More Overbought

BY Doug Kass · Jun 9, 2025, 4:27 PM EDT

BY Doug Kass · Jun 9, 2025, 4:27 PM EDT

BY Doug Kass · Jun 9, 2025, 4:15 PM EDT

I have two research calls between 2:30 p.m. and the close.

BY Doug Kass · Jun 9, 2025, 2:10 PM EDT

BY Doug Kass · Jun 9, 2025, 12:50 PM EDT

BY Doug Kass · Jun 9, 2025, 12:11 PM EDT

Here for Appleheads is the link to AAPL live 1 p.m. ET video stream and for all others seeking the sleep-inducing video version of Ambien.

BY Doug Kass · Jun 9, 2025, 11:43 AM EDT

Bonds at a low on the day.

BY Doug Kass · Jun 9, 2025, 10:49 AM EDT

Chart from 10:07 a.m. ET:

BY Doug Kass · Jun 9, 2025, 10:16 AM EDT

From Peter Boockvar:

Watching still the US producer response to lower prices, and they are doing what they should be doing, laying down more rigs. The Baker Hughes crude oil rig count fell by another 9 rigs over the past week and is now lower by a sizable 41 rigs in 6 weeks to 442. That's the least since October 2021. This was interesting too from a Bloomberg article this morning on oil where they quote a Morgan Stanley note with regards to OPEC, "Notwithstanding the around 1 million barrel a day increase in production quotas between March and June, an actual increase in production is hard to detect. Notably, it does not appear that production in Saudi Arabia has ramped up significantly." I'll also add, lower crude oil production will also lead to less production of natural gas as a byproduct. That said, with natural gas near $4 per btu, the natural gas rig count has jumped to 114 from about 100 in most of May.

I'll repeat my belief that oil is cheap in the low to mid $60s and we remain long a bunch of oil and gas stocks.

