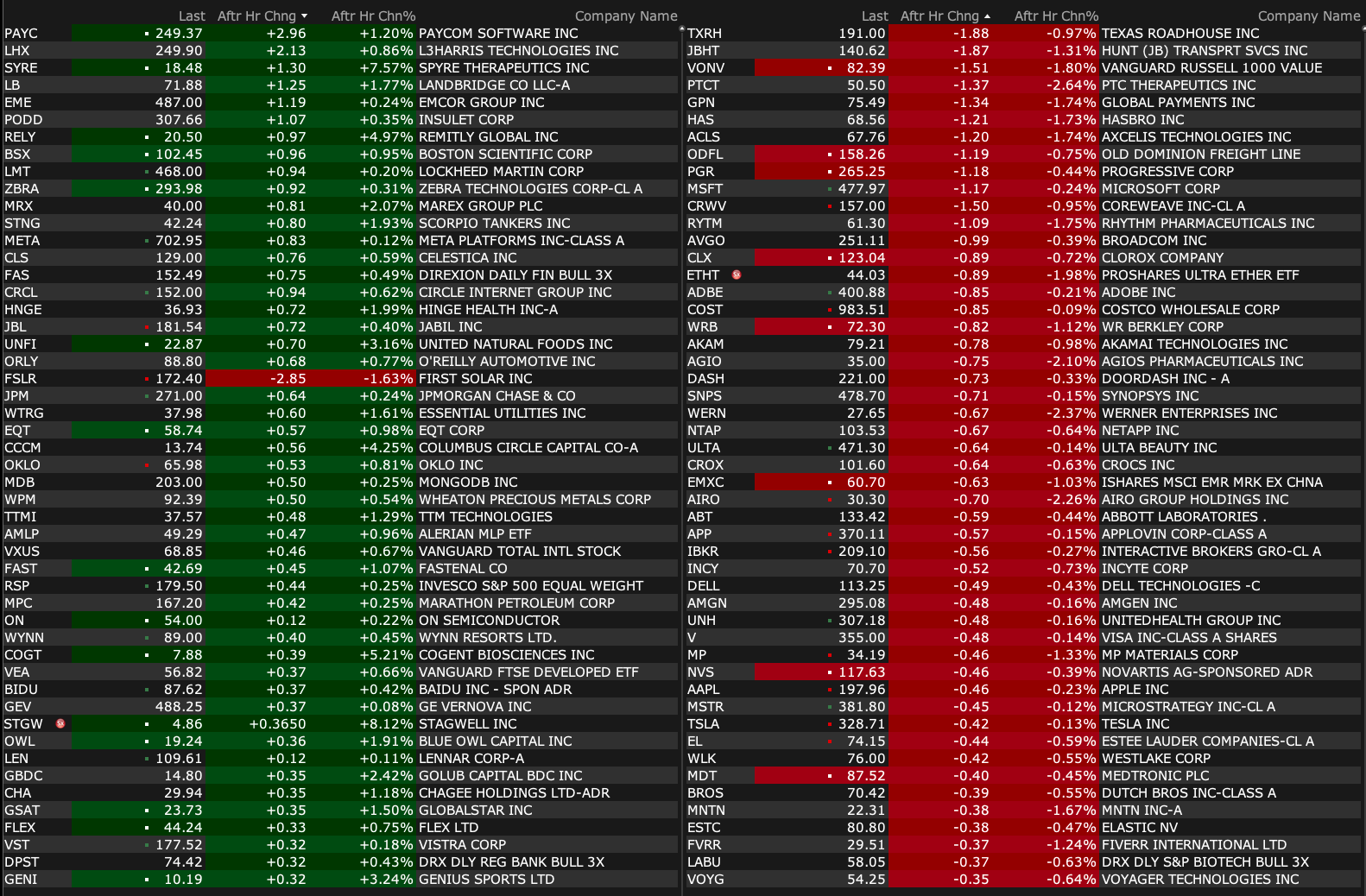

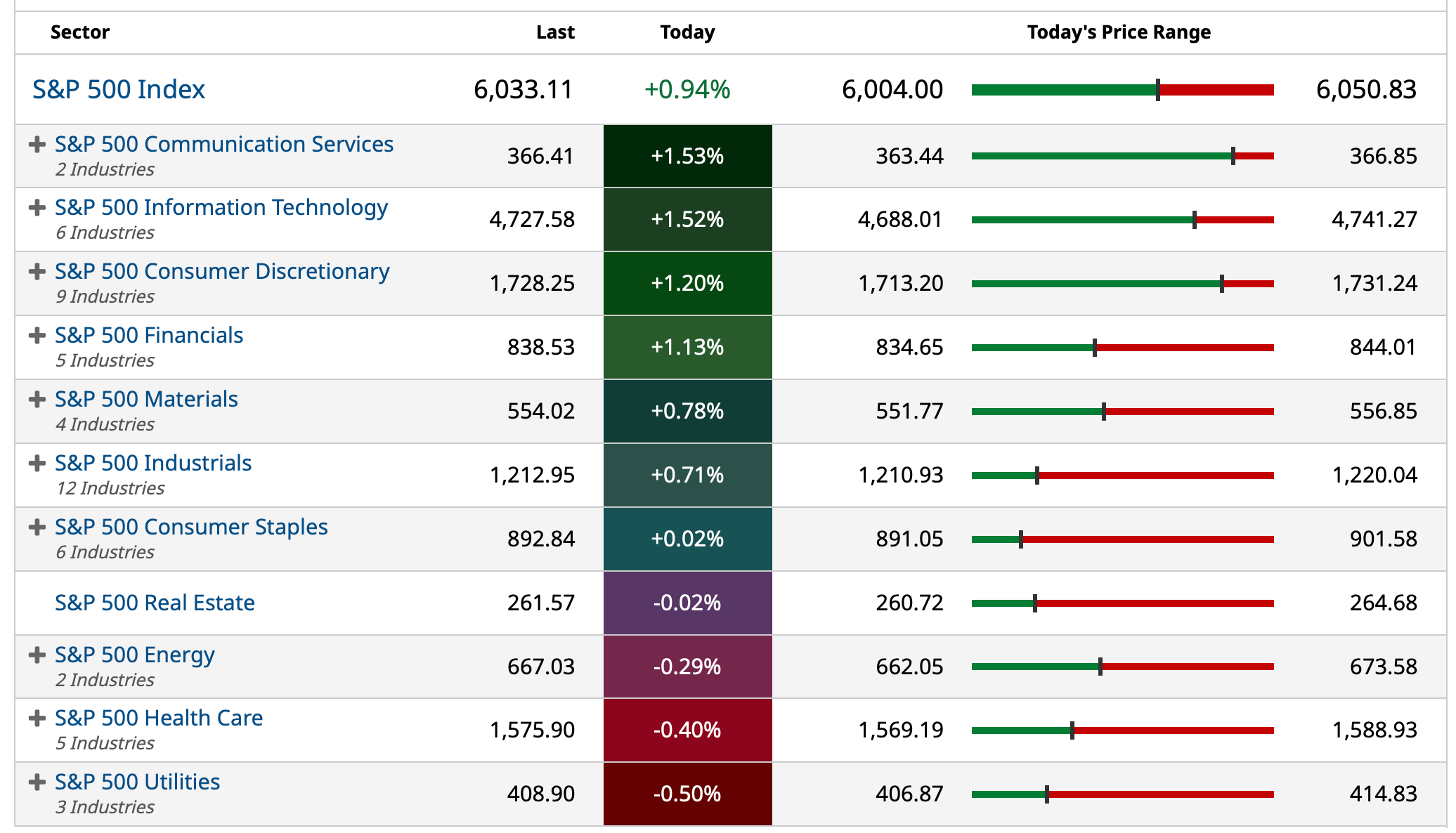

Monday's After-Hours Movers

As of 4:19 p.m.:

BY Doug Kass · Jun 16, 2025, 4:50 PM EDT

As of 4:19 p.m.:

BY Doug Kass · Jun 16, 2025, 4:50 PM EDT

BY Doug Kass · Jun 16, 2025, 4:40 PM EDT

BY Doug Kass · Jun 16, 2025, 4:26 PM EDT

No trades since the last report!

BY Doug Kass · Jun 16, 2025, 3:35 PM EDT

I have a research call between 2 p.m. and 3 p.m.

BY Doug Kass · Jun 16, 2025, 1:05 PM EDT

As of now, all of my longs (over 20 names) are very small-sized.

BY Doug Kass · Jun 16, 2025, 12:50 PM EDT

I have (dispassionately) moved to medium sized short the indices:

* SPY $604.01

* QQQ $534.96

BY Doug Kass · Jun 16, 2025, 11:50 AM EDT

Housekeeping item.

I am covering 2/3 of my small Oracle ORCL short at $211.92.

From this morning:

I shorted a small amount of Oracle (ORCL) at $219.62 on last night's continued climb higher (around 8 p.m.).

I did it solely on the overbought and high RSI — home gamers should not try this and I plan to be out of the trading short rental shortly.

