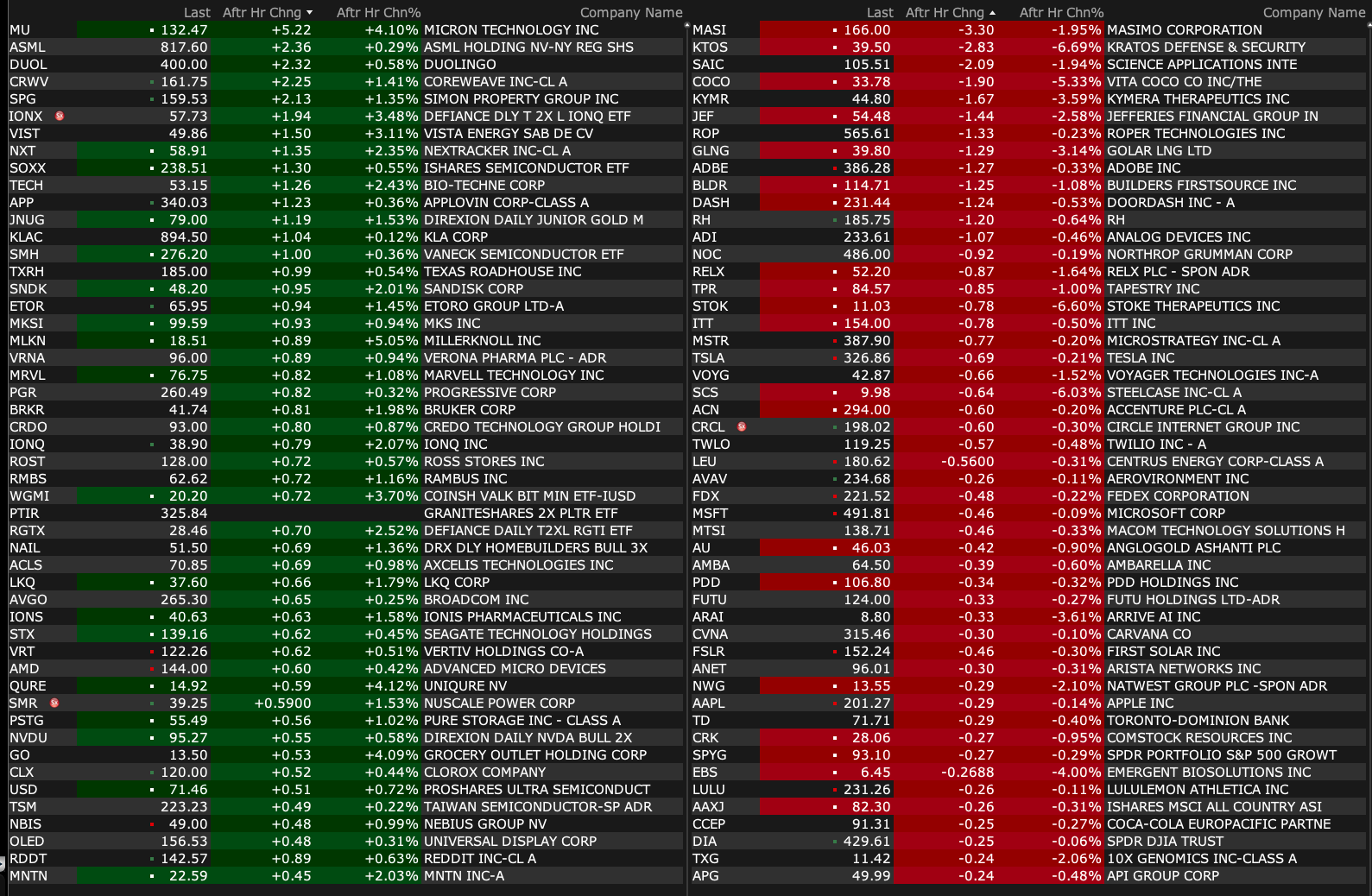

Wednesday's After-Hours Movers

As of 4:22 p.m.:

BY Doug Kass · Jun 25, 2025, 4:52 PM EDT

As of 4:22 p.m.:

BY Doug Kass · Jun 25, 2025, 4:52 PM EDT

I will be out of the office (and not writing) on Thursday and Friday as I have to address a relatively routine family medical issue in New York City.

BY Doug Kass · Jun 25, 2025, 4:45 PM EDT

BY Doug Kass · Jun 25, 2025, 4:40 PM EDT

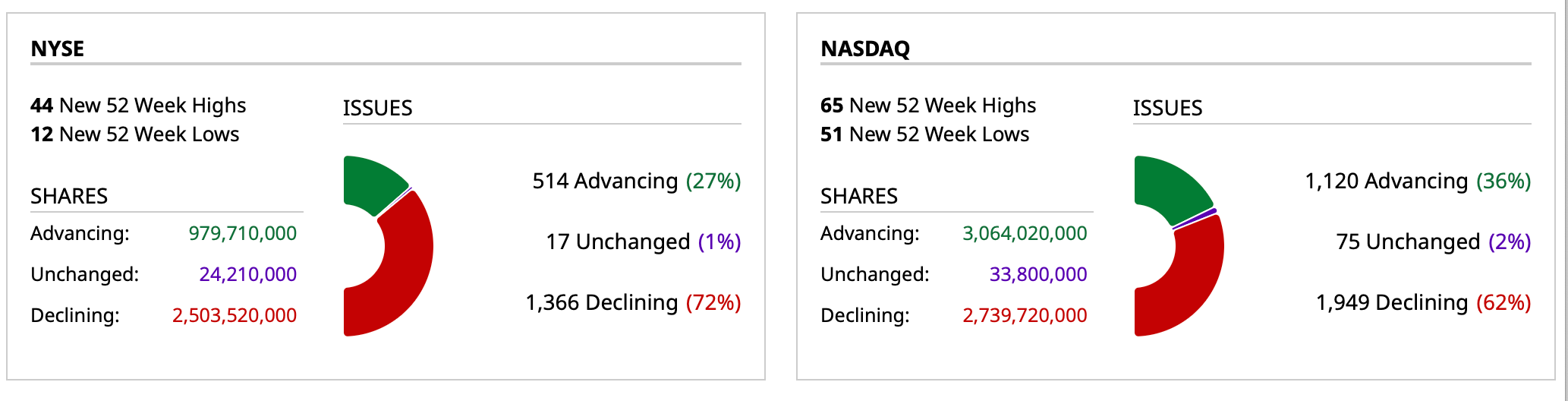

- NYSE volume 1% below its one-month average;

- NASDAQ volume 11% below its one-month average;

- VIX index: down 4.12% to 16.76

BY Doug Kass · Jun 25, 2025, 4:32 PM EDT

As of the close:

BY Doug Kass · Jun 25, 2025, 4:13 PM EDT

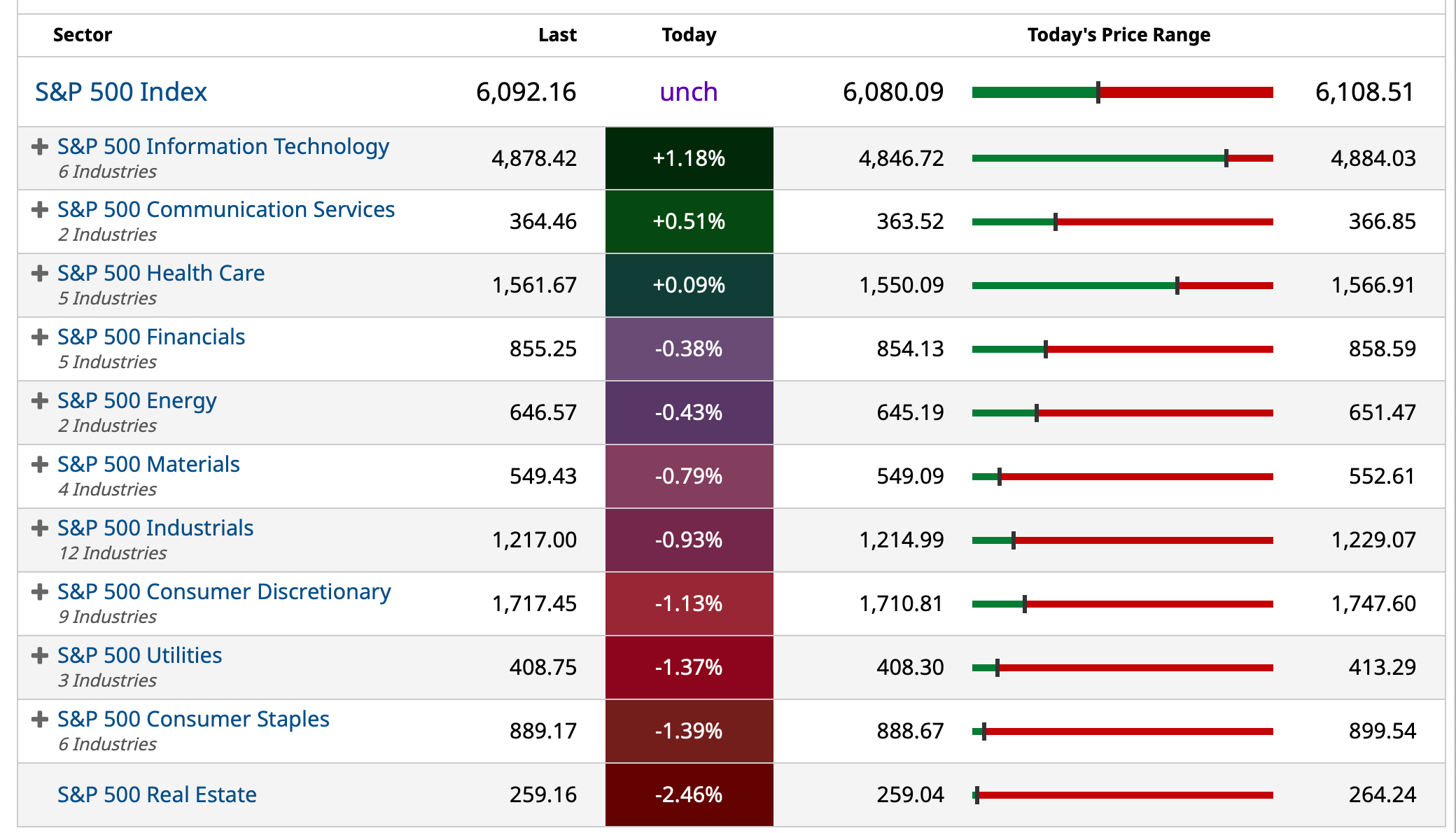

Near the close, the divergences between the averages continue:

* SPY flat

* QQQ +0.20%

* IWM -1.12%

* RSP -0.75%

BY Doug Kass · Jun 25, 2025, 4:02 PM EDT

I'm moving from small to very small in my PepsiCo PEP investment short (-$3 on the day) at $128.10.

The recent price decline is my reason.

BY Doug Kass · Jun 25, 2025, 2:48 PM EDT

BY Doug Kass · Jun 25, 2025, 2:35 PM EDT

BY Doug Kass · Jun 25, 2025, 2:00 PM EDT

With a clear cut trend of state jurisdictions taxing betting sites I have sold my DraftKings DKNG on today's strength, especially considering its rich EV/EBITDA.

BY Doug Kass · Jun 25, 2025, 1:51 PM EDT

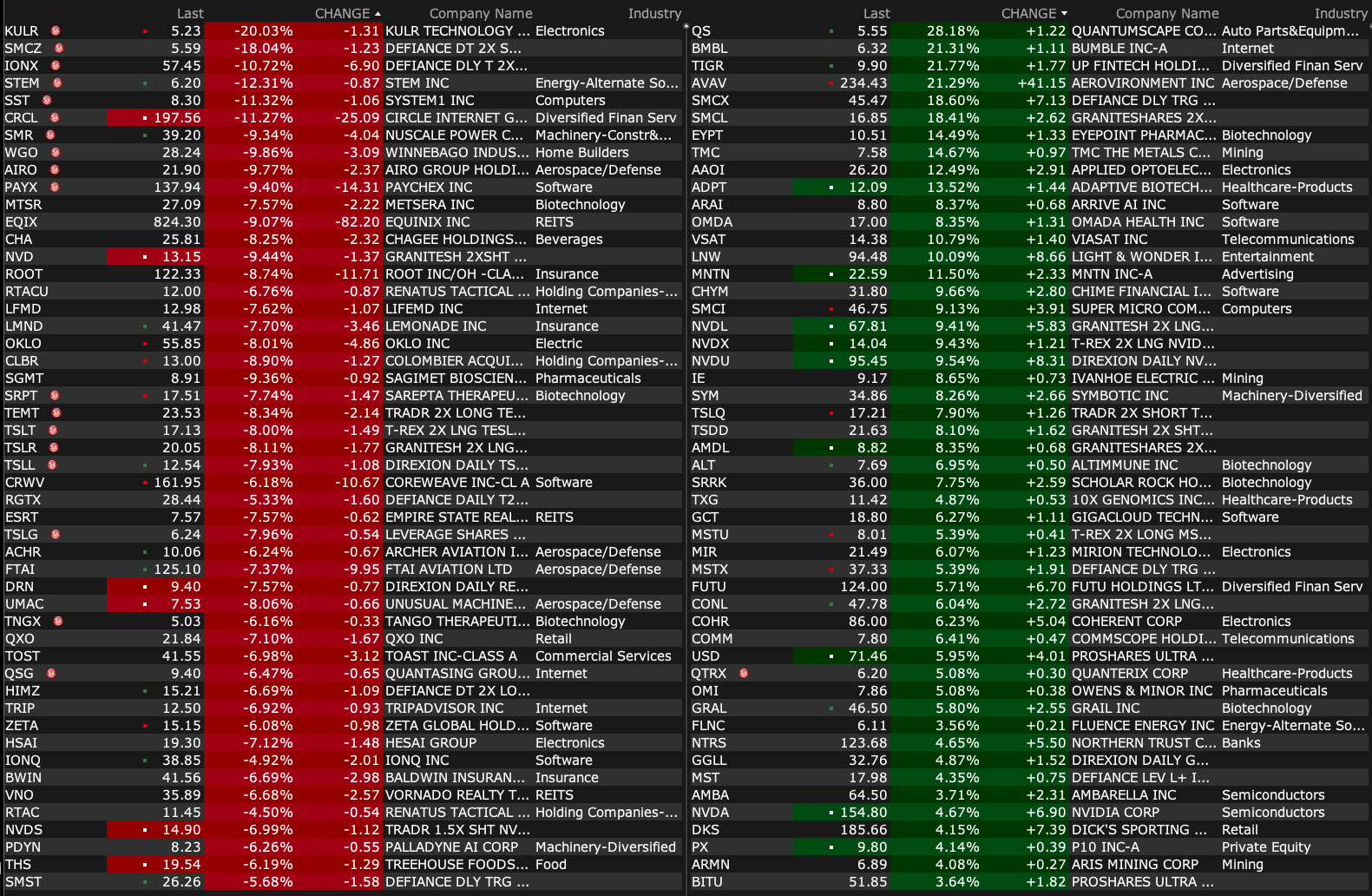

No drama investment short Winnebago WGO is down by another -7% today after its EPS call and disappointing guidance:

Winnebago reports Q3 adjusted EPS 81c, consensus 79c Reports Q3 revenue $775.1M, consensus $774.81M. "Our fiscal third-quarter results reflect both the diverse dynamics of our business segments and the challenges posed by an uncertain economic environment," said Michael Happe, President and Chief Executive Officer of Winnebago Industries. "While retail demand across the outdoor recreation sector remains soft, our dealer partners are navigating the market with prudence and agility. At Winnebago Industries, we continue to pursue discipline in every aspect of our operations. We are focused on protecting long-term profitability and sustaining strong customer relationships while aligning production closely with healthy field inventory turn targets. Most importantly, I want to thank our entire team for their dedication. Their commitment and resilience continue to power our progress and position us for future growth."

