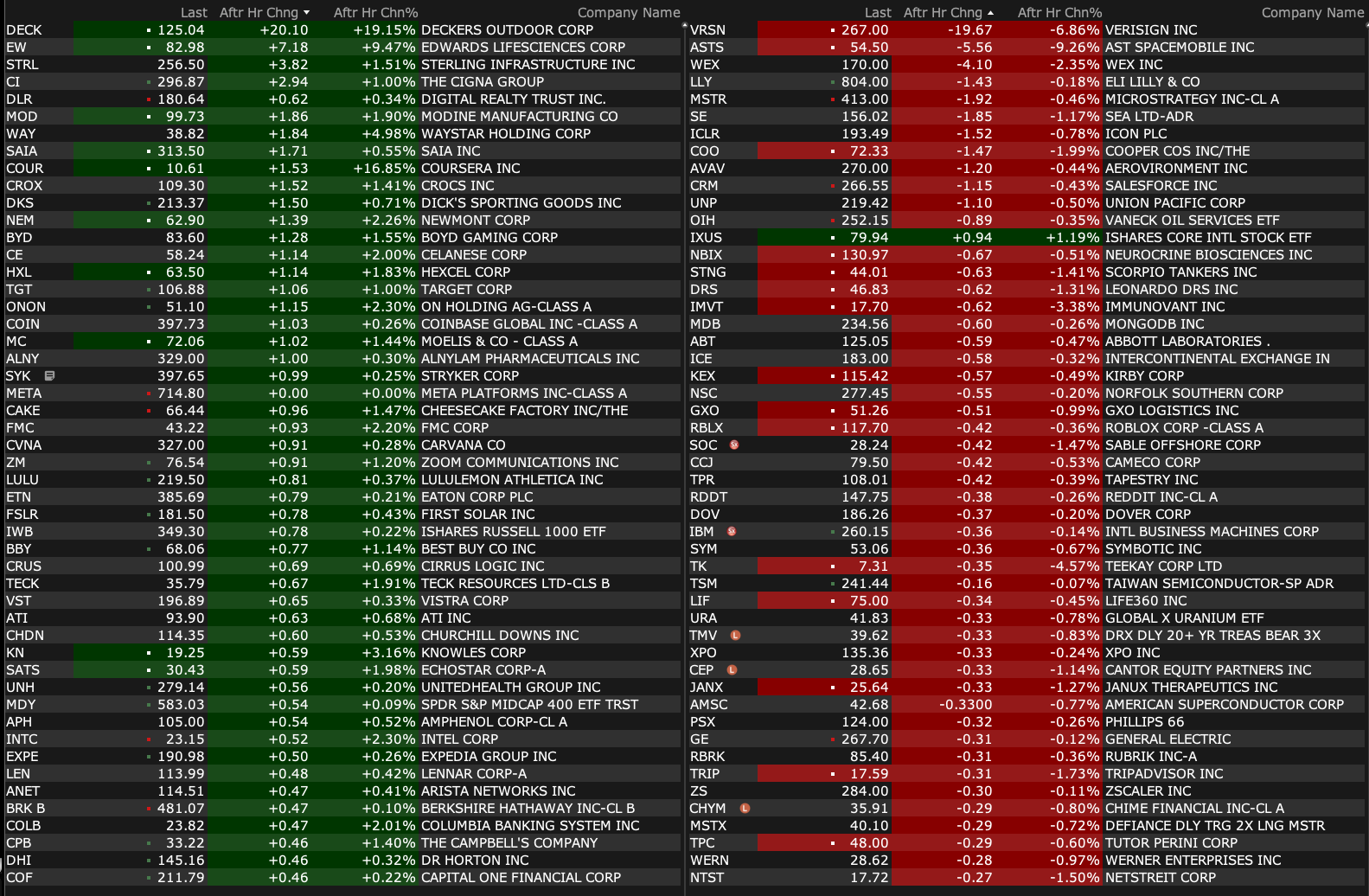

Thursday's After-Hours Movers

As of 4:21 p.m.:

BY Doug Kass · Jul 24, 2025, 5:15 PM EDT

As of 4:21 p.m.:

BY Doug Kass · Jul 24, 2025, 5:15 PM EDT

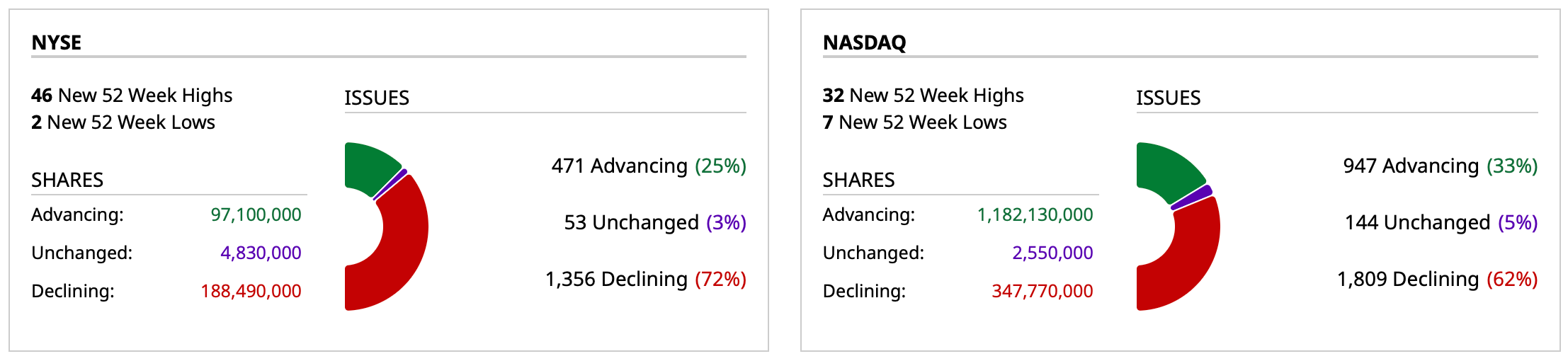

- NYSE volume 1% above its one-month average;

- NASDAQ volume 46% above its one-month average;

- VIX index: up 0.33% to 15.42

BY Doug Kass · Jul 24, 2025, 5:05 PM EDT

I won’t be returning to the office today.

