Wednesday's After-Hours Movers

As of 4:19 p.m.

BY Doug Kass · Jul 16, 2025, 4:40 PM EDT

As of 4:19 p.m.

BY Doug Kass · Jul 16, 2025, 4:40 PM EDT

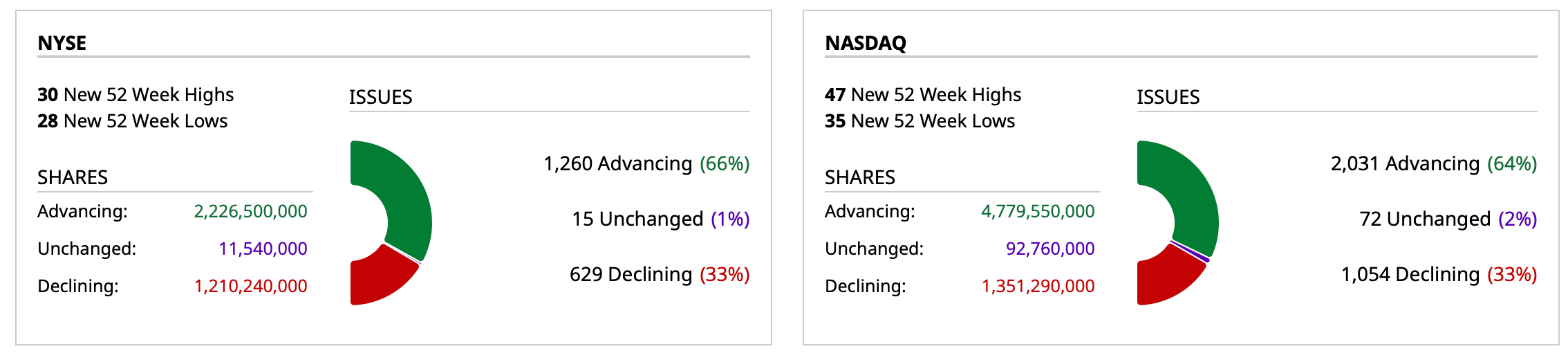

- NYSE volume flat to its one-month average;

- NASDAQ volume 7% above its one-month average;

- VIX index: down 1.27% to 17.16

BY Doug Kass · Jul 16, 2025, 4:26 PM EDT

From Peter Boockvar:

VIDEO - MRKT Call with Guy Adami : JGB's, Berkshire, Gold, Bitcoin, Earnings, Powell News and More.

I had fun appearing with Guy Adami on the RiskReversal MRKT Call today. In this episode we discuss why Japanese Government Bonds matter right now, and where the U.S. 10-year yield starts to become a real problem for equities. We benefited from seeing how assets reacted to today’s Powell leak and denial, as the news broke on air. Also, a look at Berkshire’s recent under-performance, a preview of upcoming earnings with how concentrated Mag7 names are within S&P consensus numbers. Plus, some thoughts on Bitcoin’s latest move. Hope you enjoy!

BY Doug Kass · Jul 16, 2025, 3:55 PM EDT

BY Doug Kass · Jul 16, 2025, 3:36 PM EDT

The concentrated/speculative tone of the market is rising (e.g. PLTR, CRCL, COIN, CVNA, HOOD, etc.) as large-cap tech stays in place.

And I don't know what to make of it!

BY Doug Kass · Jul 16, 2025, 3:16 PM EDT

With S&P cash +14 handles I am shorting more "in the money" index calls for September.

BY Doug Kass · Jul 16, 2025, 2:52 PM EDT

BY Doug Kass · Jul 16, 2025, 2:00 PM EDT

Over the course of the next few months the markets will be ideal for trading and sub-optimal for investing.

BY Doug Kass · Jul 16, 2025, 1:07 PM EDT

With S&P cash rallying by nearly +40 handles to breakeven, I am adding back to my short index position.

BY Doug Kass · Jul 16, 2025, 12:04 PM EDT

On the whoosh lower (S&P cash down by nearly -40 handles) based on the NY Times article that President Trump has penned a draft to fire Fed Chair Powell, I have reduced the size of my index shorts.

I plan to reshort on strength.

BY Doug Kass · Jul 16, 2025, 11:46 AM EDT

BY Doug Kass · Jul 16, 2025, 11:15 AM EDT

* Costco is down by another $14 today...

BY Doug Kass · Jul 16, 2025, 11:05 AM EDT

* In the Bull Market in Complacency...

What follows is a compilation of comments/columns in my Diary coupled with updated commentary sent to my hedge fund investors (Seabreeze Partners):

Despite our multiple objections, equities have continued to advance.

Well, I won't back down

No, I won't back down

You could stand me up at the gates of Hell

But I won't back down

No, I'll stand my ground

Won't be turned around

And I'll keep this world from draggin' me down

Gonna stand my ground

And I won't back down

- Tom Petty And The Heartbreakers - I Won't Back Down (Official Music Video)

While many are rejoicing and growing more bullish along with higher equity prices, we see the potential upside rapidly diminishing and the possible downside rapidly expanding. Indeed, according to our calculus there is now more than 4-times more risk than reward and few individual investment opportunities currently meet our standards (on the long side).

In my hedge fund I have modestly increased our net short exposure from, on average 15% in June, to about 20% in recent days. (Our short book is well diversified)

Our focus on lower than expected (consensus) corporate profits growth, persistently high interest rates and inflation, an ever-expanding budget deficit, elevated valuations and other factors support a continued ursine market outlook and net short exposure.

Here are some updates on our concerns:

* Consensus 2Q2025 S&P EPS has dropped by nearly 4% in the last few months.

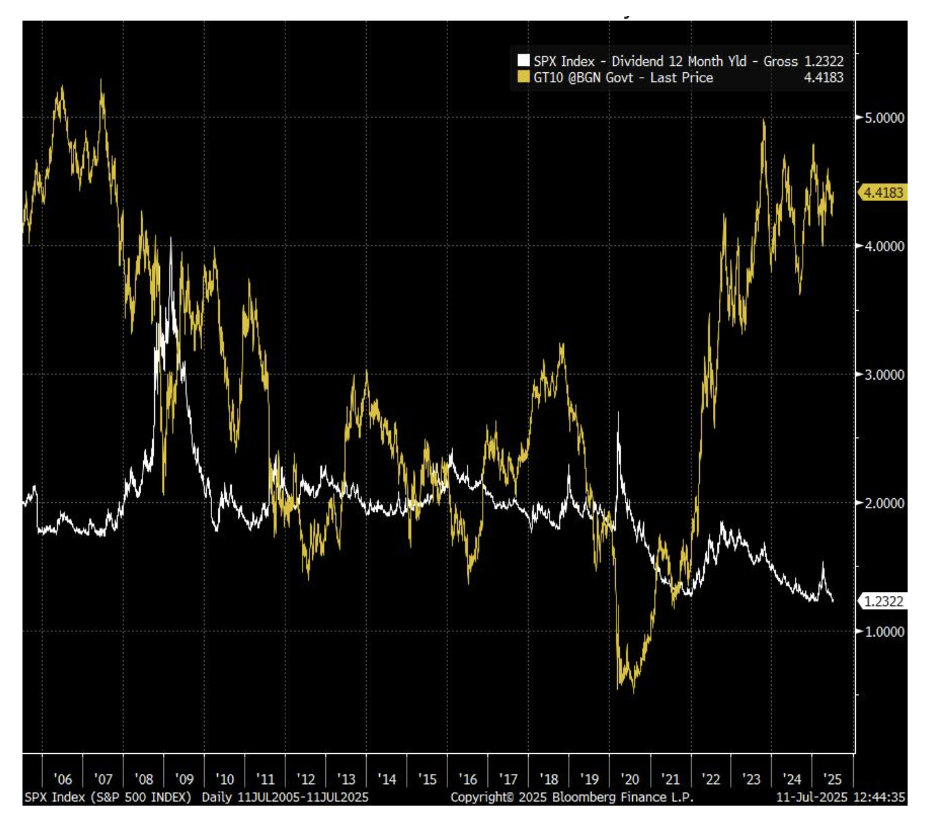

* Fixed-income markets provide an equity-like return with little risk or volatility.

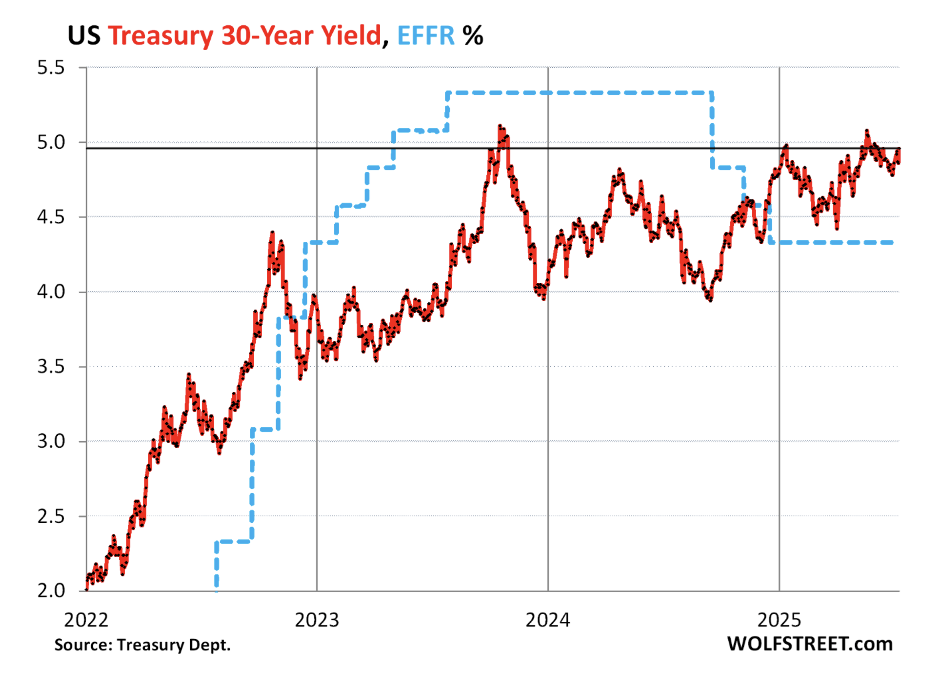

* Long-term Treasury yields have further risen (the long bond's yield is +18 basis (already) in July):

The rise in interest rates is a global phenomenon (and worldwide rates appear to be poised to breakout to the upside):

The 30-year Treasury yield (now back to late January, 2025 when equities topped) is a thermometer of the bond market’s current fears about:

1. Inflation over the long term

2. A lackadaisical Fed in face of this inflation

3. And a Mississippi River of new Treasury debt flowing into the market

* We see weakness in the U.S. residential real estate market contributing to a consumer-led economic slowdown in 2027. The housing markets (which hits above the belt) have already begun to turn down with a broad and sharp expansion in unsold home inventories across the country - particularly in California and Florida (two states that typically presage inflection points in overall national housing activity).

The spread between the average 30-year fixed mortgage rate and the 10-year yield has been fairly wide since the Fed ended QE and thereby stopped buying mortgage-backed securities and then started quantitative tightening in the second half of 2022 (as they started to unload its MBS holdings). The Fed has by now sold over $600 billion of its MBS and has said many times that it wants to get rid of its MBS entirely and only hold Treasury securities on its balance sheet.

