Closing Volume, Breadth, Sectors and Movers

Low Volume

- NYSE volume 3% below its one-month average;

- NASDAQ volume 20% below its one-month average;

- VIX index: down 6.85% to 20.12

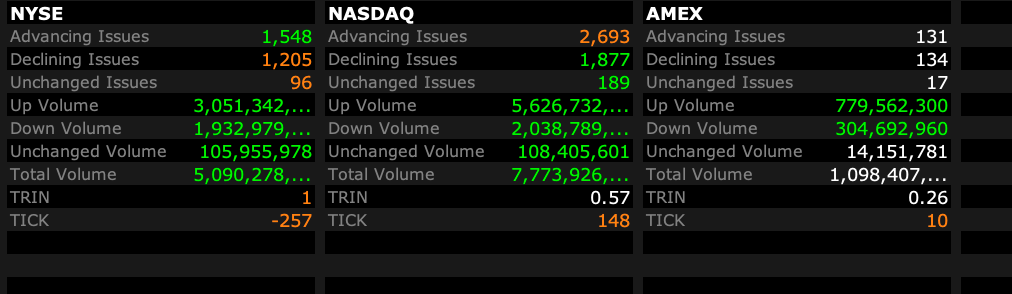

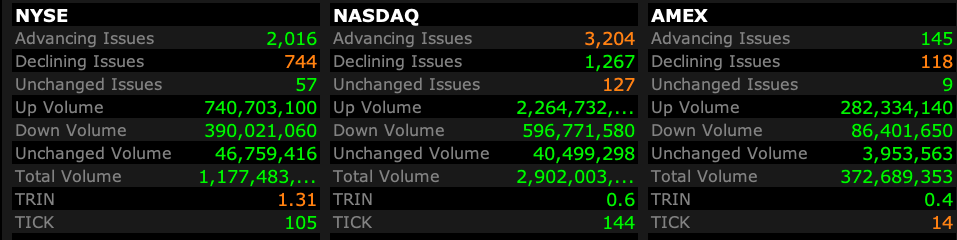

Breadth

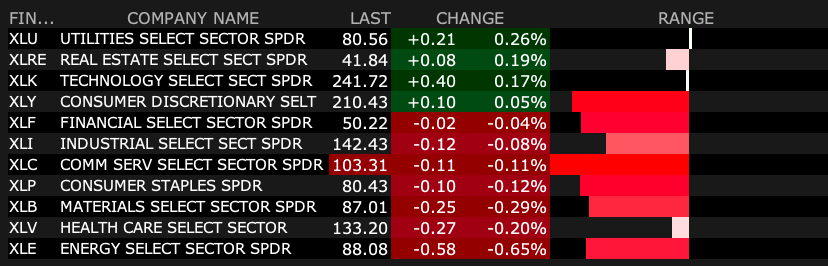

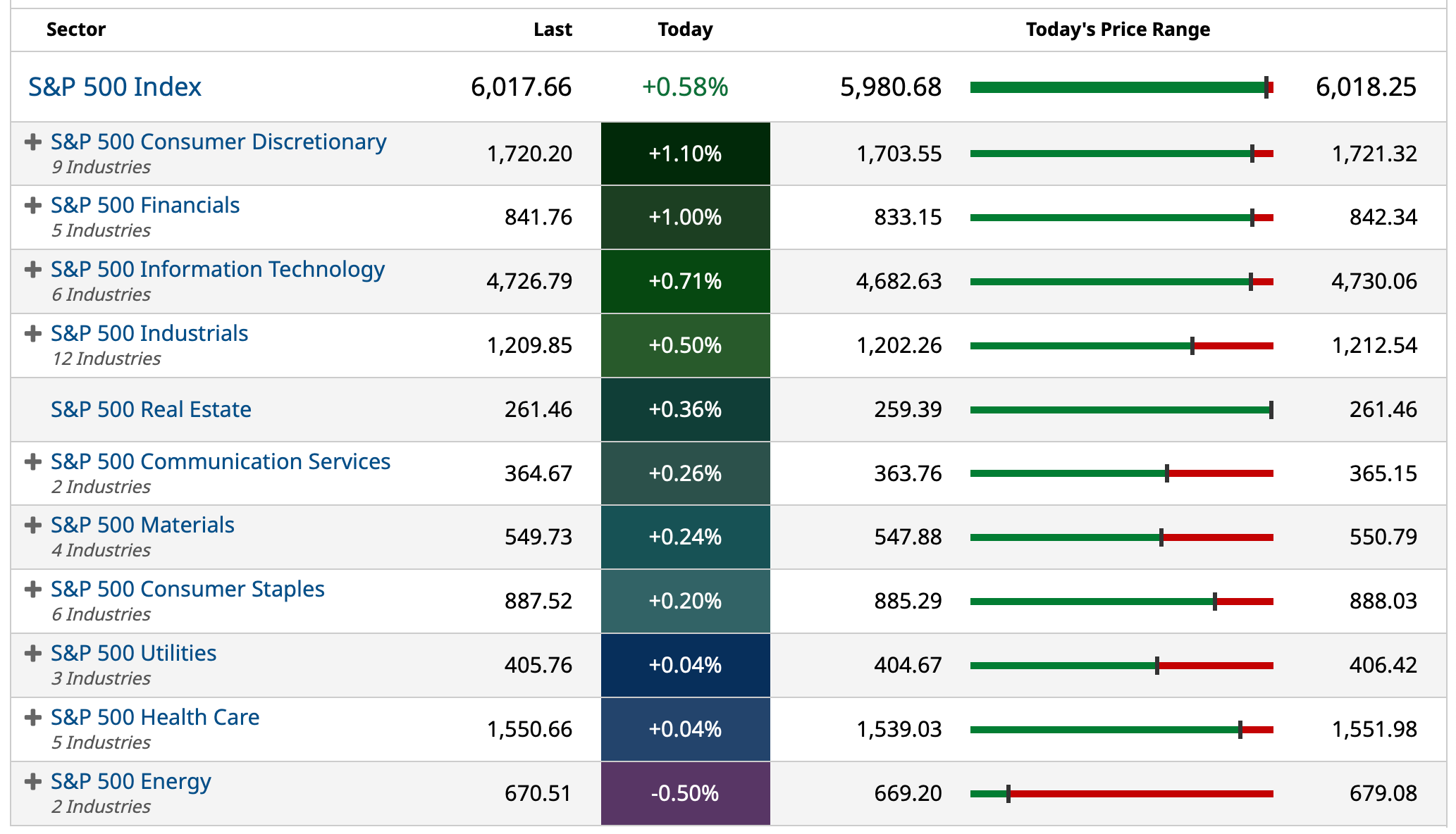

Sectors

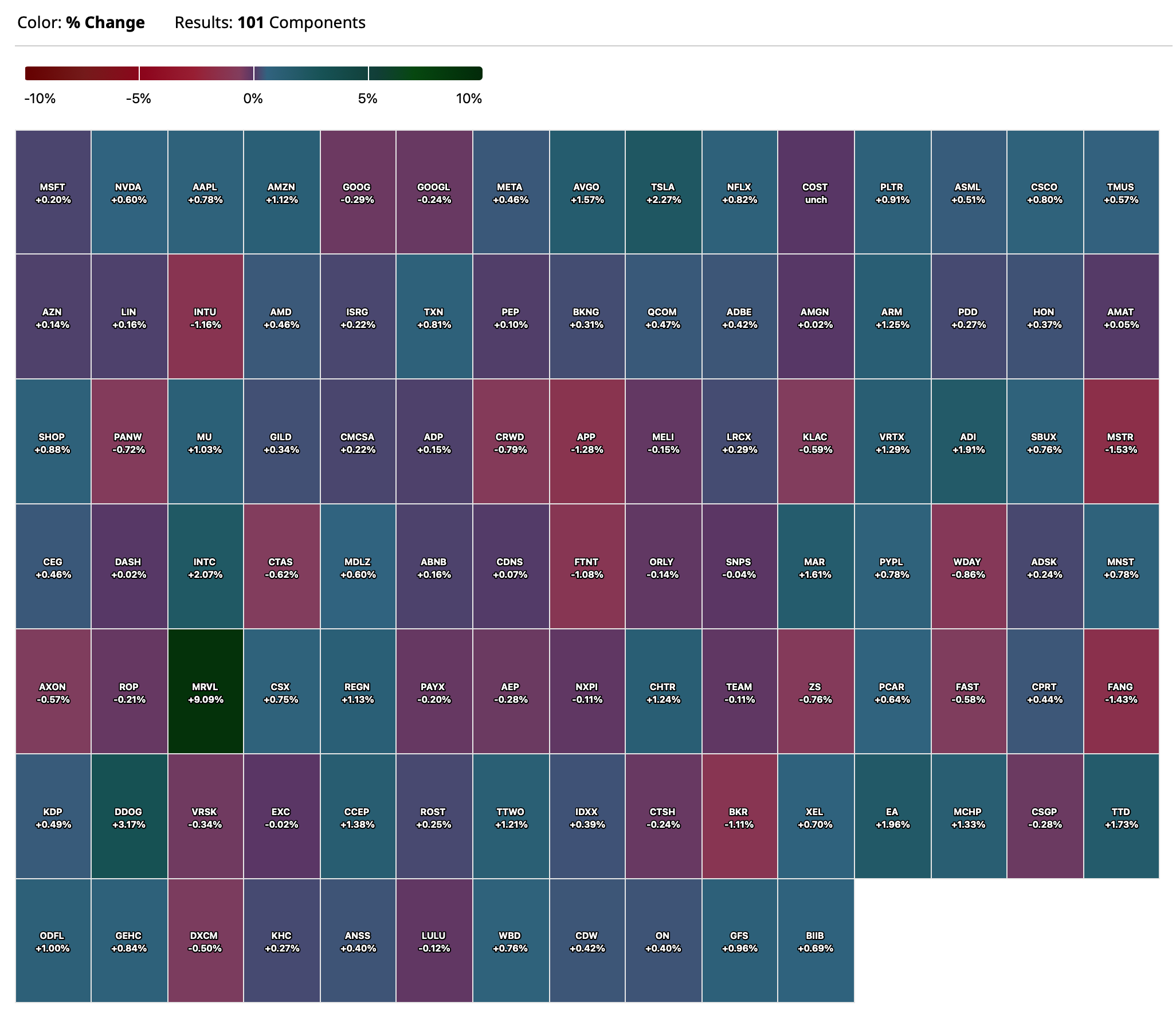

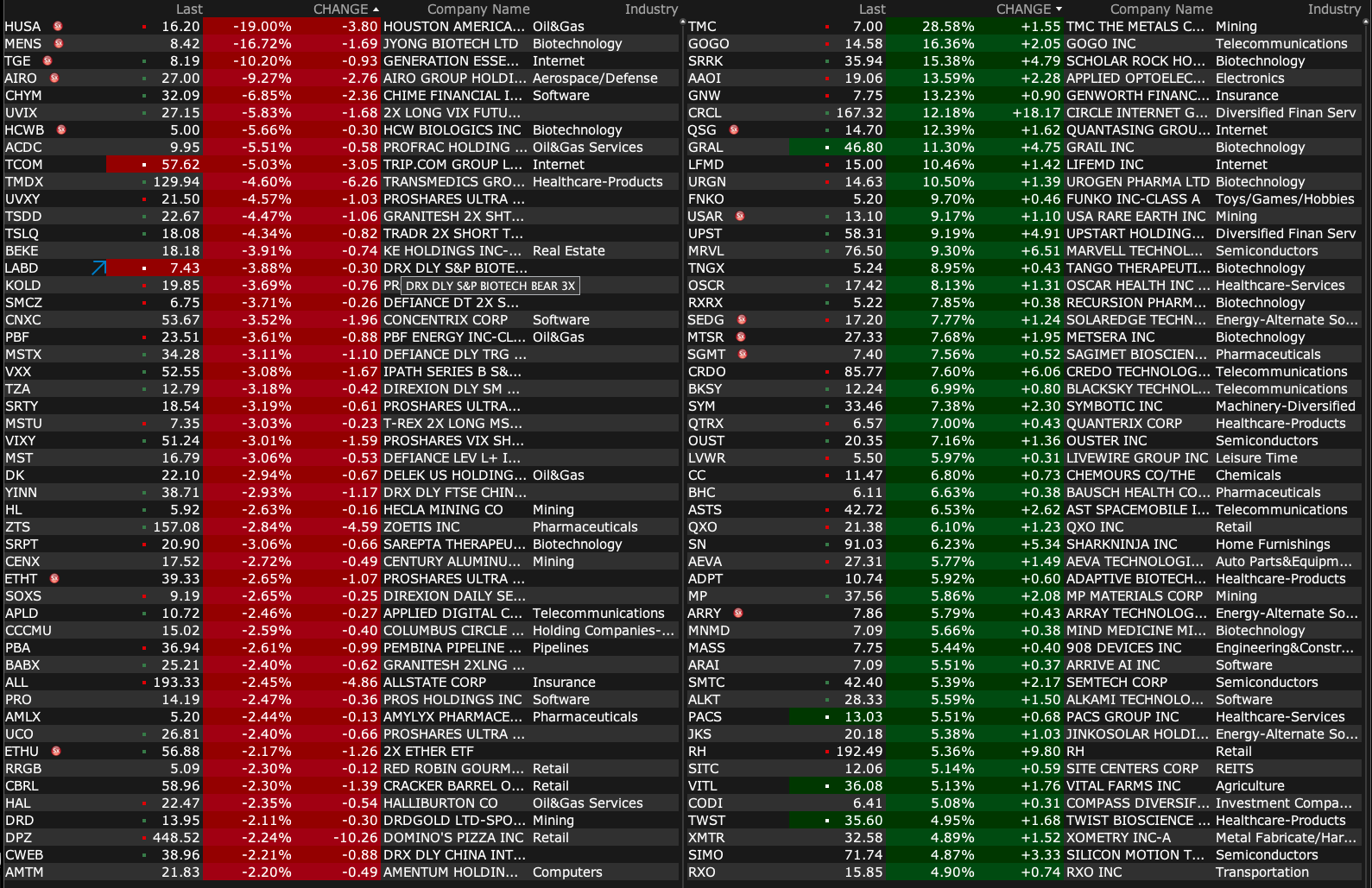

% Movers

BY Doug Kass · Jun 18, 2025, 4:20 PM EDT

- NYSE volume 3% below its one-month average;

- NASDAQ volume 20% below its one-month average;

- VIX index: down 6.85% to 20.12

BY Doug Kass · Jun 18, 2025, 4:20 PM EDT

From Peter Boockvar:

Treasury yields are at the highs of the day with the 2 yr yield at 3.95% (up 2 bps pre presser) and the 10 yr yield at 4.39-.40% (up 4 bps) in response to the message Powell is sending that he’s not ready to cut rates anytime soon. Here are some Bloomberg News generated bullet points that lay this out:

*POWELL: WANT TO SEE SOME TARIFF EFFECTS ON INF. BEFORE JUDGING

*POWELL: LABOR MARKET ISN'T CRYING OUT FOR A RATE CUT

*POWELL: GOING TO LEARN MORE ABOUT TARIFFS OVER SUMMER

*POWELL: PASS THROUGH OF TARIFFS TO CONSUMER INF. IS UNCERTAIN

*POWELL: CAN'T ASSUME TARIFF INFLATION HIT WILL JUST BE ONE-TIME

*POWELL: SIZE, AMOUNT, DURATION OF TARIFFS ARE HIGHLY UNCERTAIN

*POWELL: BEGINNING TO SEE SOME TARIFF EFFECTS, EXPECT MORE