See you all bright and early tomorrow.

BY Doug Kass · Jul 24, 2025, 2:05 PM EDT

BY Doug Kass · Jul 24, 2025, 11:40 AM EDT

BY Doug Kass · Jul 24, 2025, 11:12 AM EDT

From Peter Boockvar:

The July S&P Global PMI rose to 54.6 from 52.9. The internals though were mixed. Manufacturing fell back below 50 at 49.5 from 52.9, offset by a rise to 55.2 from 52.9 in services. I’ve stated here many times though that S&P Global does not include wholesale and retail trade which we know is a big chunk of the service economy. It also doesn’t include construction. Thus, this services component is not a complete picture relative to the ISM services index which we’ll see in a few weeks.

Also of note was this comment from S&P Global, “Business confidence about the year ahead has also deteriorated in both manufacturing and services to one of the lowest levels seen over the past 2 ½ years. Companies cite ongoing concerns over the impact of government policies, notably in terms of both tariffs and cuts to federal spending.”

This too, “Inflation pressures have meanwhile intensified. Companies most commonly attributed higher costs and selling prices to tariffs, though increased labor costs are also prevalent, in part reflecting labor shortages.” They said the rise in selling prices for goods and services was “one of the largest seen over the past three years.”

With manufacturing, “the renewed drop in demand…was often attributed to tariffs, higher prices and heightened economic uncertainty.” Also, “The deteriorating manufacturing picture was also linked to inventory control. Having built up their inventories of both raw materials and finished goods in May and June, often attributed to factories and their customers seeking to front run tariffs, manufacturers reported lower stock holdings in both cases during July. Purchasing of inputs likewise rose at a sharply reduced rate amid reduced reports of the need to front-run potential tariff hikes on imported goods. Supplier deliveries quickened as a result of the reduced pressure on supply chains.”

Here is more on costs and inflation:

“Price pressures intensified across both manufacturing and service sectors during July, widely blamed on higher goods prices due to tariffs but also in some cases due to rising labor costs. Average prices charged for goods and services rose at a rate just shy of May’s recent high to register the second-strongest monthly increase since September 2022. Services price inflation accelerated to register the second steepest increase since April 2023 and, although factory gate selling price inflation eased, the rise in charges for manufactured goods was the second largest since November 2022. Input cost inflation also picked up again, having eased slightly in June, registering the second-steepest rise since January 2023. The rate of input cost inflation remained especially sharp in manufacturing, despite cooling compared to June’s post-pandemic peak, and accelerated in services. Close to two-thirds of all manufacturers reporting higher input costs attributed these to tariffs, whilst just under half of respondents explicitly linked their increased selling prices to tariffs. However, the tariff impact was by no means limited to factories, as around 40% of service providers reporting higher selling prices explicitly mentioned tariffs.”

This was said on employment, “Employment rose for a fifth straight month as companies took on additional staff in response to rising backlogs of work. Uncompleted orders rose at a pace not witnessed since May 2022.”

Bottom line, the mixed bag economy continues on and the inflation/cost comments is worth noting for sure.

BY Doug Kass · Jul 24, 2025, 10:48 AM EDT

Tesla's TSLA quarter was god awful.

I will have more on this tomorrow morning.

BY Doug Kass · Jul 24, 2025, 10:29 AM EDT

With S&P cash I added to my short index call position.

BY Doug Kass · Jul 24, 2025, 10:17 AM EDT

From Peter Boockvar:

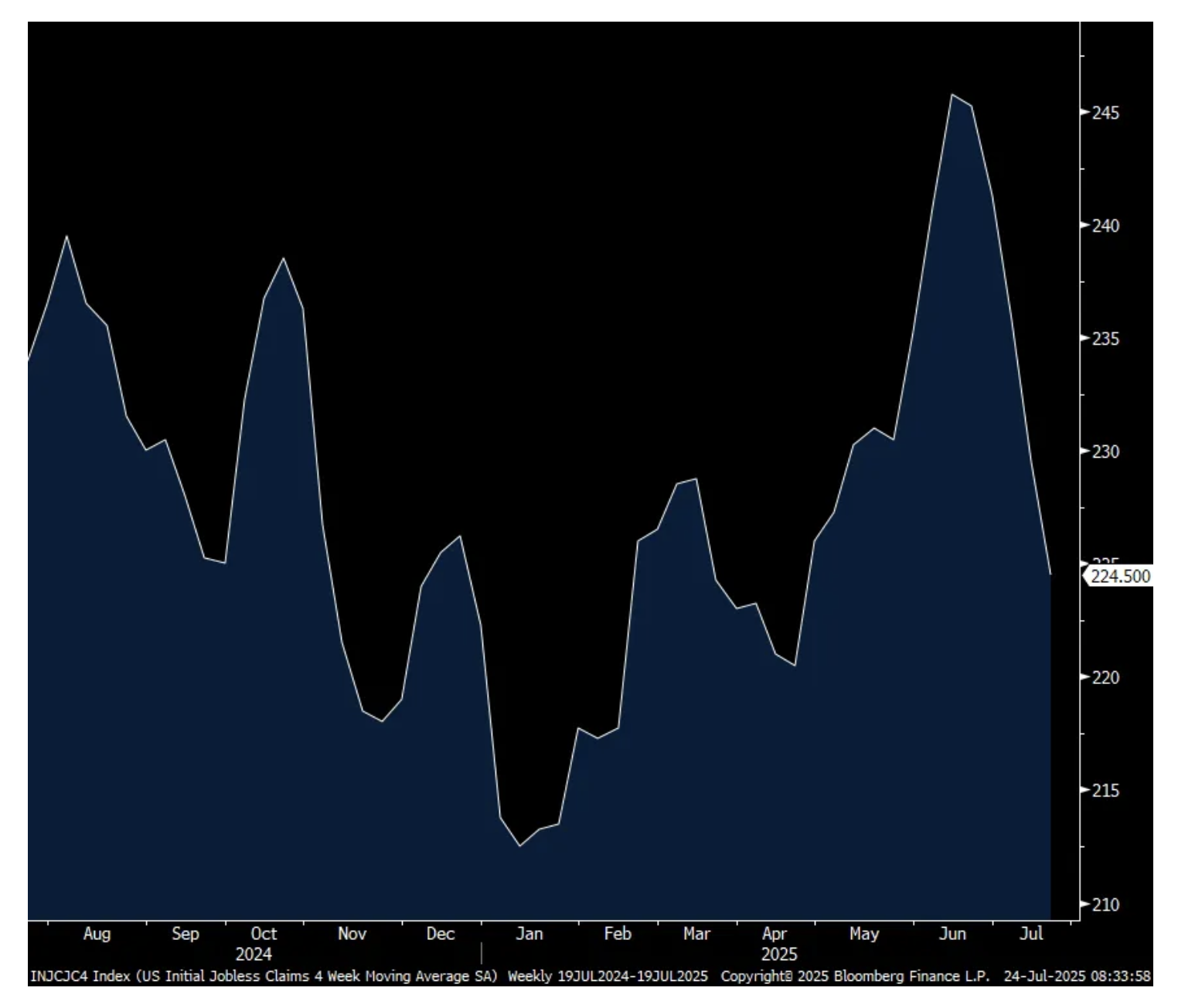

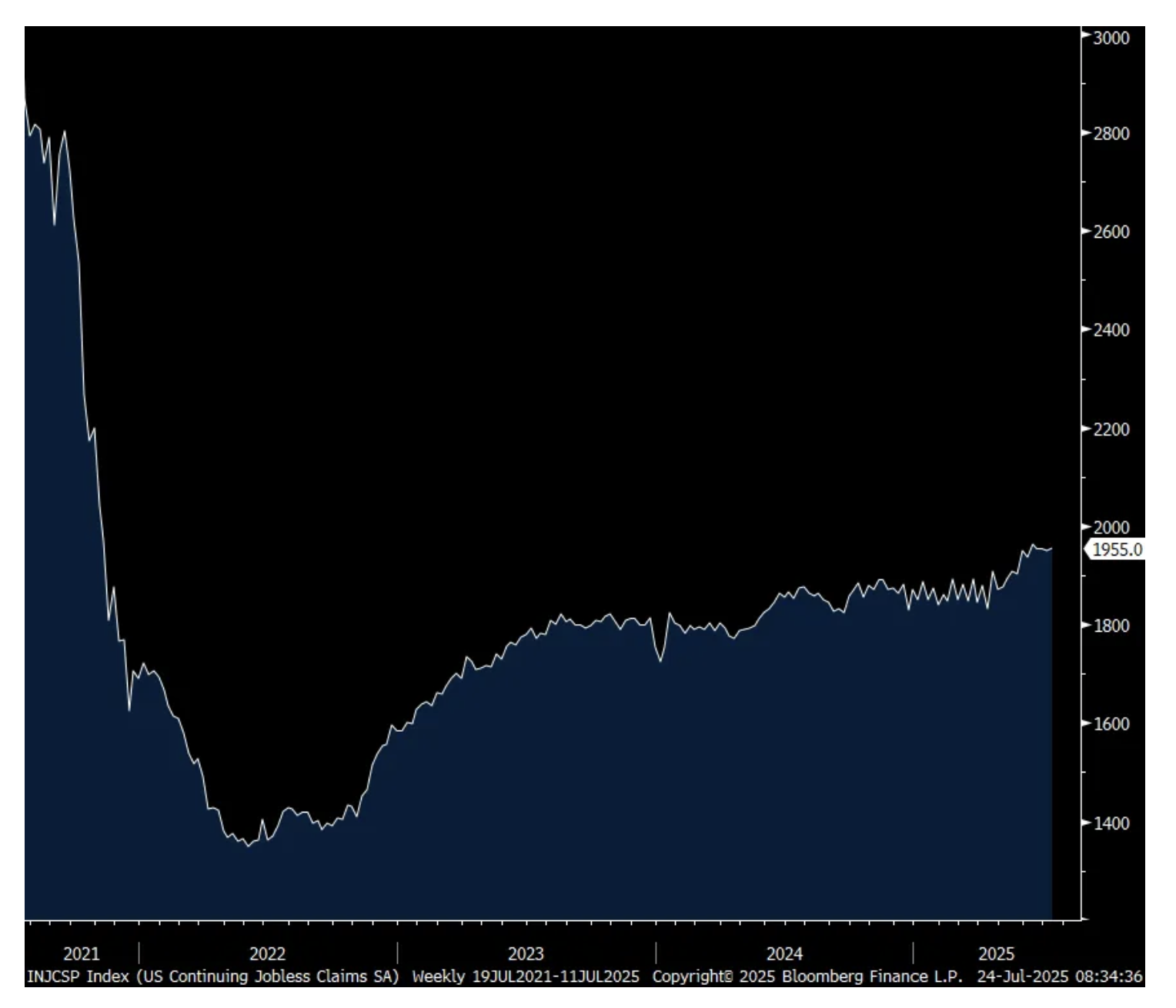

Initial jobless claims fell to 217k from 221k and that was 9k below expectations. The 4 week average dropped by 5k w/o/w to 225k. Continuing claims were as expected at 1.955mm, up 4k w/o/w.

Bottom line, the pace of firing’s, as measured here, remains impressively low while those still collecting claims still elevated, around the most since November 2021.

On the lower initial claims figure, Treasury yields are at the highs of the morning with the 10 yr at 4.42-.43% and the 30 yr yield nearing 5% at 4.98%.

Initial Jobless Claims 4 week avg

Continuing Claims

BY Doug Kass · Jul 24, 2025, 10:10 AM EDT

No trades today.