Winnebago sees FY25 adjusted EPS $1.20-$1.70, consensus $1.74 Sees FY25 revenue $2.7B-$2.8B, consensus $2.76B. "Although the macroeconomic backdrop presents near-term challenges, we remain confident in the resilience of our brands and the long-term potential of our end markets," Happe said. "With a new leadership team in place, Winnebago motorhomes is launching a comprehensive margin recapture plan centered on refreshing the product line, boosting operational efficiency and rebuilding sustained profitability beginning in fiscal 2026. The growing appeal of the outdoor lifestyle-especially among younger and more diverse consumers-continues to drive strong interest in RVing and boating. This trend supports our view for meaningful growth across our portfolio as market conditions normalize."

The EPS Call

The company is considering restructuring to eliminate redundancies and inefficiencies; Anticipating continued softness in RV activity through year-end as expanding macroeconomic uncertainty shifted consumer and dealer buying patterns in Q3

- RV industry associations recently cut their 2025 wholesale shipment forecast, driving lower Q3 margins in both Towable and Motorhome segments, with Winnebago-branded Motorhomes underperforming disproportionately.

- Margin recapture plan beginning in FY 26 to lower field inventory, improve working capital, align production with demand, reduce discretionary expenses and refresh product lineup to rebuild sustained profitability.

- Comprehensive capacity utilization analysis, manufacturing footprint review, supply-chain evolution to mitigate tariff cost pressure and organizational streamlining to eliminate redundancies and drive cost discipline.

- Surging dealer interest in Winnebago-branded Motorhomes over recent months underscores the brand’s potential for significant share gains and margin improvement once new operational initiatives take effect.

- Product lineup enhancements: Newmar Freedom Air (compact Class C) orders commence mid-summer with shipments early Q1 FY 26; Grand Design Lineage VT Class B van began Q3 shipments; Winnebago Towables launched Thrive travel trailer (<$50 K MSRP); Chris Craft’s Catalina 31 and Barletta’s 2026 helm redesigns and premium color options rolling out now.

- Thrive travel trailer delivers features of larger units at a sub-$50 K price point, aiming to capture summer travel demand in a value-focused market.

- Earned recognition by Newsweek as one of America’s most trustworthy companies for the second consecutive year, highlighting strong governance and stakeholder confidence.

BY Doug Kass · Jun 25, 2025, 1:25 PM EDT

With S&P cash +2 handles I am adding to my index puts.

BY Doug Kass · Jun 25, 2025, 12:35 PM EDT

While the S&P remains in the green, the decline in RSP and IWM is accelerating.

Breadth is deteriorating.

BY Doug Kass · Jun 25, 2025, 12:14 PM EDT

- NYSE volume is 1% below its one-month average;

- Nasdaq volume is 9% below its one-month average;

- VIX index: down 1.95% to 17.14

BY Doug Kass · Jun 25, 2025, 11:20 AM EDT

From Peter Boockvar:

After KB Home said this:

"As to market conditions, while longer term the outlook for the housing market remains favorable, driven by demographics and an undersupply of homes, consumers are continuing to demonstrate a lack of confidence about the short term, which has impacted their home purchase decisions. Affordability challenges have persisted, compounded by the variability in mortgage interest rates, which remain elevated as well as macroeconomic and geopolitical uncertainties. These factors resulted in more subdued demand during the spring selling season. As a result of this softer environment, we are revising our guidance for fiscal 2025."

