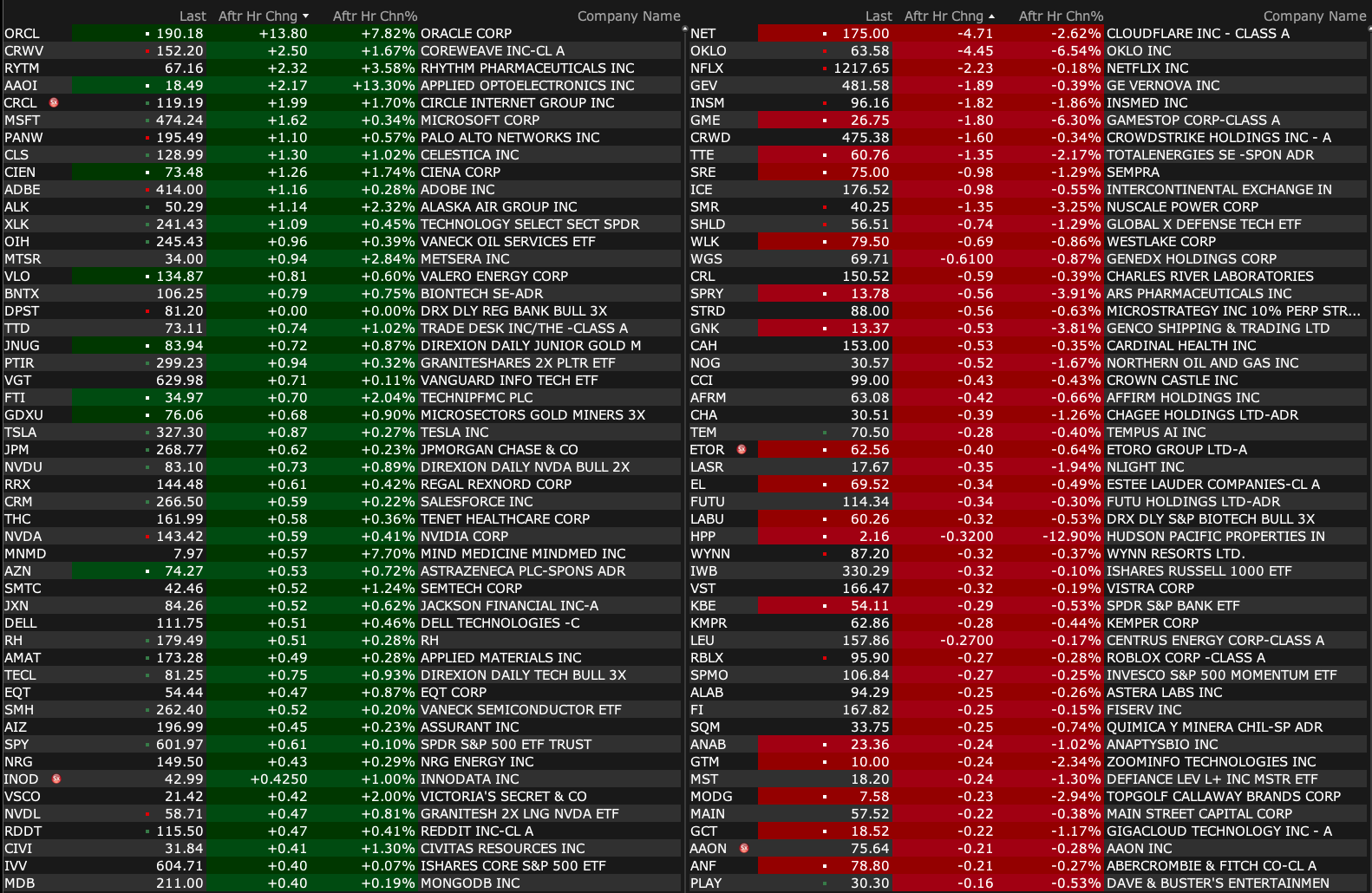

Wednesday's After-Hours Movers

As of 4:18 p.m.:

BY Doug Kass · Jun 11, 2025, 4:40 PM EDT

As of 4:18 p.m.:

BY Doug Kass · Jun 11, 2025, 4:40 PM EDT

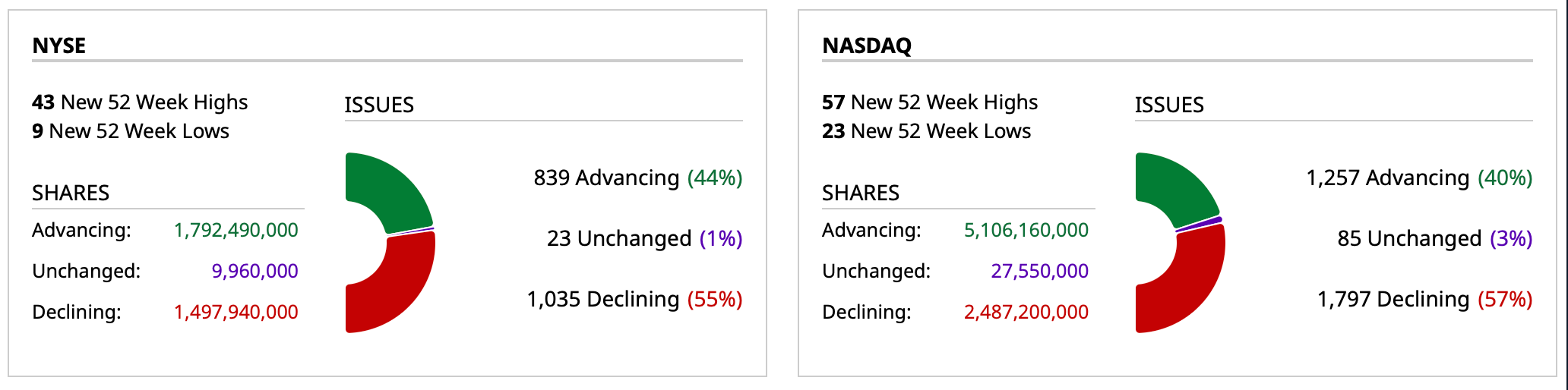

- NYSE volume 6% above its one-month average;

- NASDAQ volume 11% above its one-month average;

