 has now rallied more than 25% over the past 75 days, the largest 75-day rally since the rebound from the COVID lows. Forward-looking returns after a rally like this are quite strong. A year later, the index was higher every single time with an average return of around 20%. Shorter timeframes show strong returns as well. The S&P 500 was, on average 7% higher three months later and 13% higher six months later.” For clients worried about investing at all-time highs, our colleagues at JPM Asset Management suggest those fears are overblown and that investing at ATHs may be optimal.

SPX: 75-DAY, 25% RALLY

Source: Bloomberg Finance, L.P. as of 7/25/25

· LAST WEEK’S MACRO DATA – The Flash PMI data showed the potential for the US economy to inflect higher, with growth metrics pointing to 25Q3 growing ~2.3% up from 25Q2’s 1.3%, per S&P Global’s Chief Economist. Growth was driven by Services as Manufacturing activity deteriorated for the first time since December; supply chains continue to decongest which is also reflected in lower shipping rates. However, inflationary pressures are building via both tariffs and labor shortages, the latter of which is exacerbated by mass deportation and tighter immigration policies. Separately, the most recent CPI showed ~60% of components experiencing ~2.5% annualize inflation with both breadth and magnitude expected to increase once the tariff pause ends. Initial jobless claims declined while remain elevated.

· THIS WEEK’S MACRO DATA – The key data point is NFP where investors seek to gain clarity on the tariff headwind. The BBG consensus is 109k jobs; Feroli sees 100k jobs being added. ISM-Mfg, PCE, Consumer Sentiment, and Q2 data are also important. Lastly, the Fed meeting is expected to result in no changes, but investor will want to see if Powell hints to any criteria that will affect the September meeting. Feroli’s FOMC preview is here; he expects no changes and with no update to the DOTS, the focus is wholly on the press conference.

· US MKT INTEL VIEW – Tactically Bullish. We continue to find evidence for our bullish hypothesis: (i) resilient macro data; (ii) positive earnings growth; (iii) thawing trade war rhetoric. This week we are focused on NFP and MegaCap Tech earnings. It seems likely that this market continues to run higher at least until we get to NVDA earnings on Aug 28. NVDA is sitting on a 9-week win streak and is +84% from its YTD lows set on Apr 4. NVDA earnings may be a sell-the-news event, cueing the market to take a breather into seasonal weakness. This century, August has been a flat month, September the worst month of the year followed by Q4, which is the strongest quarter of the year.

· MONETIZATION MENU – (no change since the week of July 14, 2025) We like longs in MegaCap Tech, Cyclicals, and high beta plays. At the country/region-level, we like Australia, China (Tech), and Japan but think the US will outperform RoW in the near-term. We would consider longs in VIX or VIX products as well as SPX puts/put spreads to hedge any near-term downside.

MKT INTEL’S BULL v. BEAR

· BULL CASE – (i) Resilient Macro Data – last week’s Flash PMIs pointed to potentially accelerating economic growth, the report suggests an increase from 1.3% to 2.3%. Next, NFP needs to stay above 100k. Lastly, the Aug 12 CPI needs to remain relatively tight MoM. (ii) Earnings Growth Prints Above Expectations – with 38% of the SPX reporting this week including 4 Mag7 names,, we should be able to confirm support for the hypothesis. (iii) Trade Rhetoric Thaws – the US / JPN deal and potential for US / EU deals helped improve investor sentiment. (iv) Buybacks Come in Size – we could see buybacks exceed $500bn for 25H2, which would push FY25 buyback above $1T exceeding FY24’s record of ~$943bn. (v) M&A Provides an Ancillary Boost – The JPM Global M&A Outlook is here. The team tell us that 25H1 had $1.1T in announced volume, +13% YoY, with 31% in the Tech sector. 60% of deals were sized $1bn - $10bn. Sponsor activity continues to build, increasing expectations for 25H2. As of 25Q2, PE companies held more than 12.5k companies in inventory, which would be 7 – 8 years of exits at current pace but distributions are slowing, and returns are strained by elongated holding periods.

· BEAR CASE – (i) Stronger Tariff Headwinds – while we are not debating the presence of a tariff headwind the magnitude of such tailwind needs to materialize quickly if the market is going to roll over. This would likely be a combination softer NFP and a hawkish CPI print. (ii) Pain in Corporate America – Bears will need to see a spike in earnings misses and/or more companies will need to negatively guide or remove guidance. In 25Q1, beats were not rewarded but misses were punished; we had see misses punished more harshly only three times over the previous 10 years, based on one-day SPX moves. (iii) Trade War Escalation – though there are expectations of US deals with both China and the EU, a failed deal could lead to a tariff spike that is implemented immediately given the expiration of the Aug 1 deadline (and Aug 12 for China). The market is viewing tariffs of 15%, or less, as a positive and anything above 25% as a negative. So, a failed negotiation that led to Trump setting nominal tariffs at say 50% would be viewed as a negative, especially if the market believed that the tariff level had permanence. (iv) Bond Yields Spike / Liquidity Risk – some of this risk comes from hawkish inflation data but there are some fears that the TGA refill will reduce liquidity and could also see a rise in yields in the back of the curve. Further, any additional fiscal spend could upset the bond market’s view on debt sustainability. (v) Valuation – with the SPX trading at 22.4x on a forward P/E basis some investors may conclude that there are better opportunities ex-US especially if the USD remains weak or the market tilts more strongly toward the Value factor. Regarding the Value factor, traditionally the US has trailed international indices given the heavy presence of Tech.

