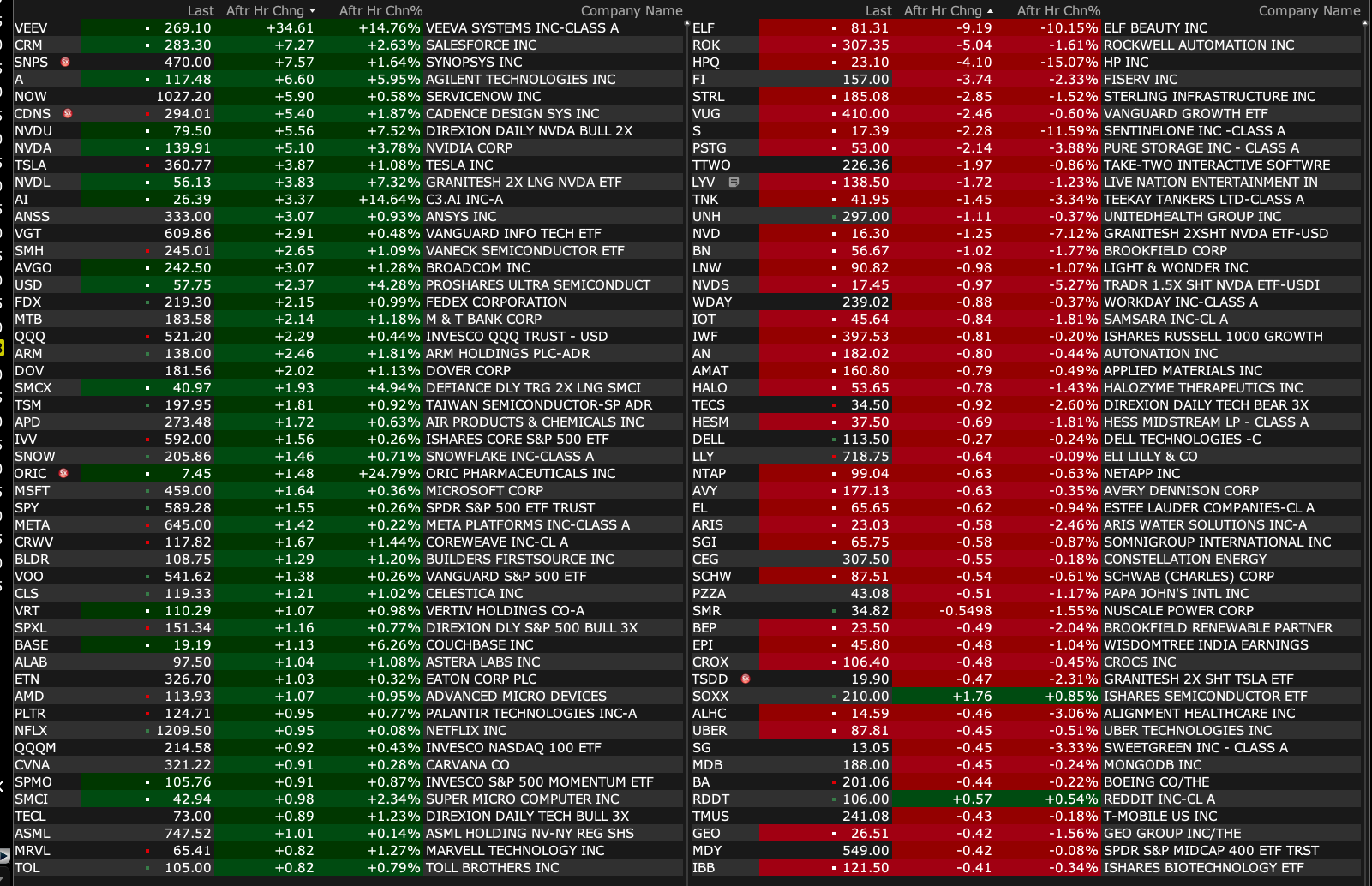

Wednesday's After-Hours Movers

As of 4:22 p.m. (Post NVDA Release)

BY Doug Kass · May 28, 2025, 4:41 PM EDT

As of 4:22 p.m. (Post NVDA Release)