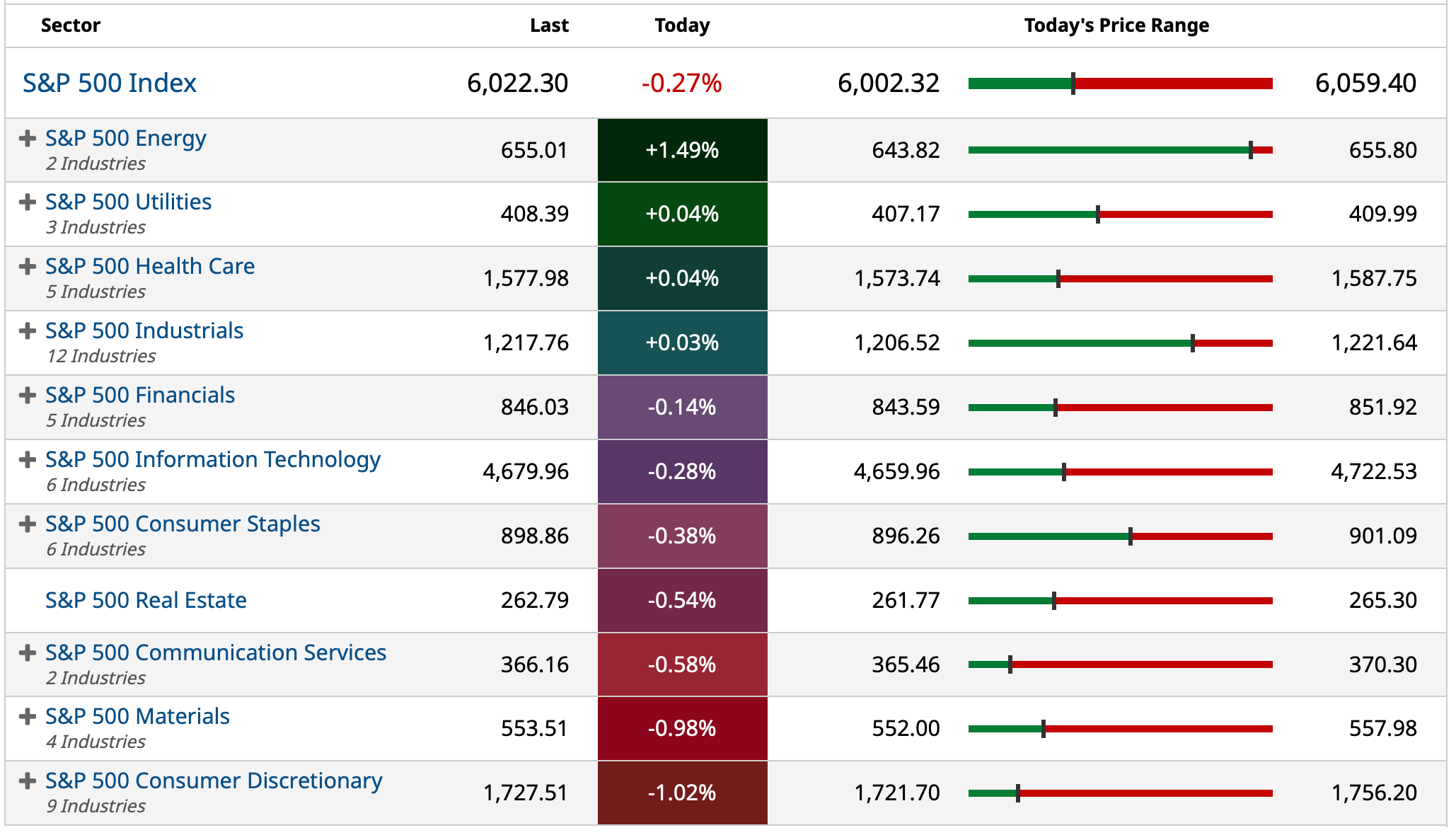

- VIX index: up 2.01% to 17.29

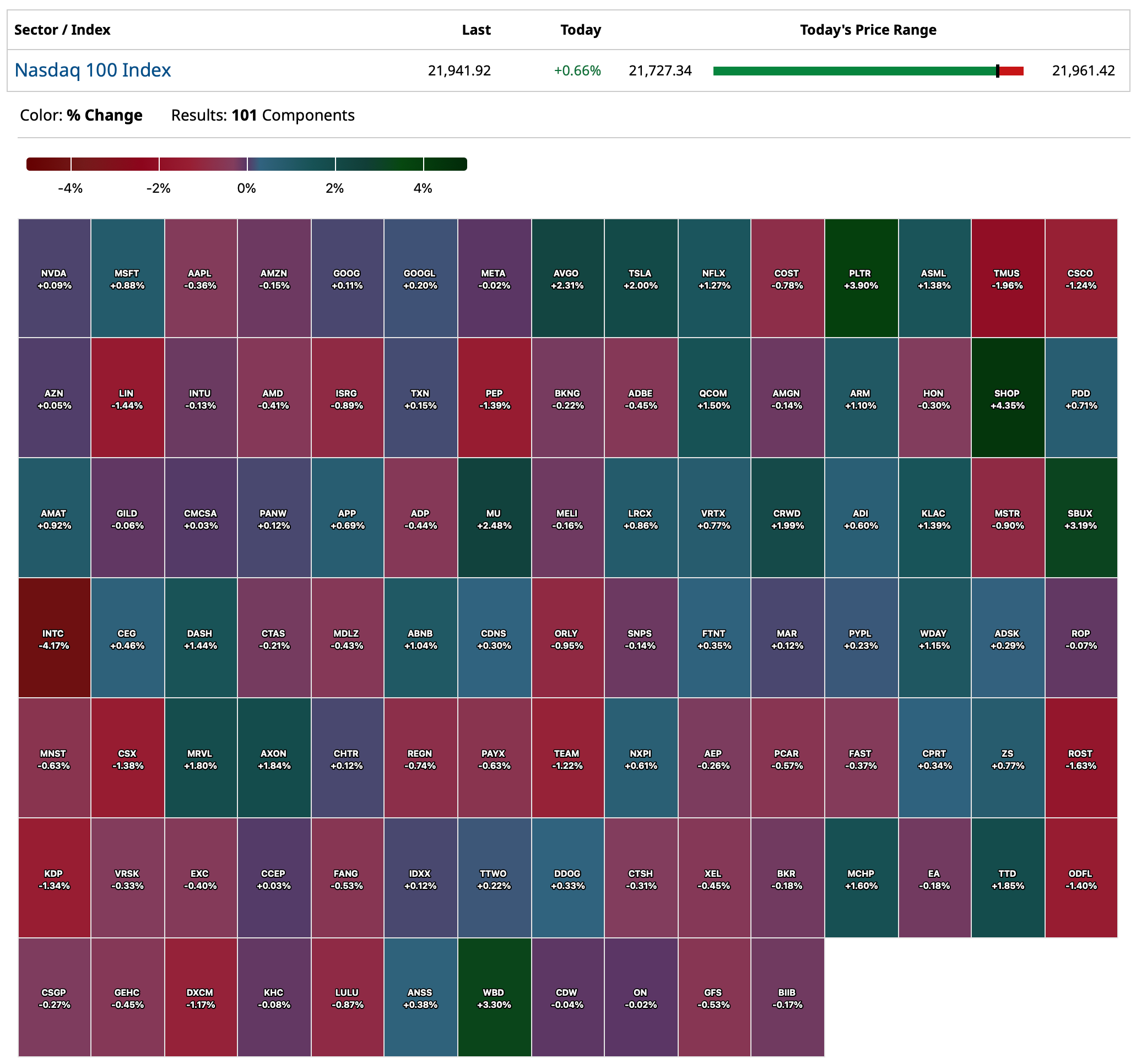

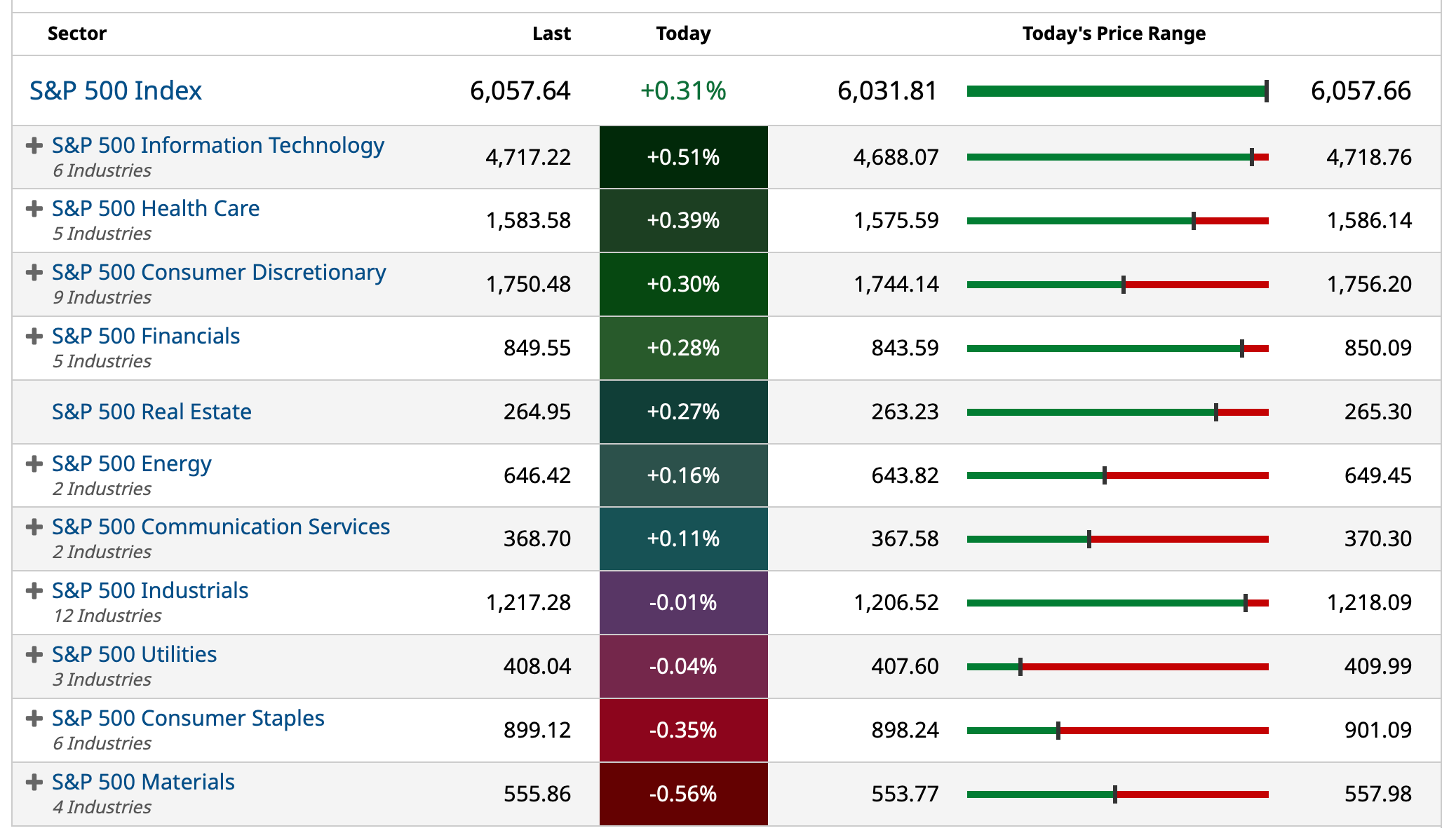

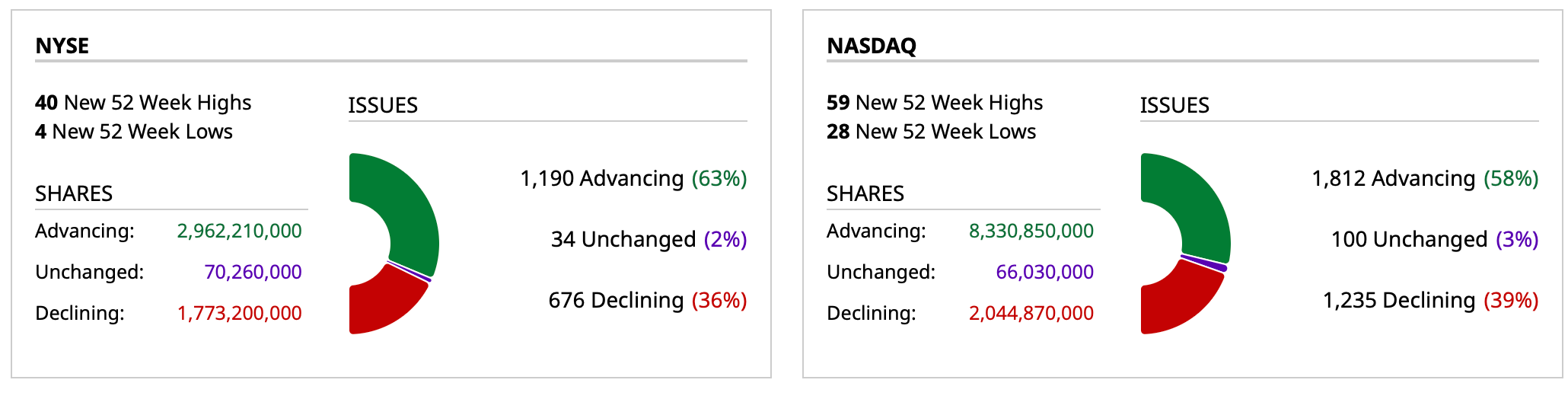

BY Doug Kass · Jun 11, 2025, 4:26 PM EDT

Thanks for reading my Diary today.

Leaving early to meet some friends.

Enjoy the evening.

Be safe.

BY Doug Kass · Jun 11, 2025, 3:45 PM EDT

From Peter Boockvar:

The 10 yr note auction was somewhat of a mixed bag but more good than not. The positive was the yield of 4.421% that was 7 bps below the when issued. Also, was the level of direct and indirect bidding that took down 91% of the auction, a similar pace last month but the most since February 2023. The drag was the bid to cover of 2.52 which was below the previous 12 month average of 2.57, a 4 month low, and the 2nd weakest since October 2024.

Bottom line, maybe in light of the benign CPI report, the 10 yr note auction was decent enough and yields fell further in response. This follows a soft 3 yr auction yesterday. Tomorrow is the 30 yr auction that typically just pension funds, insurance companies and those using that maturity to place a duration bet play in.

BY Doug Kass · Jun 11, 2025, 2:16 PM EDT

I have a quick lunch with an investor.

Back by 1:30 p.m.

BY Doug Kass · Jun 11, 2025, 12:51 PM EDT

