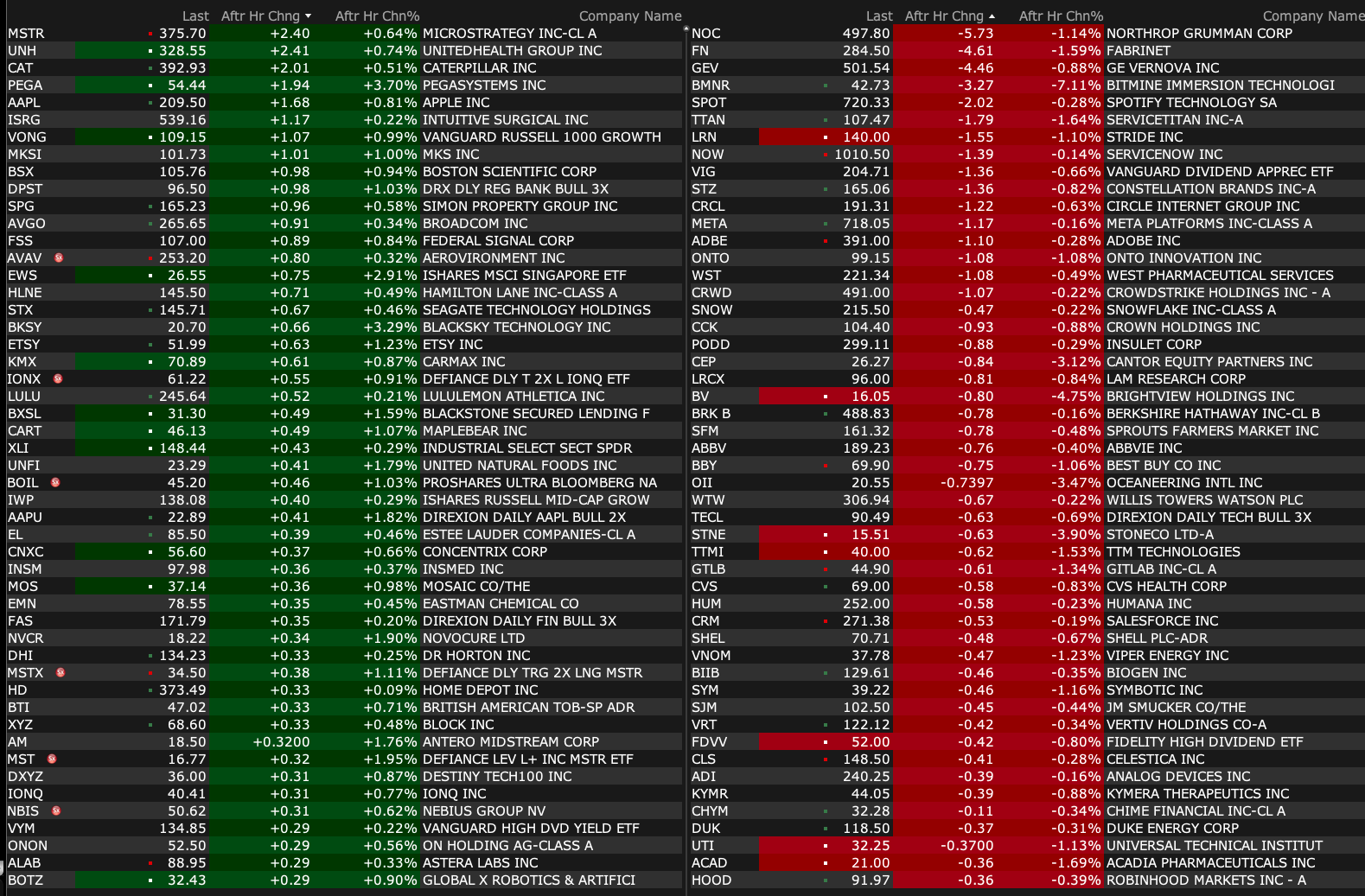

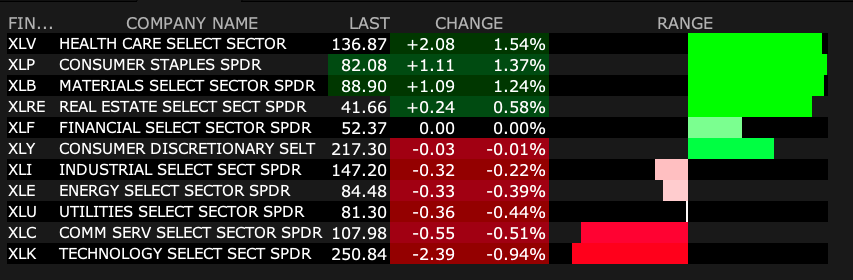

Tuesday's After-Hours Movers

As of 4:23 p.m.:

BY Doug Kass · Jul 1, 2025, 4:40 PM EDT

As of 4:23 p.m.:

BY Doug Kass · Jul 1, 2025, 4:40 PM EDT

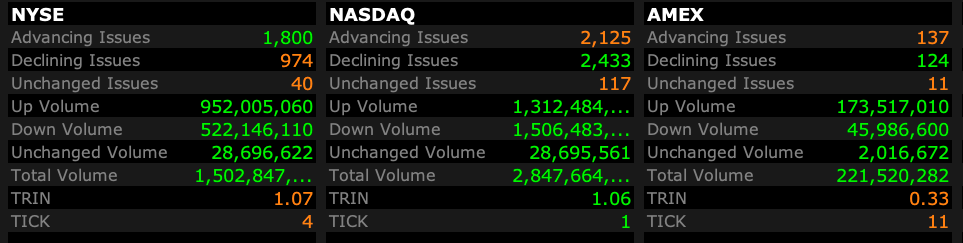

- NYSE volume 21% above its one-month average;

- NASDAQ volume 6% below its one-month average;

- VIX index: up 0.60% to 16.83

BY Doug Kass · Jul 1, 2025, 4:29 PM EDT

* July 1 is supposed to be the most bullish day of the year...

