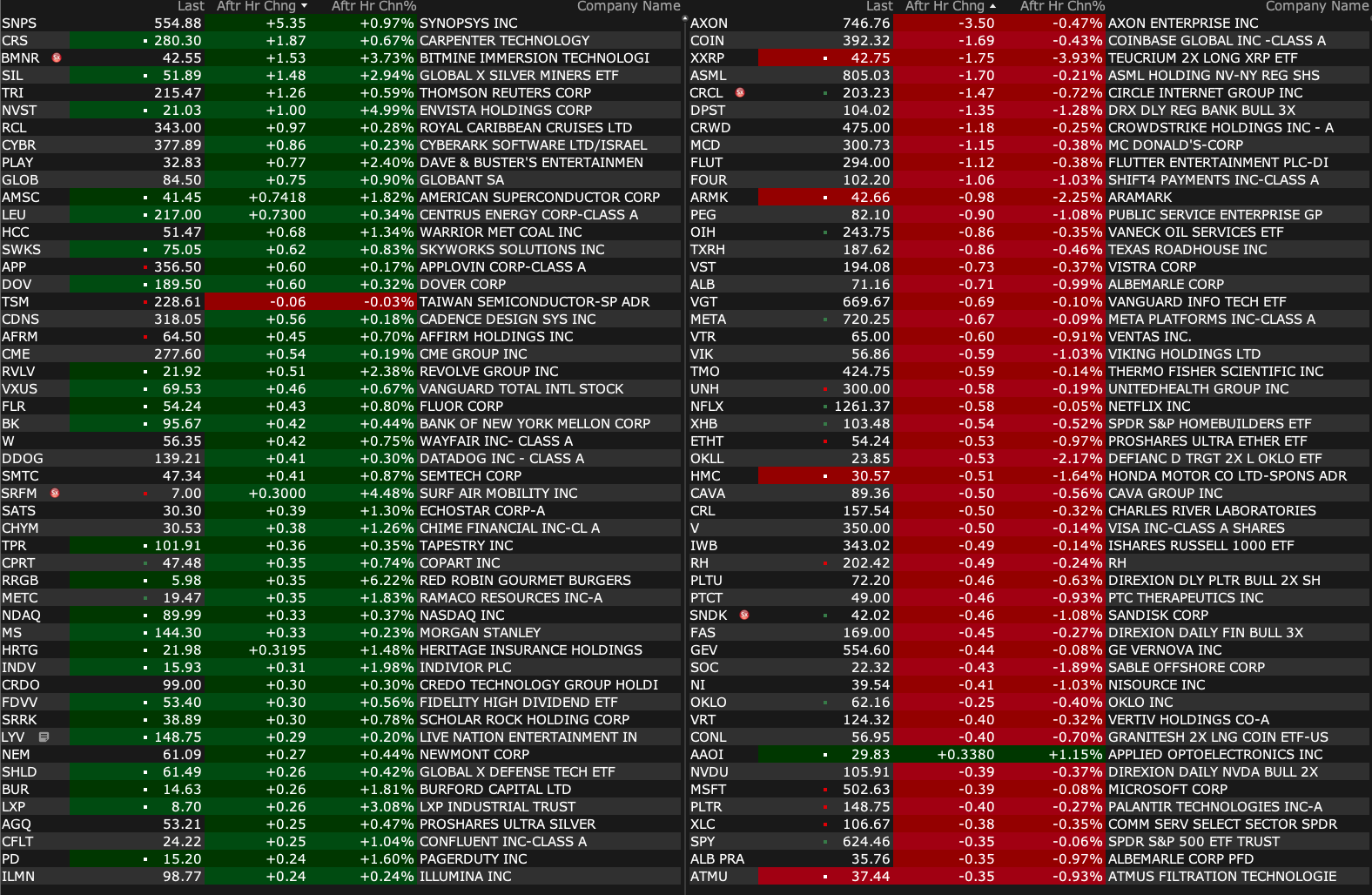

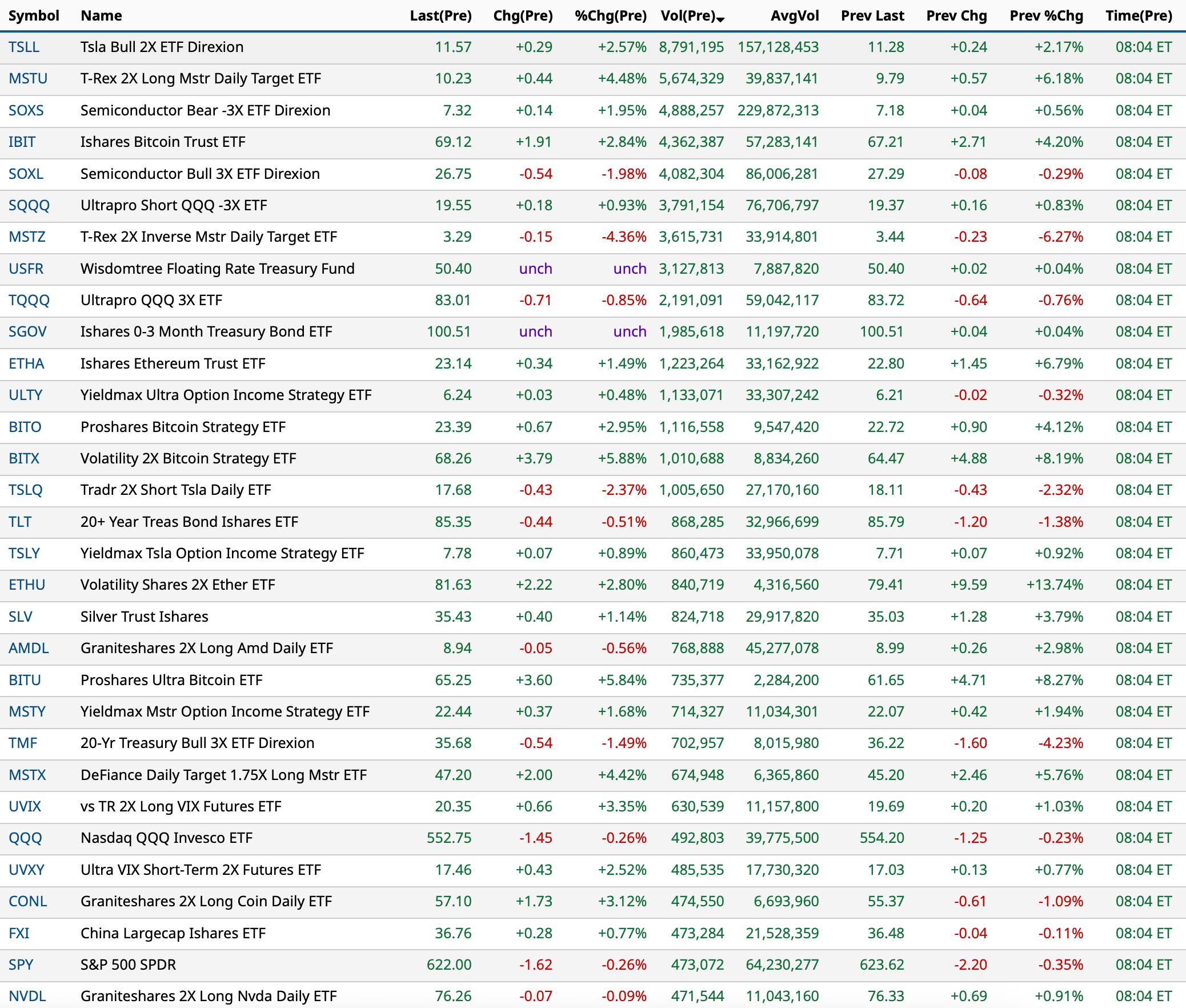

Monday's After-Hours Movers

At 4:18 p.m.:

BY Doug Kass · Jul 14, 2025, 4:45 PM EDT

At 4:18 p.m.:

BY Doug Kass · Jul 14, 2025, 4:45 PM EDT

BY Doug Kass · Jul 14, 2025, 4:32 PM EDT

Ahead of this week's bank reports I have moved to tagends in these financial holdings - C, BAC, WFC, GS, MS, JPM and AXP.

Risk/reward has changed meaningfully since early April.

BY Doug Kass · Jul 14, 2025, 4:00 PM EDT

For similar reasons (stock appreciation) as the homebuilders, I have exited all my private equity holdings (BX, KKR and APO).

