Friday Closing Advance-Decline vs. SPY

Intraday:

BY Doug Kass · Jun 13, 2025, 4:55 PM EDT

Intraday:

BY Doug Kass · Jun 13, 2025, 4:55 PM EDT

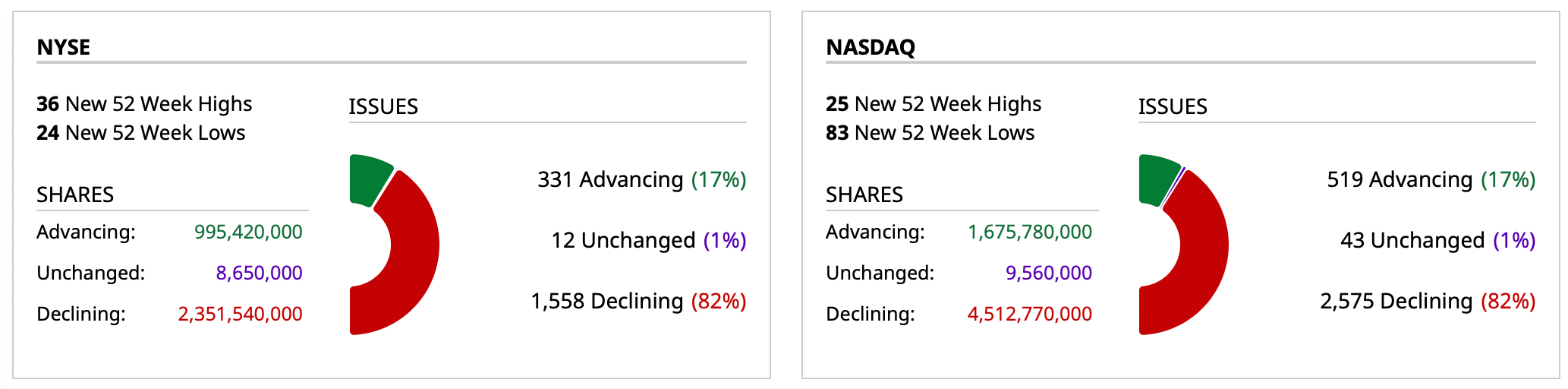

- NYSE volume 8% above its one-month average;

- NASDAQ volume, 5% below its one-month average;

- VIX index: up 17.15% to 21.11

BY Doug Kass · Jun 13, 2025, 4:44 PM EDT

Thanks for reading my Diary today and all week.

I hope I added value to your decision-making process..

Enjoy the weekend.

Be safe.

BY Doug Kass · Jun 13, 2025, 4:15 PM EDT

BY Doug Kass · Jun 13, 2025, 3:36 PM EDT

* SPY $601.44

* QQQ $531.27

From earlier in the day:

I'm re-shorting the indices with cash -23 handles.

Position: Short SPY (VS), QQQ (VS)

By Doug Kass Jun 13, 2025 11:57 AM EDT

BY Doug Kass · Jun 13, 2025, 3:00 PM EDT

From Peter Boockvar:

Positives,

1) May Israel achieve the safety, security and peace of mind by destroying the means and personnel that threaten their existence and may many in Iran who have been yearning for freedom for decades from the repressive regime finally get a chance to live it.

2) May CPI rose one tenth both headline and core, below the estimates of up .2% and .3%. The y/o/y gains of 2.4% and 2.8% compare with 2.3% and 2.8% in the month before. Helping to calm the headline figure was the 1% fall in energy prices m/o/m and down 3.5% y/o/y, mostly due to lower gasoline prices, while food prices were up by .3% m/o/m and by 2.9% y/o/y. Prices for ‘food at home’ were up by .3% m/o/m after falling by .4% last month and higher by 2.2% y/o/y. ‘Food away from home’ is where more of the food inflation is taking place as prices here were up by .3% m/o/m and 3.8% y/o/y. Services prices ex energy were up by .2% m/o/m and 3.6% y/o/y. Core goods prices were flat m/o/m and up a slight .3% y/o/y.

3) May PPI was higher by one tenth for both headline and core vs the estimate of up .2% and .3% respectively but it was fully offset by the upward revisions to April. April headline was revised up by 3 tenths to -.2% while the core rate was revised up by 2 tenths to also down .2% m/o/m. The y/o/y gain of 2.6% and 3% for both headline and core compare with 2.5% and 3.2% in the month before. Food prices were up by 1 tenth m/o/m and 3.5% y/o/y. Energy prices were flat vs April but down 4.4% y/o/y. Core goods prices rose .2% m/o/m and have been rising consistently by 2 or 3 tenths per month this year and are higher by 2.4% y/o/y. With services, prices rose by one tenth but still up 3.2% y/o/y.

