Friday's Closing Market Stats

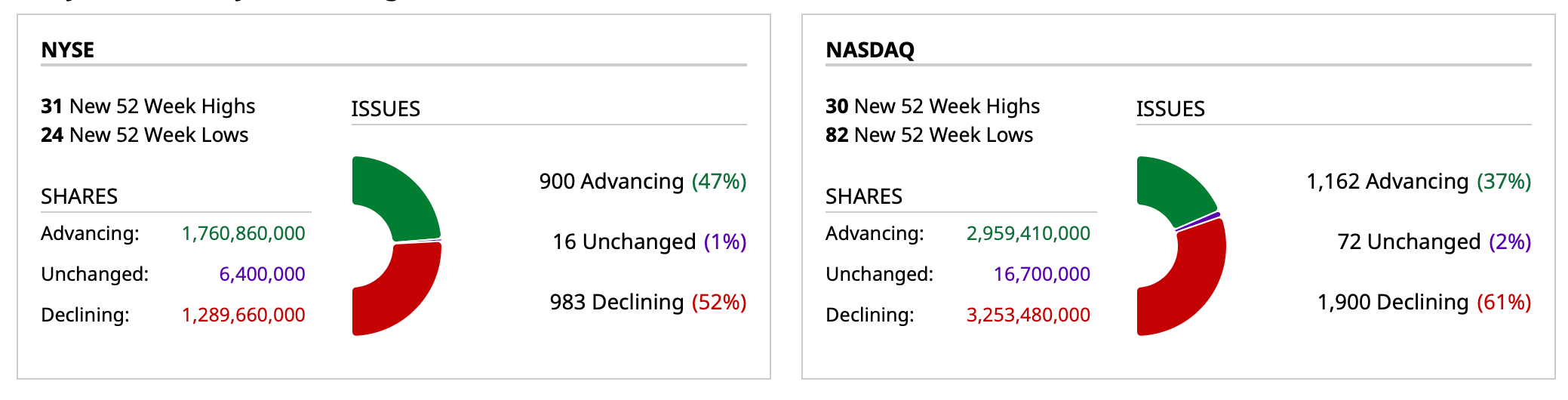

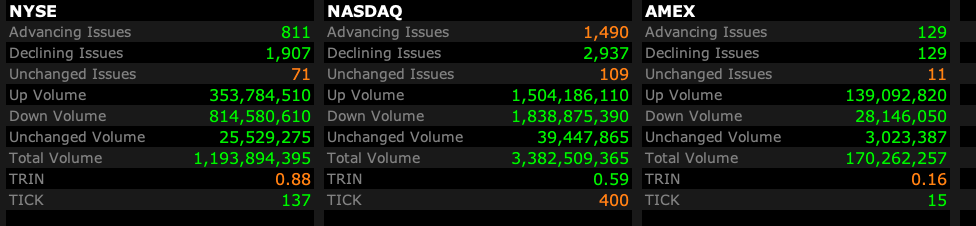

Closing Breadth

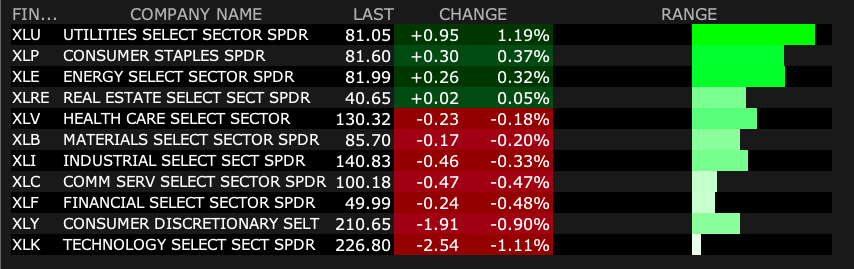

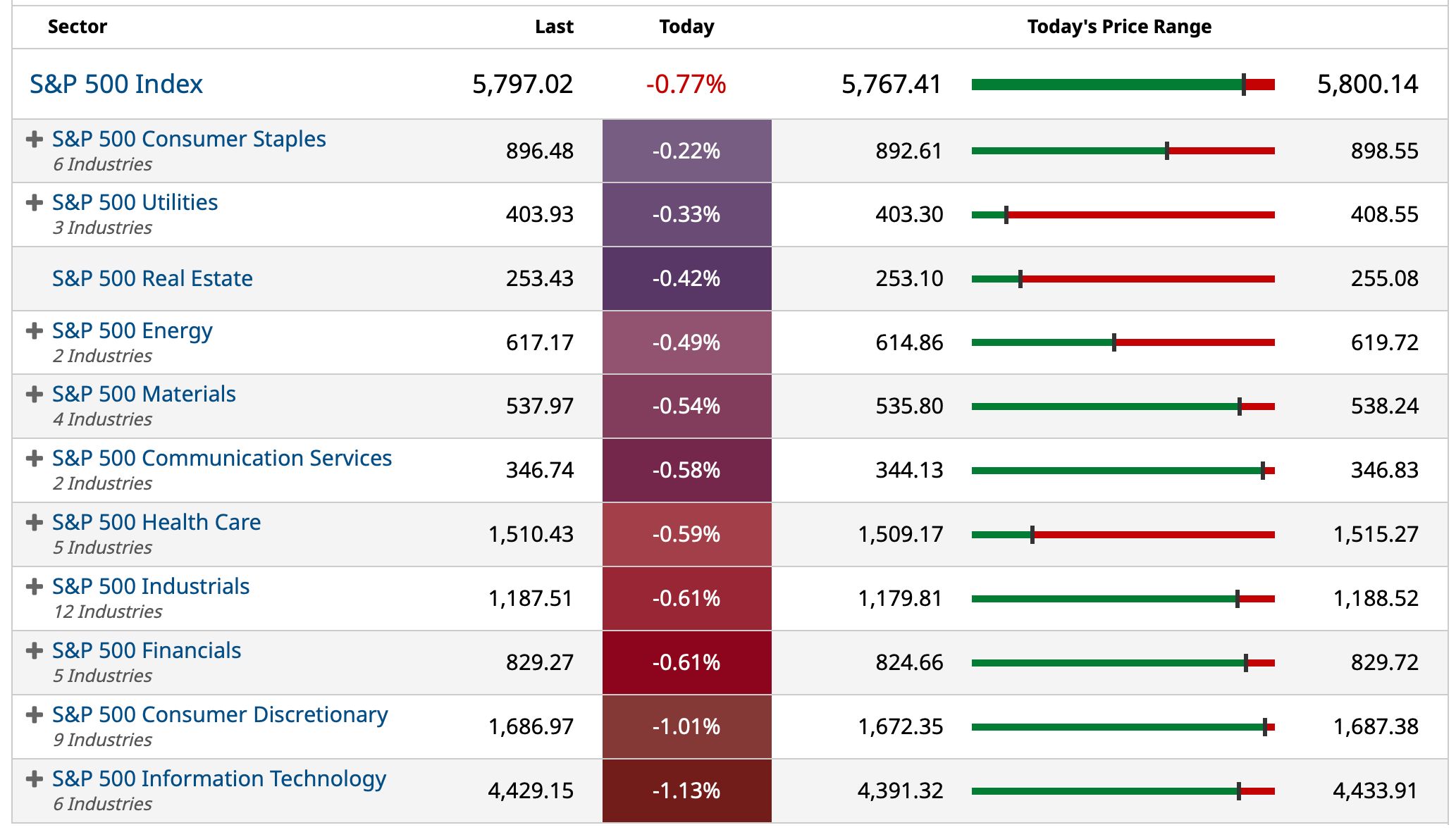

S&P 500 Sector ETFs

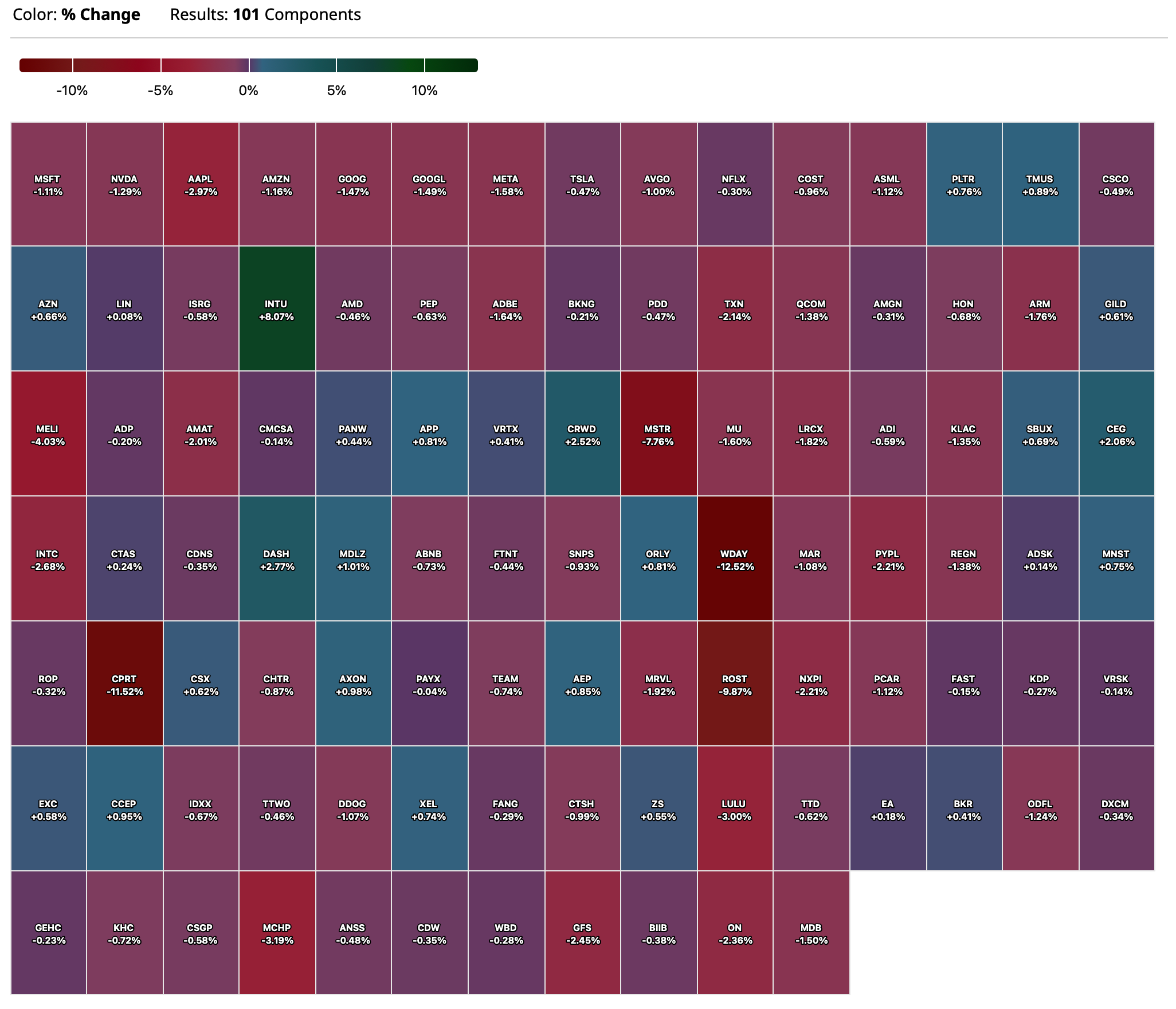

