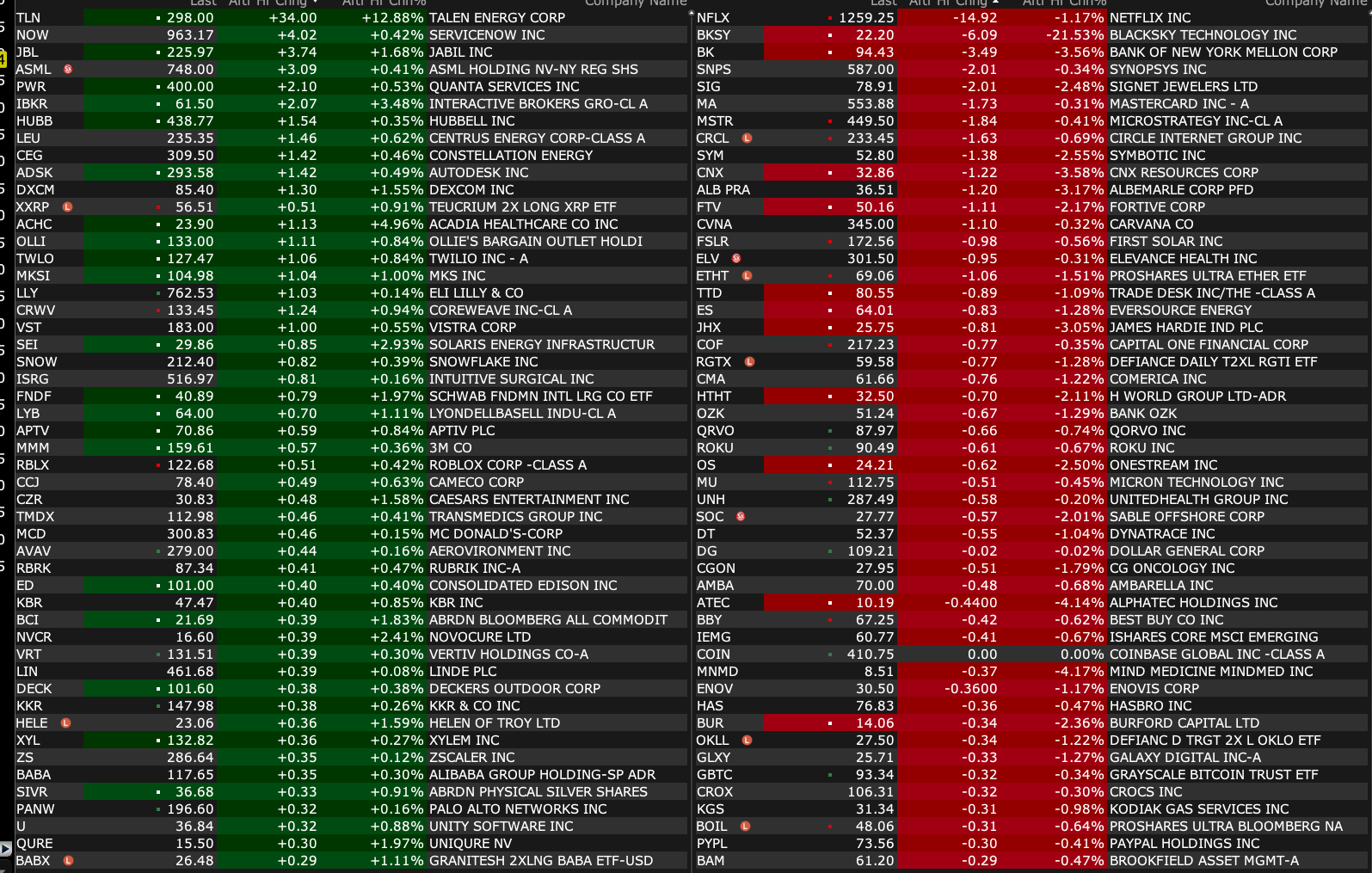

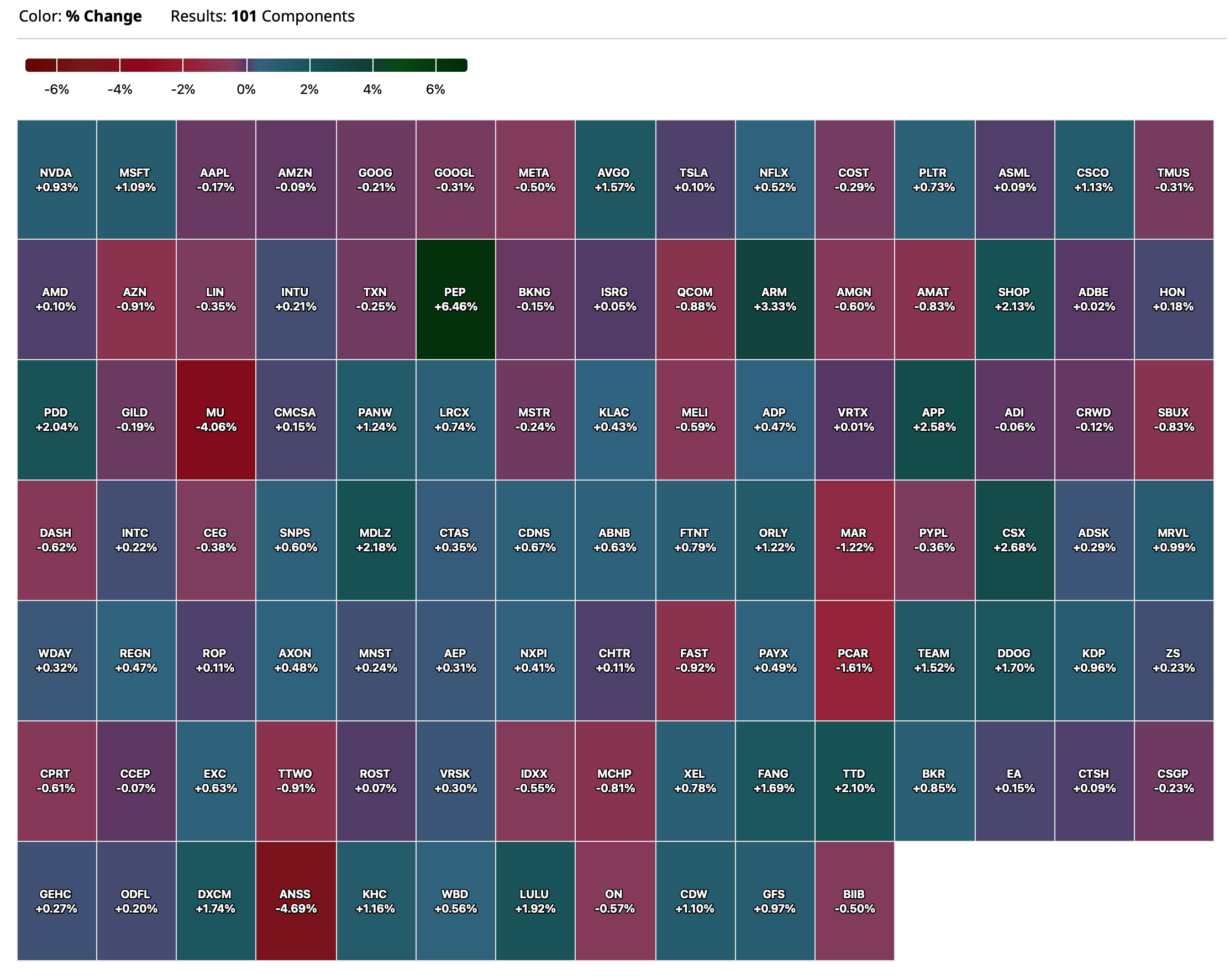

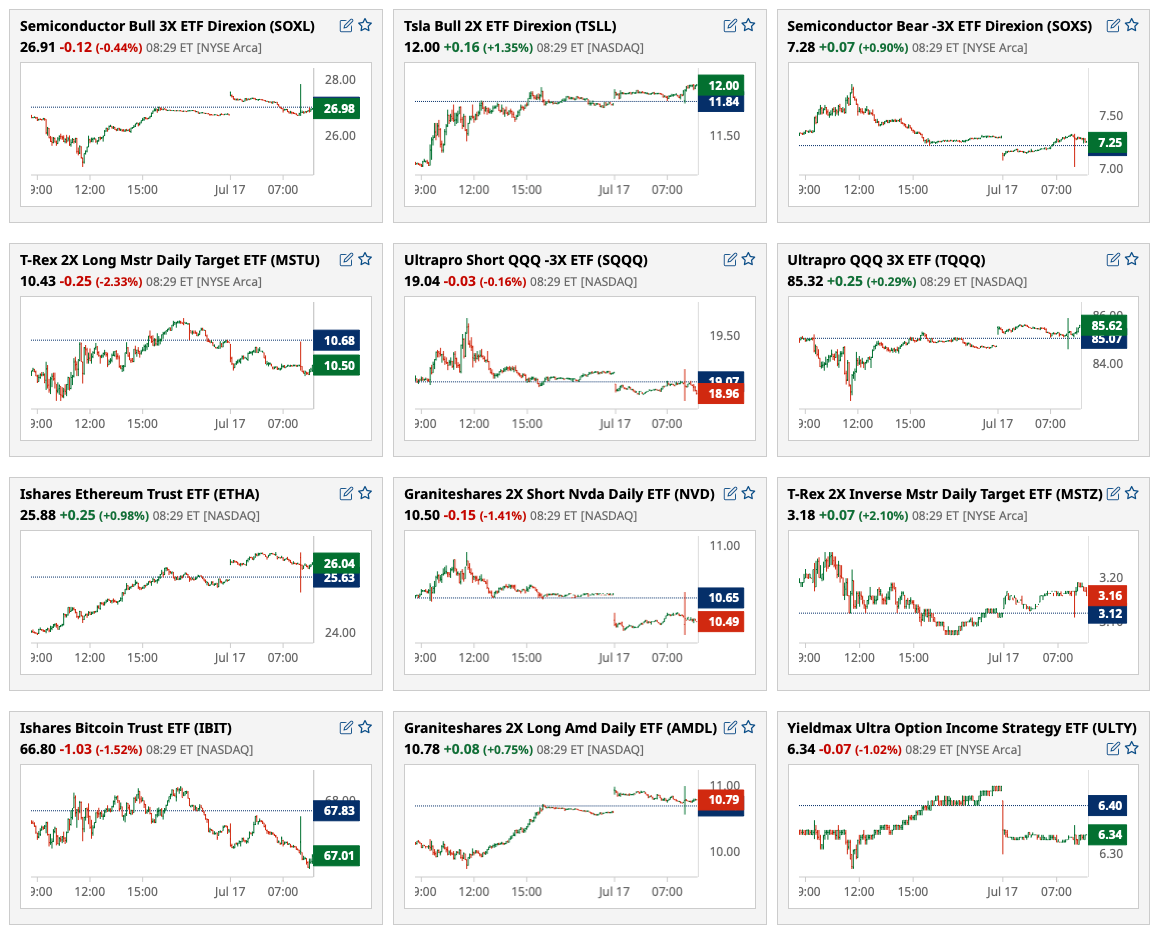

Thursday's After-Hours Movers

As of 4:20 p.m.:

BY Doug Kass · Jul 17, 2025, 4:50 PM EDT