4) The May NFIB Small Business Optimism index rebounded by 3 pts to 98.8 after four months of declines. Of note, taxes are now the number one small business problem at 18% and the last time this was the case was in December 2020. Labor quality is number two at 16% and inflation is 3rd at 14%. Also, "When asked to rate the overall health of their business, 14% reported excellent (up one point) , and 55% reported good (down one point) . Twenty-eight percent reported the health of their business was fair (up one point) and 4% reported poor (unchanged) ." The bottom line from Bill Dunkelberg, "Although optimism recovered slightly in May, uncertainty is still high among small business owners. While the economy will continue to stumble along until the major sources of uncertainty are resolved, owners reported more positive expectations on business conditions and sales growth."

5) The preliminary June UoM consumer confidence index jumped to 60.5 from 52.2 in May and April, 57 in March, 64.7 in February and 71.7 in January. Current Conditions rose to 63.7 from 58.9 while Expectations were up to 58.4 from 47.9. After going from 4.3% to 6.6% over the prior three months, one yr inflation expectations slipped back to 5.1%. The longer term 5-10 yr guess was 4.1% after peaking at 4.4% in April. Expectations for the jobs market bounced after the recent weakness. Expectations for business lifted too with the "perceived easing of pressures from tariffs." With the lift in confidence, spending intentions rose too for autos, homes, and major household items. Bottom line from the UoM, "Consumers appear to have settled somewhat from the shock of the extremely high tariffs announced in April and the policy volatility seen in the weeks that followed. However, consumers still perceive wide ranging downside risks to the economy. Their views of business conditions, personal finances, buying conditions for big ticket items, labor markets, and stock markets all remain well below six months ago in December 2024. Despite this month's notable improvement, consumers remain guarded and concerned about the trajectory of the economy."

6) The NY Fed's Consumer Expectations Survey saw a drop in inflation expectations for all three time horizons. Specifically looking out one year, they fell .4 to 3.2%. This was 3% in January and jumped to 3.6% by April. For perspective, this was at 2.5% as we entered 2020. The trade cool down also helped to lift expectations of the labor market. Spending growth expectations fell two tenths but remained in its 12 month range. Credit access rose but expectations for future credit availability weakened. Delinquency expectations did improve. Overall "Perceptions about households' current financial situations compared to a year ago and expectations about year ahead financial situations both improved slightly."

7) The Atlanta Fed said in May that wages were up 4.3% y/o/y for a 4th straight month. For 'job stayers', wages grew by 4.3% y/o/y, down slightly from the 4.4% growth seen in the prior three months. For 'job changers', wages were higher by 4.1% y/o/y vs 4.3% in the month before.

8) Even though mortgage rates held steady in the week ended 6/6 at 6.93%, purchase applications to buy a home jumped by 10.3% w/o/w after falling by 4.4% last week while refi's rebounded by 15.6% w/o/w.

9) From RH: "our industry leading growth continued into fiscal 2025 as revenue increased 12% in the first quarter despite the polarizing impact of tariff uncertainty and the worst housing market in almost 50 years…Every act of creation is first an act of destruction - Pablo Picasso. We have worked hard to destroy the former version of ourselves and are in the process of unleashing what we believe is an exponentially more inspiring and disruptive RH brand."

10) From Casey’s General Store: "We saw excellent results throughout the year in non-alcoholic beverages (they said particularly energy drinks) , as well as hot sandwiches...Our fuel team continues to grow market share, focusing on gross profit dollars while balancing fuel volume and margin." The view on their customers, "I would say the consumer is really hanging in there and continuing to visit our stores as frequently as they have historically. We're seeing good strength from the higher income consumers, those making over $100,000 a year…And even on the low end, we are seeing that traffic hanging in there. They are modifying some purchasing behavior. I think what's interesting that as we dug into this, there's two types of low income consumers. I think there's a cohort of consumers who perhaps have a family and they're really stretched to make ends meet. But we're also finding in that low income cohort, those are a lot of younger folks that are early on in their careers. And so they are lower income, but they don't behave like folks that are really stretched to make ends meet. And so think more Gen Z and younger millennials. And so the purchasing habits for those folks are very different than what you'd have for some other maybe more mature people in that income cohort."

11) From Academy Sports & Outdoors: "I think it is important to point out that as the situation has evolved, we've continued to see an increase in foot traffic from customer's household incomes over $100,000 annually. This is a pattern we have seen emerge over the past couple of quarters and it is starting to accelerate. We would expect this trend to continue as customers look to stretch their discretionary spending power by seeking out value."

12) From Chewy: Sales rose 8% and "was underpinned by strong participation from new and existing customers across a variety of Chewy's offerings and our favorable mix of core consumables and health and wellness categories. Also notable this quarter was the 12.3% y/o/y growth we delivered within hard goods."

13) From Oracle: "CapEx is going to go up because the demand right now seems almost insatiable. I mean, I don't know how to describe it. I've never seen anything remotely like this."

14) Microchip Technologies spoke at a Mizuho conference and they are seeing some inventory rebuilds. "May bookings was the highest that we've seen in many years. And so bookings has continued to improve, book-to-bill continued to improve as well."

