From Peter Boockvar:

Positives,

1) From the International Trade Court, "Because of the Constitution's express allocation of the tariff power to Congress, we do not read IEEPA to delegate an unbounded tariff authority to the President. We instead read IEEPA's provisions to impose meaningful limits on any such authority it confers."

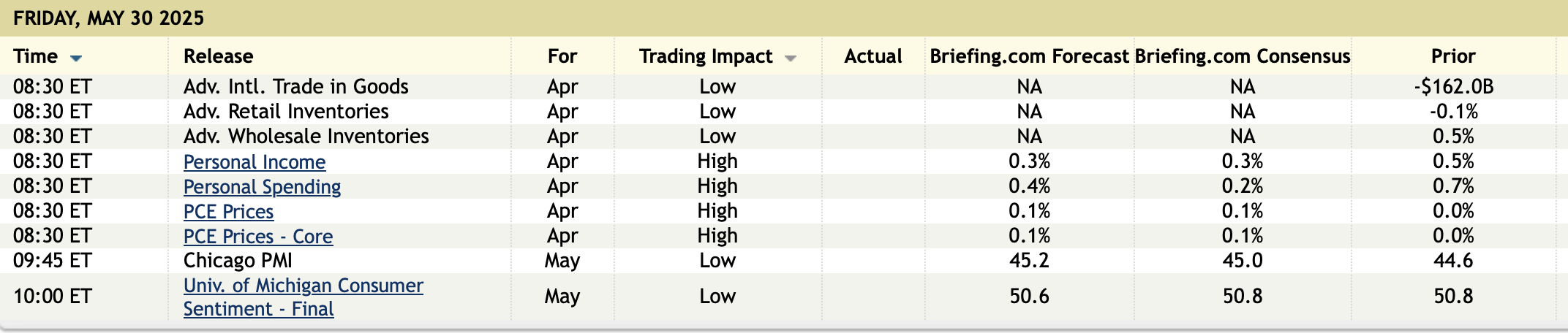

2) The PCE inflation stats were as expected with it following CPI and PPI that were reported weeks ago. Both headline and core for April rose .1% m/o/m with the y/o/y gains being 2.1% and 2.5% respectively vs 2.3% and 2.7% in the month before. Versus last year, the disinflation continued with goods prices down .4% while services inflation offset that, rising by 3.3%.

3) There was an .8% m/o/m rise in income in April that was well above the .3% consensus. This took the savings rate to 4.9% from 4.3% but the income surprise was very isolated. The main factors for the upside in income were the 6.9% rise in social security payments m/o/m and a 21% jump in farm income. Private sector wages and salaries, income was up by .5% m/o/m which is about in line with the 6 month trend.

4) Personal spending in April was higher by .2% m/o/m as forecasted. All of the gain came from the spend on services as the buying of goods was negative, particularly those for durable goods.

5) The May Conference Board’s Consumer Confidence index rebounded to 98 from 85.7 and was 11 pts above expectations. Almost all of the improvement was seen from the Expectations component which jumped to 72.8 from 55.4 while the Present Situation rose more modestly to 135.9 from 131.1. For perspective, this overall index stood at 109.6 in October 2024, 100.1 in February 2025. After rising by 100 bps in April to 7%, one yr inflation expectations slipped back by 50 bps to a still very elevated 6.5%.

6) The final May UoM consumer confidence index was 52.2 vs 50.8 initially and unchanged with April. The UoM said, "Sentiment had ebbed at the preliminary reading for May but turned a corner in the latter half of the month following the temporary pause on some tariffs on China goods. Expected business conditions improved after mid-month, likely a consequence of the trade policy announcement. However, these positive changes were offset by declines in current personal finances stemming from stagnating incomes throughout May. Overall, consumers see the outlook for the economy as no worse than last month, but they remained quite worried about the future."

7) The $87.6b April goods trade deficit which follows the tariff front running influenced $162b seen in March was well below the estimate of $143b because imports collapsed by 20% m/o/m, well more than the 3.4% rise in exports. This led to a big upward revision to the Atlanta's Q2 GDP forecast.

8) Apartment List released its National Rent Report covering May and it reflected a .4% m/o/m rise in new rent prices, up for a 4th straight month in a seasonal time of increases. But, they are still down .5% y/o/y. Supply is still coming online from many projects green lit before interest rates spiked. This drove the vacancy rate up to 7%, a new high dating back to 2017 when they started calculating this. Most are coming from the sunbelt states. Apartment List said, "2024 saw the most new apartment completions since the mid-1980s, and although we're past the peak of new multi family construction, this year is still bringing a robust level of new supply."