BY Doug Kass · May 28, 2025, 4:41 PM EDT

BY Doug Kass · May 28, 2025, 4:34 PM EDT

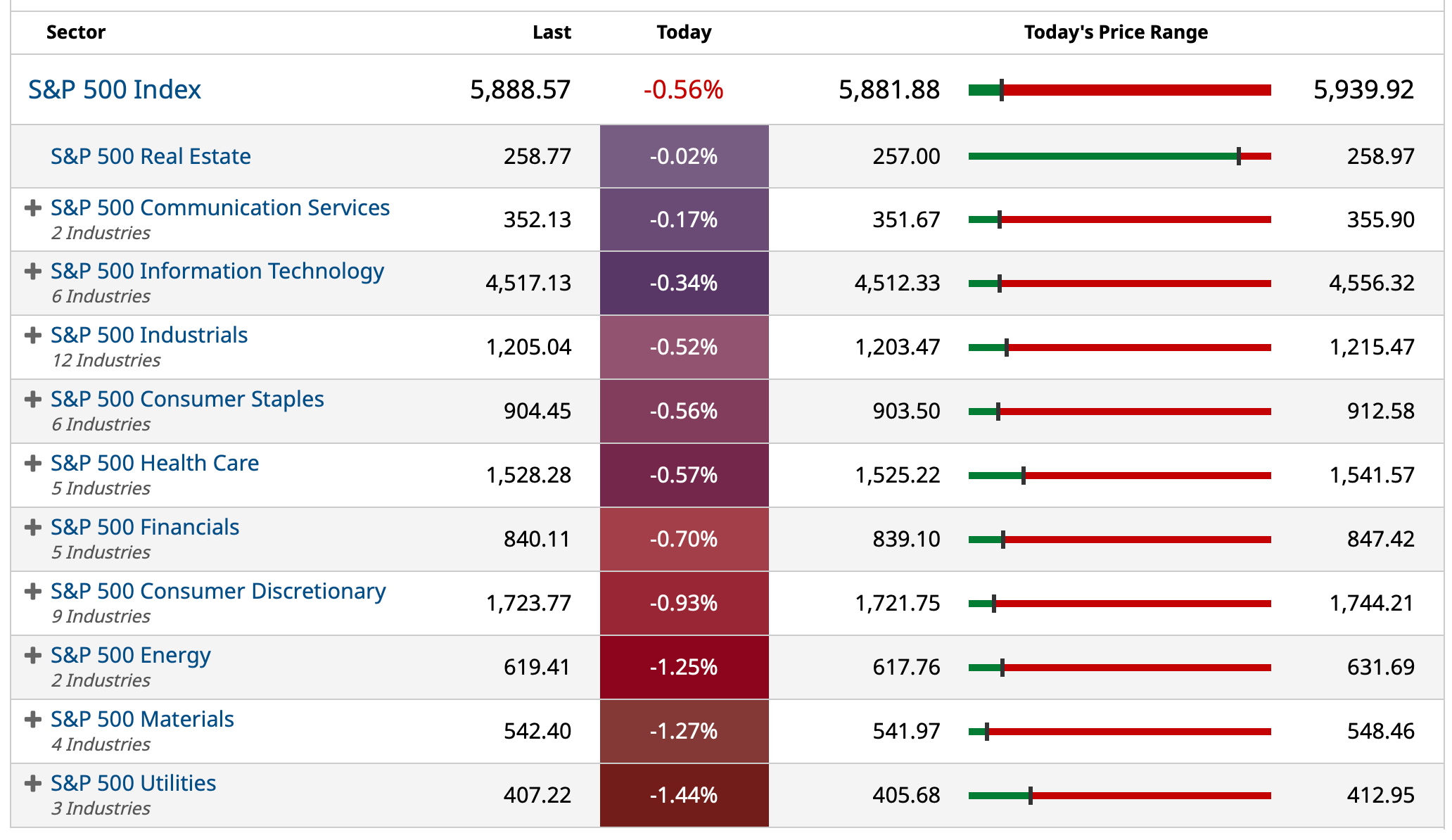

Now out of SPY and QQQ shorts as market continues to fall.

BY Doug Kass · May 28, 2025, 3:59 PM EDT

With S&P cash -38 handles (a near -50 swing from the highs) I am reducing my index shorts from small to very small:

Covered a portion of my SPY $587.52 and QQQ $518.51.

BY Doug Kass · May 28, 2025, 3:58 PM EDT

President Trump orders U.S. chip designers to cease China sales — from the Financial Times!

BY Doug Kass · May 28, 2025, 3:28 PM EDT

I just added to index shorts: SPY $590.50 and QQQ $522.22.

BY Doug Kass · May 28, 2025, 3:23 PM EDT

Briefing.com on Nvidia NVDA EPS:

NVIDIA: Earnings Preview; its $5.5 bln charge could lead to some confusion; commentary on H20 chips, tariffs and Blackwell will be key

NVIDIA (NVDA) is set to report Q1 (Apr) results today after the close with a call to follow at 5pm ET. The AI chip giant typically reports earnings around 20 minutes after the close. The current FactSet consensus calls for adjusted EPS to come in at $0.73 while revenue is expected to grow 66% yr/yr to $43.34 bln. NVDA tends to provide revenue and gross margin guidance for the next quarter. Current guidance for Q1 stands at revenue of $42.14-43.86 bln and non-GAAP gross margin of 70.5-71.5%.

BY Doug Kass · May 28, 2025, 3:20 PM EDT

I covered shorts of IWM $205.58 and RSP $176.11 on the whoosh lower — for a profit.

BY Doug Kass · May 28, 2025, 3:01 PM EDT

From Peter Boockvar:

FOMC minutes a yawner but they lay out again the challenge they face

Markets didn’t blink upon the release of the FOMC minutes from their meeting three weeks ago, which came a week before the cool down in the US/China tariff battle, because it revealed nothing new. They are in the dark as much as the rest of us are for both what will be left of the tariffs, after whatever deals will be announced, and what the flow through impact will be on growth and inflation.

They said, “Participants observed that there was considerable uncertainty surrounding the evolution of trade policy as well as about the scale, scope, timing, and persistence of associated economic effects. Significant uncertainties also surrounded changes in fiscal, regulatory, and immigration policies and their economic effects. Taken together, participants saw the uncertainty about their economic outlooks as unusually elevated.”

And in this one sentence lies their current challenge, “Participants noted that the Committee might face difficult tradeoffs if inflation proves to be more persistent while the outlooks for growth and employment weaken.”

Bottom line, for the first time in decades, the Federal Reserve is no longer that support crutch as the current macro circumstances we are currently traveling through are quite different with the particular challenge of further calming the post 40 yr high in inflation to a sustainable pace of 2% with tariffs as the fresh curveball all while economic growth has slowed to about 1% on average, estimated for the first half of 2025.

Looking to year end, the fed funds futures is only fully priced for one cut with a 72% chance priced in for a 2nd.

BY Doug Kass · May 28, 2025, 2:25 PM EDT

Bond prices under pressure, again today:

* The yield on the 2-year Treasury note is +5 basis points to 4.00%.

* The yield on the 10-year Treasury note is +5 basis points to 4.49%.

* The yield on the 30-year Treasury bond is +4 basis points to 4.99%.

BY Doug Kass · May 28, 2025, 1:21 PM EDT

Housekeeping item.

I just covered half of my Tempus AI TEM short at $53.96 (-$12).

From this morning:

* Added to (TEM) short $64.30.

By Doug Kass May 28, 2025 9:33 AM EDT

I have been short (TEM).

This morning Spruce Point Capital Management LLC published a short report: Tempus AI, Inc - Spruce Point Capital Management LLC

Position: Short TEM VS

By Doug Kass May 28, 2025 9:33 AM EDT

BY Doug Kass · May 28, 2025, 1:08 PM EDT

From Charlie!

BY Doug Kass · May 28, 2025, 11:25 AM EDT

BY Doug Kass · May 28, 2025, 10:50 AM EDT

* Emotion is taking the market over

* Downside market risk likely exceeds upside market reward by almost 3-1

It's over and done but the heart-ache lives on inside

And who's the one you're clinging to instead of me tonight

And where are you now

Now that I need you

Tears on my pillow wherever you go

I'll cry me a river that leads to your ocean

You never see me fall apartIn the words of a broken heart

It's just emotion that's taken me over

Tied up in sorrow, lost in my soul

But if you don't come back

Come home to me, darling

You know that there'll be nobody left in this world to hold me tight

Nobody left in this world to kiss goodnight

Goodnight

Goodnight

- Bee Gees - Emotions (Original)

The advance in equities over the last month has materially changed the upside reward vs. downside risk for the S&P 500 Index.