*POWELL: MANY COMPANIES EXPECT TO PASS ON TARIFF COSTS

*POWELL: TAKES TIME FOR TARIFFS TO WORK THROUGH TO END CONSUMER

*POWELL: TARIFF EFFECTS ON INFLATION COULD BE MORE PERSISTENT

*POWELL: INCREASES IN TARIFFS LIKELY TO BOOST PRICES

BY Doug Kass · Jun 18, 2025, 4:07 PM EDT

There is a large market on close buy of about $4 billion.

BY Doug Kass · Jun 18, 2025, 3:54 PM EDT

S&P cash is now -7 handles — a reversal of over 35 handles since the Fed release — I have sold my SPY puts for a nice profit.

I will re-purchase on strength.

I now have no position in the indices.

BY Doug Kass · Jun 18, 2025, 3:06 PM EDT

Wolf Street howls about hotter inflation for longer.

BY Doug Kass · Jun 18, 2025, 2:57 PM EDT

With S&P cash +28 handles I am scaling into more SPY puts.

BY Doug Kass · Jun 18, 2025, 2:47 PM EDT

From Peter Boockvar:

As has been usually the case this year, the FOMC statement was little changed from the prior meeting with just modest tweaks as the press conference becomes the real place for anything potentially news worthy and market moving. The Fed maintained its stance that “economic activity has continued to expand at a solid pace” and that the “unemployment rate remains low, and labor market conditions remain solid.” As well as, “Inflation remains somewhat elevated.”

After repeating that “The Committee is attentive to the risks to both sides of its dual mandate”, they left out this from the May meeting that they judge “that the risks of higher unemployment and higher inflation have risen.”

They off course updated for us their economic projections and I’ll just mostly focus on 2025 because their guess for 2026 and beyond is as good as yours/ours. The 2025 GDP estimate falls to 1.4% from 1.7% and in turn their unemployment rate expectations rises one tenth from March to 4.5% vs 4.2% as of May. Headline PCE goes to 3.0% from 2.7% while the core estimate moves to 3.1% from 2.8%. I’m guessing the updated inflation guess is reflective of what they think about the tariff flow through as the 2026 forecast sees it back down to 2.4% for both headline and core.

Also of note, mostly for algos, their mean fed funds rate for this year remains at 3.9%. That implies two cuts with the current mid point of the fed funds range being 4.375%. Expectations for next year with rates is a further downshift to 3.6% which is actually 20 bps above the median given in March. Their longer run view remains at 3% which implies a REAL rate of 1% if they achieve sustainably a 2% inflation rate.

Interestingly, the median dots for two cuts this year is quite split in that 7 people don’t expect any cuts this year while two see one, 7 expect two and one sees 3.

The Treasury response was more on the short end as the 2 yr yield fell 2 bps to 3.91% while the 10 yr yield is little changed. While I expect some rate cuts in the back half of this year, as seen late last year, it doesn’t guarantee that long rates fall too.

