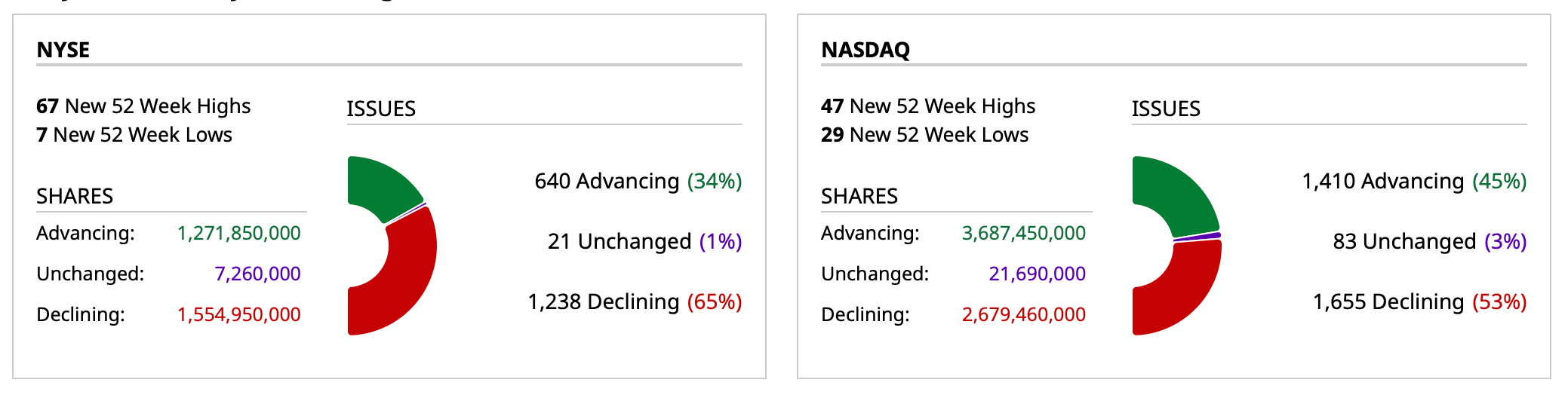

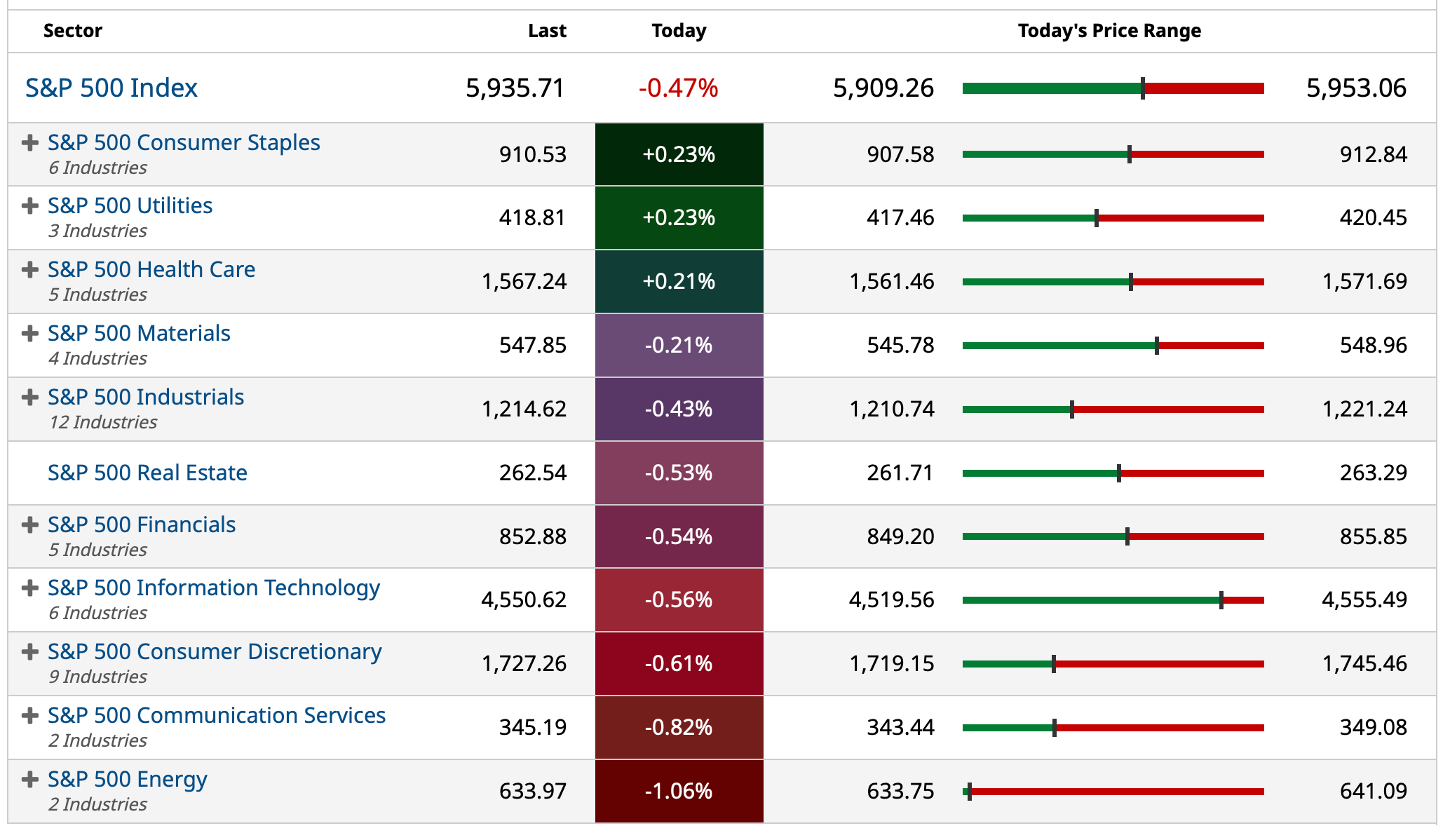

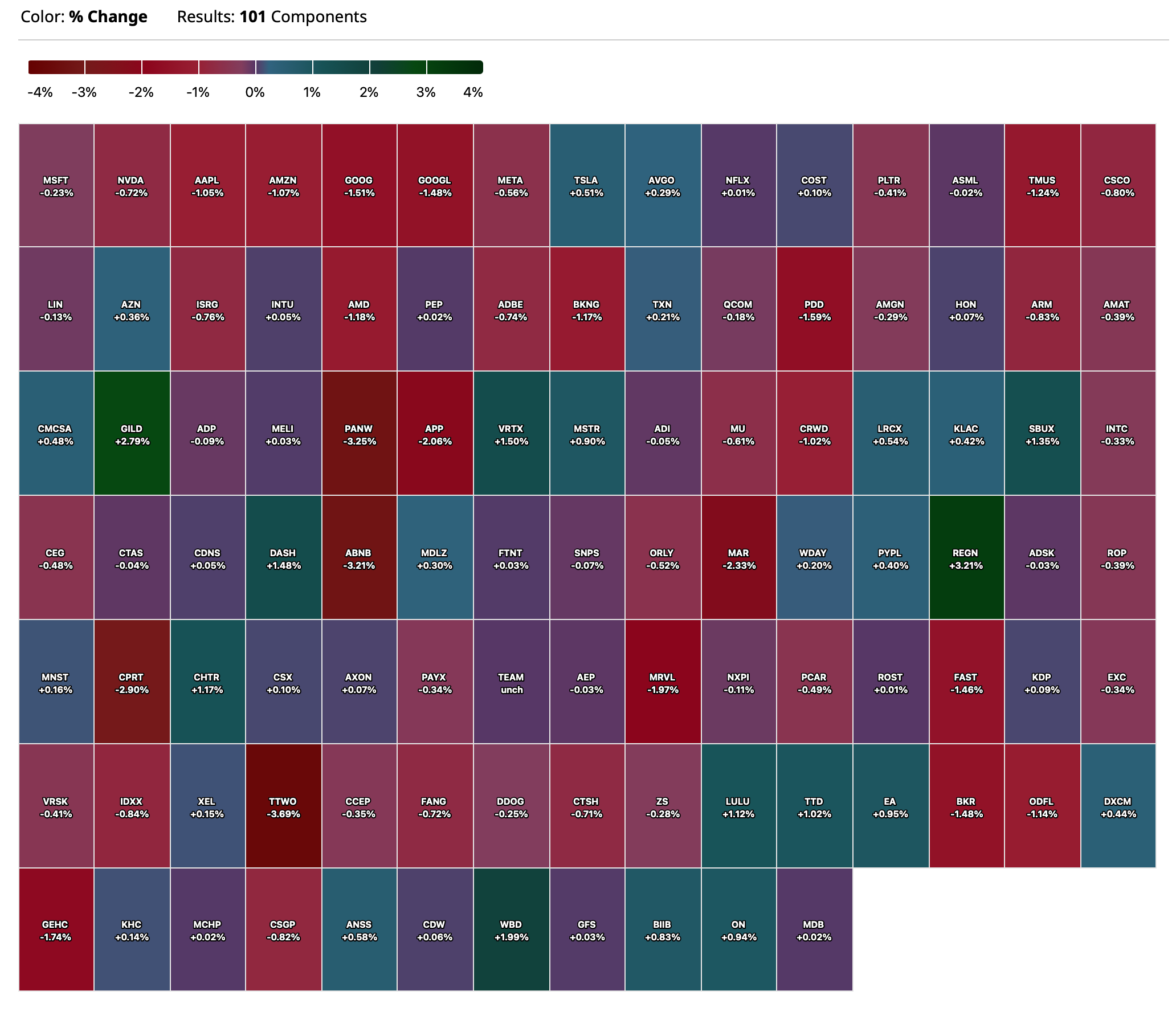

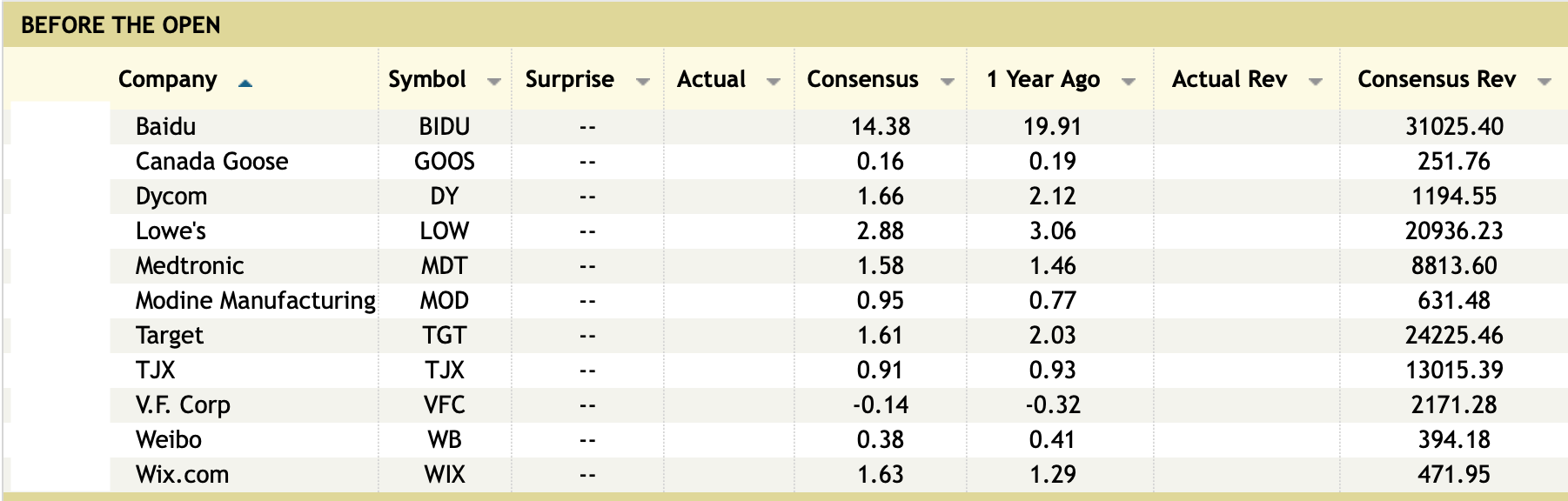

Closing Breadth, Sectors and Heat Map

