I am invested heavily in longer dated treasuries 10 ish years as an intermediate trade - if I am wrong, I can always make them a permanent investment because I am 64 and the coupons provide walking around money I do not need sell them if I am all wrong about my trade. However,

Jamie Dimon believes the bond market will crack - I believe he is likely to be correct, but I see that in more in years, not months - that is the treasury market. The corporate markets is different.. I think spreads will widen when the economy as we see now, is slowing down + there are credit events looming in commercial real estate and consumer credit and so on

The government spending bill that will be passed will in my view still be excessive in my view but not stimulative to the economy - If you take something simple as John Maynard Keynes k = 1/ 1−c1 so that ΔY=k⋅ΔG so that there is a multiplier effect of repeated consumption rounds - note that he uses Deltas - in his formulation. There. will be no positive stimulative delta in government spending for consumers in the next year - I see negative consumer deltas not positive .

This in addition to this, monetary policy is not stimulative either.

My view is the second half of the year will present hiccups in both growth earnings that will lead bonds treasury rates dropping as investors swap out of stocks

-My plan would then be to allocate to stocks as they become more reasonable priced. That said, I agree with Jamie Diamond, that we are kind of screwed on treasuries if you look further out - because Government debt is not controllable in the foreseeable future.

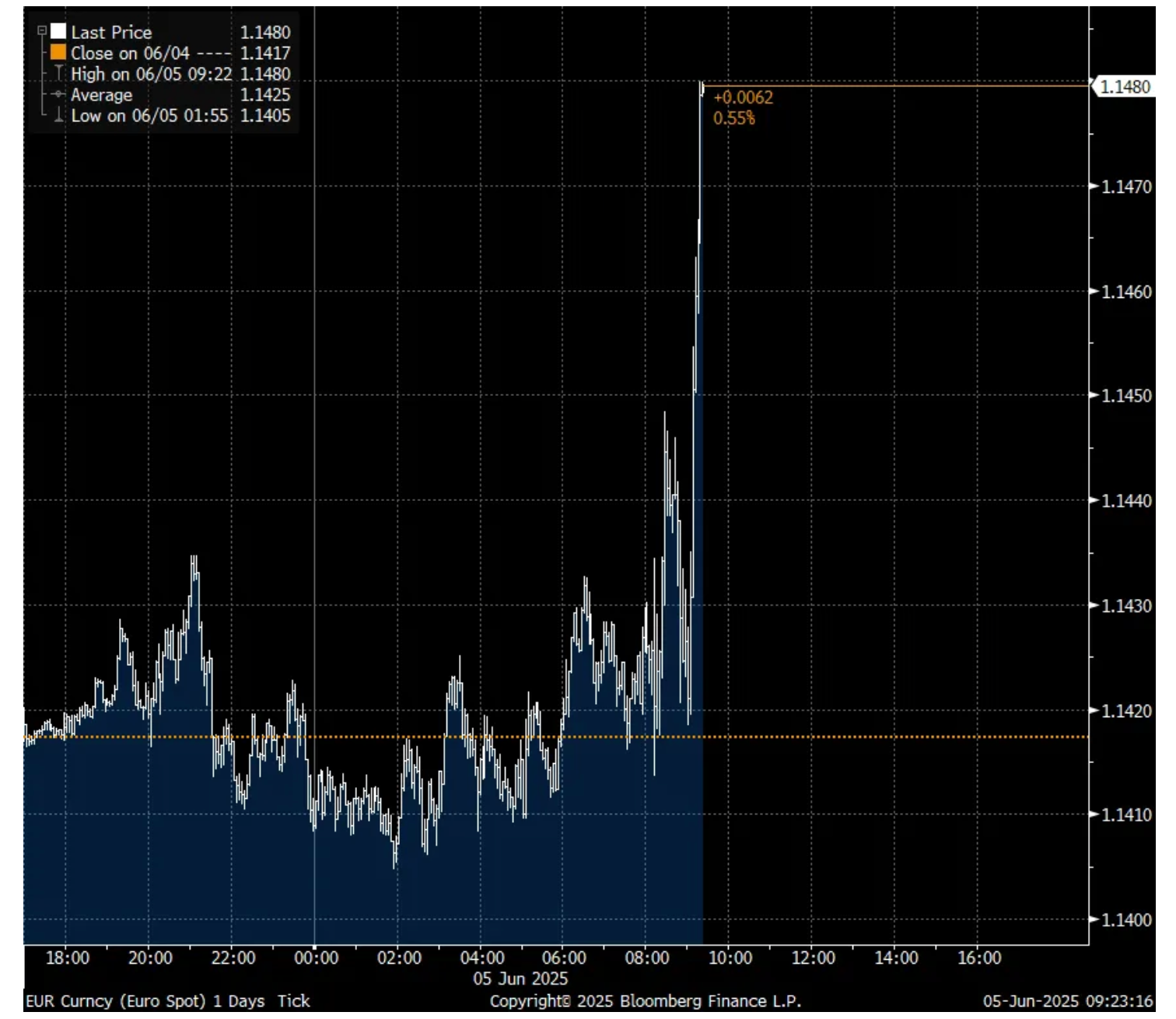

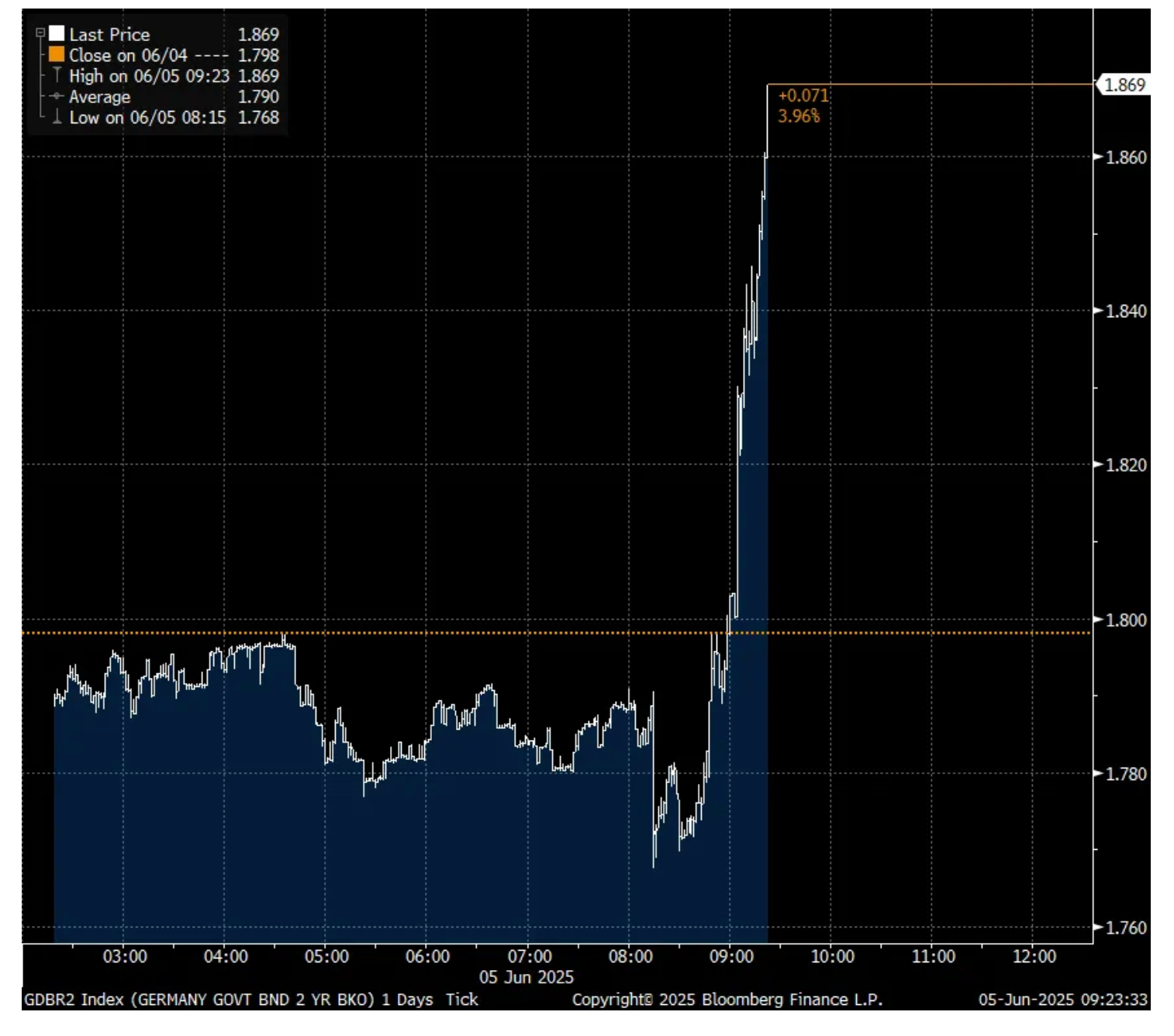

One more thing: Lagarde speaks, euro, bond yields at high of morning

In her press conference ECB president Christine Lagarde just said that they are near the end of their rate cutting cycle under the current circumstances. European bond yields are higher in response as is the euro.

