From JPMorgan:

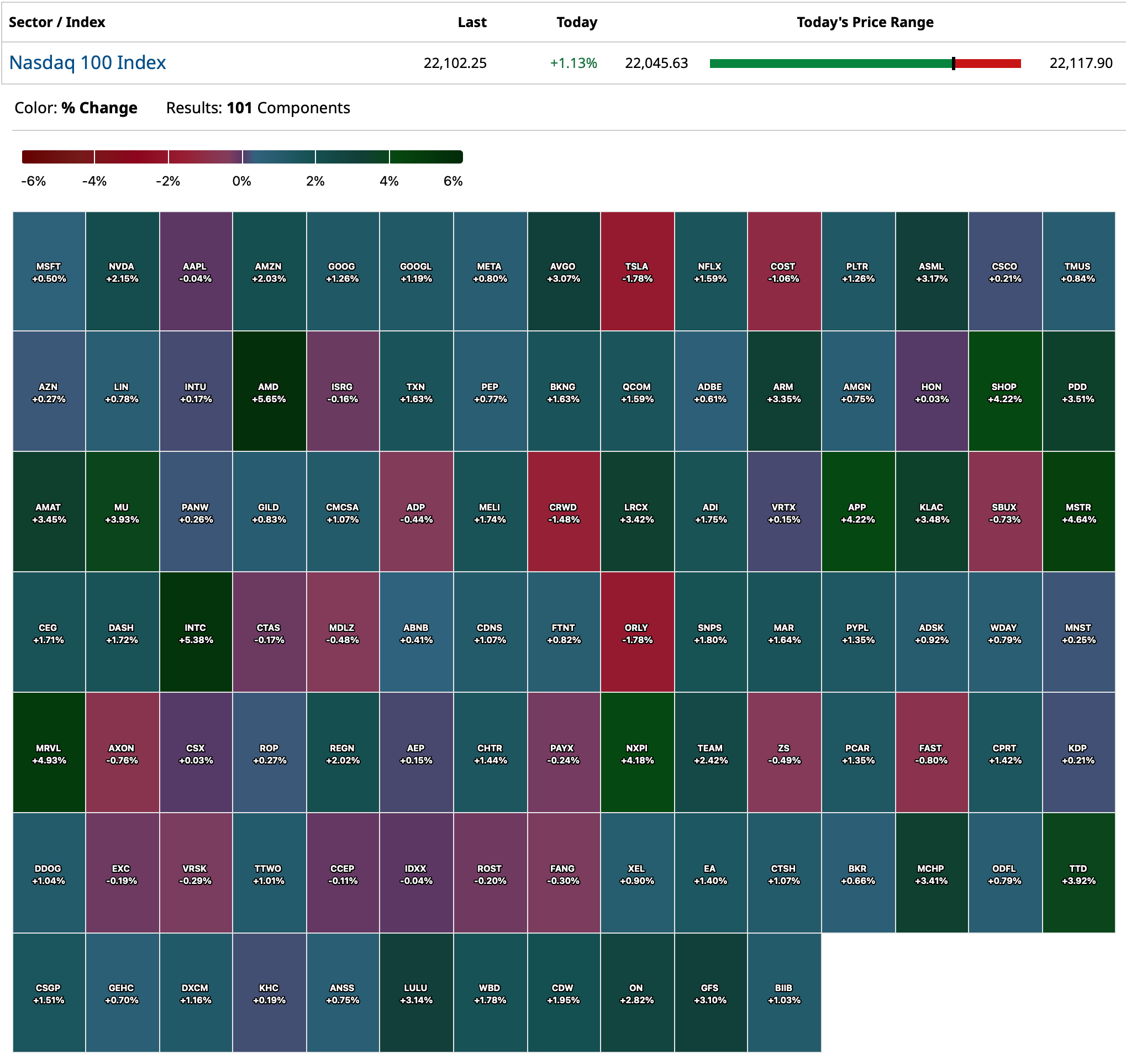

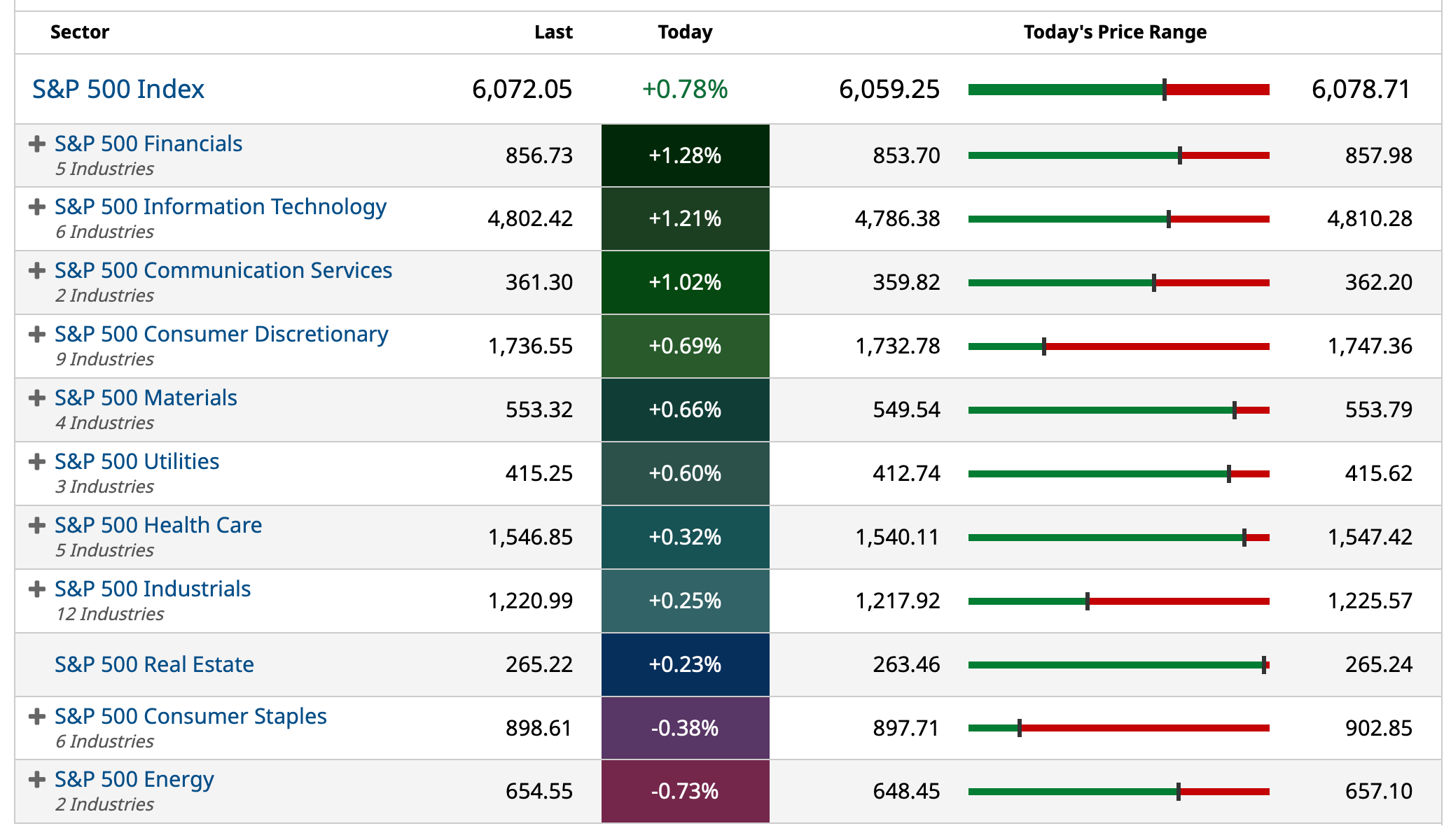

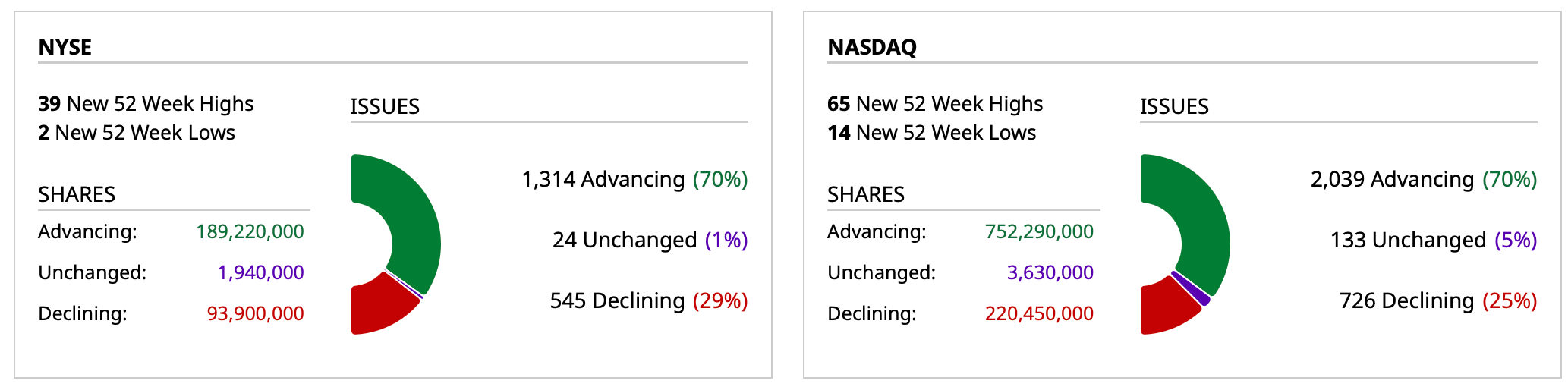

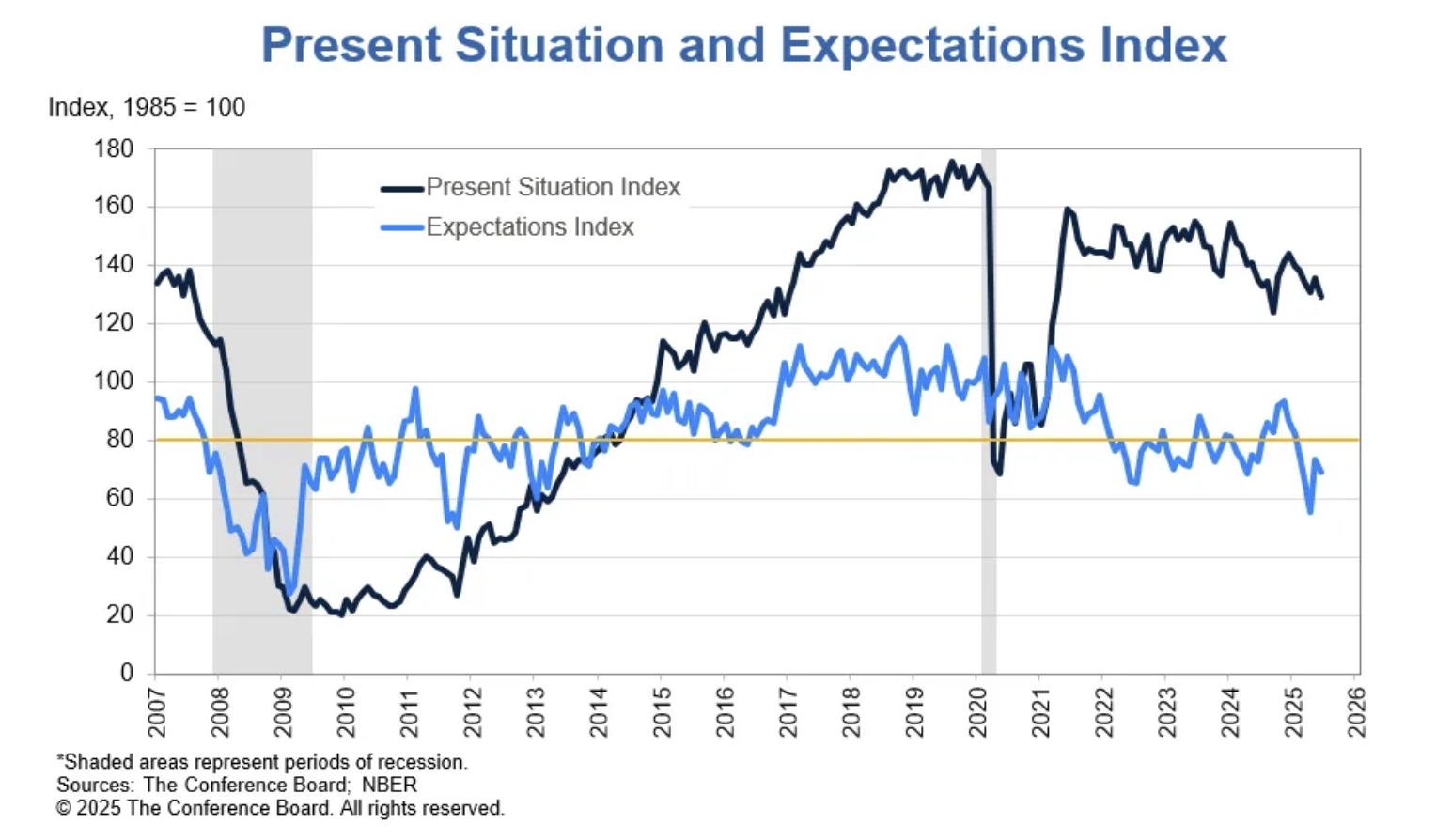

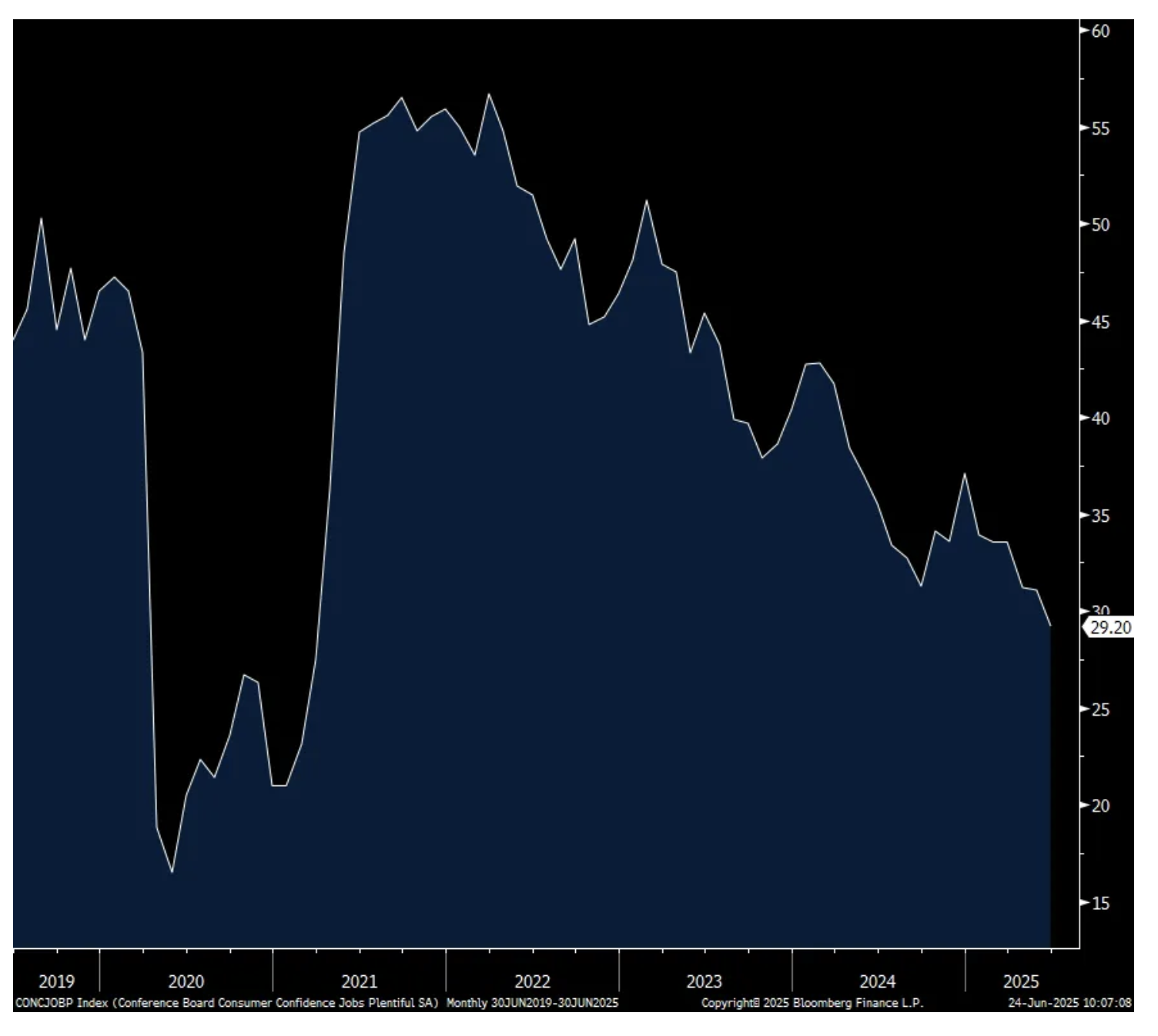