Position: Short ORCL (VS)

By Doug Kass Jun 16, 2025 6:15 AM EDT

BY Doug Kass · Jun 16, 2025, 11:38 AM EDT

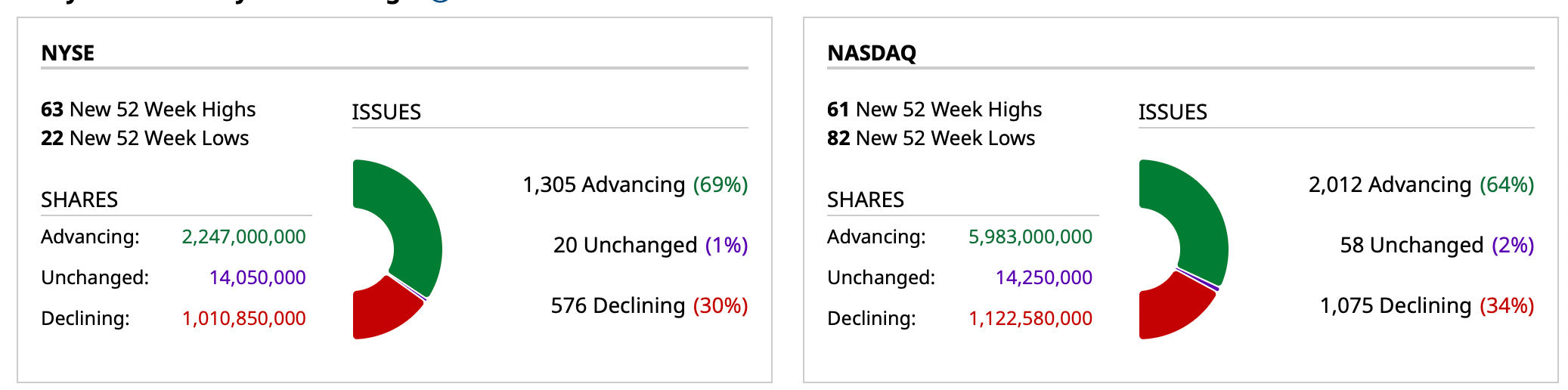

- NYSE volume 14% above its one-month average;

- Nasdaq volume flat to its one-month average;

- VIX index: down 9.17% to 18.91

BY Doug Kass · Jun 16, 2025, 11:13 AM EDT

From Peter Boockvar:

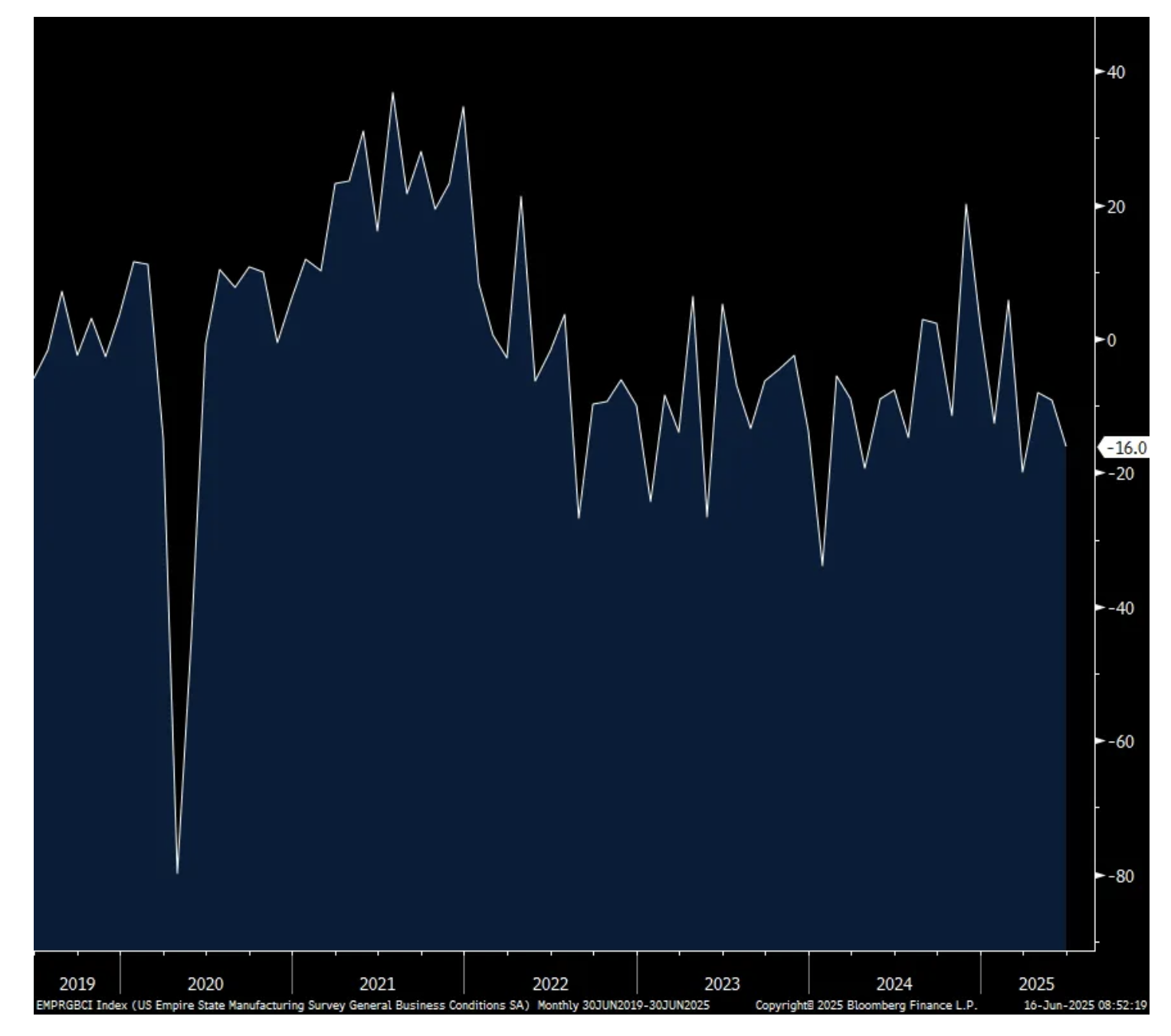

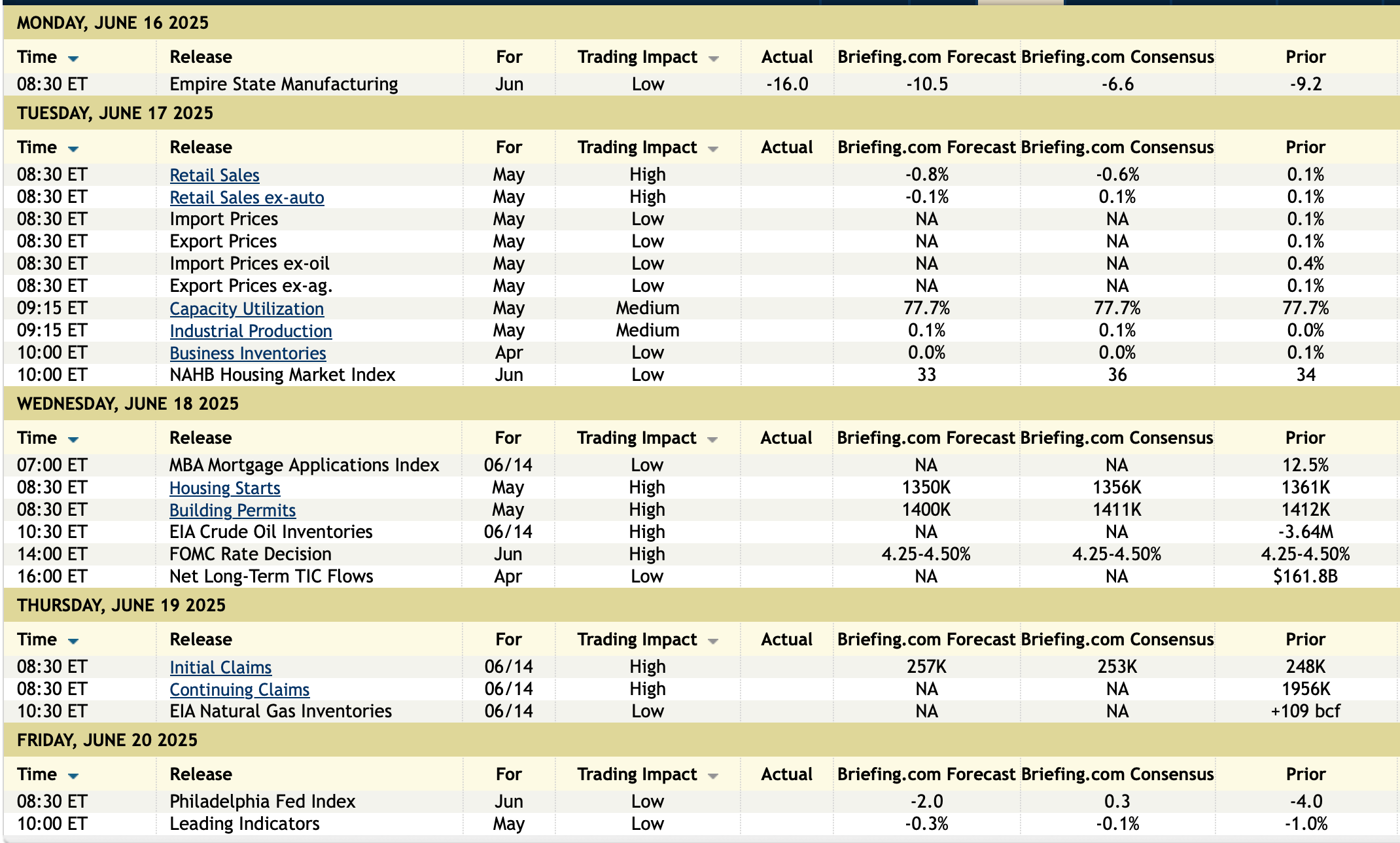

In the first June industrial figure out from the NY Fed, its manufacturing index weakened to -16 from -9.2 and was 10 pts below expectations. Understanding that the internals are extremely volatile month to month I’ll just compare June with the smoothed 6 month average. New orders were -14.2 vs -4.7. Backlogs came in at -8.3 vs -.8. Inventories were +.9 vs +6.8. Employment went positive at 4.7 vs -1.6 but the workweek stayed negative at -1.5 vs -5.5. Delivery time was +1.8 vs +2.1. Prices paid were 47.8 vs 45.1 and those received was 26.6 vs 21.6.