Crude Oil Rig Count

Natural Gas Rig Count

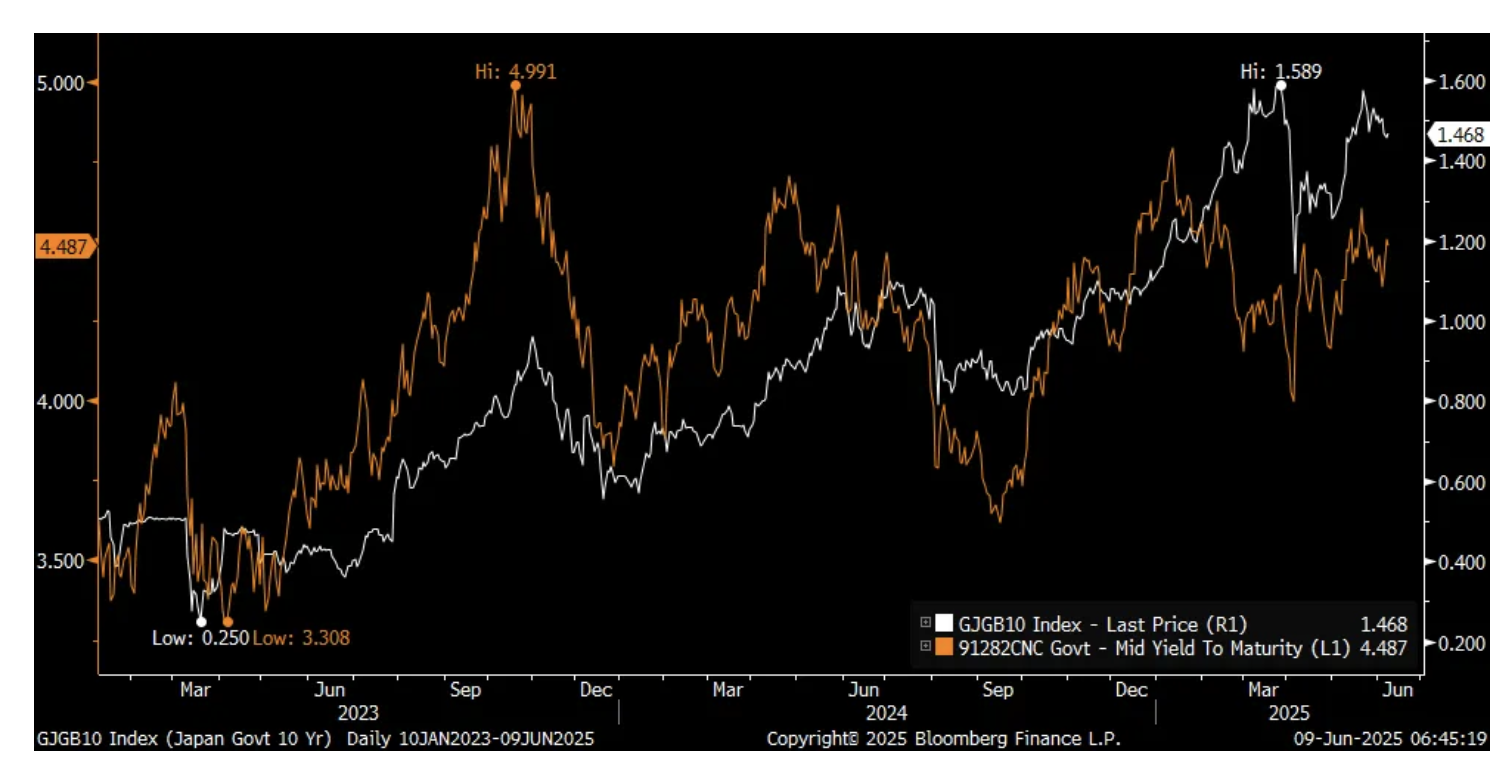

Ahead of the BoJ meeting next week we watch for any hints on what they might do with their asset purchase program of JGBs where they continue to reduce what they are buying but are becoming more sensitive to the sharp rise in yields. We've of course already got word that they are debating whether to cut back the balance sheet shrinkage but on the other hand, there was a story over the weekend that they might, as part of that, just extend into 2027 the reduction in its holdings. We also wonder if there are any talks with the US on the yen as part of any trade deal that comes. I'm skeptical though that anything comes of that.

Nikkei News reported that "The Bank of Japan, the country's biggest government bond holder, intends to continue reducing Japanese government bond purchases after April 2026, allowing interest rates to be determined more freely by the market, Nikkei has learned. The original plan to reduce JGB purchases was to last through March 2026, but that will likely be extended." JGB yields were up slightly after the recent drop, the yen is higher while the Nikkei rallied almost 1%. We continue to like and are long stocks in Japan.

I keep talking about JGB's because the BoJ was the architect of modern day extreme monetary policy with its long time experimentation of zero rates and QE that helped to suppress global interest rates, along with the help of individual country central banks post 2008. Their foot off the neck of Japanese yields beginning in 2023, along with the notable rise in global rates post 2021, matters for global rates. Especially too as Japan is still the largest foreign holder of US Treasuries. I continue to believe that the US 10 yr yield move from about 3.60% to 5% in 2023 was in reaction to the BoJ ending yield curve control.

Here's a chart of the past 2 ½ years with JGB 10 yr yield in white and US 10 yr yield in orange

A few weeks before their expected earnings release, Winnebago on Thursday lowered guidance and the stock fell 6%. We know they sell big ticket items that are discretionary and are thus challenged in the current consumer environment. This is what they said:

"What began as an encouraging selling season in March was hampered by growing macroeconomic uncertainty, resulting in worsening consumer sentiment and an increasingly cautious dealer network in the final two months of our fiscal third quarter."

"While market pressures have been observed across our portfolio, they have been most acute in our Winnebago Motorhomes business unit."

G-III Apparel Group was down 19% on Friday, the owner of DKNY, Karl Lagerfeld, and Donna Karen said this and you can assume they source product from all over the world:

"Based on incremental tariffs, we estimate the potential unmitigated tariff impact for fiscal 2026 to be approximately $135 million...We're actively working to reduce the impact through a combination of strategies, including continued sourcing diversification, vendor negotiations, selective retail price increases, disciplined inventory management, cost savings, and operational efficiencies."

I'll add this, imagine just for a second the massive management distractions and time that companies have had in dealing with all these tariffs that will most likely result in no reshoring of apparel manufacturing to the US.

They further said, "on pricing, we're actively negotiating with retailers and will selectively raise prices. With over 30 in demand brands across categories, price points, and channels, our portfolio offers strong pricing power. Consumers are willing to pay more when quality and value are clear."