From my pal "Jazzy" Jeff Hirsch:

Almanac Trader — Most Bullish Day of Year! 1st Day July S&P 500 Up...

BY Doug Kass · Jul 1, 2025, 4:22 PM EDT

BY Doug Kass · Jul 1, 2025, 4:04 PM EDT

BY Doug Kass · Jul 1, 2025, 3:40 PM EDT

From The Credit Strategist:

BY Doug Kass · Jul 1, 2025, 3:30 PM EDT

Break in.

President Trump is not planning to extend the current tariff deadline past July 9.

He doubts whether he will make a deal with Japan: Japan could play 30%-35%.

He suspects he could have a deal with India.

BY Doug Kass · Jul 1, 2025, 3:15 PM EDT

I took a loss in most of my (very small sized) Robinhood HOOD short — it's all about risk control.

But like, Arnold, I will be back.

BY Doug Kass · Jul 1, 2025, 3:05 PM EDT

BY Doug Kass · Jul 1, 2025, 3:00 PM EDT

With S&P cash down by only one handle I am back shorting the indices:

* SPY $618.16

* QQQ $548.11

BY Doug Kass · Jul 1, 2025, 1:29 PM EDT

* I plan to short this news on any rally...

BY Doug Kass · Jul 1, 2025, 12:24 PM EDT

Both yesterday's opening missive and today's opener touched on Jim Cramer's uber-enthusiastic market view ("we are in 1996") and his argument that "new and young" investors will be a source of buying (he calculated in excess of $1 trillion!).

Jim might be correct BUT the reality for the five decades I have been watching markets is this:

The less experience you have in markets, the more likely you will be ill-prepared to tolerate downturns.

The less experience you have investing, the more likely you will panic and feed the decline.

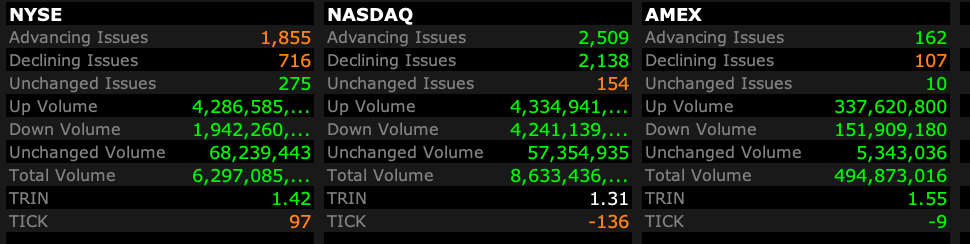

BY Doug Kass · Jul 1, 2025, 11:56 AM EDT

- NYSE volume 4% above its one-month average;

- Nasdaq volume 19% below its one-month average;