15) Taiwan's exports in May jumped by 39% y/o/y, well more than the estimate of 23% in another front running attempt. Exports to the US skyrocketed by 87% y/o/y.

Negatives,

1) In the PPI report, inflation in the pipeline was apparent as core prices for processed goods were up by .4% m/o/m after a .5% gain in April and .7% rise in March.

2) Initial jobless claims remained elevated, relative to trend, again at 248k, 6k more than expected and the same pace seen last week. The 4 week average is now 240k vs 235k last week and that is the highest since August 2023. Of importance too was the new cycle high in continuing claims which now total 1.956mm, up about 50k w/o/w.

3) According to Cass Freight, shipments fell 3.4% m/o/m in May and were down 4% y/o/y. They said, "The trade war is having a variety of effects, with pre-tariff consumer spending still supporting freight demand. The negative consequences of tariff effects are partly reflected in May data, as pre-tariff inventory stocking has started to turn to destocking, and those stocks will start to thin in the coming months." On their outlook, "Visibility remains low and highly dependent on policy developments and legal challenges. The uncertainty has lowered the economic outlook, and pre-tariff inventory building will lead to destocking regardless of the outcome of trade negotiations in the coming months."

4) Container prices for a 6th straight week were higher and have more than doubled over this time frame but the pace slowed. The Shanghai to LA route saw the price of a 40 foot container up by $38, or by .7%, w/o/w to $5,914. The trip to NY rose $121 w/o/w or 1.7% to $7,285 vs $3,500 on May 1st.

5) From Oxford Industries: "Tariff policy is challenging us in several ways. First, consumer concern about the impact of tariffs on prices and the economy is exacerbating weak consumer sentiment. Second, the rapid evolution of the tariff policy is making it exceptionally difficult to plan and forecast the business. And finally, the tariff policy is requiring us to significantly realign our supply chain, which could prove to be the catalyst for implementing some changes in our sourcing strategies that ultimately benefit our company and shareholders, but certainly present short term challenges and financial ramifications."

6) Norfolk Southern spoke at a Wells Fargo conference yesterday and said "so first two months of the quarter in the bag, how do we think June is progressing here? And we are starting to see a little bit of softness, more than what we expected, probably...It's something that we're definitely monitoring. But we'll definitely stay close to our customers on this and make sure we're looking at any leading indicators that point to any further degradation."

7) Union Pacific said at the same conference, "Industrial, a little bit of a mixed bag, but still seeing strong performance on the industrial chems and plastics. If you looked in at the premium line, that's kind of a tale of two pieces. You've got automotive, which is down q/o/q, down about 6%. You have intermodal, which is still up, but certainly you saw in our intermodal volumes this week, in total down 7%. We're hitting that air pocket that people have been looking for."

8) From Winnebago: "What began as an encouraging selling season in March was hampered by growing macroeconomic uncertainty, resulting in worsening consumer sentiment and an increasingly cautious dealer network in the final two months of our fiscal third quarter."

9) UK GDP in April contracted by .3% m/o/m, more than the estimate of down .1%, with weakness in both services and manufacturing. The area of strength was in construction.

10) In the UK, payrolls fell by 109k, well more than the estimate of down 20k and after a drop of 55k in April, revised lower by 22k. Jobless claims rose too. Wage growth in the 3 months ended April was higher by 5.2%, still solid and well above the rate of inflation but less than forecasted. Their unemployment rate as of April rose to 4.6%, the most in 4 years. The ONS said, "There continues to be weakening in the labor market, with the number of people on payroll falling notably. Feedback from our vacancies survey suggests some firms may be holding back from recruiting new workers or replacing people when they move on."

11) China's exports rose 4.8% y/o/y, just below the estimate of up 6% but trade with the US fell by 9.7% y/o/y, offset by a 15% rise in exports to India, a 12% increase to ASEAN countries and other parts of Asia. Exports to the EU were higher by 6.4% and by 7.4% to the UK.

BY Doug Kass · Jun 13, 2025, 2:45 PM EDT

* Which is surprising to this observer with all that is going on in the world and how high valuations are...

BY Doug Kass · Jun 13, 2025, 2:29 PM EDT

From Peter Boockvar:

The preliminary June UoM consumer confidence index rebounded to 60.5 from 52.2 in May and April, 57 in March, 64.7 in February and 71.7 in January. While political divergences are all over the data, it's obviously ebbed and flowed with the tariff news. The UoM said on this, "Expectations about the anticipated effects of tariffs have shaped consumers' views of the economy this year, and this month's results are no different."

Current Conditions rose to 63.7 from 58.9 while Expectations were up to 58.4 from 47.9. After going from 4.3% to 6.6% over the prior three months, one yr inflation expectations slipped back to 5.1%. The longer term 5-10 yr guess was 4.1% after peaking at 4.4% in April.