Bottom line, not much new to say here as Jay Powell, to use his own words back in August 2023 in Jackson Hole, is still seemingly “navigating by the stars under cloudy skies” in terms of economic visibility.

BY Doug Kass · Jun 18, 2025, 2:40 PM EDT

* The odds of slugflation has increased.

* The risks to higher inflation and higher unemployment are skewed to the upside.

* The prospects for rate cuts have diminished.

* The level of broad uncertainties of forecasts have risen — with a large dispersion of outcomes.

I added to SPY puts (+26 handles on the S&P).

BY Doug Kass · Jun 18, 2025, 2:13 PM EDT

Yesterday bitcoin got hit and my BITO short fell while shorts in BITB and IBIT fell a few "sticks" each.

The chart of bitcoin seems similar to when I put on my short BITO, BITB and IBIT a few weeks ago — it seems like this asset class may be rolling over.

I remain short.

BY Doug Kass · Jun 18, 2025, 2:01 PM EDT

With S&P cash now +5 handles, and down -33 handles from the day's high, I am taking my profit in short indices (SPY $598.17 and QQQ $529.11).

I am keeping my SPY puts.

BY Doug Kass · Jun 18, 2025, 1:43 PM EDT

At 12:43 p.m.:

BY Doug Kass · Jun 18, 2025, 1:00 PM EDT

My pal Larry McDonald with Danny Moses ("On The Tape")

Lawrence McDonald: Risks, Myths and Investment Opportunities

BY Doug Kass · Jun 18, 2025, 12:45 PM EDT

Here are today's "things:"

* With S&P cash +30 handles I added to my SPY puts.

* Back shorting the indices — SPY $599.96 and QQQ $531.69 common.

* Shorted more HOOD $77.39 and SCHW $89.16.

BY Doug Kass · Jun 18, 2025, 12:31 PM EDT

BY Doug Kass · Jun 18, 2025, 12:00 PM EDT

With S&P cash +30 handles I have added to my SPY puts.

BY Doug Kass · Jun 18, 2025, 11:45 AM EDT

Dan and Guy are up at 11 a.m. on MRKT CALL.

The podcast is objective and value-added.

Unlike some, the boys are not glib, they are humbled by their decades of experience.

They admit their mistakes.

I listen to them daily, without fail.

And its FREE!

Let's go to the tape! MRKT Call - Wednesday, June 18th

I should really participate with them soon on their podcast. I will ask them for another invitation!!!

BY Doug Kass · Jun 18, 2025, 11:35 AM EDT

- NYSE volume 13% below its one-month average;

- Nasdaq volume 25% below its one-month average;

- VIX index: down 8.24% to 19.82

BY Doug Kass · Jun 18, 2025, 11:21 AM EDT

BY Doug Kass · Jun 18, 2025, 11:11 AM EDT

From Peter Boockvar:

My guess is that Jay Powell will continue to be non-committal today on the timing of eventual rate cuts. I say 'eventual' because that is their tilt and bias so I agree with the markets belief of about two this year (100% chance of one priced in and 76% chance of a 2nd by yr end) but just not yet Powell will tell us. So, today could end up being pretty boring and uneventful but we'll still hear about every possible scenario that could result in still holding as is and what would precipitate a cut. On the cut, all it would take is a few months of a rising unemployment rate and I think that's the side of the mandate they will first favor. Markets will initial react to the dots but we all know about the reliability of the dots.

I know there is this kneejerk belief on the part of most to believe rate cuts are good and rate hikes are bad but there is so much more to this. Remember, right now there is $7 Trillion of cash sitting in money markets and at about a 4% interest rate on that is providing income of $280 billion to its holders annualized. This doesn't include all the cash in CD's also earning income at banks which I don't have a figure on. My friends at Quill Research and Danielle Dimartino Booth had a great stat last week in their weekly piece that "70 cents of every $1 of interest income is spent into the economy vs 2 cents of wealth effect growth via their stock market portfolios." Thus, interest rate cuts could actually REDUCE consumer spending on the part of some as their interest income gets trimmed. No free lunch here for those cheering for rate cuts.

In an interview on CNBC with Sara Eisen and Carl Quintanilla, the CEO of Cava gave us insight on the US consumer and what he’s seeing both on the input cost side and price changes to the consumer, among other comments. “In general I think the numbers are indicative of the fog that’s hanging over consumers. You think about all the macro economic fluidity, whether that’s tariff policy, immigration policy, government spending policies, and then you add on top of that all of the geopolitical uncertainty that’s been increasing. And when consumers are in a fog you don’t tend to accelerate or kind of step on the gas. Consumers are looking for that fog to lift to say I have that clarity to lean forward and I think that’s what you saw play through in the numbers.”

“We’ve seen input costs to be pretty benign as it relates to COGS or labor and that’s what we really worked to pass along those savings to our guests. We only took a 1.7% menu price increase in the beginning of this year. No plans to take further price increases. We’ve been able to under price inflation, under price CPI over 800 basis points in the past few years. Really trying to drive that value proposition for consumers when they are in that fog or feeling other price pressures around them.”