BY Doug Kass · Jul 24, 2025, 9:48 AM EDT

From Peter Boockvar:

It seems like we've reached a point where it feels the stock market will never go down. Impressive run.

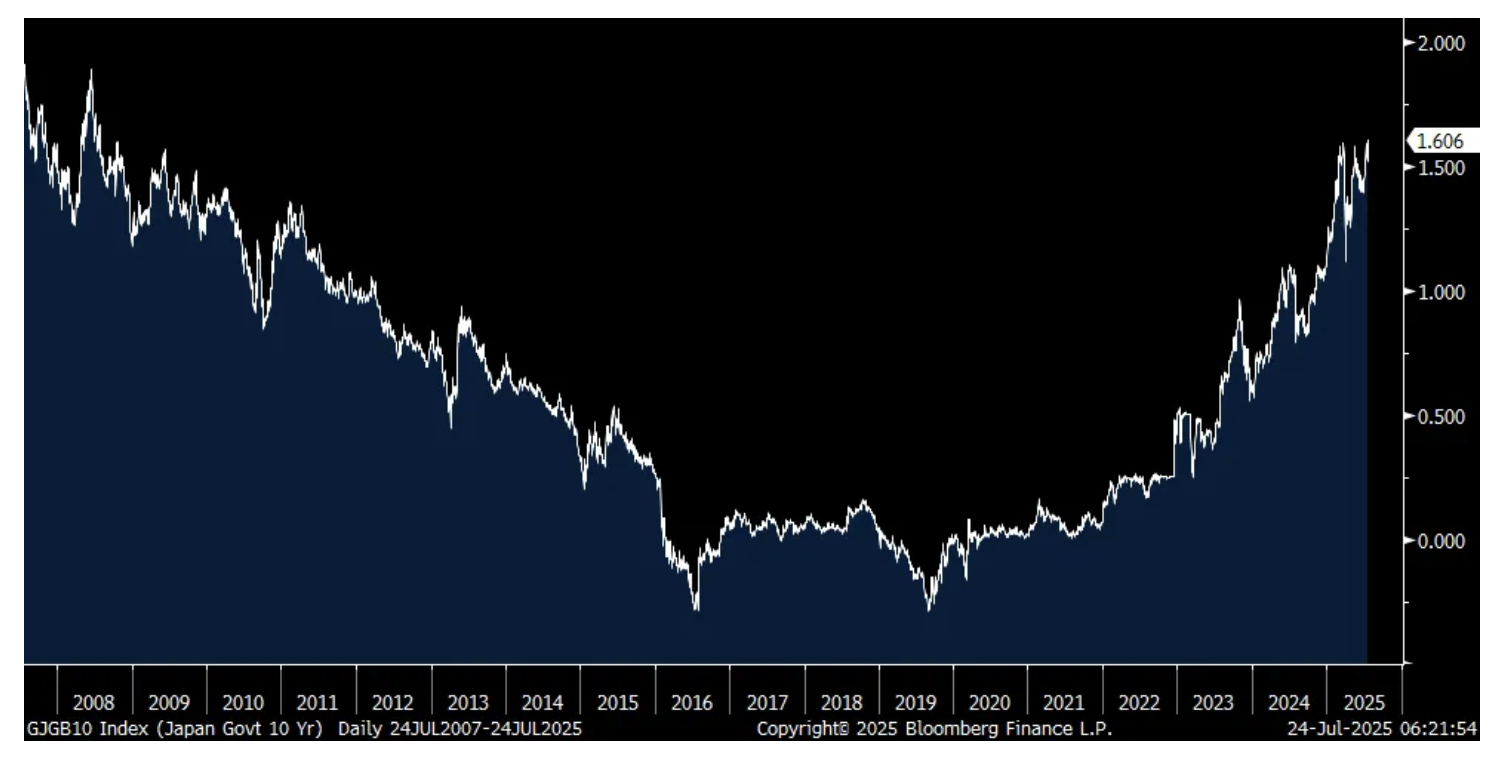

Still watching JGB yields every day, the 10 yr yield broke out to the highest level since July 2008 overnight, 17 yrs ago at 1.61% and up 2 bps. The 30 yr and 40 yr yields though fell about 3 bps. The Nikkei by the way is just 1% from a record high and we remain long Japanese stocks. Yields are moving higher in the rest of Asia, Europe and here in the US too. Still, something to watch I emphasize as there is a global aversion to taking on too much duration risk in sovereign bond land.

10 yr JGB Yield

Out yesterday was the June US Architecture Billings Index and it fell a touch to 46.8 from 47.2 in May with 50 the expansion/contraction breakeven. AIA chief economist said “Business conditions were soft nationwide in June, with a slight billing increase in the South for the first time since October. Other regions saw declining billings, though at a slower pace. While all specializations experienced softer billings, the decline slowed for commercial/industrial and institutional firms. Multifamily firms faced the weakest conditions, with further declines.” The last sentence gets to my continued point that we're sowing the seeds for an eventual uptick in rental growth in the 2nd half of 2026.

From Hilton Worldwide and whose stock fell 2.5% yesterday:

“the quarter turned out to be noisier than expected, driving system wide Rev PAR down 50 bps y/o/y. Performance was driven by continued strength in the Middle East-Africa region and Asia Pacific ex China, but offset by softer trends in the US and China.”

“second quarter comparable US RevPAR decreased 1.5%, largely driven by pressure across business transient and group, as declines in government spend and softer international inbound demand weighed on performance. For full year 2025, we expect US RevPAR growth to be at the lower end of our system wide RevPAR range.”

Their transient leisure business did better. “In the quarter, leisure transient RevPAR grew 1% as an elongated spring break window and easy y/o/y comparison supported leisure demand growth.”

From Hasbro and whose stock fell 1% yesterday:

“As we foreshadowed last quarter, most of our US retailers managed their discretionary inventory tightly through the quarter. While revenue declined, we improved margins, delivering near break even profitability through cost actions, mix and promotional spending discipline.”