Sales were down by 4.3% y/o/y. "We're cautiously optimistic about the consumer environment and we are encouraged by the health of our brands and business as we execute in the 2nd quarter and are actively taking advantage of the market disruption to further capture market share."

The Manheim wholesale used vehicle index fell 1.4% m/o/m in May, though up by 4% y/o/y. They said, "Wholesale appreciation trends were remarkably strong in April, but the market gave some of that strength back in May, though values remain well above last year's levels...The used retail days' supply remains down 5% compared to last year's levels, which is seasonally normal, as wholesale days' supply at Manheim is also currently down 5%. While the market continues to digest the impact of tariffs, we could see a bit higher level of wholesale depreciation over the summer. However, lower inventory levels may counterbalance those more aggressive depreciation trends in the coming months."

As for new car prices, they are rising in response to tariffs but not obvious to the buyer. Bloomberg had an article on Friday titled "Carmakers Use Stealth Price Hikes to Cope with Trump's Tariffs." It said, "The sticker price on a particular make and model may not have changed, at least not yet. But automakers have been quietly cutting rebates and limiting cheap financing deals, adding hundreds of dollars to buyers' monthly payments even as the companies say they're holding the line on pricing. Several have boosted delivery charges - a fee everyone must pay when buying a new vehicle - by $40 to $400 dollars, according to automotive researcher Edmunds.com Inc."

China's exports rose 4.8% y/o/y, just below the estimate of up 6% but trade with the US fell by 9.7% y/o/y, offset by a 15% rise in exports to India, a 12% increase to ASEAN countries and other parts of Asia. Exports to the EU were higher by 6.4% and by 7.4% to the UK. While China certainly needs the US market, they have diversified their customer base since 2018.

Taiwan's exports in May jumped by 39% y/o/y, well more than the estimate of 23% in another front running attempt. Exports to the US skyrocketed by 87% y/o/y.

