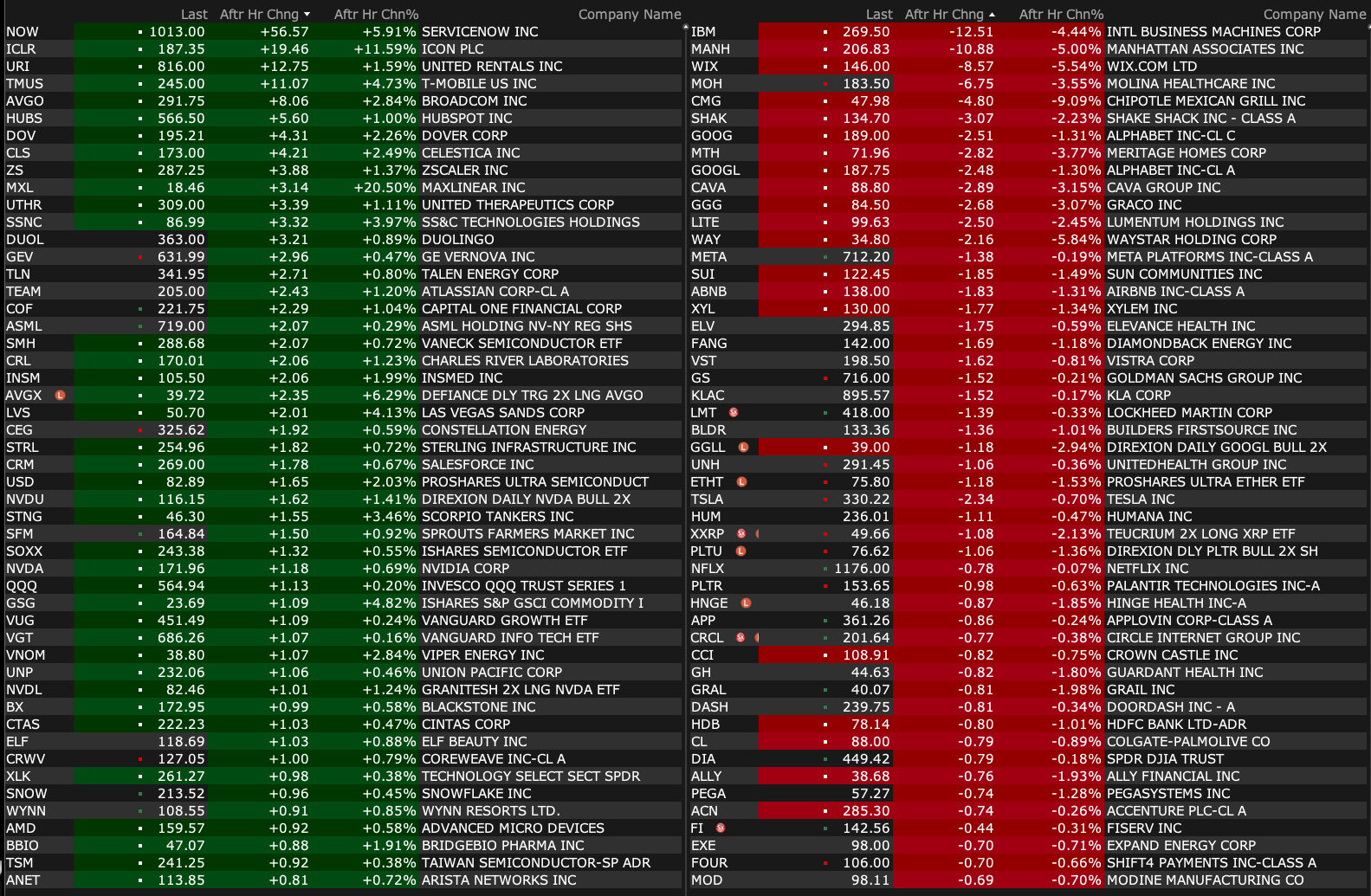

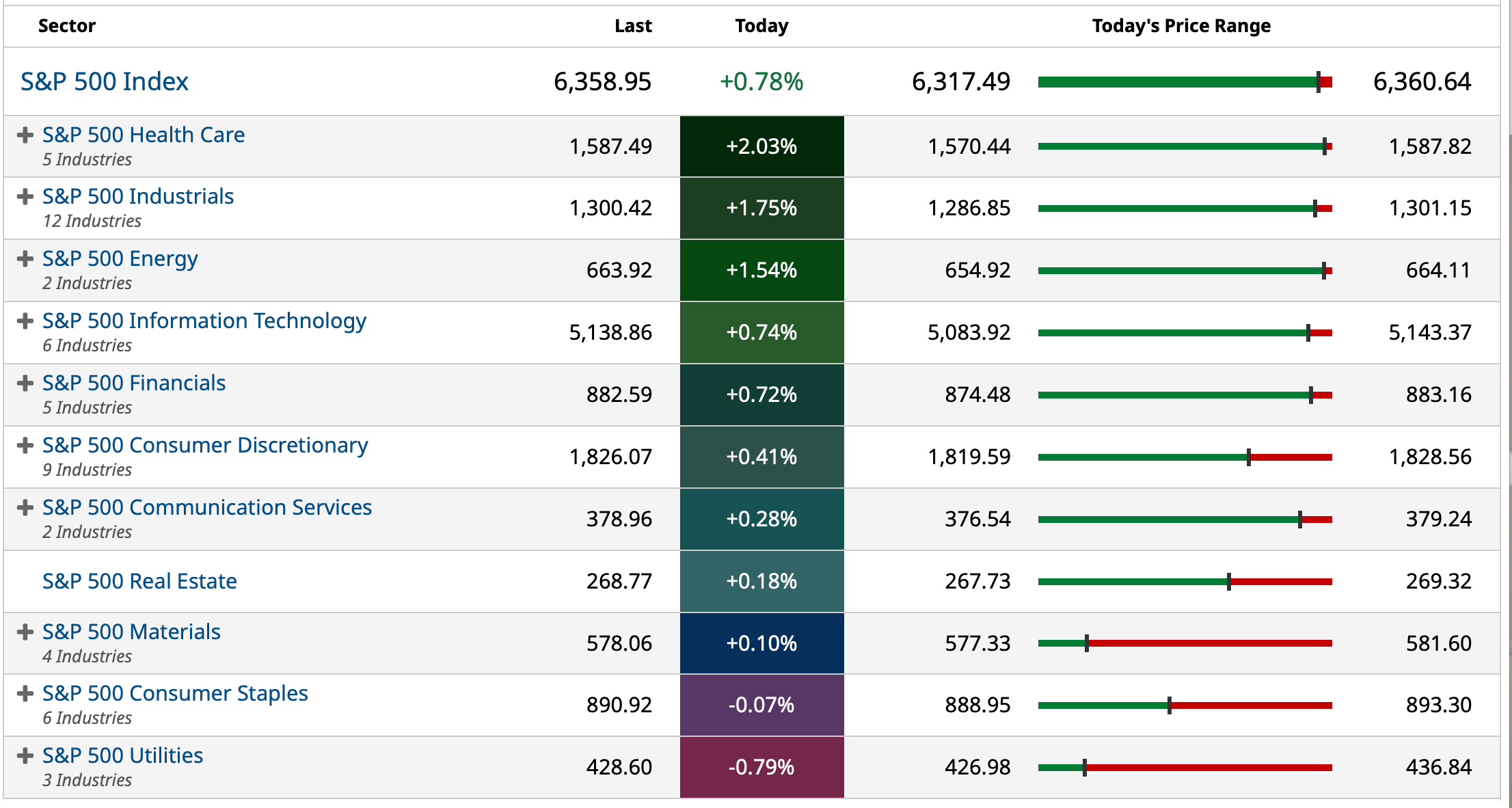

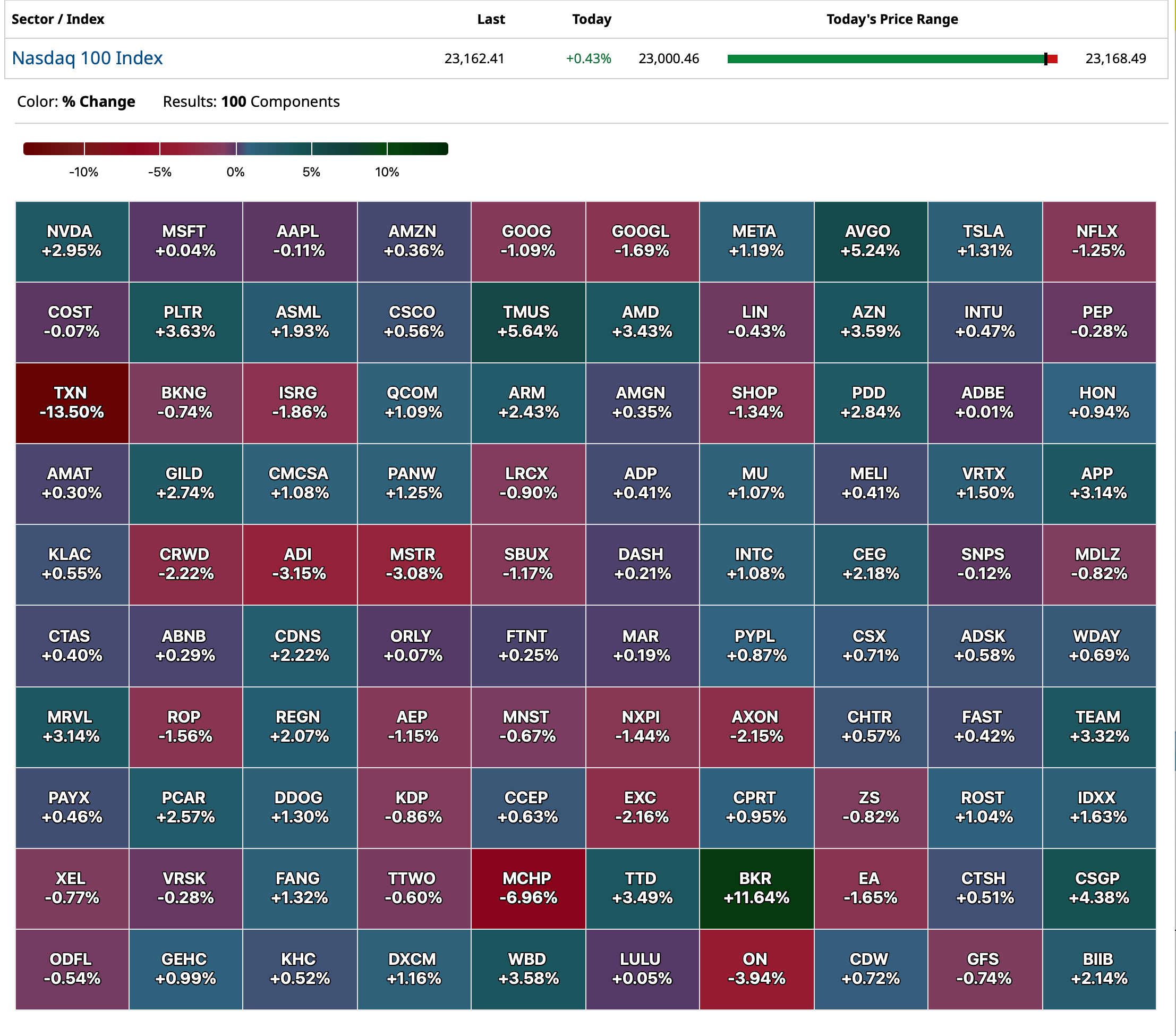

Wednesday's After-Hours Movers

As of 4:25:

BY Doug Kass · Jul 23, 2025, 4:45 PM EDT

As of 4:25:

BY Doug Kass · Jul 23, 2025, 4:45 PM EDT

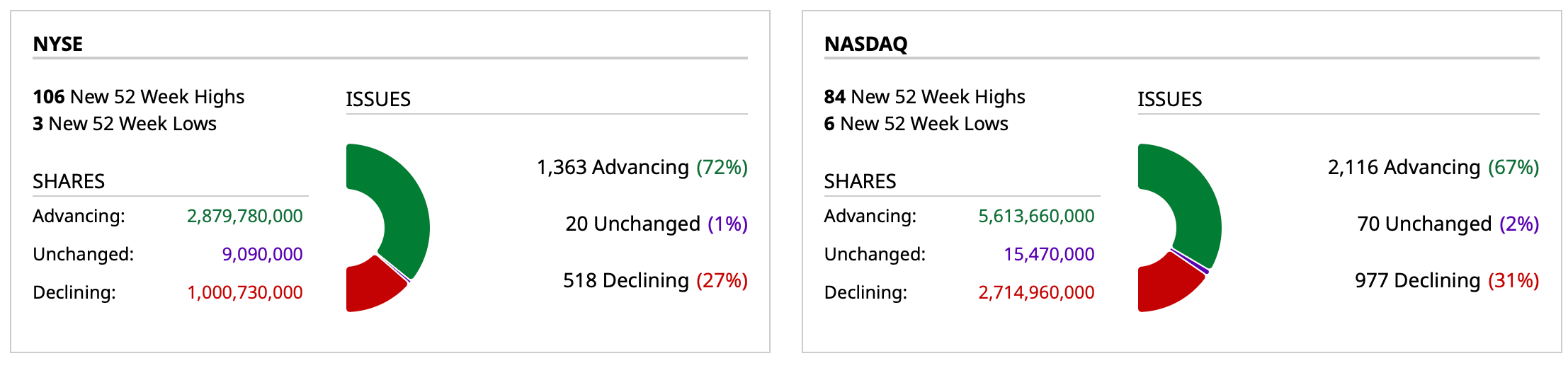

- NYSE volume 13% above its one-month average;

- NASDAQ volume 27% above its one-month average;

- VIX index: down 6.85% to 15.37

BY Doug Kass · Jul 23, 2025, 4:27 PM EDT

Thanks for reading my Diary today.

Enjoy your evening.

Be safe.

BY Doug Kass · Jul 23, 2025, 4:00 PM EDT

BY Doug Kass · Jul 23, 2025, 3:08 PM EDT

From Charlie:

BY Doug Kass · Jul 23, 2025, 3:00 PM EDT

* TLT -$0.50 on the day...

Another important factor the equity market is ignoring in its march to another high:

BY Doug Kass · Jul 23, 2025, 2:43 PM EDT

Wolf Street howls about the developing hangover in residential real estate.

BY Doug Kass · Jul 23, 2025, 2:15 PM EDT

Kiloecho

Doug.. when market continues to move against your thesis, when do you decide to 1. Question your thesis and change? 2. Or double down on it?

Dougie Kass

hourly/daily

And now, the end is near

And so I face the final curtain

My friend, I'll say it clear

I'll state my case, of which I'm certain

I've lived a life that's full

I traveled each and every highway

And more, much more than this

I did it my way

Regrets, I've had a few

But then again, too few to mention

I did what I had to do

And saw it through without exemption

I planned each charted course

Each careful step along the byway

And more, much more than this

I did it my way

- Frank Sinatra, My Way

I am further reducing St. Joe Company JOE long, which has benefited from a rotation into the homebuilder space.