Currently, I view less than 5% upside compared to 10%-15% downside -- an increasingly unattractive ratio of nearly three to one.

I am respectful of the market's extraordinary price momentum (over such a short term time frame), however, I plan to put a larger short stake in the ground on any further.

Going against the consensus grain and the herd is nothing new to me.

For the reasons mentioned in "Rethinking American Exceptionalism" and in this weekend's Barron's column (and for other reasons) I remain profoundly bearish:

* Political and geopolitical polarization and competition will probably translate into less political centrism and a reduced concern for deficits -- creating structural uncertainties, limited fiscal discipline and imprudence around the globe ... and for the possibility of bond markets to "disanchor"

* The cracks in the foundation of the Bull Market are multiple and are deepening, but they are being ignored (as market structure changes have led to price momentum (FOMO) being favored over value and common sense)

* Investors dance like Zorba the Greek (1964), Citigroup's Chuck Prince (2007) and Prince (1999) while the U.S. spends gluttonously

* Valuations and (consensus) expectations for economic and corporate profit growth are all inflated

* Being dismissed are JPMorgan CEO Jamie Dimon's dour comments on complacency and his view that the corporate credit market is "ridiculously over-stretched" (hat tip Rosie)

* Look for the soft data to move into (and weaken) the hard data led by a slowing housing market likely to provide ample near-term evidence of the exposure and vulnerability of the middle class

* Below trend-line economic growth with sticky inflation lie ahead ("slugflation") - uncomfortable for a Federal Reserve which has to make increasingly more difficult decisions

BY Doug Kass · May 28, 2025, 10:15 AM EDT

Here are today's "early things":

* Shorted more SPY $590.90 and QQQ $521.44

* Shorted ARKK $58.32.

*Shorted more GRNY $20.93.

* Added to TEM short $64.30.

* Added to TSLA short $365.44.

* Reshorted RSP $177.52 and IWM $207.73.

BY Doug Kass · May 28, 2025, 10:02 AM EDT

Kdog88

37 minutes ago

Dougie….would love your thoughts on Rosie’s tweet. Seems arbitrary to me, but maybe I am missing something.

Dougie Kass

STAFF

Just Now

i think it is nearly entirely improved because of the vigorous market recovery i tend to discount this number as a lagging indicator, kdog

BY Doug Kass · May 28, 2025, 9:45 AM EDT

Pressed TSLA short at $366.

BY Doug Kass · May 28, 2025, 9:36 AM EDT

I have been short TEM.

This morning Spruce Point Capital Management LLC published a short report: Tempus AI, Inc - Spruce Point Capital Management LLC

BY Doug Kass · May 28, 2025, 9:33 AM EDT

-SPRO +249% (PIVOT-PO Phase 3 trial on cUTIs met primary endpoint and will stop early for efficacy)

-BROG +54% (announces proposed sale of BPGIC FZE and BPGIC Phase III FZE for $125.3M in cash)

-ANF +27% (earnings, guidance)

-ITOS +19% (intends to wind down operations; Exploring potential asset sales including EOS-984, EOS-215, and a preclinical obesity program targeting ENT1)

-MNRO +19% (earnings)

-MTN +12% (Rob Katz to return as CEO, effective immediately; expects FY25 Resort Reported EBITDA to be in lower-half of prior guidance)

-JOBY +11% (Toyota confirms 15.3% stake after Joby closes $250M investment from Toyota)

-BOX +9.7% (earnings, guidance)

-MBLY +5.3% (announces Mobileye Imaging Radar Chosen by Global Automaker for Eyes-Off Driving)

-DKS +4.5% (earnings, guidance)

-M +4.1% (earnings, guidance)

-RKLB +3.1% (enters payload market by agreeing to acquire Geost for $275M in cash and stock)

-GME +2.9% (announced purchase of 4,710 BTC)

-REX +2.1% (earnings)

-CODI -14% (enters forbearance agreement with lender group)

-OKTA -12% (earnings, guidance)

-GLXY -7.3% (files to sell 29M public offering of common stock)

-PLAB -5.4% (earnings, guidance; CEO plans to retire with 1-2 years)

-EOLS -4.2% (announces departure of its CFO Sandra Beaver, effective Jun 13th)

-NCNO -3.6% (discloses 7% workforce reduction)

-CPRI -2.6% (earnings, guidance)

-BMO -2.1% (earnings)

-AZUL -2.0% (confirms initiates pre-arranged restructuring process in the United States to effectuate agreements including approximately US$1.6B in debtor-in-possession financing)

BY Doug Kass · May 28, 2025, 9:25 AM EDT

I will be reshorting IWM and RSP on the opening. (I covered both last week, at lower levels, for a profit).