“We’ve incurred minimal tariff related expense in our year to date results, as most of the impacted inventory is still sitting on the balance sheet, and is yet to flow through the P&L.”

“We’re also seeing downstream impacts from trade uncertainty across the retail landscape. Many retailers are delaying holiday inventory bills and pushed shelf resets into Q3, both of which weighed on Q2 consumer products revenue and are requiring us to remain agile in the second half.”

“Today, approximately 50% of our US toy and game volume originates from China, and we have plans in place to bring that exposure down to less than 40% by 2027 through accelerated geographic diversification.”

“Now in terms of how tariffs have impacted the category, I think the answer is it hasn’t impacted take away from the consumer that much yet, because usually it takes 5 to 8 months for a toy to go from the factory to the shelf. But I think you started to see some indications that toy prices were starting to creep up in May and June. And we think that will happen slowly and consistently, likely through the balance of the year and into next year. I don’t think you’re going to magically see one day toy prices go from X to Y. I think it’s going to be kind of more line by line, skew by skew. And over several months as the general industry kind of gets a feel for what the consumer can bear.” I bolded to highlight.

From SAP whose stock fell 5% yesterday:

“uncertainty in global markets from earlier this year remains, but SAP has an excellent pipeline for half year two in almost all markets and regions.”

“In a few individual industries impacted by uncertainty, we are seeing extended approval workflows on the customer side, for example, in the US public sector and among manufacturers affected by tariffs.”

“As we look towards half year two, we are mindful of the broader environment, including geopolitical developments, notably the ongoing uncertainty about trade policy that has contributed to elongated sales cycles in certain sectors such as US public sector and industrial manufacturing. The sequential one percentage point deceleration in current cloud backlog growth is underscoring the dampening effect on bookings in Q2. It is obviously hard, if not impossible, to predict when exactly we’ll catch up on the pushouts…Unfortunately, we have no crystal ball to reliably predict global trade policy decision making, and it goes without saying that the longer this uncertainty persists, the more pressure it is likely to put on global trade and our customers’ ability to make well informed decisions.”

“So, while capital markets appear to be optimistic and continue to perform at or near all time highs, we do prepare SAP for less favorable outcomes by focusing on elements within our control to protect our bottom line and safeguarding free cash flow in 2025.”

From OTIS and whose stock fell 12% yesterday:

On guidance, “We continue to expect a low single digit decline in the Americas. However, we are beginning to see trends improving sequentially. Our market outlook for EMEA is unchanged with low single digit growth. Asia is now anticipated to decline high single digits. This is driven by mid single digit growth in Asia Pacific, offset by a low teens decline in China. Our outlook for China is now slightly lower than our beginning of year expectation due to continued softness in the market.”

With their new equipment business, “In the US, continued uncertainty over global trade policies are causing project delays.” This resulted in them lowering guidance for the Americas to “down high single digits.” Asia is hit too, particularly China to “down low teens.”

Keycorp described the macro as “dynamic and complex”:

“Within C&I, the growth continues to be broad based across industries and regions with both large institutions and middle market clients. Most of the growth was from new clients to Key. C&I line utilization picked up approximately 50 bps to 32%. The CRE growth was primarily driven by project based deals in affordable housing, traditional multifamily and data centers.”

“While client sentiment has improved compared to where it was on our last earnings call in mid April, the environment remains dynamic. Given the macro uncertainty, we continue to hold roughly $4 billion to $5 billion more cash and other short term liquidity than we anticipate needing over the medium term.”

“Our consumer is just fine. Just a reminder, our consumers have a FICO score of about 767. And so as you look at how the credits are performing, if you look at how spending volumes are performing, our clients are in good shape. I think one of the things that the models really fail to pick up is the wealth effect and the fact that household wealth in the US over the last 15 years has increased by about $100 trillion and that’s not inconsequential.”

On their commercial customer, “I think balance sheets are healthy. Their liquidity is in good shape.” Also, “We perform a very detailed survey on 850 customers that borrow $10 million or more. 50% of them think that the current environment is an opportunity for growth. As it relates to tariffs, because that’s always a topic for everyone, 30% of our customers are impacted by tariffs, but here’s the interesting thing. Of the $56 billion that we have outstanding in C&I, only 3% are significantly impacted in a direct way by tariffs.” Category wise, they saw the best loan growth to companies in renewables, affordable housing and healthcare.

From Lamb Weston, up 16% yesterday after a tough time over the past year and the maker of French fries:

“Volume was up with wins across channels and geographies, and net sales grew. Price/mix declined, reflecting our support of customers with price and trade as we manage the competitive environment and soft restaurant traffic.” Helping volume were some contract wins.

Here is what they said about their quick serve customer, “In the US, QSR traffic improved from February’s levels but compared with the prior year was down 1% in the quarter and the fiscal year. Traffic at QSR chains specializing in hamburgers was down 2% in the quarter and 3% for the year. It’s important to note that this is on top of declines in the prior year. Restaurant traffic on a two year stack is down mid single digits with QSR hamburger focused restaurants down high single digits over the two year period.”

From Google/Alphabet and with a pop in the stock pre market:

"The 12% increase in Search and other revenue was led by growth across all verticals, with the largest contributions from retail and financial services. YouTube saw similar performance across verticals. Its 13% growth in advertising revenue was driven by direct response, followed by brand."

With Google Cloud, revenues were up 32% y/o/y with the help of course by its AI offerings.

"With respect to CapEx, in the second quarter our CapEx was $22.4 billion. The vast majority of our CapEx was invested in technical infrastructure, with approximately two-thirds of investments in servers and one third in data centers and networking equipment."

With guidance, "given the strong demand for our Cloud products and services, we now expect to invest approximately $85 billion in CapEx in 2025, up from a previous estimate of $75 billion. Our updated outlook reflects additional investment in servers, the timing of delivery of servers, and an acceleration in the pace of data center construction, primarily to meet Cloud customer demand. Looking out to 2026, we expect a further increase in CapEx due to the demand we're seeing from customers as well as growth opportunities across the company."

