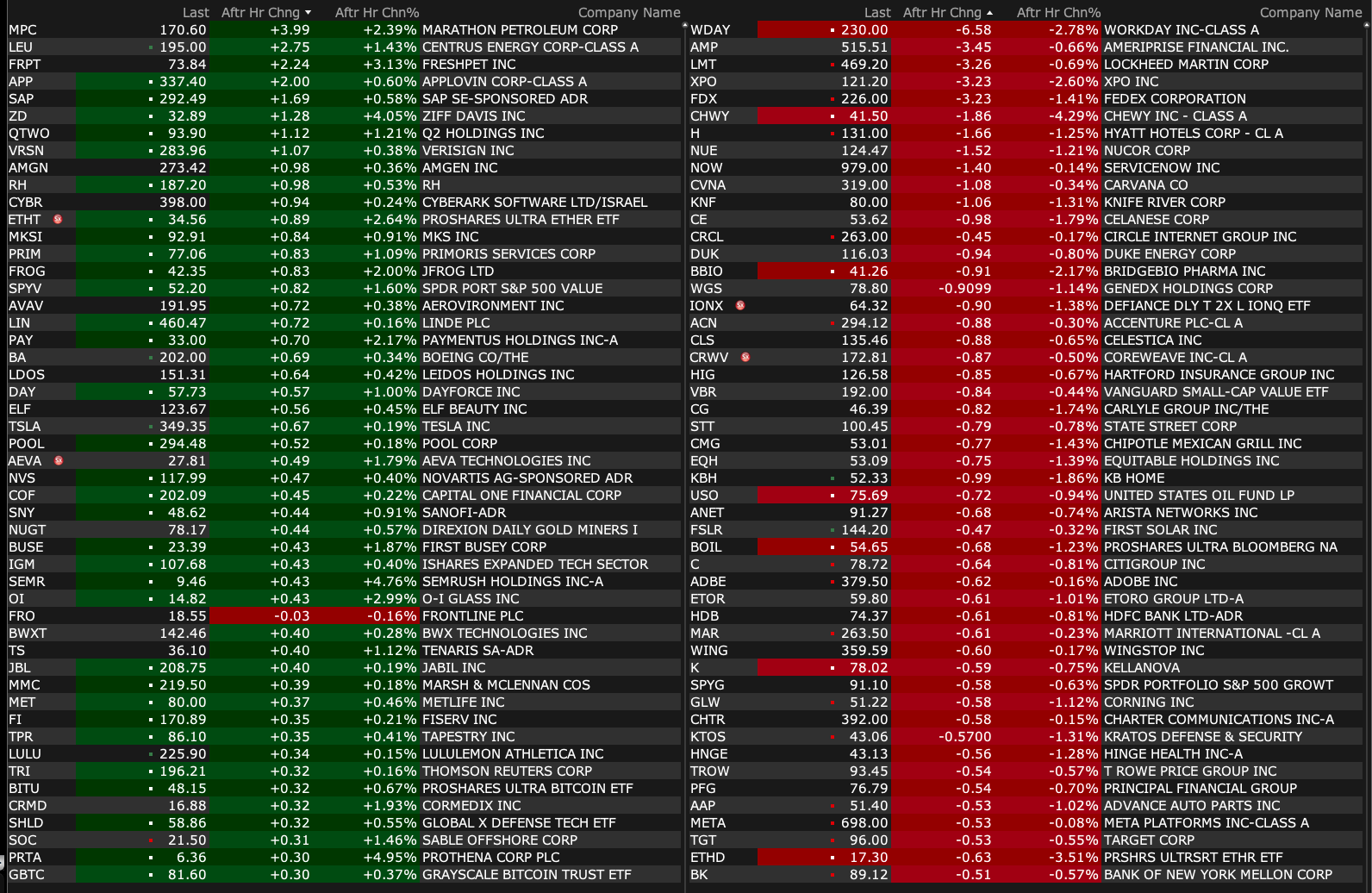

Monday's After-Hours Movers

As of 4:19 p.m.:

BY Doug Kass · Jun 23, 2025, 4:46 PM EDT

As of 4:19 p.m.:

BY Doug Kass · Jun 23, 2025, 4:46 PM EDT

BY Doug Kass · Jun 23, 2025, 4:33 PM EDT

Thanks for reading my Diary today.

Enjoy your evening.

Be safe.

BY Doug Kass · Jun 23, 2025, 4:02 PM EDT

Adding to TSNDF, GTBIF and TCNNF.

BY Doug Kass · Jun 23, 2025, 3:43 PM EDT

When observing the parade of "talking heads":

Investment wisdom and vision are always 20/20 when viewed in the rear-view mirror.

BY Doug Kass · Jun 23, 2025, 3:36 PM EDT

Here are today's "things:"

* I traded SPY (short at $596.89, cover at $594.46)/QQQ (cover at $526.86, short at $528.99) common back and forth... profitably.

* Shorted ARKK at $68.04, HOOD at $78.10, NVDA at $143.75 and SCHW at $89.31.

* Added to large GRNY short at $21.61.

* Shorted TSLA $349.95.

BY Doug Kass · Jun 23, 2025, 2:20 PM EDT

Shorted more GRNY at $21.61.