As of 4:20 p.m.:

BY Doug Kass · Jul 17, 2025, 4:50 PM EDT

BY Doug Kass · Jul 17, 2025, 4:41 PM EDT

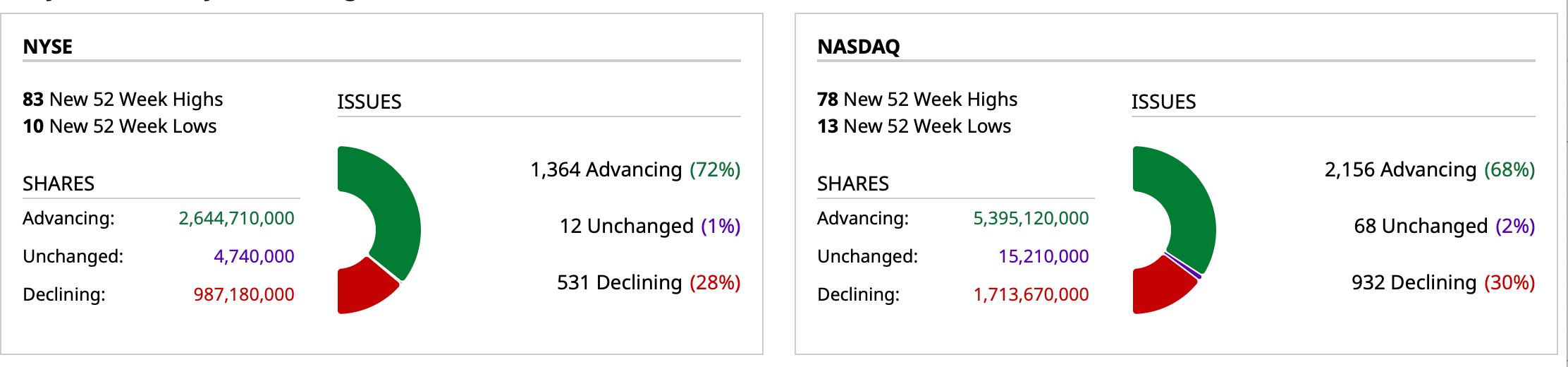

- NYSE volume 7% above its one-month average;

