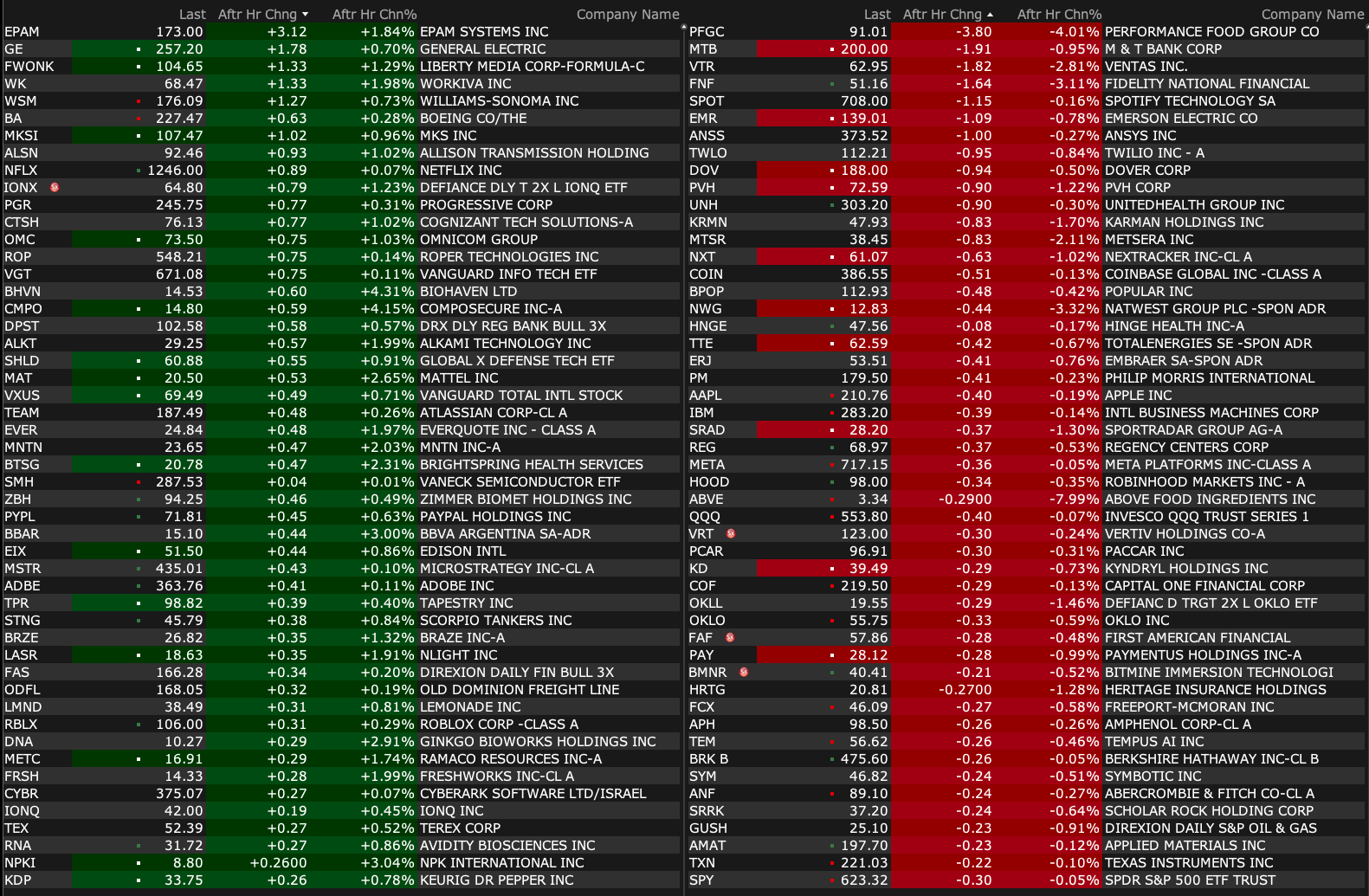

Friday's After-Hours Movers

as of 4:11 p.m.:

BY Doug Kass · Jul 11, 2025, 4:30 PM EDT

as of 4:11 p.m.:

BY Doug Kass · Jul 11, 2025, 4:30 PM EDT

- NYSE volume 11% below its one-month average;

- NASDAQ volume 11% below its one-month average;

- VIX index: up 3.30% to 16.30

BY Doug Kass · Jul 11, 2025, 4:19 PM EDT

I am cutting out early for the weekend to do some gardening.

Thanks so much for providing me with this platform today, this week and since 1997!

Thanks to our editors and my fellow contributors for your assistance and camaraderie.

Enjoy the weekend.

Be safe.

BY Doug Kass · Jul 11, 2025, 3:00 PM EDT

From Peter Boockvar

Positives,

1) Distorted by the timing of the July 4th holiday, initial jobless claims for the week ended 7/5 fell to 227k from 232k and that was 8k less than expected.

2) With the passage of the BBB, income tax rates are now permanent and companies have tax incentives to invest in their business. Though slow the rate of spending? That only really begins in a few years in another can kick.