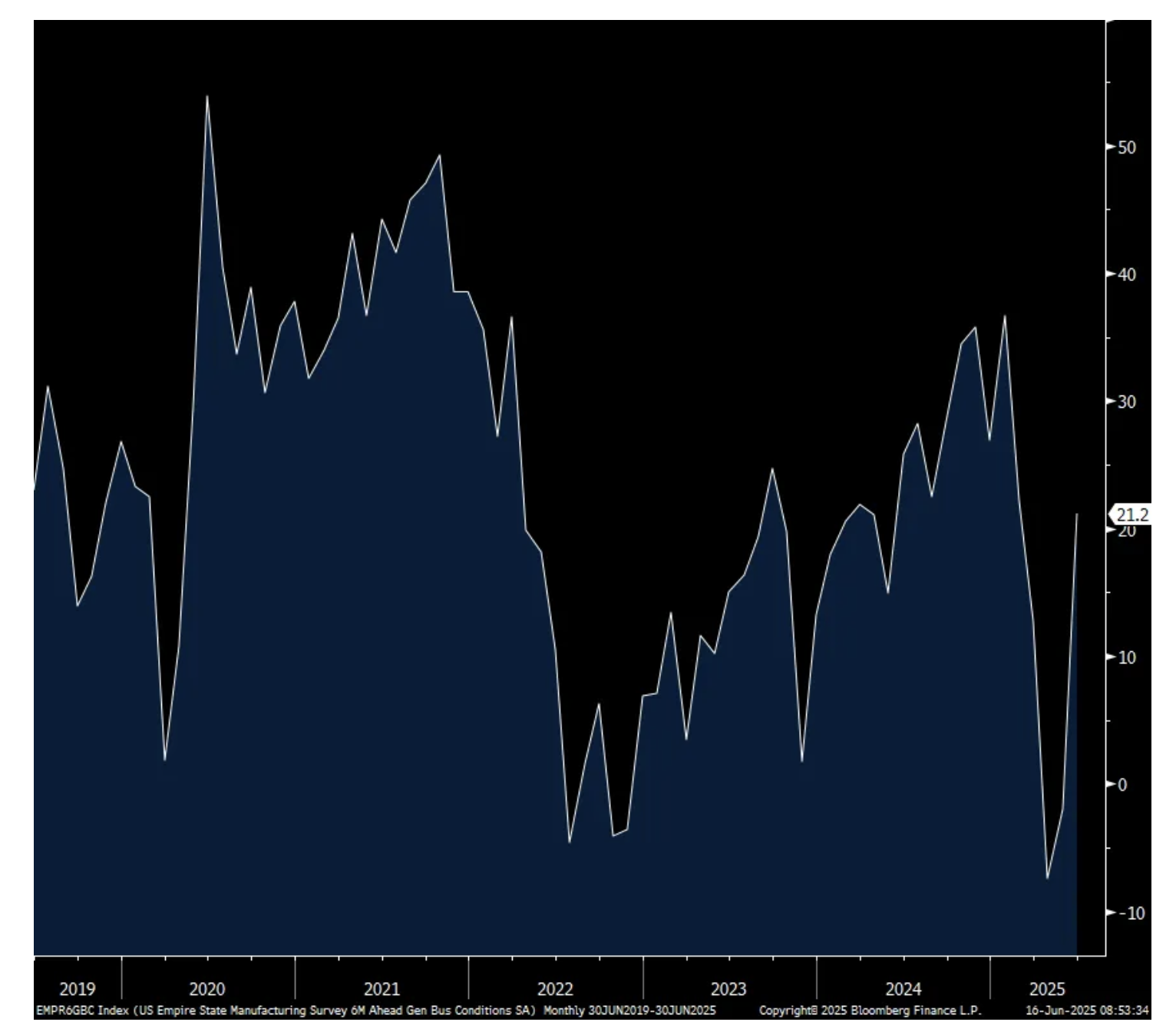

The positive was the jump in the 6 month outlook in business activity which rose to 21.2 vs -2 in May and vs the 6 month average of 13.9. However, capital spending plans remained well below zero at -7.3 vs +3.8 average over the past 6 months. Maybe the tariff front running is done because inventories fell to -14.7 vs the half yr average of -5.9.

Bottom line, since the spring of 2022, this index has spent most of its time below zero and thus in contraction, along with its regional and global peers. The bright spot though as stated was the lift in the 6 month outlook, likely on hopes for a more benign tariff outlook than feared. While tariffs don’t make the job in manufacturing any easier, we have seen some inventory rebuilding but that seems to be just front running those tariffs and could be done as seen with the inventory outlook. Semiconductor companies in particular have talked about industrial chip inventory restocking.

Nothing market moving here but a reminder that the US economy continues to be very much a mixed bag of activity with strength in upper income spending, anything touching the AI capital spending ecosystem and still robust levels of government spending but this pace in government spend is seemingly about to slow (great long term but not so short term). Weakness outside of manufacturing is still being seen in housing with the sales of existing homes no different than where it stood in 1978. Lower to middle income consumers are dealing with their own financial stresses and prioritizing needs more so than wants, with value a big winner. Construction is very uneven and only strong if benefiting from government tax benefits such as with chips and/or batteries. Capital spending outside of AI has been flat lining and now the pace of hiring is slowing with a possible pick up in firing’s as seen in the lift in initial claims, though still remains low.

NY Manufacturing Index

Six Month Business Activity Outlook

BY Doug Kass · Jun 16, 2025, 10:20 AM EDT

8 a.m. ET: Fed Treasury Repo Reference Rate;

11:30 a.m.: Treasury hosts a $76B 3 and $68B 6-Month Bill Auction;

1 p.m.: Treasury hosts a $13B 20-Year Bond Auction

BY Doug Kass · Jun 16, 2025, 10:05 AM EDT

From Peter Boockvar:

Now that everyone knows where the Strait of Hormuz is on the map (the waterway that Saudi Arabia, the UAE, Kuwait, Iraq and Iran use to ship most of their crude oil exports through), history shows never to chase a geopolitical move UNLESS actual supply disruption takes place. As oil is a key supply of cash to the Iranian regime, I don't see the strait being closed, unless the regime gets really desperate. China, Iran's biggest customer, would not be happy either if it were to happen and it would likely ignite a US military response. That said, no ship passing through seems safe for now from rogue firings. So, while I'm very bullish on oil prices/stocks here, a geopolitical premium is not the reason.

With regards to the gas fields in Iran that blew up, they seem to be gathering and processing facilities, along with storage units that are for domestic use and why global prices were not impacted. The Financial Times makes a great point on this over the weekend, "The attacks suggest Israel is attempting to weaken and disrupt Iran's domestic gas and fuel supply chains to cause shortages, rather than pursuing the country's oil and gas production or exports, which would rock the markets."

As for the last crude oil rig count figure before the price spike, it fell by another 3 rigs and now lower by 36 over the past 7 weeks and by 49 off the February high of the year and at the least since October 2021.

Crude Oil Rig Count

Meanwhile, with still the risk that Iran does something with the strait in a panic, it highlights the big mistake of using our Strategic Petroleum Reserve for manipulating prices for political purposes rather than what it was meant for, filling in actual supply disruptions of note.

SPR Inventory

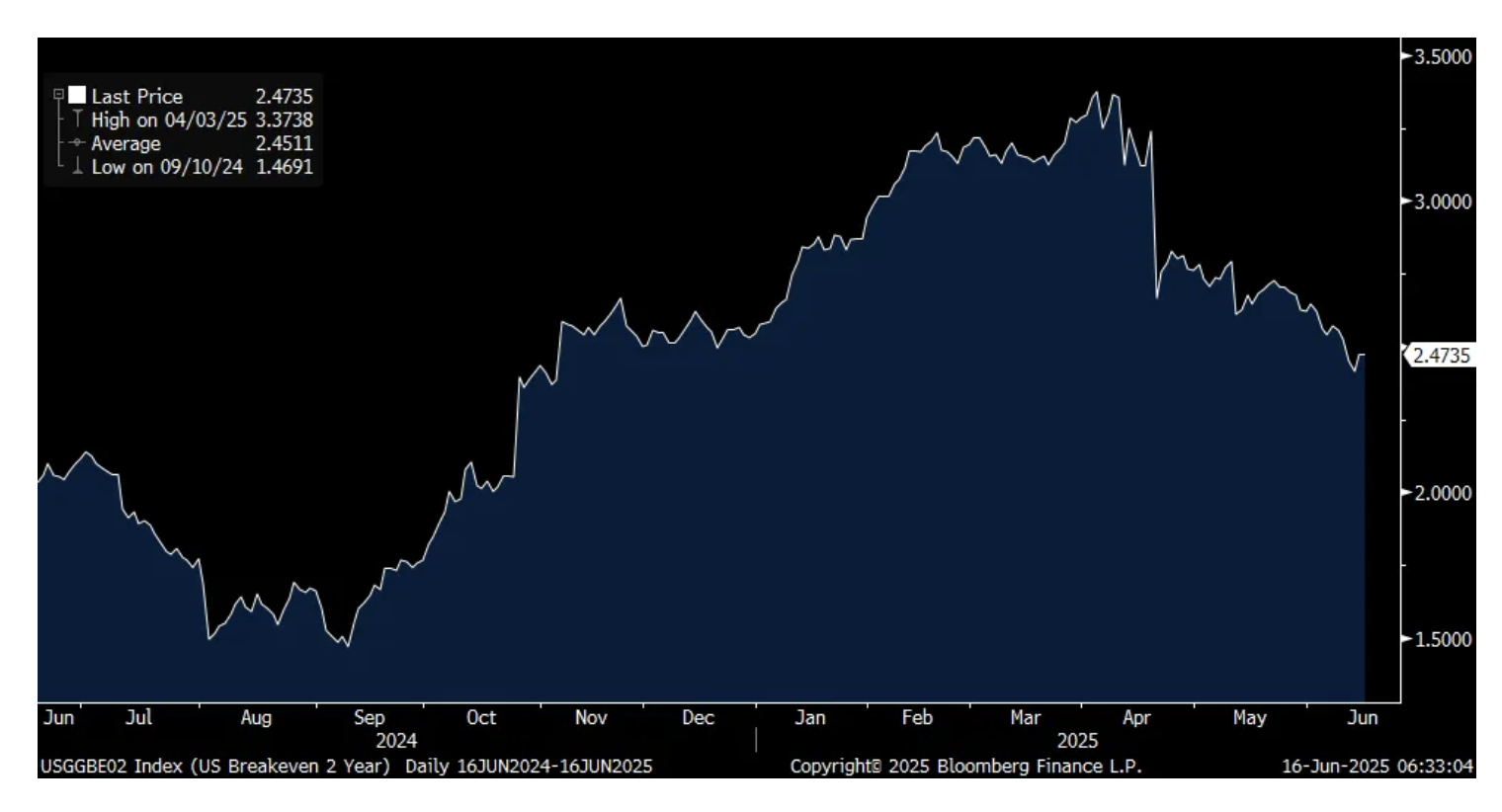

As short term inflation breakevens are highly influenced by oil prices, the 2 yr implied inflation rate did rise by 6.3 bps on Friday to 2.47% but well off its recent highs, though 100 bps off its lows last year. In fact, the one yr average is 2.45%.

