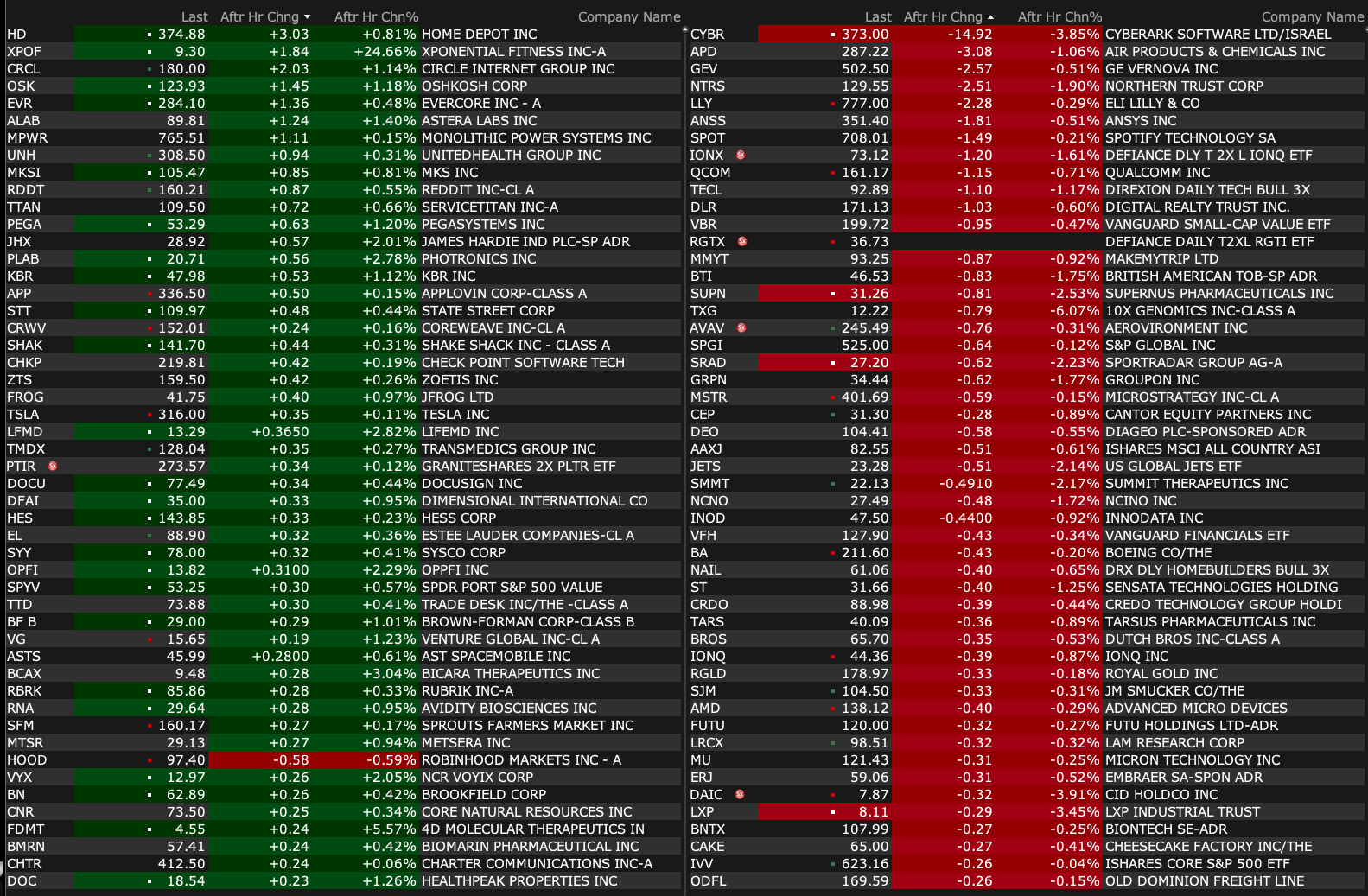

Wednesday's After-Hours Movers

At 4:15 p.m.:

BY Doug Kass · Jul 2, 2025, 4:30 PM EDT

At 4:15 p.m.:

BY Doug Kass · Jul 2, 2025, 4:30 PM EDT

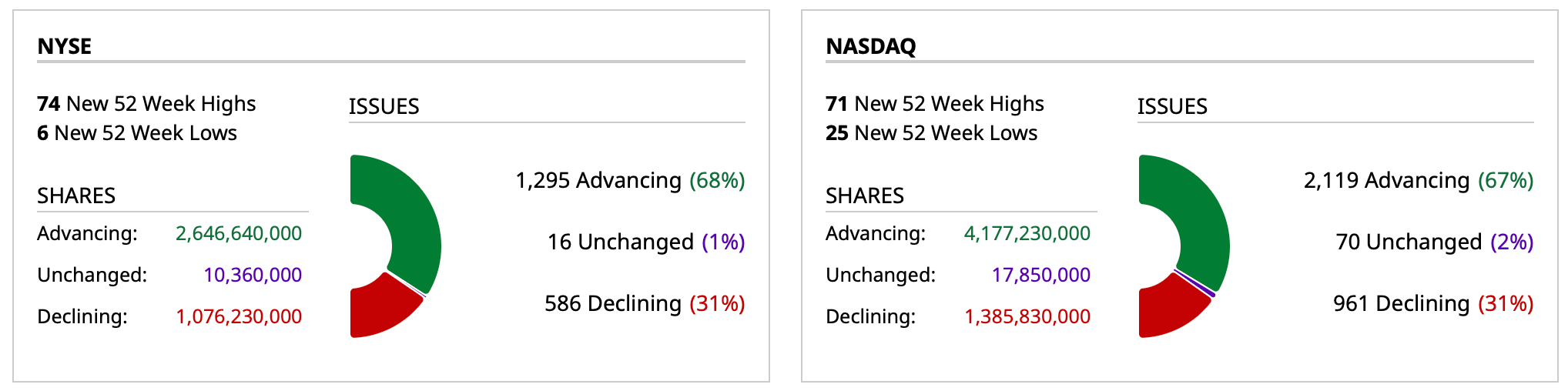

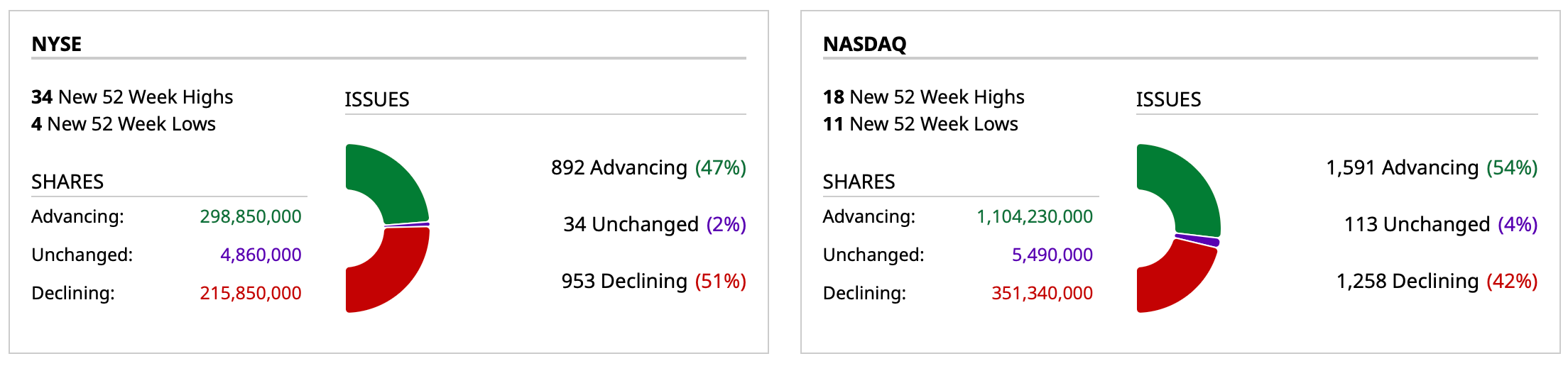

- NYSE volume 8% above its one-month average;

- NASDAQ volume 10% below its one-month average;

- VIX index: down 1.19% to 16.63

BY Doug Kass · Jul 2, 2025, 4:18 PM EDT

From Peter Boockvar:

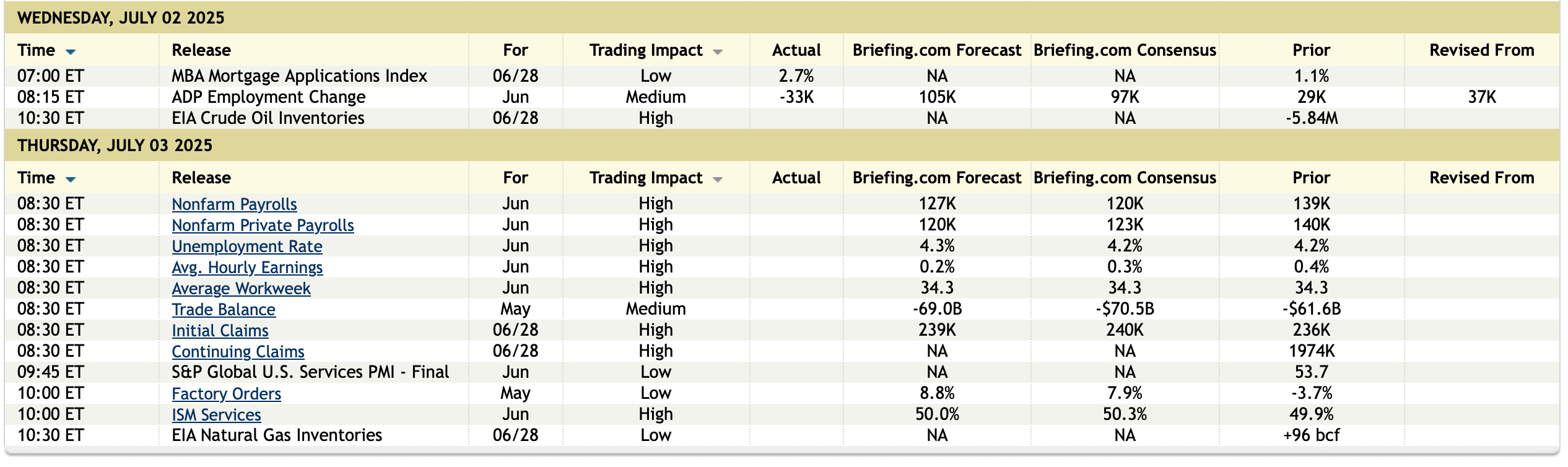

Private sector jobs lost in June according to ADP

I wasn't planning on writing this week but felt the need right now after seeing the ADP private sector jobs report. They said 33k jobs were shed in June, well worse than the estimate of an increase of 98k and follows a job gain of just 29k in May (revised down from the initial 37k print).

Again it was small business that drove the firing's with companies sized between 1-19 employees laying off a net 29k and those between 20 and 29 people shedding 18k. It spread though to medium sized businesses as those with 250-499 employees lost 27k of them while those between 50 and 249 added just 12k. Large businesses added 30k.

