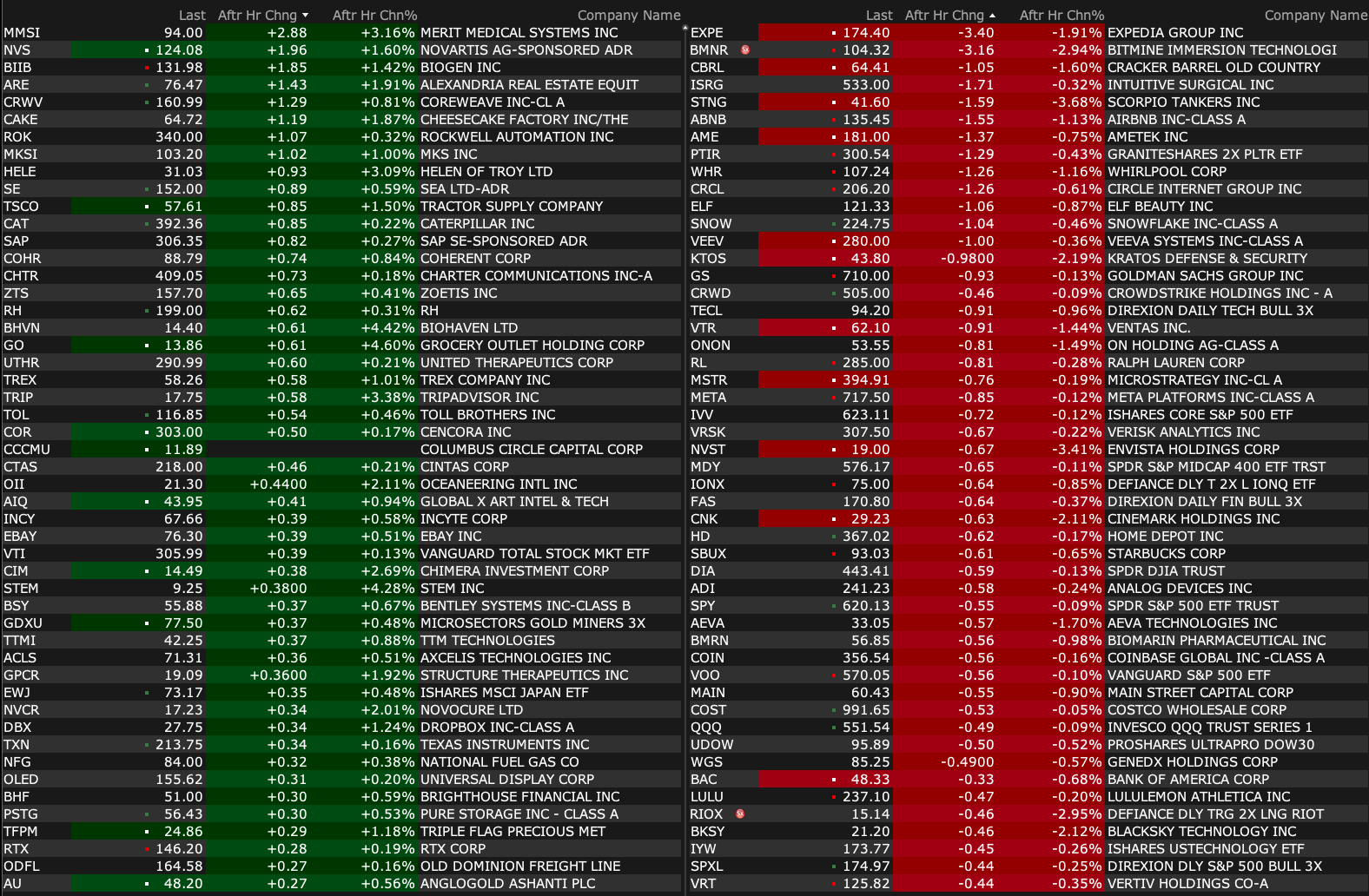

Monday's After-Hours Movers

As of 4:18 p.m.:

BY Doug Kass · Jul 7, 2025, 4:45 PM EDT

As of 4:18 p.m.:

BY Doug Kass · Jul 7, 2025, 4:45 PM EDT

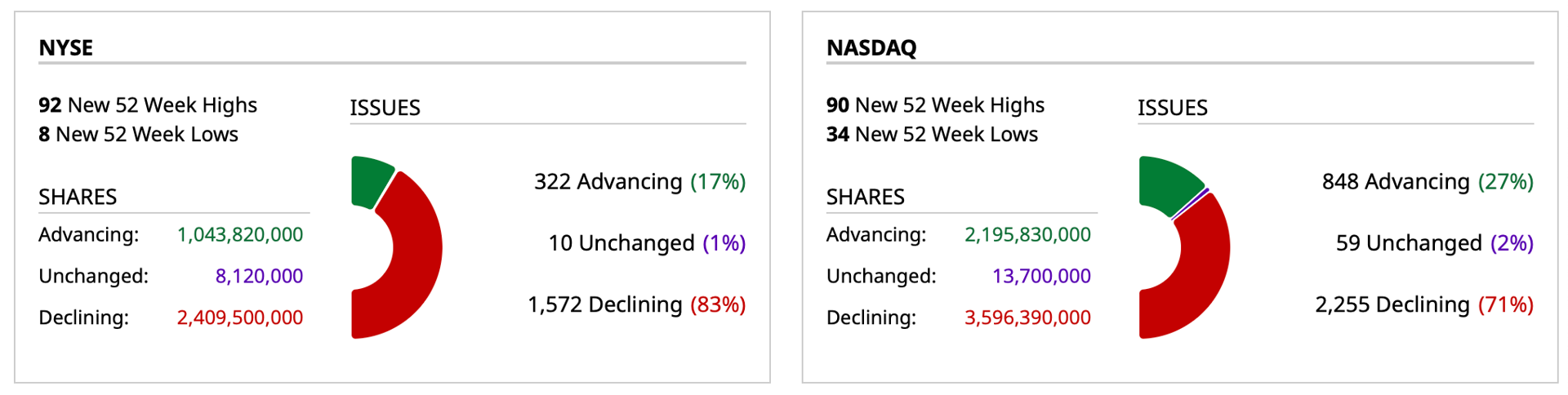

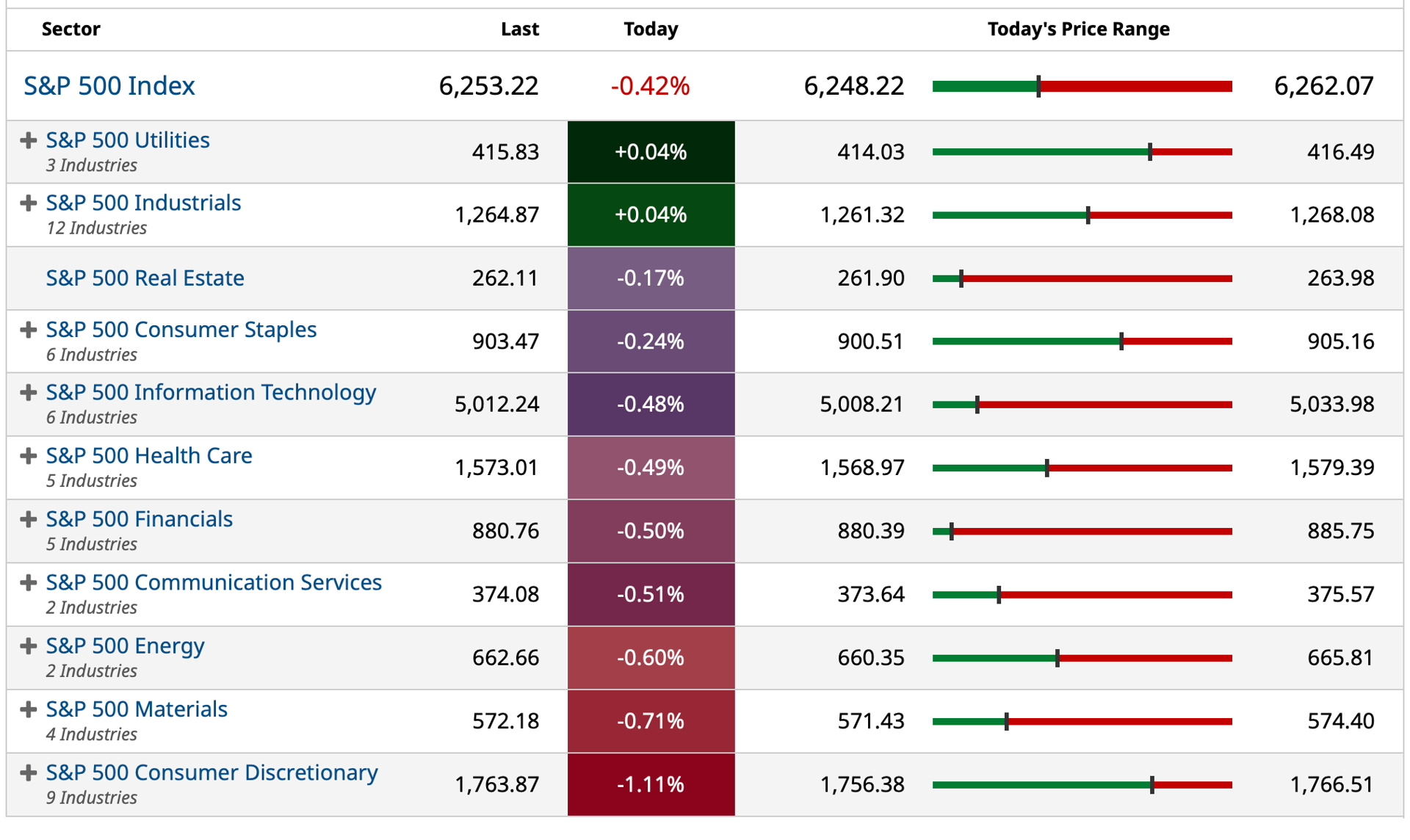

SPY (green) advanced into the close but not along with Breadth (blue)

BY Doug Kass · Jul 7, 2025, 4:35 PM EDT

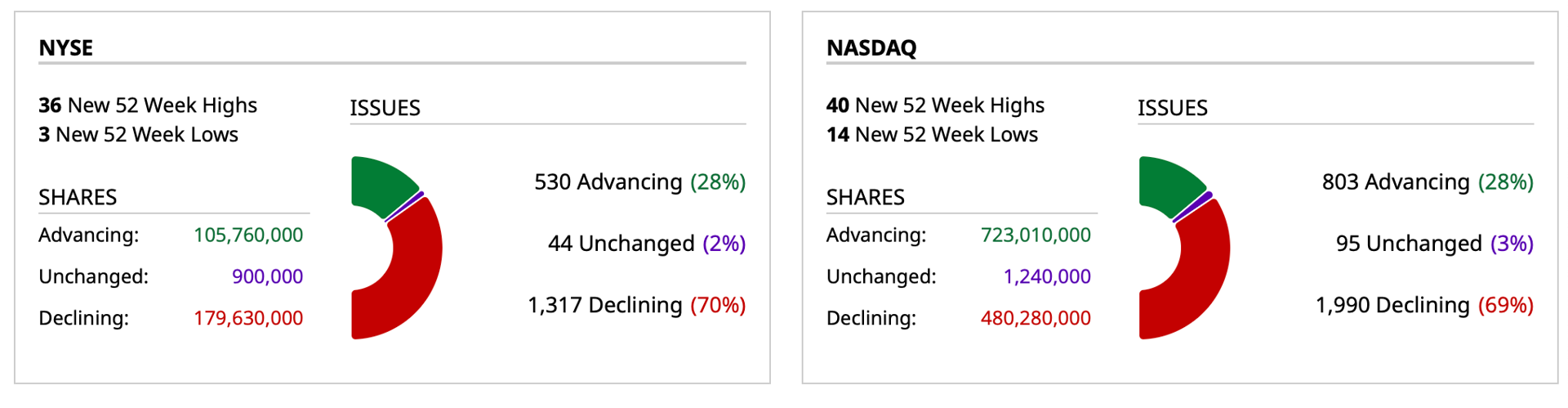

- NYSE volume 2% above its one-month average;

- NASDAQ volume 9% below its one-month average;

- VIX index: up 1.89% to 17.81

BY Doug Kass · Jul 7, 2025, 4:23 PM EDT

I am now inclined to short any rallies.

Be forewarned.

BY Doug Kass · Jul 7, 2025, 4:02 PM EDT

No trades yet today.

