Until Tomorrow

Tomorrow I will have a lot to say about today's "action" and I will update my Market Outlook.

Thanks for reading my Diary.

Enjoy the evening.

Be safe.

BY Doug Kass · Jul 15, 2025, 4:34 PM EDT

Tomorrow I will have a lot to say about today's "action" and I will update my Market Outlook.

Thanks for reading my Diary.

Enjoy the evening.

Be safe.

BY Doug Kass · Jul 15, 2025, 4:34 PM EDT

Wolf Street howls about the Fed's greatest nightmare — non tariffed inflation in services.

BY Doug Kass · Jul 15, 2025, 3:04 PM EDT

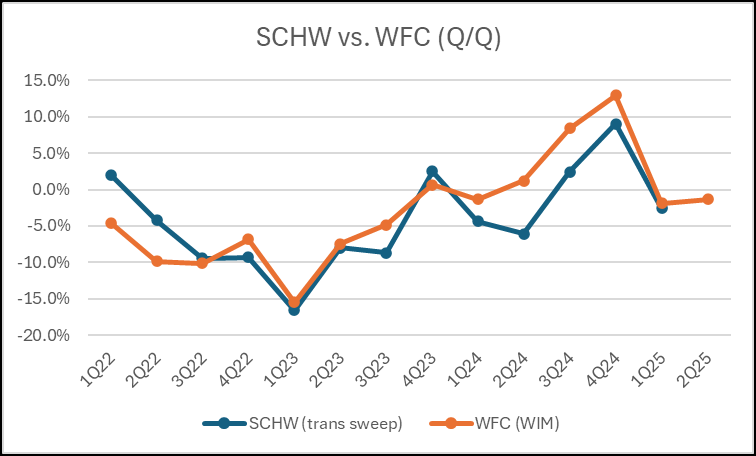

More on banks from Jefferies:

WFC down -5.3%

JPM only modestly outperforming

Citi +3% on a good print, strong call

BY Doug Kass · Jul 15, 2025, 3:00 PM EDT

Yesterday I did some serious selling of my long book... When I do such a broad exercise it is a reflection of my conviction level.

It does not necessarily mean I will be right!

* I eliminated my homebuiilders yesterday afternoon (the sector is broadly lower today, led by PHM -$5):

After posting strong stock price gains (from the lows) in the last two months I have liquidated all of my homebuilder longs this afternoon — (TOL) , (GRBK) , (KBH) and (PHM) .

Position: None

By Doug Kass Jul 14, 2025 3:50 PM EDT

* I eliminated my private equity stocks yesterday afternoon (the sector is broadly lower today, led by BX -$3):

For similar reasons (stock appreciation) as the homebuilders, I have exited all my private equity holdings ( (BX) , (KKR) and (APO) ).

Position: None

By Doug Kass Jul 14, 2025 3:55 PM EDT

* I moved to tagends in financials yesterday afternoon (the sector is broadly lower today, led by WFC -$5, GS -$12 and AXP -$8):

Ahead of this week's bank reports I have moved to tagends in these financial holdings - (C) , (BAC) , (WFC) , (GS) , (MS) , (JPM) and (AXP) .

Risk/reward has changed meaningfully since early April.

Position: Long C (VS), BAC (VS), WFC (VS), AXP (VS), GS (VS), MS (VS), JPM (VS)