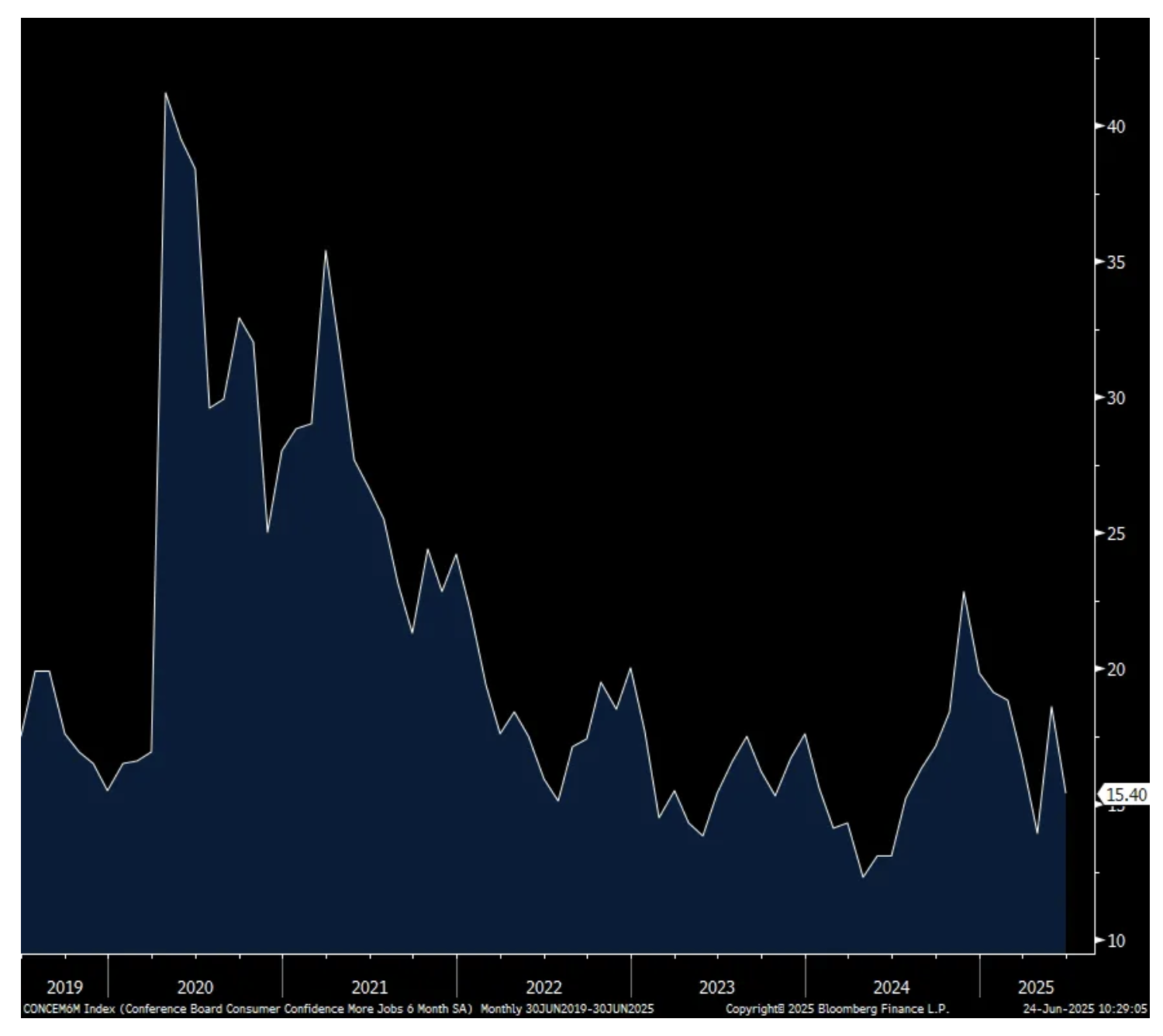

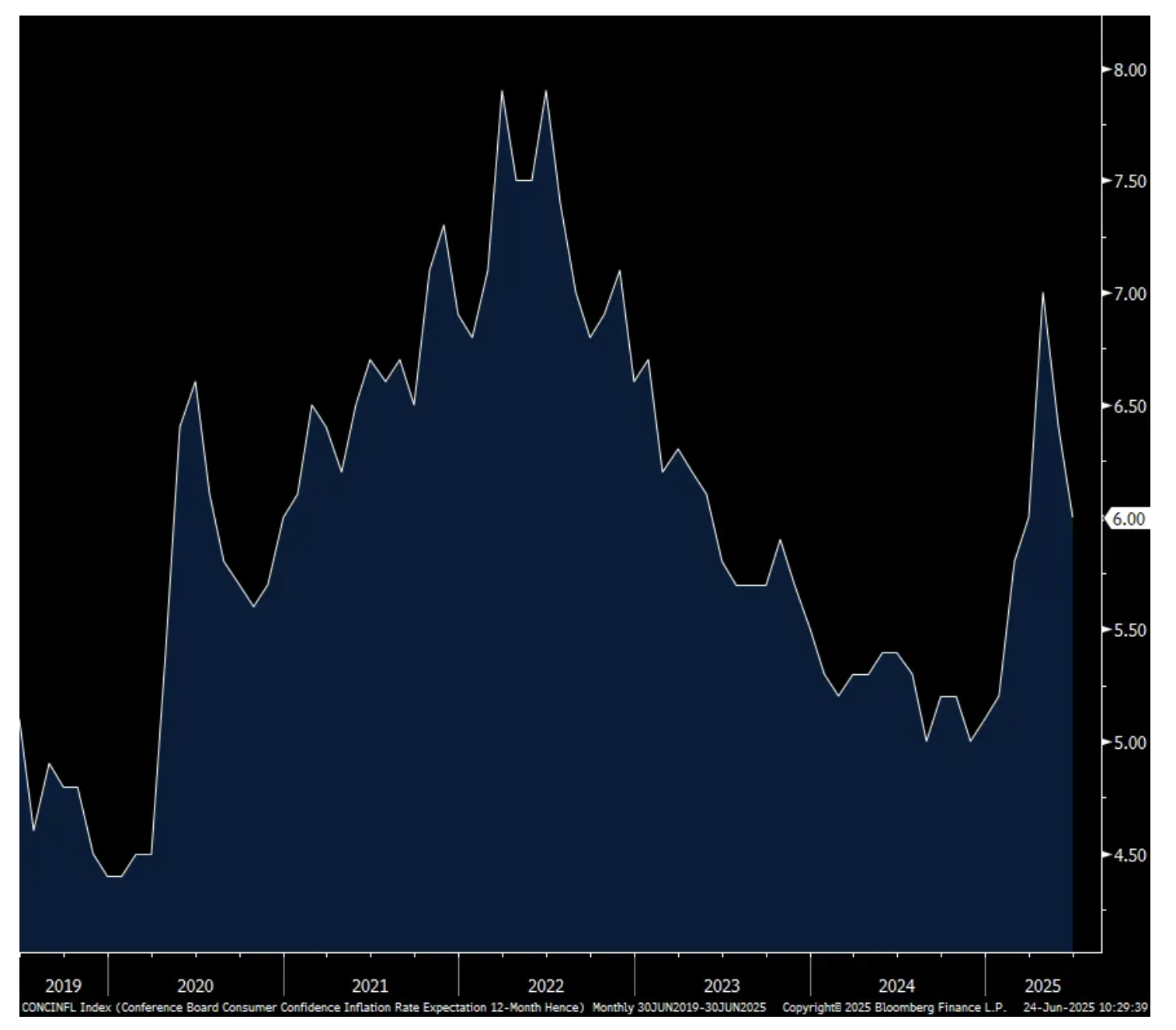

US: Futs are higher as part of a global risk-on trade. Trump announced a ceasefire between Israel and Iran after Iran’s retaliation completed. WTI has fallen 15% from Monday’s intraday high and risk assets have resumed their rally; oil shrugged off reports of Iran firing a missile to resume its move lower. Adding fuel to the rally is Fedspeak on rate cuts as soon as July; Powell testifies at 10am, day 1 of 2. Pre-mkt, Mag7 are higher led by TSLA with Semis and Cyclicals ex-Energy also higher. The yield curve is twisting steeper as USD decline continues. Cmdtys are lower, dragged by Energy, but precious metals are under pressure. Today’s macro data focus is on housing prices, Consumer Confidence, and regional Fed activity indicators.

and...

