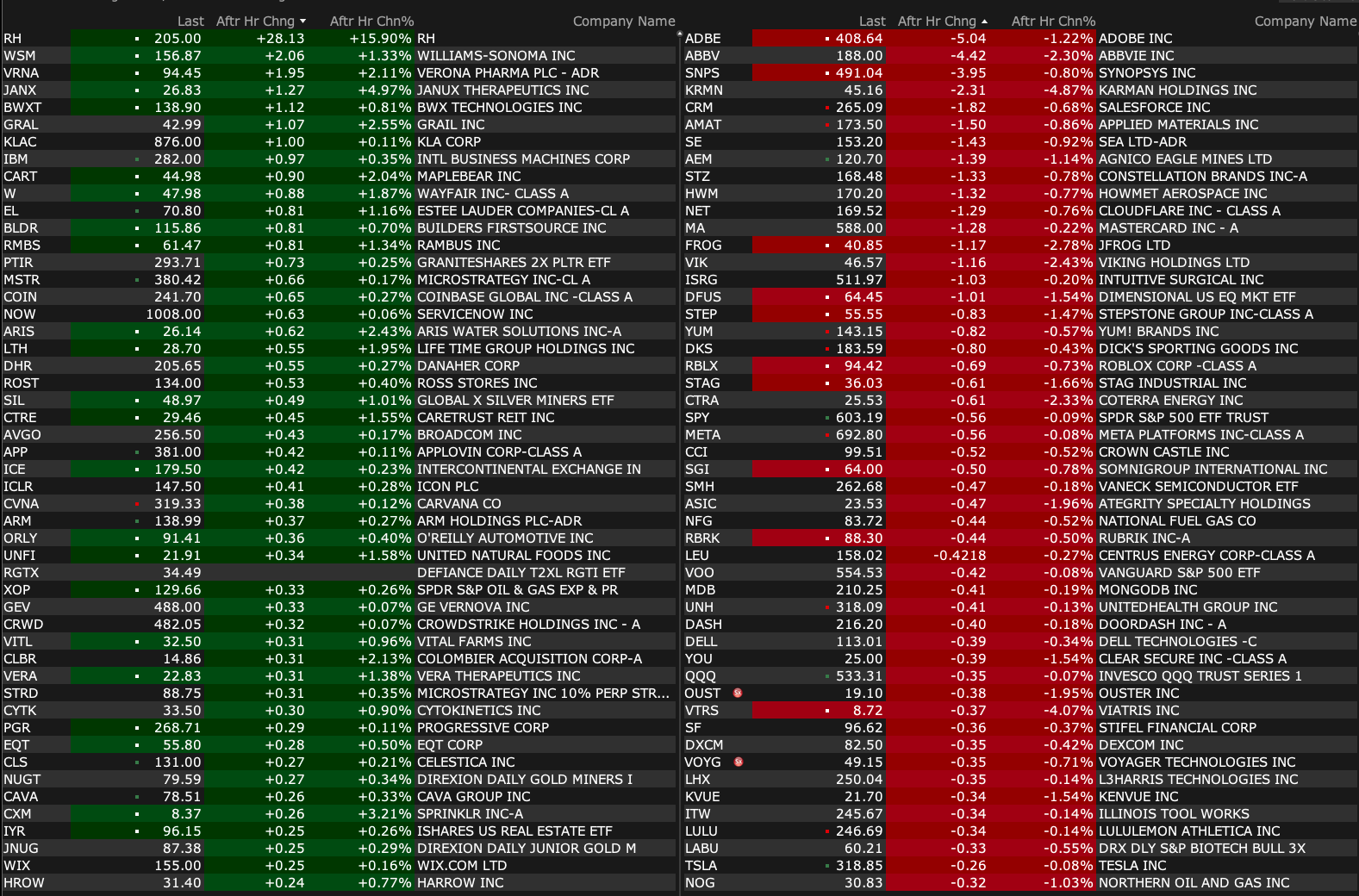

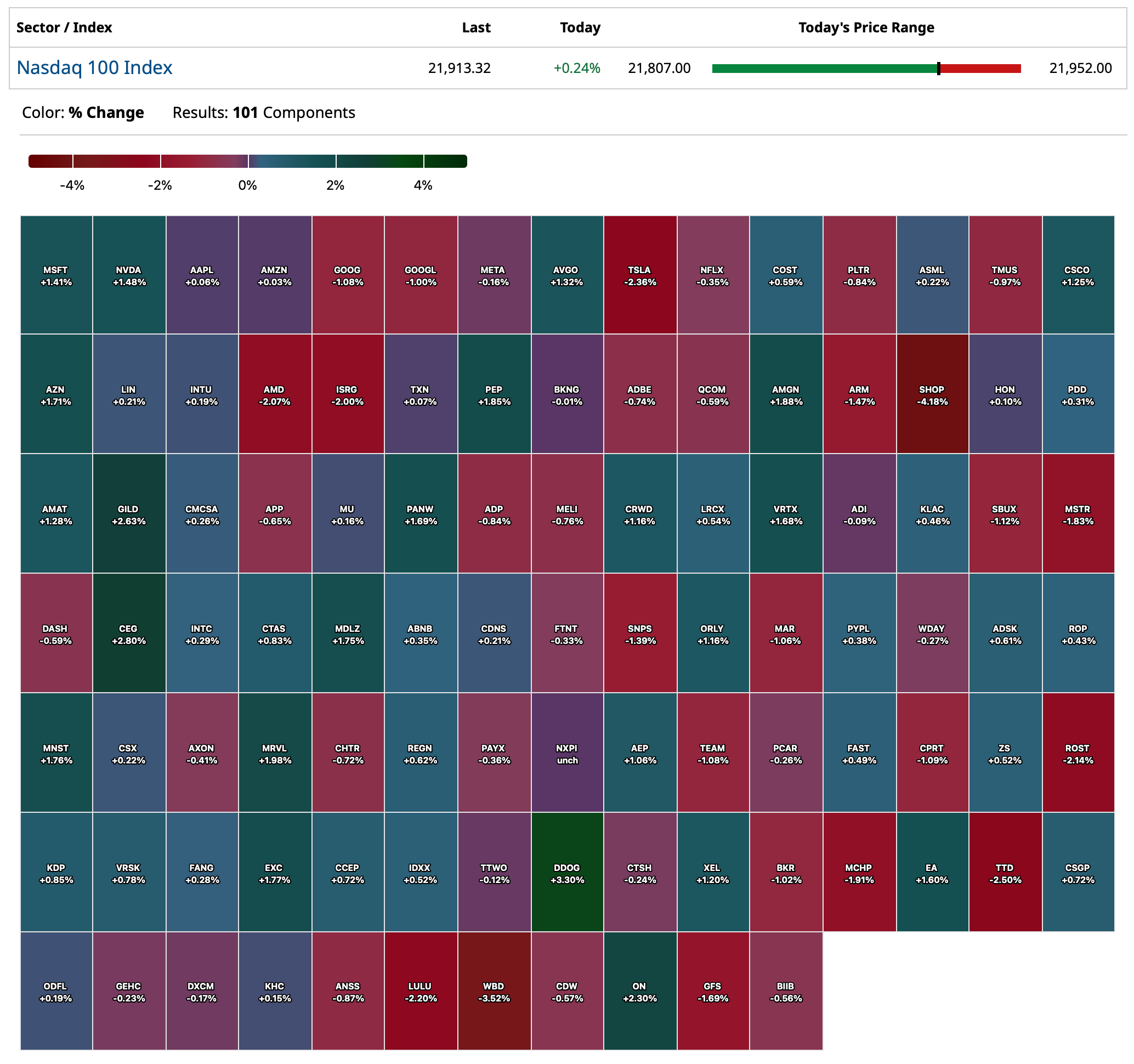

Thursday's After-Hours Movers

As of 4:21 p.m.:

BY Doug Kass · Jun 12, 2025, 5:20 PM EDT

As of 4:21 p.m.:

BY Doug Kass · Jun 12, 2025, 5:20 PM EDT

BY Doug Kass · Jun 12, 2025, 5:12 PM EDT

- NYSE volume 6% below its one-month average;

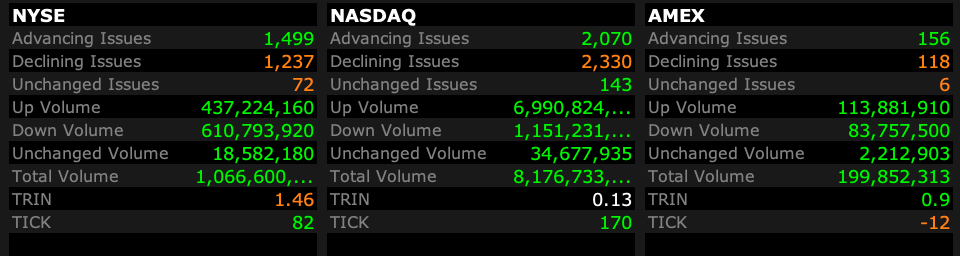

- NASDAQ volume 82% above its one-month average;

- VIX index: up 4.23% to 17.99

BY Doug Kass · Jun 12, 2025, 5:03 PM EDT

No trades since my last post!

