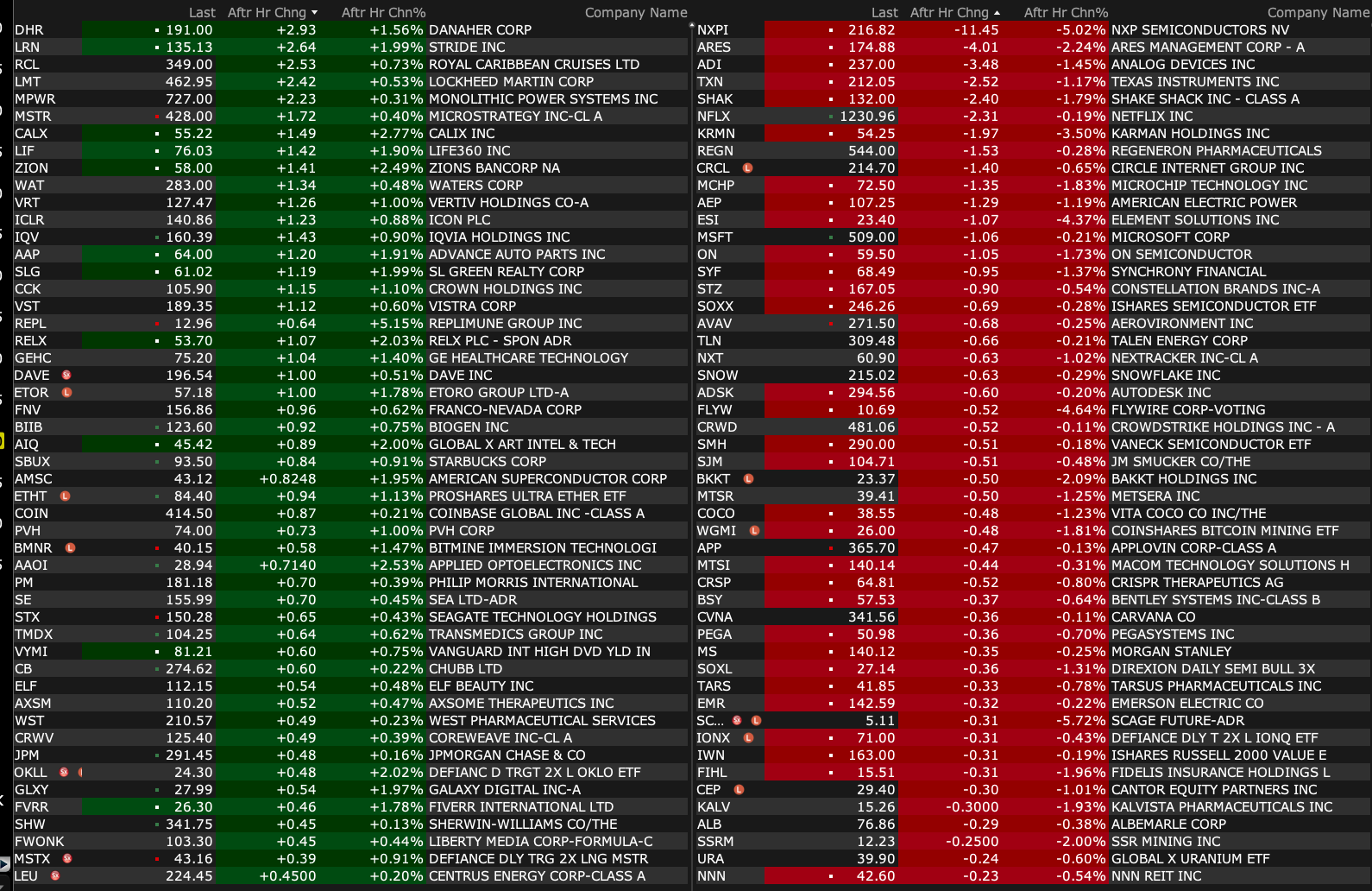

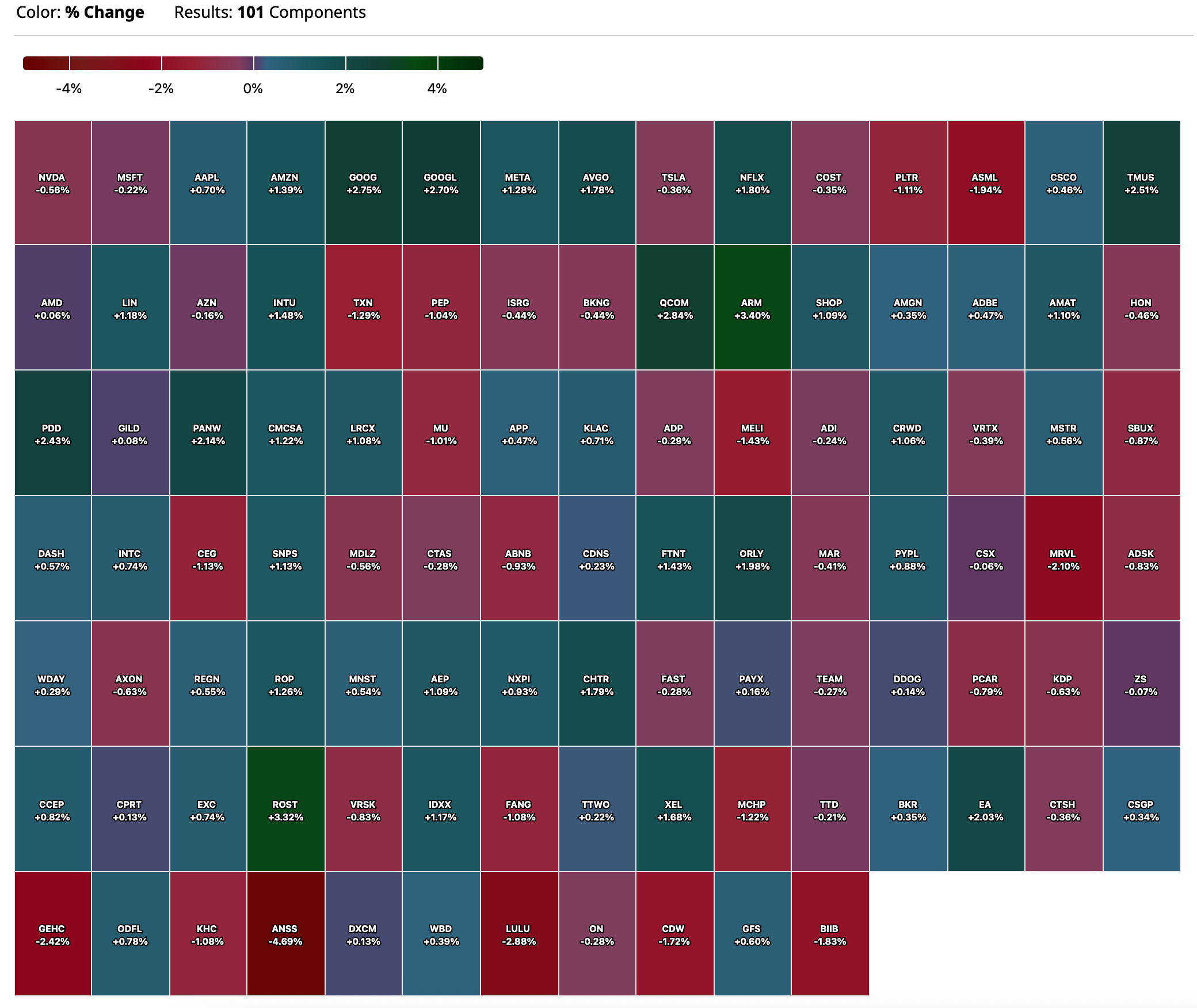

Monday's After-Hours Movers

At 4:17 p.m.:

BY Doug Kass · Jul 21, 2025, 4:53 PM EDT

At 4:17 p.m.:

BY Doug Kass · Jul 21, 2025, 4:53 PM EDT

BY Doug Kass · Jul 21, 2025, 4:48 PM EDT

BY Doug Kass · Jul 21, 2025, 4:40 PM EDT

From "The Other Dougie":

douglas cassel

I love irony, this is from chat gpt

Edward Zitron’s essay “The Hater’s Guide to the AI Bubble” is one of his most circulated and forceful critiques of the generative AI boom. It mixes media criticism, labor analysis, and takedowns of tech personalities (especially Sam Altman and OpenAI) with Zitron’s trademark polemic style. Here's an evaluation of the piece—its strengths, weaknesses, and where it lands in the larger discourse.

Summary of Key Arguments

In “The Hater’s Guide to the AI Bubble,” Zitron argues:

Strengths

1. Clear, Sharp Criticism of Power Dynamics

Zitron excels at showing how AI boosters are often talking their financial book while masking self-interest in moral or scientific terms. His argument that AI is a labor arbitrage tool (used to cut humans out of the loop) is especially timely and rarely addressed in mainstream tech optimism.

2. Effective Media Critique

He rightly points out that much of the tech press has repeated industry talking points about “intelligence,” “sentience,” and “existential risk” without adequate skepticism. He connects this to a broader failure of journalism to challenge corporate narratives.

3. Calls Out Hypocrisy and Grift

Zitron is unafraid to name names—especially figures like Sam Altman—who preach AI safety while aggressively fundraising and deploying unfinished products. His comparisons to the crypto and Web3 bubble are apt and compelling.

Weaknesses

1. Overgeneralization

Zitron paints nearly all AI development and advocacy as grift or incompetence. There’s little nuance—no distinction between OpenAI’s GPT-4 and useful narrow-AI tools in radiology, logistics, or accessibility. That makes his argument feel too sweeping.

2. No Vision for What “Good AI” Could Be

The piece is powerful in critique but lacks a constructive framework. If AI as it exists is a sham, what would a responsible, productive deployment look like? Zitron never says. This weakens the argument from a policy or ethical standpoint.

3. Style Overload

His writing is deliberately inflammatory—fun to read but also heavy on sarcasm, rhetorical questions, and contempt. That’s part of the appeal for fans, but it undermines credibility for readers seeking reasoned debate or academic rigor.

