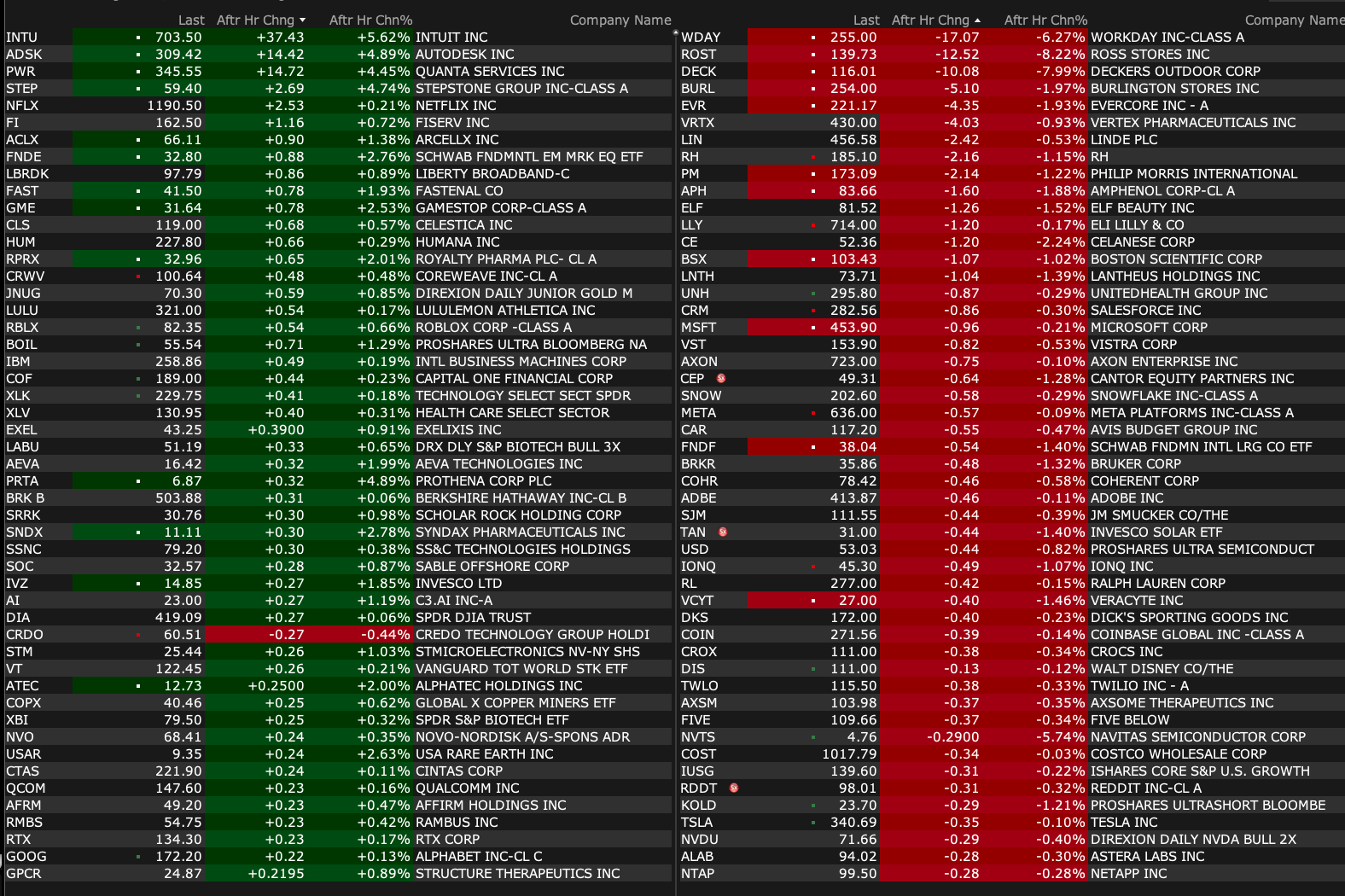

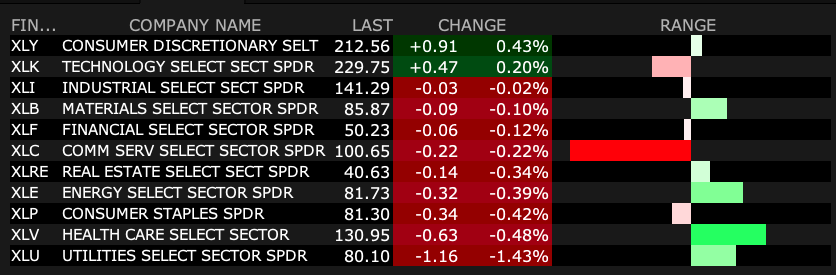

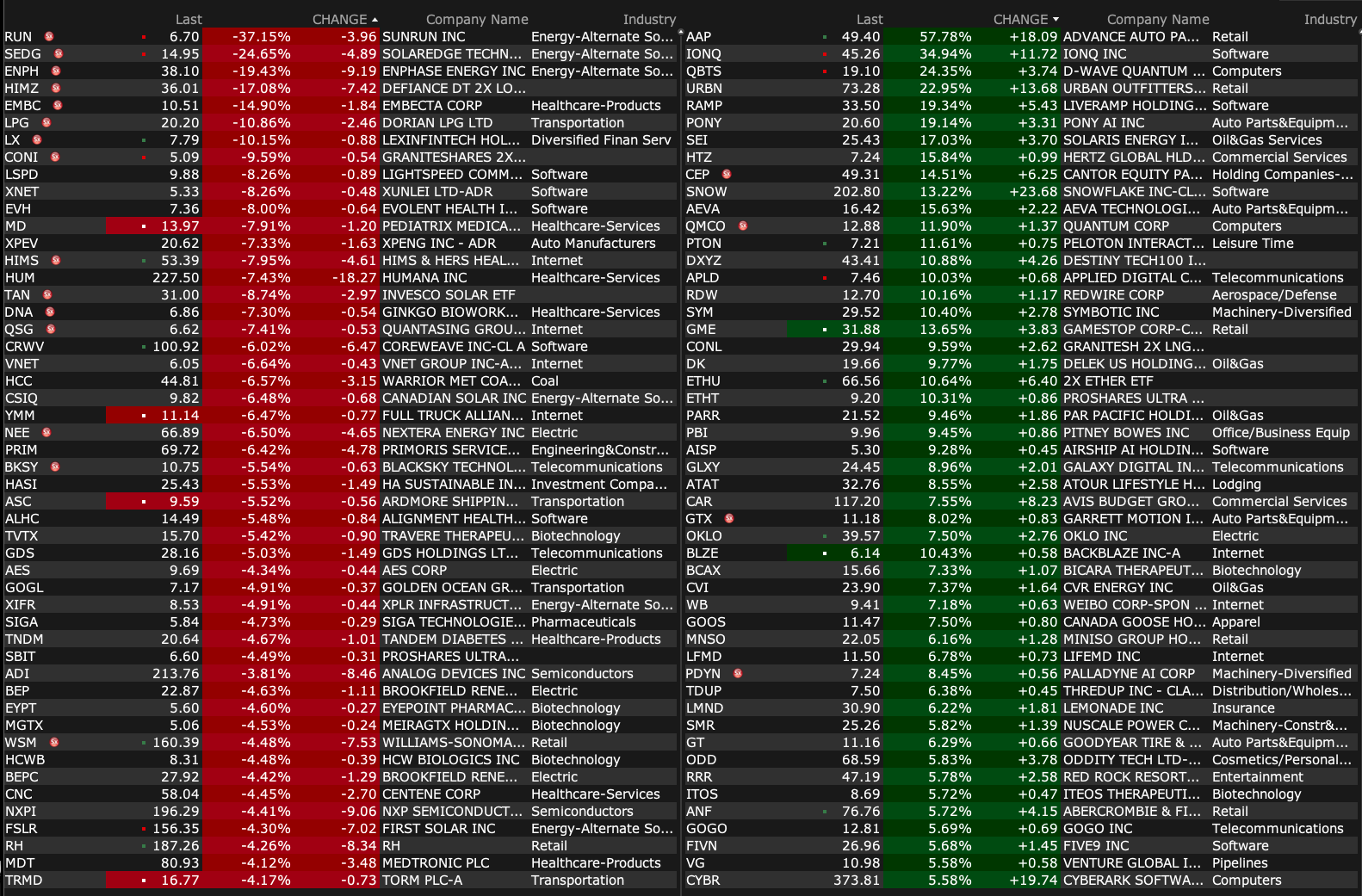

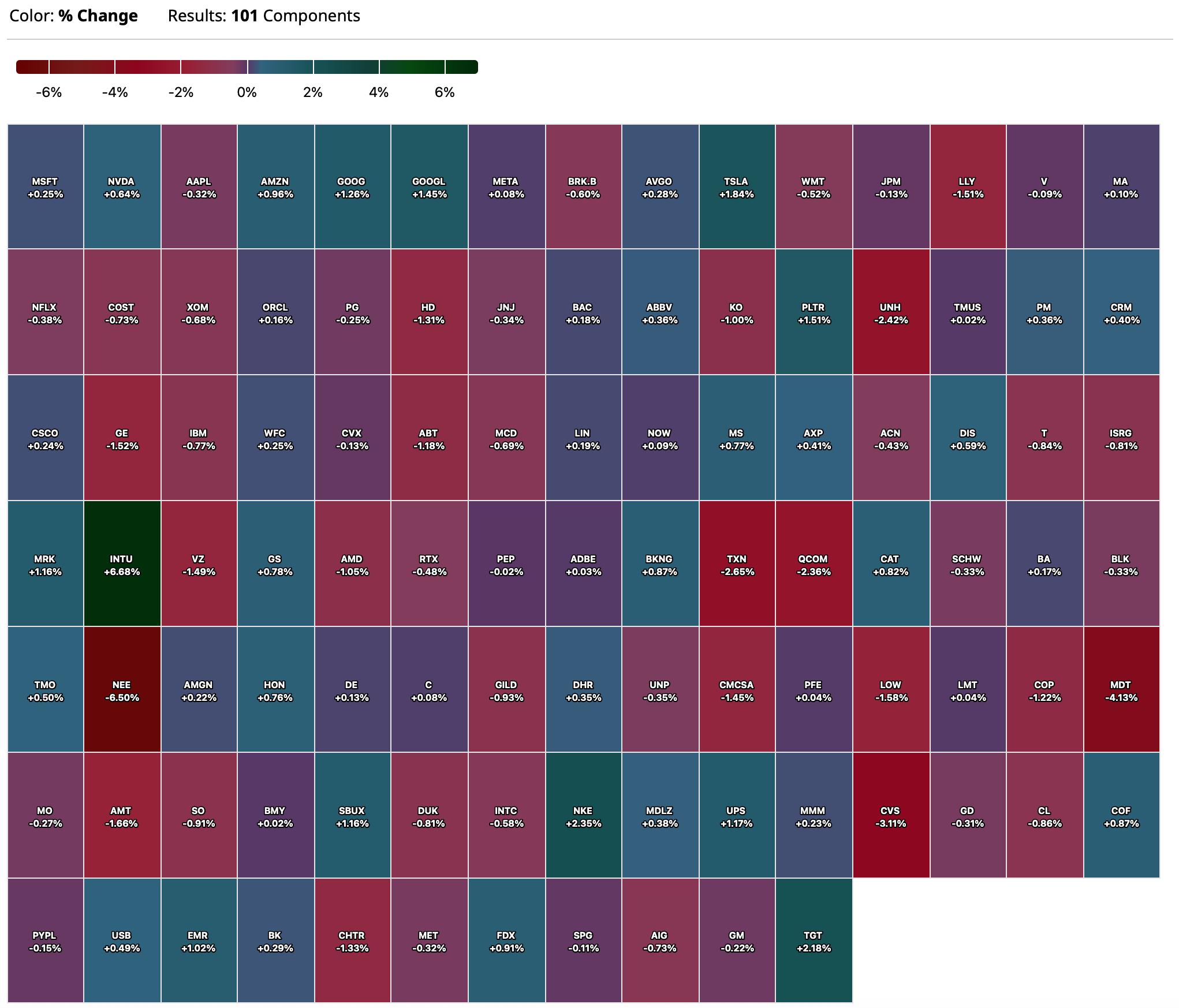

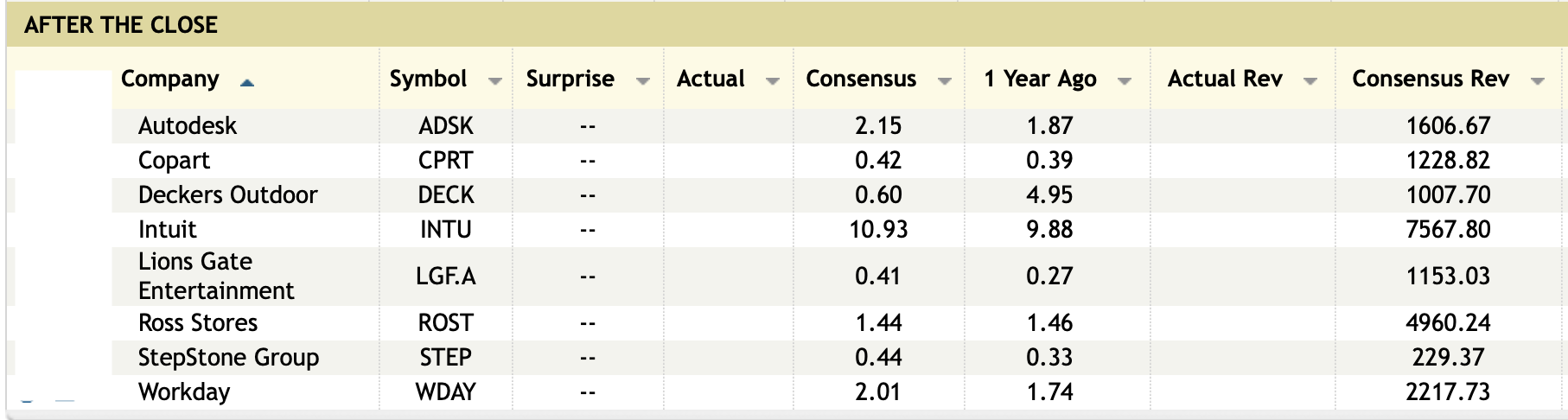

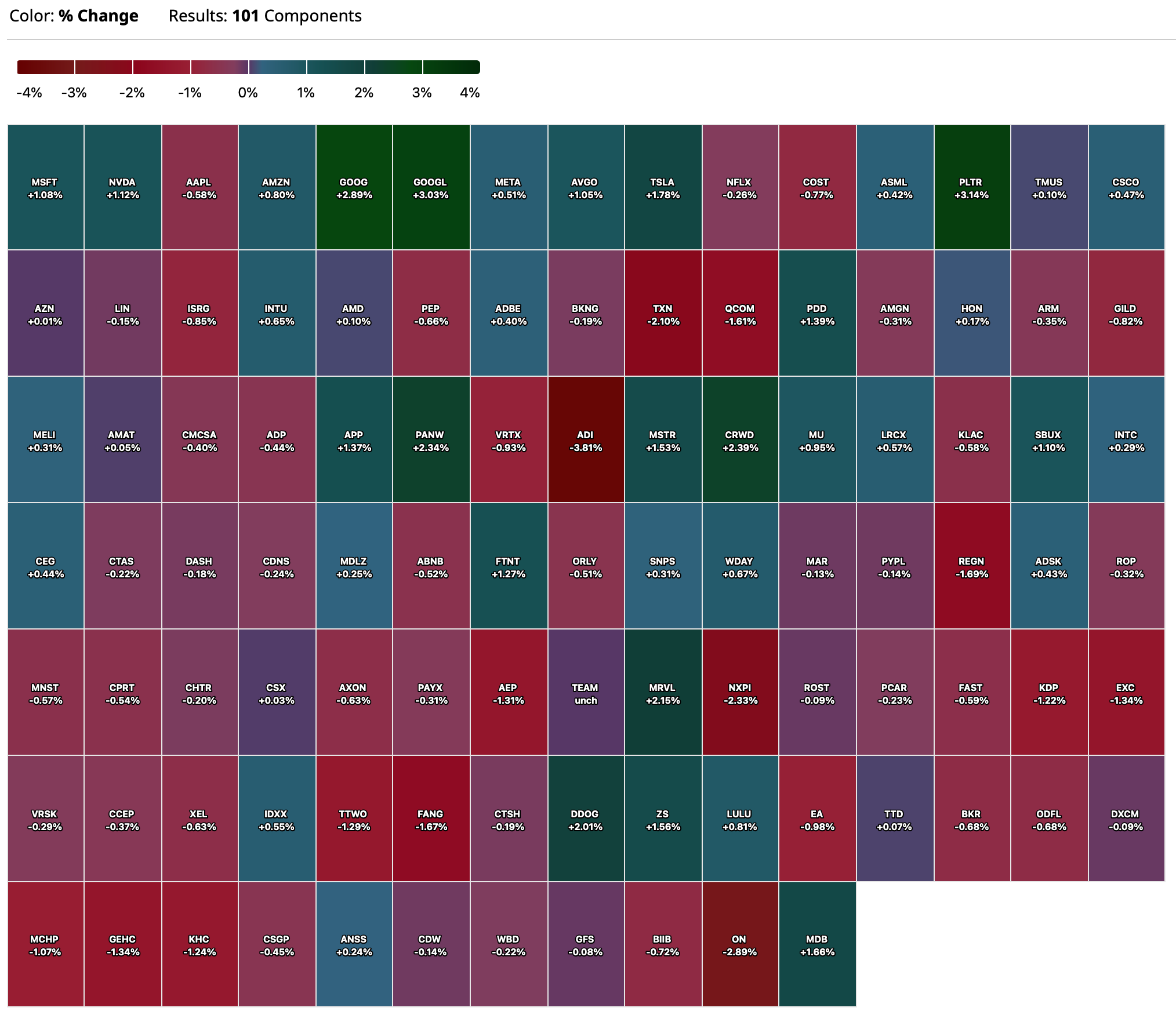

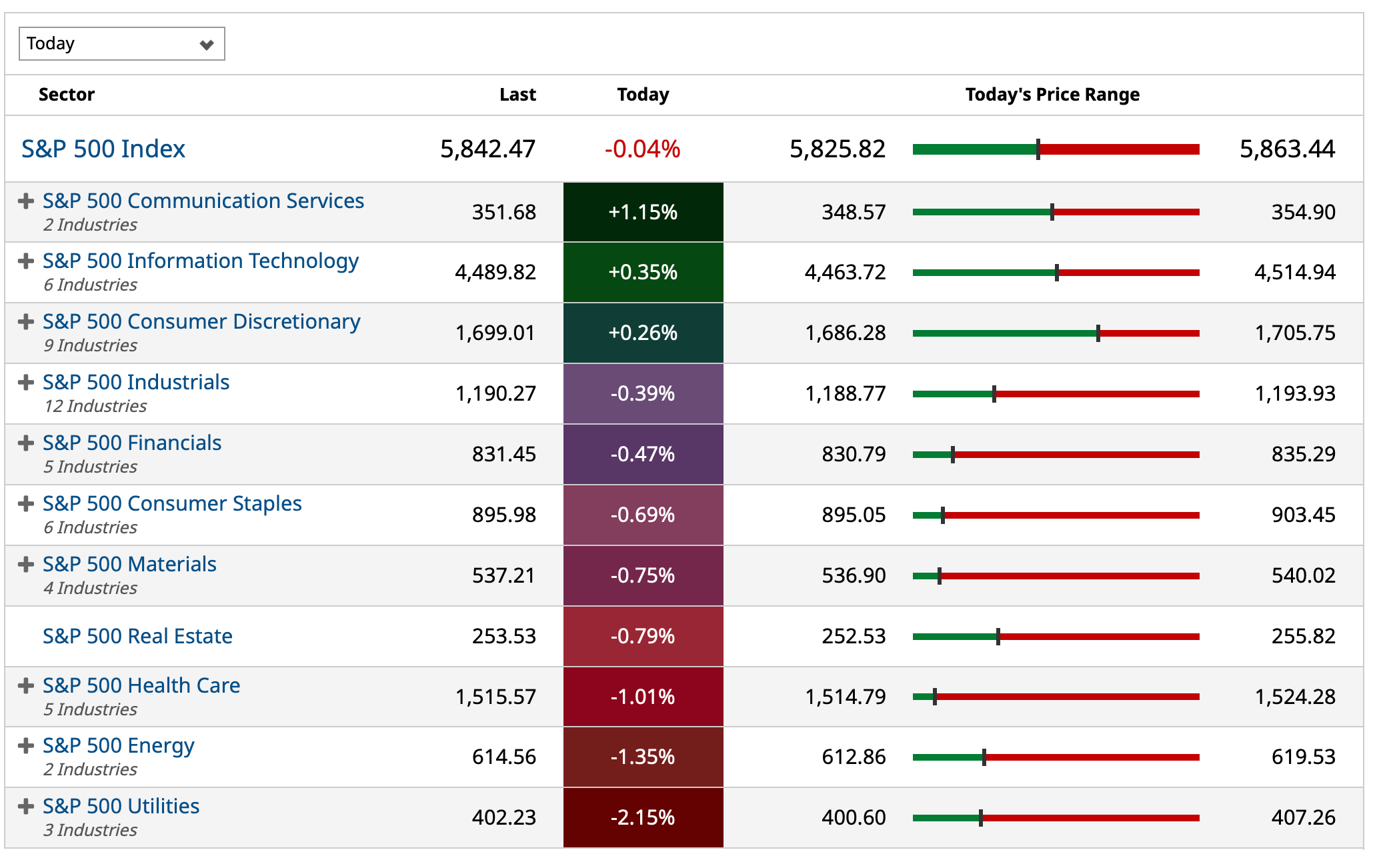

Thursday's After-Hours Movers

BY Doug Kass · May 22, 2025, 5:15 PM EDT

BY Doug Kass · May 22, 2025, 5:15 PM EDT

BY Doug Kass · May 22, 2025, 5:06 PM EDT

A sincere thanks for providing me with this platform today, this week... and since 1987! (And thanks for the important contributions and dedication of our editors who get up early to edit my stuff and make it better.)

I hope you continue to find value in my output.

Be safe.

BY Doug Kass · May 22, 2025, 3:55 PM EDT

BY Doug Kass · May 22, 2025, 3:31 PM EDT

Wolf Street howls about a weak start to the spring residential real estate selling season.

It remains my view that housing will lead a consumer-based economic slowdown in the next few months.

BY Doug Kass · May 22, 2025, 3:24 PM EDT

I'm shorting Walmart WMT at $96.36.

BY Doug Kass · May 22, 2025, 3:15 PM EDT

I added to my Nvidia NVDA short at $133.97.

BY Doug Kass · May 22, 2025, 3:05 PM EDT

Here are today's things:

* I purchased TLT long at $83.45 and sold TLT at $83.60.

* Initiated CRWV put position (for June/July).

* Initiated SCHW short at $87.49.

