Tweet of the Day (Part Four)

BY Doug Kass · Jun 17, 2025, 4:23 PM EDT

BY Doug Kass · Jun 17, 2025, 4:23 PM EDT

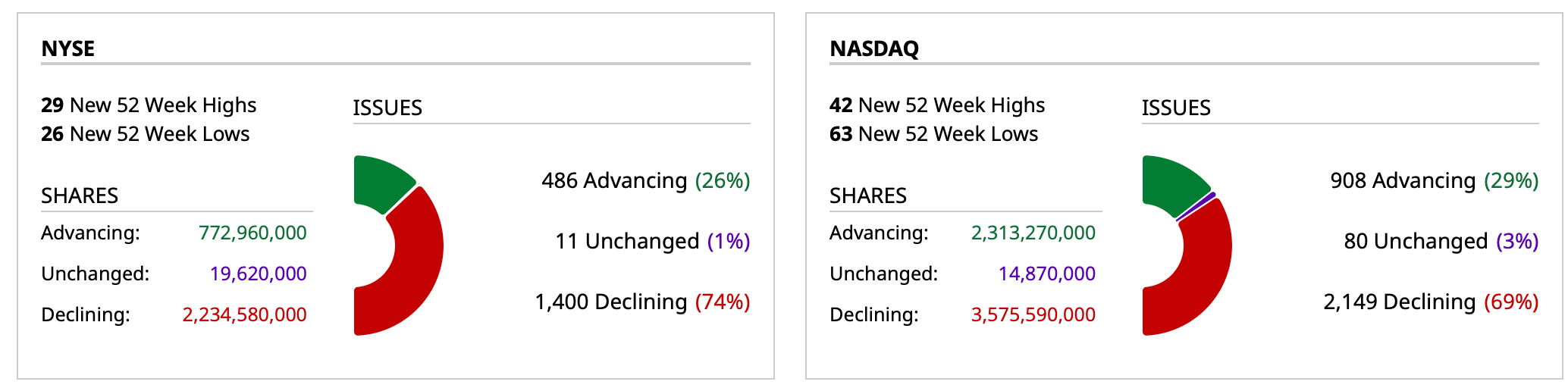

- NYSE volume 3% below its one-month average;

- NASDAQ volume 13% below its one-month average;

- VIX index: up 12.14% to 21.43

BY Doug Kass · Jun 17, 2025, 4:20 PM EDT

I have a 3:30 p.m. research meeting that will extend to after the close.

Thanks for reading my Diary today.

Enjoy the evening.

Be safe.

Normal day's end data will follow after 4 p.m.

BY Doug Kass · Jun 17, 2025, 3:45 PM EDT

TechNova

SPY : In defense of Dougie's 7 years of no returns.

Bottom Bollinger Band on SPY is siting right at the 200 SMA,

A move to $580 would not even technically be considered "Bearish".

douglas cassel

Sometimes you care less about what the market will be doing in ten years, and more about whether you will be there to see it.

BY Doug Kass · Jun 17, 2025, 3:21 PM EDT

At 2:40 p.m.:

BY Doug Kass · Jun 17, 2025, 2:58 PM EDT

BY Doug Kass · Jun 17, 2025, 2:26 PM EDT

BY Doug Kass · Jun 17, 2025, 1:45 PM EDT

Here are today's things:

* Last night I covered all my index shorts:

SPY $599.37

QQQ $530.91

* I purchased SPY puts (in the money for August) on the rally back to -14 handles.

* I initiated a short sale in Nvidia NVDA at $144.52 and Robinhood HOOD at $76.17.

* Shorted more Charles Schwab SCHW $88.69 and GRNY at $21.59.

BY Doug Kass · Jun 17, 2025, 1:31 PM EDT

Break in.

Axios is reporting that the Administration is considering a strike on Iran.

Trump considers strike on Iran ahead of crucial Situation Room meeting

BY Doug Kass · Jun 17, 2025, 1:21 PM EDT

As of 11:33 a.m.:

BY Doug Kass · Jun 17, 2025, 12:20 PM EDT

- NYSE volume 7% below its one-month average;

- NASDAQ volume 13% below its one-month average;

- VIX index: up 4.19% to 19.89

BY Doug Kass · Jun 17, 2025, 11:25 AM EDT

It continues to be my view that housing will lead a consumer-based economic slowdown in the U.S..

