From Peter Boockvar:

Positives,

1) The US July services PMI did rise to 55.2 from 52.9, though does not include wholesale and retail trade and construction too.

2) Initial jobless claims fell to 217k from 221k and that was 9k below expectations. The 4 week average dropped by 5k w/o/w to 225k. Continuing claims were as expected at 1.955mm, up 4k w/o/w, though remaining elevated.

3) The US and Japan struck a deal framework on trade.

4) The pace of existing home sales (measuring closings) in June continued to hover around the slowest rate since 1995 at 3.93mm annualized, 70k less than expected and vs 4.04mm in May. First time buyers totaled 30% of purchases which has been around the multi year trend but remaining low because of the affordability challenges we know all about. Months’ supply rose to 4.7 from 4.6 and that matches the most since November 2015 as supply in certain markets is slowly beginning to pick up. The median home price was up 2% and a needed moderation in the pace of gains, helped by that inventory increase relative to sales. The NAR said “Multiple years of undersupply are driving the record high home price. Home construction continues to lag population growth. This is holding back first time home buyers from entering the market. More supply is needed to increase the share of first time homebuyers in the coming years even though some markets appear to have a temporary oversupply at the moment.”

5) After a jump in mortgage applications ahead of July 4th and then a fall back, they were flattish w/o/w. Purchases though did rise by 3.4% while refi's dropped by 2.6%.