Today the spread between the weekly average 30-year mortgage rate and the weekly average 10-year Treasury yield is 2.34 percentage points. Over the past four decades, the spread has been this wide only four times, twice very briefly just before and at the end of the Dotcom Bust and twice during two panics - when the 10-year yield plunged amid massive quantitative easing and mortgage rates were slower to follow. Now there is no panic, the 10-year Treasury yield is near 4.5% (and likely going higher) and the Fed is doing QT...

* Stocks are very expensive against profits and interest rates:

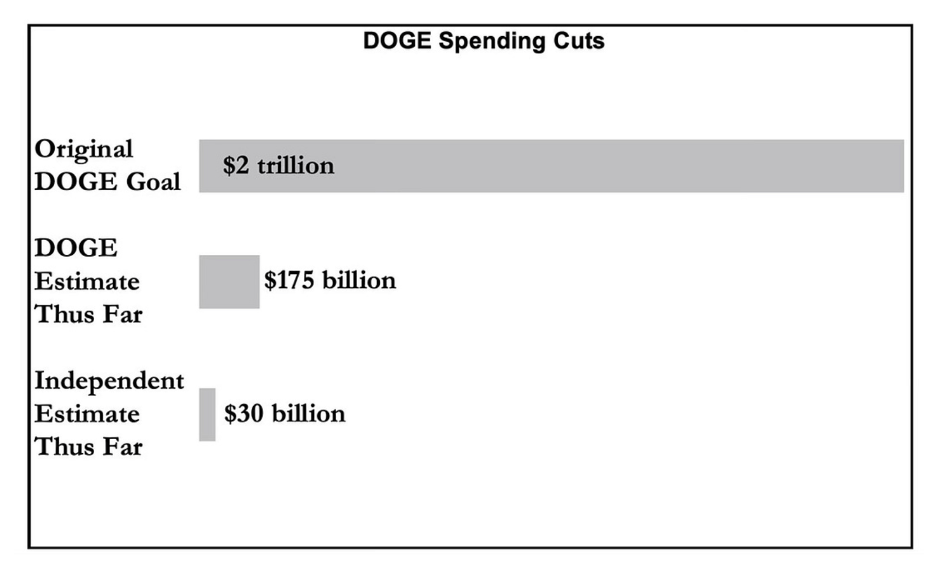

* The prospects for fiscal discipline - restraining the deficit and limiting the U.S. debt load - have deteriorated (perhaps explaining the recent rise in open market rates). The failure of DOGE was symptomatic of our nation's indifference towards cutting debt:

What follows are views on the budget crisis from the standpoint of two excellent sources (Bridgewater's Ray Dalio and John Mauldin):

Recently, Bridgewater's Ray Dalio commented on a trip he made to visit Republican and Democratic Congressional leaders in Washington, D.C. in which he discussed the growing U.S. deficits and debt load.

Dalio confirmed what we all know by now, that nothing will be done by both political parties to alter our country's trajectory of debt. Astonishingly, our Congressional leaders were in all agreement - there is no political will to steer clear of an economic crisis through tax increases and spending cuts (as they all agreed they would be voted out of office!).

Several weeks ago, Ray Dalio tweeted:

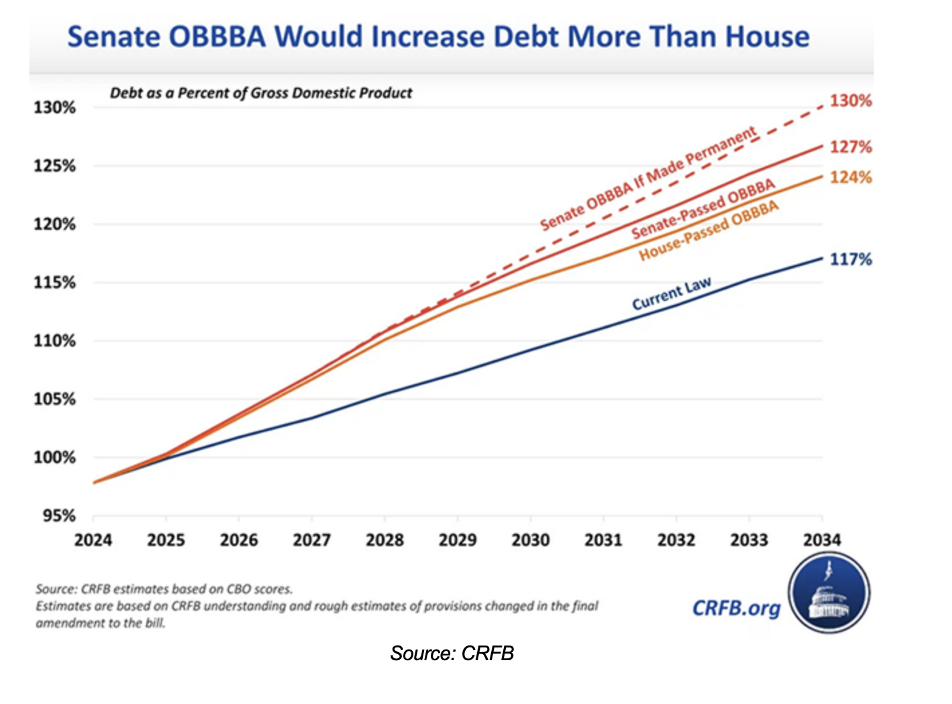

Now that the budget bill has passed Congress, we can see what the projections look like for deficits, government debt, and debt service expenses. In brief, the bill is expected to lead to spending of about $7 trillion a year with inflows of about $5 trillion a year, so the debt, which is now about 6x of the money taken in, 100 percent of GDP, and about $230,000 per American family, will rise over ten years to about 7.5x the money taken in, 130 percent of GDP, and $425,000 per family. That will increase interest and principal payments on the debt from about $10 trillion ($1 trillion in interest, $9 trillion in principal) to about $18 trillion (of which $2 trillion is interest payments), which will lead to either a big squeezing out (and cutting off) of spending and/or unimaginable tax increases, or a lot of printing and devaluing of money and pushing interest rates to unattractively low levels. This printing and devaluing is not good for those holding bonds as a storehold of wealth, and what’s bad for bonds and US credit markets is bad for everyone because the US Treasury market is the backbone of all capital markets, which are the backbones of our economic and social conditions. Unless this path is soon rectified to bring the budget deficit from roughly 7% of GDP to about 3% by making adjustments to spending, taxes, and interest rates, big, painful disruptions will likely occur.

From John Mauldin:

Another reason the federal debt keeps growing is we keep expanding the federal government’s responsibilities. It does all kinds of things that were once left to the private sector, or pays for state and local governments to do them. Once in place, these expanded roles are almost impossible to reverse. More often, they just get bigger. Hence the debt.

The latest effort to rationalize the budget will, unfortunately, do nothing of the sort. Let’s first visit the budget projections from the bipartisan and non-ideological Committee for a Responsible Federal Budget.

This is the CRFB projection for how OBBBA (the Senate version, which is what finally passed) will affect the debt.

Going into this year, CRFB estimated the federal debt would grow to 117% of GDP by 2034, assuming current law (including expiration of the 2017 tax cuts) remained in place. The OBBBA law as passed by the House would have increased this to 124%.

The Senate—which in our system is supposedly the more prudent and thoughtful chamber—made the debt impact even worse at 127%. And if the expiring provisions are made permanent, as is highly likely, it will be more like 130%.

Note also, none of this includes the impact of extraordinary events like war, pandemics, recessions, natural disasters, etc. Do you think we’ll get through the next 10 years without some such thing happening? Any of those will blow up the debt even more.

* The AI trade continues to dominate the investment landscape. It remains unclear (to us) that the hundreds of billions of AI capital spending will yield a reasonable return in the reasonable future. As well, we currently view AI “as the world’s most expensive mirror”:

From Cumberland Advisor's David Kotok who quotes me in his recent commentary:

One final thought: Where people get information and how they curate it is a growing issue. I offer readers sources and citations for as much as I can. The perils of relying on faulty informants is growing, IMO. As Churchill supposedly said, “A lie is halfway round the world before the truth has got its boots on.” (As is often the case, this aphorism actually goes back a long way. The renowned English Baptist preacher Charles. H. Spurgeon voiced it in a sermon in 1859, and the sentiment about the relative velocity of lies can be traced back to the Roman poet Virgil.)

Doug Kass (Seabreeze Partners) eloquently addressed a related issue and gave me permission to quote him. Thank you, Dougie. Here’s an excerpt from Doug’s morning missive on July 8, when he wrote about an article that reflected a misunderstanding of Grok and how it works:

It indirectly shows how AI is terribly misunderstood by the masses, and it indirectly gives a lot of perspective about the stock market. My point is NOT about the politics discussed in the article. I stay out of it, as it is unproductive. The point of my missive is what the author (conservative) does not understand. Grok was not re-programmed overnight to be “woke” because President Trump and Elon Musk are at odds again, as the author implies in the article. The issue, which has been well discussed, and is not even really a point anymore, is that generative AI can only take what is out there and spit it back out in a different format. It does not think, it only regurgitates. Thusly, if most of the news tells you the tragedy in Texas was due to a certain reason, the AI bots will tell you the same thing. Not complicated. They are the world’s most expensive mirrors. On the other hand, you could drop a billion apples in front of the world’s most powerful cameras attached to the world’s most powerful AI, and it could never come up with the theory of gravity if it already did not exist. Not new info, I have beat that horse to death, not the point of my little rant. If a journalist has no idea what is going on and how AI really works and what it does, what do you think the average person knows about AI?

Doug concludes (and I concur):

Same for the average politician or government official, frankly. They all kind of know zero. As in squat. Zilch. Nada. Zip. Jack. Bubkes. They just know what they are told, which is AI is this brand-new super genius technology that is about to find a cure for cancer and will put everyone out of work (but somehow grow GDP 10% per year at the same time).

* Much more bullish investment sentiment has followed higher stock prices. Most traditional metrics are in the 98%-tile and lie at levels that are very poor launching pads for future investment returns:

Rows and floes of angel hair

And ice cream castles in the air

And feather canyons everywhere

I've looked at clouds that way

But now they only block the sun

They rain and snow on everyone

So many things I would have done

But clouds got in my way

I've looked at clouds from both sides now

From up and down, and still somehow

It's cloud illusions I recall

I really don't know clouds at all

- Joni Mitchell, Both Sides Now.

Investors are now almost universally bullish. I have argued that investors are overly positive given the plethora of uncertainties.

Let’s Look At Both Sides Now starting with the headwinds:

Here is a partial list of my continuing concerns:

* We face the highest geopolitical risks in many decades (which will not be resolved quickly).

* We face the largest level of social and political risks in the U.S. since the Vietnam war.

* We face the greatest chance of "slugflation" (slowing economic growth and sticky inflation) since the 1970s.

* We face the biggest threat that the U.S. dollar and capital markets will no longer be a "safe haven" in modern history.

* We face the greatest debt load and deficit ever — and neither party seems to favor any fiscal discipline whatsoever.

* We face the largest capital spending spree in history (on artificial intelligence) — though the return on that investment is less certain (dot-com, it feels like Deja vu all over again.)

* We face a viable alternative to equities in fixed income (for the first time in 15 years) as bonds present an equity-equivalent yield with limited risk and volatility.

Regardless of my ursine view, at the suggestion of Oaktree's Howard Marks, I have made a list of what I believe to be the most significant and now consensus bullish arguments that could continue to buoy valuations. I will follow each point with an explanation of why I differ with some of these bullish arguments:

* There is a Fed Put: President Trump has announced that he will replace Fed Chairman Jerome Powell with a dove, leading to lower short-term interest rates.

