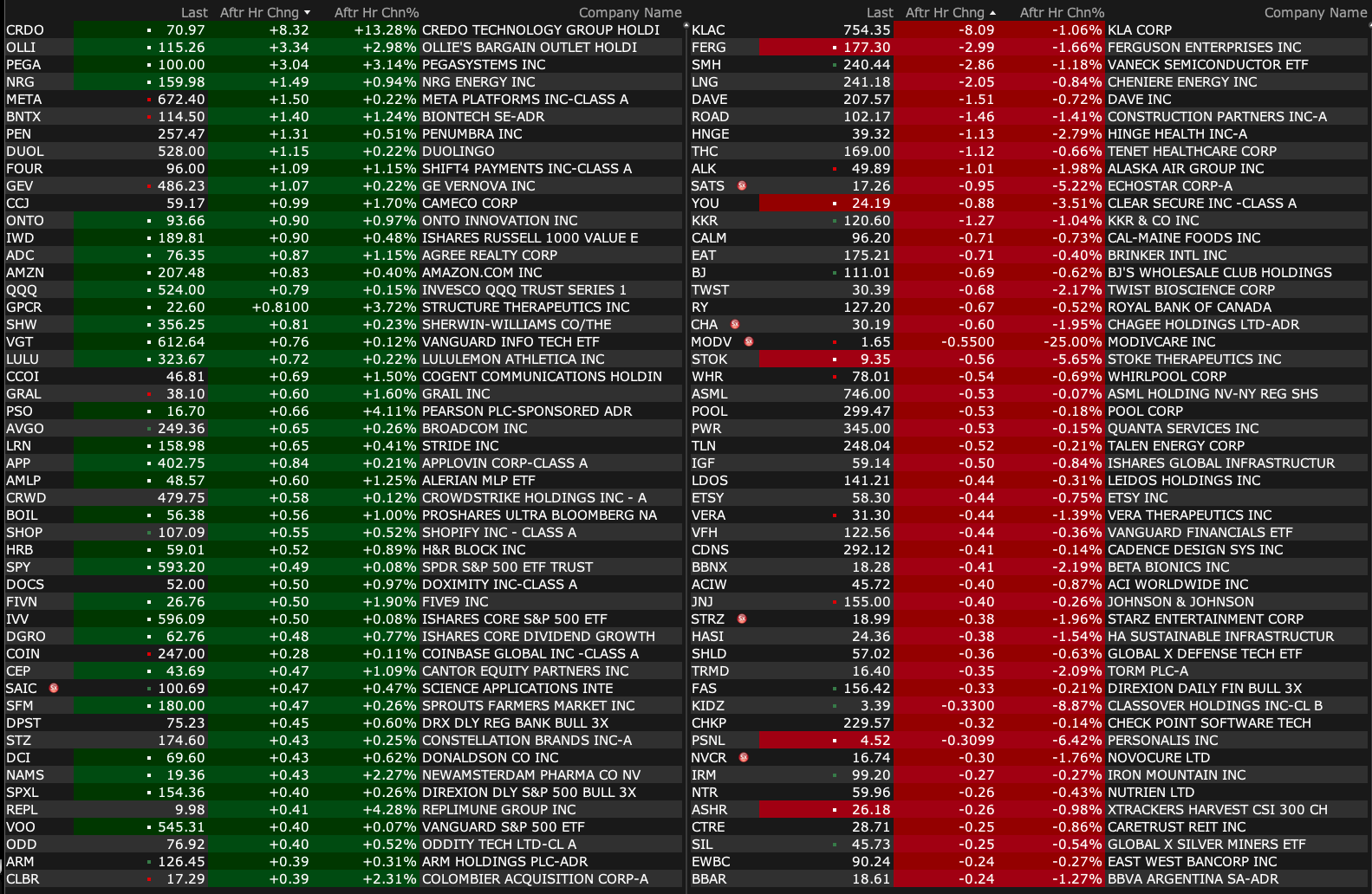

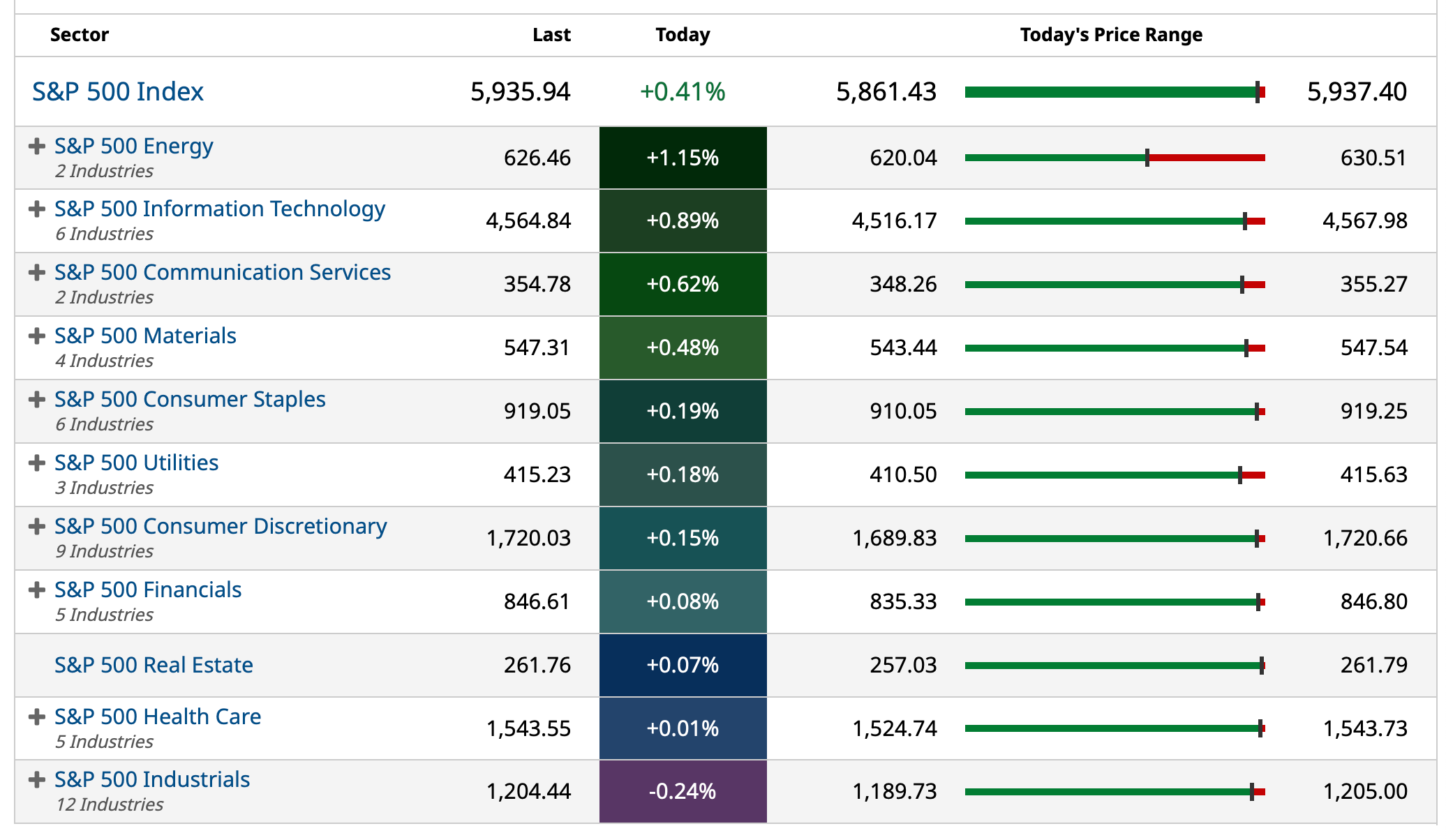

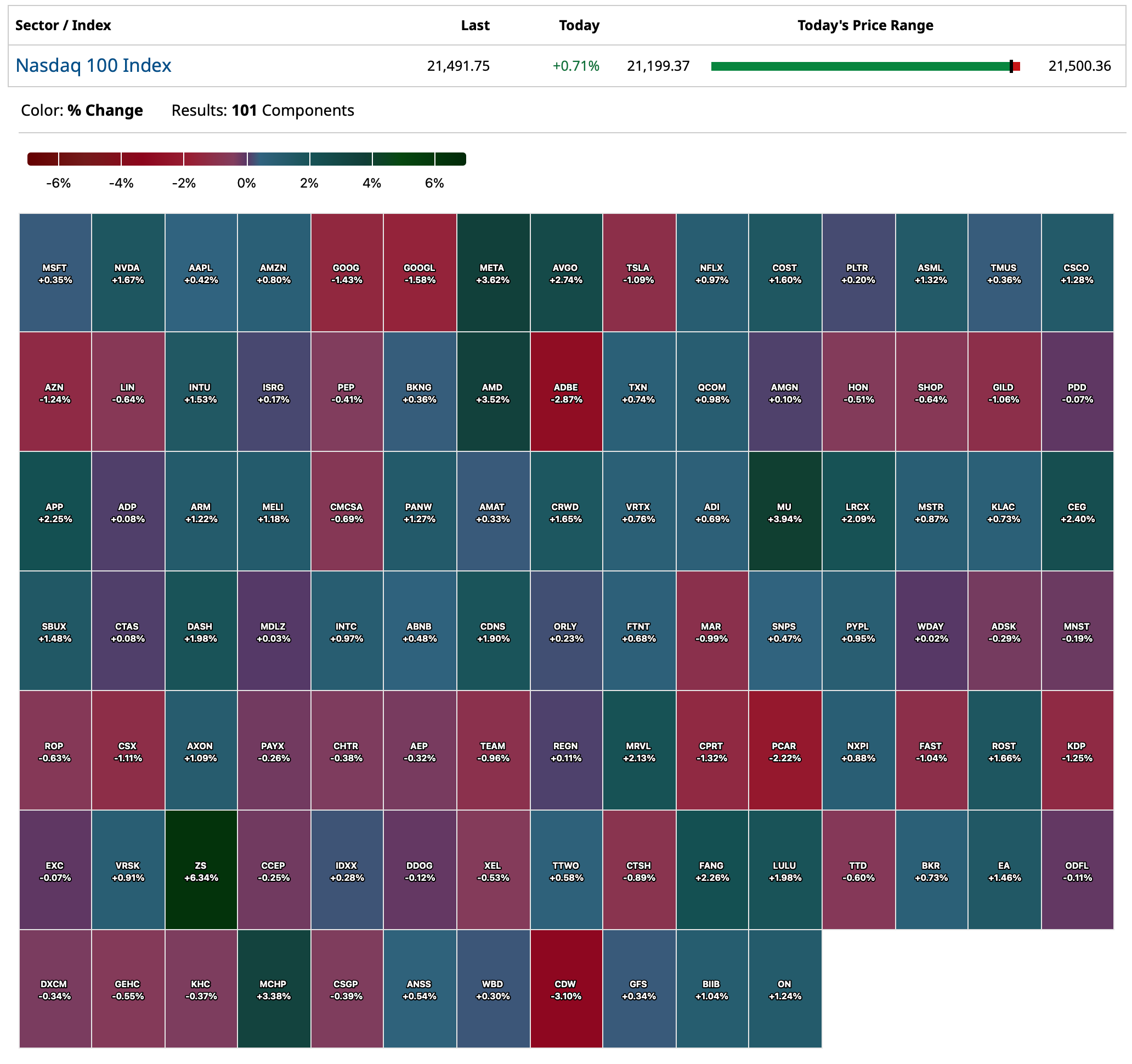

Monday's After-Hours Movers

As of 4:27 p.m.

BY Doug Kass · Jun 2, 2025, 4:32 PM EDT

As of 4:27 p.m.

BY Doug Kass · Jun 2, 2025, 4:32 PM EDT

BY Doug Kass · Jun 2, 2025, 4:25 PM EDT

I have a 3:30 p.m. research call.

BY Doug Kass · Jun 2, 2025, 3:32 PM EDT

Silver is +5% for the best day in over a year:

BY Doug Kass · Jun 2, 2025, 2:57 PM EDT

BY Doug Kass · Jun 2, 2025, 2:51 PM EDT

* Lifting my short equity exposure further...

Stocks are near their day's highs despite a rise in interest rates to the high of the day:

* The yield on the 2-year Treasury note is +3 basis points to 3.94%.

* The yield on the 10-year Treasury note is +5 basis points to 4.47%.

* The yield on the 30-year Treasury bond is +7 basis points to 5.00%.