Industry wise, jobs were lost in the usually consistent job gainer of education/health services while those in professional/business services lost 56k and financial services cut 14k jobs. Job gains were driven by leisure/hospitality, trade/transportation/utilities, information and other.

Wage gains though remain pretty good with 'job stayer' pay rising by 4.4% y/o/y and 'job changers' seeing wage growth of 6.8% y/o/y.

The bottom line from ADP, "Though layoffs continue to be rare, a hesitancy to hire and a reluctance to replace departing workers led to job losses last month. Still, the slowdown in hiring has yet to disrupt pay growth."

My bottom line is this, if we take the Atlanta Fed's current GDP Q2 estimate of 2.5% growth, which is about in line with some other private sector forecasts I've seen and combine it with the Q1 print of a contraction of .5%, you get an average first half 2025 growth rate of just 1%. That helps to smooth out the lumpiness in trade that tariffs caused.

Remember when 1% was knocking on the door of a recession? Now for some reason the current economic environment has been referred to by some as solid and resilient. I'll say again, a blanket 10% tariff on all incoming imports of goods just loaded about $330b of fresh taxes on American importers (yes, some are absorbed by the exporter) which has the effective impact of raising the corporate income tax rate to 34% from 21%. And then of course sector specific tariffs and even higher ones on China where many small businesses still rely on for materials and product.

Lastly, I go through painstaking, time consuming work to provide all the relevant company commentary from countless earnings conference calls from a variety of different companies in many varying industries and it sure has sounded like a 1% growth economy with the only areas of growth, I'll argue again, being high end consumer spending, anything touching the Gen AI buildout and still excessive government spending. We're in a recession in manufacturing, housing and many low to middle income consumers are financially stretched. Now we have lackluster global trade and flattish CapEx excluding AI.

Companies need business visibility in taxes and policy if they are going to take the risk of hiring a new employee and tariffs, on again/off again, have just thrown mud into the gears of business activity. Hopefully eventual passage of the new budget bill will provide some help in terms of income taxes and the accelerated expense deductions on certain CapEx and R&D spending, along with those on facilities (assuming its cost effective even with higher steel and aluminum prices).

BY Doug Kass · Jul 2, 2025, 3:54 PM EDT

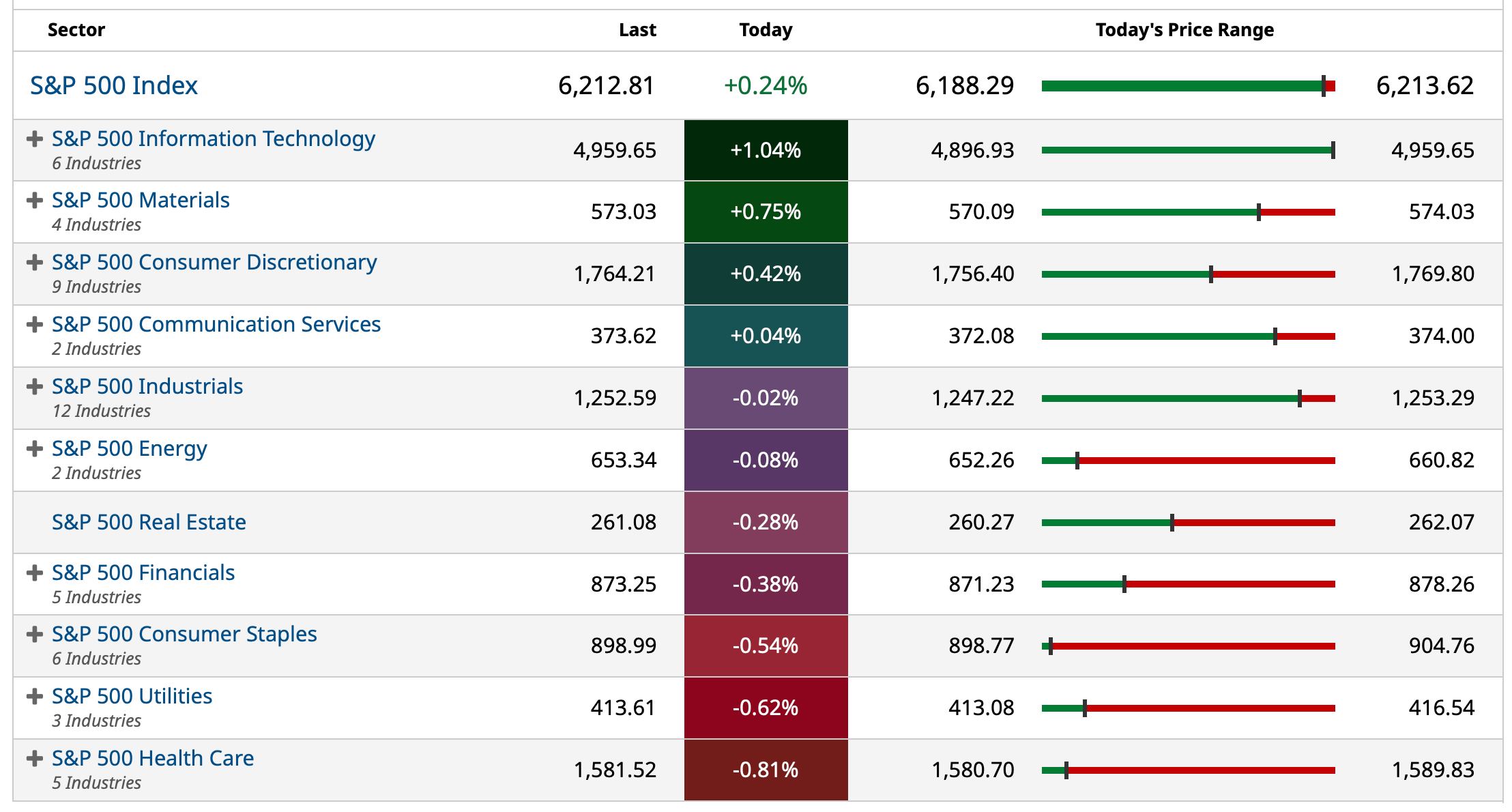

As the expression goes, this week has truly been a market of stocks — with a powerful rotation taking place.