BY Doug Kass · Jul 28, 2025, 11:05 AM EDT

From Peter Boockvar:

Whether we agree or not with the use of tariffs and the deals announced, we are getting the big ones out of the way which will allow American businesses to adjust and plan, for better or worse. And we can now focus on how this all plays out. GDP growth in the first half of 2025 averaged about 1% in the US and we of course now watch to see how the economy responds to more tariff clarity in the 2nd half, but still the impact of them. Up until now, the only thing markets have cared about is getting deals done, regardless of complexion and now maybe we get to shift the focus to the real life impact of the details. We now await what comes of the China talks, most likely something resembling the 2018-2020 talks I’m guessing at this point.

With respect to earnings, Factset updated us on Friday and said "About one-third of the way through the second quarter earnings season, the S&P 500 is reporting somewhat mixed results. On the one hand, the percentage of S&P 500 companies reporting positive earnings surprises is above average levels. On the other hand, the magnitude of earnings surprises is below average levels."

I'll add this from my friend Barry Knapp from Ironsides Macroeconomics who wrote in his weekend note published on Substack, "If we remove the technology and communication services sectors to get a read on consumption and investment outside of the artificial intelligence boom, earnings are tracking a paltry .8% and sales growth is 3.1%. That level of sales growth suggests nominal GDP was quite soft in 2Q."

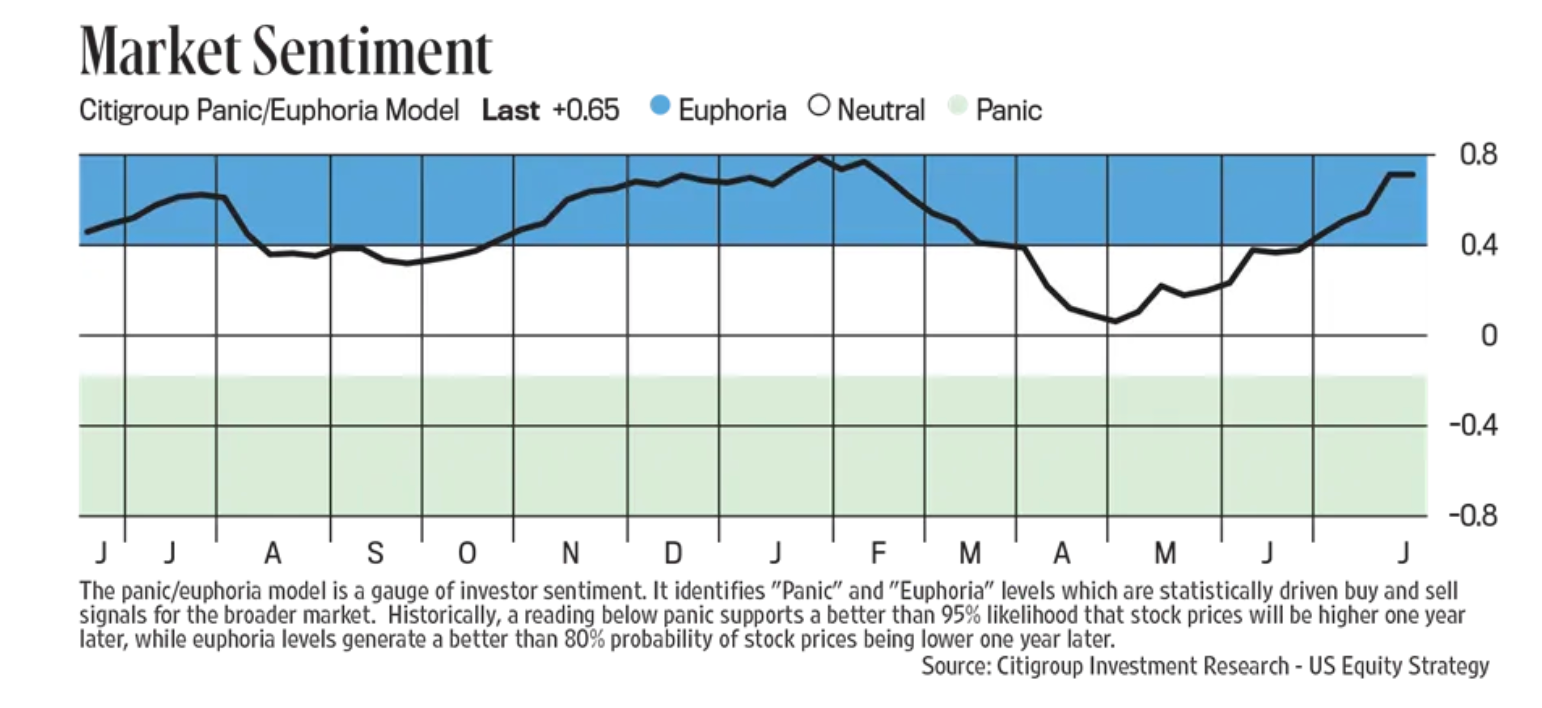

With regards to stock market sentiment, the updated Citi Panic/Euphoria index is getting further Euphoric at .65 vs .49 last week and nearing the highs seen in January/February. For reference, the Euphoria threshold starts at .41 so we are thus well above that. According to Citi, "Historically, a reading below panic supports a better than 95% likelihood that stock prices will be higher one year later, while euphoria levels generate a better than 80% probability of stock prices being lower one year later." After an amazing run off the April low, we take note.