My recent complete sales of numerous longs (in housing, financials, private equity and selected technology) have resulted in an expanded cash war chest which I want in the time ahead.

I currently see (in percentage terms) about a 5-1 risk to reward and few equities satisfy my standards for value. There is, at least in my own calculus, no margin of safety.

Subscribers have recently questioned my pessimism. (And I have as well in a recent market update). A contributor, Rev Shark, does the same.

After all these years and experience, my skin is thick. I can take any criticism — here, on social media or in my own head.

Self analysis and dealing with the criticism of others is part of the game. I don't shy from responding and, unlike almost anyone else, I fully admit my mistakes and failures. Specifically, I have admitted to failing to take advantage of the opportunity set presented since early April.

Mine is a constant reappraisal of analysis and assumptions (which I routinely present in my Diary), as noted in the exchange in The Comments section above.

As I have written, I am often wrong and always in doubt.

But, like The Chairman of the Board (Sinatra), My Way (as a value investor who considers upside reward vs. downside risk) is my national anthem.

BY Doug Kass · Jul 23, 2025, 1:48 PM EDT

From Peter Boockvar:

Home sales/Yes, lower mortgage rates would help but we need this too…

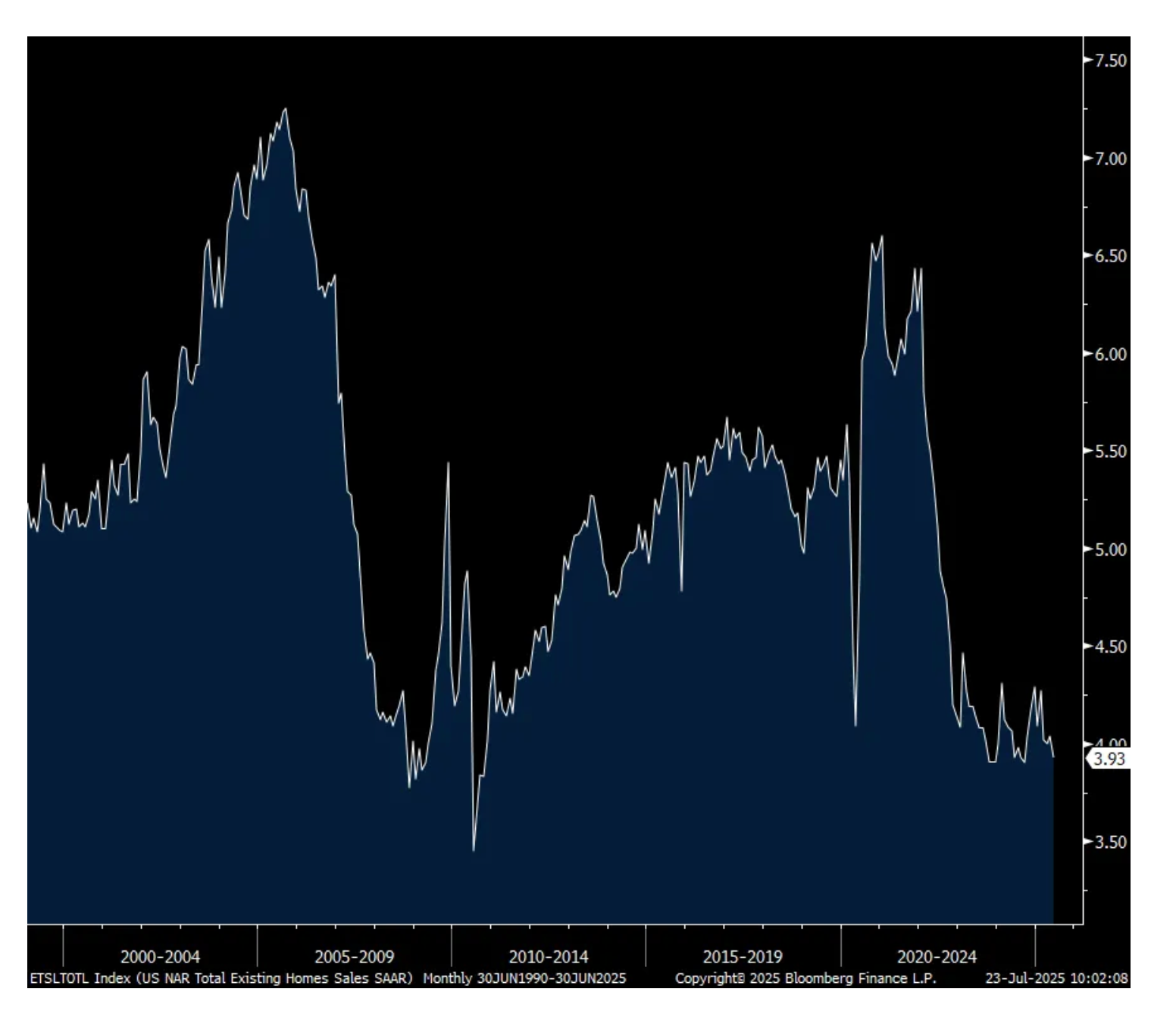

The pace of existing home sales (measuring closings) in June continued to hover around the slowest rate since 1995 at 3.93mm annualized, 70k less than expected and vs 4.04mm in May. Assume many of the contracts were signed in the March thru May time frame, and thus capturing the spring selling season.

