Monday's Closing Market Stats

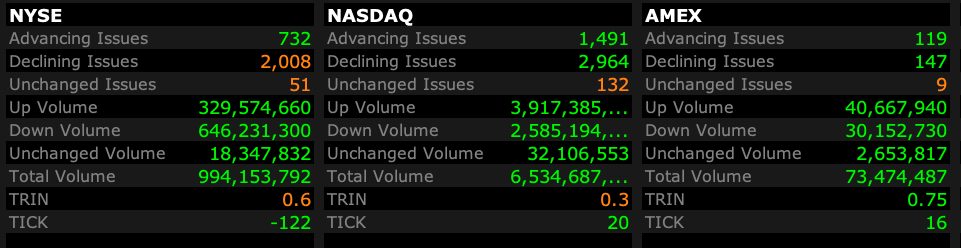

Closing Breadth

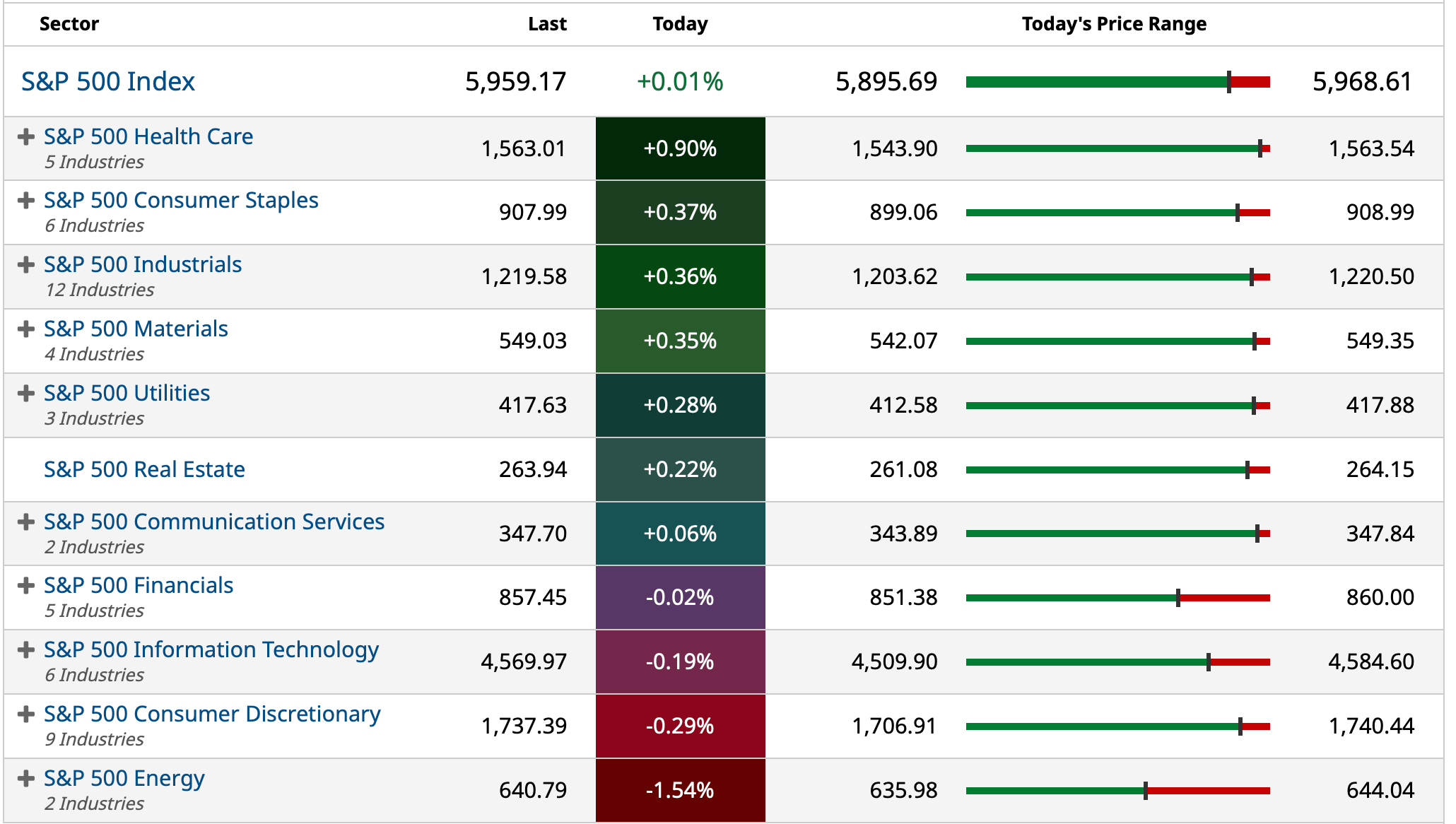

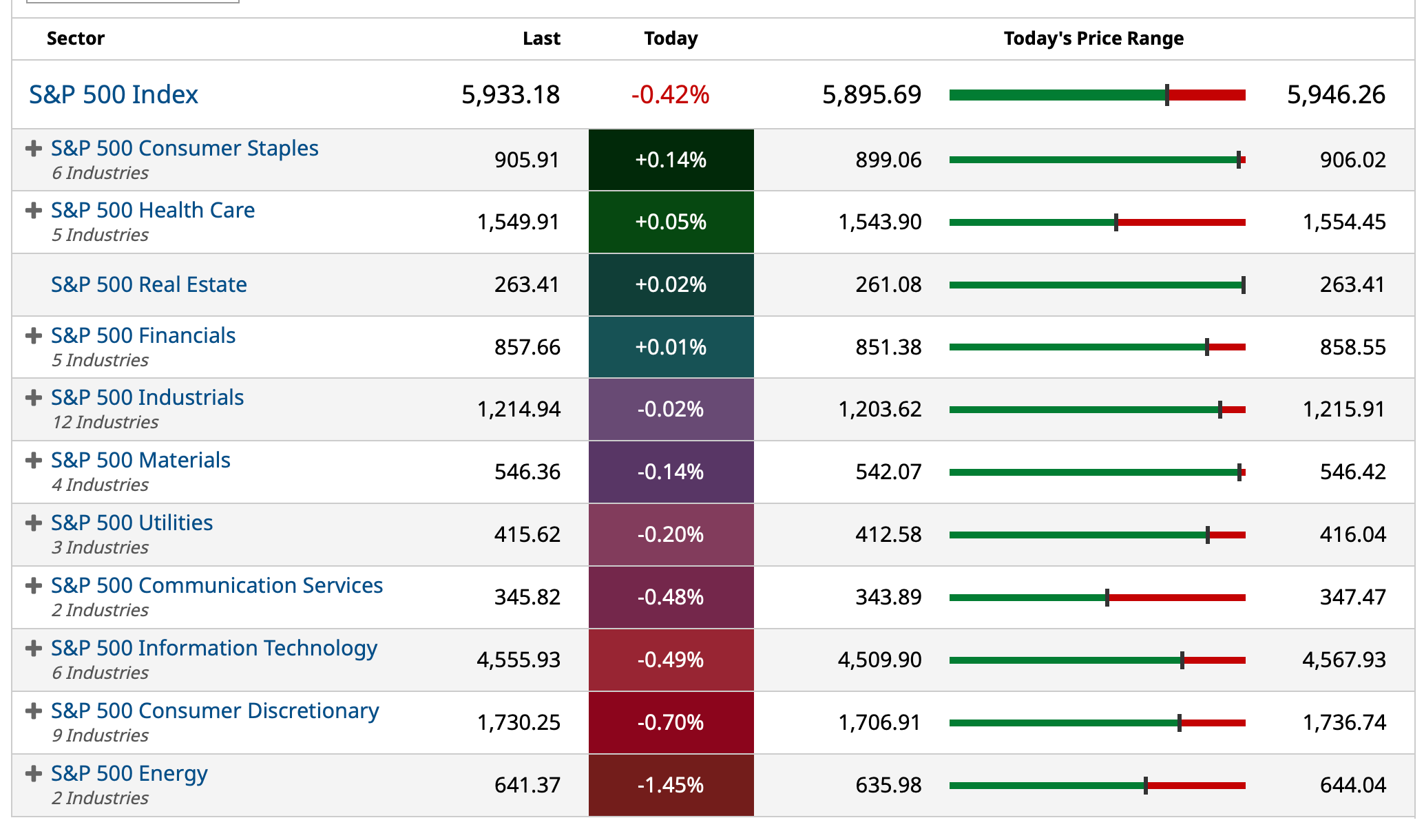

S&P 500 Sectors

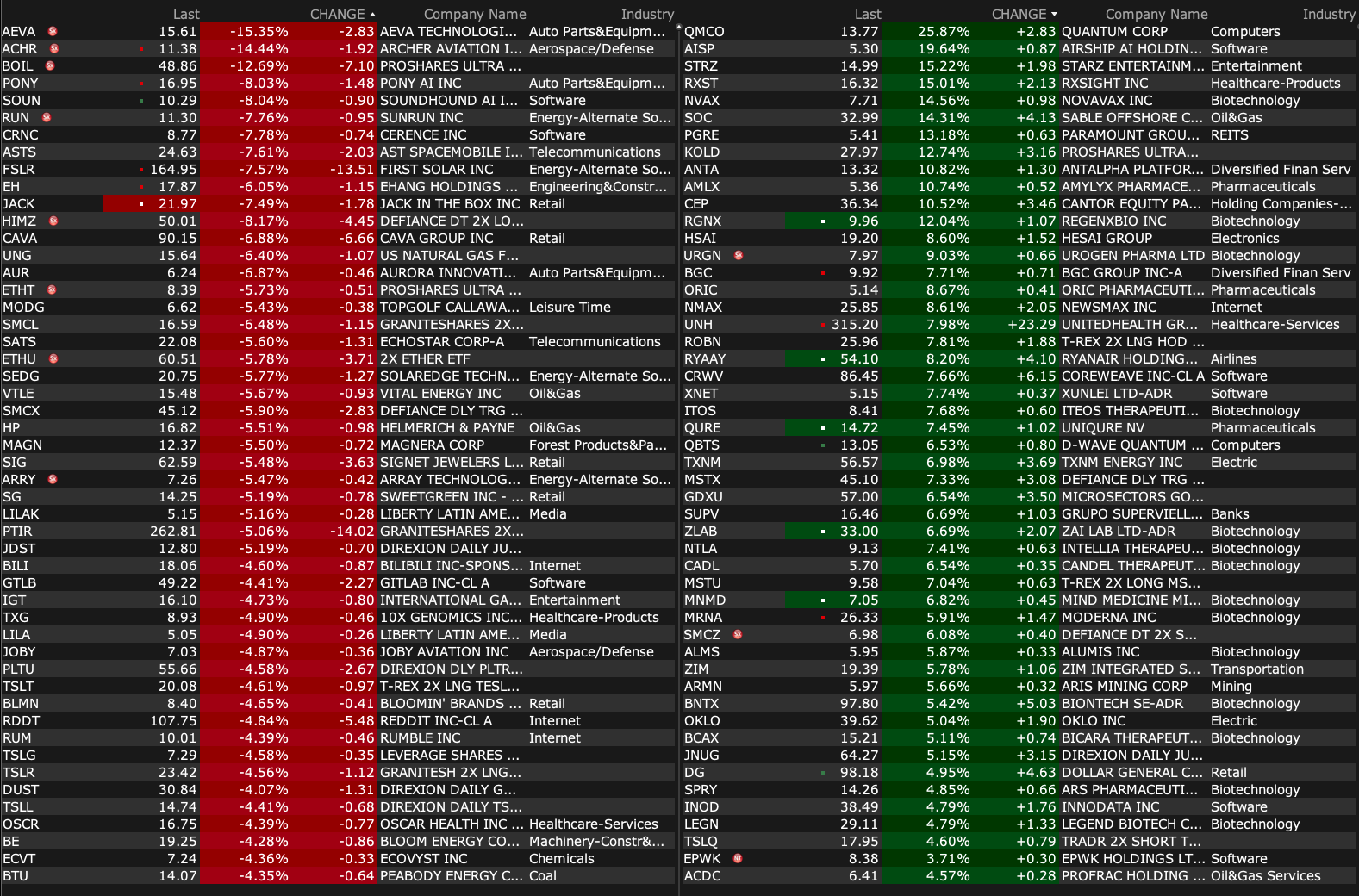

% Movers

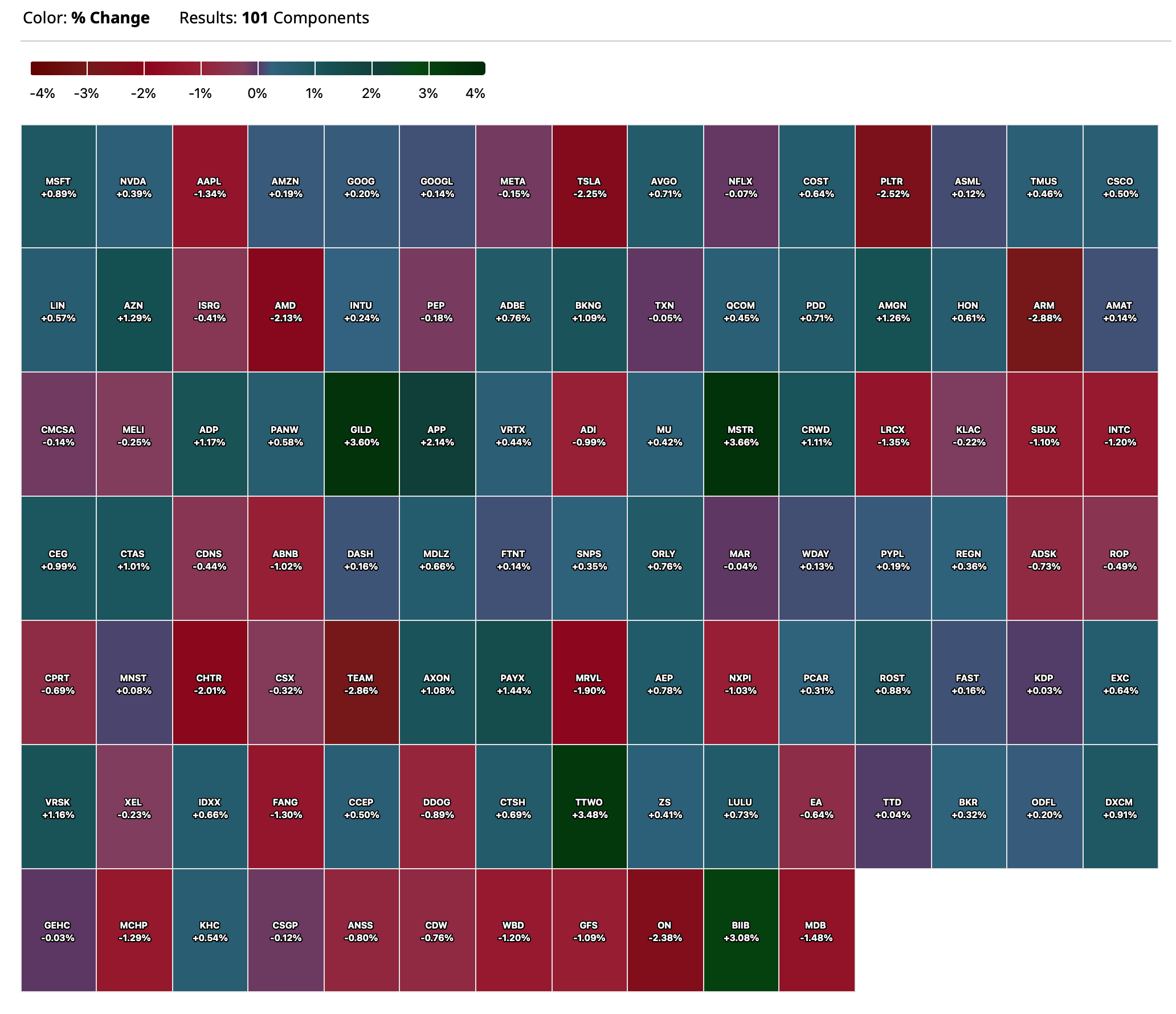

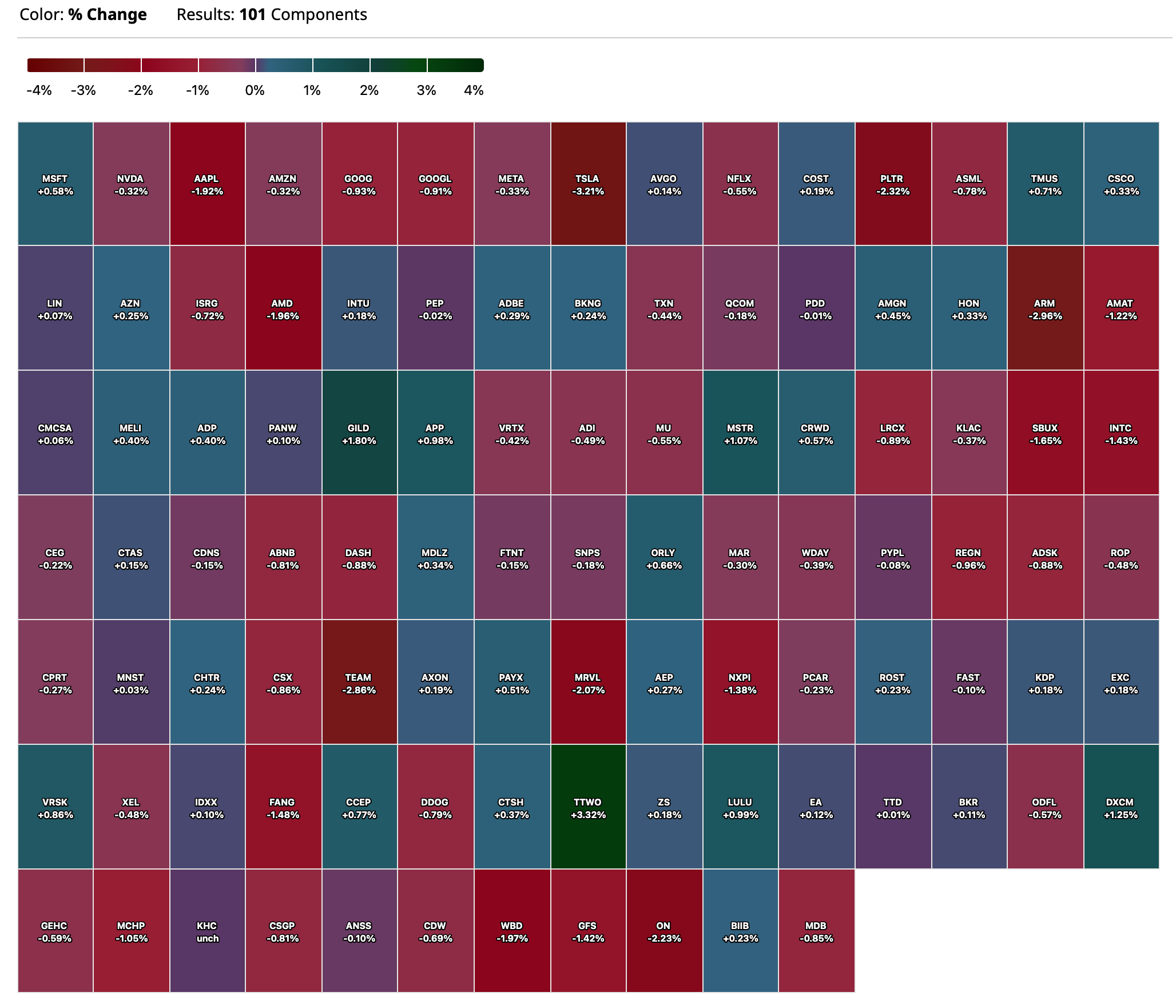

Nasdaq 100 Heat Map

BY Doug Kass · May 19, 2025, 4:14 PM EDT

BY Doug Kass · May 19, 2025, 4:14 PM EDT

I am outta here early as I want to work on tomorrow's opening missive: "Rethinking American Exceptionalism."

Thanks for reading my Diary today.

Enjoy the evening.

Be safe.

BY Doug Kass · May 19, 2025, 3:45 PM EDT

BY Doug Kass · May 19, 2025, 3:33 PM EDT

Adding to NVDA short at $135.38.

BY Doug Kass · May 19, 2025, 3:07 PM EDT

douglas cassel