By Doug Kass Jul 14, 2025 4:00 PM EDT

BY Doug Kass · Jul 15, 2025, 2:52 PM EDT

BY Doug Kass · Jul 15, 2025, 2:37 PM EDT

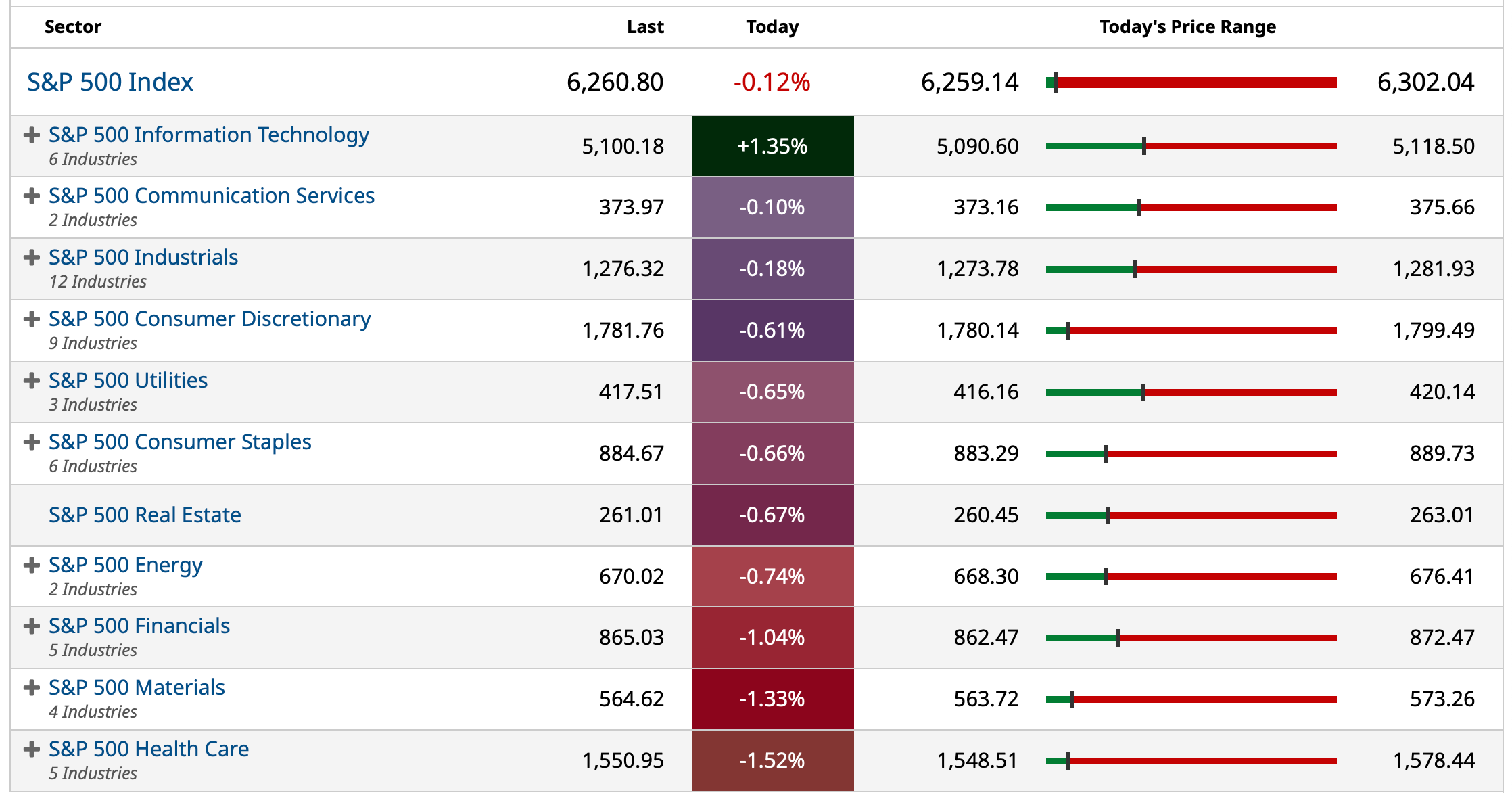

I have observed this divergence (experienced again, today) in recent days — but for now the market is unfazed:

* SPY -0.04%

* QQQ +0/60%

* IWM -1.20%

* RSP -1.03%

BY Doug Kass · Jul 15, 2025, 2:31 PM EDT

The trading session has basically performed in line with my expectations:

My guess is that we get more or less in line bank industry results (and some profit taking in the stocks, which I sold down yesterday) as well as a consensus inflation print.