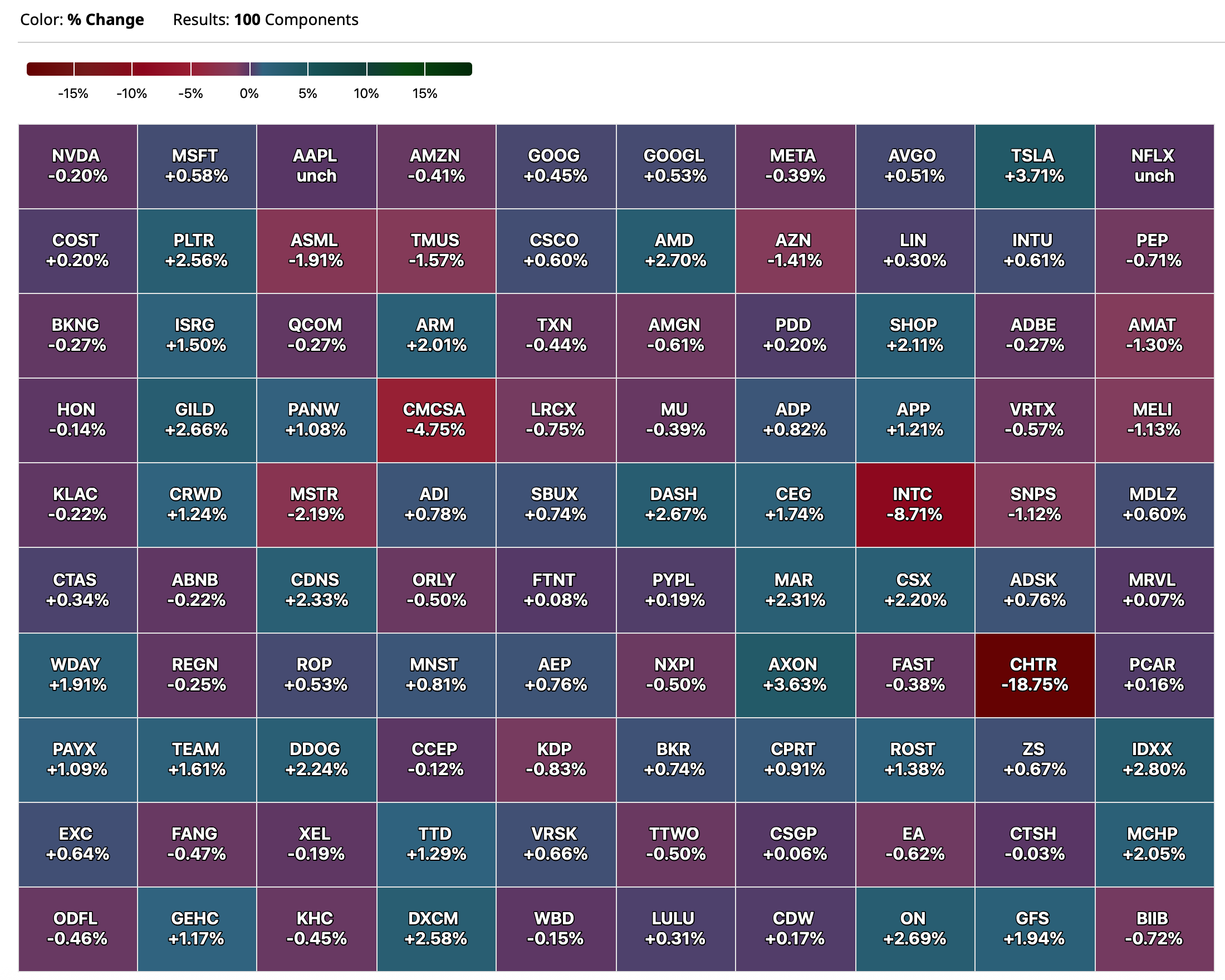

6) From Google/Alphabet: "The 12% increase in Search and other revenue was led by growth across all verticals, with the largest contributions from retail and financial services. YouTube saw similar performance across verticals. Its 13% growth in advertising revenue was driven by direct response, followed by brand." With Google Cloud, revenues were up 32% y/o/y with the help of course by its AI offerings. With guidance, "given the strong demand for our Cloud products and services, we now expect to invest approximately $85 billion in CapEx in 2025, up from a previous estimate of $75 billion. Our updated outlook reflects additional investment in servers, the timing of delivery of servers, and an acceleration in the pace of data center construction, primarily to meet Cloud customer demand. Looking out to 2026, we expect a further increase in CapEx due to the demand we're seeing from customers as well as growth opportunities across the company." We all hope at that spend of 25% of revenues is worth it.

7) From Robert Half: To fears that GenAI is going to take all of our jobs, "First of all, we know definitively that so far, AI has had very little impact on our revenues. We did a deep dive. We took it all. We took all the roles that were identified by the World Economic Forum as most vulnerable. They would include things like data entry, bookkeeping, customer service, the ones you always read about. And our data says that so far, they haven't performed any differently than the other roles." More, “Interestingly, the NFIB just did a technology survey of its constituents, 98% reported that AI had no impact to their number of employees. There are other studies that have come out recently, the National Bureau of Economic Research being one of them. That has concluded so far, no association between AI and jobs growth with the possible exception of tech companies that you read a lot about. But part of that, they're selling their own book. And so, at least so far, when you look at the staffing industry and Robert Half specifically, we can say AI has not impacted how we've performed. Now as to the future, there are opinions all over the lot. We would say that historically, the staffing industry has been great about being very fluid and pivoting to where the jobs and the skills are."

8) From LVMH: "The start of the year has been disrupted by several layers of macro uncertainties, as you are well aware, as well as currency swings impacting short term performance, albeit with a pocket of resilience. More specifically, we saw solid local demand in Europe and in the US, and a tangible sequential improvement when it comes to Mainland China in the second quarter. In addition, we saw very abrupt currency swing in Q2, which eroded the purchases of American and Chinese consumers abroad, and especially in Japan, where we faced a very abnormal growth of 57% in the same period last year."

9) From Tractor Supply: "Despite ongoing macroeconomic uncertainty and a tepid start to spring, our sales performance exceeded our modest expectations. This performance reflects continued strength in our core needs based categories and share gains across key seasonal businesses…we saw sequential comp sales improvement across the quarter. Each period performed better than the one before it, and that momentum has continued into early Q3."

10) From American Airlines: "Premium demand and spending from higher income consumers remained resilient in the second quarter. On a y/o/y basis, unit revenue in the premium cabin performed 4 points better than the main cabin."

11) From Keycorp: “Within C&I, the growth continues to be broad based across industries and regions with both large institutions and middle market clients. Most of the growth was from new clients to Key. C&I line utilization picked up approximately 50 bps to 32%. The CRE growth was primarily driven by project based deals in affordable housing, traditional multifamily and data centers.” On their customers, “Our consumer is just fine. Just a reminder, our consumers have a FICO score of about 767. And so as you look at how the credits are performing, if you look at how spending volumes are performing, our clients are in good shape. I think one of the things that the models really fail to pick up is the wealth effect and the fact that household wealth in the US over the last 15 years has increased by about $100 trillion and that’s not inconsequential.” On their commercial customer, “I think balance sheets are healthy. Their liquidity is in good shape.” Also, “We perform a very detailed survey on 850 customers that borrow $10 million or more. 50% of them think that the current environment is an opportunity for growth. As it relates to tariffs, because that’s always a topic for everyone, 30% of our customers are impacted by tariffs, but here’s the interesting thing. Of the $56 billion that we have outstanding in C&I, only 3% are significantly impacted in a direct way by tariffs.”