- VIX index: up 1.79 to 17.03

BY Doug Kass · Jul 1, 2025, 11:20 AM EDT

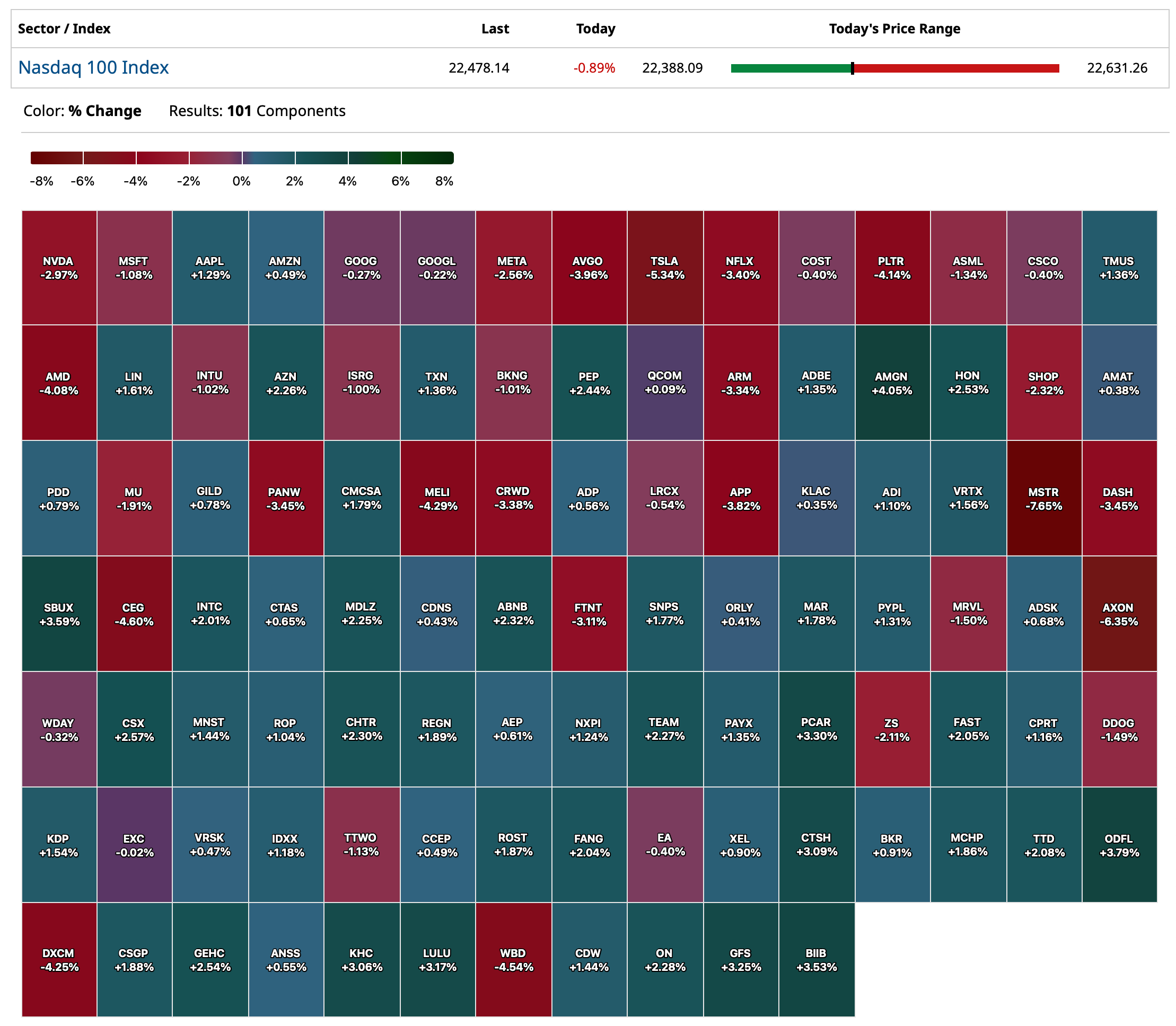

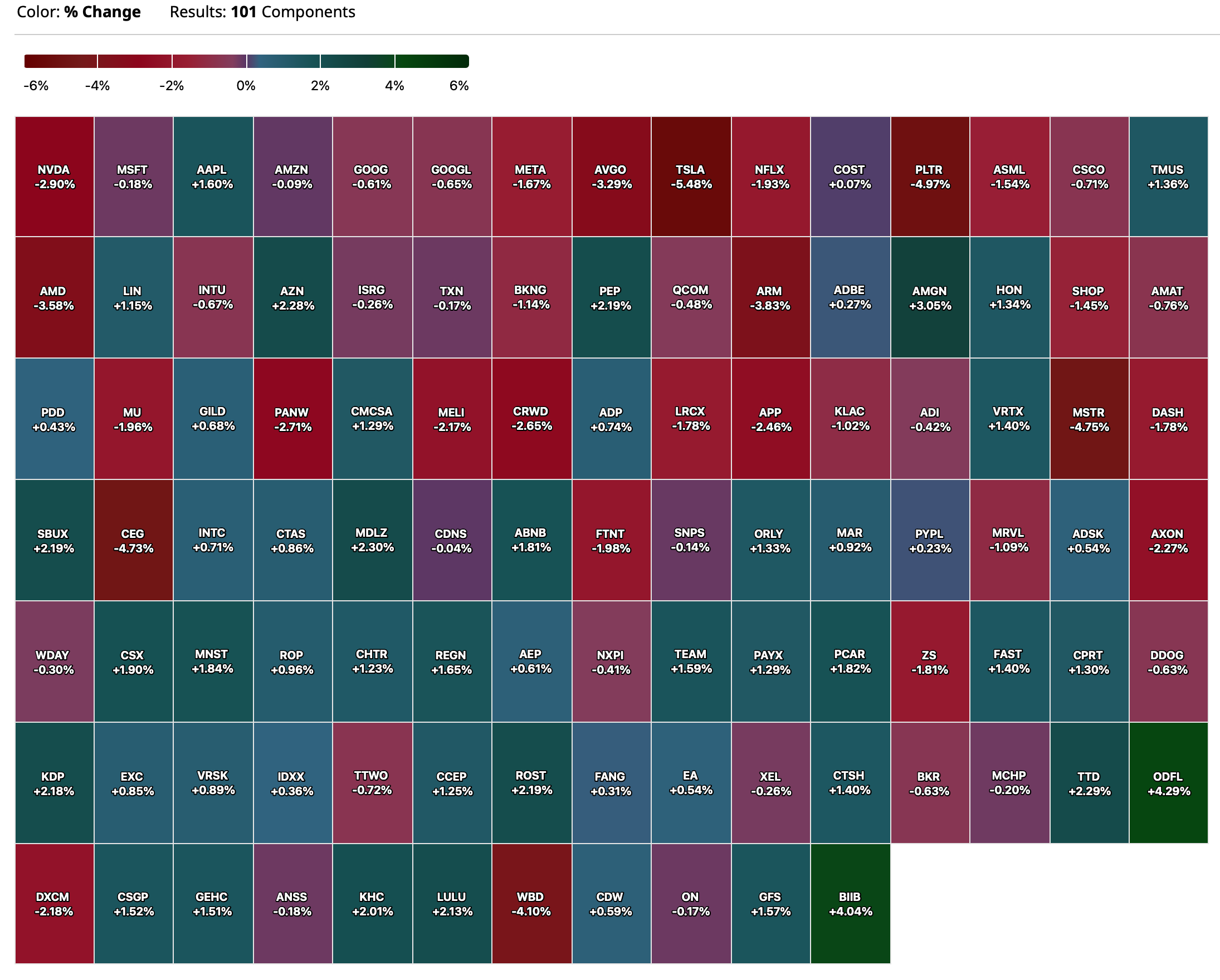

This is the first day since my Bar Mitzvah that some of the momentum stocks are succumbing to profit taking.

BY Doug Kass · Jul 1, 2025, 10:50 AM EDT

i have covered my NVDA short at $153.75 (-$4.20) for a small profit.

BY Doug Kass · Jul 1, 2025, 10:46 AM EDT

From Charlie: The Week in Charts.

BY Doug Kass · Jul 1, 2025, 10:45 AM EDT

Here are today's things:

* Added to shorts in SPY at $617.71 and QQQ $550.34.

BY Doug Kass · Jul 1, 2025, 10:25 AM EDT

“Remember, there are always two sides to every story. Understanding is a three-edged sword. Your side, their side and the truth in the middle. Get all the facts before you jump to conclusions."

- J. Michael

Investors are now almost universally bullish. However, during the past month (See The Bull Market in Complacency Is Alive and Well land Living on Wall Street) I have argued that investors are overly positive. Here is a partial list of my continuing concerns:

We face the highest geopolitical risks in many decades (which will not be resolved quickly).

We face the largest level of social and political risks in the U.S. since the Vietnam war.

We face the greatest chance of "slugflation" (slowing economic growth and sticky inflation) since the 1970s.

We face the biggest threat that the U.S. dollar and capital markets will no longer be a "safe haven" in modern history.