* I added to GRNY short at $20.69.

* I covered ARKK short at $55.49.

* I covered index shorts - SPY at $583.11, IWM at $203.24 and QQQ at $513.10 (last evening).

BY Doug Kass · May 22, 2025, 2:00 PM EDT

Hearing that Coreweave CRWV will announce an early lockup release next week.

Stay tuned.

BY Doug Kass · May 22, 2025, 1:44 PM EDT

Initiating a small short in Charles Schwab SCHW at $87.48 — against longs in Morgan Stanley MS and Goldman Sachs GS.

BY Doug Kass · May 22, 2025, 12:56 PM EDT

Buying in-the-money CoreWeave CRWV puts for several months out.

BY Doug Kass · May 22, 2025, 12:47 PM EDT

Shorting more GRNY at $20.69.

BY Doug Kass · May 22, 2025, 12:36 PM EDT

From Peter Boockvar:

The May US manufacturing and services composite PMI rose to 52.1 from 50.6 with both components higher m/o/m with the former rising to 52.3 from 50.2 and the latter at 52.3 from 50.8.

The manufacturing improvement seemed all about front running tariffs. S&P Global said “the biggest positive contribution came from inventories, which rose to the greatest extent recorded since the survey began in 2009. Longer delivery times – which are typically associated with busier manufacturing supply chains – also helped push the PMI higher, with delays the most pronounced in 31 months.” With jobs, “employment fell for a 2nd successive month.” On pricing, “input costs rose at the sharpest rate since August 2022…The latest rise in output prices was overwhelmingly linked to tariffs, having directly driven up the cost of imported inputs or caused suppliers to pass through tariff related cost increases.”

Likely reflecting the reduction in foreign travel to the US, “export orders continued to fall, dropping especially sharply for services…excluding the pandemic, the fall in exports of services was the largest recorded since comparable data were available in late 2014.” On jobs, “service sector payrolls were trimmed for the second time in four months.” On inflation, “Charges levied for services rose to the greatest extent since April 2023.”

The bottom line from S&P Global, “Business confidence has improved in May from the worrying slump seen in April, with gloom about prospects for the year ahead lifting somewhat thanks largely to the pause on higher rate tariffs…However, both sentiment and output growth remain relatively subdued, and at least some of the upturn in May can be linked to companies and their customers seeking to front run further possible tariff related issues, most notably the potential for future tariff hikes after the 90 day pause lapses in July.”

And to sum up on pricing, “The overall rise in prices charged for goods and services in May was the steepest since August 2022, which is indicative of consumer price inflation moving sharply higher.”

I have nothing more to add.