Expectations for the jobs market bounced after the recent weakness. Those that see more unemployment in the coming year fell 6 pts to 58 after going from 51 to 64 in the prior three months. Income expectations rose but remained negative and is just back to where it stood in April and March at -2.

Expectations for business lifted too with the "perceived easing of pressures from tariffs."

With the lift in confidence, spending intentions rose too for autos, homes and major household items.

Bottom line from the UoM, "Consumers appear to have settled somewhat from the shock of the extremely high tariffs announced in April and the policy volatility seen in the weeks that followed. However, consumers still perceive wide ranging downside risks to the economy. Their views of business conditions, personal finances, buying conditions for big ticket items, labor markets, and stock markets all remain well below six months ago in December 2024. Despite this month's notable improvement, consumers remain guarded and concerned about the trajectory of the economy."

More, "Prices and cost of living remain the top factor for consumers. At this time, they are still bracing for a resurgence of inflation."

And finally, "In special questions fielded in May and June, only about 21% of consumers reported that they expect to continue spending as usual on items with high price increases. In contrast, in August through October 2022, about 36% expected to hold such spending steady in the post pandemic inflationary period. These results suggest that the resilience of consumer spending now will likely hinge on inflation remaining stable." I'll add this, the labor market too.

BY Doug Kass · Jun 13, 2025, 2:21 PM EDT

BY Doug Kass · Jun 13, 2025, 2:11 PM EDT

Scott Galloway's No Mercy No Malice: "Stream On"

BY Doug Kass · Jun 13, 2025, 2:02 PM EDT

Back in the office.

Getting my sealegs back!

BY Doug Kass · Jun 13, 2025, 1:58 PM EDT

As of 1 p.m.:

BY Doug Kass · Jun 13, 2025, 1:14 PM EDT

I'm re-shorting the indices with cash -23 handles.

BY Doug Kass · Jun 13, 2025, 11:57 AM EDT

No trades since last report.

Back in hour.

BY Doug Kass · Jun 13, 2025, 11:50 AM EDT

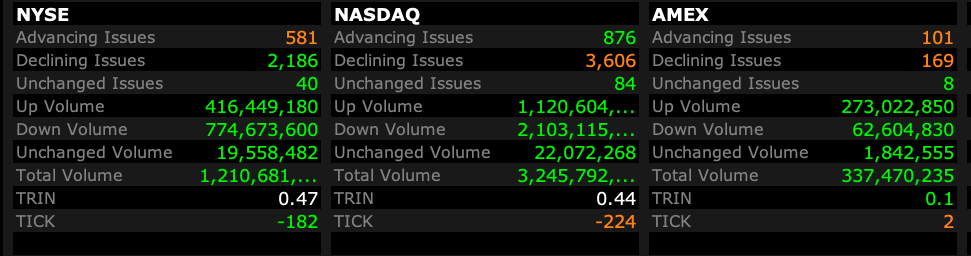

- NYSE volume 17% is above its one-month average;

- Nasdaq volume 11% is below its one-month average;

