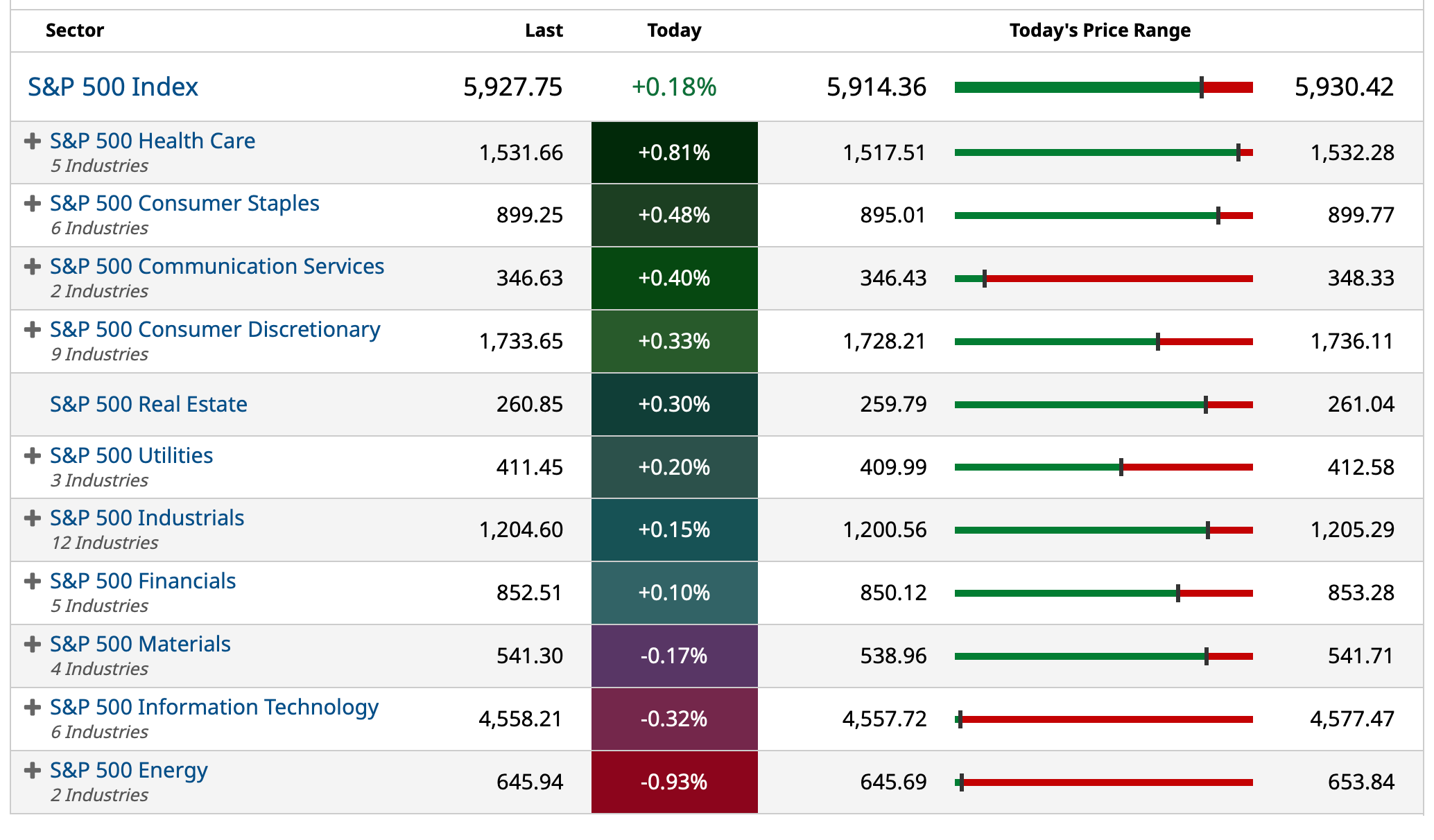

Moody's Downgrades U.S. Credit Rating

Break in!

BY Doug Kass · May 16, 2025, 5:01 PM EDT

Break in!