I was going to post Dailo's tweet, but Doug K beat me to it. His point is one I have been trumpeting here for a few years now. The zero risk associated with US government bonds has some underlying assumptions, including a responsible approach to debt and a reasonably stable currency. Historically and internationally, these assumptions are relatively unusual. The post WW2 and post oil crisis understandings that made the US dollar the world reserve currency are being actively undermined by multiple forces. The markets are realizing that our governing system lacks the incentives to fix the problem, and short of an actual revolution, is unlikely to change.

In relation to the stock market, I think one could easily make a case that many companies have better management, value propositions, and growth prospects than the US as a whole. This is one reason I question the "zero risk" of government bond in relation to stocks or corporate debt. The experience of Wiemar Germany demonstrated that companies can navigate through a period of hyperinflation that destroyed bond investors.

Of course, getting back to BTC, removing the need for reliance on human management is yet another attribute that is mostly neglected. Denominating debt in BTC would certainly remove the inflation problem, although this probably a few years away.

BY Doug Kass · May 19, 2025, 3:00 PM EDT

* SPY $594.39

* QQQ $521.26

BY Doug Kass · May 19, 2025, 2:50 PM EDT

BY Doug Kass · May 19, 2025, 2:21 PM EDT

I have a research meeting from 1:30 p.m. to about 2:30 p.m.

Radio silence.