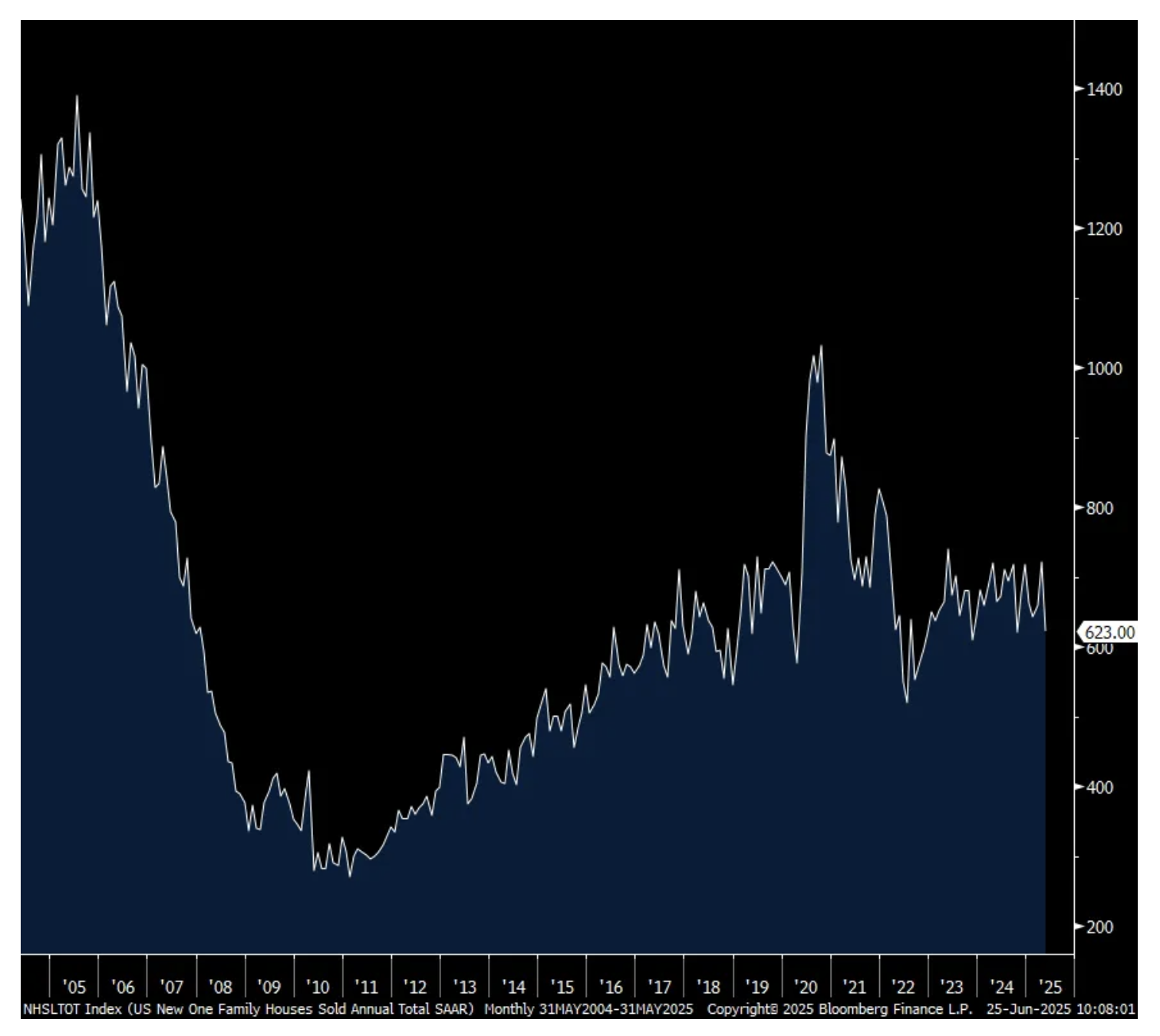

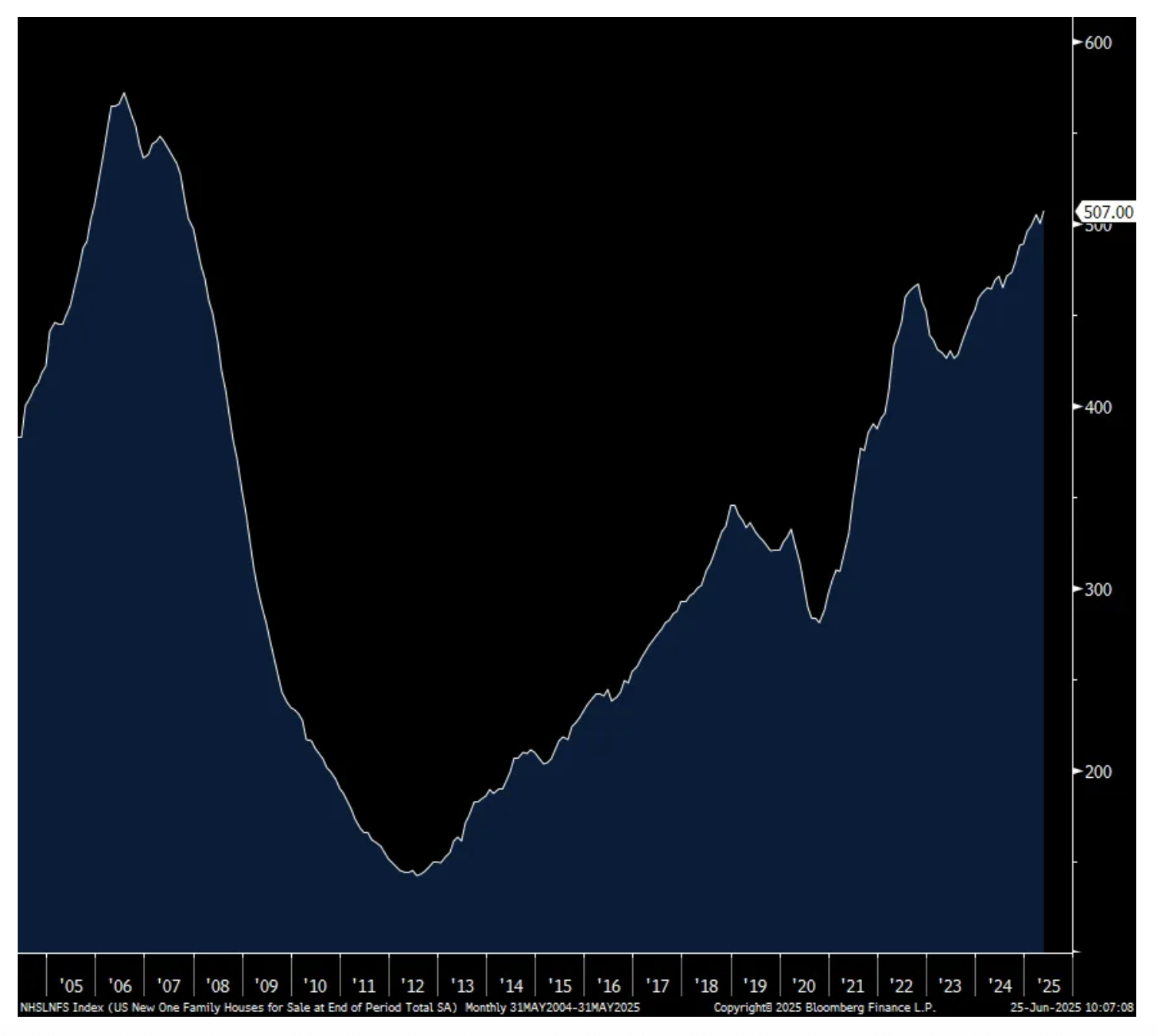

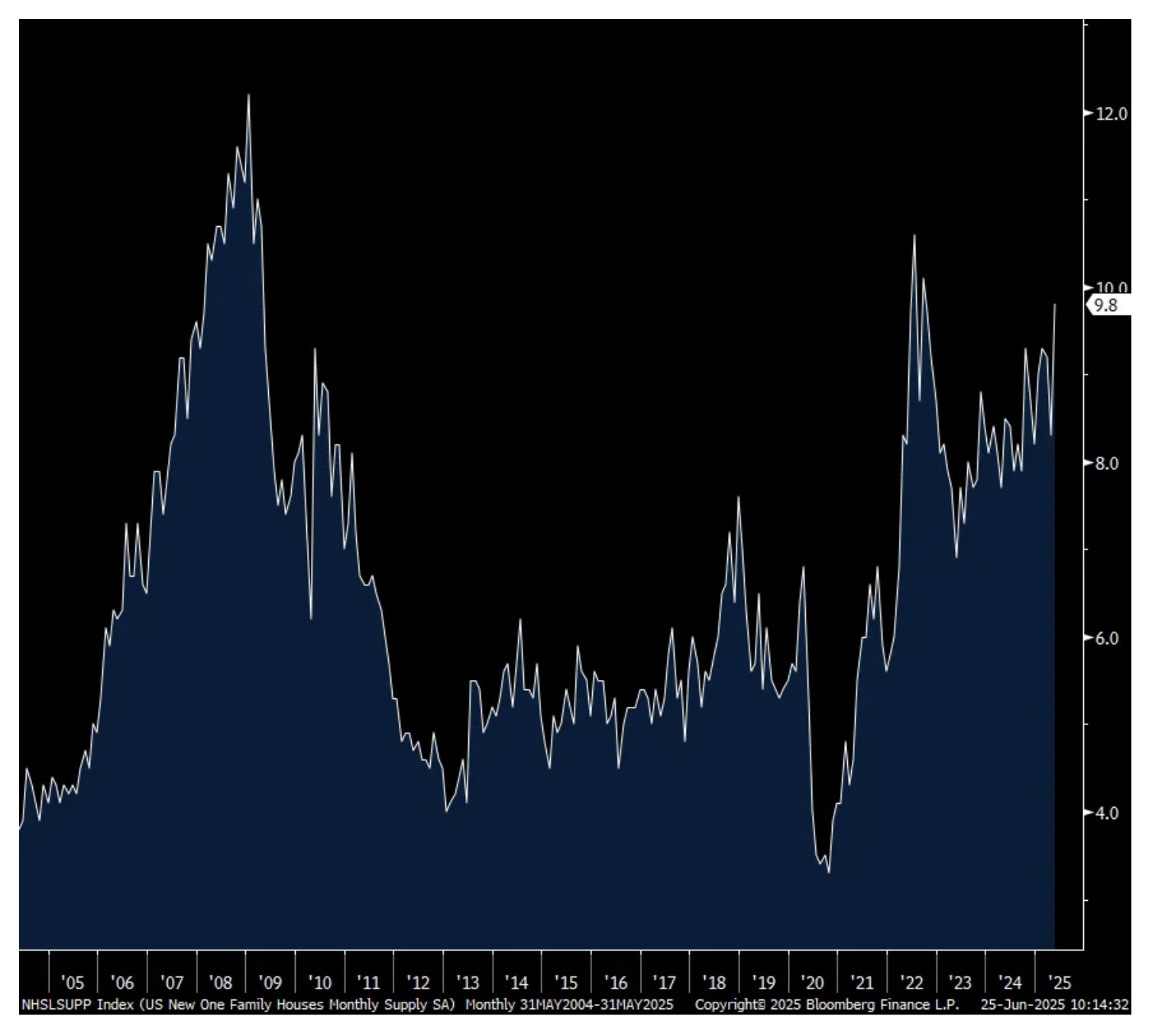

May new homes totaled 623k, 70k less than expected and April was revised down by 21k to 722k. The number of homes for sale rose to 507k which is the most since 2007 and combining this with sales puts months’ supply at 9.8, the most since September 2022. The median home price jumps around due to mix but was up 3% y/o/y after falling by .9% in the month before.

Smoothing out this volatile number has the 3 month average at 668k vs the 6 month average of 671k and the one yr average of 676k. For further perspective, the 2019 average was 685k.

I’ll follow up the KB Home comments with what Lennar said on June 16th and give them the bottom line opportunity on the new sale market:

“Consistent with last quarter’s earnings call, the macroeconomy remains challenging as mortgage interest rates have remained higher, while consumer confidence has been challenged by a wide range of uncertainties, both domestic and global. Across the housing landscape, actionable demand has been diminished by both affordability and consumer confidence, and therefore, has continued to soften.”

Home Sales

Number of Homes for Sale

Months’ Supply

BY Doug Kass · Jun 25, 2025, 10:57 AM EDT

I just covered my TSLA short at $320.73 following the unimpressive Austin robotaxi launch: "Tesla robotaxi incidents caught on camera in Austin get NHTSA concern" and the company's weak European sales, "Tesla's European car sales fall as customers switch to Chinese EVs."

Things I Did Today: Here is today's "things:"

Shorted: $349.95

BY Doug Kass · Jun 25, 2025, 10:39 AM EDT

Divergences haven't mattered in the recent melt-up but both the Russell Index IWM and the Equal Weighted S&P RSP are down -0.5% each.

Bond yields are higher, too.

So, with S&P cash +12 handles I am adding to my index shorts:

* SPY $608.24

* QQQ $543.07

BY Doug Kass · Jun 25, 2025, 9:57 AM EDT