BY Doug Kass · Jun 11, 2025, 12:28 PM EDT

BY Doug Kass · Jun 11, 2025, 11:50 AM EDT

I wanted to add several other points reinforcing my (and possibly the market's) cautious reaction to the cooler inflation print:

Based on the recent swings in the trade balance, importers likely stockpiled product ahead of Liberation Day — so they had goods to sell without being subject to a tariff penalty.

When that inventory is sold and runs out, price hikes are likely — producing hotter inflation reads in the second half of this year.

BY Doug Kass · Jun 11, 2025, 11:39 AM EDT

BY Doug Kass · Jun 11, 2025, 11:10 AM EDT

Chart from 9:45 a.m. ET:

BY Doug Kass · Jun 11, 2025, 10:25 AM EDT

From Peter Boockvar:

May CPI rose one tenth both headline and core, below the estimates of up .2% and .3%. The y/o/y gains of 2.4% and 2.8% compare with 2.3% and 2.8% in the month before and about as expected due to rounding. Helping to calm the headline figure was the 1% fall in energy prices m/o/m and down 3.5% y/o/y, mostly due to lower gasoline prices, while food prices were up by .3% m/o/m and by 2.9% y/o/y. Prices for ‘food at home’ were up by .3% m/o/m after falling by .4% last month and higher by 2.2% y/o/y. ‘Food away from home’ is where more of the food inflation is taking place as prices here were up by .3% m/o/m and 3.8% y/o/y.