The Fed now expects inflation to rise over the next few months, which is not an ideal setting for lower rates. A Fed Chair monitored and under the watchful eye of President Trump will likely produce a more uncertain monetary policy. I am not sure that a Fed Chair (with a committee of Board of Governors) will be as closely influenced by a Fed chief that works close or is even at the beckon call of the President. The capital markets could grow quite worried (with a dependent and not independent Fed); American Exceptionalism might be threatened with the selling of our currency and bonds, especially if the inflationary backdrop grows more problematic. Institutional credibility and independence will be challenged in a very public (and market!) way. Finally, wasn't there a lesson to be learned in 2024 when a one-percentage point cut in the Fed Funds rate produced higher intermediate and longer-term Treasury and mortgage rates? If this occurred, the equity risk premium would narrow ever more (with reduced S&P profits and higher risk-free interest rates).

* The current Administration is pro-business and economic growth and deregulation are the cornerstones of Trump policy.

President Trump's Big Beautiful Bill incorporates the notion of spending cuts with economic incentives (skewed toward corporations and the wealthy). There could be a populist pushback in a consumer-led slowdown. Given the deteriorating state of the business and economic cycles the outcomes of pro-business policy might be disappointing relative to expectations -- especially with the margin pressures of the evolution from globalism to nationalism.

* Geopolitical risks have been reduced with the recent aggressive attack against Iran's nuclear facilities.

Yes, for now. But there remain potential regional hotbeds that represent bonafide threats.

* With a U.S. service economy expanding, recessions are no longer likely.

I would say recessions are not endangered. But a service economy will likely cushion the magnitude of economic downturns. That said, AI could be threat to this theory of "stability," should a larger-than-expected displacement of jobs occur. The resumption of student loan repayments could further pressure personal expenditures. Also, as stated above, the shift from globalism to nationalism might prove to be a greater headwind to S&P earnings per share than the consensus expects.

* Corporate profits will grow steadily and above expectations over the balance of the year.

The rate of S&P EPS growth likely peaked in 1Q 2025. Who pays for higher tariffs, consumer or corporations? An estimated $400 billion of tariffs represent 20% of total corporate profits. It’s a Sophie's Choice: The imposition of tariffs will likely deliver either higher inflation or lower corporate profits.

* While the budget deficit and U.S. debt load are well above expectations, they are not threats, as a rising budget/debt as a percentage of GDP has been in place for years.

DOGE failed and both sides of the political view lack fiscal discipline. I would argue that, with annual interest payments now in excess of the defense budget, we are closer to seeing the reemergence of the Bond Vigilantes than ever.

* AI will provide a fountain of corporate productivity, additive to revenues and profits.

Thus far the commercial applications and user sets of AI are minimal, though this will likely change. But, as I have also argued, it is unclear whether the trillions of dollars of capital investment (by the hyperscalers and others) will result in an adequate return on invested capital. Moreover, the AI trade started in late 2022 and is almost three years old.

* Higher equities will deliver a wealth effect to the consumer and offset housing's weakness.

I agree that the consumer will benefit from a continuation of higher stock prices - but remember the S&P Index has simply returned to its late January/early February level. As to housing, the contraction is growing closer in focus and, given the disproportionate role of housing on consumer wealth, a drop in home prices could offset some of the wealth effect provided from the benefit from higher stock prices.

* American Exceptionalism is intact; if nothing else there is no alternative.

In a recent letter to investors, I suggested that it is time to rethink American Exceptionalism - and that the recent trend away from investing in the U.S. could reduce demand for domestic investments (at the margin) and the sense that we are a reliable safe haven.

* Price earnings multiples (at 23-times) are inflated, but in past periods of speculation valuations have been even higher.

This is where I disagree strongly with the bullish cabal. Isn't this simply "the greater fool's theory," in which investors are relying on a greater fool to bail them out? This hasn't worked well in the past when valuations were excessive. As reflected in an earlier exhibit in today's commentary, (historically speaking) current valuations are a poor launching point for future returns.

* The market's advance has been broadening out.

Yes, it has broadened out. But look at the lagging Russell Index, which has not been crowing. Let's keep a bead on market breadth in the weeks ahead.

* There is a massive build up in cash reserves that will flow back into equities.

The "cash on the sidelines" is as dumb as wood as an argument. First, cash should be looked at not in the absolute ($7 trillion), but as a percentage of stock market capitalization. As such, cash reserves are actually at the low end of history. Second, the maturation of the baby boomers suggests a lot of the cash is sticky (and being invested in equity-like returns now available in the fixed income markets).

* Market structure favors the bulls: The dominance of passive investing products and strategies has reduced "the float' of equities.

This is accurate. When combined with trillion-dollar buybacks (yearly), a rising demand for stocks is being met with a diminished float. For now, everyone is on the same side of the boat. Of course, when the worm turns (and equity fund redemptions rise) -- and it will eventually -- the movie goes in reverse and there will be few buyers (I am old enough to remember when the S&P slipped to 4850 2.5 months ago as sellers overwhelmed buyers.

* There is a new generation of value-insensitive investors and speculators that will buoy equities.

“There are no new eras – excesses are never permanent.”

- Bob Farrell

While equities continue to climb, risks are mounting in The Bull Market In Complacency.

BY Doug Kass · Jul 16, 2025, 10:30 AM EDT

Dougie Kass

Read my Sub Surface Weakness column and tell me where you disagree!

Thanks.

TechNova

Hey Dougie - I think your column is well formulated and well thought out as usual. I don't dis-agree with it precepts as much as I may differ with its meanings.

The Market has been buoyed by a massive rise in Global M2 and an ever falling US Dollar. This flush of liquidity has made most market participants sanguine and has pushed them to chase higher highs and ignore the negative effects of the current policies in the White House. Folks have taken to calling Trump's Tariffs Policies "Posture" and "Tactics", even though we all know that Taxes of this nature have real consequences when it comes to GDP growth.

I do believe we are headed for a pullback in the markets, and you are correct to note the underpinnings. But to me, one of the main reasons is the recent strength in the USD, which has a direct effect on Commodities. So Gold, BTC, and other Commodities are correctly bumping a bit as a reaction. I feel like a combination of Summer Seasonality, along with the first readings of inflationary pressures (as Importers finally start passing on the Taxes in the form of higher consumer prices) could contribute to a Summer Swoon, that gains momentum slowly, and peaks in August.

The reason I don't believe this pullback will be too severe as to cause the next major down cycle (don't see us going lower than SPX 5800 at worst), is that Global M2 will keep greasing the wheels, and with Trump berating JPOW on a daily basis, he gets to dangle the ZERO Interest rate carrot for traders who want to look 6 months ahead.

To me, that is the death knell. After this brief multi-week period of weakness, we will be getting many pronouncement of rate cuts. Trump will start floating 300 Basis Points.

I believe this will start the Blow Off Top Rally.

An absolute boom to the upside (SPX Target 6800 - 7000), that will raise all boats.

There will be euphoria, there will be dance, and most Market "Experts" will raise their 2026 targets to $8500.

That is when I think the whole thing will break. It will start in the Bond Market, with the long end flying high and out of control. Carry trades will unwind, starting in Japan, through Taiwanese Insurers, and through the world.

I believe the crash will be one for the books, and one that the new Gen Z traders have never gotten a change to witness.

We shall see.

BY Doug Kass · Jul 16, 2025, 10:20 AM EDT

From Peter Boockvar:

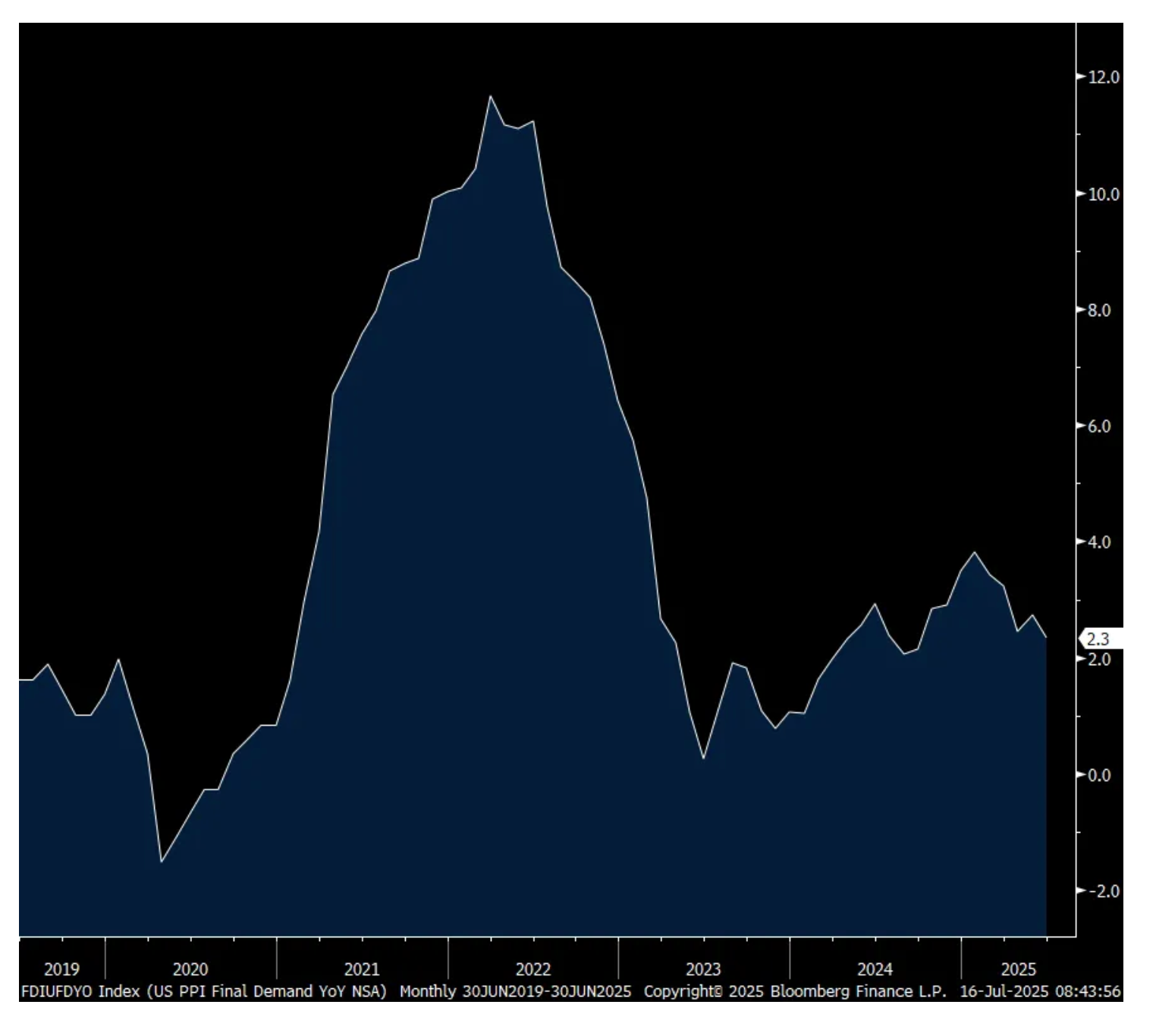

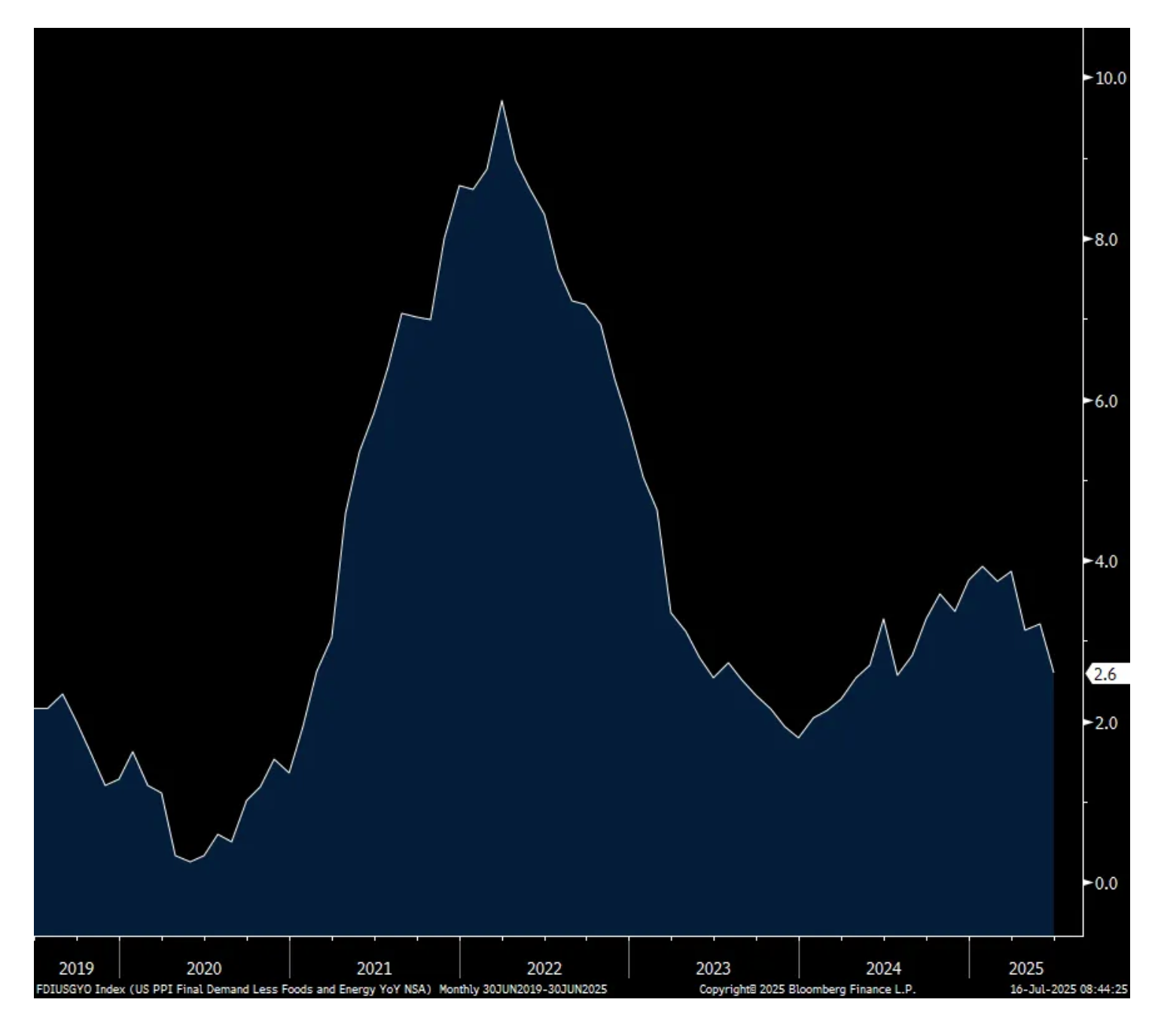

PPI stats about as expected when including revisions

If we take the upward revisions to May PPI, the June wholesale price figures were about as expected. May headline was revised up by 2 tenths to a 3 tenths gain and June saw no change from that vs the estimate of up .2%. The core rate was a touch above expectations as while June was 2 tenths below the forecast, May was revised up by 3 tenths to a .4% increase. The y/o/y gains were 2.3% headline and 2.6% core vs 2.7% and 3.2% in the month before.

The component I keep watching for an impact from tariffs is core goods prices, ex food/energy, and they rose .3% m/o/m after a .2% rise in May, and .3% increases in April and March. They are now up 2.5% y/o/y. Goods price inflation for now has bottomed.

A .9% m/o/m decline in transportation/warehousing kept a lid on services inflation as it fell one tenth m/o/m after a .4% rise in May. Truck transportation prices in particular fell .6% after rising by .5% in May. Also weighing on service prices was a 4.1% drop in ‘traveler accommodation services.’ Prices fell too for ‘automobiles and automobile parts retailing’, deposit services, airline passenger services, and food/alcohol wholesaling. On the upside, prices rose for machinery, equipment, parts and supplies wholesaling; furniture retailing; and apparel, jewelry, footwear and accessories retailing. All of those can be tied to tariffs.

Bottom line, bonds are rallying in response with yields down about 2 bps across the curve after yesterday’s selloff but including the upward May revisions, as stated, the data was about as expected. Maybe it’s a relief that it wasn’t hotter than expected. And I’ll highlight again, core goods prices are now up .2% to .3% for 6 straight months in PPI. Inflation breakevens are off about 1 bp.

Import prices should be a focus too tomorrow as it’s the initial touchpoint for importers in paying the tariffs.

Core Goods Prices (ex food/energy) m/o/m

PPI y/o/y

Core PPI y/o/y

BY Doug Kass · Jul 16, 2025, 10:05 AM EDT

Dougie Kass

I feel the same as I did at this time yesterday morning.

I am seller of strength.

BY Doug Kass · Jul 16, 2025, 9:55 AM EDT

8:00AM: Fed Bank of Richmond President Barkin (Non-Voter) speaks on "Forecasting Beyond Today's Data" before the Carroll County EDA and Chamber. Repeat of July 15th speech (Time, other details TBA)

9:15AM: Fed Bank of Cleveland President Hammack (Non-Voter) speaks on "Community Development" before the Cuyahoga County Community College Corporate College 20th Anniversary Celebration Business Breakfast, Warrensville Heights, OH (Text available. No audience Q&A. Livestream TBD)

10:00AM: Fed Board Governor Barr (Voter) speaks on "Financial Regulation" before the Brookings Institution, Washington, DC (Text available. Q&A from moderator and audience. Webcast at https://www.youtube.com/user/Brook-ingsInstitution)

6:30PM: Fed Bank of New York President Williams (Voter) gives keynote before the New York Association for Business Economics (NYABE) Distinguished Speaker Series, NYC (Text and moderated Q&A expected)

11:30AM: Treasury hosts $65B 17-Week bill Auction

BY Doug Kass · Jul 16, 2025, 9:45 AM EDT

"Opinions are like assholes, everyone has one."

- Lee Cooperman

BY Doug Kass · Jul 16, 2025, 9:30 AM EDT

BY Doug Kass · Jul 16, 2025, 9:21 AM EDT

BY Doug Kass · Jul 16, 2025, 9:10 AM EDT

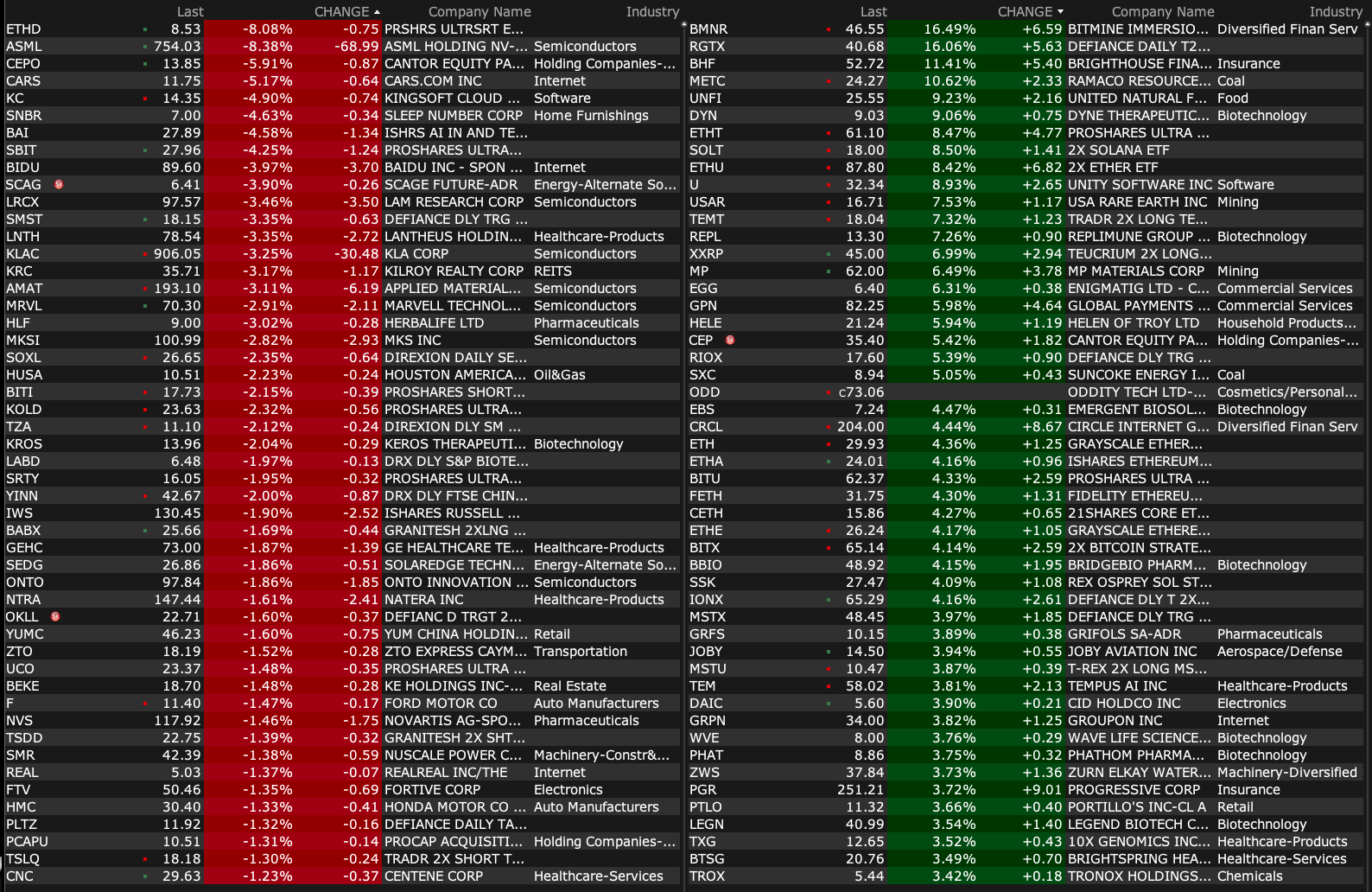

-BNRG +20% (signs MoU with ENASCO to Pioneer Nuclear SMR-Integrated Thermal Energy Storage Solutions)

-BMNR +18% (Peter Thiel acquires 9.1% stake)

-BHF +9.7% (reportedly near deal to be acquired by Aquarian)