BY Doug Kass · May 19, 2025, 1:41 PM EDT

I have moved to a medium sized short in the indices.

Latest shorts:

* SPY $593.45

* QQQ $520.22

BY Doug Kass · May 19, 2025, 12:30 PM EDT

- NYSE volume 9% below its one-month average;

- Nasdaq volume 100% above its one-month average;

- VIX index: up 7.48% to 18.53

BY Doug Kass · May 19, 2025, 11:38 AM EDT

BY Doug Kass · May 19, 2025, 11:25 AM EDT

From Peter Boockvar:

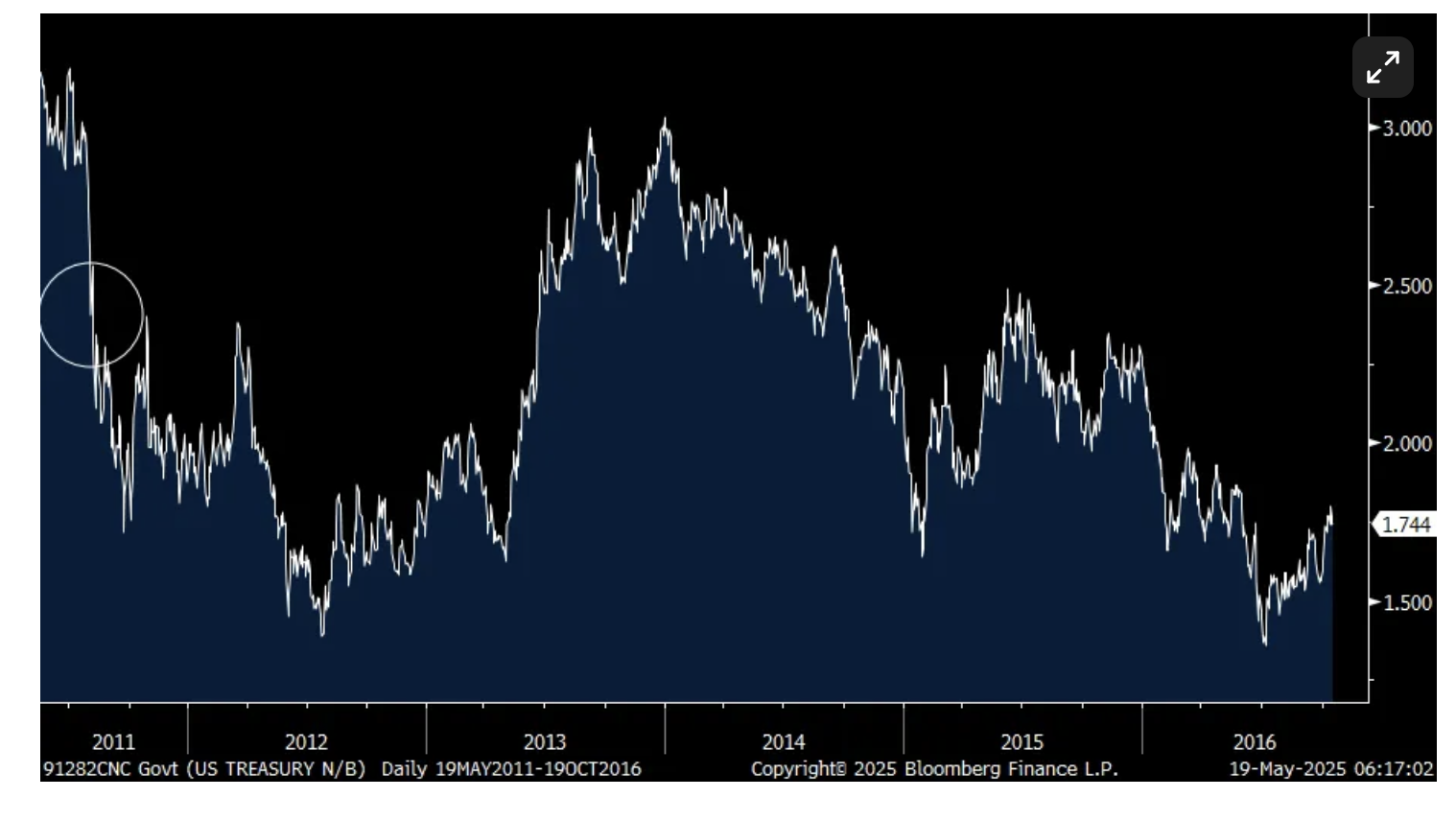

Yea, US debts and deficits now matter and I don't say that because of the Moody's downgrade as S&P did this about 14 years ago in August 2011 and it certainly didn't matter then. I say it because markets clearly care now and have for the past few years. Understand that in June 2011, the Fed had just ended QE2 and rather worry about the credit implications then of a US downgrade a few months later, the Treasury market was more worried about a double dip recession and the 10 yr yield went DOWN in the year following the downgrade. This followed a trend where yields went UP during QE1 and QE2 because of the reflationary belief of policy. Fed rate policy was a real driver then too with zero interest rates (totaling 7 years and didn't get raised until 2015). Now, the long end of the yield curve continues to speak for itself and has been for the last few years and rate cuts have been more tweaks than anything else. Then too in 2011 we were still in a bond bull market. Today, we are three years into the bear, I believe.

On the day after the S&P downgrade, the 10 yr yield response was literally one day. On Friday August 5th, 2011, the 10 yr yield jumped 16 bps to 2.56%. On Monday August 8th though, it plunged by 24 bps to 2.32%. The US dollar index also had a one day blip then. On that Friday it fell .7% to 74.6 and rallied by .25% on that Monday and one month later was unchanged. The US dollar today is of course much higher as yields are too but I think the trend is still higher for the long end and the post tariff foreign rethink of US assets is a brand new, big picture, really important new trend that I believe will continue for the coming years and that means a lower US dollar too.

I circled where 10 yr yield was in days before S&P downgrade on August 5th, 2011. The jump in 2013 was the taper tantrum.

This is what Moody's actually said:

"This one-notch downgrade on our 21-notch rating scale reflects the increase over more than a decade in government debt and interest payment ratios to levels that are significantly higher than similarly rated sovereigns."

"Successive US administrations and Congress have failed to agree on measures to reverse the trend of large annual fiscal deficits and growing interest costs. We do not believe that material multi-year reductions in mandatory spending and deficits will result from current fiscal proposals under consideration. Over the next decade, we expect larger deficits as entitlement spending rises while government revenue remains broadly flat. In turn, persistent, large fiscal deficits will drive the government's debt and interest burden higher. The US' fiscal performance is likely to deteriorate relative to its own past and compared to other highly rated sovereigns."

I'll add, we don't have a tax/revenue problem, we have a massive spending problem and unfortunately only sharply higher interest rates will get the attention of Congress and based on what is being debated right now in DC, it doesn't look like we're there yet in terms of crisis type thinking. That said, at least there is a conversation on means testing Medicaid in terms of work requirements but nothing more when it comes to our entitlement programs. I know, it's a tough, complicated conversation.

The US 10 yr yield is back above 4.50% and the 30 yr yield is at 5.02-.3% in response.

So, to my point of the foreign rethink of US assets, I've said many times here that Mag 7 stocks because a global reserve asset that not just US institutional and retail investors owned but foreigners did in a big way too, including foreign central banks. I went through some 13F's in some of the Mag 7 names as of 3/31/25 (so doesn't include the response to the April 2nd tariff announcement and pause) and here is a small sample of what I saw.