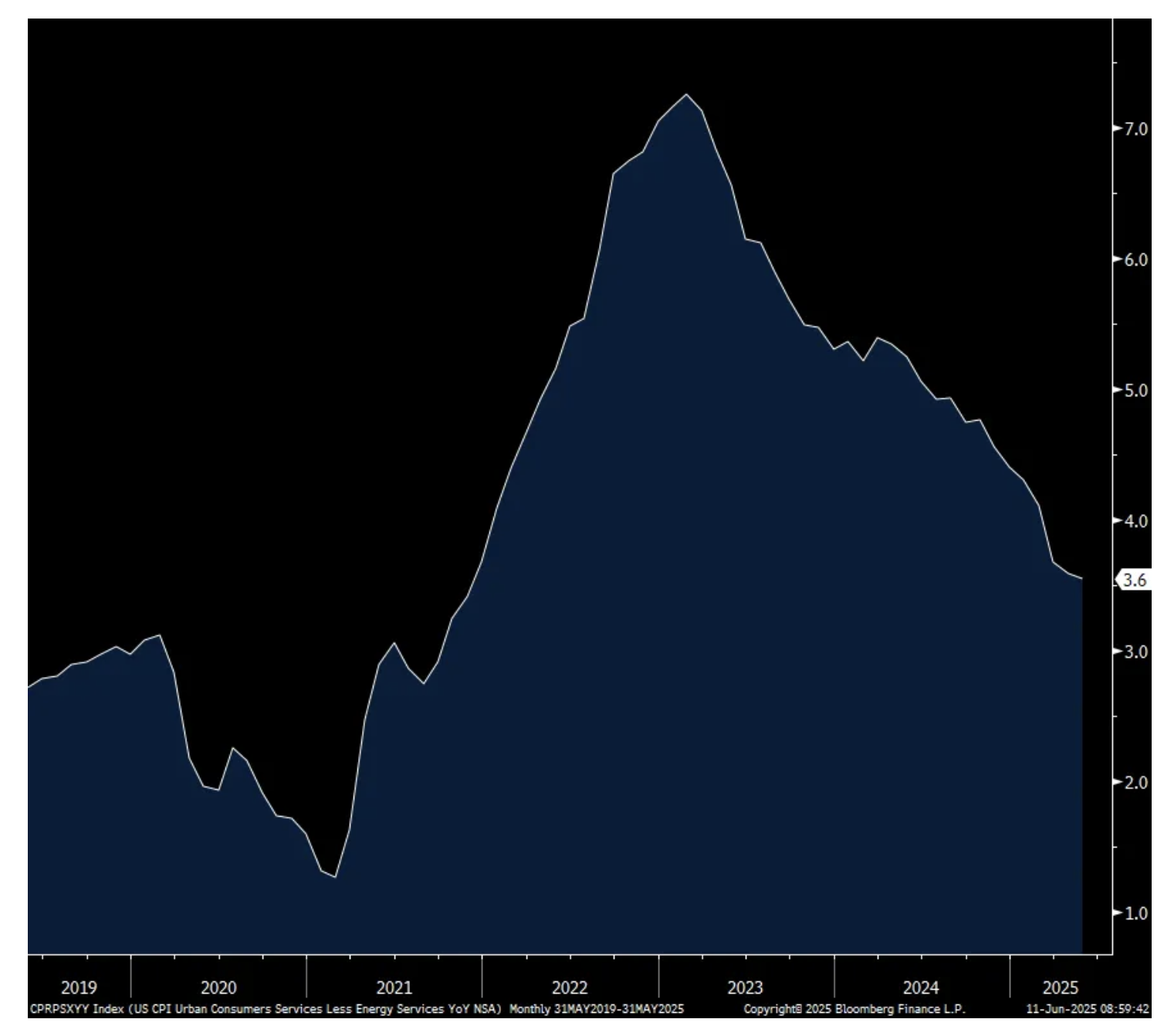

Services prices ex energy was up by .2% m/o/m and 3.6% y/o/y. The biggest component saw Owners Equivalent Rent up by .3% m/o/m and 4.2% y/o/y while Rent of Primary Residence prices grew by .2% m/o/m and 3.8% y/o/y. Medical care service prices were higher by .2% m/o/m and 3% y/o/y. This is still being VERY understated because there is no world in which health insurance prices were up by just .2% m/o/m and 2.9% y/o/y. Auto insurance continues to show robust price gains, up by .7% m/o/m, though the y/o/y gains are moderating because of tough comparisons. It was up 7% y/o/y. After a heady rise, vehicle maintenance costs were flattish, down .1% m/o/m though up by 5.1% y/o/y. Airline fares is where the deflation continues to come from in services as prices here fell 2.7% m/o/m and by 7.3% y/o/y. Also on the travel side, lodging prices were down by .1% m/o/m and by 1.7% y/o/y.

Core goods prices were flat m/o/m and up a slight .3% y/o/y. Lower used and new car prices continue to be the key reason but that should start to change. That said, as heard, higher new car prices are being hidden in other costs passed on rather than the sticker. Apparel prices were down by .4% m/o/m and .9% y/o/y. Prices for things around the house, much of which is imported, rose .3% m/o/m after a .2% gain in the month before, though up a modest .6% y/o/y. But, maybe some signs of tariff related price gains. See below.

Bottom line, a sigh of relief on the lower than expected inflation stats just as we search for where tariffs will work its way through the supply chain and end customer. Nothing much evident yet of this in goods prices, though maybe an early sign in household related stuff like the 1% one month jump in prices for flooring, 1.1% rise in window coverings, 2.3% jump for appliances, 1.1% increase for tools/hardware and supplies. I do expect core goods prices to head higher in the coming months/quarters but if they don’t, corporate margins are going to take a hit as tariffs will get eat by someone. I expect service prices should recede further this year as rents slow before inflecting higher again next year I believe. Help on how the BLS calculates health insurance costs.

Inflation expectations in the TIPS market are falling in response with the 2 yr breakeven down by 5 bps to 2.48%, the 5 yr breakeven lower by 3 bps to 2.31% and the 10 yr down by 2 bps to 2.28%. The 2 yr conventional yield is down a sharp 10 bps post number to 3.94% and the 10 yr yield is lower by almost 8 bps to 4.42%.

With regards to market expectations of Fed rate cuts, we’re back to almost a 100% chance they cut twice, 92% to be exact vs 68% chance priced in yesterday.

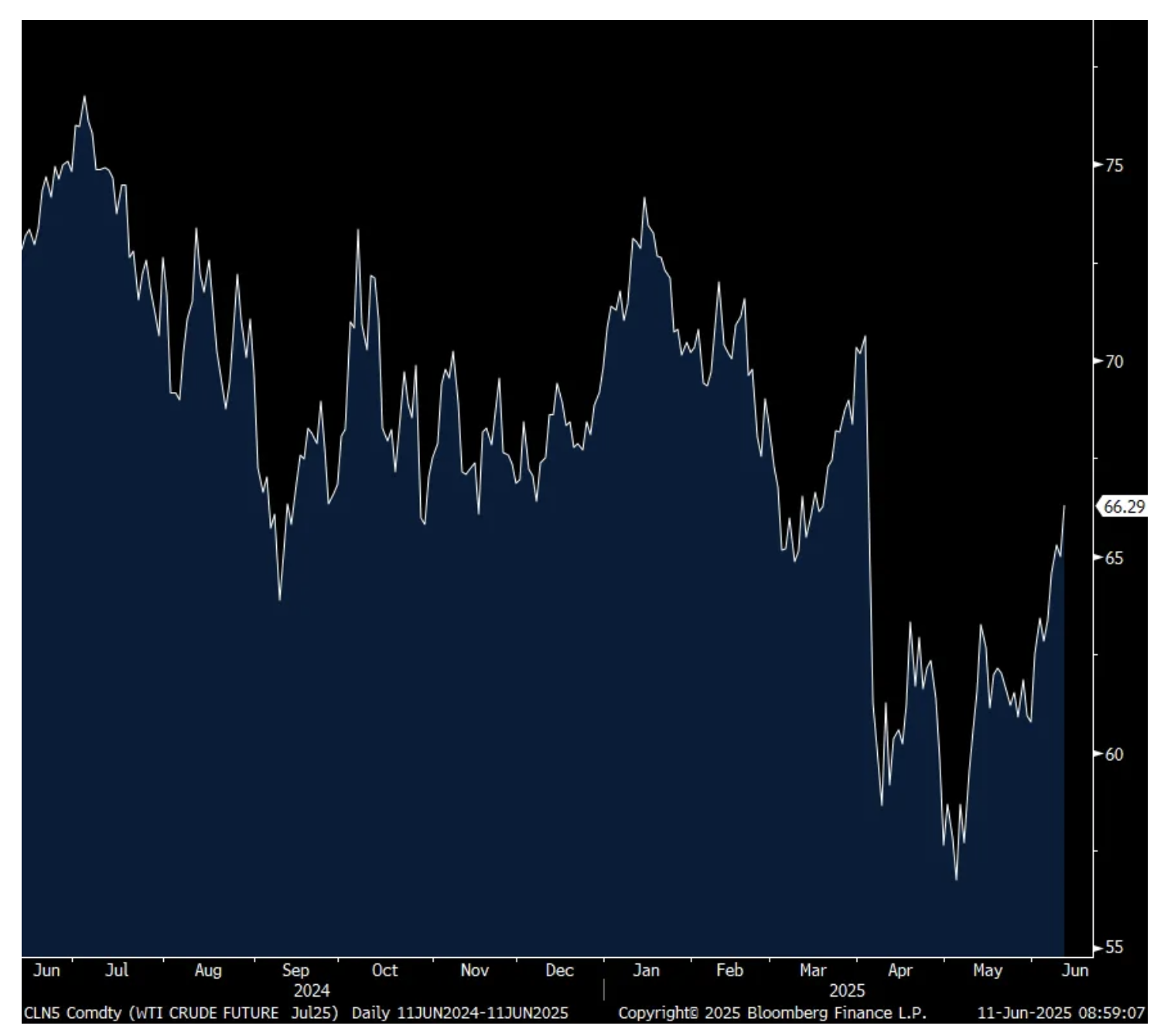

Finally, keep your eye on oil prices as they are quietly at the highest level since early April.