BY Doug Kass · Jun 12, 2025, 3:24 PM EDT

I will be out of the office at research meetings most of this afternoon and tomorrow morning.

My posts will be less frequent and shorter.

BY Doug Kass · Jun 12, 2025, 2:00 PM EDT

For over one year talking heads on financial television have expected a rebound in investment banking.

As recently as yesterday, the shows emphasized that thesis.

Ain't happening (from randorama):

Randy

50 Minutes ago

Bank of America (BAC) expects Q2 investment banking fees to decrease roughly 25%, Bloomberg News reported, citing Chief Executive Brian Moynihan.

BY Doug Kass · Jun 12, 2025, 1:00 PM EDT

"Well, you could have been anything that you wanted to

And I can tell, the way you do the things you do

The way you do the things you do (Ah baby)

The way you do the things you do (Yeah)"- The Temptations, The Way You Do The Things You Do {PBS Version} The Way You Do The Things You Do - The Temptations | Live on It's What's Happening - YouTube

Pete

11 minutes ago

Doug, Enjoyed reading the life without music column. Would love to know how many hours a day you actually work. Between research writing columns and trading you must sleep only a couple hours a night. You have more energy than I can imagine. Thanks for all you do !!!!

Dougie Kass

STAFF

3 minutes ago

i start work at about 4 am. (I have about four cups of coffee/day)

i end work about 6 pm

i spend about 2 hours of the 14 hours/day writing in my Diary - the rest is analyzing and speaking to companies as part of the process of managing Seabreeze (i also am president of my country club so that takes a small amount of time)

i eat lunch at my desk

asleep by 930PM at the latest (usually)

on weekends i sleep about 9 hours a night.

i have a lot of energy and a good work ethic - i am stimulated by the investment business and work as hard as any 25 year old

the only drugs i take are ozempic and lipitor!

BY Doug Kass · Jun 12, 2025, 12:00 PM EDT

- NYSE volume 6% below its one-month average;

- Nasdaq volume 135% above its one-month average;

- VIX index: up 1.27% to 17.48

BY Doug Kass · Jun 12, 2025, 11:45 AM EDT

* It is my view that equities been so unattractive since late 2021.

What follows is a compilation of my recent columns in my Diary as well as my commentary to my hedge fund (Seabreeze Partners) investors:

“The obscure we see eventually. The completely obvious, it seems, takes longer.”

- Edward R. Murrow

My commentary today is decidedly downbeat – some might even say dystopian. But I think my concerns are largely justified. Importantly, with markets trading at a 22-times forward price earnings multiple there is little room for disappointment.

Indeed, it is my view that adverse outcomes are likely to become more common place in the time ahead – witness the recent juvenile and angry Elon Musk/Pres. Trump exchanges. Never in my investing career has there been so many possible social, political, geopolitical, economic, interest rate and fiscal policy outcomes. Many of these possible outcomes could easily upset overvalued markets. Based on my calculus and scenario analysis, the market’s downside risk is roughly 5-times the market’s upside reward -- this is the worst ratio since late 2021.

Unfortunately, Americans continue to be exposed to unvarnished political self-interest, the continued loss of conventions and general lack of ethics and morals. (As an example is the insider trading of our Congressional members, right in front of our eyes). It is increasingly obvious that political positions of influence can easily be bought — sold by both Democrats and Republicans. To this observer, fewer and fewer politicians are even pretending that they care about the American people. This may help to explain the capital outflows out of the U.S. and that many (including ourselves) are "Rethinking American Exceptionalism." (Consider what the world outside of the U.S. thinks of us these days).

As dark as all this is, my concerns relate to both parties. The Republican party has its own set of issues while Democratic leadership doesn't even seem to exist — making the situation rather sickening. This concerning condition has real economic and investment consequences, most importantly as reflected in the continuing lack of fiscal discipline and unwillingness to address our country's debt load. I express this reality and these conditions not as political statements, but rather as economic and investing considerations. It is highly unlikely that any politician on either side of the pew will address our progressively and steadily deteriorating financial position. At this point, if they did recommend some hard decisions, they would likely be voted out of office. There are simply too many forces inside the government opposed to cutting spending to produce meaningful results -- just look at the resistance to DOGE.

Whether the "big, beautiful bill" increases or decreases the deficit by a few trillion dollars has now lost its relevance. We have already lost the ability to control the deficit -- as the total federal debt load is now projected to be nearly $50 trillion in 2030 and over $70 trillion by 2040. The harsh truth is that it is getting almost too late to dent the deficit (and the arc toward an erosion in U.S. solvency) without radical changes in non-discretionary spending and/or taxation requiring austerity and large tax increases (which would trigger a severe recession). As a consequence of the above factors (and other influences) interest rates will stay higher for much longer -- an unfriendly condition for future price earnings ratios (as interest rates are at the core of all equity valuation models). Additionally, higher interest rates (and deficit neglect by our representatives in Washington, D.C.) will result in sharply rising costs of servicing our burgeoning debt load.

As noted on Wednesday, while investor rejoiced in response to the better inflation release, I by contrast grew more negative (and added to my short exposure):

If you read JPMorgan's CPI scenario analysis you will see that given the colder inflation print this morning, the brokerage expected more than a +2% positive reaction to the print (they and others were disappointed!) :

· [5.0% probability] Core MoM prints below 0.25%. SPX gains 2% - 2.5%. The other tail outcome, similar to recent results from EU/UK, this would be a material dovish print. Look for the bond market to add back at least 2x 25bp rate cuts and for Equities to react positively to the bull steepening that likely ensues.

The reasons I think they were wrong in anticipating a +2% or better rise yesterday in the S&P are because

1) the market has likely already discounted a better than expected Core CPI,

2) the China/US tariff meeting ended up being a complete non-event with no evidence of reducing tariffs,

3) Investor may interpret this number as being less exciting for equities because companies/manufacturers are likely eating the higher costs/ tariffs, leading to concerns about lower margins and profits over the balance of the year and,

4) based on the swings in the trade balance, importers stockpiled stuff ahead of Liberation Day - so they had product in inventory to sell without tariff penalties... When that inventory runs out, they will likely have to put through price hikes and inflation will heat up.

From my pal, Richard Bernstein:

To summarize my ursine market view:

* Political and geopolitical polarization and competition will probably translate into less political centrism and a reduced concern for deficits — creating structural uncertainties, limited fiscal discipline and imprudence around the globe ... and for the possibility of bond markets to "disanchor."

* The cracks in the foundation of the bull market are multiple and are deepening, but they are being ignored (as market structure changes have led to price momentum (FOMO) being favored over value and common sense).

* With the S&P 500 Index at around 6000, the downside risk dwarfs the upside reward for equities — in a ratio of about 5-1 (negative).

* Valuations (a 22-times forward Price Earnings Ratio) and (consensus) expectations for economic and corporate profit growth are all inflated.

* Being dismissed are JPMorgan CEO Jamie Dimon's and others’ dour comments on complacency and a view that the corporate credit market is "ridiculously over-stretched.”

* Look for the soft data (see last week's weak ISM and climb in jobless claims) to move into (and weaken) the hard data led by a slowing housing market likely to provide ample near-term evidence of the exposure and vulnerability of the middle class.