-QS +41% (Cobra Separator Process Enters Baseline Production)

-GCTK +34% (Glucotrack and OneTwo Analytics Present Positive Final Results of First-In-Human Study for Continuous Blood Glucose Monitor at American Diabetes Association’s 85th Scientific Sessions)

-DTIL +18% (receives FDA Rare Pediatric Disease Designation for the treatment of Duchenne muscular dystrophy)

-BMBL +14% (raises guidance, approves workforce reduction)

-TMC +9.4% (Wedbush, Inc. Raised TMC to Outperform from Neutral, price target: $11)

-BB +8.2% (earnings, guidance)

-PONY +7.3% (added to NASDAQ Golden Dragon China Index)

-INBS +6.2% (Intelligent Bio Solutions and Spjotgard Drive Rapid Adoption of Fingerprint DrugTesting across Scandinavia)

-COIN +4.2% (HUT amends credit agreement with Coinbase)

-RSLS +4.2% (granted key international patent in Australia for Its Proprietary Diabetes Neuromodulation Technology)

-NBIS +4.1% (momentum)

-STLA +4.0% (Jefferies Raised STLA to Buy from Hold, price target: $13.20)

-SYM +3.9% (Arete Capital Partners Initiates SYM with Positive, price target: $50)

-AVAV +3.7% (earnings, guidance)

-HYLN +2.9% (signs non-binding LOI with MMR Power Solutions, a subsidiary of MMR Group)

-OKLO +2.1% (announces strategic collaborations with Hexium, a pioneering isotope enrichment company, and TerraPower, a nuclear innovation company, with the goal of ultimately accelerating domestic production of High-Assay Low-Enriched Uranium (HALEU) at industry leading cost targets)

-CURV -33% (prices 10M shares at $3.50/share)

-FBRX -18% (prices 5.63M shares at $12.00/shr for gross proceeds ~$75M)

-DAKT -9.5% (earnings)

-ASTS -6.6% (prices Repurchase of $225M of 4.25% Convertible Notes due 2032 and Registered Direct Offering of 9.5M shares of Class A Common Stock at $53.22/shr to Fund Convertible Note Repurchase)

-FDX -4.7% (earnings, guidance)

-KYMR -4.6% (Sanofi informed Kymera it will not advance one of its preclinical assets, KT-474)

-GIS -3.9% (earnings, guidance)