2) The Atlanta Fed's Wage Tracker showed 4.2% y/o/y growth in June vs 4.3% in May. Part of this is just an easy comp as it was up by 5.3% in June 2024 and still remains above the 3-4% range seen pre Covid. For a 'job stayer', the stat was similar, up 4.2% vs 4.3% in May. For a 'job switcher', wages grew by 4% from 4.1% and that actually is back in line with the pre Covid trend.

4) From the NY Fed’s Consumer Expectations Survey: "Perceptions about households’ current financial situations compared to a year ago improved markedly with a smaller share of households reporting a worse financial situation and a larger share of households reporting a better financial situation. Year-ahead expectations about households’ financial situations also improved, with a smaller share of households expecting a worse financial situation and a larger share of households expecting a better financial situation in one year from now."

5) Influenced by the July 4th holiday in terms of timing, the MBA said purchase applications rose 9.4% w/o/w and refi's were higher by 9.2%.

6) From Delta: "Turning to demand. The environment has been stable since resetting to a lower growth rate earlier this year. Overall demand for air travel remains similar to last year, with softness largely contained to main cabin and particularly during off-peak periods…Our core consumer is in good shape and continues to prioritize travel...This is evidenced by the sustained strength of our premium products and our industry leading co-brand card, with consumer spend growth on the Delta AmEx card up double digits in the first half of the year…Premium revenue continued to outpace main cabin, growing 5% on a y/o/y basis...International revenue grew 2% during the quarter...Corporate demand environment remains steady."

7) From Levi Strauss: "We saw broad based revenue growth across channels and categories as well as strong margin expansion driven by the consistent execution of our strategic priorities…While the global operating environment has become more challenging with uncertainty around tariffs and broader consumer behavior, we are navigating this period from a position of strength."

8) Both the Reserve Bank of New Zealand and Bank of Korea each kept rates unchanged as expected.

9) Consumer prices in China in June continue to see true price stability as they rose .1% y/o/y vs the estimate of down one tenth. Prices ex food and energy rose .7% y/o/y vs .6% in the month before.

10) Still trying to ship as much product as possible during the reciprocal tariff pause, which is about to come to an end, resulted in a 34% y/o/y rise in Taiwanese exports in June, more than the estimate of a 27% gain. It follows a 39% y/o/y spike in May. Exports to the US were up by 91% in particular.

Negatives,

1) Not influenced by the holiday were continuing claims for the week ended 6/28 and they rose 10k w/o/w to 1.965k as expected but at a new cycle high going back to November 2021.

2) With new tariffs on copper imports and newly announced high figures for other countries, what exactly is the overall goal at this point?

3) The June NFIB Small Business Optimism index fell slightly to 98.6 from 98.8 in May and 95.8 in April. It peaked post election at 105.1 in December. The bottom line from the NFIB was this, "Small business optimism remained steady in June while uncertainty fell. Taxes remain the top issue on Main Street, but many others are still concerned about labor quality and high labor costs."

4) Manheim said wholesale used vehicle prices rose 6.3% y/o/y and 1.6% m/o/m in June seasonally adjusted. They said, "Wholesale appreciation trends have been more volatile over Q2 as tariffs really impacted new sales and supply, which impacted the used marketplace as well. The Manheim index has generally been rising since last June, and we typically see the strongest changes for the year in the 2nd quarter as the 'spring bounce' comes to an end. As we move through the 2nd half of 2025, it's likely that some of the reported strength in the market tapers, as the y/o/y comparisons are tougher in the back half of the year. Even so, retail sales continue to run a bit hotter than prior years, and off-lease supply into the market is still on a downward path, two factors which should be fairly supportive of higher values as we move onward."

5) From Conagra: They talked about “the decline in consumer sentiment during the fourth quarter of fiscal ’25, driven by the cumulative impact of persistent inflation, rising interest rates, and overall economic uncertainty. This decline translated into more cautious spending behaviors. Consumers became increasingly focused on seeking value, prioritizing affordability, and trading down where possible. While our brands are well-positioned to deliver value and meet these shifting needs, the environment created additional pressure on volumes.” Also, “inflation remains persistent. For fiscal ’26, we expect core cost of goods inflation to be approximately 4%. To put that into context, this level of inflation in fiscal ’26 will bring our five year cumulative, net inflation to approximately 45%, a historic amount of inflation over such a short period of time. On top of that, the current tariff environment is expected to add approximately 3% to our cost of goods sold, or more than $200 million annually. This brings total anticipated inflation for fiscal ’26 to approximately 7%.”

6) From Helen of Troy: "our Q1 results were well below our expectations. Tariff related disruption on our shipments was greater than we originally expected in April. There are three tariff related impacts making up approximately 8 percentage points of the 10.8% consolidated revenue decline. One, cancellation of direct import orders from China in response to higher tariffs. Two, tariff related pull forward of orders into the fourth quarter of fiscal '25, leading to elevated inventory and lower replenishment in the first quarter of fiscal '26, which we expect to continue into the second quarter as demand continues to soften. And three, China softness driven by a shift from cross border e-commerce, the localized distribution models, and increased competition from domestic sellers driven by government subsidies." How are they mitigating the tariffs? "We are implementing and have them ready to go and essentially lined up with the retailers to implement an average price increase across our portfolio in the range of 7% to 10%. And if you look on an individual product basis, that ranges from zero because there's items we're not taking price on to as high as 15% on an individual item." Also, "Suspension of non-critical projects in capital expenditures, except those supporting supplier diversification and dual sourcing projects, reduction of personnel costs and extended pause on those projects and travel spend, prioritization of marketing, promotion and product development investments with the highest returns, and lastly, we have taken actions to improve working capital efficiencies and balance sheet productivity."