* Below trend-line economic growth (housing will lead us lower) coupled with sticky inflation lie ahead ("slugflation") — uncomfortable for a Federal Reserve which has to make increasingly more difficult decisions.

* Corporate profit growth (rising +13% in 1Q2025) will markedly decelerate in this year’s second half.

* The equity risk premium is at a two-decade low - typically consistent with a slide in equities.

* The S&P Dividend Yield is at a near record low of 1.27% - and the spread between the dividend yield and the 10-year U.S. Treasury note yield has rarely been as wide. With so many possible adverse outcomes, my baseline expectation is for seven lean months ahead over the balance of 2025:

"In the Bible, 'lean years' refer to a period of famine that follows a time of abundance, particularly in the story of Joseph in Genesis 41. The prophecy, revealed through dreams to Pharaoh, foretold seven years of great plenty in Egypt, followed by seven years of severe famine. Joseph, interpreting the dream, advised Pharaoh to prepare for the lean years by storing grain during the period of abundance. This preparation allowed Egypt to survive the famine while other surrounding lands suffered greatly."

I wanted to end this commentary with a thoughtful list of (bearish) present conditions and concerns, sent to me over the weekend by my dear friend David Rocker (a political independent who founded the successful hedge fund Rocker Partners) - it bears reading:

- The economy is clearly slowing and earnings estimates for the S&P 500 have been declining

- Price Earnings ratios are at a historically high range

- President Trump’s pre-election claims largely unfulfilled

- Conflict between Russia and Ukraine continues and efforts to solve it alienates our ally and favors Russia

- Mideast conflict continues with no end in sight

- No Iran solution and it refuses to stop enriching

- The Administration announces huge tariffs which threaten further inflation and worsen international relations

- The Administration's claims that negotiating with major trading partners will produce favorable pacts unfulfilled

- DOGE has been a failure - minor savings at great social cost which alienates many including many Republicans

- President Trump's personal support from swing voters that got him elected (women, Latinos, blacks) reversing

- The Big Beautiful Bill will worsen deficits and losing support

- Relentless attacks on law firms and the legal system

- Relentless attacks on major universities which are the envy of the world and key to many scientific advances

- Relentless efforts to force the FED to lower rates

- Firing of many regulators who could challenge President Trump's programs

- Vitriolic breakup with Musk, the President's chief financier

- Continued attempts to disregard legal rulings made against the Administration's program

- Worsening relationships with US's historical allies, weakening our influence:

* Resulting in worldwide loss of confidence in the United States

* The US credit rating is downgraded

* The US Dollar falls 8% worsening the purchasing power of Americans and making foreign investors wary about financing our deficit

* University attacks leading capable foreign students to consider studying elsewhere than in the US

* Tourism declining

David concludes by writing:

“Yet stocks are at a high level and the market reacts briefly and modestly to real negative setbacks but grows vigorously stronger to rumors to talks and future meetings. It seems that nothing can go wrong -- as traders and investors buy the dip”.

Until it doesn't. Earlier I quoted Yogi Berra - I wanted to close by quoting him again: "It's not over til it’s over."