BY Doug Kass · Jun 25, 2025, 9:10 AM EDT

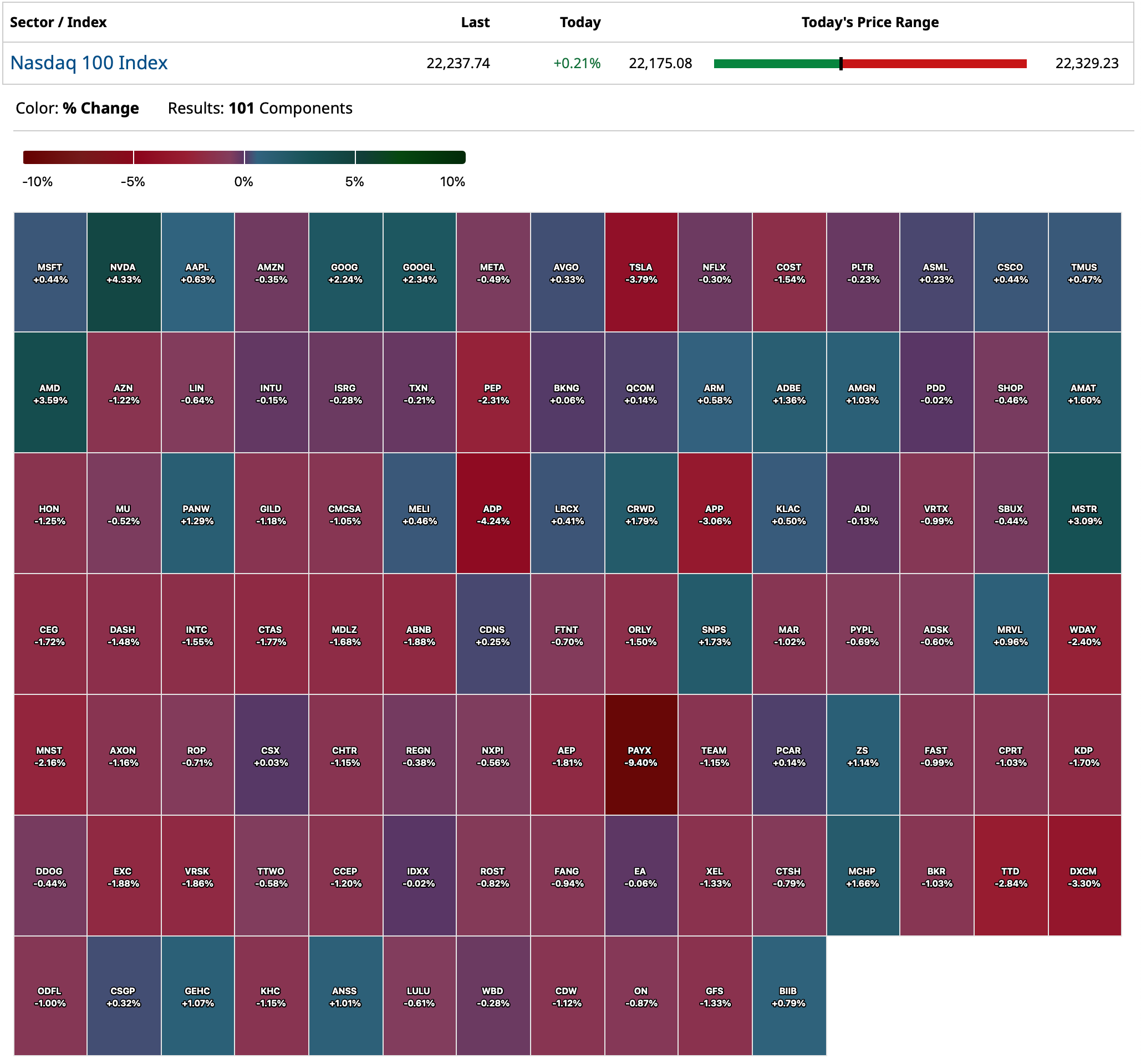

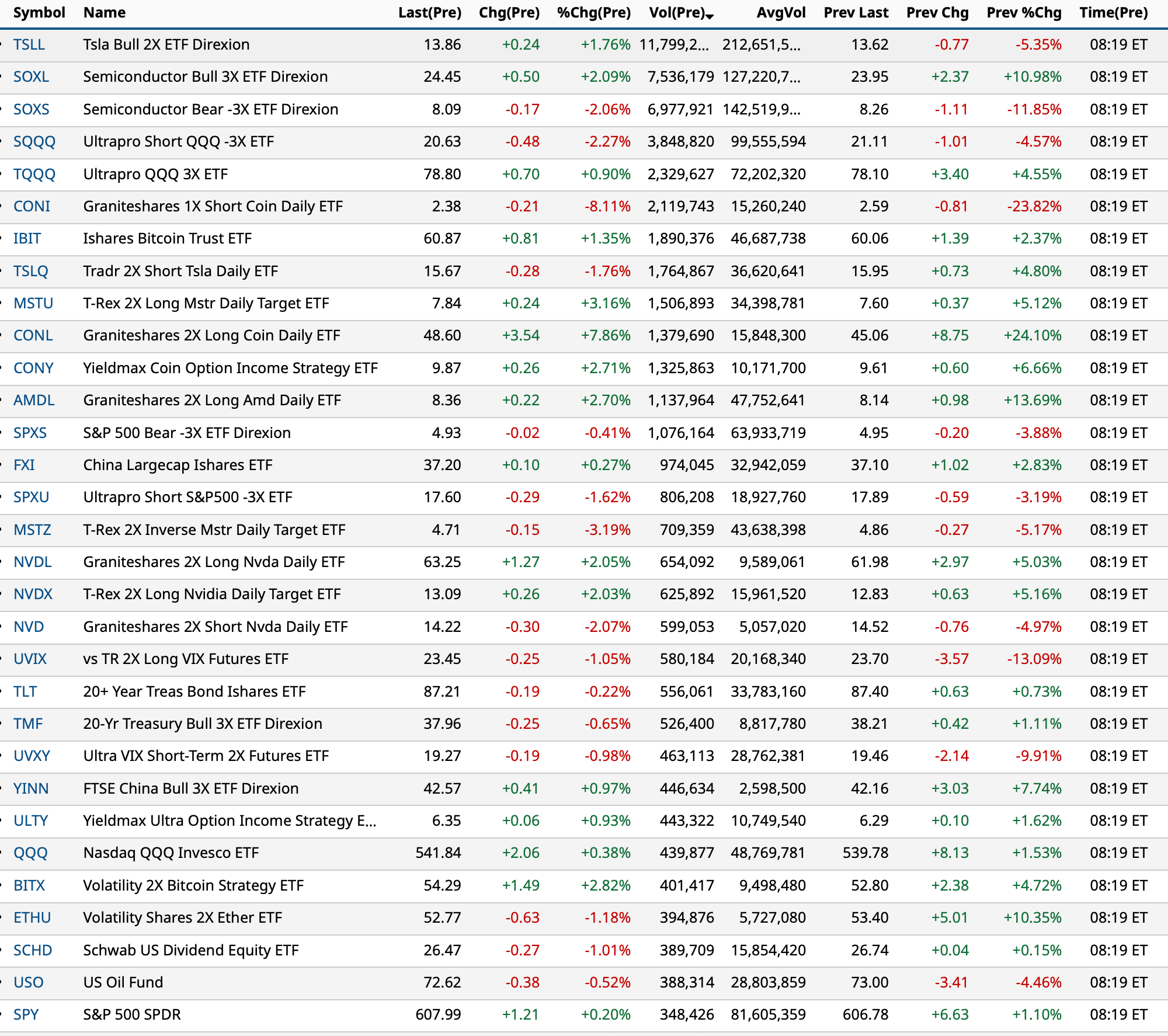

Charts from 8:19 a.m. ET:

BY Doug Kass · Jun 25, 2025, 8:59 AM EDT

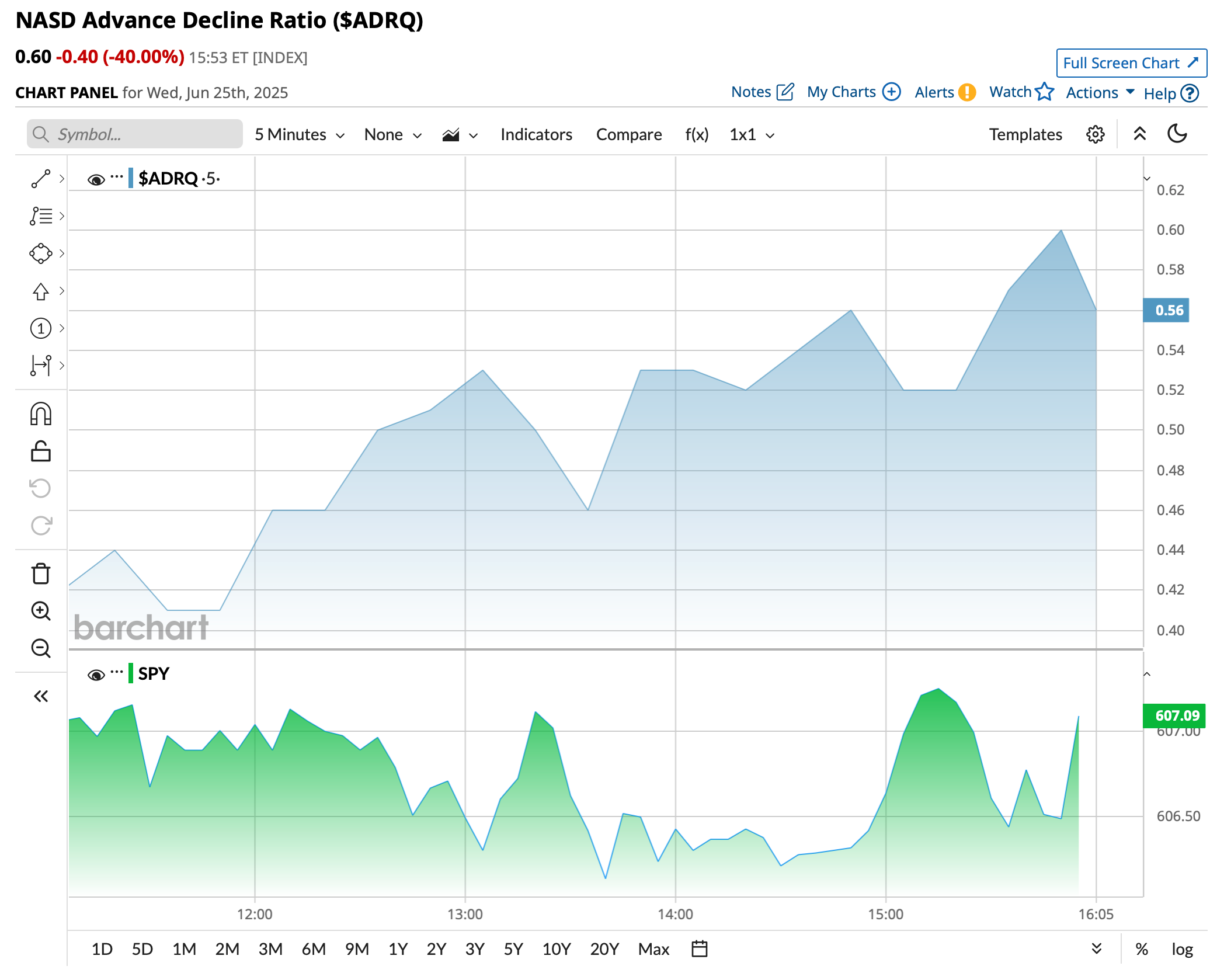

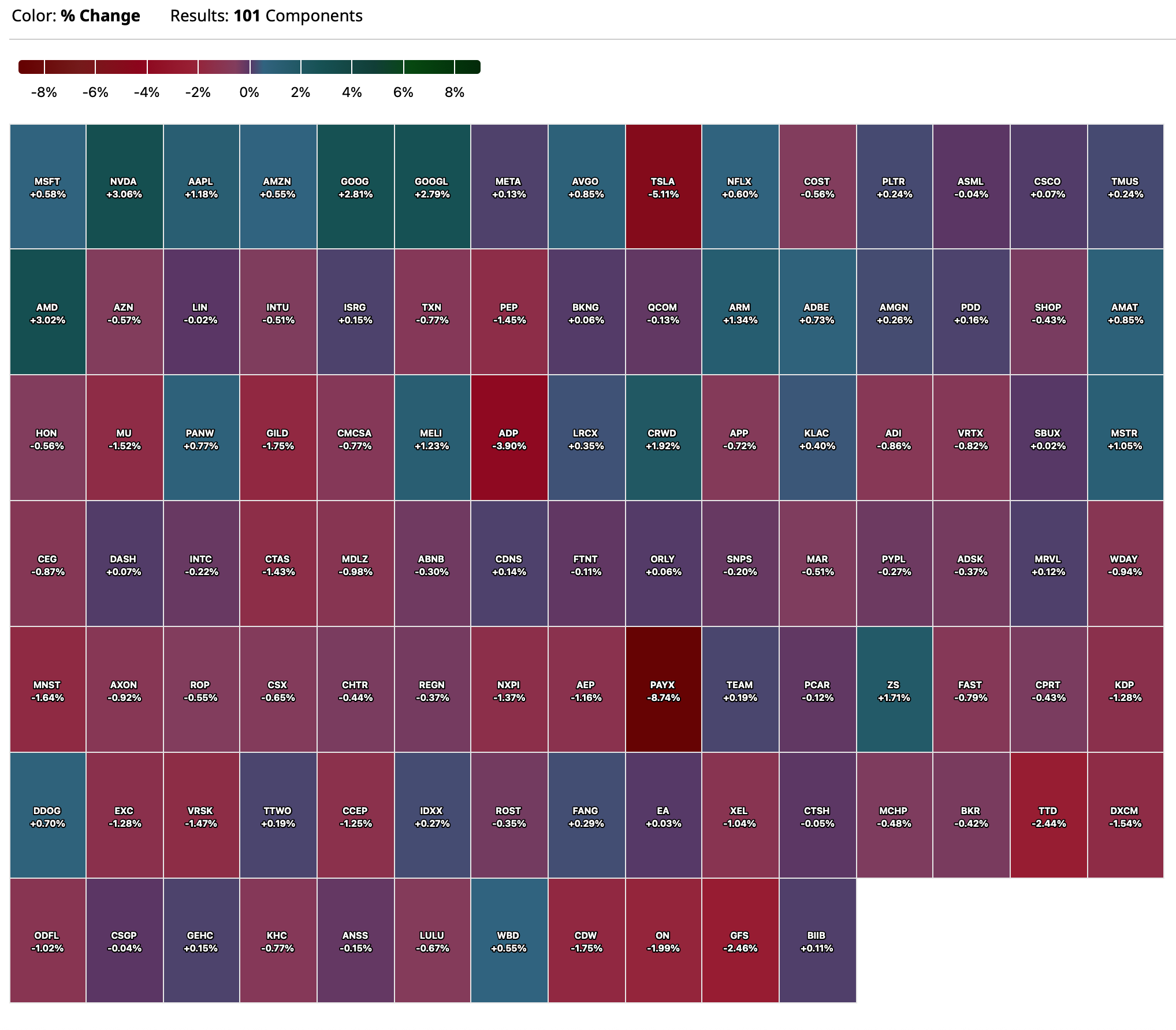

Chart from 8:40 a.m. ET:

BY Doug Kass · Jun 25, 2025, 8:44 AM EDT

From Peter Boockvar:

Regarding the NYC Mayoral race, with a world of historical precedent on the failed experiences of socialism, it remains a mystery why people still yearn for its inevitable results.

FedEx has their finger on the pulse of global commerce as good as any as they "connect 99% of the world's commerce...move $2 trillion worth of goods every year...connect 3 million shippers to more than 225 million consumers" and this is what they said last night:

After praising one of the greatest entrepreneurs the world has ever seen, Fred Smith, the CEO explained why after only 1% y/o/y revenue growth they were able to drive 8% operating income growth "in a weak demand environment" and helped by selective capacity cuts based on shifting trade flows.

"March performance was solid and in line with our expectations. Following the April 2nd tariff announcement, customer concerns increased, and as a result, volume softened. In early May, upon tariff implementation, China to US volumes deteriorated sharply and remained weak throughout the rest of the quarter. Our international export revenue was flat, reflecting the tariff related impact on our Trans-Pacific trade lane."

"US domestic volumes held up well throughout the quarter, with growth accelerating in late April and May." Not clear of course how much was tariff front running or not. See below for more color on this.

"So from a B2B perspective...we have not seen a marked improvement in the industrial economy. And that's certainly pressuring both our FedEx Ground commercial, but also our base at Express and certainty the FedEx Freight division. So we have not seen improvement there."

"From a consumer perspective, when we saw the May increase, obviously spent a lot of time looking at the data. There is no indication that we can point to that says that there was a consumer pull forward. What I can tell you is onboarding within our own pipeline was stronger in May, and that was the largest driver. Whether or not there is consumer pull forward is to be determined, which is why we gave you the range that we did from a revenue perspective" with respect to their guidance.

The cruise business is still rocking and rolling and this from Carnival as they are 93% booked for 2025:

"Yields grew by almost 6.5%, beating our guidance by 200 bps. Both ticket and onboard equally outperformed on very strong closing demand, reaffirming the strength of our consumer."