7) From Levi Strauss: With tariffs and its impact, "we estimate a gross impact before mitigation of approximately 50 bps to our gross margin for 2025. After mitigation, we expect the net impact of tariffs to be about 20 bps headwind to our full year gross margin or approximately a 40 bps impact in the second half. This will result in a $.02 and $.03 impact to '25 adjusted diluted EPS split evenly between quarter three and quarter four." As to their mitigation efforts, they include "promotional optimization, targeted pricing actions, vendor negotiations and further supply chain diversification."

8) From Kura Sushi: They reported comps down 2.1% y/o/y with price/mix up .8% "offset by negative traffic of 2.9%." "Labor as a percentage of sales increased by 50 bps due to high single digit wage inflation." In their fresh quarter they are in now, "we'll see mid to low single digit labor inflation which would be an improvement from what we've seen in Q2 and Q3." On the offset to higher costs, "Effective pricing for the quarter was 4.3%. On June 1, we took a 1% menu price increase and after lapping prior year increases, our effective price for the fourth quarter will be 3.5%." They are currently now in their fiscal Q4.

9) The UK economy unexpectedly contracted by one tenth in May vs the estimate of up .1% and follows a decline of .3% in April.

10) Japan's June PPI rose 2.9% y/o/y though as expected.

11) China said its PPI for June fell 3.6% y/o/y which was more than the estimate of down 3.2%.

12) The floods and lost lives in Texas are just heartbreaking.

BY Doug Kass · Jul 11, 2025, 2:00 PM EDT

I have a research call between 1 PM and 2 PM.

Radio silence.