BY Doug Kass · Jun 23, 2025, 2:05 PM EDT

Shorting more indices on a scale higher:

* SPY$598.95

* QQQ $531.54

BY Doug Kass · Jun 23, 2025, 1:56 PM EDT

With S&P cash +42 handles I am back shorting the indices:

*SPY $598.56

* QQQ $531.15

BY Doug Kass · Jun 23, 2025, 1:53 PM EDT

I have covered today's index (common) shorts for a profit after a near 40-handle reversal in the S&P in the last few minutes.

I plan to reshort on strength.

Back to very small on index shorts.

BY Doug Kass · Jun 23, 2025, 12:48 PM EDT

Axios is reporting that "reportedly Trump administration is preparing for Iran attack on US Gulf bases."

BY Doug Kass · Jun 23, 2025, 12:40 PM EDT

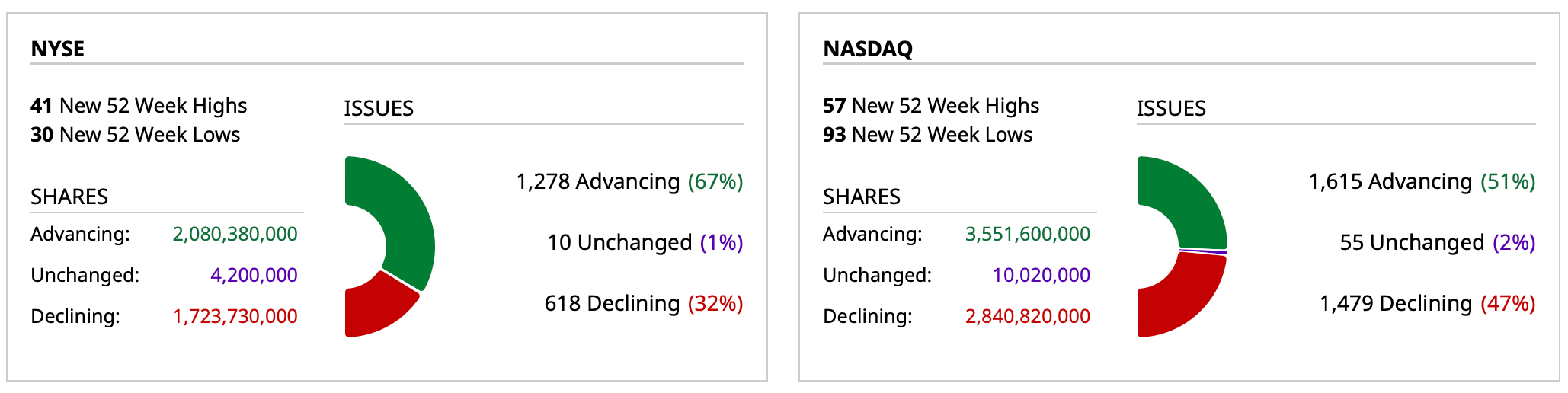

As of 12:13 p.m.:

BY Doug Kass · Jun 23, 2025, 12:35 PM EDT

BY Doug Kass · Jun 23, 2025, 12:25 PM EDT

In this small selloff from the highs, it is interesting to note that financials have led to the downside — after being early winners in the morning ramp.

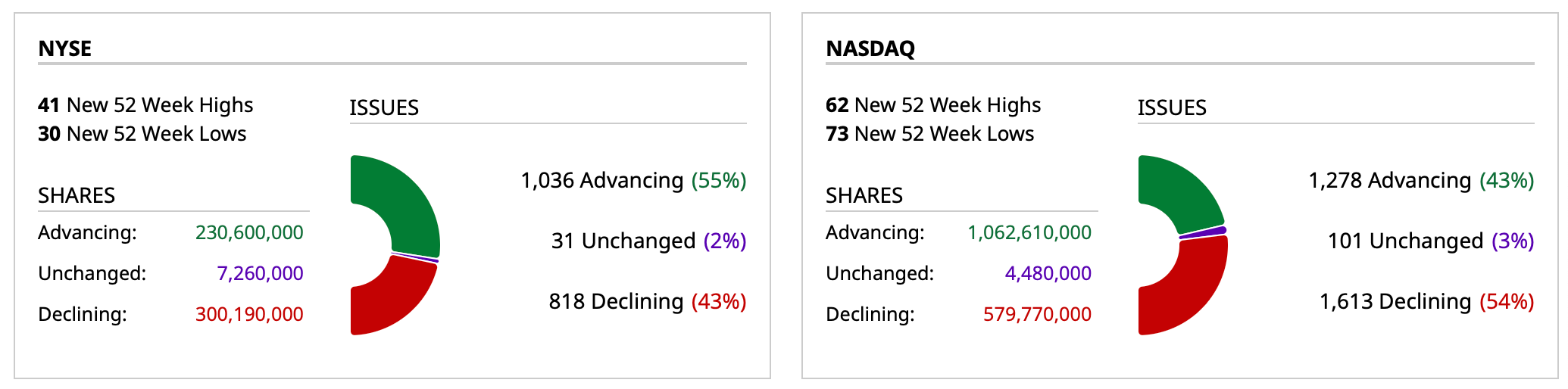

BY Doug Kass · Jun 23, 2025, 12:16 PM EDT

- NYSE volume 1% below its one-month average;

- NASDAQ volume 7% below its one-month average;

- VIX index: down 0.87% to 20.44

BY Doug Kass · Jun 23, 2025, 11:20 AM EDT

From Peter Boockvar:

Inventory building and price commentary stood out in PMI/Bowman joins Waller in getting dovish

The June S&P Global US PMI composite index fell a touch m/o/m to 52.8 from 53. The manufacturing component held at 52 while services slipped to 53.1 from 53.7. I’ll say again, for some reason their services component does not include the key areas of retail/wholesale trade and construction.