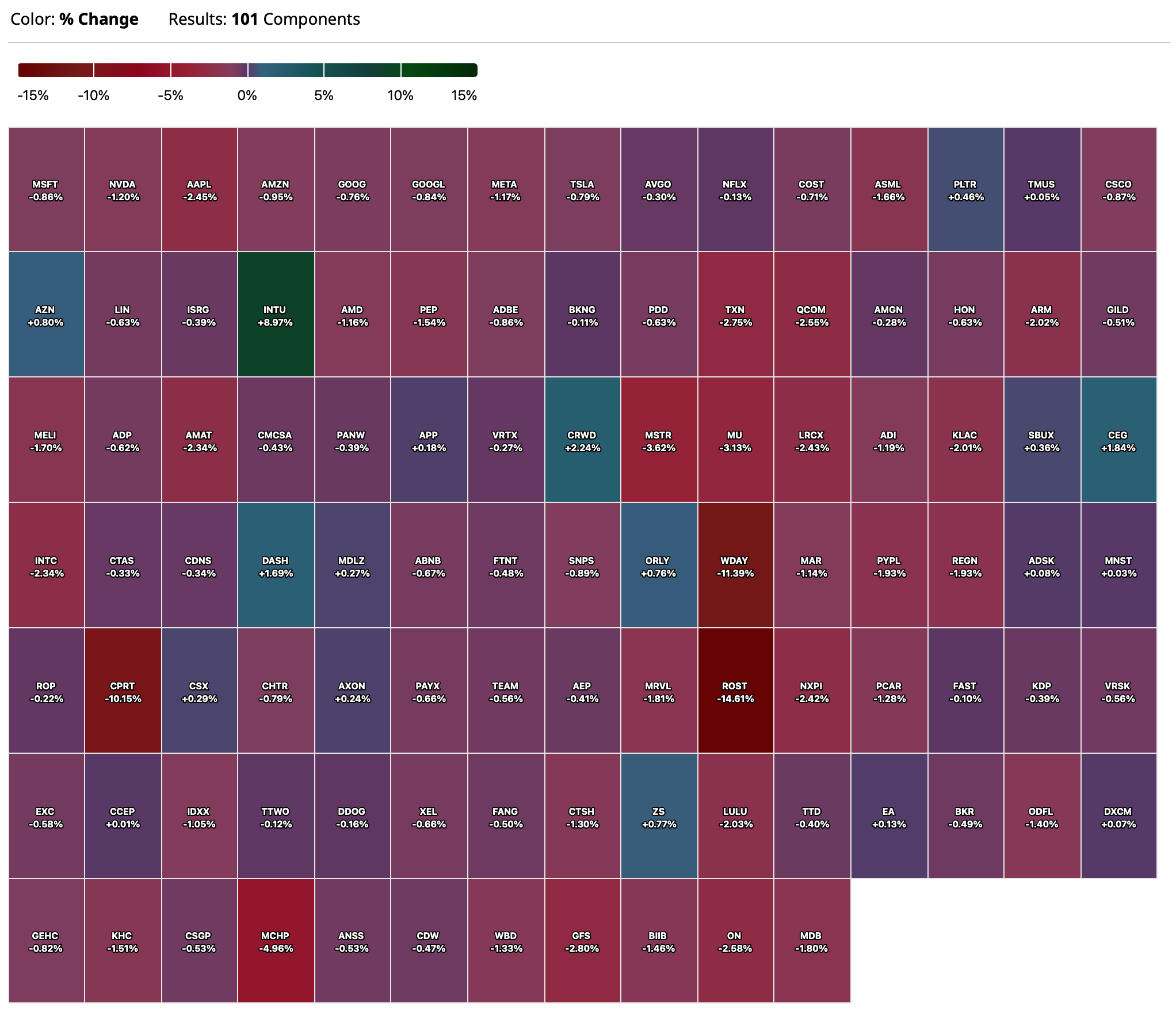

Nasdaq 100 Heat Map

BY Doug Kass · May 23, 2025, 4:38 PM EDT

BY Doug Kass · May 23, 2025, 4:38 PM EDT

Thanks for reading my Diary today, all week and since 1997 (!).

I hope my "stuff" had value to all of you.

Enjoy the long holiday weekend.

Be safe.