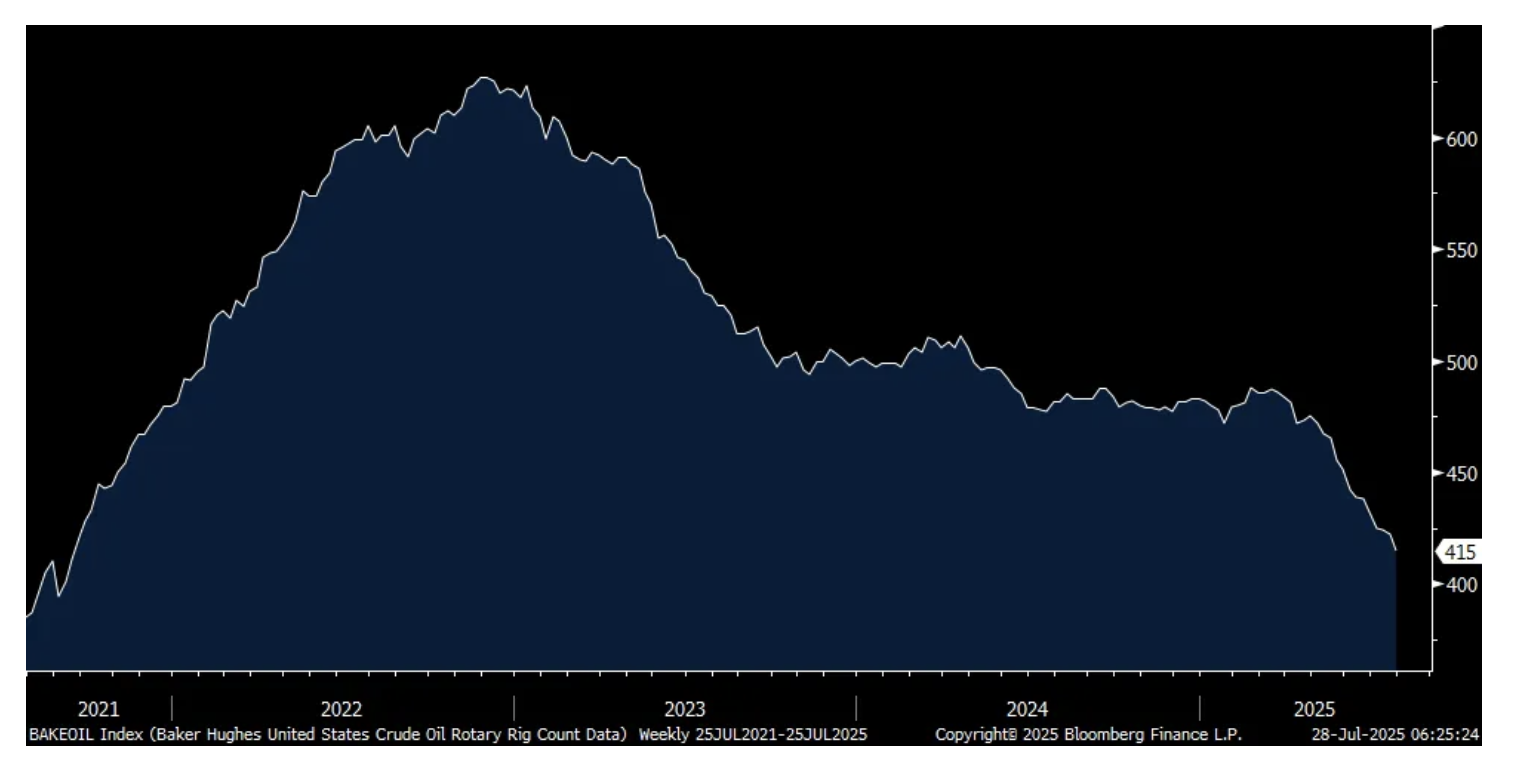

I will talk oil prices again because the US crude oil rig count fell for the 13th straight week and by 7 more rigs to 415, down 60 rigs over these three weeks and the least since mid September 2021. While US drillers are certainly much for efficient, I see it inevitable that US oil production will decline this year. Thus, I think oil price are cheap in the mid $60s and remain long oil and gas stocks.

Crude Oil Rig Count

Here are some notable quotables from earnings reports late last week:

From Weyerhauser, the largest private landowner in the US, producer of timberland/lumber/finished wood products, and a stock we own:

"After a reasonably solid first quarter, housing starts have softened over the last few months, total starts averaging 1.3 million units on a seasonally adjusted basis in the second quarter. And single family starts below 1 million units. While the broader economy appears to be holding up reasonably well, the combination of weaker consumer confidence and elevated mortgage rates has been a headwind for housing activity. As a result, the spring building season was softer than we were expecting at the outset of the year, and I suspect we'll continue to see some choppiness in the housing market in the near term."