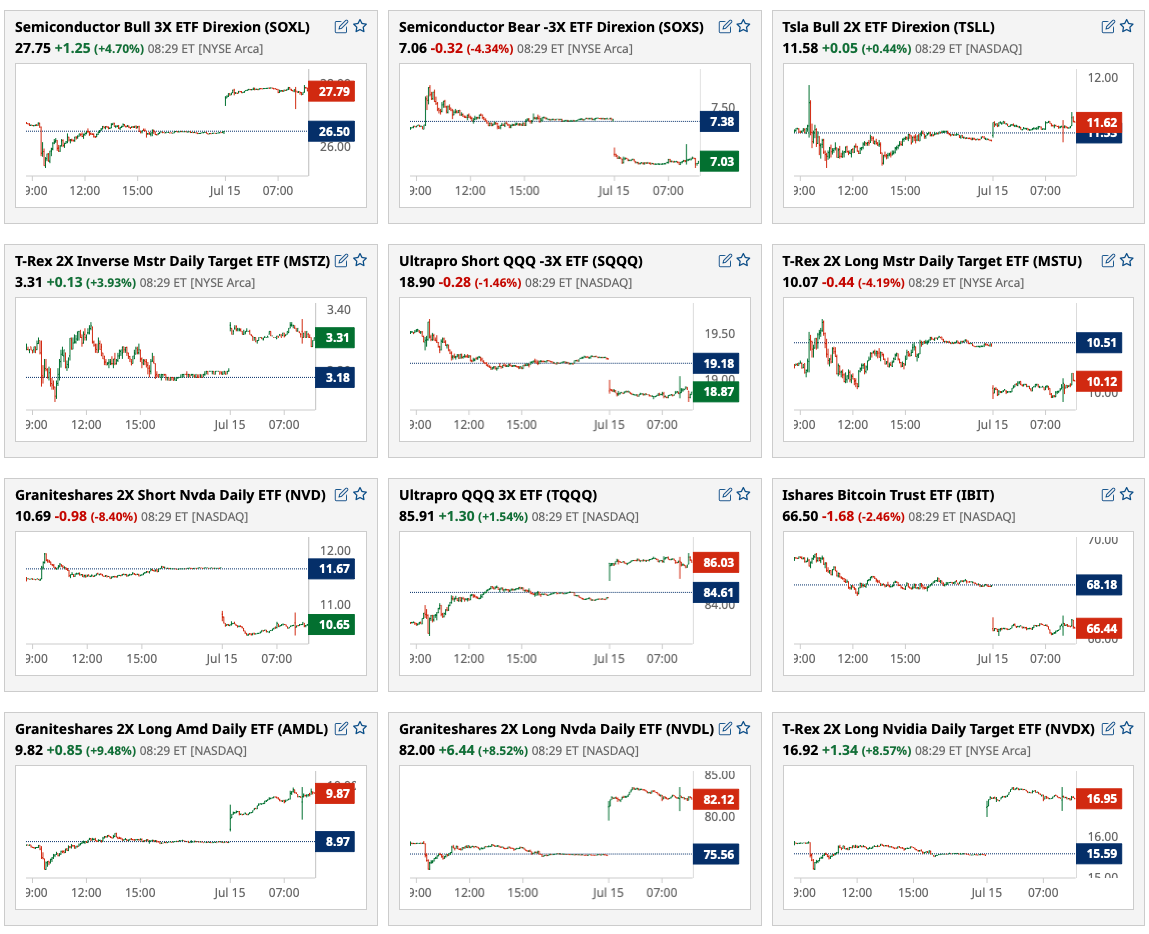

If so, I would also guess that (NVDA) will be treated as a one off and not serve as a tailwind for the average stock.

So, I wouldn't be surprised if the average equity (and the equal weighted S&P) shows little progress during the trading session.

Currently the S&P futures are +27 and I would attach a high possibility that this could be the day's high - but I have been wrong before!

Stay tuned.

By Doug Kass Jul 15, 2025 8:00 AM EDT

BY Doug Kass · Jul 15, 2025, 2:20 PM EDT

My annual physical will take longer than expected.

I should be back by 1:30.