BY Doug Kass · Jul 14, 2025, 3:55 PM EDT

After posting strong stock price gains (from the lows) in the last two months I have liquidated all of my homebuilder longs this afternoon — TOL, GRBK, KBH and PHM.

BY Doug Kass · Jul 14, 2025, 3:50 PM EDT

sbickleyinreno

Just parsed a 50 page study where these crossing assistants were out to a realistic test with decent size code bases of moderate complexity. Guess what? They increased development time by 19%, not a reduction at all. That got me thinking so I used ChatGPT Pro to parse the study and compare it to other studies that tout productivity gains. What the AI found is most of the marketing hype based studies were either over simplified use cases or projects of very low complexity. This acquisition-hire is another page in the AI crash chronicles awaiting to be played out.

I also take issue with the aqui-hire workaround to antitrust scrutiny but that is a missive for another day!

BY Doug Kass · Jul 14, 2025, 3:46 PM EDT

No trades since the opening.

Today and tomorrow are research-driven.

BY Doug Kass · Jul 14, 2025, 2:56 PM EDT

BY Doug Kass · Jul 14, 2025, 1:56 PM EDT

I have several research calls which will take up a lot of my day.

That said, here are today's "things:"

* I added to my index shorts: SPY $623.14 and QQQ $554.34

* I day traded (on the short side and then covering) bitcoin: BITB (Buy $65.44/Sell $66.66), IBIT (Buy $68.38/Sell $69.62), BITO Buy ($23.13/Sell $23.56)

* I added to my large GRNY short at $23.74.

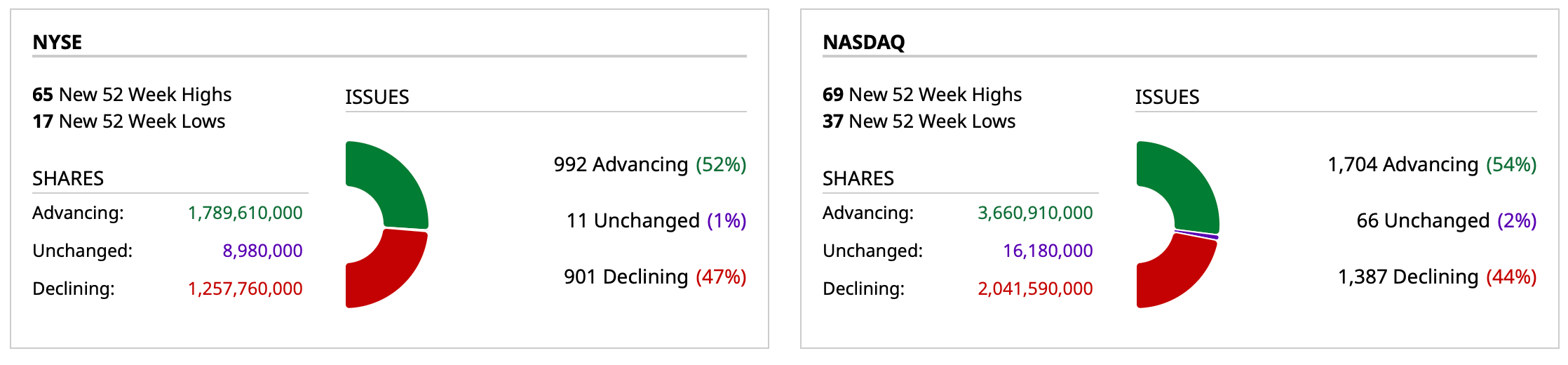

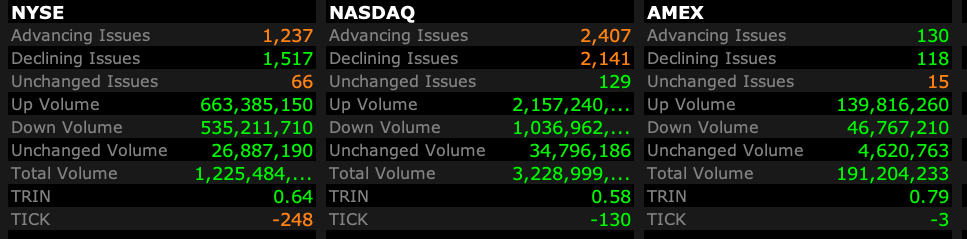

BY Doug Kass · Jul 14, 2025, 12:25 PM EDT

- NYSE volume 7% below its one-month average;