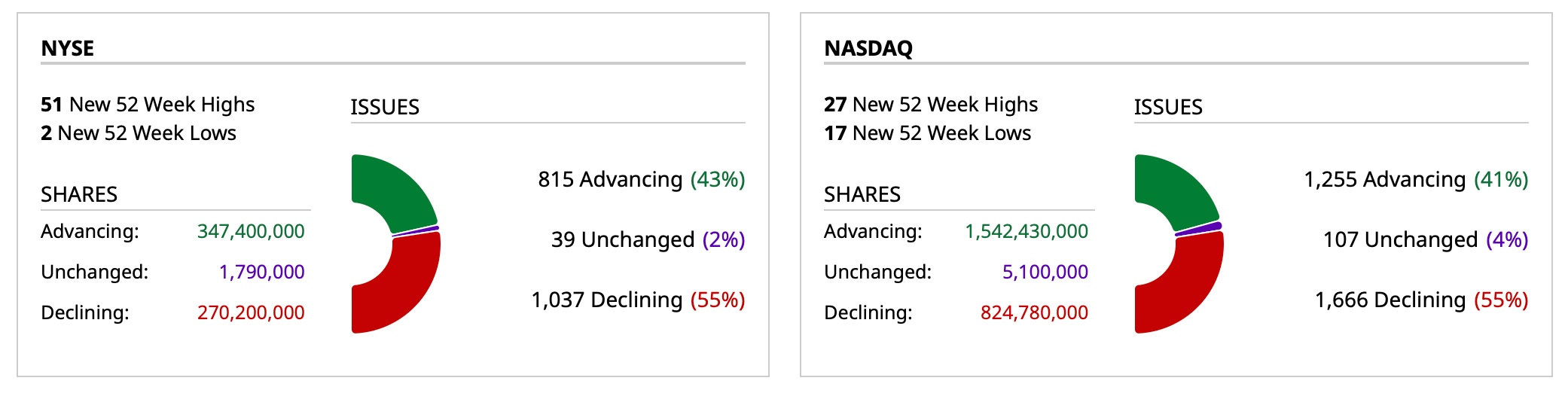

Closing Breadth

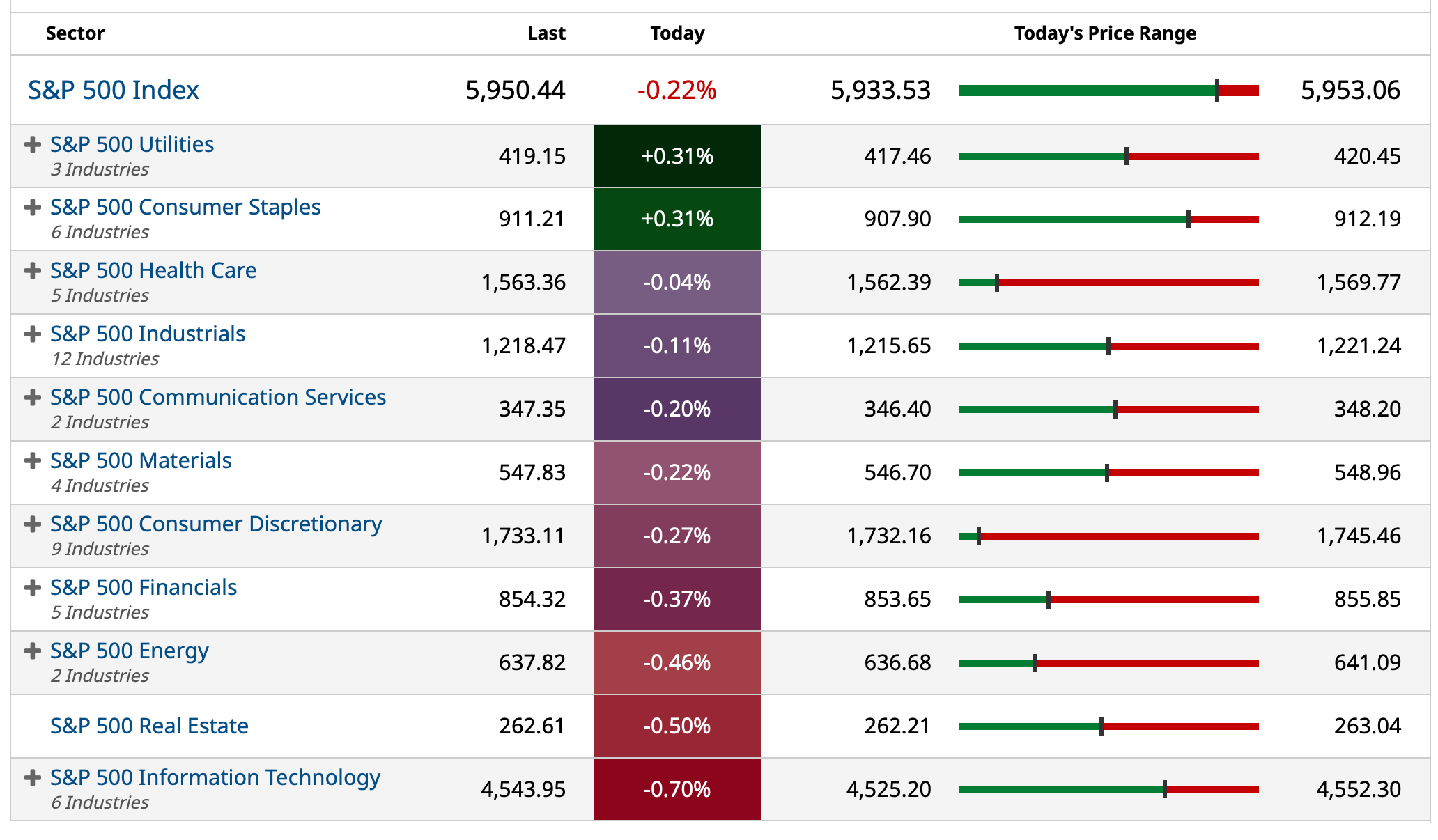

S&P 500 Sectors

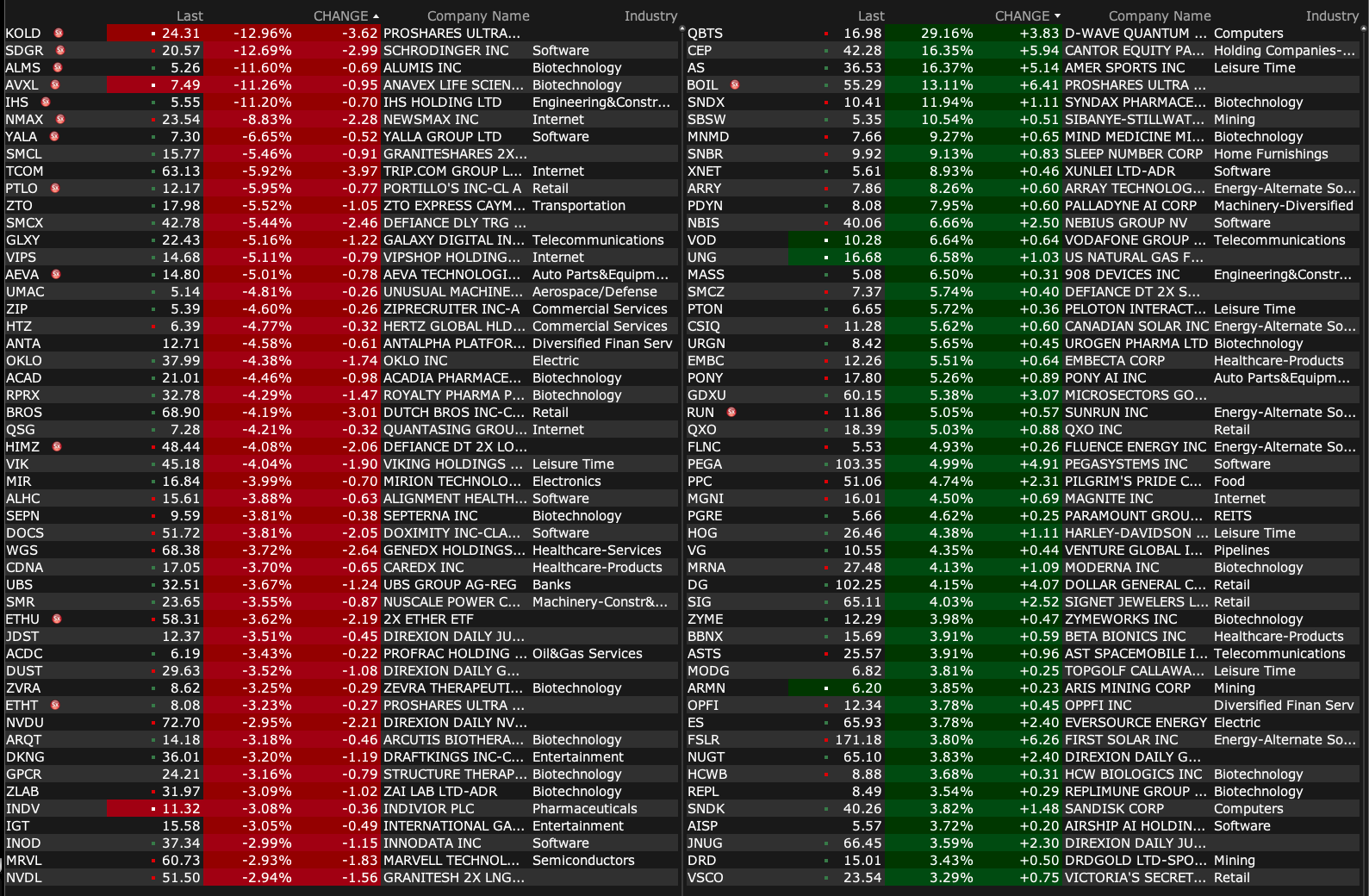