We face the greatest debt load and deficit ever — and neither party seems to favor any fiscal discipline whatsoever.

We face the largest capital spending spree in history (on artificial intelligence) — though the return on that investment is less certain (dot-com, it feels like deja vu all over again.) (More on this shortly.)

We face a viable alternative to equities in fixed income (for the first time in 15 years) as bonds present an equity-equivalent yield with limited risk and volatility.

Regardless of my ursine view, at the suggestion of Oaktree's Howard Marks, I have made a list of what I believe to be the most significant and now consensus bullish arguments that could continue to buoy valuations. I will follow each point with an explanation of why I differ with some of these arguments:

* There is a Fed Put: President Trump has announced that he will replace Fed Chairman Jerome Powell with a dove, leading to lower short-term interest rates.

The Fed now expects inflation to rise over the next few months, which is not an ideal setting for lower rates. A Fed Chair monitored and under the watchful eye of President Trump will likely produce a more uncertain monetary policy. I am not sure that a Fed Chair (with a committee of Board of Governors) will be as closely influenced by a Fed chief that works close or is even at the beckon call of the President. The capital markets could grow quite worried (with a dependent and not independent Fed); American Exceptionalism might be threatened with the selling of our currency and bonds, especially if the inflationary backdrop grows more problematic. Institutional credibility and independence will be challenged in a very public (and market!) way. Finally, wasn't there a lesson to be learned in 2024 when a one-percentage point cut in the Fed Funds rate produced higher intermediate and longer term Treasury and mortgage rates? If this occurred, the equity risk premium would narrow ever more (with reduced S&P profits and higher risk free interest rates).

* The current Administration is pro business and economic growth and deregulation are the cornerstones of Trump policy.

President Trump's Big Beautiful Bill incorporates the notion of spending cuts with economic incentives (skewed toward corporations and the wealthy). There could be a populist pushback in a consumer-led slowdown. Given the deteriorating state of the business and economic cycles the outcomes of pro business policy might be disappointing relative to expectations -- especially with the margin pressures of the evolution from globalism to nationalism.

* Geopolitical risks have been reduced with the recent aggressive attack against Iran's nuclear facilities.

Yes for now. But there remain potential regional hotbeds that represent bonafide threats.

* With a U.S. service economy expanding, recessions are no longer likely.

I would say recessions are not endangered. But a service economy will likely cushion the magnitude of economic downturns. This is a subject I addressed in Have Both Economic Cycles and Sentiment Surveys Become Less Relevant?. That said, AI could be threat to this theory of "stability," should a larger-than-expected displacement of jobs occur. The resumption of student loan repayments could further pressure personal expenditures. Also, as stated above, the shift from globalism to nationalism might prove to be a greater headwind to S&P earnings per share than the consensus expects.

* Corporate profits will grow steadily and above expectations over the balance of the year.

The rate of S&P EPS growth likely peaked in 1Q 2025. Who pays for higher tariffs, consumer or corporations? An estimated $400 billion of tariffs represent 20% of total corporate profits. Its a Sophie's Choice: The imposition of tariffs will likely deliver either higher inflation or lower corporate profits.

* While the budget deficit and U.S. debt load are well above expectations, they are not threats, as a rising budget/debt as a percentage of GDP has been in place for years.

DOGE failed and both sides of the political view lack fiscal discipline. I would argue that, with annual interest payments now in excess of the defense budget, we are closer to seeing the reemergence of the Bond Vigilantes than ever.

* AI will provide a fountain of corporate productivity, additive to revenues and profits.

Thus far the commercial applications and user sets of AI are minimal, though this will likely change. But, as I have also argued in "More Tales From Nvidia", it is unclear whether the trillions of dollars of capital investment (by the hyperscalers and others) will result in an adequate return on invested capital. Moreover, the AI trade started in 2023 and is almost three years old.

* Higher equities will deliver a wealth effect to the consumer and offset housing's weakness.

I agree that the consumer will benefit from a continuation of higher stock prices - but remember the S&P Index has simply returned to its late January/early February level. As to housing, the contraction is growing closer in focus and, given the disproportionate role of housing (it hits above the belt!) on consumer wealth, a drop in home prices could offset some of the wealth effect provided from the benefit from higher stock prices.

* American Exceptionalism is intact; if nothing else there is no alternative.

In Time To Rethink American Exceptionalism, I argue that the worm is turning. I agree to some extent, but I do believe that the recent trend away from investing in the U.S. will reduce domestic investments -- at the margin.

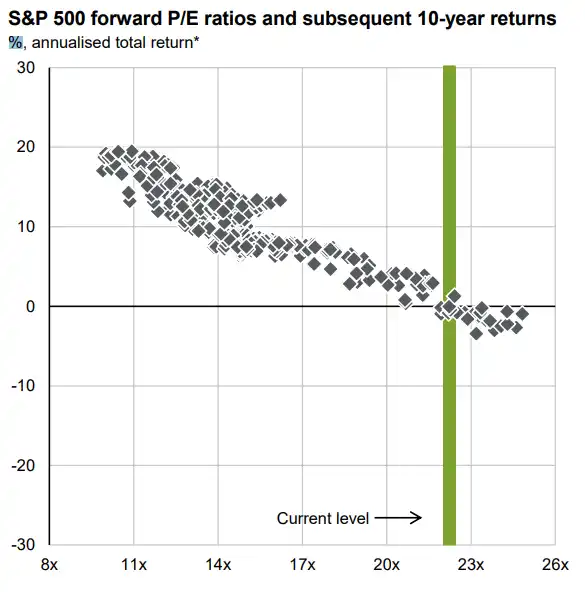

* Price earnings multiples (at 24-times) are inflated, but in past periods of speculation valuations have been even higher.