- Nasdaq volume 9% below its one-month average;

- VIX index: up 5.18% to 17.25

BY Doug Kass · Jul 14, 2025, 11:05 AM EDT

Right after the opening I added to my index shorts

* SPY $623.24

* QQQ $554.26

Long SPY puts VS QQQ puts VS; Short SPY common M calls S QQQ common M calls S

BY Doug Kass · Jul 14, 2025, 9:38 AM EDT

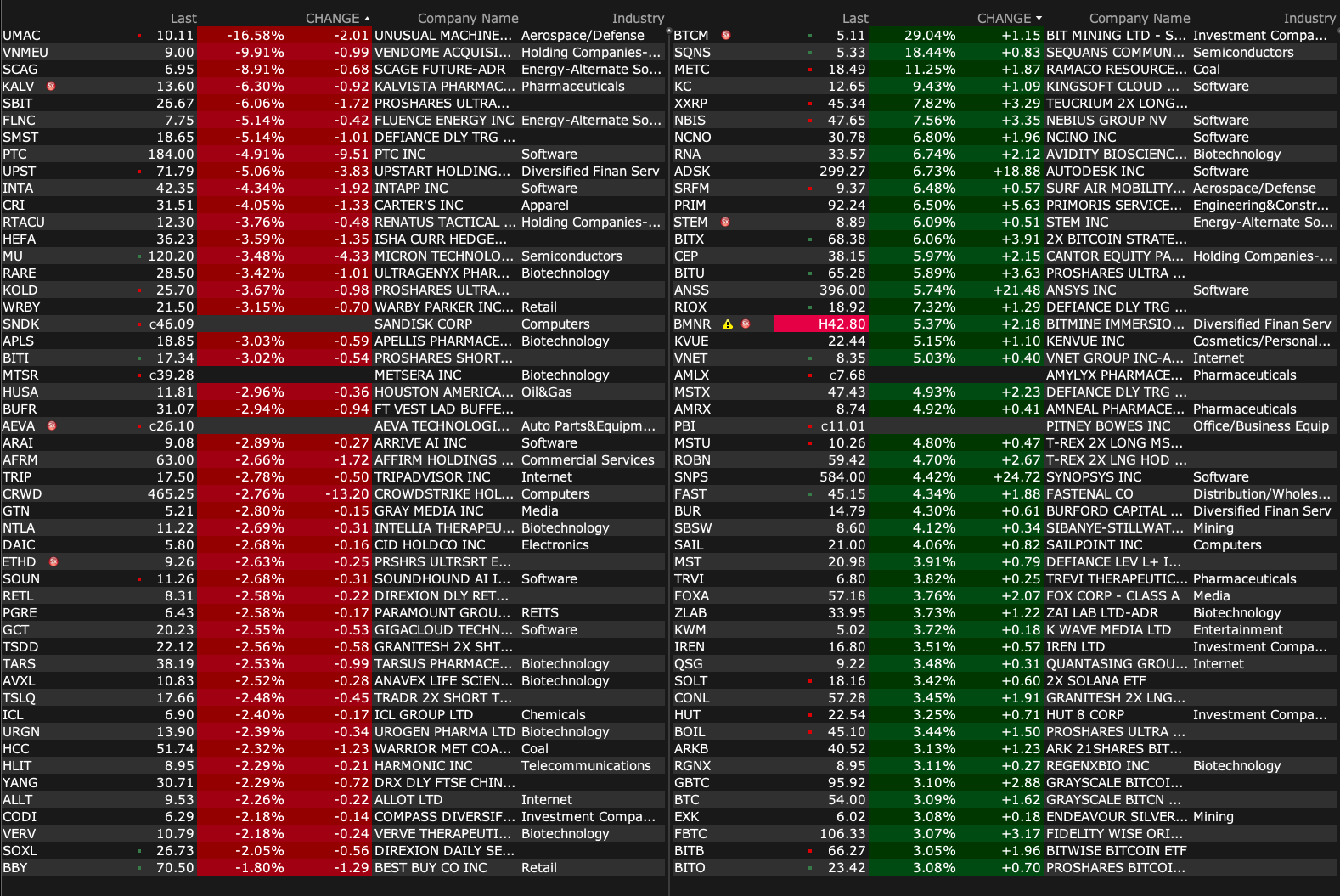

-DARE +195% (positive interim Phase 3 Results Highlight Potential of Ovaprene, Novel Hormone-Free ContraceptiveInterim Phase 3 Results Support Ovaprene’s Differentiation as a First-in-Category, Hormone-Free, Intravaginal Monthly Contraceptive)