BY Doug Kass · Jul 11, 2025, 1:05 PM EDT

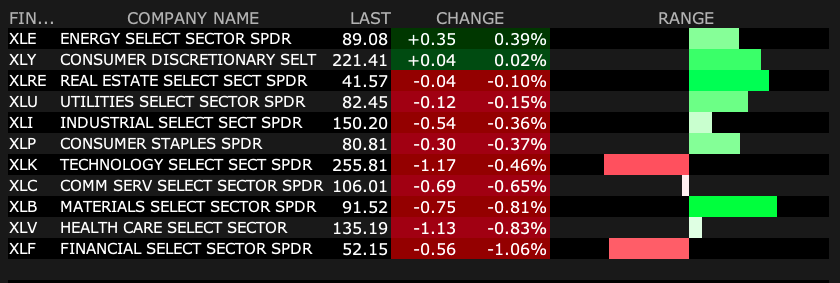

* S&P/Nasdaq flattish, Equal Weighted S&P and Russell -1.00% or so

* As breadth deteriorates/weak

SPY -0.33%

QQQ -0.08%

IWM -1.24%

RSP -0.89%

TLT -1.34%

BY Doug Kass · Jul 11, 2025, 12:55 PM EDT

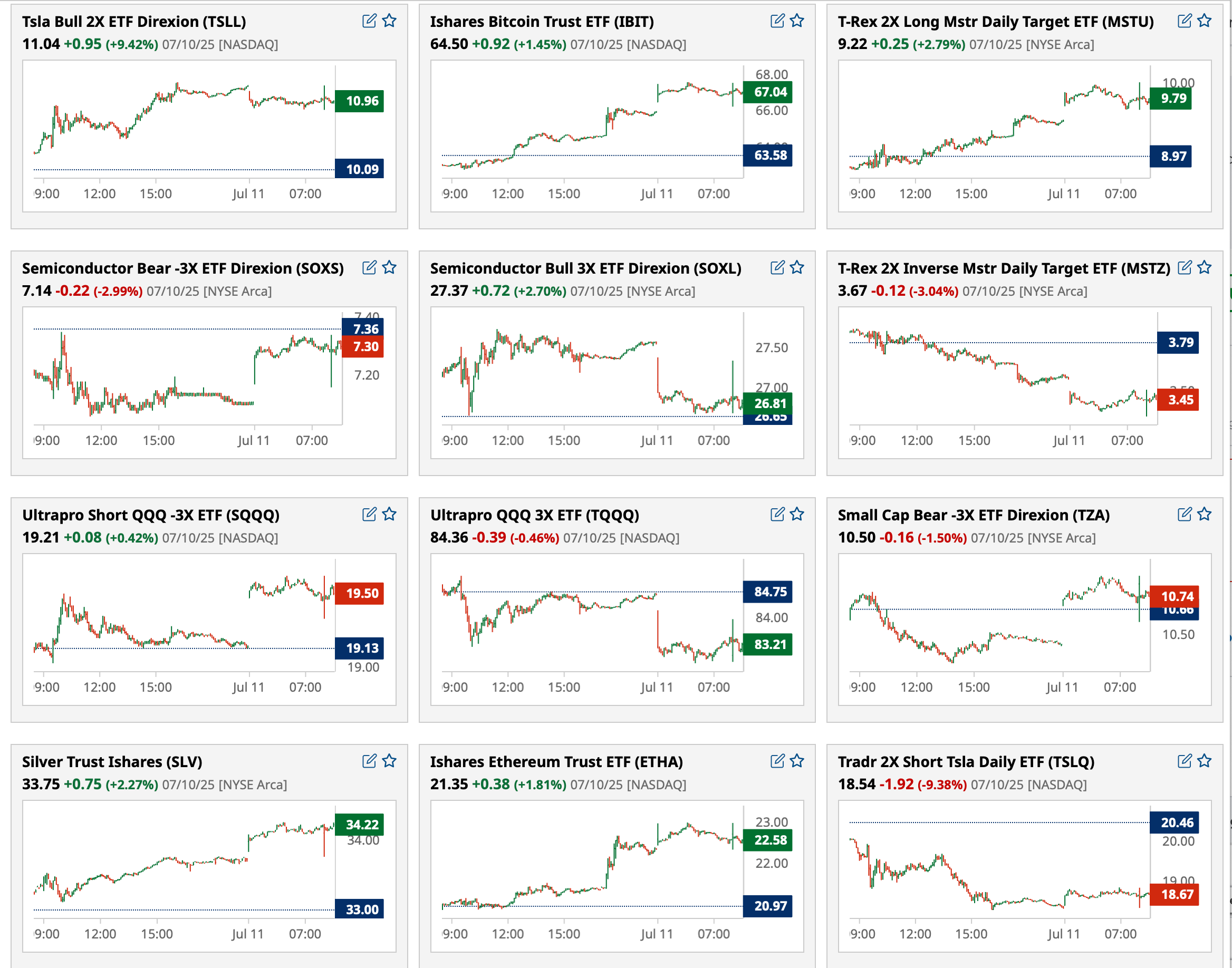

I moved from VVS bitcoin to S short this morning:

* BITO $22.64

* BITB $64.01

* IBIT $66.89

BY Doug Kass · Jul 11, 2025, 12:05 PM EDT

I added to index shorts with the rally just now:

* SPY $624.43

* QQQ $555.35

BY Doug Kass · Jul 11, 2025, 11:55 AM EDT

From a 20-something reporter on CNBC with regard to bitcoin:

"It's hard to identify downside risk..."

BY Doug Kass · Jul 11, 2025, 11:45 AM EDT

- NYSE volume 8% below its one-month average;

- Nasdaq volume 15% below its one-month average;

- VIX index: up 4.44% to 16.48

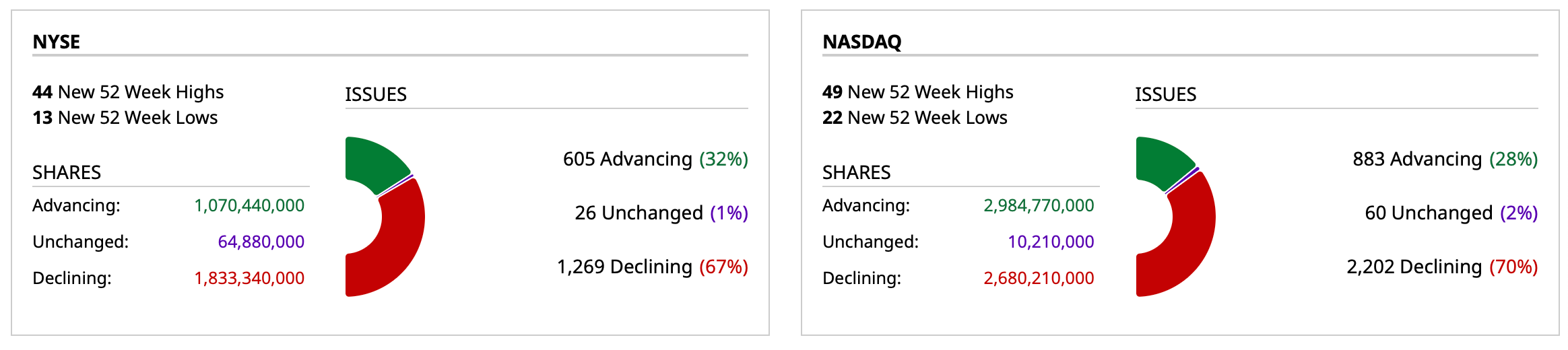

BY Doug Kass · Jul 11, 2025, 11:20 AM EDT

In a more aggressive way, I shorted the move of the Nasdaq back to unchanged.