BY Doug Kass · Jul 15, 2025, 12:00 PM EDT

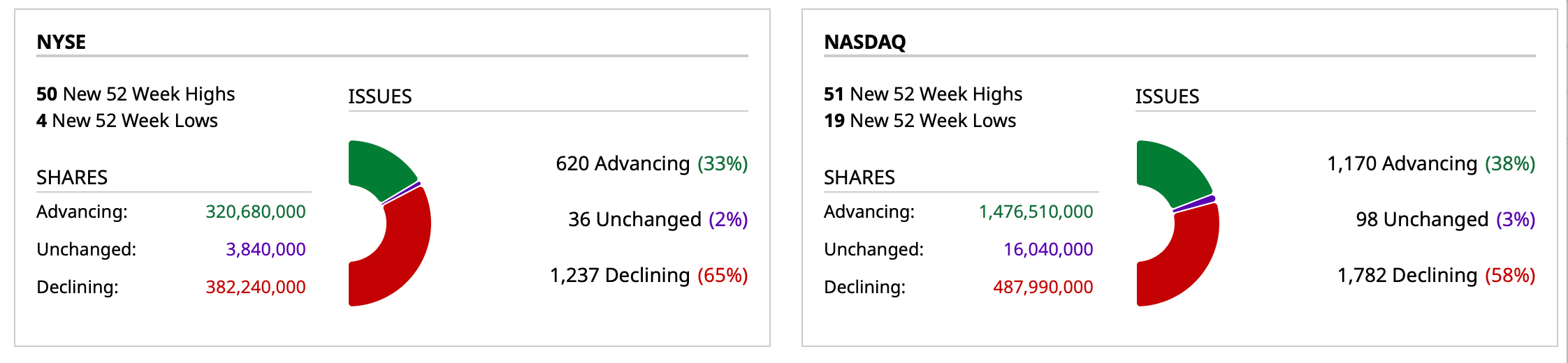

- NYSE volume 3% below its one-month average;

- NASDAQ volume 2% above its one-month average;

- VIX index: down 0.58% to 17.10

BY Doug Kass · Jul 15, 2025, 11:32 AM EDT

BY Doug Kass · Jul 15, 2025, 10:34 AM EDT

From Peter Boockvar:

Reflecting the ups and downs of orders in response to the on and off tariffs, the June Cass Freight Index was flattish from May with a .2% slight decline. They are though still down 2.4% y/o/y. Cass said "The trade war is having a variety of effects, with a few waves of pre-tariff inventory building and subsequent drawing down, but volumes were steady from May." They are expecting the 3rd year in a row of shipment declines in 2025 as the manufacturing recession continues on.

The bottom line from Cass, "Forward-looking visibility remains highly dependent on policy developments and legal challenges. The uncertainty has lowered the economic outlook, and pre-tariff inventory building will lead to destocking regardless of the outcome of trade negotiations in the coming months. The effects of tariffs may worsen, as higher goods prices reduce affordability and real incomes. With this outlook, the cycle upturn for the transportation industry remains elusive."

More on the manufacturing and industrial side of the US economy came from Fastenal yesterday in their earnings call:

"And when I think about the growth this quarter, market conditions, they haven't really helped us and remained sluggish."

"Trade policy continues to create some caution. Notwithstanding this uncertainty, we did not detect any meaningful pre-buying ahead of tariffs." They do think the market is showing signs of stabilizing.

"supply chains have gotten more expensive, and a part of our response over time will be incremental pricing...During the second quarter, we implemented three separate pricing actions, which aim to contribute 3% to 4% of price by the end of the second quarter of 2025. The phased approach to this rollout resulted in 140 bps to 170 bps of additional impact in the second quarter, with momentum building as we ended the quarter. Additional pricing actions will be necessary in the second half of 2025, with the potential to double the impact of pricing, depending upon where the deferred tariffs ultimately settle and the pace and execution of our actions." I bolded to highlight.

From Jamie Dimon in the JPM earnings release:

"Each of the lines of business performed well."

"The US economy remained resilient in the quarter. The finalization of tax reform and potential deregulation are positive for the economic outlook, however, significant risks persist - including from tariffs and trade uncertainty, worsening geopolitical conditions, high fiscal deficits and elevated asset prices. As always, we hope for the best but prepare the Firm for a wide range of scenarios." And that banker prudence mentality is why he's the best in that business, I'll add and why the stock trades at a very rich 2.8x tangible book value of $103.40.

From Charlie Scharf at Wells Fargo:

"While there continue to be risks as we look forward, activity levels have remained consistent and our strong credit performance continues to point to the strength of our commercial and consumer customers' financial position."

China's economy grew by 5.2% y/o/y in Q2, just above the estimate of 5.1% in the managed way they calculate this figure. Strength in industrial production offset a less than expected retail sales figure. The residential property market remained weak with home prices still falling. The Nvidia news last night helped to juice the Hang Seng for another 1.6% gain and taking its year to date performance to 22.6% after a solid year last year off multi year lows. When I heard a year and half ago from so many that China was uninvestable, that was all I needed to hear to want to invest.

The only thing of note in Europe was the German ZEW investor confidence index in their economy which rose to 52.7 in June from 47.5 and above the estimate of 50.4. The Current Situation component was still deeply negative but less so at -59.5 vs -72 and 6.5 pts better than expected. ZEW said, "After the strong improvements of the past two months, the positive sentiment among respondents is becoming more firmly established. Despite ongoing uncertainty due to global trade conflicts, nearly two-thirds of the experts expect the German economy to improve. Hopes for a quick resolution to the US-EU tariff dispute, along with potential economic stimulus from the German government's planned immediate investment program, appear to be shaping overall sentiment. The increased optimism is particularly reflected in significantly improved expectations for mechanical engineering and metal production, followed by the electrical industry."