-SONN +165% (announces $888M Business Combination to Launch a HYPE Cryptocurrency Treasury Reserve Strategy; to raise $5.5M in private placement of non-voting convertible preferred stock and warrants)

-MGRM +63% (to be acquired by Zimmer at $4.04/shr in cash in $177M deal)

-LION +12% (Apollo-backed Legendary Entertainment said to consider bid for Lionsgate Studios)

-DVLT +11% (IBM enters cloud services subscription agreements)

-JG +11% (BTC strength)

-SFIX +9.1% (hearing William Blair Raised SFIX to Outperform from Market Perform)

-AXL +8.0% (UBS Raised AXL to Buy from Neutral, price target: $7)

-NBIS +7.6% (Goldman Sachs Initiates NBIS with Buy, price target: $68)

-ADSK +6.6% (Autodesk said to drop pursuit of PTC)

-BMNR +5.3% (now holding ~$500M of ethereum to advance its ethereum treasury strategy)

-FAST +4.9% (earnings, guidance)

-SNPS +4.3% (China conditionally approves Synopsys-Ansys deal)

-KVUE +4.2% (reports prelim Q2; names new Interim CEO)

-IMAX +4.0% ($30.4M Global Opening for “Superman”)

-PAY +3.7% (Raymond James Raised PAY to Outperform from Market Perform, price target: $37)

-SEDG +2.7% (Barclays Raised SEDG to Equal Weight from Underweight, price target: $29)

-VC +2.1% (UBS Raised VC to Buy from Neutral, price target: $142)

-INKT -31% (hearing William Blair Cuts INKT to Market Perform from Outperform)

-WAT -9.5% (Waters and Becton Dickinson's Biosciences & Diagnostic Solutions Business to Combine)

-FLNC -5.1% (Mizuho Securities Cuts FLNC to Neutral from Outperform, price target: $10)

-PTC -4.7% (Autodesk said to drop pursuit of PTC)

-INTA -4.3% (Barclays Cuts INTA to Underweight from Equal Weight, price target: $44 from $60)

-PRGO -4.1% (divests dermacosmetics business for up to €327M)

-RARE -3.9% (receives Complete Response Letter from FDA for UX111 AAV Gene Therapy to Treat Sanfilippo Syndrome Type A (MPS IIIA); Plans to resubmit BLA)

-MU -3.3% (broker comments regarding potential sub-seasonal 2H)

-TTGT -2.8% (earnings)

-CRWD -2.7% (Morgan Stanley Cuts CRWD to Equal Weight from Overweight, price target: $495)

-AFRM -2.4% (JPM said to tell fintechs that they will have to pay for customer data; BTIG Cuts AFRM to Neutral from Buy)

BY Doug Kass · Jul 14, 2025, 9:26 AM EDT

From Peter Boockvar:

Yes, again it is most likely that earnings should be beat expectations about 75% of the time. That should not be considered as good but as baseline. As seen with Conagra and Helen of Troy last week, those impacted by tariffs will be differentiated by those who have pricing power and those who don't. Tariffs are not magically disappearing if they don't show up in consumer prices but somewhere along the supply chain someone is getting clipped. And, with the weakness in the US dollar, it's most likely that the US is eating it all because any price cuts on the part of exporters to us are being offset by the notable FX move against US importers we've seen this year.

I know much of the inflation focus this week will be on CPI and PPI but I'll call out import prices on Thursday as possibly most important as it's the first touch to tariffs. To those who say it hasn't shown up in the data, core import prices in April rose .5% m/o/m and by another .4% in May.