BY Doug Kass · Jul 7, 2025, 12:00 PM EDT

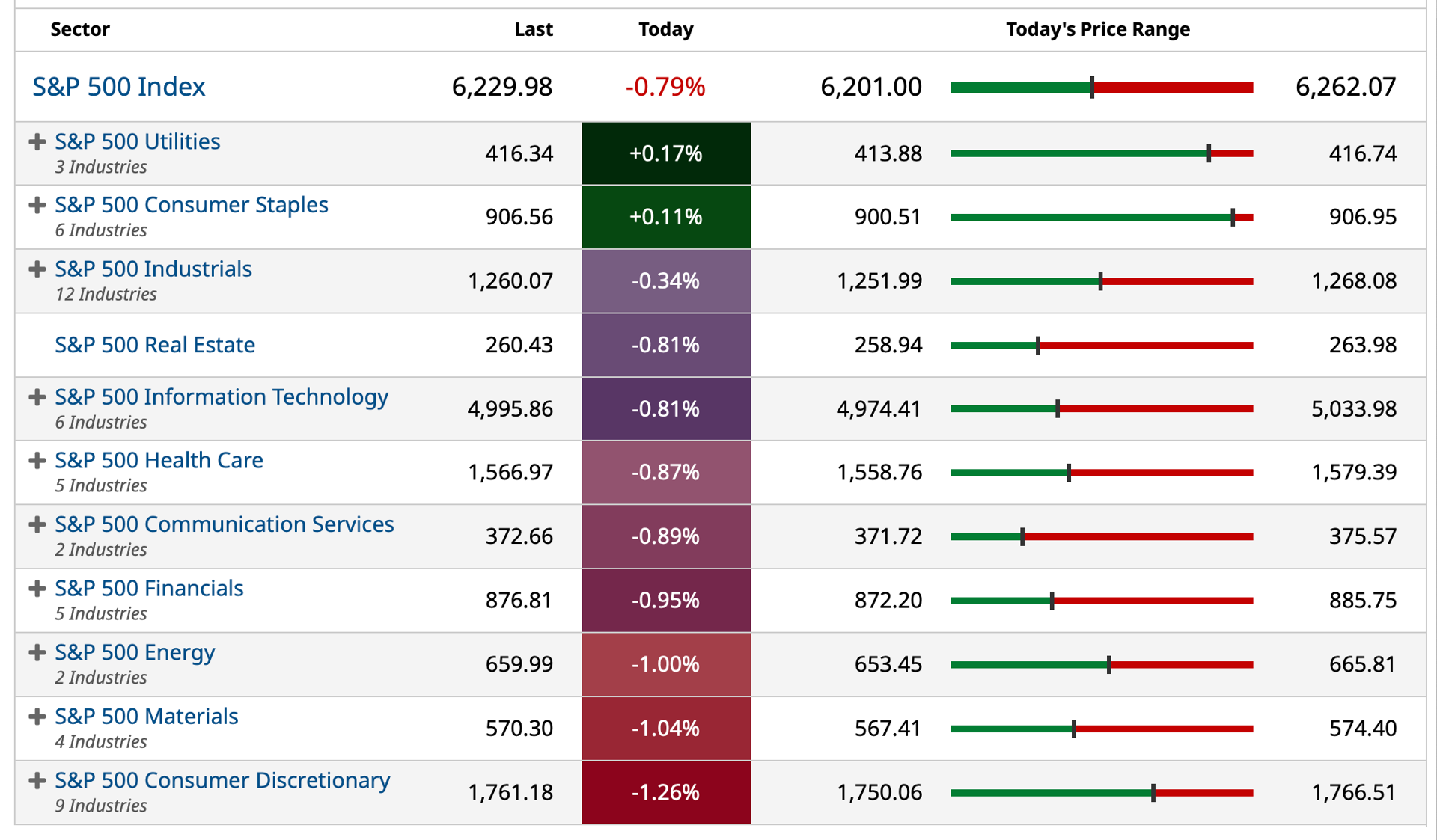

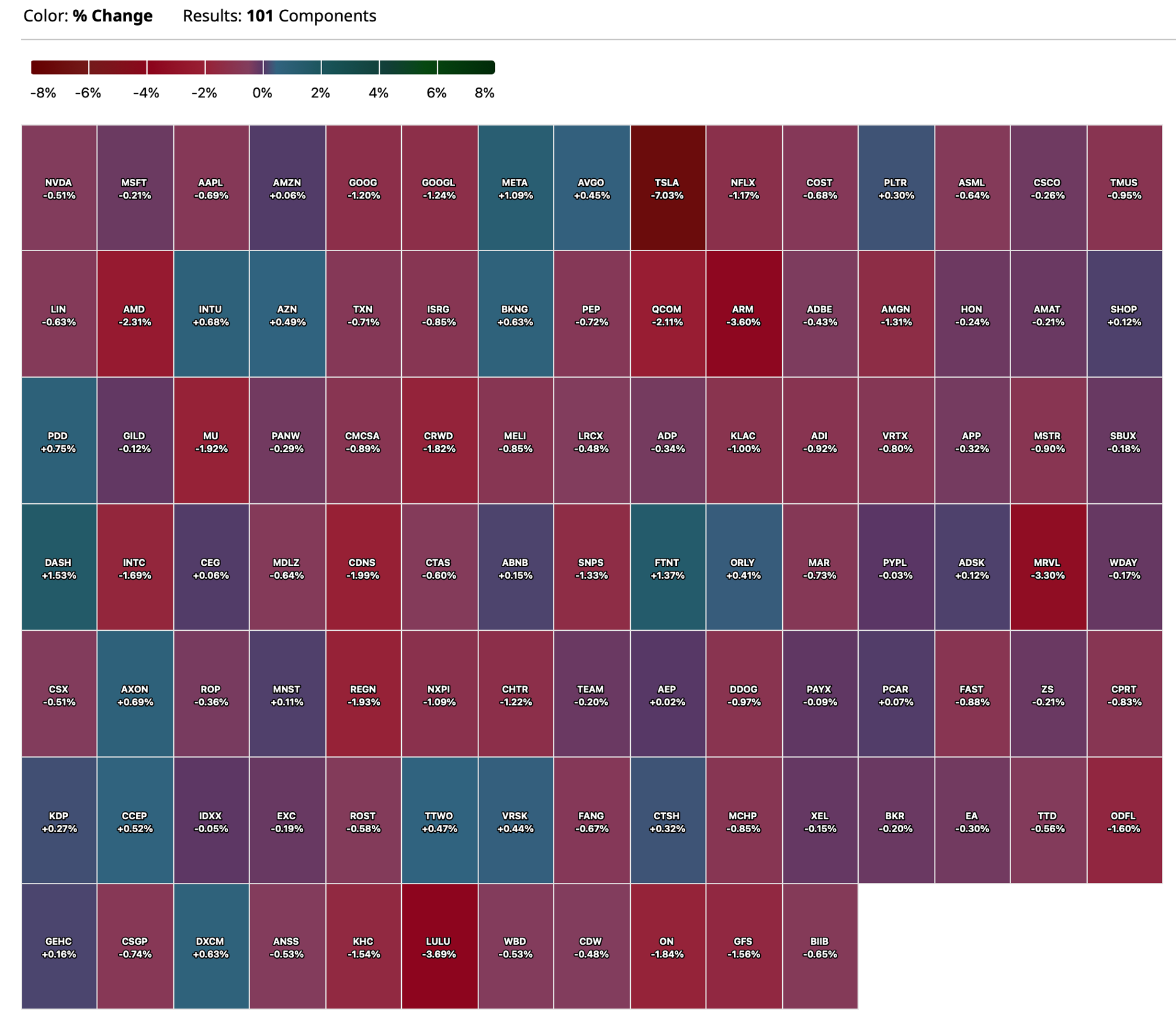

Tech XLK Leads QQQs to fresh day lows at 11 a.m.

BY Doug Kass · Jul 7, 2025, 11:30 AM EDT

BY Doug Kass · Jul 7, 2025, 11:19 AM EDT

From Charlie!