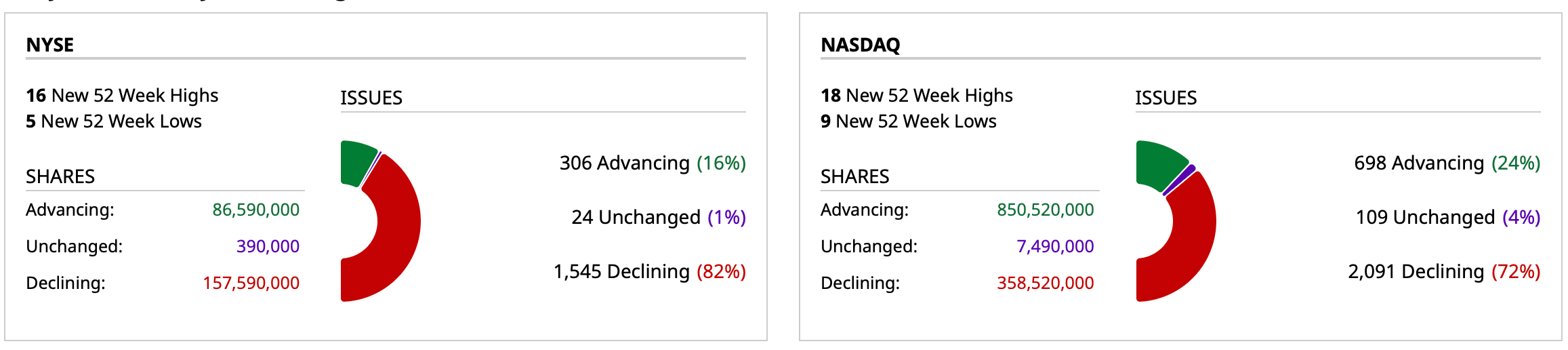

Breadth stinks up the joint - with NYSE 5-1 negative and Nasdaq 3-1 negative .

Stay tuned.

BY Doug Kass · Jul 11, 2025, 10:55 AM EDT

From Peter Boockvar:

It seems to be a settled debate on the part of some that if there is not consumer price inflation from tariffs than there is victory with its use. Unfortunately there is not enough debate on the coming hit to corporate profit margins for those companies that don't have much pricing power. Companies that make less money usually hire less and invest less in their business. See what Conagra, along with Helen of Troy, said below in their earnings call yesterday and how high their input cost inflation is now when including tariffs and the mitigation steps they are each taking.

I must say again, as a fan of low taxes, particularly on the corporate side which allows American companies to be more competitive, I am getting more and more concerned with where this tariff war is going and the economic impact. I will give basic math AGAIN with the latest post raising the possibility of a baseline tariff of 15-20% instead of 10%. With $3.3 Trillion of goods imports, a 15% blanket tariff would equal about $500b of fresh taxes and with 20%, $660 billion. The estimate for this fiscal year on tax receipts from the corporate tax is about $525b. So tariffs are possibly going to double the effective tax rate for corporations and possibly by more than that from the current 21%. Remember 2017 when all we did was seemingly rally every single day on the hopes for the eventual tax cut passage? Where are the concerns right now with this massive tax hike? I feel like I'm the only one that is worried and I'm living in some parallel universe with economic concerns. I hope I'm wrong but I'm getting more and more nervous that I won't be.

From Conagra, the largest frozen food producer in the country, along with a snacks business which includes beef jerky and popcorn:

They talked about “the decline in consumer sentiment during the fourth quarter of fiscal ’25, driven by the cumulative impact of persistent inflation, rising interest rates, and overall economic uncertainty. This decline translated into more cautious spending behaviors. Consumers became increasingly focused on seeking value, prioritizing affordability, and trading down where possible. While our brands are well-positioned to deliver value and meet these shifting needs, the environment created additional pressure on volumes.”

“inflation remains persistent. For fiscal ’26, we expect core cost of goods inflation to be approximately 4%. To put that into context, this level of inflation in fiscal ’26 will bring our five year cumulative, net inflation to approximately 45%, a historic amount of inflation over such a short period of time. On top of that, the current tariff environment is expected to add approximately 3% to our cost of goods sold, or more than $200 million annually. This brings total anticipated inflation for fiscal ’26 to approximately 7%.” I bolded for emphasis.

“Our canned food products make up the largest tariff exposure as steel and aluminum tariffs significantly increase the cost to procure tin plate steel as domestic supply is very limited.”

“We experienced double-digit inflation in categories including chicken, beef, and eggs as proteins remained highly inflationary.”

From Helen of Troy, the maker of everything from backpacks, travel gear, hair spray, blow dryers, and brushes among other things and whose stock fell 23% yesterday:

"our Q1 results were well below our expectations. Tariff related disruption on our shipments was greater than we originally expected in April. There are three tariff related impacts making up approximately 8 percentage points of the 10.8% consolidated revenue decline. One, cancellation of direct import orders from China in response to higher tariffs. Two, tariff related pull forward of orders into the fourth quarter of fiscal '25, leading to elevated inventory and lower replenishment in the first quarter of fiscal '26, which we expect to continue into the second quarter as demand continues to soften. And three, China softness driven by a shift from cross border e-commerce, the localized distribution models, and increased competition from domestic sellers driven by government subsidies."

"In addition to tariff related impacts, we also saw weeks of supply adjustment at certain key retailers as shifting consumer demand curves are being reflected in retailers inventory management practices."

"Finally, we are seeing clear evidence of the consumer trading down with average price compression of 3% to 4% in our US business (in terms of shifting to lower priced products), which impacted first quarter revenue and profitability. You may have seen other companies recently calling out trade down behavior, including the Dollar stores, which are a beneficiary of this trend."