EQUITY & MACRO NARRATIVE

With Israel/Iran seemingly defused, the market is resuming its march to/through all-time highs.; the SPX is ~2% below ATHs and we are entering a seasonally strong period for the NDX. With this geopolitical risk behind us, the Market is refocusing on the macro picture, preparing for earnings, and watching the looming deadline on the expiration of the tariff moratorium. We shift our view back to Tactically Bullish with the bullish hypothesis based on resilient macro data, positive EPS growth, and thawing trade war rhetoric. An additional tail-wind comes from dovish Fedspeak and lower energy prices. Below we share some takes on the Israel/Iran situation before going into more detail on our view with the associated Monetization Menu.

· HF PM – A symbolic, face-saving attack which was telegraphed in advance. Nothing to see here. Bigger risk will be the medium-term. Where is the uranium? Where are the centrifuges? Does Iran kick out inspectors? Do they reconstitute the nuclear program at another, less penetrable location, sucking the US back into a multi-year conflict?

· TOM SKINGSLEY (JPM Commodities) – Oil market reacting favorably to Iranian retaliation headline, very well telegraphed retaliation, no oil supply impact and with limited scope to continue up the escalation ladder on both the Iranian and US side (given current information). As we have seen from the first 5 mins of trading last night, risk premium continues to exit the market both in terms of flat price and vols. Trading are flagging this statement as key here: Iran's Supreme National Security Council said in a statement that the operation against US forces in Qatar's Al-Udeid base was successful, and that "the number of missiles used equaled the number of bombs the US employed in its attack on Iran's nuclear facilities." They [JPM Trading Desk] view this as a near max bearish outcome for a retaliation, a face saving attack with public communication they view it as proportional.

· US MKT INTEL VIEW – Now that we have moved past this particular geopolitical risk, the near-term setup is favorable for stocks. Our framework for the Tactical Bull Case is (i) resilient macro data; (ii) positive earnings growth; and (iii) an improving trade war rhetoric. Additional color on those points follows but the new information is the shifting narrative from the Fed which is dovish, and the Market is trading as though we see the easing cycle begin in July, should the inflation data hold. Probability of a Sept cut increased from 65% on Friday to 73% today; July probability increased from 16% to 21%. Keep an eye on the yield curve as a steepening tends to aid the Value trade.