Verdict

AspectEvaluationClarity Direct and accessibleAnalytical Rigor Lacks nuance; mostly polemicEvidence Use Selective and anecdotalPersuasiveness Convincing in parts, especially on labor/mediaTone Entertaining but alienating for some readers

Final Thoughts

The Hater’s Guide to the AI Bubble is an important contribution to the AI discourse—especially because it re-centers the conversation on labor, inequality, and corporate abuse, which are too often ignored in philosophical debates about AI ethics or existential risk. But it’s a polemic, not a roadmap. Readers should pair it with more balanced or technical perspectives to get the full picture.

Would you like a short summary or excerpt breakdown next?

Ask ChatGPT

BY Doug Kass · Jul 21, 2025, 4:01 PM EDT

With S&P cash +10 handles, I have covered index common shorts from early this morning:

* SPY $628.48

* QQQ $564.10

BY Doug Kass · Jul 21, 2025, 3:59 PM EDT

I am further reducing my WGO, RILY and SNBR shorts.

BY Doug Kass · Jul 21, 2025, 3:56 PM EDT

I am selling some of my very small cannabis holdings into today's ramp as some of the % gains are on the large side.

BY Doug Kass · Jul 21, 2025, 3:51 PM EDT

* Slip Sliding Away

Slip slidin' away, slip slidin' away

You know the nearer your destination

The more you're slip slidin' away

- Paul Simon, Slip Slidin' Away

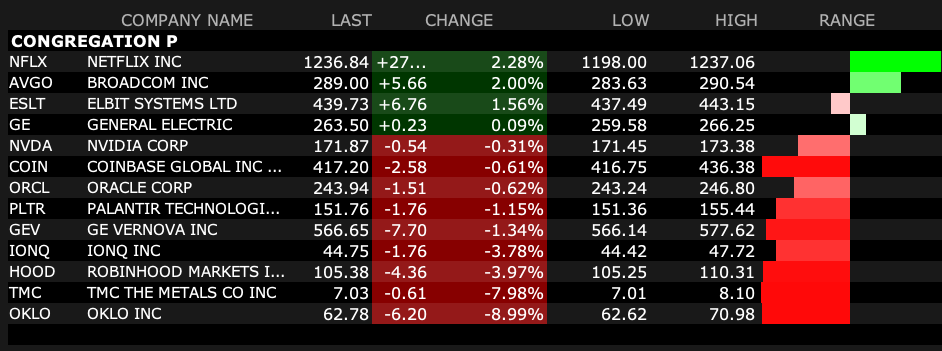

Here is a picture of Congregation P today:

The pastor, Palantir PLTR, is -$1.75.

BY Doug Kass · Jul 21, 2025, 3:44 PM EDT

Of the 13 Congregation P consituents — 8 are now lower and 5 are higher.

Netflix NFLX (+$22) is the largest price gainer, followed by Coinbase COIN (+$2.60).

Robinhood HOOD and GE Vernova GEV are the biggest price losers.

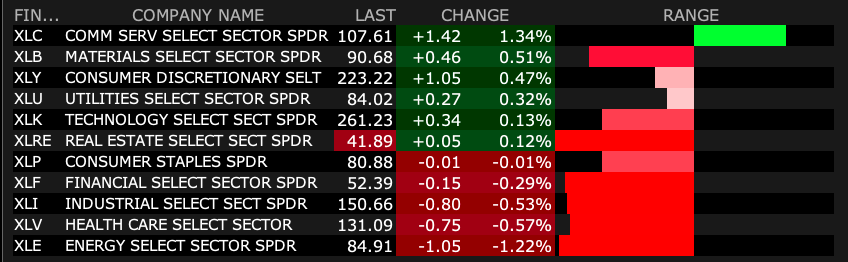

BY Doug Kass · Jul 21, 2025, 2:56 PM EDT

BY Doug Kass · Jul 21, 2025, 2:27 PM EDT

In this past weekend's Thoughts From the Frontline Inflationary Confusion - Mauldin Economics John Mauldin makes some similar (bearish) points to what I have been making in recent months:

* Inflation Break Evens are rising - causing a Fed conflict:

On Friday morning, Peter Boockvar offered this chart of two-year inflation breakeven rates, up to 2.76%, and as you can see the trend is clearly up from below 2.5% over the last month. The 5- year breakeven has gone from 2.40% to 2.54%. The market is clearly more concerned and less optimistic about inflation than the FOMC. This will be important later.

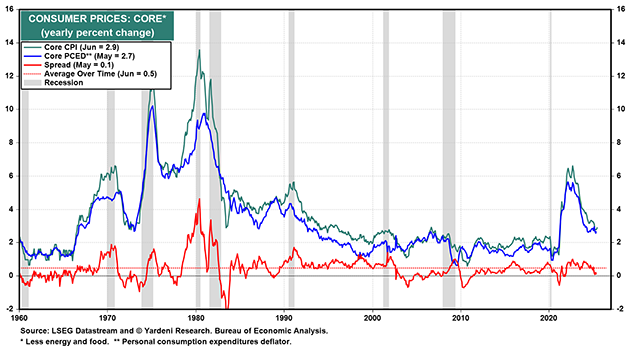

* The CPI data suggests that inflation will remain persistent:

This week’s June CPI data didn’t add much clarity. Here is Ed Yardeni’s first impression.

“Today's CPI report for June suggests that consumer price inflation is no longer declining toward the Fed's 2.0% target. Instead, it might continue to hover around 3.0% for a while as it has recently (chart). Trump's tariffs may be a contributing factor, though their impact remains debated. The core CPI inflation rate upticked to 2.9% last month, hinting that the core PCED inflation rate (at 2.7% in May) might have followed a similar trend.

