Subscriber Comments of the Day: An Unhealthy System

chrisideker

39 minutes ago

As to UNH, my last assignment before retirement was the IRO for a large Medicare Advantage plan's CIA. The role is somewhat analogous to being a probation officer for a felon after release. I have a couple of observations:

1) Healthcare fraud always sounds worse than it is.

2) Whistleblowers are usually institutional chicken littles.

3) There is usually a parallel criminal investigation to what is largely a civil matter. The resolution will be money, with potentially a few heads rolling. The whistleblowers will get up to 30% of the recovery. They are coached by whistleblower law firms who love to file qui tams against MA plans- deep pockets and extrapolatable damages.

4) Our fiscal situation is horrific. A huge portion of that is due to Medicare. If one were to account for our Medicare liability (as well as Social Security and Medicaid) in accordance with FASB 106, instead of the "pay as you go" BS of our Federal Government, the actual deficit would be about 170 trillion- instead of 37 trillion.

5) There is no appetite to touch entitlements by either party. The only way out is to dramatically reduce our per capita healthcare spend- currently the highest in the world.

6) Medicare Advantage is the most logical solution. Other countries have demonstrated this. The National Heathcare system in Israel has four managed care plans with mandatory membership. They have a longer life expectancy and 40% of the cost.

7) DOJ and HHS are not going to kill one of the few major providers of MA.

8) Notwithstanding my optimism, this investigation will last 3-4 years with headline risk throughout.

I bot UNH @ 273.85 and sold 90% of my position at 308. I fully expect a retest of the lows. I will buy below 290.

Reply

douglas cassel

30 minutes ago

I was in the industry on the billing side. About 30% of the health care spend is siphoned off by insurance and billing companies. There is no added value from these companies or the entire industry.

I am about as big a believer in capitalism as there is, but this is clearly a market failure, another "tragedy of the commons".

Fixing the system is above my pay grade, but pointing out the problems is pretty easy.

This was a great call from The Goat and my mentor:

The Chief's Signal Now Says Sell/Short!

* The "J Factor" has turned negative this morning...

For what it is worth (and it shouldn't be worth much!), I have used a proprietary buy/sell technical indicator developed by The Chief - for several decades.

For the first time in the rally it has just signaled sell.

Target faced a tough Q1 with declines in traffic and sales, especially in discretionary categories, due to prolonged inflation, waning consumer confidence, and external headwinds like tariff uncertainty and public reaction to DEI-related updates.

Target created a new enterprise acceleration office led by a seasoned executive to increase organizational speed, adaptability, and innovation amid rising uncertainty.

The merchandising team is actively planning for tariff impacts by leveraging vendor relationships and global sourcing scale; maintaining price competitiveness remains a top priority.

Management said they have many levers to use in mitigating the impact of tariffs and price is the very last resort.

Despite near-term pressures, Target is maintaining long-term investments in new stores, remodels, supply chain, and technology, supported by a strong balance sheet.

Digital channels showed resilience with mid-single-digit growth, including 36% growth in same-day delivery and continued expansion in profitable services like retail media (Roundel) and third-party marketplace (Target Plus).

Inventory shrink is moderating, and the company is seeing positive returns from new store openings and remodels.

Q1 capital expenditures totaled $790 million; full-year CapEx is now expected to come in near the lower end of the $4-$5 billion range due to updated project timing.

Paid $510 million in dividends in Q1 and plans to recommend a modest quarterly dividend increase later this year.

Expect many Q1 themes to persist in Q2, with headwinds, including continued sales pressure, tariff impacts and some additional costs to adjust inventory and receipts with continued benefits from lower shrink and productivity gains.

In the back half of the year, company said it will be lapping easier comparisons from 2024 and expect to have inventory and receipt adjustment costs in the rear view.