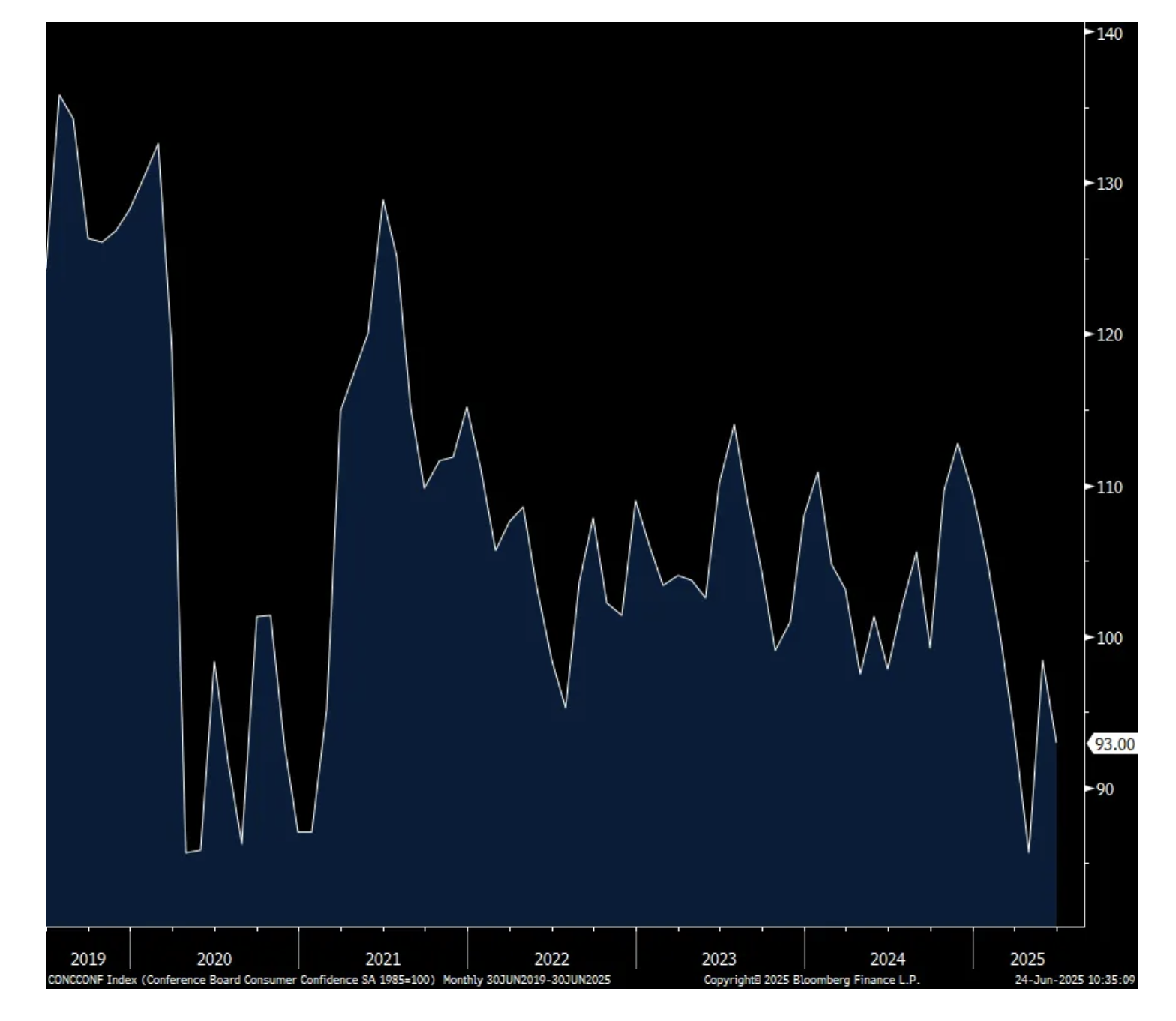

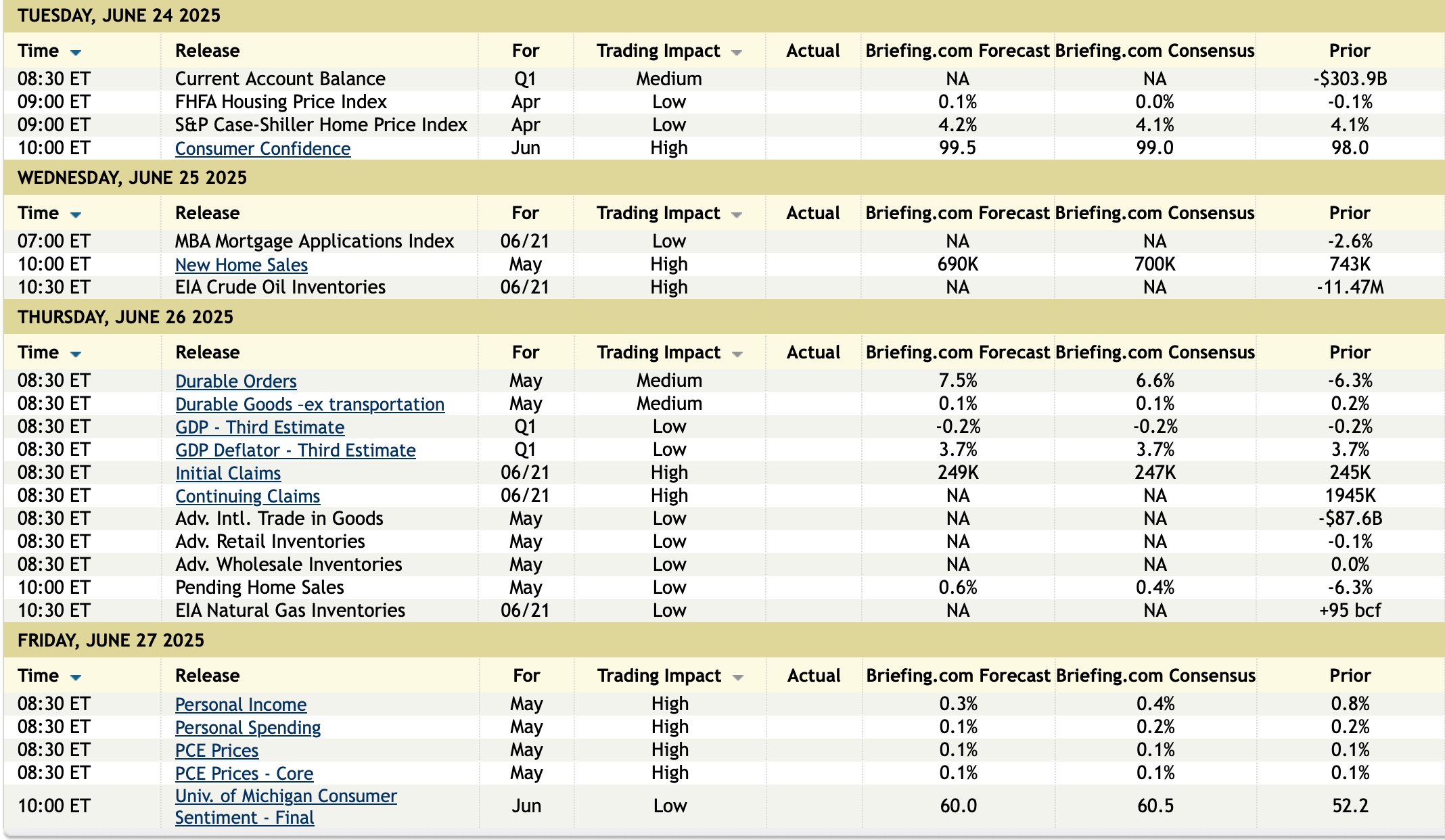

o RESILIENT MACRO DATA – the key is NFP/Initial Jobless Claims where our view is that NFP above ~100k and Initial Claims below ~275k keep this market bid. CPI will continued to be monitored for signs of inflation creeping into official prints. Separately, things like Flash PMIs and Retail Sales are important for understanding growth potential. Lastly, beaten down areas of data such as housing data can trigger some strong moves evidenced by yesterday’s 2.7% move in XHB following a better than expected Existing Homes print (4.03mm vs. 3.95mm survey; 4.00m prior).