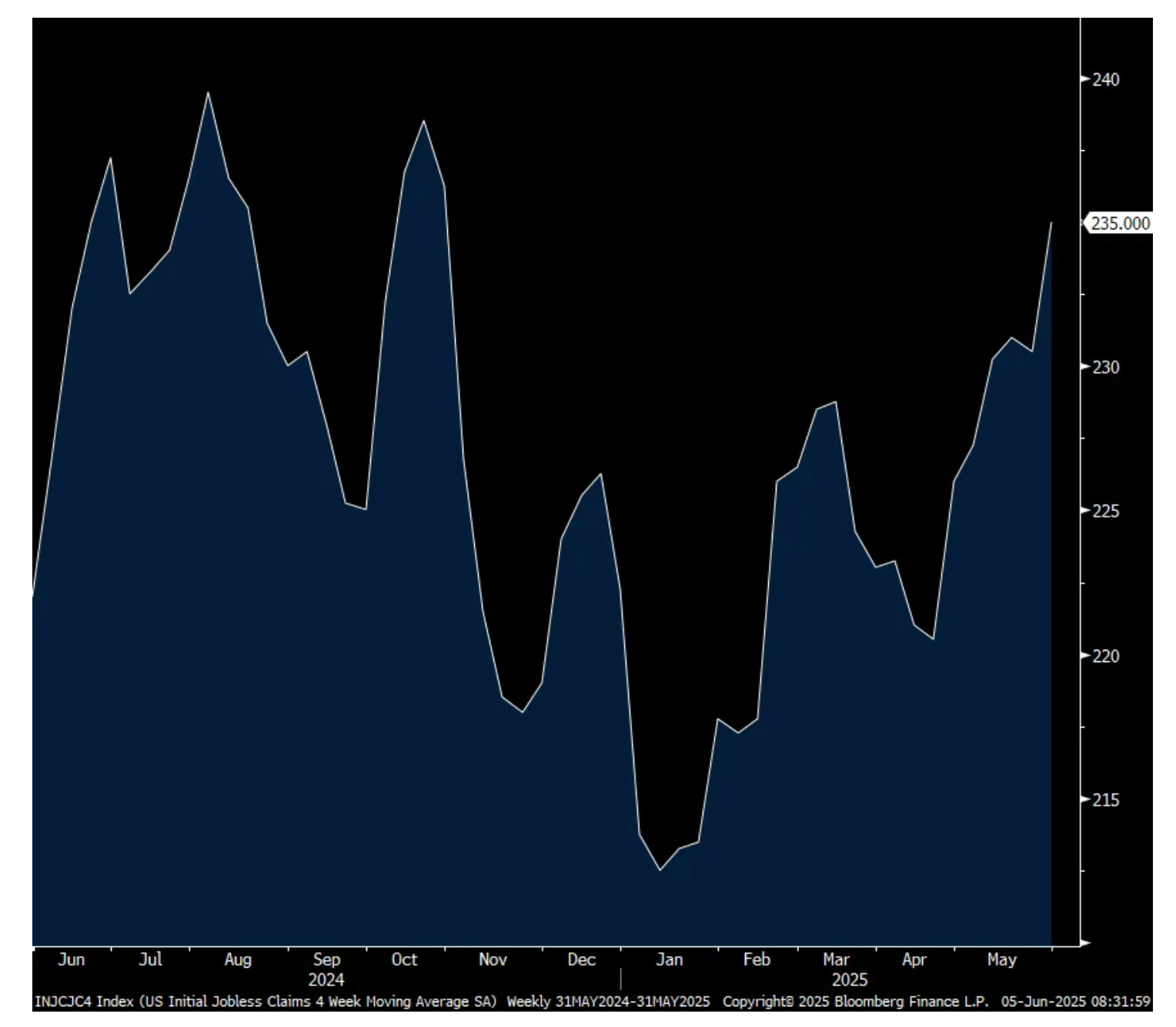

For the 2nd week in a row initial jobless claims popped above expectations. For the week ended May 31st they totaled 247k, 12 more than expected and follows 239k last week (revised down by 1k). The 4 week average shifted up to 235k from 231k and that is the most since late October. Continuing claims were 1.904mm, about as forecasted and down 3k w/o/w but still around the highest since November 2021.

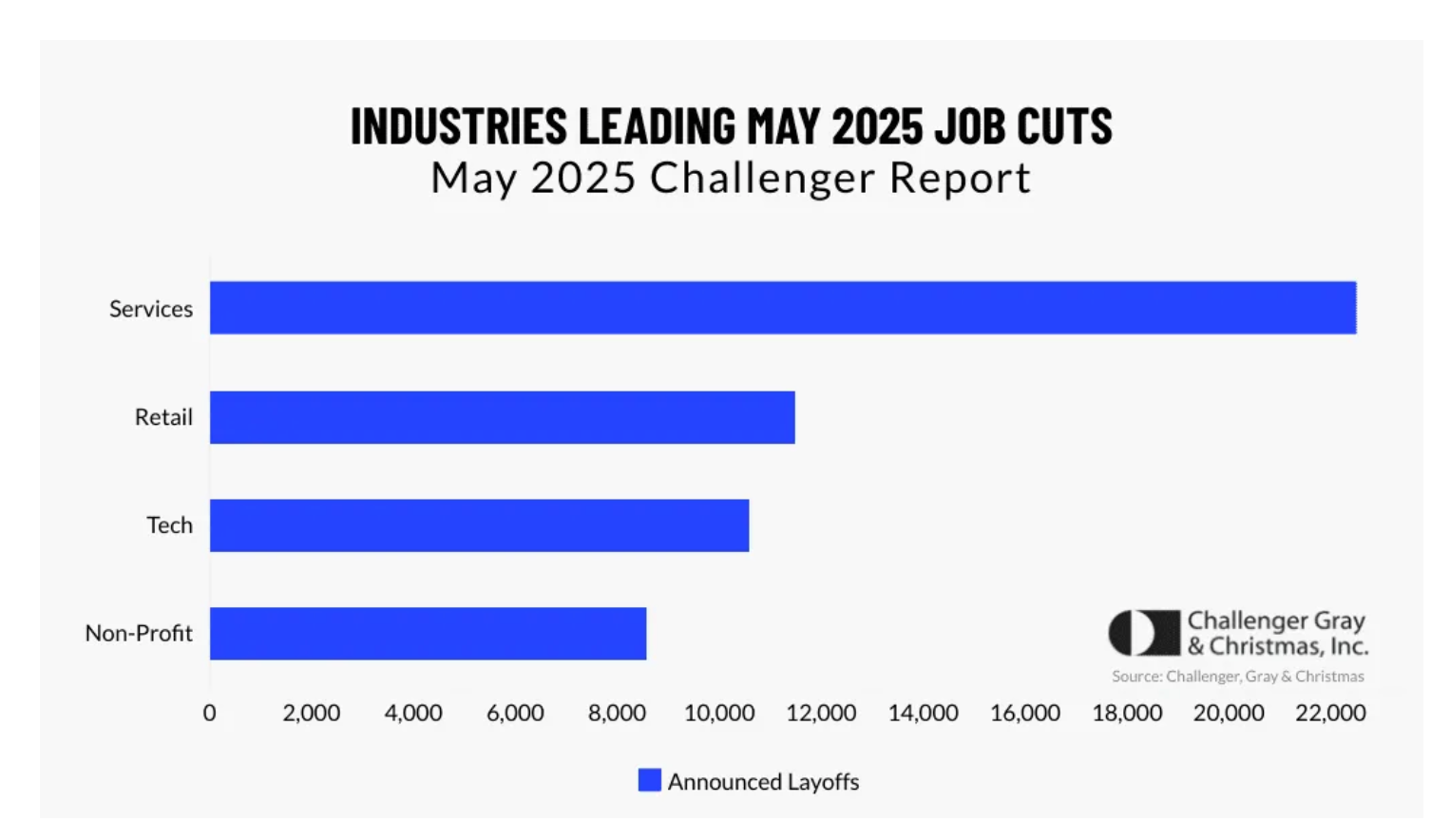

Also, Challenger reported its monthly job cut/hire data and said job cuts were up by 47% y/o/y. They said, “Tariffs, funding cuts, consumer spending, and overall economic pessimism are putting intense pressure on companies’ workforce. Companies are spending less, slowing hiring, and sending layoff notices.”

Challenger said the ‘DOGE Impact’ “remains the leading reason for job cut announcements in 2025.” The second reason cited, “market and economic conditions” followed by “closings of stores, units, or plants.”

On the flip side, hiring plans did increase by 57% y/o/y but said Challenger, “it remains historically low when compared to pre-pandemic and early-pandemic years.”

Here again is what the Fed’s Beige Book said about the labor market, “Employment has been little changed since the previous report. Most Districts described employment as flat, three Districts reported slight-to-modest increases, and two Districts reported slight declines…Comments about uncertainty delaying hiring were widespread. All Districts described lower labor demand, citing declining hours worked and overtime, hiring pauses, and staff reduction plans. Some Districts reported layoffs in certain sectors, but these layoffs were not pervasive.”

From the Challenger press release

4 week avg Initial Claims

The April trade deficit plunged to $61.6b because of a 16.3% collapse in imports, well more than offsetting the 3% rise in exports. The estimate was $66b and down from $138b in March.

My advice is to smooth out all the lumpiness in the tariff induced distortions in the economic data and average Q1 and Q2 data. So if Atlanta Fed is right (still another month left in the quarter, along with revisions to the previous ones) and Q2 GDP comes in at 4.6%, combined with the .2% contraction in Q1, the first half growth would average 2.2%.

I just concluded a very good phone call with President Xi, of China, discussing some of the intricacies of our recently made, and agreed to, Trade Deal. The call lasted approximately one and a half hours, and resulted in a very positive conclusion for both Countries. There should no longer be any questions respecting the complexity of Rare Earth products. Our respective teams will be meeting shortly at a location to be determined. We will be represented by Secretary of the Treasury Scott Bessent, Secretary of Commerce Howard Lutnick, and United States Trade Representative, Ambassador Jamieson Greer. During the conversation, President Xi graciously invited the First Lady and me to visit China, and I reciprocated. As Presidents of two Great Nations, this is something that we both look forward to doing. The conversation was focused almost entirely on TRADE. Nothing was discussed concerning Russia/Ukraine, or Iran. We will inform the Media as to scheduling and location of the soon to be meeting. Thank you for your attention to this matter!