In Nvidia, Japan's Government Pension Investment Fund sold 17.6 million shares taking their holdings to 149.5 million. The Royal Bank of Canada sold 1.5 million shares leaving them with still a large 81.6 million shares. HSBC sold 7.1 million shares and hold 80 million as of 3/31. Mitsubishi UFJ sold 16.4 million shares to 66.5 million. CIBC sold shares as did Toronto Dominion and Schroders. The Swiss National Bank slightly shed some shares, selling 225k shares but still leaving a large holding of 69 million shares. I await the updated holdings of the Norges Bank.

In Microsoft, Japan's Government Pension Investment Fund sold 4.1 million shares which was about 10% of their holdings. RBC sold about 1 million shares to 31 million. HSBC actually added some shares, 622k to 24.5 million. The Swiss National Bank tweaked its holdings lower by 27k to just under 20 million. Schroders sold 280k shares to 18.3 million while TD and CIBC saw slight increases.

My guess is that a pronounced trend likely took place in April.

The March TIC data came out late Friday and foreigners bought a large $123b of US notes and bonds with private buyers making up $82b of it. Central banks bought the balance but after four months of selling. The trend has been lower holdings from foreign central banks where in contrast a lot of buying has been on the private side and including hedge funds. That in March was captured by the holdings of the Cayman Islands which was the 2nd biggest buyer, totaling $37.5b. Foreign flows also come thru UK banks and the UK is now the 2nd biggest holder of US Treasuries as a result. Japan remains the biggest at $1.13 trillion while China's holdings are down to $765b, lower by almost $20b in March. As the basis trade started to unwind in April, the next TIC report will be important to see in the Cayman Island holdings.

While foreigners still buy US Treasuries in totality, they continue to buy less as a % of total marketable securities. Those holdings are at about 30% vs about 50% 15 years ago.

Moving on. If Walmart ends up eating some of the tariffs as some want, we shouldn't feel any better because less profits for them means less hiring, less capital spending, less discounting on non-tariff items and lower eventual total returns to shareholders. Pick your poison.

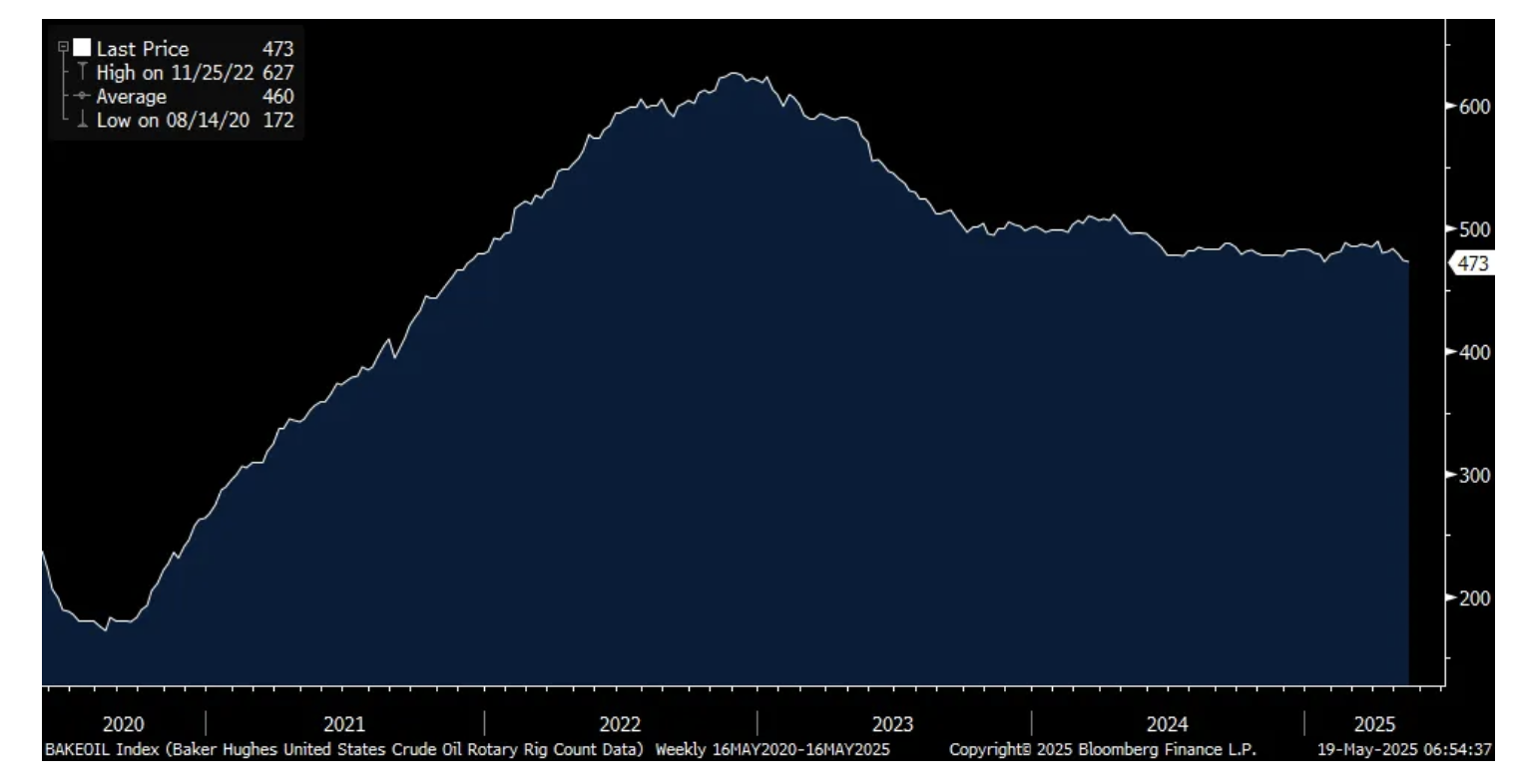

In response to lower oil prices, the US crude oil rig count fell for a 3rd week by one and by 10 over this time frame. At 473 rigs it is just one rig from matching the least since December 2021. As heard from Diamondback Energy and others, US shale oil production is peaking out, both at current oil prices and from a geology perspective. Low prices are in the process of curing low prices. We remain bullish and long oil and gas stocks.

Crude oil rig count

We heard in Q1 earnings reports from US airlines that international travel had softened to the US. Ryanair said the same today as international travelers are coming less so to the US. From the earnings call, "I think there might be a trend, there's a perception, certainly in Europe, that the US is an unwelcoming destination at the moment. That seems to be translating, maybe to a bit more holidaying at home in Europe. We see no decline in the inbound transatlantic to Europe this year. And, all of the metrics we see forward bookings into Spain, Italy, Greece, the holiday, the islands this summer has been reasonably strong."

China reported some April economic stats with retail sales light relative to expectations, though still up 5.1% y/o/y while industrial production was above the forecast, up 6.1% y/o/y. Home prices continue to fall, both new and existing and remains a problem but we're at least multiple years into it, thus implying closer to the end than the beginning of the downturn. With regards to China's manufacturing sector, for products they make for US consumption they are certainly experiencing pain. For stuff they make for non-US customers, particularly in autos, electrical equipment, robotics, rail, etc..., they are doing just fine.