12) From Capital One: "So the US consumer is in a great place here that we continue to see the US consumer as a source of strength in the economy. The unemployment rate remains low and stable, job creation remains healthy, real wages are, of course, growing steadily. Consumer debt servicing burdens remain stable and near pre-pandemic levels. In our card portfolio, we're seeing improving delinquency rates and lower delinquency entries. And payment rates are improving on a y/o/y basis. Now of course, the circumstances of individual consumers and households will vary, as they always do…And as we've mentioned in past earnings calls, some pockets of consumers are feeling pressure from the cumulative effects of inflation and higher interest rates. And we're still seeing some delayed charge-off effects from the pandemic, although the improving trend in our delinquency suggest these effects are moderating. But on the whole, I'd say the US consumer is in really quite good shape. And of course, like all of you, we're keeping a close eye on the potential impact of tariffs and other public policy changes."

13) From Zions Bancorp: "While we see some signs of economic slowing, the magnitude and imminence of tariff related risks noted in our first quarter call feel like they've abated somewhat. As a result, we are incrementally more sanguine about potential growth in our outlook."

14) From AmEx: "Total card member spending was up 7%, which was consistent with the pattern we've seen this year, while spend in some of the travel categories, like airlines and lodging, was softer overall. Spending was a quarterly record." More on this, "We live in uncertain times, but I think people are continuing to live their lives. And what we're seeing right now is very consistent spending. You're seeing a little bit of a slowdown in airline, not necessarily front of the cabin. You're seeing a little bit of a slowdown in lodging, but again, not necessarily on the high transactions, which are up. But goods and services continue to be resilient and our GenZs and our millennial’s continue to be consistent." They said "restaurant spending continued to be very strong, up 8% FX adjusted."

15) From GM: “In the US, the industry saw a spike in demand during the quarter due to tariff related sales pull ahead, especially in April and May. Then in June and July, demand returned to levels that are in line with our full year outlook of 16 million units.”

16) From Coca Cola: Specifically on their North American market, "The aggregate spend is holding up. Yes, there's some pressure in those with lower incomes where we're targeting some affordability and some special focus on marketing and occasions. So I think the overall outlook continues to be resilient and we're investing for growth in that."

17) From Lamb Weston: “Volume was up with wins across channels and geographies, and net sales grew. Price/mix declined, reflecting our support of customers with price and trade as we manage the competitive environment and soft restaurant traffic.”

18) The German July IFO business confidence index rose to 88.6 from 88.4, the best since May 2024, though below the estimate of 89. Notwithstanding the uptick, the IFO said "The upturn in the Germany economy remains sluggish."

19) Here are the overseas PMIs which mostly showed slight improvement. Japan: manufacturing 48.8 vs 50.1, services 53.5 vs 51.7. Australia: manufacturing 51.6 vs 50.6, services 53.8 vs 51.8. India: manufacturing 59.2 vs 58.4, services 59.8 vs 60.4. Eurozone: manufacturing 49.8 vs 49.5, services 51.2 vs 50.5. UK: manufacturing 48.2 vs 47.7, services 51.2 vs 52.8.

20) Specifically in the Eurozone, S&P Global said "The Eurozone economy appears to be gradually regaining momentum. The recession in the manufacturing sector is coming to an end, and growth in the services sector accelerated slightly in July."