BY Doug Kass · May 16, 2025, 5:01 PM EDT

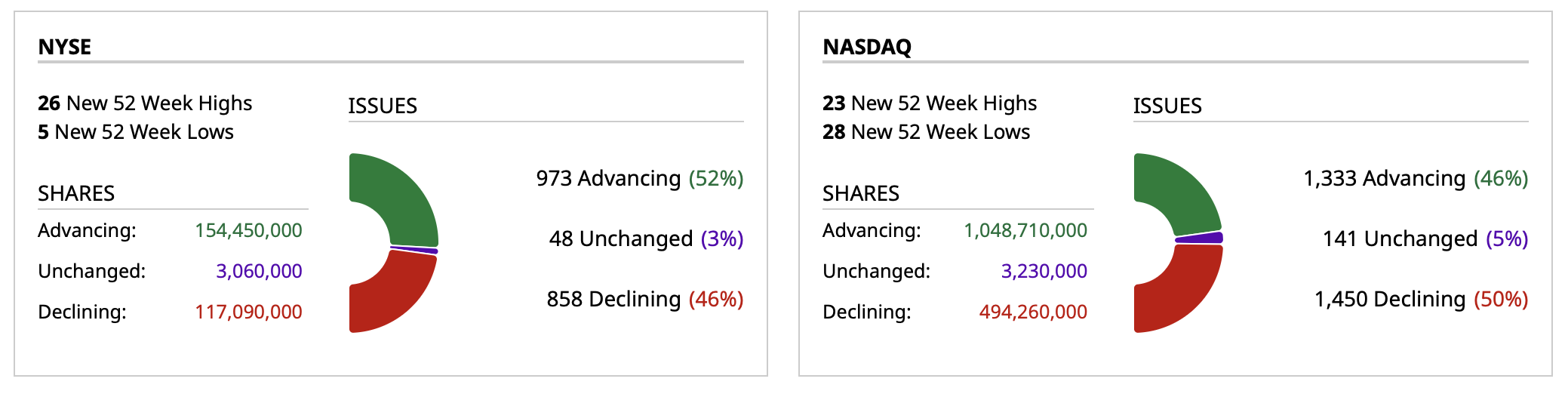

- NYSE volume 3% above its one-month average

- NASDAQ volume 20% above its one-month average

- VIX index: down 3.37% to 17.23

BY Doug Kass · May 16, 2025, 4:29 PM EDT

I am leaving early for the weekend — as I have seen enough!

Thanks for reading my Diary today and all week.

I hope my output was useful.

Enjoy the weekend.

Be safe.

BY Doug Kass · May 16, 2025, 3:05 PM EDT

Houskeeping item.

I closed out a successful short today — ABR ($10.55).

BY Doug Kass · May 16, 2025, 2:39 PM EDT

Housekeeping item.

I have begun to sell my Freshpet FRPT position (+$5 today). Will be out by day's end.

BY Doug Kass · May 16, 2025, 2:10 PM EDT

BY Doug Kass · May 16, 2025, 2:00 PM EDT

BY Doug Kass · May 16, 2025, 1:48 PM EDT

Scott Galloway's No Mercy No Malice... "The Fix."

BY Doug Kass · May 16, 2025, 12:40 PM EDT

BY Doug Kass · May 16, 2025, 12:01 PM EDT

Apple: KeyBanc Capital Markets stays cautious on Apple: iPhone 16, AI unlikely to spur upgrades; valuation still stretched

"Remain Sector Weight on Apple; Our broader thesis on iPhone 16 and Apple Intelligence failing to drive an upgrade cycle remains intact. While we believe the recent announcement of a tariff exemption on smartphones was one of the best outcomes for Apple going forward, we remain cautious given: 1) ‘26 growth expectations remain high in an uncertain consumer spending environment; 2) upgrade rates remain muted; 3) competition in China appears elevated; and 4) legal risks for Services with the Google DOJ lawsuit and App Store changes. With AAPL trading at ~21x our ‘26 adj. EBITDA vs. the three-year average of ~21x, we think AAPL remains expensive relative to the growth."