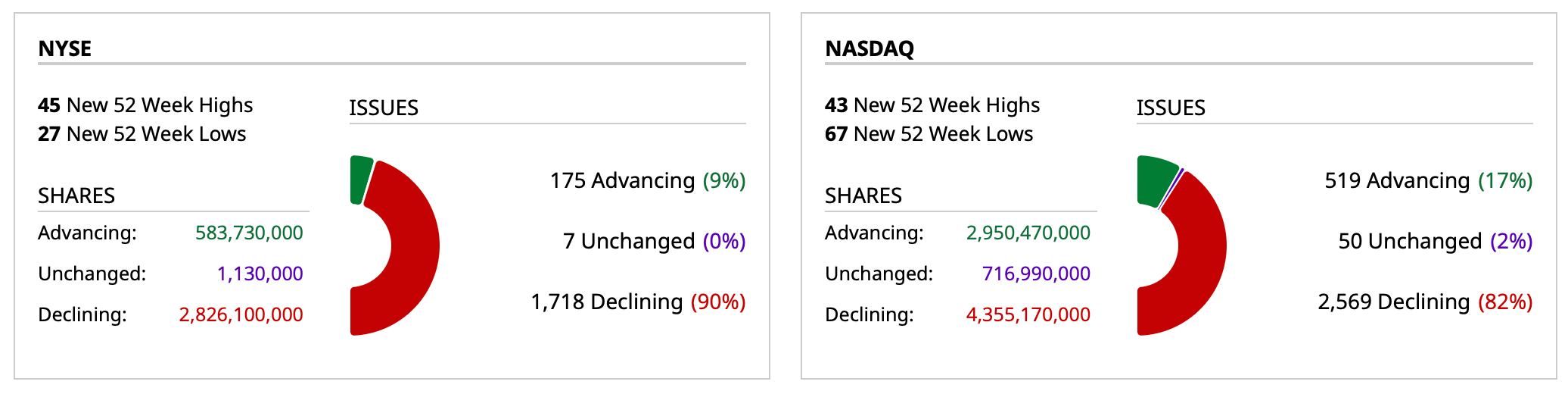

JGB yields continued higher overnight with the 40 yr yield now up in 10 out of the last 11 days and by 43 bps in this time frame. The 10 yr yield was up by 2.2 bps to 1.53% and is approaching the recent 17 yr high of 1.59%. The selling spilled over to other sovereign bond markets in Asia and also in Europe too day with European yields up 5-7 bps across the board. This explains too why the US 10 yr yield is back above 4.50% and the 30 yr yield has a 5 handle again.

Negatively impacting European rates was the higher than expected UK CPI figure for April. Headline CPI was up by 3.5% y/o/y, two tenths more than anticipated. The core rate was higher by 3.8% y/o/y, also two tenths above the estimate. A 28% m/o/m rise in airfares because of the timing of Easter this year was a main factor for the upside but gilt yields are still higher as are inflation breakevens in the UK. The pound is a hair below the highest level vs the US dollar since February 2022.