“President Donald Trump is pushing for the Federal Reserve to cut the federal funds rate (FFR) from 4.33% to 1.00%. This reduction would lower net interest payments on the federal debt, helping to reduce the US budget deficit. A lower FFR could also weaken the dollar, boosting exports and reducing imports. However, Fed Chair Jerome Powell and most Federal Open Market Committee (FOMC) participants are reluctant to cut rates, especially to 1.00%, due to concerns that Trump's tariffs could hinder progress toward the Fed's 2.0% inflation target.

“The June CPI report reinforces the FOMC's cautious stance. Although Trump's tariffs may not yet be significantly driving inflation, they appear to be contributing to inflation stalling at around 3.0%, supporting the FOMC's hesitation to lower the FFR.”

* Imported prices are again rising (sequentially):

Peter then included a list of mostly imported goods and their change in the CPI data from May to June.

- Floor coverings +2.2%

- Window coverings +2.2%

- Other Linens + 5.5%

- Laundry Equipment +1.8%

- Other Appliances +2.0%

- Clocks, lamps, & decorator items +1.6%

- Non-electric cookware & tableware +3.7%

- Tools, hardware, & supplies +1.2%

- Apparel +.4% with men's shirts & sweaters up 4.3%

- Footwear +.7%

- Tires +.9%

- Video & Audio products +.8%

- Sports vehicles including bicycles +1.0%

- Sports equipment +1.8%

- Toys +1.8%

Again, those are one-month price changes. They may or may not continue to climb at these rates. Businesses are trying to figure out how much of the tariff impact they can pass through to customers and how much they’ll have to absorb. Choose your poison: Either corporations make less money (impacting valuations and the stock market) or consumers pay more money.

This will likely evolve over time, with more monthly price increases in consumer goods offset by lower service prices. And the tariff rates themselves are often moving targets, too.

* Corporate profit margin expectations are too high:

Wolf Richter thinks companies will have a hard time raising prices.

“Companies have lots of room to eat the tariffs, after making gigantic profits as they jacked up consumer prices in 2020–2024 to very high levels. Now they’re finding out that consumers have had it, that they’re no longer willing to pay whatever, that price increases are a demand killer, and that tariffs are now hard to pass on because consumers reduce their purchases of those products in response.”

If he’s right, then the tariff impact will manifest mostly as lower corporate profits instead of higher prices. That would suggest the recent inflation pressure will be temporary. You might even call it “transitory.” But we don’t know this yet. Whether you love or hate the tariffs, I caution everyone not to assume you know how they’ll affect the economy. This is a complex situation that could go in many directions.

* There are a plethora of increased uncertainties:

I think Powell will finish his term as chair. Right now, betting markets have Kevin Warsh as the odds on favorite, and I think he would be an excellent choice both temperamentally and from a market perspective. (I should note that lately when I write something, Trump has a way of changing things that makes me look less than prescient. I hope I didn’t jinx Powell.)

Many conflicting things are happening on the inflation front. We don’t know how it will all shake out. There’s a lot of confirmation bias happening among investors and economists. If you’re convinced inflation is coming, you perk up when you see news that supports your view. Ditto if you think tariffs are awesome and will produce an economic boom.

The truth is more subtle: We Don’t Know Yet. We live in extraordinarily confusing times. Seemingly impossible things are happening all around us. I myself am pretty confident in the long-term future. But the next year or two? My crystal ball is broken.

Sometimes, especially in markets driven by price (as passive products and strategies overwhelm active management), fundamentals move to the back burner.

This is one of those times.

I don't think it will last.

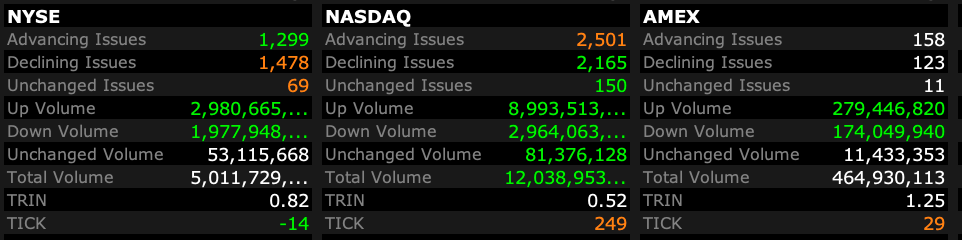

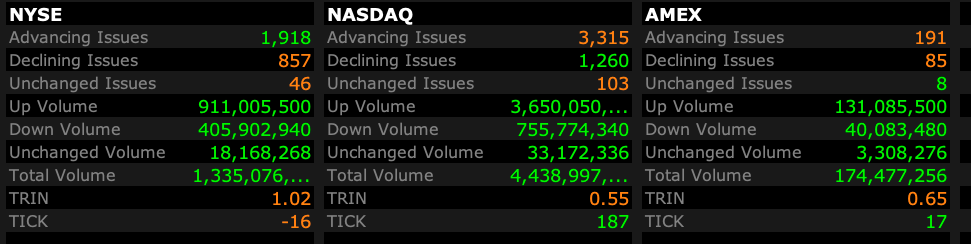

BY Doug Kass · Jul 21, 2025, 12:00 PM EDT

- NYSE volume flat to its one-month average;