The manufacturing index holding above 50 can be attributed mostly to the inventory restocking going on in response to tariff policy. S&P Global said “June saw further inventory building in manufacturing. Purchasing of inputs was expanded at the fastest rate in 37 months, causing inventories of inputs to also rise again, increasing at the 2nd fastest rate in over three years following May’s survey record rise. Inventories of finished goods at factories meanwhile registered the largest rise for nine months; a rise that was among the greatest in the survey’s 18 year history.” A gain in employment also helped this component.

New orders for both manufacturers and service providers dipped a touch from May and S&P Global said gains were still seen, “driven by rising domestic demand” as “This serviced to mask a fall in export orders in June.” I’m guessing in part due to reduced travel, “Services exports have suffered the largest quarterly contraction since late 2022 in the three months to June.”

What also stood out in the report was the commentary on inflation/pricing with the biggest influence not surprisingly being tariffs. “Price pressures rose sharply across both manufacturing and service sectors during June, the former reporting an especially steep increase, and again commonly linked to tariffs.” On the manufacturing side, “input prices and selling prices both rose at rates not seen since July 2022, as higher costs were passed on to customers. Close to two-thirds of all manufacturers reporting higher input costs attributed these to tariffs, whilst just over half of respondents linked increased selling prices to tariffs.”

With services on this, “prices also rose sharply…likewise often attributed to tariffs but also reflecting higher financing, wage and fuel costs. Service sector input costs and selling prices nonetheless rose at slower rates than in May, in part reflecting more intense competition.”

Combining the two, “the overall rise in costs was still the 2nd largest since the start of 2023. The rise in prices charged for goods and services was the 2nd highest since September 2022.”

Bottom line, inventory builds stood out as did the commentary on tariff induced inflation (for now).

While Jay Powell sounded last week more inclined to wait on how this plays out, Governor Michelle Bowman is joining Chris Waller in believing that July should be a rate cut possibility. She said today “Should inflation pressures remain contained, I would support lowering the policy rate as soon as our next meeting in order to bring it closer to its neutral setting and to sustain a healthy labor market.”

Yields are at the lows of the day in response. The fed funds futures are now pricing in fully 50 bps of cuts this year and now a 20% chance of a 3rd. After Powell spoke but before Waller, the odds of a 2nd were about 70%.

BY Doug Kass · Jun 23, 2025, 10:57 AM EDT

Keep in mind the Fed's Bowman is likely auditioning to be Fed Chair:

She commented this morning that she is "Open to cut rates as soon as July if inflation remains subdued; Haven't seen from impact from trade developments; Labor market is solid, but signs of softness are emerging."

As well:

- Tariffs likely to have small impact on inflation; Upward pressure from tariffs appear to be offset

- Upcoming leverage rule proposal a first step in reforming distorted bank capital requirements

- Fed to take comment and look at potential fixes on enhanced supplementary leverage ratio (ESLR)

- Fed to host conference July 22nd conference on bank capital

BY Doug Kass · Jun 23, 2025, 10:29 AM EDT

With S&P cash +34 handles, I have moved to medium-sized short the indices.

BY Doug Kass · Jun 23, 2025, 10:18 AM EDT

* Today, in the business media, everyone will represent themselves as a Middle East expert.

* I am not a Middle East expert but I am of the belief that the bombing in Iran confirms an ongoing (and geopolitical) risk that is being underappreciated by investors (OVER THE INTERMEDIATE TERM) who are willing to pay 23x for earnings.

* In an unemotional manner, I am expanding my short exposure in the early morning market "strength."

On Sundays, the bulls get so bored

When they are asked to show off for us

There is the sun, the sand, and the arena

There are the bulls ready to bleed for us

It's the time when grocery clerks become Don Juan

It's the time when all ugly girls

Turn into swans, hah

Who can say of what he's found

That bull who turns and paws the ground

And suddenly he sees himself all nude, hah

Who can say of what he dreams

That bull who hears the silent screams

From the open mouths of multitudes

- Jacques Brel Is Alive and Well And Living in Paris, The Bulls (Les taureaux)

No doubt this morning the business media will look at the subdued response in stock futures as an undeniably bullish indicator.

The bulls will also rejoice at the modest reaction.

However, I think this is short-sighted.

I view the near-term reaction differently than both the business media and the bullish cabal.

Let me explain.

Tactically (meaning over the next few weeks/months vs. next few hours/days) I view the weekend news (i.e., U.S. bombing Iran's nuclear facilities) as less of a short-term issue and more of an intermediate-term issue — as it confirms my growing concerns regarding poor outcomes.

In last week's Diary columns I consistently highlighted the multiple uncertainties (many of which could have an adverse impact on our capital markets). Several of my statements "bear" rereading:

By contrast, over the last decade I have reminded subscribers that I wake up every morning before trading starts and I ask these questions of myself. Unfortunately I don't like the answers — those answers have haunted me and they are potentially market and valuation unfriendly:

and...

Let's now shift to my near-term concerns that have been thoroughly dismissed in The Bull Market In Complacency.

On Monday (The Bear Market Will Be Back) and Tuesday (The Bear Market Will Be Back (Like Before)... I'll Fight the Fight and Win the War) I outlined a number of factors that investors should be concerned with:

* We face the highest geopolitical risks in many decades (which will not be resolved quickly).