- VIX index: up 15.09% to 20.74

BY Doug Kass · Jun 13, 2025, 11:00 AM EDT

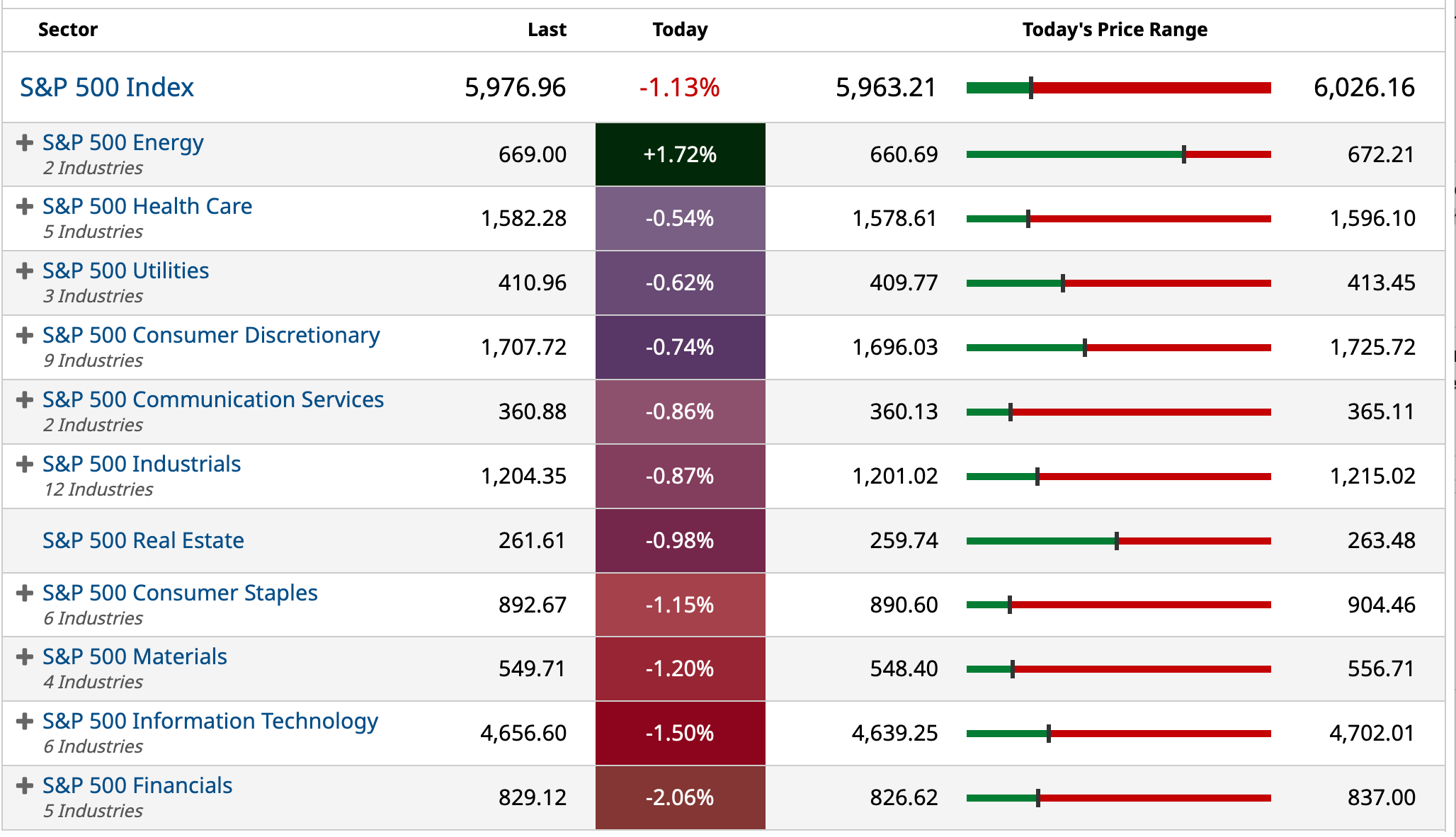

* Yesterday's domestic and international developments underscore the many possible adverse market outcomes...

* As equities fall and the price of crude oil rises (+9%)

* The 'Long Boom Curse' may apply today!

“The obscure we see eventually. The completely obvious, it seems, takes longer.”

- Edward R. Murrow

Following a remarkable climb in equities since early April, it is being argued by a growing body of market participants that a new bull market leg has emerged, coincident with a virtuous economic and corporate profit cycle that may lie ahead: "Carson Group: Welcome to the Start of a New Bull Market?"

It should be emphasized that many of the newly minted bulls were actually scared shitless during the first week of April. They are the most optimistic today -- reminding us of The Divine Ms. M's (Helene Meisler) quote:"There is nothing like price to change sentiment."

I strenuously disagree with the newly minted market optimism. In fact, it is my view that not since Wired Magazine's ill-timed late 1990s cover story "The Long Boom: A History of the Future, 1980-2020" ( authored by Peter Schwartz and Peter Leyden) has a new investing paradigm been forecast:

“We’re facing 25 years of prosperity, freedom, and a better environment for the whole world. You got a problem with that?”

Of course that remarkably upbeat (but wrong footed) column was followed quickly followed by a -80% drawdown in the Nasdaq Index! To me, the "Long Boom Curse" probably also applies today!

In yesterday's market update (Downside Market Risk Is About 5-Times Upside Reward) I make the opposite case -- that there is no new investing paradigm ahead as we could not only face seven lean months over the balance of 2025 but, perhaps, another 6.5 lean years after that.

To summarize some of my concerns:

* We face the highest geopolitical risks in many decades (which will not be resolved quickly).

* We face the largest level of social and political risks in the U.S. since the Vietnam war.

* We face the greatest chance of "slugflation" (slowing economic growth and sticky inflation) since the 1970s.

* We face the biggest threat that the U.S. dollar and capital markets will no longer be a "safe haven" in modern history.

See: NDR: Breakdown for U.S. dollar?

* We face the greatest debt load and deficit ever -- and neither party seems to favor any fiscal discipline whatsover.

* We face the largest capital spending spree in history (on artificial intelligence) -- though the return on that investment is less certain (dot.com, it feels like deja vu all over again.)

* We face a viable alternative to equities in fixed income (for the first time in 15 years) as bonds present an equity-equivalent yield with limited risk and volatility.