BY Doug Kass · May 23, 2025, 3:46 PM EDT

BY Doug Kass · May 23, 2025, 3:22 PM EDT

BY Doug Kass · May 23, 2025, 3:10 PM EDT

This is not an SNL short or Spinal Tap sort of mockumentary. Way too much $ slooshing around AI...

BY Doug Kass · May 23, 2025, 3:05 PM EDT

BY Doug Kass · May 23, 2025, 2:57 PM EDT

BY Doug Kass · May 23, 2025, 2:23 PM EDT

BY Doug Kass · May 23, 2025, 1:55 PM EDT

* Cannabis ETF MSOS owns 36 million shares

In my industry review of cannabis, "Cannabis' Weak Foundation, Uncertain Future and Continuing Challenges," I was critical of the industry's largest ETF, MSOS.

Here is what I wrote (note boldface):

Investing In Cannabis

* Construct your own portfolio of financially and operationally strong cannabis companies

* Avoid the MSOS ETF (MSOS) When I began to invest in cannabis my chosen vehicle was MSOS — the industry's largest ETF (by far!). MSOS traded actively and the shares were readily and easily tradeable. It took me years to conclude that I would rather invest in individual cannabis stocks rather than MSOS.

* To begin with, I would rather structure my own ETF by creating my package vis a vis the MSOS manager's selected holdings. I don't need to pay a fee if I can more efficiently construct my own cannabis portfolio.

* I have too often seen the MSOS portfolio manager dispose of positions in the best companies (e.g. Green Thumb) and using those positions as an ATM to fund third and fourth tier cannabis holdings (and perhaps inadvertently providing an "out" for insiders in the process!).

* On that score, for years the MSOS ETF has had positions in certain cannabis holdings that are likely to fail or be so diluted out in financings that equity holders feel like the company has gone bankrupt!

* A relatively liquid MSOS whose constituent holdings are illiquid could lead to manipulation. I can't be certain but my guess is that there has been some unsavory actors contributing along the way to MSOS shares falling from above $50/share to about $3/share. Frankly, given that the components of MSOS are illiquid, I do think (though it is hard to prove) that the industry would have been better off if MSOS never existed. MSOS has clearly become the tail that wags the cannabis dog.

Today 4Front FFNTF filed for a court-appointed receiver All 4Front Subsidiaries File for Court-Appointed Receiver and News - 4Front Ventures

MSOS owns 36 million shares of the company:

Jason Spatafora on X:

Enough said.

BY Doug Kass · May 23, 2025, 1:45 PM EDT

From Peter Boockvar:

Positives,

1) The May US manufacturing and services composite PMI rose to 52.1 from 50.6 with both components higher m/o/m with the former rising to 52.3 from 50.2 and the latter at 52.3 from 50.8. The bottom line from S&P Global, “Business confidence has improved in May from the worrying slump seen in April, with gloom about prospects for the year ahead lifting somewhat thanks largely to the pause on higher rate tariffs…However, both sentiment and output growth remain relatively subdued, and at least some of the upturn in May can be linked to companies and their customers seeking to front run further possible tariff related issues, most notably the potential for future tariff hikes after the 90 day pause lapses in July.” And to sum up on pricing, “The overall rise in prices charged for goods and services in May was the steepest since August 2022, which is indicative of consumer price inflation moving sharply higher.”

2) Initial claims fell to 227k from 229k and that was 3k below expectations. The 4 week average is now 232k vs 231k in the week before.

3) New home sales in April, measuring contract signings, totaled 743k, 48k above expectations but completely offset by a 54k downward revision to March to 670k.

4) From BJ's Wholesale: "The drivers of our business remain strong. Membership continues to grow nicely. Our continued improvements in merchandising and digital convenience are driving traffic, and we're gaining share in our clubs and gas stations."

5) From Williams Sonoma: Comps rose 3.4% y/o/y with all brands positive. "In the quarter, we saw an acceleration of the positive comp trend coming out of Q4, despite consumer distraction with tariffs, continued geopolitical uncertainty, and no material improvement in the housing market."

6) From Advance Auto Parts: "After a challenging start to the year for the industry, we began to see demand rebound in late February led by our Pro business. For the quarter, Pro grew in the low single digit range, including 8 consecutive weeks of positive comparable sales growth in the US. This positive momentum in Pro has continued during the first four weeks of Q2, driven by our focus on providing exceptional service."

7) From Ralph Lauren: Both top and bottom line exceeded their expectations. "This strong performance was broad based, driven by every geography and channel. For the full year, we delivered 8% top line growth, including record revenues for our international businesses, Europe and Asia, which together now comprise the majority of total company revenues."

8) From Urban Outfitters: "Despite the noise in the headlines and the broader economic uncertainty, our customers continued to show resilience in Q1. We haven't seen any signs of a demand slowdown. In fact, customers were eager for fresh spring fashion, and our teams delivered from compelling assortments to standout store experiences and inspiring marketing. We exceeded their expectations. The result, positive comps across every brand and every segment."

9) From TJX: "Overall comp sales grew 3% at the high end of our plan. Every division, both in the US and internationally drove increases in comp sales and customer transactions...As always, we offered great value to our shoppers every day at each of our retail banners. Looking ahead, we are convinced that our value proposition and the flexibility of our business will continue to be a winning retail formula...Overall, comp sales growth was almost entirely driven by an increase in customer transactions. Comps in both our apparel and home categories increased with home outperforming apparel."

10) From American Sports: Their US business is just 26% of total sales and they have an upper income customer. "Our performance was led by strong growth and profitability in both technical apparel and outdoor performance, as well as solid sales and margin results in ball and racquet. In addition to the continued broad based trends from our flagship brand Arc'teryx. I'd like to highlight the growing momentum behind the Salomon sneakers...Furthermore, our market leading hard goods equipment franchises delivered better than expected results for both winter sports equipment (particularly skiing) and the Wilson ball and racquet."

11) From Workday: "While there's heightened macro uncertainty, particularly across certain markets and verticals, we haven't seen this meaningfully impact our business and our growth prospects."

12) From Palo Alto Networks: "I think we're back to normal in a way. But there was, as you can imagine, not too far long ago, there were conversations around tariffs around the world. There were all kinds of supply chain shocks that were anticipated, which did cause some of our customers to think, oh my god, what's going to happen, next time I ship a car across the border, it's going to be twice as expensive, or I can't ship anything, what am I doing over here? So you saw that little sort of uncertainty in the market, which happened to be in the last month of our quarter."

13) From Viking Holdings: "given the current macroeconomic landscape, I'd also like to provide an update on how bookings are trending. When we last met in mid-March, we noted that January was the best booking month in the history of the company. We can also say that this was the best wave season in our history, with more guests booked and at higher pricing. Since wave, we are pleased to say this momentum has continued, specifically given 2025 is practically sold, and we look to future seasons, bookings in April and May are up y/o/y. In fact, May is off to an outstanding start with the last few weeks showing good bookings strength."

14) India remains an economic rock with its manufacturing and services May composite index higher by 1.5 pts m/o/m to 61.2.

15) The German May IFO business confidence index rose to 87.5 from 86.9 with all of the gain in the Expectations component while the Current Assessment fell slightly. The index is now at the highest level since June 2024 on the optimism with the outlook on the heels of the upcoming fiscal largess. IFO said "The German economy is slowing regaining its footing." Helping was a lift in the beleaguered manufacturing sector. IFO said "The upturn in sentiment was particularly strong in the food industry, while sentiment in the chemical industry deteriorated slightly."

16) The RBA cut rates by 25 bps as expected but alluded to the discussion of 50 bps. They have room to move.

Negatives,

1) Just when we thought we'd reached peak tariff uncertainty...