-RGTI +9.7% (achieves its mid-year performance milestone of 99.5% median two-qubit gate* fidelity on its modular 36-qubit system)

-INBS +9.0% (signs global deal to distribute SmarTest Patch outside US and Canada)

-UNFI +8.2% (guidance)

-U +7.5% (hearing Jefferies raises price target)

-RMCF +7.3% (earnings)

-GPN +6.3% (Elliott Management has built a stake in GPN following Worldpay deal)

-LOBO +6.0% (enters strategic partnership with APOZ for U.S. market breakthrough)

-FHN +4.8% (earnings, guidance)

-PGR +2.9% (earnings)

-PLD +2.5% (earnings, guidance)

-APO +2.4% (said in discussions to buy stake in Atletico Madrid)

-PNC +2.2% (earnings, guidance)

-QXO +2.2% (CitiGroup Initiates QXO with Buy, price target: $33)

-JNJ +1.9% (earnings, guidance)

-DEO +1.8% (confirms CEO departure and succession plan; affirms outlook)

-KAPA -10% (reports Phase 2 ENV-105 safety data in mCRPC trial)

-ASML -7.4% (earnings, guidance)

-KMTS -6.7% (earnings, guidance)

-BIDU -3.8% (hearing Jefferies cuts price target)

-ARDT -3.5% (Tier1 firm Cuts ARDT to Underperform from Neutral, price target: $14.60 from $15.50)

-AXTA -2.0% (BMO Capital Markets Cuts AXTA to Market Perform from Outperform, price target: $33 from $51)

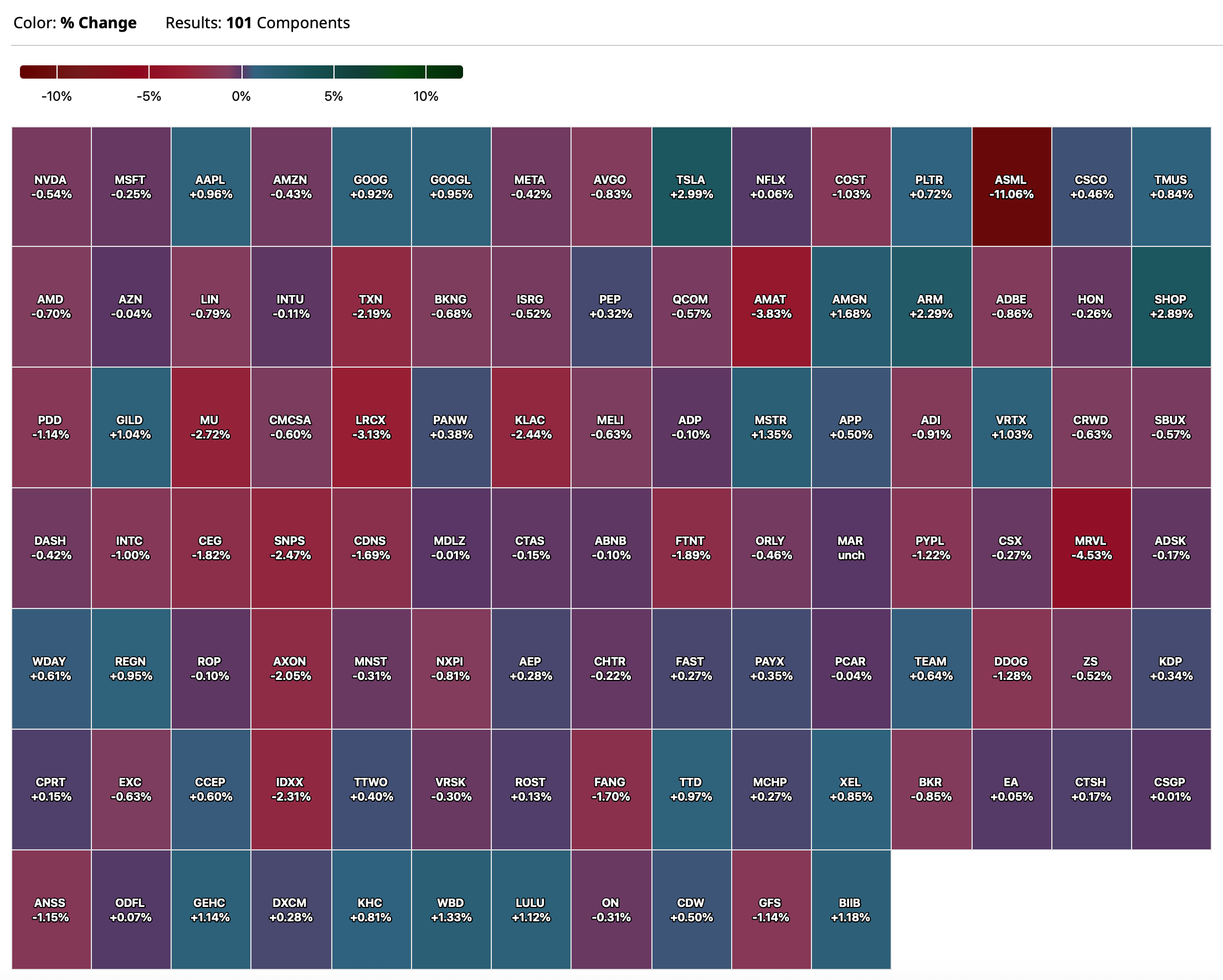

BY Doug Kass · Jul 16, 2025, 9:01 AM EDT

From Peter Boockvar:

The June CPI figure should put to rest the debate over whether tariffs are consumer inflationary, aka raise the cost of living for the items directly impacted. We saw the equivalent of 12 month gains in prices in just one month in a variety of goods prices and I list the m/o/m increases below. The question instead is how many months of flow through do we get (Helen of Troy said their 7-10% price increases will come over the coming months) and whether they are one time in nature. Theoretically they should be one time but mucking up global supply chains may lead to more than just a one time price change. Also, on the positive side, I do expect a continued deceleration in services inflation as slower rent growth continues to work its way through the CPI calculation. That said, we are sowing the seeds for an eventual acceleration in rental growth next year as current excess supply gets absorbed and little new multi family construction is taking place.

Price rise in June from May in select mostly imported goods:

Floor coverings +2.2%

Window coverings +2.2%

Other Linens + 5.5%

Laundry Equipment +1.8%

Other Appliances +2.0%

Clocks, lamps, & decorator items +1.6%

Non-electric cookware & tableware +3.7%

Tools, hardware, & supplies +1.2%

Apparel +.4% with men's shirts & sweaters up 4.3%

Footwear +.7%

Tires +.9%

Video & Audio products +.8%

Sports vehicles including bicycles +1.0%

Sports equipment +1.8%

Toys +1.8%

While CPI reflected a decline in used car prices, the Manheim wholesale used vehicle index is at the highest level since October 2023 and up 6.3% y/o/y.