BY Doug Kass · May 16, 2025, 11:45 AM EDT

BY Doug Kass · May 16, 2025, 11:35 AM EDT

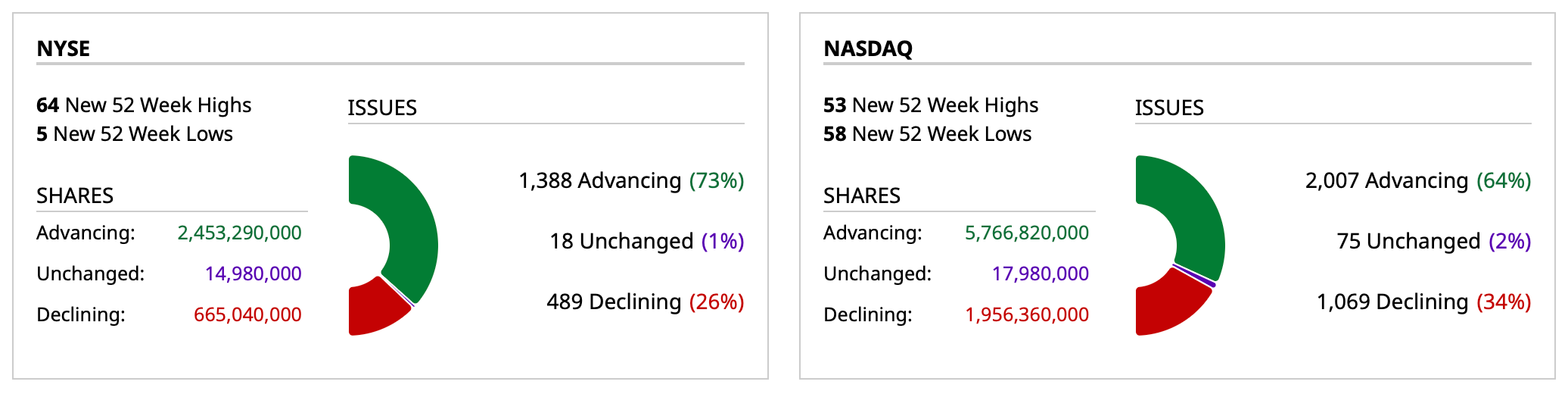

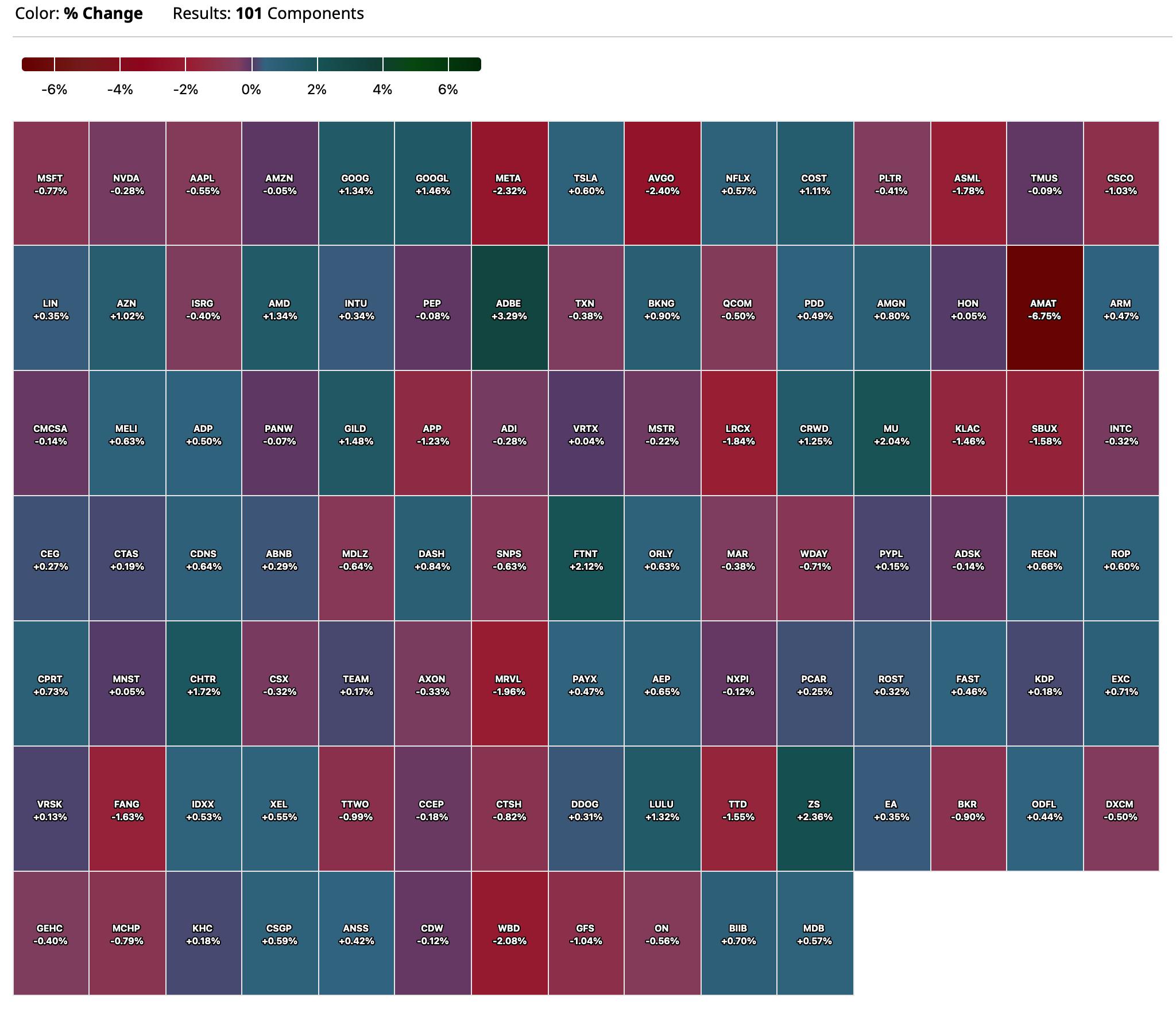

- NYSE volume 26% above its one-month average;

- Nasdaq volume 25% above its one-month average;

- VIX index: down 0.90% to 17.67

BY Doug Kass · May 16, 2025, 11:20 AM EDT

From Peter Boockvar:

Positives,

1) The US and China decided to save the back-to-school season and Christmas, and countless small businesses (both here and there) to some extent, depending on where the final tariff rates settle out at.

2) The April CPI rose .2% m/o/m both headline and core, one tenth below expectations for each. The y/o/y gains are now 2.3% and 2.8% respectively vs 2.4% and 2.8% in the month before. Energy prices were higher by .7% m/o/m but still down 3.7% y/o/y. Food at home prices dropped by .4% m/o/m helped by lower egg prices, though still up 2% y/o/y while those food prices out of home were higher by .4% and 3.9% y/o/y. Service prices ex energy rose .3% m/o/m and 3.6% y/o/y with again help by higher rents. On the core goods side, no signs yet of tariff induced inflation as prices were up just .1% m/o/m and by the same amount y/o/y.

3) The April PPI unexpectedly fell by .5% m/o/m vs the estimate of up .2% with much offset by an upward revision of 4 tenths to the March read to flat from down .4%. They were up 2.4% and 3.1% y/o/y. The core rate was lower by 4 tenths vs the forecast of up .3% while March was revised up by 5 tenths. On the goods side, ex food and energy saw prices up by .4% m/o/m and 