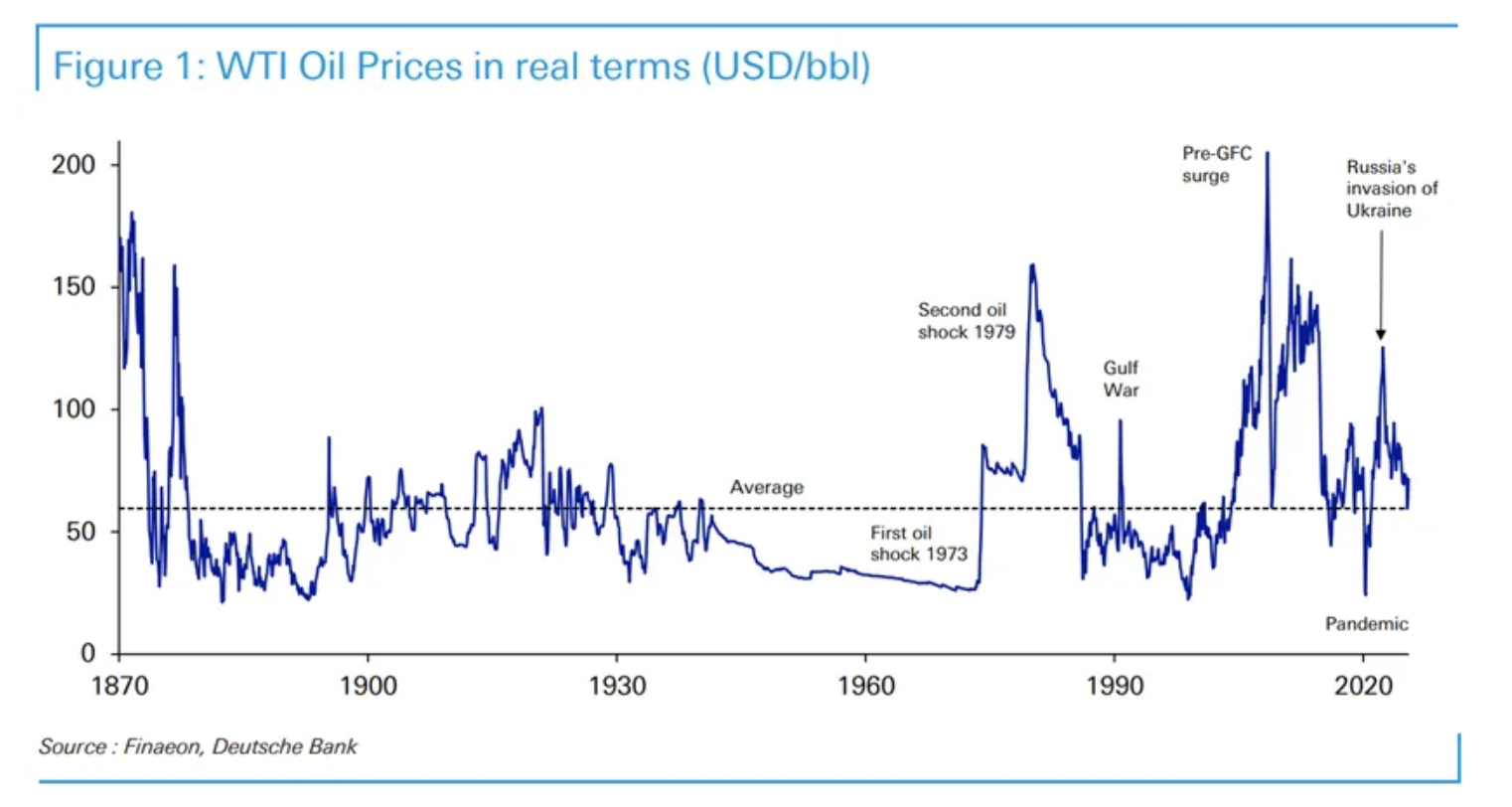

I thought this was a pretty interesting chart from Jim Reid at Deutsche Bank that he posted yesterday to give perspective on the current price of oil in REAL terms. Relative to the last 150 plus years, it's still pretty cheap.

After the March and April export rush ahead of tariffs, Japan's exports in May fell by 1.7% y/o/y but that wasn't as much as the estimate of down 3.7%. Interestingly, export volumes were up by 1.8% so maybe Japanese exporters absorbed initially some of the tariff costs, particularly on autos as auto exports were down by 25% y/o/y but volumes were lower by just 4%. On Japan's trade talks with the US, they seem to be at an impasse.