This is where I disagree strongly with the bullish cabal. Isn't this simply "the greater fool's theory," in which investors are relying on a greater fool to bale them out? This hasn't worked well in the past when valuations were excessive. As reflected in the illustration below, (historically speaking) current valuations are a poor launching point for future returns:

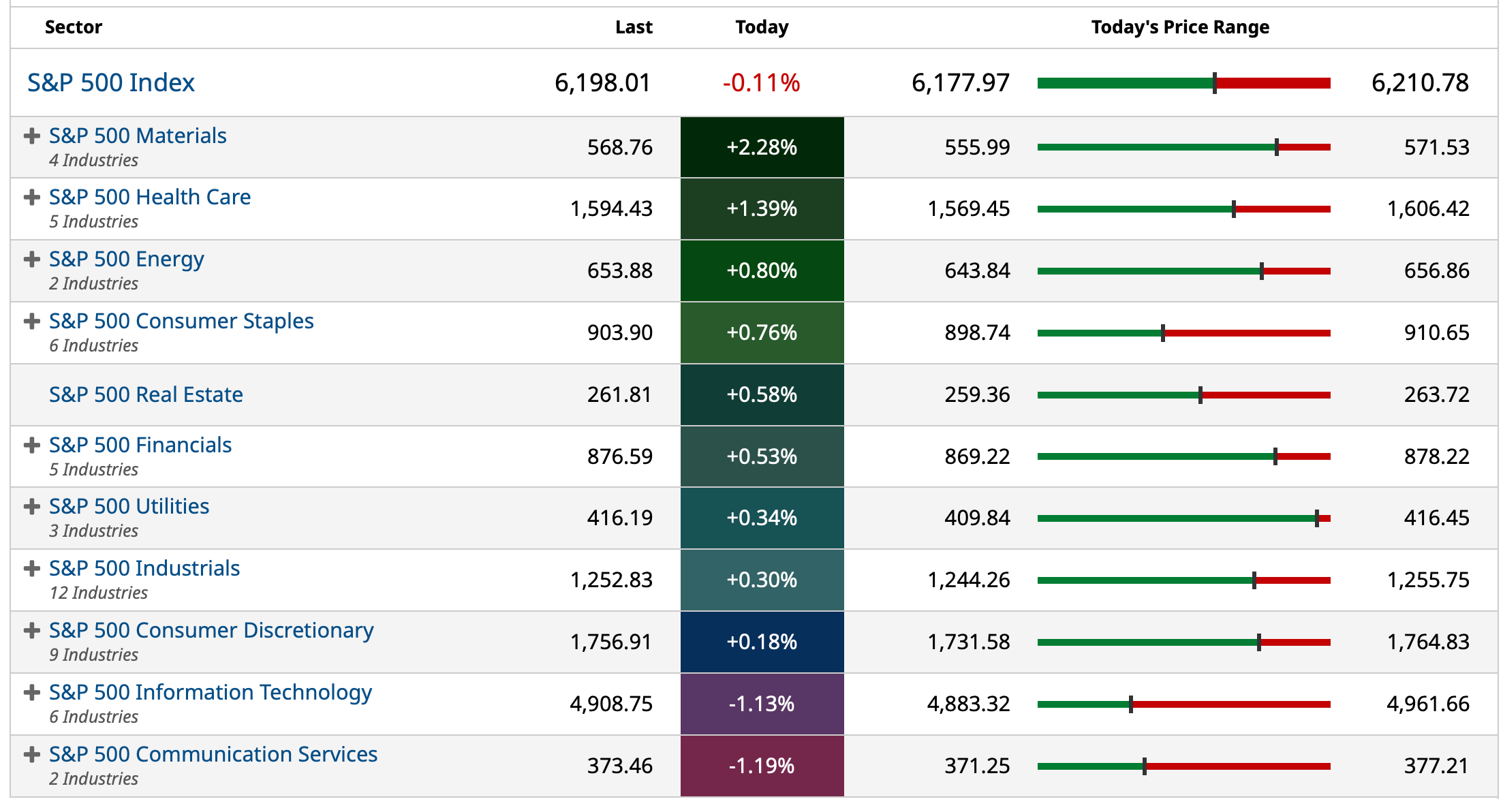

* The market's advance has been broadening out.

Yes, it has broadened out. But look at the lagging Russell Index, which has not been crowing. Let's keep a bead on market breadth in the weeks ahead.

* There is a massive build up in cash reserves that will flow back into equities.

The "cash on the sidelines" is as dumb as wood as an argument. First, cash should be looked at not in the absolute ($7 trillion), but as a percentage of stock market capitalization. As such, cash reserves are actually at the low end of history. Second, the maturation of the baby boomers suggests a lot of the cash is sticky (and being invested in equity-like returns now available in the fixed income markets).

* Market structure favors the bulls: The dominance of passive investing products and strategies has reduced "the float' of equities.

This is accurate. When combined with trillion dollar buybacks (yearly), a rising demand for stocks is being met with a diminished float. For now everyone is on the same side of of the boat. Of course, when the worm turns (and equity fund redemptions rise) -- and it will eventually -- the movie goes in reverse and there will be few buyers (I am old enough to remember when the S&P slipped to 4850 2.5 months ago as sellers overwhelmed buyers.

* There is a new generation of investors and speculators that will buoy equities.

(This is Jim Cramer's argument). As I explain the speculation may be more likely to end poorly than being sustained as Jim suggests.