Negatives,

1) The US S&P Global manufacturing PMI fell back below 50 at 49.5 from 52.9. For the overall index, including services, S&P Global said “Business confidence about the year ahead has also deteriorated in both manufacturing and services to one of the lowest levels seen over the past 2 ½ years. Companies cite ongoing concerns over the impact of government policies, notably in terms of both tariffs and cuts to federal spending.” This too, “Price pressures intensified across both manufacturing and service sectors during July, widely blamed on higher goods prices due to tariffs but also in some cases due to rising labor costs. Average prices charged for goods and services rose at a rate just shy of May’s recent high to register the second-strongest monthly increase since September 2022. Services price inflation accelerated to register the second steepest increase since April 2023 and, although factory gate selling price inflation eased, the rise in charges for manufactured goods was the second largest since November 2022. Input cost inflation also picked up again, having eased slightly in June, registering the second-steepest rise since January 2023. The rate of input cost inflation remained especially sharp in manufacturing, despite cooling compared to June’s post-pandemic peak, and accelerated in services. Close to two-thirds of all manufacturers reporting higher input costs attributed these to tariffs, whilst just under half of respondents explicitly linked their increased selling prices to tariffs. However, the tariff impact was by no means limited to factories, as around 40% of service providers reporting higher selling prices explicitly mentioned tariffs.”

2) It looks like the baseline tariff rate will be about 15%, around a 100 year high.

3) The July Richmond manufacturing index fell to -20 from -8. The KC index was +1 vs -2.

4) While an improvement from June, the July Philly services index was -10.3.

5) June core durable goods orders retreated by 7 tenths m/o/m after a 2% jump in May. That was below the estimate of a one tenth increase, partly offset by a 3 tenths upward revision to last month. Related to the AI/data center buildout, electrical equipment orders were up 9.2% y/o/y, computers/electronics higher by 5.4% and machinery up by 5.3%. Auto orders were up by .9% m/o/m but by just 1.3% y/o/y. Core durable goods orders are up 1.3% in the first half of 2025 from the December 2024 level and that is in nominal terms.

6) The June US Architecture Billings Index fell a touch to 46.8 from 47.2 in May with 50 the expansion/contraction breakeven. AIA chief economist said “Business conditions were soft nationwide in June, with a slight billing increase in the South for the first time since October. Other regions saw declining billings, though at a slower pace. While all specializations experienced softer billings, the decline slowed for commercial/industrial and institutional firms. Multifamily firms faced the weakest conditions, with further declines.”

7) New home sales in June totaled 627k, little changed from the 623k seen in May and below the estimate of 650k.

8) From Robert Half: "Elevated global economic uncertainty persisted throughout the quarter, extending client and job seeker caution, elongating decision cycles and subduing hiring activity and new project starts. Revenue levels fell modestly during the first two months of the quarter, then stabilized at lower levels in June, which continued post quarter into July." They have a division called Protiviti that is a consulting firm and in this division, "growth rates have moderated as a result of continued economic uncertainty. This has extended conversion timelines from opportunity identification to project start and reduced average project size."

9) From Chipotle: Comps fell 4% y/o/y. "While we experienced a slowdown in our underlying trend in May, we did see momentum build as we rolled out our summer marketing initiatives and leaned into hospitality. And exiting the quarter, we returned to a positive comp and transaction trends, which have continued into July…However, considering the ongoing volatility in our trends in the consumer environment, we now anticipate comparable sales to be about flat for the full year…July has been a bit choppy over the last couple of weeks. I think it's due to kind of some post holiday as well as some weather that we've seen." Also, "I think much of what we're experiencing right now is due to macro and the low income consumer is looking for value as a price point. At present you have to look no further than what's going on with our competitors with snack occasion or $5 meals and that's where the consumer is drifting towards as value as a price point because of low consumer sentiment."

10) From Domino’s: “Our second quarter financial results continue to be impacted by a challenging macro backdrop…we continue to expect our US comp for the year to be 3% and that it will be higher in the 2nd half due to the timing of our initiatives. This assumes that the pressured macro environment we have seen through the first half of the year in QSR pizza remains the same.”

11) From Tootsie Roll: "Many companies in the consumer products industry have increased selling prices in order to improve price realization in response to increasing input costs in recent years. We have implemented price increases as well during this period in order to mitigate certain input cost increases and recover our margin declines. Although we made progress in restoring our margins in second quarter and first half 2025, certain ingredients and packaging materials unit costs, including cocoa and chocolate, have increased in first half 2025 compared to 2024. Cocoa and chocolate markets continue at significantly elevated levels compared to historical prices in past years. As a result, we expect to incur even higher costs for these ingredients during the balance of 2025 and into 2026 as many of our older supply contracts expire and new contracts at higher costs become effective. Although the Company continues to monitor its input costs, we are mindful of the effects and limits when passing on the above discussed higher input costs to our customers as well as the final consumers of our products."