- Nasdaq volume 35% above its one-month average;

- VIX index: up 0.79% to 16.54

BY Doug Kass · Jul 21, 2025, 11:11 AM EDT

The NDX 14-day relative strength index is now at the highest level since Summer, 2024:

BY Doug Kass · Jul 21, 2025, 10:51 AM EDT

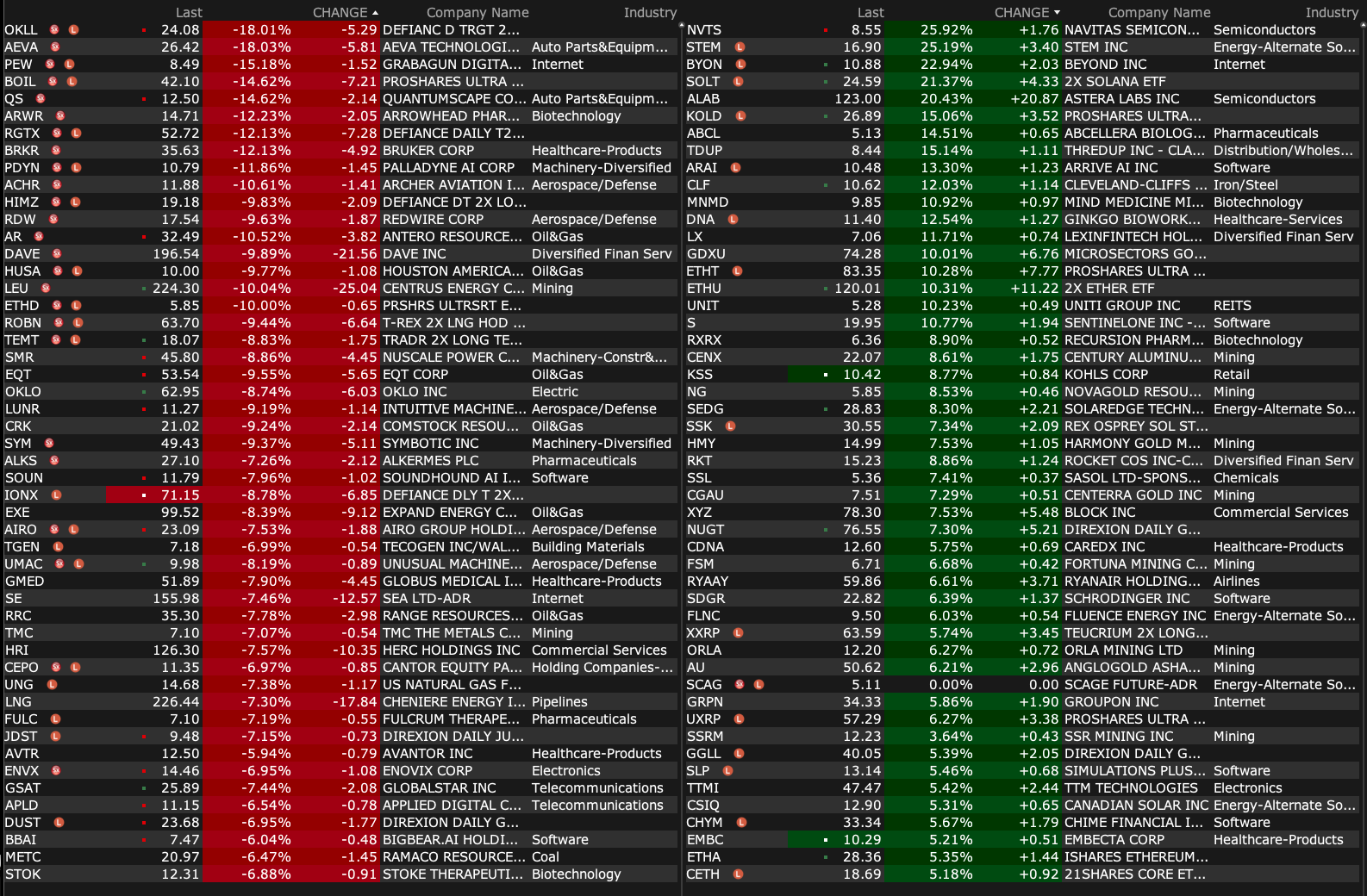

This sort of action epitomizes the current state of the market.

BUZZ's largest holdings are AST Spacemobile ASTS, Rocket lab RKT, Robinhood HOOD, AMD AMD, Coinbase COIN, Palantir PLTR, Tesla TSLA and Nvidia NVDA.

Source: Peter Boockvar

BY Doug Kass · Jul 21, 2025, 10:35 AM EDT

I have covered WMT and COST shorts for a small profit.

BY Doug Kass · Jul 21, 2025, 10:14 AM EDT

I have sold out the balance of my financial longs this morning.