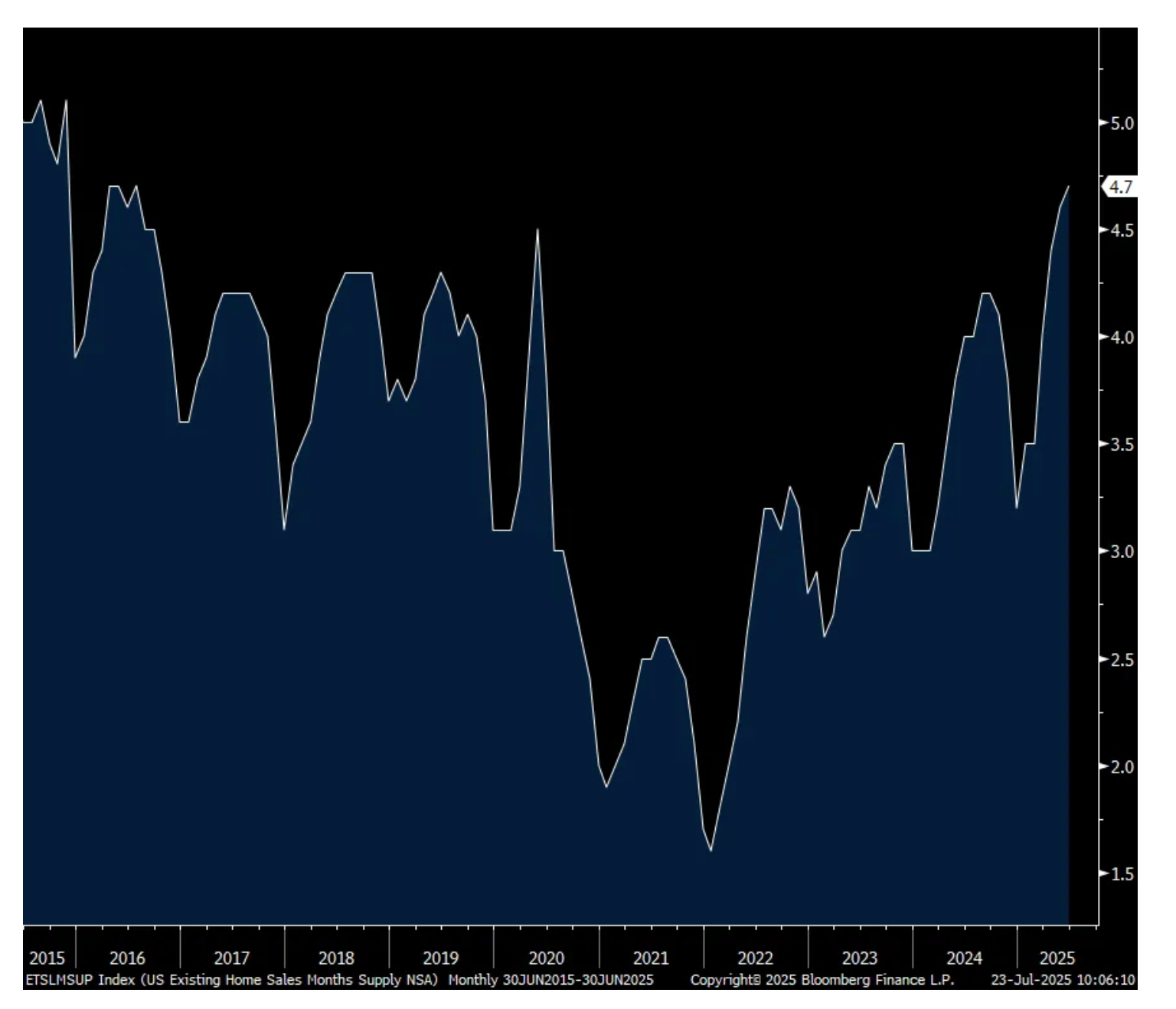

First time buyers totaled 30% of purchases which has been around the multi year trend but remaining low because of the affordability challenges we know all about. Months’ supply rose to 4.7 from 4.6 and that matches the most since November 2015 as supply in certain markets is slowly beginning to pick up.

The median home price was up 2% and a needed moderation in the pace of gains, helped by that inventory increase relative to sales. I do want to give my 2 cents on this common belief that the key to make buying a home purchase more affordable is just having lower mortgage rates. If the last 20 years is any lesson, it’s that lower mortgage rates when there is NOT a coincident increase in the supply of homes just leads to higher home prices and LESS affordable homes. Or at least the lower financing costs are completely offset by a higher price paid for the home.

We need both more housing supply and lower mortgage rates COMBINED in order to make buying a home more affordable, especially for that first time home buyer. I’ll ask those older baby boomers out there, it’s time to downsize and provide more supply to the market.

The NAR said “Multiple years of undersupply are driving the record high home price. Home construction continues to lag population growth. This is holding back first time home buyers from entering the market. More supply is needed to increase the share of first time homebuyers in the coming years even though some markets appear to have a temporary oversupply at the moment.”

With regards to the possible impact of lower mortgage rates, the NAR does an all else equal calculation. “If the average mortgage rates were to decline to 6%, our scenario analysis suggest an additional 160,000 renters becoming first time homeowners and elevated sales activity from existing homeowners.”

Just a reminder by the way, exactly one year ago the average 30 yr mortgage rate was 6.82% according to the MBA when the fed funds rate was 100 bps higher. Today with the lower fed funds rate that average 30 yr mortgage rate is 6.84%.

Existing Home Sales

Months’ Supply

BY Doug Kass · Jul 23, 2025, 12:30 PM EDT

The reason for the quick move higher was a Financial Times report that the U.S. and EU are close to a 15% tariff deal.

BY Doug Kass · Jul 23, 2025, 12:05 PM EDT

Dan and Guy are back together on MRKT CALL today at 11 AM.

Watch because:

* They are both seasoned and bright.

* They are humble and admit their mistakes.

* They don't take themselves too seriously and they follow up (and admit) their mistakes.

* Dan provides timely short-term (stock and option) opportunities.

* Guy has a good historical perspective on the markets.

* The podcast is free.

Let's Go To The Tape! (Hat tip Warner Wolf)

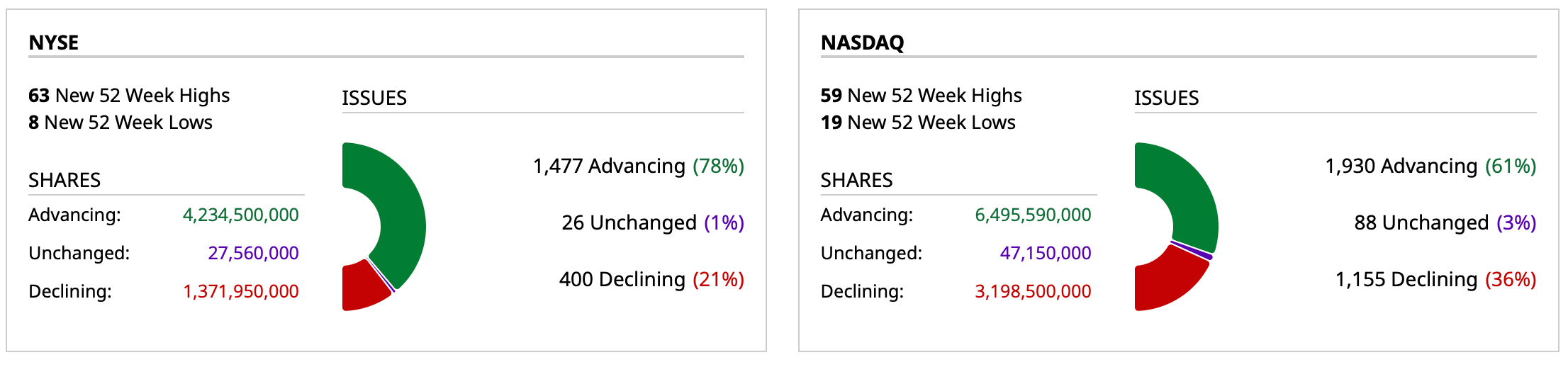

BY Doug Kass · Jul 23, 2025, 11:45 AM EDT

- NYSE volume10% below its one-month average;

- Nasdaq volume 33% below its one-month average; - VIX index: down 3.03% to 16

- VIX index: down 3.03% to 16

BY Doug Kass · Jul 23, 2025, 11:21 AM EDT

With S&P cash +20 handles I am adding to my index call short holdings.

BY Doug Kass · Jul 23, 2025, 11:08 AM EDT

BY Doug Kass · Jul 23, 2025, 11:07 AM EDT

douglas cassel

1 hour ago

Whether you are a fan of Dr. Faustus or Gollum, everyone has the contrary angel at your shoulder telling you that what you are thinking might be wrong. In some ways, I see myself as the embodiment of that concept here. So, in response to the consensus that the market is going nuts, rising out of greed and momentum, I offer the following glimmers of hope. Perhaps the market is going up for some reason?

1) AI might actually work, improving productivity and profits.

2) Crypto might be more than a Ponzi scheme, and represent a paradigm shift in transactions and value.

3) Trump's programs might revitalize US manufacturing, release pent up economic vitality, and not result in the end of the world.

4) Reality might catch up to China, and the perils of a planned economy will slow or end their path to world domination.

I am far more vocal than others here in proclaiming I have little conviction about what the truth might actually be. That position does give me the advantage of not rejecting contrary opinions without consideration. I am emotionally prepared for the bears to be correct, and the markets and crypto to drop dramatically. I have a plan. However, I am also somewhat prepared to profit if the markets continue to rise. I might not make as much as those fully aligned in the proper direction, but that is a trade-off one has to make. Like some people have said, I have lost far more money anticipating market drops than suffering from them. We will see.