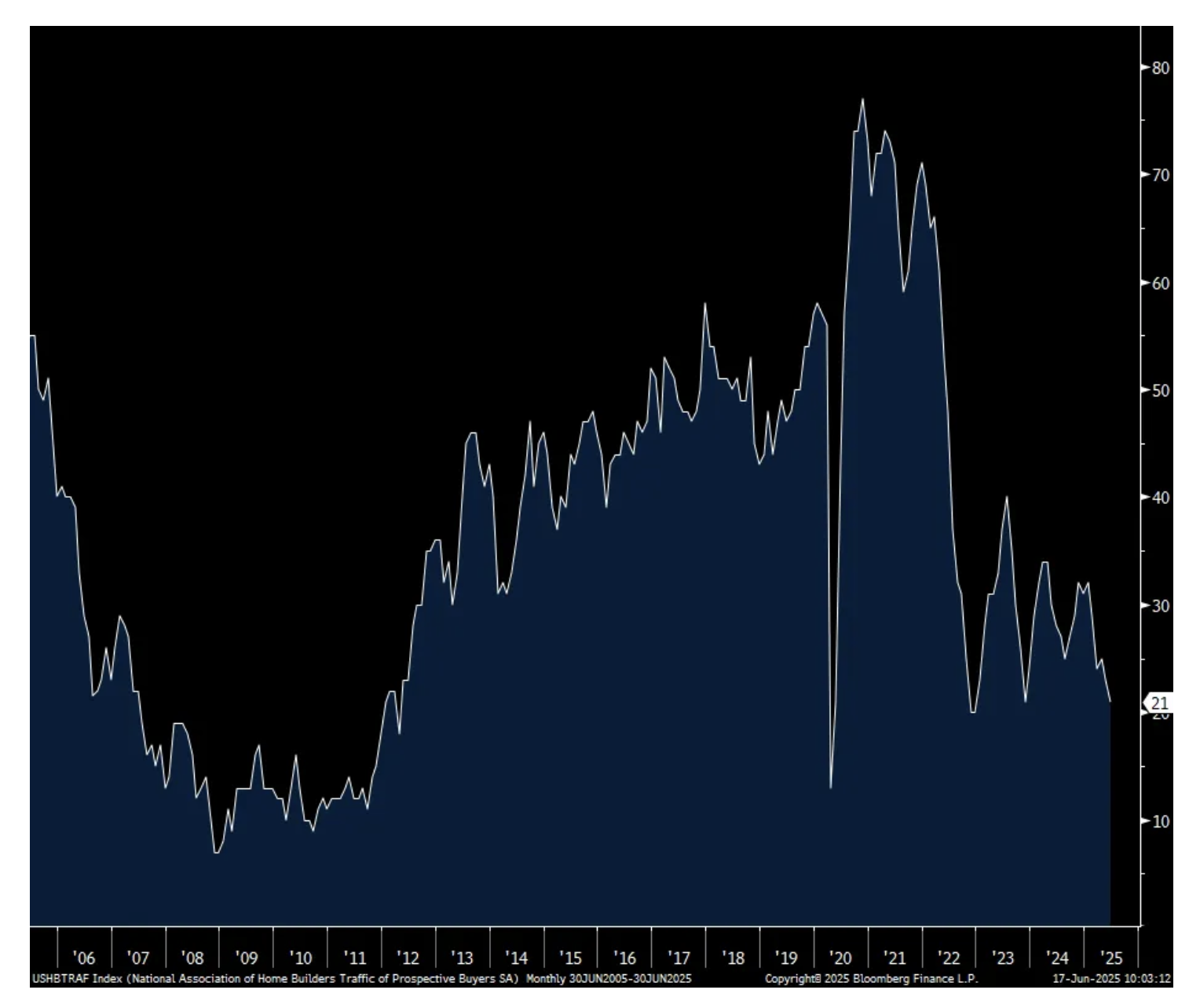

From Rosie:

The U.S. housing market remains in a complete state of disarray, beset by stretched affordability levels and a recent rise in unsold inventory (beginning to depress real estate prices). The NAHB survey rounded out today’s long list of data releases and it was weak — receding to 32 in June from 34 in May and defying a consensus expecting an improvement to 36. So much for Lennar’s earnings release, though it did reveal a soft demand underbelly. The fact that the Treasury market cannot seem to rally off of numbers like we have seen so far today underlines how much bond investor anxiety there is over the tariff file, the budget-busting bill making its way through Congress, and now the Mideast-induced run-up in oil prices.

The NAHB index dropped in four of the past five months and is at its lowest level since December 2022. It really says something that, at 32, the headline is bordering on the pandemic low of 30 in April 2020, not to mention pressing against the same level that presaged the recession that began in December 2007. Headline is also lower than it was at any point in the 2001 economic downturn. I plead with Jay Powell to find a different term than “solid” to describe the economy — time for refresher.

Regionally, the weakest areas are now the once-hot South (lowest since June 2012) and the West (its lowest since January 2012). And in terms of segments, all three were disappointing: buyer traffic fell to 21 from 23 in May (tied for the weakest print since December 2022); the six-month sales outlook (40 from 42 — the lowest since November 2023); and current sales (37 to 35 — the lowest since June 2012) also declined...

BY Doug Kass · Jun 17, 2025, 11:17 AM EDT

Long August in the money SPY puts.

I plan on expanding this position on any market strength.

BY Doug Kass · Jun 17, 2025, 11:03 AM EDT

Shorting NVDA at $144.62.

Added to large (GRNY) short at $21.59.

BY Doug Kass · Jun 17, 2025, 10:58 AM EDT

From Peter Boockvar;

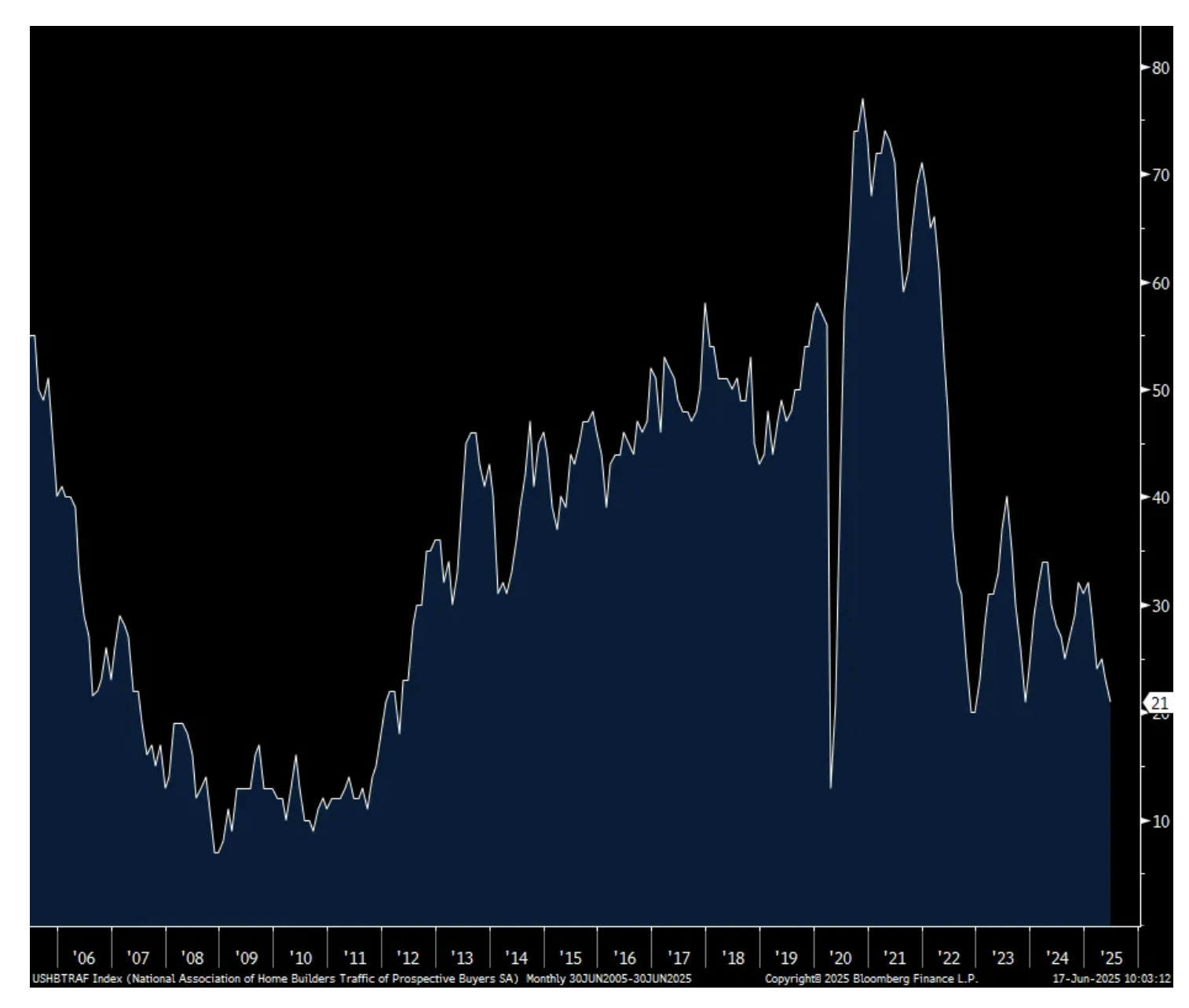

The mood of homebuilders in June remained dour with the NAHB builder sentiment index falling further to just 32 from 34 in May and vs. the estimate of 36. That’s the lowest since December 2022. Both the Present and Future components were down by 2 pts m/o/m while Prospective Buyers Traffic fell to just 21, also down 2 pts. Again, 50 is the breakeven between expansion and contraction.