BY Doug Kass · Jul 7, 2025, 11:00 AM EDT

BY Doug Kass · Jul 7, 2025, 9:56 AM EDT

BY Doug Kass · Jul 7, 2025, 9:45 AM EDT

BY Doug Kass · Jul 7, 2025, 9:30 AM EDT

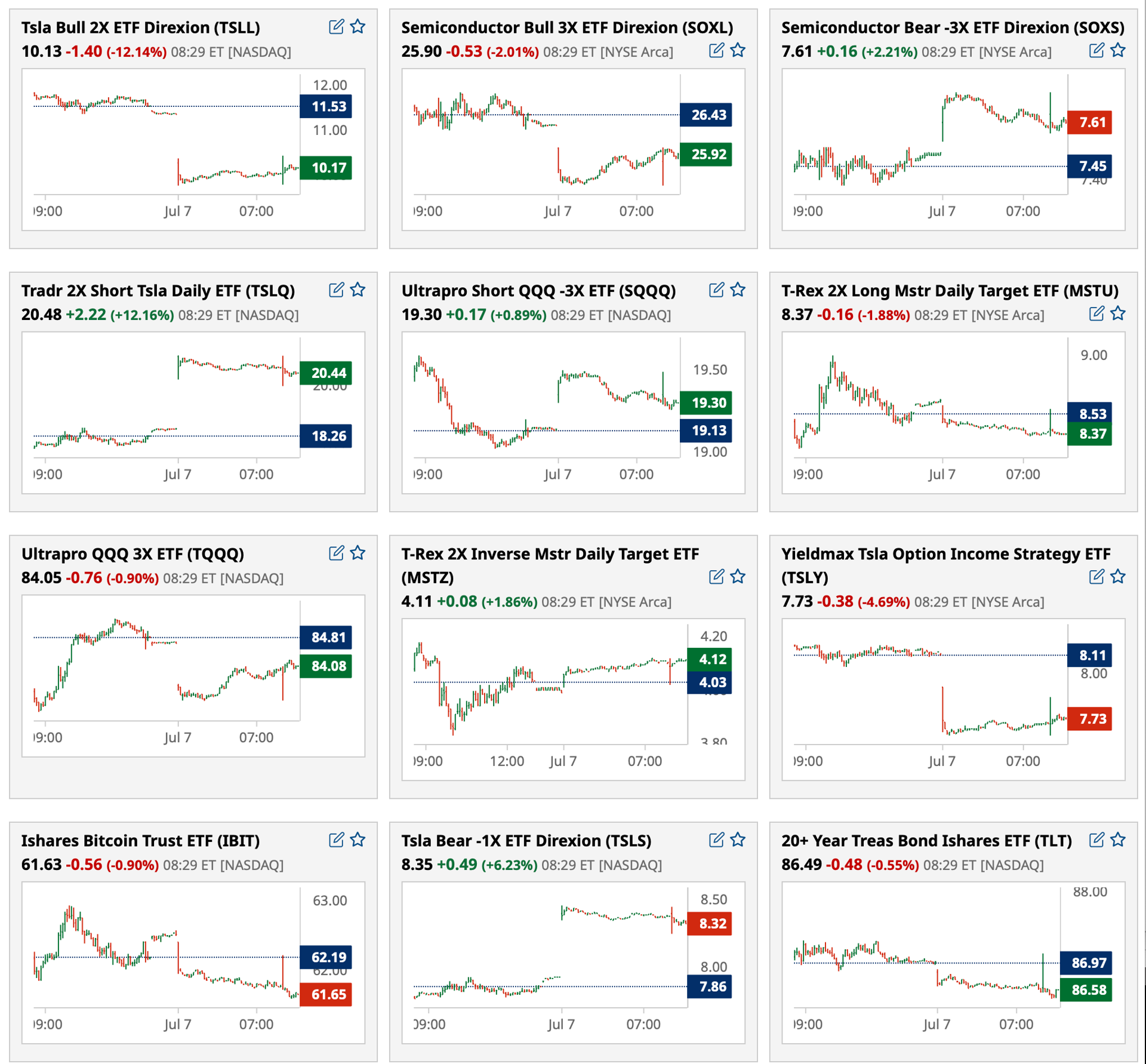

Charts from 8:29 a.m. ET:

BY Doug Kass · Jul 7, 2025, 9:15 AM EDT

From Peter Boockvar:

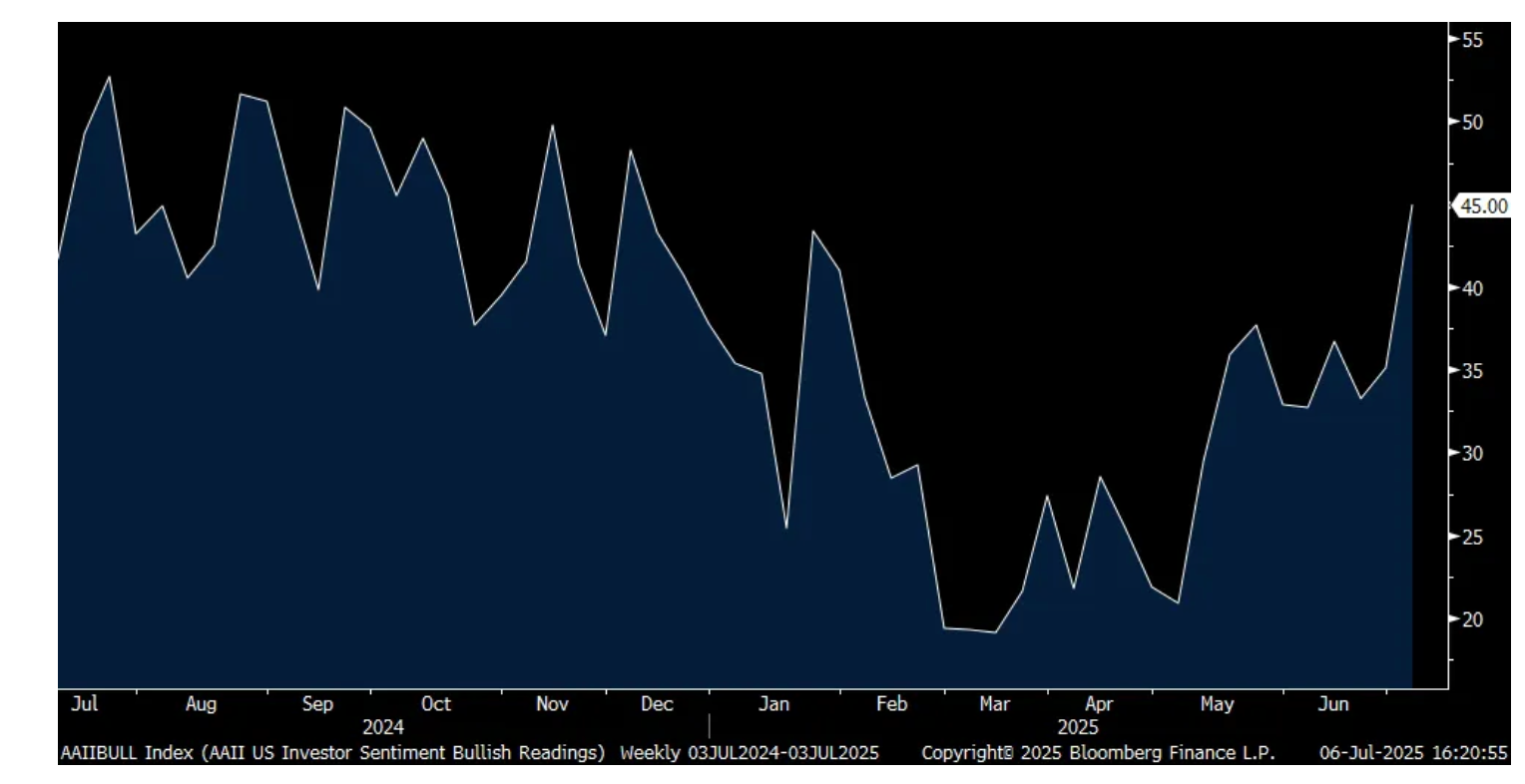

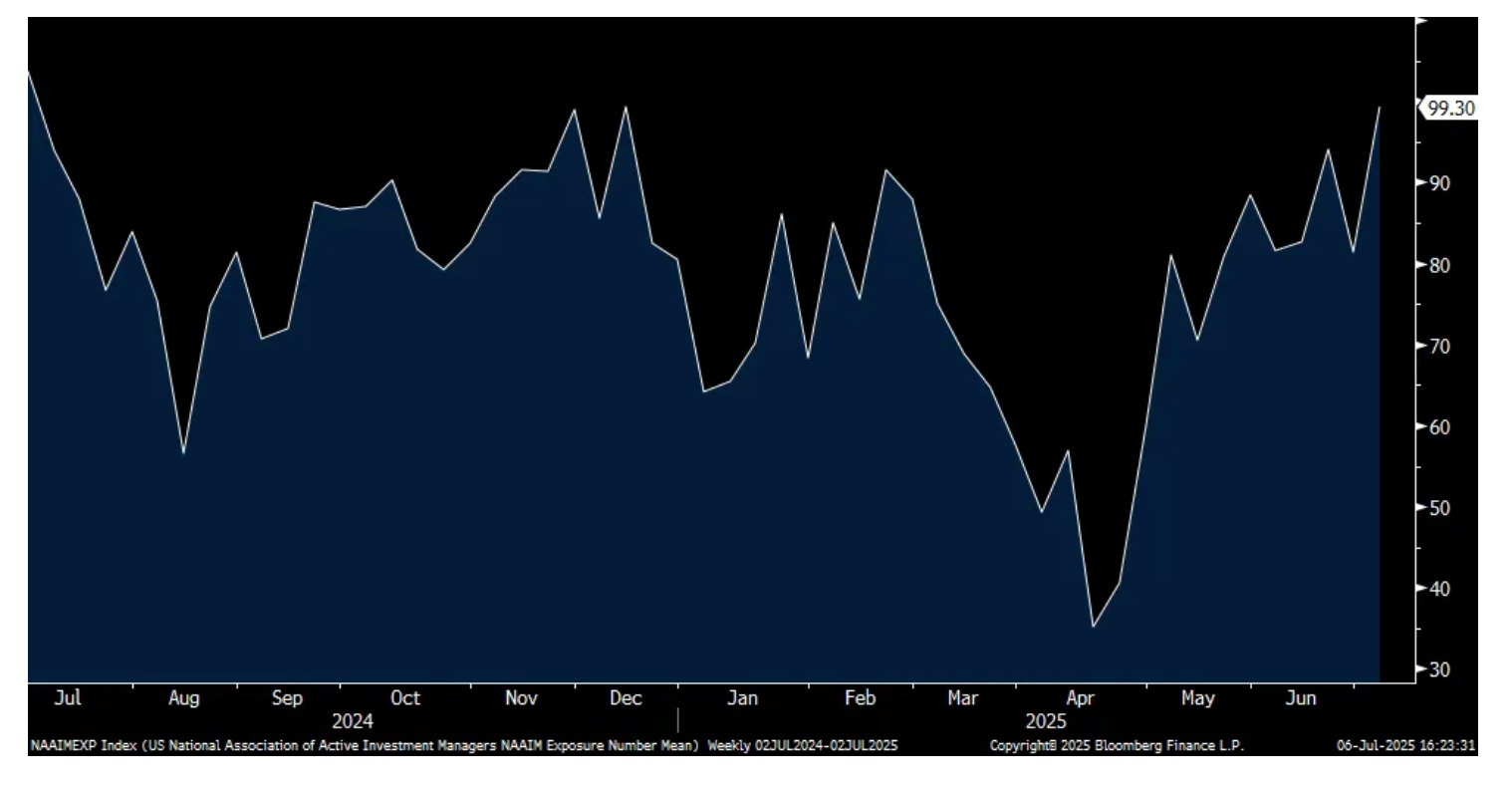

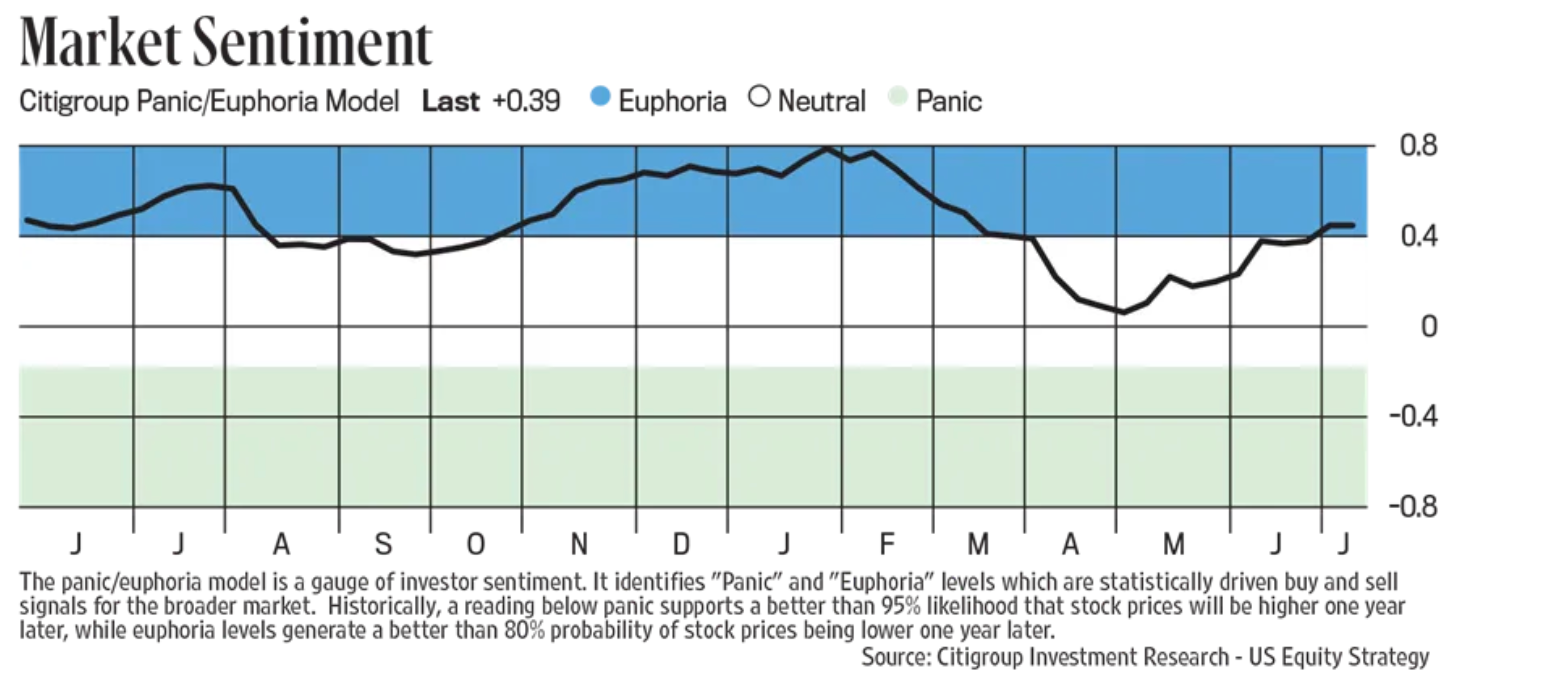

There has been one thing missing from this rally off the April lows and that's been much bullish exuberance, which itself is a positive from a contrarian perspective, something I mentioned a few weeks ago. That though has changed as all the sentiment indicators I look at are now pretty bulled up. Nothing extreme but now getting stretched.

Investors Intelligence jumped to 51 from 38.8 while Bears fell to 21.6 from 28.6, both rather large one week moves for each in this survey. The Bull/Bear spread in the weekly AAII survey moved to the highest since January as Bulls rose 9.9 pts w/o/w to 45, the most since mid December. This surpassed Bears which came in at 33.1, down 7.2 pts w/o/w to the least since late January.

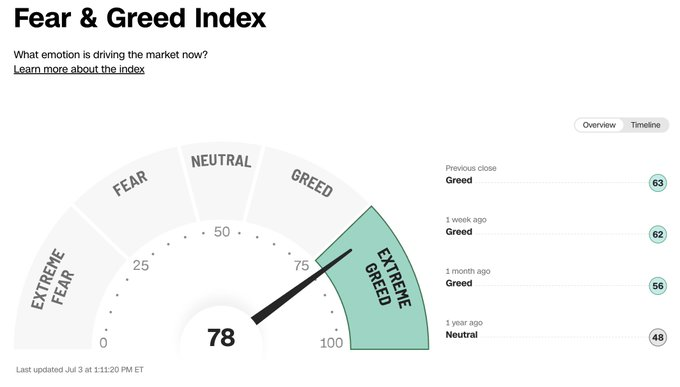

The National Association of Active Investment Managers Exposure Index popped to 99.3 with it rarely going above 100. That's the highest print for this gauge since July 2024. The CNN Fear/Greed index moved into the 'Extreme Greed' lane at 78 vs 63 one week ago. Lastly, the Citi Panic/Euphoria index is back in Euphoria.

Bottom line, as stated there is nothing extreme yet but we're now finally getting giddy and from a contrarian view, it's worth taking note in the short term.

AAII Bulls

NAAIM Exposure Index

Citi Panic/Euphoria Index

If there is one thing the Vietnam trade deal did (outside of raise the cost of our imports from them to 30% which includes the base line 10%), it raises the chances that instead of a fresh 10% across the board tariff, the blended rate will likely be higher. To put numbers around this again, we import about $3.3 Trillion of goods so a 10% blanket tariff would cost $330b. If the average number is going to be something like 15% instead, then we're talking about $500b. For perspective, the US government takes in about $525b of corporate income taxes so we're essentially doubling the rate from the current 21%. As a fan of lower taxes, particularly the 2017 cut in the corporate rate to 21%, I hope you can understand my displeasure with tariffs. Yes, exporters to us will eat some of it but with the weaker dollar, it won't be much.