BY Doug Kass · Jul 2, 2025, 2:44 PM EDT

Back in the office.

Getting my sea legs back.

BY Doug Kass · Jul 2, 2025, 1:33 PM EDT

- NYSE volume 2% below its one-month average;

- Nasdaq volume 13% below its one-month average;

- VIX index: down 0.42% to 16.76

BY Doug Kass · Jul 2, 2025, 11:04 AM EDT

BY Doug Kass · Jul 2, 2025, 11:00 AM EDT

Knowledge@Wharton on AI and creativity: Knowledge at Wharton

BY Doug Kass · Jul 2, 2025, 10:00 AM EDT

BY Doug Kass · Jul 2, 2025, 9:37 AM EDT

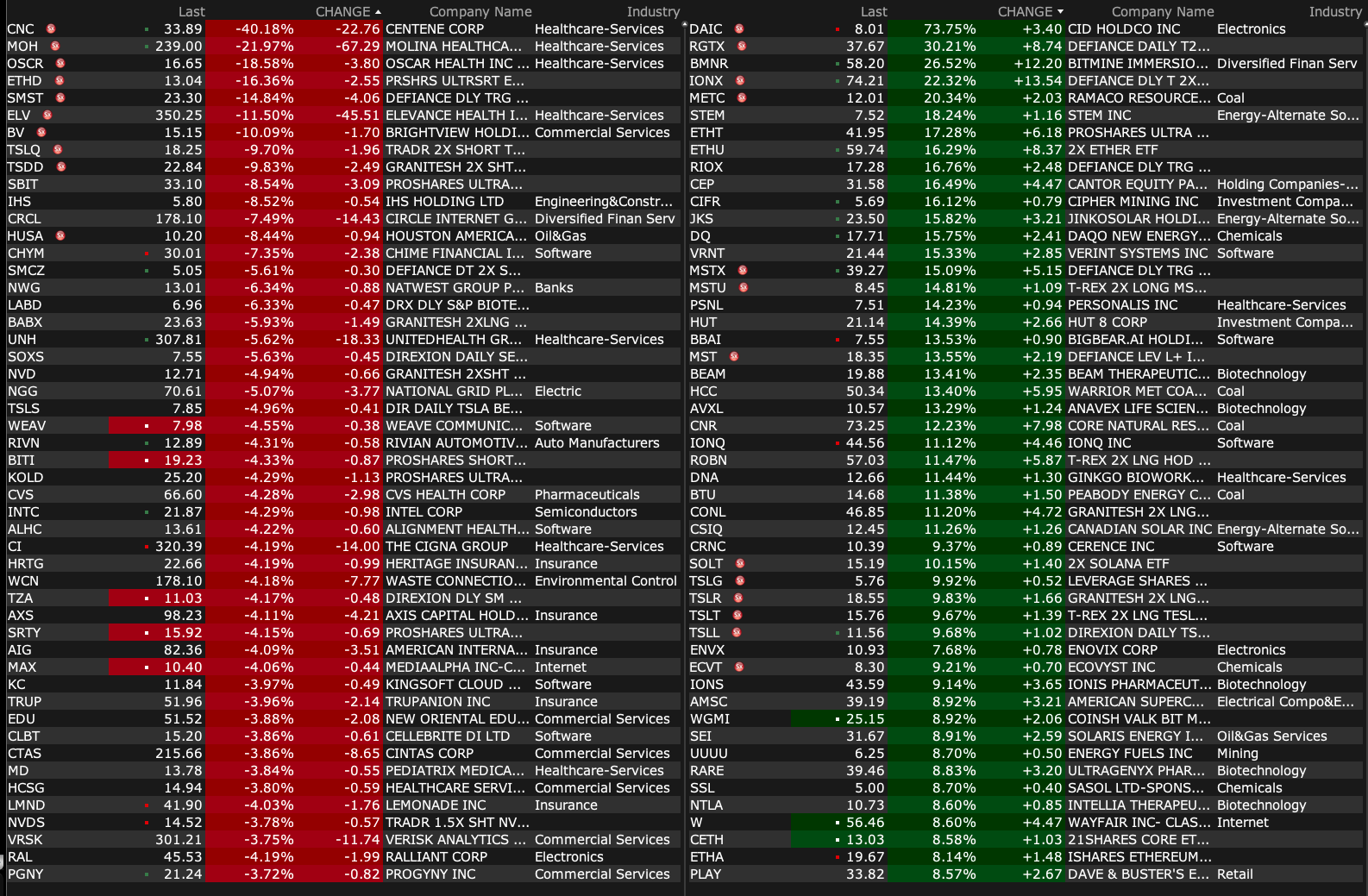

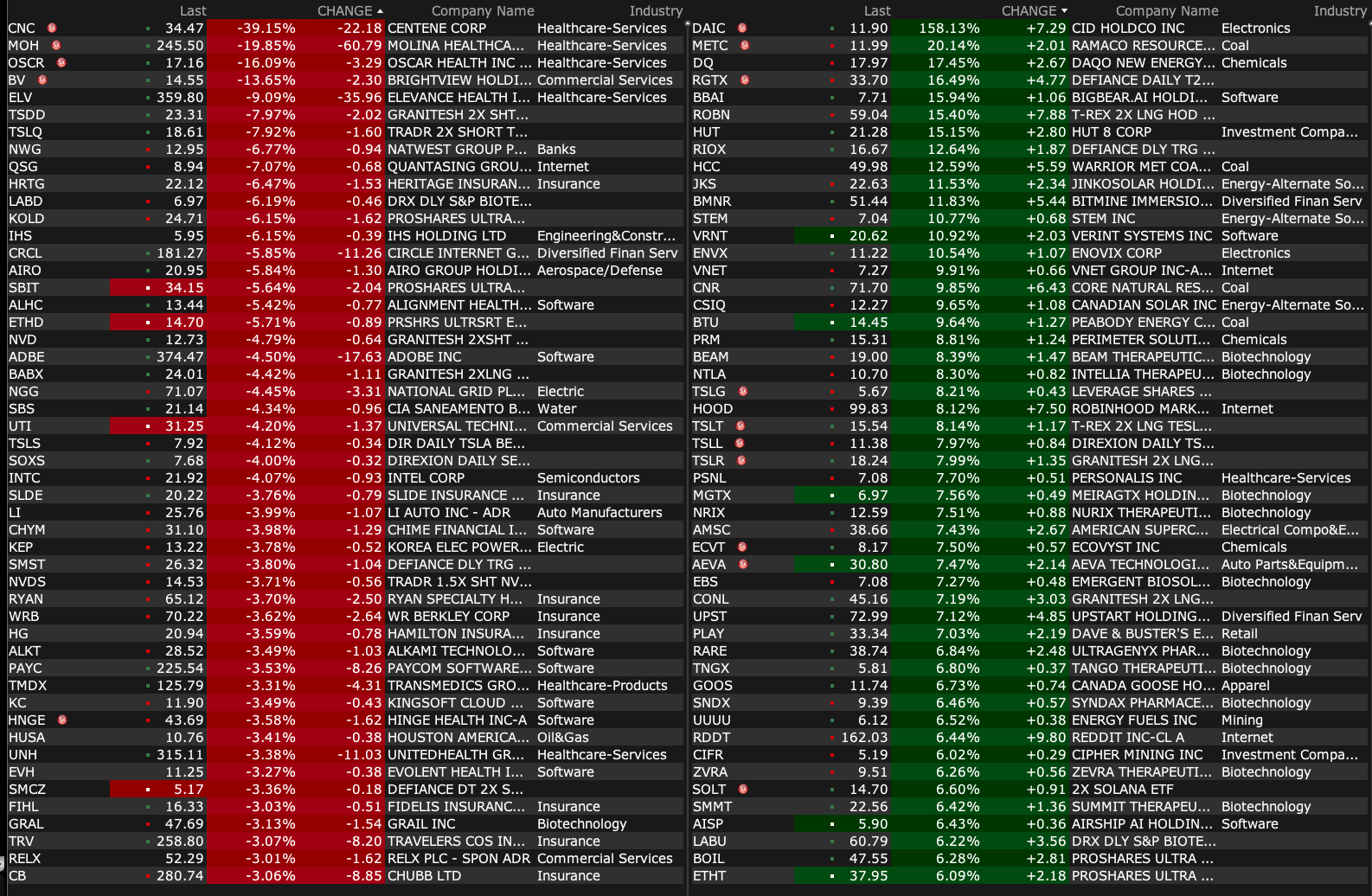

-GBX +13% (earnings, guidance)

-VRNT +7.4% (reportedly Thoma Bravo in negotiations to acquire Verint Systems)

-UNF +3.1% (earnings, guidance)

-STM +2.6% (Oddo Securities Raised STM.FR to Outperform from Neutral, price target: €32)

-PII +2.5% (announces amendment to existing Credit Agreement and full prepayment of senior notes)

-JACK +2.4% (adopts Limited Duration Stockholder Rights Plan in response to the accumulation of the Company’s stock by Biglari Capital Corp)

-ABEO +2.2% (closes sale of Rare Pediatric Disease Priority Review Voucher for $155M)

-CAVA +2.1% (Keybanc/Pacific Crest Initiates CAVA with Overweight, price target: $100)

-ROST +2.0% (Jefferies Raised ROST to Buy from Hold, price target: $150 from $135)

-CRIS -38% (announces $7M Registered Direct and Concurrent Private Placement)

-CNC -30% (withdraws FY25 EPS guidance due to worse than anticipated health marketplace data)

-MOH -12% (lower in sympathy with CNC)

-BV -11% (cuts FY25 revenue guidance)

-TTGT -9.2% (reports prelim Q1 revenue)

-ELV -3.5% (lower in sympathy with CNC)