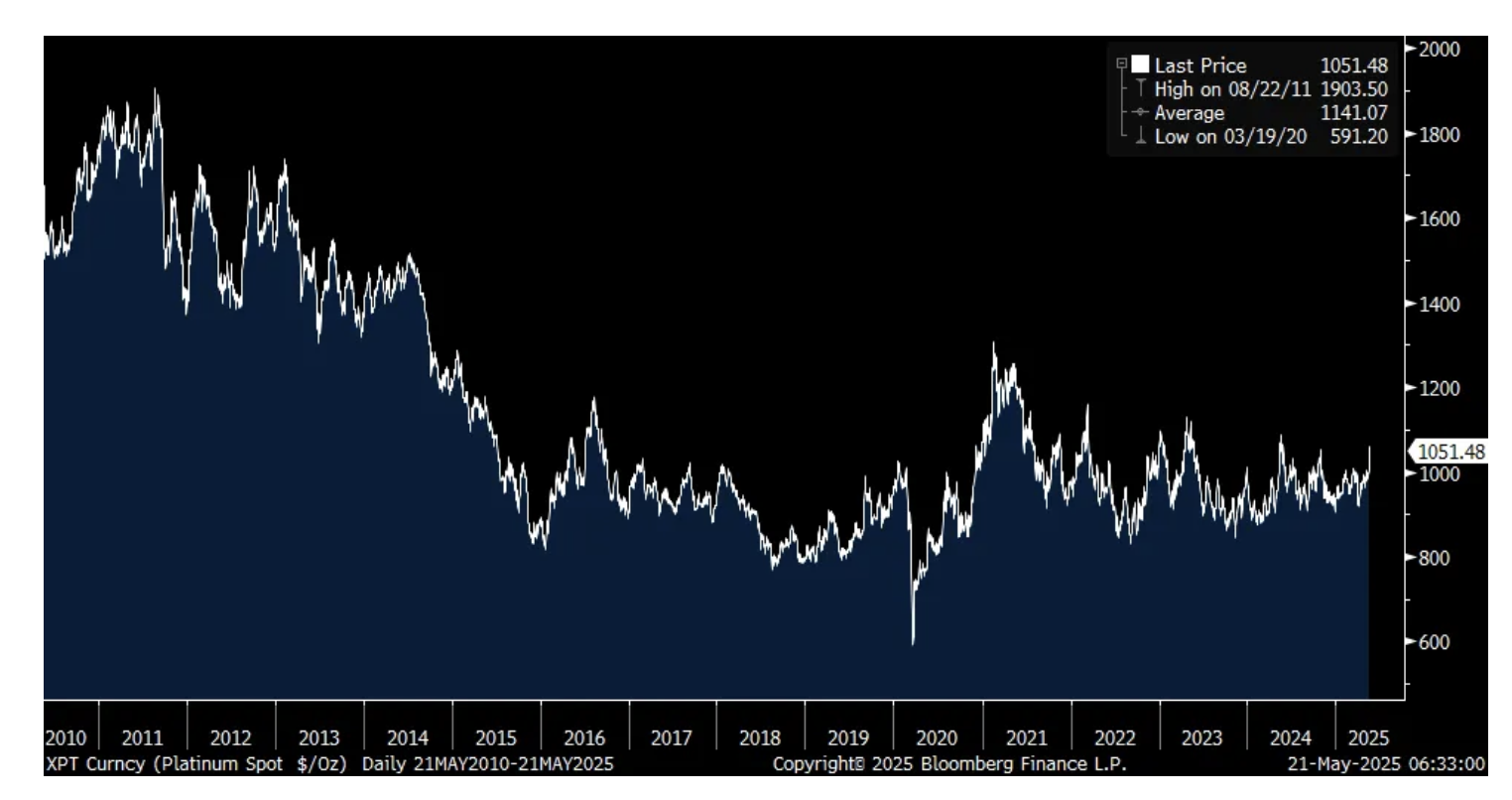

Gold is regaining some life again after the recent correction and we remain bullish and long as its reserve asset importance becomes further solidified. Silver too has a bid and I want to point out platinum, another precious metal we are long and bullish on. Platinum yesterday closed at a one yr high, though is still down 45% from its peak in 2011. About 40% of demand use for platinum goes into catalytic converters used for taming exhaust emissions and with hybrids seemingly winning the VHS/Betamax battle against full EVs, the demand for this metal should continue on. And in fact, the World Platinum Investment Council forecasts supply deficits relative to demand in the few years to come after deficits seen in the past few years.

A catalyst for the 5.6% rally in platinum yesterday was a Bloomberg story titled "China Imports the Most Platinum in a Year as Squeeze Tightens." China happens to be the largest consumer of platinum in the world. If you're looking for a cheap asset, and a hard asset at that, this is one of them.