* We face the largest level of social and political risks in the U.S. since the Vietnam war.

* We face the greatest chance of "slugflation" (slowing economic growth and sticky inflation) since the 1970s.

* We face the biggest threat that the U.S. dollar and capital markets will no longer be a "safe haven" in modern history.

* We face the greatest debt load and deficit ever — and neither party seems to favor any fiscal discipline whatsoever.

* We face the largest capital spending spree in history (on artificial intelligence) — though the return on that investment is less certain (dot-com, it feels like deja vu all over again.) (More on this shortly.)

* We face a viable alternative to equities in fixed income (for the first time in 15 years) as bonds present an equity-equivalent yield with limited risk and volatility.

Unlike many I see the modest (or NO!) reaction to the U.S. bombing in this morning's futures not as a frustrating reaction but as an opportunity to strategically expand my short exposure (especially given current valuations levels):

BY Doug Kass · Jun 23, 2025, 9:30 AM EDT

11:30 a.m.: Treasury hosts a $76B 3 and $68B 6-Month Bill Auction

3 a.m.: Fed Board Governor Waller (Voter) gives opening remarks before the 2025 International Journal of Central Banking Conference, Prague, Czech Republic (Text available. No Q&A. No webcast);

10:00: Fed Vice Chair for Supervision Bowman (Voter) speaks on monetary policy and banking before the 2025 International Journal of Central Banking Conference, Prague, Czech Republic (Text available. No Q&A. Webcast);

1:10 p.m.: Fed Bank of Chicago President Goolsbee (Voter) participates in a moderated question-and-answer session before the Milwaukee Business Journal Mid-Year Outlook 2025, Milwaukee, WI (Embargoed text TBD. Livestream);

2:30: Fed Governor Adriana Kugler (Voter) gives welcome remarks before a "Fed Listens" event hosted by the Federal Reserve Bank of New York, Schenectady, NY (Text available. No Q&A. Livestream);

2:30: Fed Bank of New York President Williams (Voter) speaks at a Fed Listens event hosted by SUNY Schenectady Community College, NYC

BY Doug Kass · Jun 23, 2025, 9:22 AM EDT

-CDTX +85% (announces Topline Results from its Phase 2b NAVIGATE Trial Evaluating CD388, a Non-Vaccine Preventative of Seasonal Influenza)

-SPTN +49% (to be acquired C&S Wholesale Grocers for $26.90/shr in cash)

-EXEL +20% (announces Zanzalintinib in Combination with an Immune Checkpoint Inhibitor Improved Overall Survival in STELLAR-303 Phase 3 Pivotal Trial in Patients with Metastatic Colorectal Cancer)

-ZETA +16% (momentum potentially stemming from social media mentions)

-CRMD +15% (issues update related to its Large Dialysis Organization (LDO) customer and planned implementation in H2 2025; raises Q2 guidance)

-LAB +14% (sells SomaLogic unit to Illumina for $350M cash up front and up to $425M in total proceeds inclusive of near-term milestone payments)

-FI +6.2% (confirms plans to launch a new Fiserv digital asset platform, including a new stablecoin (FIUSD) that will be added to Fiserv’s existing banking and payments infrastructure by the end of the year)

-NTRS +5.9% (Bank of New York Mellon said to be interested in merger with the company)

-LI +4.5% (strength ahead of upcoming SUV launch)

-DJT +2.9% (announces $400M share repurchase authorization)

-CRCL +2.6% (confirms strategic collaboration with Fiserv)

-FMC +2.4% (Wells Fargo Raised FMC to Overweight from Equal Weight, price target: $50)

-EL +2.3% (Deutsche Bank Raised EL to Buy from Hold, price target: $95)

-AMD +2.1% (Melius Research Raised AMD to Buy from Hold, price target: $175)

-CMPS -35% (reports data from the ongoing Phase 3 COMP005 trial)

-HIMS -22% (Novo Nordisk confirms to terminate collaboration with Hims & Hers Health, Inc. due to concerns about their illegal mass compounding and deceptive marketing)

-GUTS -15% (reports 3-Month REVEAL-1 Cohort Data for Revita)

-WOLF -11% (entered into a Restructuring Support Agreement with key lenders)

-LRMR -8.5% (announces FDA Recommendations on Safety Database, and Other Details of Nomlabofusp BLA Submission for Friedreich’s Ataxia Program)

-NVO -6.8% (confirms to terminate collaboration with Hims & Hers Health, Inc. due to concerns about their illegal mass compounding and deceptive marketing)

-CMC -4.1% (earnings, guidance)

-SMCI -3.5% (files to sell offering of $2.0B of Convertible senior unsecured notes due 2030)