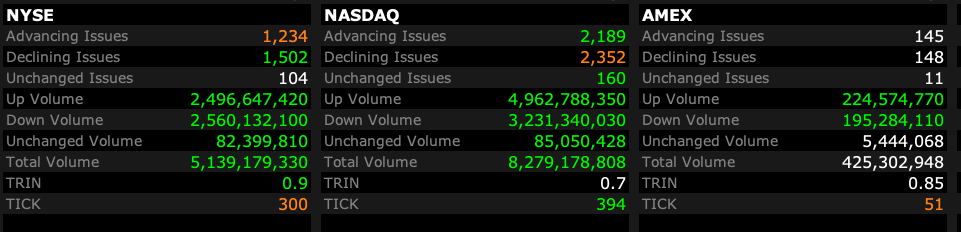

BY Doug Kass · May 22, 2025, 11:45 AM EDT

- NYSE volume 4% below its one-month average;

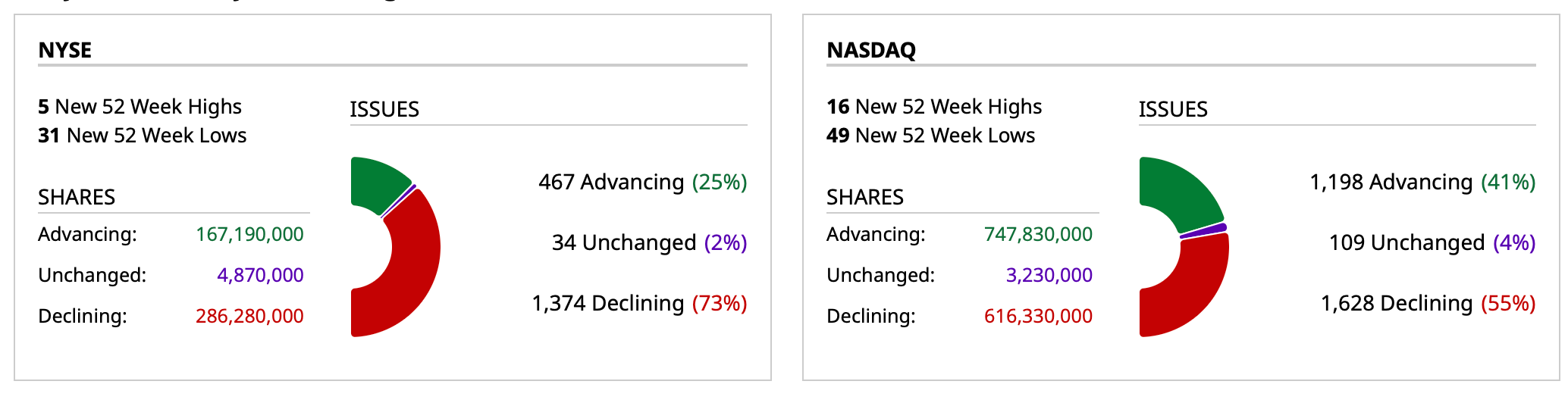

- Nasdaq volume 23% below its one-month average;

- VIX index: down 0.48 to 20.77

BY Doug Kass · May 22, 2025, 11:30 AM EDT

My second tweet of the day:

BY Doug Kass · May 22, 2025, 11:22 AM EDT

From Peter Boockvar:

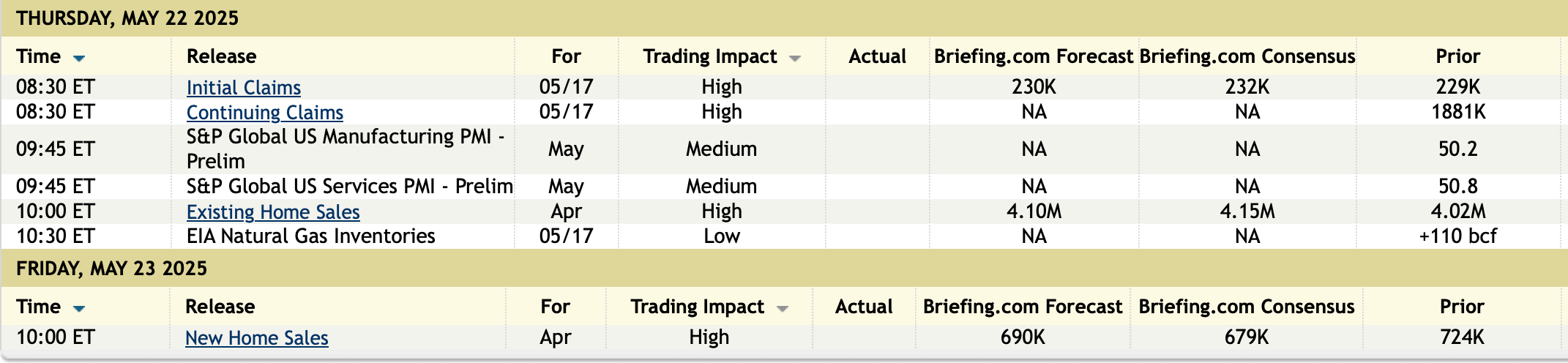

Initial claims fell to 227k from 229k and that was 3k below expectations. The 4 week average is now 232k vs 231k in the week before. Continuing claims, delayed by a week, though remained elevated around the highest since November 2021 at 1.903mm vs 1.867mm in the week before.