I'll add this, with expectations of full year 2025 revenues for Alphabet of $337b, the CapEx is an incredible 25% of this.

From Tesla, with the stock down pre market:

"The One Big Bill has a lot of changes that would affect our business in the near term. The first among those changes is the repeal of the IRA EV credit of $7,500 by the end of this quarter. Given the abrupt change, we have limited supply of vehicles in the US this quarter, as we have already within lead times to order parts to build cars."

"we're in this weird transition period, where we will lose a lot of incentives in the US. There's a lot of incentives actually in many other parts of the world, but we'll lose them in the US...On the other hand, autonomy is most advanced and most available from a regulatory standpoint in the US. So, does that mean we could have a few rough quarters? Yes, we probably could have a few rough quarters. I'm not saying we will, but we could. Q4, Q1, maybe Q2. But once you get to autonomy at scale in the second half of next year, certainly by the end of next year, I would be surprised if Tesla's economics are not very compelling."

"If you're in the US and looking to buy a car, place your order now as we may not be able to guarantee delivery orders placed in the later part of August and beyond. But we'll also make changes to certain emissions standards by reducing the amount of penalty to zero. This, in turn, will have an impact on the new sales of regulatory credits to other OEMs and, in turn, will lead to lower earnings. While we never plan our business around such sales, it will nonetheless impact our total revenues quite fast."

"We've started seeing the impact of tariffs in our P&L. Sequentially, the cost of tariffs increased around $300 million, with approximately two-thirds of that impact in automotive and rest in energy. However, given the latency in manufacturing and sales, the full impacts will come through in the following quarters, and so cost will increase in the near term. While we are doing our best to manage these impacts, we are in an unpredictable environment on the tariff front."

"The Big Bill has certain adverse impacts even for the energy business, most notably on the residential storage business due to the early expiration of consumer credits by the end of the year."

This was an interesting question from Adam Jonas, "So Elon, as Tesla moves into this next phase of physical AI, autonomous, humanoids, robotaxis, etc..., world changing civilizational species changing technology with dual purpose, are you comfortable moving Tesla in this direction while only having a 13% stake in the company? Is that sustainable or do you still insist that something needs to happen given your current lack of control on the types of technologies you're getting into?"

Elon's answer, "Yes. That is a major concern for me, as I've mentioned in the past, and I hope that is addressed at the upcoming shareholder's meeting. But yes, it is a big deal, like, I want to find that I've got so little control that I can easily be ousted by activist shareholders after having bought these army of humanoid robots. I think, as I mentioned before, I think my control over Tesla should be enough to ensure that it goes in a good direction, but not so much control that I can't be thrown out if I go crazy."

From Chipotle, and whose stock is down sharply pre market:

Comps fell 4% y/o/y. "While we experienced a slowdown in our underlying trend in May, we did see momentum build as we rolled out our summer marketing initiatives and leaned into hospitality. And exiting the quarter, we returned to a positive comp and transaction trends, which have continued into July."

"However, considering the ongoing volatility in our trends in the consumer environment, we now anticipate comparable sales to be about flat for the full year."

"July has been a bit choppy over the last couple of weeks. I think it's due to kind of some post holiday as well as some weather that we've seen."

"I think much of what we're experiencing right now is due to macro and the low income consumer is looking for value as a price point. At present you have to look no further than what's going on with our competitors with snack occasion or $5 meals and that's where the consumer is drifting towards as value as a price point because of low consumer sentiment."

They see "underlying cost of sales inflation to be in the low single digit range for the remainder of the year" and that excludes tariffs. They expect "wage inflation in the low single digit range for the remainder of the year."

Here was the quick lay of the macro land from the CEO of IBM and whose stock is down pre market:

"I'll start by saying that we appreciate the administration's priority on economic growth and focused regulation, which will strengthen the US competitive position. We believe this will result in long term value creation and enable technology to contribute to economic growth. Technology continues to serve as a key competitive advantage, allowing businesses to scale, drive efficiencies, and fuel growth, and we saw this play out in the quarter. While not a major factor overall, geopolitical tensions are prompting a few clients to move cautiously. US Federal spending was also somewhat constrained in the first half, but we do not expect it to create long-term headwinds."

Here is a quick rundown of the July global PMI's out today and ahead of the US one at 9:45am est. Services still outperforming manufacturing.

Japan: manufacturing 48.8 vs 50.1, services 53.5 vs 51.7

Australia: manufacturing 51.6 vs 50.6, services 53.8 vs 51.8

India: manufacturing 59.2 vs 58.4, services 59.8 vs 60.4

Eurozone: manufacturing 49.8 vs 49.5, services 51.2 vs 50.5

UK: manufacturing 48.2 vs 47.7, services 51.2 vs 52.8

In the Eurozone, S&P Global said "The Eurozone economy appears to be gradually regaining momentum. The recession in the manufacturing sector is coming to an end, and growth in the services sector accelerated slightly in July."

The ECB by the way is expected to leave interest rates unchanged today at 2%.

In the UK, the July report "shows the economy struggling to expand as we move into the second half of the year. Output growth weakened to a pace indicative of the economy growing at a mere .1% quarterly rate, with risks tilted to the downside in the coming months. The sluggish output growth reported in July reflected headwinds of deteriorating order books, subdued business confidence and rising costs, all of which were widely linked to the ongoing impact of the policy changes announced in last autumn's Budget and the broader destabilizing effects of geopolitical uncertainty."