Services Prices ex Energy y/o/y

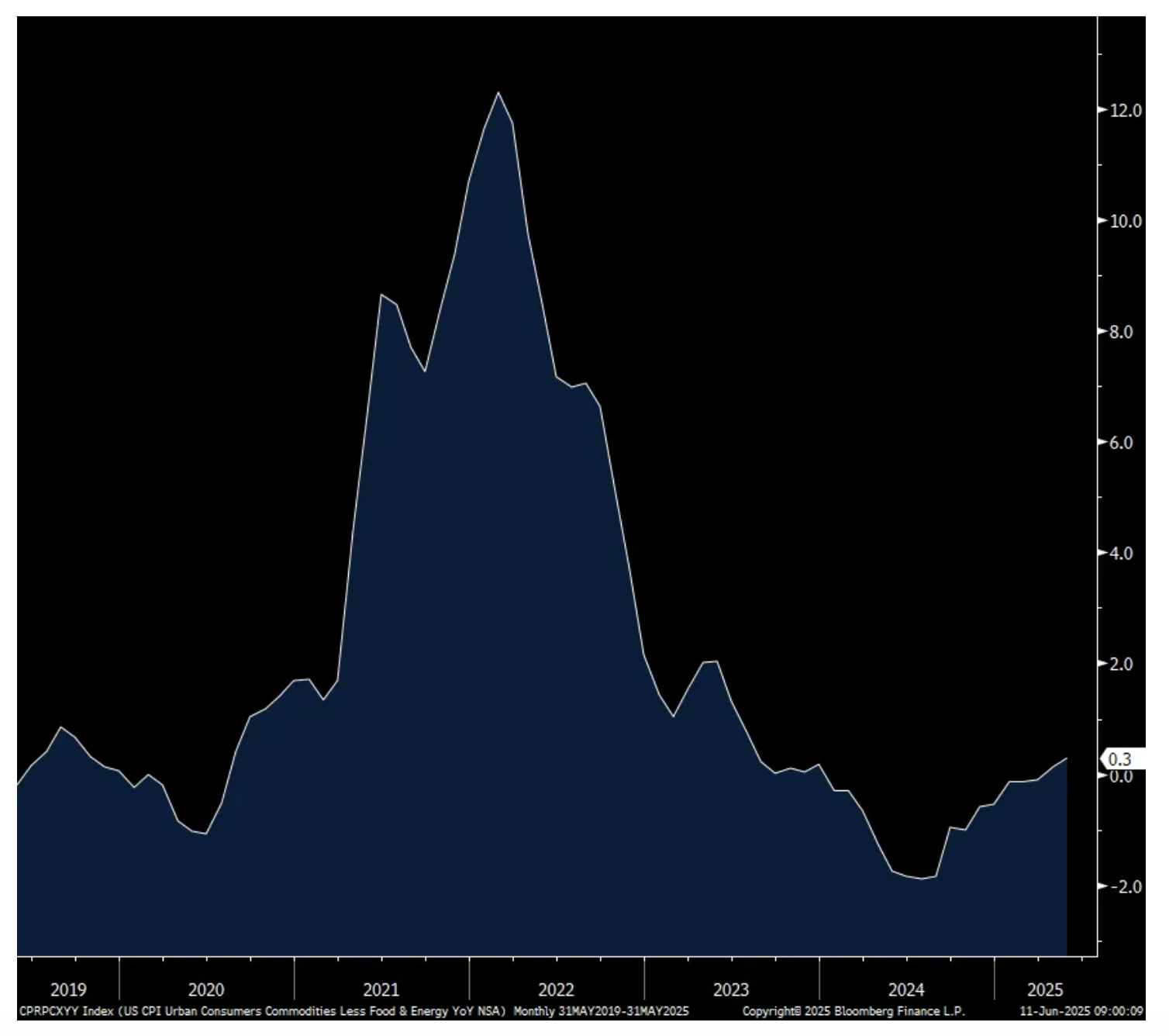

Core Goods Prices y/o/y

Oil Prices

BY Doug Kass · Jun 11, 2025, 10:10 AM EDT

If you read JPMorgan's CPI scenario analysis you will see that given the colder inflation print, the brokerage expected more than a +2% positive reaction to the print:

· [5.0%] Core MoM prints below 0.25%. SPX gains 2% - 2.5%. The other tail outcome, similar to recent results from EU/UK, this would be a material dovish print. Look for the bond market to add back at least 2x 25bp rate cuts and for Equities to react positively to the bull steepening that likely ensues.

The reason I think they are wrong in the +2% estimated rise in the S&P is because

1) the market has likely already discounted a better than expected Core CPI and, more importantly,

2) the China/US tariff meeting ended up being a complete non-event (with no evidence of lowering tariffs) and

3) market participants may interpret this number as being less exciting for equities because companies/manufacturers are likely eating the higher costs/ tariffs, leading to concerns about lower margins and profits over the balance of the year.

Ludicrous, I say.

BY Doug Kass · Jun 11, 2025, 9:50 AM EDT

BY Doug Kass · Jun 11, 2025, 9:39 AM EDT

Added to shorts in indexes:

* SPY $605.08

* QQQ $536.55

BY Doug Kass · Jun 11, 2025, 9:30 AM EDT

It looks like Mike Tyson has officially entered the ring — this time, to bring a little common sense to Washington by pushing for cannabis rescheduling. If Iron Mike can get Donald Trump to say anything constructive about cannabis, it could be a game-changing moment — sparking some much-needed momentum for the cause.

That said, let’s not forget: we’re still waiting on Terry Cole to be confirmed as DEA Administrator. If history is any guide, Biden’s nominees have taken an average of 100 days to get the Senate nod once they hit the calendar. So buckle up — we might be in for a bit of a wait before this next round starts.

BY Doug Kass · Jun 11, 2025, 9:29 AM EDT

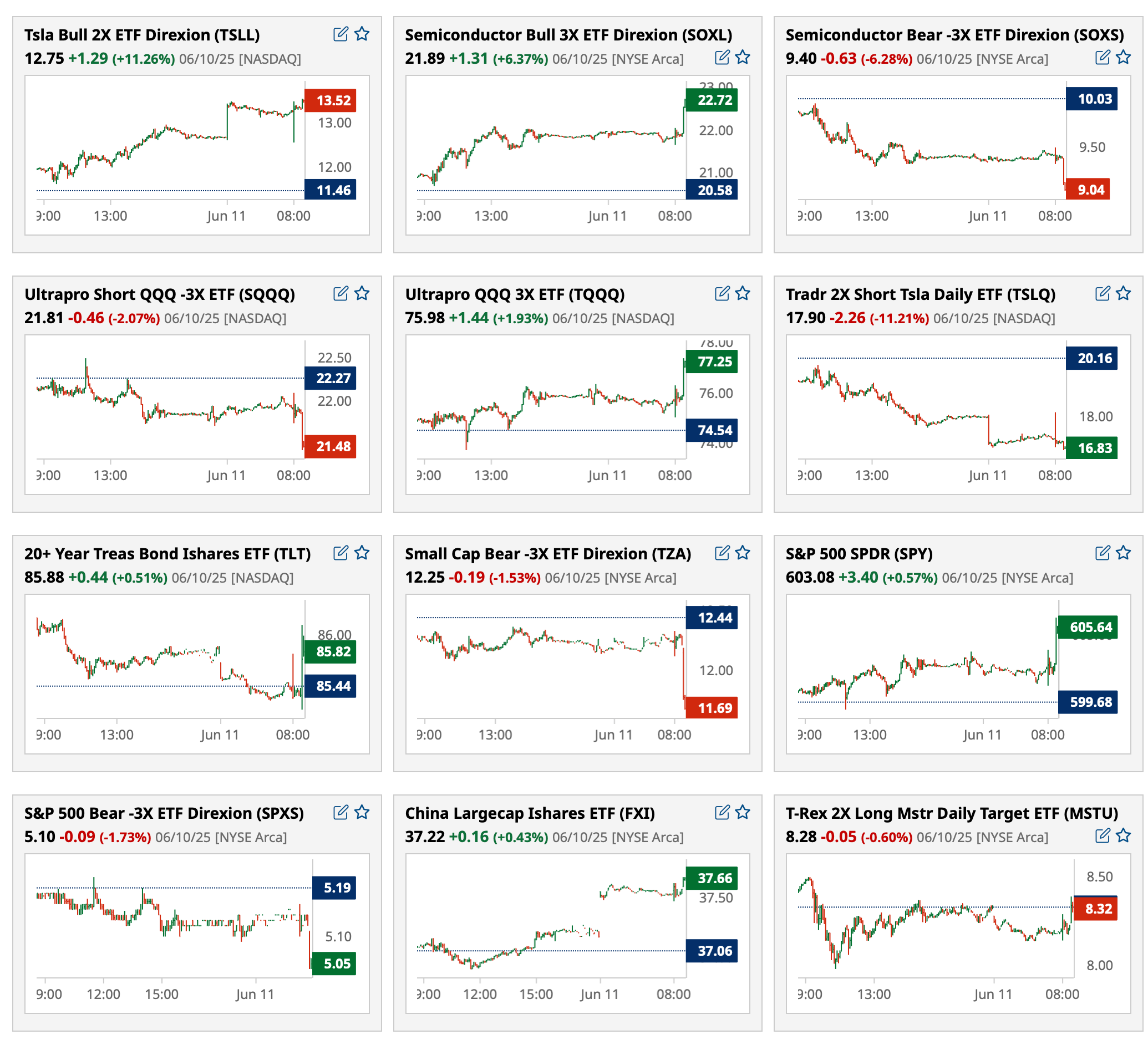

Most active premarket ETFs as of 8:34 a.m. ET:

BY Doug Kass · Jun 11, 2025, 9:13 AM EDT

-VXRT +66% (reports positive topline results from the Phase 1 clinical trial evaluating its second-generation oral pill norovirus vaccine constructs head-to-head against its first-generation constructs)

-OUST +15% (Digital Lidar technology OS1 Approved by Defense Department for Unmanned Aircraft)

-SFIX +15% (earnings, guidance)

-DV +14% (raises guidance ahead of Innovation Day)

-SAIL +11% (earnings, guidance)

-TLN +7.0% (announces expanding existing nuclear energy relationship with Amazon to provide carbon-free energy from Talen’s Susquehanna nuclear power plant to Amazon Web Services data centers in the region)

-PLAY +5.9% (earnings, guidance)

-SBFM +5.9% (subsidiary Nora Pharma launches generic gabapentin for neuropathic pain)

-SSTK +5.7% (receives Stockholder Approval for Proposed Merger with Getty Images)

-LAES +4.3% (to provide 30M digital certificates for Landis+Gyr smart meters in Asia Pacific)

-PCRX +3.1% (unveils Three-Year Clinical Data Following a Single Local Administration of Investigational Gene Therapy, PCRX-201, in Patients with Moderate-to-Severe Osteoarthritis of the Knee)

-SMR +3.0% (strength in nuclear-related names)

-INSM +2.9% (hearing price target raised at Morgan Stanley following PAH study data)

-TSLA +2.5% (hope of improved relations between CEO Musk and President Trump)

-DPRO -27% (prices $13.75M public offering of 5.5M shares at $2.50/shr)

-JILL -19% (earnings, guidance)

-AMSC -18% (prices 4.13M shares at $28.00/shr in $115.5M public offering)

-CABA -15% (announces New Rese-cel Safety and Efficacy Data in Patients with Myositis, Lupus and Scleroderma to Be Presented at the EULAR 2025 Congress; terminates $200M ATM Sales Agreement with TD Cowen; files to sell stock and warrants of indeterminate amount)

-GTLB -13% (earnings, guidance)

-CHWY -7.6% (earnings, guidance)

-IREN -6.8% (prices $500M convertible notes due 2029 with capped call hedge)

-MP -6.7% (weakness following President Trump statement that China will supply rare earth elements as part of a trade agreement)

-THC -5.7% (hospital space weakness)

-CLF -5.2% (US and Mexico near deal to cut steel tariffs and set a cap on imports)

-RUN -5.0% (Jefferies Cuts RUN to Underperform from Hold, price target: $5)

-GME -4.4% (earnings)

-VRA -4.3% (earnings, guidance; CEO to depart)

-NUE -4.0% (US and Mexico near deal to cut steel tariffs and set a cap on imports)

-ETSY -3.7% (files to sell $650M convertible senior notes due 2030, with option for additional $50M)

-SMMT -2.6% (SVB Leerink LLC Initiates SMMT with Underperform, price target: $12)

-INGM -2.3% (Morgan Stanley Cuts INGM to Equal Weight from Overweight, price target: $22)

BY Doug Kass · Jun 11, 2025, 8:58 AM EDT

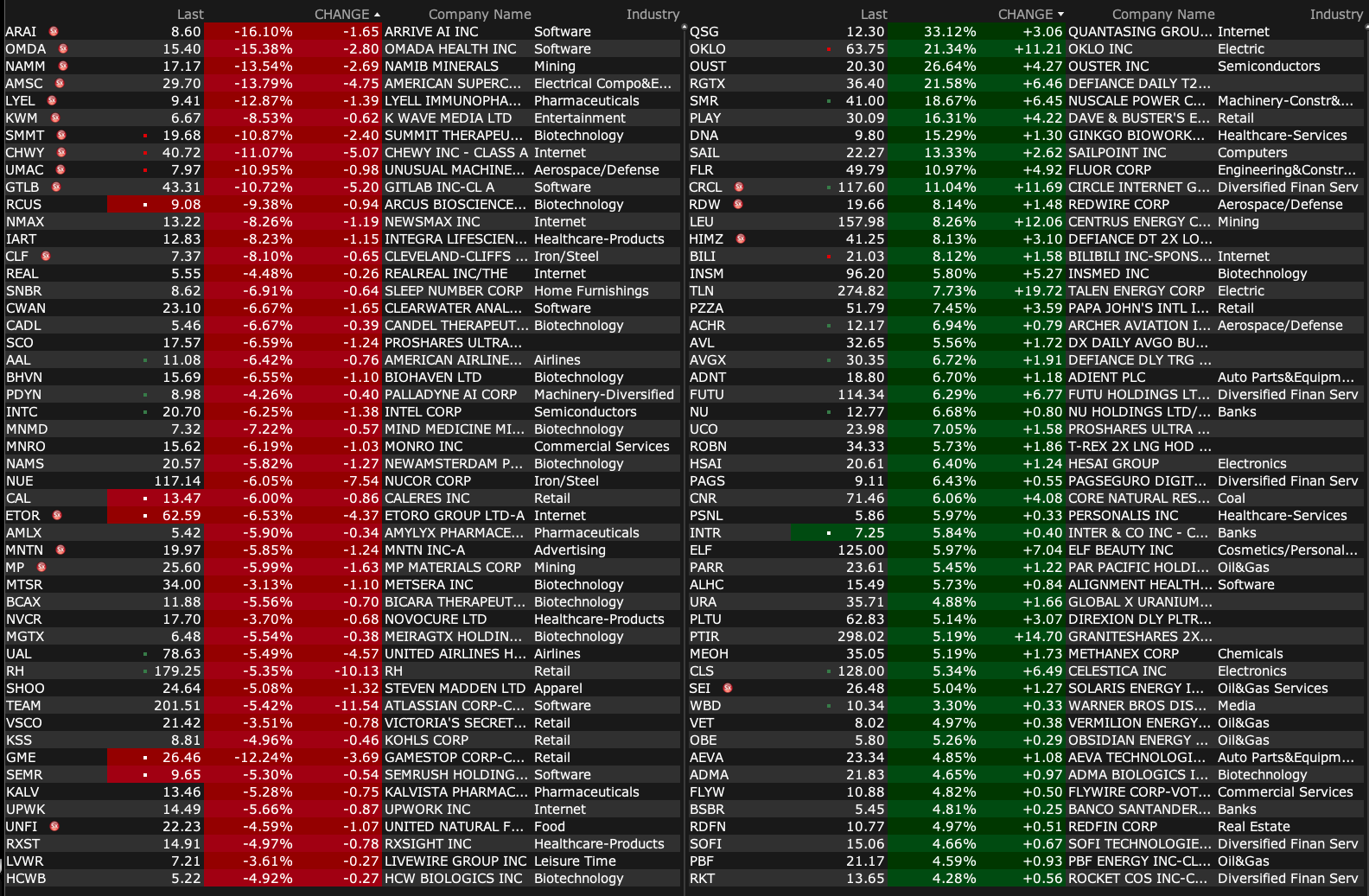

Premarket percentage movers as of 8:41 a.m. ET:

BY Doug Kass · Jun 11, 2025, 8:55 AM EDT

From Peter Boockvar:

That seemed like a lot of conversations between the U.S. and China teams over the past few days only to go back to the trade outline of a month ago. It again begs the question of what does an ultimate deal look like that would be anything different than what was struck in 2020? That said, we know right now the discussions are solely on the key items that each side needs from each other like rare earths, semi's, airplane parts, ethane, etc...

Meanwhile there is a Bloomberg News story today on the talks with the EU that said, "The European Union believes trade negotiations with the US could extend beyond President Donald Trump's July 9 deadline, even as the speed of the talks has increased over the past week. The EU sees reaching an agreement on the principles of a deal by July 9 as a best-case scenario, which would allow further talks to work out the details, according to people familiar with the matter. The US is expected to respond to the latest round of negotiations in the coming days and provide clarity on the next steps."