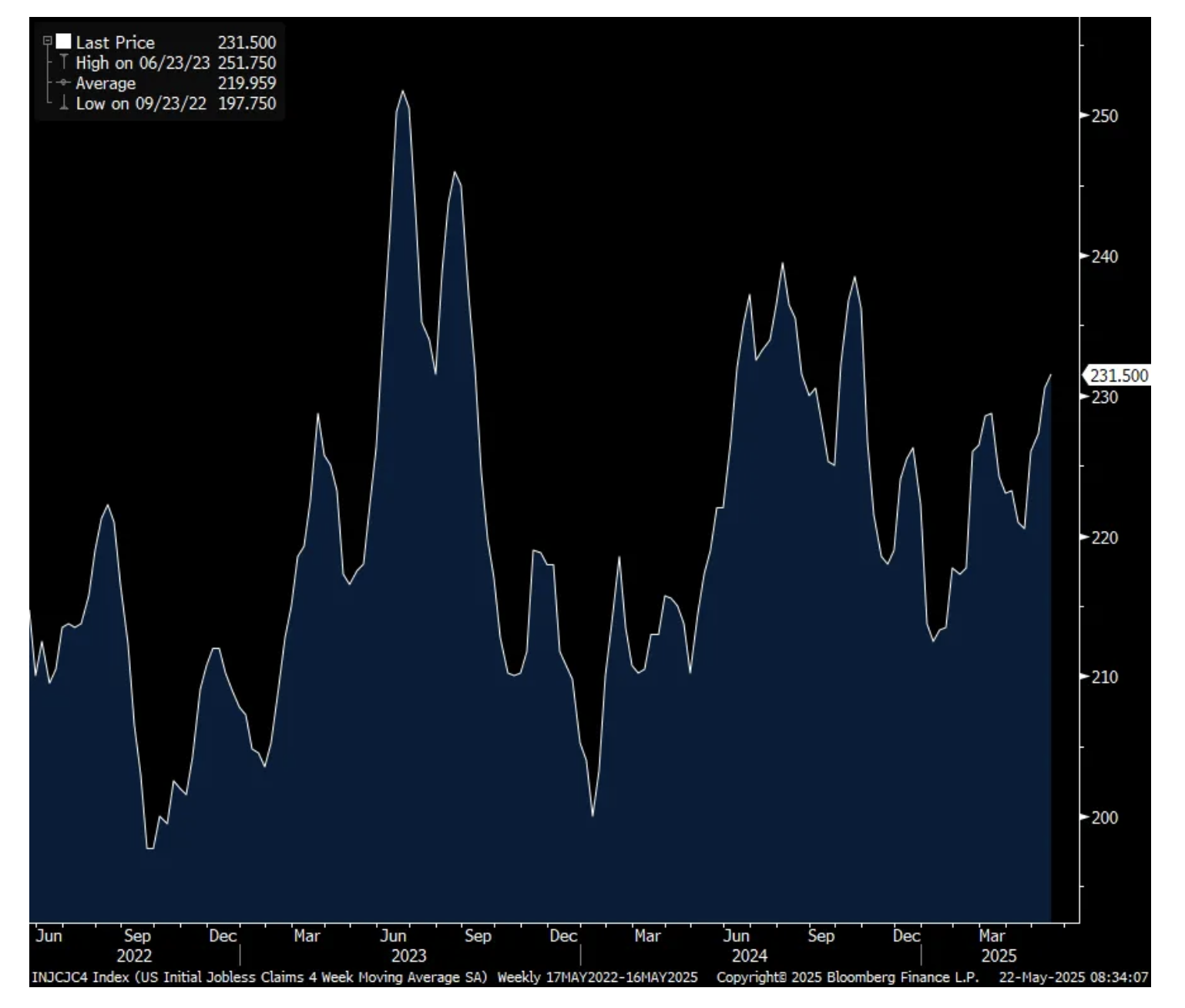

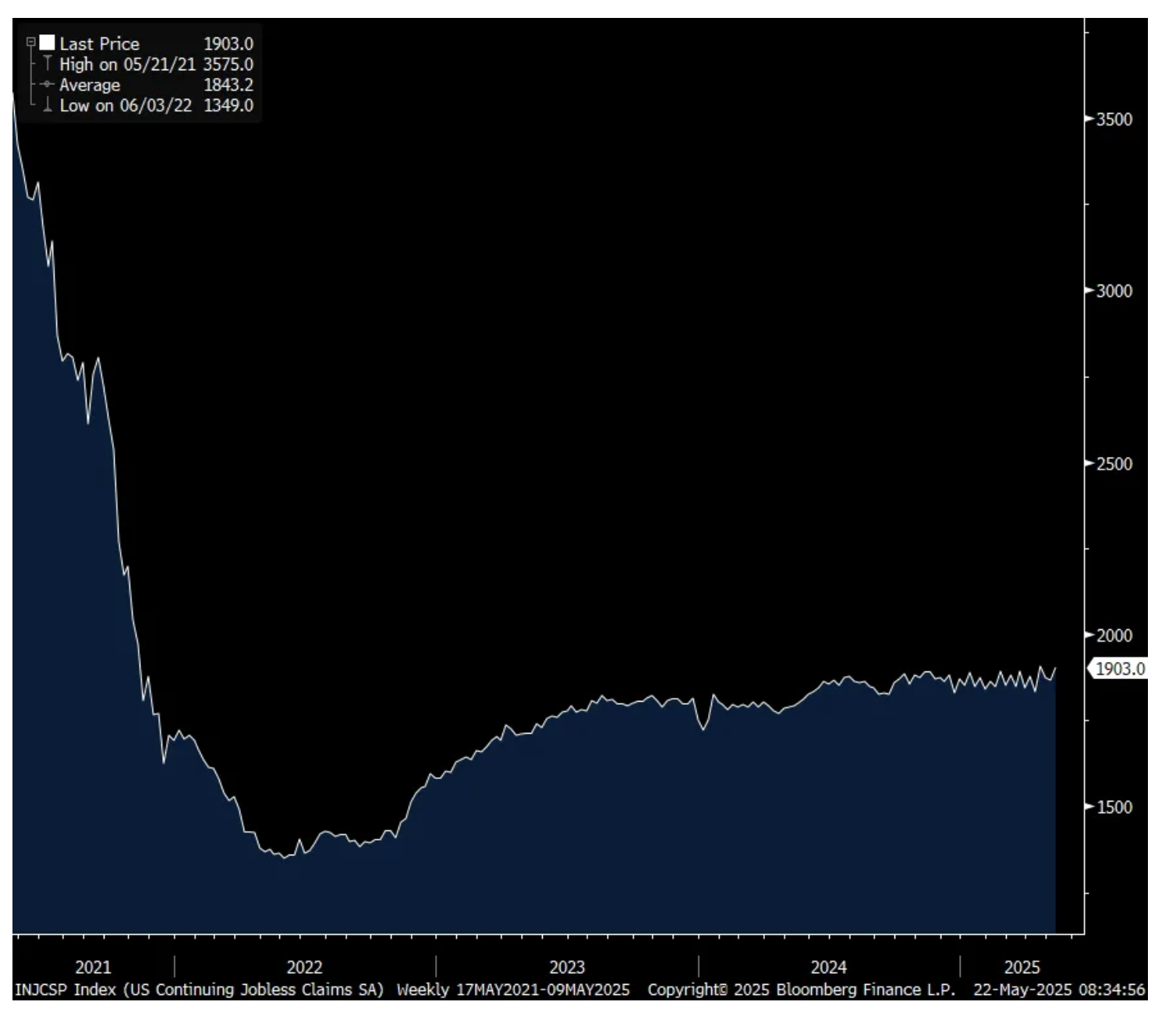

Bottom line, you can assume that with the China tariff cool down (though the rates remain very high), businesses are all waiting to see how things play out, along with the negotiations with everyone else, and thus aren’t moving yet to cut any labor costs, if needed. On the other hand, they are clearly slowing the pace of hiring, not wanting to commit just yet to increasing labor costs, until the economic sky clears a bit.

4 week avg Initial Claims

Continuing Claims

BY Doug Kass · May 22, 2025, 11:11 AM EDT

BY Doug Kass · May 22, 2025, 11:00 AM EDT

* If correlations between stocks and bonds goes back to the 1990s, the risk of a great unwind of leveraged (long) risk parity and other vol controlled strategies and products exists

I recently wrote that we might be in a setting -- back about 3-4 decades ago - in which both bonds and stocks dropped at the same time.

Well, yesterday, equities dropped by -1.8% while bond yields gapped higher (and bond prices gapped lower. equivalent to the percentage decline in stocks).

If this correlation persists, as I also suggested recently, it could be the sudden death of risk parity and other quantitative strategies that allocate between equities and fixed income -- based on an assessment of risk.

And that could lead to the great unwind of leveraged long risk parity products and strategies:

Position: None

Apr 15, 2025 6:25 AM EDT

Back to the future?

Maybe.

BY Doug Kass · May 22, 2025, 10:35 AM EDT

From Peter Boockvar:

As always the case, sentiment follows price. And just as there were a lot of bears at around 4,800 in the S&P 500, now of course there are a lot more bulls near 6,000. Investors Intelligence said yesterday that Bulls rose 6.5 pts to 42.3 from 35.8 last week. Bears have fallen to 26.9 from 30.2. At the market lows, bulls stood at just 23.5 while bears were at 35.3. AAII today said Bulls were up for a 3rd week, by 1.8 pts to 37.7, the most since late January. Bears fell by 7.7 pts to 36.7 which is the lowest since late January. The CNN Fear/Greed index has gone from 3 in early April, got as high as 70 a few days ago and closed yesterday at 66. Bottom line, nothing extreme here but the sentiment has obviously gotten a lot more comfortable which means we all should not be from a contrarian standpoint and yesterday's selloff was the first sign of that.

Yes, we saw the big move up in US yields, globally too, yesterday. But, what was also again very noteworthy was the further weakness in the US dollar in the face of the rate rise here. The Dollar index fell back below 100. Understand the importance of the dollar moves if there is a foreign rethink of its holdings of US assets. Many of these assets are not FX hedged so as the dollar weakens, that itself could exaggerate the foreign selling of stocks/bonds and anything else and the foreign selling in turn exaggerates the dollar weakness. What I now have my eye on is the US CLO market because Japanese investors are large holders. JBBB is a Janus etf that holds CLOs rated between B and BBB.

JGB yields continued higher with the 40 yr yield now up for the 11th day in the past 12 and by 50 bps over these last few weeks to 3.69%. The 10 yr yield was up almost 5 bps to 1.57% and is just 1.5 bps from the highest level since 2008. The catalyst overnight for the further moves were these comments from BoJ board member Asahi Noguchi, "The moves are indeed sudden, but I can't simply conclude that they are abnormal. There is the market's own judgment at play here, so I believe it would be inappropriate to intervene without reason and attempt to manipulate the situation in any way." Surprising to hear from a BoJ member who does NOT want to intervene.