2.5% y/o/y, an early signs of tariff increases passing thru. Services deflation was the lid on PPI as they fell by .7% m/o/m because of a 1.6% drop in trade prices and .4% decline in transportation/warehousing. The BLS said “Over 40% of the April decline in the index for final demand services is attributable to margins for machinery and vehicle wholesaling, which dropped 6.1%.”

4) Initial jobless claims were about as expected at 229k, no change from the prior week and staying low. The 4 week average did tick up to 231k from 227k as a print of 216k dropped out. Continuing claims totaled 1.881mm and are staying elevated though.

5) In the weekly MBA data, purchase applications rose 2.3% w/o/w, though refi’s were flattish, down .4%.

6) From Walmart: Walmart US comps up 4.5% and Sam's higher by 6.7% and "Those strong Q1 results were not driven by inflation. Transactions and units drove our top line. Globally, we grew e-commerce 22% with each segment delivering growth of at least 20%. Inventory is in good shape."

7) From Cava: They saw 10.8% comp gains "driven by 7.5% traffic...In a fluid macroeconomic environment, our performance this past quarter underscores the strength of our value proposition and the enduring relevance of our brand." On their customer, "As it relates to the data and what we have been seeing, nothing in our data suggests that our consumers are challenged...Our premium attachment continues to be high...our per person average continues to increase and we have positive traffic across all geographies, all income strata, all formats and all dayparts."