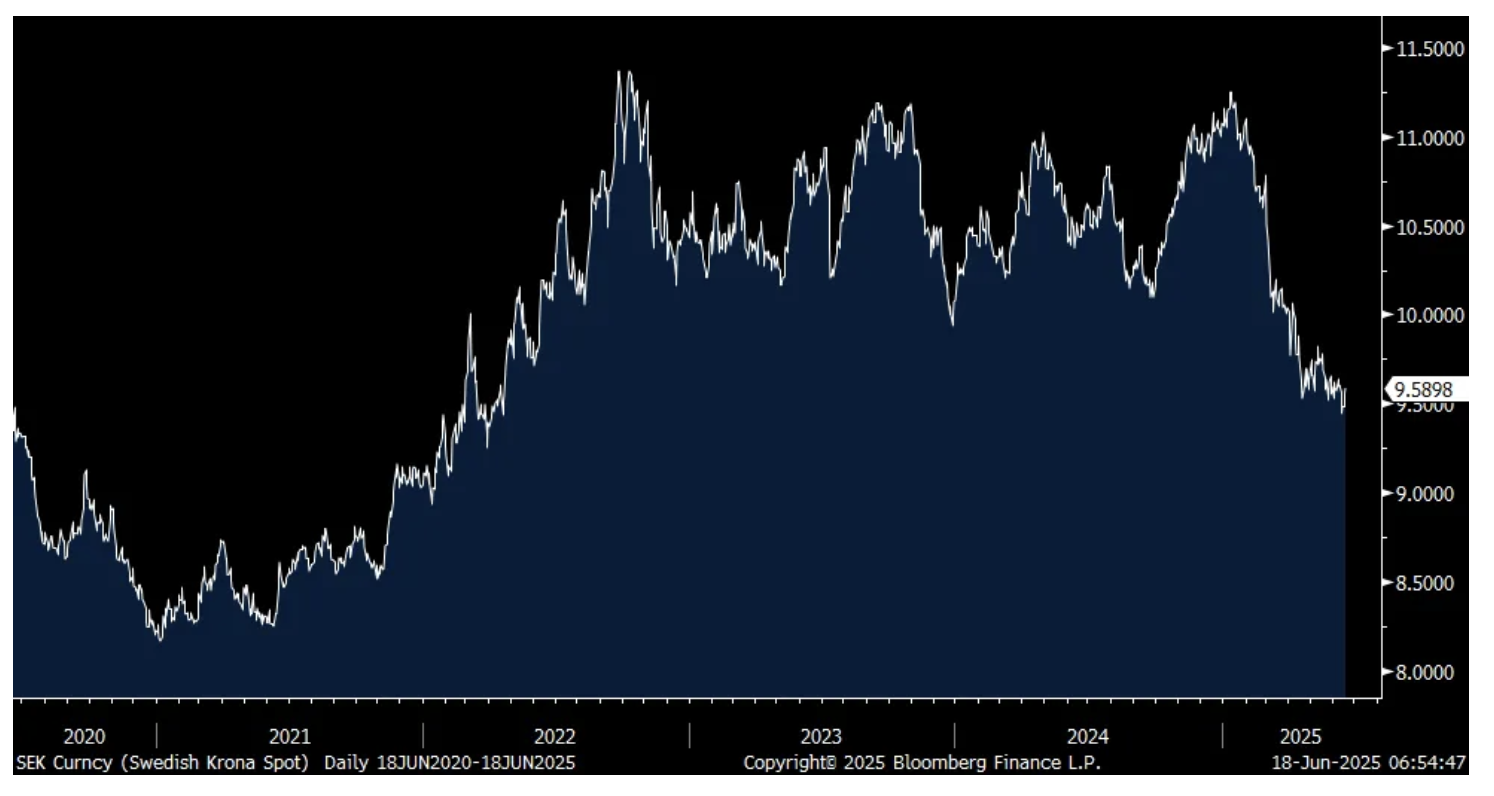

Ahead of the BoE and SNB meetings tomorrow, the Swedish Riksbank followed the ECB from a few weeks ago and cut rates by 25 bps to 2% as expected and said more cuts might come this year. Governor Thedeen said "The Swedish economy has lost momentum which has meant more limited inflationary pressure allowing space for more stimulus. The judgement we make today is that there is some probability of another cut this year."

The Swedish Krona is weaker on those comments but still near the highest level vs the US dollar since April 2022.

Krona

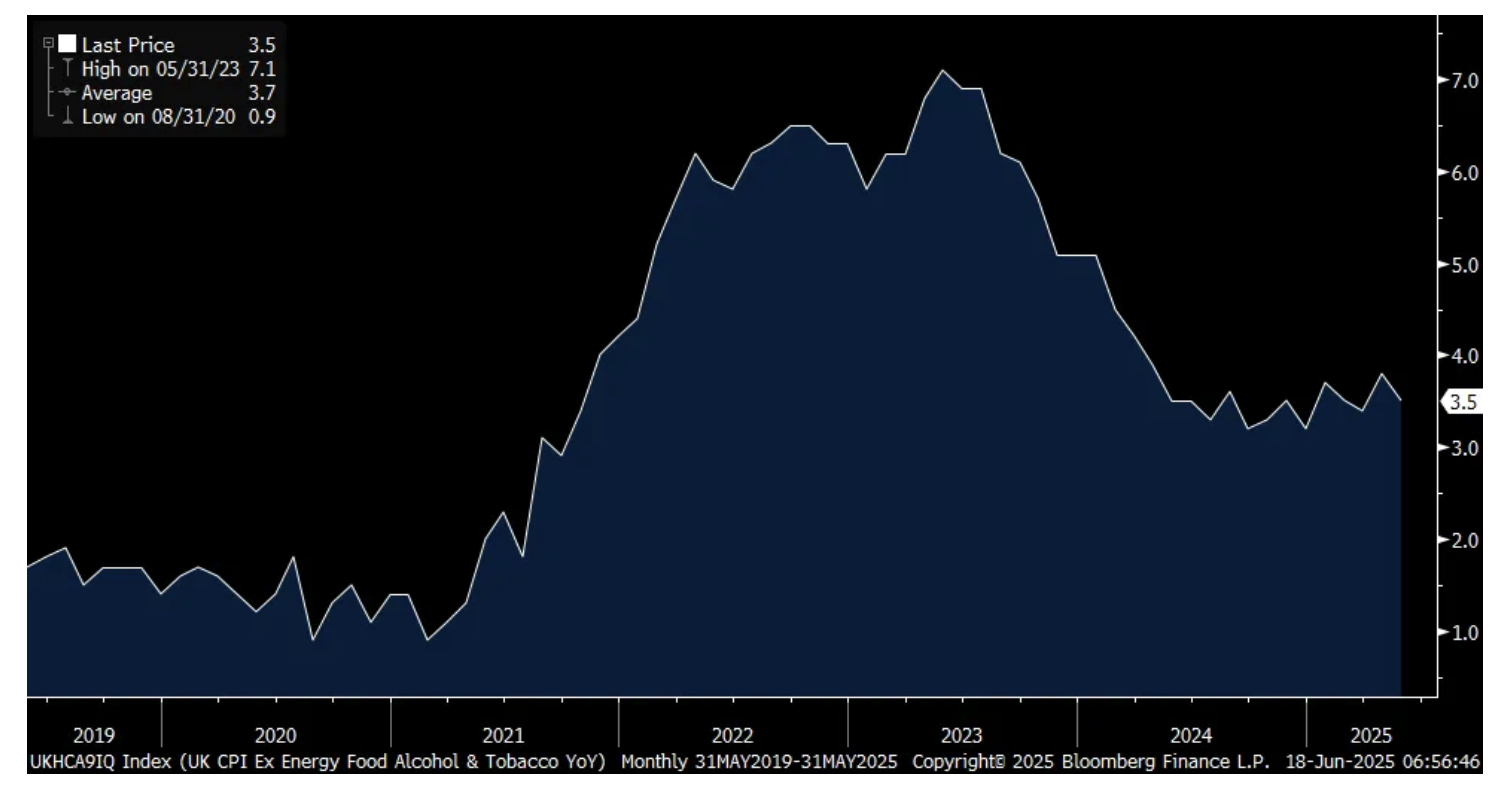

The May UK inflation stats were about as expected with headline CPI higher by 3.4% y/o/y vs 3.5% in the month before while the core rate was up 3.5% vs 3.8% in April. Services inflation continues to drive it, rising by 4.7% y/o/y, though down from 5.4% in April. Inflation breakevens are higher by 4 bps to 3.22% for the 10 yr but that could be a response to the move in oil prices late yesterday. Gilt yields are down while the pound is steady. The Bank of England is expected to hold its base rate tomorrow unchanged at 4.25% and we'll hear how they are thinking about the influence of oil prices in their thinking now that brent crude is up $10 in two weeks.

Core CPI in the UK y/o/y

BY Doug Kass · Jun 18, 2025, 10:30 AM EDT

* When we stop questioning, complacency leads the way.

* Investors are astonishingly bullish and dismissive of a plethora or possible adverse outcomes.