Dougie Kass

STAFF

6 minutes ago

The market is a complex mosaic.

I am often wrong and always in doubt.

My bearish thesis has been wrong for 1 1/2 years.

While I have been profitable in 17 of the last 18 months (the only monthly loss was 22 basis points) - while being wrong sided. Good risk control but bad market vision.

Nonetheless, I failed to embrace an opportunity set because of my concerns.

Most of my concerns remain, some are intensifying at a point in time valuation (not EPS growth) has explained the market's rise.

I have now eliminated most of my long book (some of which was purchased in April 2025.

I see about 5x more risk than reward and I see no "margin of safety."

Wrong is wrong but as I constantly update my assumptions I am sticking to my guns.

Hopefully I wont shoot myself in the foot.

BY Doug Kass · Jul 23, 2025, 10:25 AM EDT

Charts from 9:46 a.m. ET:

BY Doug Kass · Jul 23, 2025, 10:05 AM EDT

* It feels like deja vu all over again

* And provides us with another example of an overvalued market and frothy speculation....

Premarket Trading This Morning

BY Doug Kass · Jul 23, 2025, 9:51 AM EDT

From Peter Boockvar:

I want to quickly start by saying that Bleakley Financial Group has officially changed its name to One Point BFG Wealth Partners. Same firm, new brand name fyi that I remain CIO of.

So after seeing the 15% tariff levied on all Japanese imported goods, let's assume that the new baseline tariff rate will be that, instead of 10%, on all imported goods. We import about $3.3 Trillion of goods and let's minus out about $400 Billion of tariff free USMCA stuff from Canada and Mexico and we have $2.9 Trillion that will be taxed at 15% and that equals $435 Billion of taxes on US consumers and businesses and with the weakness in the US dollar, we end up paying about all of that. For context again, US companies pay about $525 Billion of corporate income taxes to the US government.

A bizarre political and economic theory world we now live in I'll argue again where the right embraces these higher taxes, after ridiculing all others, and cheer 'all the money we're taking in' while the left, who typically wants to tax anything that moves, is a critic.

By the way, while we all hope US automakers will be able to sell more cars/trucks into the Japanese market, Japan has NOT had a tariff on US auto imports since 1977. Yes, they have some emission standards and certification requirements but don't for a second think that is why they haven't bought our cars much over the years, even though we do sell vehicles there.

I'll say the positive is that hopefully we're coming to the end of all the tariff cloudiness in terms of what the ultimate rates will be so businesses can plan around them.

I said on Monday that the fate of Prime Minister Ishiba and the inflation worry reason as to why he lost his support was going to directly impact JGB yields. With a trade framework now agreed upon, Ishiba's hold on power looks more tenuous with the replacement more likely than not supporting more fiscal stimulus. ALSO, the BoJ Deputy Governor today said in response, "This agreement is a big major breakthrough. Uncertainty stemming from tariffs will be lowered for Japan's economy." By publicly commenting, this could be a hint of coming rate hikes, though not next week.

So, JGB yields are popping again and this time across the yield curve as we also saw a soft 40 yr bond auction there. The 2 yr yield jumped 7 bps. The 10 yr yield was up by a like amount and matching the highest level since 2008. The 30 yr yield was higher by 5 bps to just shy of its record high dating back to 1999 while the 40 yr yield rose by 8 bps. The TOPIX jumped by 3.2% and we are still long Japanese stocks as they remain inexpensive with this index trading at 16x earnings with a 2.7% dividend yield with solid companies with multinational exposure.

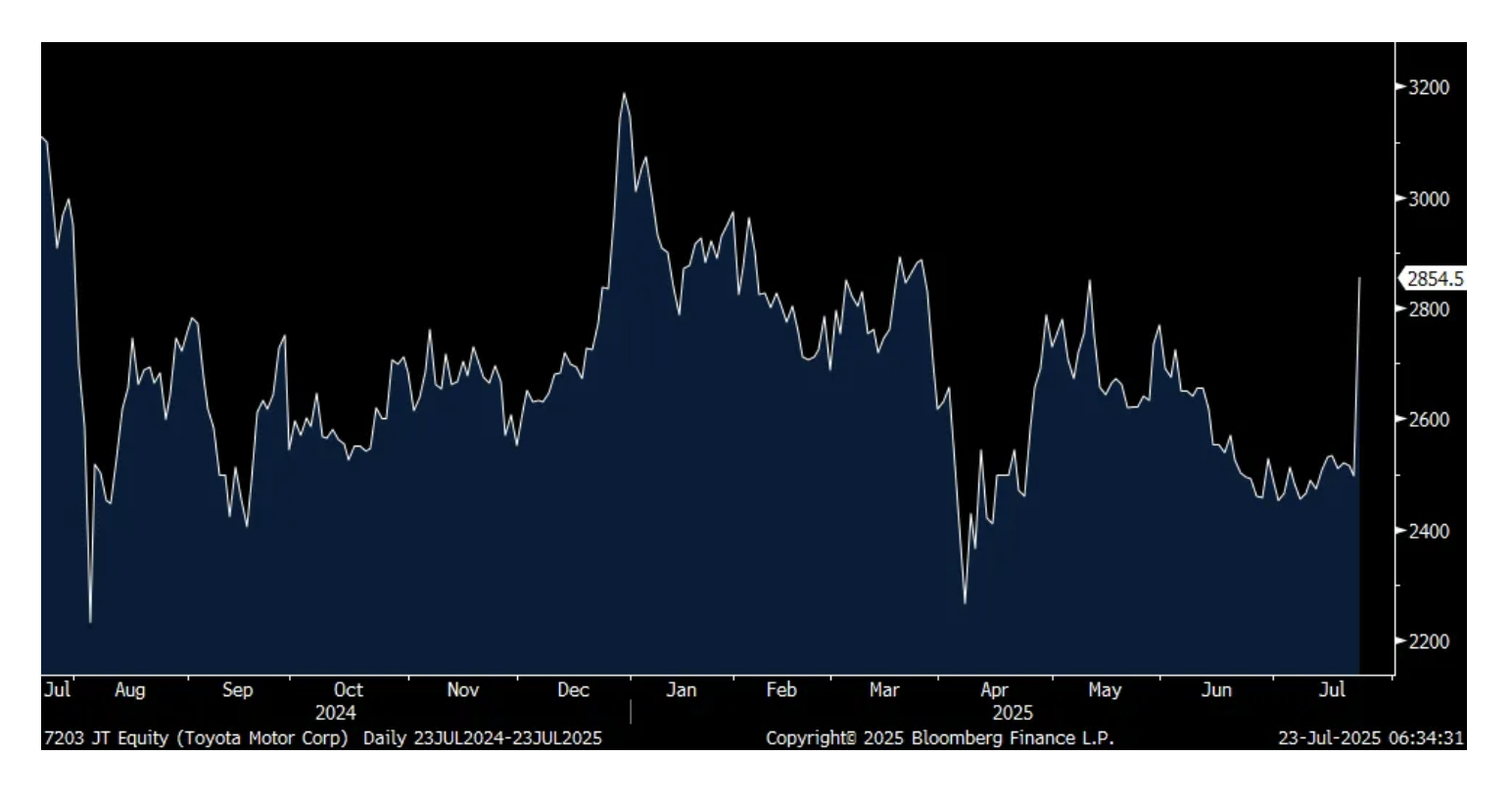

In sympathy yields are rising in Europe and the US. With stocks pricing in 25% tariffs instead of 15%, Japanese auto maker stocks all spiked overnight and drove that TOPIX gain (pun intended). Toyota Motor rallied by 14%, Honda by 11% and Nissan by 8%. European car makers are rising too with Volkswagen higher by 7.3%, BMW by 5% and Mercedes by 5.7%.

10 yr JGB Yield

Now when we all talk about the US dollar and its weakness this year, most view it versus other fiat currencies like the euro, yen and pound which are the biggest components of the DXY. Well, the US dollar continues to tank versus the price of gold which is back to being a stone's throw from a fresh record high. We remain bullish and long.

Toyota Motor

Gold

On the US economy, if the Atlanta Fed is right that Q2 GDP growth will be about 2.5%, that means first half 2025 growth will average about 1% as we need to smooth both quarters together because of the timing distortions of goods purchases/shipments with the tariffs. While I've heard the word 'resilient' a lot from company CEO's in calls so far, that does not imply that growth is strong. We continue to have a very mixed and uneven economy and that's not just my opinion, that is coming from companies themselves if you are reading/hearing what they are saying.

From DR Horton:

“New home demand continues to be impacted by ongoing affordability constraints and cautious consumer sentiment. Where necessary, we have increased incentives to drive traffic and incremental sales. Our cancellation rate remains at the low end of our historical range, indicating that buyers in today’s market are able to qualify financially and are committed to their home purchase, despite the volatility and uncertainty of the current economic environment.”

“I think the incentives throughout the quarter were a bit choppy and we’ve responded to the market…as we work through the end of spring and deep into the summer selling season, our incentives have increased some to maintain our pace.”

“Our recent sales and currently our sales and backlog do reflect a higher cost of incentives. And so the closings that we see into July, August, September, we do expect margins to take that step down that we had previously anticipated would occur in Q3.”

“We’re seeing more of our buyers select an FHA product and we’ve probably been very heavily incentivizing that FHFA product, offering a 3.99%, our most attractive interest rate on the FHA. So that’s led more buyers to select that program.”

From Pulte:

“Our business results continue to demonstrate the benefit of having large and stable operations in the Midwest, Southeast, and Northeast, and these work to offset some of the more challenging market conditions the industry is facing out West and in Texas.”

“Over the past few quarters, our industry has routinely referenced demand conditions as being volatile, and that remains the most accurate description of buyer activity in the first and second quarters. Within a market demonstrating a typical seasonal pattern from month to month, we do see days of strong demand followed by days displaying a step down in activity.”

“Feedback from would be homebuyers indicates a variety of concerns ranging from affordability and the inability to sell an existing home to a slowing economy and the fear of potentially losing their job. In sum, I think consumer confidence is uncertain at best, and confidence is something that’s difficult to solve with a lower price or higher incentive.”