The NAHB highlighted the challenges, “Buyers are increasingly moving to the sidelines due to elevated mortgage rates and tariff and economic uncertainty. To help address affordability concerns and bring hesitant buyers off the fence, a growing number of builders are moving to cut prices.”

More, “Rising inventory levels and prospective home buyers who are on hold waiting for affordability conditions to improve are resulting in weakening price growth in most markets and generating price declines for resales in a growing number of markets. Given current market conditions, NAHB is forecasting a decline in single-family starts for 2025.”

I have nothing to add but this, the NAHB has estimated in the past that the housing industry, including everything associated with it, makes up anywhere between 15-18% of US GDP. I’ll say again, US economic growth is very uneven and mixed.

NAHB

Prospective Buyers Traffic

BY Doug Kass · Jun 17, 2025, 10:55 AM EDT

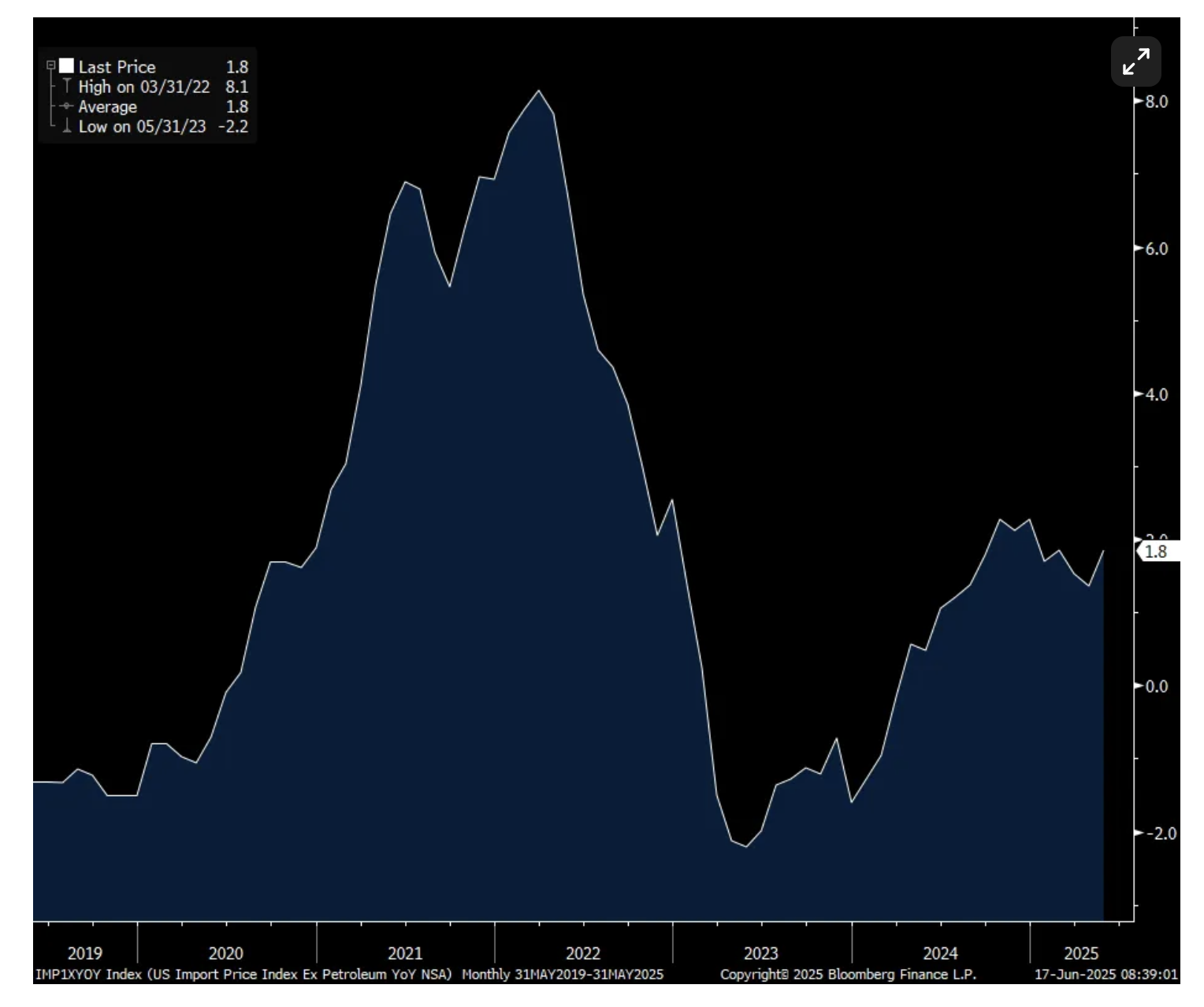

From Peter Boockvar:

May import prices, with the on again, off again tariff situation as we know, were flat m/o/m headline vs the estimate of down 2 tenths. Ex petro saw prices up .2% after a .4% rise in April. They are up 1.8% y/o/y. Of note, import prices ex food and energy popped .4% after a .5% gain in April and can be the first early signs of the impact of tariffs. They are now up 1.3% y/o/y after an .8% rise in April, and 1.1% increase in March.

Specifically, the prices of durable industrial supplies jumped by 1.2% in May after rising by 1% in April. Capital goods prices were up by .2% m/o/m after being up .7% in April. No impact yet though with the imports of autos/parts where prices were up by one tenth after a two tenths gain in April. Consumer goods prices ex autos were up by .2% m/o/m.

After going through more countless earnings calls, many companies are doing their best to mitigate the tariffs (some have more flexibility than others) and many have yet to raise prices, though said they will, but import prices won’t wait and the core rate jump over April and May is worth watching from here.

Import prices ex petro y/o/y

Core retail sales in May rose .4% m/o/m, one tenth above expectations and April was revised up by one tenth to down .1%.

I would have thought there was front running going on, as I heard from some retailers, but auto sales fell 3.5% m/o/m and electronics were down by .6%. There was weakness too in building materials, down by 2.7% m/o/m but more likely reflecting the tough housing market. Sales fell too for the necessities of food/beverages and health/personal care. Restaurant/bars also saw a decline in sales of .9% m/o/m but still up 6.4% y/o/y.

On the flip side, sales remain strong for online, up by .9% m/o/m and 6.3% y/o/y. Sales for clothing were higher by .8% m/o/m and 5.8% y/o/y. They were up too for sporting goods and in the miscellaneous category that grew by 2.9% m/o/m but after a 3.7% drop in the month before. They are up 7.8% y/o/y and includes everything from dollar stores, pet stores, convenience stores, etc…Furniture sales were up by 1.2% m/o/m and by 8.8% y/o/y.

Bottom line, while core retail sales were a touch above the estimate, the big ticket items of autos and building materials, not included in the core calculation, were quite weak as stated. Overall, the mixed picture of the US consumer, with clear separation between upper income and those below, continues.