2) The US Federal Government no longer has a AAA credit rating from any of the three major agencies. Said Moody's, "This one-notch downgrade on our 21-notch rating scale reflects the increase over more than a decade in government debt and interest payment ratios to levels that are significantly higher than similarly rated sovereigns...Successive US administrations and Congress have failed to agree on measures to reverse the trend of large annual fiscal deficits and growing interest costs. We do not believe that material multi-year reductions in mandatory spending and deficits will result from current fiscal proposals under consideration. Over the next decade, we expect larger deficits as entitlement spending rises while government revenue remains broadly flat. In turn, persistent, large fiscal deficits will drive the government's debt and interest burden higher. The US' fiscal performance is likely to deteriorate relative to its own past and compared to other highly rated sovereigns."

3) Continuing claims, delayed by a week, remained elevated around the highest since November 2021 at 1.903mm vs 1.867mm in the week before.

4) From Shanghai to LA, the price of a 40 foot container went up by $61 to $3,197. The Shanghai to NY route saw a price gain of $177 to $4,527. But, it could have been worse in terms of increases.

5) From the Dallas Banking Conditions survey: "Loan volume grew slightly while loan demand was unchanged in May. Credit tightening continued, but loan pricing declined. Loan nonperformance decelerated sharply, increasing at the slowest pace since the end of 2022. Nevertheless, bankers reported a continued contraction in general business activity. Bankers are less optimistic about the outlook. On net, survey respondents still expect an improvement in loan demand and business activity six months from now, but that sentiment is less broad based than in previous months, and loan nonperformance is expected to increase."

6) The April US Architecture Billings Index fell further below 50 to 43.2 from 44.1 in March. Most notable was the drop to 40.5 from 45.1 in the commercial/industrial sector, joining multi-family residential around the 40 level. The chief economist there said, "Uncertainty as to the economic outlook continues to hold back progress on new construction projects. Despite the slowdown in billing activity, architecture firms continue to navigate this business cycle quite effectively, as staffing at firms remains relatively stable and project backlogs are holding up better than expected."

7) Mortgage applications fell 5.1% w/o/w. With a 6 bp rise in the average 30 yr mortgage rate to 6.92%, purchase apps fell 5.2% and refi's were lower by 5%.

8) While somewhat old news because contracts were signed months ago, existing home sales (measuring closings) totaled just 4mm home in April, around 30 yr lows and remaining below even the depressed levels in 2008/2009 and even with a bigger population. The positive for the first time buyer though is that inventories are rising, providing more choice and possibly lower prices to offset still high mortgage rates.

9) A weak 20 yr bond auction sends the 10 yr yield back above 4.50% and the 30 yr north of 5%.

10) JGB yields continue to pop higher. The catalyst this week was a weak 20 yr auction where the bid to cover fell to the least since August 2012 at 2.50 vs 2.96 in the prior auction. The tail of 1.14 is the most since 1987.

11) From Ross Stores: "From a pricing standpoint, we expect modest but broad based inflationary pressure across the retail industry, and we will remain focused on maintaining a substantial pricing umbrella below traditional retailers in order to deliver the bargains our customers have come to expect from us." As for full year guidance, "there are simply too many unknown variables that are limiting our visibility into the second half of the fiscal year, and we believe it is prudent to withdraw our previously provided annual guidance at this time...we have limited visibility on how customer demands may evolve over the balance of the year, given prolonged inflation, deteriorating consumer sentiment, and still elevated and potentially fluctuating tariff levels...And the impact of tariffs, we expect to start hitting the customer in the July, late June timeframe."

12) From Target: "For several years now we've seen pressure in our discretionary businesses as spending adjusted down from elevated levels during the pandemic and then moved further away in the face of historically high inflation in needs based categories. On top of those ongoing challenges, we faced several additional headwinds this quarter, including five consecutive months of declining consumer confidence, uncertainty regarding the impact of potential tariffs, and the reaction to the updates we shared on Belonging in January (the woke stuff they did) . While we believe each of these factors played a role in our first quarter performance, we can't reliably estimate the impact of each one separately...In planning for the remainder of the year, we believe it's prudent to expect that current top-line pressures will continue in the near term...As we've shared, for multiple quarters, consumers have been choiceful in their buying decisions, and recent declines in consumer confidence have made them even more cautious. They're focused on finding ways to save as they manage their family's budget. However, as we've noted before, consumers are still making discretionary purchases when they find products at the right intersection of style, quality, and value."

13) From BJ's Wholesale: "Our perishables, grocery, and sundries division delivered more than 4% comp growth in the first quarter, with unit volumes increasing across all three divisions...Our general merchandise and services division comps decreased slightly in the first quarter." With respect to how they will respond to tariffs, "We're always leaning into our model to deliver value, and while upward pressure on costs may drive prices higher, we are doing everything possible to minimize the impact to our members."

14) From Williams Sonoma: "We recognize that the housing market, and therefore the furniture industry, may remain soft this year, as interest rates are still high. Therefore, our growth strategy emphasizes a broad and inspirational non-furniture assortment, including seasonal and decorative accessories, textiles, and housewares."

15) From Home Depot: "Our customers engaged across smaller projects and in our spring events...However, the higher interest rate environment continues to pressure larger remodeling projects...we continue to see softer engagement in larger discretionary projects where customers typically use financing to fund the project such as kitchen and bath remodels."

16) From Lowe's: "And although we are pleased with our continued progress in customer services, our financial results also reflect ongoing pressure in DIY, bigger ticket, discretionary demand, and a slower start to spring versus last year, with exceptionally unfavorable weather across much of the country in February. As the weather normalized, we were encouraged by our business performance."

17) From Toll Brothers: "We experienced softer demand in the second quarter due to a decline in consumer confidence driven by increased economic uncertainty. These conditions have continued into our third quarter. In this environment, we believe prioritizing price and margin over pace makes the most strategic sense."

18) From Decker's: "As a result of macroeconomic uncertainty related to global trade policy, we will not be providing a formal outlook for fiscal year 2026 at this time...Based on the tariffs as of today's date, which are still subject to change, we expect to face an increase of up to $150 million to our cost of goods sold in fiscal year 2026 with a related yet to be determined impact to demand." They will take, like all other companies, mitigation efforts to offset this but "We also believe there is potential to see demand erosion associated with the combination of price increases and general softness in the consumer spending environment."

19) From Advance Auto Parts: "Shifting to DIY. During the 2nd half of Q1, we saw an improvement in DIY trends, although the weekly volatility continues to remain high. Maintenance related categories such as fluids, chemicals and oil are performing relatively better, suggesting that DIY consumers remain cautious in their overall spending. As we look ahead, we expect the DIY environment to remain challenged due to the potential for higher broad based consumer goods inflation impacting household budgets."

20) From Ralph Lauren: "We expect this year's performance to be heavily weighted to the first half of the year, notably Q1, with first half revenues up roughly mid single digits. While we have not seen a change in our underlying business trends from Q4 into Q1 to date, we believe it is prudent to take a more cautious view on the 2nd half of the year based on a number of macro indicators, notably the impact of tariffs, weakening consumer confidence in the US, and increased risk of a broader consumer pullback and a more uncertain global operating environment in general." On pricing, "We are assessing additional pricing actions for fall '25 and spring '26 to mitigate the potential impact of evolving tariffs. This is on top of the proactive pricing we already planned for fall '25 in North America and Asia."

21) From Ryanair: "I think there might be a trend, there's a perception, certainly in Europe, that the US is an unwelcoming destination at the moment. That seems to be translating, maybe to a bit more holidaying at home in Europe. We see no decline in the inbound transatlantic to Europe this year. And, all of the metrics we see forward bookings into Spain, Italy, Greece, the holiday, the islands this summer has been reasonably strong."

22) CNBC reported that "Nike will raise prices on a wide range of footwear, apparel and equipment as soon as this week as the retail industry braces for tariffs to hit its profits." Specifically, "Prices for Nike apparel and equipment for adults will increase between $2 and $10, a person familiar with the matter said. Footwear priced between $100 and $150 will see a hike of $5, while sneakers priced above $150 will see a $10 increase, the person said...The price hikes will be in effect by June 1, but could be seen on shelves as soon as this week, the person said. The increases cover a large portion of Nike's assortment, but many products will remain the same price."

