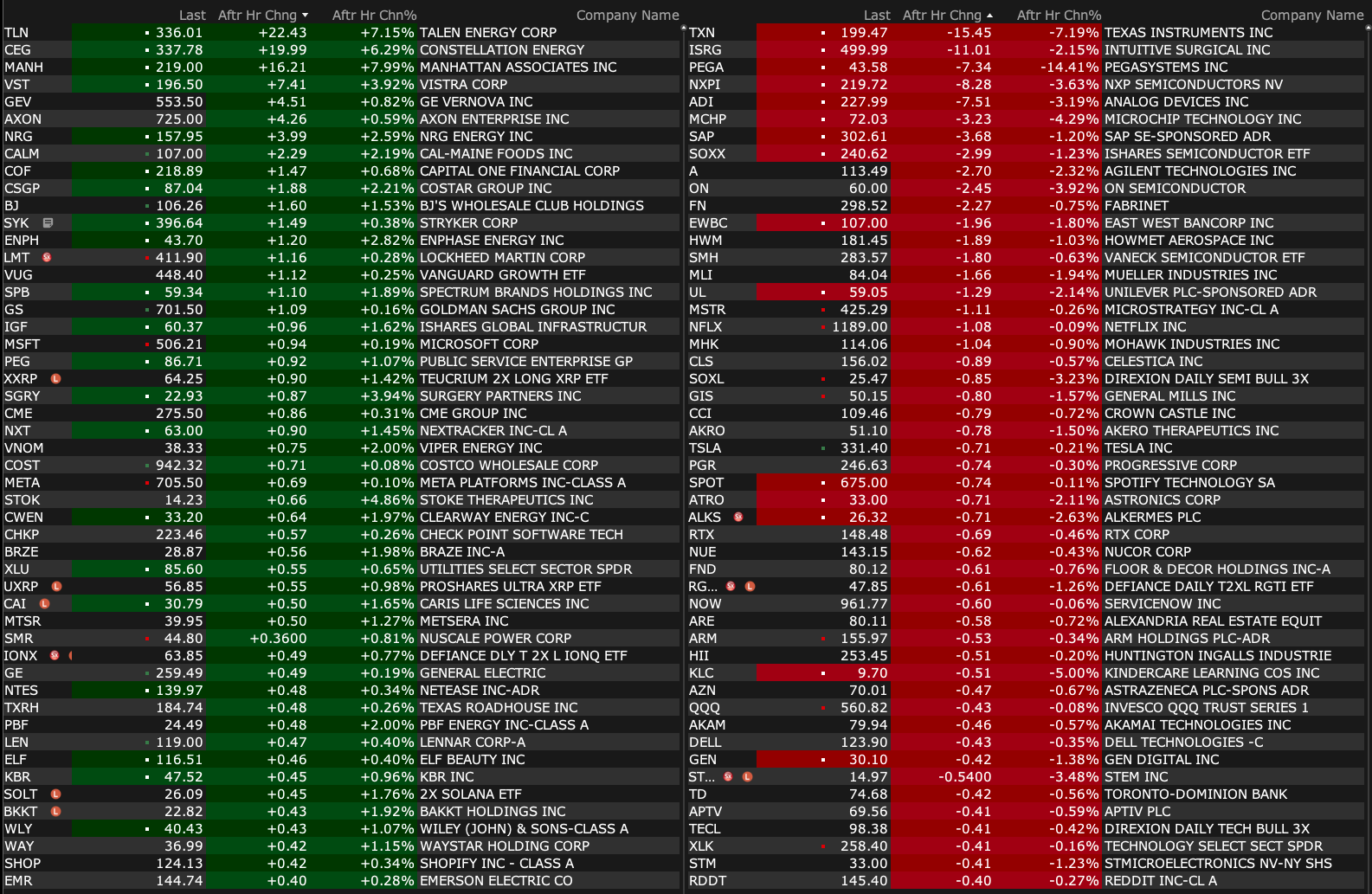

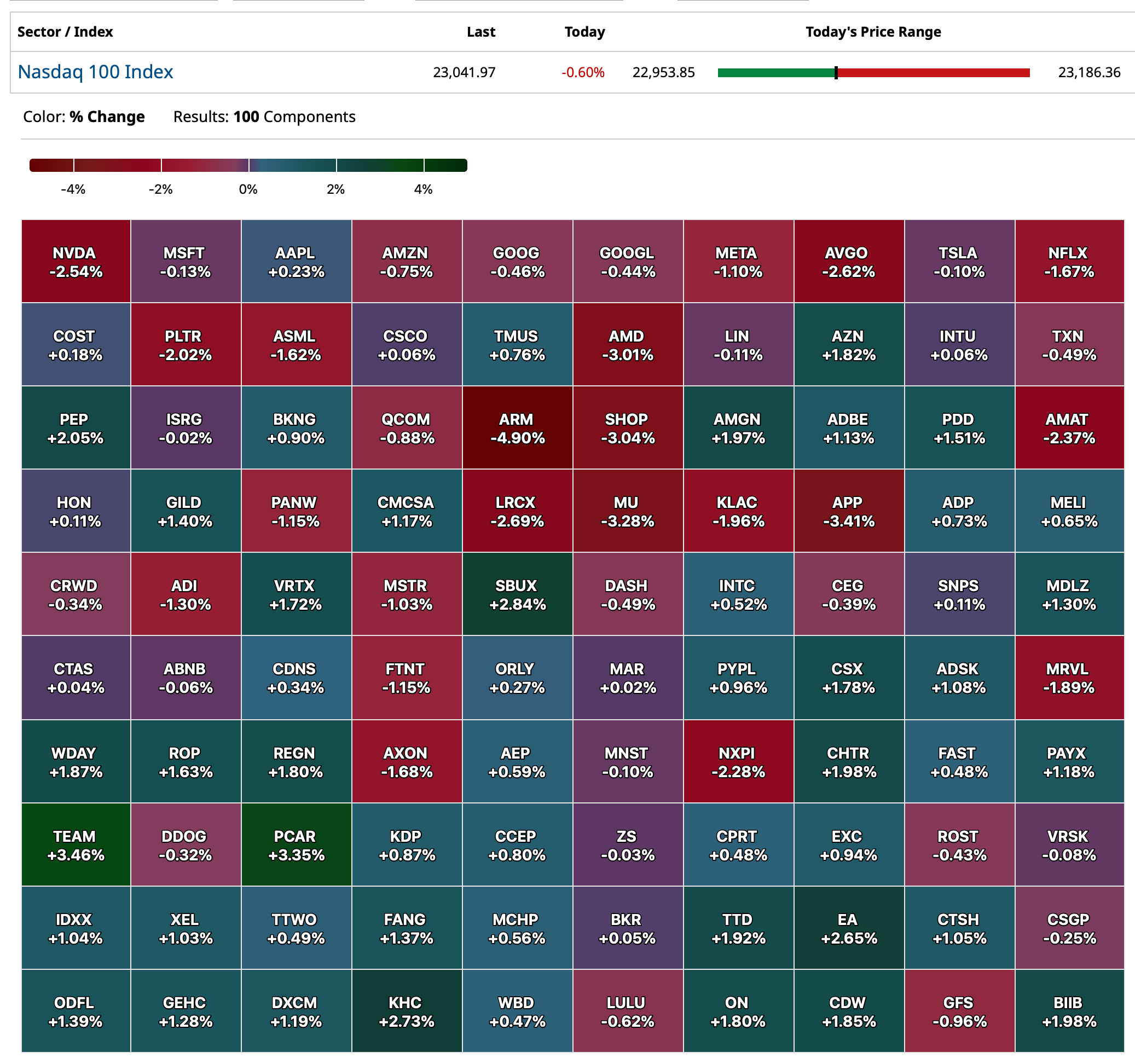

Tuesday's After-Hours Movers

BY Doug Kass · Jul 22, 2025, 4:38 PM EDT

BY Doug Kass · Jul 22, 2025, 4:38 PM EDT

BY Doug Kass · Jul 22, 2025, 4:31 PM EDT

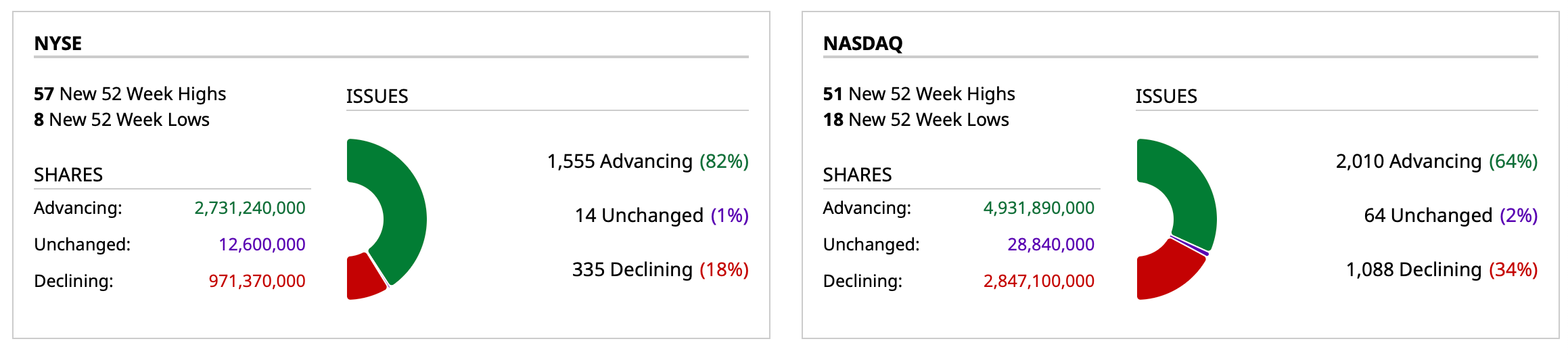

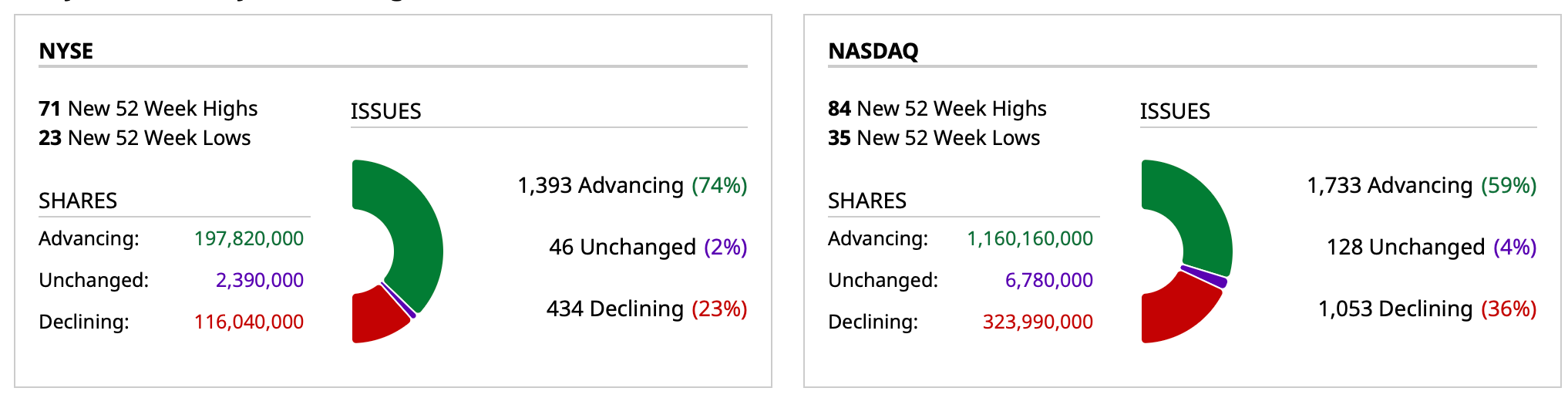