- NASDAQ volume 18% above its one-month average;

- VIX index: down 3.73% to 16.52

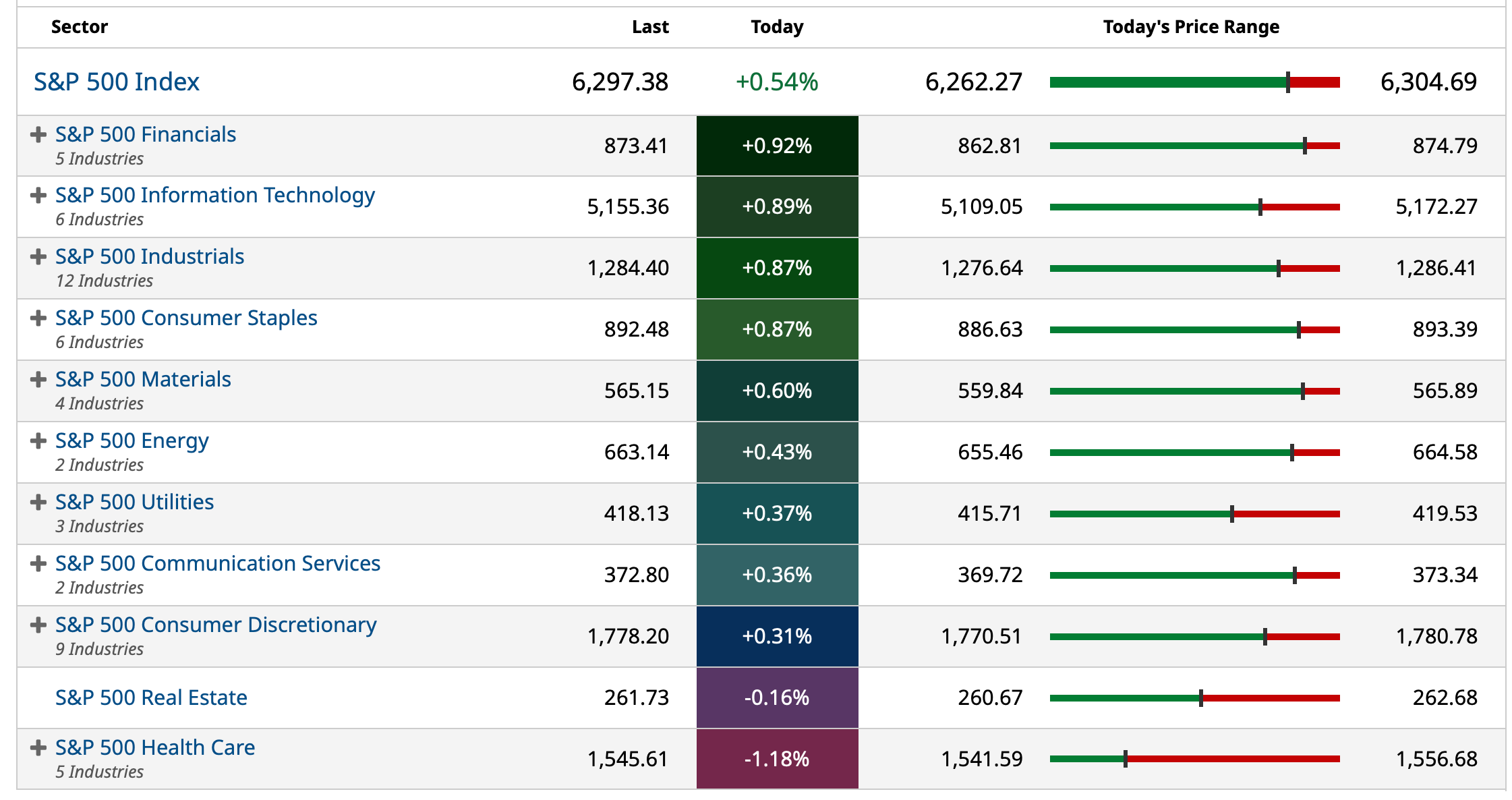

BY Doug Kass · Jul 17, 2025, 4:36 PM EDT

Dougie Kass

The market continues to defy odds and my expectations.

I invest/trade unemotionally but I have to admit that I am frustrated.

BY Doug Kass · Jul 17, 2025, 3:25 PM EDT

I am adding to my RSP short at $184.33.

Mostly a research day.

BY Doug Kass · Jul 17, 2025, 3:17 PM EDT

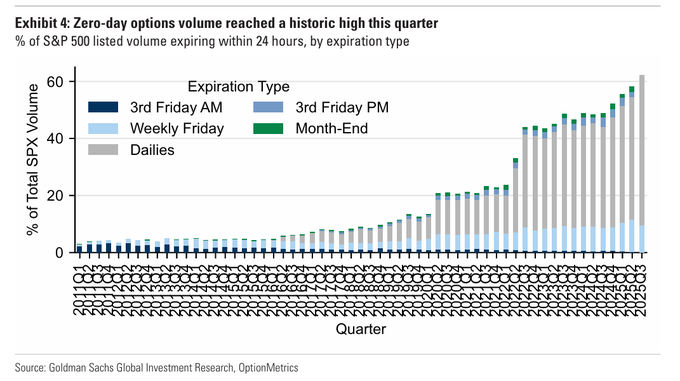

* Yo eleven!

0DTE options now exceed about two-thirds of daily trading volume.

BY Doug Kass · Jul 17, 2025, 2:14 PM EDT

I should have mentioned earlier this week when I sold out my homebuilders. I continue to hold JOE.

BY Doug Kass · Jul 17, 2025, 1:44 PM EDT

I am out of my KO short.