This number is never market moving but the DAX is holding its year to date gain of 21.5% in euros and 37% in US dollars. Bund yields after the latest jump are slipping while the euro is a bit higher.

BY Doug Kass · Jul 15, 2025, 9:30 AM EDT

BY Doug Kass · Jul 15, 2025, 9:20 AM EDT

BY Doug Kass · Jul 15, 2025, 9:10 AM EDT

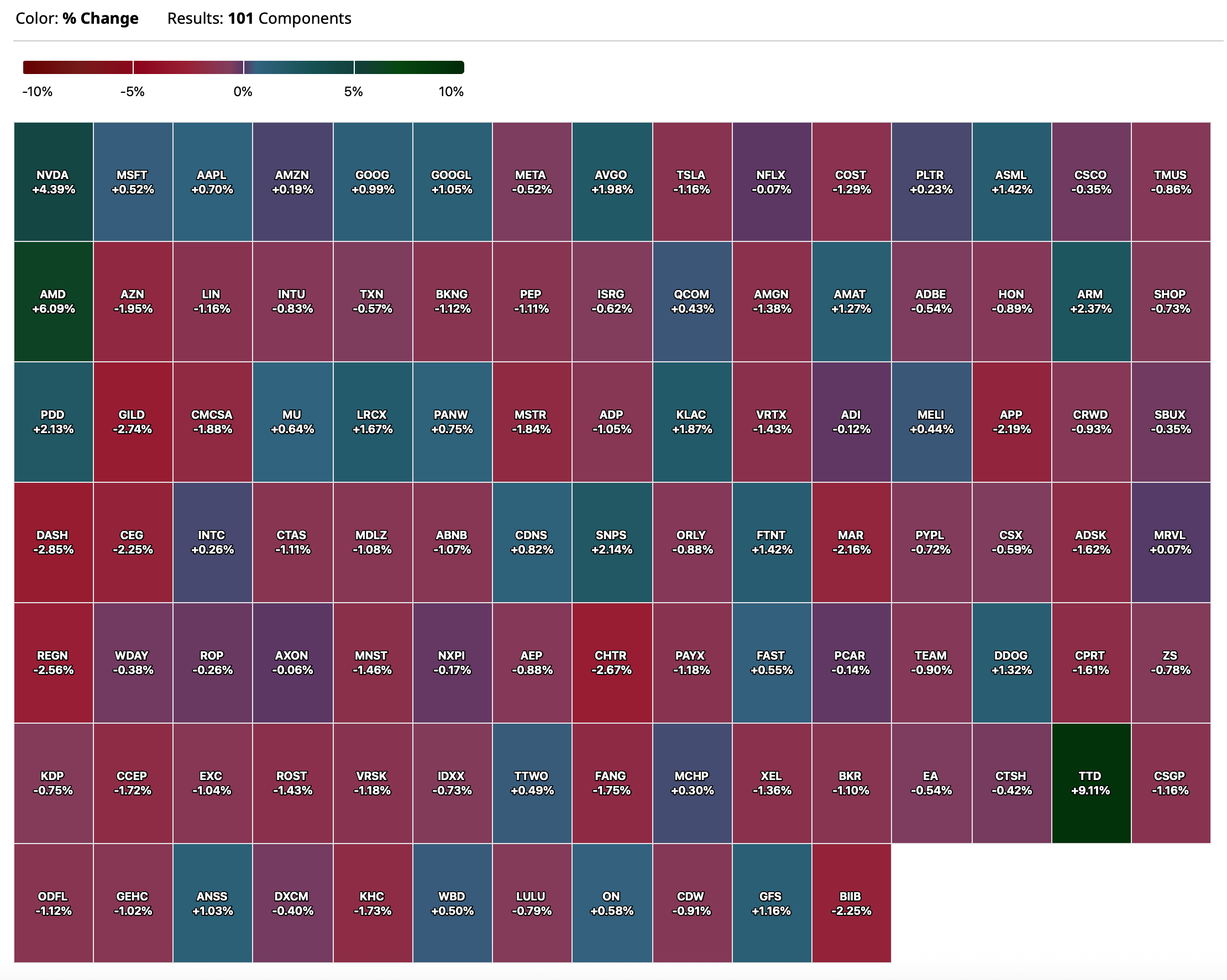

-ANGO +13% (earnings, guidance)