9) From Best Buy: "We believe the consumer has remained resilient while dealing with persistent inflation, making them value focused and thoughtful about big ticket purchases. We also still see a customer that is willing to spend on high price point products when they need to or when there is technology innovation."

10) From Ulta Beauty: "During the quarter, amidst considerable macro noise and uncertainty, guests responded positively to key actions that we took to drive our business, including improved execution, exciting new and exclusive brand launches, evolve promotional plans, and relevant marketing."

11) From Elf Beauty: "Looking at Q1 to date, we are seeing our consumption trends better than what we saw in Q4 and continuing to trend well ahead of the category. In the month of April, we were the only top five cosmetics brand to post growth with Elf gaining an additional 130 bps of market share in the US."

12) From Burlington Stores: "As we discussed in our Q4 call in early March, the quarter started off slowly with the trend in February being negatively impacted by unfavorable weather and a slower pace of tax refunds vs last year. We were pleased that the sales trend picked up in the March and April period, once these factors began to normalize."

13) From Gap: "Old Navy and Gap saw growth across all income cohorts, with Old Navy gaining share in both top and bottom cohorts and Gap gaining share in top and middle cohorts, showing our strategic intent is working."

14) From Dick's Sporting Goods: "In Q1, we saw growth in both average ticket and transactions. In fact, compared to the same period last year, more athletes purchased from us, they purchased more frequently and they spent more each trip."

15) From Dell: Revenue was up 5% and in particular, "We experienced exceptionally strong demand for AI optimized servers, building on the momentum discussed in February...That said, given the scale of these opportunities, variability in timing, and choices around technology, the inherent nonlinear nature of demand and associated shipments is likely to persist...We saw double digit demand growth across small business, medium business and large enterprise. Commercial demand was strongest in North America, with EMEA and Asia Pac both up double digits. While the PC refresh remains behind prior cycles, we are seeing indicators that the installed base is upgrading to new Windows 11 PCs, many of them AI PCs."

16) From Salesforce: "We saw very strong growth in our small and medium market business. It really surprised us."

17) French CPI figure for May was up .6% y/o/y vs the estimate of up .9% with a drop in energy prices most helping, down by 8.1% y/o/y. Services inflation also moderated to 2.1% growth from 2.4% in April y/o/y. Manufactured goods prices were lower by .2% y/o/y for a 3rd month.

18) Spanish and Italian May CPI were about as expected with the former up 1.9% y/o/y and the latter higher by 1.9% y/o/y too.

19) The May Economic Confidence index for the Eurozone was up 1 pt m/o/m to 94.8 and above the estimate of 94.1. That though compares with 95.1 in March and 96.2 in February. Manufacturing confidence improved to the least negative in a few years, but the services component fell to the lowest in a few years. Retail and construction confidence got back what it lost in April while consumer confidence remains soft, though less so m/o/m.

20) The Bank of Korea cut interest rates by 25 bps as expected to 2.50% and said this about the outlook, "Since growth momentum has weakened more significantly than initially expected, we believe there's a possibility rates will be cut more than we thought going forward."

Negatives,

1) Initial jobless claims jumped to 240k from 226k and that was 10k more than expected. The 4 week average though was unchanged at 231k because of a print of 241k fell out. Of particular note too, continuing claims rose to 1.919mm from 1.893mm which is the most since November 2021.

2) Pending home sales fell 6.3% m/o/m in April after rising by 5.5% in March and well below the estimate of down 1%. The NAR said, “Despite an increase in housing inventory, we are not seeing higher home sales. Lower mortgage rates are essential to bring home buyers back into the housing market.”

3) Non defense capital goods aircraft line for April was lower by 1.3% m/o/m vs the estimate of down .2%, only partly offset by a 2 tenths upward revision to March, seeing a .3% increase.

4) Q1 GDP is old news but was left little revised, down .2% vs the initial print of -.3%. Within though, personal spending was revised lower to 1.2% q/o/q annualized growth vs 1.8% in the first round. Inventories were revised up, government spending was less negative and capital spending was a bit better than initially reported.

5) The World Container Index said the price of a 40 foot container from Shanghai to LA rose another 17% w/o/w to $3,738, up $541. That's a 3 month high. The price of a trip from Shanghai to NY was up by 14% w/o/w to $5,172, up by $645.