BY Doug Kass · Jul 24, 2025, 9:45 AM EDT

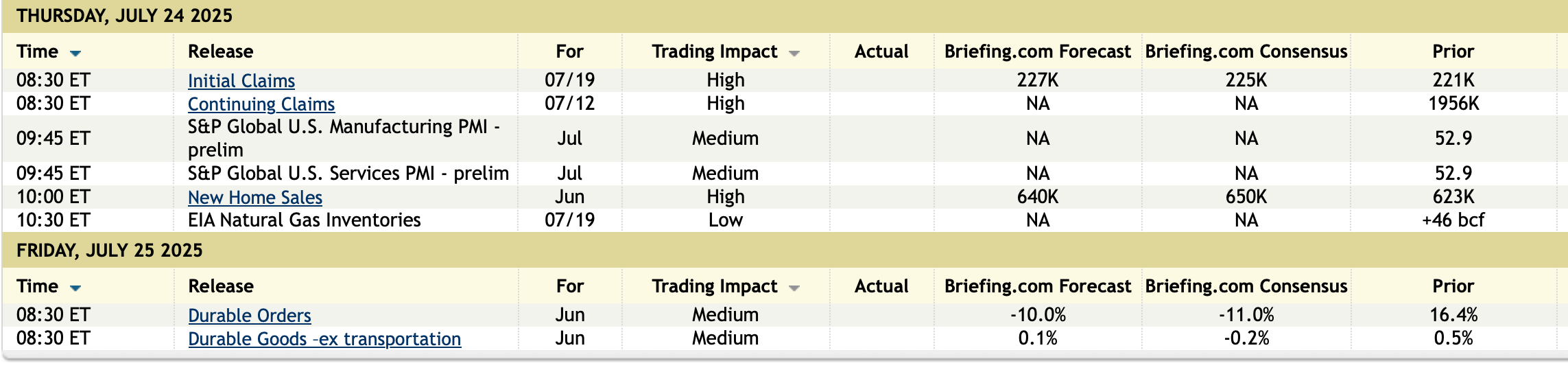

Economic Calendar

Treasury Auctions

11 a.m.: Treasury announces a 3 and 6 month bill auction;

11: Treasury's Note Announcement;

11:30; Treasury hosts a $95 billion four and $85 billion eight week bill auction;

1 p.m.: Treasury hosts a $21 billion 10-Year TIPS Auction

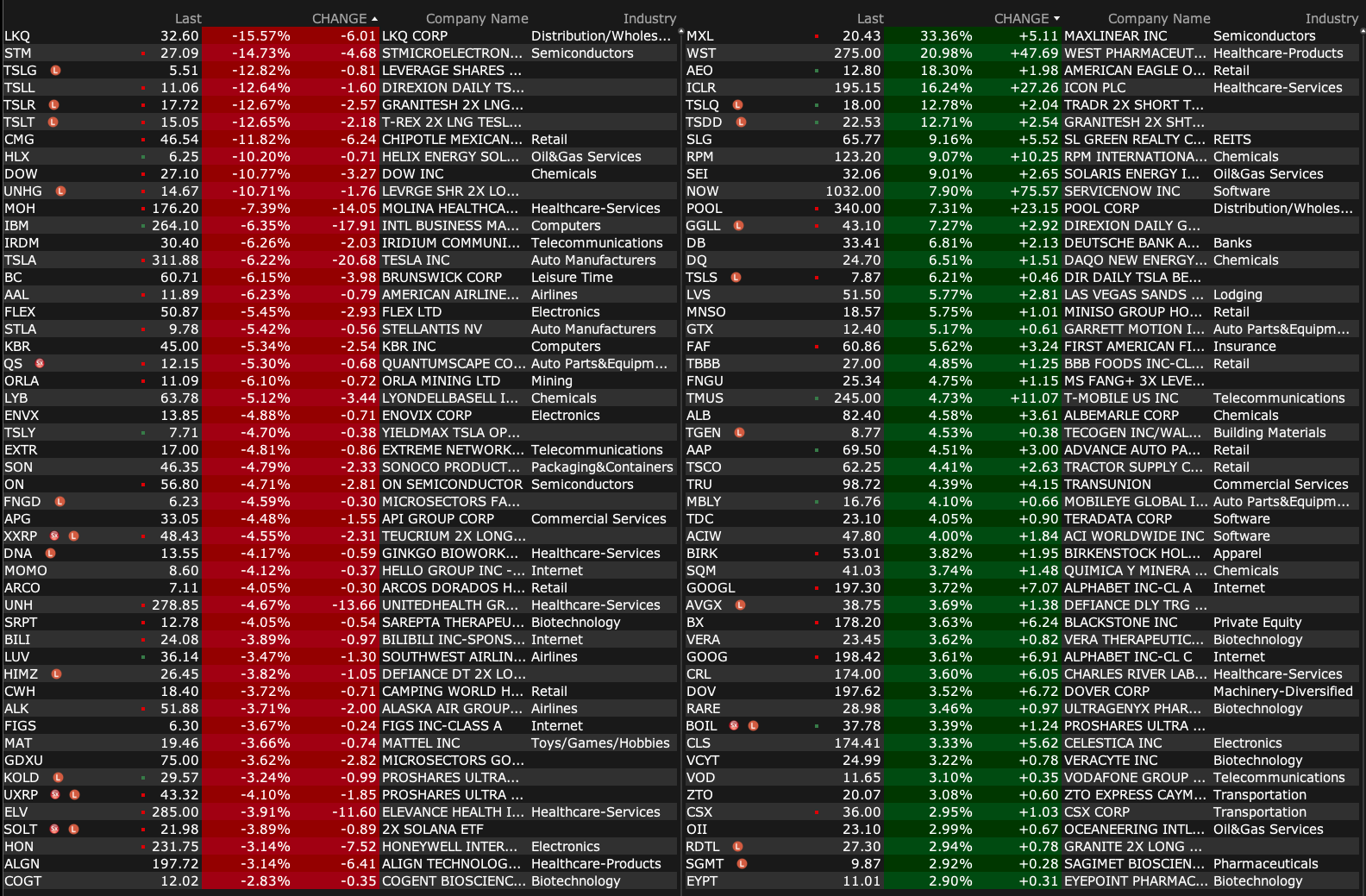

BY Doug Kass · Jul 24, 2025, 9:25 AM EDT

-MXL +26% (earnings, guidance)

-CIO +24% (to be taken private in ~$1.1B deal with MCME Carell)

-WST +19% (earnings, guidance)

-HLX +12% (earnings, guidance)