BY Doug Kass · Jul 17, 2025, 12:35 PM EDT

I have two research meetings at 12 PM and 1 PM.

Back at 1:30.

BY Doug Kass · Jul 17, 2025, 12:25 PM EDT

- NYSE volume is 5% above its one-month average;

- Nasdaq volume is 20% above its one-month average;

- VIX index: down 0.99% to 16.99

BY Doug Kass · Jul 17, 2025, 11:15 AM EDT

With S&P cash +16 handles I am back buying index puts.

BY Doug Kass · Jul 17, 2025, 10:58 AM EDT

From Peter Boockvar:

As Jay Powell is likely going to remain in his seat until May 2026, I’m not going to add much here as I believe we all agree that it would be a mistake if he was fired. Hat tip to my friend Brent Donnelly for reminding me of a speech that Arthur Burns, the Fed Chair under Richard Nixon and during that inflationary time, gave in 1979 titled “The Anguish of Central Banking.” This was most relevant to the current circumstances:

“In most countries, the central bank is an instrumentality of the executive branch of government - carrying out monetary policy according to the wishes of the head of government or the ministry of finance. Some industrial democracies, to be sure, have substantially independent central banks, and that is certainly the case in the United States. Viewed in the abstract, the Federal Reserve System had the power to abort the inflation at its incipient stage 15 years ago or at any later point, and it has the power to end it today. At any time within that period, it could have restricted the money supply and created sufficient strains in financial and industrial markets to terminate inflation with little delay. It did not do so because the Federal Reserve was itself caught up in the philosophic and political currents that were transforming American life and culture."

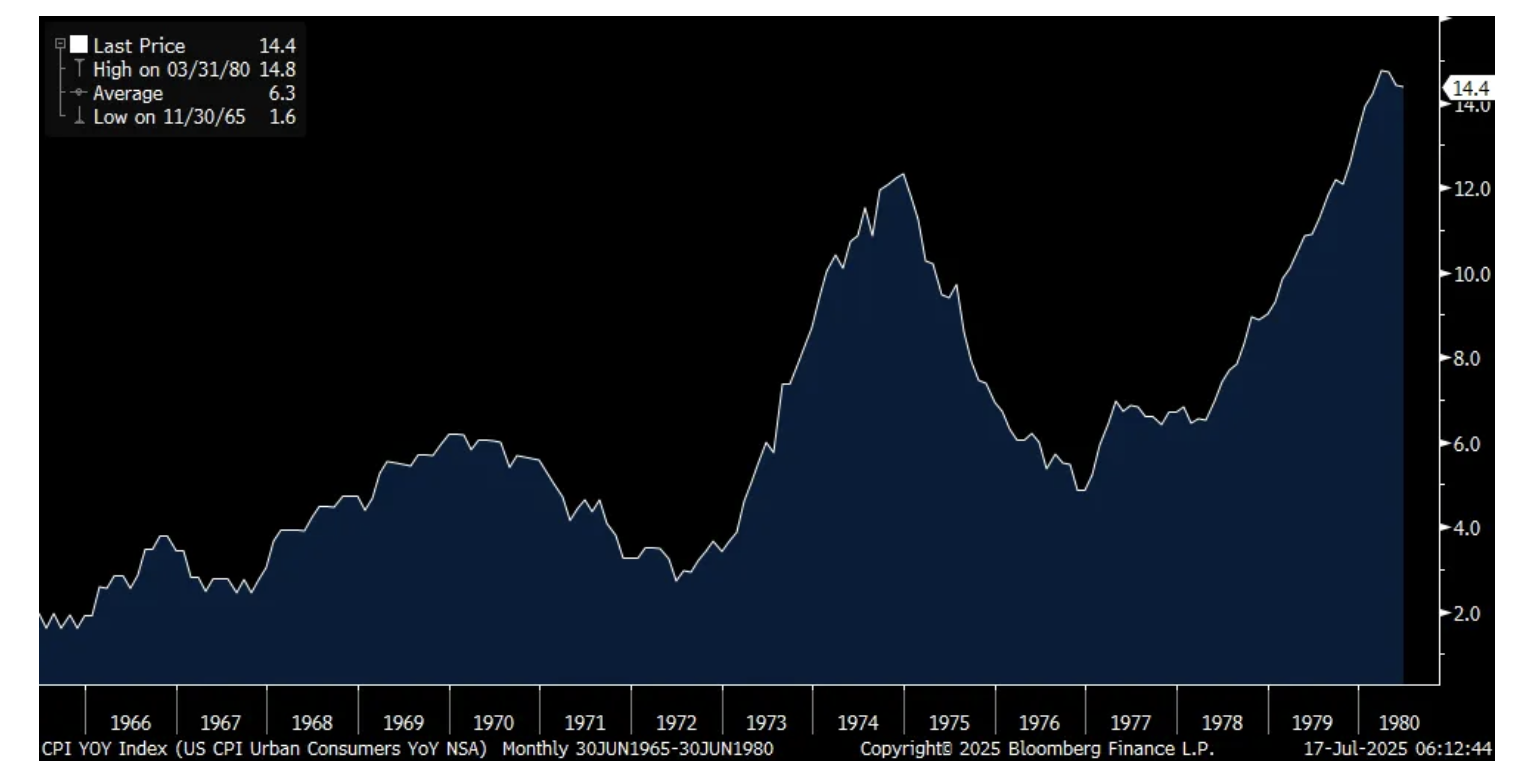

Note that it was the summer of 1972, months before the November election that Nixon was really cajoling Burns for easy money and you can see the result. CPI in June 1972 went from 2.7% to 12% by December 1974.

CPY 1965-1980 y/o/y

From the Fed’s Beige Book, it does read like blah economic growth but slightly better than the prior Beige Book. “Economic activity increased slightly from late May through early July. Five Districts reported slight or modest gains, five had flat activity, and the remaining two Districts noted modest declines in activity. That represented an improvement over the previous report, in which half of Districts reported at least slight declines in activity. Uncertainty remained elevated, contributing to ongoing caution by businesses.”

“Nonauto consumer spending declined in most Districts, softening slightly overall. Auto sales receded modestly on average, after consumers had rushed to buy vehicles earlier this year to avoid tariffs. Tourism activity was mixed, manufacturing activity edged lower, and nonfinancial services activity was little changed on average but varied across Districts.”

“Loan volume increased slightly in most Districts. Construction activity slowed somewhat, constrained by rising costs in some Districts. Home sales were flat or little changed in most Districts, and nonresidential real estate activity was also mostly steady.”