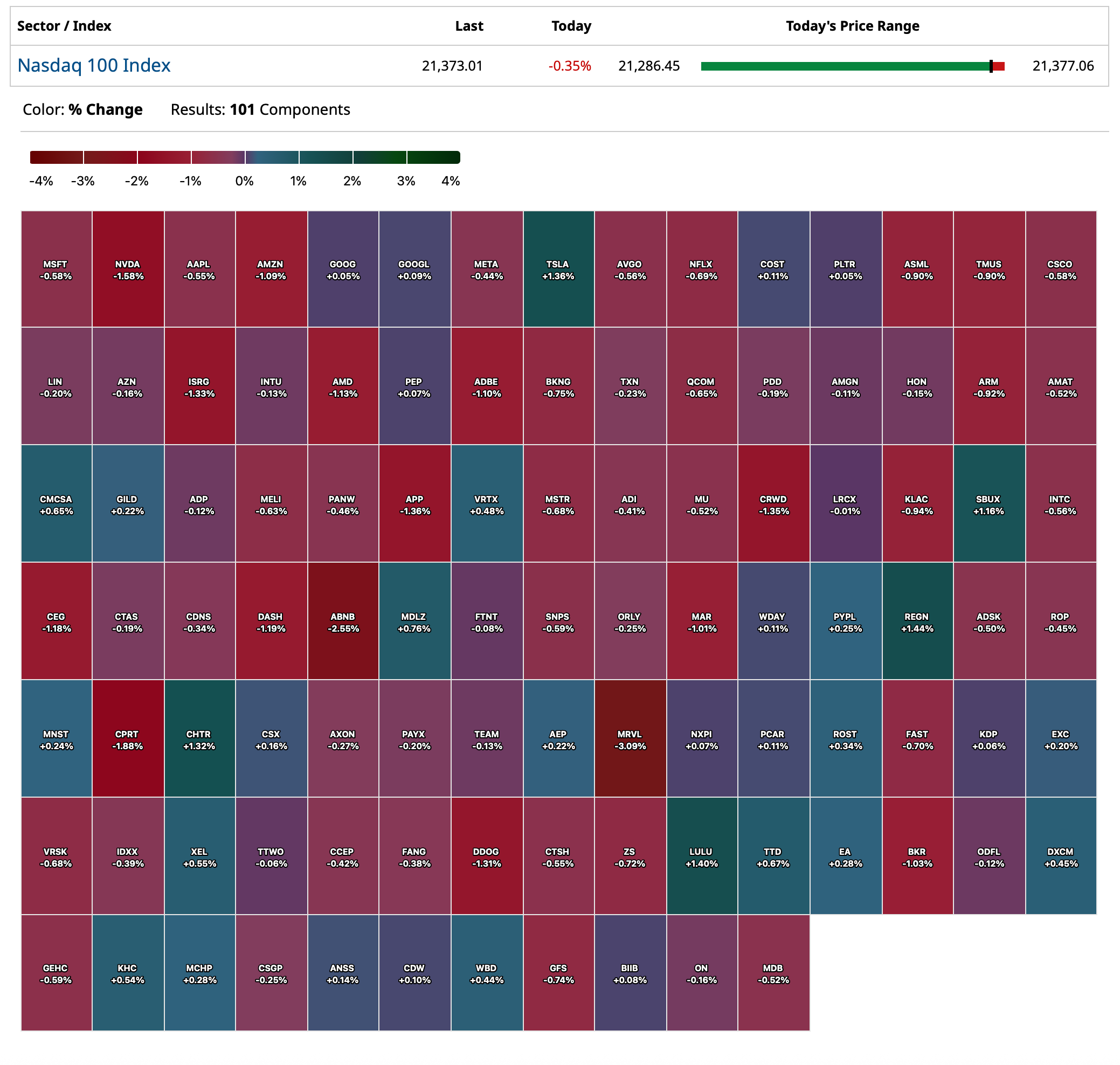

Nasdaq 100 Heat Map

BY Doug Kass · May 20, 2025, 4:16 PM EDT

BY Doug Kass · May 20, 2025, 4:16 PM EDT

BY Doug Kass · May 20, 2025, 3:25 PM EDT

Housekeeping item.