For those who think we won't see any noticeable rise in tariff induced consumer inflation because it hasn't shown up in yet in CPI, even though it has showed up in import prices and core PPI, a story in Nikkei News last week said "Nearly three months since the US imposed a 25% tariff on automobile imports, Japanese carmakers are starting to raise prices and preparing to boost American production. Toyota has decided to increase vehicle sales prices in the US by an average of $270 from July. The company said it made the decision based on the announcements of price hikes by a number of competitors, as well as market trends."

"Japanese automakers kept prices unchanged at first after the tariffs were imposed. But Subaru and Mitsubishi Motors have since raised them, while Mazda Motor is exploring doing so. They have little choice but to raise prices, having reached their limit in absorbing cost increases."

Tariffs yes can be a one time price change but tell that to the person who needs to buy a car right now. Also, if all of this mucks up supply chains for the next few years and limits the new production of things, maybe it is more than just a one time text book price adjustment.

With respect to the BBBill, the biggest fiscal stimulant is certainly the accelerated expensing opportunities for plant and equipment and R&D investments. As CapEx ex Gen AI has been flattish for the past few years, we hope for a lift and see how companies balance this with the tariffs they are absorbing. Keep in mind, building a factory right now is more expensive because of steel and aluminum tariffs and guess who we receive much of our industrial equipment that goes into US factories, China, Vietnam and some others. The extension of current income tax rates is just more of the same, but certainly better than having them expire. No taxes levied on tips and overtime seen to 'clock out' above low income thresholds so it seems like only a modest economic stimulant.

On the government spending side, it seems that anything noticeable in terms of slowing its pace doesn't kick in until 2027 with the Medicaid changes. The DOGE related cuts of about $150b per year are something but not much in the context of annual federal government spending of about $7t and that is only going higher in the coming years.

As it is hard to find one bull on the price of oil, outside of myself and only a few others, I'm going to continue to point out the falling US rig count as drillers try to offset the OPEC supply increases, in terms of the global equilibrium. The weekly US crude oil rig count fell for the 10th straight week and by another 7 rigs to just 425. For perspective, we started the year at 483 and now sit at the least since September 2021.

Also out last week was the fresh Dallas Fed Oil & Gas Survey. It said, "Oil and gas production decreased slightly in the second quarter, according to executives at exploration and production firms. The oil production index fell from 5.6 in the first quarter to -8.9 in the second quarter. Meanwhile, the natural gas production index also turned negative, declining from 4.8 to -4.5."

Here were some of the noteworthy E&P company comments:

"The Liberation Day chaos and tariff antics have harmed the domestic energy industry. Drill, baby, drill will not happen with this level of volatility. Companies will continue to lay down rigs and frack spreads."

"There is constant noise coming from the administration saying $50-per-barrel oil is the target. Everyone should understand that $50 is not a sustainable price for oil. It needs to be mid $60s."

"Increased steel costs and other costs for drilling wells are affecting our business. The increased costs change the production economics."

"The current political uncertainty is causing apprehension and concern about small, independent oil and gas companies’ economic viability."

"Thank God the previous administration is gone and so are their anti-energy policies!"

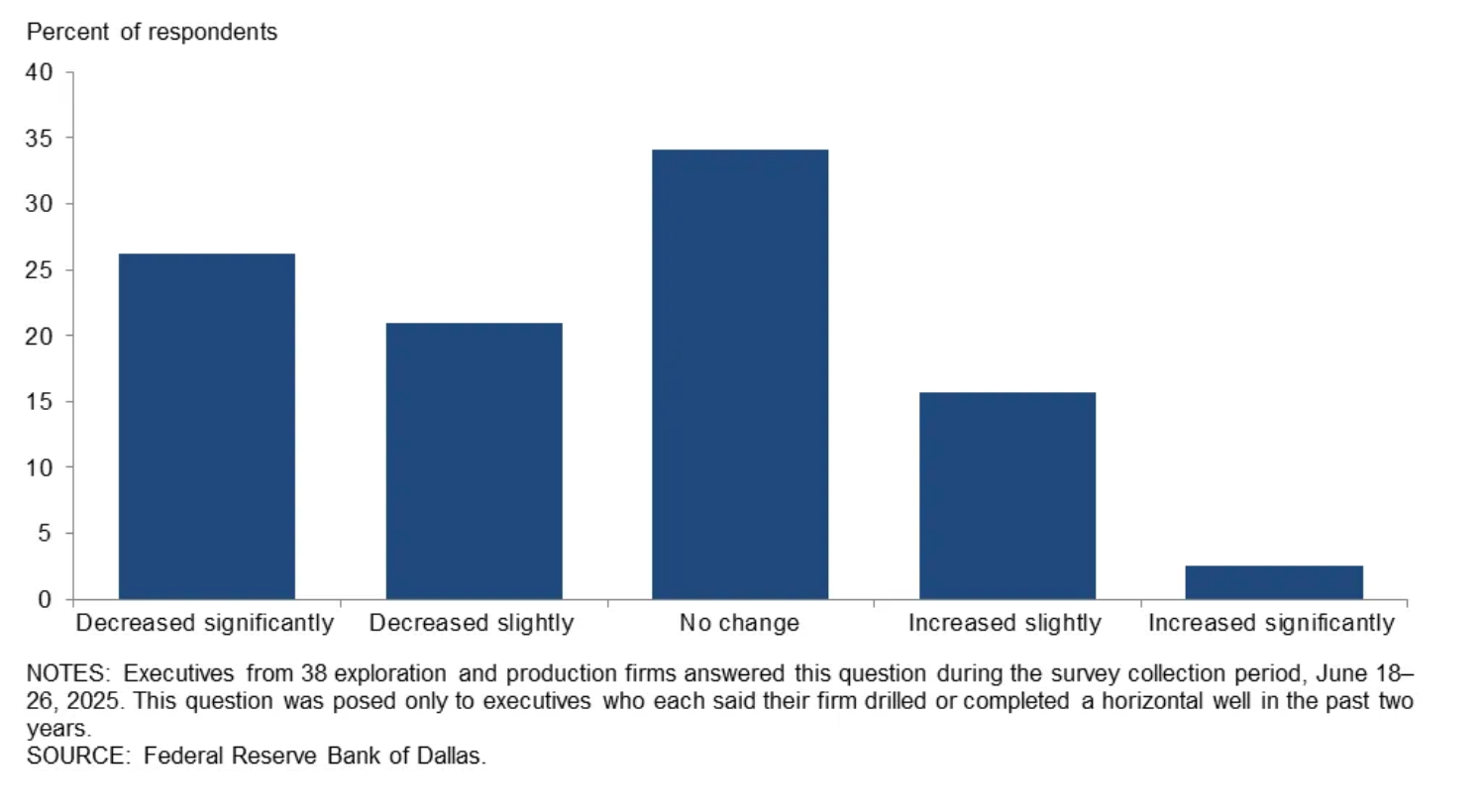

There were also a few special questions and here was one of them, "How has the number of wells your firm expects to drill in 2025 changed since the start of the year?" The answer, "Almost half of executives surveyed expect to drill fewer wells in 2025 than they planned at the start of the year. Twenty-six percent said they expect the number of wells they drill to 'decrease significantly,' and 21% said it would 'decrease slightly.' Conversely, 16% said drilling expectations 'increased slightly' and 3% said they 'increased significantly.' The balance saw no change.

Crude Oil Rig Count

Answers to the drilling question

One of my go to earnings calls on the industrial/manufacturing sector of the US economy outside of Fastenal is MSC Industrial who reported earnings last week. From them of note:

"conditions in our manufacturing end markets remain subdued. Most of our primary end markets remain soft, including automotive and fabricated metals, which continue to contract as reflected in the industrial production index."