BY Doug Kass · Jun 2, 2025, 1:36 PM EDT

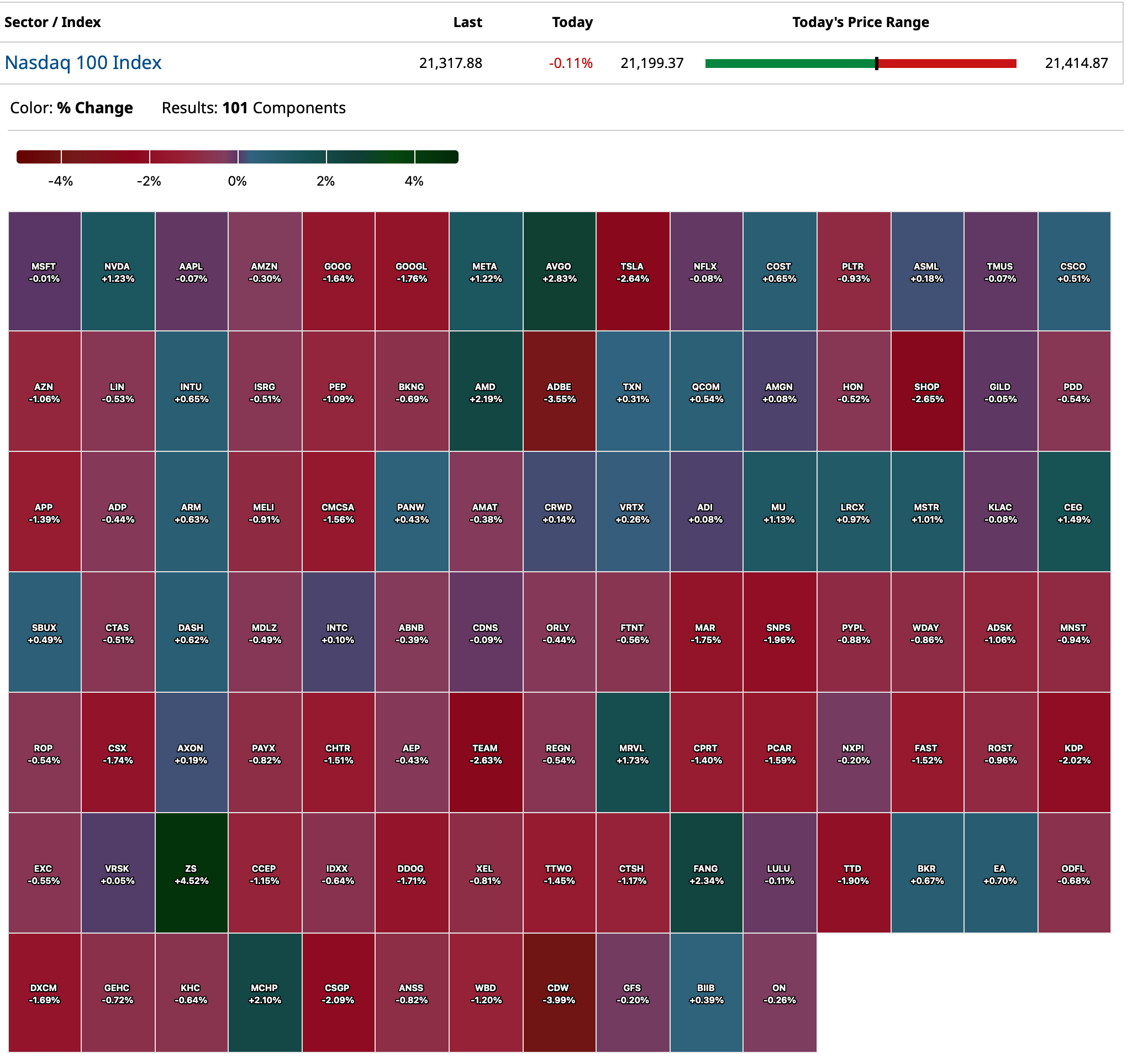

With S&P cash +2 handles I have shorted more SPY at $590.30 and QQQ at $521.40.

Added to GRNY at $20.87 and ARKK at $57.11 shorts.

BY Doug Kass · Jun 2, 2025, 1:18 PM EDT

More index shorts with S&P cash -2 handles:

* SPY $589.93

* QQQ $520.83

You can assume that on strength I will be scaling into a medium-sized index short.

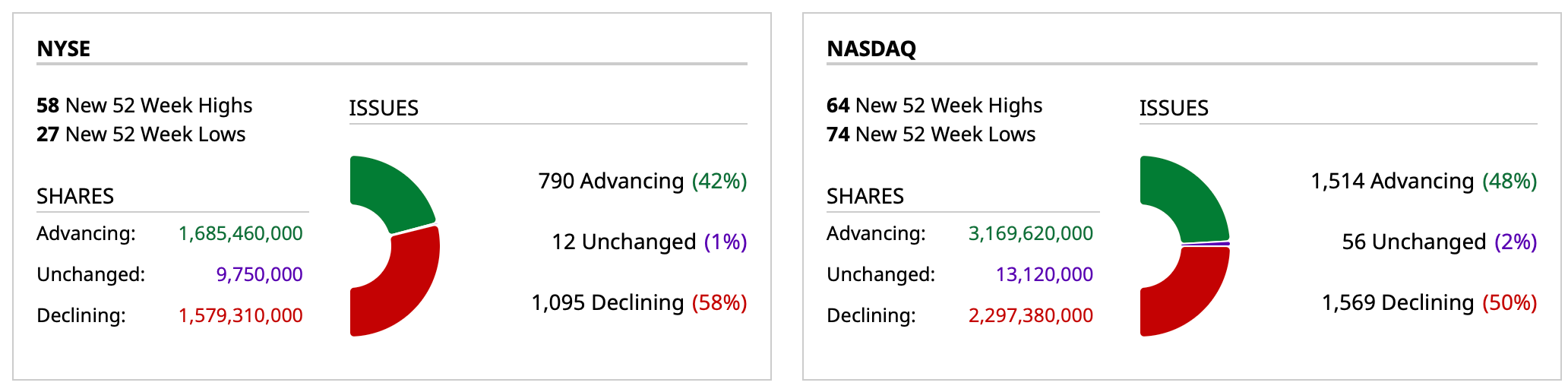

BY Doug Kass · Jun 2, 2025, 12:08 PM EDT

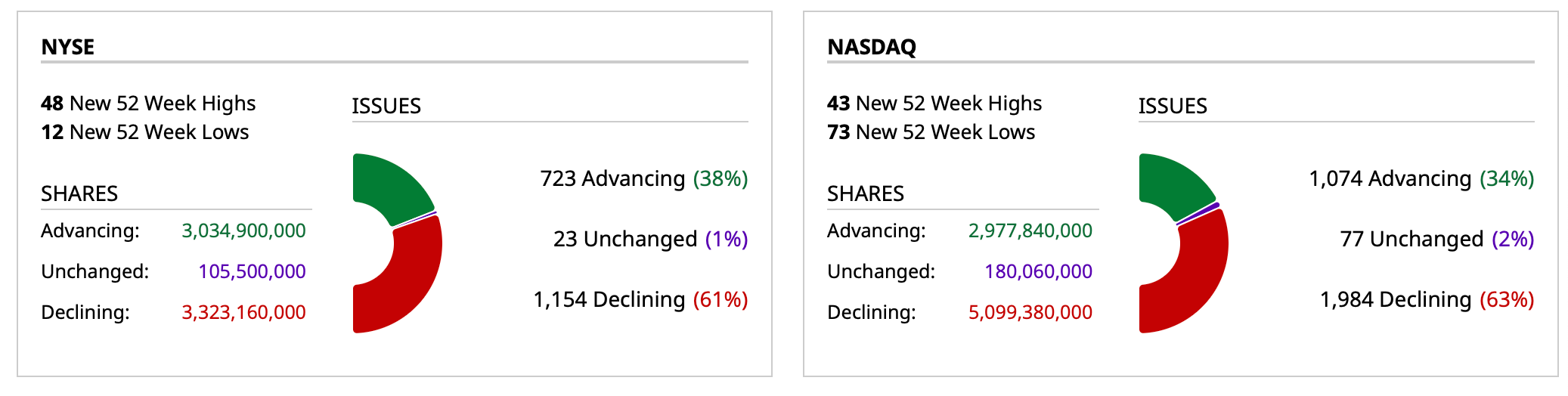

- NYSE volume is 7% above its one-month average;

- Nasdaq volume is 30% below its one-month average;

- VIX index is up 2.48% to 19.03

BY Doug Kass · Jun 2, 2025, 11:45 AM EDT

Bonds make a day's low and I am adding to index shorts on the reversal higher — GRNY, SPY and IWM.