6) Read the comment section of the Dallas manufacturing survey which came in at -15.3., https://www.dallasfed.org/research/surveys/tmos/2025/2505#tab-comments

7) The May Chicago manufacturing index fell to 40.5 from 44.6. The Richmond index was -9 vs -13.

8) From Costco: "Our buyers continued to do an excellent job finding new and exciting items at great values, which are resonating well with our members, even as they remain very choiceful in their spending on discretionary items." On pricing/inflation, "Fresh food and sundries inflation remained relatively similar to last quarter. In non-foods, we saw low single digit inflation return for the first time in a number of quarters. This was driven primarily by imported items. As a reminder, about a third of our sales in the US are imported and about two-thirds of those ales are in non-foods. Items imported from China represent about 8% of total US sales."

9) From Best Buy: "For the most part, customer behavior in Q1 did not change materially from the commentary we have shared for the past several quarters. Customers continued to be deal focused and attracted to more predictable sales moments...We've been very clear and saying consumers are making trade-offs, and we can see that within our categories."

10) From Ulta Beauty: "Consumer engagement with beauty remains healthy, and our insights indicated beauty and wellness remain a top priority for beauty enthusiasts who tell us that they're more willing to make trade-offs in other discretionary areas to maintain their beauty regiments. At the same time, they are cautious and value is an increasingly important priority as they navigate ongoing wallet pressures."

11) From Burlington Stores: On the consumer, "Clearly, we saw a deceleration in our comp trend from Q4 to Q1. Our comp growth in the first quarter was flat...To understand this trend, we have analyzed our own internal sales data. This shows the slowdown from Q4 to Q1 was broad based across trade areas with different demographic characteristics. This is just one quarter, so it is too early to say, if the slowdown that we saw in our trend from Q4 to Q1 is the start of a broader pullback in consumer spending."

12) From Gap: Banana Republic comps were flat "as we continue to focus on re-establishing this premium brand in our portfolio. And as we expected, Athleta comps have been challenging, down 8%." The cost of tariffs? "based on what we know today, if current tariffs of 30% on most imports from China and 10% on most imports from other countries remain for the balance of the year, we estimate a gross incremental cost of approximately $250 million to $300 million. We currently have strategies to mitigate more than half of that amount."

13) From Capri Holding: "Overall, our business remained challenged and we were disappointed with our performance. Revenue decreased 15% during the quarter as we were impacted by the continued softening demand for fashion luxury goods globally."

14) From Macy's: "Given uncertainty regarding the tariff impact on consumer health and demand, we believe it's prudent to incorporate a more choiceful consumer into our outlook for the quarter and for the remainder of the year. Our second quarter and full year guidance ranges assume that the promotional landscape intensifies as the year progresses, international tourism does not rebound and we continue to reinvest savings from closed stores and distribution centers in the initiatives that support our long-term growth."

15) From Elf Beauty: "To partially mitigate the impact from tariffs, we plan to take $1 increase on our entire product assortment globally, effective August 1. We are intentional in not going beyond that $1 to preserve our value proposition...This is only the third price increase we've taken in our 21 year history, unlike many of our competitors who regularly take price increases. Historically, consumers have been able to accept a dollar increase."

16) From Dell: "The consumer market remains challenged, consumer revenue declined 19%, and the industry pricing remained competitive."

17) From HP: "Against the backdrop of a highly dynamic landscape, we delivered another quarter of solid top line growth driven by continued momentum in the Personal Systems commercial business. However, due to additional tariff costs that could not be fully mitigated in the quarter, our non-GAAP operating profit fell short of expectations...We continue to expect the PC market will grow in 2025, but softer than originally planned, driven by increased macro uncertainty...In Print, we continue to expect the market to decline, low single digits for calendar year 2025."

18) From Okta: "We continue to take a prudent approach to forward guidance that factors in our go-to-market specialization that was rolled out in Q1 of FY26. Additionally, we're now factoring in potential risks related to the uncertain economic environment for the remainder of FY26."

19) From Booz Allen Hamilton: "The federal government is rethinking agency missions, finding ways to accomplish those missions differently and looking for ways to reduce spending and increase efficiency. To get there, we are seeing agency reorganizations, reductions in government personnel and spending levels, as well as contract reviews. These are especially acute in civilian agencies, and as a result, we are seeing a decrease in the pace of awards in civil, as well as run rate changes in some of our contracts. At the same time, the government is leading initiatives to improve procurement regulations and practices, such as the revision of the Federal Acquisitions Regulation or FAR and we expect to see more contracts move to fixed price and outcome based."