"Based on conversations with our homebuilder customers, the biggest issue right now is consumer confidence and general uncertainty around trade policy, inflation, and unemployment. That said, there are potential catalysts for improvement in the second half of the year. For example, we now have clarity on the tax bill, and we could see additional trade deals emerge in the coming days and week, providing more certainty around trade and tariff policy. We might also get some support from the Fed on interest rates later this year."

"Turning to the repair and remodel market, activity has been softer year-to-date relative to 2024, largely driven by many of the same factors impacting the residential construction market. In addition, R&R activity continues to be impacted by lower turnover of existing homes, given higher mortgage rates and the lock-in effect. In the near term, we'll likely continue to see a more muted R&R environment until consumer confidence improves and interest rates move lower."

From Mohawk Industries, the floor covering company and whose stock rose 4% Friday:

"A dominant trend across our geography is consumers' deferral of large discretionary purchases, which has reduced demand in our industry for almost three years. Geopolitical events, inflation, and low housing turnover are contributing to market uncertainty that is limiting residential remodeling and new construction. The commercial channel continues to outperform residential. However, the architectural billings index in the US is forecasting slowing conditions."

In dealing with tariffs, "We have begun to address the implemented tariffs through price adjustments and supply chain optimization."

How much are they going to raise prices? "We've announced 8% increases that we are implementing in the market as we speak. The industry will have to increase further with higher tariffs. There's currently some delays on impact with inventory in the system, and we're obviously also reviewing other alternatives to optimize our supply chain to compensate for the tariffs." I bolded to emphasize and we saw in the June CPI report big m/o/m price increases in most things related to the home, including floor coverings.

From AutoNation and whose stock rose 1.5% Friday:

"As was the case with the industry, our unit sales growth was strongest at the start of the quarter and moderated in May and June. And clearly there was a pull ahead of sales in late March and April in reaction to the tariff announcement, and it stands to reason that some portion of that demand was pulled ahead from the latter part of the second quarter."

"Now I know tariffs continue to be top of mind, and apart from the volume shifting I mentioned earlier, we saw limited additional impact in our Q2 results from tariffs. MSRP and invoice prices have been stable, and the June CPI report showed continued modest m/o/m declines in new and used vehicle pricing." I'll add, what was not mentioned is what I'm hearing from some dealers is that they are trying to offset tariffs in other ways like higher financing costs, tweaks to warranty deals and higher service/maintenance prices.

"We believe the objective of maintaining market share, particularly in critical segments will operate equally with the desire to offset any new tariffs and as I've said previously, we expect that AutoNation to some extent will be cushioned from many new tariffs by a cross shopping effect, whereby demand for non-impacted or lesser impacted brands and models will potentially support those for more effected counterparts. And naturally, in this situation, we hold both sides of the trade with our broad portfolio of brands and models, which I think gives us a distinct advantage."

That said, "you will see price increases in the marketplace, but very, very measured and very, very deliberate."

From Lear, who makes a variety of different auto parts and whose stock fell 8% Friday:

With respect to global vehicle production, "Production volumes declined by 3% in North America and by 2% in Europe, while volumes in China were up 9%."

"Over 90% of our direct imports from Mexico and Canada comply with USMCA requirements and therefore remain exempt from automotive tariffs. Based on the current tariff policies and volume expectations, our gross tariff exposure is approximately $210 million for 2025."

"Trade policies continue to evolve and could change our exposure over time. For example, the implementation of tariffs on copper and the increase in rates for steel could impact commodity prices. For copper, we purchased approximately 200 million pounds per year and have index and scrap recovery agreements that are intended to cover approximately 90% of our exposure. For steel, we purchased approximately 3 billion pounds per year. As with copper, approximately 90% of our steel exposure is indexed."

As for guidance, "At the midpoint of our guidance range, we assume that global industry production will be flat compared to 2024 or down 2% on a Lear sales weighted basis, driven primarily by lower volumes in our two largest markets, North America and Europe."

From SAIA, the trucking company and whose stock rallied 7% Friday after they beat reduced expectations:

Second quarter revenue fell .7% y/o/y "due to continued muted volume trends as a result of the macroeconomic landscape. Overall, shipments per workday were down 2.8% y/o/y."

"While we continue to see strong results in our newer markets, the overall shipment trends reflect a continued cautious approach from customers amidst an ever changing economic landscape."

From Deckers Outdoor, the maker of HOKA and Ugg and whose stock rallied 11% Friday:

"HOKA delivered its largest quarter in its history, driving strong sell throughs during this period of key model transitions."

"The strength of our business continues to be driven by the remarkable growth in our international markets, with HOKA and UGG both contributing to Decker's 50% increase in international revenue, while navigating a choppy US consumer environment."

"On tariffs, we are still awaiting final details, but based on the recent updates, assuming Vietnam increases 10% to 20%, we would expect to face a total of $185 million of unmitigated impact to our cost of goods sold in fiscal year 2026, up from our previously provided estimate of up to $150 million. As we said last quarter, we put in measures to recapture up to approximately $75 million, and we'll continue to evaluate additional levers for potential further mitigation."