BY Doug Kass · Jun 2, 2025, 11:40 AM EDT

Adding to GRNY short at $20.81.

BY Doug Kass · Jun 2, 2025, 11:34 AM EDT

From Peter Boockvar:

The May ISM manufacturing index fell a touch to 48.5 from 48.7, 1 pt below expectations and at a 5 month low. New orders rose slightly by .4 pts but remained under 50 at 47.6. Backlogs were up too to 47.1 but off the depressed level of 43.7 and still less than 50. Inventories, after being above 50 in March and April, fell back under to 46.7.

With new orders, ISM said “new orders continue to slow, as which party will pay for potential tariff costs is still the prime topic of negotiations between buyers and sellers. A lack of new orders from overseas customers is also a key factor.”

On inventories, “This reading in contraction territory indicates that the pull forward of materials by companies to minimize the financial impacts of tariffs is largely completed.”

Export orders are at a depressed 40.1, lower by 3 pts m/o/m and imports plunged by 7.2 pts to 39.9, the lowest since May 2009. ISM said, “New export orders contracted sharply due to the combination of slow overseas growth, as well as the application of counter tariffs applied to a multitude of U.S.-manufactured products.” On imports, “Imports continue to contract as demand has reduced the need to maintain import levels from previous months, as well as due to the impact of tariff pricing.”

The reason why the April trade goods deficit shrunk so much is because imports collapsed.

BY Doug Kass · Jun 2, 2025, 11:25 AM EDT

From Robbo:

Robbo

26 Minutes ago

From a really smart guy, Tom Sosnoff: JUNE 2, 2025

Sosnoff Says...

With Bitcoin hovering around new highs, there’s been a lot of noise recently in the crypto space. So much so, it feels like the magic crypto bus is loaded way beyond capacity. And the self-proclaimed driver of the bus is none other than Michael Saylor. He’s the CEO of MSTR and a very interesting character who loves to talk his book. I am still having trouble, however, trying to figure him out. I cannot decide whether he is some kind of innovative genius or a very accomplished con artist. The more I read about him and the more I listen to Saylor himself, I am leaning towards grifter. I think Strategy’s strategy is closer to that of a Ponzi scheme than it is a legit business model. Strategy (the name alone screams that it’s not really a strategy) has a market cap that exceeds $103B. Yet they only hold $66B in Bitcoin. That’s a 50% premium above the already high price of Bitcoin. So why would someone buy MSTR instead of cash Bitcoin? Possibly for the leverage or maybe because it’s a familiar investment vehicle. At least that’s what the investment bankers raising capital will tell you. Sorry, but that still makes no sense to me. And that’s not all. Unfortunately, grifters generally attract other grifters and at least two other companies, both with shaky ethical backgrounds, just decided to follow the lead of Saylor. Enter GameStop (GME) and Trump Media (DJT). Both of these companies recently raised capital using convertible paper to buy Bitcoin. GME raised $1.3B and DJT raised $1B of convertible debt. For those new to convertible debt, they are hybrid securities that are essentially corporate bonds which can be converted into a predetermined number of common shares. Only in these latest offerings by GME and DJT, and similar to MSTR latest offerings, there is no interest to be paid and no posted conversion rates. Who would make such an investment? Why would anyone buy an asset at a 50% premium, not receive any interest for loaning the capital, and not know the eventual conversion rate? Unless Bitcoin never has a downtick, somebody is going to lose a lot of money. Run, Forest, Run!

BY Doug Kass · Jun 2, 2025, 11:10 AM EDT

With affordability stretched (to levels never seen) and supply of unsold homes increasing, I continue to expect a consumer-led economic slowdown led by housing:

This also helps to explain the inability of homebuilder shares to rally much and why I would hold off buying until the herd realized the slowdown has hit.

BY Doug Kass · Jun 2, 2025, 11:00 AM EDT

From Peter Boockvar:

This week tariffs on steel and aluminum will go to 50% from 25% as we know and I again went back to look at the business response a few months ago when first initiated, and the experience of 2018. The US Chamber of Commerce wrote a piece in March 2025 titled "How the Steel and Aluminum Tariffs are Hurting US Manufacturing." They said "US steel benchmarks are now roughly twice world prices. Aluminum prices are also up sharply as more than half of US demand is met by imports, most of which come from Canada."

And, "Price hikes for industrial inputs like steel and aluminum hurt a broad swath of downstream manufacturers across the United States, from the auto and aerospace sectors to food producers and the oil and gas sector. For every job in steel production, there are roughly 80 Americans employed by manufacturers that use steel as an input, and the ratio of upstream-to-downstream employment in aluminum is 1-to-177."

We'll see what further retaliation we then get from this ramping up.

The Tax Foundation wrote a piece in September 2022 titled "How the Section 232 Tariffs on Steel and Aluminum Harmed the Economy." The key findings:

1)"The Section 232 tariffs on imports of steel and aluminum raised the cost of production for manufacturers, reducing employment in those industries, raising prices for consumers, and hurting exports."

2)"The jobs 'saved' in the steel producing industries from the tariffs came at a high cost to consumers, at roughly $650,000 per job saved according to the Peterson Institute for International Economics."

3)According to Tax Foundation estimates, repealing the Section 232 tariffs would increase long-run GDP by 0.02 percent and create more than 4,000 jobs.

4)Other estimates, such as those from economists Lydia Cox and Kadee Russ, suggest that job losses from the tariffs were as high as 75,000."

Here's color on #2 from Peterson report, "tariffs would only create about 8,700 jobs in the steel industry...The section 232 tariffs would raise aggregate income in the steel industry by about $2.4 billion in 2018 but raise costs for steel consumers by about $5.6 billion. This implies a cost of nearly $650,000 for every job created."

I'll add one more thing, the cost of construction is about to jump further so building the manufacturing facilities that we want to add here to reshore production is getting much more expensive to build. Also, I'll say again, enjoy the slowdown in rental growth for renters because not only are multi family starts falling, they are about to fall much further because the cost of building apartments is going to go up even more notably.

I reiterate my positive stance on oil and gas stocks as the US rig count for crude oil continues to drop in response to low prices but also the reality of a likely peak in shale oil production for geological reasons. In their new quarterly report, my friend Adam Rozencwajg and his partner Leigh Goehring said that more than 80% of non OPEC oil production growth over the past 15 years came from US shale. Something to watch.

The Baker Huges US crude oil rig count fell for the 5th straight week, by another 4 rigs to 461, the least since November 2021.

Even with the OPEC production increases (maybe the new higher quotas are just meeting up with what was already being pumped), oil is jumping today with the US dollar weakness and maybe with the rig count drop. Gold and silver too are higher. The US dollar index is back below 99 and that is likely helping to lift commodity prices as well.

Crude Oil Rig Count

Ahead of the US May ISM manufacturing index at 10am est, a bunch of overseas PMI's came out.

China's state sector weighted manufacturing PMI rose a .5 pt to 49.5 as expected. The non-manufacturing component remained above 50 at 50.3 vs 50.4 in the month before. We'll get the private sector weighted one tonight. Remember that more than 80% of employment in urban areas in the country are employed by private companies.