8) From Richemont: "In fiscal year '25, Richemont delivered a robust performance in an uncertain macroeconomic environment…Over the year we saw double digit growth in all our regions except Asia Pacific, which remained impacted by soft demand in China."

9) From Boot Barn: "Turning to current business. We are now six weeks into the first quarter of fiscal '26, and we have continued to see broad based growth as consolidated same store sales increased 9%, driven by increased transactions and full price selling. While we are pleased to see the strong trend of the business continue into fiscal '26, we recognize the ongoing uncertainty with respect to tariffs."

10) From Applied Materials: "we have not seen significant changes in market demand. Our customers remain focused on winning the race to be first to market with transformative new technologies…In the near term, we see overall demand and customer investments continuing at the expected rate and pace, even in the current environment, and the long term secular drivers for growth in our business remains intact."

11) From Cisco: "Despite the uncertain macro environment, this demonstrates the valuable outcomes we are delivering for customers in the era of AI.” On what they are seeing in terms of spending behavior from their customers, "we haven't seen any meaningful change in how they're purchasing. And so we haven't seen any customers really fundamentally slowing down. They're still committed to the technology transition. I think the AI transition is just so important that they're going to continue to spin until they just absolutely have to stop. And I think that as of right now, they're still comfortable." Also, "As it relates to pull-forwards, look, I think I'm sure there was an order here and there from a customer who decided to pull something forward because they were concerned about tariffs, but we looked at a ton of data points to see if we saw any signs of broad based pull ahead business, and we did not."

12) From Sphere Entertainment: Answering a question on Vegas visitation from overseas, "Las Vegas has over 40 million visitors every year so far. We've seen that the international accounts for a little over 20% of the guests to Sphere and 10% for concerts. We really haven't seen any change. So I think, there's a little going on in our economy with that right? Maybe later on we'll see some substantive reaction from the marketplace, but right now we're really not seeing it. So, and even if we did, it doesn't account for that big of a difference, right? And, I think in general, when it comes to concerts, demand exceeds capacity."

13) The UK economy grew by .7% q/o/q which was one tenth above the estimate and by 1.3% y/o/y. The service sector again led the way but there was definitely pull forward type behavior as exports and imports both jumped much more than anticipated.

14) Expectations for an improving German economy spiked in May as measured by the ZEW which rose to +25.2 from -14. The estimate was +11.3. The current situation remains tough though as it came in at -82 vs -81.2 in the month before.

Negatives,

1) As seen in the May NY and Philly industrial surveys, the manufacturing recession continued on. The NY index was -9.2 vs -8.1 in the prior month. The Philly index was -4 vs -26.4 in April.

2) April import prices rose .1% m/o/m vs the estimate of down .3% but was almost all offset by a downward revision of 3 tenths to March. Import prices ex food and energy grew by .5% m/o/m and up by .8% y/o/y. Tariffs have yet to all show up as import prices for industrial supplies fell by .5% m/o/m, but capital goods prices were up by .6% m/o/m and higher by .2% for autos/parts and by .3% for consumer goods, also m/o/m.

3) Core retail sales in April fell by .2% m/o/m instead of rising by .3% as forecasted and only slightly offset by a one tenth upward revision to March. Not included here were auto sales that after spiking by 5.5% in March due to the pull forward, was flattish m/o/m in April. Building materials rose for a 2nd month after 4 months of declines and by .8% m/o/m.

4) The May preliminary UoM consumer confidence index fell to just 50.8 from 52.2, below expectations of 53.4 and less than 1 pt from a multi decade low. Current Economic Conditions were own by 2.2 pts m/o/m while Expectations were lower by .8 pts. One yr inflation expectations jumped again to 7.3% and was just 2.6% in November. The 5-10 yr guess rose to 4.6% from 4.4% and was 3.2% in November. Employment expectations fell 1 pt to within 1 pt of matching the lowest since 2009. The income component dropped by 6 pts to the weakest since January 2013. Notwithstanding the further drop in overall confidence, spending intentions on vehicles, homes and major household items were a touch higher, though after the April decline. As we know this survey has become very politically divided, most of the m/o/m May drop in confidence was from Republicans. Not surprisingly, “Tariffs were spontaneously mentioned by nearly three-quarters of consumers, up from almost 60% in April; uncertainty over trade policy continues to dominate consumers’ thinking about the economy.” Note that this survey took place from April 22nd to May 13th, and thus 2 days after the China pause. “Many survey measures showed some signs of improvement following the temporary reduction of China tariffs, but these initial upticks were too small to alter the overall picture – consumers continue to express somber views about the economy.” Lastly on this, “A whopping 73% of consumers offered unsolicited comments about tariffs, including nearly two-thirds of Republicans, showing that these concerns cross partisan lines. A substantial share of these comments specifically mentioned the high level of uncertainty and unpredictability of trade policy, suggesting that this week’s development is unlikely to result in a resurgence of confidence in the economy, consistent with trends seen following the April 9 pause on reciprocal tariffs.”