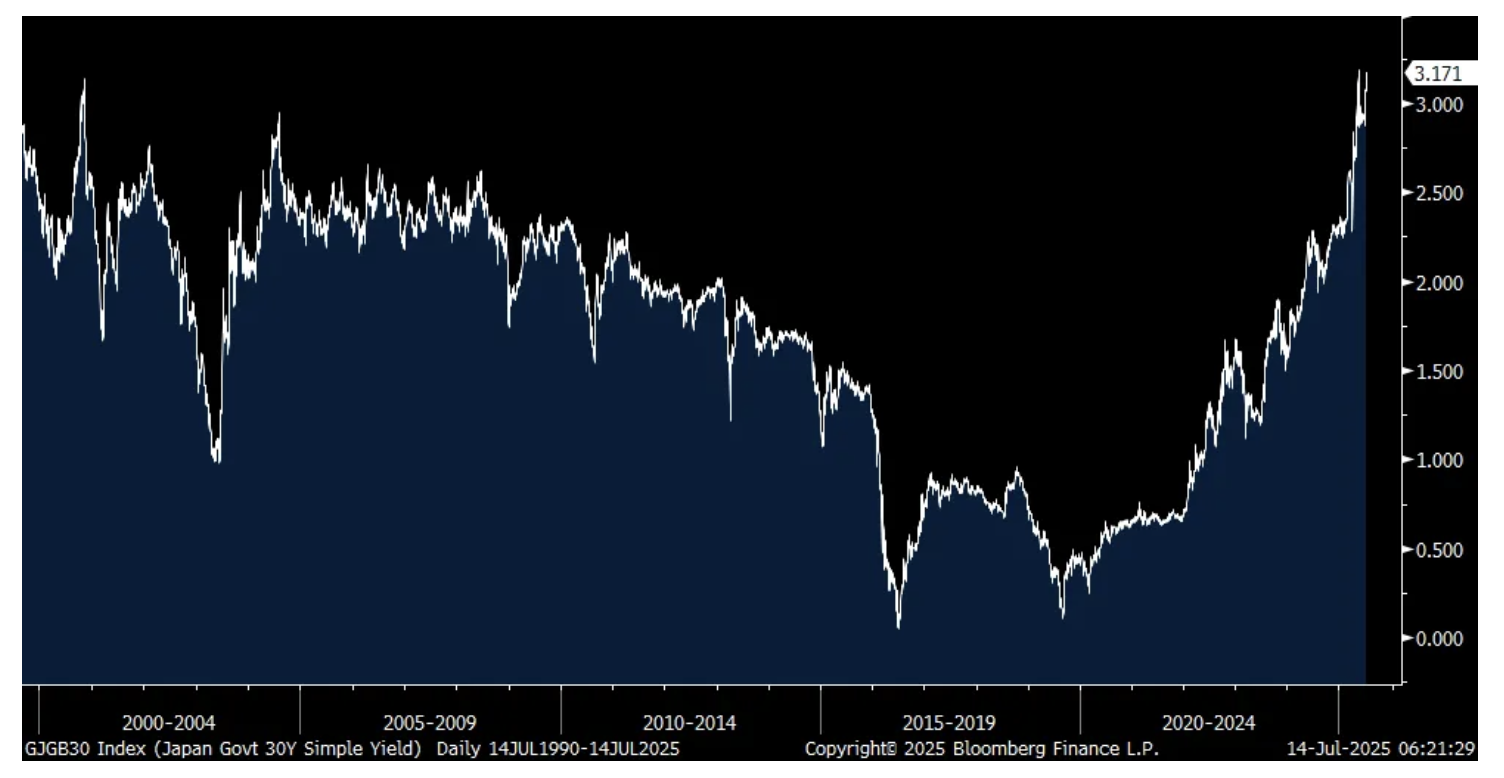

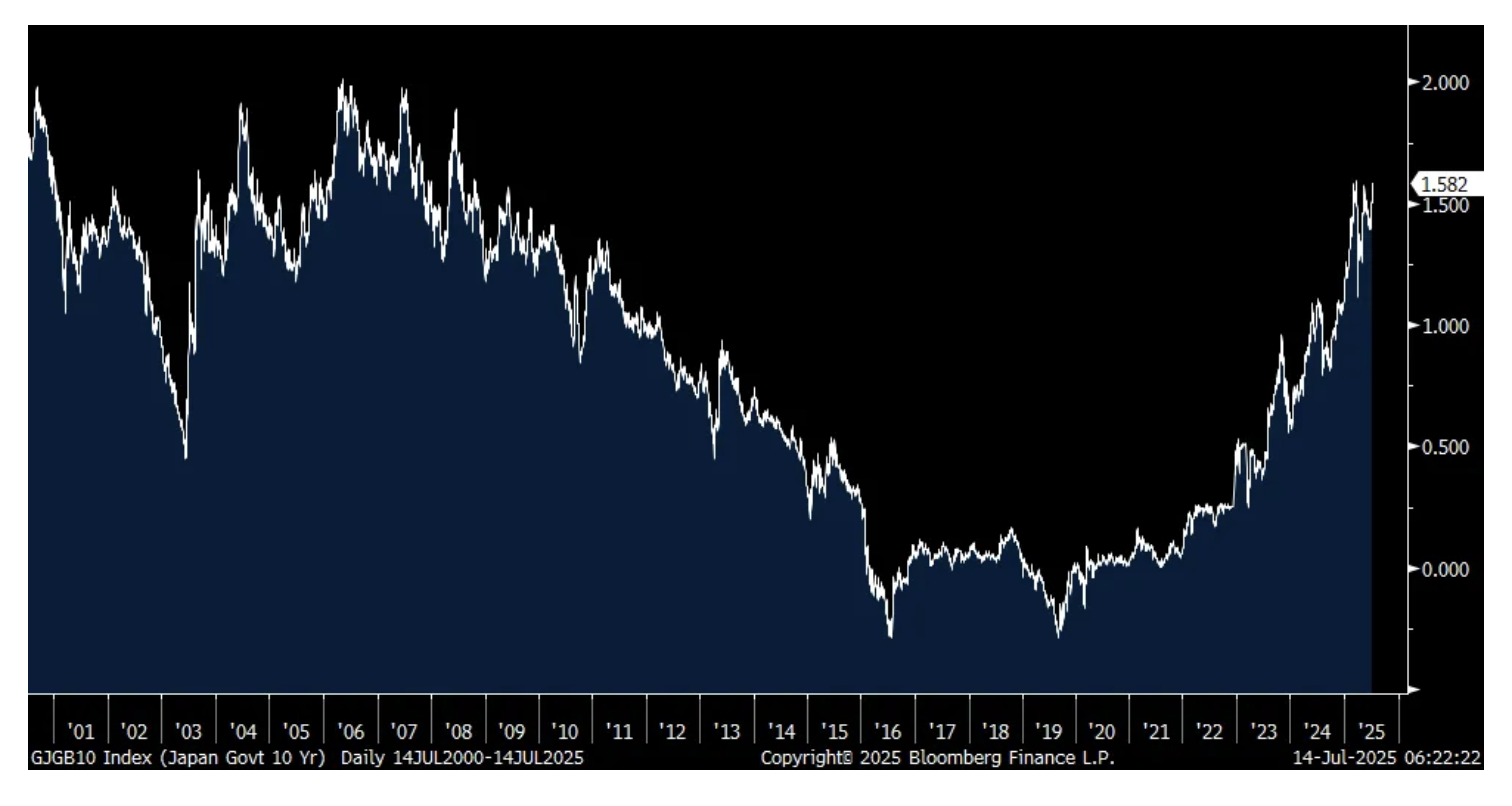

With a continued focus on long term interest rates globally, they jumped again in Japan with their 40 yr yield higher by 8 bps to 3.44%, the highest since late May. The 30 yr yield, up by 11 bps to 3.17% is just one bp from matching the highest level since 1999 when this maturity was first issued. Go back to 2008 was the last time the 10 yr JGB yield was this high at 1.58%, up 6 bps overnight. In 6 days in Japan they have an upper house election and that is creating the angst today as fiscal issues are front and center.

Fiscal disorder is the focus of bond duration buyers and they want no part of it. The US 30 yr yield is at 4.96-.97% and we of course watch that 5% level again. European yields though are little changed today.

30 yr JGB Yield

10 yr JGB Yield

I'll argue again that oil prices are cheap and going higher and are moving up today to just below $70 for WTI. It's becoming clear that the market is tight even with continued OPEC quota increases or at least it seems that all the quota changes were just going back to where oil production already stands. Also, the US oil rig count fell for an 11th straight week, down by 1 rig and by 51 in this time frame to 424, the least since September 2021.