BY Doug Kass · Jul 2, 2025, 9:15 AM EDT

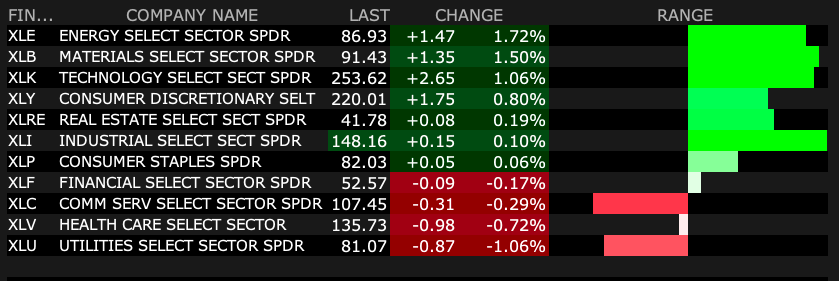

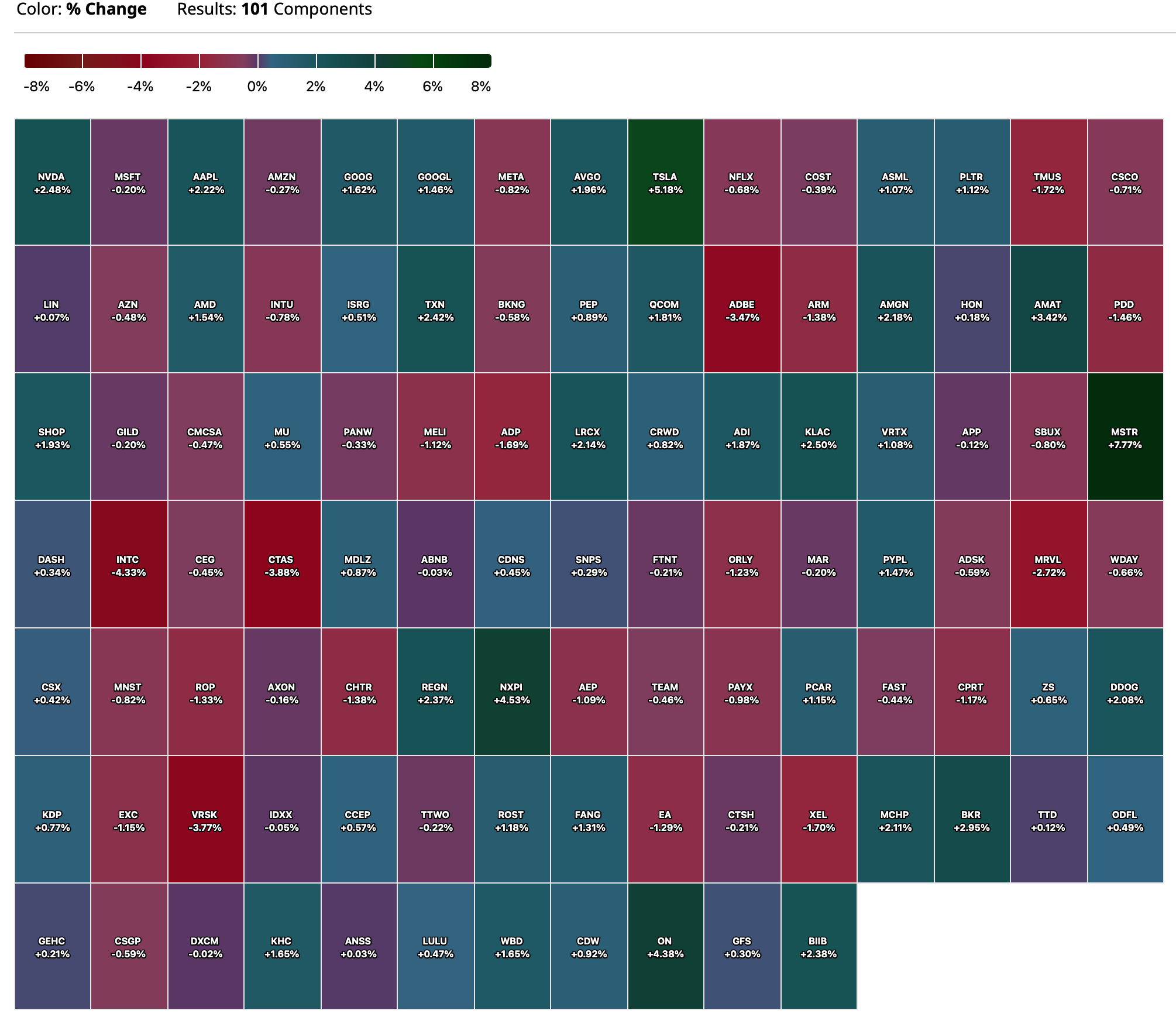

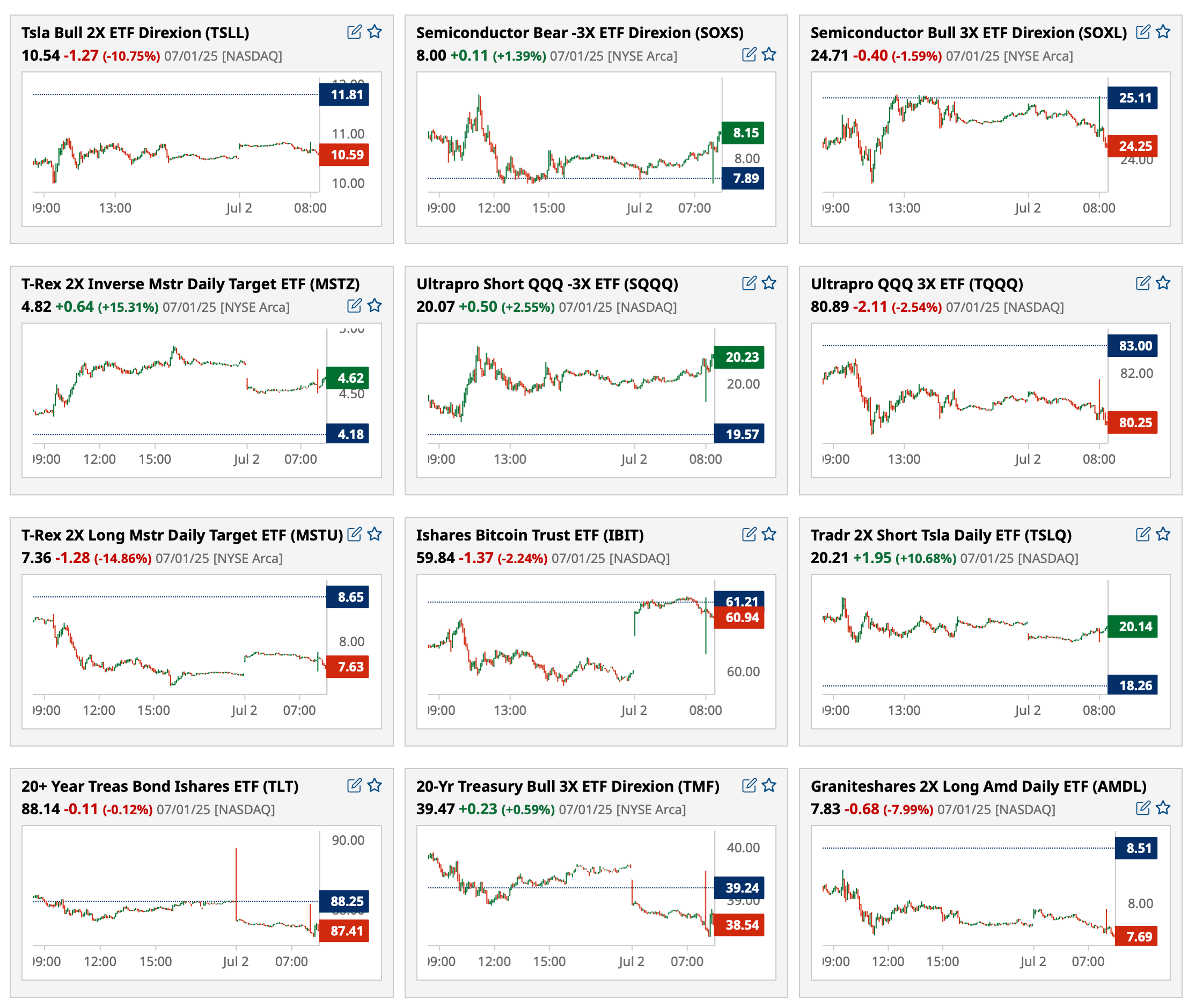