From GM:

“In the US, the industry saw a spike in demand during the quarter due to tariff related sales pull ahead, especially in April and May. Then in June and July, demand returned to levels that are in line with our full year outlook of 16 million units.”

“Despite slower EV industry growth, we believe the long term future is profitable electric vehicle production and this continues to be our North Star.”

“we’re still on track to offset at least 30% of the $4 billion to $5 billion full year 2025 tariff impact through strategic actions such as manufacturing adjustments, targeted cost initiatives and consistent pricing.”

From Texas Instruments whose stock is down 12% pre market on softer than expected guidance with clear evidence that Q1/Q2 saw tariff buying pull forwards and now the hangover is here:

"We continued to see two distinct dynamics at play. First, tariffs and geopolitics are disrupting and reshaping global supply chains...Second, the semiconductor cycle is playing out. Cyclical recovery is continuing, while customer inventories remain at low levels."

Sector wise and keeping in mind the inventory build was needed ahead of finalized tariffs, "The automotive market increased mid single digits y/o/y and decreased low single digits sequentially. Personal electronics grew around 25% y/o/y and grew upper single digits sequentially. Enterprise systems grew about 40% y/o/y grew about 10% sequentially. And lastly, communications equipment grew more than 50% y/o/y and was up 10% sequentially."

On the inventory build with tariffs, "during the last call, when there is a change of dynamics, like tariffs are being added, and I go back to April, customers are sitting on very low inventories. I think it's a good assumption to make that customers will want to have a little bit more inventory, and we did see that phenomenon. We did see that in the early part of the quarter, there was an acceleration of demand." They expect that pull forward to continue into Q3 BUT because Q2 "ran a little hot. This is where I want to be a little bit more cautious into Q3." I bolded to highlight. And China was a main reason as they rushed to buy stuff in Q2.

Specifically on auto, "The automotive recovery has been shallow...that automotive has not recovered yet."

From Coca Cola, a stock we own:

"Two year volume trends were on track in April and May but decelerated in June in the face of adverse weather in several key markets and pockets of consumer pressure. Several markets that were weaker in the first quarter improved volumes sequentially, including the US and Europe."

Specifically on their North American market, "The aggregate spend is holding up. Yes, there's some pressure in those with lower incomes where we're targeting some affordability and some special focus on marketing and occasions. So I think the overall outlook continues to be resilient and we're investing for growth in that."

From Capital One who had a good quarter, is integrating the Discover acquisition and whose stock is rising pre market by about 3%:

"So the US consumer is in a great place here that we continue to see the US consumer as a source of strength in the economy. The unemployment rate remains low and stable, job creation remains healthy, real wages are, of course, growing steadily. Consumer debt servicing burdens remain stable and near pre-pandemic levels. In our card portfolio, we're seeing improving delinquency rates and lower delinquency entries. And payment rates are improving on a y/o/y basis. Now of course, the circumstances of individual consumers and households will vary, as they always do."

"And as we've mentioned in past earnings calls, some pockets of consumers are feeling pressure from the cumulative effects of inflation and higher interest rates. And we're still seeing some delayed charge-off effects from the pandemic, although the improving trend in our delinquency suggest these effects are moderating. But on the whole, I'd say the US consumer is in really quite good shape. And of course, like all of you, we're keeping a close eye on the potential impact of tariffs and other public policy changes."

"And sort of with the tariffs, there's been a lot of uncertainty. But for now, even in that area, of course, we've all seen markets rebound, most economic metrics have remained strong. And we haven't seen any adverse signals in our credit performance in spend or in payments, even in the most leading edge data. We're also watching closely as student loan repayments and collections resume after a pause of almost five years. Specifically, we're watching the performance of card and auto customers with student loans, and especially those customers whose student loans are now being reported as delinquent."

After a jump in mortgage applications ahead of July 4th and then a fall back, they were flattish w/o/w. Purchases though did rise by 3.4% while refi's dropped by 2.6%. The average 30 yr mortgage rate ticked up to 6.84%, a 4 week high but should slip next week with the drop in the 10 yr Treasury yield.