-TTD +13% (to replace ANSS in the S&P 500 Index)

-MP +10% (reportedly Apple to announce a $500M commitment to MP Materials)

-CRWV +7.1% (to commit up to $6B to equip a new, state-of-the-art data center in Lancaster, Pennsylvania, purpose-built to power the most cutting-edge AI use cases)

-JAMF +6.3% (raises guidance; announces strategic reinvestment plan including job cuts)

-AMD +4.9% (said to resume MI308 chip shipments to China once license cleared, as speculated)

-BIDU +4.7% (Baidu and Uber sign multi-year strategic partnership to deploy thousands of Baidu's Apollo Go autonomous vehicles (AVs) on the Uber platform across multiple global markets outside of the U.S. and mainland China)

-NVDA +4.4% (filing applications to sell the NVIDIA H20 GPU again and to resume H20 sales to China)

-WPP +4.0% (discussed potential merger with ACN)

-ETN +2.4% (accelerates the transformation of data center infrastructure with NVIDIA)

-ORGO -16% (CMS proposes cutting spending on skin substitute products by 90%)

-MYNZ -11% (H1 summary)

-WFC -3.3% (earnings, guidance)

-BLK -2.3% (earnings)

BY Doug Kass · Jul 15, 2025, 9:00 AM EDT

FED SPEAKERS

9:15 a.m.: Fed Vice Chair for Supervision Bowman (Voter) gives welcome remarks before the "Unleashing a Financially Inclusive Future" conference hosted by the Federal Reserve, Washington, DC (Webcast at federalreserve.gov. Other details TBA);

12:45 p.m.: Fed Board Governor Barr (Voter) speaks before the "Unleashing a Financially Inclusive Future" conference hosted by the Federal Reserve, Washington, DC (Webcast at federalreserve.gov. Text available. No Q&A);

1:00: Fed Bank of Richmond President Barkin (Non-Voter) speaks on "Forecasting Beyond Today's Data" before the Greater Baltimore Committee. Repeat of June 26th speech, Baltimore, MD (Audience Q&A expected. No separate media Q&A);

2:45: Fed Bank of Boston Collins (Voter) delivers the closing keynote at the NABE conference: A View from the Federal Reserve, Washington, DC (Embargoed text expected. Q&A from moderator. No media Q&A)

7:45: Fed Bank of Dallas Logan (Non-Voter) delivers remarks and discusses the Federal Reserve and the current economy in an event hosted by the World Affairs Council of San Antonio, San Antonio, TX (Text available. Audience Q&A expected. No media Q&A. Virtual stream available, link TBA)

TREASURY AUCTIONS:

11:00 a.m.: Treasury Announces a 4 and 8 Week Bill Auction;

11:30: Treasury hosts a $70B 6-Week Bill Auction

BY Doug Kass · Jul 15, 2025, 8:45 AM EDT

BY Doug Kass · Jul 15, 2025, 8:32 AM EDT

Amen:

BY Doug Kass · Jul 15, 2025, 8:30 AM EDT

From JPMorgan:

US: Futs are higher, led by Tech with the biggest news being that the US is allowing NVDA to resume its H2O chip sales to China; there had been chatter of a chips-for-rare earths pact to thaw US/China trade relations. NVDA is +5.3% pre-mkt, AMD +3.5%, MRVL +2.85, AVGO +1.4%. The balance of Mag7 is mostly higher, Semis are poised to be the best sub-group, and Cyclicals are higher with banks with a mild bid into earnings this morning. Bond yields are lower as the curve bull flattens into CPI with some FICC client convos pointing to a dovish CPI print. USD is weaker and cmdtys are declining across all 3 complexes though precious, crude, and sugar remain bid. Today’s focus is the unofficial kick off 25Q2 earnings and Banks have a low bar to cross and CPI is not yet expected to reflect the expected inflation from the trade war.

and.......

PM MARKET INTEL EQUITY & MACRO NARRATIVEMarket resilience continues and investors seem likely to look through any negative trade war updates until August 1 where the consensus view is that Trump either rolls that expiration date and/or reduces aggregate tariff levels back to the 10% experienced during the first 90-day delay. That said, some feel that the performance of the markets emboldens Trump to take a harder line such that another market swoon may be necessary to reduce average tariff levels, though few expect another ‘Liberation Day’ like move where the SPX fell more than 10% in two session and the 10Y yield increased by more than 40 bp. The NVDA news seems like a positive step but whether we see any additional de-escalation in the very near-term remains to be seen.