"One of our mitigating levers is price adjustments. Since our last call, the majority of these have been communicated, and I would note that we have not seen any material changes to our order book resulting from these increases." My bold.

BY Doug Kass · Jul 28, 2025, 10:50 AM EDT

fishplay

29 minutes ago

I posted the link below after the close Friday. Several watched and found it useful. Since many-including me-take the weekend off and don't look after market closes, I repost this AM if anyone cares to view.

Worthy weekend listen. Good to get views other than the typical one here on this blog. Plus Paulsen makes very many suasive points, and what he says explains much of what the market is doing and why so many here are frustrated trying to be short, hedged, or long puts.

Oh, and my best buddy who has worked with me for decades in the market sent the Paulsen link below. He worked with Paulsen for over five years at WFC and knows him well. Do listen.

BY Doug Kass · Jul 28, 2025, 10:30 AM EDT

From FactSet (h/t Peter Boockvar):

"About one-third of the way through the second quarter earnings season, the S&P 500 is reporting somewhat mixed results. On the one hand, the percentage of S&P 500 companies reporting positive earnings surprises is above average levels. On the other hand, the magnitude of earnings surprises is below average levels."

BY Doug Kass · Jul 28, 2025, 10:15 AM EDT

* Listen to the Bible's Joseph (in Genesis) and not to the price following investment managers and strategists

* Better yet, listen to Warren Buffett (below) as he describes the herd's inevitable acceptance of "God's Plan":

Once a bull market gets underway and once you reach the point where everybody has made money no matter what system he or she followed, a crowd is attracted into the game that is responding not to interest rates and profits but simply to the fact that it seems a mistake to be out of stocks. In effect, these people superimpose an I-can't-miss-the-party factor on top of the fundamental factors that drive the market. Like Pavlov's dog, these "investors" learn that when the bell rings - in this case, the one that opens the New York Stock Exchange at 9:30 a.m. - they get fed. Through this daily reinforcement, they become convinced that there is a God and that He wants them to get rich.

- Warren Buffett, November 1999

The Oracle of Omaha delivered the above quote only a few months before the end of the dot-com boom. By March, 2000 the Nasdaq made a seminal top and commenced on a sutherly route that would cause a -80% drawdown in that Index.

A vivid illustration of the acceptance of "God's Plan" was made in the infamous quote by Citigroup's former CEO Chuck Prince in July, 2007 -- a few months before the Great Financial Crisis which also led to a similar market decline:

"When the music stops, in terms of liquidity, things will be complicated. But as long as the music is playing, you've got to get up and dance. We're still dancing."

In both the Winter of 1999 and in the Summer of 2007 day traders and speculation ran amok and a rising market was an almost accepted part of the zeitgeist.

Conditions today are clearly much different than in 1999 and 2007 - today's market leaders are healthy/profitable companies with deep moats (and not companies with no or limited futures). Regardless, we face a host of secular headwinds that could be more long lasting than at prior market peaks - the most important of which are:

* A rising probability of "slugflation" (prickly inflation, disappointing economic growth)

* Undisciplined fiscal policy by both parties that will likely lead to a continued and large deficit, adding to our nation's debtload

* Valuations that are in the 98%-tile, a poor launching pad for future investment returns

Over the last few weeks the markets have been buoyed by, among other factors, the Administration's "tariff" agreements which have been viewed by market participants as a big net investment positive.

Most recently, the energetic reaction to a series of economically unfriendly tariff announcements and "agreements" are an exclamation point of unbridled and, arguably, poorly analyzed blind political and market enthusiasm. Moreover, the goal posts have been constantly been moved (in attempts to represent tariff policy success).

From John Mauldin ( "Thoughts From The Front Line) over the weekend in "Uncertainties Squared" Uncertainty Squared - Mauldin Economics:

The unjustified bows taken by the current Administration were outlined in The Financial Times late last week:

According to Trump and his administration, in return for a reduction in tariffs, Japan would invest $550 billion in certain U.S. sectors and give the United States 90% of the profits.

Japanese officials, however, say the profit sharing isn’t so set in stone: A Friday slideshow presentation in Japan’s Cabinet Office, contra the White House, said profit distribution would be “based on the degree of contribution and risk taken by each party,” according to The Financial Times.

The FT also reports conflicting messages between Washington and Tokyo as to whether that $550 billion commitment is, as team Trump sees it, a guarantee or, as Japan’s negotiator Ryosei Akazawa sees it, an upper limit and not “a target or commitment.”

Mireya Solís, a senior fellow at the Brookings Institution, told The Financial Times that the deal contains “nothing inspiring,” and that “both sides made promises that we can’t be sure will be kept” and “there are no guarantees on what the actual level of investments from Japan will be.”

The inconsistent interpretations of the deal could be because it was hastily pulled together over the course of an hour and 10 minutes between Trump and Akazawa on Tuesday, according to the FT, which cited “officials familiar with the U.S.-Japan talks.” And, moreover, “Japanese officials said there was no written agreement with Washington—and no legally binding one would be drawn up.”