BY Doug Kass · Jun 17, 2025, 10:15 AM EDT

From Peter Boockvar:

If there is an inflation stat that would most quickly reflect the price impact from tariffs it would be today's import price data for May. But, also of importance is to see what the US dollar weakness is doing in terms making imports more expensive.

As the US dollar still can't get out of its own way and is hovering around the weakest level since March 2022, a pretty interesting Bloomberg News article was out yesterday titled "Many Exporters No Longer Want Dollars, US Bank Executive says." Now, the article is long on anecdotes with no hard figures but it still reflects what is possibly a game changing moment where foreigners re-access the extent to which they want to own the US dollar (on top of the rethink that is going on globally as to the level of US assets foreigners want to own after piling in over the last bunch of years).

The piece says, "When Paula Comings, the head of currency sales for US Bancorp, talks to US importers, she increasingly hears the same message: Their foreign counterparties no longer want to be paid in dollars. Instead, they ask for settlement in euros, Chinese renminbi, the Mexican peso and the Canadian dollar, looking to limit their exposure to further swings in the greenback." Comings said, "A lot of clients previously were reluctant because dollars were sacred in the eyes of the supplier. Now the vibe from the overseas vendors seems to be, 'Just give us our currency.' "

Here's an example given, "A lumber company from the Midwest now converts its US cash into euros before paying for hardwood imports from Europe - a change from its previous practice of simply sending dollars. The move was spurred in part by a 2% discount offered by its European supplier for making payments in the single currency."

A few more, "Another client, a homeware retailer that imports from China, renegotiated its terms with suppliers and plans to settle its next bill in yuan. A third customer, a US food company sourcing equipment from Italy, agreed to pay its dues in the common currency, causing it to receive a more favorable rate on a purchase worth 400,000 euros."

Finally, a quote from Karl Schamotta, chief market strategist at cross border payments firm Corpay in Toronto, "The change is difficult to quantify in real time, but in markets from East Asia to Latin America, a growing number of exporters are opting to denominate contracts in euro, yuan, or even local currencies."

Major global sea change going on as 'times they are a changin'.

We continue to like and own non dollar assets like international stocks, bonds (local currency), precious metals and other commodities.

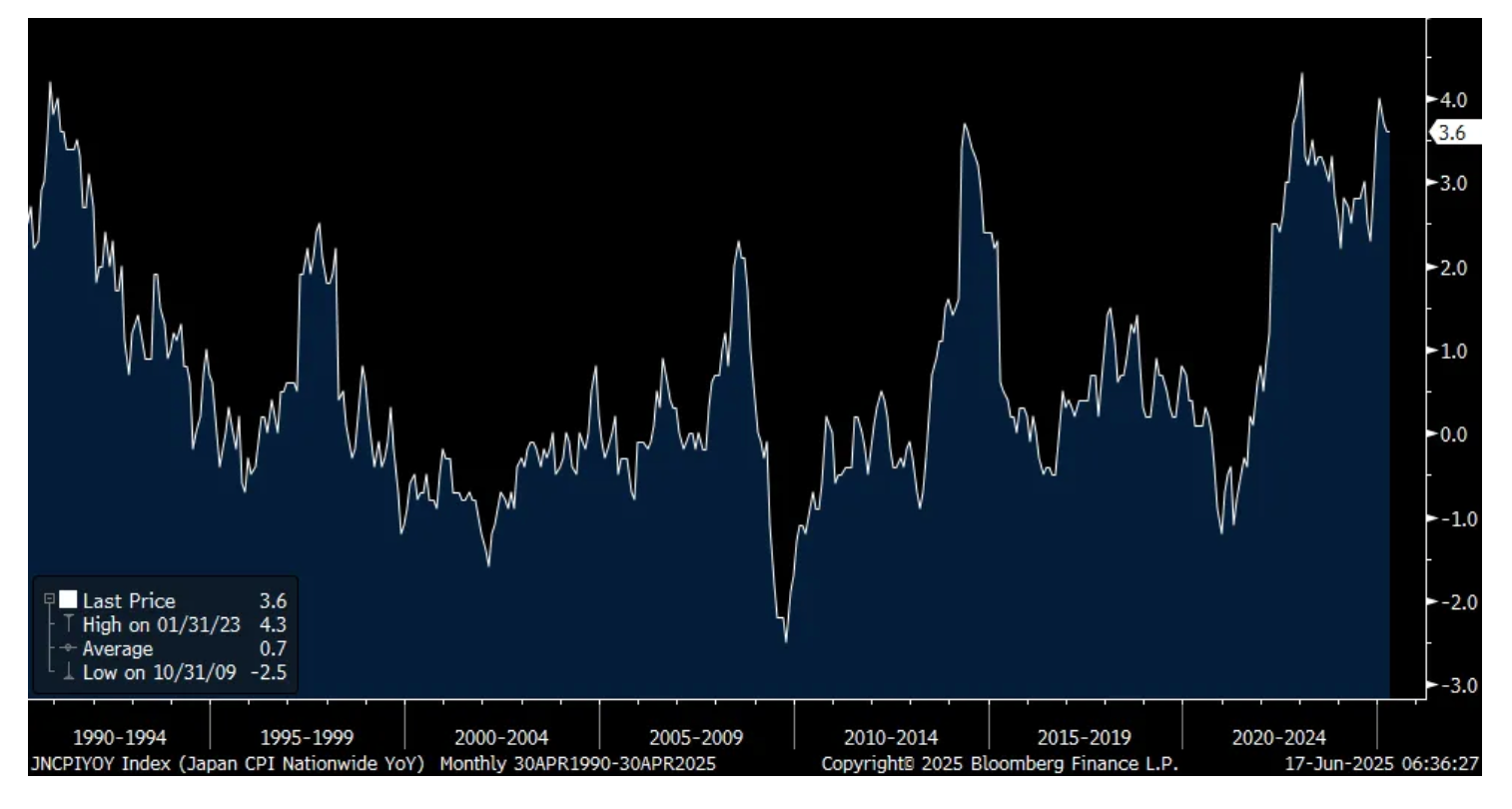

I want to chime in again on the tariff/inflation debate as I continue to believe it is just too simplistic to say tariffs are a one time step up in price, therefore it's not inflationary. Now, there is a great example of a one time step up in price and that was over the years when the Japanese government would raise the value added tax. Note on the chart below that almost each spike was due to that. One time step up in price with no follow through.

Why I think the current tariff strategy can bleed into more than just one time is because of the disruption and shifting of supply chains that will result from it. It creates a lot of friction. Production that is done in China for example is because it's the best product at the cheapest price and replacing that to the exact extent is tough. Maybe similar quality can be produced elsewhere but not necessarily at the same price and shifting around supply chains in response to the tariff landscape can take a few years with likely higher costs as a result.