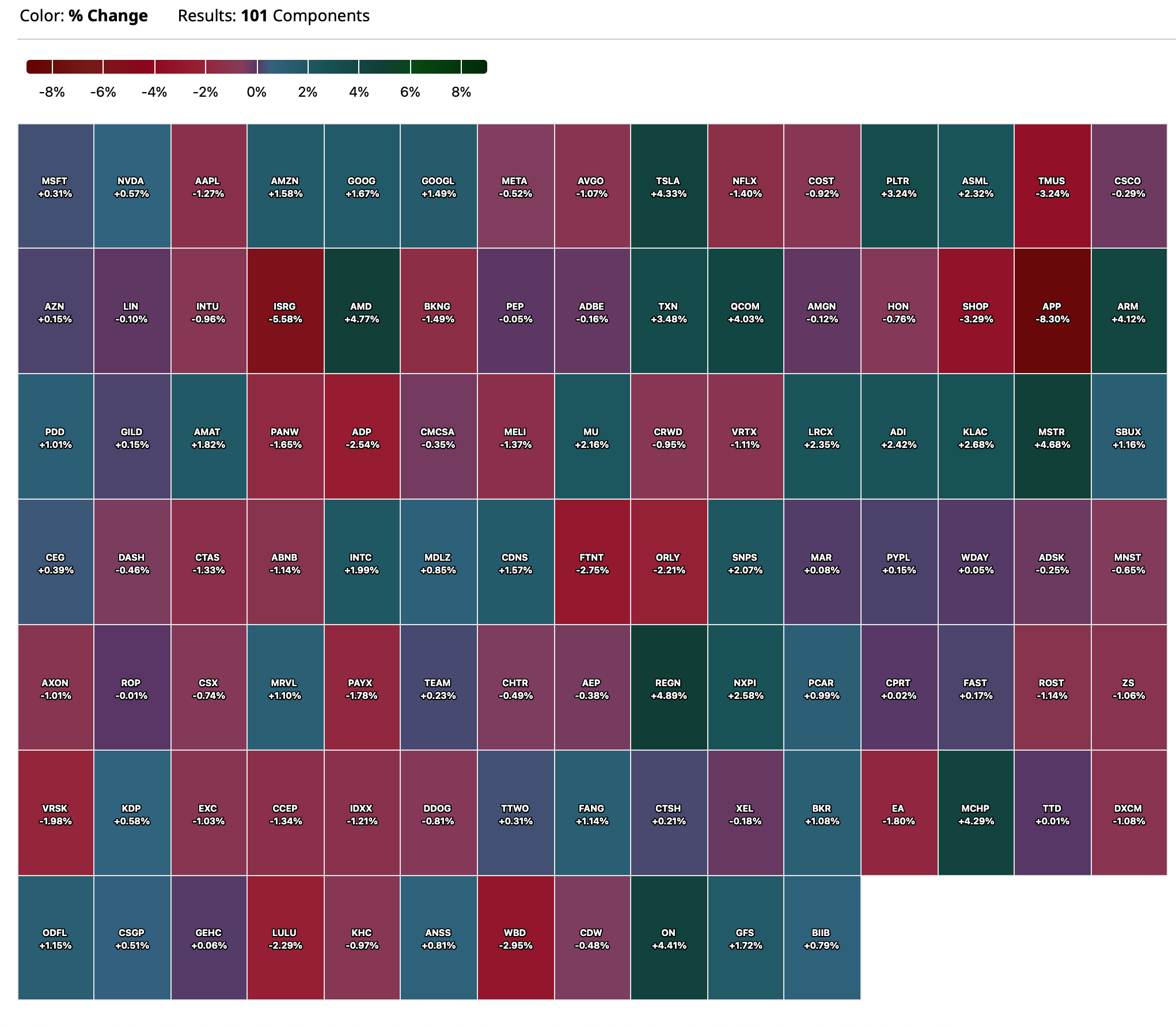

BY Doug Kass · Jun 9, 2025, 9:45 AM EDT

-MTSR +20% (reports positive Phase 1 results for MET-233i clinical trial)

-CRCL +17% (strength following IPO)

-GHM +16% (earnings, guidance)

-BLDE +14% (momentum)

-ANIX +12% (announces Poster Presentation on Ovarian Cancer CAR-T Clinical Trial at the ESMO Gynaecological Cancers Congress 2025)

-VFS +11% (earnings)

-IONQ +8.9% (to acquire Oxford Ionics in $1.075B deal to accelerate quantum roadmap; highlights results of collaborative research program with AstraZeneca, Amazon Web Services (AWS), and NVIDIA)

-WBD +7.8% (to separate into two media companies, Streaming Studios and Global Networks; guidance)

-RDW +4.1% (amends agreement for $925M Edge Autonomy acquisition)

-SYF +3.4% (OnePay and Synchrony to launch credit card program with Walmart)

-MRK +2.4% (Enlicitide meets primary and key secondary endpoints in two Phase 3 PCSK9 trials)

-NOVA -28% (to cut workforce by 55%)

-PLCE -24% (earnings)

-OPEN -12% (proposes discretionary reverse stock split of up to 1-for-50)

-SATS -11% (reportedly company considering Chapter 11 bankruptcy filing)

-ISRG -3.6% (Deutsche Bank Cuts ISRG to Sell from Hold, price target: $440)

-AXSM -3.5% (provides Update on the New Drug Application (NDA) for AXS-14 for the Management of Fibromyalgia)

-HOOD -3.5% (Redburn Atlantic Cuts HOOD to Sell from Neutral, price target: $48)

-APP -3.4% (weakness following not being added to S&P 500 Index)

-MLTX -2.3% (reportedly Merck held talks to purchase MoonLake for $3B+ (timing uncertain))

-MBLY -2.1% (Goldman Sachs Cuts MBLY to Neutral from Buy, price target: $17)