BY Doug Kass · May 28, 2025, 9:05 AM EDT

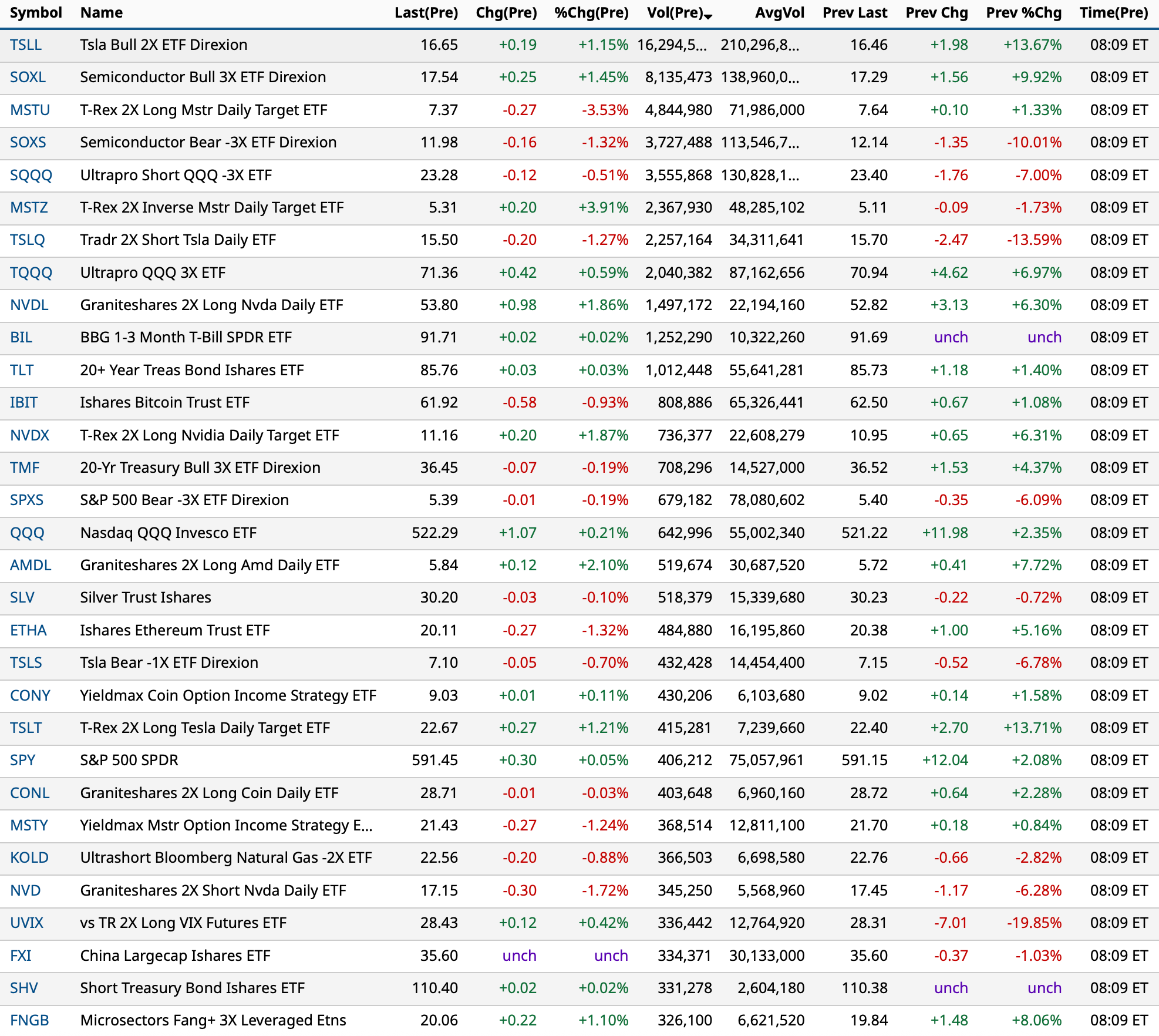

Charts from 8:09 a.m. ET:

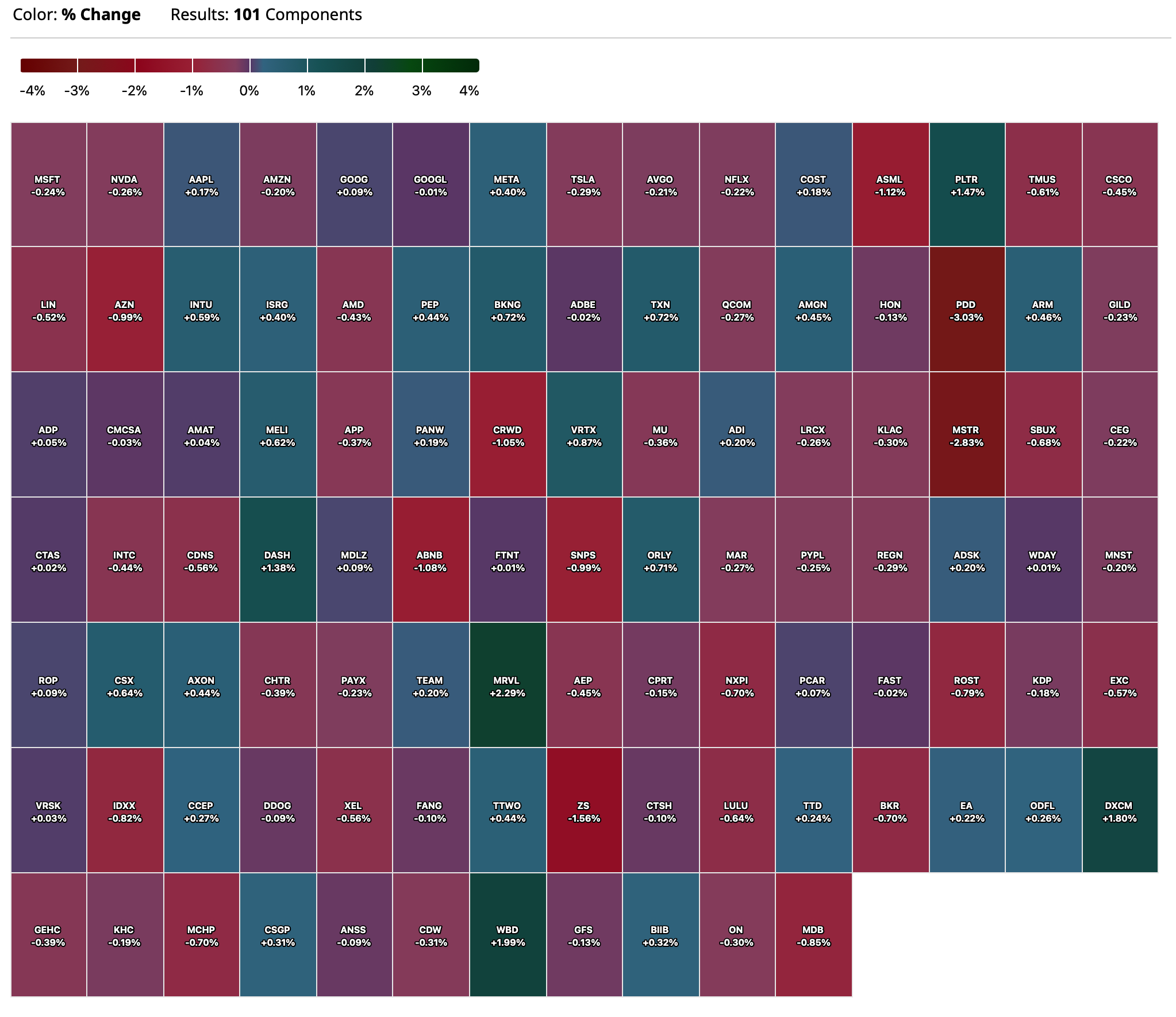

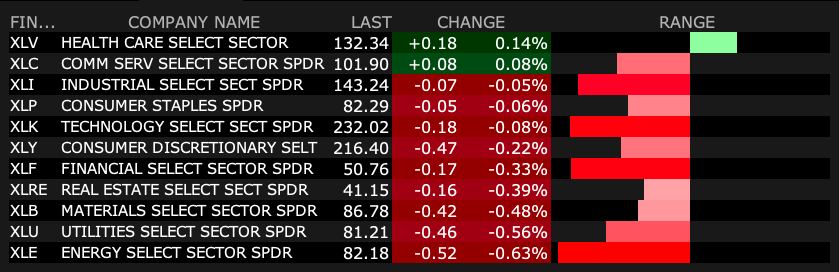

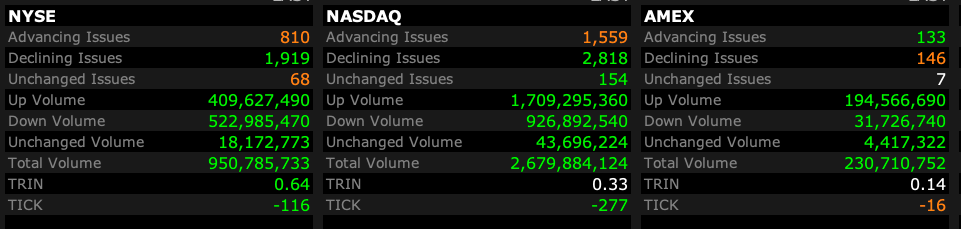

BY Doug Kass · May 28, 2025, 9:00 AM EDT

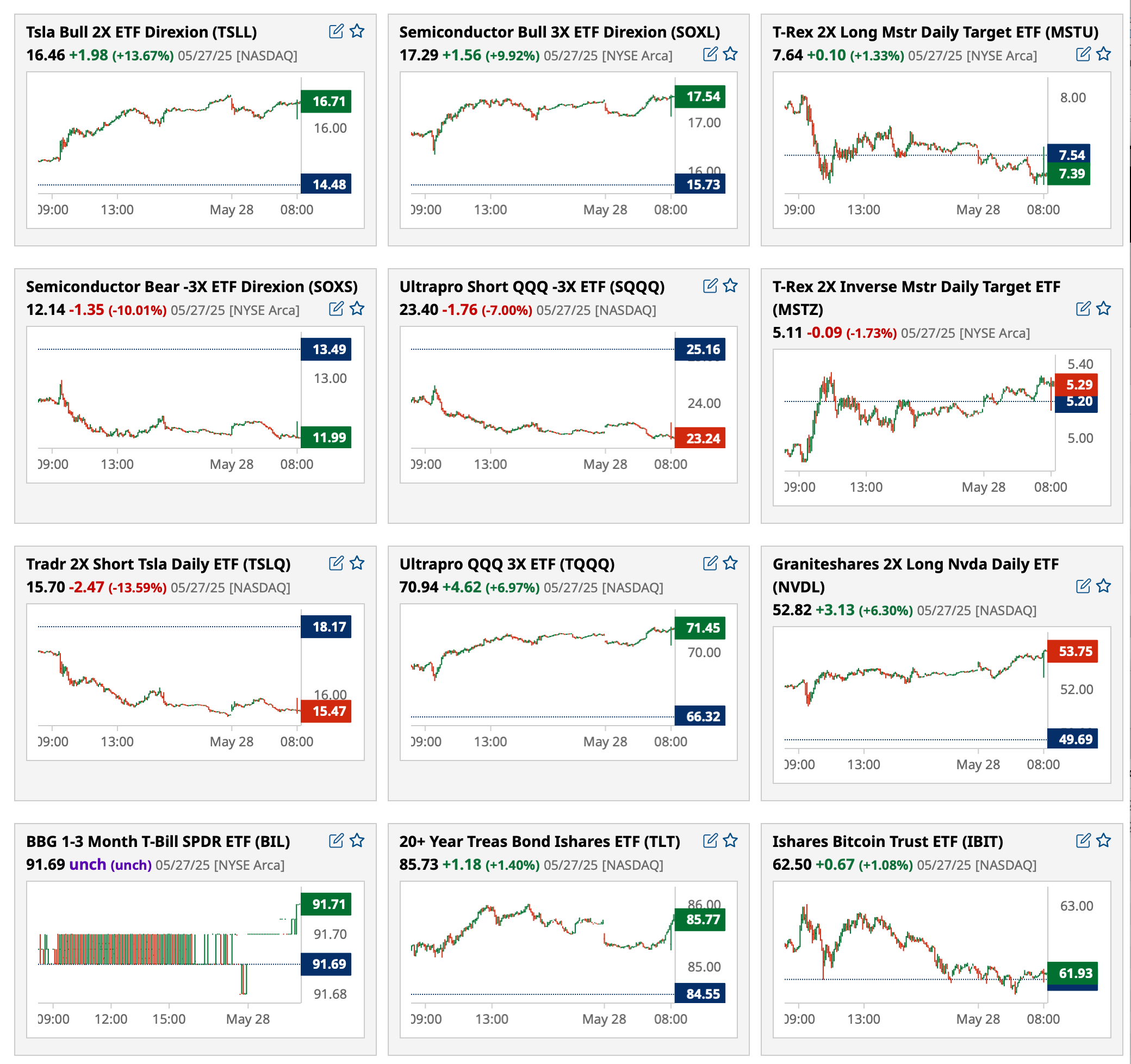