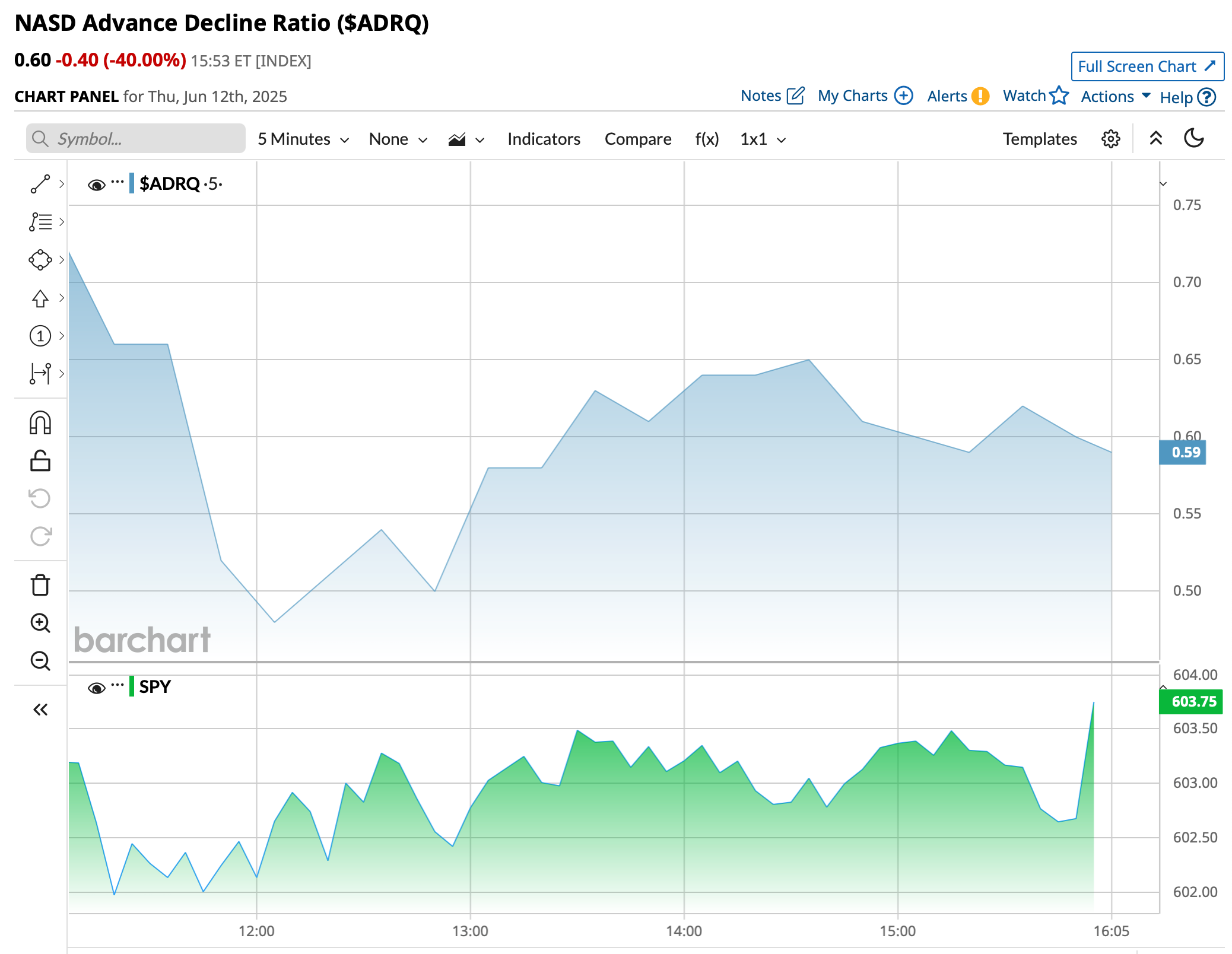

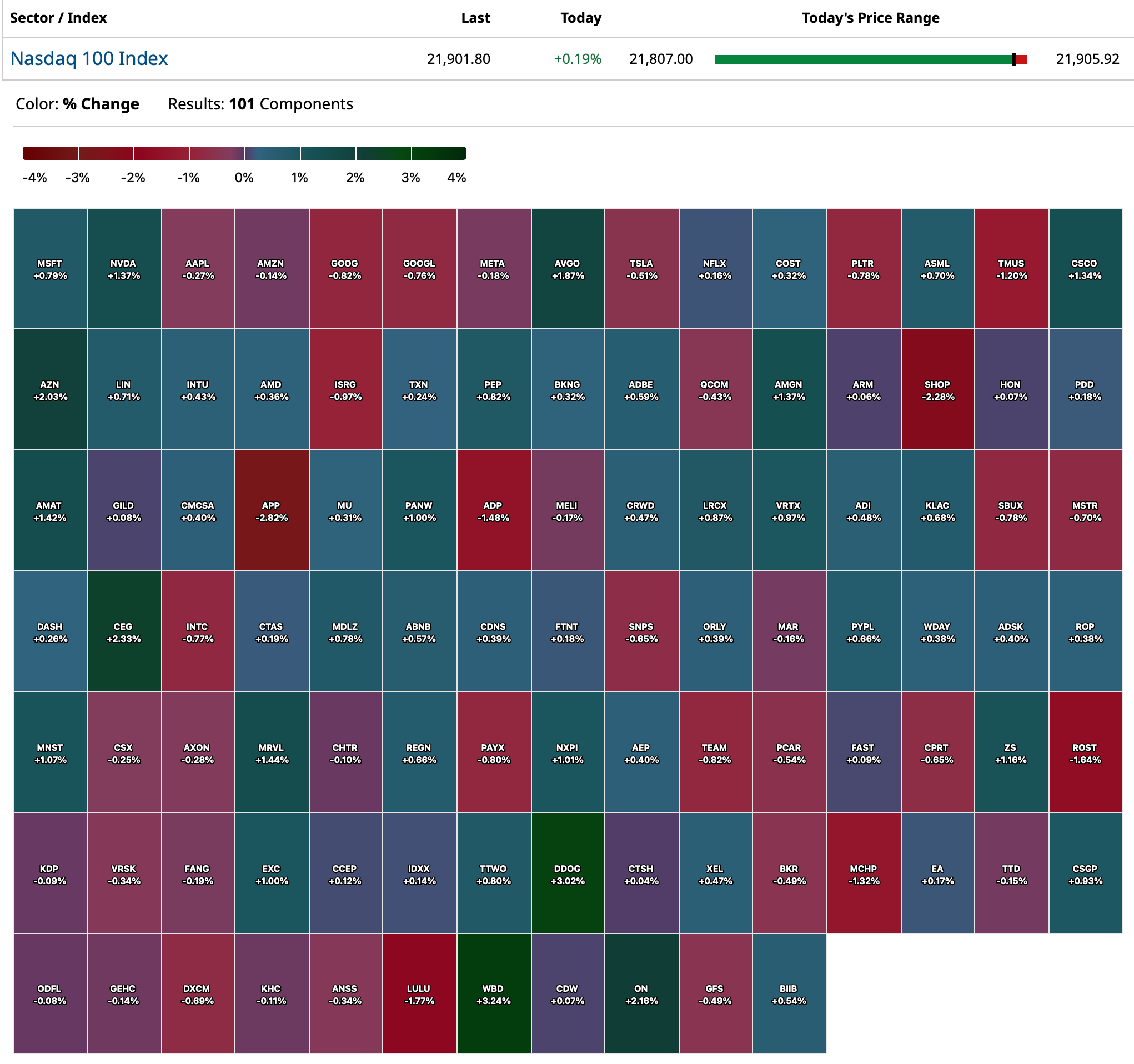

BY Doug Kass · Jun 12, 2025, 11:00 AM EDT

Chart from 9:45 a.m. ET:

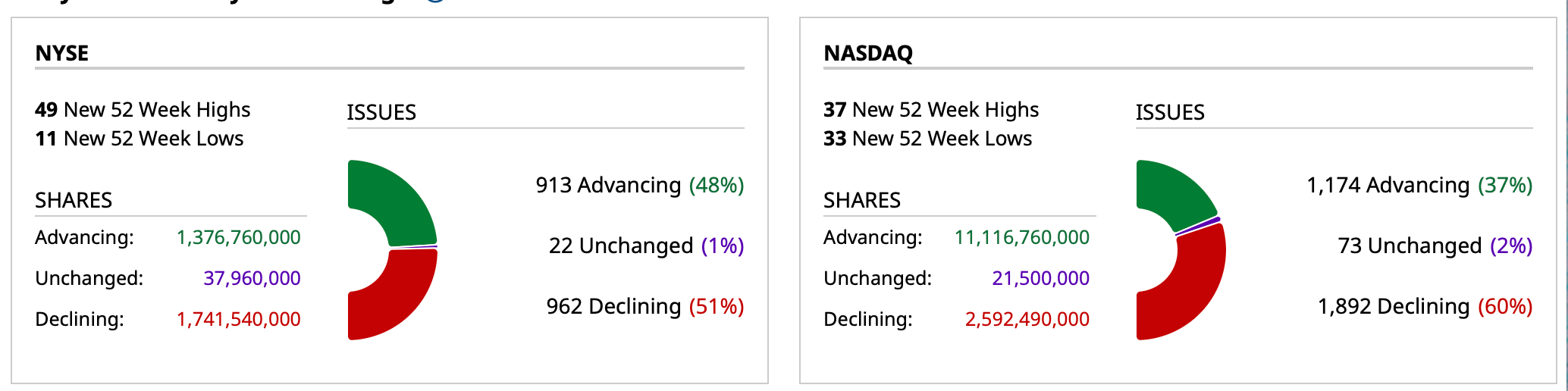

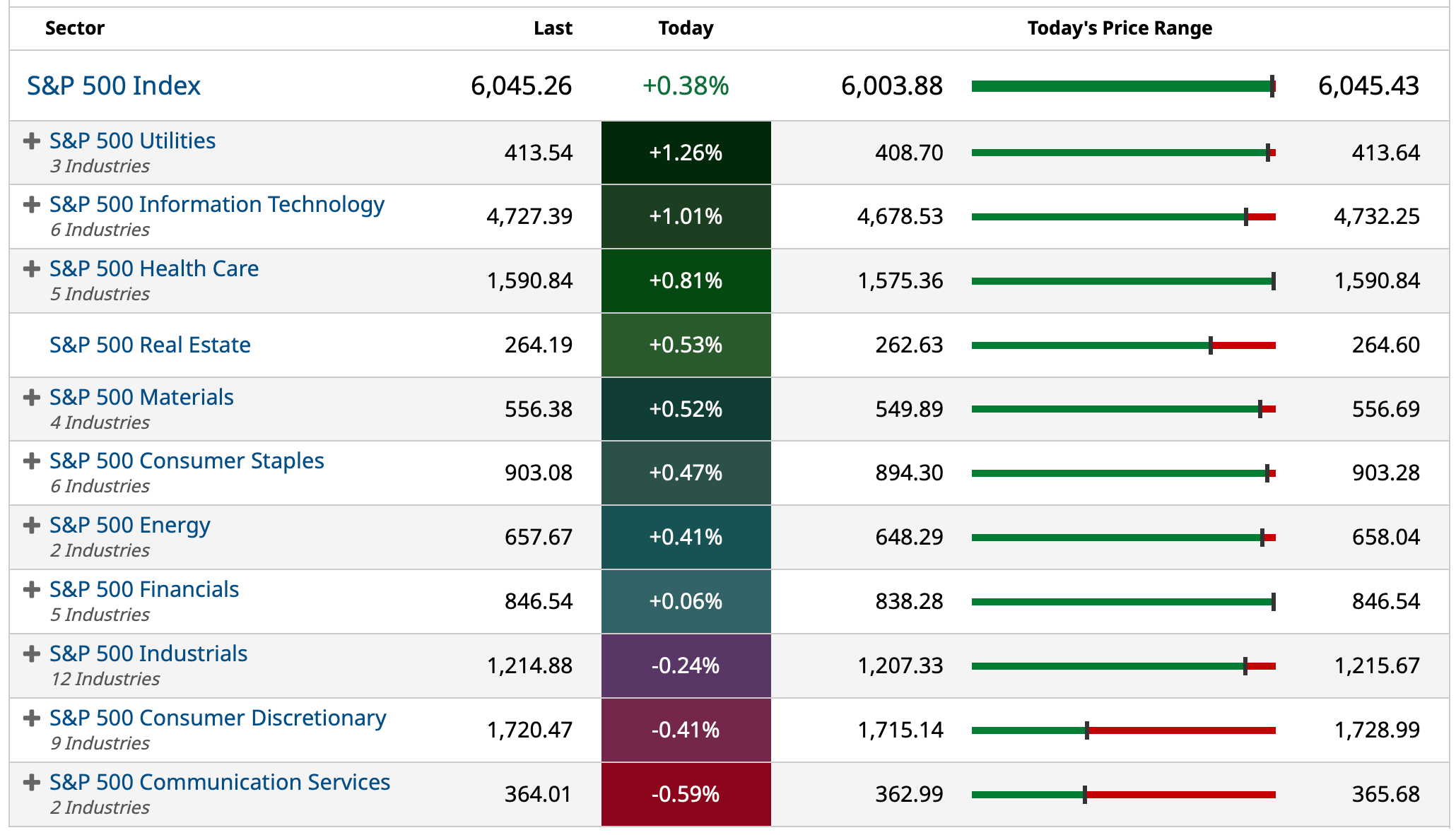

BY Doug Kass · Jun 12, 2025, 10:30 AM EDT

BY Doug Kass · Jun 12, 2025, 10:21 AM EDT

On the rally to even I have added to my index shorts:

* SPY $601.03

* QQQ $532.21

BY Doug Kass · Jun 12, 2025, 10:07 AM EDT

From Peter Boockvar:

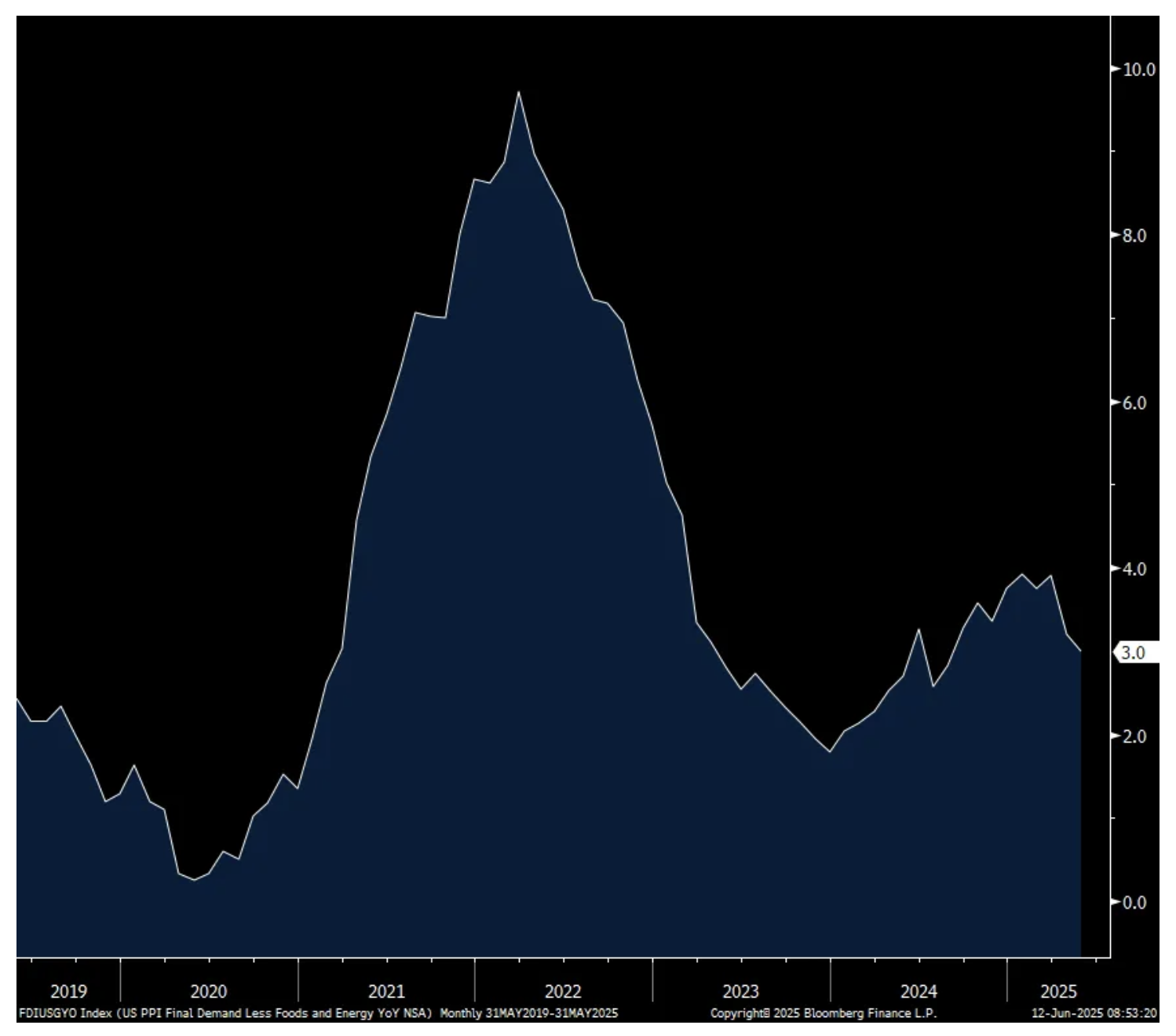

May PPI was higher by one tenth for both headline and core vs the estimate of up .2% and .3% respectively but it was fully offset by the upward revisions to April. April headline was revised up by 3 tenths to -.2% while the core rate was revised up by 2 tenths to also down .2% m/o/m. The y/o/y gain of 2.6% and 3% for both headline and core compare with 2.5% and 3.2% in the month before. Food prices were up by 1 tenth m/o/m and 3.5% y/o/y. Energy prices were flat vs April but down 4.4% y/o/y.

Core goods prices rose .2% m/o/m and have been rising consistently by 2 or 3 tenths per month this year and are higher by 2.4% y/o/y.

With services, prices rose by one tenth but still up 3.2% y/o/y. A big jump was seen in margins for ‘machinery and vehicle wholesaling’ by 2.9% after a drop in the previous month of .9%. Prices rose too for traveler accommodation, apparel/footwear retailing, alcohol retailing and system software publishing. On the downside, similar to what was seen in CPI, airline passenger service prices fell 1.1%. Prices were down too for furniture retailing and Wall Street related stuff like securities brokerage, investment advice, etc… and portfolio management.

Inflation in the pipeline was apparent as core prices for processed goods were up by .4% m/o/m after a .5% gain in April and .7% rise in March.

Bottom line, core goods prices at the wholesale level continue higher and likely means that consumer price goods prices are bottoming out BUT if they are not, margins are going to get squeezed. The wholesale stage of the supply chain are the front lines of the tariff situation and where it’s first absorbed and has begun to show up here. As for services, there is so much distortion going on with the delivery of goods being front loaded, stock piling at warehouses, etc… and retailer responses to the products they are procuring.

As CPI is really the market moving figure, today’s about in line data didn’t move the needle much but the consistent rise in core goods wholesale prices is something to keep in mind. Inflation breakevens are down about 1 bps across the curve after the greater move down yesterday.

Core PPI y/o/y

Initial jobless claims remained elevated, relative to trend, again at 248k, 6k more than expected and the same pace seen last week. The 4 week average is now 240k vs 235k last week and that is the highest since August 2023. Of importance too was the new cycle high in continuing claims which now total 1.956mm, up about 50k w/o/w.