2 yr Inflation Breakeven

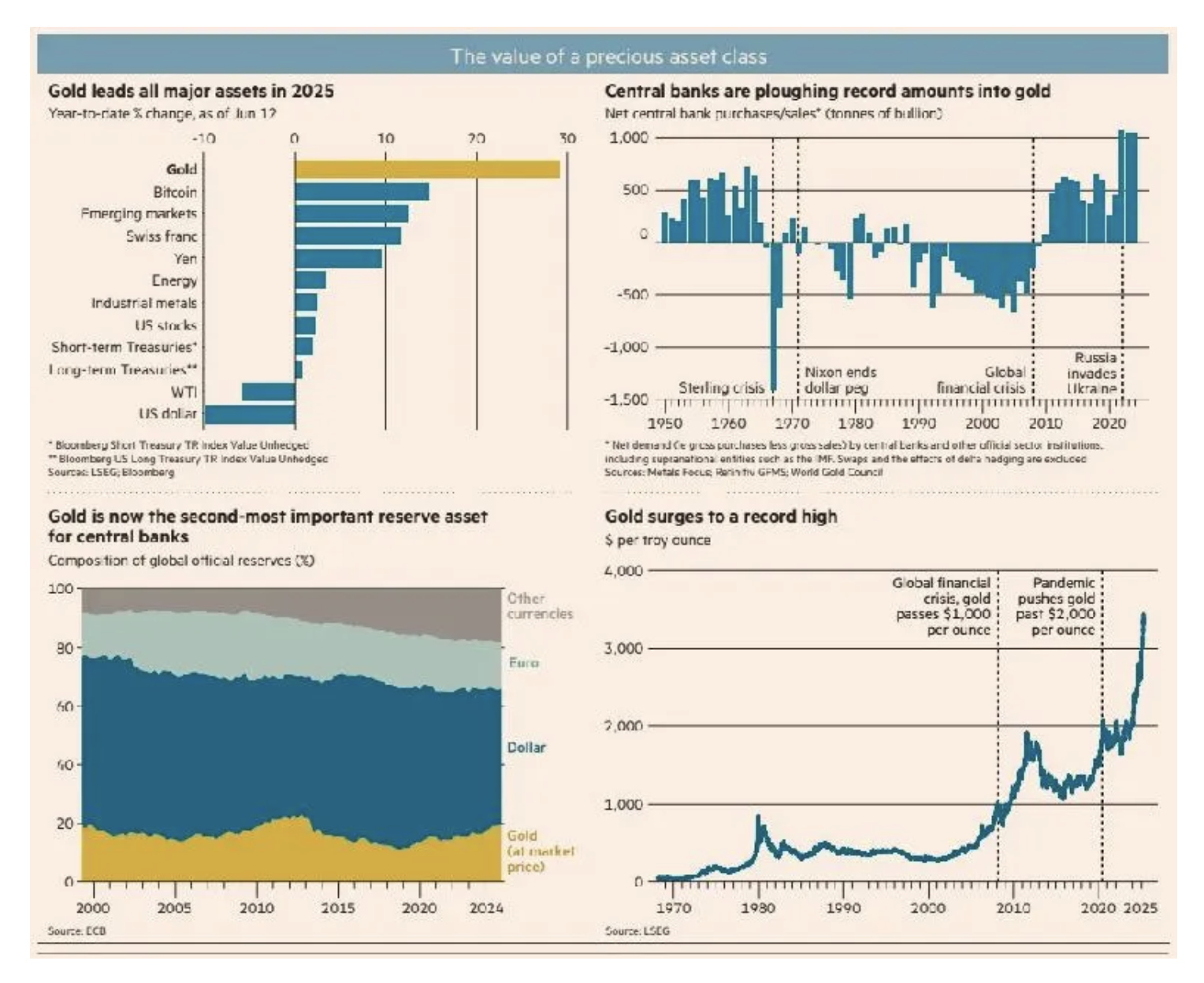

Last week the ECB in a paper said that gold is now the #2 global reserve asset on the books of central banks, helped by both purchases and price appreciation, surpassing the euro and behind the US dollar. The Weekend FT had good charts on this.

While the Fed meets on Wednesday, the Bank of Japan gathers too and we await what they will say on their asset purchases. Chatter is that they will slow the pace of balance sheet shrinkage but also leave open the possibility of more rate hikes this year, with the latter influencing the long end of the curve and the former doing it with the short end. What happens there impacts what happens here in terms of fund flows and longer term rate moves.

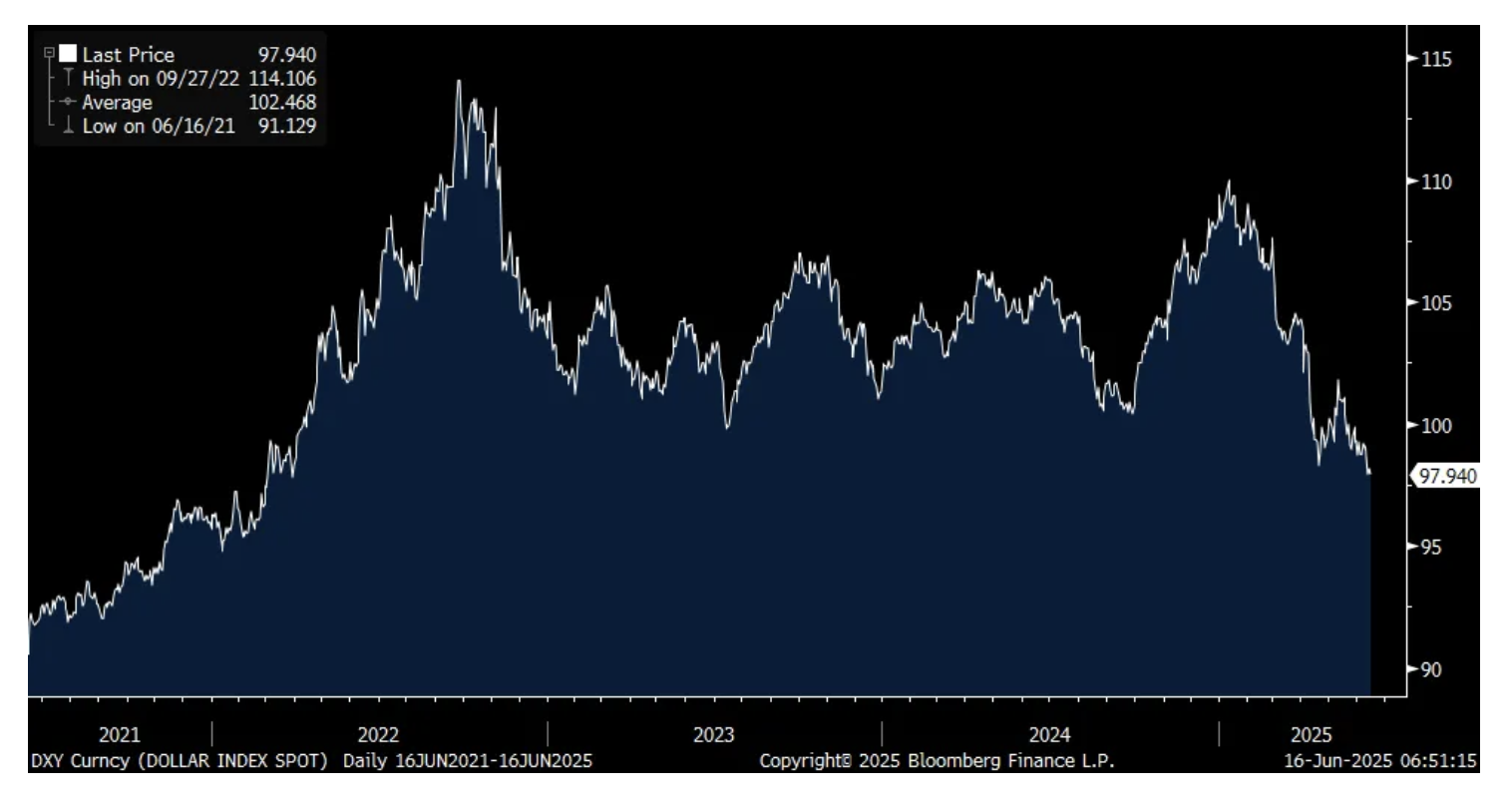

With US Treasuries, while they rallied last week, Friday's sell off in the face of the oil price spike, or maybe because of it, was noteworthy. And, today's US dollar weakness is giving back Friday's modest rise. No safe haven status here, gold is instead.

40 yr JGB Yield

China reported some May data. Retail sales grew by 6.4% y/o/y, above the estimate of 4.9% but likely helped by cash for clunkers type policy that only pulls forward spending at the expense of future spending. I’d rather see an organic improvement in consumer spending. Also boosting sales was the 618 (usually goes from June 1-June 18) shopping festival that takes place each year that started in late May rather than on June 1st. Industrial production was higher by 5.8% y/o/y, just under the estimate of 6%. Not surprising, property investment remained weak, down by 10.7% with home prices, both new and used, still falling in May m/o/m.