12) From American Airlines: "The strength in international premium was offset by domestic leisure weakness. Domestic unit revenue was down approximately 6% y/o/y as softness in the main cabin persisted throughout the second quarter. While domestic unit revenue is expected to remain lower y/o/y in the third quarter, we expect that July will be the low point and that performance will improve sequentially each month in the quarter as industry capacity growth slows and demand strengthens."

13) From Hilton worldwide: “the quarter turned out to be noisier than expected, driving system wide Rev PAR down 50 bps y/o/y. Performance was driven by continued strength in the Middle East-Africa region and Asia Pacific ex China, but offset by softer trends in the US and China…second quarter comparable US RevPAR decreased 1.5%, largely driven by pressure across business transient and group, as declines in government spend and softer international inbound demand weighed on performance. For full year 2025, we expect US RevPAR growth to be at the lower end of our system wide RevPAR range.”

14) From Hasbro: “As we foreshadowed last quarter, most of our US retailers managed their discretionary inventory tightly through the quarter. While revenue declined, we improved margins, delivering near break even profitability through cost actions, mix and promotional spending discipline…We’ve incurred minimal tariff related expense in our year to date results, as most of the impacted inventory is still sitting on the balance sheet, and is yet to flow through the P&L…We’re also seeing downstream impacts from trade uncertainty across the retail landscape. Many retailers are delaying holiday inventory bills and pushed shelf resets into Q3, both of which weighed on Q2 consumer products revenue and are requiring us to remain agile in the second half.” Finally on pricing, “Now in terms of how tariffs have impacted the category, I think the answer is it hasn’t impacted take away from the consumer that much yet, because usually it takes 5 to 8 months for a toy to go from the factory to the shelf. But I think you started to see some indications that toy prices were starting to creep up in May and June. And we think that will happen slowly and consistently, likely through the balance of the year and into next year. I don’t think you’re going to magically see one day toy prices go from X to Y. I think it’s going to be kind of more line by line, skew by skew. And over several months as the general industry kind of gets a feel for what the consumer can bear.”

15) From Lamb Weston: “In the US, QSR traffic improved from February’s levels but compared with the prior year was down 1% in the quarter and the fiscal year. Traffic at QSR chains specializing in hamburgers was down 2% in the quarter and 3% for the year. It’s important to note that this is on top of declines in the prior year. Restaurant traffic on a two year stack is down mid single digits with QSR hamburger focused restaurants down high single digits over the two year period.”

16) From SAP: “uncertainty in global markets from earlier this year remains, but SAP has an excellent pipeline for half year two in almost all markets and regions…In a few individual industries impacted by uncertainty, we are seeing extended approval workflows on the customer side, for example, in the US public sector and among manufacturers affected by tariffs.”

17) From IBM: "I'll start by saying that we appreciate the administration's priority on economic growth and focused regulation, which will strengthen the US competitive position. We believe this will result in long term value creation and enable technology to contribute to economic growth. Technology continues to serve as a key competitive advantage, allowing businesses to scale, drive efficiencies, and fuel growth, and we saw this play out in the quarter. While not a major factor overall, geopolitical tensions are prompting a few clients to move cautiously. US Federal spending was also somewhat constrained in the first half, but we do not expect it to create long-term headwinds."

18) From Dow and who cut their dividend by 50%: "the prolonged downcycle our industry has been experiencing was further amplified this quarter by heightened trade and geopolitical uncertainties, which have strained profitability across our industry…Additionally, growing signs of oversupply from newer market entrants being exported to other regions at anti-competitive economics requires an aggressive industry response and regulatory action to restore competitive dynamics."

19) From OTIS: With their new equipment business, “In the US, continued uncertainty over global trade policies are causing project delays.” This resulted in them lowering guidance for the Americas to “down high single digits.” Asia is hit too, particularly China to “down low teens.”

20) From Tesla: "The One Big Bill has a lot of changes that would affect our business in the near term. The first among those changes is the repeal of the IRA EV credit of $7,500 by the end of this quarter. Given the abrupt change, we have limited supply of vehicles in the US this quarter, as we have already within lead times to order parts to build cars…we're in this weird transition period, where we will lose a lot of incentives in the US. There's a lot of incentives actually in many other parts of the world, but we'll lose them in the US...On the other hand, autonomy is most advanced and most available from a regulatory standpoint in the US. So, does that mean we could have a few rough quarters? Yes, we probably could have a few rough quarters. I'm not saying we will, but we could. Q4, Q1, maybe Q2. But once you get to autonomy at scale in the second half of next year, certainly by the end of next year, I would be surprised if Tesla's economics are not very compelling."