On the labor market, “Employment increased very slightly overall, with one District noting modest increases, six reporting slight increases, three no change, and two noting slight declines. Hiring remained generally cautious, which many contacts attributed to ongoing economic and policy uncertainty…Although reports of layoffs were limited in all industries, they were somewhat more common among manufacturers.”

And, “Looking ahead, many contacts expected to postpone major hiring and layoff decisions until uncertainty diminished.”

With pay, “Wages increased modestly overall, extending recent trends, with reports that ranged from flat wages to moderate growth.”

With respect to costs and pricing, “Prices increased across Districts, with seven characterizing price growth as moderate and five characterizing it as modest, mostly similar to the previous report.” On the cost side, “In all twelve Districts, businesses reported experiencing modest to pronounced input cost pressures related to tariffs, especially for raw materials used in manufacturing and construction. Rising insurance costs represented another widespread source of pricing pressure.”

On the pass thru side, “Many firms passed on at least a portion of cost increases to consumers through price hikes or surcharges, although some held off raising prices because of customers' growing price sensitivity, resulting in compressed profit margins.” I bolded to highlight.

And from here, “Contacts in a wide range of industries expected cost pressures to remain elevated in the coming months, increasing the likelihood that consumer prices will start to rise more rapidly by late summer.”

I’ll add, it all sounds like a 1-1.5% type growth economy with some having the ability to manage tariffs better than others with respect to whether consumers pay and/or the business does. See below Moynihan’s comments and he agrees with me on 1.5%.

Here were some of the comments on the tariff influence:

Boston:

"prices at selected specialty food stores and restaurants rose moderately in response to tariffs—but otherwise retail and tourism contacts reported steady prices."

"Manufacturing firms not exposed to tariffs reported flat input and output prices, while other manufacturers experienced modest to moderate cost increases from tariffs and raised prices by above-average margins to account for infrequent price adjustments."

NY:

"the pace of input price increases remained steep as tariff-related cost increases were widespread. Many businesses reported continuing to pass on some or all tariff cost increases to their customers. A manufacturer of doors for a Manhattan construction project reported a significant jump in costs due to the tariffs on steel. Several food and beverage establishments reported significant concerns about the rising costs of inputs. Tariffs have pushed up the cost of auto parts and dealers are generally passing these on to customers. A regional retailer described selectively raising prices on goods with less elastic demand that were not subject to tariffs, in order to offset rising costs among tariffed goods. An appliance manufacturer noted that tariff surcharges were disappearing as higher costs were now baked into prices overall."

Philly:

"Many contacts reported tariff-related increases in costs and prices, but some contacts noted that cost increases haven't materialized or were more limited than expected. However, most contacts expected further tariff impacts in the coming months. The indexes for future prices paid and future prices received continued to suggest that manufacturing firms expect price increases over the next six months. Both indexes moved higher and remained well above their historical nonrecession averages."

Cleveland:

"On balance, contacts' reports indicated that nonlabor input costs continued to rise at a robust pace in recent weeks and that the cost stabilization seen during 2024 had dissipated. Many manufacturers noted that tariffs had increased the costs of the materials they import, and some retailers reported tariff-related cost increases from foreign and domestic suppliers."

"Across industries, contacts continued to report raising prices to cover costs related to tariffs and elevated prices of materials and insurance. Many reports indicated increased price sensitivity related to softening demand. This sensitivity was evidenced by contacts selectively and cautiously increasing prices, holding prices steady while making other cost-saving changes, and, in some cases, cutting prices to compete. Other signs of this sensitivity were the dips in sales after commercial construction contacts raised their prices. Still, several contacts in manufacturing and professional and business services anticipated increasing prices in the near term ahead of contract renewals."

Atlanta:

"Many businesses reported inflationary concerns surrounding the direct and indirect effects of trade policy and related uncertainty. Firms with exposure to tariffs continued to describe various approaches to cost pass-through, such as sharing tariff-related cost increases with both suppliers and customers. Some businesses have raised prices ahead of imposed tariffs. Others said they were waiting to raise prices until they had more clarity on trade policy, which puts pressure on margins but minimizes price volatility. Several contacts noted they were still working through pre-tariff inventories, thus delaying price adjustments. Contacts continued to reconfigure supply chains amid trade turmoil but noted difficulties executing plans given the uncertainty around final tariff levels for different countries."

Chicago:

"Several manufacturers cited increases in costs of materials due to tariffs, including for steel, aluminum, tungsten, and magnets. Overall, producer prices increased moderately while consumer prices rose modestly. One retail industry analyst said that they expected tariffs to be felt broadly at the consumer level in late July and early August although they were not yet materially impacting retail prices."

St. Louis:

"Some contacts reported absorbing higher costs, but many contacts reported passing along these costs to customers. A bourbon producer reported that they were absorbing higher costs, and an auto dealer reported that, for the time being, the manufacturer was absorbing tariff-related costs. A packaging company reported facing a pigment surcharge of 10 percent to 15 percent in anticipation of tariffs and that they were not passing it along to customers due to competition with larger manufacturers. On the contrary, a construction company reported that HVAC equipment and utility billing had increased and that those costs had to be passed along. Consumer packaged goods companies reported increasing prices, which will raise costs for grocery stores over the next 90 days. A wellness center reported that service providers had responded to higher costs by offering more add-on services. A manufacturing company in Memphis reported they had raised prices significantly to offset the tariff cost on steel and aluminum as well as tariffs on imports from China."

Minneapolis:

"Price increases were modest overall with a slower rate of increase than the last report, but price pressures were greater among manufacturing contacts. About a quarter of District firms increased the prices they charged to customers in June from a month earlier, according to a monthly survey, and about the same percentage anticipated increasing their prices in the month ahead. Slightly less than half of respondents reported increased input prices over the previous month. Manufacturers continued to report that suppliers added surcharges on orders in response to tariffs, particularly those on steel and aluminum. A construction materials supplier commented that "it seems that prices have gone up out of fear that prices will go up." In contrast, a custom manufacturer reported that tariffs impacted only a small percentage of their inputs."

KC:

"Manufacturers and service providers both experienced profit margin compression with input prices increasing more than retail prices. However, some firms reported they are planning broad-based price increases across product lines to maintain profitability. For example, the costs of sourcing used car inventory rose, which contacts indicated will lead to persistent auto price pressures. Expectations of price growth remained elevated in most other consumer-oriented sectors as well."