23) On the heels of the dramatic rise in Japanese JGB yields, the April CPI rose 3.6% y/o/y, one tenth above expectations while prices ex food and energy grew by 3% as forecasted.

24) Japan's manufacturing and services May composite index fell back under 50 at 49.8 from 51.2 with all of the weakness in services as manufacturing ticked up a touch to 49 from 48.7.

25) Australia's PMI index was 50.6 vs 51 with no change in manufacturing at 51.7 while services fell .5 pt to 50.5.

26) In the Eurozone May PMI, manufacturing was up .4 pts to 49.4 but services were down at 48.9 from 50.1. The two biggest economies in the region continue to lag as Germany's composite index was at 48.6 and France's was at 48. S&P global said, “The eurozone economy just cannot seem to find its footing. Since January, the overall PMI has shown only the slightest hint of growth and in May, the private sector actually slipped into contraction. Do not blame US tariffs for this one. In fact, efforts to get ahead of those tariffs might partly explain why manufacturing has held up a bit better lately. Manufacturers have now increased production for the third straight month, and for the first time since April 2022, new orders did not decline. On the flip side, service providers, who are generally less exposed to US trade policy, except in areas like international logistics, are seeing business activity shrink for the first time since November 2024. While foreign demand for services is softening, it is the sluggish domestic demand that seems to be dragging the sector down."

27) The UK also saw a below 50 print at 49.4, though up from 48.5 in April with manufacturing badly lagging still at 45.1 while services rose back above 50 at 50.2. S&P Global said, "After an 'awful April', businesses reported a milder May. Business confidence has rebounded from April's recent low, which had seen confidence collapse to a degree not seen since the Truss Budget of 2022, and price pressures have moderated after spiking higher. Sunny weather also provided a welcome boost to business activity in some parts of the economy. However, output still fell slightly when measured across all goods and services for a 2nd successive month, hinting at the possibility of the economy contracting in the second quarter."

28) French business confidence in May was down by 1 pt with particular weakness in manufacturing and services.

29) The May UK industrial orders index fell to -30 from -26 and that was 6 pts below expectations. That's the weakest since January. CBI said "Sentiment among UK manufacturers seems poor, reflecting a combination of rising domestic business costs and US tariff uncertainty. Many respondents to the survey reported a reluctance to spend among their customers."

30) UK April headline CPI was up by 3.5% y/o/y, two tenths more than anticipated. The core rate was higher by 3.8% y/o/y, also two tenths above the estimate. A 28% m/o/m rise in airfares because of the timing of Easter this year was a main factor for the upside.

31) China reported some April economic stats with retail sales light relative to expectations, though still up 5.1% y/o/y while industrial production was above the forecast, up 6.1% y/o/y. Home prices continue to fall.

32) See ya Norm,

BY Doug Kass · May 23, 2025, 1:25 PM EDT

Scott Galloway's No Mercy/No Malice: Rise of the Toligarchs | No Mercy / No Malice

BY Doug Kass · May 23, 2025, 1:10 PM EDT

BY Doug Kass · May 23, 2025, 12:41 PM EDT

- NYSE volume 5% below its one-month average

- Nasdaq volume 12% below its one-month average

- VIX index + 9.07 to 22.12

BY Doug Kass · May 23, 2025, 11:50 AM EDT

Excerpt:

They are clearly baking a gigantic currency crisis into the cake. Ray Dalio gets it right. The rating agencies excuse or explanation for why the US still has an investment grade credit rating is that a country with a printing press can never default because it can just print enough money out of thin air to pay interest on its bonds, and it can do that forever. So, it’s triple A credit, which does not make any sense at all because if you just print a lot of money out of thin air to pay your debts, then your currency goes down in value, and you are paying back your creditors with depreciating currency, which is a form of default. The credit rating agencies are only looking at one kind of default where we just stop paying. They are not looking at paying with cheaper currency year after year, and we stiff our creditors that way. That’s why you don’t want to own Treasury bonds. They are not going to stop paying interest, but the interest will not cover inflation going forward. So, you will have a net real loss until they just crater, and then you will have a massive capital loss.

BY Doug Kass · May 23, 2025, 11:30 AM EDT

Here are today's "things":

*I covered my AAPL short at $194.45.

* I covered my NVDA short at $129.34.

* I shorted more SCHW at $87.20.

* I shorted more WMT at $95.98.

* I shorted more (GRNY) at $20.46.

BY Doug Kass · May 23, 2025, 11:12 AM EDT

BY Doug Kass · May 23, 2025, 10:56 AM EDT

From Peter Boockvar:

In light of the dip in the S&P futures for reasons we all know this morning, I'll just say this. Capitalism works best when it is left alone as businesses and consumers are left free to trade goods and services at prices agreed upon by both sides as it is a highly competitive world out there. Unfortunately we keep straying from that basic economic concept with a muscled top-down approach. The best thing a government can do is lower as many economic barriers as possible with regards to taxes, regulations, permitting, etc... and watch the private sector do its economic magic. I know not everyone plays fair but 'you can't always get what you want, but if you try sometime you'll find, you get what you need.' I'll leave it at that.

No better way to put your finger on the pulse of the consumer than to hear from those who directly sell to them. Visibility remains cloudy and companies are jumping through hoops.

From Ross Stores and whose stock is down sharpy pre-market as they lowered guidance for the next quarter:

Comps were flat y/o/y and said after a tough February (likely weather induced) they said business got better thereafter.

"From a pricing standpoint, we expect modest but broad based inflationary pressure across the retail industry, and we will remain focused on maintaining a substantial pricing umbrella below traditional retailers in order to deliver the bargains our customers have come to expect from us."

As for full year guidance, "there are simply too many unknown variables that are limiting our visibility into the second half of the fiscal year, and we believe it is prudent to withdraw our previously provided annual guidance at this time...we have limited visibility on how customer demands may evolve over the balance of the year, given prolonged inflation, deteriorating consumer sentiment, and still elevated and potentially fluctuating tariff levels."

"And the impact of tariffs, we expect to start hitting the customer in the July, late June timeframe."

From BJ's Wholesale who had a good quarter:

"Consumers are always looking for value, but it's paramount in challenging times like these...Consumers across the country have digested meaningful inflation over the past few years, and the uncertain economic environment drove members to prioritize value in their purchases during the quarter."

"Our perishables, grocery, and sundries division delivered more than 4% comp growth in the first quarter, with unit volumes increasing across all three divisions...Our general merchandise and services division comps decreased slightly in the first quarter."

They grew comps in toys and apparel and also in consumer electronics, "led by computer equipment such as laptops, desktops and monitors." But, "Unfavorable weather and pressures on consumer sentiment impacted the big ticket, highly discretionary categories such as patio sets, gazebos, and outdoor sheds in the quarter."

"The drivers of our business remain strong. Membership continues to grow nicely. Our continued improvements in merchandising and digital convenience are driving traffic, and we're gaining share in our clubs and gas stations."

With respect to how they will respond to tariffs, "We're always leaning into our model to deliver value, and while upward pressure on costs may drive prices higher, we are doing everything possible to minimize the impact to our members."

From Williams Sonoma and whose stock fell about 4.5% after earnings:

Comps rose 3.4% y/o/y with all brands positive. "In the quarter, we saw an acceleration of the positive comp trend coming out of Q4, despite consumer distraction with tariffs, continued geopolitical uncertainty, and no material improvement in the housing market." They also believe that they are taking market share.

"We recognize that the housing market, and therefore the furniture industry, may remain soft this year, as interest rates are still high. Therefore, our growth strategy emphasizes a broad and inspirational non-furniture assortment, including seasonal and decorative accessories, textiles, and housewares."