Also, we know rents are the biggest piece of CPI (about 30% of headline and 40% of core) and the cost of construction continues to rise with 50% tariffs now on steel, aluminum and tariffs too on lumber and a variety of other imports. We are enjoying the benefit of slowing rents currently because of the flood of supply of completed projects but new building is slowing and rents should resume higher next year and into 2027 as too the cost of buying home for many remains unaffordable. A lasting impact from tariffs, but certainly also a higher cost of financing an influence too.

And whether higher taxes/tariffs are eaten by the consumer or not, they don't just disappear and someone's margin is reduced at the end of the day.

I'll give my back of the envelope calculation again. A 10% blanket tariff on all imports totals about $330b. That compares with the corporate tax receipts of $525b. Add the two together and you have an effective corporate income tax rate of 34% on about $2.5 trillion of pre tax income (the implied figure from 21% rate and collections of $525b). It's like the 2017 corporate tax cut never happened. I would have preferred lowering it to 15% across the board as a way to encourage the reshoring of US production. Let us be Ireland.

Japan CPI, VAT induced one time price jumps (1989, 1997, 2014)

Speaking of housing, this was from Lennar's press release last night:

"While we continue to see softness in the housing market due to affordability challenges and a decline in consumer confidence, we adhered to our strategy of driving starts, sales, and closings in order to build long-term efficiencies in our business."

"Reflecting softer market conditions, our average sales price, net of incentives, declined to $389,000. As mortgage interest rates remained higher and consumer confidence continued to weaken, we drove volume with starts while incentivizing sales to enable affordability and help consumers to purchase homes."

The Bank of Japan did what was expected with regards to tapering its balance sheet reduction but it won't start until April 2026 where they will downshift its asset purchases by 200b yen per quarter (about $1.5b) from the current slowing pace of 400b per quarter and which compares with monthly bond buying of a still large 4 trillion yen.

Governor Ueda said "It's desirable to continue tapering to allow yields to move more freely reflecting market forces. But tapering too rapidly could cause unintended impact on market stability."

It's unclear on when they might raise rates again with its overnight rate still at just .50%. Ueda said "I won't comment on the likelihood of near term interest rate hike. But I would say we would like to look at hard data that will be coming out. We would also like to see whether currently elevated headline inflation will moderate, or whether it could affect underlying inflation. It will be a comprehensive decision based on various other data, too."

With the possibility still, though Ueda was not entirely clear, of another rate hike this year and QT tapering not happening until next year, JGB yields are a bit higher overnight while the yen is flat vs the US dollar.

The one data point of note in Europe was the June German ZEW investor confidence index in their economy which jumped to 47.5 from 25.2 and 12.5 pts above expectations. Almost the entire gain was in the Expectations component which rose by almost 24 pts. The Current Situation was still deeply negative at -72 but less so vs the -82 in May. ZEW said, "Recent growth in investment and consumer demand have been contributing factors. This development also seems to strengthen the assessment that the fiscal policy measures announced by the new German government can provide a boost to the economy. Combined with the recent interest rate cuts by the ECB, this could bring economic stagnation in Germany, which has lasted for almost three years, to an end."

Nothing market moving with the ZEW but certainly reflects the optimism brewing there. The euro is unchanged vs the US dollar but around the best level since November 2021. Bund yields are slightly higher while the DAX is selling off, though still up 17.6% in euro terms and by 31% in dollars.

BY Doug Kass · Jun 17, 2025, 9:45 AM EDT

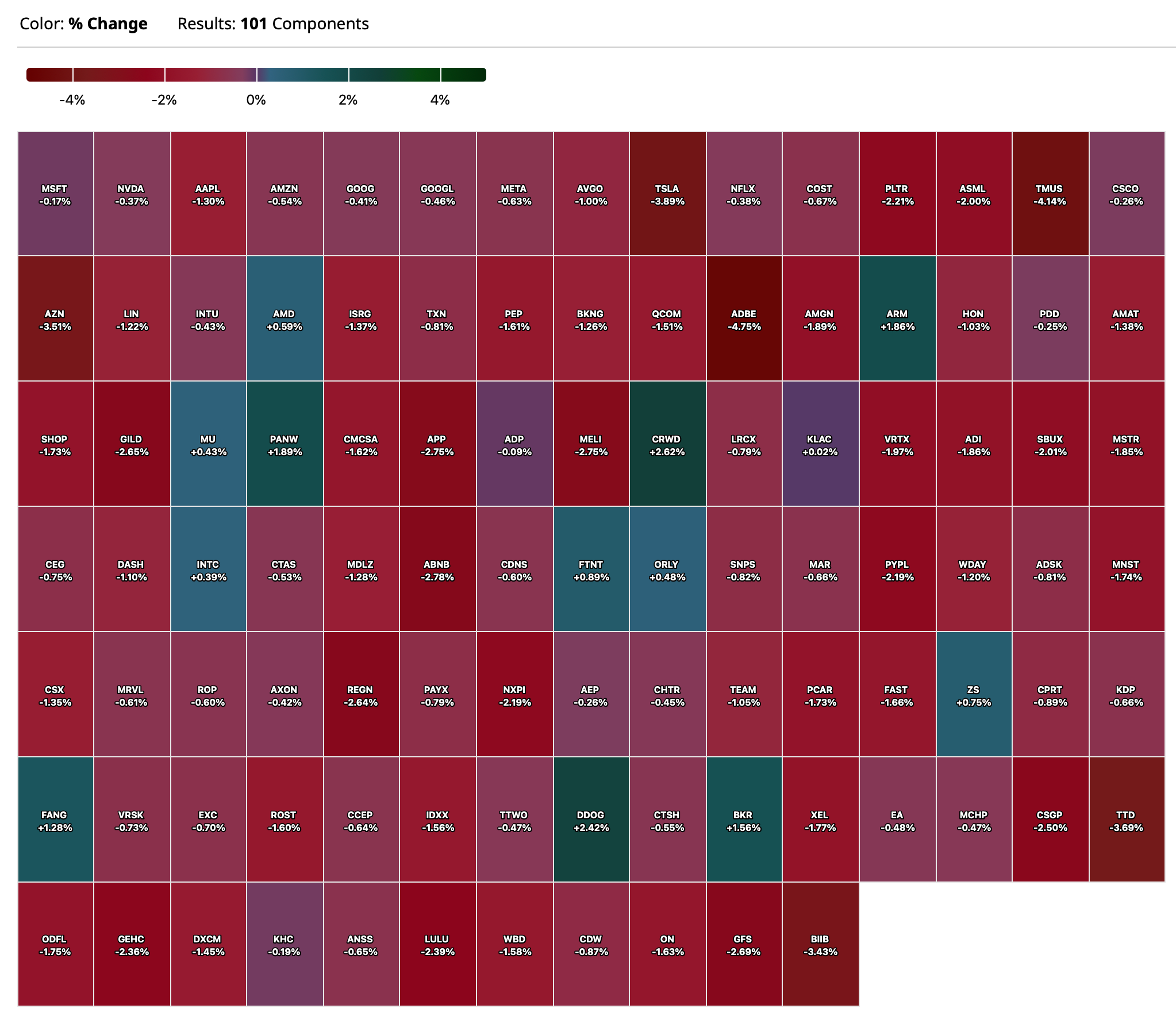

-VERV +76% (Lilly confirms to acquire Verve Therapeutics to advance one-time treatments for people with high cardiovascular risk at $10.50/shr in cash plus additional $3.00/shr CVR)