10 yr JGB Yield

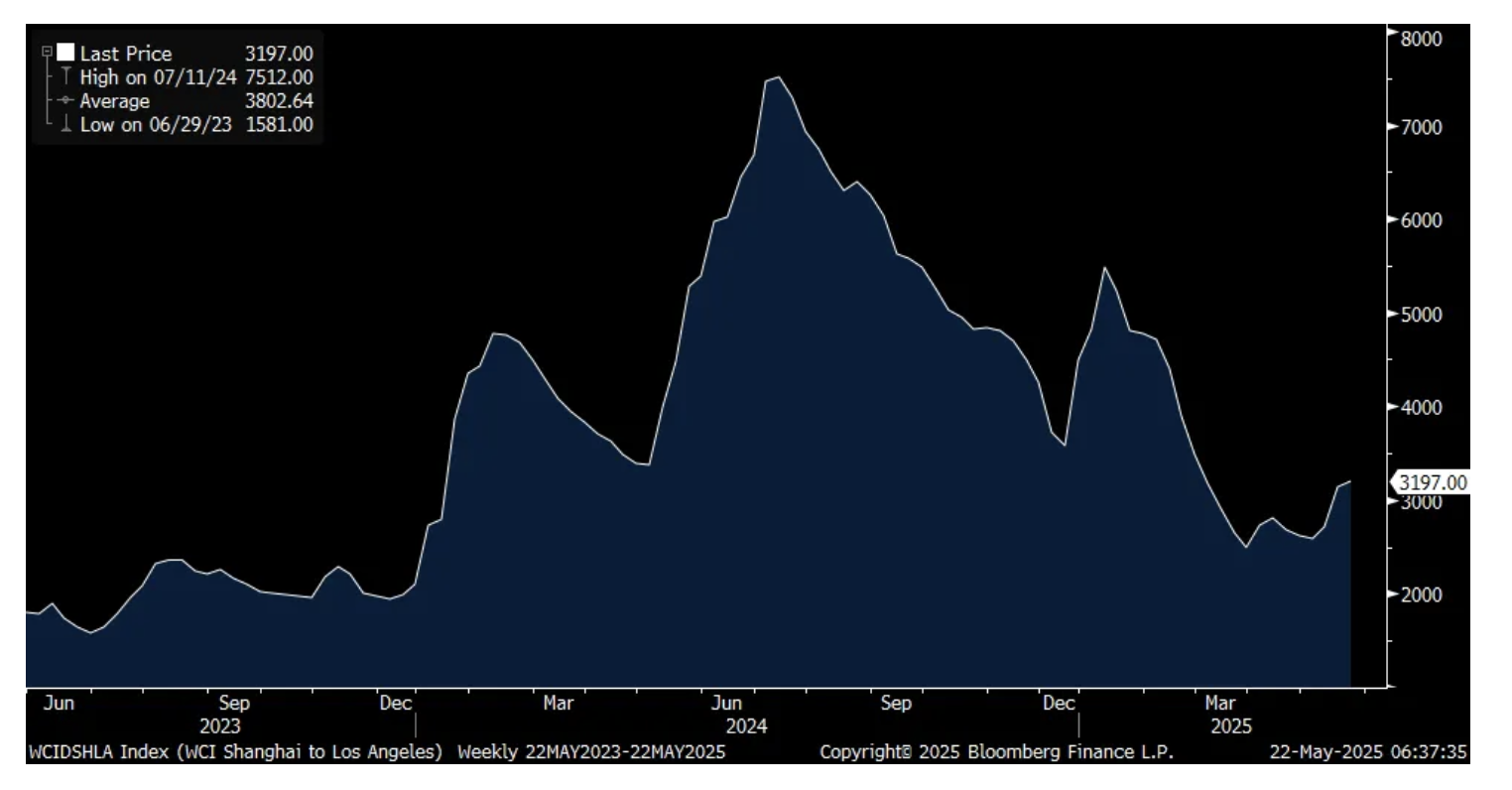

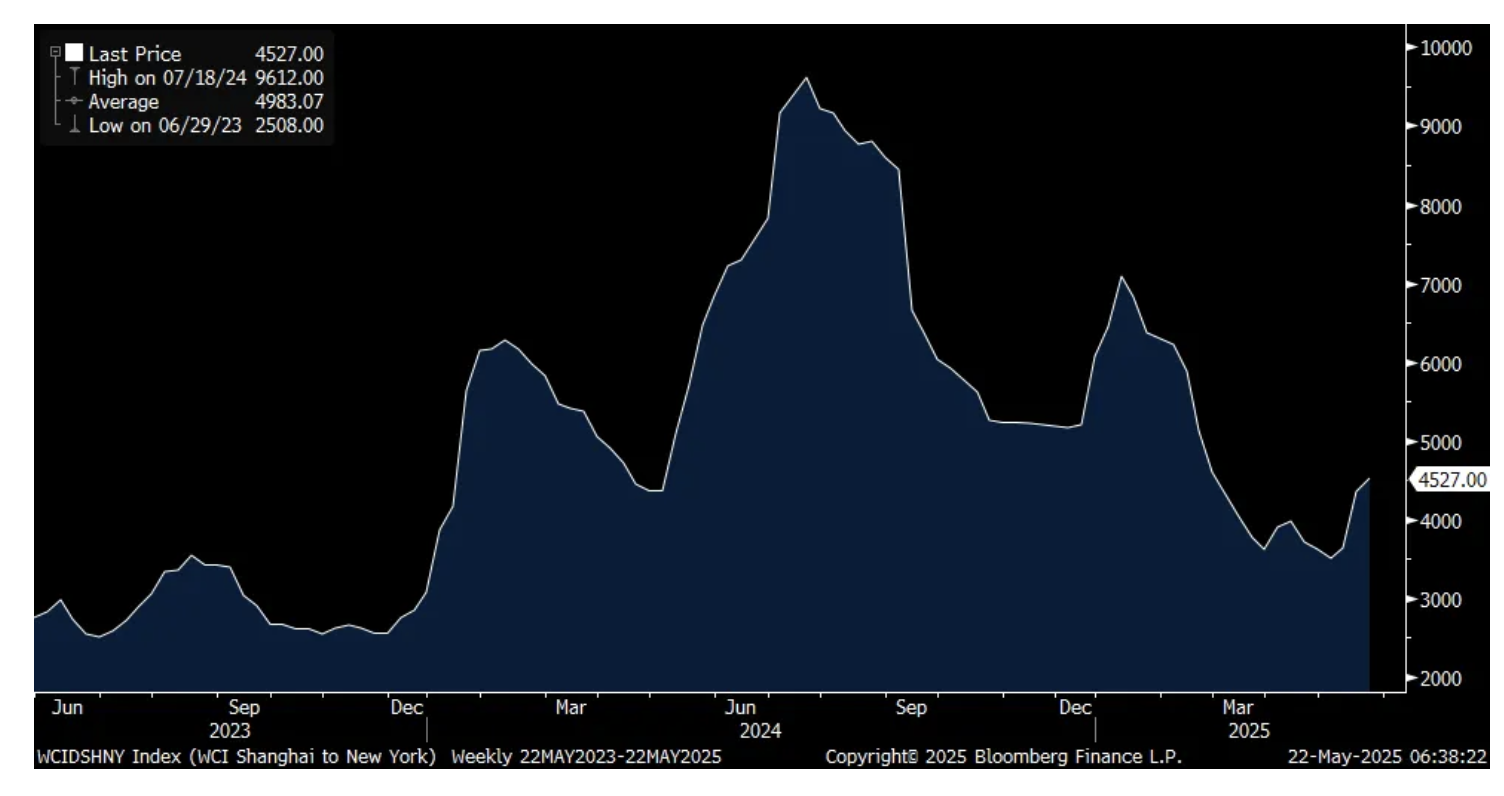

Updated container shipping prices just came out and after last week's sharp rise, they were only up modestly w/o/w. From Shanghai to LA, the price of a 40 foot container went up by $61 to $3,197. The Shanghai to NY route saw a price gain of $177 to $4,527. I'm surprised they didn't go up more which maybe implies that a 30% tariff on imported Chinese goods is still punitive.

Shanghai to LA

Shanghai to NY

Ahead of the May US manufacturing and services PMI today, Japan's composite index fell back under 50 at 49.8 from 51.2 with all of the weakness in services as manufacturing ticked up a touch to 49 from 48.7. Services fell to 50.8 from 52.4. Australia's index was 50.6 vs 51 with no change in manufacturing at 51.7 while services fell .5 pt to 50.5. India remains an economic rock with its composite index higher by 1.5 pts m/o/m to 61.2.

In the Eurozone, manufacturing was up .4 pts to 49.4 but services were down at 48.9 from 50.1. The two biggest economies in the region continue to lag as Germany's composite index was at 48.6 and France's was at 48.

S&P global said, “The eurozone economy just cannot seem to find its footing. Since January, the overall PMI has shown only the slightest hint of growth and in May, the private sector actually slipped into contraction. Do not blame US tariffs for this one. In fact, efforts to get ahead of those tariffs might partly explain why manufacturing has held up a bit better lately. Manufacturers have now increased production for the third straight month, and for the first time since April 2022, new orders did not decline. On the flip side, service providers, who are generally less exposed to US trade policy, except in areas like international logistics, are seeing business activity shrink for the first time since November 2024. While foreign demand for services is softening, it is the sluggish domestic demand that seems to be dragging the sector down."

And, “May’s snapshot is not pretty. Looking ahead, companies are only cautiously optimistic. The expectations index is still well below its long-term average. However, there are reasons for confidence in the longer term. The recovery in manufacturing is broad-based, with encouraging signs coming out of both Germany and France. Further interest rate cuts could provide a boost, and lower oil prices compared to last year are also helping. Germany, in particular, might be gearing up to reclaim its role as the eurozone’s economic engine, thanks to a potentially very expansionary fiscal policy."