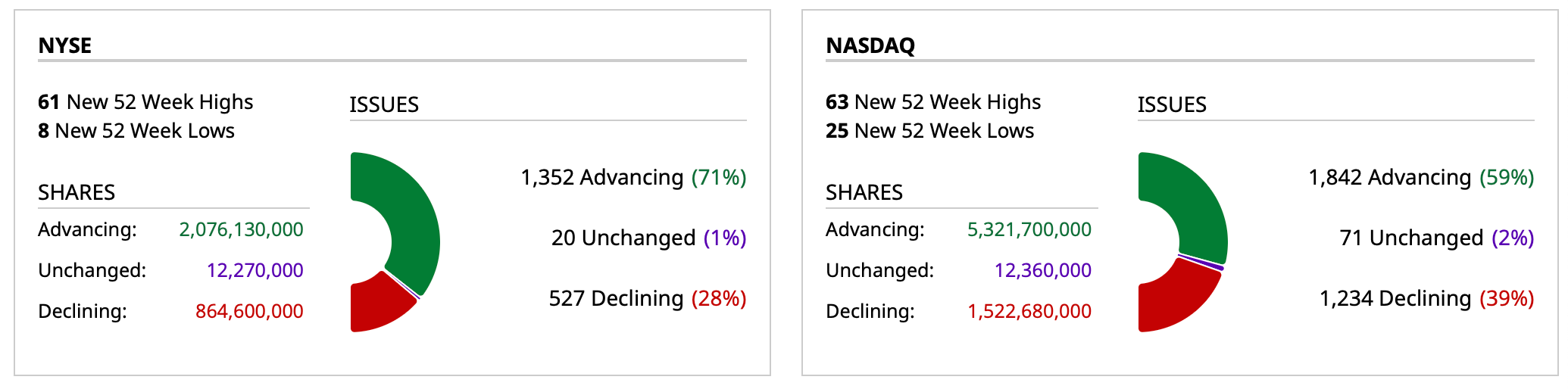

BY Doug Kass · Jun 9, 2025, 9:30 AM EDT

BY Doug Kass · Jun 9, 2025, 9:23 AM EDT