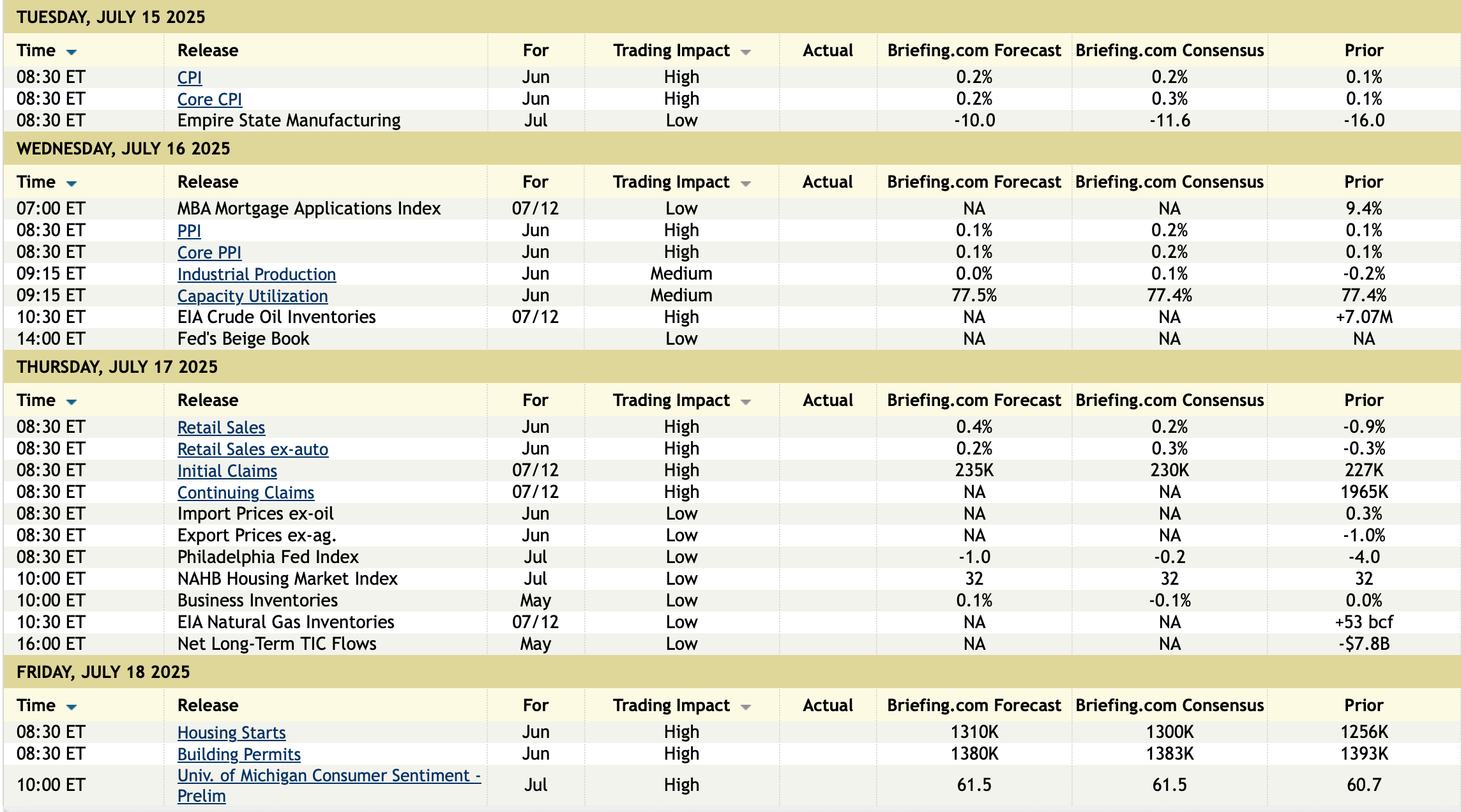

CPI SCENARIO ANALYSISFeroli’s CPI preview is here. For CPI he sees Headline MoM printing +0.28% and Core MoM printing +0.29%, both numbers are in line with the Street. This equates to 2.7% YoY for Headline (up from 2.4% last month) and 3.0% YoY for Core, the highest since Feb 2025. The following scenario analysis is NOT A PRODUCT OF JPM RESEARCH, this is a trading desk view from JPM US Market Intelligence. This month we focus on Core MoM outcomes and 1-days SPX moves. · [5.0%] Core MoM prints above 0.37%. SPX loses 1% - 2%· [25.0%] Core MoM prints between 0.32% - 0.37%. SPX loses 0.50% - 1.25%· [35.0%] Core MoM prints between 0.28% - 0.32%. SPX gains 0.25% - 0.75%· [30.0%] Core MoM prints between 0.23% - 0.28%. SPX gains 0.75% - 1.25%· [5.0%] Core MoM prints below 0.23%. SPX gains 1.5% - 2%· WHAT ARE OPTIONS PRICING? Options that expire on Tuesday are pricing ~85bp move based on Friday’s closing prices.·

US MARKET INTEL – The risk/reward of this print is skewed to the upside as the market await the potential worst of tariff-induced inflation. After the recession warnings of 2023 and 2024, the market is not giving prognosticators the benefit of the doubt with calls for an inflation spike. While we agree with our Economists that we are highly likely to experience a price spike, it seems that we are at least a month away from having a print whose magnitude may spook the market. Assuming this prints in line, the market refocused on August 1 trade deadlines, Aug 1 NFP, and then the Aug 12 CPI prints. Further, this print is unlikely to significantly shift Fed cut expectations. That said, the Fed’s Goolsbee mentioned that new tariffs have clouded the inflation outlook which likely means that any Fed action is delayed. Given how much of the presumed inflation spike is tied to tariffs, it is worthwhile to read Abiel Reinhart’s latest note on effective tariff rates where he finds that the effective tariff rate was 12.3% as Canada/Mexico effective rates surprised to the downside (full note is here).

BY Doug Kass · Jul 15, 2025, 8:25 AM EDT

BY Doug Kass · Jul 15, 2025, 8:10 AM EDT

Expanding Index shorts:

* SPY $627.34

* QQQ $559.87