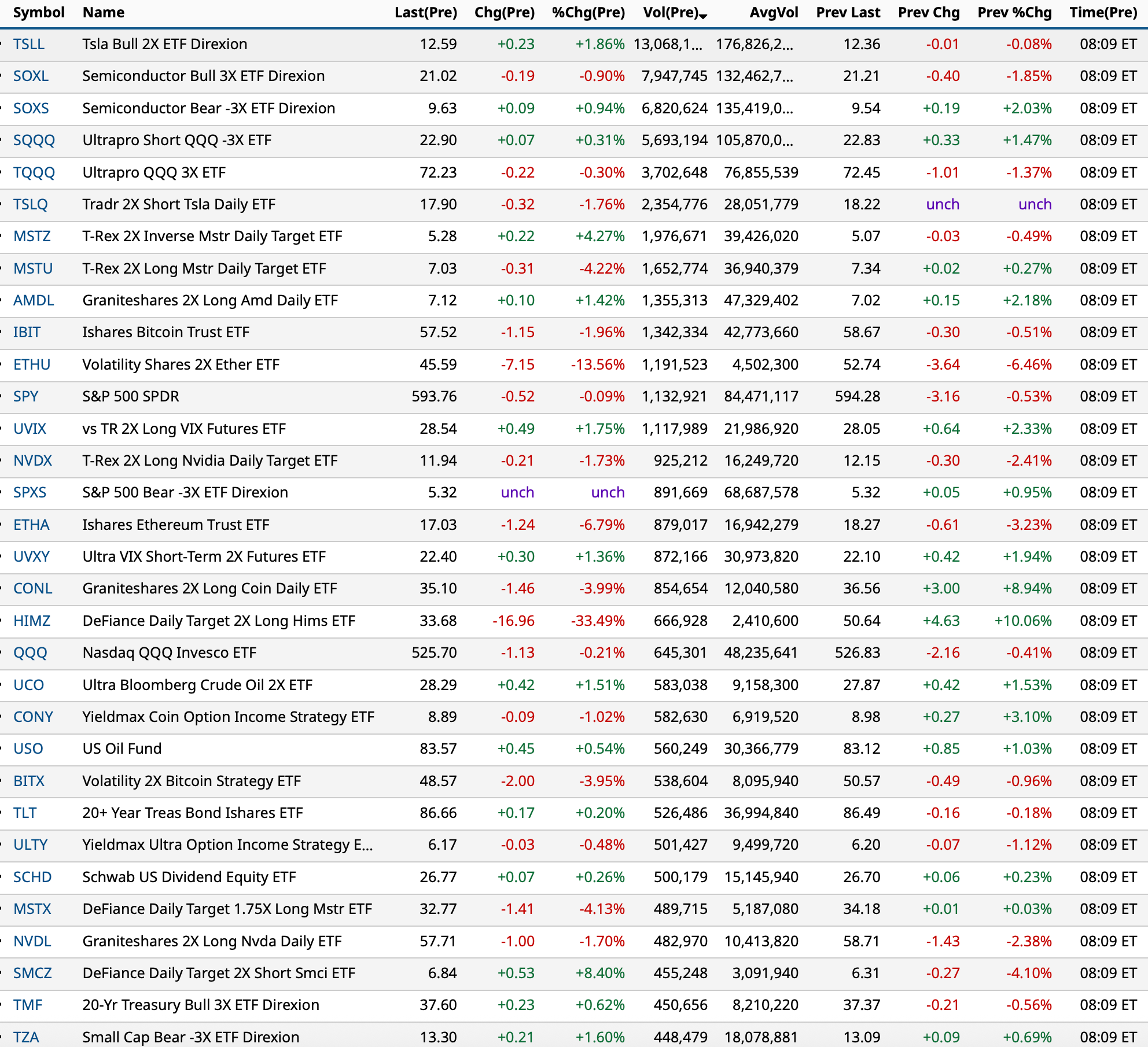

BY Doug Kass · Jun 23, 2025, 9:15 AM EDT