- NYSE volume 9% above its one-month average;

- NASDAQ volume 23% above its one-month average;

- VIX index: 16.65

BY Doug Kass · Jul 22, 2025, 4:18 PM EDT

BY Doug Kass · Jul 22, 2025, 3:47 PM EDT

I have a 3:30 PM research call.

Back after the close.

BY Doug Kass · Jul 22, 2025, 3:30 PM EDT

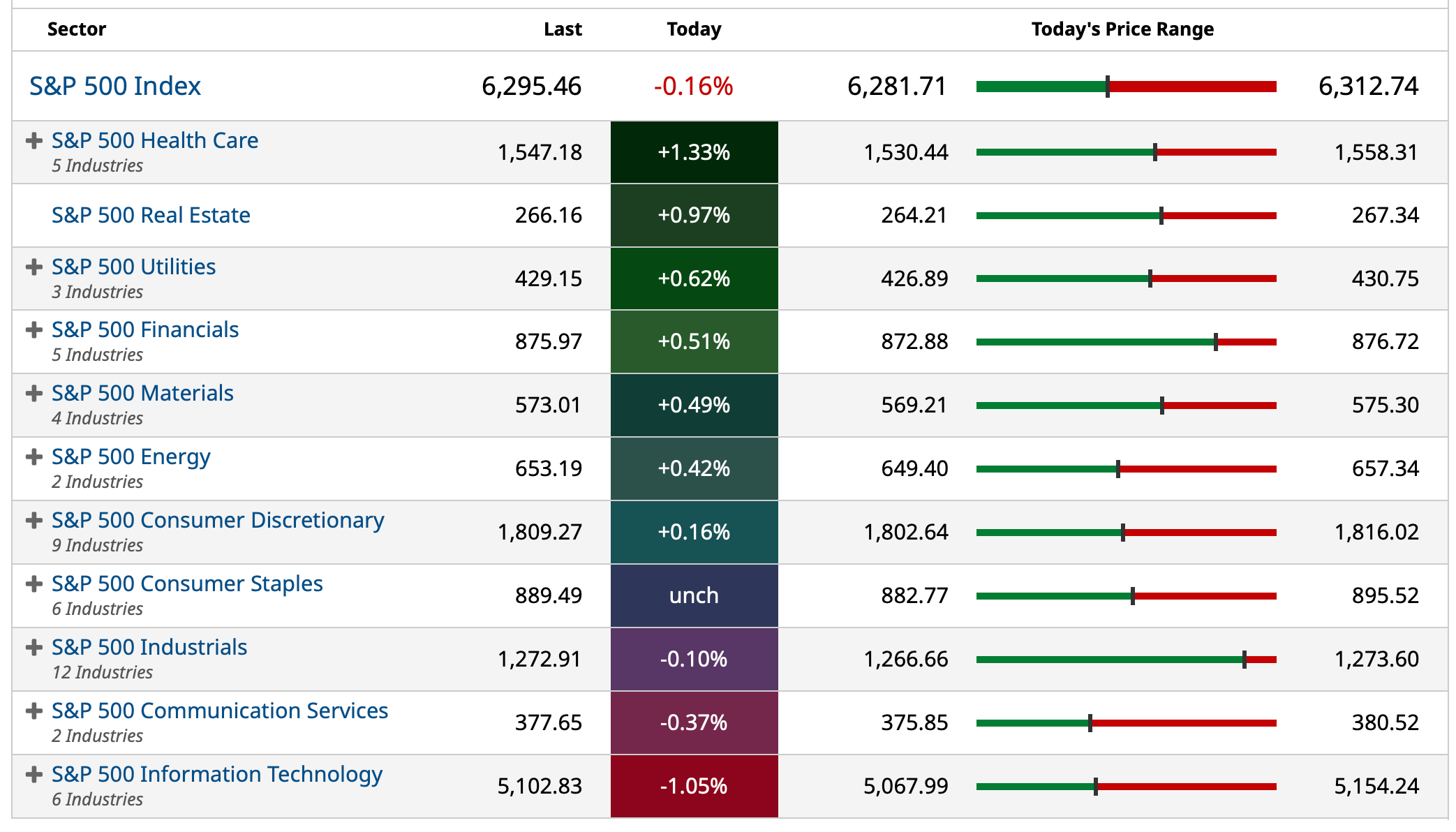

As of 3:00 p.m.:

BY Doug Kass · Jul 22, 2025, 3:05 PM EDT

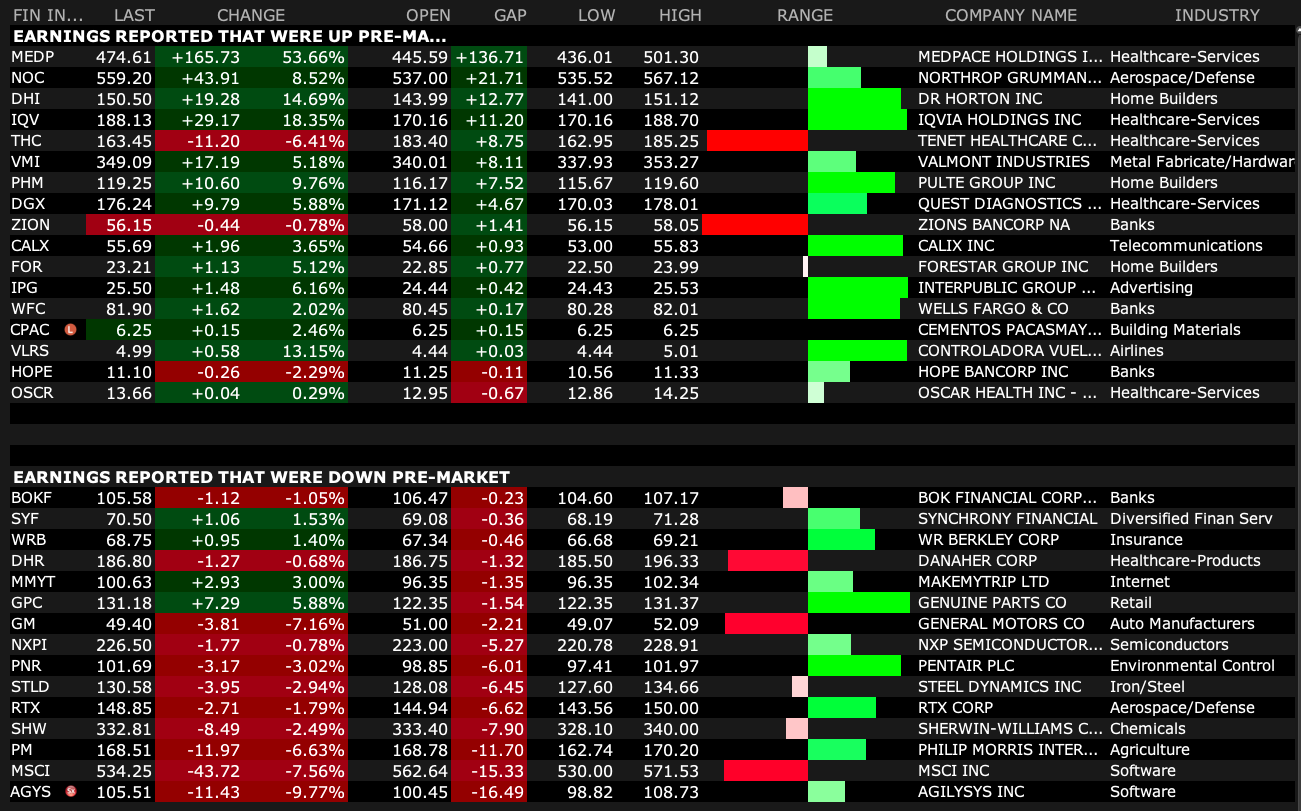

Several earnings reporters that have since reversed from opening gap price.

BY Doug Kass · Jul 22, 2025, 12:57 PM EDT

- NYSE volume 21% above its one-month average;

- Nasdaq volume 34% above its one-month average;

- VIX index: up 1.92% to 16.97

BY Doug Kass · Jul 22, 2025, 11:05 AM EDT

With S&P cash rallying to being down only -7 handles I am adding to my short index calls.

BY Doug Kass · Jul 22, 2025, 10:43 AM EDT

Dougie Kass

STAFF

9 minutes ago

Cole was approved by the Senate to be the Head of DEA.

Cannabis stocks rallied on the news.

However, my contacts say Cole is adamantly against rescheduling - though a number of people (Mike Tyson, etc.) are trying to have the President go over the top on rescheduling.

I will be out of most of my cannabis equities by the close of trading today.

BY Doug Kass · Jul 22, 2025, 10:35 AM EDT

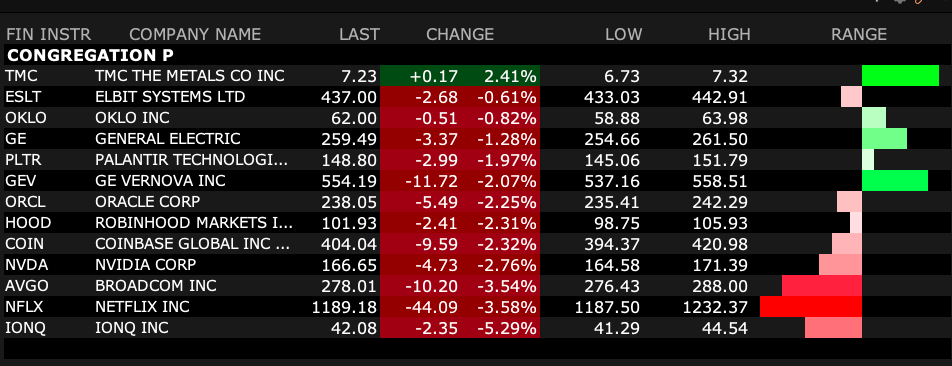

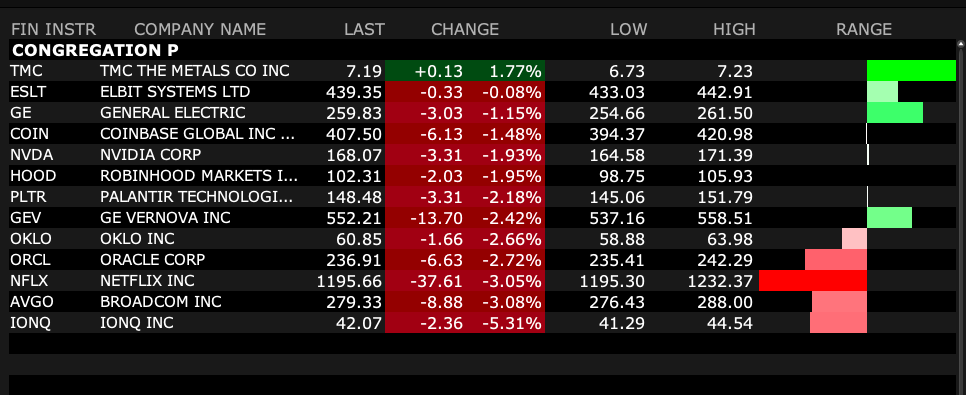

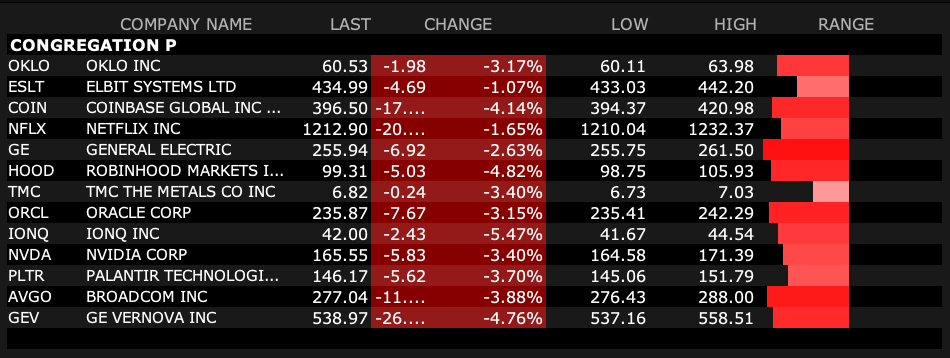

All the constituents of Congregation P are down on the day:

BY Doug Kass · Jul 22, 2025, 10:17 AM EDT

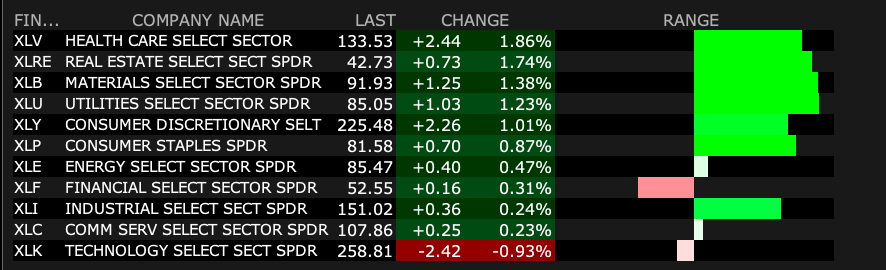

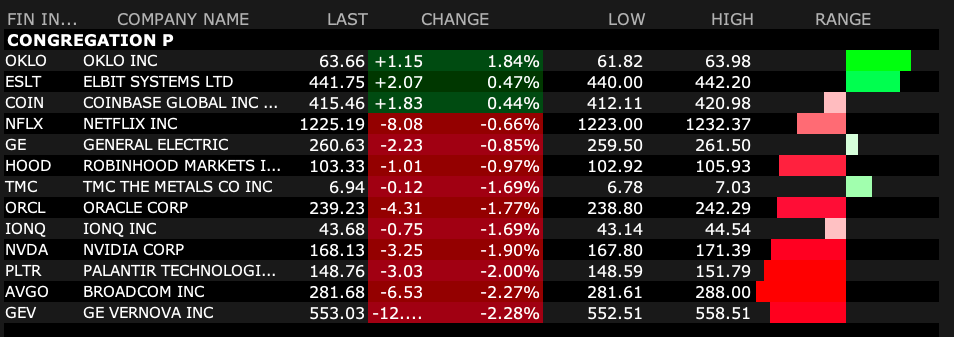

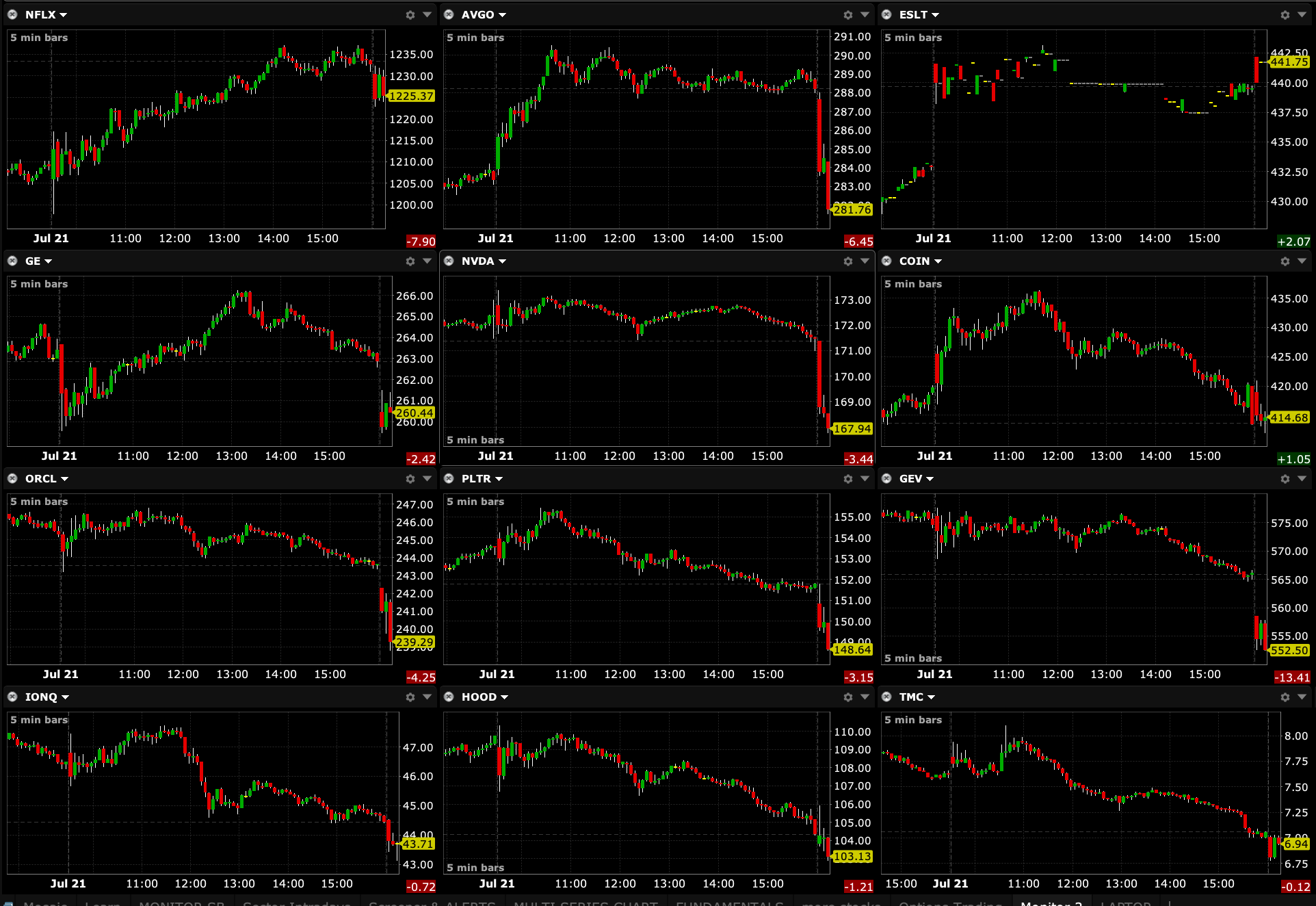

Well, isn't that special! Charts from 9:44 a.m., with mini-graphs:

BY Doug Kass · Jul 22, 2025, 10:06 AM EDT

GRNY (GRNY) is my largest ETF short because its components (Congregation P) may be the most vulnerable equities extant.

BY Doug Kass · Jul 22, 2025, 10:01 AM EDT

With S&P cash flat, I am expanding my short Index calls.

BY Doug Kass · Jul 22, 2025, 9:35 AM EDT

From Peter Boockvar:

With Japanese markets opened after Monday's holiday close, the response to the election results were muted in both JGBs and the Nikkei with yields little changed as were stocks. The yen today is flat after yesterday's rebound. If there is one institution in Japan that didn't get the message of the election it was the BoJ. Bloomberg is reporting that "Bank of Japan officials see little need to shift their policy stance of gradually raising interest rates in the wake of Prime Minister Shigeru Ishiba's latest election setback, according to people familiar with the matter."

They've been so 'gradual' with the rate hikes that Ishiba lost his parliamentary support from both sides of the house because of the voter pushback against inflation rising faster than wages. That said, they still plan on raising interest rates according to "the people" cited in the article so there remains higher JGB yield risk which will continue to have global repercussions depending on to what extent. The BoJ meets next week and no change in policy is expected yet as they await to see the results of the trade negotiations with the US side.

Finally, with respect to JGB yields and the possible consequence of the election results, "While the outcome of the election doesn't change the BoJ's policy trajectory for now, some officials see a need to monitor any upward impact on inflation if the government does indeed loosen fiscal policy considerably, the people said. The officials see risks rising for inflation after price growth turned stronger than they expected mainly due to a surge in rice prices and other food-related items, they said." I believe we are not out of the woods with respect to the risk of rising long-term interest rates and I do expect a continued rise in global long-term interest rates.