Dallas:

"Manufacturing raw materials prices and finished goods prices rose further in June after rising following the April tariff announcement. A few energy contacts reported higher input costs because of the steel tariffs. A transportation equipment manufacturer noted that even prices for domestic steel have increased as demand shifted from imported steel to domestically produced steel."

SF:

"Price increases were reported across a wide range of industries, including manufacturing, health care, real estate, and financial services. Insurance prices rose notably, and modest increases were reported in fresh food prices. Higher tariffs, particularly for companies using hardware components, intensified the pressure on their final prices, leading some manufacturers to include an explicit tariff surcharge. The cost of raw materials remained elevated, although prices for lumber and manufactured wood products were reportedly depressed."

To some notable earnings comments.

Brian Moynihan sounded positive on the economic backdrop, similar to his peers but tends to not deflate his consumer spending comments for inflation when talking about it:

“We continue to see solid consumer spending data…improving credit quality…plenty of household net worth growth in the market growth, and also the account balances, again, staying strong above where they were pre-pandemic.”

“We see solid commercial loan growth, and we see good credit quality with the exception of CRE in office…But we also see our clients continue to see clarity with the changes in trade and tariffs, and now with the tax bill passing, we can see them start to understand the future and expect them to behave accordingly.”

“We saw improving market conditions during the quarter, and that leads our worldwide leading research team to continue to predict no recession, a modestly growing economy at about 1.5% at the end of the year and continued no Fed rate cuts till next year.”

From United Airlines, whose stock is down pre market:

"Beginning in early July, United has seen a sequential 6 point acceleration in demand and a double-digit acceleration in business demand vs the second quarter. The airline attributes this to less geopolitical and macroeconomic uncertainty." They gave guidance that was about in line with expectations.

Premium cabin revenue rose 5.6% y/o/y while basic economy saw growth of 1.7%.

From Alcoa:

"With the increase in the US Section 232 tariff rate from 25% to 50%, we expect quarterly tariff costs to approximate $215 million based on an LME of $2,600 and a Midwest premium of $.67 per pound."

"From a demand perspective, conditions remain steady in both Europe and North America, although sector performance is mixed. Electrical and Packaging continue to perform well. Construction appears to be stabilizing and Automotive remains the most affected by tariff related uncertainty. In China, easing trade tensions with the US are providing a modest boost to demand."

"On the supply side, growth was limited in the second quarter with only marginal increases from smelter restarts and expansions. Global production remains constrained, particularly outside of China."

To some overseas economic data, Japan said its June exports fell .5% y/o/y vs the estimate of a gain of .5%. Specifically car and steel exports were down, likely tariff influenced with total exports to the US down by 11.4% y/o/y. This though was partly due to Japanese exporters absorbing some of the tariffs as the amount of cars exported to the US rose y/o/y. That said, a few weeks ago stories started to come out that Japanese automakers were done absorbing costs and were going to start raising prices.

The UK labor market was soft again in June with a drop in 'payrolled employees' of 41k vs the estimate of -35k. The positive was that while May was negative too, it was less so with an upward revision of 84k to -25k. Their unemployment rate thru May rose to 4.7% from 4.6% and that is the highest since June 2021. Weekly earnings ex bonus remained strong, rising by 5% y/o/y. Chancellor Reeves and her higher imposed payroll and insurance taxes really has been a damper on the UK labor market and why the Labor Party's poll numbers have tanked. While gilt yields are higher, along with yields across Europe, the pound is down vs the US dollar while the FTSE 100 is rallying.