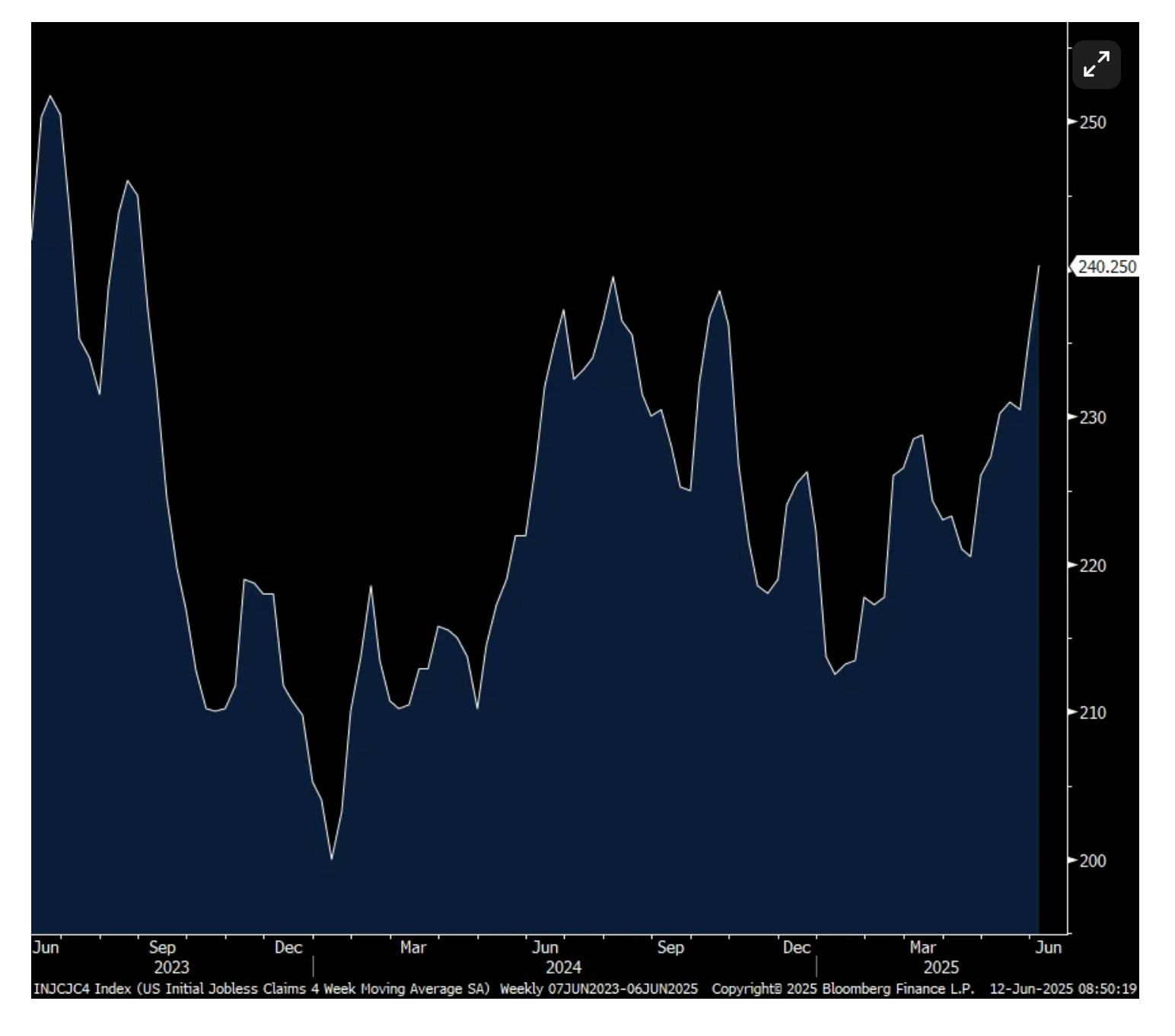

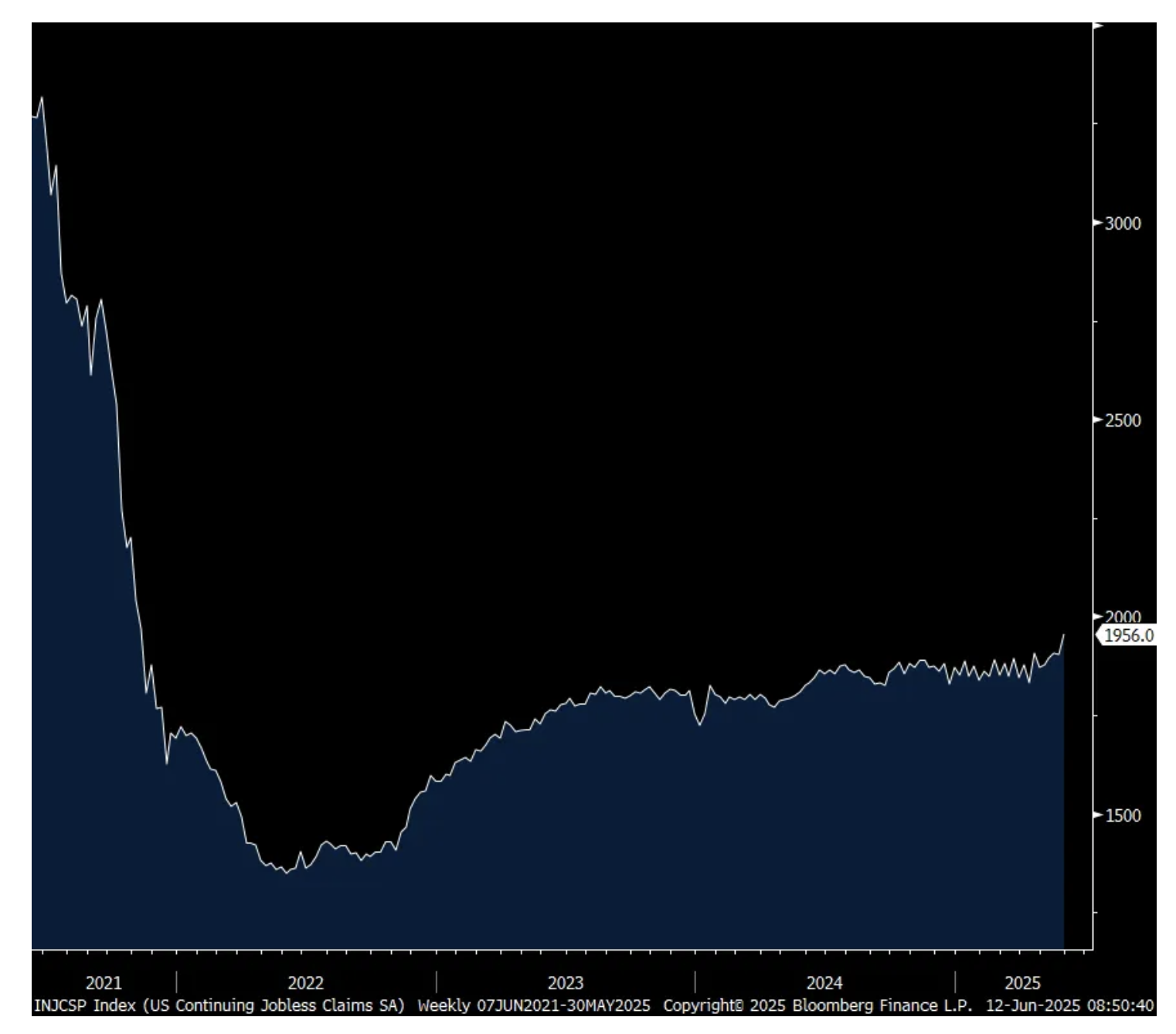

Bottom line, the continuing claims figure is further evidence of the slowing pace of hiring. The inflection higher now in initial claims is possibly an early sign of a pick up in the pace of firing’s. We’ve certainly seen small businesses shedding workers, as ADP said last week.

4 week avg Initial Claims

Continuing Claims

BY Doug Kass · Jun 12, 2025, 10:05 AM EDT

Seeing a vicious rotation out of financials this morning.

This should not be market friendly.

BY Doug Kass · Jun 12, 2025, 9:45 AM EDT

From JPMorgan (who got it wrong yesterday!):

Yesterday, Bulls got what they wanted out of CPI but the market failed to hold rallies as (i) US/China deal offered no incrementally positive news and that the rare earth export licenses will have a 6-month expiry means that we will have to replay these negotiations later this year and (ii) Energy prices spiked on US/Iran escalation ahead of today’s scheduled meetings; Iran threatened US military bases should discussions sour and then the US issued an order to clear non-essential staff from surrounding countries (RTRS).

So, is that it for this portion of the Equity rally? No. We maintain the tactically bullish hypothesis based on (i) resilient macro data; (ii) positive EPS growth; and (iii) improving trade talks. A few thoughts:

· IS A DOVISH CPI BULLISH? My colleague Jon Rogerson mentioned that the weaker CPI may mean that businesses have less runway to raise prices with the next steps after this margin compression being layoffs. I do not have the data to support or refute this, but this phenomenon is exactly why we are hyper-focused on NFP and weekly claims. The trend is a weakening labor market, and we hypothesize that as long as we see NFP above 100k this Bull Rally should continue. That said, keep an eye on initial claims and anything in the 270k – 280k is a red flag that would likely need to be pared with a sub-100k NFP print to verify.