BY Doug Kass · Jul 21, 2025, 10:00 AM EDT

BY Doug Kass · Jul 21, 2025, 9:20 AM EDT

Note that SPY and QQQ take a backseat to more active premarket ETFs (bottom of the ranking list by volume):

BY Doug Kass · Jul 21, 2025, 9:10 AM EDT

I reentered a short on SPY/QQQ common in the premarket:

* SPY $629.44

* QQQ $563.09

BY Doug Kass · Jul 21, 2025, 9:08 AM EDT

-DYNX +31% (The Ether Machine to go public with >$1.5B of fully committed capital)

-UPXI +14% (acquires 100K SOL, bringing treasury holdings to 1.8M SOL valued at $331M)

-AVAH +12% (hearing Jefferies Raised AVAH to Buy from Hold, price target: $6)

-XYZ +9.6% (to be added to the S&P500, effective on Jul 23rd)

-IAS +8.8% (momentum)

-AMRX +7.5% (reports prelim Q2, issues strong FY guidance; announces proposed refinancing of existing credit agreement, including Private Offering of Senior Secured Notes due 2032)

-CLF +7.5% (earnings, guidance)

-PINS +5.1% (Morgan Stanley Raised PINS to Overweight from Equal Weight, price target: $45)

-VZ +4.8% (earnings, guidance)

-CHTR +4.2% (strength in sympathy with VZ and ahead of reporting earnings later this week)

-DPZ +3.7% (earnings)

-DLTR +2.6% (hearing Barclays Raised DLTR to Overweight from Equal Weight, price target: $120)

-ETSY +2.6% (Morgan Stanley Raised ETSY to Equal Weight from Underweight, price target: $50)

-KRRO +2.4% (receives EMA Orphan Drug Designation for KRRO-110)

-EQIX +2.2% (reportedly Elliott to boost stake)

-RDY +2.2% (receives US FDA ANDA approval for Nicotine Polacrilex)

-EVO -13% (cuts FY25 guidance)

-BRKR -11% (prelim Q2 earnings, guidance)

-SRPT -7.9% (affirms FDA revoked the platform technology designation for AAVrh74 platform technology previously granted on June 2, 2025)

-ZK -5.2% (reportedly Chinese EV brands Zeekr and Neta have inflated their vehicle sales using a "zero-mileage used cars" insurance scheme)

BY Doug Kass · Jul 21, 2025, 8:49 AM EDT

From Peter Boockvar:

As most of us expected, Japanese Prime Minister Shigeru Ishiba lost his governing majority in the upper house election yesterday, securing just 47 LDP seats vs the 50 he needed but it could have been worse based on estimates I saw. Either way, he said he's not resigning but without the majority in the lower house too, he's essentially a lame duck at this point. As the yen has weakened over the last few weeks ahead of the election, they are bouncing even with the uncertainty of what fiscal policy might come of this. JGB futures though did trade lower while the cash market and equities didn't trade because of a national holiday.