On one of their mitigation steps, "we have implemented strategic price increases that will take effect near the end of summer." So, price increases are coming from some. "Looking at the full fiscal year, based on tariffs currently in place, current inventory levels and consumer demand trends, we continue to expect that the vast majority of direct tariff costs will impact the second half of our fiscal year, which is largely aligned with our planned price increases."

How big are those price increases going to be? "We are implementing and have them ready to go and essentially lined up with the retailers to implement an average price increase across our portfolio in the range of 7% to 10%. And if you look on an individual product basis, that ranges from zero because there's items we're not taking price on to as high as 15% on an individual item." I bolded for emphasis.

Also, "Suspension of non-critical projects in capital expenditures, except those supporting supplier diversification and dual sourcing projects, reduction of personnel costs and extended pause on those projects and travel spend, prioritization of marketing, promotion and product development investments with the highest returns, and lastly, we have taken actions to improve working capital efficiencies and balance sheet productivity."

From Delta, where we know travel remains an economic bright spot:

"Turning to demand. The environment has been stable since resetting to a lower growth rate earlier this year. Overall demand for air travel remains similar to last year, with softness largely contained to main cabin and particularly during off-peak periods."

"Our core consumer is in good shape and continues to prioritize travel...This is evidenced by the sustained strength of our premium products and our industry leading co-brand card, with consumer spend growth on the Delta AmEx card up double digits in the first half of the year."

"On the supply side, we're encouraged by the industry's actions to align capacity with demand as we move beyond the peak summer period. Importantly, seats at the lower end of the market are scheduled to contract as carriers adjust to the environment and work to improve financial performance."

"We have also adjusted to a lower growth environment and as discussed in April, our focus is managing the levers in our control to generate strong earnings and free cash flow. This includes adjusting our capacity to match demand and aggressively managing our cost base to deliver on our commitments."

Levi's had a good quarter and is getting rewarded with a pre-market stock lift. They said, "We saw broad based revenue growth across channels and categories as well as strong margin expansion driven by the consistent execution of our strategic priorities."

They've improved their DTC business and is becoming more than just a denim brand. "While the global operating environment has become more challenging with uncertainty around tariffs and broader consumer behavior, we are navigating this period from a position of strength."

With tariffs and its impact, "we estimate a gross impact before mitigation of approximately 50 bps to our gross margin for 2025. After mitigation, we expect the net impact of tariffs to be about 20 bps headwind to our full year gross margin or approximately a 40 bps impact in the second half. This will result in a $.02 and $.03 impact to '25 adjusted diluted EPS split evenly between quarter three and quarter four."

As to their mitigation efforts, they include "promotional optimization, targeted pricing actions, vendor negotiations and further supply chain diversification."

Fed Governor Chris Waller who spoke yesterday and made it a point to say he's not being political by wanting a July rate cut, also gave us his view on where the Fed's balance sheet should settle out at. "I believe we can likely continue to let a share of maturing and prepaying securities roll off our balance sheet for some time, reducing reserve balances." He believes bank reserves can fall to about $2.7 Trillion from the current level of around $3.26 Trillion and that would imply a further drop in the overall Fed balance sheet of about $900b to $5.8 Trillion.

This is the first time I've seen some hard numbers of what the possible ultimate goal is with the balance sheet as Powell in the past as told us that he'll know it when he sees it in terms of the right levels.

The UK economy unexpectedly contracted by one tenth in May vs the estimate of up .1% and follows a decline of .3% in April. The Starmer government did themselves no favors by raising labor costs via higher payroll costs on employers.

It's not just copper prices that continue to rally, silver today is up about 3% to the highest level since 2011 and we remain bullish and long.

Silver

BY Doug Kass · Jul 11, 2025, 10:15 AM EDT

Shorted more SPY at $623.24.

BY Doug Kass · Jul 11, 2025, 10:13 AM EDT

Shorted more QQQ at $553.74.

BY Doug Kass · Jul 11, 2025, 9:56 AM EDT

I am at my largest net short exposure since February, 2025.

BY Doug Kass · Jul 11, 2025, 9:52 AM EDT

No trades (yet) today.

BY Doug Kass · Jul 11, 2025, 9:40 AM EDT

BY Doug Kass · Jul 11, 2025, 9:30 AM EDT

BY Doug Kass · Jul 11, 2025, 9:13 AM EDT

-GAUZ +16% (announces insider purchases of 560K shares by CEO & Co-Founder Peso and second largest long-term investor Weinstein)

-CEP +10% (Twenty One Capital files draft S-4 for proposed merger)

-UPXI +8.4% (prices $200M concurrent private placement of common stock and convertible notes both priced above the at-the-market)

-PFGC +7.9% (reportedly US Foods expressed interest in Performance Food Group)

-LEVI +7.8% (earnings, guidance)

-AMC +7.3% (Wedbush, Inc. Raised AMC to Outperform from Neutral, price target: $4)

-PSMT +6.1% (earnings)