o POSITIVE EARNINGS GROWTH – SPX earnings in 25Q1 printed +12.9% growth YoY; Mag7 printed +27.7%. For 25Q2, the SPX is expected to print +4.9% earnings growth YoY; Mag7 is expected to print +14.0%. During the first two months of the quarter, analyst EPS cuts totaled to 4.0% vs. 2.5% being the long-term average. One key risk is the market’s reaction to potentially muddled forward guidance. In Q1, Mislav noted, “Despite the healthy Q1 earnings delivery, stock price reaction to beats was more muted. Companies missing estimates are being penalized by more than typical, while those beating estimates are being rewarded by less than average”.

o IMPROVING TRADE WAR RHETORIC – Recent headlines point to potential deals with the EU, India, Japan, and Vietnam around the July 9 expiration of the tariff moratorium. Bessent had mentioned rolling that date for countries negotiating in good faith. A reversion to ‘Liberation Day’ levels would be negative for risk assets and think the Trump Put kicks in before that happens. If not before that day, the subsequent hit to risk assets and spike in vol would likely re-active the Trump Put. We see a full return to ‘Liberation Day’ levels as a low probability event.

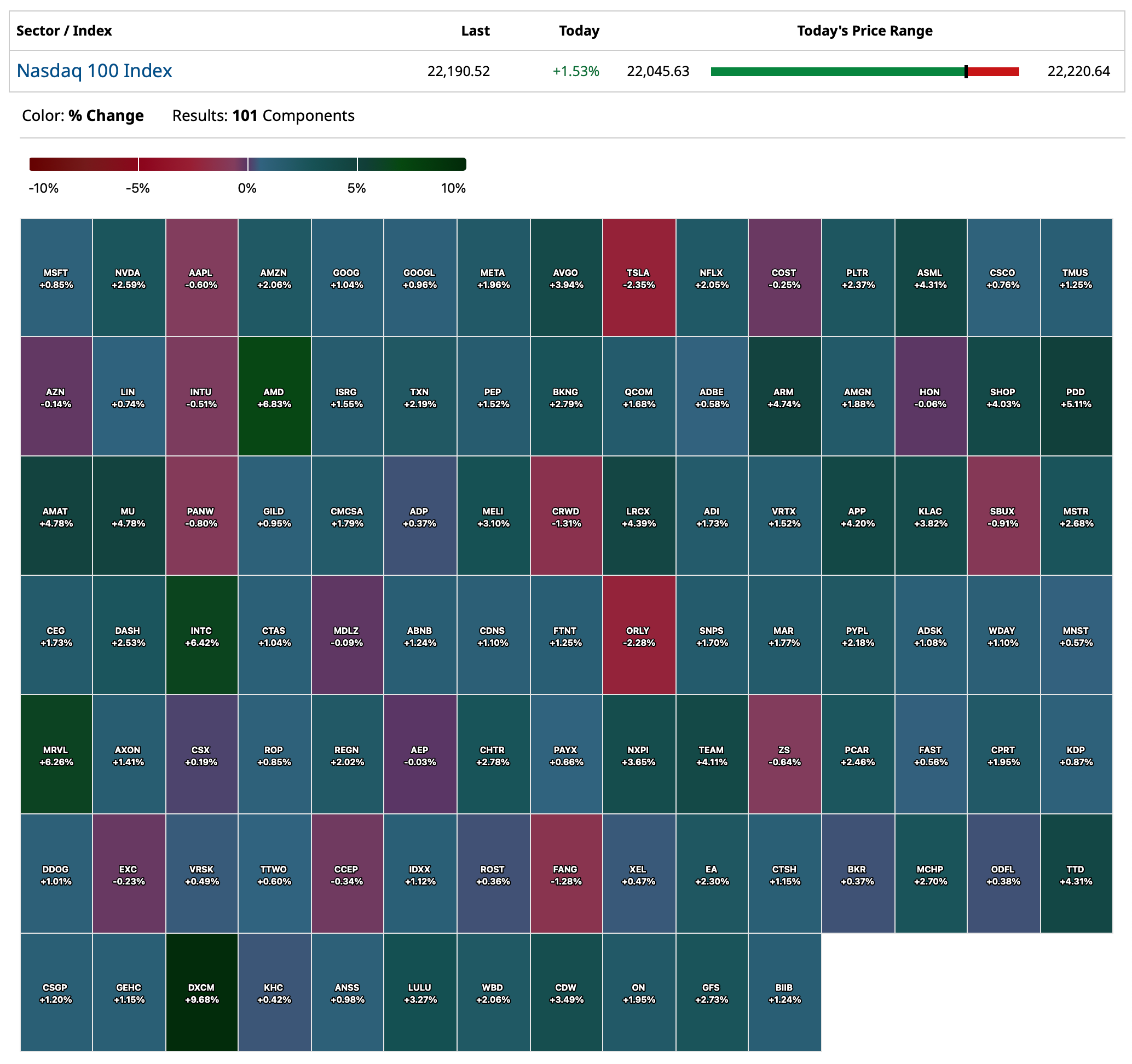

o SEASONALITY – We are entering positive seasonality for the NDX. Over the last 25 years, the NDX has delivered an average return of 2.1%, the third strongest month of the year behind Oct/Nov. NDX has printed positively in 16 of the last 17 years, 94%, averaging a 4.6% return in those up-years. This contrasts with Semis (SOX index) which is already in a period of seasonal weakness, with June, August, and September tending to produce negative returns.