-CERO +54% (announces FDA Orphan Drug Designation Granted to CER-1236 for the Treatment of Acute Myeloid Leukemia)

-BIOA +7.3% (announced the launch of an initiative to comprehensively profile and analyze samples from the HUNT Biobank in Norway)

-OKLO +5.0% (nuclear power company strength following US Senate extending credits for nuclear energy to 2036)

-RELY +4.5% (US Senate bill includes exemption to House’s 3.5% remittance tax if the transfer are financed via an account with US bank or US issued card)

-SMR +4.4% (nuclear power company strength following US Senate extending credits for nuclear energy to 2036)

-SYRE +3.7% (announces Positive Interim Phase 1 Results for Two Next-Generation TL1A Antibody Programs, and Provides Clinical Development Updates Expected to Deliver 9 Phase 2 Readouts)

-DATS +3.6% (subsidiary RPM Interactive Files Registration Statement for Proposed IPO)

-JBL +3.1% (earnings, guidance)

-ALKS +2.4% (UBS Raised ALKS to Buy from Neutral, price target: $42 from $33)

-AMD +2.3% (momentum amid potential AWS partnership)

-RUN -38% (US Senate supports ending wind, solar tax credits)

-SEDG -32% (US Senate supports ending wind, solar tax credits)

-ENPH -21% (US Senate supports ending wind, solar tax credits)

-DYN -19% (US FDA has granted Breakthrough Therapy Designation to DYNE-101 for the treatment of myotonic dystrophy type 1)

-FSLR -19% (US Senate supports ending wind, solar tax credits)

-RDW -18% (prices 15.5M shares at $16.75/shr in $260M upsized offering)

-ARRY -15% (US Senate supports ending wind, solar tax credits)

-SGRY -14% (concludes discussions with Bain Capital)

-NXT -11% (US Senate supports ending wind, solar tax credits)

-FVR -5.7% (downside momentum following termination of CFO and Co-CEO)

-JBLU -5.3% (to cut more flights and other costs with breakeven in 2025 unlikely)

BY Doug Kass · Jun 17, 2025, 9:35 AM EDT

* Reestablished HOOD short at $76.05.

* Adding to very small short in SCHW at $88.31.

BY Doug Kass · Jun 17, 2025, 9:28 AM EDT

* Including reported numbers this morning...

BY Doug Kass · Jun 17, 2025, 9:13 AM EDT

At 8:39 a.m.:

BY Doug Kass · Jun 17, 2025, 9:00 AM EDT

From JPMorgan:

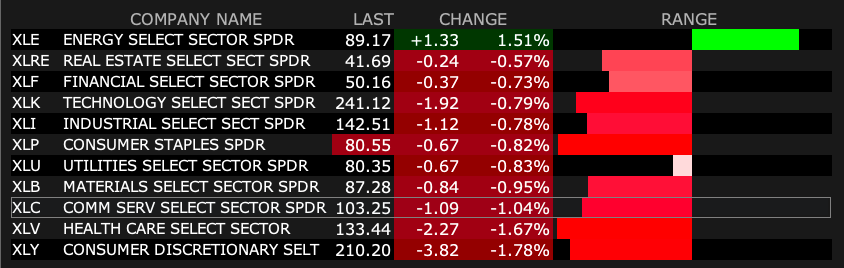

US: Futs are lower on escalation/contagion worries in the Middle East as Trump leaves G7 early post a warning to evac Tehran; he has not yet spoken to Iran on a ceasefire. A draft of the Senate’s version of the budget/tax bill drawing complaints from fiscal hawks and Section 899 features sees its first ex-US backlash with one money mgrs freezing all long-term investments in the US, per BBG. Pre-mkt, Mag7/Semis are weaker amid a stronger USD, lower bond yields, and higher cmdty prices. The Energy complex continues its gains and both Base and Precious have a bid. Retail Sales is the key macro data print today where Feroli sees the Control Group increasing 0.5% MoM.

and...

EQUITY & MACRO NARRATIVE

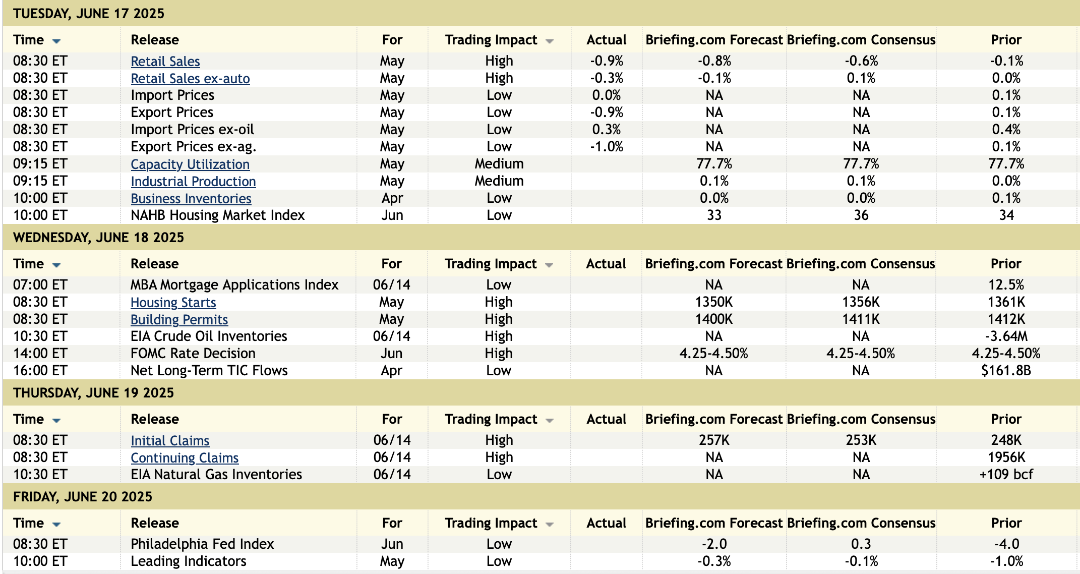

Today’s session may be more volatile than yesterday’s given (i) no new trade deals emanating from G7; (ii) the first draft of the Senate bill points to July 4 likely being too optimistic to complete the bill; (iii) corporate sector pushback to Section 899 (BBG); and (iv) heightened uncertainty surrounding both Israel/Iran and Russia/Ukraine. Keep an eye on Retail Sales as a stronger number than can help buttress the idea that the US Consumer can continue to support the economy as the various trade, tax, and monetary policy outlooks solidify.