- Small retailers on ‘vacation from hell’ as they seek clarity on Trump’s China tariffs (CNBC)

· HOW MUCH SHOULD WE CARE ABOUT US / IRAN? At this time, it feels like the probability of a kinetic conflict between the countries is very low. For investors with Energy exposure, this another catalyst to squeeze/close shorts and to potentially to drive a reallocation to the sector. Energy has been one of the most underweight sectors during the run since April. Should we be wrong on a kinetic conflict, what are the risks? (i) WTI could move to $73 - $75/bbl –Tarek Hamid in Credit Research/Strategy mentions that Iran produces ~3mm bpd and knocking out 1mm bpd would likely be worth ~$10/bbl. Yesterday’s price action suggest ~30% chance of a kinetic conflict. (ii) Inflation spike – could dent spending and consumer/biz/investor sentiment, depending on the length of any conflict. Natasha Kaneva had published on conflicts involving Middle East conflicts and oil price impacts, while not the same may give a reference point.

· WAS YESTERDAY’S US / CHINA DEAL A GAME-CHANGER? No. While there is a sense that a rare earths-for-chips swap may eventually play out, which would buttress the Tech/AI trade in both US and APAC, that is not exactly what we received. The details have not been fully released but the rare earth supply may be the trump card in any future discussions. Yesterday’s client conversations reveal a wait and see approach to any trade deals but there is an increasing sense that with only 2 deals on the tape and the deadline less than a month away that we see a flurry of deals hit the tape or, more likely, the July 9 deadline is rolled again since Trump seems to avoid any activity that risks re-introducing the ‘Recession’ narrative.

o Bessent floats extending tariff pause for countries in ‘good faith’ trade talks (CNBC)

o Trump’s ‘done’ deal with China: Trade damage already done and will remain, logistics firms, retailers say (CNBC)

· ANY VIEWS ON 25Q2 EARNINGS SEASON? FactSet reveals that analysts have made larger than normal cuts to their Q2 estimates, cutting by 4% from Mar 31 to May 29, vs. 2.5% average decline. Mag7 printed more than 25% EPS growth in Q1, and signs point to another robust quarter, so we may be setting up for another stronger than expected quarter but with muddled guidance, such that beats are not rewarded and misses are crushed.

· US MKT INTEL VIEW – we like buying stocks and if PPI confirms the disinflationary trend, then that may give investors confidence that yesterday’s CPI print was not a fluke. That said, if the next two trading sessions are both weaker then we will like cut risk into the weekend as part of the story may be positioning which is neutral but given the run we may be gearing up for a 3-4% pullback in the absence of positive catalysts.

BY Doug Kass · Jun 12, 2025, 9:35 AM EDT

-CVAC +32% (to be acquired by BioNTech at ~$5.46/ADS in ~$1.25B all-stock deal)

-CVGW +14% (announces Receipt of Unsolicited proposal at $32/shr)

-AAOI +12% (announces first volume shipment of data center transceivers to recently engaged major hyperscale Customer)

-ORCL +8.3% (earnings, guidance)

-CRMT +7.3% (earnings)

-VOYG +4.8% (post-IPO momentum)

-DAN +4.1% (to sell Off-Highway Business to Allison Transmission for $2.7B)

-HYMC -19% (files to sell $40M unit offering)

-GME -16% (files to sell private offering of $1.75B of Convertible Senior Notes due 2032)

-BA -7.5% (Air India 787-8 Boeing Dreamliner plane crashes at India's Ahmedabad airport soon after take-off)

-OXM -7.5% (earnings, guidance)

-OKLO -6.1% (files to sell $400M public offering of common stock)

-GE -4.3% (manufactured engines in the Air India 787-8 Boeing Dreamliner plane crash)

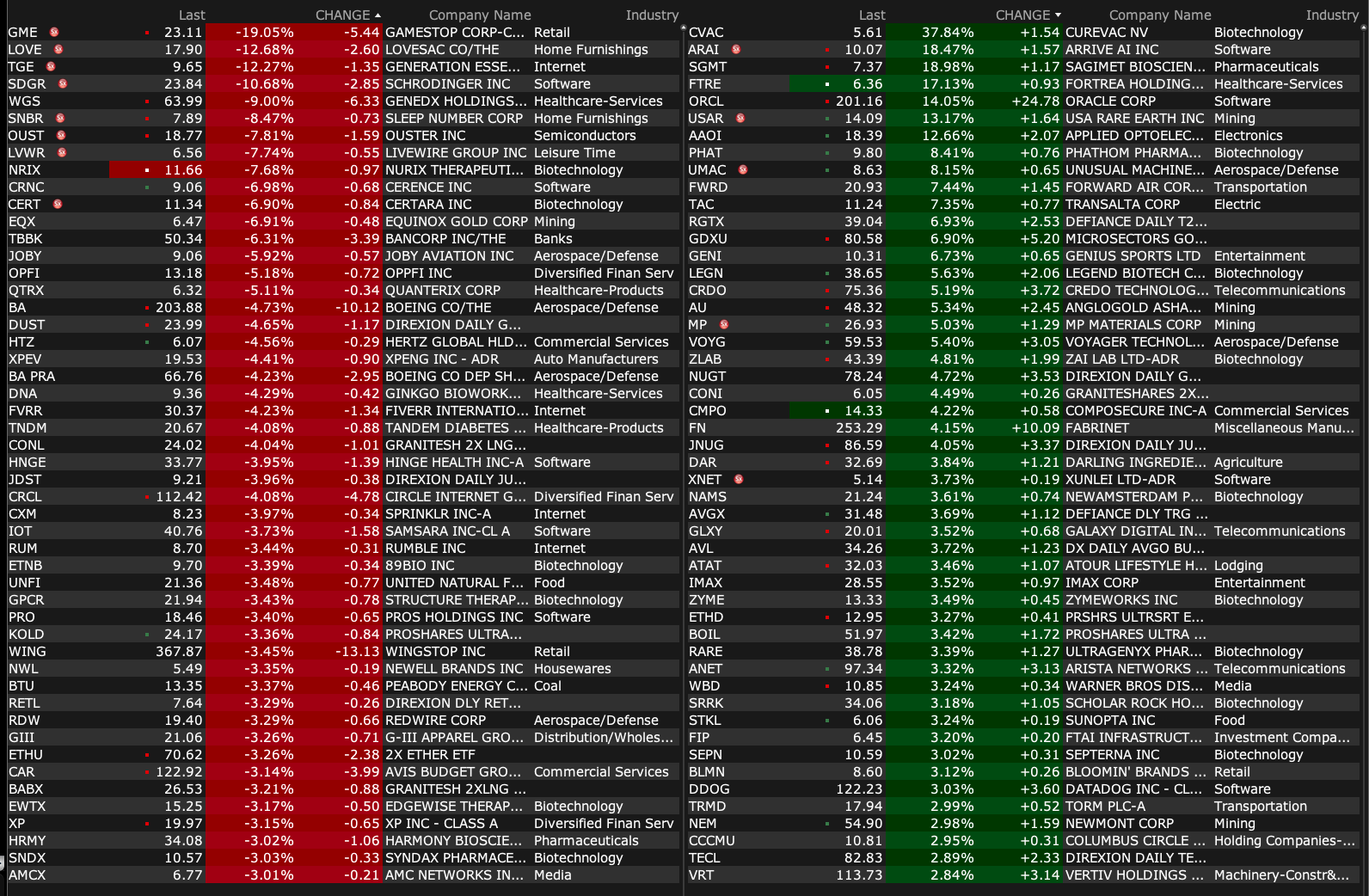

BY Doug Kass · Jun 12, 2025, 9:22 AM EDT

Chart from 8:43 a.m. ET:

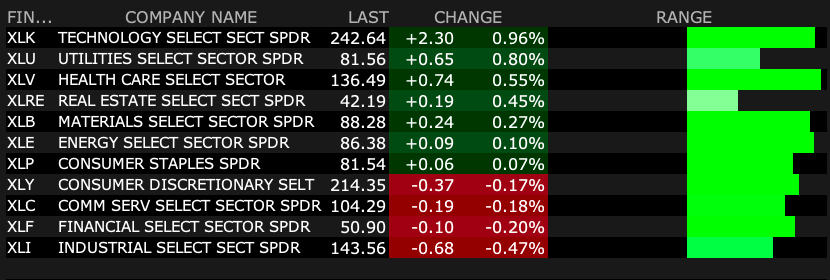

BY Doug Kass · Jun 12, 2025, 9:15 AM EDT

Charts from 8:24 a.m. ET:

BY Doug Kass · Jun 12, 2025, 9:05 AM EDT

* "God only knows" where the market is headed!"