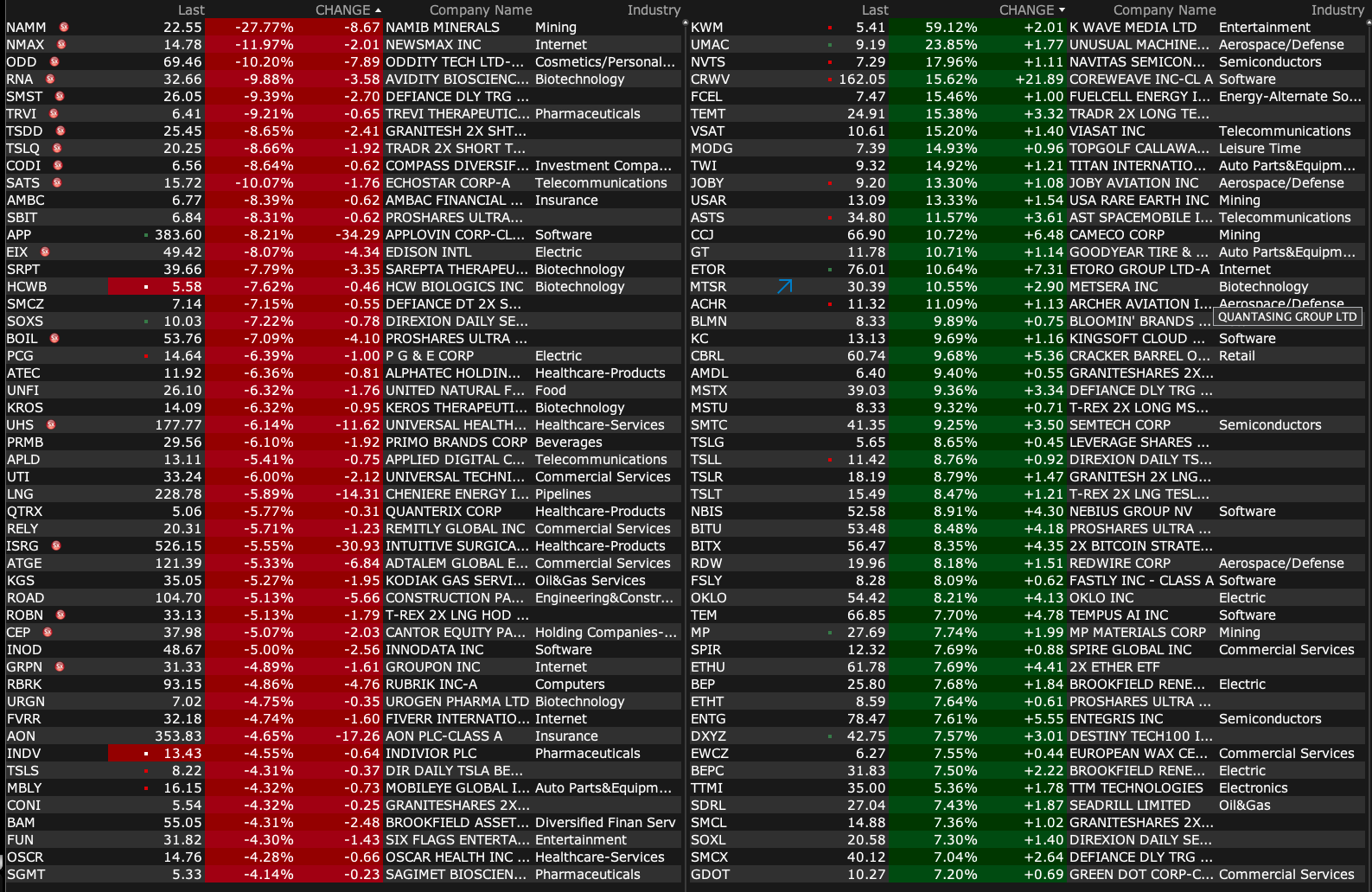

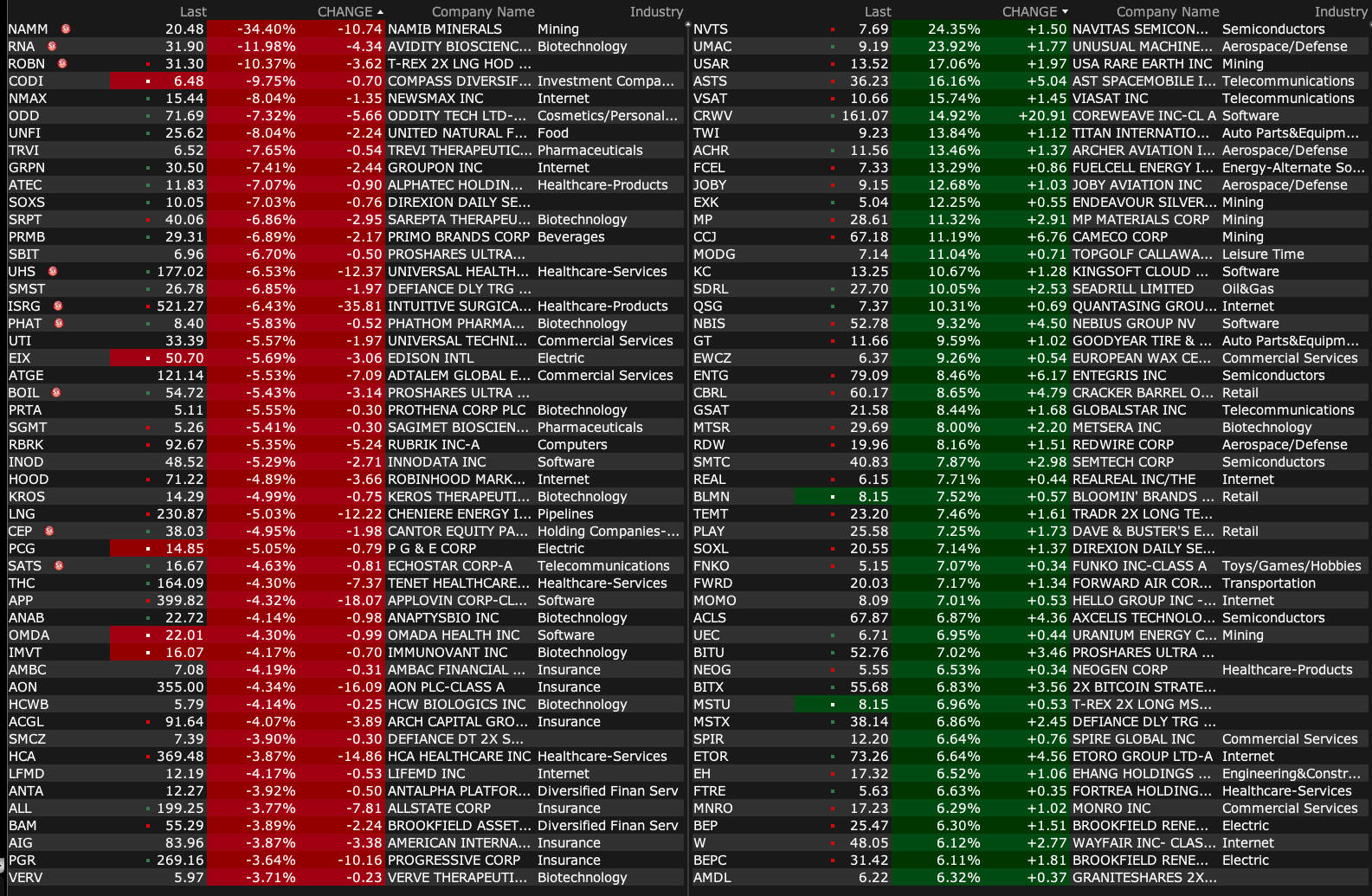

Premarket percentage movers as of 8:37 a.m. ET:

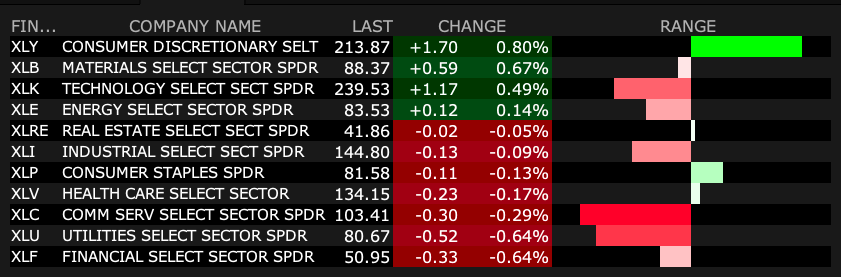

BY Doug Kass · Jun 9, 2025, 9:10 AM EDT

Most active premarket exchange-traded funds as of 8:14 a.m. ET:

BY Doug Kass · Jun 9, 2025, 8:57 AM EDT

This is a thoughtful list of (bearish) present conditions, sent to me over the weekend by my good pal David Rocker (a political independent who founded the successful hedge fund Rocker Partners). It bears reading:

- The economy is clearly slowing and earnings estimates for the S&P 500 have been declining

- Price Earnings ratios are at a historically high range

- President Trump’s pre-election claims largely unfulfilled

- Conflict between Russia and Ukraine continues and efforts to solve it alienates our ally and favors Russia

- Mideast conflict continues with no end in sight

- No Iran solution and it refuses to stop enriching

- The Administration announces huge tariffs which threaten further inflation and worsen international relations

- The Administration's claims that negotiating with major trading partners will produce favorable pacts unfulfilled

- DOGE has been a failure — minor savings at great social cost which alienates many including many Republicans

- President Trump's personal support from swing voters that got him elected (women, Latinos, blacks) reversing

- The Big Beautiful Bill will worsen deficits and losing support

- Relentless attacks on law firms and the legal system

- Relentless attacks on major universities which are the envy of the world and key to many scientific advances

- Relentless efforts to force the Fed to lower rates

- Firing of many regulators who could challenge President Trump's programs

- Vitriolic breakup with Musk, the President's chief financier

- Continued attempts to disregard legal rulings made against the Administration's program

- Worsening relationships with U.S.'s historical allies, weakening our influence:

* Resulting in worldwide loss of confidence in the United States

* The U.S. credit rating is downgraded

* The U.S. dollar falls 8%, worsening the purchasing power of Americans and making foreign investors wary about financing our deficit

* University attacks leading capable foreign students to consider studying elsewhere than in the U.S.

* Tourism declining

Yet stocks are at a high level and the market reacts briefly and modestly to real negative setbacks but grows vigorously stronger to rumors to talks and future meetings.

It seems that nothing can go wrong — as traders and investors buy the dip...

Until it doesn't.

BY Doug Kass · Jun 9, 2025, 7:57 AM EDT

Adding to index shorts:

* SPY $600.21

* QQQ $530.45

BY Doug Kass · Jun 9, 2025, 7:50 AM EDT

Bonus — Here are some great links:

Musk vs. Trump Showdown, Silver Breakout

BY Doug Kass · Jun 9, 2025, 6:25 AM EDT

BY Doug Kass · Jun 9, 2025, 6:15 AM EDT

Robinhood HOOD was not added to the S&P 500 Index on Friday night.

As posted on the Comments Section, I shorted HOOD at $80 and covered under $75.

BY Doug Kass · Jun 9, 2025, 6:05 AM EDT

Baird downgrades Tesla TSLA.

BY Doug Kass · Jun 9, 2025, 5:55 AM EDT

The S&P Short Range Oscillator moved further into overbought territory, rising from 2.2% to 3.26%.

BY Doug Kass · Jun 9, 2025, 5:45 AM EDT