Platinum

The April US Architecture Billings Index fell further below 50 to 43.2 from 44.1 in March. Most notable was the drop to 40.5 from 45.1 in the commercial/industrial sector, joining multi-family residential around the 40 level. The chief economist there said, "Uncertainty as to the economic outlook continues to hold back progress on new construction projects. Despite the slowdown in billing activity, architecture firms continue to navigate this business cycle quite effectively, as staffing at firms remains relatively stable and project backlogs are holding up better than expected."

To some earnings reports that include a window into the behavior of the consumer.

From Home Depot:

"Our customers engaged across smaller projects and in our spring events...However, the higher interest rate environment continues to pressure larger remodeling projects...we continue to see softer engagement in larger discretionary projects where customers typically use financing to fund the project such as kitchen and bath remodels."

"During the first quarter, Pro comp sales were positive and outpaced the DIY customer."

"In the first quarter, six of our 16 merchandising departments posted positive comps, including appliances, plumbing, indoor garden, electrical, outdoor gardens and building materials. During the first quarter, our comp average ticket was essentially flat, and comp transactions decreased .5%."

They remain optimistic on their business this year and why they reaffirmed guidance with hopes for an eventual lift in bigger renovations. "Our consumer has a job, increasing wages, increases of home equity are up as much as 50% since the end of '19, why haven't we seen that larger remodeling cycle, particularly as people stay in their homes?" Yes, it is partly financing costs but many did this in 2020, 2021 during Covid.

To repeat from yesterday, Home Depot sources more than 50% of its items domestically and has really diversified supply chains elsewhere. Also, they have a 10% net income margin so has a lot more wiggle room in dealing with tariffs than Walmart and other retailers.

Target missed numbers and cited in its earnings release "a highly challenging environment."

American Sports stock spiked by 19% yesterday on a good quarter and reflecting that consumers are still spending on athletic apparel and sporting goods. Also, their US business is just 26% of total sales and they have an upper income customer. "Our performance was led by strong growth and profitability in both technical apparel and outdoor performance, as well as solid sales and margin results in ball and racquet. In addition to the continued broad based trends from our flagship brand Arc'teryx. I'd like to highlight the growing momentum behind the Salomon sneakers...Furthermore, our market leading hard goods equipment franchises delivered better than expected results for both winter sports equipment (particularly skiing) and the Wilson ball and racquet."

Viking Holdings, the river cruise company catering to upper income consumers, saw its stock fall 5% after numbers on questions about its guidance but business still seems to be pretty good.

"Overall, we had a busy first quarter, driven by additional capacity and strong demand that led to almost $900 million of revenue. Notably, revenue for the first quarter is almost three times higher than what we generated in 2019...We believe that this reflects the strong demand for our product and the disciplined execution of our growth strategy."

"We continue to experience strong demand for our core products with 92% of our 2025 capacity already sold...To this end, our focus is on 2026, which is off to a great start with 37% of our core capacity already sold as of May 11."

Also, "given the current macroeconomic landscape, I'd also like to provide an update on how bookings are trending. When we last met in mid-March, we noted that January was the best booking month in the history of the company. We can also say that this was the best wave season in our history, with more guests booked and at higher pricing. Since wave, we are pleased to say this momentum has continued, specifically given 2025 is practically sold, and we look to future seasons, bookings in April and May are up y/o/y. In fact, May is off to an outstanding start with the last few weeks showing good bookings strength."

Toll Brothers beat numbers and its stock is up pre-market. "We believe these results highlight the strength of our broadly diversified luxury product offerings, price points and geographies, our balance portfolio of build-to-order and spec homes, and our strategy of prioritizing sales price and margin over pace in the current environment."

It seems to be the builders that focus on lower priced homes that are having more affordability challenges with their customers. Their earnings call is this morning.