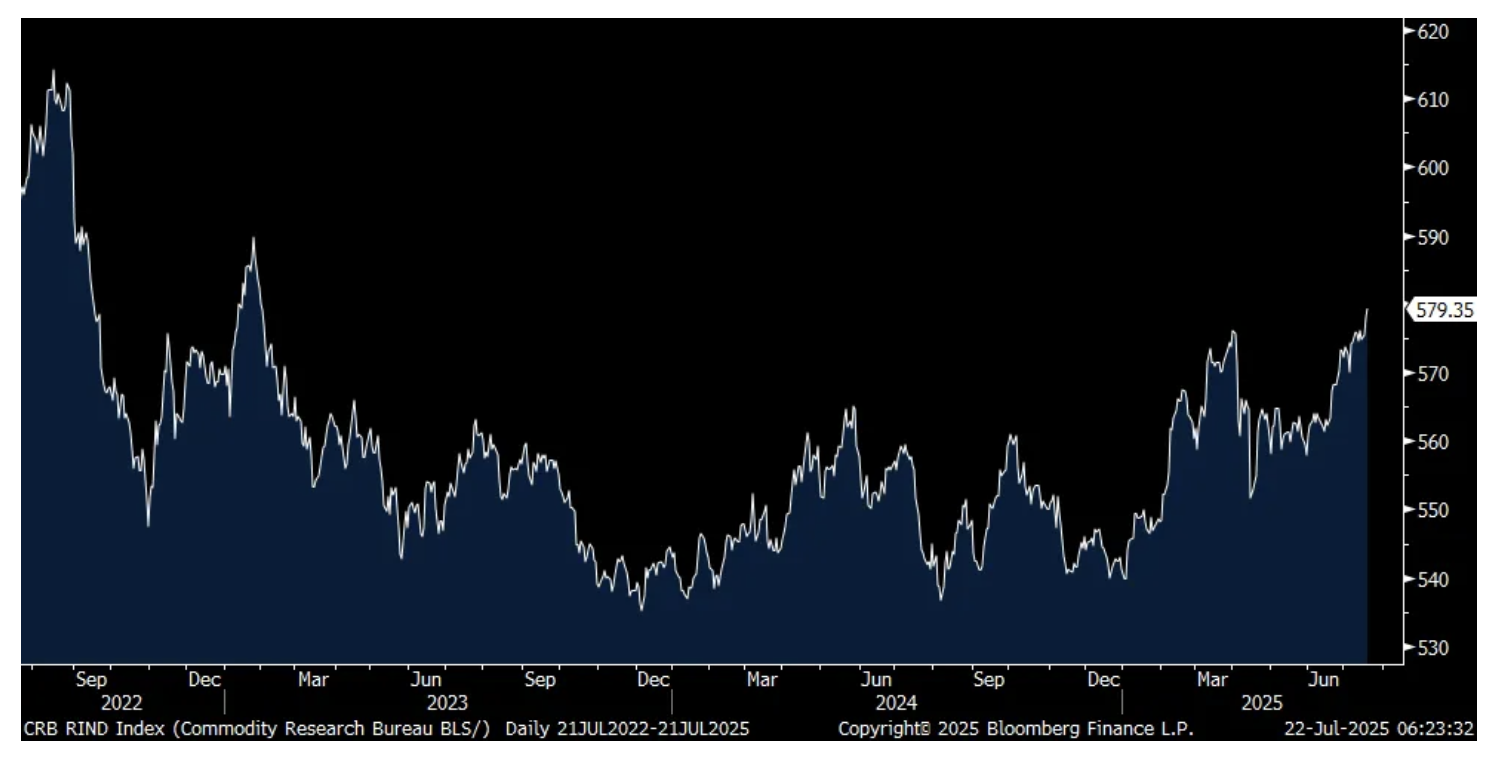

Speaking of inflation, the CRB raw industrials index has broken out to the upside as it closed yesterday at the highest level since February 2023. I argued a few weeks ago that this was shaping up to be a good looking chart. What I like about this index is that it includes some commodities that don't trade on markets and thus are not speculated on. They are also all spot prices. The index includes burlap, print cloth, tin, copper scrap, rosin, wool, cotton, rubber, zine, hides, steel scrap, lead scrap and tallow.

CRB Raw Industrials Index

DR Horton stock is rallying pre market after earnings and said this in their earnings release:

"New home demand continues to be impacted by ongoing affordability constraints and cautious consumer sentiment. We expect our sales incentives to remain elevated and increase further during the fourth quarter, the extent to which will depend on the strength of demand during the remainder of summer, changes in mortgage interest rates and other market conditions."

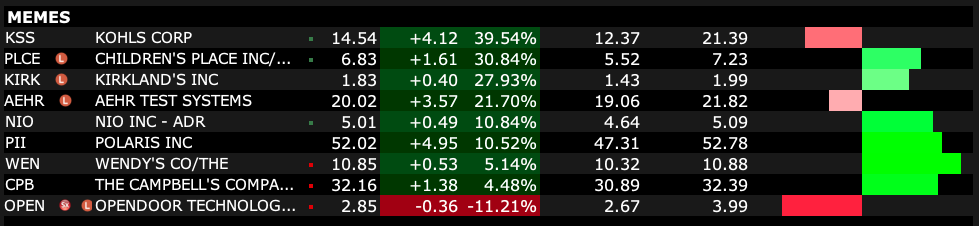

Speaking of a housing stock, that was some rise in Opendoor, a company that flips homes and now has become a meme stock because some random money manager was tweeting about it. The stock closed Q2 at $.53 and traded as high as $5 yesterday. Let's party like its 2021.

OPEN

Pulte Homes just reported too and said this:

"Over the course of the 2025 spring selling season, we saw consumers dealing with a range of issues from high interest rates and challenged affordability to macro concerns about the strength of the economy. We are encouraged, however, by the positive consumer response we saw to the pullbacks in interest rates in late June and at times earlier in the year." I'll add, there really wasn't much of a change in mortgage rates as they fell 13 bps in June and have since risen 3 bps in July to a still elevated 6.82% that risks going higher if the Fed aggressively cuts rates under someone else other than Powell.

From Domino's Pizza:

“Our second quarter financial results continue to be impacted by a challenging macro backdrop.”

Comps rose 3.4% y/o/y “on the strength of our parmesan stuffed crust pizza launch, which drove positive transaction counts. Average ticket benefited from 1.4% of pricing and the addition of stuffed crust, which carries a higher price point…Our carryout comps were up 5.8%.”

“we continue to expect our US comp for the year to be 3% and that it will be higher in the 2nd half due to the timing of our initiatives. This assumes that the pressured macro environment we have seen through the first half of the year in QSR pizza remains the same.”

“I think the important thing to understand right now is whether it’s pizza or burgers or QSR in general, there is pressure because consumers are looking for value and what you’re seeing is a restaurant industry where we’re providing a lot of value.”

NXP Semiconductor is down sharply pre-market, where half their revenue is to the auto sector with the balance in mostly other industrial markets. Revenue fell 6% y/o/y and guidance disappointed the markets. Their call is this morning.

Speaking of autos, the GM numbers were about in line but margins fell. In their slide deck they said "Calendar 2025 gross tariff impact unchanged at $4-5B...Making solid progress to mitigate at least 30% of this impact through manufacturing adjustments, targeted cost initiatives, and consistent pricing." So by my math, they will or we the customer will be eating about $2.8-$3.5b of the tariffs.

From Steel Dynamics, a supposed beneficiary of the steel tariffs but whose stock is down pre-market:

"During the second quarter 2025, steel pricing stabilized at higher levels, resulting in a significant sequential improvement in consolidated operating income of 39% and adjusted EBITDA of 19%."

But, "The uncertainty regarding trade policy continues to cause hesitancy in customer order patterns across our businesses, despite healthy underlying demand factors, such as manufacturing onshoring, infrastructure program funding, and increased regionalization of supply chains in the US. This hesitancy, combined with an inventory overhang of coated flat rolled steel, resulted in lower steel and steel fabrication shipments in the second quarter 2025."

From Sherwin Williams which is down sharply pre-market:

"Given the demand softness in the quarter, which we expect will continue if not deteriorate in the second half of the year, we aggressively accelerated and increased our restructuring actions, resulting in pre-tax expenses of $59 million."

They saw strength in residential repaint but weakness in "commercial, new residential and property maintenance." Also, "Consumer Brands Group sales decreased resulting from continued soft North American DIY demand" and FX influences. Performance coatings saw growth in Europe, Asia and Latin America but "offset by a decrease in North America...Packaging remained the strongest performer as sales increased by a double digit percentage."

From Zions Bancorp, a regional bank based in Salt Lake City:

"While we see some signs of economic slowing, the magnitude and imminence of tariff related risks noted in our first quarter call feel like they've abated somewhat. As a result, we are incrementally more sanguine about potential growth in our outlook."