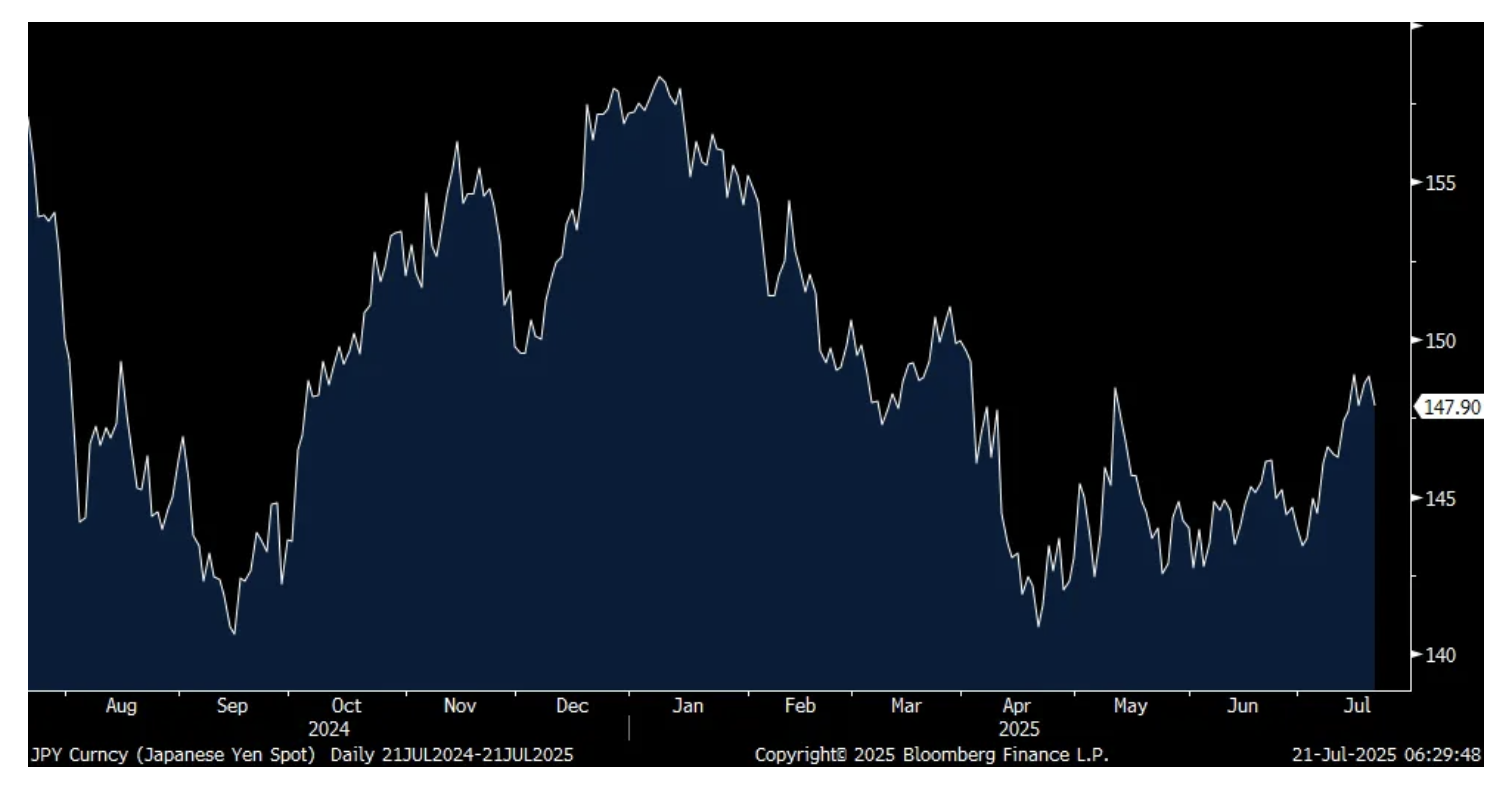

The most important message to take is that we were reminded again that what a populace hates the most is inflation, especially when one's income doesn't keep up. We saw it in the US, and we've seen it throughout history, particularly the protests in France in 2018 known as the Yellow Vest protests when Macron tried to raise energy taxes. The BoJ hoped for years that they would achieve higher inflation and now that they did, no one is happy about it except them, and they don't seem to be doing anything about it with an overnight rate of just .50%. That has now cost Ishiba his leadership support.

Yen

Speaking of the cost of living in the US, last week the June CPI told us that health insurance costs went up just 3.4% y/o/y. That of course is not reality and this article from the Weekend WSJ reminded us of what reality is for some. Titled, "Obamacare Insurers Seek Double Digit Premium Hikes Next Year", it said "Blue Cross & Blue Shield of Illinois wants a 27% hike, while its sister Blue Cross plan in Texas is asking 21%. The largest ACA plans in Washington state, Georgia and Rhode Island are all looking for premiums to surge more than 20%." The smallest increases the article mentioned were from a program in NY and Oregon where insurance costs are about to rise by 8%.

Of course monetary policy can't directly impact this (only indirectly via the state of the labor market where many get their insurance) but it reflects challenges still with inflation that clearly is not reflected in how the BLS calculates health insurance in CPI.

I'll continue to argue for a bottoming process taking place with crude oil prices. The US crude oil rig count as of 7/18 fell for the 12th straight week and by another 2 to 422 and has fallen by 53 over these three weeks. That's the least since September 2021.

Crude Oil Rig Count

From American Express whose stock fell 2.4% Friday:

"Total card member spending was up 7%, which was consistent with the pattern we've seen this year, while spend in some of the travel categories, like airlines and lodging, was softer overall. Spending was a quarterly record."

More on this, "We live in uncertain times, but I think people are continuing to live their lives. And what we're seeing right now is very consistent spending. You're seeing a little bit of a slowdown in airline, not necessarily front of the cabin. You're seeing a little bit of a slowdown in lodging, but again, not necessarily on the high transactions, which are up. But goods and services continue to be resilient and our GenZs and our millennial’s continue to be consistent." I'll add to the latter, a lot of the growth here is just the less use of cash and more and more transactions take place using digital/credit.

They said "restaurant spending continued to be very strong, up 8% FX adjusted."

"Our fastest growing cohorts kept up their momentum. In the US consumer business, millennial spend was up 10% and GenZ spend was growing around 40%, though starting from a smaller base. And our international business continued to grow in double digits, up 12% FX adjusted in the quarter."

"Transaction growth up 9% is another indicator of strong customer engagement and is largely consistent with what we've been seeing over the past few quarters."

AmEx was a bit more cautious on their small and medium-sized business customers. "I think SMBs are a little bit more circumspect, I think, than the consumers are right now. And so not buying maybe as much inventory and maybe not spending as much. And so I think they're going to need probably a little bit more assurance from and economic perspective longer term for that to get going."

"Our growth in premium products over the past few years has further strengthened the credit quality of our portfolio, resulting in very strong credit performance. Q2 delinquency and write off rates remained low, with delinquency rates flat to Q1, while write-off rates declined."

From Ally Financial, a big lender to the auto sector and whose stock fell about 1% Friday:

"In Retail Auto, the net charge-off rate was 175 bps, down 37 bps sequentially, and 6 bps y/o/y. This marks the second consecutive quarter of y/o/y improvement, reflecting the strong performance from recent vintages and continued enhancements to our digital servicing capabilities. That said, we remain mindful of the elevated level of uncertainty that we are currently navigating."

"We continued to observe stable and consistent delinquency performance trends across the 2022 and 2024 vintages and added the 2025 vintage to the disclosure." A key reason is this is in response to tightened lending standards over the past few years.

"delinquencies have improved, but we'd still characterize them as elevated."

"Looking holistically at credit measures, we remain encouraged by the performance of the portfolio and the effectiveness of our servicing strategies, but remain cautious of macroeconomic uncertainty going forward."

From MMM whose stock fell 3.7% Friday after a solid run:

Organic sales rose 1.5% y/o/y "with all three business groups reporting positive growth for the third quarter in a row."