Productivity is one of the most important drivers of economic growth. With all the AI, why is productivity tanking? Not a great start with regards to getting to 10% growth in the economy with 10-20% unemployment, and curing cancer:

"Nonfarm business sector labor productivity in the United States fell by 1.5% in Q1 2025, compared to the preliminary estimate of a 0.8% decrease and following a 1.7% rise in the previous period. It was the first decline in productivity since Q2 2022."

Boockvar on (Lack of) Growth, Tariff Response, Metals

From Peter Boockvar:

Doesn't sound like much growth/Tariff response/Container prices spike/Silver and platinum breaking out/Value, Value, Value winning

I'm sorry but this just doesn't sound like an economy that is seeing much growth. From the Fed's Beige Book yesterday in describing their view of the US economy, "Reports across the twelve Federal Reserve Districts indicate that economic activity has declined slightly since the previous report. Half of the Districts reported slight to moderate declines in activity, three Districts reported no change, and three Districts reported slight growth."

And we can understand why, "All Districts reported elevated levels of economic and policy uncertainty, which have led to hesitancy and a cautious approach to business and household decisions."

Specifically, "Manufacturing activity declined slightly. Consumer spending reports were mixed, with most Districts reporting slight declines or no change; however, some Districts reported increases in spending on items expected to be affected by tariffs. Residential real estate sales were little changed, and most District reports on new home construction indicate flat or slowing construction activity. Reports on bank loan demand and capital spending plans were mixed."

Not surprisingly with all the front running around tariffs, "Activity at ports was robust, while reports on transportation and warehouse activity in other areas were mixed."

Lastly in their summary section, "On balance, the outlook remains slightly pessimistic and uncertain, unchanged relative to the previous report. However, a few District reports indicate the outlook has deteriorated while a few others indicate the outlook has improved."

Ahead of tomorrow's payroll report and post the soft ADP one seen yesterday, "Employment has been little changed since the previous report. Most Districts described employment as flat, three Districts reported slight-to-modest increases, and two Districts reported slight declines." And then this, "Comments about uncertainty delaying hiring were widespread. All Districts described lower labor demand, citing declining hours worked and overtime, hiring pauses, and staff reduction plans. Some Districts reported layoffs in certain sectors, but these layoffs were not pervasive."

On the cost pressure side from tariffs, "There were widespread reports of contacts expecting costs and prices to rise at a faster rate going forward. A few Districts described these expected cost increases as strong, significant, or substantial. All District reports indicated that higher tariff rates were putting upward pressure on costs and prices."

And how are companies responding to this?, "contacts' responses to these higher costs varied, including increasing prices on affected items, increasing prices on all items, reducing profit margins, and adding temporary fees or surcharges. Contacts that plan to pass along tariff-related costs expect to do so within three months."

All sounds like a tough spot for the Fed, though I expect a few rate cut tweaks by year end.

The NY Fed yesterday released its survey of tariffs and how companies are responding. They said, "about three-quarters of businesses facing tariff induced cost increases in both the manufacturing and service sectors passed along at least some of these higher costs to their customers by raising prices. Almost a third of manufacturers and about 45% of service firms reported fully passing along all tariff-related cost increases, while 45% of manufacturers and a third of service firms said they passed along some but not all of the cost increase."

"At the other end of the spectrum, roughly a quarter of both types of firms said they absorbed all tariff-related cost increases and were not raising their prices."

And how quickly are companies responding to the tariff taxes? "Price increases happened rapidly: over half of both manufacturers and service firms said they raised prices within a month of experiencing tariff related cost increases - many within a day or week. Another quarter indicated they had raised prices (or planned to do so) within one to three months of such cost increases, while few were waiting longer than three months."

Container rates exploded higher this past week and are up now 5 weeks in a row in the rush to procure whatever is needed. The Shanghai to LA container price spiked 57% w/o/w, by $2,138 to $5,876. The Shanghai to NY journey will now cost you $7,164, up 39% w/o/w, by $1,992.

Shanghai to LA

Shanghai to NY

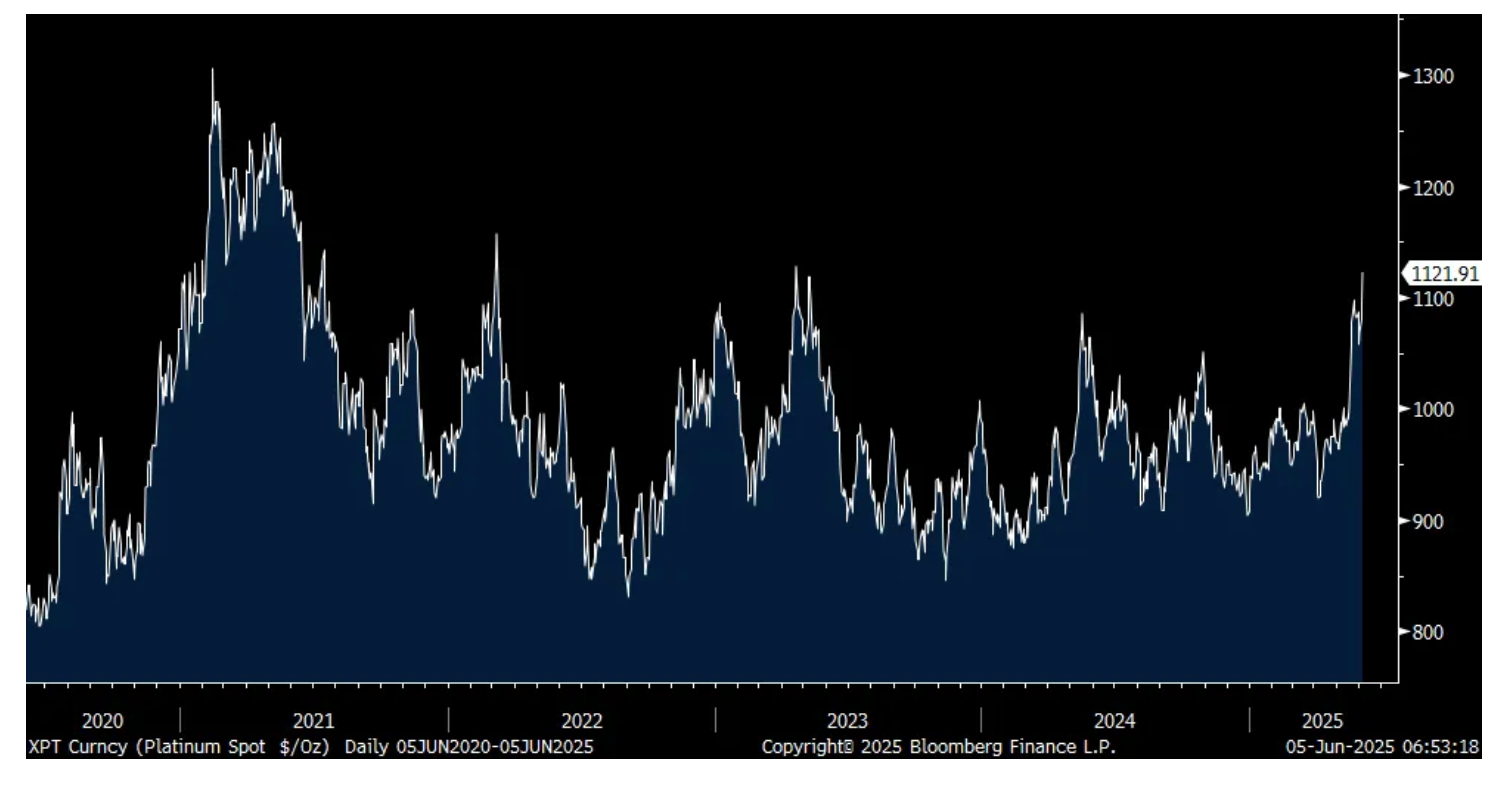

Last month I mentioned my bullish and long stake in platinum. Today the price is jumping to the highest level since April 2023. Silver too has busted out to a 13 yr high and we remain bullish and long. Both are finally playing some catch up to the move higher in gold. And with platinum, hybrids are winning the EV race and hybrids use as much, if not more platinum and palladium, in its cars than internal combustion engine vehicles.

Platinum

Silver

JGB yields fell overnight as Reuters reported that "The Bank of Japan is considering slowing the pace of tapering in its bond purchases from next fiscal year onward, said four sources familiar with its thinking, a move that would signal its focus on avoiding big bond market disruptions." I did see this story yesterday and wouldn't be surprised if it was a factor in the drop in US yields. The BoJ though can't rest easy as the April wage data continues to be good with base pay rising by 2.2% y/o/y but REAL wages are still falling with inflation running higher than that.

China's May private sector services Caixin PMI rose a touch to 51 from 50.7 and as expected. Caixin said, "Overall sentiment remained positive in the Chinese service sector midway through the 2nd quarter of 2025. Firms were hopeful that improvements in global trade conditions and business development plans could help to spur sales and boost activity levels over the next 12 months. The level of confidence strengthened since April, but remained below average."

The Bank of Canada said this in their statement after holding rates steady yesterday and why they stood pat, "Recent surveys indicate that households continue to expect that tariffs will raise prices and many businesses say they intend to pass on the cost of higher tariffs. The Bank will be watching all these indicators closely to gauge how inflationary pressures are evolving."

The bottom line from them on doing nothing, "With uncertainty about US tariffs still high, the Canadian economy softer but not sharply weaker, and some unexpected firmness in recent inflation data, Governing Council decided to hold the policy rate as we gain more information on US trade policy and its impacts."