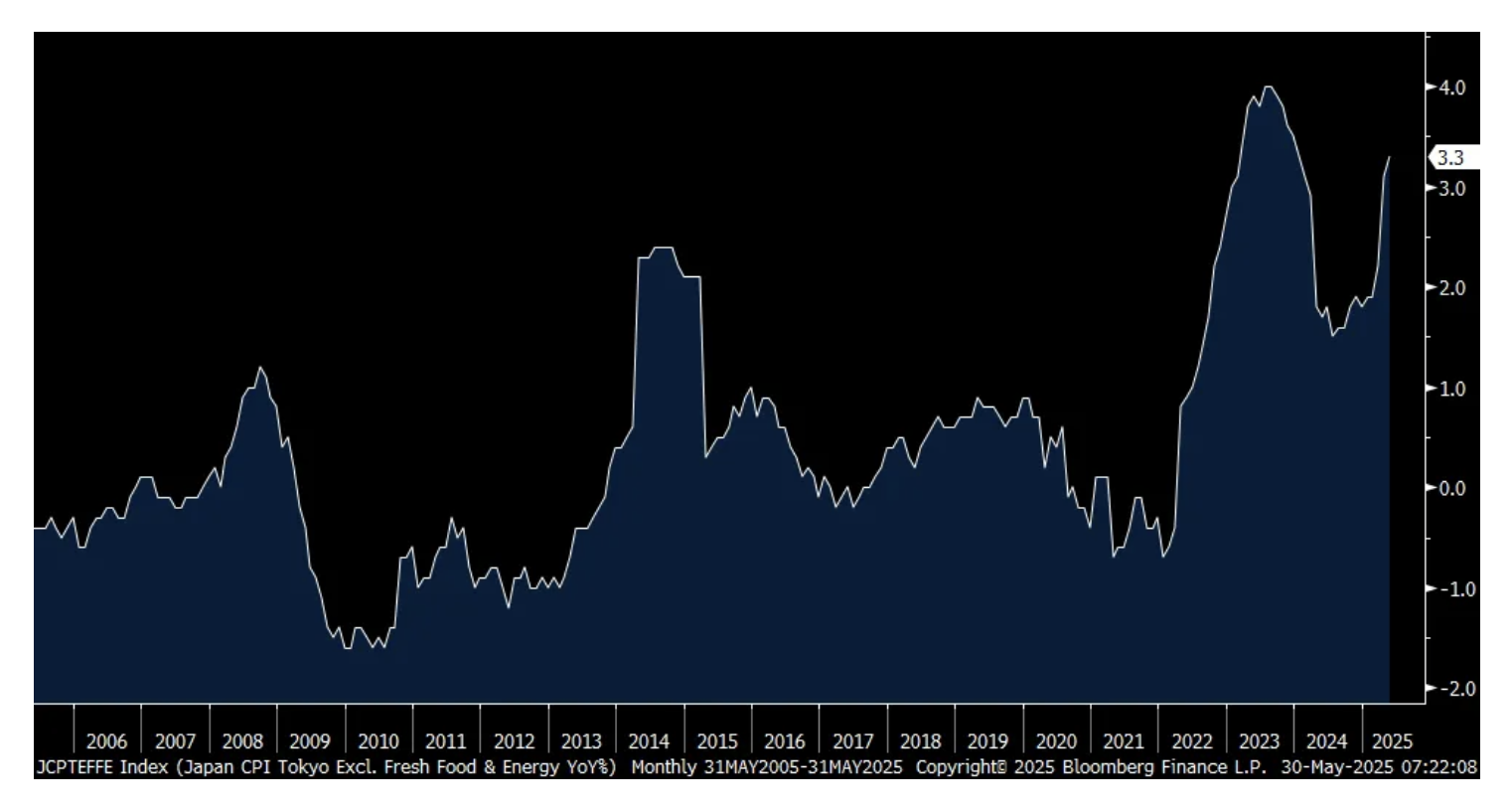

20) Consumer price inflation in Japan remained hot in May. Tokyo CPI rose 3.3% y/o/y ex food and energy, up from 3.1% in April and one tenth above expectations. The headline rate was higher by 3.4% y/o/y. Due to a spike in the price of rice, food costs rose 5.8% y/o/y.

21) Germany's May CPI rose 2.1% y/o/y, one tenth more than expected.