They reiterated the guidance they gave last quarter but "reflects that which we know today, and we are not assuming any significant upside or downside from broader macroeconomic factors." It also includes the 30% tariffs on China and the 10% global ones.

From Deckers Outdoors, a stock down notably pre market as they lowered guidance and the maker of Hoka and UGGs:

Hoka sales were up 10% y/o/y and UGG by 4%.

"As a result of macroeconomic uncertainty related to global trade policy, we will not be providing a formal outlook for fiscal year 2026 at this time...Based on the tariffs as of today's date, which are still subject to change, we expect to face an increase of up to $150 million to our cost of goods sold in fiscal year 2026 with a related yet to be determined impact to demand." This even as China is just 5% of their sourcing as they rely much more on Vietnam.

They will take, like all other companies, mitigation efforts to offset this but "We also believe there is potential to see demand erosion associated with the combination of price increases and general softness in the consumer spending environment."

"As we turn the page to fiscal year 2026, it is clear that we're operating in a very different environment."

From Advance Auto Parts that was up an incredible 57% yesterday, after a rough few years, on growing signs of a turnaround:

"After a challenging start to the year for the industry, we began to see demand rebound in late February led by our Pro business. For the quarter, Pro grew in the low single digit range, including 8 consecutive weeks of positive comparable sales growth in the US. This positive momentum in Pro has continued during the first four weeks of Q2, driven by our focus on providing exceptional service."

"Shifting to DIY. During the 2nd half of Q1, we saw an improvement in DIY trends, although the weekly volatility continues to remain high. Maintenance related categories such as fluids, chemicals and oil are performing relatively better, suggesting that DIY consumers remain cautious in their overall spending. As we look ahead, we expect the DIY environment to remain challenged due to the potential for higher broad based consumer goods inflation impacting household budgets."

Overall, "We believe the combination of an aging and growing vehicle fleet in the US coupled with the relatively non-discretionary nature of auto part spending, puts Advance and the industry in a favorable position to navigate through a volatile environment."

From Ralph Lauren who continues to outperform with its focus on the upper income spender:

Both top and bottom line exceeded their expectations. "This strong performance was broad based, driven by every geography and channel. For the full year, we delivered 8% top line growth, including record revenues for our international businesses, Europe and Asia, which together now comprise the majority of total company revenues."

"As we turn to fiscal '26, the global operating environment has become more challenged with uncertainty around tariffs and broader consumer behavior. Despite macro pressures, we are well positioned, having fundamentally transformed our business and built a more agile organization over the past several years."

"We expect this year's performance to be heavily weighted to the first half of the year, notably Q1, with first half revenues up roughly mid single digits. While we have not seen a change in our underlying business trends from Q4 into Q1 to date, we believe it is prudent to take a more cautious view on the 2nd half of the year based on a number of macro indicators, notably the impact of tariffs, weakening consumer confidence in the US, and increased risk of a broader consumer pullback and a more uncertain global operating environment in general."

On pricing, "We are assessing additional pricing actions for fall '25 and spring '26 to mitigate the potential impact of evolving tariffs. This is on top of the proactive pricing we already planned for fall '25 in North America and Asia."

From Workday and whose stock is down pre market:

"While there's heightened macro uncertainty, particularly across certain markets and verticals, we haven't seen this meaningfully impact our business and our growth prospects."

To the overseas data of note. On the heels of the dramatic rise in Japanese JGB yields, the April CPI rose 3.6% y/o/y, one tenth above expectations while prices ex food and energy grew by 3% as forecasted. Keep in mind that the BoJ still has the overnight rate at just .50%. JGB yields though are little changed after quite a move and I cannot emphasize enough how important it is to keep a close eye on this situation.

BoJ Governor Ueda by the way chimed in yesterday at the G7 meeting yesterday by saying "I want to refrain from commenting on specifics on short term moves in bond yields. But I will keep watching them closely, of course."

BY Doug Kass · May 23, 2025, 10:35 AM EDT

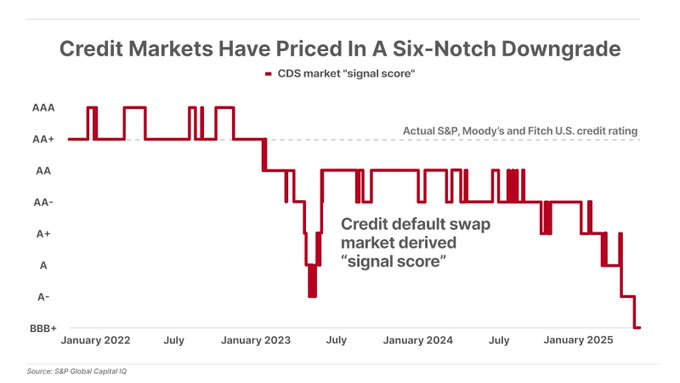

* Investors dance like Zorba the Greek (1964), Citigroup's Chuck Prince (2007) and Prince (1999) while the U.S. spends gluttonously

Just a day after the $3.8 trillion "Beautiful Bill" was passed in the House of Representatives, the cost of U.S. credit default swaps (which pay off in the event of default) have astonishingly intersected with the price of Greece's credit default swaps:

The bill's debt impact -- with a 220% debt-to-GDP ratio by 2055 -- reflects the Republican party's ideological shift to the Democratic party's liberal big spending of the past.

The chart below shows credit default prices for U.S. Treasuries anticipating a six-level credit downgrade from their current AA+ rating (down from BBB+) -- that is just three notches above a "junk" rating:

It is shocking to me why equities don’t seem to care that we are Greece now.

It could just be retail once again hoovering up the institutional selling. Retail does not know any better, but if that is the case, I have no idea where they keep finding the money.

Could be the pros think this forces quantitative easing or something of that ilk, but it feels like at some point that is no longer a solution and does more harm than good, because the combination of this and everything else going on (tariffs, trade tension, etc.) will almost surely lead to a big inflation problem.

The real solution is cutting expenses, and biting the bullet that way, but neither party seems willing to do that. (See Rethinking American Exceptionalism)

But the pain that comes from cutting expense is at least a real solution and better than the type of pain that comes from continuing to do what we are doing.

Zorba The Greek is a novel that delves into some profound themes such as the nature of life - contrasting the intellectual pursuit of knowledge with the raw experience of living, emphasizing the importance of embracing life's uncertainties.

Maybe this is all as simple as Zorba The Greek's Final Dance! Zorba the Greek - The Final Dance

Worse yet, to this observer, today's expanding debt crisis may be eerily similar to 2007 when Citigroup's CEO, Chuck Prince famously said, amid early signs of the subprime mortgage crisis as the financial crisis (and Great Recession) unfolded:

"As long as the music is playing, you've got to get up and dance."

The quote has been interpreted as suggesting a lack of foresight and a willingness to continue risky practices even as warning signs emerged. While investors.... Dance, Dance, Dance. I am also reminded of Prince 1999 premonitions as the dot.com bubble began to mature:

The sky was all purple

There were people runnin' everywhere

Tryin' to run from the destruction

You know I didn't even care

Say, say, 2000-00, party over

Oops, out of time

So tonight I'm gonna party like it's 1999

Be forewarned.

BY Doug Kass · May 23, 2025, 9:50 AM EDT

I covered my NVDA trading short rental a $129.34 for a profit.