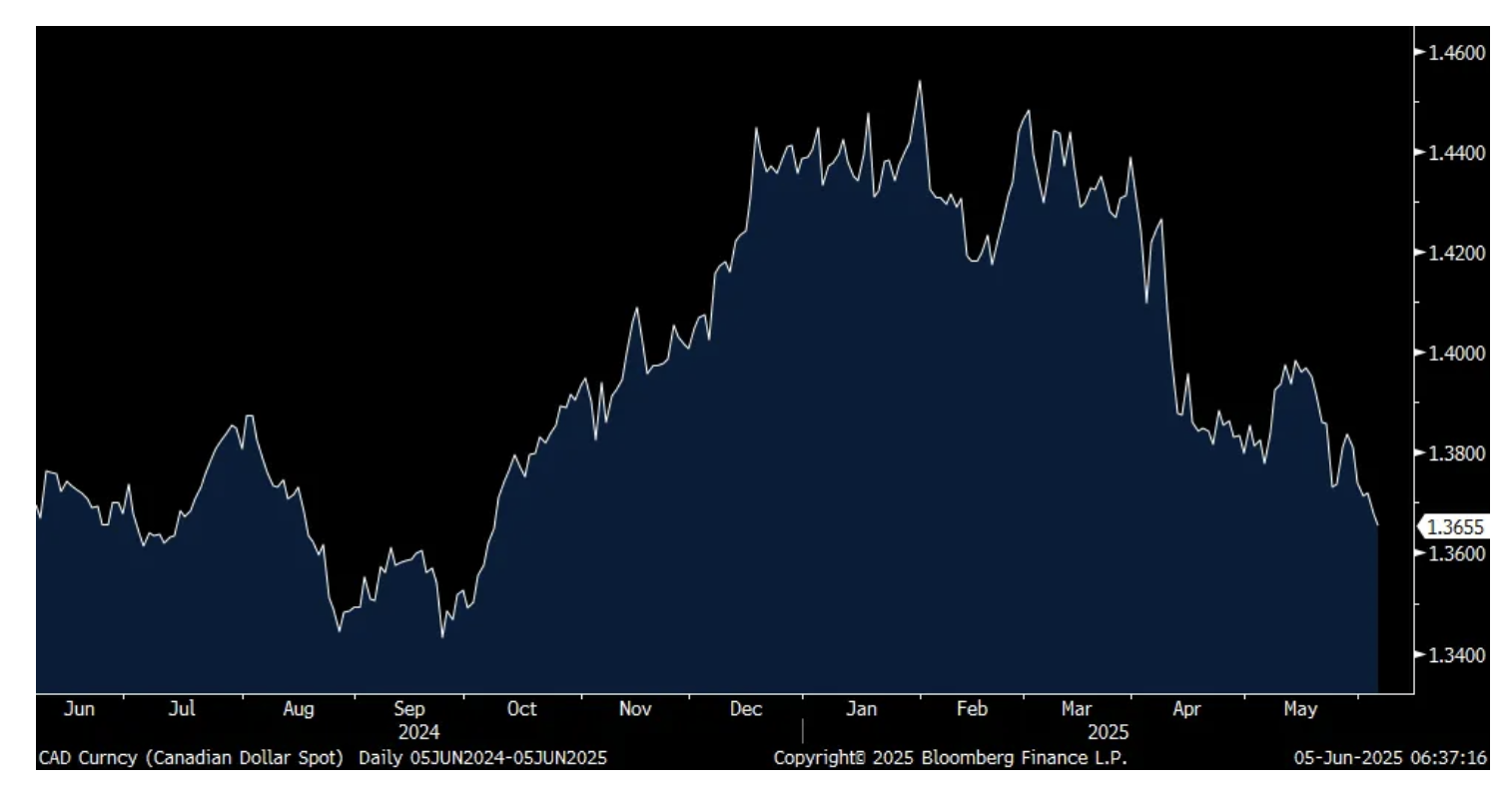

The rally in the Canadian dollar over the past few days has it at the highest level vs the US dollar since October 2024.

Canadian$

To some earnings comments.

From Dollar ($1.25) Tree:

"Dollar Tree's 5.4% comp was nicely balanced with traffic up 2.5% and ticket up 2.8%. Category performance was strong across the board with consumables comp up 6.4% and discretionary comp up 4.6%, our highest discretionary comp since Q4 of 2022."

"Each week, more shoppers across a diverse range of economic and demographic backgrounds are responding to the appeal of Dollar Tree's unique value, convenience, and discovery proposition...New customers and increasing trip frequency are both driving share gains."

"Trade-in trends remains strong as we attract customers from other retail channels. In recent quarters, higher income customers have been a meaningful growth driver for us. In Q1, we had measurable sales improvement across all income levels, with the most growth coming from our higher income customers. In particular, we saw a meaningful traffic increase from customers with household incomes of more than $100,000, demonstrating Dollar Tree's broad appeal." I bolded for emphasis.

Finally and why they are getting more customers, "In the current environment, our low prices and smaller pack sizes are perfect for families trying to manage a tight household budget, and our expanded assortment is attractive to all customers across every income level."

Dollar General said similar things.

From Five Below, another discounter:

Their comps grew 7.1% and via increased transactions of 6.2% and comp ticket of .9%. Their strategy, "Providing fresh, trend-right, and quality products at amazing value is what we are known for and what makes us special."

How are they dealing with tariffs? "Our plans include vendor negotiations, diversification of sourcing, continued investment in new value-packed products, as well as assortment and pricing adjustments with a focus on reducing the number of price points."

And value, as we clearly know, resonates. "We also refocused on value and ensured that we had really great outstanding value and relevant value and relative value in the marketplace that the customers have definitely reacted to."

Big ticket items though continue to be challenged and this is what Thor Industries had to say, the maker of RVs and such:

"We expect the fourth quarter of our fiscal 2025 and the first quarter of our fiscal 2026 to be challenging. The current economic uncertainty has led to downward pressure on consumer confidence and has negatively impacted retail pull-through."

They still had a decent quarter but "margin pressures persist as we continue to manage through softer retail and wholesale demand in our North American Motorized and European segments."

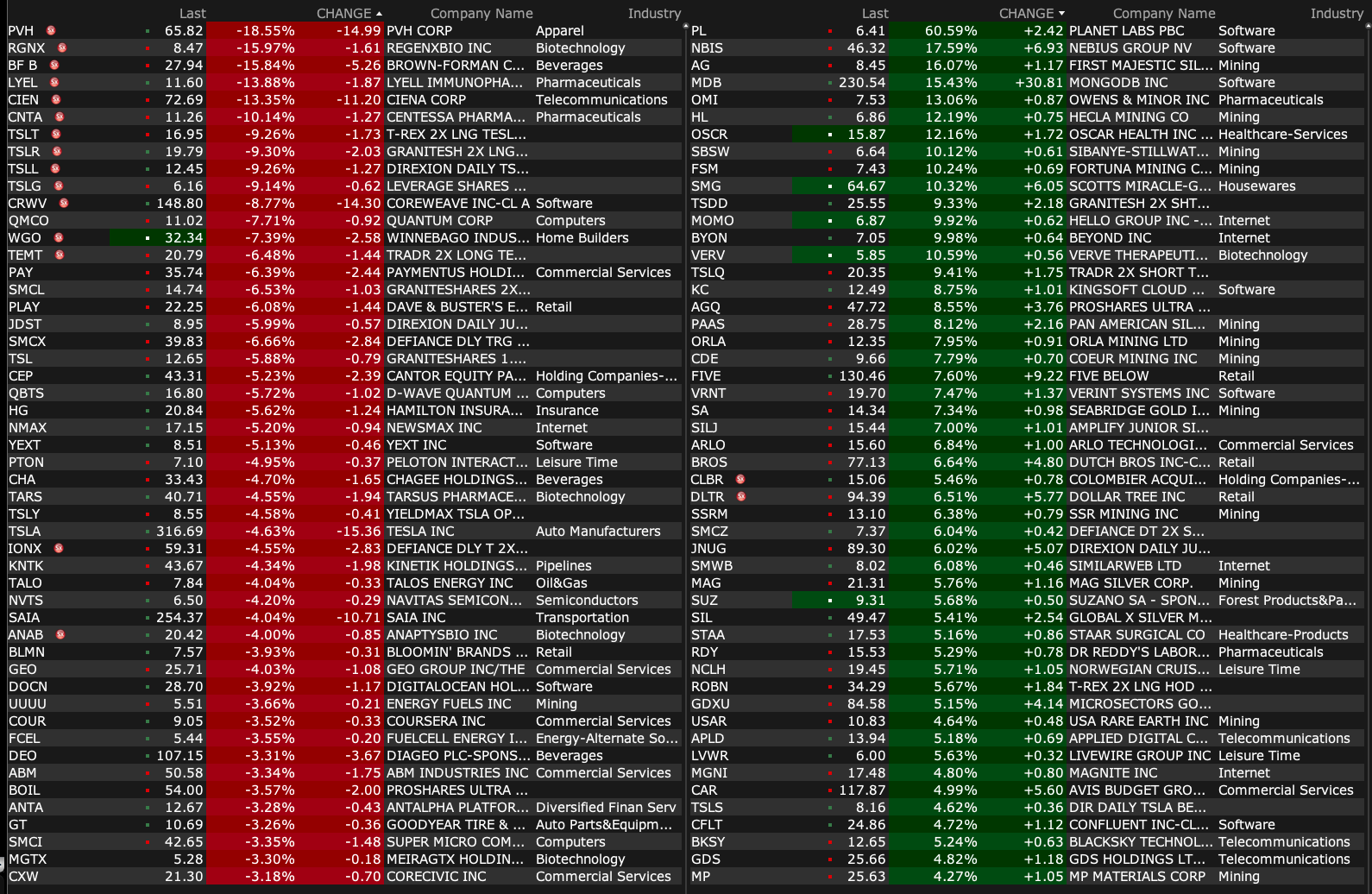

PVH is down sharply pre market as they lowered earnings guidance, though reaffirmed the top line as "We are navigating a highly dynamic and uncertain macroeconomic environment that is impacting our industry, our consumers, and our business results."