As I have also noted, what is most surprising is that market enthusiasm has multiplied at a point of time in which price-earnings multiples are at an elevated 22-times. Here are some snippets from my Thursday column, which support my more ursine view, which is backed by rising, not declining uncertainties:

My commentary today is decidedly downbeat – some might even say dystopian. But I think my concerns are largely justified. Importantly, with markets trading at a 22-times forward price earnings multiple there is little room for disappointment.Indeed, it is my view that adverse outcomes are likely to become more common place in the time ahead – witness the recent juvenile and angry Elon Musk/Pres. Trump exchanges. Never in my investing career has there been so many possible social, political, geopolitical, economic, interest rate and fiscal policy outcomes. Many of these possible outcomes could easily upset overvalued markets. Based on my calculus and scenario analysis, the market’s downside risk is roughly 5-times the market’s upside reward -- this is the worst ratio since late 2021...

Unfortunately, Americans continue to be exposed to unvarnished political self-interest, the continued loss of conventions and general lack of ethics and morals. (As an example is the insider trading of our Congressional members, right in front of our eyes). It is increasingly obvious that political positions of influence can easily be bought — sold by both Democrats and Republicans. To this observer, fewer and fewer politicians are even pretending that they care about the American people. This may help to explain the capital outflows out of the U.S. and that many (including ourselves) are "Rethinking American Exceptionalism." (Consider what the world outside of the U.S. thinks of us these days).

As dark as all this is, my concerns relate to both parties. The Republican party has its own set of issues while Democratic leadership doesn't even seem to exist — making the situation rather sickening. This concerning condition has real economic and investment consequences, most importantly as reflected in the continuing lack of fiscal discipline and unwillingness to address our country's debt load. I express this reality and these conditions not as political statements, but rather as economic and investing considerations. It is highly unlikely that any politician on either side of the pew will address our progressively and steadily deteriorating financial position. At this point, if they did recommend some hard decisions, they would likely be voted out of office. There are simply too many forces inside the government opposed to cutting spending to produce meaningful results -- just look at the resistance to DOGE.

Whether the "big, beautiful bill" increases or decreases the deficit by a few trillion dollars has now lost its relevance. We have already lost the ability to control the deficit -- as the total federal debt load is now projected to be nearly $50 trillion in 2030 and over $70 trillion by 2040. The harsh truth is that it is getting almost too late to dent the deficit (and the arc toward an erosion in U.S. solvency) without radical changes in non-discretionary spending and/or taxation requiring austerity and large tax increases (which would trigger a severe recession). As a consequence of the above factors (and other influences) interest rates will stay higher for much longer -- an unfriendly condition for future price earnings ratios (as interest rates are at the core of all equity valuation models). Additionally, higher interest rates (and deficit neglect by our representatives in Washington, D.C.) will result in sharply rising costs of servicing our burgeoning debt load.

* Political and geopolitical polarization and competition will probably translate into less political centrism and a reduced concern for deficits — creating structural uncertainties, limited fiscal discipline and imprudence around the globe ... and for the possibility of bond markets to "disanchor."

* The cracks in the foundation of the bull market are multiple and are deepening, but they are being ignored (as market structure changes have led to price momentum (FOMO) being favored over value and common sense).

* With the S&P 500 Index at around 6000, the downside risk dwarfs the upside reward for equities — in a ratio of about 5-1 (negative).

* Valuations (a 22-times forward Price Earnings Ratio) and (consensus) expectations for economic and corporate profit growth are all inflated.

* Being dismissed are JPMorgan CEO Jamie Dimon's and others’ dour comments on complacency and a view that the corporate credit market is "ridiculously over-stretched.”

* Look for the soft data (see last week's weak ISM and climb in jobless claims) to move into (and weaken) the hard data led by a slowing housing market likely to provide ample near-term evidence of the exposure and vulnerability of the middle class.

* Below trend-line economic growth (housing will lead us lower) coupled with sticky inflation lie ahead ("slugflation") — uncomfortable for a Federal Reserve which has to make increasingly more difficult decisions.

* Corporate profit growth (rising +13% in first quarter 2025) will markedly decelerate in this year’s second half.

* The equity risk premium is at a two-decade low - typically consistent with a slide in equities.

* The S&P Dividend Yield is at a near record low of 1.27% - and the spread between the dividend yield and the 10-year U.S. Treasury note yield has rarely been as wide. With so many possible adverse outcomes, my baseline expectation is for seven lean months ahead over the balance of 2025:

"In the Bible, 'lean years' refer to a period of famine that follows a time of abundance, particularly in the story of Joseph in Genesis 41. The prophecy, revealed through dreams to Pharaoh, foretold seven years of great plenty in Egypt, followed by seven years of severe famine. Joseph, interpreting the dream, advised Pharaoh to prepare for the lean years by storing grain during the period of abundance. This preparation allowed Egypt to survive the famine while other surrounding lands suffered greatly."