Palo Alto Networks helped to explain why CapEx on building out AI capabilities remains strong:

"Let's be clear, you can't walk around the street corner at a conference without hearing the words AI. The urgency to adopt AI is omnipresent in all of our customers. It no longer seems to be a choice. It is becoming a strategic imperative for every customer as the risk of inaction is too high. During every conference, every customer conversation, the topic of AI transformation is more and more frequent and now the conversation is shifting to Agentic AI. What's fascinating is this is actually creating a higher sense of urgency amongst our customers to undertake their technology transformations, transformations that require a fundamental change in their infrastructure."

And Palo Alto wants to sell you the cybersecurity software as part of this.

On what they are seeing from a macro perspective. "I think we're back to normal in a way. But there was, as you can imagine, not too far long ago, there were conversations around tariffs around the world. There were all kinds of supply chain shocks that were anticipated, which did cause some of our customers to think, oh my god, what's going to happen, next time I ship a car across the border, it's going to be twice as expensive, or I can't ship anything, what am I doing over here? So you saw that little sort of uncertainty in the market, which happened to be in the last month of our quarter."

"It was not an easy quarter to execute. Had we not had the tariff conversations or geopolitical tensions, it would have been much easier to sail through it. But we had our lessons from the pandemic. We had our lessons from the supply chain crisis. So we had to go back and pull up our shorts and execute the same practices that we did then."

"And we're kind of like on the same sort of cadence now in Q4, because we are trying to stay ahead of the curve, because I don't think many of our customers changed their plans from a transformation perspective, but there was a pause for a few days where they were trying to figure out where the market goes. And thankfully, as you see, that we seem to have overcome that as a global economy. So there's a little more, I'd say stability in the business climate than there was towards the sort of, I'll say, the early to mid part of April."

Shifting back to the economic data, mortgage applications fell 5.1% w/o/w. With a 6 bp rise in the average 30 yr mortgage rate to 6.92%, purchase apps fell 5.2% and refi's were lower by 5%. A 50% rise in home prices over the past 5 years and around a 7% mortgage rate continues to be a challenge for that first time buyer.

After a 4% y/o/y export rise in March, they slowed to a 2% gain in April in Japan with of course the tariff distortions flowing thru the figures. We'll see how things settle out at in coming months when we get past all the pull forward and the hangover.

Takes everything you've got Taking a break from all your worries Sure would help a lot Wouldn't you like to get away?

… All those nights when you've got no lights The check is in the mail And your little angel Hung the cat up by it's tail And your third fiance didn't show

… Sometimes you wanna go Where everybody knows your name And they're always glad you came You wanna be where you can see (ah-ah) Our troubles are all the same (ah-ah) You wanna be where everybody knows your name