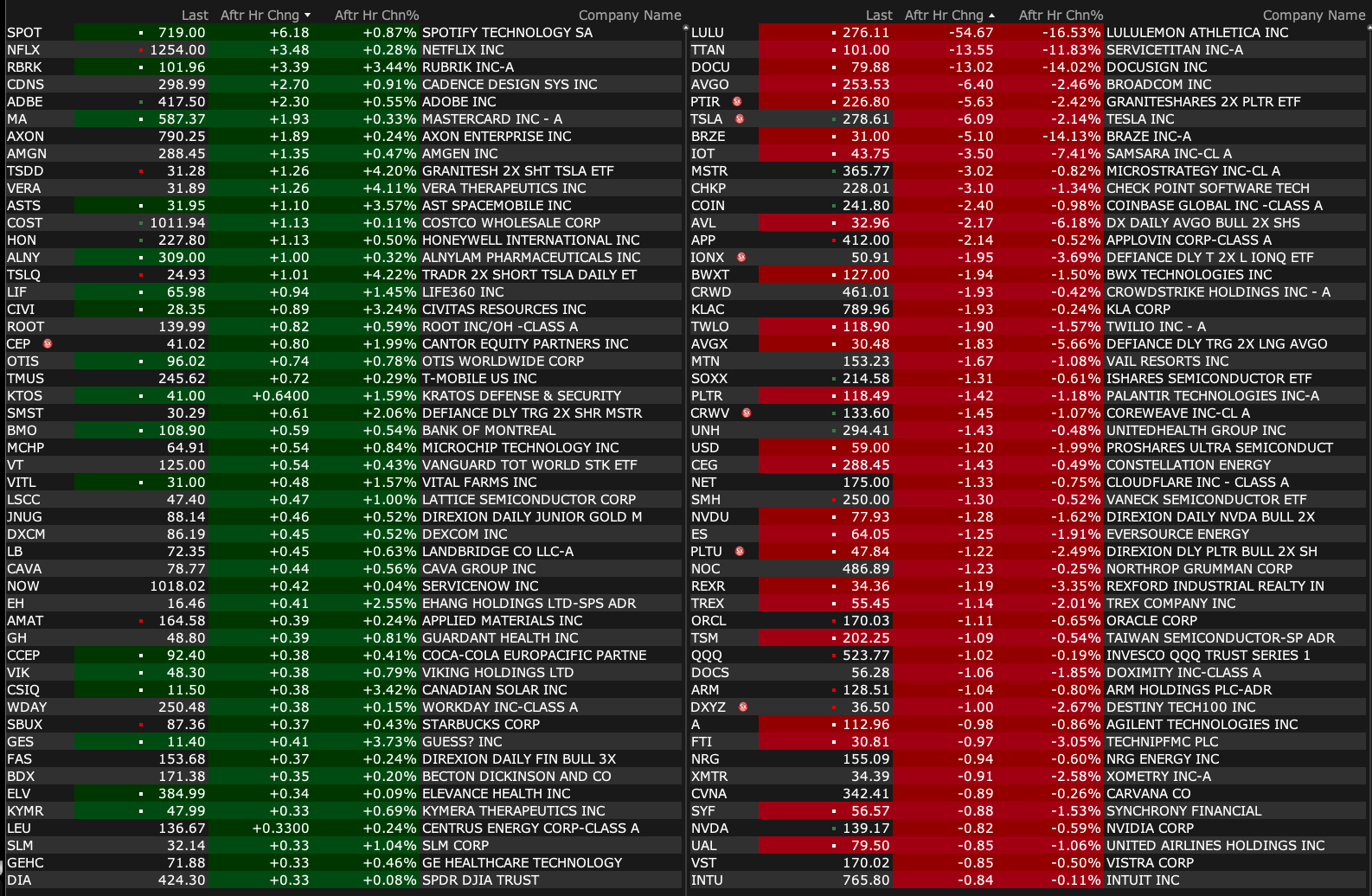

-BW +19% (agrees to sell Its Diamond Power International Business to Austria-based ANDRITZ for $177M)

-MDB +17% (earnings, guidance)

-DLTH +10% (earnings, guidance)

-FIVE +9.9% (earnings, guidance; partners with Uber Eats)

-MAIA +8.0% (median overall survival (OS) from ateganosine (THIO) treatment extends to 17.8 months in latest data from Phase 2 THIO-101 Clinical Trial in Non-Small Cell Lung Cancer)

-CBRL +4.0% (earnings, guidance)

-WDH +3.3% (earnings)

-LE +2.7% (earnings, guidance)

Downside:

-FUFU -14% (earnings)

-PVH -9.1% (earnings, guidance)

-WGO -8.4% (cuts guidance)

-CIEN -5.2% (earnings)

-CHWY -3.1% (Jefferies Cuts CHWY to Hold from Buy, price target: $43)

-TSLA -3.0% (downside momentum)

-TTC -2.7% (guidance)

-WEC -2.2% (files to sell offering of $700M of Convertible Senior Notes due 2028)

AMD Intrigues, Job Insecurity Looms, Beige Book Flashes ... Yellow

It could have gotten ugly, one might have thought. The information started trickling out on Wednesday morning. It certainly wasn't pretty. There was no bouquet of flowers tossed down from on high to brighten the mood. There would be no aroma of freshly baked bread wafting across the street to disguise the wretched stench of decay. There would be no knight in shining armor that could arise from the shadows to defend the citizenry from their fears. Still, as the numbers hit publication... as viewpoints expressing pessimism spread ... equity markets hung in there, supported by demand for debt securities that suppressed yields. That suppressed interest rates. So, it was. So now, it has been written.

Suddenly, after a spate of negative reports had taken stocks down from their early morning and mid-morning highs, bond traders started buying U.S. Treasuries. On Wednesday, the U.S. Ten-Year Note, our nation's benchmark debt security, went out paying just 4.36%, down 11 basis points for the day. The Two-Year Note yielded just 3.88% (-8 bps) by day's end. The prospect for lower interest rates going forward allowed stocks to breathe and hold their levels on a day that they might otherwise have suffered a bout of profit taking. Just a day after investors had seen the S&P 500 technically confirm last Thursday's bullish change of trend.

Friday's Bureau of Labor Statistics Employment Report for May could still turn markets on their ear, Or not. The "big, beautiful bill" could pass. Or not. Talks between Pres. Trump and China's Pres. Xi could go well. Or not. Heads on a swivel, gang. Two sources of water. Clean socks. Full battle rattle. What impacted the markets on Wednesday? What's about to impact our marketplace? Let's go...

Private Sector Job Creation

Uh oh. On Wednesday morning, the ADP Report on private sector hiring for May showed just 37,000 jobs created during the month. This was the fewest jobs shown as having been created by this report for any single month in more than two years. This shows a deceleration from April's creation of 60,000 private sector jobs and badly missed the consensus view for 110,000 jobs created. This does not necessarily mean that Friday's Bureau of Labor Statistics print will be weak, but it could. Anything this ugly on Friday will not pass unnoticed by investors.

Services Economy Contracts

The ISM Non-Manufacturing Index hit the tape at 49.9 (50 is the line in these surveys between expansion and contraction), just a few days after the ISM Manufacturing Index had crossed the tape at 48.5. The real worry for May is the component labeled "New Orders," which is the single most important item in any business survey. For the month New Orders printed at 46.4 for Services and 47.6 for Manufacturing. That's nasty.

Inventories and Backlogged Orders both also showed decay. Didn't anything show expansion? Oh, you bet your tail something did. Inflation did. Prices printed at a red hot 68.7 for the services economy and a white hot 69.4 for the manufacturing economy. Does that mean that we'll see reacceleration of consumer level inflation for May? I would think this is likely. We'll almost certainly see that producer level inflation has come back to life.

The Beige Book

The Federal Reserve released their Beige Book on Wednesday afternoon. The Beige Book, for the new kids, is a central bank publication containing anecdotal economic information from across the Fed's 12 regional districts, released eight times a year ahead of policy decisions. The Fed will make its next decision on monetary policy on June 18.

On overall economic activity: "Reports across the 12 Federal Reserve Districts indicate that economic activity has declined slightly since the previous report. Half of the Districts reported slight to moderate declines in activity, three Districts reported no change, and three Districts reported slight growth."

New York... "Economic activity in the Second District continued to decline modestly amid heightened uncertainty."

Philadelphia... "Business activity declined modestly in the current Beige Book period, as it did in the last period."

Minneapolis... "The District contracted slightly overall."

Kansas City... "Overall activity declined moderately, driven by lower retail spending, a decline in the demand for single-family homes, and a slight contraction in manufacturing."

San Francisco... "Economic activity slowed slightly."

Elsewhere, Richmond, Atlanta and Chicago reported slight expansion, while Dallas, Cleveland and St. Louis reported no change in business activity.

Fed Funds Futures

Fed Funds Futures markets trading in Chicago are now pricing in a 76% probability for a quarter-point rate cut on Sept. 17 and a 54% likelihood for another quarter-point rate cut on Oct. 29. That would be it for the year. Two more rate quarter-percentage point cuts are currently being priced in for 2026.