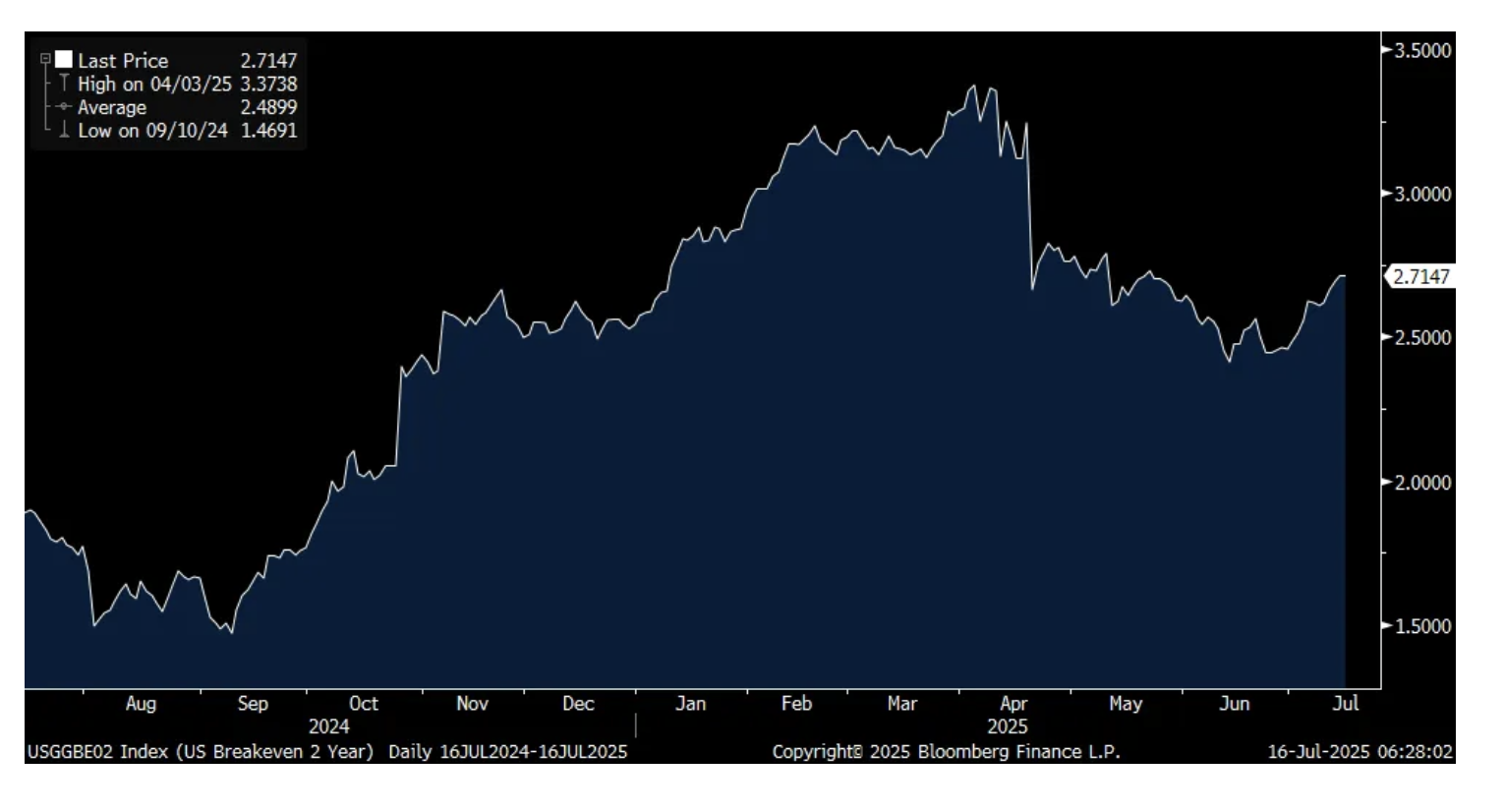

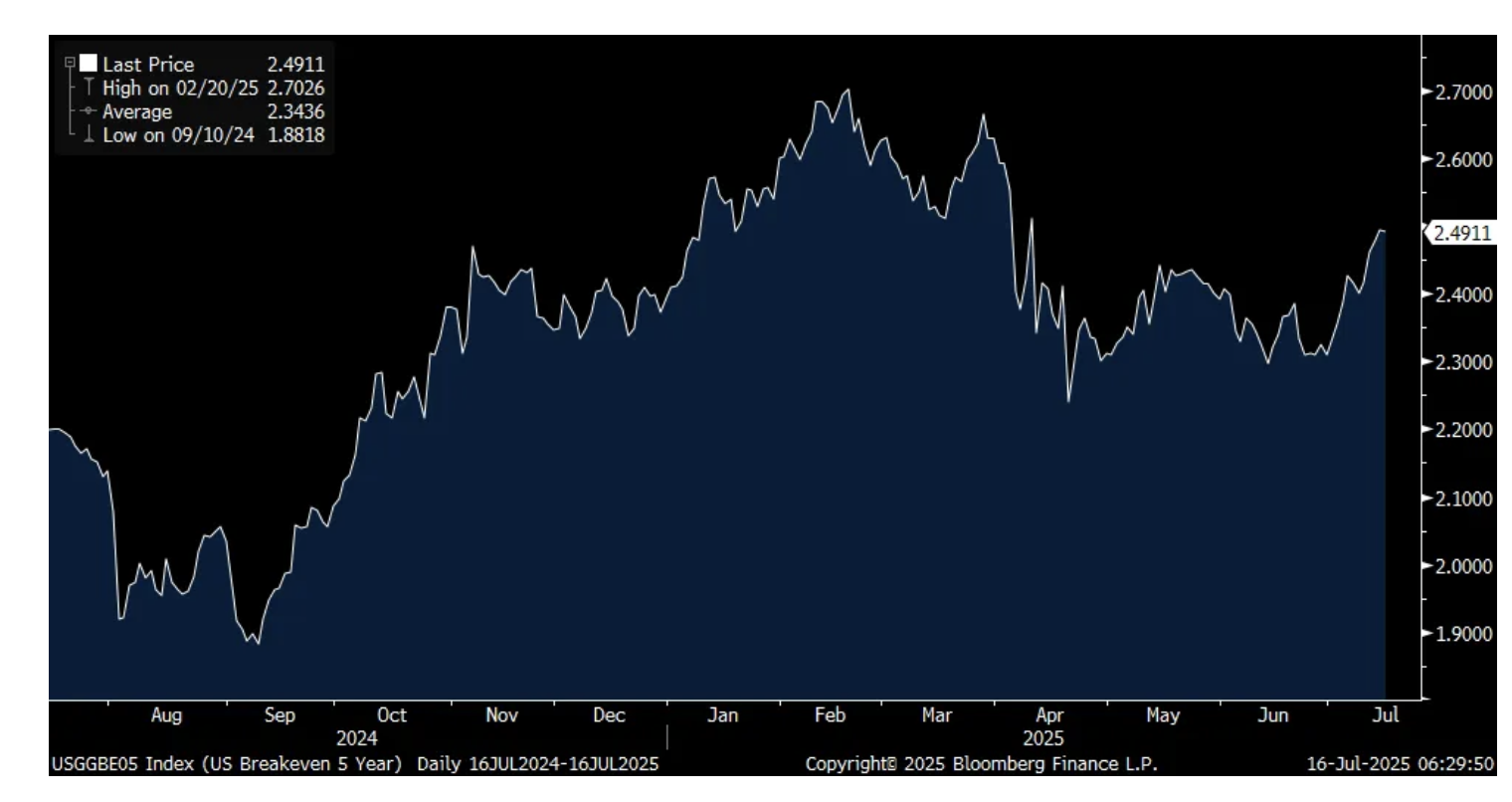

We of course saw a rise in interest rates across the curve as people looked under the hood of the CPI report and inflation breakevens were up as well. The 2 yr was higher by 2 bps after a 3 bps rise Monday and 4 bps increase on Friday. At 2.71% it's at a 2 month high, though still off its early April, Liberation Day, recent high. The 5 yr breakeven at 2.49% is at the highest since April 9th. Nothing alarming here at all but furthers my belief that any rate cuts we get from the Fed this year will just be tweaks more than anything.

2 yr Inflation Breakeven

5 yr Inflation Breakeven

On to some earnings calls.

From JP Morgan:

On debt and equity underwriting, "Our pipeline remains robust, and the outlook, along with the market tone and sentiment, is notably more upbeat."

"credit costs were $696 million, driven by builds in our C&I portfolio, including new lending activity and downgrades to a handful of names."

When asked about the financial health of their middle market customers, Dimon said "we continue to struggle to see signs of weakness...the consumer basically seems to be fine. Now, few things are true. Like, if you look at indicators of stress, not surprisingly, you see a little bit more stress in the lower income bands than you see in the higher income bands, but that's always true. That's pretty much definitionally true, and nothing out of line with our expectations."

"Our delinquency rates are also in line with expectations. You saw that we kept our net charge-off guidance unchanged. So, all of that looks kind of fine, and, to be honest, as we've said before, fundamentally, while there are nuances around the edges, consumer credit is primarily about labor markets, and in a world with 4.1% unemployment rate, it's just going to be hard, especially in our portfolio, to see a lot of weakness."

On tariffs, the CFO said "you recall the slide that we did at Investor Day, kind of highlighting that different sectors are going to have different experiences as a function of their margins, their sensitivity to input costs, the amount of pricing power, the amount of leverage, and where the rules actually land. But people are obviously getting some time to adjust, and we're watching it very closely. So, we'll see."

Of note too in the call with its stock trading at 2.8x tangible book, and while they are still buying back stock at current levels, Dimon said "I don't like buying back the stock at almost 3x tangible book. No one's going to convince me that's a brilliant thing to do."

Jane Fraser at Citi, a stock we own, always provides a good lay of the macro land in her earnings calls:

"Now let's turn to the environment. Well, it's proven to be more resilient than most of us anticipated, but we aren't dropping our guard as we begin the second half of the year. We expect to see goods prices start ticking up over the summer as tariffs take effect, and we have seen pauses in CapEx and hiring amongst our client base. All of that said, the strength of the US economy, driven by the American entrepreneur and a healthy consumer, has certainly been exceeding expectations of late. As I've been speaking to CEOs, I've yet again been impressed by the adaptability of our private sector, aided by the depth and breadth of the American capital markets."

From Wells Fargo:

"We maintained our strong credit discipline and credit performance continued to improve in the second quarter with lower net loan charge-offs from both the year ago and the first quarter. Losses in both our consumer and commercial portfolios improved from a year ago."

"As we look ahead, what we see regarding the health of our clients and customers has not changed. Consumers and businesses remain strong, as unemployment remains low, and inflation remains in check. Credit card spending growth softened very slightly in the second quarter, but it's still up y/o/y, and remains strong overall. And debit card spending growth has remained strong and consistent with what we saw in prior quarters."

"Consumer delinquencies continue to improve from a year ago, and commercial credit performance continued to be relatively strong. Deposit flows for both our consumer and commercial clients were in line with seasonal trends."

On tariffs, "I've (the CEO) had the opportunity to meet with many of our commercial banking clients this past quarter, and many have conveyed optimism that the administration is working to level the trade playing field. They would like certainty, but prioritize a good outcome for US trade above short term certainty. Many have found ways to avoid passing the 10% tariffs onto their customers. At the same time, they are preparing for the downside and are not growing inventories or hires aggressively and developing contingency plans if the downside scenario occurs."

"As I've said before, we are hopeful that the results of the current negotiations will make our clients more competitive and help drive stronger economic growth in the US. But there is uncertainty, and we should recognize there is risk to the downside, as the markets seem to have priced in successful outcomes."

From JB Hunt:

"While we continue to focus on operational excellence, driving productivity, and managing our costs, inflationary pressures, primarily in wages, insurance, both casualty and medical, and equipment costs, more than offset those efforts and weighed on margins vs the prior year period."

"During the quarter, overall customer demand trended modestly below normal seasonality. As customers adapted to changes in global trade policy, the timing and direction of freight flows were impacted. That said, demand for our intermodal service remained strong. We continue to see customers convert more freight to intermodal from the highway."

"In our brokerage and truck segments, demand followed more normal seasonal patterns, including some market tightness in May around the annual road check event, however, the market tightness was relatively short lived and truckload spot rates remained soft, suggesting the truckload market, while close to equilibrium, continues to experience some excess capacity."

And on tariffs, "I'll close with some comments on trade policy, demand and peak. When we meet with customers, how they are adapting to trade policy remains top of mind. However, accurately forecasting demand is their biggest challenge. Our customer base is diverse, both in terms of size and industry, and each customer continuously adjusts their supply chains to meet their unique needs. Recent examples are some customers have pulled freight forward, some continue to execute demand driven strategies, and others are making changes to their country of origin and manufacturing plans. This added complexity, lack of accurate forecasts, and potential for volatility is why our peak seasons surcharge programs are staring earlier this year."

From Albertsons who is directly touching the consumer:

"we continue to see the customers seeking value. We're selling more on promotion. That's been happening for quite some time now. We're leaning heavily into owned brands, understanding that."

"As I think about the customer, we were looking at some category information and it's been interesting, some of our top performing categories in the first quarter, it was kind of a tale of two cities. We absolutely saw increases in the shift into pork and ground beef as one example, again, indicating that the customer is looking for value. We also saw strong growth in our deli chicken business as an example, knowing that I think customers are always looking for quick and easy meal solutions. And with the increase of food away from home, I think inflation was almost 4%, we're absolutely providing value there."

From ASML:

"We continue to see increasing uncertainty driven by macro economic and geopolitical developments. Therefore, while we still prepare for growth in 2026, we cannot confirm it at this stage."

With tariffs, "Customers are watching that landscape but are currently faced with that uncertainty. As soon as that becomes clearer, then also their investment plans will become clearer."

I said last week to look past the weekly MBA mortgage application data because of the influence of the July 4th holiday. So, after a 9.4% rise for the week ended 7/4, they fell by 10% for the week ended 7/11. We'll thus look to next week for more normal, not holiday distorted data.

UK June CPI surprised to the upside with a headline gain of 3.6% y/o/y vs the estimate of 3.4% and up from 3.4% in May. The core rate also exceeded expectations by two tenths in a 3.7% rise y/o/y. A 4.4% jump in food prices was a factor for the headline and also higher payroll taxes and minimum wage increases flowed into higher consumer prices. Services inflation rose 4.7% y/o/y, the same pace seen in May.

Gilt yields are higher in response but the 10 yr inflation breakeven is unchanged. The pound is higher as is the FTSE 100. The UK economy has its challenges but there are many cheap stocks there.

BY Doug Kass · Jul 16, 2025, 8:55 AM EDT

* Of a downside-kind....

What do I mean by this and how did I come to the conclusion?