If there is one industry that is particularly sensitive and vulnerable to tariffs it is the toy business. The WSJ has an article on this today and they quote Greg Ahearn, the CEO of the Toy Association, an industry trade group. They write that he said "Roughly 60% of toymakers have executed layoffs in the past two months...'You can see the severity' hitting the industry, he said."

"The cuts span from giants such as Hasbro, which last month laid off 3% of its global workforce in a cost cutting push, to smaller companies like Lovevery. The company, which sells subscription based play kits and learning programs, enacted a 20% staff reduction in May, just months after posting its first quarterly profit."

More from Ahearn, "Hasbro will lay off 3% of employees, medium sized companies will lay off 20%, and small entrepreneurs are indicating that they're at risk of going out of business...These tariffs aren't numbers our industry can work under."

So, all that money that the US govt is collecting is coming from the US private sector, and unfortunately bankrupting some of the contributors to it. What is further maddening to me is that there was no circumstance under which that we were going to start making toys again in the US, so why use tariffs? And if we did, it would be robots doing so.

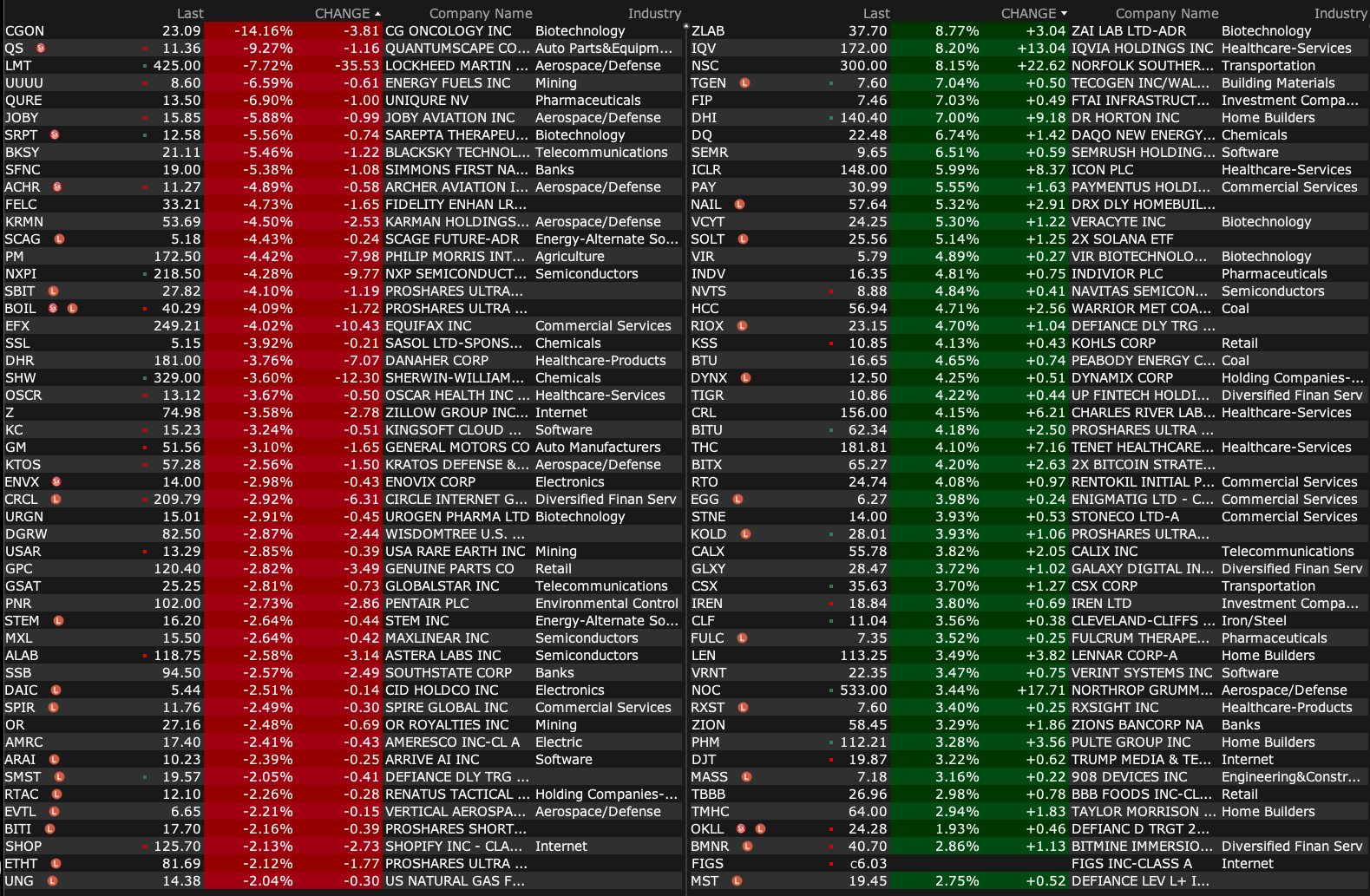

BY Doug Kass · Jul 22, 2025, 9:30 AM EDT

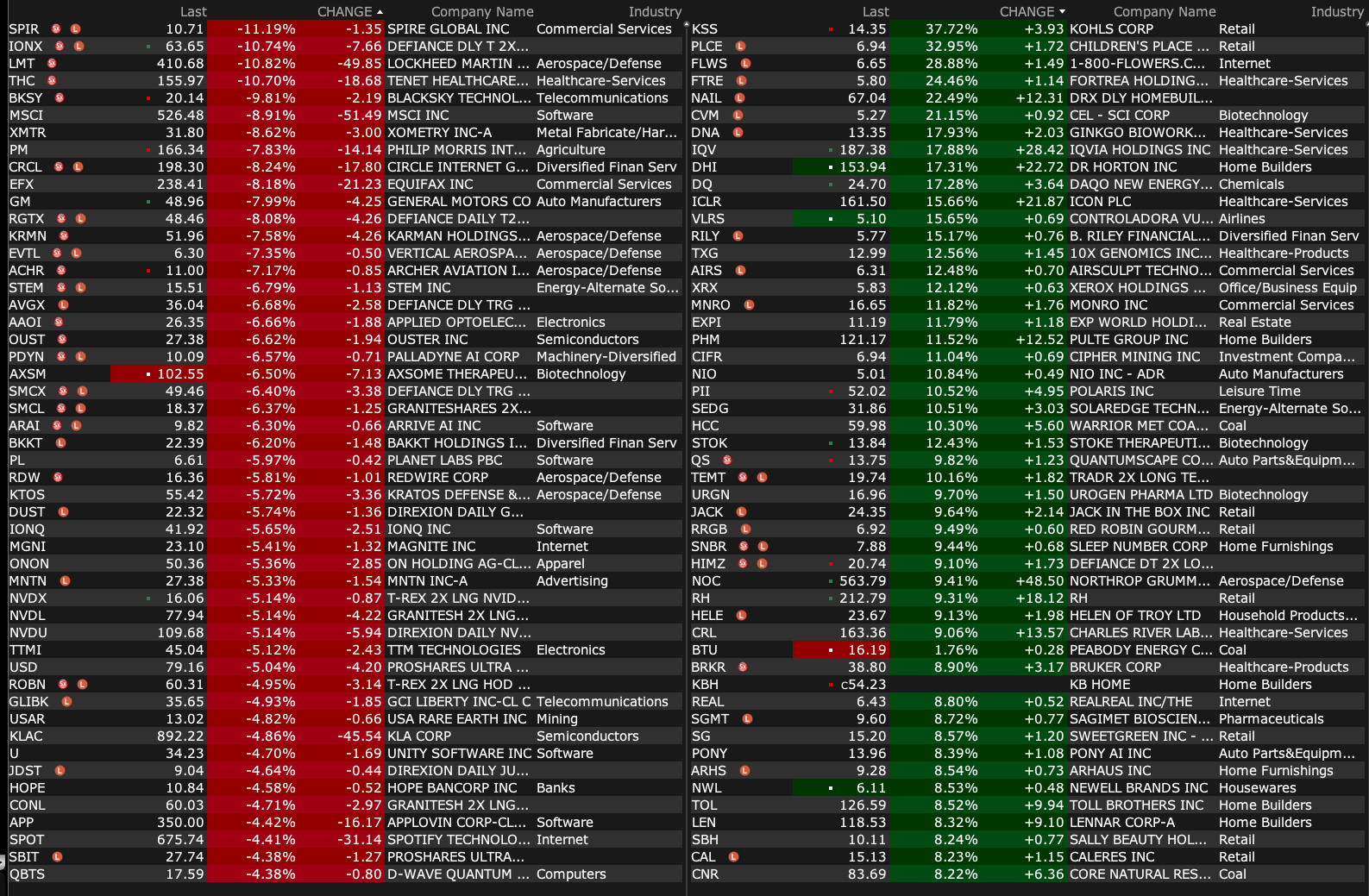

-MEDP +44% (earnings, guidance)