Dollar Index Trades Lower

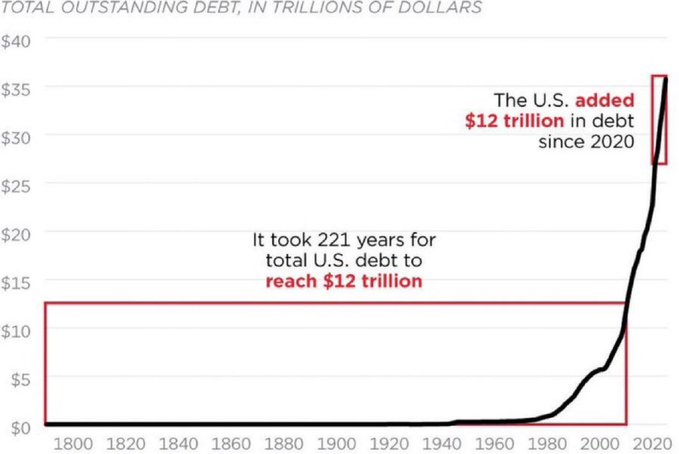

The Congressional Budget Office, which is non-partisan, but not always correct, assessed the president's "big, beautiful bill" and reported on Wednesday its expectation that over 10 years the bill, if passed into law, would increase deficits by $2.4 trillion. There is a real concern over passage in the Senate now, with a number of fiscal conservatives fretting that the budget cuts in the bill don't go far enough and other senators showing dismay that these cuts go too far.

I tend to agree with the fiscal hawks here, as that is my nature as an economist. That, my friends, is neither here nor there. What matters is that the U.S. Dollar Index traded lower on this news and that while Treasury securities showed strength due to weakness in the above economic news, that the long end of the spectrum of Treasury securities could become unanchored should the federal government continue to behave in a fiscally reckless manner. The weaker dollar would indeed be inflationary.