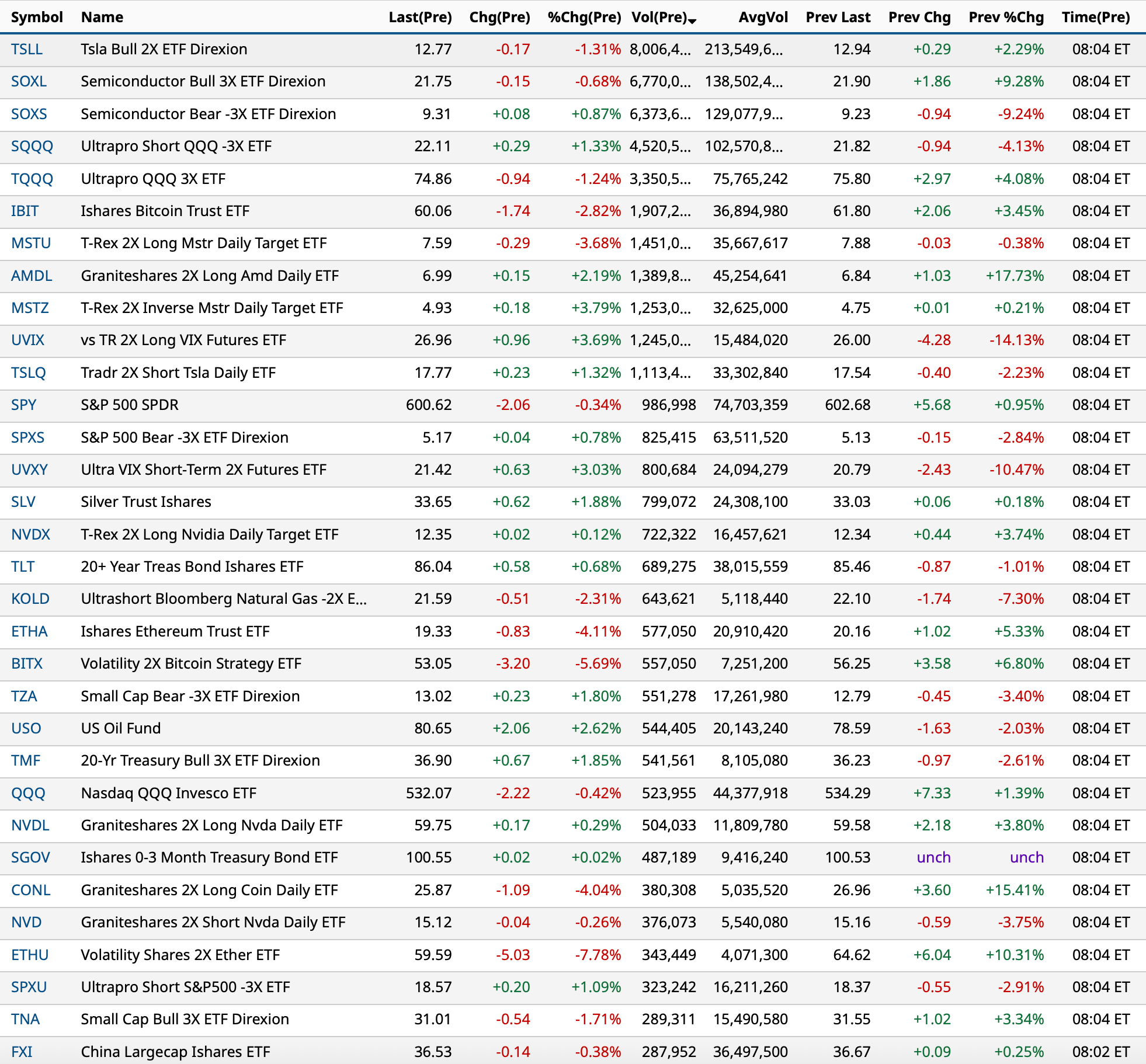

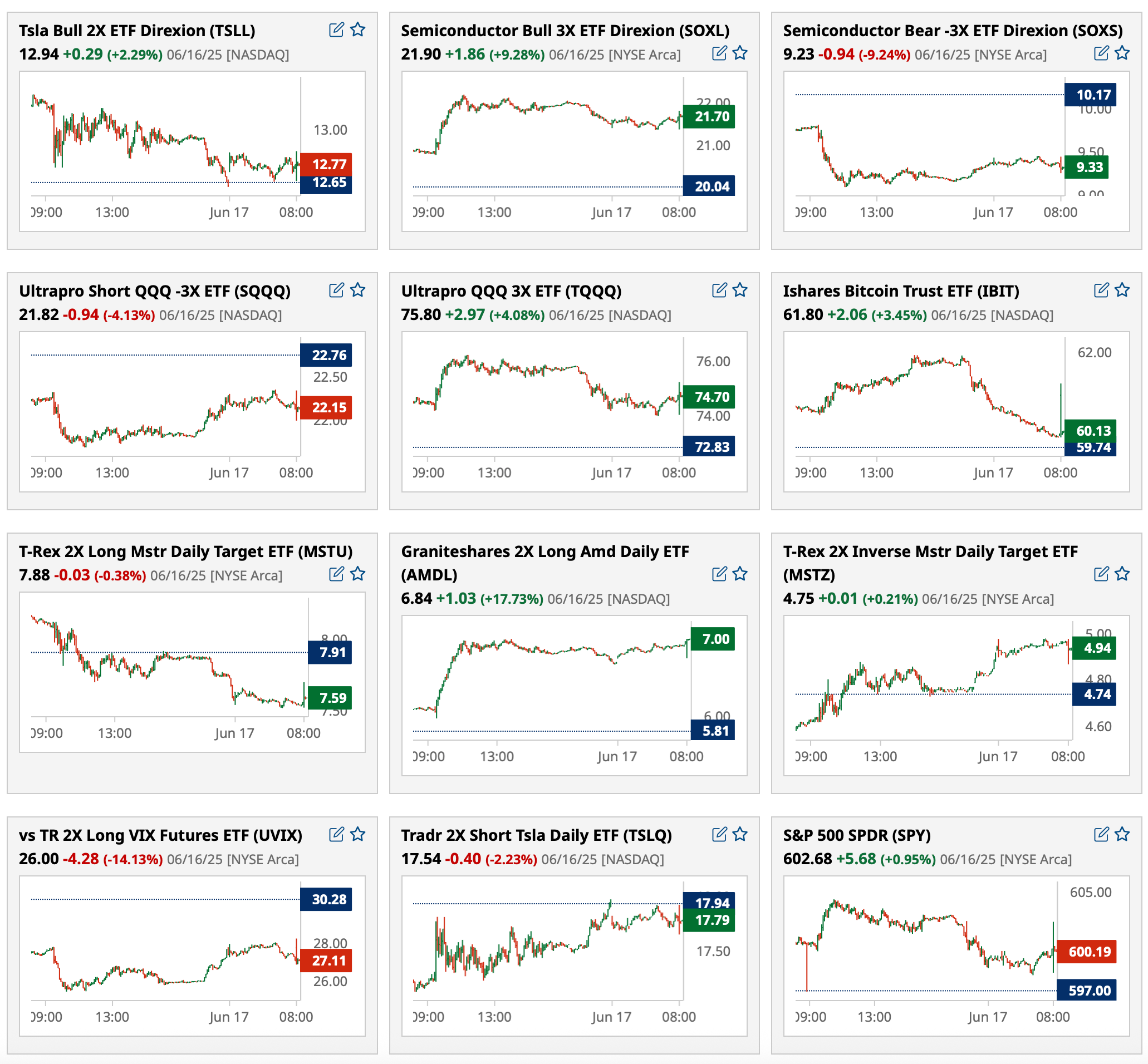

BY Doug Kass · Jun 17, 2025, 8:50 AM EDT

As of 8:04 a.m.:

BY Doug Kass · Jun 17, 2025, 8:35 AM EDT

* Like Hamilton's Leslie Odom, Jr., I am "Waiting for It!"