-OPEN +20% (meme momentum)

-AEHR +12% (received follow-on orders from major hyperscaler for 8 Sonoma ultra-high-power systems to burn-in AI chips)

-IQV +8.2% (earnings, guidance)

-DHI +6.8% (earnings, guidance)

-MCRB +4.0% (Thomas DesRosier and Marella Thorell appointed co-CEOs)

-CSX +3.9% (reportedly Berkshire's BNSF is considering bid for a rival railway)

-DDC +3.9% (files $500M shelf for BTC strategy)

-PHM +3.1% (earnings)

-NOC +3.0% (earnings, guidance)

-BMNR +2.8% (ARK Invest Acquires $182M worth of common shares)

-IPG +2.8% (earnings, guidance)

-KOPN +2.8% (Kopin and HMDmd commence production deliveries of Wearable Surgical Display Systems to Carl Zeiss Meditec)

-HOPE +2.6% (earnings, guidance)

-REPL -76% (receives Complete Response Letter from FDA for RP1 Biologics License Application for Treatment of Advanced Melanoma)

-CGON -14% (downside momentum)

-AGYS -12% (earnings, guidance)

-PGEN -11% (downside momentum)

-LMT -7.6% (earnings, guidance)

-KRMN -5.9% (reports prelim Q2; files to sell up to 20M shares for selling holders)

-SRPT -5.9% (announces voluntary pause of ELEVIDYS shipments in the US)

-BMI -5.8% (earnings)

-PM -5.2% (earnings, guidance)

-EFX -4.1% (earnings, guidance)

-NXPI -3.8% (earnings, guidance)

-CRCL -3.0% (Compass Point Research Cuts CRCL to Sell from Neutral, price target: $130 from $205)

-GM -2.9% (earnings, guidance)

-PNR -2.9% (earnings, guidance)

BY Doug Kass · Jul 22, 2025, 9:21 AM EDT

BY Doug Kass · Jul 22, 2025, 9:03 AM EDT

BY Doug Kass · Jul 22, 2025, 8:50 AM EDT

* Or, maybe, consider finally sitting down after the glorious and godsend run over the last year?

As suggested in Monday's opener, in order to get a bead on future market action, my eyes are focused away from Mag 7 and towards Congregation P.

Monday, one of Congregation P's most generous and charitable congregants, Robinhood Markets HOOD (a favorite of the market's parish and many growth-oriented ETFs like Tom Lee's GRNY (its largest weighting at near 4%), declined by -$5.40 and is two dollars lower in premarket trading Tuesday.

Congregation P's (arguably) excessively promotional and ubiquitous pastor, Palantir PLTR (seventh largest weighting in GRNY) faltered by -$1.75 Monday and is also another two dollars lower in premarket trading.

Say hallelujah!

From Monday morning:

These days the market hymnals are taken out every week between Monday thru Friday in The Church of What Is Happening Now.

Day after day in one such Church, the Congregation P rise, worship and sing hallelujahs hearing the spirit say... "All Rise" —almost regardless of outside influences (e.g. interest rates, inflation, geopolitical developments, fiscal policy and valuations).

Congregation P is the holy hush of a collection of righteous equities that seem to be a force onto themselves — always rising and nearly incapable of ever declining:

C - Coinbase

O - Oracle

N - Nvidia

G - GE Verona

R - Robinhood

E - Elbit Systems

G - GE Aerospace

A - AVGO

T - The Metals Company

I - IonQ

O - OKLO

N - Netflix

In addition, having a most sacred place in the hearts and souls of investors is Palantir — who I offer out as the leading church goer and congregant — ergo the acronym, Congregation P.

Though this congregation is not led by Joel Olsteen, market participants' attachment to Congregation P is almost religious — with their own equally passionate pastors (you know their names!).

The fate of our markets is tied no longer with Mag 7 but with Congregation P.

May God help us all.

By Doug Kass Jul 21, 2025 7:30 AM EDT

BY Doug Kass · Jul 22, 2025, 7:30 AM EDT

From JPMorgan:

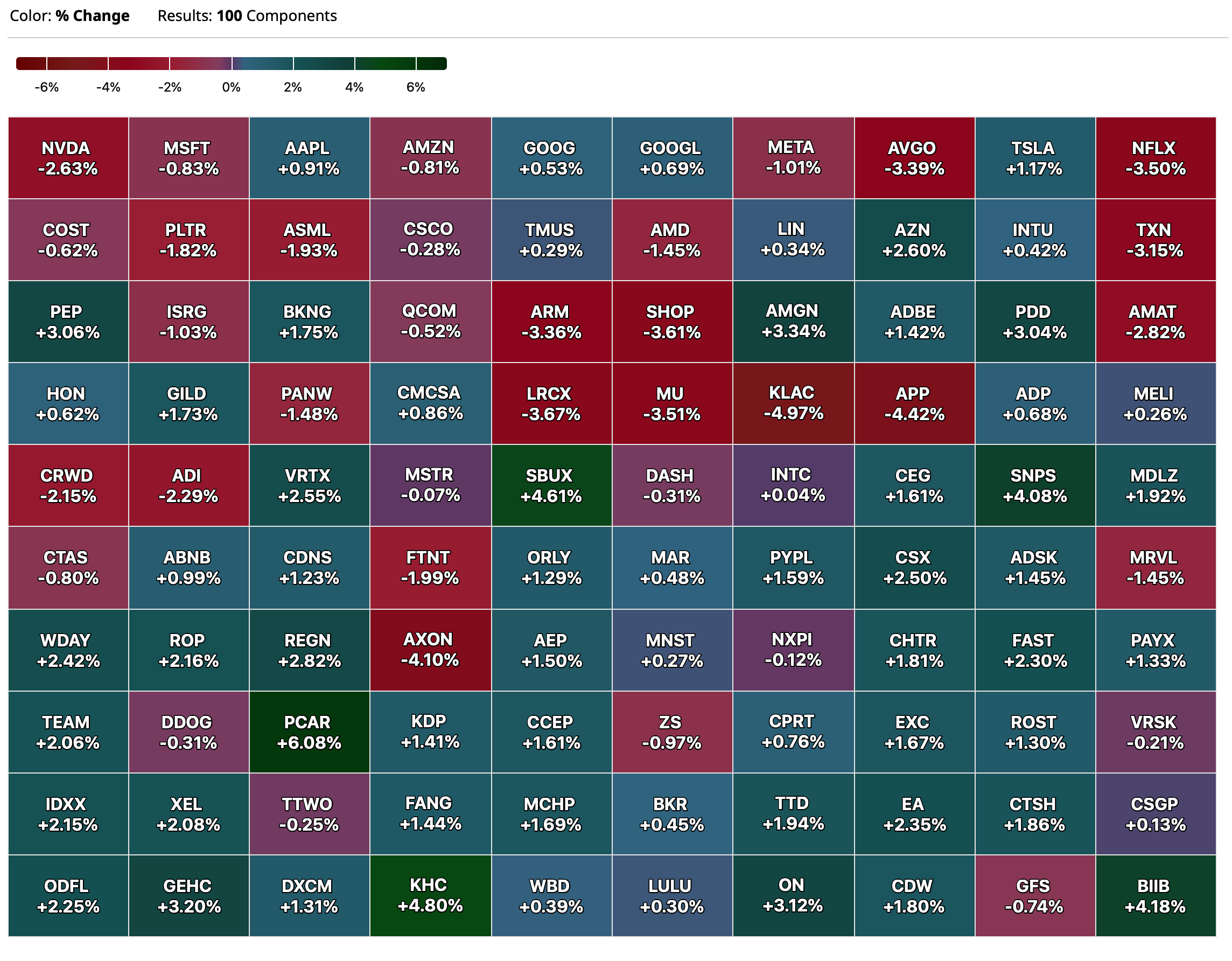

US: Futs are slightly weaker following record highs in both SPX/NDX while RTY sits ~8.5% below its ATH. The yield curve is seeing a slight twist steeper with 10s and 30s +1bp; USD is flat after having yesterday seeing its largest daily decline since June 12. Cmdtys are weaker with Energy/Precious lower, base higher, and Ags mixed. Pre-mkt, Mag7 names are mixed with AAPL, GOOG, and META higher and NVDA pulling Semis lower. Cyclicals are weaker with Industrials outperforming. Today’s macro data focus is on regional Fed activity indicators.

and..