UK Unemployment Rate

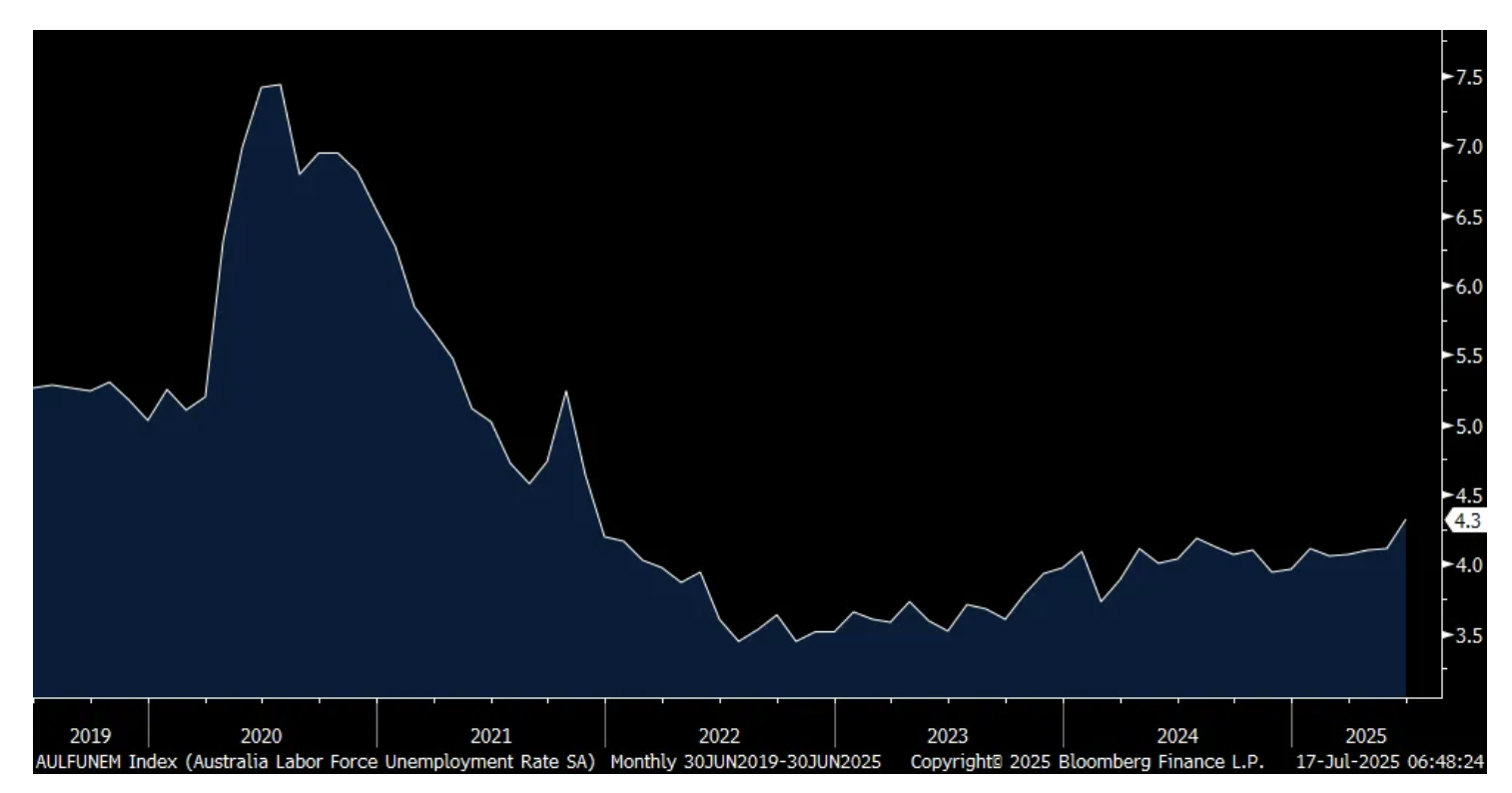

The June unemployment rate in Australia rose to 4.3% from 4.1% and that is the highest since November 2021.

Australia Unemployment Rate

BY Doug Kass · Jul 17, 2025, 10:11 AM EDT

With S&P cash +5 handles I am expanding my short index calls.

BY Doug Kass · Jul 17, 2025, 9:45 AM EDT

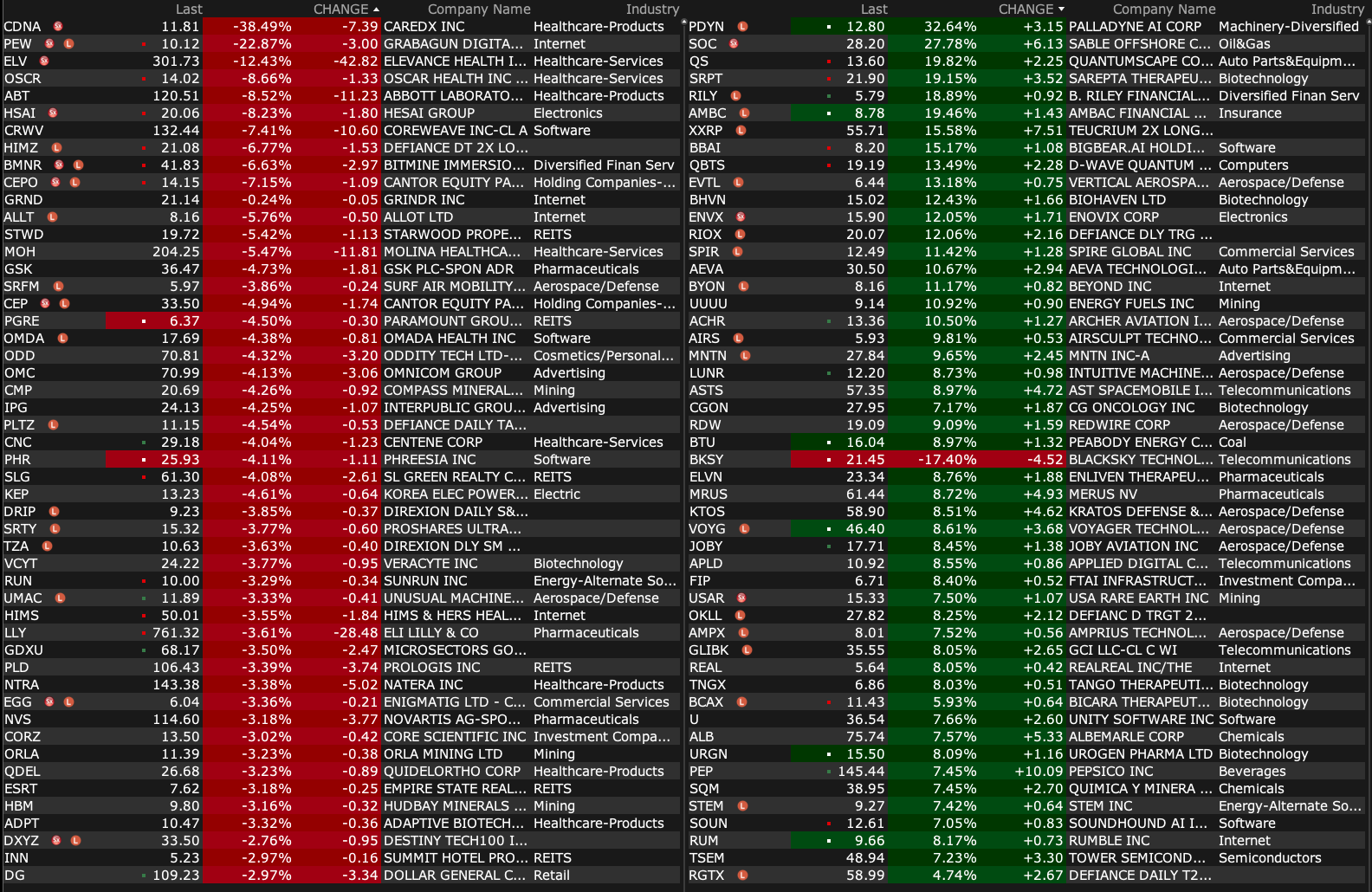

BY Doug Kass · Jul 17, 2025, 9:22 AM EDT

BY Doug Kass · Jul 17, 2025, 9:12 AM EDT

-LCID +37% (UBER to purchase $300M of LCID common stock in private placement; files Preliminary Proxy Statement with the SEC to Initiate Plan for Reverse Stock Split)

-SRPT +28% (reaches agreement with FDA on revised ELEVIDYS labeling; announces strategic restructuring, pipeline prioritization plan including 36% workforce reduction; reports prelim Q2)

-MCRI +17% (earnings)

-DGXX +15% (acquires Supermicro NVIDIA B200 Systems to Launch Tier 3 NeoCloud AI Infrastructure)

-RCKT +13% (receives FDA Regenerative Medicine Advanced Therapy (RMAT) Designation for RP-A601 Gene Therapy for PKP2-Arrhythmogenic Cardiomyopathy)

-ACTU +12% (advances Clinical Program in Ewing Sarcoma After Positive Phase 1 Trial Demonstrates Complete and Partial Responses in Difficult-to-Treat Pediatric Sarcomas)

-EVTL +8.3% (completes world’s first public airport-to-airport flight)

-BMNR +8.1% (holds ~$1B of Ethereum to advance its Ethereum Treasury Strategy)