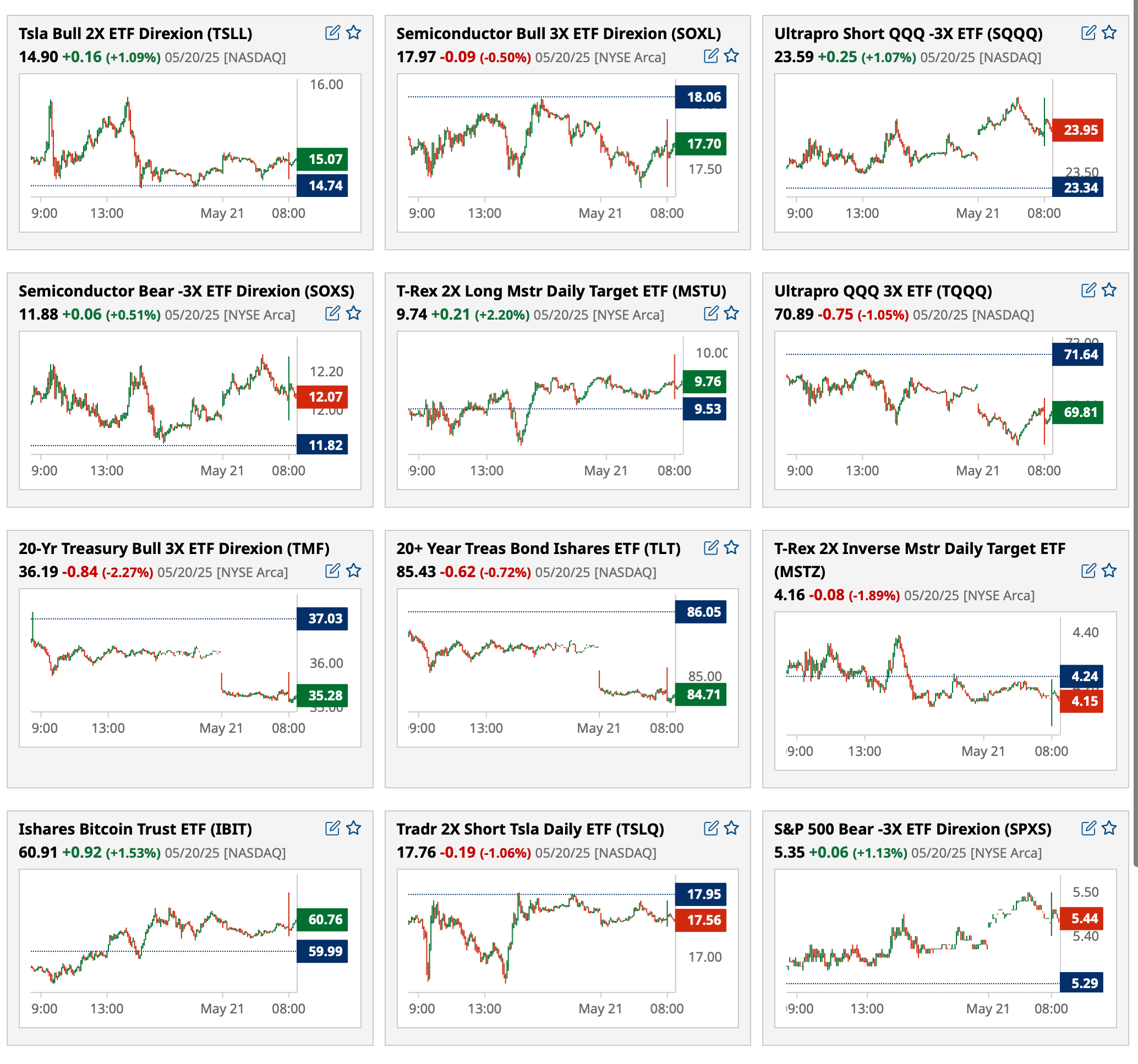

* Political and geopolitical polarization and competition will probably translate into less political centrism and a reduced concern for deficits - creating structural uncertainties, limited fiscal discipline and imprudence around the globe ... and for the possibility of bond markets to "disanchor"

* The cracks in the foundation of the Bull Market are multiple and are deepening, but they are being ignored (as market structure changes have led to price momentum (FOMO) being favored over value and common sense)