JPM MARKET INTEL EQUITY & MACRO NARRATIVE

Yesterday was the first day that our JPM Beta and JPM Momentum baskets moved lower on the same day since June 10; the SPX posted another record high closing above 6,300 for the first time. Flagging as Dubravko has flagged the risk of a Beta Factor unwind and, recently, Beta had closed higher on the days when Momentum sold off, contribution to sub-index volatility despite major indices moving higher. More details on Dubravko’s latest note are in one of the below sections.

VOL UPDATE – Ilan Benhamou

· The market is pricing is some elevated risk around the July FOMC despite the bond market seeing less than 5% change of the Fed making a move.

· “SPX term structure is pricing in just a 1.0% for the week ending in 8/1, which is generally in line with what one would expect on a “normal” NFP week. In other words, people seem to assign virtually no premium to big earnings releases happening this week (AAPL, AMZN, MSFT, META) nor Trump’s tariff deadline supposedly expiring that Friday.”

· WHAT’S THE TRADE? Ilan likes being Long SPX plus Long VIX. Thematically, he likes longs in the AI-theme and the crypto ecosystem. With AI, likes being long into NVDA earnings (Aug 28) which coincides with the seasonal end of Equity Strength, which typically dissipates around Labor Day.

o Bram Kaplan sees SPX vol as screening cheap. It may make sense to add some Aug 1st expiration downside protection (SPX or SPY put spreads) as NFP averages about a 1% move and current options pricing reflects that you get tariff deadline and earnings for free (including AAPL, AMZN, MSFT, META, and MA). Bram’s full note is here.

DUBRAVKO: RISING MARKET COMPLACENCY WITH HIGH BETA AT RECORD CROWDING, RISK REWARD OF LOW VOL EQUITIES ONCE AGAIN ATTRACTIVE. His full note is here which contains multiple screens including High Beta names at-risk, a general US Crowded Stocks screen, and a Low Vol Aristocrats basket (JPAMLVAR Index).

· Dubravko tells us that there have been 3x extreme crowding episodes YTD, (i) Momentum Factor crowding in January which reached 100%-ile; (ii) Low Vol crowding in April which reached 96%-ile; and (iii) currently High Beta crowding which is at 100%-ile.

o US MKT INTEL NOTE – Dubravko’s High Beta basket is NOT the same as Delta-One’s Beta basket (JPBPURE Index on BBG). The main difference is that Dubravko’s baskets contains a heavier weighting of Tech/Semis and a lower weight in Financials.

· High Beta crowding has been driven by, “a combination of markets increasingly pricing in a goldilocks outcome (e.g. growth resilience and easing Fed expectations), tariff exhaustion (e.g. the so-called “TACO trade”), and institutional investors chasing more levered and speculative equity segments of the market, see report. This has resulted in a steady decline in short interest for High Beta (Figure 15) and more aggressive equity loading from the previously crowded defensive positioning.”

· The pace of the crowding in High Beta is what makes it particularly at-risk of an unwind. The positioning increased from 25%-ile to 100%-ile in 3 months which is the fastest pace over the last 30 years. This pace appears to be driven by more technical variables than micro/macro and is thus viewed as an unsustainable move.

· This crowding is occurring at a time with Momentum Factor crowded is back to 99%-ile. The most recent weakness in Momentum has been somewhat offset by the appreciation in Beta. So a dual unwind could cause problems for investors.

· RISKS – The primary risk to Dubravko’s view is a reacceleration of the business cycle (trade deals / clarity, broadening capex cycle and healthier capital markets activity amidst Fed easing), which could support a prolonged rally in High Beta segments (cyclicals, value, small caps, speculative growth / unprofitable companies).

MISLAV: HURDLE RATE IS LOW FOR THIS QUARTER (25Q2 EARNINGS), BUT 2H PROJECTIONS ARE STEEPER. His full note is here

· 25Q2 EPS growth rate expectations are +3.5% YoY, down from +11% YoY at the beginning of 2025. Q2 lowered expectations are being reflected in Discretionary, Industrials, Energy, and Materials.

o Mag7 is expected to see +14% EPS growth YoY vs. 25Q1 were the cohort printed 32% EPS growth vs. 17% expected.

o SPX493 is expected to see +1% EPS growth YoY. In 25Q1, SPX493 delivered +7% EPS growth YoY vs. +3% expected.

o From a macro perspective, the weaker USD and resilient economy should be tailwinds to this earnings season. Tariff commentary will be important.

· Given the lower bar, Mislav expects companies to beat expectations but worries that given the strength of the current Equity rally that earnings beats will not be rewarded.

· For 25H2, earnings expectations for an +11% growth rate vs. historical, median growth rate of +2.7%. He worries that H2 expectations are too optimistic given likely slowing in economic growth, decelerating top-line growth, and softer pricing/lower margins. Commodity-related sector, Discretionary, and Utilities are driving the decline.

BY Doug Kass · Jul 22, 2025, 7:10 AM EDT

Bonus — Here are some great links:

BY Doug Kass · Jul 22, 2025, 6:53 AM EDT

BY Doug Kass · Jul 22, 2025, 6:20 AM EDT

In case you missed it:

Here are today's things:

* I shorted the indices earlier in the day and covered on the late day dip - (SPY) (short $628.67/covered $628.48) and QQQ (shorted $562.38/covered 563.30).

* On the rally I shorted more SPY/QQQ calls.

* I liquidated my remaining financial stocks: (C) $93.58, (BAC) $47.28, (WFC) $80.69, (JPM) $292.26, (AXP) $306.21, (MS) $140.67, (GS) $707.45.

* I eliminated several cannabis stocks on strength caused by possible pro cannabis appointments in Washington DC: (CURLF) , (CRLBF) and (VRNOF) . Pared down (TCNNF) , (GTBIF) , (GLASF) , TSNDF.

* I covered two consumer stocks (profitably)- (COST) $949.75 and (WMT) $95.87. And I reduced some others (WGO) , (SNBR) .

Position: Long TCNNF (VVS), GTBIF (VVS), TSNDF (VVS), WGO (VS), SNBF (VS)

By Doug Kass Jul 21, 2025 11:11 PM EDT

BY Doug Kass · Jul 22, 2025, 6:10 AM EDT

BY Doug Kass · Jul 22, 2025, 5:55 AM EDT

The S&P Short Range Oscillator moved from 0.08% to 1.30% — that's slightly overbought from neutral.

BY Doug Kass · Jul 22, 2025, 5:45 AM EDT

Here are today's things:

* I shorted the indices earlier in the day and covered on the late day dip - SPY (short $628.67/covered $628.48) and QQQ (shorted $562.38/covered 563.30).

* On the rally I shorted more SPY/QQQ calls.

* I liquidated my remaining financial stocks: C $93.58, BAC $47.28, WFC $80.69, JPM $292.26, AXP $306.21, MS $140.67, GS $707.45.

* I eliminated several cannabis stocks on strength caused by possible pro cannabis appointments in Washington DC: CURLF, CRLBF and VRNOF. Pared down TCNNF, GTBIF, GLASF, TSNDF.

* I covered two consumer stocks (profitably)- COST $949.75 and WMT $95.87. And I reduced some others WGO, SNBR.

BY Doug Kass · Jul 21, 2025, 11:11 PM EDT