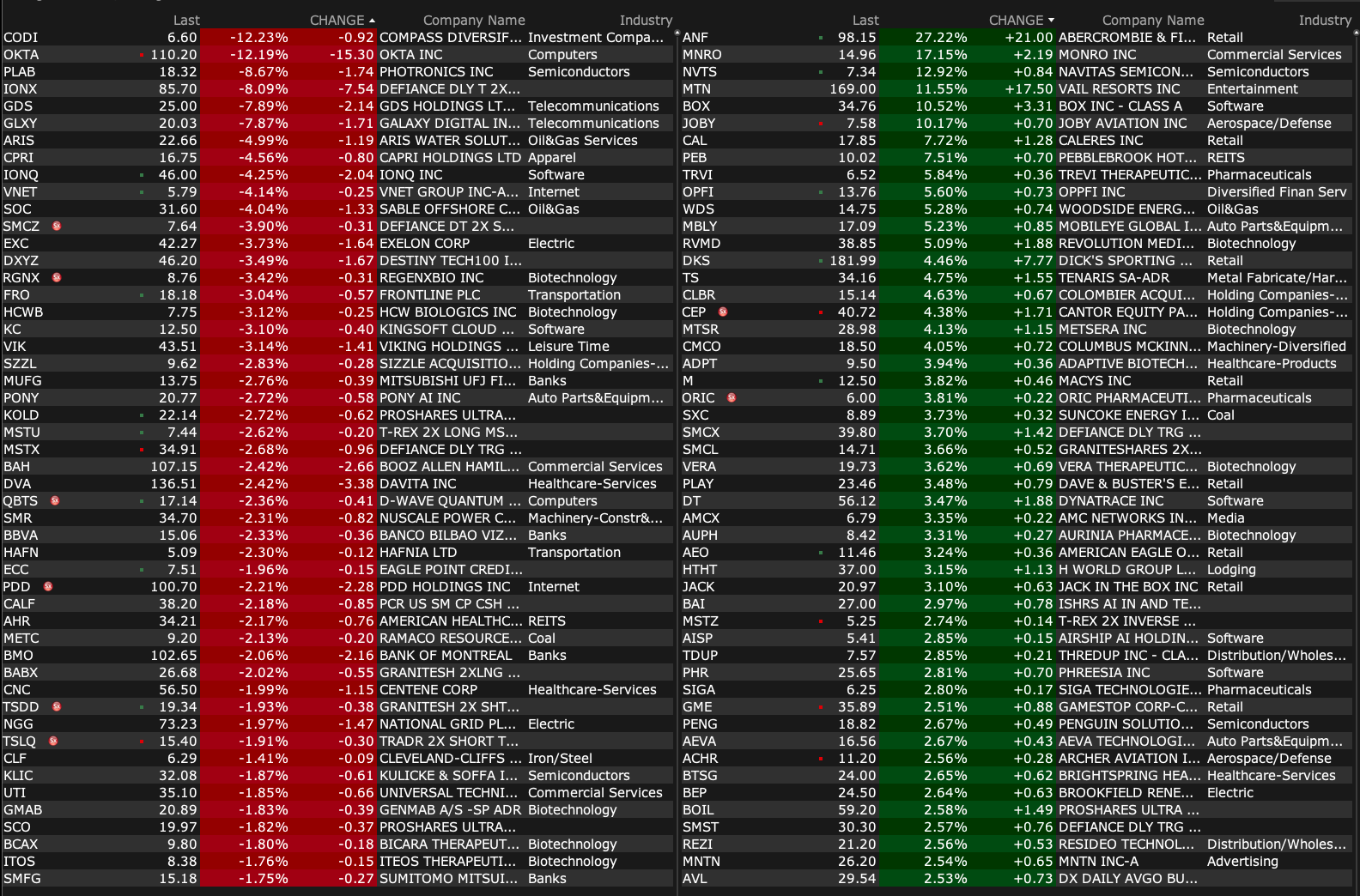

Premarket percentage movers at 8:28 a.m. ET:

BY Doug Kass · May 28, 2025, 8:50 AM EDT

BY Doug Kass · May 28, 2025, 8:41 AM EDT

From Peter Boockvar:

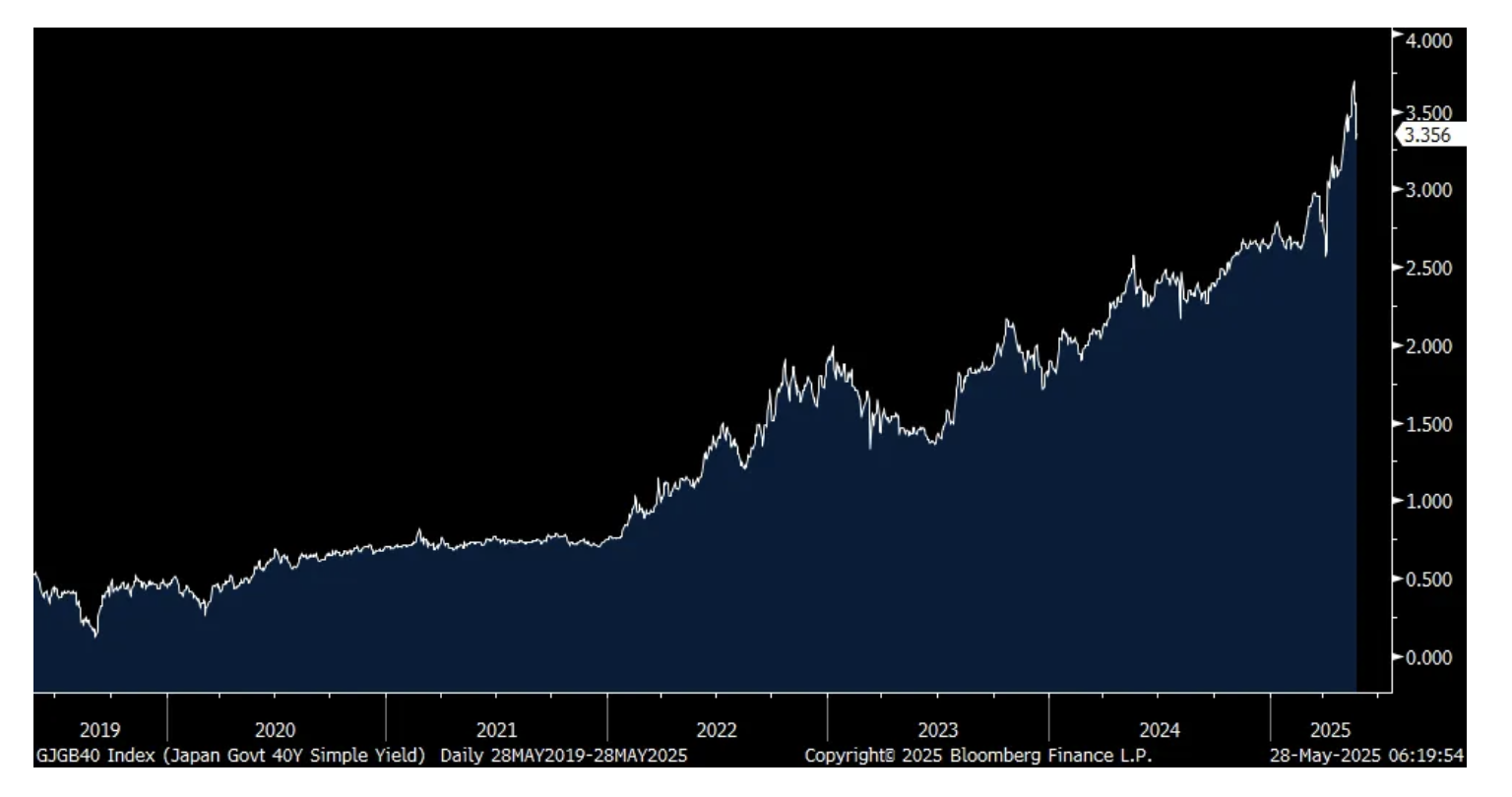

We learned again today that watching the results of Japanese bond auctions is a new thing we need to monitor because what happens there influences what happens here. The 40 yr JGB auction was not good. The bid to cover was just 2.21 vs 2.92 in the auction before and the lowest since July 2024. The 5 yr average is 2.54. Luckily yesterday's news on talk of a cut to long term JGB issuance cooled things down as the 40 yr yield rose just 3.3 bps in response to the weak auction. The 10 yr JGB yield rose by 4.5 bps, gaining back what it lost yesterday. Again, something to watch because European bonds are lower as are Treasuries following the JGB move.

By the way, BoJ Governor Kazuo Ueda was in front of the Japanese parliament and commented on what is going on in the JGB market but didn't say much in terms of substance. "If super long-term interest rates fluctuate significantly, we will keep in mind the possibility that such fluctuations could affect long-term or even short to medium term interest rates." It's not clear though at what level the BoJ steps in if this JGB selloff continues but on a mark to market basis, the BoJ is taking some big losses on its existing holdings.

40 yr JGB Yield

The helpful thing about going through the Dallas manufacturing index is not the headline figure, nor the very volatile internals but what companies in a variety of industries are saying themselves. Again, the May report was littered with tariff talk and I bolded for emphasis some things that stood out. By the way, the index was -15.3. It's been above zero just twice since early 2022 and those two months came right after the election.

Chemical manufacturing

The basic materials market is being impacted by the tariff uncertainties and overall lower consumer confidence levels as we work through the policy changes impacting the markets. "Uncertainty" is the key word, and getting to a "new norm" so that business planning and forecasts can stabilize sooner than later is our hope as we look out six months. Fiscal policy decisions on future interest rate adjustments to boost internal U.S. growth are a key factor in the basic materials markets as it relates to the building/construction and automotive sectors.

Decision-making remains extremely difficult due to extreme tariff uncertainty.

Computer and electronic product manufacturing

We are still seeing a slowdown in RFQs [requests for quotations] and new orders, but we believe that is largely due to the uncertainty related to tariffs. As new deals are announced, especially with China, we expect normal business activity and growth to resume. We are moving forward with our capital investment plans to support future growth.

I would say the uncertainty has decreased in the very short term (up to 90 days) based on the U.S.–China tariff rollback. However, it is hard to be certain of where we are heading next because the process has been so volatile. The rollback is helpful and more manageable for our business and should get us through the summer reasonably well, but we are quite uncertain of what a more lasting solution looks like. Will it be worse or better than what we see in the next 90 days? That remains to be seen.

We have had a couple of companies contact us recently to buy us. I think the industry is being bought out by private capital.

Fabricated metal product manufacturing

We have a large order delayed until 2026.

Food manufacturing

DOGE [Department of Government Efficiency] has killed us. Our customers are fighting tariff increases and dramatic funding cuts from USDA [U.S. Department of Agriculture] and USAID [United States Agency for International Development].

We are still worried about immigration and its impact on employment. We are also concerned about an upcoming recession.

It appears the customer has remained strong, but my perception of the general economy has gone down. President Trump’s tariff fight will only worsen the world's business activity.

Furniture and related product manufacturing

Some projects are on hold due to uncertainty in the global climate. There is a continued increase in business in hospitality, health care and data centers.

As a middle-market metal fabricator, we have witnessed policy unfavorably impacting demand. Unfortunately, raw materials costs are increasing from domestic suppliers, and our retail customers are in a complete quandary as they reorganize supply chains (many previously overhauled during/after the pandemic) and understand how the consumer is being impacted by the one-two punch of inflation and tariffs.

Business sucks.

Machinery manufacturing

We had our best month in two years and hope this trend continues.

It's a battle! We thought and anticipated things would be more stable, heading in the right direction, and far more productive by now. One-third into the new year and now we're thinking surely things will improve by year-end. It's admittedly frustrating and disconcerting not to have a better plan with greater confidence than what we have presently. Our sales team is kicking over every rock. Our operations team has squeezed every penny. It's just tough sledding in the here and now.

It looks like business is slowing down again.

Miscellaneous manufacturing

Tariffs [are an issue affecting our business].

The tariff situation is controlling our business to date.

Tariffs are causing us many issues: increasing costs as we try to increase U.S. manufacturing, and the price of components has increased.

Nonmetallic mineral product manufacturing

Forty-two percent tariffs on our product is much better than 157 percent. But it's still 42 percent. It cuts into profits and sales.

Paper manufacturing

Business is still moderately slow.

Primary metal manufacturing

We are making capital expenditures to open manufacturing processes for new product offerings.

We should be busier this time of the year, but orders are under last year's.

Printing and related support activities

We are fortunate to be full of work that was entered months ago and is seasonal to this time of year. We are working overtime and life is good; however, the other jobs that we should be doing are not out there at the moment. It seems all this chaos from the tariffs and ramblings out of Washington, D.C. have caused a rather big decline in activity in the graphic arts segment that we serve. If not for this large amount of seasonal work, we would be stupid slow. When we follow up with our customers, we are hearing the same thing: that they are slow and don't have any projects to send to us to work on.