Charts from 8:24 a.m. ET:

BY Doug Kass · Jul 2, 2025, 9:00 AM EDT

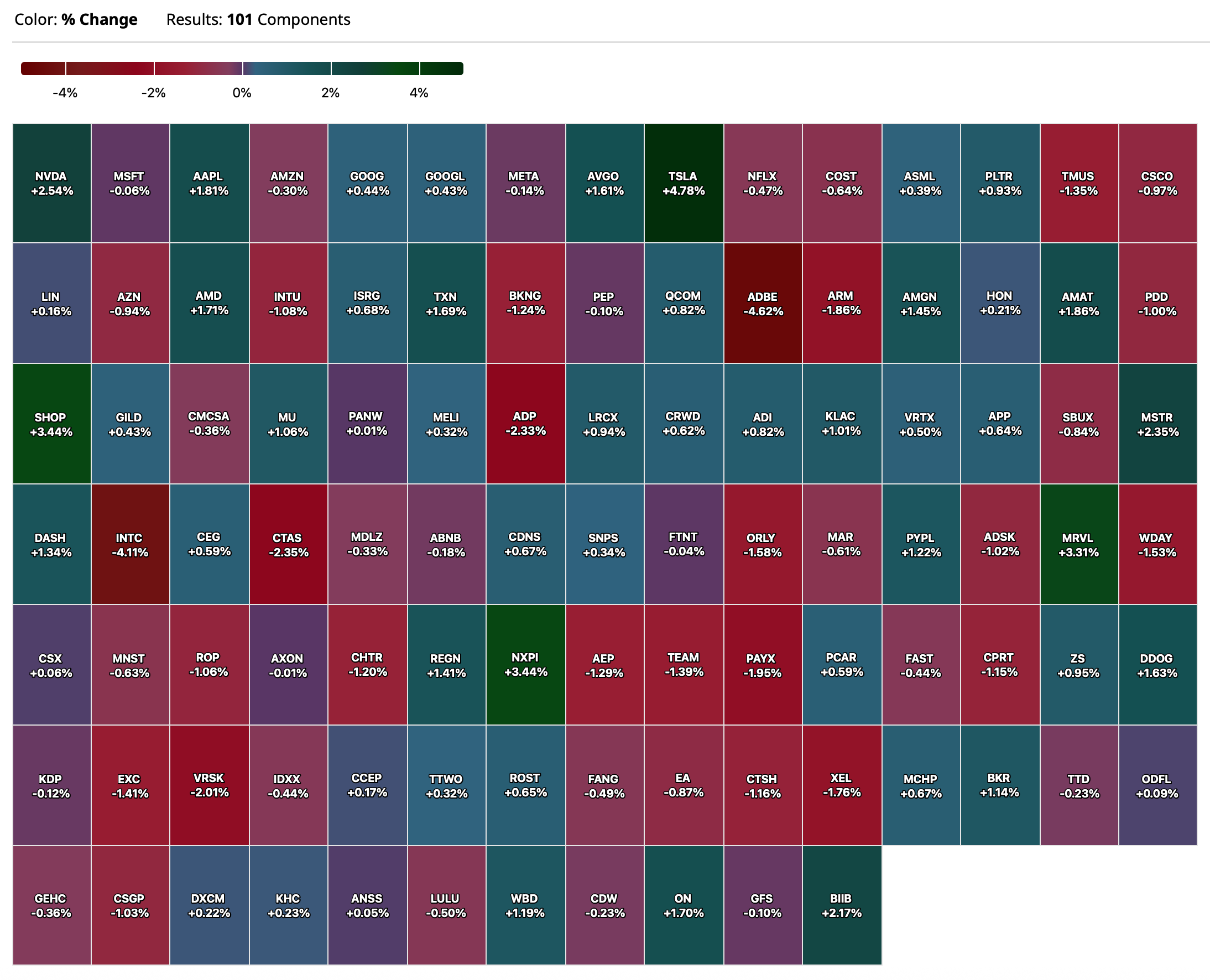

Chart from 8:22 a.m. ET:

BY Doug Kass · Jul 2, 2025, 8:45 AM EDT

11 a.m.: Fed Bank of Atlanta President Bostic (Non-Voter) gives keynote speech on U.S. monetary policy in the IMFS Distinguished Lecture Series hosted by Institute for Monetary and Financial Stability, Frankfurt, Germany (Embargoed text available. Audience Q&A expected. Livestream available)

11:30 a.m.: Treasury Hosts a $65 billion 17-Week Bill Auction

BY Doug Kass · Jul 2, 2025, 8:30 AM EDT

BY Doug Kass · Jul 2, 2025, 7:45 AM EDT

BY Doug Kass · Jul 2, 2025, 7:30 AM EDT

From JPMorgan:

US: Futs are flattish with small caps outperforming as we see signs of a Value rotation as H2 kicks off. Pre-mkt, Mag7 names are mixed on small magnitude; Cyclicals led by Financials are poised to outperform on heighted capital return. Bond yields are higher as the curve bear steepens and USD has a bid. Cmdtys are rallying across all 3 complexes. Yesterday, stocks fell into the bell on Trump comments about not extending the July 9 deadline and possibly not reaching a deal with Japan.

and...

EQUITY & MACRO NARRATIVE

Beginning with trade, Trump mentioned that he is not thinking about rolling the July 9 deadline despite earlier comments from Bessent that countries negotiating in good faith would see that deadline extended. Further, he mentioned that it is unlikely that a deal is done with Japan and that they would have to pay 30% – 35%, or more. The market sold off on the headlines but later retraced most of the losses.

Separately, the Momentum “unwind” was the primary topic in yesterday’s session. Our Momentum Index, JPMPURE Index, which is a L/S index was down more than 5% at one before closing down 4.0%, -2.9z. What triggered this? The index closed with the long leg down 1.8% and the short led squeezing 2.2%, so more squeeze induced than a cutting of long positions which aligns with things like Autos (JP1BAUT index) +4.2%, Homebuilder (XHB) +4.2%, Transports ex-Airlines (JP1BTXA Index) +3.7%, and Retailers (JP1RTL index) +3.0%. This seems less like a traditional Momentum unwind and more like position squaring into macro data this week.

We think the JOLTS and ISM-Mfg prints were a net positive, increasing the likelihood of an in line NFP print; specifically, JOLTS showed renewed hiring interest with fewer layoffs and the higher quits rate points to increased confidence people feel about switching jobs. ISM-Mfg beat headline expectations while the sub-indices missed expectations; the report’s author concluded that the economy is growing, and the report shows that the growth is accelerating. ISM-Mfg has been under 50 for the most part since late 2022 and today’s 49.0 print is the sixth reading of that level of higher since October 2022. In the final PMI-Mfg update, the report’s chief economist states:

Many client conversations point to an understanding of inflationary pressure which have yet to be fully reflected in CPI / PCE data but very few are believers in a growth reboot which could, should it materialize, propel stocks to significantly higher levels.

Lastly, the tax/budget bill passed the Senate where it is expected to find less resistance in the House. The immediate risk is to bond yields and bond vol upon passage. Longer-term, one key macro implication is the additional stress on the lowest income consumers, decreasing income 2.9% for the lowest quintile while increasing income 1.9% for the top 1%, per analysis performed by the Yale Budget Lab (full note is here). For Equities and Credit, this may create further dispersion within the Consumer sectors while potentially raising defaults across consumer loan products. Bloomberg reviews major elements of the bill here.

Today’s major macro print is ADP. Mike Feroli tells us, “The ADP estimate of private-sector employment gains has slowed significantly, rising 81k per month over the last three months vs. 148k per month in the prior year. The BLS [NFP] figures have not shown the same degree of slowdown, though downward revisions could move BLS [NFP] closer to ADP. The average absolute error on first prints or revised prints over the last year is 70-80k. While this report is not the best predictor of BLS [NFP] on a month-to-month basis, we think it is useful to see if the report continues to signal that job growth is slowing.”

BY Doug Kass · Jul 2, 2025, 7:13 AM EDT

BY Doug Kass · Jul 2, 2025, 7:03 AM EDT

BY Doug Kass · Jul 2, 2025, 6:48 AM EDT

It is worth reposting:

BY Doug Kass · Jul 2, 2025, 6:38 AM EDT

I have two research meetings this morning — outside of the office — so my posts will be less frequent and shorter.

BY Doug Kass · Jul 2, 2025, 6:28 AM EDT

BY Doug Kass · Jul 2, 2025, 6:18 AM EDT

Wolf Street howls about the CMBS markets' delinquency rates.

BY Doug Kass · Jul 2, 2025, 6:08 AM EDT

I am adding to index shorts:

* SPY $618.40

* QQQ $547.49

Long SPY puts VS QQQ VS

Short SPY common M calls VS QQQ common M calls VS

BY Doug Kass · Jul 2, 2025, 5:58 AM EDT

The S&P Short Range Oscillator climbed from 5.1% vs. 4.35% — we are in a deeper overbought.

Here is more evidence of an overbought... Officially Overbought… Again - by Frank Cappelleri

BY Doug Kass · Jul 2, 2025, 5:48 AM EDT