-RUN +12% (launches Home Energy Plan with Tesla to Cut Costs and Boost Backup Power for Texans)

-SEI +10% (earnings, guidance)

-RPM +9.2% (earnings, guidance)

-OPEN +8.3% (meme momentum)

-POOL +8.3% (earnings, guidance)

-NOW +7.5% (earnings, guidance)

-LVS +6.7% (earnings)

-RJF +4.8% (earnings)

-TSCO +4.5% (earnings, guidance)

-TMUS +4.0% (earnings, guidance)

-GOOGL +3.7% (earnings, guidance)

-MBLY +3.7% (earnings, guidance)

-VSTM +3.7% (granted Fast Track Designation for VS-7375 for the Treatment of KRAS G12D-mutated Locally Advanced or Metastatic Pancreatic Cancer)

-CSX +3.0% (earnings, guidance)

-VRNS +3.0% (Jefferies Raised VRNS to Buy from Hold, price target: $65)

-BX +2.7% (earnings)

-DOV +2.7% (earnings, guidance)

-SAH +2.6% (earnings)

-FCN +2.3% (earnings, guidance)

-HNI +2.2% (earnings, guidance)

-NVCR +2.2% (earnings)

-ADT +2.0% (earnings, guidance)

-ASGN +2.0% (earnings, guidance)

-CYH -29% (earnings, guidance)

-LKQ -14% (earnings, guidance)

-CMG -12% (earnings, guidance)

-DOW -9.8% (earnings, guidance)

-IRDM -6.9% (earnings, guidance)

-MOH -6.9% (earnings, guidance)

-AAL -6.6% (earnings, guidance)

-VKTX -6.6% (earnings)

-IBM -6.4% (earnings, guidance)

-TSLA -6.2% (earnings, guidance, color)

-BC -6.1% (earnings, guidance)

-UNH -4.3% (proactively reached out to the DOJ after reviewing media reports about investigations into certain aspects of the Company’s participation in the Medicare program)

-DNUT -4.2% (profit taking off recent meme momentum)

-LUV -3.9% (earnings, guidance)

-MAT -3.9% (earnings, guidance)

-HON -3.2% (earnings, guidance)

-ALK -3.0% (earnings, guidance)

BY Doug Kass · Jul 24, 2025, 9:15 AM EDT

BY Doug Kass · Jul 24, 2025, 9:05 AM EDT

BY Doug Kass · Jul 24, 2025, 8:50 AM EDT

I think I bruised or fractured a rib doing yard work this past weekend.

I have an appointment with my doctor at around 1:30 p.m.

As his office is a distance away from my office I will be out for a few hours this afternoon.

BY Doug Kass · Jul 24, 2025, 8:23 AM EDT

From JPMorgan:

US: Futs are higher led by Tech with small caps lower after yesterday’s outperformance. The AI Theme is driving Tech following GOOG earnings with capex boost helping AVGO/NVDA; TSLA -6% on choppy guidance. Cyclicals stronger pre-mkt led by Industrials. Bond yields are 1bp from 2s to 30s with USD seeing its first bid in 5 sessions. Cmdtys are higher led by Ags/Energy with weakness in both Base/Precious. Today’s macro data focus is on Flash PMIs, Jobless Claims, Home Sales, and regional Fed activity indicators.

and...

JPM MARKET INTEL EQUITY & MACRO NARRATIVE

Another day, another record high. With the US / Japan deal announced and the US / EU deal on deck it feels like not even a soft earnings print from a major company can derail this bullish run. That said, today we get a look at the next batch of meaningful macro data ahead of next Friday’s NFP print. While Bullishness is not yet consensus, client conversation reveal that even those that skewed bearish are throwing in the towel. The combination of the Momentum Unwind and Meme Mania 2.0 are reducing (eliminating?) people’s ability to hold alpha shorts. Combine that with positive comments on M&A pipeline and the impending buyback bid and the storm clouds appear to be lifting ahead of the previously feared Aug 1 deadline. Now, if that US / EU hits the tape, we get a deal from China next week, and the macro data holds up and look for this market to take a significant step higher. If we had this conversation a month ago (or even last week) this would seem like a tail-risk, now it feels like this is the base case.

· INITIAL JOBLESS CLAIMS – Feroli sees claims increasing from 221k to 225k, which below the 4-week moving average of 229.5k. The YTD high is 250k.

· FLASH PMIs – Feroli sees PMI-Mfg printing 52.0 vs. 52.7 survey; 52.9 prior. He sees PMI-Srvcs printing 53.0 vs. 53.0 survey; 52.9 prior. Feroli notes that last month’s MFG print was the highest since 2022 and sees a step down despite stronger Empire Mfg and Philly Fed readings. For Srvcs, sees the index moving sideways despite the potential for tariff escalation to weight on activity.

· US MKT INTEL – Tactically Bullish. A hypothesis is based on (i) resilient macro data, (ii) positive earnings growth and (iii) thawing trade rhetoric.

· MONETIZATION MENU (repost from July 21 Morning Briefing) – We like longs in MegaCap Tech, Cyclicals, and high beta plays. At the country/region-level, we like Australia, China (Tech), and Japan but think the US will outperform RoW in the near-term. We would consider longs in VIX or VIX products as well as SPX puts/put spreads to hedge any near-term downside.

BY Doug Kass · Jul 24, 2025, 7:05 AM EDT

douglas cassel

actual article is behind paywall

The Economist:

BY Doug Kass · Jul 24, 2025, 6:53 AM EDT

* Yesterday the technicians were gushing (confidentally) about the gold setup (GLD fell by -$4 and is down by another -$2 in premarket)

* Today technicians are gushing (very confidentally) about U.S. equities...

Bonus — Here are some great links:

BY Doug Kass · Jul 24, 2025, 6:10 AM EDT

BY Doug Kass · Jul 24, 2025, 5:55 AM EDT

The S&P Short Range Oscillator climbed a bit deeper into overbought — it's now at 1.97% vs. 1.71% .

BY Doug Kass · Jul 24, 2025, 5:45 AM EDT