Oil Rig Count

The German chemical behemoth BASF lowered guidance on Friday and said "Due to ongoing macroeconomic and geopolitical uncertainties, BASF is adjusting its assumptions for the full year 2025. The global gross domestic product is projected to grow less in 2025 than previously assumed. This development is essentially attributable to the US tariffs announced in early April and the resulting uncertainties in the market. Against this background, the US dollar has depreciated significantly against the euro. The growth of global industrial production is also expected to slow down. As a result, in 2025, market demand for chemical products will likely grow less than previously expected. Due to continued high product availability on the market, margins continue to remain under pressure, especially upstream."

Fastenal slightly beat earnings and revenue estimates and said the 8.6% top line growth "largely reflects the contribution from improved customer contract signings over the past six quarters. Market conditions remained sluggish, providing minimal contribution." Also, "Changes in foreign exchange rates positively affected sales in the 2nd quarter of 2025 by approximately 10 bps."

"Our manufacturing end markets outperformed primarily due to the relative strength we are experiencing with key account customers with significant managed spend where our service model and technology are particularly impactful. This disproportionately benefits manufacturing customers."

Also, "The non-residential construction end market experienced growth for the first time in ten consecutive quarters. Other end markets were favorably impacted by growth with warehousing and storage, and data center customers, which were partially offset by declining sales with resellers."

The China trade data for June was a bit above expectations with exports up 5.8% y/o/y vs the estimate of up 5%. Imports, many of which end up in eventual exports, grew by 1.1% y/o/y vs the forecast of up .3%. This data is beginning to reflect the post product procurement rush but still weighed down by remaining high tariff rates with the US. Exports to the US specifically dropped 16% after plunging by 34% in May. Exports in contrast were up by 17% to Southeast Asia. China continues to try to find new customers, and/or expanded ones.

BY Doug Kass · Jul 14, 2025, 9:00 AM EDT

BY Doug Kass · Jul 14, 2025, 8:45 AM EDT

BY Doug Kass · Jul 14, 2025, 8:30 AM EDT

Bonus - here are some great links:

Stock Market and Crypto Analysis

Expect Summer Rally to 6500s and Then A Shallow Correction

Option Expriration Week - Typically Strong (Jazzy Jeff Hirsch)

BY Doug Kass · Jul 14, 2025, 6:45 AM EDT

From JPMorgan:

US MKT INTEL – Reiterate our Tactical Bullish call. Thoughts on macro data, trade, near-term risks, geopolitics.

and...

US: Futs are lower on elevated tariff levels on announcements Friday/Saturday, though futures have cut their overnight losses roughly in half. Yield curve is seeing a slight bear steepening as USD is flat. Pre-mkt, Mag7 names are mostly lower with NVDA/TSLA in the green. Semis are under pressure and Cyclicals are mixed, as are Defensives pointing to a choppy session. Cmdtys are stronger across all 3 complexes with crude, natgas, and silver the standouts. Macro data kicks off tmrw with CPI plus the unofficial start to earnings season with Banks.

and...

JPM MARKET INTEL EQUITY & MACRO NARRATIVE

Last week, the SPX was down 31bp with NDX trading inline and RTY falling 63bp. Trump added volatility via tariff updates and the Momentum Unwind created some below the index-level turmoil. This week, markets receive CPI and Retail Sales on the macro side and 25Q2 earnings season kicks off with Banks. Further, will the market continue to look through elevated tariff levels believing Trump will pivot to lower levels or any near-term downside is bought going into the Aug 1 deadline? We think Yes and thus maintain our Tactical Bullish view as the market focuses on earnings. To complete this section, we walk through some topics that are affecting our investment hypothesis. The TL; DR is that we are bullish but see risks building with the most acute being inflation, it impacts on bond yields/stocks, and economic growth; the genesis of our concern stems from the trade war and ancillary government policies. With single stock shorts losing their efficacy, you may consider custom and/or factor hedges via our Delta-One team or downside index / ETF protection via our Equity Derivatives team.

BY Doug Kass · Jul 14, 2025, 6:30 AM EDT

The S&P Short Term Oscillator is at 4.99% vs. 7.77% — still overbought.

BY Doug Kass · Jul 14, 2025, 6:14 AM EDT

Professor Scott Galloway's No Mercy No Malice... "Ice Age"

BY Doug Kass · Jul 14, 2025, 6:07 AM EDT