21) From Texas Instruments: "We continued to see two distinct dynamics at play. First, tariffs and geopolitics are disrupting and reshaping global supply chains...Second, the semiconductor cycle is playing out. Cyclical recovery is continuing, while customer inventories remain at low levels.” On the inventory build with tariffs, "during the last call, when there is a change of dynamics, like tariffs are being added, and I go back to April, customers are sitting on very low inventories. I think it's a good assumption to make that customers will want to have a little bit more inventory, and we did see that phenomenon. We did see that in the early part of the quarter, there was an acceleration of demand." They expect that pull forward to continue into Q3 BUT because Q2 "ran a little hot. This is where I want to be a little bit more cautious into Q3."

22) From MMM: Based on "several key macro trends we're tracking...all metrics reflect a global economy that remains sluggish and moving laterally, not materially improving or worsening."

23) From DR Horton: “New home demand continues to be impacted by ongoing affordability constraints and cautious consumer sentiment. Where necessary, we have increased incentives to drive traffic and incremental sales. Our cancellation rate remains at the low end of our historical range, indicating that buyers in today’s market are able to qualify financially and are committed to their home purchase, despite the volatility and uncertainty of the current economic environment…I think the incentives throughout the quarter were a bit choppy and we’ve responded to the market…as we work through the end of spring and deep into the summer selling season, our incentives have increased some to maintain our pace…Our recent sales and currently our sales and backlog do reflect a higher cost of incentives. And so the closings that we see into July, August, September, we do expect margins to take that step down that we had previously anticipated would occur in Q3.”

24) From Pulte: “Over the past few quarters, our industry has routinely referenced demand conditions as being volatile, and that remains the most accurate description of buyer activity in the first and second quarters. Within a market demonstrating a typical seasonal pattern from month to month, we do see days of strong demand followed by days displaying a step down in activity…Feedback from would be homebuyers indicates a variety of concerns ranging from affordability and the inability to sell an existing home to a slowing economy and the fear of potentially losing their job. In sum, I think consumer confidence is uncertain at best, and confidence is something that’s difficult to solve with a lower price or higher incentive.”

25) From Steel Dynamics: "During the second quarter 2025, steel pricing stabilized at higher levels, resulting in a significant sequential improvement in consolidated operating income of 39% and adjusted EBITDA of 19%." But, "The uncertainty regarding trade policy continues to cause hesitancy in customer order patterns across our businesses, despite healthy underlying demand factors, such as manufacturing onshoring, infrastructure program funding, and increased regionalization of supply chains in the US. This hesitancy, combined with an inventory overhang of coated flat rolled steel, resulted in lower steel and steel fabrication shipments in the second quarter 2025."

26) From Sherwin Williams: "Given the demand softness in the quarter, which we expect will continue if not deteriorate in the second half of the year, we aggressively accelerated and increased our restructuring actions, resulting in pre-tax expenses of $59 million."

27) July Tokyo CPI rose 3.1% ex food and energy y/o/y but as expected and at the same pace seen in June. This is the 4th straight month with a 3 handle while the BoJ still has the overnight rate at just .50%.

28) The June UK retail sales figure ex auto fuel rose .6% m/o/m, half the estimate. It was a hot weather month in June in the UK which helped food and drink. Online retailing did ok too. This coincides with still soft UK consumer confidence. The GFK report on this last night fell to -19 from -18. The noteworthy thing in this index was the 7 pt rise in the 'savings' component to 34, the highest since November 2007. GFK referred to this as "contingency funds" and reflecting a more cautious consumer.

29) In the UK S&P Global July report it said it "shows the economy struggling to expand as we move into the second half of the year. Output growth weakened to a pace indicative of the economy growing at a mere .1% quarterly rate, with risks tilted to the downside in the coming months. The sluggish output growth reported in July reflected headwinds of deteriorating order books, subdued business confidence and rising costs, all of which were widely linked to the ongoing impact of the policy changes announced in last autumn's Budget and the broader destabilizing effects of geopolitical uncertainty."

30) Tough week on the celebrity front losing Ozzy, the Hulkster, Theo (Malcolm-Jamal Warner) and Chuck Mangione.