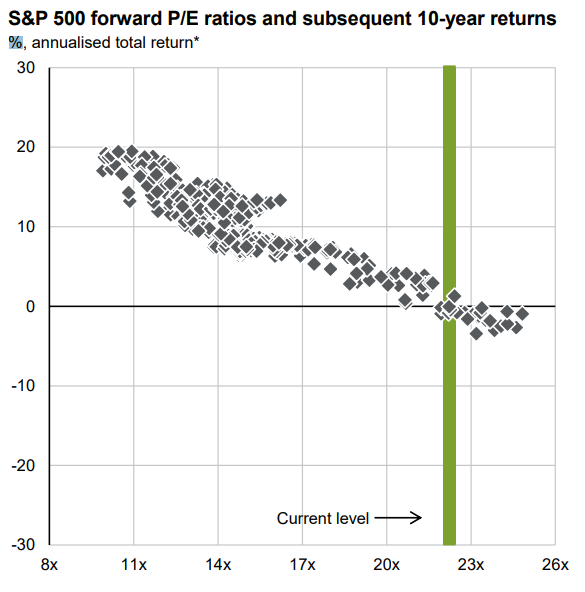

* A price-earnings multiple of 23x is historically a very poor launching pad for future investment returns (see chart below).

* Today's opener invokes the words of John Maudlin, Felix Zulauf, Andy Grove, Bloomberg's Lisa Abramowicz, Tim Russert, Howard Marks, Warren Buffett, Jacques Brel, Barry and Robin Gibb and The Divine Ms M (Helene Meisler).

On Sundays, the bulls get so bored

When they are asked to show off for us

There is the sun, the sand, and the arena

There are the bulls ready to bleed for us

It's the time when grocery clerks become Don Juan

It's the time when all ugly girls

Turn into swans, hah

Who can say of what he's found

That bull who turns and paws the ground

And suddenly he sees himself all nude, hah

Who can say of what he dreams

That bull who hears the silent screams

From the open mouths of multitudes

- Jacques Brel Is Alive and Well And Living in Paris, The Bulls (Les taureaux)

Two weeks ago, I read (as I have for a number of years) John Mauldin's luminous weekly commentary in Thoughts From the Front Line in which he summarized some of the comments from his annual Strategic Investment Conference. (Run, don't walk to read "Thoughts From The Front Line" — subscribe, it's free!)

John has been a great pal of mine for several decades throughout which I have read his musings in detail and with interest. I was initially attracted to his writings (and thoughts) because of his facts-based market and economic analysis. I particularly admired his objectivity (and ability to react to changing conditions and trends), common sense, logic of argument and deep dives.

John constantly exhibits an ability to give you the facts (nothing but the facts!) and to, in a non-consensus way, bring up "takes" and new ideas from his analysis that I hadn't thought about. (Therein lies the value-added to me).

What caught my eye was his May 31, 2025 issue entitled "Bullish Highlights" in which John highlighted the generally upbeat equity market perspective that permeated his conference (as "pessimism is decreasing").

A vivid example was (an historically skeptical) Felix Zulauf, a former Barron's Roundtable member and Swiss money manager who expects a move to 7,000 in the S&P Index:

“So, if somebody puts a gun to my head, I would say on the S&P 7,000... and then 9,000 again thereafter."

- Felix Zulauf

As I am at the polar opposite of Felix (as I am a short-term bear), I thought after reading Felix's musings, that if he is bullish and sees equities going to new highs — I should pay heed to him.

With Felix joining the herd's bullish chorus I reexamined over several days (as John has taught me to do over the year) my ursine market view.

Despite Felix's apparent bullish turn and after that reexamination (following my second time viewing his SIC presentation) I remain stalwartly negative — and I have concluded that (what I would describe as) The Bull Market in Complacency may soon come to an abrupt end.

Most everyone focuses on two big headwinds — and are of the belief that both will soon be resolved, as these factors rarely lead to impacting the long-term economic and investing trends — and will likely lead to an extension of the April-June market climb:

* Tariffs

* The Israel/Iran Conflict

As I will explain, my concerns run far deeper that these two issues, though these headwinds may not be as short lived and trivial as bulls suggest.

In the words of a broken heart

It's just emotion that's taking me over

Tied up in sorrow, lost in my soul

- Bee Gees, Emotion

Let's briefly examine how market structure has contributed to where we are today (6,000 on the S&P Index), why emotion (and FOMO) have taken over and what other concerns I have:

Passive products/strategies, institutional and individual investors now, greater than ever, worship at the altar of price and price momentum.

The business shows are a reflection/microcosm of the consensus sentiment and are now, almost universally bullish. (Bears are scoffed out these days.)

By contrast, over the last decade I have reminded subscribers that I wake up every morning before trading starts and I ask these questions of myself. Unfortunately I don't like the answers — those answers have haunted me and they are potentially market and valuation unfriendly:

Let's now shift to my near-term concerns that have been thoroughly dismissed in The Bull Market In Complacency.

On Monday (The Bear Market Will Be Back) and Tuesday (The Bear Market Will Be Back (Like Before)... I'll Fight the Fight and Win the War) I outlined a number of factors that investors should be concerned with:

* We face the highest geopolitical risks in many decades (which will not be resolved quickly).

* We face the largest level of social and political risks in the U.S. since the Vietnam war.

* We face the greatest chance of "slugflation" (slowing economic growth and sticky inflation) since the 1970s.

* We face the biggest threat that the U.S. dollar and capital markets will no longer be a "safe haven" in modern history.

* We face the greatest debt load and deficit ever — and neither party seems to favor any fiscal discipline whatsoever.

* We face the largest capital spending spree in history (on artificial intelligence) — though the return on that investment is less certain (dot-com, it feels like deja vu all over again.) (More on this shortly.)

* We face a viable alternative to equities in fixed income (for the first time in 15 years) as bonds present an equity-equivalent yield with limited risk and volatility.

These are bonafide and legitimate issues that are being ignored.

We never hear any of these concerns on the shows (they are being glossed over, at best), particularly when stocks are flirting at their highs.

But, like Tim Russert did as the longest standing moderator of Meet The Press ... let's examine what today's bulls also confidentally said in the past:

1. At the end of 2021, after a strong year, the consensus was very bullish. Equities fell by approximately -20% in 2022.

2. At the end of 2022, the consensus was negative and the S&P rose by about +20% in 2023.

3. At the end of 2023, the consensus was mixed and the S&P rose, again by about +20% in 2024.

4. At the end of 2024, the consensus was very bullish and, thus far the S&P is up only modestly (after experiencing a near -20% drawdown between late January and early April)

The other question rarely asked on the shows is what price are we paying for the confident view expressed by investors?