Elsewhere, most remain below 50: Taiwan 48.6 vs 47.8, South Korea 47.7 vs 47.5, Vietnam 49.8 vs 45.6, Indonesia 47.4 vs 46.7, Philippines 50.1 vs 53 and India the bright spot at 57.6 vs 58.2. Japan's stayed below 50 after the revision at 49.4 while Australia's was a touch above 50.

Some quick comments on a few. From the Taiwan release, "Manufacturers in Taiwan reported weaker business conditions for the third month running in May, with panel members often highlighting the adverse impact of US tariffs and market uncertainty on demand."

In Vietnam, "May saw a more stable picture in terms of US tariff policies than April, helping lead to a renewed expansion in output and improved business confidence. That said, manufacturers remained wary of the impact of tariffs and again saw a marked reduction in new export orders which contributed to a continued decline in new business overall."

The Eurozone May manufacturing index was left unrevised at 49.4 while the UK saw a lift to 46.4 from the initial print but still remaining well below 50.

Bottom line, the global manufacturing recession continues on.

Fed Governor Chris Waller continues to jockey for the Fed Chair when Powell leaves as he really leans forward to lay out his case for eventual rate cuts this year in contrast to most of his peers. "Assuming that the effective tariff rate settles close to my lower tariff scenario, that underlying inflation continues to make progress to our 2% goal, and that the labor market remains solid, I would be supporting 'good news' rate cuts later this year."

He also said of note, "As of today, I see downside risks to economic activity and employment and upside risks to inflation in the second half of 2025, but how these risks evolve is strongly tied to how trade policy evolves." So the possibility of a stagflationary situation on one hand, and 'good news' rate cuts on the other.

The short end is not responding much and in fact, the 2 yr yield is up 1 bp after falling by 4 bps Friday and 5 on Thursday.

BY Doug Kass · Jun 2, 2025, 10:25 AM EDT

* Shorting indexes on morning reversal and early month equity inflows

Beside my overall ursine view the near term rationale for raising short exposure are:

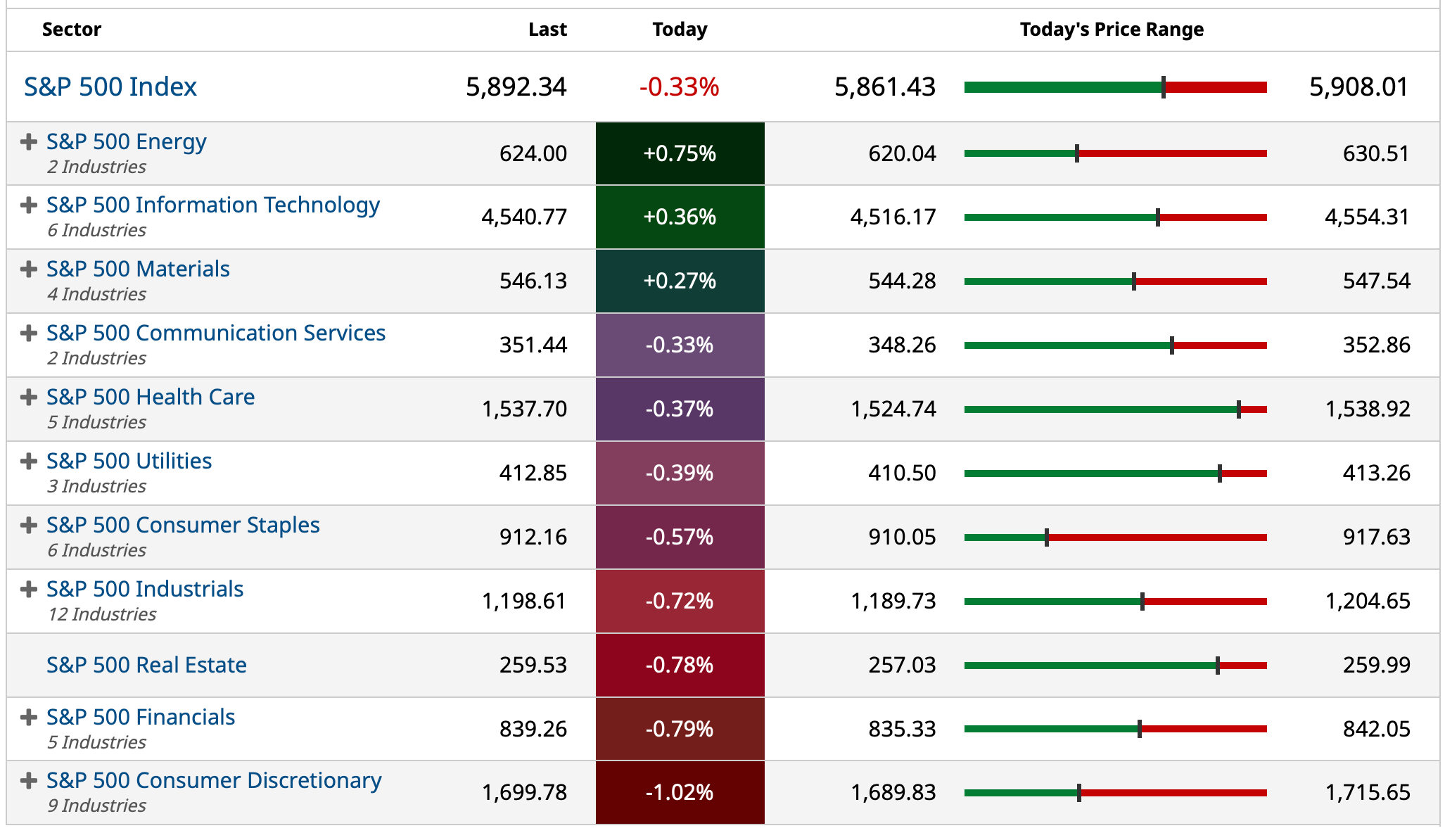

Weakness in financials.

RSP -0.67% despite a rally in the Senior Averages.

The Russell isn't crowing, either.

BY Doug Kass · Jun 2, 2025, 10:15 AM EDT

* The herd believes that AI will produce productivity gains and (corporate profit) margin improvement, justifying 22-times forward price earnings ratios

* But (memo to the consensus), how can the U.S. economy grow anywhere historical rates if AI meaningfully disrupts employment?

Here are some pretty over the top comments from the CEO and founder of Anthropic:

“AI could wipe out half of all entry-level white-collar jobs — and spike unemployment to 10-20% in the next one to five years, Amodei told us in an interview from his San Francisco office.”

"Cancer is cured, the economy grows at 10% a year, the budget is balanced — and 20% of people don't have jobs."

There are several issues here - why would a top AI executive be so hyperbolic and whether the positive impact of AI on productivity/corporate profits and adverse impact of AI on the jobs market are being accurately assessed by investors (which is incorporated in a 22-times forward price-to-earnings multiple)?

Why would the Anthropic CEO say these types of things? These are the types of comments that just beg for extreme government oversight and regulation, globally, if anyone really believed them. As an executive of a business, who would want that?