China has implemented a bunch of 'cash for clunkers' type stimulus initiatives to spur consumer spending that I'm not a fan of as it's just short term in nature in terms of its impact and it just pulls forward behavior. That said, spending on leisure and hospitality has done much better as seen by robust domestic travel figures and attendance to Macau.

BY Doug Kass · May 19, 2025, 11:15 AM EDT

Bret Jensen

13 minutes ago

The highest 30-Year Treasury yield in 2023 is the last thing the housing sector needs. Fun Factoid: Just over 70% of people with active real estate licenses did not close a single sale over the past 12 months. I think many agents are going to exit the industry before this downturn bottoms

BY Doug Kass · May 19, 2025, 11:05 AM EDT

Shorting more GRNY (Fundstrat Granny Shots) at $21.01.

BY Doug Kass · May 19, 2025, 10:59 AM EDT

BY Doug Kass · May 19, 2025, 10:55 AM EDT

From JPMorgan:

US: Futs are lower as the US debt downgrade has triggered a global de-risking. The yield curve is bear steepening with the 30Y yield hitting its highest level since Nov 2023 and the USD selling off. Pre-mkt, MegaCap Tech names are down 2-4%+ with Semis/Cyclicals under pressure. Cmdtys are mixed with energy/base lower and precious/ags higher. Today’s macro data focus is the 6x Fedspeakers and the Leading Indicators Index.

and...

EQUITY & MACRO NARRATIVE

The SPX breached 5,900 a level thought to represent both resistance as well as a milestone for the “buyers who live higher” to jump back into the market. Next stop? 6,144 is the all-time high and sits 3.1% away from Friday’s close. We remain tactically bullish, looking for the SPX to breach its all-time high.

· PULLBACK POTENTIAL – We do think the risk of a pullback is increasing but another correction is unlikely. What are the possible factors that could lead to a near-term pullback? (i) NVDA earnings miss – SPX has been up 19.6% since its April 8 low, led by a 30.5% rally in Mag7. NVDA earnings on May 28th will be the next catalyst to assess the strength of MegaCap Tech/Semis; given that chips purchasing were major achievements from Trump’s trade negotiation trips, the risk/reward of this earnings release is skewed positively, but a downside miss on guidance could lead to a pullback in tech; (ii) Stalled trade negotiations or a negative shock on US-China deal – given the positive surprise in US-China trade negotiation, 10% seems to be the new baseline on trade negotiation. Japan/India/South Korea/Australia are still on the list for investors to watch for upcoming trade deals or Memorandum of Understanding (“MoU”). (iii) Positioning – Positioning Intelligence tells us that the 4wk change in their Tactical Positioning Monitor reached a 1.7z level earlier this week (data as of May 16th). This would suggest the pendulum has swung somewhat more positively (the positive changes over the past month include buying from Retail, rebound in futures and options, and increase in HF gross exposure).” On the aggregated level, the positioning has moved up from -1z to -0.2z, close to neutral and 39th percentile dating to 2015. In addition, JPM Strategy teams (here and here) notes a slowing of retail buying impulse, largely completed short covering by macro hedge funds, and a continued lack of buying by foreign investors. Overall, while positioning is not necessarily a headwind for equities at current level, it may no longer serve as a support for continued rally.

· CONCENTRATION RISK – 2025 YTD (through May 15) SPX is +0.6% vs. Mag7 -4.7% vs. SPX493 +2.4% but with Mag7 quickly bridging the performance gap highlights another issue flagged by clients, concentration risk. Clients worry about a move higher led by MegaCap Tech, with relatively light positioning; this would resemble 24H1, where Mag7 returned 37.3% vs. SPX 14.5%. Though in 24Q3, Mag7 underperformed by 220bp, before closing 24Q4 leading by 1129bp. While we agree that a narrow rally is unlikely to boost investor sentiment it does not prevent the market from moving higher. The key remains earnings growth.

Source: JP Morgan Asset Management

· SMALL-CAPS LED RALLY? RTY is now up for six consecutive weeks, adding 15.3% since Apr 4 vs. SPX +17% and NDX +22.7%. Can small-caps bridge the gap and take over as leader? No. In our May 12 Morning Briefing we referenced using options to play upside in SMid-caps as we thought we would have seen a more violent short squeeze given the recent surge in RTY short interest. Clients who needed to cover shorts appear to have done so and now clients are not offsides should this rally continue. Further, with yields appearing to be sticky around 4.50% this likely pushes investors into larger-cap plays; and, if one wanted a defensive tilt that would likely be MegaCap Tech rather than traditional Defensives (HC turmoil; Utilities react poorly to higher yields).

Source: JP Morgan Asset Management

· SEASONALITY – on a 10-year basis, seasonality is positive for June – July. Over the last 10 years, July has been the second strongest month, averaging 3.35% for the SPX with a 100% hit rate. June has been the fourth strongest month, averaging 1.15% with an 80% hit rate.

· US MKT INTEL VIEW – Tactically Bullish. Our investment hypothesis remains intact: resilient macro data, better than expected earnings, and a thawing trade war. This week brings Flash PMIs and Consumer-sector earnings in a market which we think can be characterized as, “good news is good news and bad news is ignored”. Much of the current rally has been technical/positioning led we do feel that many investors are unlikely to get short at these levels due to: (i) potential for positive trade deals (Canada, China, EU, or Mexico) would continue to reset growth/earnings expectations higher and the timing is unpredictable for announcements; (ii) NVDA earnings are a key catalyst and with Trump’s Middle East tour the forward guidance could exceed expectations; (iii) ‘hard’ macro data has failed to show any material deterioration and we likely need to see a spike to weekly jobless claims (maybe 280k – 300k range), a fall in NFP (maybe under 50k – 70k), and/or Retail Sales turning negative; and (iv) M&A/Capital Markets appear to have been turned back on and robust pipeline of deals tends to coincide with bull markets. While we acknowledge that the risk/reward for the SPX may be close to neutral, we think there is more upside to this market before we get to a point where we think it people will get bearish which would be highlighted by net-bullish positioning at a time when the macro data begins to see material declines.

BY Doug Kass · May 19, 2025, 10:40 AM EDT

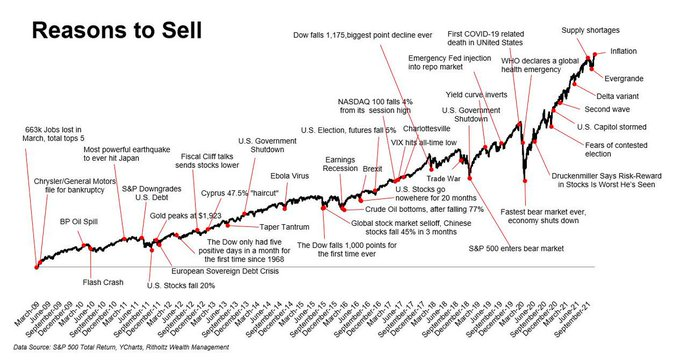

A reminder: there are always reasons to sell:

BY Doug Kass · May 19, 2025, 10:29 AM EDT

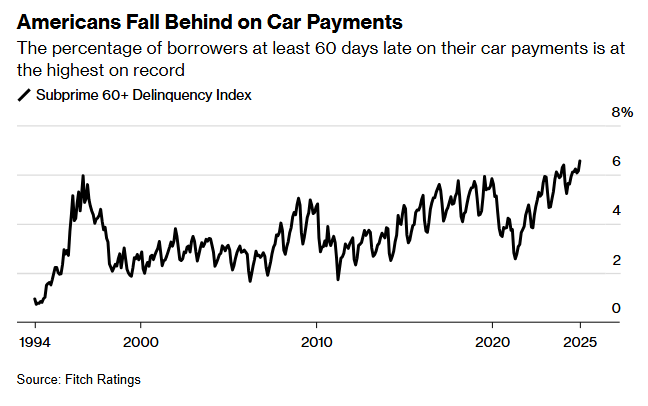

Highest delinquencies ever recorded:

BY Doug Kass · May 19, 2025, 10:13 AM EDT

Added to Index shorts with S&P cash continuing to rally (now -23 handles):

* SPY $591.87

* QQQ $518,81

BY Doug Kass · May 19, 2025, 10:09 AM EDT

To paraphrase Warren Buffett, politicians often lie like ministers of finance on the eve of devaluation:

BY Doug Kass · May 19, 2025, 9:59 AM EDT

With S&P cash -45 handles I added to my index shorts:

* SPY $590.33

* QQQ $517.32.