BY Doug Kass · Jun 13, 2025, 9:30 AM EDT

Charts from 8:49 a.m. ET:

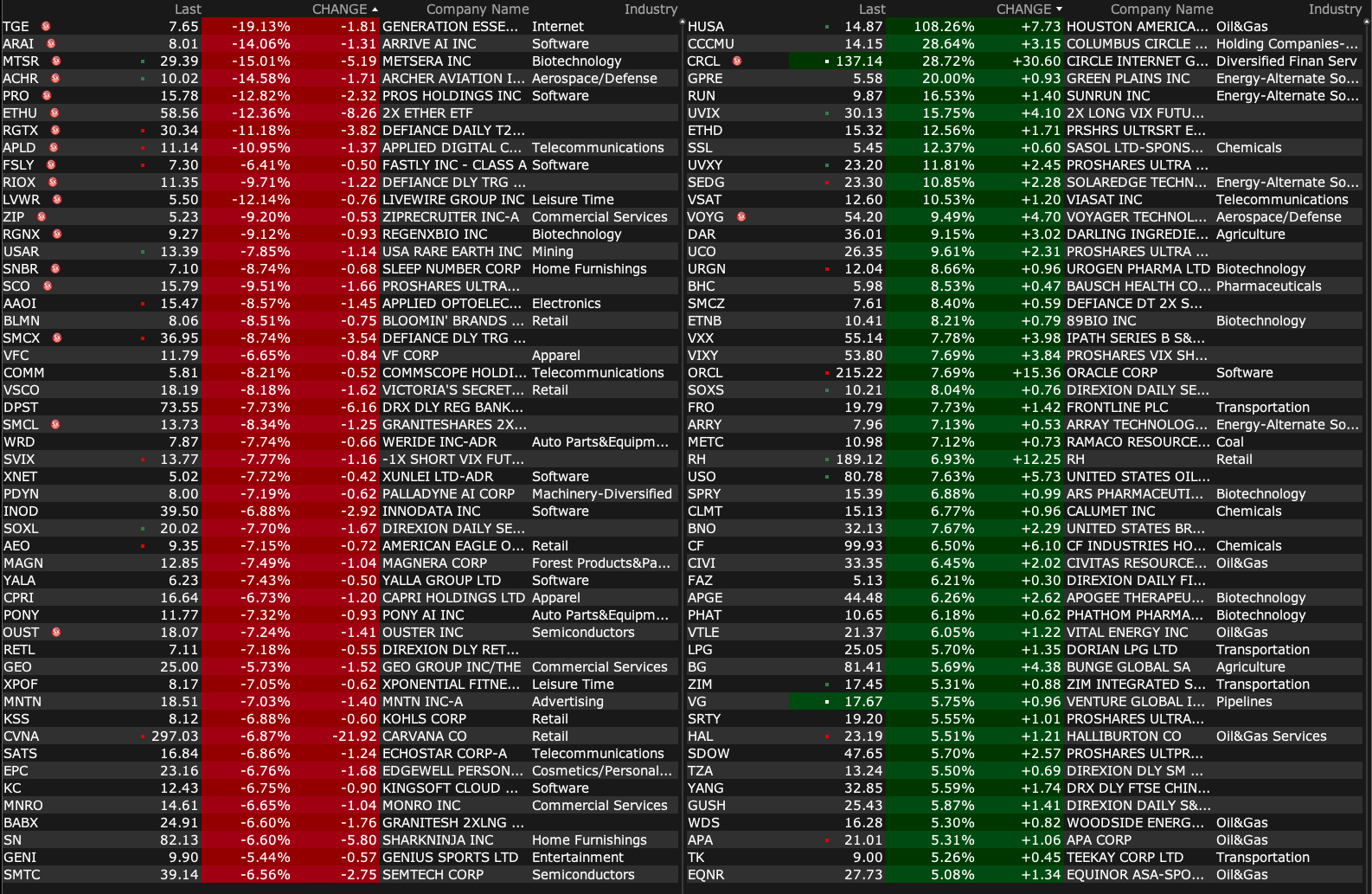

BY Doug Kass · Jun 13, 2025, 9:22 AM EDT

-RH +19% (earnings, guidance)

-ZKH +6.5% (announces $50M new share repurchase program (~10% of market cap))

-NMM +3.8% (shippers higher amid Middle East tensions)

-RTX +3.8% (defense higher amid Middle East tensions)

-XOM +2.9% (oil prices rise amid Middle East tensions)

-LMT +2.8% (defense higher amid Middle East tensions)

-CRCL +2.3% (momentum)

-ACHR -15% (files to sell $850M in Class A common stock)

-OKLO -6.8% (prices 6.67M shares at $60/shr)

-CCL -5.1% (leisure, travel stocks lower amid Middle East tensions)

-DAL -4.9% (leisure, travel stocks lower amid Middle East tensions)

-X -4.1% (reportedly Nippon Steel deal may stall if Japan side is not given "freedom of management")

-ADBE -3.7% (earnings, guidance)

-SNPS -3.1% (China said to delay approval of $35B chip-merger with Ansys)

-ELVN -2.6% (files to sell $200M in stock and pre-funded warrants following updated data from Phase 1 Clinical Trial of ELVN-001 in CMLat EHA 2025 Congress)

-V -2.4% (AMZN, WMT consider issuing own stablecoins in the US)