This may fall into the “he doth protest too much” bucket — just like Elizabeth Holmes at Theranos. The more it was clear Theranos was failing and could not do what people (investors, partners, the public) were told, the more grandiose Holmes' claims became.

All of these businesses are incredibly capital consumptive — they lose money like nothing ever previously known to mankind. They are in constant fundraising mode. “Hey guys, the technology isn’t working and scaling like we thought it would, can I have another $100bb at a 2x markup to the last round we just did 3 months ago” is just not that compelling of a pitch to investors. But what he is saying now, boy, if it could just do 25% of what he claims, well then you are on to something.

This of course comes at the same time as the CEO of Klarna is telling everyone he is firing the AI he put in place, and hiring the humans back, because the AI is failing so badly at even the simple use case job.

I would also love to know how the economy grows 6% to 7% a year with 10%-20% unemployment? I am sure Anthropic can hallucinate a good answer to that one!

Moreover, if AI was going to do all these things, would Jensen Huang be selling Nvivida NVDA hand over fist all of the sudden?

My views:

The IT revolution gutted blue collar workers in the 1990s. The AI revolution is likely to gut white collar workers in the next decade, especially entry level jobs (See the Tweet about Meta fully automating Ad creation above). Unemployment will probably spike higher and no one — our politicians, economists and strategists are talking about this. No one is talking about preparing the work force for dramatic change and the radical transformation of most companies.Will the machine do it better than man? The data of college graduates difficulty in finding jobs today is presaging the issue. The disruptive AI train can't be easily stopped according to a recent book written by Jim Vandehel and Mike Allen, which I highly recommend.

Whether AI will be as effective as many proclaim, stay tuned (and I remain skeptical).

BY Doug Kass · Jun 2, 2025, 9:45 AM EDT

Added to my very small Index short just now:

* SPY $589.48

* QQQ $520.21

BY Doug Kass · Jun 2, 2025, 9:41 AM EDT

FED SPEAKERS

10:15 a.m.: Fed Bank of Dallas President Logan (Non-Voter) participates in moderated conversation before the Eleventh District Banking Conference hosted by the Federal Reserve Bank of Dallas, Dallas, TX (No text. Livestream available. Audience Q&A expected. No media Q&A);

12:45 p.m.: Fed Bank of Chicago President Goolsbee (Voter) participates in a moderated question-and-answer session before the 2025 Quad Cities Business Journal Mid-Year Economic Review, Davenport, IA (Livestream available. Embargoed text TBD)

TREASURY AUCTIONS

11:00 a.m.: US Treasury's Buyback Announcement (Cash Management)

11:30 a.m.: Treasury hosts a $76B 3 and $68B 6-Month Bill Auction

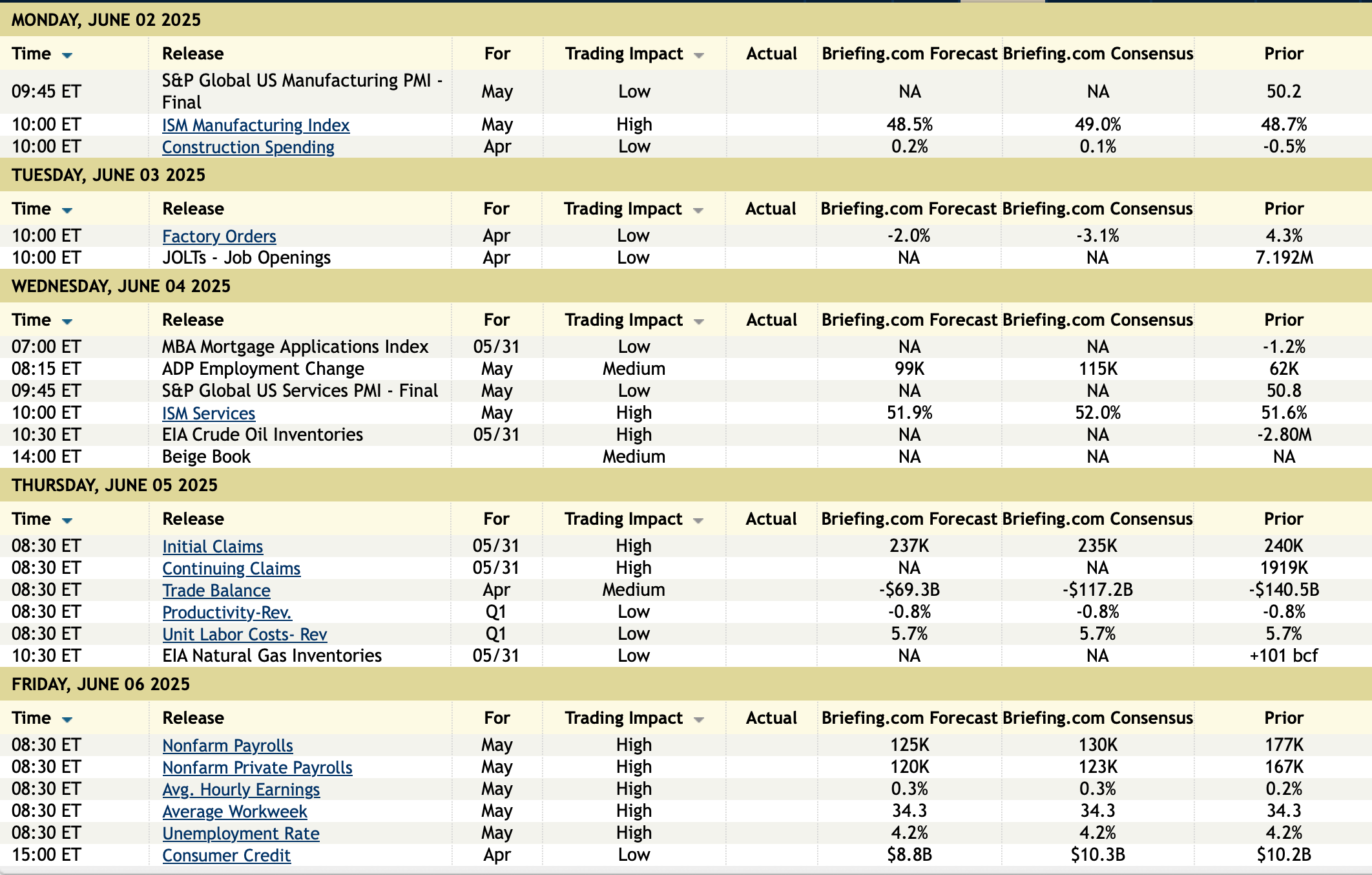

ECONOMIC CALENDAR FOR THE WEEK

BY Doug Kass · Jun 2, 2025, 9:30 AM EDT

-VERA +58% (Atacicept achieved 46% Proteinuria Reduction in ORIGIN Phase 3 Trial in Adults with IgA Nephropathy)

-WETO +39% (signs up to $300M XRP Treasury Management Agreement with Top-Tier Manager Samara Alpha)

-KYMR +38% (announces Positive First-in-Human Results from Phase 1 Healthy Volunteer Clinical Trial of KT-621, a First-in-Class, Oral STAT6 Degrader)