BY Doug Kass · May 19, 2025, 9:56 AM EDT

8:30 a.m.: Fed Bank of Atlanta President Bostic (Non-Voter) gives welcome remarks before the 2025 Financial Markets Conference - "Financial Intermediation In Transition: How Will Policy Adapt?" hosted by the Federal Reserve Bank of Atlanta, Fernandina Beach, FL (No text. Livestream available);

8:45 a.m.: Fed Vice Chair Jefferson (Voter) gives the Keynote at the Federal Reserve Bank of Atlanta’s 2025 Financial Markets Conference, Fernandina Beach, FL;

8:45 a.m.: Fed Bank of Atlanta President Bostic (Non-Voter) moderates a discussion before the 2025 Financial Markets Conference - "Financial Intermediation In Transition: How Will Policy Adapt?" hosted by the Federal Reserve Bank of Atlanta, Fernandina Beach, FL (Livestream available);

8:45 a.m.: Fed Bank of New York President Williams (Voter) participates in moderated discussion on the economic outlook before the Mortgage Bankers Association Secondary and Capital Markets Conference, NY Marriott Marquis, NYC (No text. Moderated Q&A expected);

11:30 a.m.: FOMC Closed Board Meeting. Review and determination by the Board of Governors of the advance and discount rates to be charged by the Federal Reserve Banks. https://www.federalreserve.gov/aboutthefed/boardmeetings/20250519closed.htm;

1:15 p.m.: Fed Bank of Dallas President Logan (Non-Voter) is panel moderator for "Policy Session 2: The Increasing Role of Nonbank Institutions in the Treasury and Money Markets" at the 2025 Financial Markets Conference - "Financial Intermediation In Transition: How Will Policy Adapt?" hosted by the Federal Reserve Bank of Atlanta, Fernandina Beach, FL (Livestream available);

1:30 p.m.: Fed Bank of Minneapolis President Kashkari (Non-Voter) participates in conversation before the Minnesota Young American Leaders Program (MYALP) at the University of Minnesota, MN (No prepared/embargoed text. Audience Q&A expected. No media Q&A. Livestream at minneapolisfed.org.)

BY Doug Kass · May 19, 2025, 9:45 AM EDT

-NVAX +19% (confirms U.S. FDA Approves BLA for Novavax's COVID-19 Vaccine; to receive $175M milestone payment from SNY)

-SOC +17% (restarts oil production at Santa Ynez Unit with strong early output; raises H2 avg daily production guidance)

-PRME +10% (announces Breakthrough Clinical Data Showing Rapid Restoration of DHR Positivity after Single Infusion of PM359, an Investigational Prime Editor for Chronic Granulomatous Disease)

-TXNM +9.4% (to be acquired by Blackstone Infrastructure for $61.25/shr in cash, valued at $11.5B including debt and preferred stock)

-BLBX +8.7% (merger target REalloys signs Joint MOU with Saskatchewan Research Council enabling processing of rare Earth materials for high performance magnet production in Q2:2025)

-RXST +4.2% (Wells Fargo Raised RXST to Overweight from Equal Weight, price target: $25 from $17)

-UNH +4.2% (buying off recent weakness; CEO buys 87K common shares)

-BBWI +2.2% (guides Q1, affirms FY25; appoints new CEO)

-DTSS +2.2% (secures $100M in 5G-AI service contracts)

-PGRE +2.1% (announces review of strategic alternatives to maximize shareholder value and management transition)

-RDDT -6.6% (Wells Fargo Cuts RDDT to Equal Weight from Overweight, price target: $115)

-GILT -6.0% (earnings, guidance)

-TH -4.9% (earnings, guidance)

-NVDA -2.8% (CEO keynote speech at COMPUTEX 2025)

-SHAK -2.7% (TD Cowen Cuts SHAK to Hold from Buy, price target: $105)