The Hang Seng rallied by .7% and is now up 20% year to date and by 41% since the beginning of 2024 when I expressed my belief that it would start to outperform the S&P 500.

BY Doug Kass · Jun 16, 2025, 9:49 AM EDT

Adding to Index shorts:

* SPY $601.20

* QQQ $531.96

BY Doug Kass · Jun 16, 2025, 9:44 AM EDT

Let's start this "Tales" with a CNET article: "LetChatGPT Just Got 'Absolutely Wrecked' at Chess, Losing to a 1970s-Era Atari 2600 - An engineer's experiment yielded a surprising result for OpenAI's popular chatbot."

It looks like an Atari 2600 can be had for $54.95. It came out in 1977. The chip running that thing is a tiny fraction of what is in a modern day handset, and might be what is in a modern day Toto toilet (in my view, the single best invention since the internet): I think at one point, a single NVDA board was going for close to $100,000. It takes thousands, if not well into the tens of thousands, of chips to train an AI model. I have heard numbers of up to 100,000:

Having said all of that, using Gen AI as the underlying technology, I suspect it could be “trained” to play chess. Not sure exactly how. Maybe would have to feed it billions of images of what the optimal move is in each situation.

But I think the potential number of moves in chess is an incomprehensibly large number. It cannot be fed what to do in every situation. Whatever is done, the end result would be something that would not beat the best human chess players. It would be incredibly expensive to get there (capital cost of the compute and training cost), and expensive to run. And of course, the training methodology would have to be developed by humans!

P.S. now I am wondering what the theoretical AI-powered Toto might do? And god forbid it hallucinated, do I end up with a mouth wash instead of a tush wash?😊

BY Doug Kass · Jun 16, 2025, 9:35 AM EDT

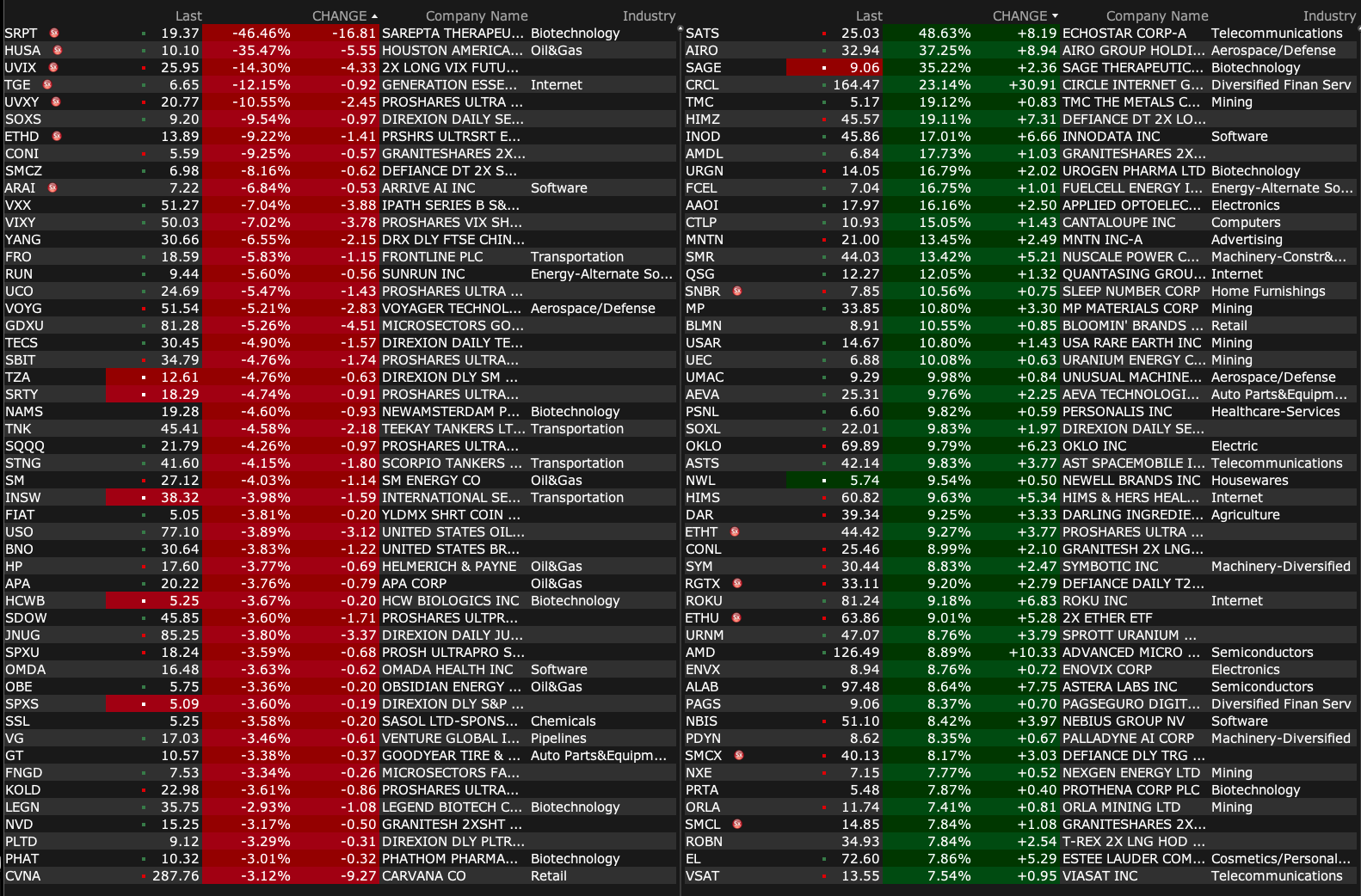

-SATS +43% (reportedly President Trump has urged EchoStar Chairman Charlie Ergen and FCC Chairman Carr to reach a deal on EchoStar spectrum)

-SAGE +36% (to be acquired by Supernus Pharma at $8.50/shr in cash plus non-tradable CVR worth up to $3.50/shr total, up to $12.00/shr or $795M)

-SVRE +34% (signs Preliminary Agreement with Leading European ADAS Technology Provider for Sensor Fusion Collaboration)

-SONM +28% (receives unsolicited indication of interest to be acquired by Doogee for $3.60/shr cash)

-AIRO +25% (post-IPO momentum)

-SBET +16% (bounce off recent lows)

-SSII +12% (announces Successful Completion of First Robotic Cardiac Surgery in the Western Hemisphere Utilizing the Company’s SSi Mantra 3 Surgical Robotic System)

-CANF +10% (to present Phase IIa Pancreatic Cancer Study Progress during Partnering Meetings at the 2025 BIO International Convention in Boston)

-CRCL +9.7% (post-IPO momentum)

-RITR +9.3% (proposes to Issue Bitcoin "RBTC" Pegged Token and Plans to Apply for "RHKD" Hong Kong's Stablecoin License)

-AIOT +9.0% (earnings)

-TE +8.6% (advances $850M planned 5GW solar cell plant)

-TMC +8.3% (announces Strategic Investment from Non-Ferrous Metal Refining and pCAM Technology Provider Korea Zinc, which will invest strategic equity investment in TMC of $85.2M in exchange for 19.6M common shares at $4.34/shr)

-ROKU +8.1% (Amazon Ads and Roku Announce Partnership Creating the Largest Authenticated CTV Footprint)

-LTRN +7.9% (announces clinical observations for a patient in Lantern’s Phase 2 HARMONIC clinical trial)

-VSCO +7.5% (Holder Barington Capital Group (1%) said to 'push' to overhaul Company board)

-INCY +7.4% (hearing Stifel Nicolaus Raised INCY to Buy from Hold, price target: $107)

-FWRD +5.6% (reportedly receiving takeover interest from private equity)

-MNTN +5.3% (Raymond James Initiates MNTN with Outperform, price target: $27)

-X +5.1% (US President Trump approves merger with Nippon SteelUS Pres Trump approves merger with Nippon Steel)

-ACHR +5.0% (raises $850M Following White House Executive Order To Accelerate U.S. eVTOL Rollout; signs deal to deploy Midnight aircraft in Indonesia)

-CELH +5.0% (TD Cowen Raised CELH to Buy from Hold, price target: $55 from $37)

-HDSN +4.7% (B. Riley FBR, Inc. Raised HDSN to Buy from Neutral, price target: $9)

-SW +3.9% (Jefferies Raised SW to Buy from Hold, price target: $55)

-PSNY +2.9% (announces $200M equity investment entity that is controlled by Mr. Shufu (Eric) Li, Founder and Chairman of Geely Holding Group)

-SRPT -38% (reportedly Roche discontinued the commercial and clinical use of Elevidys after two cases of fatal acute liver failure)

-KALV -6.3% (announces Delay in FDA Decision on Sebetralstat NDA for Hereditary Angioedema Due to "Agency Resource Constraints"; FDA anticipates reaching a decision within approximately four weeks)

-PETS -2.0% (prelim earnings)