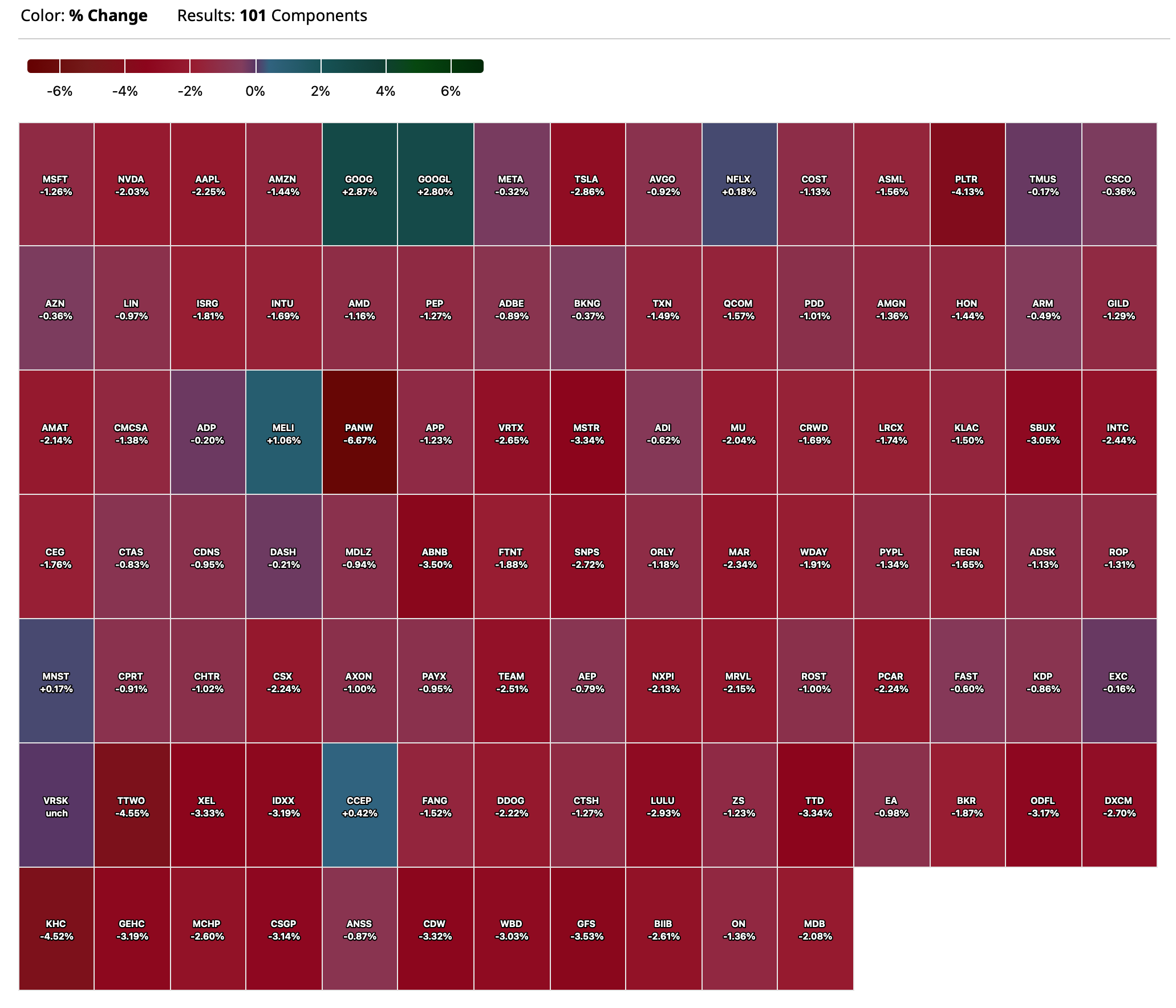

* With the S&P 500 Index at 5965, the downside risk dwarfs the upside reward for equities - in a ratio of about 3-1 (negative)

* Valuations and (consensus) expectations for economic and corporate profit growth are all inflated* Being dismissed are JPMorgan CEO Jamie Dimon's dour comments on complacency and his view that the corporate credit market is "ridiculously over-stretched" (hat tip Rosie)

* Look for the soft data to move into (and weaken) the hard data led by a slowing housing market likely to provide ample near-term evidence of the exposure and vulnerability of the middle class

* Below trend-line economic growth with sticky inflation lie ahead ("slugflation") - uncomfortable for a Federal Reserve which has to make increasingly more difficult decisions

As mentioned in yesterday's opening missive, "Rethinking American Exceptionalism," a reduced level of concentrated safe-haven buying of U.S. bonds and stocks is being reflected again this morning in higher bond yields and lower stock futures (-43 handles):

* The yield on the 10-year US Treasury note is +6 basis points to yield 4.54%.

* The yield on the 30-year US Treasury bond is also +6 basis points to yield 5.03%.