BY Doug Kass · May 19, 2025, 9:22 AM EDT

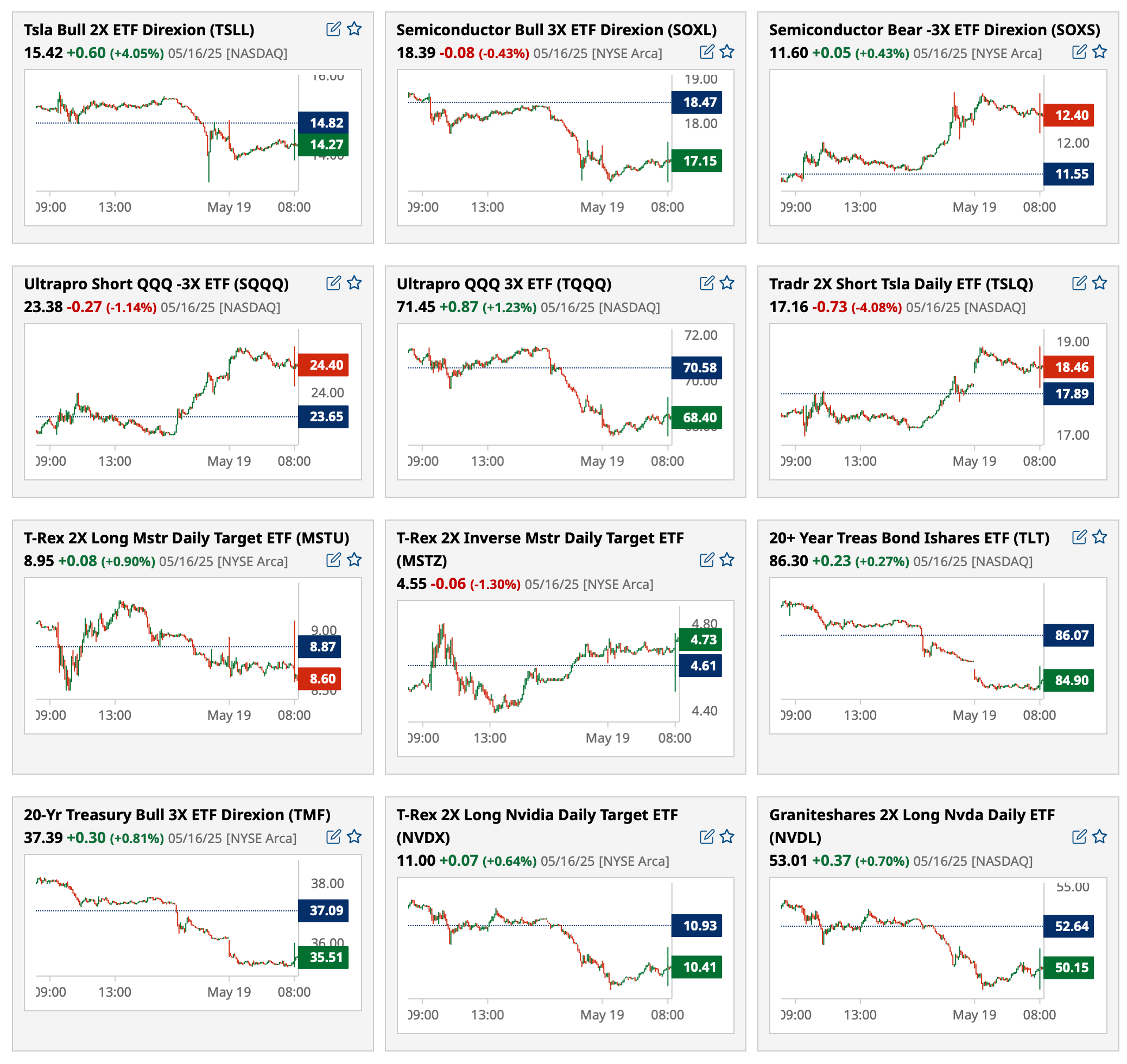

Most active premarket ETFs at 8:09 a.m. ET:

BY Doug Kass · May 19, 2025, 9:15 AM EDT

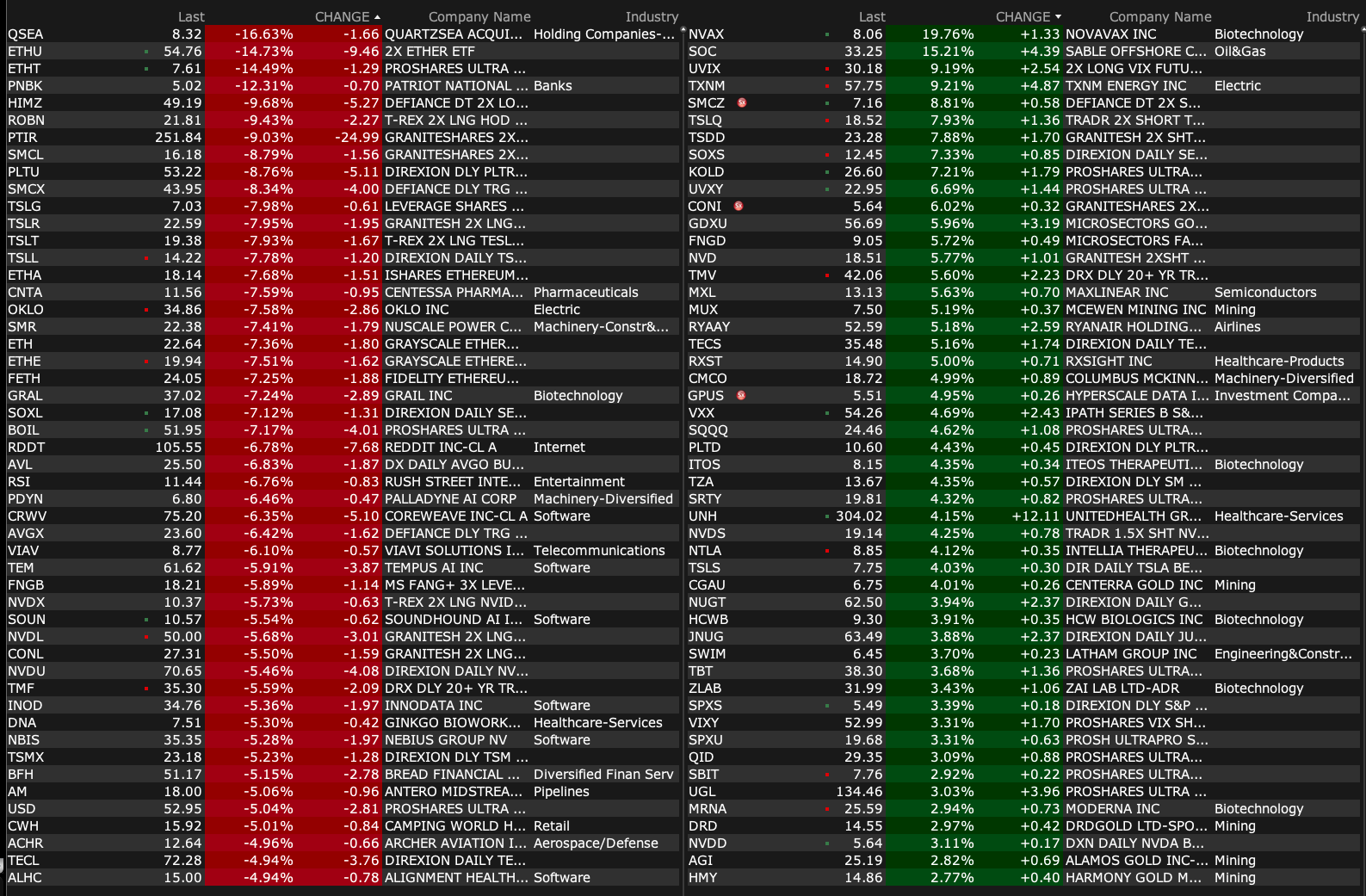

Premarket percentage movers as of 8:27 a.m. ET:

BY Doug Kass · May 19, 2025, 9:03 AM EDT

BY Doug Kass · May 19, 2025, 8:59 AM EDT

BY Doug Kass · May 19, 2025, 8:45 AM EDT

BY Doug Kass · May 19, 2025, 8:30 AM EDT

BY Doug Kass · May 19, 2025, 8:30 AM EDT

BY Doug Kass · May 19, 2025, 7:58 AM EDT

* Oy!

BY Doug Kass · May 19, 2025, 7:45 AM EDT

Remember my column from the other day? Can't Find My Way Home.

BY Doug Kass · May 19, 2025, 7:26 AM EDT

* At Friday's close, technicians were unanimously bullish (see below)

* But some of the best stock charts lie at the bottom of the Ocean...

Bonus - here are some great links:

My Favorite Chart this Past Week - by Frank Cappelleri

How Will Stocks Perform This Memorial Day Week?

Tom Lee: There's still upside for stocks and pullbacks will be shallow

BY Doug Kass · May 19, 2025, 7:12 AM EDT

Tom Lee Remains Bullish

Tom Lee: There's still upside for stocks and pullbacks will be shallow

BY Doug Kass · May 19, 2025, 7:08 AM EDT

The gaps were never filled:

BY Doug Kass · May 19, 2025, 6:58 AM EDT

BY Doug Kass · May 19, 2025, 6:48 AM EDT

BY Doug Kass · May 19, 2025, 6:38 AM EDT

The S&P Short Range Oscillator remain in overbought — at 5.36% vs. 5.77%.

BY Doug Kass · May 19, 2025, 6:28 AM EDT

BY Doug Kass · May 19, 2025, 6:12 AM EDT

BY Doug Kass · May 19, 2025, 6:02 AM EDT

BY Doug Kass · May 19, 2025, 5:52 AM EDT