Does a 23x price-earnings multiple incorporate investors' optimism?

Does a 23x price-earnings multiple provide a "margin of safety?"

We do know, as illustrated in the chart I started today's opener with, that a 23x price-earnings multiple is historically a poor launching pad for future investment returns. This chart is so important that I am repeating it here:

To conclude this section, perhaps the overriding complacency simply reflects that investors today are trend followers and are acting like first-level thinkers:

"First-level thinking is simplistic and superficial, and just about everyone can do it - a bad sign for anything involving an attempt at superiority. All the first-level thinker needs is an opinion about the future, as in: 'The outlook for the company is favorable, meaning the stock will go up.'

"Second-level thinking is deep, complex and convoluted. The second-level thinker takes many things into account:

- Howard Marks, It's Not Easy (Sept. 9, 2015)

* And Bloomberg's U.S. Economic Surprise Index is at the year's lows.

Two additional fundamental concerns should be underscored.

I am stupefied that the bullish cabal is comfortably and confidentally extrapolating 1Q2025 S&P EPS and U.S. economic growth data.

First, most bulls respond to today's elevated valuations that earnings will grow rapidly (corporate profits are the lifeblood of our markets), making a P/E multiple of 23x not unreasonable.

This, too, I disagree with:

With prices paid moving up and the prices received component now moving down — corporate profit margin squeeze/pressure likely lies ahead.

Again, consensus S&P 2025-2026 EPS estimates are too high and at a starting point of 23x forward EPS — problematic for equities.

Second, Bloomberg's U.S. Economic Surprise Index has turned the most negative thus far in 2025:

When we stop questioning, complacency leads the way.

Technically and fundamentally, we are already seeing more than tiny cracks - that's how it starts.

And as we grow more complacent, cracks will deepen and widen.

Let's end with some sage and simple advice from Warren Buffett, The Oracle of Omaha:

"Price is what we pay, value is what we get."

BY Doug Kass · Jun 18, 2025, 9:30 AM EDT

-LGHL +68% (secures $600M Facility to launch Hyperliquid (HYPE) Treasury)

-GHLD +27% (Bayview Asset Management signs Definitive Agreement to acquire company in $1.3B all-cash deal at $20/shr)

-PRE +17% (divests ACT Genomics to Delta Electronics as Part of up to $71.8M deal)

-KFY +12% (earnings, guidance)

-ESEA +11% (earnings)

-GMS +8.7% (earnings, guidance)

-SRRK +5.5% (reports Phase 2 EMBRAZE Trial Results Demonstrating Statistically Significant Preservation of Lean Mass with Apitegromab During Tirzepatide-Induced Weight Loss)

-MRVL +4.3% (guidance)

-CRCL +3.2% (GENIUIS stablecoin bill approval)

-PAA +3.2% (Keyera to acquire Plains' Canadian NGL business in $5.2B cash transaction)

-GNW +2.7% (hearing Keefe Bruyette Raised GNW to Outperform from Market Perform, price target: $9)

-NUE +2.7% (guidance)

-AFRM +2.0% (reportedly Prudential unit lends $500M in private credit to Affirm)

-BMEA -26% (prices 19.45M shares at $2.00/shr for gross proceeds ~$40M)

-RGC -18% (profit-taking)

-ACB -13% (earnings)

-HUSA -11% (prices 223.7K common shares at $10.60 in registered direct offering)

-BTDR -8.4% (prices $330M convertible notes due 2031)

-RUN -2.3% (RBC Cuts RUN to Sector Perform from Outperform, price target: $5)

-PGR -2.2% (reports May net premiums written)

BY Doug Kass · Jun 18, 2025, 9:16 AM EDT

Charts from 8:14 a.m. ET:

BY Doug Kass · Jun 18, 2025, 9:10 AM EDT

Chart from 8:33 a.m. ET:

BY Doug Kass · Jun 18, 2025, 8:58 AM EDT

Bonus — Here are some great links:

Solar, European Financials and Spain Flame Out as Oil and Vol Surges

BY Doug Kass · Jun 18, 2025, 6:45 AM EDT

A constant refrain of mine — housing will lead a consumer-based slowdown:

BY Doug Kass · Jun 18, 2025, 6:35 AM EDT

From JPMorgan (which is becoming a two-handed strategist (see boldface!) — on one hand this, on the other hand that):

Futs are higher into Fed Day as the market shrugs off geopolitics. Pre-mkt, Mag7/Semis are outperforming; Cyclicals poised for a strong day as Financials get a boost from de-reg. In FICC, bond yields are lower, USD weaker, and cmdtys seeing profit-taking. While the Fed is the focal point of today’s macro data, keep an eye on initial claims and an update to the trend. TIC data at 4pm will show (lagged) foreign ownership of Treasuries.

and...

EQUITY & MACRO NARRATIVE

With chatter of the US getting involved in the Israeli/Iranian conflict we saw the risk off moves that many expected on Monday: oil up, bond yields down, USD bid, and stocks seeing supply. Many client conversations point to the demolition of the underground, uranium enrichment facility being the last major milestone; if true, it is unclear if US involvement would last beyond this type of strike. Question is how long this lasts. The combined moves from Friday and Tuesday are what we had in mind when we shifted our view to Cautious from Tactically Bullish. If this situation is adjudicated quickly, then think Equities resume their march higher with ATHs the target. Should signs (market expectations) point to this situation persisting into July then that will require a rethink. Until then, we like buying the dip.

BY Doug Kass · Jun 18, 2025, 6:25 AM EDT

Wolf Street howls about retail sales.

BY Doug Kass · Jun 18, 2025, 6:15 AM EDT

I am back shorting the indices, with S&P futures +23 handles:

* SPY $599.98

* QQQ $531.72

BY Doug Kass · Jun 18, 2025, 6:05 AM EDT

In a divided world, full of too much chaos and hate we still have Paul McCartney:

BY Doug Kass · Jun 18, 2025, 5:55 AM EDT

The S&P Short Range Oscillator is at 1.07% vs. 3/11%, moving back towards neutral.

BY Doug Kass · Jun 18, 2025, 5:45 AM EDT