"Our book position is in line with last year's record levels and at historically high prices. Our elongated advanced booking window and limited capacity growth give us flexibility to patiently take price."

"we definitely saw more volatility in the month of April, that's probably should not be unexpected...But May, nicely better than April. And the first couple of weeks of June, nicely better than May."

On the consumer, "So we haven't seen anything that's really showing us a differentiation in patterns between the lower end consumer and those that are looking for the premium or even the luxury. So nothing in particular to speak of. I'd go back to what I've said a lot, which a lot of people say, is we are an incredibly stupid value when it comes to the alternatives. And when people are looking to take vacation, because they do, we hold up really, really well. And the lower down you come in income, the more important that becomes because they have to make their dollars really earn on their vacation. And that's what we try to do for everybody."

"In a world of heightened volatility, the amazing cruise experiences our portfolio of cruise brands deliver at a truly exceptional value simply stand out."

I'll say this again, thinking that Fed rate cuts are good and hikes are bad is superficial and skin deep. That baby boomer that is cruising could be using interest income they are deriving from the 4% ish interest rate they are receiving on their money market/Treasury holdings. Thus, further cuts in rates eats into the interest income received by many.

I will post this again from last week the great stat from my great friend Danielle Dimartino Booth that "70 cents of every $1 of interest income is spent into the economy vs 2 cents of wealth effect growth via their stock market portfolios."

With an average 30 yr mortgage rate of 6.88%, up 4 bps w/o/w, purchase applications were little changed, down by .4% w/o/w. Refi's rose 3% though but after falling by 2.1% in the week before.

Aussie bonds are rallying after a 2.1% May CPI y/o/y print which was 2 tenths below expectations and sets up the RBA for a July rate cut. The trimmed mean was higher by 2.4% vs 2.8% in April. The Aussie$ though is unchanged, but still near the highest level vs the US dollar since last November. The ASX was flat.

BY Doug Kass · Jun 25, 2025, 8:15 AM EDT

Housing will likely lead a consumer-led economic slowdown:

BY Doug Kass · Jun 25, 2025, 7:42 AM EDT

From Knowledge@Wharton: What’s the Best Strategy to Grow Your Business?

BY Doug Kass · Jun 25, 2025, 7:15 AM EDT

From JPMorgan:

US: Futs are flat after NDX set a new ATH yesterday amid a thawing of geopolitical risk. As the market moves back to trade, taxes, and earnings there are incrementally positive headlines on US/Mexico looking at a lowering effective tariffs rates around a quota system and US/China where China is looking to reduce the flow of fentanyl precursors, a potential goodwill measure. Pre-mkt, Mag7/Semis are seeing a bid; Cyclicals are mixed with Fins higher, but Industrials dragged by FDX. Bond yields are mostly flat amid USD strength. Cmdtys are weaker with Energy seeing a relief rally/deadcat bounce. Today’s macro data focus is on Powell’s day 2 of 2 testimony, 5Y bond auction, and new home sales.

and...

EQUITY & MACRO NARRATIVE

News reports have surfaced that the US did a minimal amount of damage to the Iranian nuclear program, setting their ambitions back by months but not permanently, including the unknown whereabouts of more than 400kg of below-weapons grade enriched uranium. What does this mean for markets? At this stage, we think the Market will look through this report given the ceasefire agreement. Iranian military capabilities have been significantly compromised by Israeli strikes and that will take time to rebuild if it happens at all. For now, de-escalation appears to be the near-term path. The obvious caveats being a re-escalation that either targets Iran’s export supply chain or an attack on a NATO country.

· US Strikes Had Limited Impact on Iran’s Nuclear Program, Early Report Shows (BBG)

Yesterday seemed like the unofficial restart of the bull market with geopolitics behind us and assurances of economic strength via Fedspeak. Our desk flows were very strong and interesting to see markets move without outsized Retail participation; JPM estimates $1.25bn of buying vs. $512mm (1-month avg, +1.6z). Markets should continue their march higher and keep an eye on Friday’s Senate vote on the budget/tax bill. While we expect the bill to eventually pass the Senate Parliamentarian has removed several aspect of the bill and Senate/House do not yet seem aligned. If the bill fails to pass on its first try, we may see bond yields move lower as the yield curve bull steepens, which would be good for higher beta plays, Cyclicals, and Value plays, generally.

The biggest near-term data point is next week’s NFP print (BBG survey is +116k jobs and 4.3% unemployment rate) where an inline or stronger print will continue to propel the market higher. Powell mentioned that June – August data should begin to reflect tariff impact; his comments were focused on inflation but could show up in labor markets, too. The NY Fed found that most business have begun passing all tariff costs (see charts below); the majority of businesses passed along these costs within 3 months. Keep an eye on freight rates which may reflect both heighted demand but also potential strikes in the Red Sea/Middle East, impacting goods inflation.

· New freight container wave to beat China tariffs deadline begins at nation’s busiest ports (CNBC)

· POWELL: LOWER INFLATION, WEAKER LABOR COULD MEAN EARLIER CUT

· POWELL: MAJORITY FEELS IT APPROPRIATE TO CUT LATER THIS YEAR

· POWELL: WE DO EXPECT TARIFF INFLATION TO SHOW UP MORE

· POWELL: EXPECT MEANINGFUL TARIFF EFFECTS IN JUNE, JULY, AUGUST

BY Doug Kass · Jun 25, 2025, 7:00 AM EDT

Bonus — Here are some great links:

Broker and Dealers Ready to Go

Dangerous to Make a Broader Tech Call

BY Doug Kass · Jun 25, 2025, 6:40 AM EDT

Reposting from last night if some left early:

President "Bobby": Mr. Gardner, do you agree with Ben, or do you think that we can stimulate growth through temporary incentives?

[Long pause]

Chance the Gardener: As long as the roots are not severed, all is well. And all will be well in the garden.

President "Bobby": In the garden.

Chance the Gardener: Yes. In the garden, growth has it seasons. First comes spring and summer, but then we have fall and winter. And then we get spring and summer again.

President "Bobby": Spring and summer.

Chance the Gardener: Yes.

President "Bobby": Then fall and winter.

Chance the Gardener: Yes.

Benjamin Rand: I think what our insightful young friend is saying is that we welcome the inevitable seasons of nature, but we're upset by the seasons of our economy.

Chance the Gardener: Yes! There will be growth in the spring!

Benjamin Rand: Hmm!

Chance the Gardener: Hmm!

President "Bobby": Hm. Well, Mr. Gardner, I must admit that is one of the most refreshing and optimistic statements I've heard in a very, very long time.

[Benjamin Rand applauds]

President "Bobby": I admire your good, solid sense. That's precisely what we lack on Capitol Hill.

- Being There Being There

Federal Express (FDX) reports a beat but guides first quarter revenues to flat to +2%.

The shares were +$6 coincident with EPS report and before the guidance — and are now -$12.

Position: None

By Doug Kass Jun 24, 2025 4:45 PM EDT

BY Doug Kass · Jun 25, 2025, 6:25 AM EDT

The S&P Short Range Oscillator rose to 1.54% vs. 0.92% — overbought but still not way overbought.

BY Doug Kass · Jun 25, 2025, 6:10 AM EDT

Wolf Street howls about the U.S. dollar.

BY Doug Kass · Jun 25, 2025, 5:59 AM EDT

Added to index shorts:

* SPY $607.31

* QQQ $540.62

BY Doug Kass · Jun 25, 2025, 5:48 AM EDT