5) Housing starts and permits were a bit under expectations. Single family starts fell to 927k from 947k but rose to 434k from 392k for multi family. Permits were down for both with single family in particular at the lowest level in 2 years.

6) The NAHB May builder sentiment index dropped a sharp 6 pts to 34 from 40, well under the estimate of no change and matches the weakest since December 2022. Most of the decline came in the Present Situation which declined by 8 pts while Expectations were down 1 pt to 42. Prospective Buyers Traffic remains depressed and a bit more so at 23 vs 25, so less than half the breakeven of 50. The problem in housing remains both a supply and demand issue. The NAHB said “The spring home buying season has gotten off to a slow start as persistent elevated interest rates, policy uncertainty and building material costs factors hurt builder sentiment in May.” Also, “the overall actions on tariffs in recent weeks have had a negative impact on builders, as 78% reported difficulties pricing their homes recently due to uncertainty around material prices.” What are builders doing to push sales? “The survey “revealed that 34% of builders cut home prices in May, up from 29% in April and the highest level since December 2023 (36%) . Meanwhile, the average price reduction was 5% in May, unchanged from the previous month. The use of sales incentives was 61% in May, the same rate as the previous month.”

7) The May NY services index was -16.2 vs -19.8 and below zero for an 8th straight month.

8) The World Container Index for a 40 ft container saw the Shanghai to LA price rise by 16% w/o/w, by $423 in absolute dollars, to $3,136. That's the highest since early March. The trip from Shanghai to NY jumped 19%, by $704 to $4,350, the highest since late February. The CEO of Flexport thinks these rates will be between $6-7k by June.

9) The April NFIB small business optimism index fell to 95.8 from 97.4. It's lower for a 4th straight month and is back to approaching the 93.7 level it was at in October 2024 right before the election. The bottom line, "Uncertainty continues to be a major impediment for small business owners in operating their business in April, affecting everything from hiring plans to investment decisions. While owners are still trying to fill a high number of current job openings, their outlook on business conditions is less supportive of future business investments." Also, "The percent of small business owners reporting labor quality as the single most important problem for business was unchanged from March at 19%, remaining the top issue for the 3rd consecutive month."

10) US April industrial production was flat m/o/m while the manufacturing component fell by .4%, though about as expected.

11) From Walmart: "we're positioned to manage the cost pressure from tariffs as well or better than anyone. But even at the reduced levels, the higher tariffs will result in higher prices." What are they seeing from their customer? The same, "which are that customers, in some cases, we've heard of some concern, they remain choiceful and consistent and we continue to see customers prioritizing value and speed of delivery. We have seen growth across all income cohorts in the quarter."

12) From Jack in the Box: "It's well known that there is significant pressure on multiple income cohorts, and we've seen the results in our negative traffic. There are definitely more headwinds than tailwinds at the moment for most within our industry." Their comps fell 4.4% y/o/y for the Jack brand and by 3.6% for Del Taco.

13) From American Eagle: "At this time, the company is withdrawing its previously provided fiscal year 2025 guidance due to macro uncertainty and as management reviews forward plans in the context of first quarter results…We are clearly disappointed with our execution in the first quarter. Merchandising strategies did not drive the results we anticipated, leading to higher promotions and excess inventory. As a result, we have taken an inventory write down on spring and summer goods."

14) From Landstar: "The freight environment in the 2025 first quarter was characterized by relatively soft demand, weather impacts, and readily available truck capacity. The impact of accumulated inflation remains a drag on the amount of truckload freight generated in relation to consumer spending. Truck capacity continues to be readily available with small pockets of supply demand equilibrium, and market conditions continue to favor the shipper amidst choppy conditions in the industrial economy."