With regards to inflation in the region, "Manufacturing input costs decreased for the second consecutive month, and to the largest extent since March 2024. On the other hand, services input prices were up sharply again, with the pace of inflation slightly stronger than in April. Overall, input costs increased at a broadly similar pace to that seen in the previous month, with inflation just below the series average."

The UK also saw a below 50 print at 49.4, though up from 48.5 in April with manufacturing badly lagging still at 45.1 while services rose back above 50 at 50.2. S&P Global said, "After an 'awful April', businesses reported a milder May. Business confidence has rebounded from April's recent low, which had seen confidence collapse to a degree not seen since the Truss Budget of 2022, and price pressures have moderated after spiking higher. Sunny weather also provided a welcome boost to business activity in some parts of the economy. However, output still fell slightly when measured across all goods and services for a 2nd successive month, hinting at the possibility of the economy contracting in the second quarter."

On pricing, "UK private sector companies indicated a sharp increase in their average cost burdens during May, although the rate of inflation eased considerably from April's 26 month high. Similarly, output charge inflation eased to its lowest so far in 2025. Higher input prices were attributed to strong pay increases, as well as rising utility bills, shipping costs and prices paid for technology services." On the flip side, lower energy prices were cited by many firms.

Also out in Europe was the German May IFO business confidence index which rose to 87.5 from 86.9 with all of the gain in the Expectations component while the Current Assessment fell slightly. The index is now at the highest level since June 2024 on the optimism with the outlook on the heels of the upcoming fiscal largess. IFO said "The German economy is slowing regaining its footing." Helping was a lift in the beleaguered manufacturing sector. IFO said "The upturn in sentiment was particularly strong in the food industry, while sentiment in the chemical industry deteriorated slightly."

French business confidence in May was down by 1 pt with particular weakness in manufacturing and services.

The May UK industrial orders index fell to -30 from -26 and that was 6 pts below expectations. That's the weakest since January. CBI said "Sentiment among UK manufacturers seems poor, reflecting a combination of rising domestic business costs and US tariff uncertainty. Many respondents to the survey reported a reluctance to spend among their customers."

Before I get to some earnings calls, CNBC reported today that "Nike will raise prices on a wide range of footwear, apparel and equipment as soon as this week as the retail industry braces for tariffs to hit its profits." Specifically, "Prices for Nike apparel and equipment for adults will increase between $2 and $10, a person familiar with the matter said. Footwear priced between $100 and $150 will see a hike of $5, while sneakers priced above $150 will see a $10 increase, the person said."

"The price hikes will be in effect by June 1, but could be seen on shelves as soon as this week, the person said. The increases cover a large portion of Nike's assortment, but many products will remain the same price."

A one time price increase or not, consumers still have PTSD from 2021 and 2022 price spikes that have continued on since.

From Target:

"For several years now we've seen pressure in our discretionary businesses as spending adjusted down from elevated levels during the pandemic and then moved further away in the face of historically high inflation in needs based categories. On top of those ongoing challenges, we faced several additional headwinds this quarter, including five consecutive months of declining consumer confidence, uncertainty regarding the impact of potential tariffs, and the reaction to the updates we shared on Belonging in January (the woke stuff they did). While we believe each of these factors played a role in our first quarter performance, we can't reliably estimate the impact of each one separately."

"In planning for the remainder of the year, we believe it's prudent to expect that current top-line pressures will continue in the near term."

"As we've shared, for multiple quarters, consumers have been choiceful in their buying decisions, and recent declines in consumer confidence have made them even more cautious. They're focused on finding ways to save as they manage their family's budget. However, as we've noted before, consumers are still making discretionary purchases when they find products at the right intersection of style, quality, and value."

In the quarter, "net sales were down 2.8%, reflecting a decline in traffic as well as a lower average basket."

From Lowe's:

"And although we are pleased with our continued progress in customer services, our financial results also reflect ongoing pressure in DIY, bigger ticket, discretionary demand, and a slower start to spring versus last year, with exceptionally unfavorable weather across much of the country in February. As the weather normalized, we were encouraged by our business performance."

From TJX, the go to value spot for many things:

"Overall comp sales grew 3% at the high end of our plan. Every division, both in the US and internationally drove increases in comp sales and customer transactions."

"As always, we offered great value to our shoppers every day at each of our retail banners. Looking ahead, we are convinced that our value proposition and the flexibility of our business will continue to be a winning retail formula."

"Overall, comp sales growth was almost entirely driven by an increase in customer transactions. Comps in both our apparel and home categories increased with home outperforming apparel."

From Urban Outfitters, whose stock is popping pre market after good numbers with particular strength in its Anthropologie and Free People brands:

This is how they are managing the tariffs, "First, negotiating better terms with our vendors. Second, shifting our countries of origin, where possible. Third, shifting our mode of transportation from air to boat. And lastly, gently and sparingly raising some prices. Please note that any price increases will be very strategic, protecting opening price points and only targeting areas where we believe we could raise prices without affecting the overall customer experience."

"Despite the noise in the headlines and the broader economic uncertainty, our customers continued to show resilience in Q1. We haven't seen any signs of a demand slowdown. In fact, customers were eager for fresh spring fashion, and our teams delivered from compelling assortments to standout store experiences and inspiring marketing. We exceeded their expectations. The result, positive comps across every brand and every segment."

From Toll Brothers:

"We experienced softer demand in the second quarter due to a decline in consumer confidence driven by increased economic uncertainty. These conditions have continued into our third quarter. In this environment, we believe prioritizing price and margin over pace makes the most strategic sense."

"Our average sales prices in the quarter was approximately $983,000 compared to $1 million in our first quarter and $967,000 in the second quarter of fiscal 2024. Given the softer demand environment, we modestly increased incentives in the quarter. Overall, incentives were approximately 7% of the average sales price, up from our recent average of 5% to 6%."

BY Doug Kass · May 22, 2025, 10:15 AM EDT

* Avoid the crowd and always consider the contrarian.

In Tuesday's opening missive I aggressively warned about the possibility of an abrupt reversal and the end of the march higher in equities — and The End of the (Macro) Free Lunch — in "Rethinking American Exceptionalism."

Several minutes later I warned, as TLT plummeted, that the rapid rise in interest rates could soon choke off the market rally:

Doug Kass

STAFF

TLT drop problematic, adding to shorts.

Position: None.

By Doug Kass May 20, 2025 9:47 AM EDT

Yesterday's (Wednesday) opener summarized my concerns:

… Making your way in the world today

Takes everything you've got

Taking a break from all your worries

Sure would help a lot

Wouldn't you like to get away?

… All those nights when you've got no lights

The check is in the mail

And your little angel

Hung the cat up by it's tail

And your third fiance didn't show

… Sometimes you wanna go

Where everybody knows your name

And they're always glad you came

You wanna be where you can see (ah-ah)

Our troubles are all the same (ah-ah)

You wanna be where everybody knows your name

- Cheers full theme song (from 200th show)

You all know my name by now (!) and you all know why I have embraced an increasingly negative market view.

While Bull Markets (and we have had one for more than two years) die hard, "our troubles are all the same."

Indeed, my primary conclusions (below) from yesterday's opener, "Rethinking American Exceptionalism" remain intact - I am a (short) seller on any rally:

* Political and geopolitical polarization and competition will probably translate into less political centrism and a reduced concern for deficits - creating structural uncertainties, limited fiscal discipline and imprudence around the globe ... and for the possibility of bond markets to "disanchor"

* The cracks in the foundation of the Bull Market are multiple and are deepening, but they are being ignored (as market structure changes have led to price momentum (FOMO) being favored over value and common sense)

* With the S&P 500 Index at 5965, the downside risk dwarfs the upside reward for equities - in a ratio of about 3-1 (negative)

* Valuations and (consensus) expectations for economic and corporate profit growth are all inflated* Being dismissed are JPMorgan CEO Jamie Dimon's dour comments on complacency and his view that the corporate credit market is "ridiculously over-stretched" (hat tip Rosie)

* Look for the soft data to move into (and weaken) the hard data led by a slowing housing market likely to provide ample near-term evidence of the exposure and vulnerability of the middle class

* Below trend-line economic growth with sticky inflation lie ahead ("slugflation") - uncomfortable for a Federal Reserve which has to make increasingly more difficult decisions

I agree with Pete.

RIP Norm.

"Sometimes you wanna go

Where everybody knows your name

And they're always glad you came"

By Doug Kass May 21, 2025 7:17 AM EDT

Do your own homework, rely on your own wit (common sense and analysis).

At times, avoid the herd and always consider the contrarian.

And, caveat emptor.

I continue to believe that equities topped out in late January, 2025, so may have The Mag 7, which could resemble The Nifty Fifty (seminal) top in January 1973, and that a negative year is likely for the S&P index.