Based on "several key macro trends we're tracking...all metrics reflect a global economy that remains sluggish and moving laterally, not materially improving or worsening."

"Our Safety and General Industrial businesses were up low single digits in the first half and are both beginning to see a pickup due to our commercial excellence initiatives. Auto will be flattish in the second half, a step up from decline in the first half due to share gains in new models, while consumer electronics is likely to soften a bit in the back half due to slower demand for premium devices."

Also, "Auto aftermarket will remain challenged and consumers will likely follow a similar pattern to the first half due to the subdued US retail environment."

Tariffs are going to cost them $.50 per share this year after their mitigation efforts.

Finally, on stock market sentiment. The Citi Panic/Euphoria index moved further into Euphoria at .49, the highest since early March. Last week the Investors Intelligence got further stretched with a Bull/Bear spread now at 33.9 with Bulls at 54.7 vs 53.8 in the week before while Bears slipped to 20.8 from 21.2. I consider a spread of 40 to be extreme. The AAII retail investor survey continues to be more neutral with Bulls at 39.3 vs Bears at 39. The CNN Fear/Greed index is at 75, right on the dividing line between 'Greed' and 'Extreme Greed.' The NAAIM Exposure Index was 83.7 last week, off its nearly 100 print of a few weeks ago but elevated.

Bottom line, nothing alarming from a contrarian standpoint in terms of extremities in sentiment but still take note of the Citi survey and the near 40 pt Bull/Bear spread in II.

BY Doug Kass · Jul 21, 2025, 8:37 AM EDT

These days the market hymnals are taken out every week between Monday thru Friday in The Church of What Is Happening Now.

Day after day in one such Church, the Congregation P rise, worship and sing hallelujahs hearing the spirit say... "All Rise" —almost regardless of outside influences (e.g. interest rates, inflation, geopolitical developments, fiscal policy and valuations).

Congregation P is the holy hush of a collection of righteous equities that seem to be a force onto themselves — always rising and nearly incapable of ever declining:

C - Coinbase

O - Oracle

N - Nvidia

G - GE Verona

R - Robinhood

E - Elbit Systems

G - GE Aerospace

A - AVGO

T - The Metals Company

I - IonQ

O - OKLO

N - Netflix

In addition, having a most sacred place in the hearts and souls of investors is Palantir — who I offer out as the leading church goer and congregant — ergo the acronym, Congregation P.

Though this congregation is not led by Joel Olsteen, market participants' attachment to Congregation P is almost religious — with their own equally passionate pastors (you know their names!).

The fate of our markets is tied no longer with Mag 7 but with Congregation P.

May God help us all.

BY Doug Kass · Jul 21, 2025, 7:30 AM EDT

From JPMorgan:

US: Futs are higher. Over the weekend, headlines were relatively muted in the US. Globally, Japan’s ruling party lost its majority in the upper house, but the PM Ishiba still pledged to stay in office. Pre-market, MegaCap Tech sees TSLA (+1.6%) leading gains, followed by GOOGL (+0.9%) and META (+0.6%); Utilities and Consumer Discretionary are outperforming. Yields are lower and USD is lower; 2-, 5-, 10-, 30yr yields are 2bp, 3bp, 4bp lower. Commodities are mixed with base metals higher and oil lower.

and...

JPM MARKET INTEL EQUITY & MACRO NARRATIVE

Last week, the SPX was up 59bp with NDX outperforming (+1.3%) and RTY adding 23bp. 10Y yield was largely unchanged; USD added 64bp. Overall, last week's narrative was characterized by Goldilocks macro data and robust earnings. CPI, PPI, and Import Prices all surprised to the dovish side as the scenario of an early (June) tariff-induced spike in inflation being avoided. Growth data, including Retail Sales, Jobless Claims, Industrial Production and Philly Fed Outlooks, showed a still resilient growth environment and healthy US consumers.

Q2 Earnings was off to a strong start, but stocks reactions were mixed. For large-cap banks, FactSet data (here) shows that Financials has the largest positive surprise in earnings, averaging +11.5% in the first week. XLF finished the week with a +73bp gain, with a -1.7% selloff on the first day of banks earnings (July 15). Positioning Intelligence tells us that they observed “profit taking in large caps post positive earnings prints, while regionals were brought”. Lastly, the Trump vs. Powell debate led to some intraday volatility in rates. We saw yield curve twist steeper and all three major indices decline before Trump denied that he will fire Powell later in the afternoon.

This week, 16% of SPX will report earnings, concentrating on Consumer Discretionary, Industrials, Communication Services and Materials. GOOG/L and TSLA will kick off Mag 7 earnings on Wednesday (July 23). On macro data, we will receive global PMIs on Thursday, which will be the first batch of July growth data.

BY Doug Kass · Jul 21, 2025, 6:45 AM EDT

Bonus — Here are some great links:

"Jazzy" Jeff Hirsch - Seasonal Weakness Typically Starts Mid-July

BY Doug Kass · Jul 21, 2025, 6:20 AM EDT

BY Doug Kass · Jul 21, 2025, 5:55 AM EDT

The S&P Short Range Osciallator shifted back to neutral at Friday's close — standing at

0.08% vs. 1.57%.

BY Doug Kass · Jul 21, 2025, 5:45 AM EDT