From earlier this week:

Adding to (NVDA) short at $135.38.Position: Short NVDA (S)By Doug Kass

NONE

May 19, 2025 3:07 PM EDT

BY Doug Kass · May 23, 2025, 9:35 AM EDT

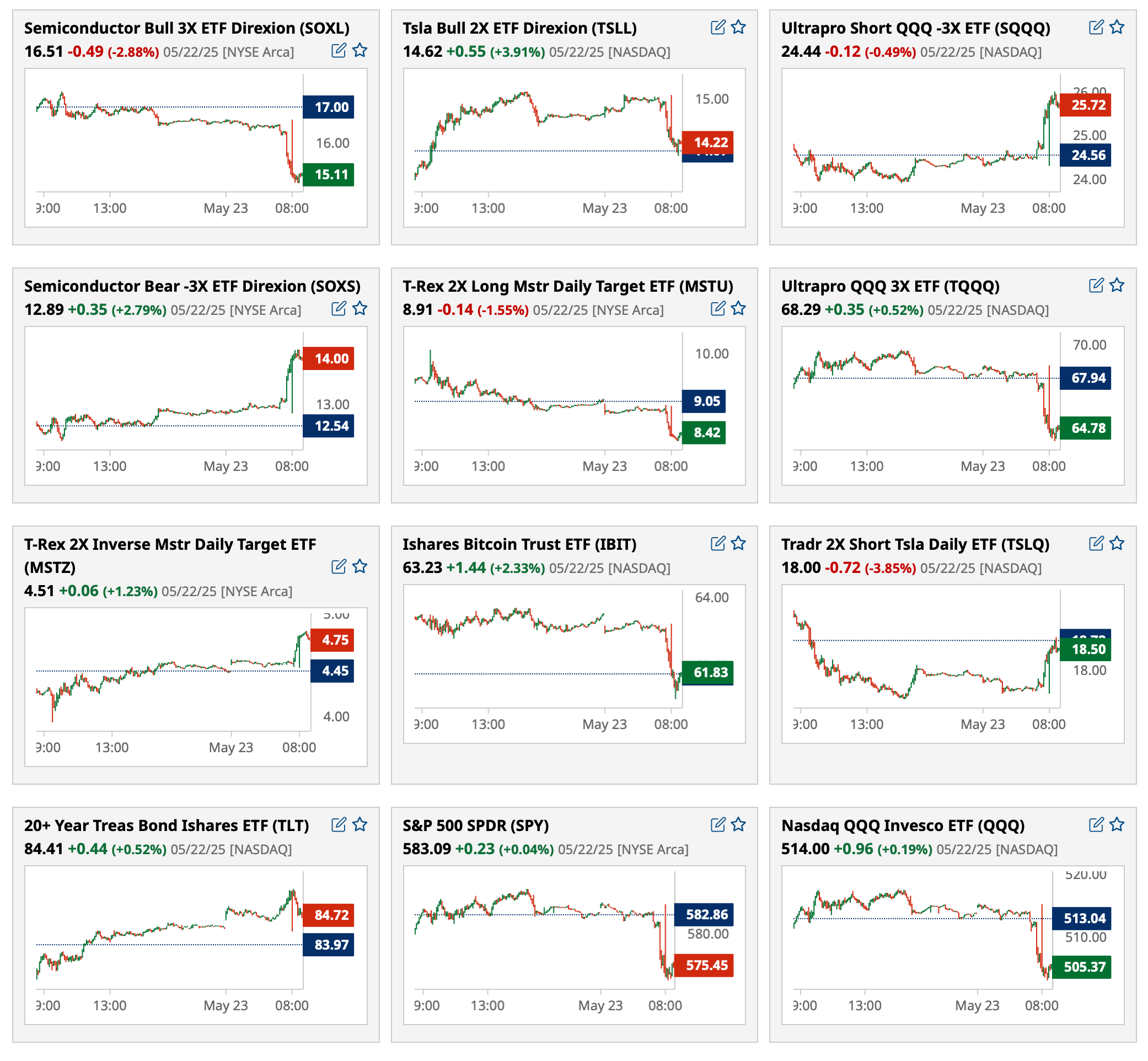

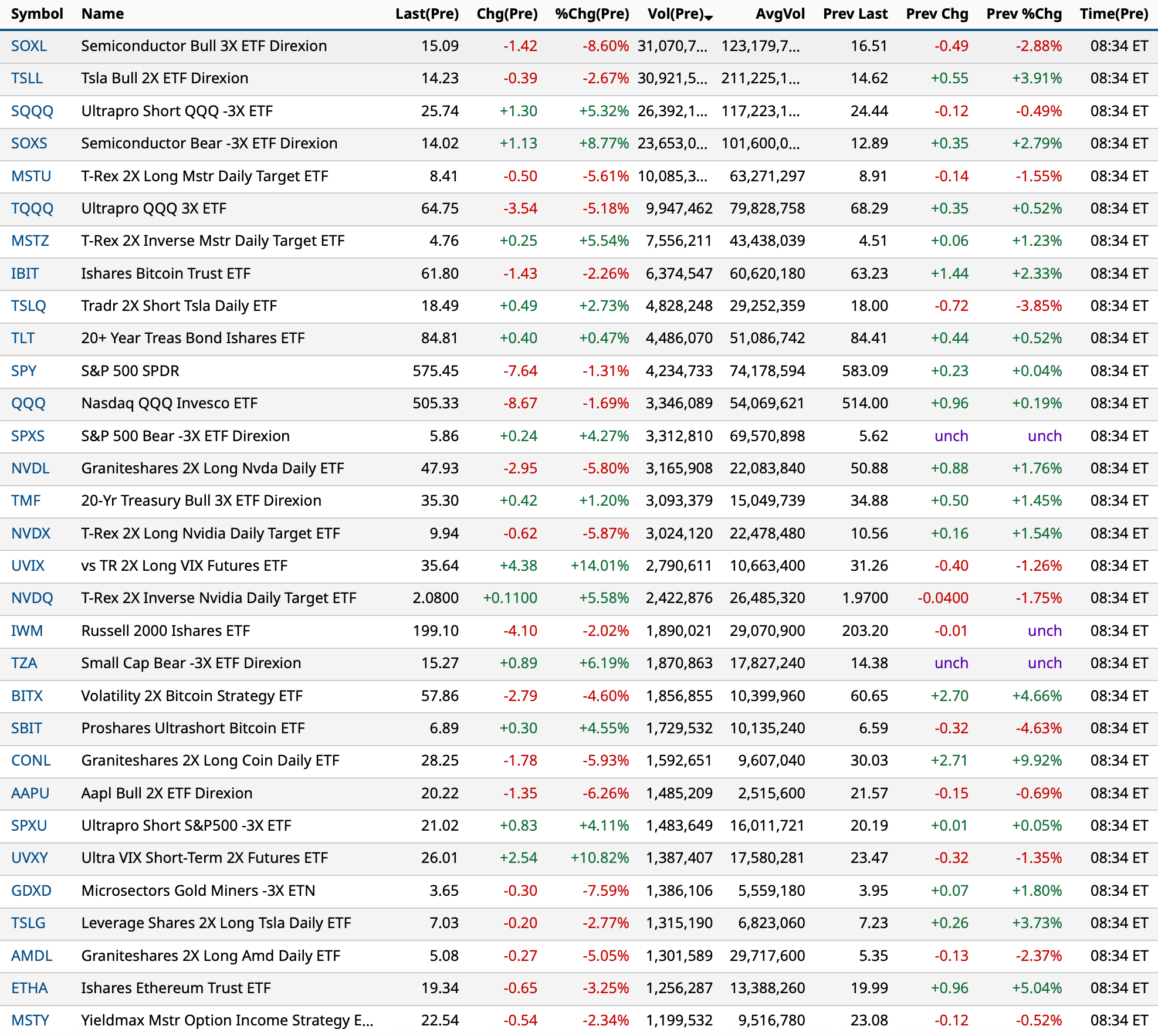

Most active prearket ETFs as of 8:34 a.m. ET:

BY Doug Kass · May 23, 2025, 9:18 AM EDT

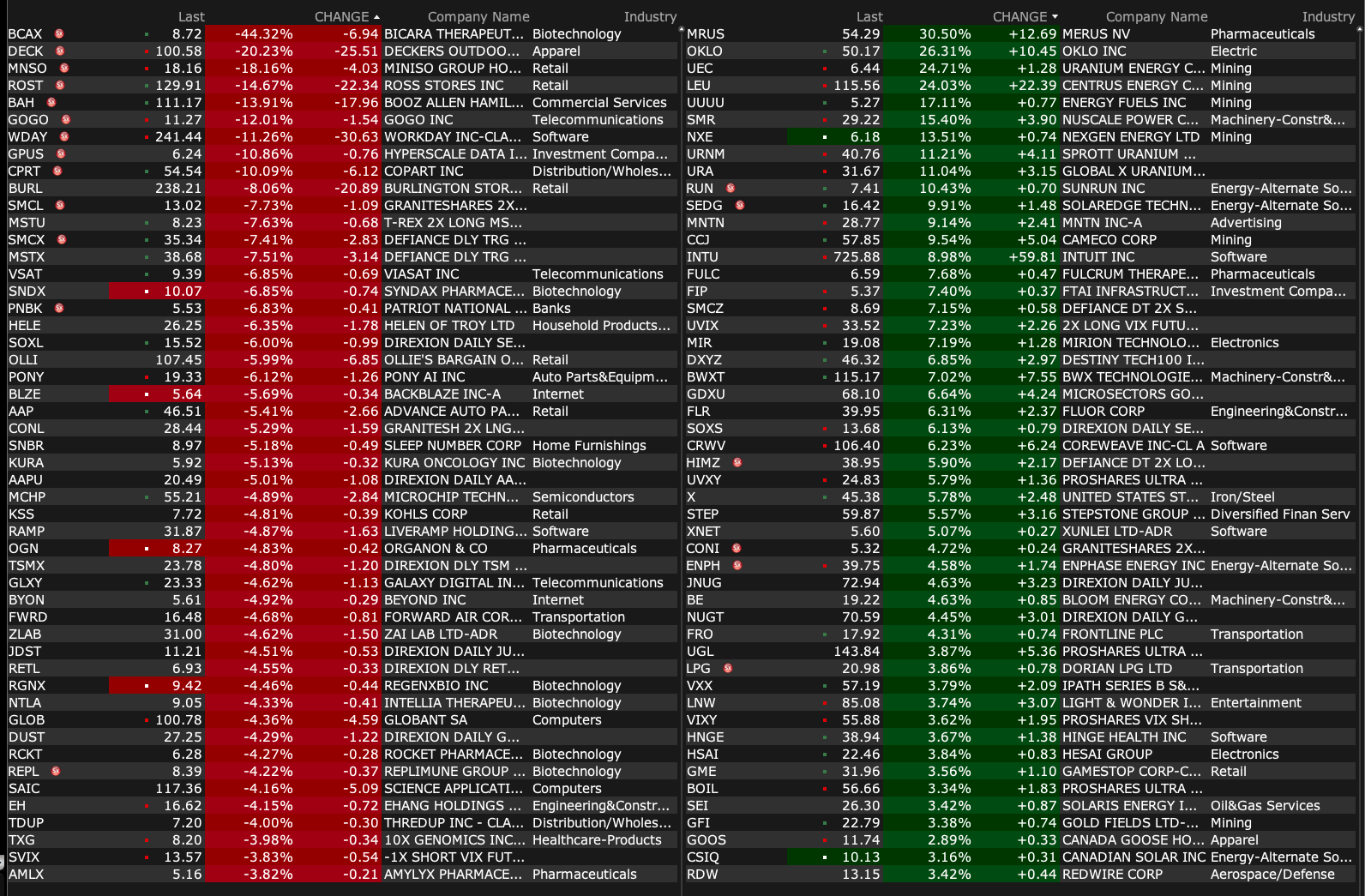

Premarket percentage movers at 8:53 a.m. ET:

BY Doug Kass · May 23, 2025, 9:06 AM EDT

-LITM +18% (nuclear stock strength as President Trump likely to sign executive order to support domestic nuclear energy industry)

-MRUS +13% (Petosemtamab with Pembrolizumab interim data demonstrates robust efficacy and durability in 1L PD-L1+ r/m HNSCC)

-FULC +7.8% (SVB Leerink LLC Raised FULC to Outperform from Market Perform, price target: $12)

-INTU +6.8% (earnings, guidance)

-SNDX +6.5% (competitor Kura Oncology reports data from KOMET-001 with menin inhibitor ziftomenib)

-ADSK +1.7% (earnings, guidance)

-BCAX -23% (announces Publication of an Abstract with Updated Interim Data from Phase 1/1b Trial of Ficerafusp alfa in 1L R/M HNSCC at the 2025 ASCO Annual Meeting)

-DECK -19% (earnings, not providing FY guidance; names new Board Chair)

-HNRG -19% (previously disclosed Conversion Transaction Commitment Agreement with leading global datacenter developer being terminated by the counterparty)

-BAH -15% (earnings, guidance)

-ROST -13% (earnings, withdraws FY guidance)

-WDAY -8.2% (earnings, guidance)

-CPRT -5.9% (earnings)

-AAPL -3.9% (US President Trump: Threatening >25% tariff on Apple unless iPhone's are built in US)

-STM -3.0% (European ADRs weak from Trump Truth Social post recommending 50% straight tariff on EU by June 1st)

BY Doug Kass · May 23, 2025, 8:55 AM EDT

On Morgan Stanley's Mike Wilson Appearance on Fast Money Last Night:

BY Doug Kass · May 23, 2025, 8:17 AM EDT

BY Doug Kass · May 23, 2025, 8:02 AM EDT

Now President Trump goes after EU on tariffs:

Stock futures -70 handles.

BY Doug Kass · May 23, 2025, 7:51 AM EDT

BY Doug Kass · May 23, 2025, 7:49 AM EDT

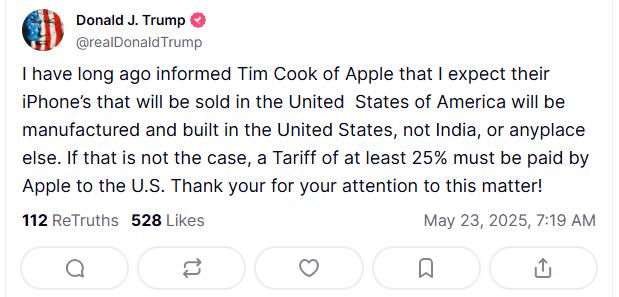

BY Doug Kass · May 23, 2025, 7:40 AM EDT

Break in!

President Trump threatens tariffs on Apple AAPL if iPhones are not made in the U.S..

Stock futures fall.

I just covered my Apple short -$7.

BY Doug Kass · May 23, 2025, 7:28 AM EDT

Bonus — Here are some great links:

Equity Market's Rally Will Peter Out

Should You Be Concerned About the Markets?

BY Doug Kass · May 23, 2025, 7:05 AM EDT

This week in "Rethinking American Exceptionalism" I emphasized my expectations that The Mag 7 likely made an important top in January 2025, similar to the seminal top in The Nifty Fifty in January 1973.

Here you go. I will let you decide (I think this is called a "flag"):

Chart of The Mag 7

BY Doug Kass · May 23, 2025, 6:50 AM EDT

New shorts yesterday — Walmart WMT and Schwab SCHW.

Today's new short, Palantir PLTR.

BY Doug Kass · May 23, 2025, 6:40 AM EDT

Coming up, my opener, "We Are All Greece Now."

But first — here is a "solution" to our disturbing debt picture:

BY Doug Kass · May 23, 2025, 6:30 AM EDT

The S&P Short Range Oscillator slipped from 3.04% to 1.92%.

Moving towards neutral and is less overbought.

BY Doug Kass · May 23, 2025, 6:20 AM EDT

BY Doug Kass · May 23, 2025, 6:11 AM EDT

I took a trading short rental in Palantir PLTR ($124) based on, in part, on today's insider sales announcement:

BY Doug Kass · May 23, 2025, 6:02 AM EDT