Textile product mills

We did see orders pick up this month, but there is still a lot of uncertainty regarding tariff implications. Our suppliers haven't passed on price increases yet but have communicated that they are coming (levels and specifics to be determined). We are in a holding pattern until tariff deals are announced and we can react accordingly.

On to what some publicly traded companies said on their earnings calls.

From Autozone whose stock fell about 3.5% yesterday:

Domestic retail comps rose 3%, "which is the best retail growth we have reported since the second quarter of FY22." International comps grew by 8.1% y/o/y.

"we found the quarter's cadence to be somewhat predictable with the tax refund season's normal impact on sales...The variation being driven by our domestic DIY business with cooler weather and the Easter holiday shifting into our last four weeks vs last year, falling in the middle four week segment."

More on their DIY business. "While the macro environment and the uncertainty around tariffs have forced customers to be cautious with spending, the consistency of our failure and maintenance businesses continued this past quarter. We saw an improving trend in our maintenance and failure categories on a y/o/y basis. Discretionary categories, the smallest part of our business, have been under pressure for several quarters now. Historically, when our consumer is under pressure, our maintenance and failure categories begin to outperform discretionary categories."

"Our commercial comp, on the other hand, was more consistent over the 12 weeks of the quarter."

Okta is down 11% pre market on guidance that wasn't as robust as hoped for. "We continue to take a prudent approach to forward guidance that factors in our go-to-market specialization that was rolled out in Q1 of FY26. Additionally, we're now factoring in potential risks related to the uncertain economic environment for the remainder of FY26."

More behind this. "What we are putting in it thinking about it going forward - there's just a feeling in the environment, if you will. I don't have a lot of quants to back up what I'm saying. It's more based on customer conversations, reading the news, talking to the sales teams. It's just out there and we're just - the tone feels like it's changed. We're not saying it's absolutely certain, but what we're saying is that we're putting it into the guidance."

Macy's just reported a better than expected quarter but with comps still negative and they lowered full year guidance "to account for several factors including: initial and current tariffs; some moderation in consumer discretionary spending; and a heightened competitive promotional landscape."

Dicks Sporting Goods reported slightly better earnings and maintained its guidance. “We are reaffirming our 2025 outlook, which reflects our strong start to the year and confidence in our strategies and operational strength while still acknowledging the dynamic macroeconomic environment.”

With the average 30 yr mortgage rate approaching 7% again, at 6.98%, refi’s fell 7.1% w/o/w, down for a 3rd week but purchase apps were higher by 2.7% w/o/w.

BY Doug Kass · May 28, 2025, 8:19 AM EDT

Knowledge@Wharton... "How Science Can Fix Its Trust Problem"

BY Doug Kass · May 28, 2025, 7:31 AM EDT

I am reshorting TSLA at $365.22.

BY Doug Kass · May 28, 2025, 7:10 AM EDT

I was mentioned in Barron's over the weekend:

BY Doug Kass · May 28, 2025, 6:59 AM EDT

Bonus — Here are some great links:

BY Doug Kass · May 28, 2025, 6:34 AM EDT

In premarket trading I am expanding my index shorts, with the objective of moving to medium-sized (shorting on a scale higher):

* SPY $590.47

* QQQ $520.91

BY Doug Kass · May 28, 2025, 6:24 AM EDT

While I am respectful of the strong market momentum (to the upside) I believe the market's upside is dwarfed by the downside now:

* I reinitiated a small Index short in SPY at $591.37 and QQQ at $521.39.

* I added to ARKK short at $58.

* I added to GRNY short at $20.90.

* I added to several individual short equity names (that I have not disclosed) at the close of trading on Tuesday.

BY Doug Kass · May 28, 2025, 6:05 AM EDT

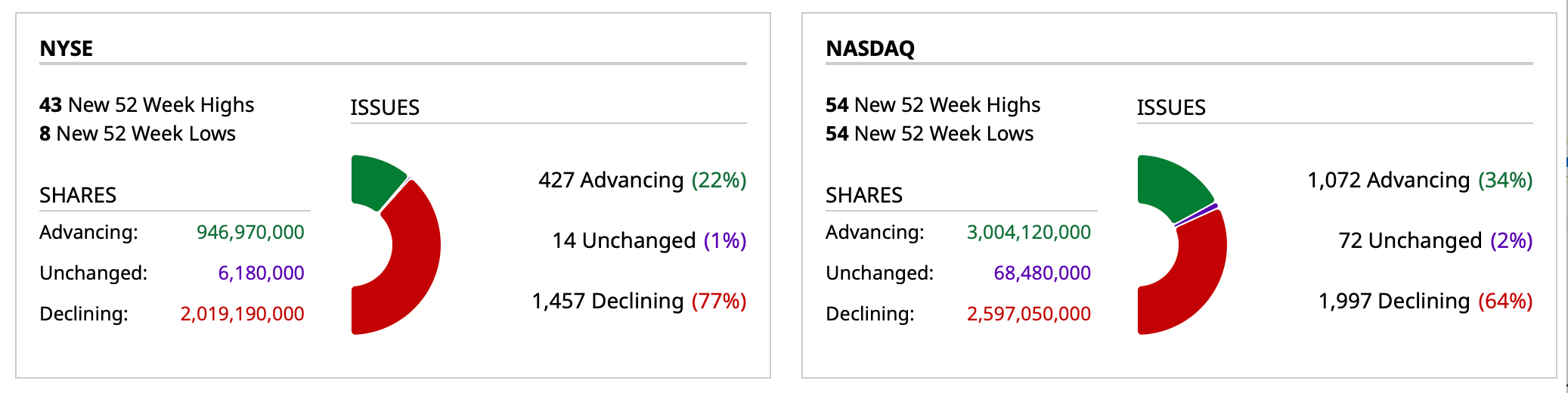

The S&P Short Range Oscillator remains overbought — but only slightly so.

1.24% vs. 0.97%.

BY Doug Kass · May 28, 2025, 5:55 AM EDT

I apologize for yesterday's disappearance but our office was without power and internet all day.

BY Doug Kass · May 28, 2025, 5:45 AM EDT