Marketplace

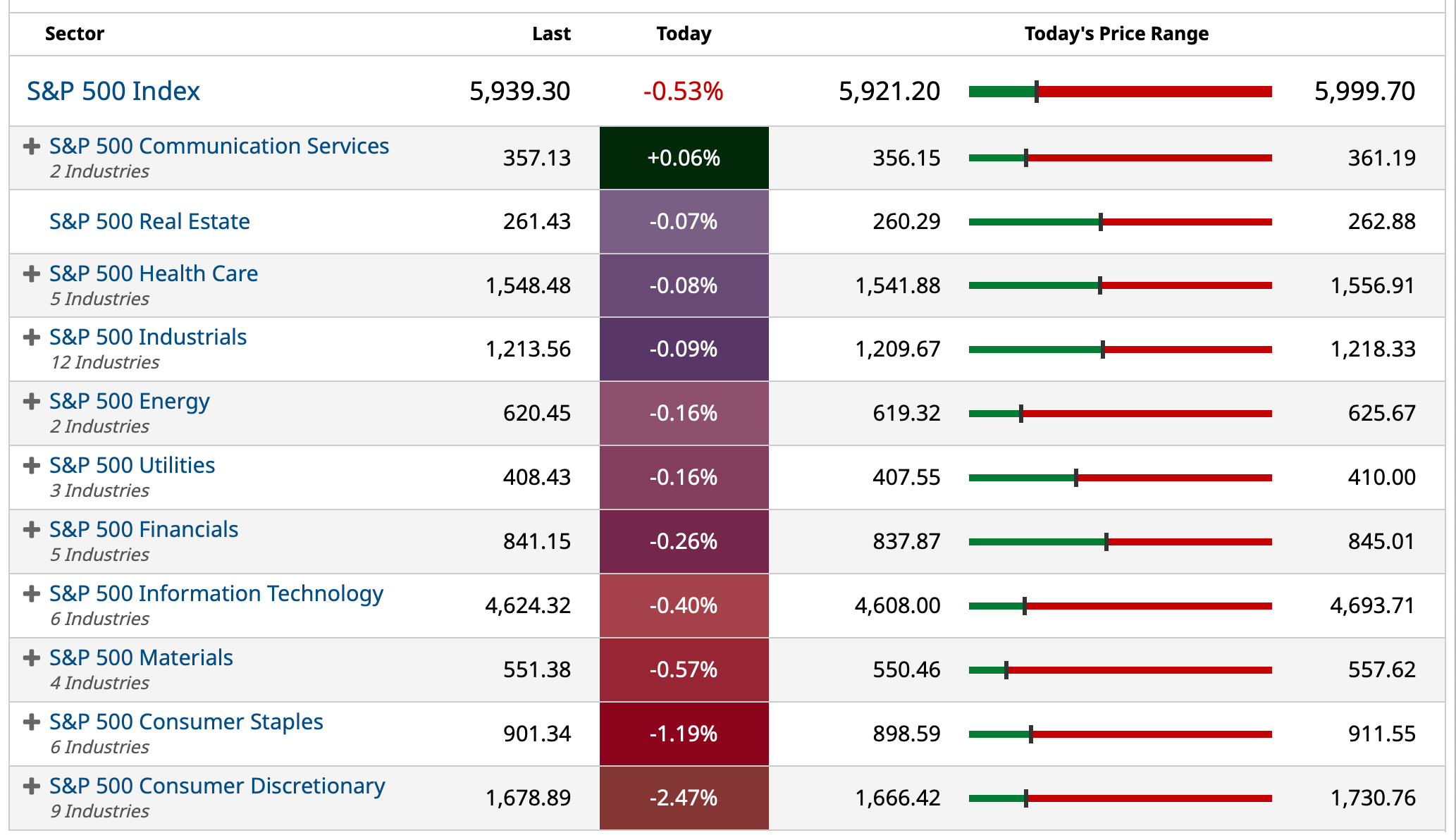

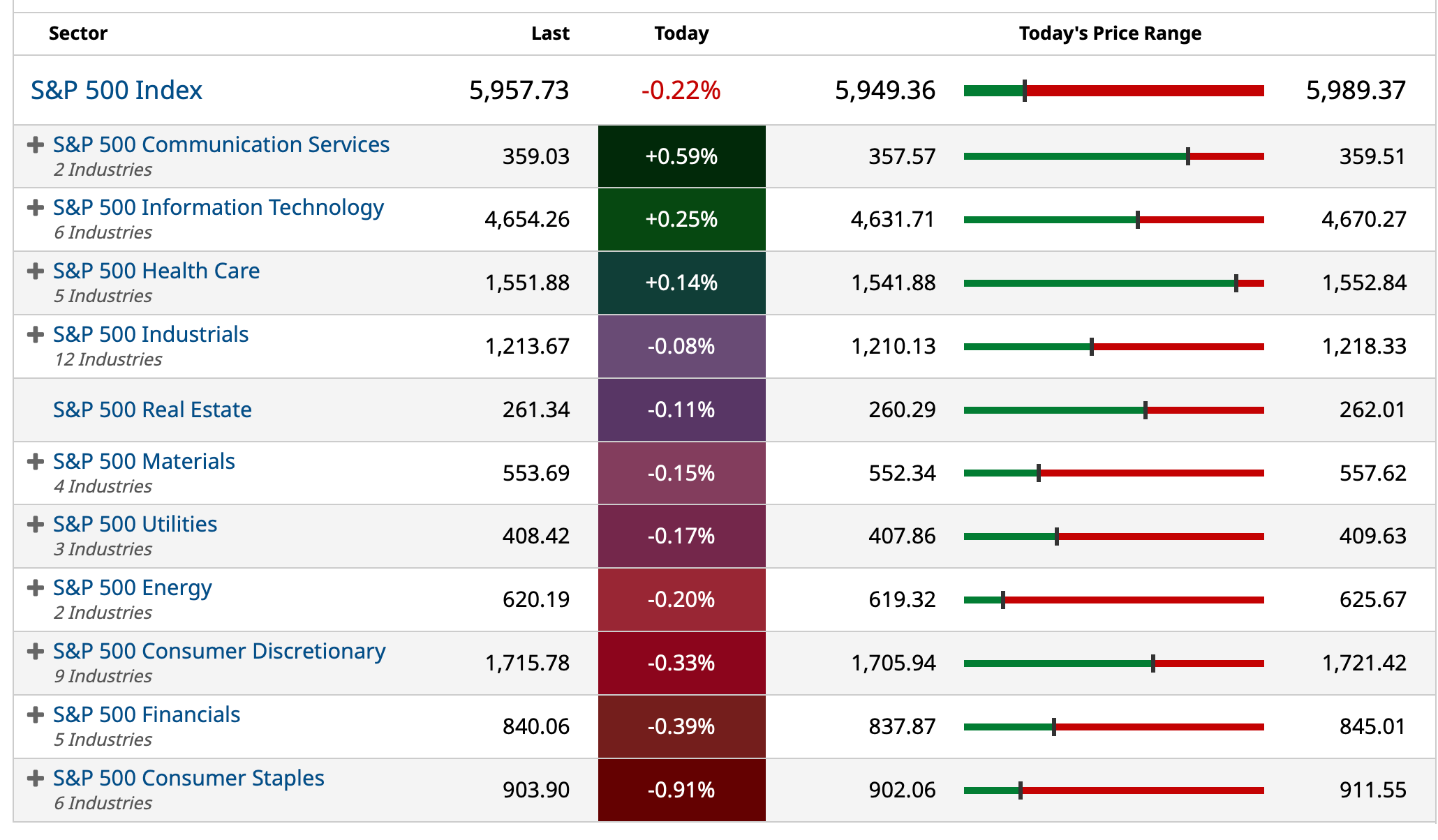

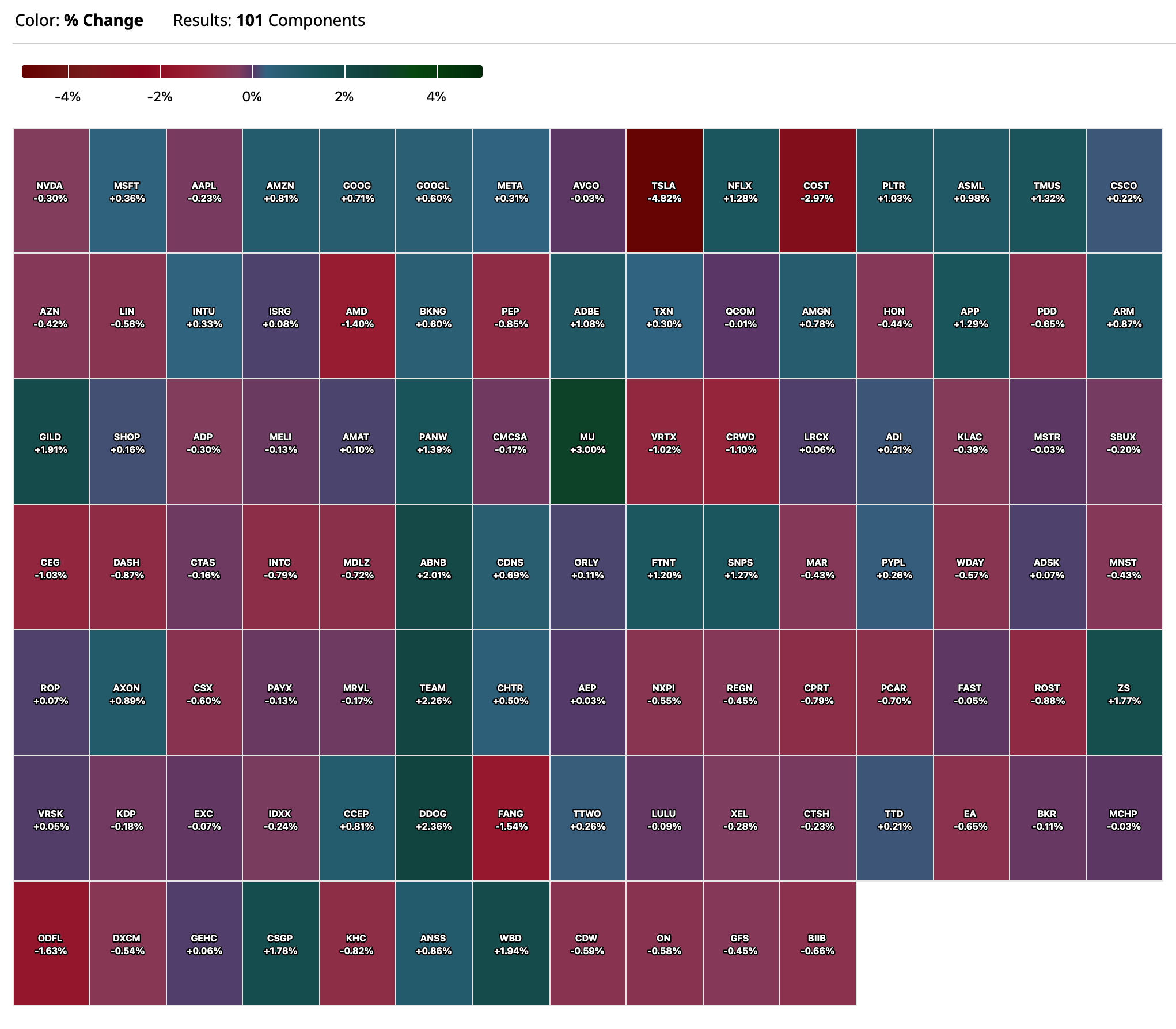

On Wednesday, the S&P 500 closed essentially flat (+0.01%), while the Nasdaq Composite gained 0.32% thanks to a 1.39% run made by the Philadelphia Semiconductor Index. Marvell Technologies MRVL and ON Semiconductor ON led that group for the day. Otherwise, not a lot changed on Wednesday. The Dow Transports gave up 0.46%, while the small to midcap indices all gave back between 0.2% and 0.26%.

Six of the 11 S&P sector SPDR ETFs closed out Wednesday's regular session in the green, led by the Communication Services XLC fund that only gained 0.64%. While only five of these funds closed in the red, Energy XLE gave up 1.95% as exploration, refining and pipeline stocks all took a pounding, and the Utilities XLU gave back 1.75%.

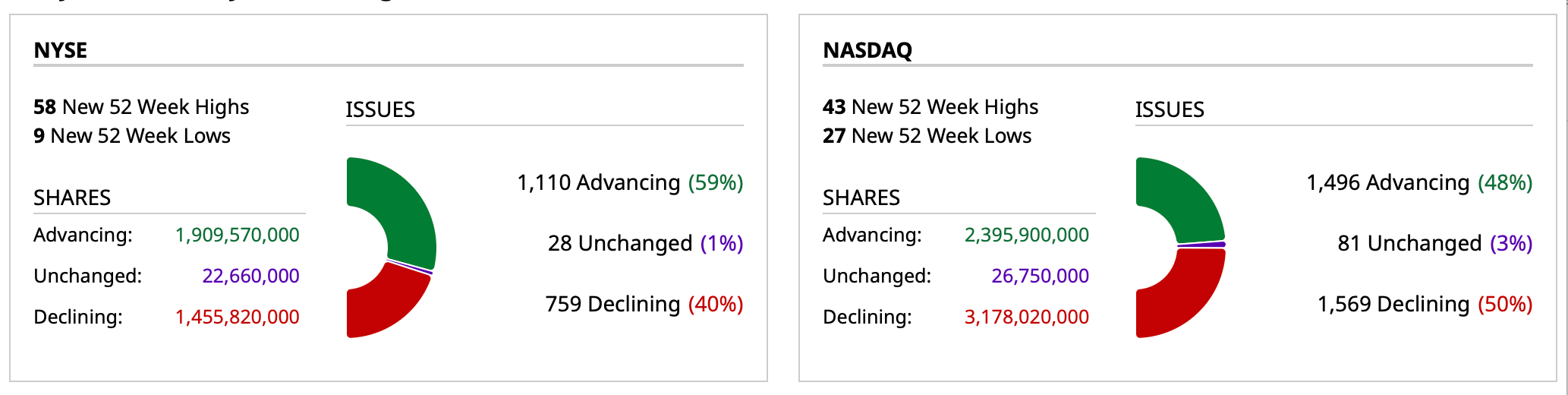

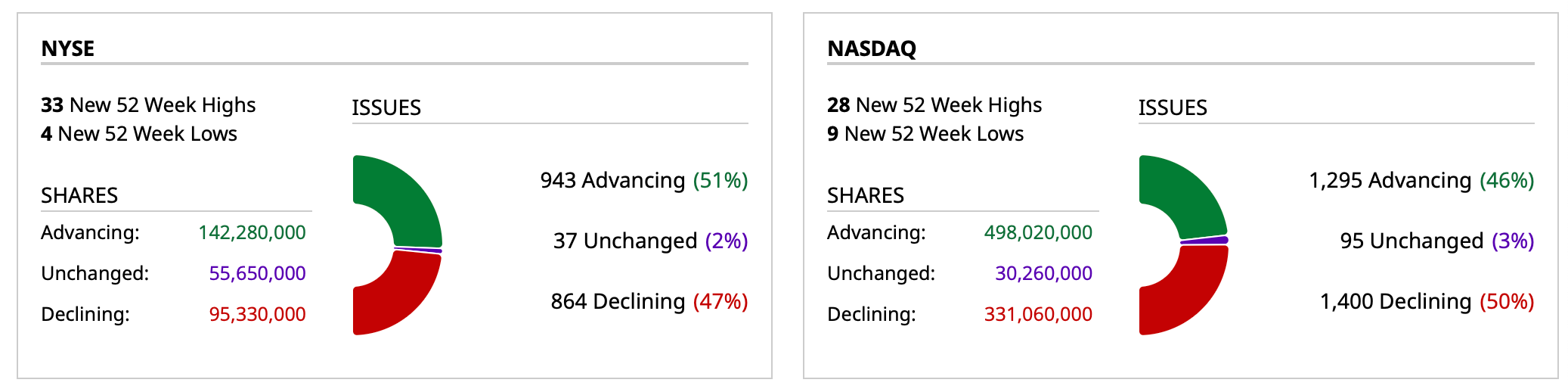

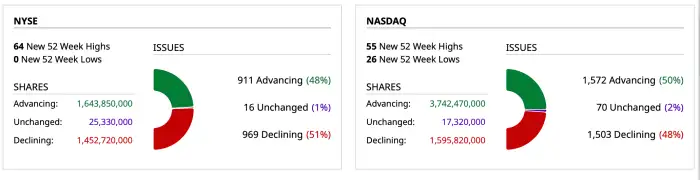

Breadth

Winners beat losers on the NYSE on Wednesday by just three issues. This was largely a 50/50 split. Winners did lead losers at the Nasdaq by a 6-to-5 margin. Advancing volume did take a nifty 65.5% share of composite Nasdaq-listed trade on Wednesday, but just a 45.8% share of composite NYSE-listed activity.

Most importantly, on a day-over-day basis, aggregate trade contracted across NYSE-listings by 5.2% and across Nasdaq-listed securities by 3.7%. Aggregate trade across the membership of the S&P 500 also fell 9% short of the trading volume 50-day simple moving average for the index on Wednesday after falling just 4% short of that line in the sand on Tuesday.

Does this render Wednesday's market as less significant that it might otherwise be? In short, technically, the answer is "yes." Price discovery is always more meaningful and more impactful when increased trading volume implies increased professional participation.

Readers will see just how incredibly accurate technical analysis has been through this recent period. On Wednesday, the index, though quiet, did build on Tuesday's confirmation of Thursday's change in trend.