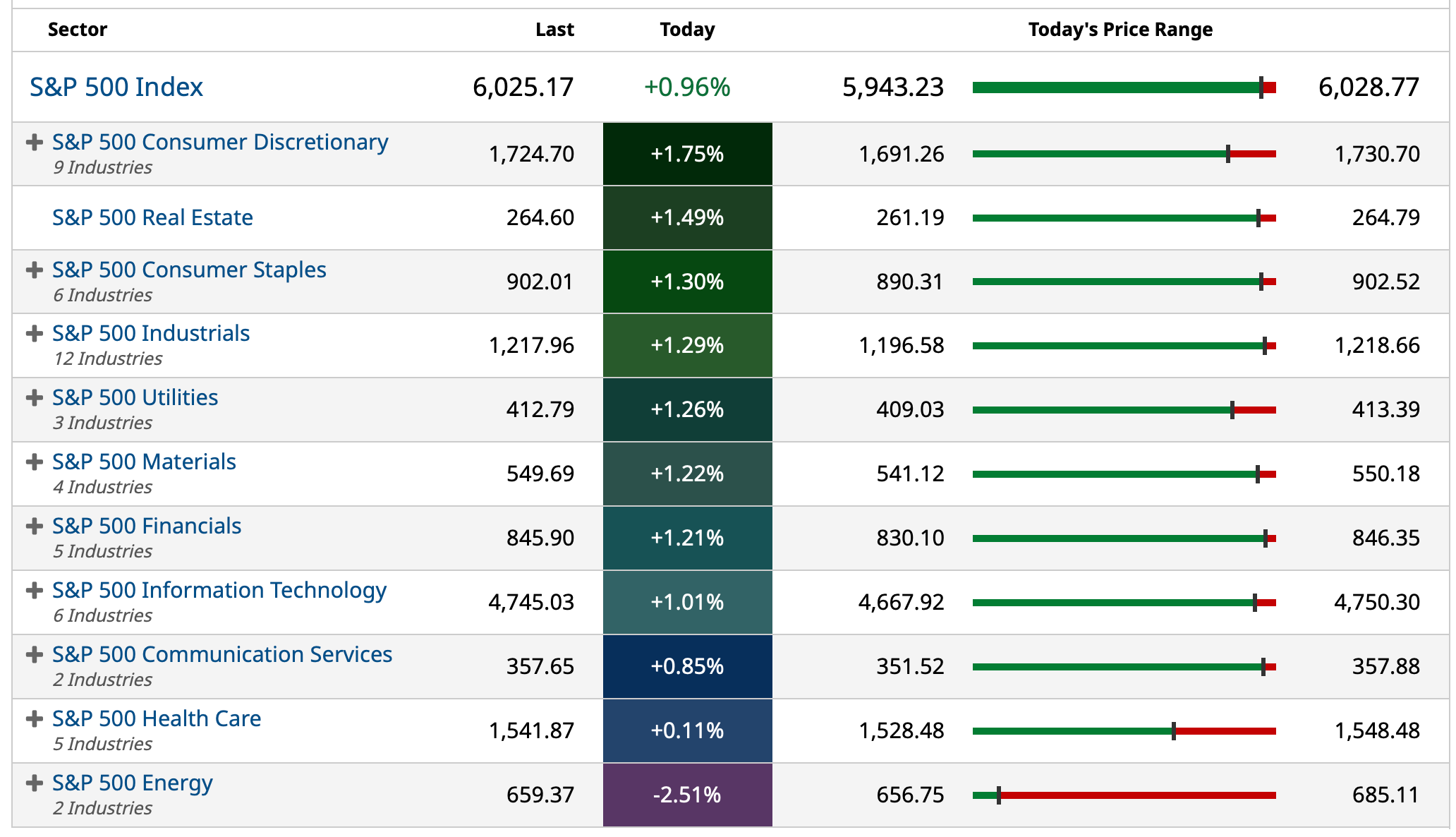

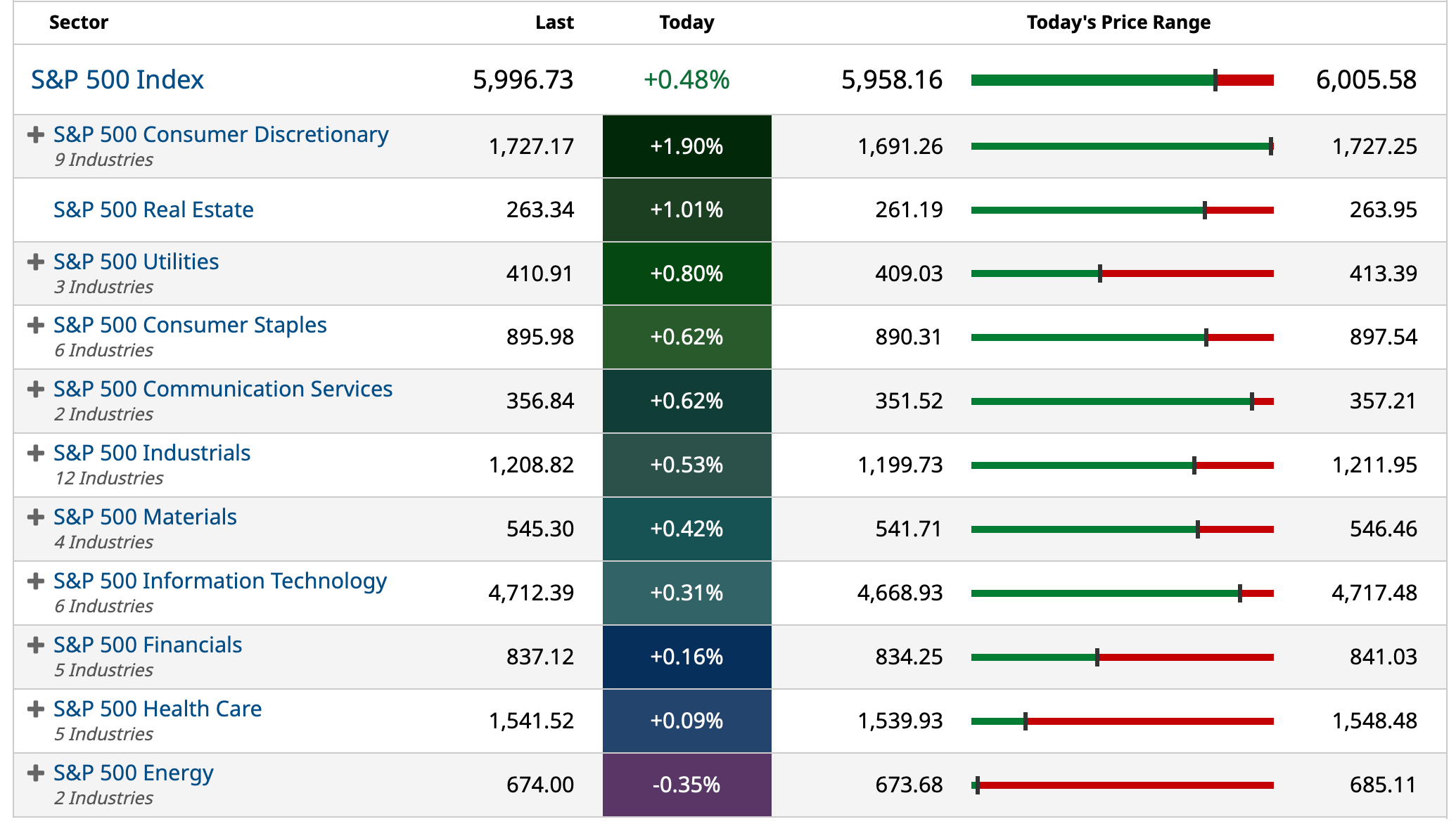

Charts from 8:09 a.m. ET:

BY Doug Kass · Jun 23, 2025, 9:00 AM EDT

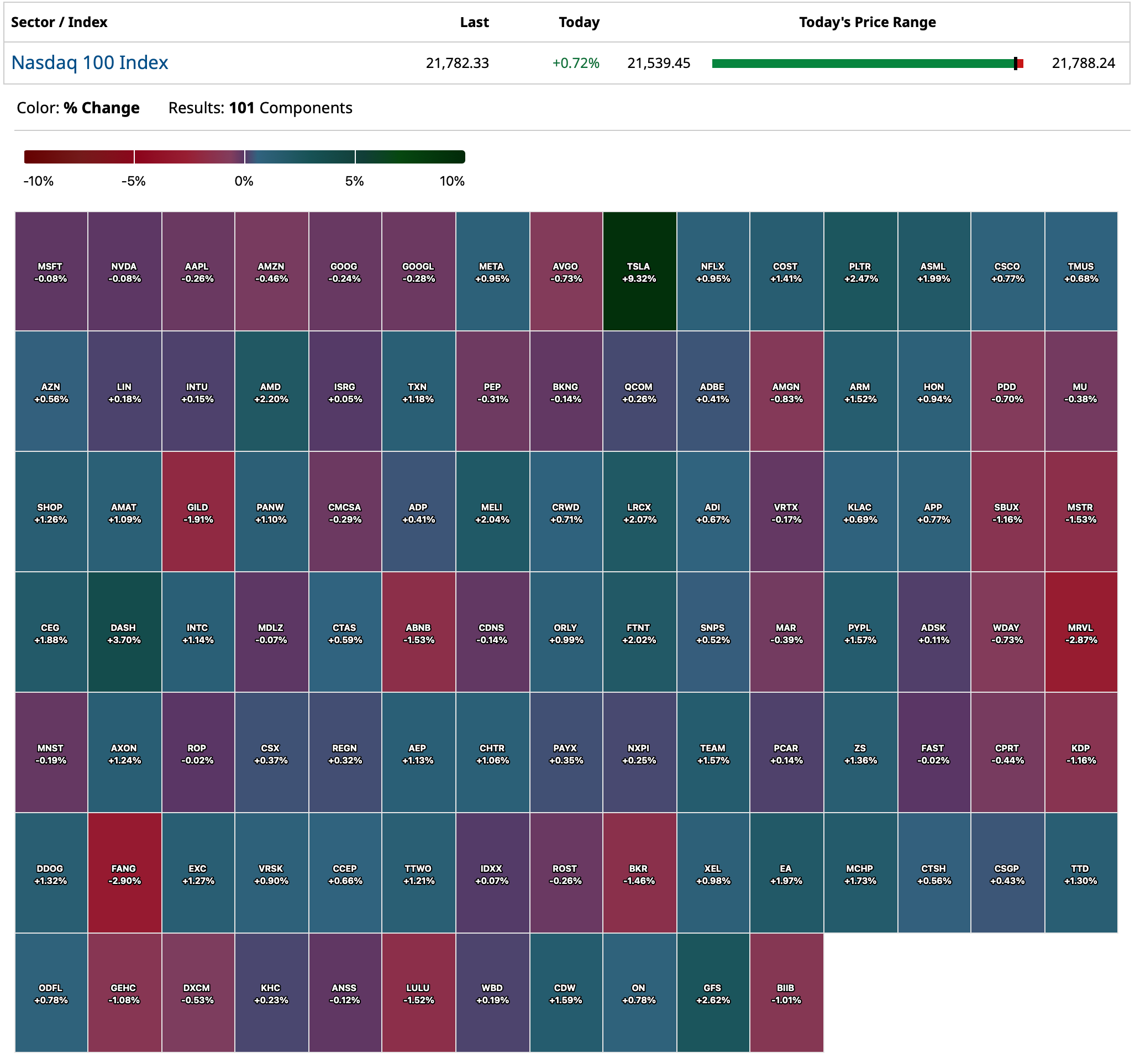

Chart from 8:19 a.m. ET:

BY Doug Kass · Jun 23, 2025, 8:45 AM EDT

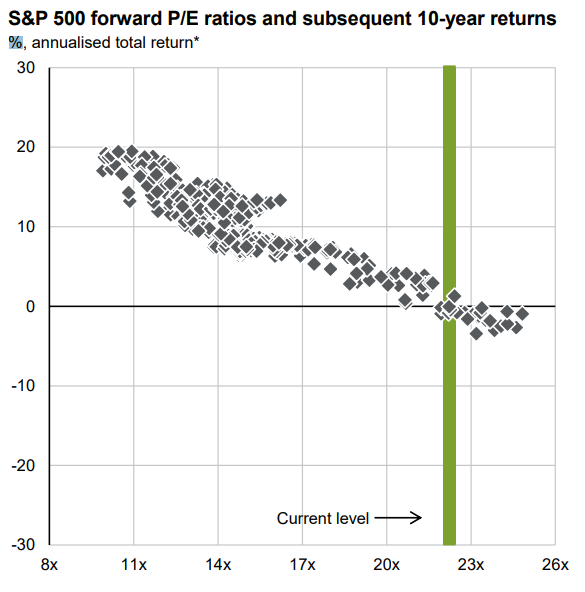

Thanks to John Mauldin:

BY Doug Kass · Jun 23, 2025, 8:00 AM EDT

BY Doug Kass · Jun 23, 2025, 7:00 AM EDT

From JPMorgan:

US: Futs initially fell 70bp after the weekend escalation in the Middle East tension (US hit three key nuclear facilities in Iran) but rebounded overnight with oil prices falling. Mag 7 are mostly higher, led by TSLA (+1.5% after the Robotaxi launch), META (+0.4%) and GOOG/L (+0.4%). Bond yields are largely unchanged; USD is 64bp higher. Commodities are largely flat.

and...