Does Trump’s so-called “largest deal in history” even count as a deal at all? Brad Setser, senior fellow at the Council on Foreign Relations,

We will examine the other concerns I have later in this missive.

I continue to be of the view that after seven years of prosperity and abundance - we will likely face seven lean years of famine in the markets:

"In the Bible, 'lean years' refer to a period of famine that follows a time of abundance, particularly in the story of Joseph in Genesis 41. The prophecy, revealed through dreams to Pharaoh, foretold seven years of great plenty in Egypt, followed by seven years of severe famine. Joseph, interpreting the dream, advised Pharaoh to prepare for the lean years by storing grain during the period of abundance. This preparation allowed Egypt to survive the famine while other surrounding lands suffered greatly."

Ten days ago I wrote the following, in Kids Today - the zeitgeist today is similar to that 26 years ago near the end of the dot.com boom:

Five weeks ago I wrote about my broader concerns:

JUN 13, 2025 9:30 a.m. ET: Goodbye Goldilocks (Hello Reality)

* Yesterday's domestic and international developments underscore the many possible adverse market outcomes...

* As equities fall and the price of crude oil rises (+9%)

* The 'Long Boom Curse' may apply today!

The obscure we see eventually. The completely obvious, it seems, takes longer.”

- Edward R. Murrow

Following a remarkable climb in equities since early April, it is being argued by a growing body of market participants that a new bull market leg has emerged, coincident with a virtuous economic and corporate profit cycle that may lie ahead: "Carson Group: Welcome to the Start of a New Bull Market?"

It should be emphasized that many of the newly minted bulls were actually scared shitless during the first week of April. They are the most optimistic today -- reminding us of The Divine Ms. M's (Helene Meisler) quote:"There is nothing like price to change sentiment."

I strenuously disagree with the newly minted market optimism. In fact, it is my view that not since Wired Magazine's ill-timed late 1990s cover story "The Long Boom: A History of the Future, 1980-2020" ( authored by Peter Schwartz and Peter Leyden) has a new investing paradigm been forecast:

“We’re facing 25 years of prosperity, freedom, and a better environment for the whole world. You got a problem with that?”

Of course that remarkably upbeat (but wrong footed) column was followed quickly followed by a -80% drawdown in the Nasdaq Index!

To me, the "Long Boom Curse" probably also applies today!

In yesterday's market update (Downside Market Risk Is About 5-Times Upside Reward) I make the opposite case -- that there is no new investing paradigm ahead as we could not only face seven lean months over the balance of 2025 but, perhaps, another 6.5 lean years after that.

To summarize some of my concerns:

* We face the highest geopolitical risks in many decades (which will not be resolved quickly).

* We face the largest level of social and political risks in the U.S. since the Vietnam war.

* We face the greatest chance of "slugflation" (slowing economic growth and sticky inflation) since the 1970s.

* We face the biggest threat that the U.S. dollar and capital markets will no longer be a "safe haven" in modern history.

See: NDR: Breakdown for U.S. dollar?

* We face the greatest debt load and deficit ever -- and neither party seems to favor any fiscal discipline whatsover.

* We face the largest capital spending spree in history (on artificial intelligence) -- though the return on that investment is less certain (dot.com, it feels like deja vu all over again.)

* We face a viable alternative to equities in fixed income (for the first time in 15 years) as bonds present an equity-equivalent yield with limited risk and volatility.

As I have also noted, what is most surprising is that market enthusiasm has multiplied at a point of time in which price-earnings multiples are at an elevated 22-times. Here are some snippets from my Thursday column, which support my more ursine view, which is backed by rising, not declining uncertainties:

My commentary today is decidedly downbeat – some might even say dystopian. But I think my concerns are largely justified. Importantly, with markets trading at a 22-times forward price earnings multiple there is little room for disappointment.Indeed, it is my view that adverse outcomes are likely to become more common place in the time ahead – witness the recent juvenile and angry Elon Musk/Pres. Trump exchanges. Never in my investing career has there been so many possible social, political, geopolitical, economic, interest rate and fiscal policy outcomes. Many of these possible outcomes could easily upset overvalued markets. Based on my calculus and scenario analysis, the market’s downside risk is roughly 5-times the market’s upside reward -- this is the worst ratio since late 2021...

Unfortunately, Americans continue to be exposed to unvarnished political self-interest, the continued loss of conventions and general lack of ethics and morals. (As an example is the insider trading of our Congressional members, right in front of our eyes). It is increasingly obvious that political positions of influence can easily be bought — sold by both Democrats and Republicans. To this observer, fewer and fewer politicians are even pretending that they care about the American people. This may help to explain the capital outflows out of the U.S. and that many (including ourselves) are "Rethinking American Exceptionalism." (Consider what the world outside of the U.S. thinks of us these days).

As dark as all this is, my concerns relate to both parties. The Republican party has its own set of issues while Democratic leadership doesn't even seem to exist — making the situation rather sickening. This concerning condition has real economic and investment consequences, most importantly as reflected in the continuing lack of fiscal discipline and unwillingness to address our country's debt load. I express this reality and these conditions not as political statements, but rather as economic and investing considerations. It is highly unlikely that any politician on either side of the pew will address our progressively and steadily deteriorating financial position. At this point, if they did recommend some hard decisions, they would likely be voted out of office. There are simply too many forces inside the government opposed to cutting spending to produce meaningful results -- just look at the resistance to DOGE.