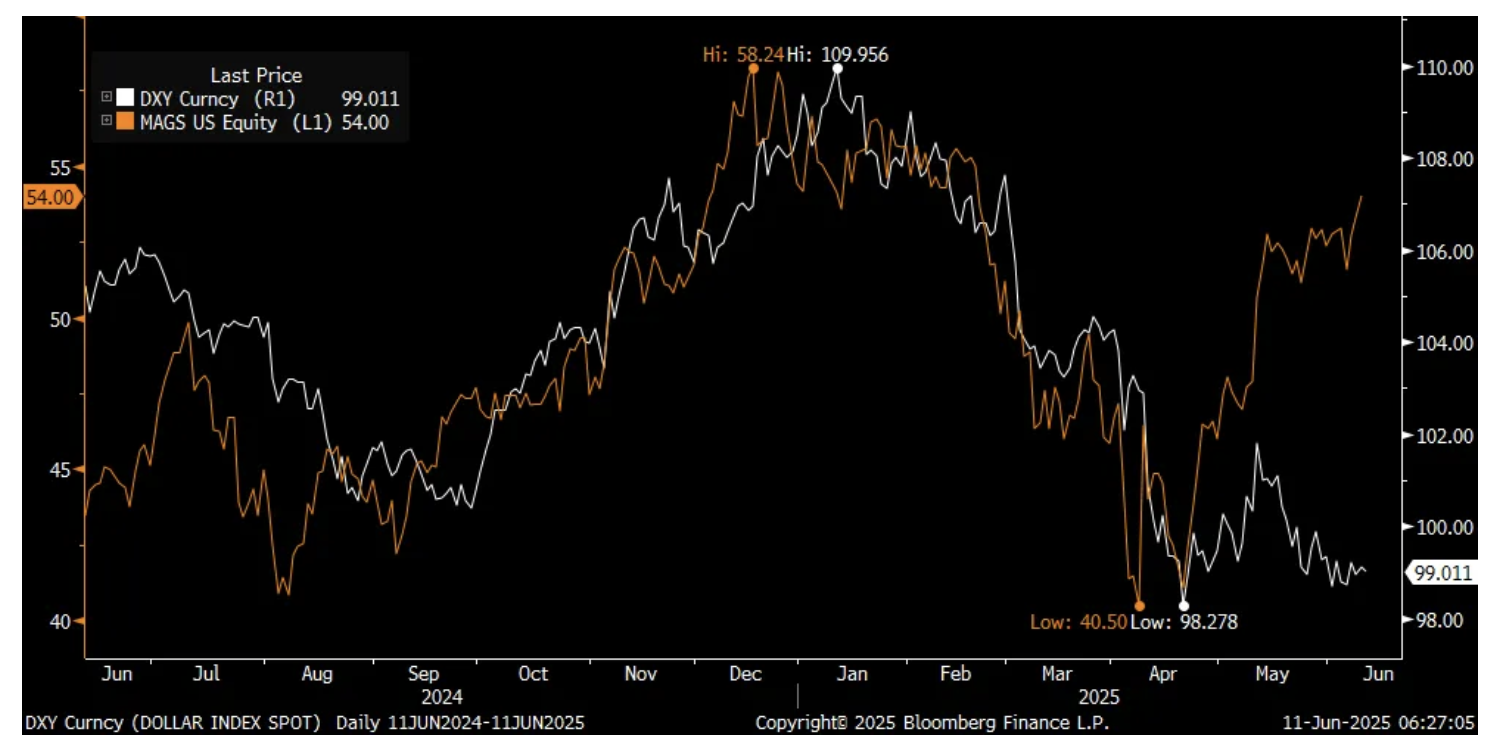

I want to update a chart for you of the US dollar and the MAG7 index as with the rally in the latter and the former that can't get out of its own way, they have separated in terms of its movements. I argued earlier in the year that the MAG7 stock group became a reserve asset for foreign investors, both private and official (sovereign wealth funds and central banks), that was about to unwind to some extent as the foreign allocation to US assets just got too large. Up until April 9th, the two pretty much mimicked each other in terms of performance over the past year.

MAGS etf in orange, DXY in white

Casey's General Store is one of my go to consumer touching conference calls as their convenience stores reach all parts of the US population. The stock ripped higher by 11.6% yesterday on good revenue growth, fuel margins and better earnings and has been rewarded by markets with a 31x P/E ratio.

"We saw excellent results throughout the year in non-alcoholic beverages (they said particularly energy drinks), as well as hot sandwiches...Our fuel team continues to grow market share, focusing on gross profit dollars while balancing fuel volume and margin."

They gave a wide 2-5% same store sale guidance for their fiscal yr 2026 and said "I do think with everything going on in the world, it's reasonable to have a little bit of conservatism there on the low end. And so we factor that into the guidance."

February was a tough month because of weather and something we heard from many retailers but "March came back at 3.7%, April came back at 5%, and May was in the guidance range."

The view on their customers, "I would say the consumer is really hanging in there and continuing to visit our stores as frequently as they have historically. We're seeing good strength from the higher income consumers, those making over $100,000 a year." We know that is something we've heard from the dollar stores, along with the warehouse clubs.

"And even on the low end, we are seeing that traffic hanging in there. They are modifying some purchasing behavior. I think what's interesting that as we dug into this, there's two types of low income consumers. I think there's a cohort of consumers who perhaps have a family and they're really stretched to make ends meet. But we're also finding in that low income cohort, those are a lot of younger folks that are early on in their careers. And so they are lower income, but they don't behave like folks that are really stretched to make ends meet. And so think more Gen Z and younger millennials. And so the purchasing habits for those folks are very different than what you'd have for some other maybe more mature people in that income cohort."

On inflation, "we haven't seen a lot of inflation just yet on the commodity side of things...On the grocery and general merchandise business, outside of tobacco and almost exclusively cigarettes, we're not seeing a lot of inflation there either. So I would say at this point, we're not seeing any flow through of any sort of tariff impact as of yet."

Academy Sports & Outdoors talked also about its income cohort visiting the stores in its earnings call. "I think it is important to point out that as the situation has evolved, we've continued to see an increase in foot traffic from customer's household incomes over $100,000 annually. This is a pattern we have seen emerge over the past couple of quarters and it is starting accelerate. We would expect this trend to continue as customers look to stretch their discretionary spending power by seeking out value."

Comps fell 3.7% in the quarter but much due to February weather and April finished positively. For those that own stock in Nike, "Nike was a key sales driver across all three areas and as you'd expect, was one of our best performing brands in the quarter."

"Looking at performance by category, footwear and apparel continued to perform well...Within our sports and recreation category, outdoor cooking and baseball posted positive comps as spring started to materialize across the country, especially in our footprint. While we saw encouraging results in baseball, total team sports underperformed primarily coming from softness in basketball and a slower start to the quarter in golf."

"In outdoors, fishing and firearms performed well, while ammunition, paddle and power marine remain challenged."

Norfolk Southern spoke at a Wells Fargo conference yesterday and said "so first two months of the quarter in the bag, how do we think June is progressing here? And we are starting to see a little bit of softness, more than what we expected, probably...It's something that we're definitely monitoring. But we'll definitely stay close to our customers on this and make sure we're looking at any leading indicators that point to any further degradation."

"We're seeing some pressure within the steel markets, within grain, within our aggregates markets. So there's definitely some pressure there on the merchandise side."

Union Pacific said at the same conference, "Industrial, a little bit of a mixed bag, but still seeing strong performance on the industrial chems and plastics. If you looked in at the premium line, that's kind of a tale of two pieces. You've got automotive, which is down q/o/q, down about 6%. You have intermodal, which is still up, but certainly you saw in our intermodal volumes this week, in total down 7%. We're hitting that air pocket that people have been looking for."

Microchip Technologies spoke at a Mizuho conference and they are seeing some inventory rebuilds. "May bookings was the highest that we've seen in many years. And so bookings has continued to improve, book-to-bill continued to improve as well."

And to the question, "Is that a commentary across all the markets like automotive, industrial?" The answer, "So yes, we're seeing it come across from all different marketplaces. We're starting to see that a lot of our customers, distribution, inventory has really started to bottom out. And people are having to replenish now."

From JM Smucker whose stock fell 15.6% yesterday as those chocolate twinkies weren't enough to lift sales in the Hostess division:

This line was surprising, "Overall, the dog snacks category continues to be impacted by a slowdown in discretionary spending largely driven by inflationary pressures."

They were also hit by tariffs on their coffee business as "Green coffee is an unavailable natural resource that cannot be grown in the continental US due to its reliance on a tropical climate. We currently purchase approximately 500 million pounds of green coffee annually, with the majority coming from Brazil and Vietnam, the two largest producing countries."

Even though mortgage rates held steady in the week ended 6/6 at 6.93%, purchase applications to buy a home jumped by 10.3% w/o/w after falling by 4.4% last week while refi's rebounded by 15.6% w/o/w. We are of course about to wrap up the spring selling season.