BY Doug Kass · Jul 1, 2025, 9:35 AM EDT

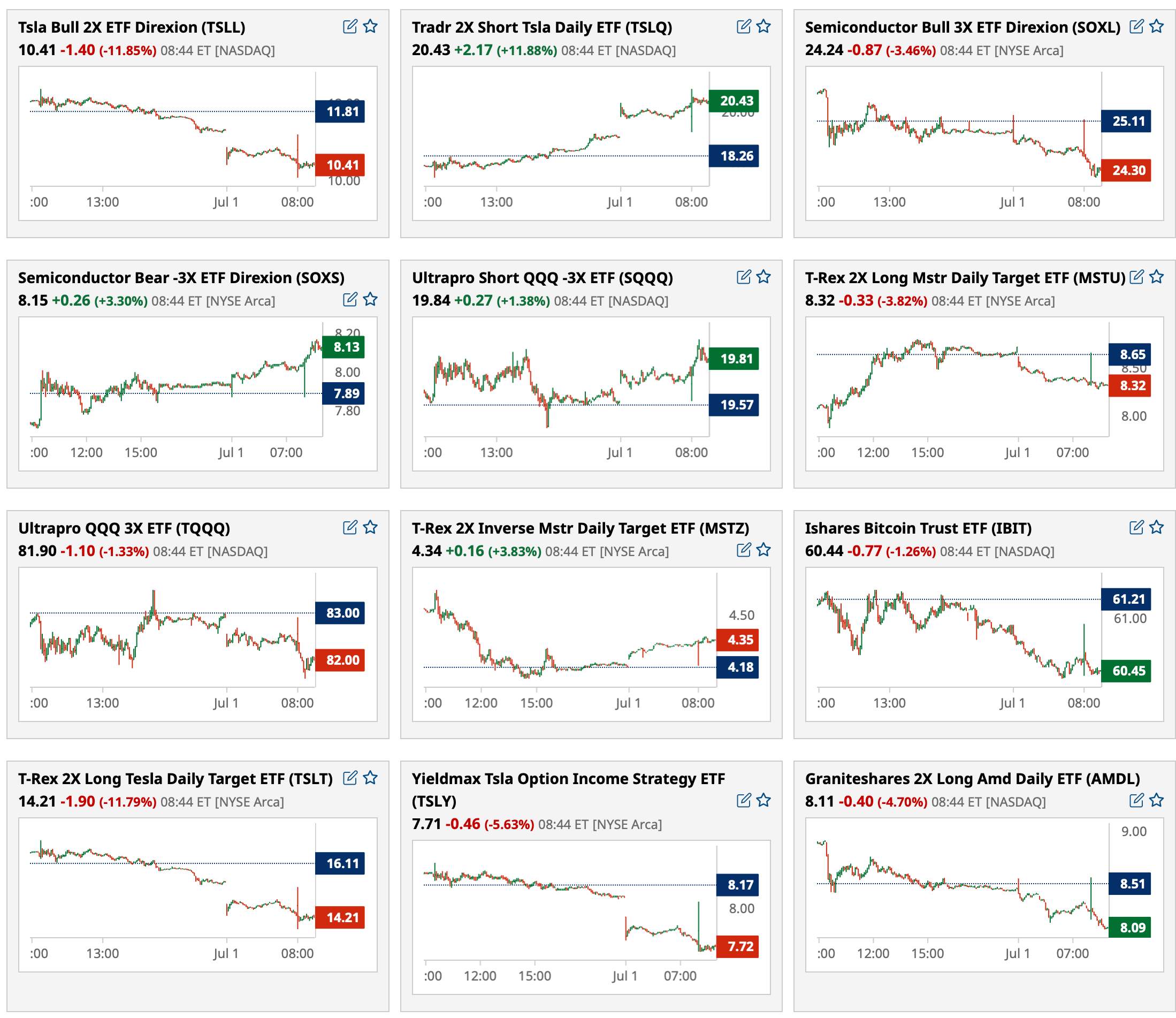

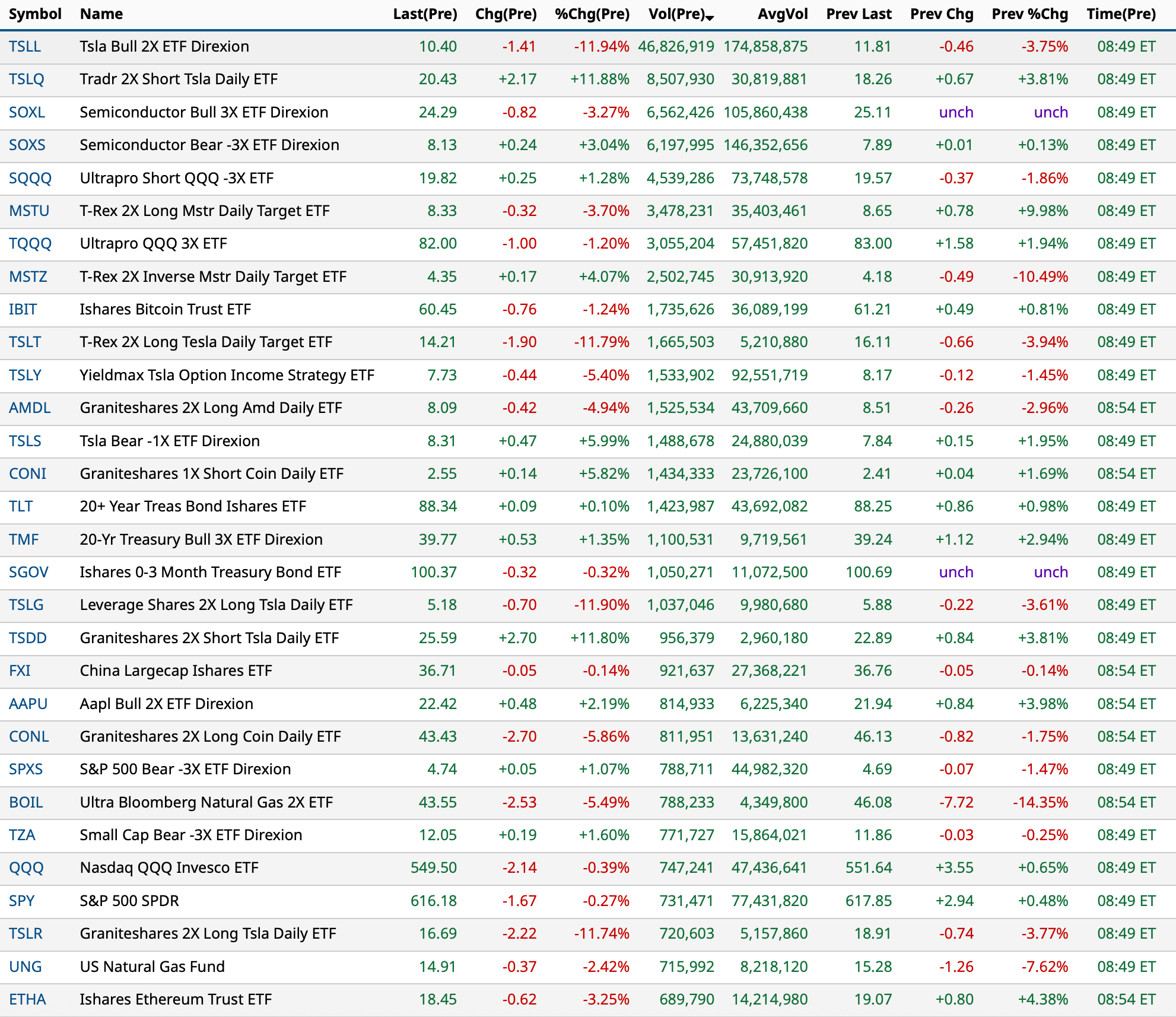

Most active premarket ETFs as of 8:49 a.m.:

BY Doug Kass · Jul 1, 2025, 9:30 AM EDT

Chart from 9:09 a.m. ET:

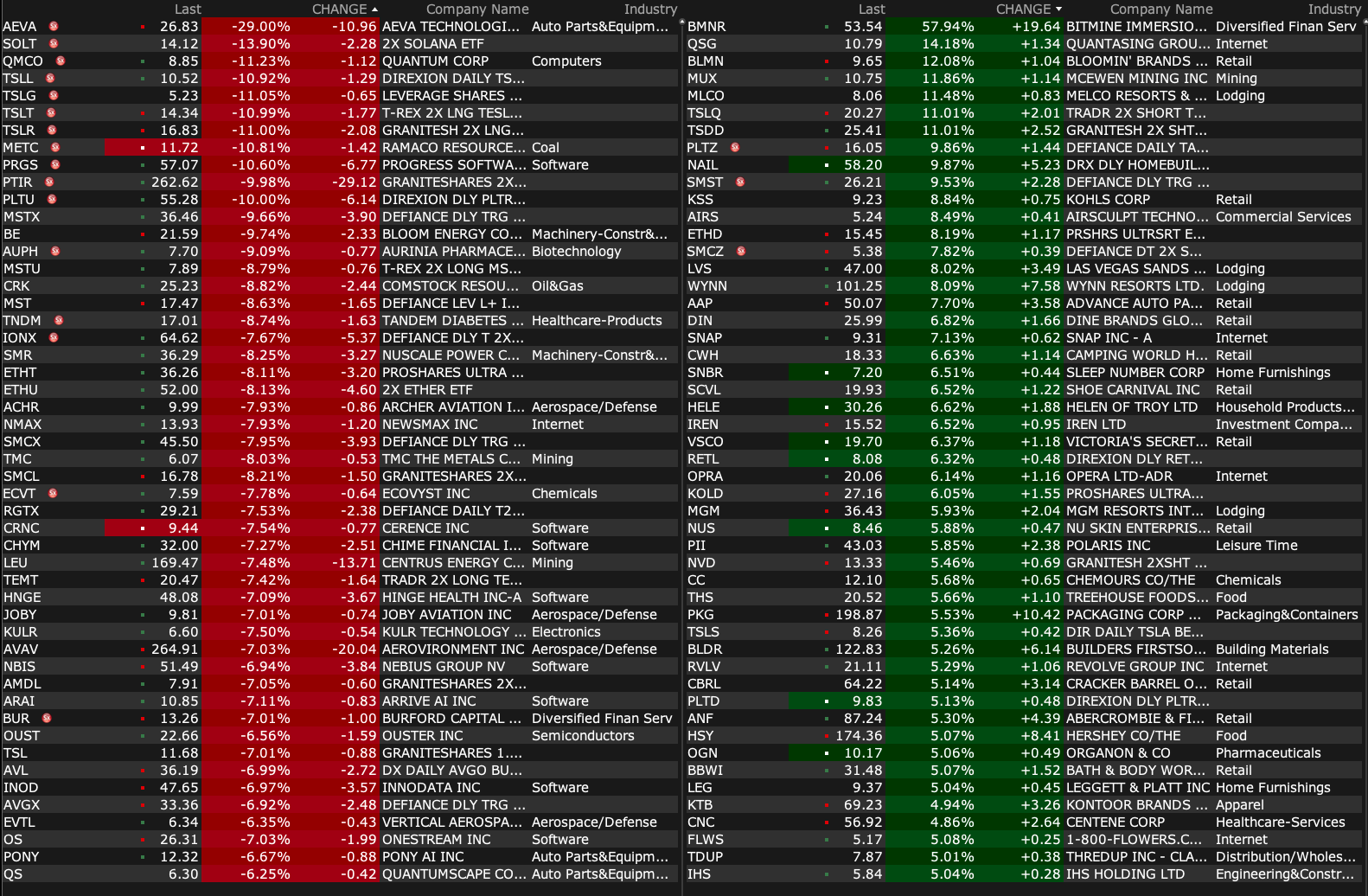

BY Doug Kass · Jul 1, 2025, 9:25 AM EDT

-WOLF +79% (files for reorganization under Chapter 11; expects to emerge out of bankruptcy by the end of the third quarter)

-VVOS +64% (receives Medicare Approval for VidaSleep Oral Appliance)

-BMNR +45% (momentum)

-ATAI +24% (announces with Beckley Psytech Positive Topline Results from the Phase 2b Study of BPL-003 in Patients with Treatment-Resistant Depression; files $50M private placement)

-FLUX +15% (secures $2M order for G80-420 lithium-ion battery packs from major US airline)