Whether the "big, beautiful bill" increases or decreases the deficit by a few trillion dollars has now lost its relevance. We have already lost the ability to control the deficit -- as the total federal debt load is now projected to be nearly $50 trillion in 2030 and over $70 trillion by 2040. The harsh truth is that it is getting almost too late to dent the deficit (and the arc toward an erosion in U.S. solvency) without radical changes in non-discretionary spending and/or taxation requiring austerity and large tax increases (which would trigger a severe recession). As a consequence of the above factors (and other influences) interest rates will stay higher for much longer -- an unfriendly condition for future price earnings ratios (as interest rates are at the core of all equity valuation models). Additionally, higher interest rates (and deficit neglect by our representatives in Washington, D.C.) will result in sharply rising costs of servicing our burgeoning debt load.

Bottom Line

* Political and geopolitical polarization and competition will probably translate into less political centrism and a reduced concern for deficits — creating structural uncertainties, limited fiscal discipline and imprudence around the globe ... and for the possibility of bond markets to "disanchor."

* The cracks in the foundation of the bull market are multiple and are deepening, but they are being ignored (as market structure changes have led to price momentum (FOMO) being favored over value and common sense).

* With the S&P 500 Index at around 6000, the downside risk dwarfs the upside reward for equities — in a ratio of about 5-1 (negative).

* Valuations (a 22-times forward Price Earnings Ratio) and (consensus) expectations for economic and corporate profit growth are all inflated.

* Being dismissed are JPMorgan CEO Jamie Dimon's and others’ dour comments on complacency and a view that the corporate credit market is "ridiculously over-stretched.”

* Look for the soft data (see last week's weak ISM and climb in jobless claims) to move into (and weaken) the hard data led by a slowing housing market likely to provide ample near-term evidence of the exposure and vulnerability of the middle class.

* Below trend-line economic growth (housing will lead us lower) coupled with sticky inflation lie ahead ("slugflation") — uncomfortable for a Federal Reserve which has to make increasingly more difficult decisions.

* Corporate profit growth (rising +13% in first quarter 2025) will markedly decelerate in this year’s second half.

* The equity risk premium is at a two-decade low - typically consistent with a slide in equities.

* The S&P Dividend Yield is at a near record low of 1.27% - and the spread between the dividend yield and the 10-year U.S. Treasury note yield has rarely been as wide. With so many possible adverse outcomes, my baseline expectation is for seven lean months ahead over the balance of 2025.

BY Doug Kass · Jul 28, 2025, 9:45 AM EDT

I took a small profit in last night Index (common shorts) - covered just now:

* SPY $637.68

* QQQ $567.72

On strength I plan to add to my Index calls shorts today.