BY Doug Kass · Jun 11, 2025, 8:35 AM EDT

BY Doug Kass · Jun 11, 2025, 8:18 AM EDT

dave wells

i probably missed it but have you updated your thoughts on pot stocks ?? long glasf...they trade like death warmed over

Dougie Kass

yes i have written several columns in last month

bottom line:

BY Doug Kass · Jun 11, 2025, 7:50 AM EDT

* Yields again climb... as equities continue to decouple from bonds

Yesterday I cautioned about a reversal in bond prices (lower):

Bond prices are now well off their day's highs.

Watch (TLT) closely.

Position: None.

By Doug Kass Jun 10, 2025 10:46 AM EDT

This morning, bond prices continue to sag (and yields are climbing further):

* The yield on the 2-year Treasury note is +2 basis points to 4.13%.

* The yield on the 10-year Treasury note is +3 basis points to 4.51%.

* The yield on the 30-year Treasury bond is +3 basis points to 4.97%.

For now, market participants are ignoring the persistency of higher interest rates, a likely deceleration in corporate profit growth (over the balance of 2025), a further narrowing in the equity risk premium and numerous other headwinds.

But, as night follows day, interest rates form the foundation of stock market valuations (discounted dividend and cash flow models) — and, at some point in time, will "count for something."

BY Doug Kass · Jun 11, 2025, 7:35 AM EDT

BY Doug Kass · Jun 11, 2025, 7:25 AM EDT

* Glory Days... Calls for S&P 7000 are appearing

Bonus — Here are some great links:

BY Doug Kass · Jun 11, 2025, 6:55 AM EDT

BY Doug Kass · Jun 11, 2025, 6:45 AM EDT

BY Doug Kass · Jun 11, 2025, 6:35 AM EDT

From JPMorgan (good CPI scenario analysis):

US MKT INTEL CPI SCENARIO ANALYSIS – Feroli sees Headline MoM printing +0.16% and Core MoM printing +0.31%, both numbers are in line with the Street. This equates to 2.4% YoY for Headline and 2.9% YoY for Core. If correct, we see Feroli’s outcome has having ~35% probability and would push the SPX as high as 75bps that day.

and...

· US: Futs are flat into the CPI print after the US/China agreement failed to create gains. US/China agree to a framework of a deal with few details though talk around rare earths being solved is giving optimism. US/Mexico close to a deal on steel tariffs by using import caps, which would be higher than the previous cap, and would remove the 50% tariff on steel below said cap; this looks like a reversion to 2018 levels and may be a template for talks with Canada. The G7 summit will carry add’l weight as we are ~month away the expiration of the 90-day tariff delay, with only a US/UK framework on the tape. Pre-mkt, Mag7 names are mostly higher with TSLA (+5.7%), GOOG (+1.4%), and META (+1.2%) the standouts. Semis and Cyclicals poised to outperform. The yield curve is twisting steeper, USD is flat, and cmdtys are mixed with crude flat, natgas/base/precious rallying, and Ags down.

and...

EQUITY & MACRO NARRATIVE

Look for an in-line or dovish CPI print to propel markets to ATHs but for a hawkish print to be penalized more than a dovish print would be rewarded. We like running long risk into month-end as event risk returns. While CPI appears to be a positive catalyst, this is an ancillary event to US/China trade talks. Some thoughts on the Momentum Factor unwind before jumping into CPI scenario analysis.

· US MOMENTUM UNWIND (Manish Sinha) – Ahead of CPI, it's interesting to see the rotation between Growth (JPGPURE Index) vs Value (JPVPURE Index). Typically, investors cover their Value shorts when they expect an inflation cycle.

o Momentum (JPMPURE Index) underperforms is attributed to Laggards (JPMOLAG Index) from today's squeeze of crowded shorts (JPCROWS Index). Squeeze in Beta & Res-Vol often indicates investors are covering positions ahead of a growth cycle. Covering Value positions, like today, suggests that investors anticipate an inflationary cycle.

o The Beta factor (JPBPURE Index), which is long Growth vs short Value, is negatively impacted due to this rotation.

· EU MOMENTUM UNWIND (Federico Manicardi) – This morning moves in Equity Internals (both in Europe and Japan) and FX (to a lower extent) somewhat reminds us of post Geneva talks with the difference that people are now long (particularly in Europe), so Beta is not moving while Momentum is down. We have been more cautious on Europe directionally since May 22nd on a series of risks (e.g. 2Q earnings due to FX and GDP payback from front-loading, positioning/CTA flows headwinds, now politics etc. see here). I wouldn’t increase directional risk in Europe here but still rather look at US (AI/Tech mainly but watching RTY short squeeze).

o The focus today is on how/if we should change the Playbook in Europe i.e. from Domestics/EU Recovery theme to Tariff Losers/US Exposed/Exporters. There are two things to bear in mind (and also the reason to be less impulsive to chase moves). First, that typically large MOMENTUM drops reverses (Chart below from D1). Second, the exposure seems relatively higher on MOMENTUM longs.

o Hence, when think what moves in Crowded shorts (Semis, Healthcare, Autos, Luxury, Energy, PP etc.) and Crowded Longs (Banks, Defence, Insurance, Construction, Germany, Utilities etc.) should be faded/chased our (very tentative) preliminary conclusions would be to look for dips in Germany (MDAX) and perhaps Banks (but would wait a bit longer). On the Short Side, Semis and Healthcare is where we would prob focus.

CPI SCENARIO ANALYSIS

Feroli’s CPI preview is here. For CPI he sees Headline MoM printing +0.16% and Core MoM printing +0.31%, both numbers are in line with the Street. This equates to 2.4% YoY for Headline and 2.9% YoY for Core.

The following scenario analysis is NOT A PRODUCT OF JPM RESEARCH, this is a trading desk view from JPM US Market Intelligence. This month we focus on Core MoM outcomes and 1-days SPX moves.

· [5.0%] Core MoM prints above 0.40%. SPX loses 2% - 3%. The first tail outcome, likely triggered by both hotter than expected Core Services and Core Goods. An outcome that is incongruent with NFP, in terms of what is likely to be witnesses from the trade war. That said, a print of this kind would likely map to higher than expected inflationary impulse from the trade war. Look for the yield curve to reprice higher, reflecting a stagflationary outcome. Longer-term, if we saw growth hold up (Retail Sales would be the next print) then we could see the 10Y yield make a run at 5%.

· [25.0%] Core MoM prints between 0.35% - 0.40%. SPX loses 1.25% - 1.75%. Here, we likely see Core Services remaining hotter, likely from OER remaining sticky. Bonds would react negatively to this type of print and think any additional cuts would be priced into later in the year given the expectation for a spike in inflation this summer.

· [35.0%] Core MoM prints between 0.30% - 0.35%. SPX loses 0.25% to gains 0.75%. The base case outcome range but at the higher end we see a slight sell-off while the lower end of the range continues the rally.

· [30.0%] Core MoM prints between 0.25% - 0.30%. SPX gains 1% - 1.5%. Given the recent dovish CPI prints across the G7, we think there is a slightly higher chance that this outcome unfolds, creating a skewed distribution.

· [5.0%] Core MoM prints below 0.25%. SPX gains 2% - 2.5%. The other tail outcome, similar to recent results from EU/UK, this would be a material dovish print. Look for the bond market to add back at least 2x 25bp rate cuts and for Equities to react positively to the bull steepening that likely ensues.

· WHAT ARE OPTIONS PRICING? Options that expire on Wednesday are showing a 1% implied move, based upon Monday’s closing prices.

· US MARKET INTEL – We think a dovish print is more likely than a hawkish print given the recent inflation prints in EU/UK; however, positioning suggests that a hawkish print will be punished more than a dovish print will be rewarded. We look for an inline/dovish print to push the market to, and through, all-time highs this week or next. A dovish print is likely to induce another squeeze for higher beta segments of the market. Longer-term, keep an eye on shipping prices and the feed-through to Core Goods, as prices have recently spiked.

BY Doug Kass · Jun 11, 2025, 6:25 AM EDT

BY Doug Kass · Jun 11, 2025, 6:15 AM EDT

The S&P Short Range Oscillator stands at 3.13% vs. 4.22% — still overbought.

BY Doug Kass · Jun 11, 2025, 6:05 AM EDT

I added to a very small Tesla TSLA short at $333.27.

BY Doug Kass · Jun 11, 2025, 5:54 AM EDT