There is a lot to unpack:

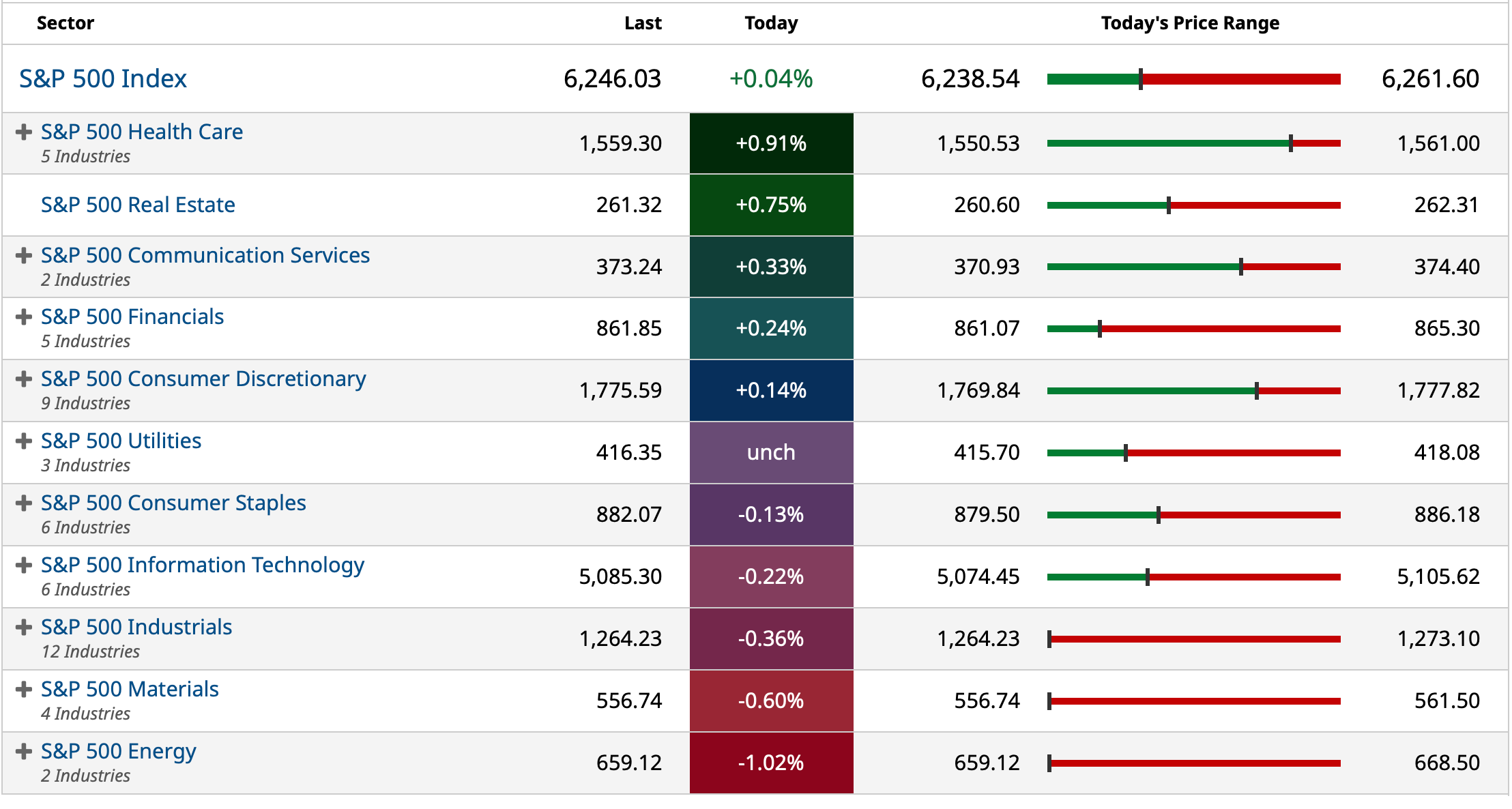

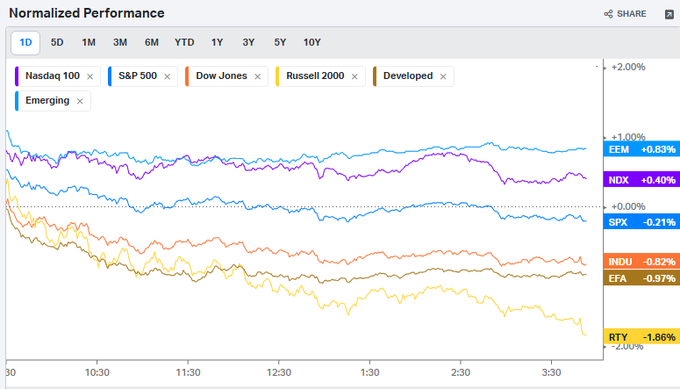

First, as chronicled in the late afternoon, the divergence between indices grew more obvious/extreme on Tuesday:

* SPY -0.49%

* QQQ +0.00%

* IWM -1.99% (memo to Tom Lee I am still waiting for the Russell to rally and to begin crowing!)

* RSP -1.39% (equal weighted S&P, which I have been shorting in recent days)

Second, the brief gap higher in the premarket was "newsy" — generated by the news that Nvidia NVDA "is hopeful" that it will be able to resume H20 AI chip sales to China "soon" and by non-eventful bank earnings reports, which as I noted during the previous day may have discounted the likely results (with the strong share price performance leading up to them).

The S&P index failed to break out on the NVDA news:

As I wrote and expected in my column (below) and in the chart above — at 8 AM, stock prices quickly faded and closed at the day's lows, indicating, for now, demand for stocks may have been sated:

My guess is that we get more or less in line bank industry results (and some profit taking in the stocks, which I sold down yesterday) as well as a consensus inflation print.

If so, I would also guess that (NVDA) will be treated as a one off and not serve as a tailwind for the average stock.

So, I wouldn't be surprised if the average equity (and the equal weighted S&P) shows little progress during the trading session.

Currently the S&P futures are +27 and I would attach a high possibility that this could be the day's high - but I have been wrong before!

Stay tuned.

By Doug Kass Jul 15, 2025 8:00 AM EDT

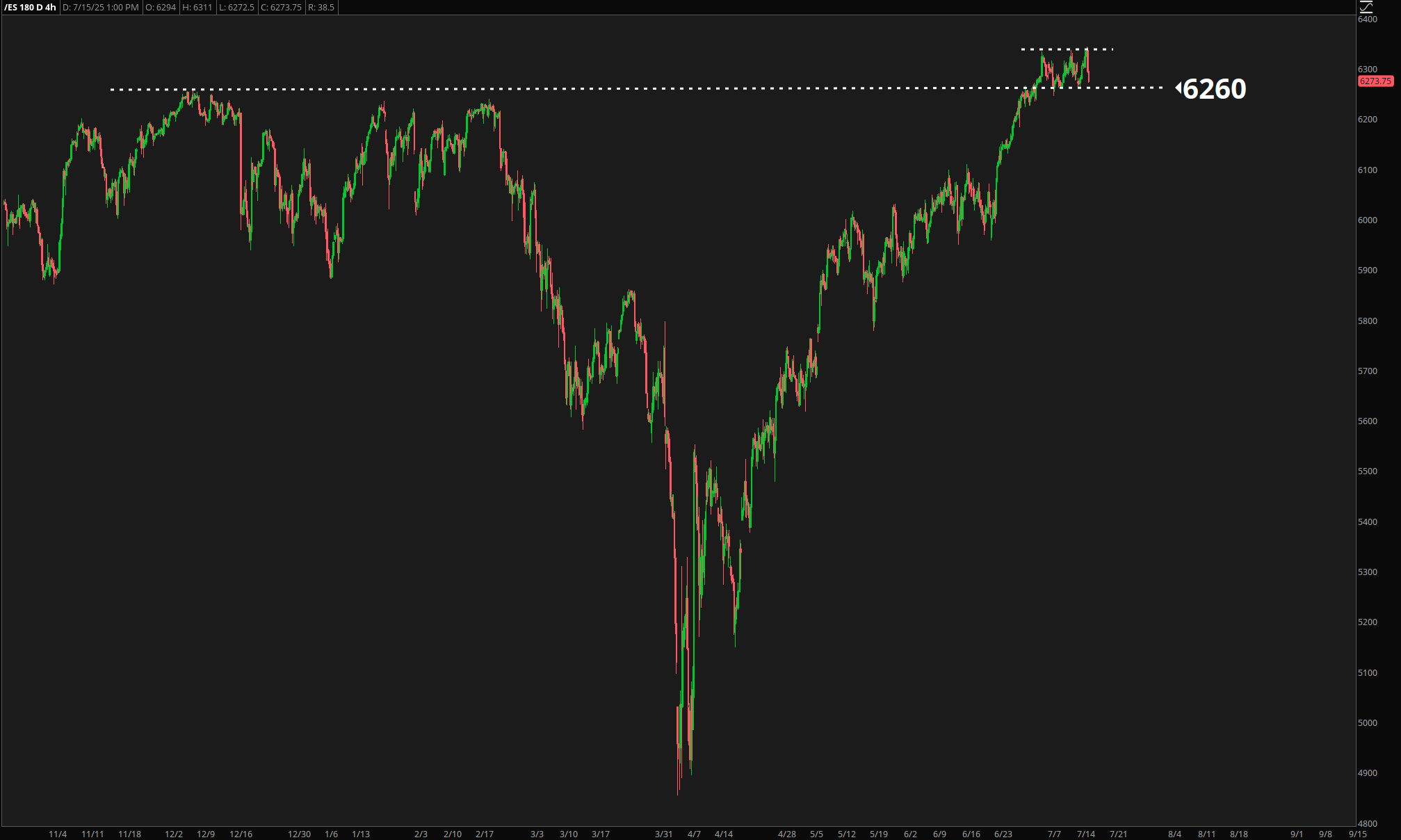

If S&P futures breach 6260 to the downside, we might have a failed breakout and bullish trap pattern:

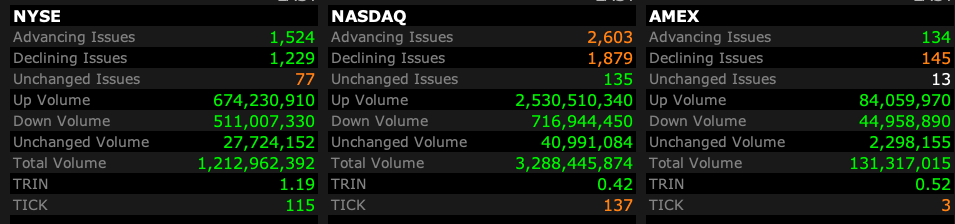

Third, market breadth stunk up the joint. Indeed there has never been a day with such good investment returns and such lousy breadth:

Looks like close to an engulfing bearish candle on the S&P index:

And, the Russell Wasn't Crowing — just look at the closing puke of the IWM chart:

Fourth, speculative assets dropped (e.g. bitcoin -3%). Importantly, high yield is starting to roll over:

By contrast, the U.S. dollar may be turning higher (negative for equities which have tended to move inversely to our currency):

Fifth, if you watch the "shows" over the last 48 hours, any discussion of a possible overvalued market was dismissed (out of hand). Hubris and complacency was shining through every appearance. There was never a mention of how 23x P/E multiple is a poor launching pad for another leg in the market's advance.