* Though it appears that no one else is in "The Room Where It Happens," I continue to be of the view that the S&P index may have made a 2025 high in late January.

* Though the Schuyler Sisters on Fin TV may disagree, "Look Around (to my concerns below)"... I view the downside risk to now be over 5x the upside reward.

* I still expect a high-single-digit to low-double-digit drop in the indices for the full year.

For this morning's opening comments I simply call on and repost yesterday's opening missive — as my comments continue to be relevant:

* But bull markets die hard...

You say

The price of my love's not a price that you're willing to pay

You cry

In your tea, which you hurl in the sea when you see me go by

Why so sad?

Remember, we made an arrangement when you went away

Now, you're making me mad

Remember, despite our estrangement, I'm your man

You'll be back, soon, you'll see

You'll remember you belong to me

You'll be back, time will tell

You'll remember that I served you well

Oceans rise, empires fall

We have seen each other through it all

And when push comes to shove

I will send a fully armed battalion to remind you of my love!

- You'll Be Back - Hamilton (Original Cast 2016 - Live)

As expressed in the last two weeks ("Downside Market Risk Is About 5-Times Upside Reward" and "Goodbye Goldilocks (Hello Reality)") I expect equities to be pressured over the next few months.

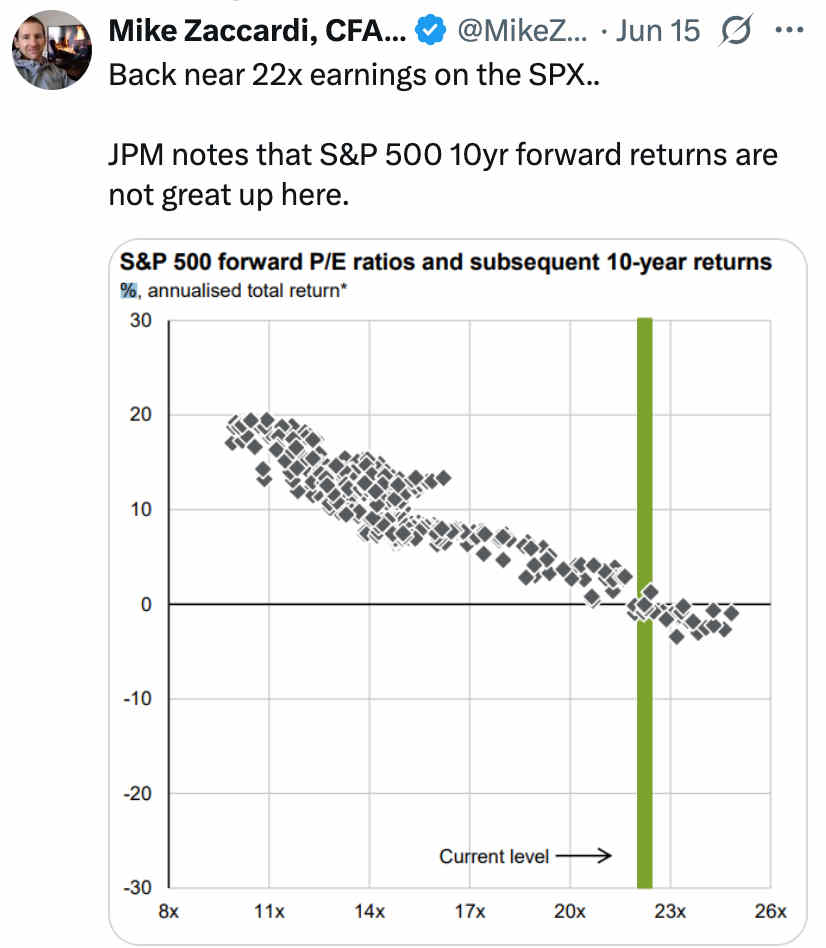

The Israeli/Iran conflict (now into its fourth day) is yet another of a long list of uncertainties that investors face. And with a starting point of a 22.5-times price earnings ratio, investors are underappreciating and underpricing risk:

* We face the highest geopolitical risks in many decades (which will not be resolved quickly).

* We face the largest level of social and political risks in the U.S. since the Vietnam war.

* We face the greatest chance of "slugflation" (slowing economic growth and sticky inflation) since the 1970s.

* We face the biggest threat that the U.S. dollar and capital markets will no longer be a "safe haven" in modern history.

* We face the greatest debt load and deficit ever — and neither party seems to favor any fiscal discipline whatsoever.

* We face the largest capital spending spree in history (on artificial intelligence) — though the return on that investment is less certain (dot.com, it feels like deja vu all over again.) (More on this shortly)

* We face a viable alternative to equities in fixed income (for the first time in 15 years) as bonds present an equity-equivalent yield with limited risk and volatility.

As I noted on Thursday, I plan to expand my short exposure on any further rallies.

Recognizing the strength of price momentum since early April I plan to give the market a relatively wide berth in scaling into shorts.

By Doug Kass Jun 16, 2025 8:27 AM EDT

BY Doug Kass · Jun 17, 2025, 8:00 AM EDT

* Guest input!

Investment strategists Gene Wilder and Marty Feldman on today's equity market...

BY Doug Kass · Jun 17, 2025, 7:10 AM EDT

BY Doug Kass · Jun 17, 2025, 7:00 AM EDT

andiman1

9 hours ago

Tomorrow oil will prob be through the roof

https://www.yahoo.com/news/trump-does-not-intend-sign-212700121.html

BY Doug Kass · Jun 17, 2025, 6:40 AM EDT

BY Doug Kass · Jun 17, 2025, 6:25 AM EDT

BY Doug Kass · Jun 17, 2025, 6:15 AM EDT

BY Doug Kass · Jun 17, 2025, 6:05 AM EDT

The S&P Short Range Oscillator has climbed to 3.11% vs. 2.20% — more overbought.

BY Doug Kass · Jun 17, 2025, 5:55 AM EDT

Dougie Kass

I covered all of my Index trading short rentals on the Trump Tweet... suggesting escalation in Iran.

Covered at:

BY Doug Kass · Jun 17, 2025, 5:45 AM EDT