-PRAX +6.3% (receives FDA Breakthrough Therapy Designation for Relutrigine for treatment of Seizures associated with SCN2A and SCN8A Developmental and Epileptic Encephalopathies)

-CSX +5.2% (UNP said to examine acquisition of 'a rival')

-MAN +4.9% (earnings, guidance)

-TOST +3.8% (Deutsche Bank Raised TOST to Buy from Hold, price target: $54)

-NSC +3.4% (UNP said to examine acquisition of 'a rival')

-AIR +3.3% (earnings, guidance)

-PEP +3.1% (earnings, guidance)

-PGY +2.9% (reports prelim Q2)

-NB -17% (files to sell common shares)

-STXS -8.1% (files to sell $12.5M Registered Direct Offering of Common Stock)

-ABT -5.2% (earnings, guidance)

-MP -4.8% (prices $650M upsized offering of 11.8M shares at $55.0/shr)

-USB -4.1% (earnings, guidance)

-MU -3.6% (weakness in sympathy with SK Hynix following Goldman downgrade)

-ADM -2.8% (President Trump says KO agrees to use cane sugar in Coke in the US)

-UNP -2.5% (UNP said to examine acquisition of 'a rival')

BY Doug Kass · Jul 17, 2025, 9:04 AM EDT

FED SPEAKERS

10:00 a.m.: Fed Board Governor Kugler (Voter) speaks on "A View of the Housing Market and U.S. Economic Outlook" before the Housing Partnership Network Symposium, Washington, DC (Text available. No Q&A. Webcast );

12:00 p.m.: New York Federal Reserve Bank Director of Research Athreya speaks on National and Regional Economic Outlook at General Membership Luncheon, NYC;

12:45: Fed Bank of San Francisco President C. Daly (Non-Voter) speaks on Inflation, Monetary Policy and the U.S. Economy at the 2025 Rocky Mountain Economic Summit, WY (The event will be livestreamed and will also be made available as a recording);

1:30: Fed Board Governor Cook (Voter) speaks on "Artificial Intelligence and Innovation" before virtual National Bureau of Economic Research (NBER) Summer Institute: Digital Economics and Artificial Intelligence, Washington, DC (Text available. Q&A from moderator. Livestream);

7:30: Fed Board Governor Waller (Voter) speaks on the economic outlook before the Money Marketeers of New York University, NYC (Text available. Q&A from moderator and audience. Audio-only stream access: 1 646 558 8656, meeting ID 522723)

TREASURY AUCTION

11:30 a.m.: Treasury hosts a $90B 4 and $80B 8 Week Bill Auction.

BY Doug Kass · Jul 17, 2025, 8:55 AM EDT

BY Doug Kass · Jul 17, 2025, 8:35 AM EDT

From Scott Rubner: Global Market Intelligence (GMI) | August Views - Citadel Securities

BY Doug Kass · Jul 17, 2025, 8:17 AM EDT

Who's sorry now?

Who's sorry now?

Whose heart is achin' for breakin' each vow?

Who's sad and blue? Who's cryin' too?

Just like I cried over you

Right to the end

Just like a friend

I tried to warn you somehow

You had your way

Now you must pay

I'm glad that you're sorry now

- Connie Francis, Who's Sorry Now?

As I mentioned yesterday in "Cracks Below the Surface" there are a number of emerging technical conditions that suggest equities might falter in the near term.

We will see (by the end of August) who will be sorry now... and who will be seen as today's fool:

The tears I cried for you could fill an ocean

But you don't care how many tears I cry

And though you only lead me on and hurt me

I couldn't bring myself to say goodbye

'Cause everybody's somebody's fool

Everybody's somebody's plaything

And there are no exceptions to the rule

Yes, everybody's somebody's fool

- Connie Francis, Everybody's Somebody's Fool

RIP Connie Francis.

Connie Francis, Whose Ballads Dominated ’60s Pop Music, Dies at 87 - The New York Times

BY Doug Kass · Jul 17, 2025, 7:55 AM EDT

BY Doug Kass · Jul 17, 2025, 7:17 AM EDT

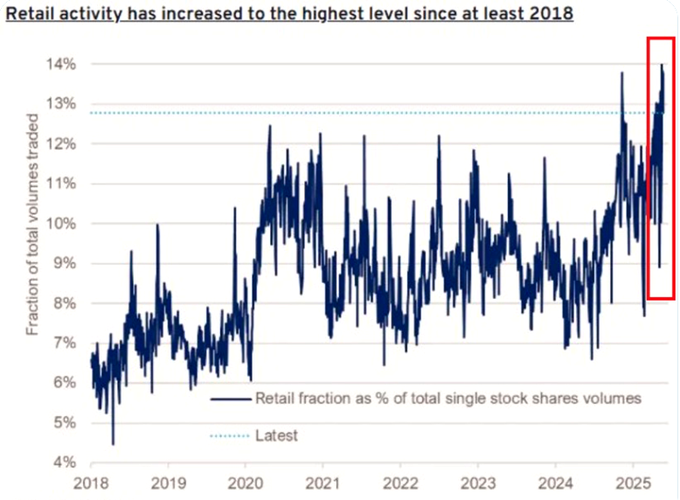

* Things you see near a market top

* With apologies to Mad Magazine...

At 14%, retail's share of overall trading has hit a seven-year high.

This exceeds the 12% market share during the 2020-2021 meme frenzy.

BY Doug Kass · Jul 17, 2025, 7:05 AM EDT

From Divine this morning in S&P Losing Steam:

But it’s also that a week ago the number of stocks making new lows was a mere 11 issues. Now that number stands at 40. For most of the day on Wednesday there were actually more new lows than highs on the NYSE but that shifted late in the day to give us eight more highs than lows.

Yet the market itself doesn’t seem to want to go down. Of course as I noted a week ago, just when you think it will never go down again, it somehow manages to do so.

From Wally:

BY Doug Kass · Jul 17, 2025, 6:31 AM EDT

* The technical bandwagon goes "all in " on crypto this morning...

Bonus — Here are some great links:

Three Reasons to Expect Higher Prices

Breadth Just Broke and No One Told the Index

BY Doug Kass · Jul 17, 2025, 6:11 AM EDT

The S&P Short Range Oscillator stands at 1.97% vs. 2.82% — so it is less overbought than Tuesday (the most recent reading) and last week.

BY Doug Kass · Jul 17, 2025, 5:45 AM EDT