* But my view is that the market's downside risk is now roughly 5x the upside reward.

* This column in dedicated to my bff, Pablo, who brought music into my life 55 years ago.

"I may not always love you

But long as there are stars above you

You never need to doubt it

I'll make you so sure about it

God only knows what I'd be without you"

- The Beach Boys, God Only Knows

Frederick Nietzsche highlighted his belief in the essential role of music in the human experience and its ability to add depth and meaning to life in this quote:

"Without music, life would be a mistake."

This is why music has been such a large part of my own life and why I communicate many of my investment views coupled with a relevant song in my Diary over the last 28 years.

As to the market outlook, my upcoming column makes the case that the downside risk to the market now exceeds the upside reward by about 5x. That's the most unfavorable reward vs. risk since late 2021.

The chart below shows a potentially negative trendline break in the S&P Index:

The S&P 500 Index

But I digress...

This week Sly Stone and The Beach Boys' Brian Wilson passed away.

I was never a great Beach Boys fan until the early 1970s when my bff (and closest pal at Wharton and still my oldest friend), Pablo, turned me on to the group and the surf sound. He is responsible for my love of music that I hold to this day. Pablo, the former Mayor of Roslyn Estates, has a remarkably expansive collection of 45 records (and also one of the largest Lionel train collections in the world). He and I went on to produce a rock and roll revival (when we were yutes) — a travelling concert with Ricky Nelson, Bo Diddley, Bobby Vee and The Marvelettes!

My favorite Beach Boys song, "Don't Worry Baby" was written by Brian Wilson and Roger Christian.

From noted music critic Dave Marsh:

Getting back to Sly Stone — who I wrote about on Tuesday — my favorite song by The Family Stone was "Dance to the Music."

Again Dave Marsh:

RIP Brian Wilson.

BY Doug Kass · Jun 12, 2025, 8:43 AM EDT

From Peter Boockvar:

The US dollar is breaking down today as measured by DXY to the weakest level since March 2022. I'll argue again, the world is rethinking their allocations to US assets from the extreme levels they held as we entered 2025 and they want less exposure. In kind, gold is up by $60 above $3,400 and hovering around its record high. We remain bullish and long, along with silver and platinum and many international stocks and bonds (local currency) that are too benefiting from the dollar weakness.

DXY

I mentioned on Monday some of the ways car dealers are passing on tariff induced higher vehicle prices to the rest of us without having to change the sticker price. Moves like cutting rebates, limiting cheap financing deals and raising delivery charges are some of what is being done. In case you didn't see, in yesterday's WSJ, they had an article titled "The Latest Casualty of the Tariff War: Free Shipping." The first sentence of the piece, "Retailers are cutting back on free shipping to offset the steep costs of tariffs. Some online merchants are eliminating free shipping, while others are raising the amount customers must spend to qualify for the perk of broader efforts to pass along higher costs to consumers."

Here's an example they gave, "Modern Picnic, which sells lunchboxes designed to look like handbags, recently raised the threshold for shoppers to qualify for free shipping to $300 from $150...The company now charges $15 for shipping on orders under $300. The fee doesn't cover all of Modern Picnic's delivery charges, but it helps to mitigate the increased expenses from tariffs and rising shipping costs."

I'm sure some suppliers overseas are eating some of the tariffs but I have to believe that US customers along the supply chain, include the consumer, are eating most of it in some fashion where I'm not sure which of these pricing techniques shows up in the BLS calculation of PPI, CPI, and PCE, if at all.

Container prices for a 6th straight week were higher and have more than doubled over this time frame but the pace slowed. The Shanghai to LA route saw the price of a 40 foot container up by $38, or by .7%, w/o/w to $5,914. The trip to NY rose $121 w/o/w or 1.7% to $7,285 vs $3,500 on May 1st. Assume all of these increased costs are being absorbed by US importers.

Shanghai to LA

Shanghai to NY

Checking stock market sentiment, Bulls now total more than Bears in the AAII survey for the first time since late January with the S&P 500 back near the highs. Bulls rose by 4 pts to 36.7 while Bears were down by 7.8 pts to 33.6. The Investors Intelligence survey saw Bulls up 1.5 pts w/o/w to 39.2 while Bears slipped to 25.5 from 26.4. The CNN Fear/Greed index was 62 yesterday, in the 'Greed' category. The Citi Panic/Euphoria index is around neutral.

Bottom line, there has been a shift to more bullishness with less bears but not to any extreme highlighting still some skepticism with the rally which is a good thing from a contrarian perspective. On the other hand, we are a ways away from the fear seen in April.

Wage growth might falter with the slowing pace of hiring but at least for now it's still hanging in there. We continue to see that in the ADP data and the Atlanta Fed said so yesterday through May with wages up 4.3% y/o/y for a 4th straight month. For 'job stayers', wages grew by 4.3% y/o/y, down slightly from the 4.4% growth seen in the prior three months. For 'job changers', wages were higher by 4.1% y/o/y vs 4.3% in the month before. I'm guessing less labor supply in some particular areas of the economy due to the tighter immigration situation could be a factor, especially in construction and leisure/hospitality. And the pace of wage growth is still running well above pre Covid trends.

Atlanta Wage Growth Tracker

Following the soft jobs data out of the UK for both April and May, partly in response to the higher labor taxes implemented by the new Labor government and tariffs too, UK GDP in April contracted by .3% m/o/m, more than the estimate of down .1%, with weakness in both services and manufacturing. The area of strength was in construction. Gilt yields are falling again but the pound is stronger along with many other currencies, as stated, vs the US dollar

To some earnings comments.

From Chewy whose stock fell about 10% yesterday but the numbers seemed ok:

"Sales rose 8% and "was underpinned by strong participation from new and existing customers across a variety of Chewy's offerings and our favorable mix of core consumables and health and wellness categories. Also notable this quarter was the 12.3% y/o/y growth we delivered within hard goods."

"And from a pricing standpoint, we're not really baking in any sort of inflation throughout the year, although it may not be surprising to hear that as sort of tariffs continue to roll out, the industry might actually react by adjusting some pricing in hard goods or categories that are discretionary. And if that's the case, we stand ready to respond to that." They do though have 85% of their sales from consumables "with domestic input source streams. So we see very little impact from tariffs on Chewy in fiscal year '25 and what we have seen we've embedded in our guidance."

From Oxford Industries, an apparel manufacturer and whose stock is down 6% pre market because comps fell 5% vs their previous guidance of down 2-4%:

"Our own experience during the quarter was similar to what we've seen over the last several quarters, and that is that the consumer responds most strongly to new, innovative, and differentiated product, and to promotions where the perceived value is high. Complicating this situation is the rapidly evolving US international trade policy, particularly with regard to tariffs."

"Tariff policy is challenging us in several ways. First, consumer concern about the impact of tariffs on prices and the economy is exacerbating weak consumer sentiment. Second, the rapid evolution of the tariff policy is making it exceptionally difficult to plan and forecast the business. And finally, the tariff policy is requiring us to significantly realign our supply chain, which could prove to be the catalyst for implementing some changes in our sourcing strategies that ultimately benefit our company and shareholders, but certainly present short term challenges and financial ramifications." I don't believe our trade deficit in apparel goods is a national emergency.

Oracle is up sharply pre market and these comments from Larry Ellison stood out on the AI landscape and referring to the company rise in CapEx to build it out:

"CapEx is going to go up because the demand right now seems almost insatiable. I mean, I don't know how to describe it. I've never seen anything remotely like this."

BY Doug Kass · Jun 12, 2025, 8:35 AM EDT

BY Doug Kass · Jun 12, 2025, 8:12 AM EDT

* Yesterday was a "crude awakening" — in several ways...

Bonus — Here are some great links:

S&P Flashes V-Bottom Indicator

BY Doug Kass · Jun 12, 2025, 6:07 AM EDT

The S&P Short Range Oscillator has grown increasingly overbought — at 4.2% vs. 3.1%.

BY Doug Kass · Jun 12, 2025, 5:45 AM EDT