BY Doug Kass · Jul 28, 2025, 9:20 AM EDT

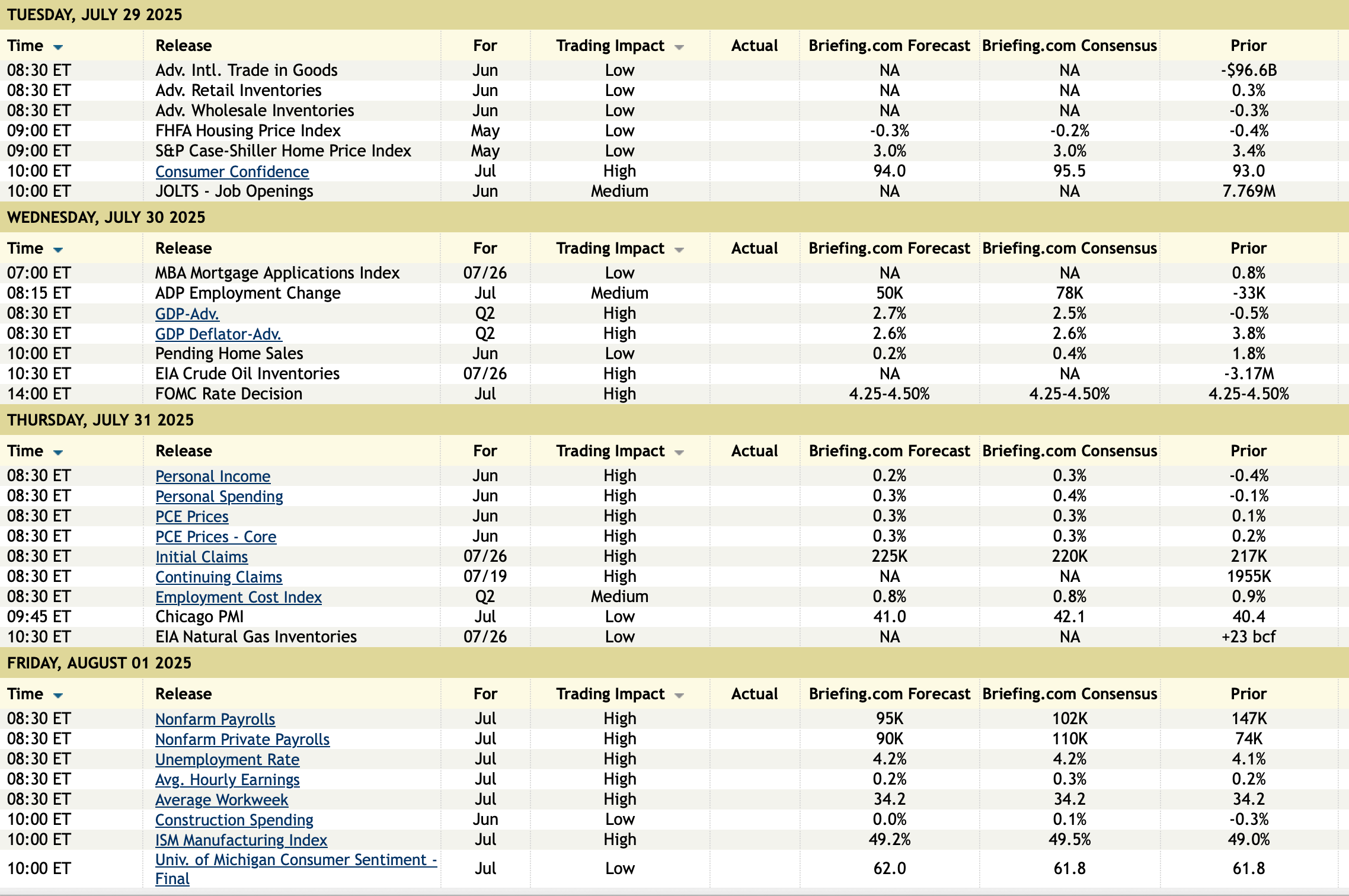

10:30 a.m.: Dallas Fed Manufacturing Activity (July);

TREASURY AUCTIONS FOR TODAY

11:30: Treasury hosts a $82B 3 and $73B 6-Month Bill Auction;

11:30: Treasury hosts a $69B 2-Year Note Auction;

1:00 p.m.: Treasury hosts a 70B 5-Year Note Auction; 3:00 p.m.: Treasury's Financing Estimates

ECONOMIC CALENDAR FOR REMAINDER OF WEEK

BY Doug Kass · Jul 28, 2025, 9:17 AM EDT

BY Doug Kass · Jul 28, 2025, 9:15 AM EDT

BY Doug Kass · Jul 28, 2025, 9:06 AM EDT

-CELC +205% (announces positive topline results from PIK3CA Wild-Type Cohort of Phase 3 VIKTORIA-1 Clinical Trial)

-LIDR +16% (launches OPTIS, a full-stack, flexible lidar solution designed to transform how customers across industries perceive and respond to their unique environments)

-MAIA +11% (receives FDA Fast Track designation to ateganosine for NSCLC)

-STXS +11% (receives FDA 510(k) clearance for MAGiC Sweep, the world’s first robotically navigated high-density EP mapping catheter)

-ZYME +10% (announces FDA Clearance of Investigational NDA for ZW251, a Novel Glypican 3-Targeted Topoisomerase 1 Inhibitor Antibody-Drug Conjugate)

-ENTX +9.0% (receives FDA Agreement on BMD as Primary Endpoint for EB613 Registrational, Phase 3 Study in Post-Menopausal Women with Osteoporosis)

-WRD +7.5% (company’s Robotaxi was granted Saudi Arabia's first Robotaxi autonomous driving permit)

-PD +6.1% (TD Cowen Raised PD to Buy from Hold, price target: $22)

-PONY +6.1% (among the first to receive permit for Fully Driverless Commercial Robotaxi Services in Shanghai’s Pudong New Area)

-VG +5.4% (momentum)

-NKE +4.0% (JPMorgan Chase and Co Raised NKE to Overweight from Neutral, price target: $93 from $64)

-ASML +3.8% (strength following announcement that Samsung will produce semiconductors for Tesla, key customer for ASML)

-LNG +3.8% (EU commits $250B annually to liquefied natural gas purchase)

-LENZ +3.4% (announces NMPA Submission of New Drug Application for LNZ100 in China for the Treatment of Presbyopia)

-AREC +3.3% (oil strength following US/EU trade deal)

-RVTY -6.0% (earnings, guidance)

-ARLP -3.4% (earnings, guidance)

BY Doug Kass · Jul 28, 2025, 8:52 AM EDT

I re-entered a short in SPY and QQQ common.

About 8 p.m. last night:

* SPY $639.21

* QQQ $569.00

BY Doug Kass · Jul 28, 2025, 6:36 AM EDT

* Technicians are now giddy...

Bonus — Here are some great links:

(Jazzy Jeff) August Has Been Even Weaker in Post-Election Years

Stock Market and Crypto Analysis

BY Doug Kass · Jul 28, 2025, 6:10 AM EDT

The S&P Short Range Oscillator shifted higher — to 1.90% (overbought) vs. 0.32%.

BY Doug Kass · Jul 28, 2025, 5:55 AM EDT

Wolf Street howls about the La-La-Land of loose monetary policy.

BY Doug Kass · Jul 28, 2025, 5:45 AM EDT

If something like this is not "papered" it isn't really a deal. My two cents 3/3 ft.com/content/c1183b…