"Aerospace remains a bright spot, with continued growth and a strong outlook. The more broad based softness we're seeing is reflected in sentiment readings such as in the MBI (Metalworking Business Index). After turning positive in March for the first time in nearly two years, MBI readings returned to negative numbers in April and May, reflecting customer caution around tariffs and general uncertainty. And we saw this reflected in our own sales numbers."

"We experienced a soft April that went beyond Easter timing. Conversations in the field suggest that our customers took a temporary pause in activity as they contemplated the impact of tariffs on their business. While this short lull in activity was followed by improving trends in May and those that continued into June, there remains hesitancy and caution among our customer base around future production levels."

BY Doug Kass · Jul 7, 2025, 9:00 AM EDT

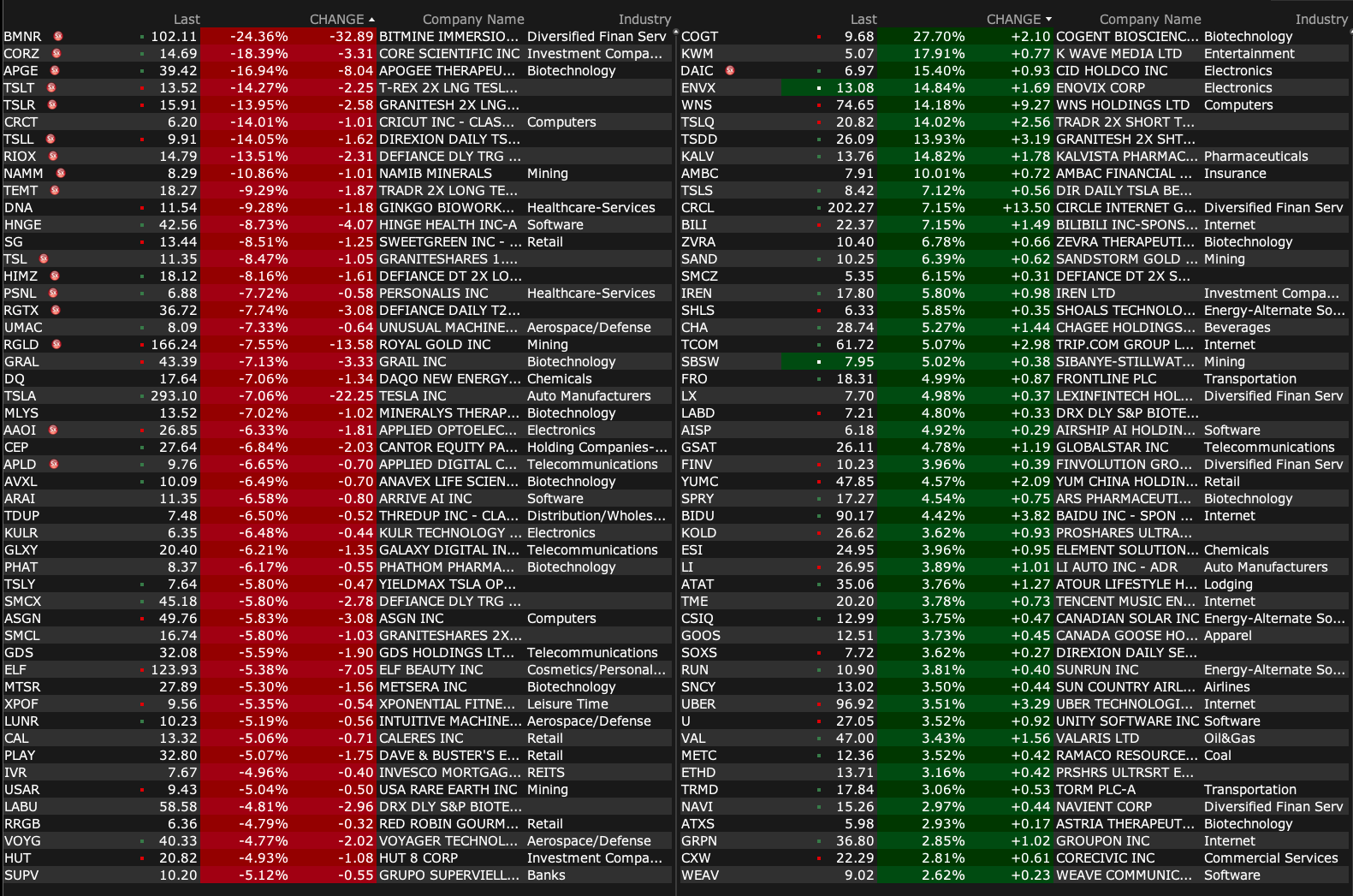

-NAK +28% (provides update on negotiations with EPA)

-COGT +17% (announces positive top-line results achieving statistical significance across all primary and key secondary endpoints from the summit trial of Bezuclastinib in patients with non-advanced systemic mastocytosis)

-KALV +16% (US FDA Approves EKTERLY (sebetralstat), oral on-demand treatment for Hereditary Angioedema; will launch EKTERLY in the U.S. immediately)

-APGE +15% (to host call to report Part A 16-Week Data from the Phase 2 APEX Trial of APG777 in Patients with Moderate-to-Severe Atopic Dermatitis on July 7, 2025; APEX Part A met all primary and key secondary endpoints)

-WNS +14% (to be acquired by Capgemini for $76.50/shr in $3.3B deal)

-SAND +9.4% (Royal Gold to acquire Sandstorm Gold)

-GEO +6.8% (detention center funding passes)

-CXW +6.1% (detention center funding passes)

-RKLB +3.8% (momentum)

-COLL +3.6% (announces $150M share repurchase program)

-PAHC +3.6% (JPMorgan Chase and Co Raised PAHC to Overweight from Neutral, price target: $35)

-SHLS +3.2% (Jefferies Raised SHLS to Buy from Hold, price target: $7.20)

-TCOM +3.0% (MakeMyTrip will pay approximately $3B to repurchase a portion of its Class B ordinary shares from Trip.com)

-DNLI +2.1% (announces FDA Acceptance and Priority Review of Biologics License Application (BLA) for Tividenofusp Alfa for Hunter Syndrome (MPS II))

-JSPR -71% (provides clinical data update from Briquilimab Studies in Chronic Spontaneous Urticaria)

-BULL -8.9% (announces $1B Standby Equity Agreement with Yorkville Advisors)

-TSLA -6.6% (CEO Elon Musk confirming he will form the "America Party" as a third party in US politics; William Blair Cuts TSLA to Market Perform from Outperform)

-STLA -3.8% (broker downgrade)

-RGLD -3.3% (to acquire Sandstorm Gold and Horizon Copper)

-RBLX -2.5% (profit-taking following recent strength)

BY Doug Kass · Jul 7, 2025, 8:36 AM EDT

Chart from 8:13 a.m. ET:

BY Doug Kass · Jul 7, 2025, 8:18 AM EDT

BY Doug Kass · Jul 7, 2025, 7:55 AM EDT

BY Doug Kass · Jul 7, 2025, 7:45 AM EDT

Professor Galloway's No Mercy No Malice... "The Grown Up Tax Bill"

BY Doug Kass · Jul 7, 2025, 7:30 AM EDT

I am offering more ARKK and HOOD in premarket.

BY Doug Kass · Jul 7, 2025, 7:12 AM EDT

BY Doug Kass · Jul 7, 2025, 7:00 AM EDT

From JPMorgan:

US: Futs are weaker as we head into the July 9 deadline which appears to have been rolled to Aug 1. Trump said either a deal will be done, or a country will get a letter; 12 letters are set to be sent today. Anyone aligning with BRICS ‘Anti-American’ stance is subject to an add’l 10% tariff. OPEC+ did another supply hike, this time for 548k bpd. Pre-mkt, NDX/RTY are underperforming but Tech is being dragged by TSLA post Musk’s announcement of a new political party. Semis/Cyclicals under pressure. Yield curve is twisting steeper, USD stronger, and cmdtys declining (Ags, metals). This is a light macro data week into next week’s CPI and kick off to earnings season.

and...