-HUSA +5.6% (secures $100M Equity Line of Credit to Fuel Growth and Support Strategic Acquisitions; Secures $5M in Strategic Financing to Acquire Texas Gulf Coast Development Site)

-AVAV +3.8% (reportedly Def Sec Hegseth has ordered drone production and deployment surge)

-MDT +3.2% (RDN NCA proposal)

-SOC +3.1% (discloses Santa Barbara County Superior Court denied a motion to stay California Coastal Commission’s Apr 10th Cease and Desist Order regarding Sable Offshore's maintenance and repair work in the coastal zone)

-MSTR +3.0% (BTC strength)

-MIST -30% (announces proposed public offering of shares and warrants of indeterminate amount)

-KPTI -13% (engaged in confidential discussions with potential investors, including new and existing investors in connection with potential financing transactions; To cut workforce by 20% of headcount)

-FEIM -5.4% (earnings)

BY Doug Kass · Jul 11, 2025, 8:57 AM EDT

BY Doug Kass · Jul 11, 2025, 8:38 AM EDT

hmeisler

STAFF

7 minutes ago

Above Dougie has an Eisenhower quote about GM and the country. But there also used to be a 'GM Rule' for the markets: if GM fails to make a new high every 4 months (i.e. if four months passes and GM does not make a new high) the overall market is in trouble. It had like a 90% win rate for decades. Why? There was a time that GM or a company related to it employed 1 in 7 Americans.

The lesson: there is always some hot stock that everyone thinks the whole market hinges on (looking at you AAPL) that eventually sees the market move on.

...

And how about this Walt Deemer General Motors story when we worked together at Putnam Managment in Boston: Walt's Wit and Wisdom - Why the Case of GM and the Fable of the Fishing Boat May Apply to Tech Stocks Today

BY Doug Kass · Jul 11, 2025, 8:22 AM EDT

BY Doug Kass · Jul 11, 2025, 7:35 AM EDT

From JPMorgan:

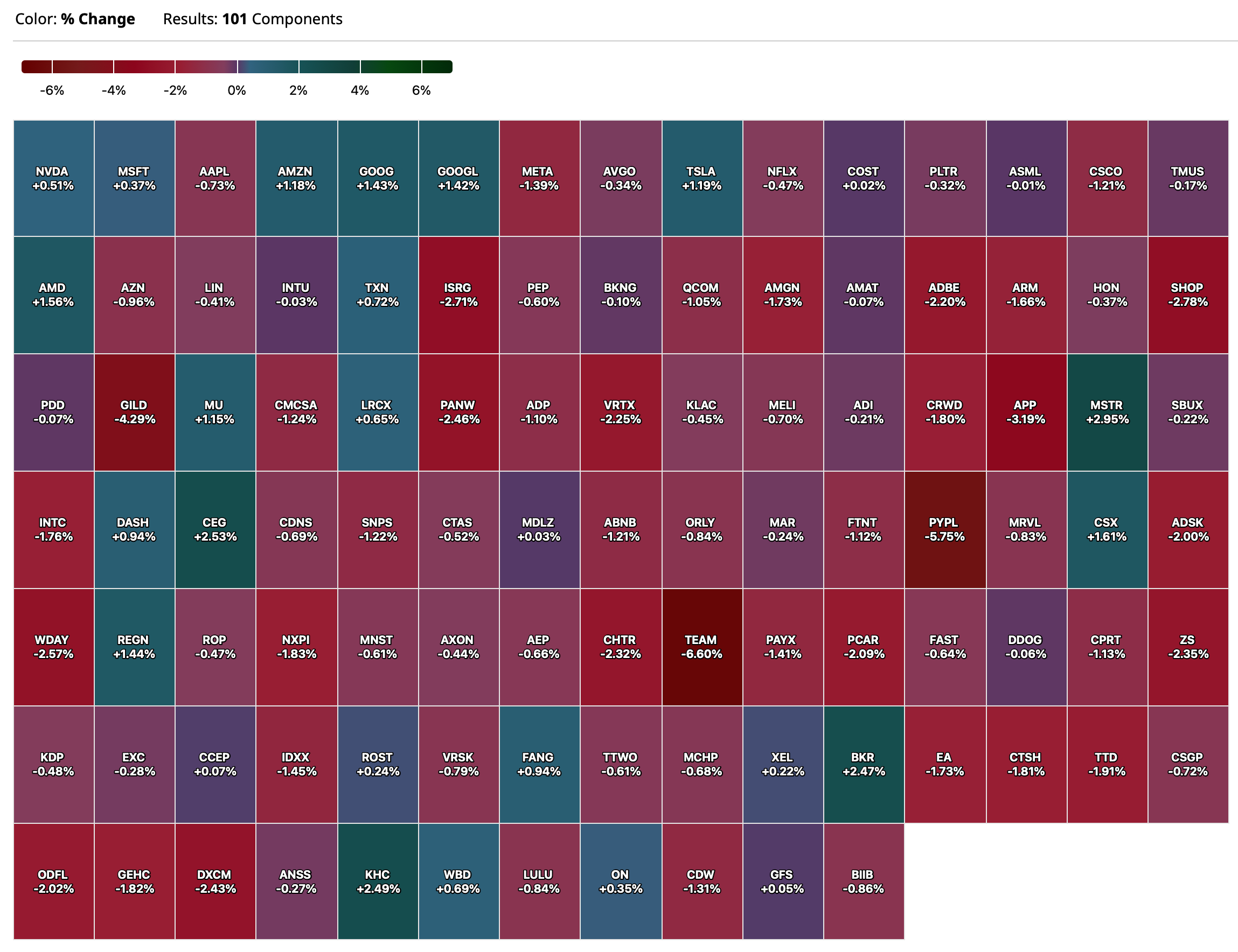

US: Futs are weaker. Tariff talk is an overhang as Trump threatens Canada with a 35% tariff rate and discusses higher baseline tariffs on most trading partners; the EU letter is expected to be sent today. Pre-market, MegaCap Tech sees META (-1.7%) underperforming, followed by NVDA (-1.6%) and GOOGL (-1.6%); Consumer Discretionary and Utilities are outperforming. Yields are lower and USD is higher; 2-, 5-, 10-, 30-yr yields are down 1.9bp, 1.8bp, 1.6bp, and 1.0bp respectively. Commodities are mixed, with base metals higher and precious metals lower.

and...

Futures are lower amid the major tariff updates after market close yesterday: Trump announced the 35% tariffs on Canadian goods, with baseline tariffs possibly rising from 10%to 15-20%. Trump implied that the EU letter can be expected today. Stock futures fell ~60bp; USDCAD rose modestly from 1.36 to 1.37. Overall, the reaction has been much muted compared to the sequence of tariff announcement earlier in Q2 as investors still look for policy shift or deal announcements ahead of the August deadline. As we moved into the earnings season (banks will kick off the season next Tuesday), DAL and LEVI both pointed to the healthy demand and resilient consumers this quarter.

BY Doug Kass · Jul 11, 2025, 7:15 AM EDT

BY Doug Kass · Jul 11, 2025, 7:00 AM EDT

* And, if so, what might it mean...

As President Eisenhower was fond of saying (about the critical link between business and politics):

"As goes General Motors, so goes the nation."

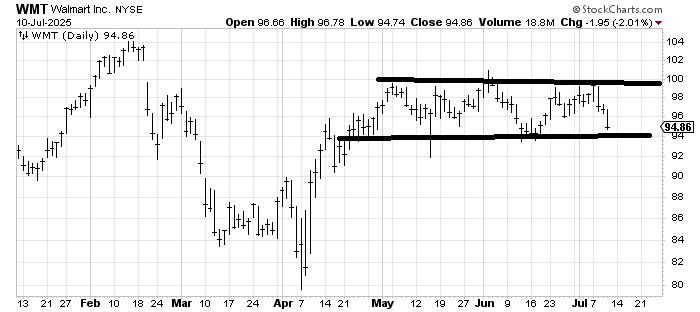

I would argue, for a host of obvious reasons, that Walmart WMT has replaced General Motors GM as a leading indicator in recent decades.

As noted this week, I have been expanding my consumer shorts. (See my notes on the downturns in Florida and California housing, which could result in a consumer-led economic disappointment).

Specifically, two popular Wall Street faves (Costco COST (which disappointed in monthly sales yesterday) and WMT) have been the objects of my recent disaffection (and shorting).

Here is what The Divine Ms M wrote about Walmart this morning:

An example of a stock that threatened to break in mid-June is Walmart (WMT). It has been my contention, since May, that this stock looks to be in a trading range between 95-100, which so far has been the case.

You see how it got saved from breaking in mid-June? And here it is retesting that area once again? A save keeps the indicators the same as they are now. If charts like this start breaking, the indicators will start to roll over.

BY Doug Kass · Jul 11, 2025, 6:30 AM EDT

The S&P Short Range Oscillator scooted much higher (to 7.77% vs. 5.97%) into an extremely overbought condition at the close of trading Thursday.

My net short exposure has expanded commensurately as I very much like the short setup. (But, admittedly, I have been wrong before!)

As I noted earlier this week (Tuesday):

* I am positioning accordingly...

The overbought and excessive investor optimism are getting aligned:

* The S&P Short Range Oscillator is overbought at 6.89% vs. 8.25%.

* The CNN Fear and Greed Indicator is at Extreme Greed:

Fear and Greed Index - Investor Sentiment | CNN

* NAAIM exposure (at 100), Investors Intelligence Bulls jump to 51% over Bears, AAII Bulls climb by 10 to 45% (highest of the year), Equity Put/Call below 0.50, NYSE DSI at 87 and Nasdaq at 86, and Citi Panic/Euphoria moves to "euphoria."

While I respect the price action, recognize the role of market structure (the dominance of passive investing) and herd mentality (as more traders and investors than at any time in history worship at the altar of price momentum), I am planning to position to a more negative market exposure on any rally.

By Doug Kass Jul 8, 2025 5:49 AM EDT

BY Doug Kass · Jul 11, 2025, 6:18 AM EDT

* It always starts in Florida and California...

Wolf Street howls about the rapid climb in unsold homes in Florida.

BY Doug Kass · Jul 11, 2025, 5:50 AM EDT