-TIL +30% (BMY cancer drug partnership; appoints Jamie Freedman, M.D., Ph.D., as Chief Medical Officer, effective immediately)

-BPMC +27% (to be acquired by Sanofi at $129.00/shr for equity value of $9.1B)

-CLF +25% (President Trump says he will double US steel tariffs from 25% to 50% "to protect American industry", effective on June 4th)

-TBPH +14% (sells remaining royalty interest in Trelegy Ellipta to GSK for $225M cash; affirms FY25 guidance)

-BNTX +11% (partners with BMY to globally Co-Develop and Co-Commercialize Next-generation Bispecific Antibody Candidate BNT327 Broadly for Multiple Solid Tumor Types)

-NUE +11% (President Trump says he will double US steel tariffs from 25% to 50% "to protect American industry", effective on June 4th; BMO Capital Markets Raised NUE to Outperform from Market Perform, price target: $145)

-ATAI +10% (combines with atai Life Sciences to Create Global Leader in Psychedelic Mental Health Therapies)

-LQDA +9.9% (schedules First Commercial Shipment of YUTREPIA (treprostinil) Inhalation Powder for Patients with PAH and PH-ILD)

-APLD +8.9% (announces 250MW AI Data Center Lease with CoreWeave in North Dakota)

-KURA +7.2% (Kura Oncology and Kyowa Kirin announce FDA Acceptance and Priority Review of New Drug Application for Ziftomenib in Adults with Relapsed or Refractory NPM1-Mutant AML)

-SGBX +5.9% (signs Letter of Intent to acquire Giant Containers Inc.; terms not disclosed)

-CANG +5.5% (founders entered into a securities purchase agreement to sell up to 10M shares for $70M)

-AQMS +3.4% (announces Allowance of Foundational U.S. Patent for Lithium Battery Recycling Technology)

-MRNA +3.0% (new COVID vaccine achievs FDA clearance for seniors and at-risk population)

-RCUS +2.5% (initial data from the ARC-20 Study of Casdatifan plus Cabozantinib showed nearly half of patients with Metastatic Kidney Cancer had a confirmed response)

-CRWV +2.4% (announces 250MW AI Data Center Lease with CoreWeave in North Dakota)

-ASPI +2.0% (announce Supply Agreement with Isotopia for Gadolinium-160 to Accelerate Terbium-161 Production for Advanced Cancer Therapies)

-XLO -27% (warrant offering of indeterminate amount)

-SAIC -6.5% (earnings, guidance)

-DKNG -6.1% (Illinois lawmakers propose FY budget including tax hike on sports betting)

-OKLO -5.5% (files $1B mixed shelf)

-INDP -4.2% (doses first patient in Phase 1b/2 combination study of Decoy20 with PD-1 Checkpoint Inhibitor Tislelizumab)

-LI -2.6% (reports May deliveries)

BY Doug Kass · Jun 2, 2025, 9:22 AM EDT

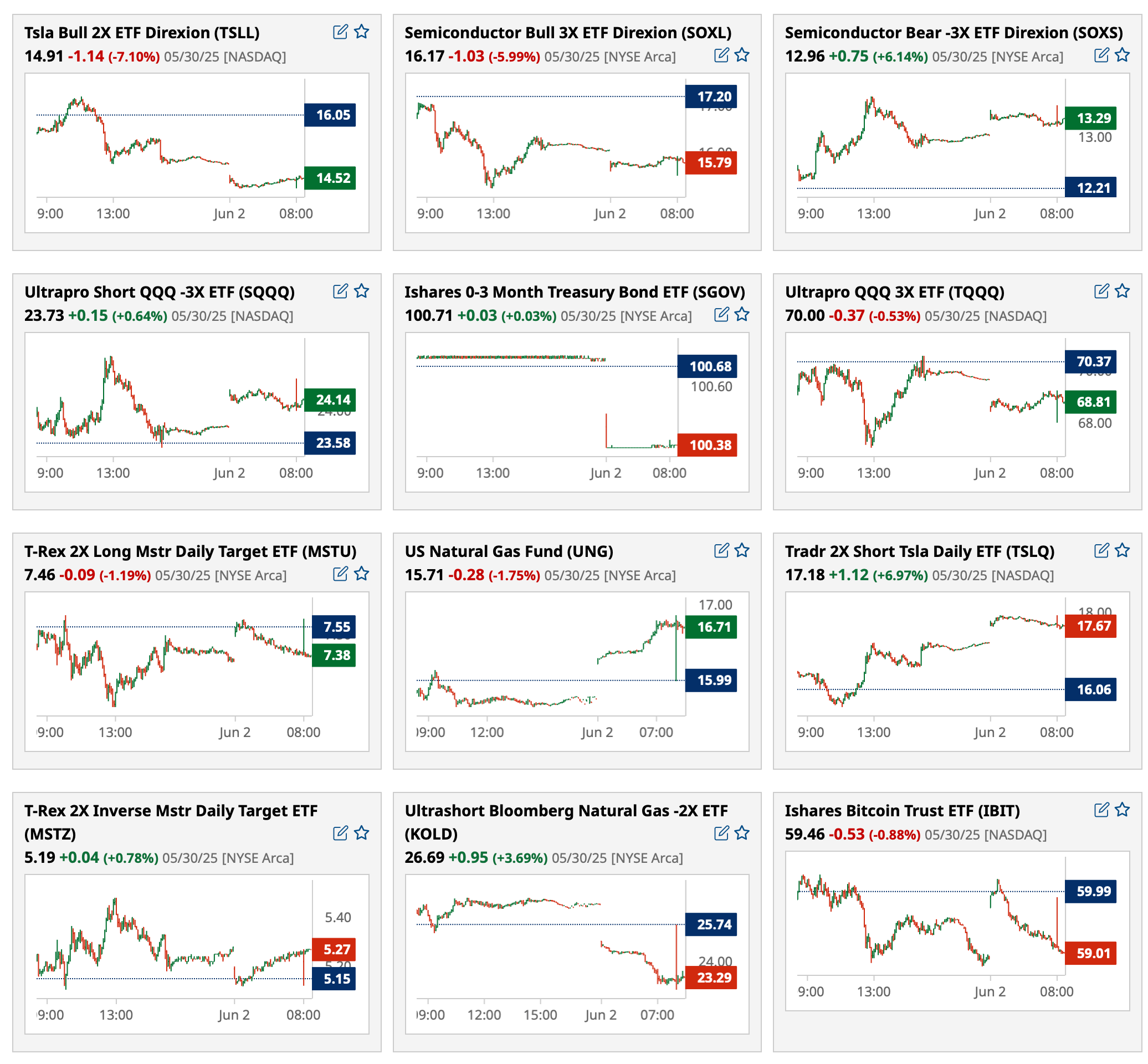

BY Doug Kass · Jun 2, 2025, 9:12 AM EDT

Most active premarket ETFs as of 8:19 a.m. ET:

BY Doug Kass · Jun 2, 2025, 9:07 AM EDT

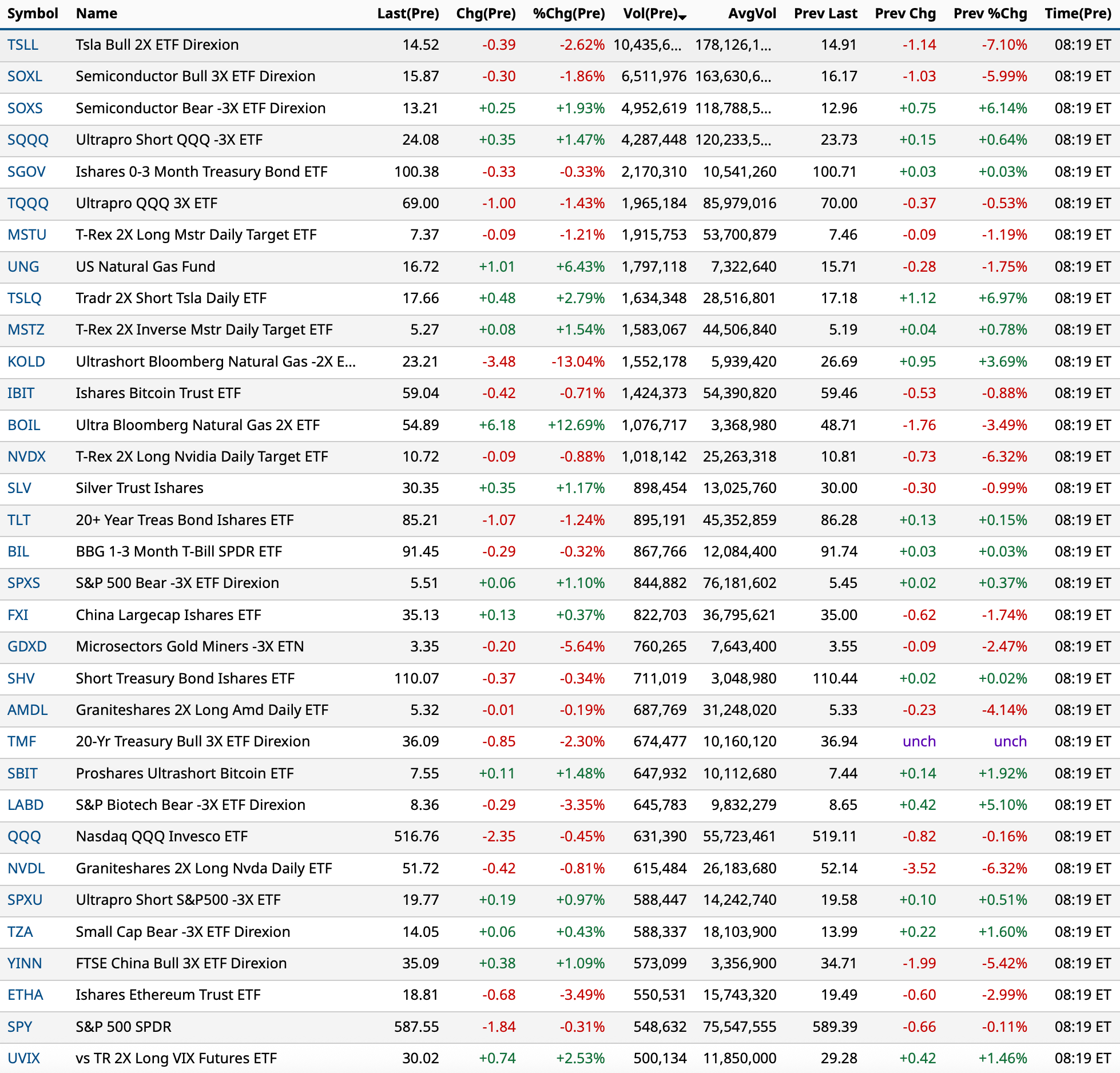

Premarket percentage movers at 8:39 a.m. ET:

BY Doug Kass · Jun 2, 2025, 8:54 AM EDT

BY Doug Kass · Jun 2, 2025, 8:42 AM EDT

* Contrarian thoughts from Dougie and Bloomberg's Bramo...

Last month I made the (controversial) case that the economic cycle has become less relevant:

Well per below, I think we have our answer. The U.S. economy, as things are measured now (including government spend), is in fact recession proof.

We technically didn’t have a recession in the middle years under the prior administration, when nearly everyone thought there was a going to be a recession, including financial minds that thought we were in one or would have one, and the population that felt like we were in one (and voted thusly).

We seemingly are not going to have a recession now either, even with everything that has gone on, on top of the residue of what had gone on and an overspent and overborrowed consumer.

Therefore, by hook or by crook, we have a recession-proof economy.

That, however, does not mean we do not have a crisis-proof economy.

As the economy has shifted from manufacturing based to service based, it has also become increasingly financialized. We really have not had recessions for a long time, what we really had was financial crisis-induced slowings in the economy, plus Covid (where we left with an inflation problem due to the circular relationship between government excess and monetary policy that was too loose too long).

Ex Covid, all the economic problems in recent history were really the result of monetary policy that was too loose, and government excess, as opposed to a natural business cycle. Far from traditional recessions. Instead of moving from expansion to contraction at a business level, we move from financial crisis to crisis that are functions of monetary policy and the government.

At any rate, for the time being, all of this is good for the equity markets, which they correctly sniffed out (especially those who got to have dinner and drinks with the right guys in the government). Chaos seemingly smoothed over, and looking at the budget, the government continues to spend like drunken sailors. The one caveat to all of this is the bond market, which for good reason, for the time being is not cooperating like it used to (bonds and equities are decoupling for the third day in a row):

Bond prices continued to decline throughout the day:

* The yield on the 2-year U.S. Treasury note rose by 2 basis points to 4.02%.

* The yield on the 10-year U.S. Treasury note rose by over 4 basis points to 4.50%.

* The yield on the 30-year U.S. Treasury note is 6 basis points higher to 4.95%.

What this all means for the neutral rate, is anyone’s guess, but my view is it is higher than previously thought. We shall see. And the next crisis, we shall see too...

From APR 28, 2025 9:30 AM EDT:

By Doug Kass May 13, 2025 4:31 PM EDT

This morning Bloomberg's Bramo chimes in with a tweet from our own Peter Tchir on the growing irrelevance of consumer sentiment surveys:

BY Doug Kass · Jun 2, 2025, 7:30 AM EDT

Reread my Rethinking American Exceptionalism:

BY Doug Kass · Jun 2, 2025, 7:13 AM EDT

Bonus - Here are some great charts:

Why a Strong May Has Bulls Smiling

Stock Market and Crypto Analysis (I shorted bitcoin last week!)

BY Doug Kass · Jun 2, 2025, 6:45 AM EDT

BY Doug Kass · Jun 2, 2025, 6:29 AM EDT

The real rate of the long bond:

BY Doug Kass · Jun 2, 2025, 6:15 AM EDT

RIP Stan Fischer.

BY Doug Kass · Jun 2, 2025, 6:09 AM EDT

The S&P Short Range Oscillator has moved back to neutral (at -0.20% from 0.90%).

BY Doug Kass · Jun 2, 2025, 5:44 AM EDT