I also think, that despite last night's heart-breaking loss, the New York Knicks will beat the Indiana Pacers in seven games.

BY Doug Kass · May 22, 2025, 9:30 AM EDT

-NVTS +162% (NVIDIA selects Navitas to collaborate on Next Generation 800 V HVDC Architecture)

-XAGE +63% (receives favorable decision from NASDAQ Hearings Panel allowing company to continue listing on the exchange following proposed merger with 20/20 BioLabs. Inc.)

-AAP +36% (earnings, guidance)

-BDRX +21% (announces award of additional $3.0M grant from CPRIT to support Registrational eRapa Phase 3 Program in FAP)

-URBN +17% (earnings, color)

-TITN +10% (earnings, guidance)

-LUMN +9.2% (AT&T to acquire Lumen's Mass Markets Fiber Business for $5.75B in cash)

-PBI +9.2% (appoints Kurt Wolf as Chief Executive Officer, effective immediately; Affirms FY25 guidance)

-SIDU +8.3% (launches Fortis VPX, a ruggedized, AI-powered 3U OpenVPX module supporting complex missions from sea to space)

-SNOW +8.2% (earnings, guidance)

-RAMP +8.7% (earnings, guidance)

-DOMO +5.3% (earnings, guidance)

-AMSC +3.6% (earnings, guidance)

-SLNH +3.6% (to launch first solar-powered data center with 75 MW project)

-ADI +3.1% (earnings, guidance)

-BJ +2.6% (earnings, guidance)

-OMCL +2.1% (guidance)

-REPL +2.1% (earnings)

-CVM -47% (prices 2M shares at $2.50/share)

-SOC -5.5% (prices 8.7M shares at $29.50/share)

-BZ -3.7% (earnings, guidance)

BY Doug Kass · May 22, 2025, 9:21 AM EDT

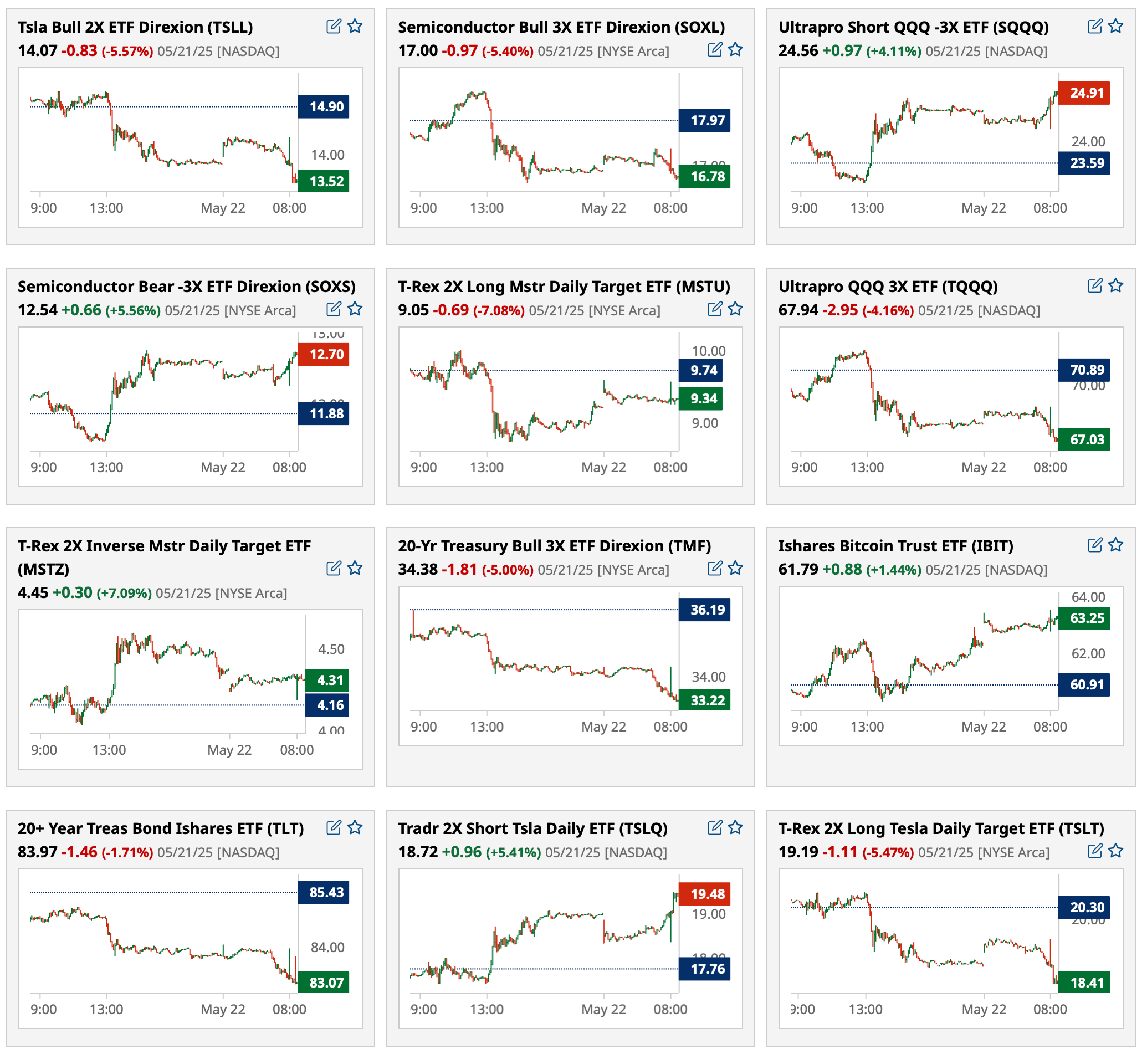

Most active premarket ETFs as of 8:24 a.m.:

BY Doug Kass · May 22, 2025, 9:13 AM EDT

Out of TLT trading long rental at $83.63 for a tiny profit.

BY Doug Kass · May 22, 2025, 9:02 AM EDT

Premarket percentage movers at 8:39 a.m. ET:

BY Doug Kass · May 22, 2025, 9:00 AM EDT

8 a.m.: Fed Bank of Richmond President Barkin (Non-Voter) participates in a fireside chat before the Roanoke Regional Chamber of Commerce and Roanoke Business Council, Roanoke, VA (No text. No livestream. No media Q&A);

2 p.m.: Fed Bank of New York President Williams (Voter) gives keynote before Monetary Policy Implementation Workshop: "

BY Doug Kass · May 22, 2025, 8:55 AM EDT

I reshorted TSLA yesterday:

TSLA Reshorts Tesla (TSLA) at $346.61Position: Short TSLA VS

Short TSLA S

May 21, 2025 10:21 AM EDT

BY Doug Kass · May 22, 2025, 8:45 AM EDT

Adding to TLT at $83.12.

BY Doug Kass · May 22, 2025, 8:39 AM EDT

Covering my RSP trading short rental in premarket trading.

BY Doug Kass · May 22, 2025, 8:34 AM EDT

BY Doug Kass · May 22, 2025, 8:30 AM EDT

BY Doug Kass · May 22, 2025, 8:16 AM EDT

Covering ARKK in premarket trading for a profit.

BY Doug Kass · May 22, 2025, 8:09 AM EDT

The two-decade low in the U.S. equity risk premium suggests a challenging backdrop for equities, as the balance between downside risk and upside reward is less favorable than in the past:

BY Doug Kass · May 22, 2025, 8:02 AM EDT

BY Doug Kass · May 22, 2025, 7:52 AM EDT

BY Doug Kass · May 22, 2025, 7:42 AM EDT

BY Doug Kass · May 22, 2025, 7:34 AM EDT

BY Doug Kass · May 22, 2025, 7:10 AM EDT

* Technicians operate in herds.

* The last week was about a soaring equity market (no more).

* Now replaced by soaring cryptocurrency prices.

* Caveat emptor.

Bonus - Here are some great links:

BY Doug Kass · May 22, 2025, 6:55 AM EDT

Doomberg on "Actuarial Explanations."

BY Doug Kass · May 22, 2025, 6:45 AM EDT

BY Doug Kass · May 22, 2025, 6:35 AM EDT

I took a small long trading rental in TLT at $83.79 at 4:01 a.m. this morning.

And, as posted, I covered all my index shorts last night at around 7:30 p.m.

BY Doug Kass · May 22, 2025, 6:25 AM EDT

The S&P Short Range Oscillator dropped to 3.04% from 5.73%.

BY Doug Kass · May 22, 2025, 6:15 AM EDT

* Covered my Index shorts last night...

Dougie Kass

At 7:30PM I am covering all of my Index shorts:

I have no Index positions on now.

BY Doug Kass · May 22, 2025, 6:04 AM EDT