This morning I shorted Home Depot HD at about $387 — just covered at $375.50.

BY Doug Kass · May 20, 2025, 3:04 PM EDT

With S&P cash -43 handles I have taken in this morning's index shorts for a profit:

* SPY $590,94

* QQQ $518.06

From earlier this morning:

Adding to index shorts:

* (SPY) $594.25

* (QQQ) $521.03

Position: Short SPY (M), QQQ (M)

By Doug Kass May 20, 2025 7:55 AM EDT

BY Doug Kass · May 20, 2025, 2:51 PM EDT

* I am genuinely appreciative for subs taking the time to comment on this morning's opening missive.

LifeLongLearner

DK, My sincere gratitude on sharing your wisdom with us. Enjoyed every word of your brilliant essay on American Exceptionalism. Infact I am going to copy it in my personal journal.(if the editors are ok with it)

Your analysis doesn’t merely track economic symptoms; it diagnoses the disease.

Few market voices possess the clarity, conviction, and intellectual courage to cut through the prevailing noise. You with remarkable wisdom and foresight, has articulated not just a market outlook — but a deeper structural reckoning with the illusion of perpetual prosperity.

The rally in equities may indeed be a “last hurrah.” But what follows need not be financial nihilism — it could instead be a redistribution of trust: away from centralized systems and toward sovereign, trust-minimized assets. ( as Master Jedi always says that since BTC is getting decoupled from equity markets - perhaps that’s the answer for a decentralized asset that is immune to fiscal recklessness).

Many Thanks

douglas cassel

Great opener, why we pay to be here.

No real objections to your conclusions.

My questions mainly revolve around where do we go from here?

Myself, and others, are prone to making generalized vague predictions about the fall of empires etc, but the realities of major changes are much more granular. Watching history happen day to day is much like the second hand of the clock. It is where the movement is, but doesn't tell you the time.

Will the USA's loss of exceptionality be gradual and piecemeal, like Englands, or marked by upheaval and violence?

Could AI, quantum computing and other technologies delay the process, or more importantly change the parameters, and remake the world in a significant way?

Is China the inevitable victor, or will their own myriad problems stymie their ascent?

Even in falling economies, some sectors and companies do well. How do we ferret them out?

Do we all have to become short sellers? What about crypto?

Many many questions.

BY Doug Kass · May 20, 2025, 2:33 PM EDT

BY Doug Kass · May 20, 2025, 2:10 PM EDT

Shorted more IWM at $209.69.

BY Doug Kass · May 20, 2025, 2:00 PM EDT

I added to shorts: GRNY, HD and ARKK.

BY Doug Kass · May 20, 2025, 1:55 PM EDT

Wednesday May 21

BY Doug Kass · May 20, 2025, 1:45 PM EDT

No trades since early in the morning.

BY Doug Kass · May 20, 2025, 12:57 PM EDT

- NYSE volume 11% below its one-month average

- NASDAQ volume flat to the one-month average

- VIX index: up 0.88% to 18.

BY Doug Kass · May 20, 2025, 11:27 AM EDT

- The Home Depot will become the only home improvement big box retailer to offer Kill’s branded primer products

- The higher interest rate environment continues to pressure larger remodeling projects.

- Inflation from core commodity categories positively impacted our average ticket by approximately 30 basis points driven by inflation in lumber and copper.

- The worst concerns have passed as stock markets recover and recession expectations decline

- We anticipate that twelve months from now no single country outside of the United States will represent more than 10% of our purchases

- Big ticket comp transactions for those over $1,000 were positive 0.3% compared to the first quarter of last year.

U.S. comps were –3.3% in February, +1.3% in March and +1.8% in April; We expect total sales growth to outpace sales comp with sales growth of approximately 2.8% and comp sales growth of approximately positive 1% compared to fiscal twenty twenty four

BY Doug Kass · May 20, 2025, 10:49 AM EDT

* Political and geopolitical polarization and competition will probably translate into less political centrism and a reduced concern for deficits - creating structural uncertainties, limited fiscal discipline and imprudence around the globe ... and for the possibility of bond markets to "disanchor"

* The cracks in the foundation of the Bull Market are multiple and are deepening, but they are being ignored (as market structure changes have led to price momentum (FOMO) being favored over value and common sense)

* With the S&P 500 Index at 5965, the downside risk dwarfs the upside reward for equities - in a ratio of about 3-1 (negative)

* Valuations and (consensus) expectations for economic and corporate profit growth are all inflated

* Being dismissed are JPMorgan CEO Jamie Dimon's dour comments on complacency and his view that the corporate credit market is "ridiculously over-stretched" (hat tip Rosie)

* Look for the soft data to move into (and weaken) the hard data led by a slowing housing market likely to provide ample near-term evidence of the exposure and vulnerability of the middle class

* Below trend-line economic growth with sticky inflation lie ahead ("slugflation") - uncomfortable for a Federal Reserve which has to make increasingly more difficult decisions

"In investing, there are no called strikes. People can throw any stock at me and I don't have to swing - and nobody is going to call me out on called strikes... It's an enormously advantageous game."

- Warren Buffett

What follows is a compilation of my recent commentary in my Daily Diary on TheStreet Pro and comments recently delivered to my investors at my hedge fund, Seabreeze Partners:

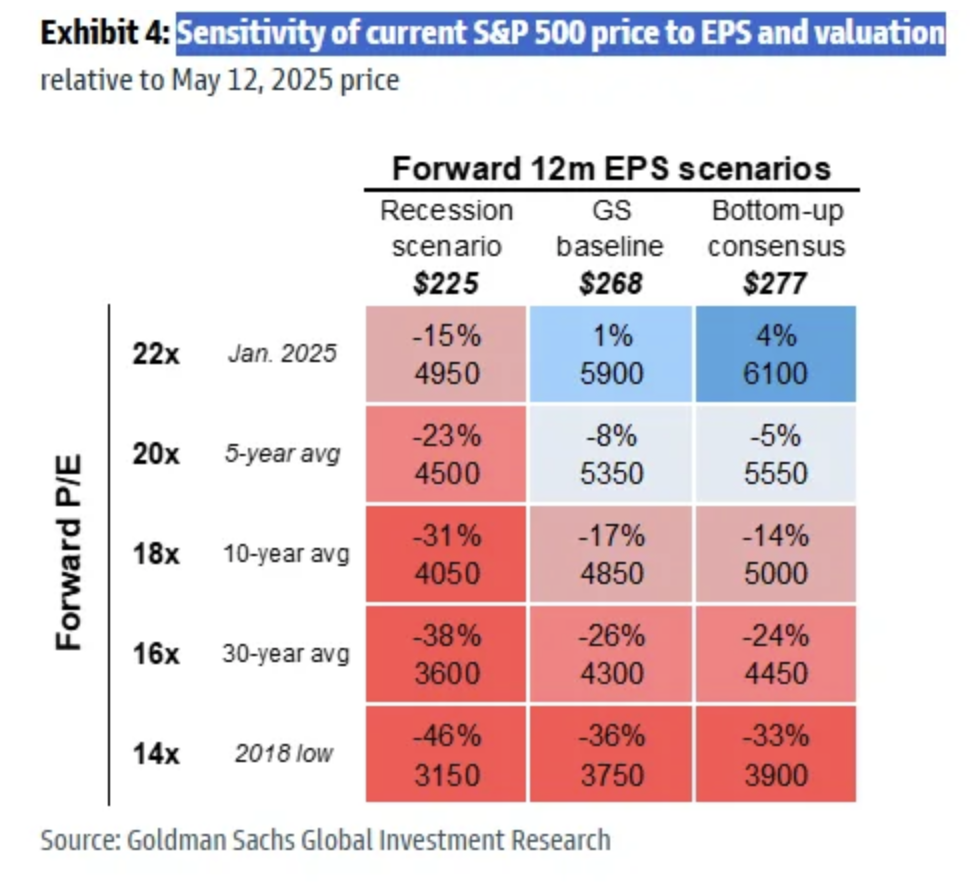

At the core of my ursine market view is that consensus profit expectations are too high. I remain defensively positioned in the belief that consensus S&P 2025-2026 earnings per share expectations of $270/share are too ambitious (and likely to fall closer to $250/share).

The S&P 500 Index currently stands at about 5965. Here is a reasonable sensitivity matrix of S&P profit, valuation and price expectations; it identifies the degree of risk to stock prices should, as we expect, corporate profits disappoint and price earnings multiple decline:

There are numerous potential and deepening cracks in the foundation of economic and profit growth - setting the stage for an unattractive upside reward v downside risk for the U.S. stock market over the remainder of the year. (We believe there is about 3x more downside than upside today.)