BY Doug Kass · Jun 16, 2025, 9:21 AM EDT

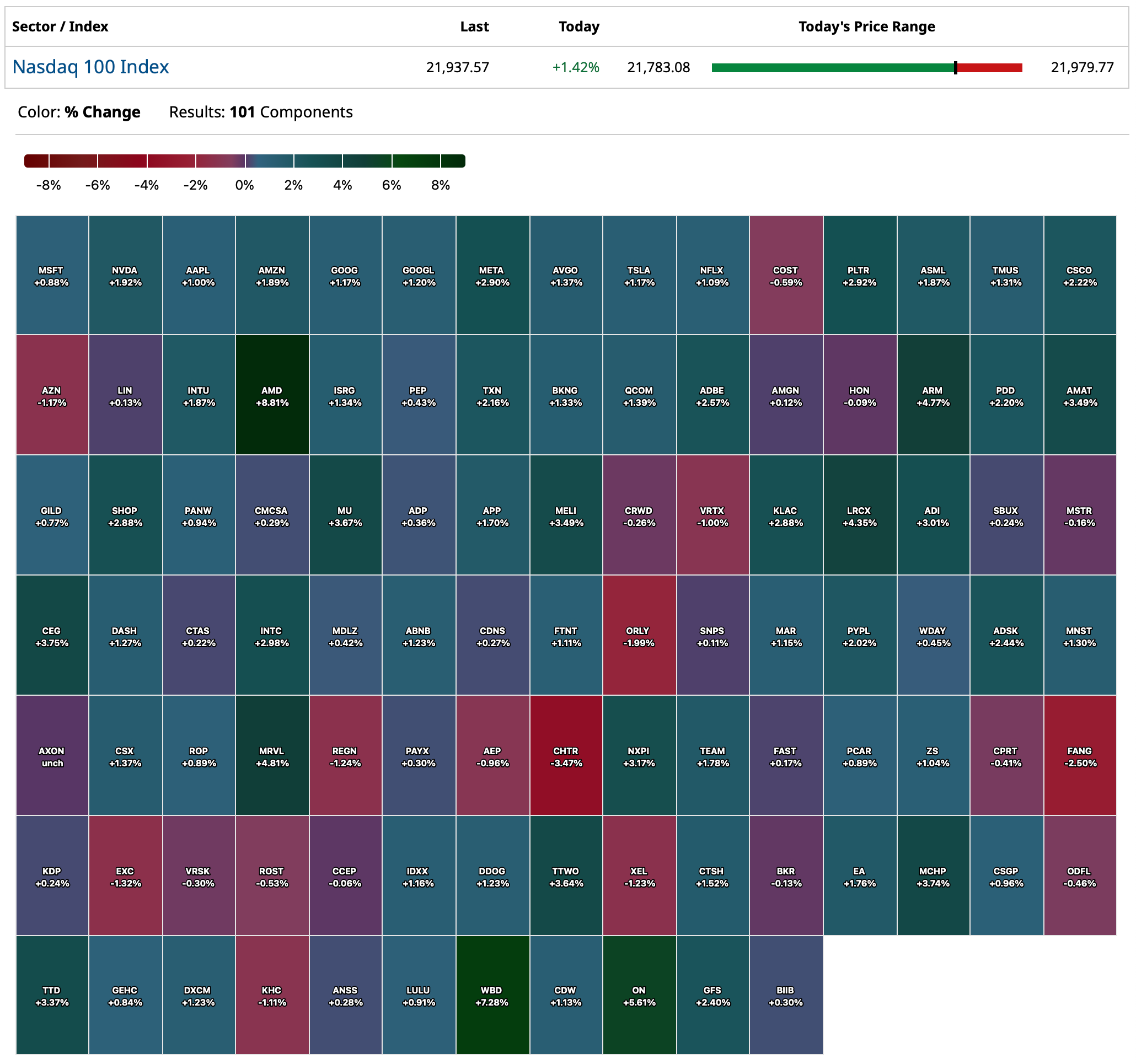

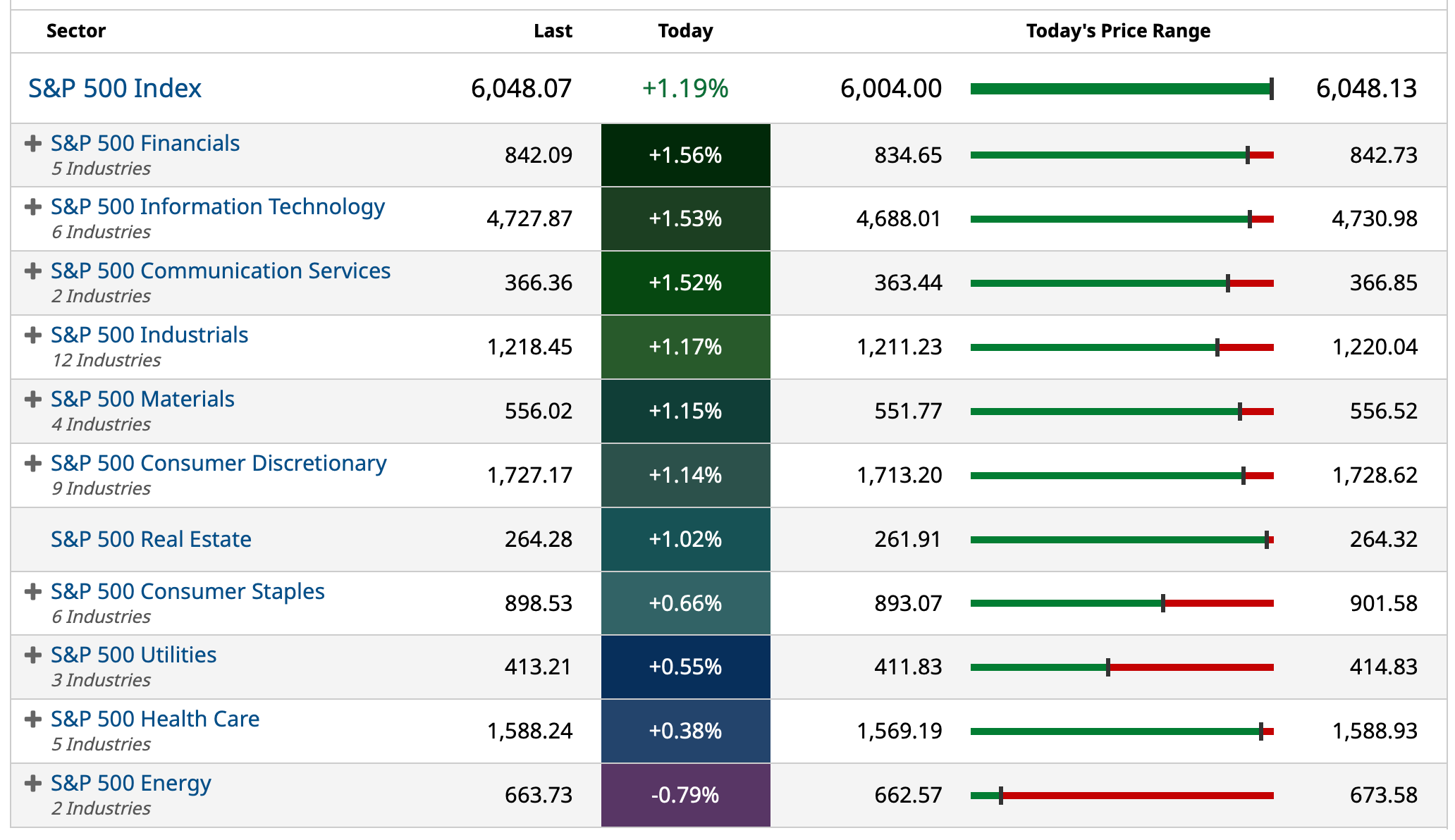

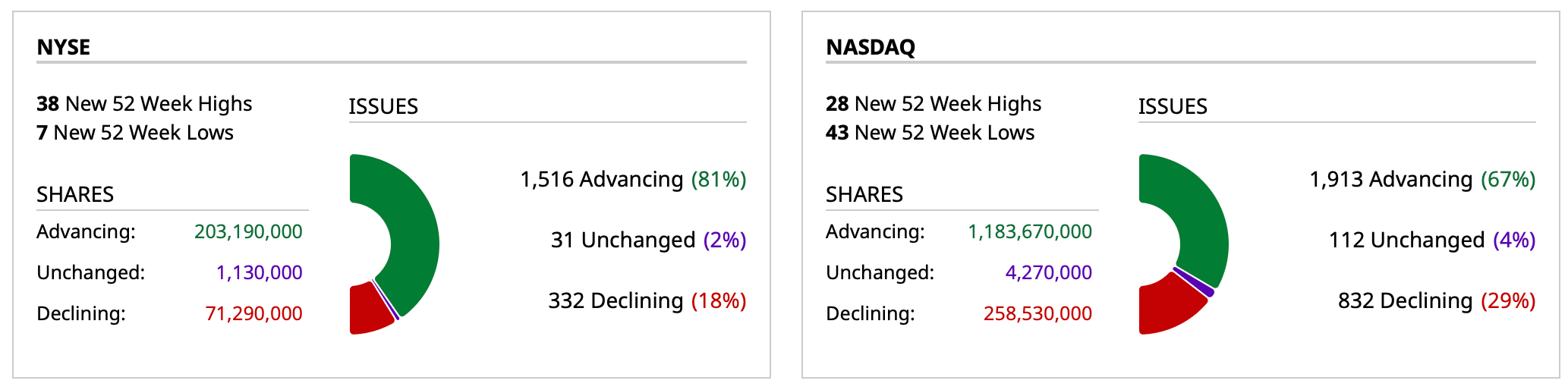

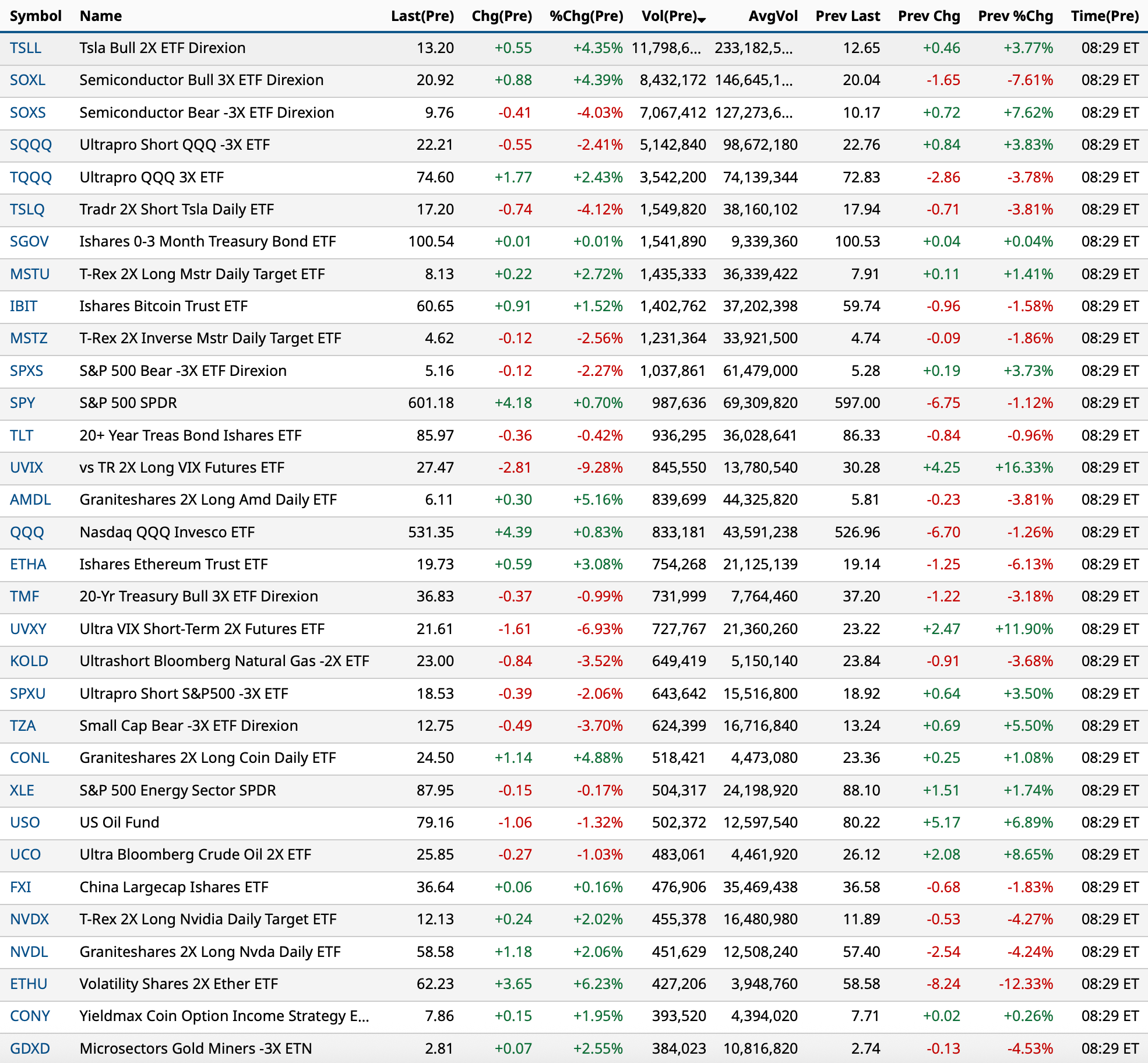

Charts from 8:29 a.m. ET:

BY Doug Kass · Jun 16, 2025, 9:13 AM EDT

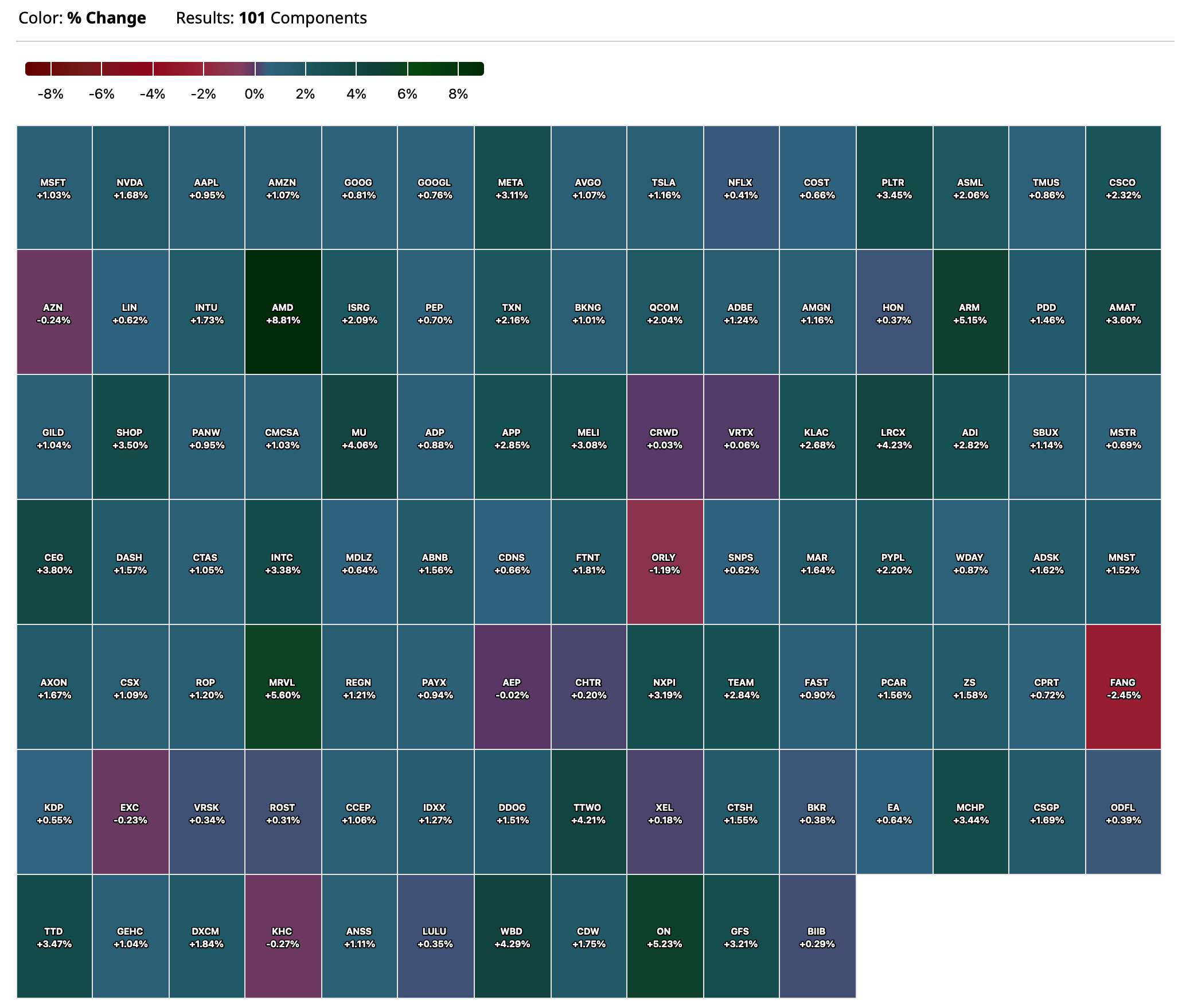

Chart from 8:46 a.m. ET:

BY Doug Kass · Jun 16, 2025, 9:03 AM EDT

* But bull markets die hard...

You say

The price of my love's not a price that you're willing to pay

You cry

In your tea, which you hurl in the sea when you see me go by

Why so sad?

Remember, we made an arrangement when you went away

Now, you're making me mad

Remember, despite our estrangement, I'm your man

You'll be back, soon, you'll see

You'll remember you belong to me

You'll be back, time will tell

You'll remember that I served you well

Oceans rise, empires fall

We have seen each other through it all

And when push comes to shove

I will send a fully armed battalion to remind you of my love!

- You'll Be Back - Hamilton (Original Cast 2016 - Live)

With S&P futures +30 handles, reversing an earlier -30 handle decline near Sunday night's opening -- it continues to be clear that bull markets die hard.

As expressed in the last two weeks, however ("Downside Market Risk Is About 5-Times Upside Reward" and "Goodbye Goldilocks (Hello Reality)") I expect equities to be pressured over the next few months.

The Israeli/Iran conflict (now into its fourth day) is yet another of a long list of uncertainties that investors face. And with a starting point of a 22.5-times price earnings ratio, investors are underappreciating and underpricing risk:

* We face the highest geopolitical risks in many decades (which will not be resolved quickly).

* We face the largest level of social and political risks in the U.S. since the Vietnam war.

* We face the greatest chance of "slugflation" (slowing economic growth and sticky inflation) since the 1970s.

* We face the biggest threat that the U.S. dollar and capital markets will no longer be a "safe haven" in modern history.

* We face the greatest debt load and deficit ever -- and neither party seems to favor any fiscal discipline whatsoever.