EQUITY & MACRO NARRATIVE

SPX fell -22bp last week amid elevated geopolitical risks since the initial attack on Iran’s nuclear program and military leadership on June 12th; NDX and RTY lost -43bp and -17bp, respectively. Oil added another +2.7% last week with WTI closing at $74.9 last Friday. FOMC last Wednesday was mostly in line with expectations: (i) the Fed maintains the forecast of 50bp cut in 2025 and sees only 1 cut in 2026; (ii) Powell indicates that the Fed will maintain its wait-and-see mode and sees policy uncertainty remaining elevated. The Retail Sales prints were largely mixed given a weaker headline number (due to auto pullback) and stronger Control Group. Progress on the trade deals remained muted at the G7 meetings.

Over the weekend, the major development came from the Middle East as the US hitting three key nuclear facilities in Iran; both Iran and Israel launched fresh airstrikes since US’s attacks.

· ESCALATION POTENTIAL IN THE MIDDLE EAST – Potential escalation could include: (i) attacks on US assets in the Middle East. (ii) disruption in oil supply: Iran parliament reportedly backs closing Straits of Hormuz (AXIOS), but there has not yet been explicit threats from Iran. One article from POLITICO also highlighted that cyber is one of the tool of Iran’s potential retaliation (“attacks on poorly secured U.S. networks and Internet-connected devices”). We published below in June 16th Morning Briefing: “This conflict may spread from an operation to destroy nuclear and ballistic missile capabilities to one that looks more like regime change; if the latter, then should be considered multi-month/multi-quarter type of conflict. If we avoid escalation, the negative impact on markets may be 1-3 weeks. Natasha flagged the potential for crude prices to move to $120/bbl. This would exacerbate the current trend which has seen WTI +20% MTD with gasoline +9.3%; UK and European Natgas are +13.7% and +12.7%, though returns are in USD.”

· ECON IMPACTS – Feroli (here) tells us that if crude oil prices stay around $75, that would increase gas prices by 12%. In that case, we can expect CPI to increase by 0.4%, with real consumption falling by 0.25%. However, the team does not see this increase in oil prices to significantly change the outlook: (i) the absolute level of oil prices remains low; (ii) the oil intensity of the US economy has declined; (iii) US has transformed into a net oil exporter.

· MACRO DATA – This week, the key macro data will be Global PMIs (Monday) and PCE (Friday). Feroli sees PMI-Mfg to print 51.5 vs. 52.0 prior and PMI-Srvcs to print 53.5 vs. 53.7 prior; he points out that business activity and new business indexes have been volatile this year due to “press releases frequently citing policy and economic uncertainty along with the administration’s move to cut federal budgets resulting in contract cuts.” He sees Headline PCE and Core PCE to prints 0.11% (vs. 0.1% prior) and 0.13% (vs. 0.1% prior), respectively.

· FED (FEROLI) – Last week, the September dots still shows two cuts this year with one additional in 2026. Feroli (here) points that both the FOMC statement and Powell’s press conference were more on the optimistic side as Powell indicated that business leaders are “much more positive and constructive than three months ago.” The team continues to expect only one cut this year in December.

· OTHER RISKS TO CONSIDER (below from June 16th Morning Briefing, data updated as of June 23, 2025)

o PROFIT-TAKING – YTD US returns have not been impressive but since the April 8 low, we have seen some strong moves with the SPX +19.8%, NDX +26.5%, SPX Tech sector +34.4%, SOX Index +45.4%, ARKK +67.2%, Retailers +24.0%, and WTI +25.8%. We may see investors take profits given the heightened uncertainty from geopolitics and trade. In some sub-sectors, seasonality is turning negative. E.g., SOX Index has averaged a -1.1% return in June, over the last 25 years, and then has increased that loss with an average return of -3.1% from July – September. The SOX has been seen more negative returns than positive June – Sept, with stats summarized below. Lastly, positioning in Semis appears to be stretched.

BY Doug Kass · Jun 23, 2025, 6:44 AM EDT

I added to the following shorts:

* NVDA $143.43

* HOOD $77.83

BY Doug Kass · Jun 23, 2025, 6:20 AM EDT

The S&P Short Range Oscillator slipped from 1.15% to 0.91%.

BY Doug Kass · Jun 23, 2025, 6:10 AM EDT

BY Doug Kass · Jun 23, 2025, 5:57 AM EDT

Stock futures have moved dramatically off the low of about -50 handles early Sunday night to +16 handles now.

Shorts might just about give up after such a rally from the lows, but I look at this as an opportunity to get shorter.

I am dispassionately reestablishing my index shorts:

* SPY $595.82

* QQQ $527.71

BY Doug Kass · Jun 23, 2025, 5:46 AM EDT