-BTAI +10% (receives Second Positive Recommendation from Data Safety Monitoring Board (DSMB) to Continue SERENITY At-Home Pivotal Phase 3 Safety Trial for Acute Treatment of Agitation Associated with Bipolar Disorders or Schizophrenia)

-ADAG +9.7% (announces up to $25M strategic investment from Sanofi)

-LVS +6.0% (strength following Macau Jun gaming revenue data)

-WYNN +5.1% (strength following Macau Jun gaming revenue data)

-RKLB +3.2% (announces successful completion of its Critical Design Review (CDR) for the Space Development Agency's (SDA) Tranche 2 Transport Layer-Beta (T2TL-Beta) program)

-INV +3.1% (unit Accelsius Holdings issued $13.0M of convertible notes with option to issue up to $2.0M more)

-SNAP +2.5% (Utah Attorney General's office sues Snapchat over alleged experimental AI tech)

-TTD +2.4% (CitiGroup Reiterates TTD with Buy, price target: $90; adding Upside 90-Day Catalyst Watch)

-OGEN -21% (prices public offering of up to $20M of Preferred Stock and Warrants)

-DYN -11% (prices 24.2M shares at $8.25/share)

-INMB -9.5% (multiple broker downgrades)

-RAY -8.6% (prices $5.2M Public Offering of 26.0M shares at $0.20/shr)

-AVAV -7.7% (files mixed shelf of an indeterminate amount)

-AMC -6.0% (agrees with Creditors on ~$223M of new money financing that will primarily be used to refinance debt maturing in 2026 and immediate equitization of at least $143M of existing debt, with potential to convert up to a total of $337M of existing debt)

-TSLA -6.0% (sales decline in June in Sweden/Denmark; feud with President Trump reignited)

-WBD -5.2% (Diversified Holdings LLC sells 100M shares)

-DXCM -4.6% (reportedly HHS will soon launch a large scale effort to encourage Americans to use wearable health devices like Continuous Glucose Monitoring devices)

-SG -3.8% (downside momentum)

-PRGS -3.0% (earnings, guidance)

BY Doug Kass · Jul 1, 2025, 9:16 AM EDT

From the "other dougie":

douglas cassel

This is stolen from a news blog I read. Once upon a time, I did this for a living. It is hard. This goes to my belief that AI might not be ready for general intelligence, but will make real advances in some more limited areas.

Microsoft has built an artificial intelligence-powered medical tool it claims is four times more successful than human doctors at diagnosing complex ailments, as the tech giant unveils research it believes could speed up treatment. The “Microsoft AI Diagnostic Orchestrator” is the first initiative to come out of an AI health unit formed last year by Mustafa Suleyman with staff poached from DeepMind, the research lab he co-founded and which is now owned by rival Google. In an interview with the Financial Times, the chief executive of Microsoft AI said the trial was a step on the path to “medical superintelligence” that could help solve staffing crises and long waiting times for overstretched health systems. Microsoft’s new system is underpinned by a so-called “orchestrator” that creates virtual panels of five AI agents acting as “doctors” — each with a distinct role, such as coming up with hypotheses or choosing diagnostic tests — which interact and “debate” together to choose a course of action. To test its capabilities, “MAI-DxO” was fed 304 studies from the New England Journal of Medicine (NEJM) that describe how some of the most complicated cases were solved by doctors. This allowed researchers to test if the program could figure out the correct diagnosis and relay its decision-making process, using a new technique called “chain of debate”, which makes AI reasoning models give a step-by-step account of how they solve problems. Microsoft used leading large language models from OpenAI, Meta, Anthropic, Google, xAI and DeepSeek. The orchestrator made all LLMs perform better, but worked best with OpenAI’s o3 reasoning model to correctly solve 85.5 per cent of the NEJM cases. That compared with about 20 per cent by experienced human doctors, but those physicians were not allowed access to textbooks or to ask colleagues in the trial, which could have increased their success rate. A version of the technology could soon also be deployed in Microsoft’s Copilot AI chatbot and Bing search engine, which handle 50 million health queries a day. Suleyman said Microsoft is nearing “AI models that are not just a little bit better, but dramatically better, than human performance: faster, cheaper and four times more accurate”. (Source: ft.com, italics mine)

BY Doug Kass · Jul 1, 2025, 7:39 AM EDT

Bonus — Here are some great links:

July 1 Is The Most Bullish Day of the Year (Jazzy Jeff Hirsch)

BY Doug Kass · Jul 1, 2025, 6:35 AM EDT

From JPMorgan:

US: Futs are weaker, dragged by Tech as TSLA is -5% pre-mkt on Musk v Trump part 2. Pre-mkt, the balance of Mag7 is mixed with Staples outperforming. Bond yields are lower as the curve flattens with USD continuing to decline, setting another 52-wk low. USD had its worst H1 since 1973 while SPX has its best quarter since 23Q1. Cmdtys are weaker ex-precious metals. Today is the first piece of the labor market puzzle with JOLTS but we also receive ISM-MFG and vehicle sales. Powell speaks at 9.30am. The voting process on the tax/budget bill continues.

and...

EQUITY & MACRO NARRATIVE

Yesterday was an uninformative session with macro data kicking off today, capped by Thursday’s NFP print into the holiday. Overshadowed by labor markets, we do receive ISM and regional Fed activity indicators this week with two weeks before earnings season kicks off. The Musk v. Trump social media fight returns with TSLA experiencing downside risk, let’s see how long this lasts but the balance of the Mag7 / MegaCap Tech remain attractive to investors. Retail investors returned yesterday, buying ~$3.0bn of stock vs. $514mm (1-month average, +5.4z).

BY Doug Kass · Jul 1, 2025, 6:25 AM EDT

Wolf Street howls about rising home supplies of unsold units.

BY Doug Kass · Jul 1, 2025, 6:15 AM EDT

The S&P Short Range Oscillator finally is getting quite overbought — at 4.35% vs. 2.23%.

BY Doug Kass · Jul 1, 2025, 6:06 AM EDT