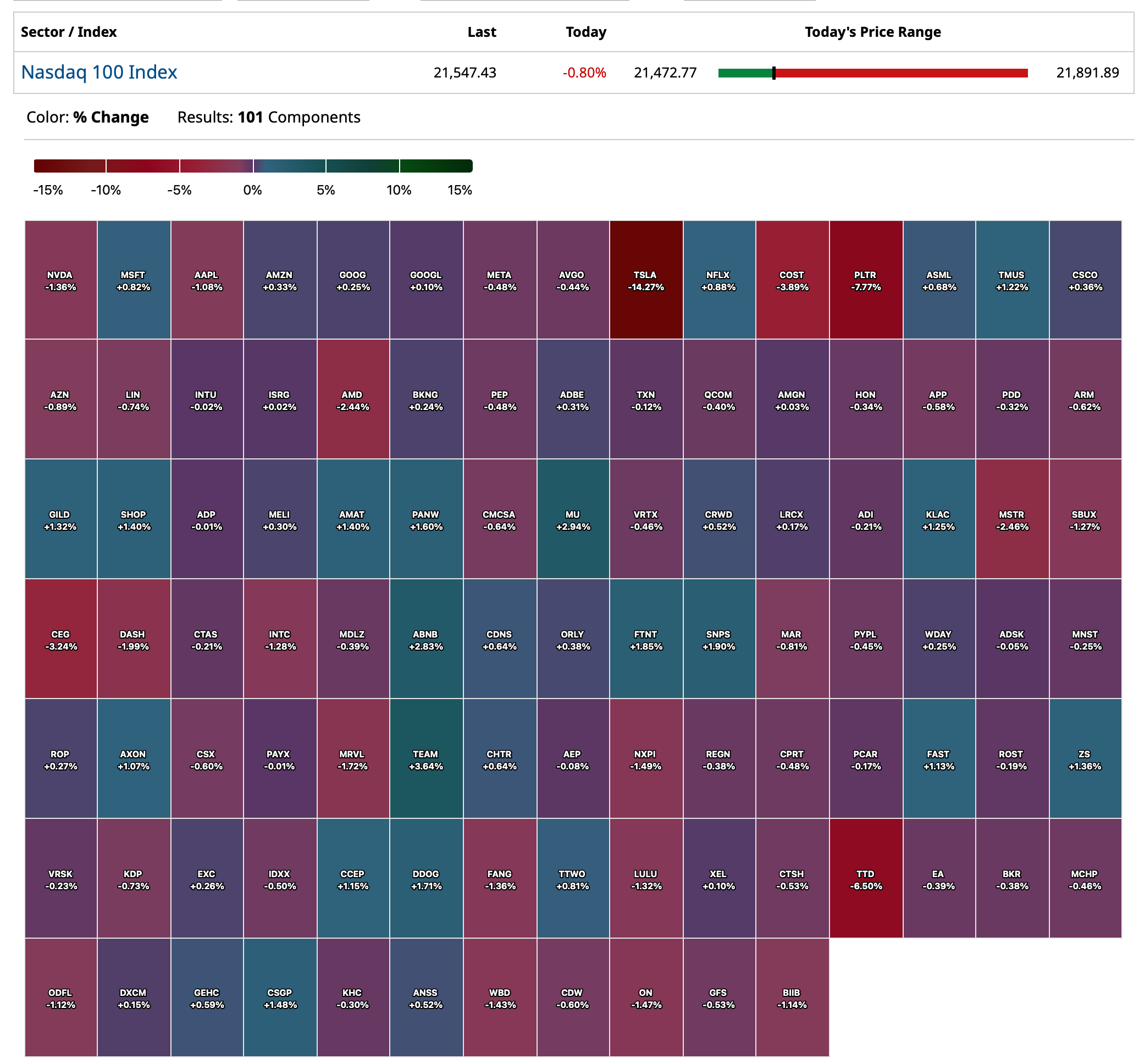

AMD Tapes on the Foil

Is Advanced Micro Devices AMD getting ready to make a serious run at industry leader Nvidia NVDA? Is Lisa Su getting ready to make a serious run at Jensen Huang? Maybe. Check out these past few moves that largely flew under the radar:

June 4th: AMD announces the acquisition of open-source software company Brium in an effort to further its prowess in generative artificial intelligence. Terms of the deal were not disclosed.

May 28th: AMD announced the acquisition of silicon photonics company Enosemi to boost co-packaging and the firm's prowess in generative AI. Terms of the deal were not disclosed.

May 20th: AMD announced the divestiture of its ZT Systems, which is a data center manufacturing company for $3 billion. But the firm retained ZT's 1,200-person engineering team at a cost of about $1.6 billion or $1.33 million per engineer. This should improve AMD's competitiveness in the data center GPU market.

My Conclusion? AMD is back among my top 10 holdings when ranked by weighting (number 10) after a long hiatus. We skipped much of the 2024 decline. Our net basis is currently $99.91. I expect to continue to buy the stock on weakness when that opportunity arises going forward. Nvidia remains my 15th heaviest allocation. I have no plans to add.

Economics (All Times Eastern)

08:30 - Initial Jobless Claims (Weekly): Expecting 230K, Last 229K.

Surprise #2: The "other" romance, between Trump/Musk, doesn't make it past Spring 2025.

National protests and demonstrations emerge and demands from a wide array of members of both the Republican and Democratic parties (including conservatives and liberals) call for "ousting" Elon Musk, an unelected official, from playing such a dominant role in the U.S. government.

Bernie Sanders, taking the Senate's mantle of opposition to Musk, tweets about Elon Musk's and other billionaires' outsized role in the government:

"The precedent set in the last few months should upset every American who believes in our democratic form of government. In 2024, just 150 billionaire families spent almost $2 billion to purchase political candidates. Since the election in November, Elon Musk, Jeff Bezos and Mark Zuckerberg got $300 billion richer and are now worth $1 trillion combined. It appears that from now on no major legislation can be passed without the approval of Elon Musk, the wealthiest person in our country. That's not Democracy, it's Oligarchy. We must fight for an economy that works for all, not just the few. Elon Musk is an unelected official that is essentially acting a the President of the United States. We must pass legislation that changes this!"

Funded by George Soros, the law firm Boies, Schiller & Flexner launches a suit restricting the role of unelected officials without official positions in the Administration (like Elon Musk and Vivek Ramaswamy). The suit ends up going to the Supreme Court but is unresolved by year-end.

Reading the room (and increasingly uncomfortable with Musk's notoriety), President Trump begins to be openly critical of Musk and finally abandons him entirely.

Musk lashes out and retaliates by forming his own party and has a nervous breakdown.

Separately, Tesla makes little progress in "full self driving." The U.S. government takes away the $7,500 tax credit, competition from China intensifies, unit sales drop by double digits and Tesla's profits collapse. In addition, an "accounting issue" (related to warranties) is uncovered by a short-oriented research boutique. All these factors cause the shares of (TSLA) to drop to $100/share.

Elon Musk's non-Tesla investments suffer from reduced U.S. government support.

Musk grows ever more unhinged throughout 2025 - his mother attempts a family intervention.

US: Futs are flat. Pre-market, Mag 7 are mostly higher except for TSLA (-1.6%): AMZN +0.6%, GOOG/L +0.3%. Yield curve is largely unchanged; USD is flat. Commodities are mostly mixed with notable outperformance in silver (+3.1%). News flow since yesterday’s close has been largely muted: headlines continue to focus on trade negotiation development, particularly implication on rare earth curbs (BBG and CNBC) and upcoming Trump-Xi call.

and...

EQUITY & MACRO NARRATIVE

Yesterday, equities traded within a 40bp range today and closed flat. The more notable price actions are in UST: bond yields fell 8-10bp across the curve given the 3x dovish macro data release (ADP, ISM-Srvcs and Beige Book). Jay Barry also added that: “It is notable that the curve did not steepen, but we think some of this can be explained by the less negative fiscal news, as CBO scoring of the One Big Beautiful Bill Act was not far from private estimates at $2.4tn over the next decade, whereas the CBO forecasts tariff revenue could raise $2.8tn over the same period if rates are made permanent ” (here)

May labor data are largely mixed so far (stronger ISM-Srvcs employment vs. miss in ADP), and Friday’s NFP should provide a clear signal. The Street sees 130k survey vs. 120k BBG whisper vs. 177k prior. We see 100k as the key threshold test on the recession narrative; our full scenario analysis is here and below.

I was surprised to see stock futures trade higher when I awoke at 4 a.m. (S&P +16 and Nasdaq futures +75 about an hour ago) given the weak close (more tariff controversy and worse-than-expected U.S. economic data) and that financials (a key and leading market sector) opened higher and closed at the day's lows on Wednesday.

I took the advantage — as noted and shorted more indices:

* SPY $597.31

* QQQ $530.36

Breadth, after a strong day on Tuesday, was flat to negative on the close (and a number of leading market equities (e.g. PLTR, NVDA, TSLA) ended the day negative in price:

Finally, with a range of only 24 points the S&P moved narrowly on Wednesday:

* But a series of solid questioning by two Fin TV hosts...

After every panelist on the show endorsed CrowdStrike CRWD on CNBC's Half Time two days ago — prior to the company's disappointing EPS release in which the shares dropped by as much as -$40/share — the show revisited CRWD after the fall in trading on Wednesday.

As a follow-up, Fin TV's Scott Wapner did a good job in questioning one of the buyers, Joe Terranova, in the segment Chart of the Day: Crowdstrike. But Joe's response was lacking and confusing.

Here is Jim Cramer's interview with George Kurtz, CrowdStrike's CEO, last night. The CEO's response to Jim's question about buying the stock back was weak and not well thought out. Here again (as was the case with Judge Wapner) Jim did a fine job in pressing the CEO.