BY Doug Kass · Jul 15, 2025, 8:09 AM EDT

My guess is that we get more or less in line bank industry results (and some profit taking in the stocks, which I sold down yesterday) as well as a consensus inflation print.

If so, I would also guess that NVDA will be treated as a one off and not serve as a tailwind for the average stock.

So, I wouldn't be surprised if the average equity (and the equal weighted S&P) shows little progress during the trading session.

Currently the S&P futures are +27 and I would attach a high possibility that this could be the day's high - but I have been wrong before!

Stay tuned.

BY Doug Kass · Jul 15, 2025, 8:00 AM EDT

BY Doug Kass · Jul 15, 2025, 7:56 AM EDT

Jeffries on JPM and WFC results (I am down to tagends longs after yesterday's sales):

JPM results are awesome

NET – Balance sheet growth awesome, RWA leverage notable – for the win. $25 FY27 is too low WFC results open for debate

NET – results fine but I don’t know that we have any answers here. Core vs Markets NII disclosure is pulled/and used as the explanation….BS is fine. Capital/RWA leverage = TBD… Are FY26 NII est at risk? --- see below. Combined with the lack of post AC RWA leverage……I would argue yes, maybe…

BY Doug Kass · Jul 15, 2025, 7:51 AM EDT

“Embedded in today’s relative strength

are tomorrow’s narratives.”

- Jeff deGraaf

Bonus - here are some great charts:

A View From The Floor Freedom Capital Markets Weekly Market Letter - July 13th, 2025

Risk-On Not Tiptoeing — It’s Charging 🚀

Episode 260: Mid-Summer Cooling?

Why the Stock Market Goes Higher in the Second Half | TCAF 199

BY Doug Kass · Jul 15, 2025, 6:44 AM EDT

More climbing unsold housing inventory from Wolf Street.

BY Doug Kass · Jul 15, 2025, 6:20 AM EDT

Here was the big market moving news last night:

Nvidia says it hopes to resume H20 AI chip sales to China 'soon'

BY Doug Kass · Jul 15, 2025, 6:10 AM EDT

The S&P Short Range Oscillator sits at an overbought at 4.75% vs. 4.99%

Long SPY puts VS QQQ puts VS

Short SPY common M calls S QQQ common M calls S

BY Doug Kass · Jul 15, 2025, 5:55 AM EDT

I have a routine MD appointment (annual physical) at 10 AM this morning.

BY Doug Kass · Jul 15, 2025, 5:45 AM EDT