Most importantly, as we will briefly discuss this morning, the excess stock market valuations (greater than 21-times), partly associated with the acceptance of the notion of American Exceptionalism, is likely to unwind as U.S. dominance is increasingly questioned by other countries.

As in the 1947 play, A Streetcar Named Desire, the U.S. has begun to resemble Blanche DuBois, the aging Southern belle who lives in a perpetual panic about her fading beauty and concerns about how others perceive her looks -- "relying on the kindness of strangers" to fund our twin deficits.

In the case of the U.S., those strangers (other countries) are investing in their own undervalued equity markets, stimulating their home economies and bringing their savings home.

If this continues (and we believe it will) the centerpieces of globalization -- a strong U.S. dollar and highly valued U.S. equities and Treasuries -- will continue to suffer in a regime change.

Moreover, current price earnings multiples demand near perfection of economic and profit outcomes. Unfortunately, there has rarely been so many possible outcomes (many of them adverse) as there exists today.

As in late 2021, there are numerous fundamental concerns that immediately confront investors today (and are being ignored):

It is our continued expectation that interest rates (and inflation) will likely stay high and valuations are back to being inflated (after the recent market rally).

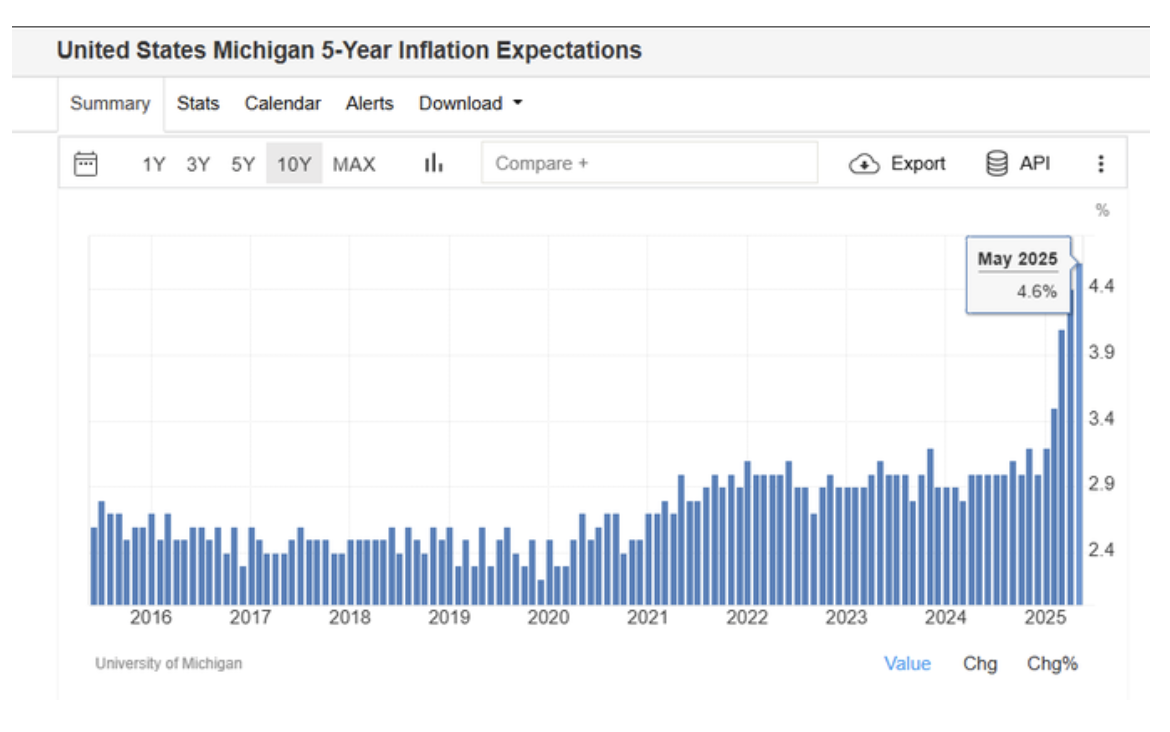

Inflation expectations are climbing:

Recent proposals point to even greater federal budget deficits than are currently in place.

- Barrons

The failure of either party to address federal budget deficits (more on this later in our commentary) is giving the bond market, charged with funding those deficits, a darkening mood.

The yield on the 10-year benchmark Treasury note has risen by 30-basis points recently (to 4.50%) while the 30-year long bond yield has climbed by 40-basis points (to 5.00%) -- levels that provide equity -- like returns with little risk and volatility.

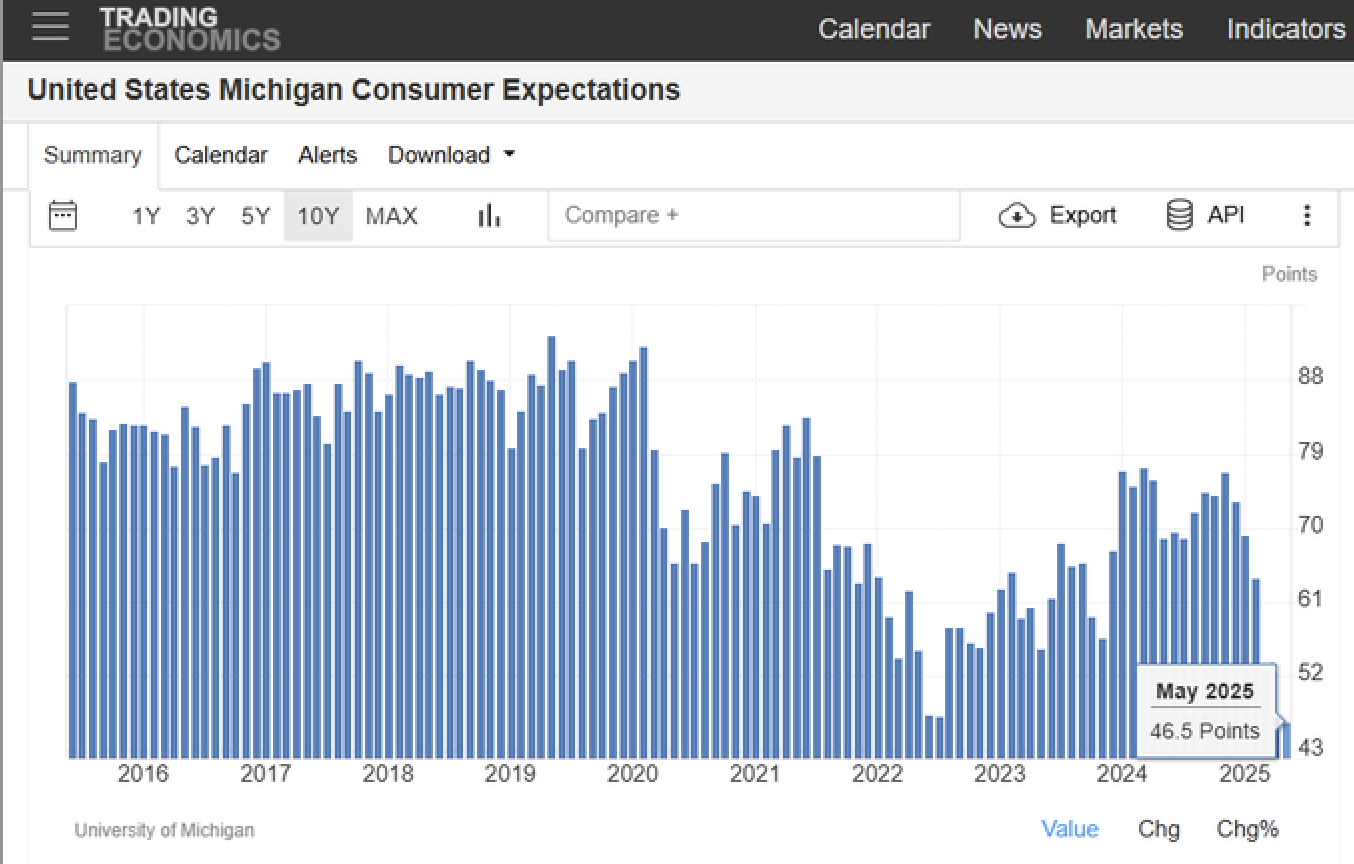

This climb in interest rates is occurring even as consumer sentiment is eroding:

"You can ignore reality, but you cannot ignore the consequences of ignoring reality."

- Ayn Rand

In this morning's missive we will begin to look longer term and consider the consequences of the economic and profit cycle, the turn away from globalism and towards reshoring (and its deleterious impact on profit margins) and other factors - that could result (much like the Pharaoh's prophecy) of substandard stock market returns over the next few years:

"In the Bible, 'lean years' refer to a period of famine that follows a time of abundance, particularly in the story of Joseph in Genesis 41. The prophecy, revealed through dreams to Pharaoh, foretold seven years of great plenty in Egypt, followed by seven years of severe famine. Joseph, interpreting the dream, advised Pharaoh to prepare for the lean years by storing grain during the period of abundance. This preparation allowed Egypt to survive the famine while other surrounding lands suffered greatly."