* We face the largest capital spending spree in history (on artificial intelligence) -- though the return on that investment is less certain (dot.com, it feels like deja vu all over again.) (More on this shortly)

* We face a viable alternative to equities in fixed income (for the first time in 15 years) as bonds present an equity-equivalent yield with limited risk and volatility.

As I noted on Thursday, I plan to expand my short exposure on any further rallies.

Recognizing the strength of price momentum since early April I plan to give the market a relatively wide berth in scaling into shorts.

BY Doug Kass · Jun 16, 2025, 8:27 AM EDT

BY Doug Kass · Jun 16, 2025, 7:20 AM EDT

* From the "other" Dougie

douglas cassel

The Israeli-Iran "experts" are wrong yet again. The latest obsession has been the need for USA involvement to destroy the underground Iranian nuclear facilities. It is true that without bunker busters, and the USA planes to deliver them, the bunkers are too deep for Israeli bombs.

As anyone can see, the Israeli's have been planning this attack for 30 years. Presidents such as Obama or Harris would never have agreed to enter such a war. The Israeli's have thought of this and have a plan. They will not stop this war without destruction of the Iranian nuclear threat.

The Israeli's have achieved air dominance, a specific term, they can operate without significant interference from the opposing air force.

If the USA does not offer bunker busters, the Israeli's will send in ground soldiers to destroy these facilities. Probably planes with soldiers that land near the facilities. You heard it here first.

A few more things.

1) Killing civilians with random ballistic missiles has little military value. Germany, England, and the USA killed millions of civilians in WW2 with minimal military impact. The news companies adding up casualties is just not relevant.

2) The markets being up might be a realization that the world without a nuclear armed, fanatical Iranian regime might be a much better place.

Less funding of terrorist groups all over the world.