BY Doug Kass · Jul 23, 2025, 9:35 AM EDT

BY Doug Kass · Jul 23, 2025, 9:21 AM EDT

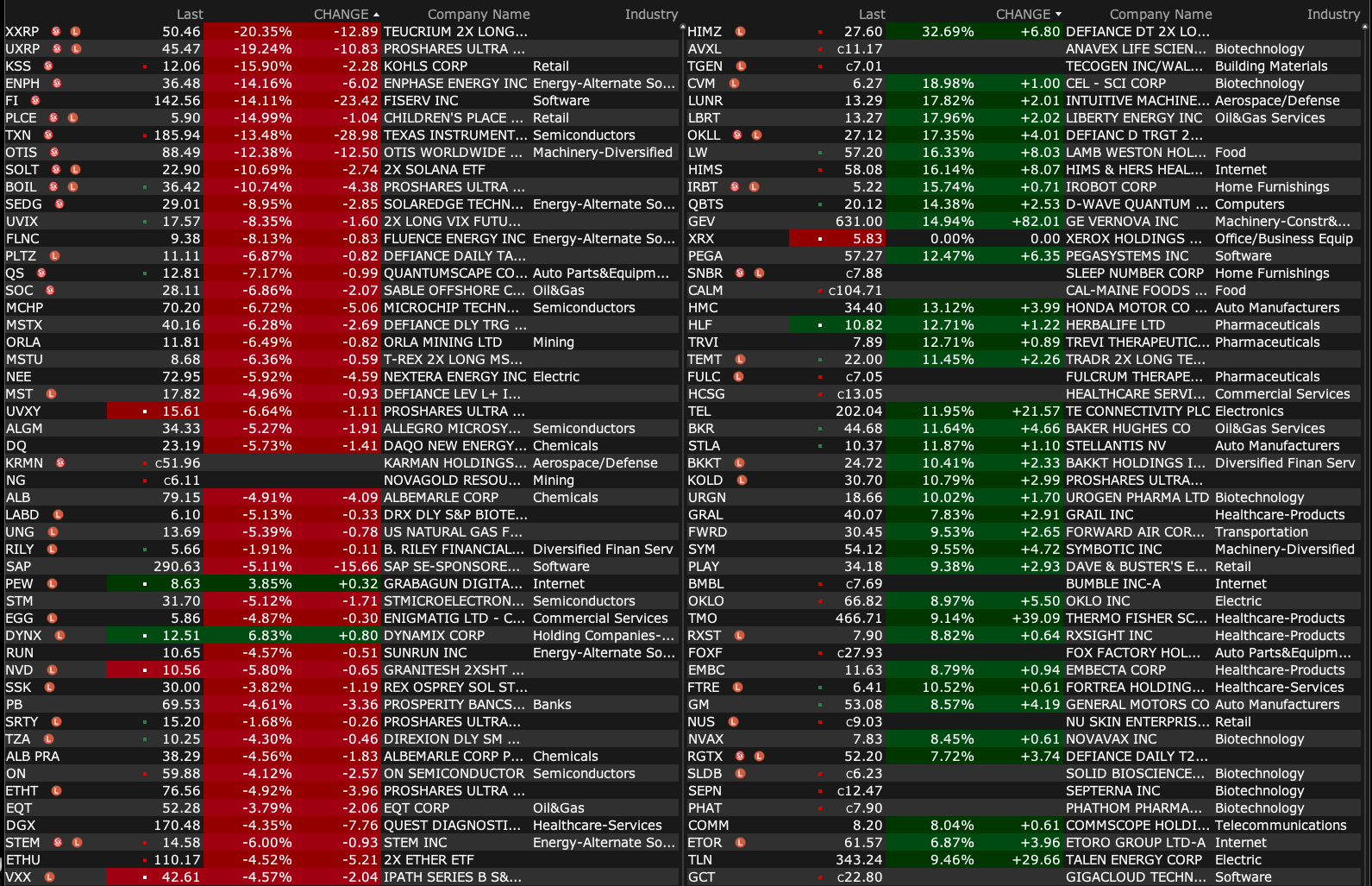

BY Doug Kass · Jul 23, 2025, 9:13 AM EDT

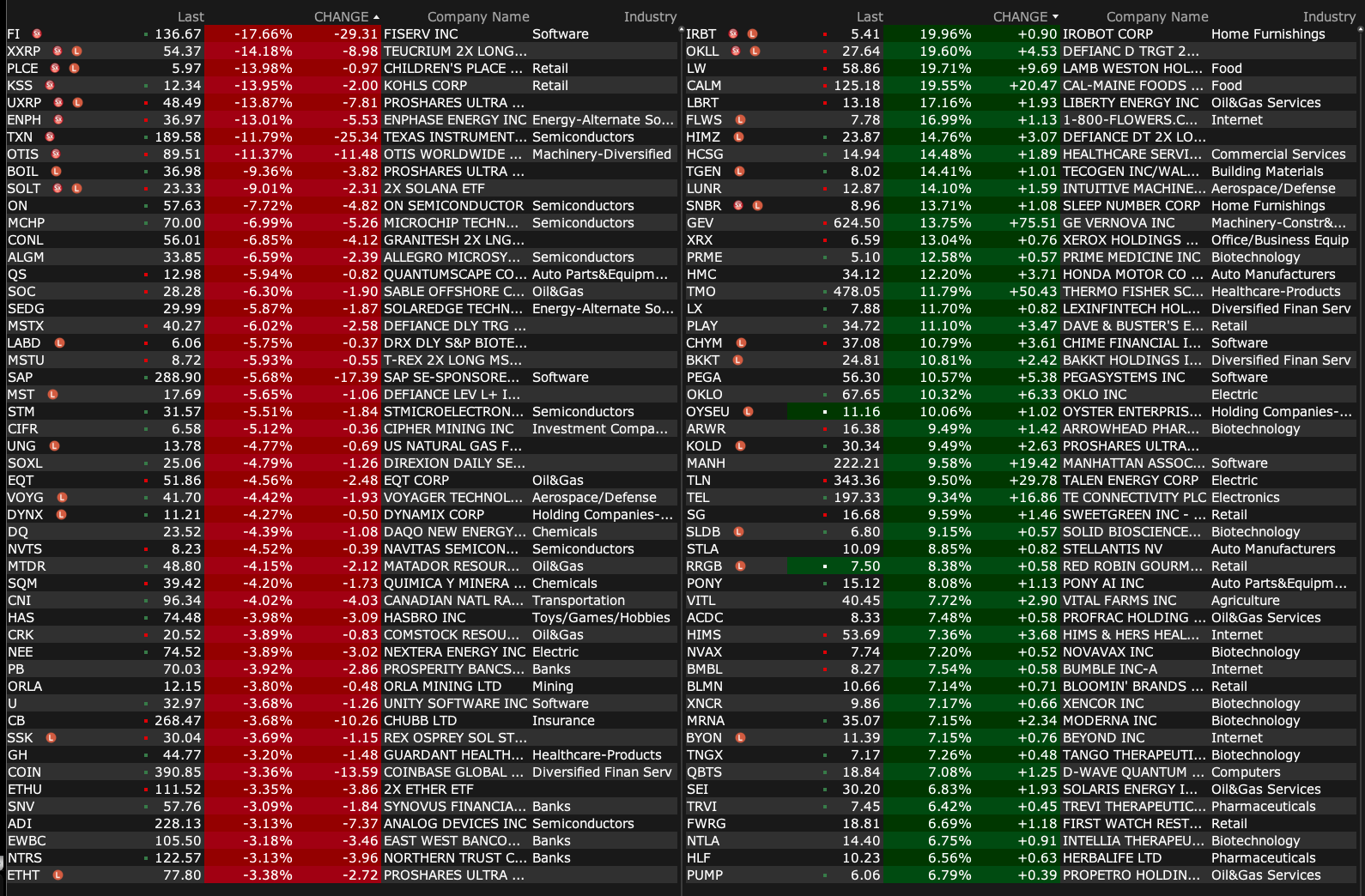

-ABVX +495% (announces positive Phase 3 results from both ABTECT 8-Week Induction Trials Investigating Obefazimod, its First-in-Class Oral miR-124 Enhancer, in Moderate to Severely Active Ulcerative Colitis)

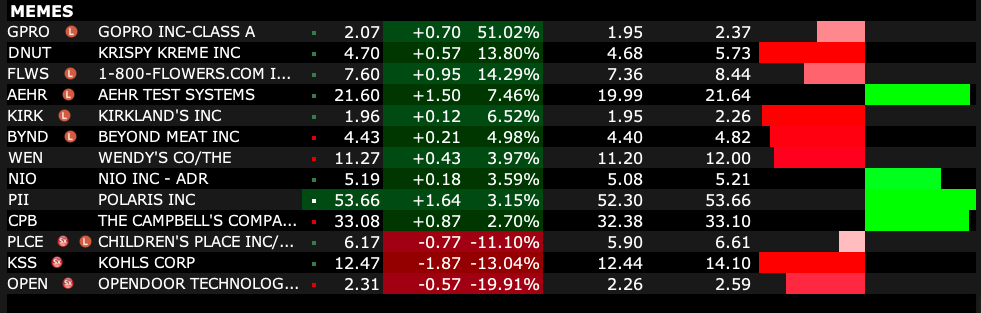

-DNUT +33% (meme stock momentum)

-DALN +16% (confirms receipt of unsolicited non-binding acquisition proposal from MNG Enterprises to be acquired at $16.50/shr in cash)

-PRG +15% (earnings, guidance)

-COOP +8.6% (earnings)

-AENT +6.7% (appoints Amanda Gnecco as CFO)

-LBRT +6.7% (OKLO launches with Liberty Energy a next-gen integrated power solution)

-CALM +6.5% (earnings)

-GEV +6.5% (earnings, guidance)

-LII +6.5% (earnings, guidance)

-APH +5.8% (earnings, guidance)

-LW +5.0% (earnings, guidance)

-TMO +4.3% (earnings)

-HAS +4.1% (earnings, guidance)

-TEL +3.9% (earnings, guidance)

-CLBT +3.2% (U.S. Department of Justice to sponsor Cellebrite for FedRAMP ATO)

-GD +3.0% (earnings)

-COF +2.9% (earnings)

-NTRS +2.7% (earnings)

-BLNK +2.6% (Universal Media Teams with Blink Charging to launch first “EV Totem” installations in Salt Lake City)

-TDY +2.4% (earnings, guidance)

-CSGP +2.2% (earnings, guidance)

-FI -18% (earnings, guidance)

-TXN -9.7% (earnings, guidance)

-ANIP -7.3% (NEW DAY Clinical Trial of ILUVIEN for use in patients with Diabetic Macular Edema (DME) did not reach the threshold for statistical significance)

-OTLY -6.8% (earnings, guidance)

-CNI -4.7% (earnings, guidance)

-MARA -4.7% (files to sell $850M zero coupon convertible 2026 Senior Notes)

-ON -4.7% (lower in sympathy with TXN)

-PEGA -4.6% (earnings)

-T -3.7% (earnings, guidance)

-U -2.8% (hearing BTIG Cuts U to Sell from Neutral, price target: $25)

-HLT -2.2% (earnings, guidance)