The post Cold War era of endless credit, inexpensive labor, military neglect, product (supply) reliance on our political adversaries, energy dependence, unchecked migration, and the illusion of high margins was never unsustainable - it was always brittle.

The illusion of prosperity was elongated with the $5 trillion Covid stimulus packages and a $20 trillion rise in our country's debt load. Wall Street and our capital markets thrived (with only one or two temporary pauses) even though Main Street suffered from stagnating real wage growth - the disconnect and schism between headline prosperity and lived experience grew ever wider.

But, all the while, reality was catching up as the foundation was cracking.

It was the system that aged and inevitably buckled under its own contradictions.

Change, especially of the political-kind that we are see today, was inevitable.

The recalibration or realignment that we are likely to begin witnessing may be violent or gradual - the course is currently uncertain - but is bound to be messy and has only started.

To us, the likely adverse impact of valuations seems more certain.

The subject is broad and spending a couple of thousand words expressing my views doesn't do justice to the topic.

Let's call this... Rethinking American Exceptionalism.

We all recognize that the America's Exceptionalism and our country's safe haven status will likely continue. Our "system" is superior and the most trusted in the world -- whether ranked economically or legally.

Nonetheless, we are concerned, at the margin, that our Exceptionalism is "less so" - and, as such, will likely hurt stock market valuations. result in equity diversification away from the U.S. and lead to further increases in domestic interest rates.

Let's very briefly summarize the major foundational cracks:

* The Reversal of Globalization Will Become An Expensive Truth For Corporations and Consumers: Tariffs proposed are leading to ever higher inflation and lower S&P profits. As to the tariff "pause," investors appear to be convinced that a 30% tariff rate on China and a 13% average tariff rate on the world (compared to 2.5% in 2025) are both normal and manageable. (Nothing like a 10-percentage point levy on this $30 trillion beast called "Global Trade.") This will lead to higher inflation over the balance of the year, serve as a consumption tax on the U.S. consumer and lead, according to Strategas' David Clifton, a one percent reduction in GDP.

* Our Trade Deficit and Debt Load Is Not Being Addressed By Either Political Party: The Administration's Department of Government Efficiency (DOGE) effort has failed to save taxpayers much and the Democrats are unwilling to approach our deficit and borrowings in a serious manner. We are of the view that our country's pristine debt rating could be subject to downgrades in the months ahead.

It can be now argued that U.S. debt growth is unsustainable. Already non-U.S. investors are avoiding our debt. This may create a demand shock as other countries begin to disinvest from our Treasuries. Yields will likely rise, which will trigger inflation because the Treasury will have to print more money - causing a death spiral of debt.

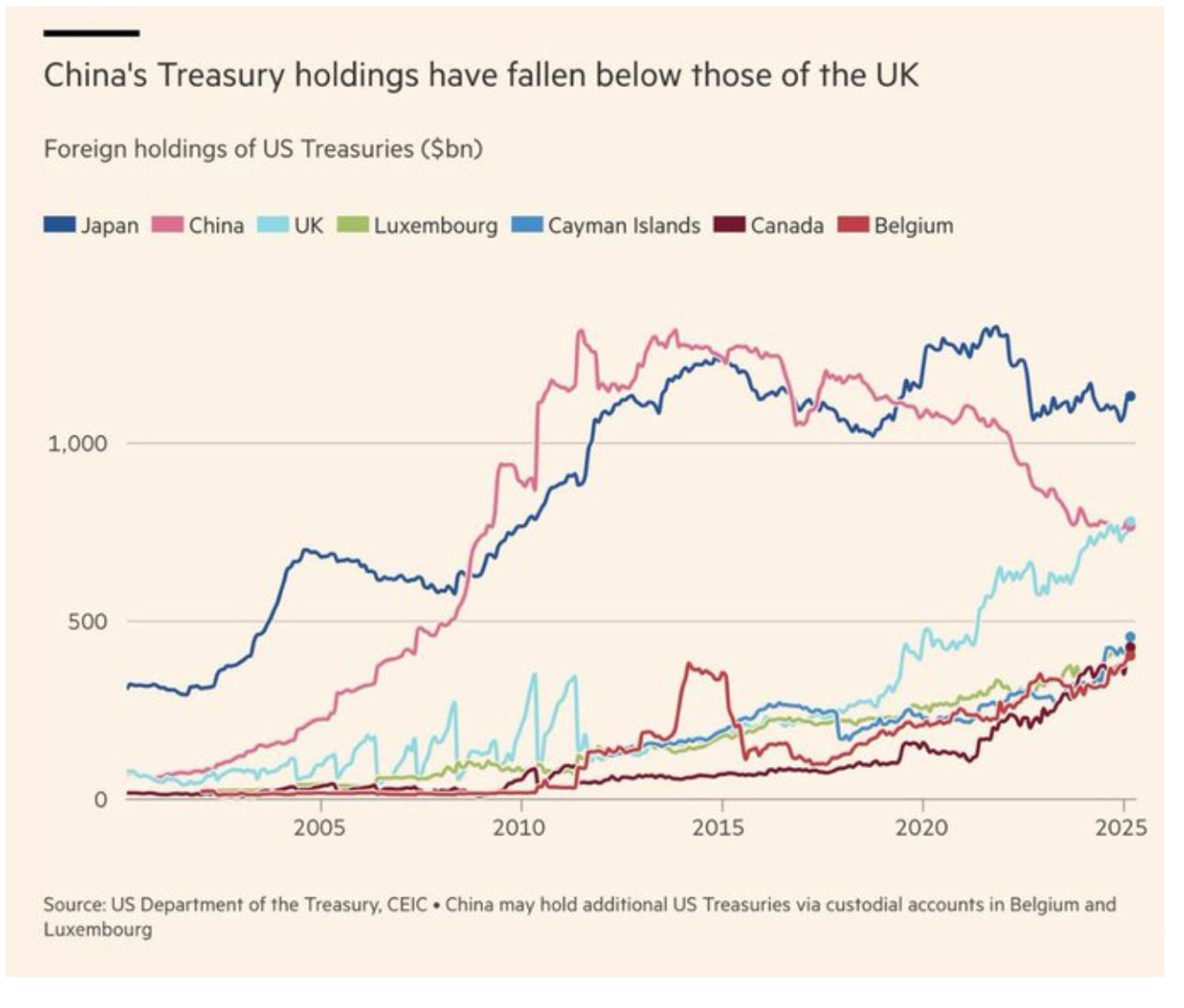

The largest holders of our debt (Japan and China) are liquidating our Treasuries at a rapid rate. The U.K. is picking up the slack but, as previously noted, this is not keeping U.S. interest rates from rising - the long bond is at the highest yield in 18 years:

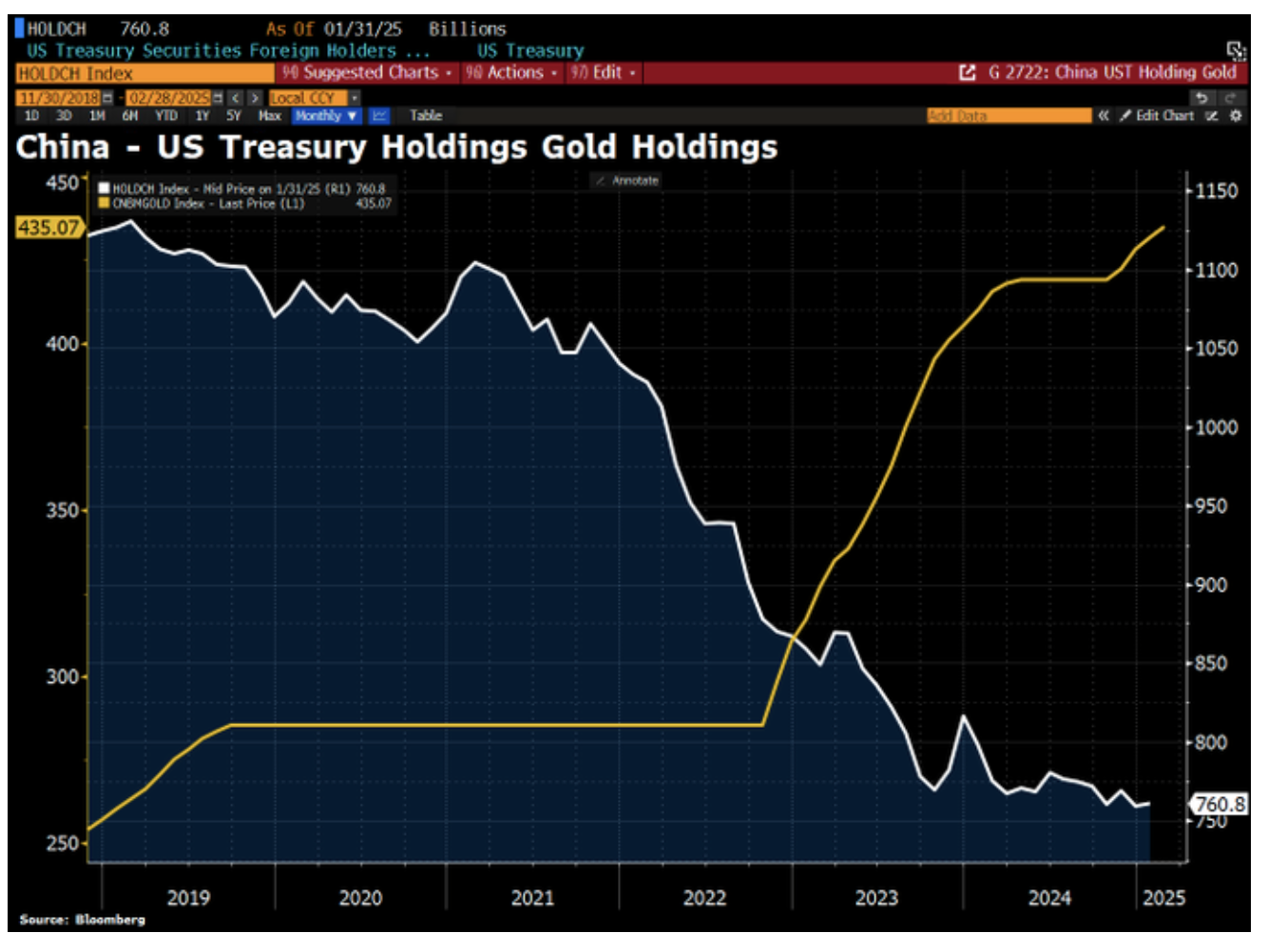

In place of U.S. Treasury holdings, China is buying gold:

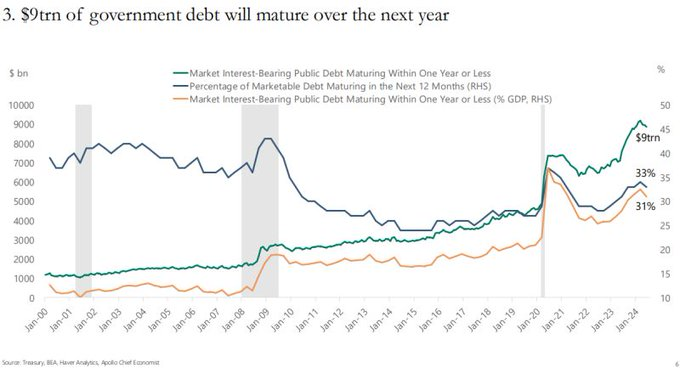

At a time in which the U.S. needs to refinance $9 trillion of debt in the next twelve months - interest rates are climbing and the Fed is quantitatively tightening:

There are only two ways to sell so much debt:

* With higher yields.

* Or the Fed steps in and buys the debt.

Both outcomes are inflationary.

Knowing this, investors will likely demand higher yields - leading to more adverse rate and economic outcomes:

Seeing the U.S. dollar as an inflationary asset, other countries could accelerate the sale of our debt, raising the risk that the dollar will no longer be seen as the reserve currency of the world. This possible condition is what Bridgewater's Ray Dalio describes as the "breakdown of the global monetary order."

At the same time, the self-induced tariff "crisis" is being manifested in continuing inflationary pressures, making it difficult for interest rates to drop, reinforcing the debt problem and likely producing "slugflation" (sluggish economic growth/persistent inflation).

“I'm not terribly affected by the fact that the crowds are agreeing with me or disagreeing with me. I'll do whatever my own sense tells me. The trick is simply to sit and think.”

- Warren Buffett

To paraphrase Winston Churchill, the rally of the past few weeks does not likely represent the end of the market's decline. It is more likely that we are facing the beginning of a broader market decline (that initially began in January, 2025). Our baseline expectation for a negative return for the S&P 500 Index in 2025 remains unaltered. Equities likely peaked (for the year) in January and large cap technology stocks (The Mag7) may have reached a seminal top three months ago (much like The Nifty Fifty topped in January, 1973). We see some potentially serious cracks in the foundation of economic and corporate profit growth - and in global economic cooperation:

* Higher Debt = Higher Interest Rate Burden

* The Fed Is Trapped Between Inflation and Insolvency

* Dollar Reserve Status is Eroding

Political and geopolitical polarization and competition will probably translate into less political centrism and a reduced concern for deficits- creating structural uncertainties, limited fiscal discipline and imprudence around the globe ... and for the possibility of bond markets to "disanchor."

U.S. debt, in particular, will likely weigh on future S&P investment returns.

This is not the end of the U.S. safe haven status nor does this imply a systemic collapse.

But it is likely end of the free (macro) lunch.

BY Doug Kass · May 20, 2025, 9:52 AM EDT

Doug Kass

STAFF

TLT drop problematic, adding to shorts.

BY Doug Kass · May 20, 2025, 9:47 AM EDT

Most active premarket ETFs as of 8:19 a.m. ET:

BY Doug Kass · May 20, 2025, 9:19 AM EDT

Premarket percentage movers at 8:37 a.m. ET:

BY Doug Kass · May 20, 2025, 9:09 AM EDT

-NRXS +172% (US FDA clears IB-Stim for treating functional dyspepsia-related pain and nausea in youth aged 8–21)

-QBTS +17% (announces general availability of its Advantage2 quantum computing system)

-AS +9.9% (earnings, guidance)

-BULL +8.3% (momentum)

-PEGA +6.7% (to replace Nordstorm in S&P MidCap 400 Index, effective May 22nd)

-GDS +6.0% (earnings, guidance)

-IBRX +5.4% (Piper/Sandler Raised IBRX to Overweight from Neutral, price target: $5 from $4.25)

-PONY +5.3% (earnings)

-BILI +3.6% (earnings)

-VSCO +3.0% (adopts rights plan to block control by BBRC)

-UNH +2.7% (momentum)

-HD +2.1% (earnings, guidance)

-VIPS -8.9% (earnings, guidance)

-YALA -8.0% (earnings, guidance)

-TCOM -4.8% (earnings)

-RMD -4.1% (rival Apnimed posts positive clinical trial results for sleep apnea therapy)

-TRML -3.8% (announces topline results from the Ongoing Phase 2 TRANQUILITY Trial Evaluating Pacibekitug in Patients with Elevated High-Sensitivity C-reactive Protein and Chronic Kidney Disease)

-MDB -2.1% (Loop Capital Cuts MDB to Hold from Buy, price target: $190)

BY Doug Kass · May 20, 2025, 8:59 AM EDT

8:00 a.m. ET: Fed Treasury Repo Reference Rate;

8:30: Philly Fed Non-Manufacturing Activity (May);

8:55: Johnson Redbook Retail Sales Reports (w/e 5/17);

11:00: Treasury Announces a 4 and 8 Week Bill Auction; 11:00AM: Treasury's Buyback Announcement (Liquidity Support); 11:30AM: Treasury hosts a $70B 6-Week Bill Auction

9:00 a.m. : Fed Bank of Atlanta President Bostic (Non-Voter) gives welcome back remarks before the 2025 Financial Markets Conference - "Financial Intermediation In Transition: How Will Policy Adapt?" hosted by the Federal Reserve Bank of Atlanta, Fernandina Beach, FL (Livestream available);

9:00: Fed Bank of Richmond President Barkin (Non-Voter) gives opening remarks before the "Elevating What Works" 2025 Investing in Rural America Conference hosted by the Federal Reserve Bank of Richmond, Roanoke, VA (Other details TBA);

9:30: Fed Bank of Boston posts remarks of President Susan Collins (Voter) before a closed "Fed Listens" event in Keene, New Hampshire (Text available at bostonfed.org.);

1:00 p.m.: Fed Bank of St. Louis President Musalem (Voter) speaks on the U.S. economy and monetary policy in a moderated conversation before the Economic Club of Minnesota, Minneapolis, MN (Livestream and in-person options available. Audience Q&A expected. Text anticipated. No media availability);

5:00: Fed Board Governor Kugler (Voter) gives commencement address before the Spring 2025 Berkeley Economics Commencement Ceremony (Text available. No Q&A.Livestream at https://www.youtube.com/live/ndqAg-M3Sqw)

7:00: Fed Bank of San Francisco President Daly (Non-Voter) and Federal Reserve Bank of Cleveland President Beth Hammack (Non-Voter) give keynotes, and Fed Bank of Atlanta President Bostic (Non-Voter) moderates a discussion before the 2025 Financial Markets Conference - "Financial Intermediation In Transition: How Will Policy Adapt?" hosted by the Federal Reserve Bank of Atlanta, Fernandina Beach, FL (Audience Q&A expected. Click for livestream.