3) Russia is dependent upon Iranian drones and missiles. Without them

Ukraine is in a much better position.

4). I said it before. Modern societies cannot function without electricity, gasoline and lights. Israel has the capability of cutting these things off for a large portion of Iran. This war is close to being decided.

Israel Takes Control of Iran’s Skies—a Feat That Still Eludes Russia in Ukraine

BY Doug Kass · Jun 16, 2025, 7:10 AM EDT

From JPMorgan (moving from tactically bullish to cautious!):

· US MKT INTEL – moving from tactically bullish to cautious, heightened potential for a pullback creating a buy-the-dip moment. Longer-term the foundation for the bull case remains intact, assuming we receive tariff relief and/or make permanent current levels.

and...

EQUITY & MACRO NARRATIVE

The SPX officially re-entered bull market territory last week, breaching the 20% threshold but given the rapid shift in geopolitics and looming deadline for the expiration of the trade deals, with Trump to set levels this week or next, it seems likely that markets are set for a near-term pullback. We are shifting our view to tactically cautious, with a pullback risk increasing following an assumed spike in volatility across multiple asset classes and positioning becoming increasingly stretched. While we think that much of the bull case remains in replace, it feels prudent to be more conservative with risk until we gain more clarity on US involvement in the Middle East, the extent to which energy prices spike, the impact on bond yields/USD, and ultimately whether this latest conflict drives a further move away from dollar-denominated assets.

· ESCALATION POTENTIAL – On Sunday, Trump indicated that the US may get involved while also indicating that he is open to having Russian mediate the conflict; Russia is a strategic ally of Iran having work against the US in recent wars in Iraq and Syria (BBG). Separately, Trump vetoed a plan to kill Iran’s Supreme Leader (RTRS; US News). This conflict may spread from an operation to destroy nuclear and ballistic missile capabilities to one that looks more like regime change; if the latter, then should be considered multi-month/multi-quarter type of conflict. If we avoid escalation, the negative impact on markets may be 1-3 weeks.

· SHORT-TERM INFLATION SPIKE – Natasha flagged the potential for crude prices to move to $120/bbl. This would exacerbate the current trend which has seen WTI +20% MTD with gasoline +9.3%; UK and European natgas are +13.7% and +12.7%, though returns are in USD.

· PROFIT-TAKING – YTD US returns have not been impressive but since the April 8 low, we have seen some strong moves with the SPX +20%, NDX +26.6%, SPX Tech sector +33.35, SOX Index +42.7%, ARKK +53.5%, Retailers +21.3%, and WTI +22.5% (full chart is after the Monetization Menu section). We may see investors take profits given the heightened uncertainty from geopolitics and trade. In some sub-sectors, seasonality is turning negative. E.g., SOX Index has averaged a -1.1% return in June, over the last 25 years, and then has increased that loss with an average return of -3.1% from July – September. The SOX has been seen more negative returns than positive June – Sept, with stats summarized below. Lastly, positioning in Semis appears to be stretched.

· ROTATION POTENTIAL – When viewing performance from the April 8 bottom to Friday, SPX is +20% vs. global returns (MXWO) of 19.9%, EU (MXEU) +18.2%, APAC (MXAP) +19.1%, and Latam (MXLA) of 19.4%. YTD, SPX trails global returns by 350bp, APAC by 748bp, EU by 1818bp, and Latam by 2097bp. Given the recent performance of US Tech and global AI, it seems unlikely that we see a similar performance gap by the US as that witnessed in the first quarter of the year. The commodity price spike will create some distinct country-level winners the role of the consumer may be critical when viewing DM opportunities; the US consumer is relatively stronger than their counterparts so may be better able to withstand the energy price spike despite the tariff uncertainty. Further, the USD may return to being a safety haven, further pressuring ex-US trades.

· US MKT INTEL VIEW – We shift from tactically bullish to cautious; our new hypothesis looks to trade around the spike in geopolitical tensions while navigating pullback risk. Any consolidation is likely to be shallow given the spike in energy prices may not derail the bull case, we think there is a buy-the-dip moment on any pullback. Positioning indicates that, irrespective of Israel/Iran, the market was setting up for a pullback. That said, Friday’s price action felt muted, potentially as investors await to better understand the Israel/Iran situation. While there has been a strong buy-the-dip mentality with investors having been rewarded for fading negative news this year, we think it best to pull back on risk into this week. The combination of (i) Russia targeting Ukrainian refining sites and thus increasing the probability of Ukraine doing a similar activity and (ii) the escalating situation in the Middle East with energy infra being a key target means that we are likely to see a materially higher move in energy prices. This occurs at a time when consumer (and investor) sentiment is hitting local highs and muddles an already complicated inflation story.

o RISKS – (i) a quick resolution of Israel/Iran without further escalation in Russia/Ukraine – futures are trading as though the conflict has been resolved without chance of further escalation; (ii) a series of trade deals is able to decrease inflation expectations despite the energy price spike; (iii) investors start pricing in a US fiscal stimulus from a higher/new budget allocation to military spending.

BY Doug Kass · Jun 16, 2025, 7:00 AM EDT

and...

and...

Note: As I have chronicled in my Diary, there have been a plethora of "false starts" (to be sold) in terms of favorable legislative gains for the cannabis industry. So we should treat these tweets with skepticism. That said, stay tuned...

BY Doug Kass · Jun 16, 2025, 6:50 AM EDT

BY Doug Kass · Jun 16, 2025, 6:35 AM EDT

BY Doug Kass · Jun 16, 2025, 6:25 AM EDT

I shorted a small amount of Oracle ORCL at $219.62 on last night's continued climb higher (around 8 p.m.).

I did it solely on the overbought and high RSI — home gamers should not try this and I plan to be out of the trading short rental shortly.

BY Doug Kass · Jun 16, 2025, 6:15 AM EDT

BY Doug Kass · Jun 16, 2025, 6:05 AM EDT

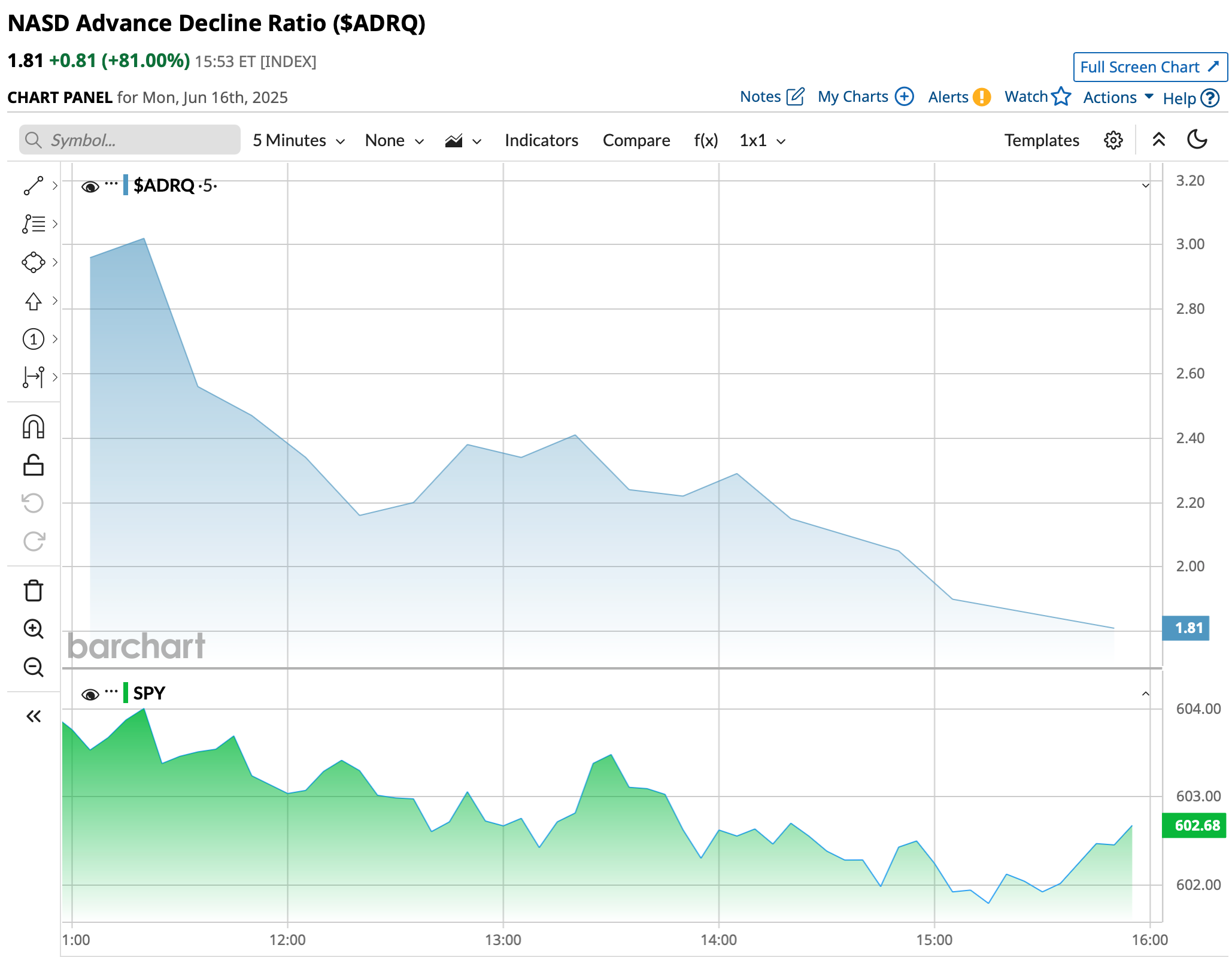

The S&P Short Range Oscillator slipped from 3.32% to 2.73%.

BY Doug Kass · Jun 16, 2025, 5:55 AM EDT

I shorted the indices on a +30 handle boost in stock futures:

* SPY $599.50

* QQQ $529.46

BY Doug Kass · Jun 16, 2025, 5:45 AM EDT