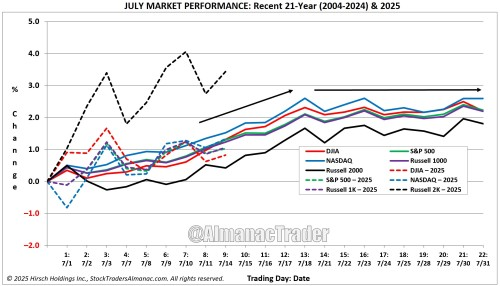

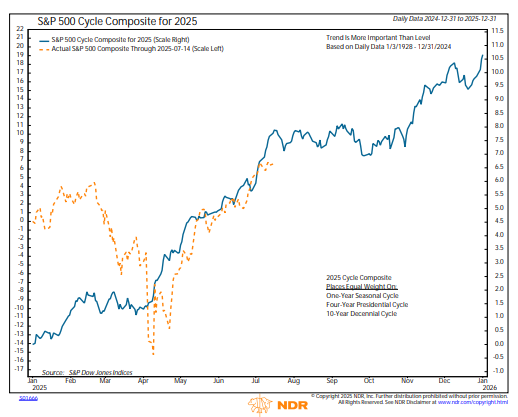

Sixth, as noted by both The Stock Almanac's Jeff Hirsch and Ned Davis Research, we are entering a seasonally weak period:

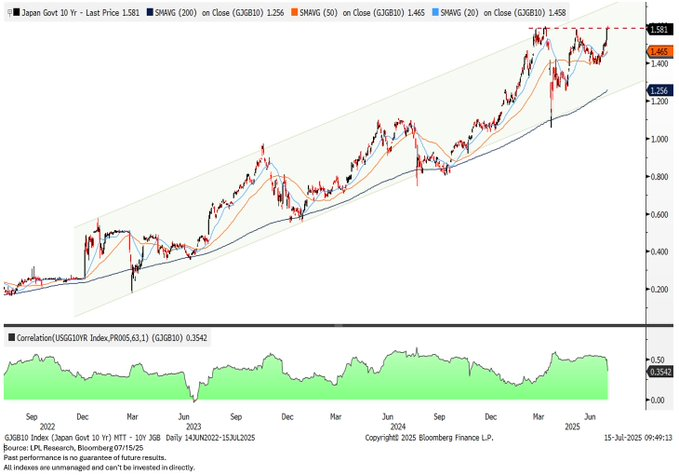

Seventh, global interest rates continued to rise on Tuesday:

BY Doug Kass · Jul 16, 2025, 8:15 AM EDT

Given my increasingly bearish market view (see my revised market outlook which will be up around 10 a.m.) - I am shorting a package of high beta/high octane market leaders.

As I don't feel most retail investors should engage in short selling - I won't be listing the names... but think AI, semis, etc.

Short A High Beta Package

BY Doug Kass · Jul 16, 2025, 8:09 AM EDT

BY Doug Kass · Jul 16, 2025, 7:30 AM EDT

* Yell and roar and sell some more...

I have followed banks for more decades than I would like to admit. (Like everyone I am fallible — I am often in doubt and I make many mistakes. But when at Putnam Managment in Boston, I was named the country's top buy-side bank analyst by Institutional Investor Magazine).

Nowhere on the "shows'" discussion of bank stocks this week was there an analysis of valuation (relative to tangible book).

Most panelists/guests felt (call it first-level thinking) that bank stocks were headed higher, likely primarily because they have been recently climbing and, secondarily, that, in all likelihood second-quarter EPS would be satisfactory relative to consensus expectations.

JPMorgan's JPM shares are now trading at over 3x tangible net worth.

JPMorgan's shares (and many other money center banks) have never traded in such a rare atmosphere.

Banking is a commodity (and certain sectors like investment management are increasingly being commodized), with, increasingly, large demands to spend for technology.

Currently, excess returns are being generated by the banking industry.

As economic challenges rise (housing and credit demands fall and loan losses rise), those excess returns will be threatened.

Two days ago, ahead of second-quarter bank earnings, I sold most of my bank and financial stocks.

JPMorgan's Jamie Dimon appears to agree with me — he has continually sold plenty of his stock holdings over the course of this year.

As for me, I am far more influenced by the JPMorgan chairman's actions than a bunch of panelists who superficially regurgitate the bank's earnings release — without much industry knowledge and whose body of analytical work on banks is generally miles long but only inches deep.

BY Doug Kass · Jul 16, 2025, 7:00 AM EDT

Remember, JPMorgan research wrote (prior to yesterday morning's inflation print) that equities would climb vigorously if the print was +0.23% or lower.

Instead, stocks fell. (The print was +0.23%. See the JPM explanation below - they remain bullish on equities):

Our scenario analysis was a large miss. Coming into the print, Inflation Traders were preparing for a dovish print, relative to expectations. Seemingly, that is what we received but we saw bond yields move high, stalling the Equity rally and hurting small-caps, especially consumer-related plays such as Homebuilders (XHB -3.5%), Retailers (XRT -2.2%), Autos (JP1BAUT Index -2.7%). Separately, Banks were hit despites a decent set of earnings, XLF -1.7% and KRE -3.5%. On Friday (July 11) rate cut probabilities were 63.4% for Sep, 58.6% for Oct, and 71.7% for December. Yesterday those probabilities fell to 55.0% for Sep, 51.0% for Oct, and 65.7% for Dec. Even before the reversal lower in stocks and higher in yields, Equities felt a touch stretched. My colleague Ilan Benhamou flags that the combination of NVDA news, bank earnings, and CPI that the SPX should have been up at least 1%, so we may be gearing up for a breather to this rally. WTD, the Momentum Factor has retraced about 40% of its recent losses so some of the aforementioned losses may be more tied to Momentum Shorts being re-shorted. Lastly, a client flags that the DXY / USD short has been one of the bigger macro consensus trades and that unwind may be leading all of the moves witnesses yesterday.

· DOES THIS CHANGE THE VIEW? No, we remain tactically bullish. While a critical mass of Equity investors were bulled up on the prospect of rate cuts, that is not part of our hypothesis. We think an environment where the US avoids a stagflationary outcome and growth stays around trend levels with inflation contained would keep the Fed on the sidelines, push investors into larger-cap names while avoiding higher beta / unprofitable Tech plays, would be the best outcome for the index.

From JPMorgan:

US: Futs are flattish with RTY seeing an early outperformance bid. Bond yields are flat as is the USD. Pre-mkt, Mag7/Semis are mixed as are Cyclicals with Banks seeing an offer into the next batch of earnings. Cmdtys are mostly higher with Ags leading, precious following and energy weaker. Today’s macro data focus is on PPI to update the PCE forecast. We have another batch of Fedspeakers.

and...

JPM MARKET INTEL EQUITY & MACRO NARRATIVE

Yesterday, NDX closed at a record, SPX was off a touch, and RTY was hit on the increase in bond yields. Both bank earnings and CPI seemingly gave the market what it wanted but we saw a material repricing of Fed expectations plus USD strength that created a headwind to Equities.

CPI POST-MORTEM

· ABIEL REINHART (Econ) – The core CPI rose 0.23%m/m in June, a bit below expectations (JPMC: 0.29%, consensus: 0.3%), and the over-year-ago rate accelerated from 2.8% to 2.9%, remaining somewhat above the Fed’s target in a way that should keep them on hold pending any significant break in the labor market. Our early forecast for the core PCE deflator is 0.28%m/m, which would leave the over-year-ago rate at 2.7% (close to rounding to 2.8%). Headline CPI inflation rose 0.29%m/m, in line with expectations. In the core details, core goods rose 0.20%m/m, the most since February, while core services increased 0.25%. On the goods side, new autos continued to slide despite the recent tariffs and firmer signals from industry pricing data, falling 0.3%m/m and down 2.5% saar over 3 months. Used vehicles also fell 0.7%, continuing to unwind some recent firmness. However, year-over-year core goods rose 0.7%, the most in about two years. Within services, lodging away from home fell a large 2.9%, another weak print for a travel related category, while airline fare was almost flat after four straight months of large declines. OER rose 0.3%, and 3.8% saar over 3 months, near the lower end for this cycle.

· MARK WHITWORTH (Rates) – Lots of question on the reversal this morning. We have seen some selling, mostly in the 10y part of the curve. Part of this move feels like a buy the rumor, sell the fact kind of price action.

· Meaning, I think markets have gotten over their skis. Mostly stocks. But also, in the front end of the UST curve- too much Fed priced in for the data received (labor market strong > inflation not showing much tariff impact YET - Godot?). If correct, then that means the curve has been steeper than it 'should' be (mostly b/c ONLY the front end has been too rich). The back end, in isolation, should have a tough time holding a bid with the fiscal/debt issues + inflation not going away + labor market tight and getting tighter with immigration.

· MARISSA GITLER (Futs/Options) – Taking together all the mkt moves from today.. Broadly… Takeaway from CPI is that tariff-related inflation actually does appear to exist. Combine that with at 4.1 UE, And it gives reason for the Fed to stay on hold. That translates to: gold down, yields up, inflation up, USD up. NQ >RTY. SPX flattish (potentially implies margins being protected).

· For all the talk on the fixed income move today, what's materializing in equities today is pretty interesting.. While the SPX move appears fairly contained.. R2K is getting smoked... And more telling equal weight SPX is underperforming… as >87% of S&P 500 is negative right now.

· Why? Because the odds of a July cut just went to 0. And sept odds have peeled back closer to 50/50 while just ~44bp are priced for the year. CPI today was enough to secure the Fed on hold, especially in the context of the 4.1% UE rate from this month's payroll report.

· Diving deeper into sector moves.. The banks move offers a good manifestation of what's plaguing the market.. Both regionals and diversified banks are selling off materially despite positive prints this morning.. While the results weren't bad.. The bar was just too high.

· US MKT INTEL (Right after the print) – his is a dovish print with Core CPI MoM coming in below expectations and earnings measuring printing below expectations. So, we are still in wait-and-see mode for when we see the inflation pass-through which may still be 1-2 months away. Per Steve Bruner, unrounded Core was 0.228% and unrounded Supercore was 0.212% with soft vehicle prices being the primary driver (no pun intended) but how long can that last with tariffs at these levels? On Vehicles, New Vehicles printed -0.3% vs. +0.3% estimated with things like apparel and medical care seeing hawkish prints. Overall, we like being long risk into month-end (longer if Trump rolls the Aug 1 deadline).

· Banks kicked off earnings this morning and general message is one of a resilient economy based on color from commercial banks, loan growth, and delinquency/charge-off data. Separately, Bessent’s interview with BBG TV some color discussion in the bullets below:

· The is no intent to fire Powell (contradicts Hassett’s comments over the weekend) but the expectation is for him to step down as a Governor once a new Fed chair takes over. The process to replace him has begun and that Bessent is involved but ultimately up to Trump. Also, said that the concept of a Shadow Chair would be confusing for markets. Comments designed to assuage any concerns for Rates folks.

· On NVDA, the H2O ban was a negotiating tactic. Our view is that China holds the upper hand in this trade war versus US given that China has diversified away from the US in terms of their exports, and they own virtually all rare earth production/refining, globally. Recall ~80% of US military hardware is dependent on China-originated rare earths. If this is the first step in thawing the US/China relationship then that is a positive. He said to NOT worry about the Aug 12 deadline with China and that he is meeting with his Chinese counterpart in the next few weeks.

· AMD is also expected to get a license to resume shipments of the MI308 chip to China. Should be a good day for Semis.

· On inflation, says the trend is most important and that currently inflation is not accelerating but that he had not yet (as of 7.20am) seen the CPI data. Further, says not to overemphasize one inflation print.

· CONCLUSION = BUY STOCKS. Our view has been (i) resilience economy + (ii) growing earnings – (iii) trade escalation = Bull Market. Today, we seemingly received boosts to all parts of that equation. We like a mix of Tech and Cyclicals and think it makes sense to take some shots with the higher-beta plays and/or those where positioning is relatively light such as ARKK, Retailers, Transports, and Homebuilders.

BY Doug Kass · Jul 16, 2025, 6:40 AM EDT

Doomberg on rare earths metals.

BY Doug Kass · Jul 16, 2025, 6:30 AM EDT

Bonus — Here are some great links:

Summer Rally May Have Room to Run, But Might Be Running Out of Gas

BY Doug Kass · Jul 16, 2025, 6:10 AM EDT

The S&P Short Range Oscillator moved to 2.82% vs. 4.85%, reducing the overbought condition.

BY Doug Kass · Jul 16, 2025, 5:58 AM EDT