BY Doug Kass · May 20, 2025, 8:47 AM EDT

From Peter Boockvar:

Nice rebound in Treasuries yesterday so let's draw a technical line in the sand at about 4.55% in the 10 yr yield and 5% in the 30 yr yield. Lines though have been crossed in the very long end of the Japanese JGB market as the 40 yr yield leaped higher by 12 bps to 3.59% and that is a fresh record high for this security since it was introduced in 2008. I've said before, I like looking at the 40 yr yield in Japan because it is the least manipulated by an overnight rate of just .50%. The 30 yr JGB yield was higher by almost 13 bps to 3.11%. That's the 2nd highest close since 1999 when it was first issued and the 20 yr yield was up by 12 bps to 2.54%.

The catalyst overnight in Japan was a weak 20 yr auction where the bid to cover fell to the least since August 2012 at 2.50 vs 2.96 in the prior auction. The tail of 1.14 is the most since 1987.

Remember too that the BoJ continues to reduce the size of asset purchases. By the way, the 10 yr yield was higher too but just a touch and by 4 bps over the past two days to 1.51% so this move was really on the very longer end of the Japanese curve.

We are not out of the global bond woods as duration can hurt and countries with excessive debt with no plans to control it are being watched more closely by the global bond police. The Nikkei was little changed overnight while the yen is slightly higher.

On the flip side with respect to global bond yields, Australia's government bonds (AGBs) rallied sharply as while the RBA cut rates by 25 bps as expected to 3.85%, Governor Michele Bullock in her press conference said they considered cutting by 50 bps. She is a hawk so this was a surprise. She said "There was a bit of discussion about hold and that was sort of put aside pretty quickly. The discussion then was about 50 and 25. The board was of the view that 25 was the right number on this occasion."

Also, "To the extent that we think there's still restrictiveness in monetary policy, and we think there is a bit, then that would give us opportunities to lower the interest rate further." In response, the 2 yr yield plunged by 16 bps and the 10 yr by 12 bps. The Aussie$ is lower too vs the US dollar.

With a debt to GDP ratio of just 44%, the Australian bond market is not the neighborhood where the bond police are patrolling to the extent they are elsewhere.

40 yr JGB Yield

Australian 10 yr yield

NY Fed president John Williams, Governor Philip Jefferson and Atlanta president Raphael Bostic all sounded yesterday in no rush to cut rates. Williams said "It's not going to be that in June we're going to understand what's happening here, or in July. It's going to be a process of collecting data, getting a better picture, and watching things as they develop."

Jefferson said "Given the level of uncertainty that we're facing right now, I believe that it is appropriate that we wait and see how the policies evolve over time and their impact." On prices, "I believe it's important that monetary policy make sure that any increase in the price level is not converted into a sustained increase in inflation."

Bostic said "Given the trajectory of our two mandates, our two charges, I worry a lot about the inflation side, and mainly because we're seeing expectations move in a troublesome way."

A rate cut by July is now down to just 36% but the fed funds futures market is still pricing in fully 50 bps of cuts by year end.

The May Banking Conditions Survey was released yesterday by the Dallas Fed and here was the summary:

"Loan volume grew slightly while loan demand was unchanged in May. Credit tightening continued, but loan pricing declined. Loan nonperformance decelerated sharply, increasing at the slowest pace since the end of 2022. Nevertheless, bankers reported a continued contraction in general business activity. Bankers are less optimistic about the outlook. On net, survey respondents still expect an improvement in loan demand and business activity six months from now, but that sentiment is less broad based than in previous months, and loan nonperformance is expected to increase."

The data was collected between May 6 and 14 so it does capture a few days after the China trade truce.

Here were comments from some bankers that answered the survey and it was littered with the word 'uncertainty'

Home Depot missed bottom line estimates and comps but beat the top line and reaffirmed full year guidance so the stock is popping about 3% pre-market. In the press release they said "Our first quarter results were in line with our expectations as we saw continued customer engagement across smaller projects and in our spring events." The CFO told CNBC ahead of its conference call, "Because of our scale, the great partnerships we have with our suppliers and productivity that we continue to drive in our business, we intend to generally maintain our current pricing levels across our portfolio." He said more than half of what they sell is sourced within the US and for the balance, they have diversified their supply chains where 'no single country outside of the US will represent more than 10% of the company's purchases' according to the article.

Walmart in contrast has a bigger reliance on China for its products and much lower profit margins than Home Depot. In 2024, Home Depot's net income margin was 10% vs Walmart's at 3%.

BY Doug Kass · May 20, 2025, 8:22 AM EDT

Adding to index shorts:

* SPY $594.25

* QQQ $521.03

BY Doug Kass · May 20, 2025, 7:55 AM EDT

“There’s an extraordinary amount of complacency. That’s my own view.”

— Jamie Dimon, May 19th

Well, yesterday was much more about the bond market than the equity market as the long bond yield got as high as 5.03% and then closed the day on a reverse trip to 4.91% at the close. The major averages were little changed, and if not for UnitedHealth Group (UNH), the Dow would have been down -10 points instead of being up +137 points. But that was just one stock. And one that says very little about the state of the economy — about which there should be some concern given Jamie Dimon’s dour comments on complacency and the ridiculously over-stretched market for corporate credit. Volume was mixed, falling on the New York Stock Exchange, in a low-conviction market — not discussed on bubblevision, which focuses exclusively on the price. Decliners barely outnumbered advancers on the Nasdaq and came in ahead 5-to-4 on the NYSE.

The mantra out of the likes of Scott Bessent (“lagging indicator”) and Tom Lee (“largely non-event”) ignores the significance of the world’s reserve currency being graded below AAA status by all three major rating agencies — the difference between now and the summer of 2011 is that only one agency had downgraded the U.S. ranking and the Fed was hoovering assets on its balance sheet under Bernanke like there was no tomorrow (more on this below). Not to mention how the stock market freaked out back then but then figured out that the central bank had your back. The Fed does not have your back this time, and the funds rate is +425 basis points higher today than it was back then. Real rates were 0%; today, they are over 2%! Recession fear in 2011 was alive and well; it is nobody’s base-case forecast today.

The Tea Party looked after fiscal policy following the 2010 midterms — there were no ridiculous measures to cut taxes on tips or overtime. Fiscal restraint took over with time. There was no alternative to stocks back then but, come on, today, you can garner a 6% yield on BB-rated bonds, 5.6% on 30-year Ginnie Mae coupons, and 4.8% on short-dated financial paper which look just fine from where we sit. Not to mention 5% on the long bond. You like 4% free cash flow yields on the S&P 500? Knock yourself out. As Herman Melville’s 1853 classic “Bartleby the Scrivener” would put it, “I would prefer not to.” Look it up. It’s a classic refrain about resisting conformity, and totally in vogue for the times we are in today.

BY Doug Kass · May 20, 2025, 7:45 AM EDT

There is nary a naysayer.

The S&P index has advanced six days in a row and is up substantially from early in April.

The S&P Short Range Oscillator is deeper in overbought (at 5.82%).

S&P cash RSI is now at 91.9:

For a fundamental viewpoint on this trade, see my opening missive coming up, Rethinking American Exceptionalism.

BY Doug Kass · May 20, 2025, 7:00 AM EDT

I am adding to my ARKK short at $57.40.

BY Doug Kass · May 20, 2025, 6:50 AM EDT

* Earnings guidance is souring...

The bullish narrative is that S&P profits are "holding in."

This is unlikely, going forward:

BY Doug Kass · May 20, 2025, 6:40 AM EDT

* The prevailing (and defiant view from technicians is.... "good try Moody's!"

Bonus — Here are some great links:

The Market Just Flipped - Did You Catch It?

BY Doug Kass · May 20, 2025, 6:25 AM EDT

BY Doug Kass · May 20, 2025, 6:16 AM EDT

From Charlie!

BY Doug Kass · May 20, 2025, 6:05 AM EDT

Wolf Street howls about the yen carry trade.

The issue and ramifications of rising Japanese inflation and a spike in bond yields were totally unnoticed by the business media and the bullish cabal on Monday.

From Bramo this morning:

From Larry McDonald:

BY Doug Kass · May 20, 2025, 5:55 AM EDT

The S&P Short Range Oscillator moves to further overbought territory — now at 5.82 from 5.36.

BY Doug Kass · May 20, 2025, 5:45 AM EDT