BY Doug Kass · Jul 23, 2025, 9:01 AM EDT

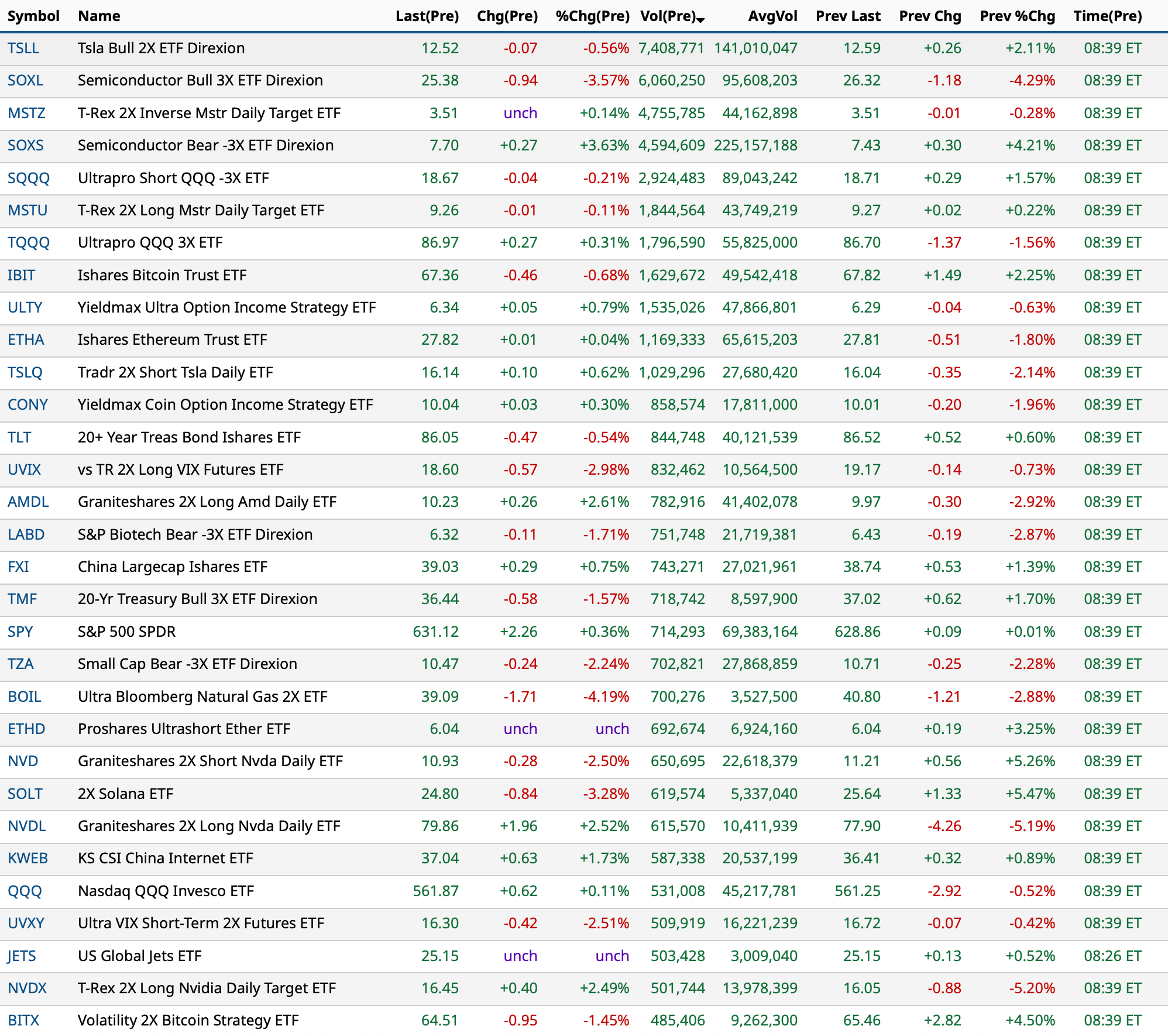

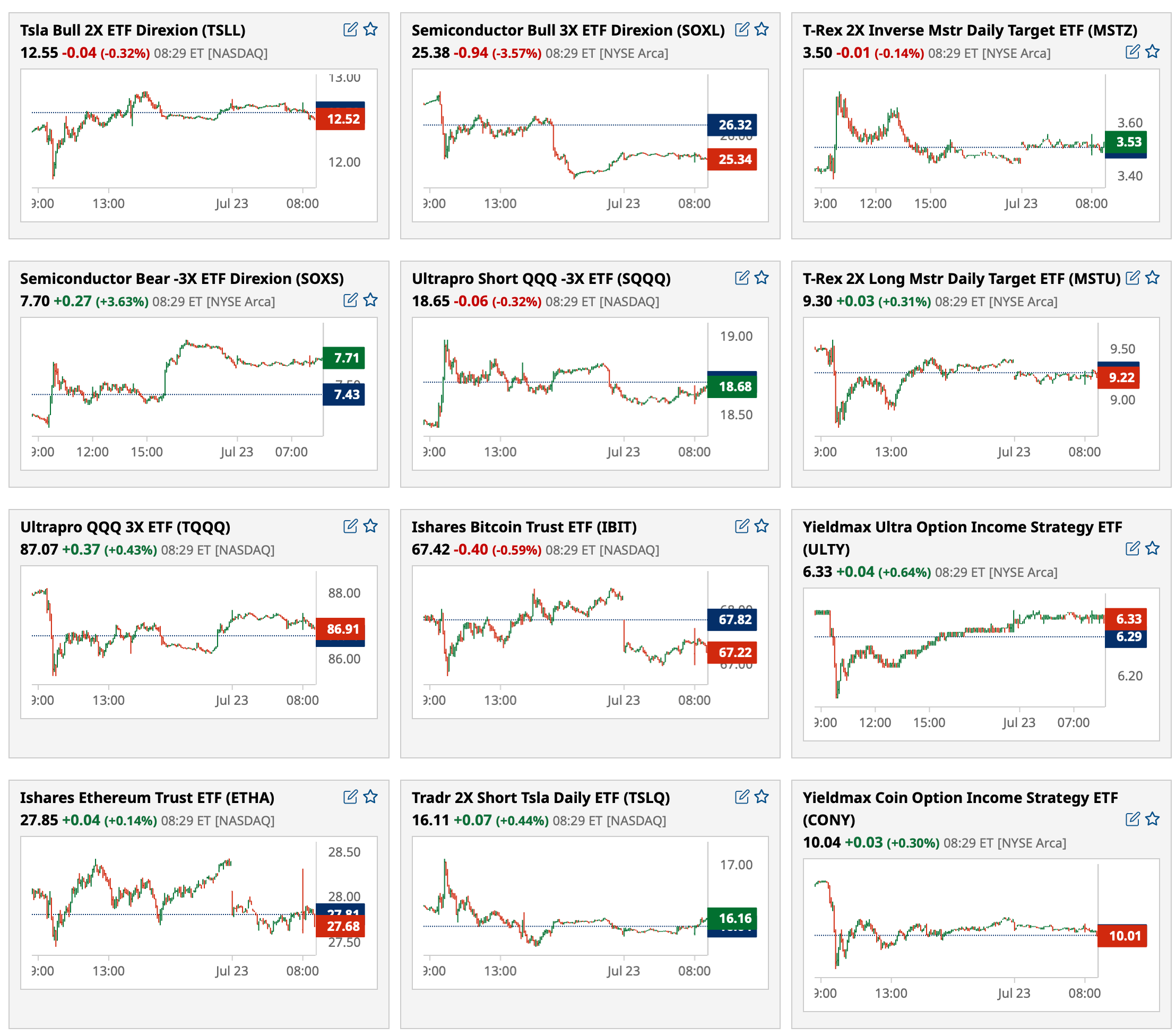

BY Doug Kass · Jul 23, 2025, 8:39 AM EDT

* I guess... I Just Wasn't Made For These Times

Well she got her daddy's car

And she cruised through the hamburger stand now

Seems she forgot all about the library

Like she told her old man now

And with the radio blasting

Goes cruising just as fast as she can now

And she'll have fun fun fun

'Til her daddy takes the T-bird away

(Fun fun fun 'til her daddy takes the T-bird away)

- Beach Boys (Brian Wilson and Mike Love), Fun, Fun, Fun

Not so much fun for this bear.

What a weird trading session Tuesday:

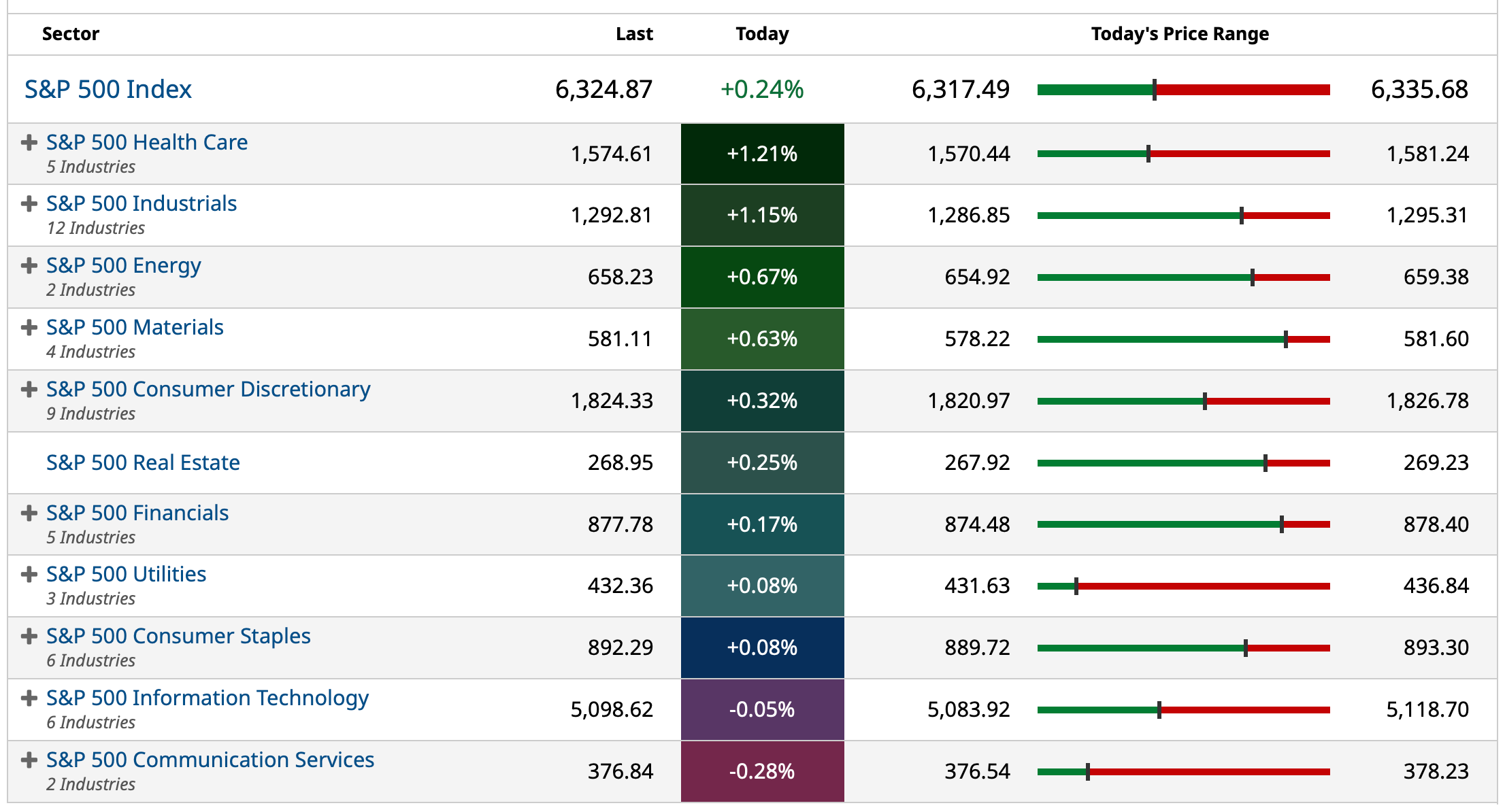

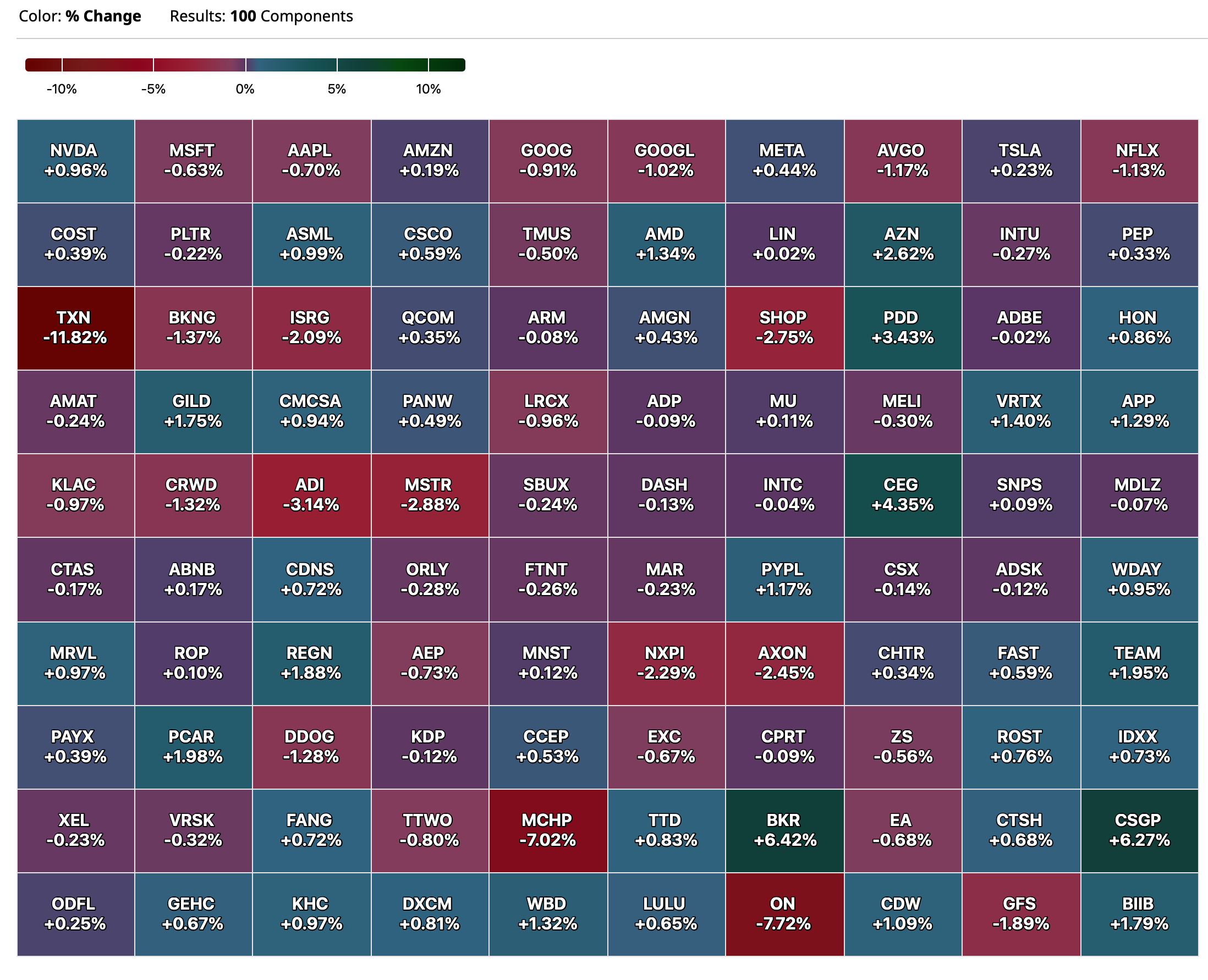

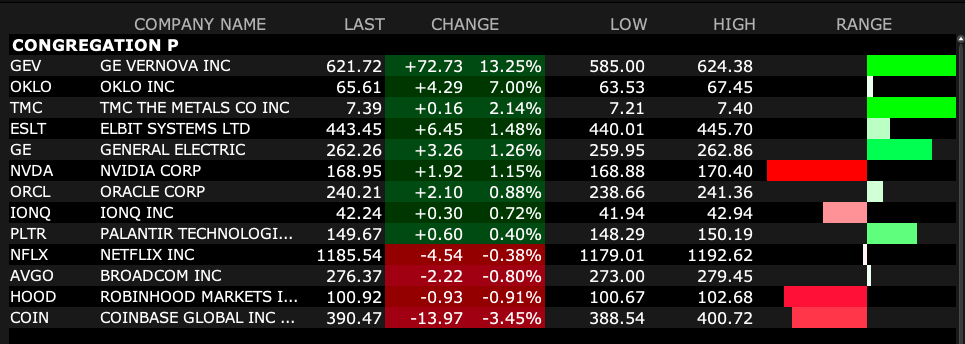

Mag 7 and Congregation P took a back seat to the banks and homebuilders which exploded along with The Russell Index. (I continue to see a roll over in the former market leaders, ergo my large GRNY short).

Market participants continue to reward investors and traders with a steady expansion in multiples over the last two months.

Fears of rising inflation breakevens, a new high in the Commodities Research Index and the journey towards an uncertain backdrop for corporate profit growth (owing, in part, to the imposition of tariffs) continue to be largely ignored. As was Texas Instruments' TXN weak guidance ignored.

Back to the mother's milk of markets, corporate profits. The fact is, though many in the business media say the opposite, earnings estimates are dropping and not increasing — as equities climb.

From Rosie this morning:

"Not just that, but 2025 consensus earnings estimates for the S&P 500 (compiled by FactSet) are -3% lower since the start of the year, but the S&P 500 is up more than +7.0% in a market driven solely by sentiment and multiple expansion (the meme stock trade has made a huge resurrection in the retail investor base)."

I Just Wasn't Made For These Times sums up the situation. The song from the legendary Pet Sounds album addressed the tortured Brian Wilson's feeling of alienation and became one of his defining songs.

If you’re gonna put the word “fun” in a song title not once but thrice, you damn well better deliver on that promise — and this early Beach Boys hit is one of the most gleefully infectious expressions of youthful rule-breaking ever put to wax. The Chuck Berry-indebted guitar riff that opens “Fun, Fun, Fun” is the pop-rock equivalent of a shiny T-Bird tearing out of a parking lot, and the energetic rush of Love’s lead vocal keeps this T-bird in high gear as it races all around town on a sunny California day. The lyrics aren’t poetry, but they do exactly what they need to without a wasted word, spinning a concise slice-of-life tale of what the ideal day looked like for an American teen in the early ‘60s: hamburgers, loud radios, fast cars, flirting and pissing off the old man.

- J. Lynch

BY Doug Kass · Jul 23, 2025, 8:00 AM EDT

BY Doug Kass · Jul 23, 2025, 7:10 AM EDT

From JPMorgan:

US: Futs are higher following the US / JPN trade deal, triggering a global risk-on rally. Japan will pay a 15% tariff (down from 25%) with the auto sector tariffs reduced to 15% (also from 25%). This may reduce pressure on the Aug 1 deadline. US / China mtg next week to work on a trade deal with either a deal or an extension most likely. Pre-mkt, US futs are lagging their global counterparts as Value is leading. Mag7 names are all higher with GOOG/TSLA earnings today. Cyclicals are unsurprisingly higher. Also, Meme stocks are ripping pre-mkt, adding 15% - 45% depending on the name. Bond yields are rising across the globe as growth expectations reset higher. USD is flat and cmdtys are mixed with Energy/Ags weaker and Metals rallying. Today’s macro data focus is on housing.

and...

JPM MARKET INTEL EQUITY & MACRO NARRATIVE

Yesterday was a day characterized by a low magnitude of moves in major indices but violent moves under the surface. While SPX, NDX, and RTY closed +6bp, -50bp, and +79bp, respectively, we saw large moves in things such as Homebuilders (JP1BBLD Index, +9.1% or +3.6z), Popular Inflation Shorts (JPINCRWS Index, +3.6% or +2.3z), High Short Interest (JPTASHTE Index +2.7% or 0.9z) with Momentum L/S (JPMPURE Index -3.9% or -3.0z) and Value L/S (JPPQVAL Index +2.7% or +1.9z).

· MOMENTUM UNWIND – Last week, we saw our Momentum Factor basket (JPMPURE Index) retract ~45% of its losses from unwind that began at the end of June. After yesterday’s move, the unwind set a new low and the factor is down ~8% from its highs. Speaking with Manish Sinha (Delta-One, Factor Spec), he tells me that typically, we can expect Momentum to decline 12% –15%, and a 20% decline would be extreme. Please contact your JPM Sales Coverage if you would like to arrange a call with Manish.

SPX vs. MOMENTUM FACTOR vs. BETA FACTOR

BETA UNWIND – Our Beta Factor L/S (JPBPURE Index) had a more than 2% intra-day reversal, closing in the green. Similarly, ARKK closed down 55bps but well off its intraday low of -3%. These moves are happening with very light Retail participation. Our JPM Retail Participation Tracker from Emma Wu showed that Retail investors bought $28mm vs. $519mm (1-month avg, -1.2z). So, this appears to be follow-on covering from the HF community which had a more than 2z short covering day last Thursday (July 17). The resurgence of the Meme Rally makes single stock shorting more treacherous; our JPM Meme basket (JPXXMEME Index) is up 7.9% MTD vs. SPX +1.7%.

· TRADE – (i) US / China to meet in Stockholm and it appears that pushing back of the Aug 12 tariff deadline is likely; Trump said that he will meet Xi in China in the ‘not too distant future’. (ii) US / Japan talking are ‘going very well’ and the catalyst for a deal may have been the Japanese elections. (iii) Trump re-announced a trade deal with Indonesia; the deal is said to include a supply of critical minerals with Indonesia also dropping 99% of its tariffs. The 19% tariff for Indonesia is down from 34% on ‘Liberation Day’. (iv) US / Philippines are said to have an imminent deal and Trump cut the 20% tariff to 19% which remains above the 17% level from ‘Liberation Day’. (v) Separately, Bessent claims that the US will return to 3%+ real GDP growth by 26Q1.

· POWELL – Having fielded a number of questions on this topic some thoughts, (i) replacing Powell does not guarantee rate cuts since the Fed chair is only one vote on the FOMC and the most recent Fed Minutes and subsequent comments from those not gunning for Powell’s job reveal a wait-and-see approach given resilient labor market with inflation pointing higher; (ii) at this point a resignation and a firing are likely to have the same outcome … loss of confidence in the Fed being independent which should mean that the yield curve twists steeper. What would be the impact on markets? I wrote this last week: In terms of market behavior, the yield curve twisted steeper, the USD declined, gold/silver moved higher, and in stocks all 3 major indices moved lower with Semis underperforming but ARKK among the best performers. EM and International Equities outperformed following the USD depreciation. Interestingly, our JPM Defensives baskets (JPAMDEFN Index) moved higher while defensives sectors such as Staples and Utilities declined. Longer-term, should another episode materialize with stronger magnitude the risks to the real economy come via the housing market as mortgage rates move higher with the 30Y yield.

o FEROLI: How Safe is Powell’s Job – his full note is here

· PREPPING FOR AUGUST 1 – The consensus appears to be that the Aug 1 deal is likely be pushed back. If not, the market is likely to take a leg lower given that many of the tariffs via tariff letters are at levels exceeding their ‘Liberation Day’ levels which triggered a 10% correction in two days. While we do not think the magnitude of a pullback approaches that level, if tariffs are left in place then we likely move lower on that day but more heavily on Monday, Aug 4 if there are no updates over the weekend. As referenced yesterday, SPX options expiring on Aug 1 are only pricing in the NFP move of ~1%, which is aligned with recent releases, meaning that you get both the trade deadline and some MegaCap Tech earnings releases for free. In the event that the trade situation is adjudicated on/before Aug 1, would consider rolling those Aug 1 options to Aug 15 to capture CPI. Ex-trade, the primary macro risks are (i) softer NFP print and/or (ii) a hawkish CPI print.

BY Doug Kass · Jul 23, 2025, 6:55 AM EDT

BY Doug Kass · Jul 23, 2025, 6:45 AM EDT

* The technical mavens are all optimistic on gold this morning...

Bonus — Here are some great links:

How Low Volatility Streaks End Matter

BY Doug Kass · Jul 23, 2025, 6:30 AM EDT

BY Doug Kass · Jul 23, 2025, 6:20 AM EDT

BY Doug Kass · Jul 23, 2025, 6:10 AM EDT

The S&P Short Range Oscillator moved to 1.71% from 1.3%.

BY Doug Kass · Jul 23, 2025, 5:55 AM EDT

BY Doug Kass · Jul 23, 2025, 5:45 AM EDT