EQUITY & MACRO NARRATIVE

This week is all about trade deals, so we share our views below and then revisit the other elements of the tactical bull case, (i) resilient macro data and (ii) positive earnings growth.

· TRADE WAR – So far, the US has an agreement with the UK, a détente with China, and a framework with Vietnam. Both Bessent and Trump have warned that a lack of agreement could reverts tariffs back to ‘Liberation Day ‘ levels, going live Aug 1; this effectively rolls the July 9 deadline to Aug 1. The US is actively trying get countries to reduce their reliance on China, triggering a warning From China not to hurt them during negotiations. My colleague Matt See has a detailed note on Trade War and the impact on APAC here. A few topics that Matt raised and some additional color:

o BASELINE TARIFFS? Is it the 10% placed on countries during the 90-day delay, also the base rate for the UK, or do we see something like 20% level for Vietnam (and 40% for transshipments)? Recent client conversations point to a level substantially less then ‘Liberation Day’ levels with some assuming 10% is the most likely outcome and others pointing to Us allies receiving higher than expected tariffs on ‘Liberation Day’ as an indicator that legacy relationship may not mean much in this trade war. Our (Mkt Intel) view is that a return to ‘Liberation Day’ levels, for the largest trading partners, is unlikely given the likelihood of an extreme move in bonds and stocks and the reactivation of the ‘Trump Put’.

o WHO HAS PRIORITY? Trump mentioned that he is sending out tariff letters to 12 countries today; the nature of the letters is the setting of tariff levels with a “take it or leave it” mandate per CNBC. Trump did not indicate which countries would receive a letter.

o ESCALATE TO DE-ESCALATE? When viewing Vietnam through the lens of US v. China, where Vietnam was one of the biggest beneficiaries of Trade War 1.0 as companies shifted supply chains from China to Vietnam pushing Vietnam to have the third largest trade imbalance with the US. Do we see the US apply similar pressure on other perceived China proxies/close trading partners? Recall, the Chinese rare earth export licenses have a 6-month lifespan so there will be more discussions before year-end. While the market has primarily focused on US / China, we could see the EU escalate in the event that a deal is not struck.

o LIBERATION DAY 2.0? We do not think so. A failure to sign a number of deals this week and a reversion to ‘Liberation Day’ levels would be a worst case scenario for risk assets. The SPX fell 12.6% over the four trading sessions post ‘Liberation Day’ as the 10Y yield increased from 4.13% to 4.29% over the same time period before increasing to 4.49% over the next three sessions. Longer-term, investors will be concerned with the total effective tariff rate which is 13.1% based on analysis by Mike Feroli and team (Vietnam deal would increase it from 13.1% to 13.4%).

o US MKT INTEL THOUGHTS ON TRADE – For us the keys are the EU and Japan given China’s 90-day deadline expires on Aug 12. Canada and Mexico may score some exemptions but think full renegotiation of USMCA (aka NAFTA 2.0) will be more critical than any framework achieved this month. As stated, we do not think we see a reversion to ‘Liberation Day’ levels though Trump may choose to make an example of a country to force the hands of other countries. In any case, we do think you see an increase on volatility this week potentially with a pullback but ultimately would buy that dip. Regarding the strike of the ‘Trump Put’, we think it likely that a 3-5% pullback in stocks would activate that, especially if that move happened over one or two sessions but think a spike to bond yields would trigger a faster reaction, e.g. 10Y yield moving back above 4.50% (closed at 4.35% on July 3).

BY Doug Kass · Jul 7, 2025, 6:45 AM EDT

* The Musk/Trump romance was short lived — as I predicted in my "15 Surprises for 2025"

* DOGE, drugs and Rock and Roll...and a new political party planned by Elon Musk

"Surprise #2: The "other" romance, between Trump/Musk, doesn't make it past Spring 2025.

Reading the room (and increasingly uncomfortable with Musk's nororiety), President Trump begins to be openly critical of Musk and finally abandons him entirely.

Musk lashes out and retaliates by forming his own party and has a nervous breakdown.

Separately, Tesla makes little progress in "full self driving." The U.S. government takes away the $7,500 tax credit, competition from China intensifies, unit sales drop by double digits and Tesla's profits collapse. In addition, an "accounting issue" (related to warranties) is uncovered by a short-oriented research boutique. All these factors cause the shares of (TSLA) to drop to $100/share. Reading the room (and increasingly uncomfortable with Musk's notoriety), President Trump begins to be openly critical of Musk and finally abandons him entirely.

- My 15 Surprises for 2025, Kass Diary

After the falling out with President Trump, Elon Musk has announced the creation of a new political party (The America Party) over the weekend.

Here is a repost of my June 2025 column which expanded on my expectation of a Trump/Musk fissure (initially written back in December):

Remember when you held me tight

And you kissed me all through the night

Think of all that we've been through

And breaking up is hard to do

- Neil Sedaka, "Breaking Up Is Hard To Do"

Here was my Surprise #2 in my 15 Surprises for 2025:

Surprise #2: The "other" romance, between Trump/Musk, doesn't make it past Spring 2025.

National protests and demonstrations emerge and demands from a wide array of members of both the Republican and Democratic parties (including conservatives and liberals) call for "ousting" Elon Musk, an unelected official, from playing such a dominant role in the U.S. government.

Bernie Sanders, taking the Senate's mantle of opposition to Musk, tweets about Elon Musk's and other billionaires' outsized role in the government:

"The precedent set in the last few months should upset every American who believes in our democratic form of government. In 2024, just 150 billionaire families spent almost $2 billion to purchase political candidates. Since the election in November, Elon Musk, Jeff Bezos and Mark Zuckerberg got $300 billion richer and are now worth $1 trillion combined. It appears that from now on no major legislation can be passed without the approval of Elon Musk, the wealthiest person in our country. That's not Democracy, it's Oligarchy. We must fight for an economy that works for all, not just the few. Elon Musk is an unelected official that is essentially acting as the President of the United States. We must pass legislation that changes this!"

Funded by George Soros, the law firm Boies, Schiller & Flexner launches a suit restricting the role of unelected officials without official positions in the Administration (like Elon Musk and Vivek Ramaswamy). The suit ends up going to the Supreme Court but is unresolved by year-end.

Reading the room (and increasingly uncomfortable with Musk's notoriety), President Trump begins to be openly critical of Musk and finally abandons him entirely.

Musk lashes out and retaliates by forming his own party and has a nervous breakdown.

Separately, Tesla makes little progress in "full self driving." The U.S. government takes away the $7,500 tax credit, competition from China intensifies, unit sales drop by double digits and Tesla's profits collapse. In addition, an "accounting issue" (related to warranties) is uncovered by a short-oriented research boutique. All these factors cause the shares of (TSLA) to drop to $100/share.

Elon Musk's non-Tesla investments suffer from reduced U.S. government support.

Musk grows ever more unhinged throughout 2025 - his mother attempts a family intervention.

BY Doug Kass · Jul 7, 2025, 6:25 AM EDT

BY Doug Kass · Jul 7, 2025, 6:15 AM EDT

I will be out most of the day today and tomorrow on business meetings (research, conferences).

My posts will be less frequent and shorter.

BY Doug Kass · Jul 7, 2025, 6:02 AM EDT

The S&P Short Range Oscillator has vaulted higher the last few days and now stands in a deep overbought at 8.25% vs. 7.38%.

My net short exposure is representative of this move.

BY Doug Kass · Jul 7, 2025, 5:45 AM EDT