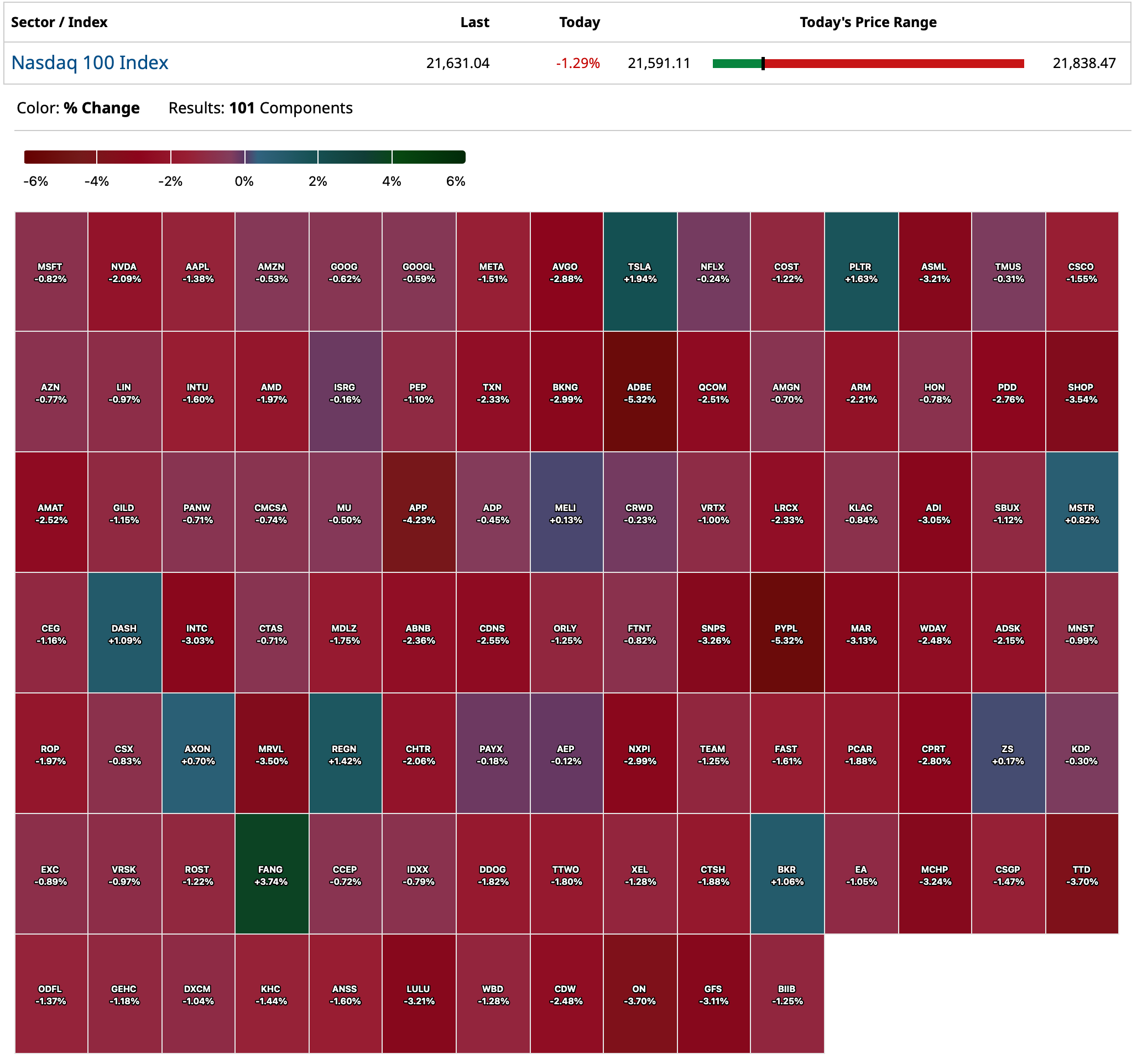

BY Doug Kass · Jun 13, 2025, 9:13 AM EDT

Chart from 8:19 a.m. ET:

BY Doug Kass · Jun 13, 2025, 8:29 AM EDT

* As is typical over history, sentiment recovers at the top.

Bonus — Here are some great links:

BY Doug Kass · Jun 13, 2025, 6:20 AM EDT

I am still on the road visiting companies.

I will be back at around noon so my posts will be brief and less freqent.

BY Doug Kass · Jun 13, 2025, 6:10 AM EDT

The S&P Short Range Oscillator remains overbought at 3.72% vs. 4.20%.

As noted earlier, I have no index positions on currently.

BY Doug Kass · Jun 13, 2025, 5:58 AM EDT

From the Comments Section:

Dougie Kass

I have covered my SPY and QQQ shorts and I have purchased SPY against my short SPY calls.

I am now delta equivalent neutral in the Indices.

BY Doug Kass · Jun 13, 2025, 5:48 AM EDT