15) From Simon Property: "Projecting and predicting sales is really difficult because to the extent that there is a retailer that imports goods from China, even with today's kind of reduction in kind of tit for tat, you're still talking about 30% tariff, which is material. And at this point, many retailers are either halting ordering goods from China, which could affect their inventory levels, trying to source it elsewhere, which they may or may not be successful with. And so it's a relatively big unknown to the extent that there is a reliance on China even on today's recent news…And given margins, those tariffs in the 30-ish percent, I think are going to give retailers pause whether or not they can afford to have goods shipped to them from China. To the extent that it is in the more flat 10%, I think it's really retailer dependent. I think they're going to probably operate business as usual. They'll I think try to pass a little bit on to the consumer, they'll try to get the manufacturer to take some of it and they may take some of it as well." On the shopper, "So the consumer, I think is fine. I do think they're being a little more cautious. And I do think tourism is - this may be the wrong word, flattening, waning, what are the different phases of the moon? Waxing, waning, whatever it is? I think tourism to the US is going to be cautious this year, whether it's from Mexican nationals, Canadians, Europeans, we've just seen a little bit on the border. On the other hand, the dollar is weaker, so maybe that offsets it...And so you put it all together, the economy is clearly a little bit uncertain. You put it all together and it makes it really hard to predict sales right now."

16) From Topgolf Calloway: "As of this call, and assuming current rates of approximately 10% for all countries of origin other than Mexico, Canada and China; this year's unmitigated impact would be approximately $25 million, an increase of $20 million vs our last call. Looking forward, if these are the final rates, we believe we will be able to mitigate some portion by further optimizing operations and accelerating cost reduction and margin programs. We then believe we will have the ability to pass the balance on, with only a minor impact to demand." With regards to Topgolf, "using external data, our fun scores remain high and consumer feedback on the experience remains definitively positive, both in absolute terms and relative to our competitive set. But over the last 18 months, as the mid income consumer has become more stretched, Topgolf has begun to be perceived as relatively expensive. And in a slowing consumer environment, this is a significant but."

17) From Barry Sternlicht on the Starwood Property Trust call: "The economy is going to weaken. I just was talking to CEOs of Fortune 100 companies in the past few days, returning from the West Coast and there will be issues on shelves and there will be prices for consumers to absorb. And you kind of already were in a recession, you kind of saw it at the lower half of the country and the top 10%, 15% of the country was carrying spending in consumption. And now, we'll see how the wealth effect actually plays through. Actually, the markets have recovered shockingly to pre-Liberation Day highs, but that doesn't really feel right. And things like travel are clearly off. I guess it was Expedia that reported and then Airbnb, and we've seen the travel numbers, the airlines have talked about their stress as international travel in the United States dissipates. But it will go somewhere. So, Canadians will go to Europe or they'll go to the Caribbean. They may not come here."

18) The March and April jobs data out of the UK was about as expected, though April saw a drop of 32k jobs. Higher employment costs (national insurance and minimum wages) implemented by the Starmer government isn't helping. Wage growth in the 3 months ended March rose 5.6% ex bonuses and continues to run well above the rate of inflation. Their unemployment rate rose one tenth to 4.5% which happens to be the highest since July 2021.

19) Japan’s economy contracted by .7% q/o/q annualized in Q1, more than the estimated drop of .3% but partly offset by a two tenths increase to Q4 to 2.4% growth.

BY Doug Kass · May 16, 2025, 10:58 AM EDT

Here are today's "things":

I shorted more IWM at $209.11.

I shorted NVDA $136.43.

I shorted more ARKK $57.77

BY Doug Kass · May 16, 2025, 10:57 AM EDT

BY Doug Kass · May 16, 2025, 10:45 AM EDT

* The "J Factor" has turned negative this morning...

For what it is worth (and it shouldn't be worth much!), I have used a proprietary buy/sell technical indicator developed by The Chief - for several decades.

For the first time in the rally it has just signaled sell.

BY Doug Kass · May 16, 2025, 10:17 AM EDT

Adding to ARKK short at $57.75.

BY Doug Kass · May 16, 2025, 10:05 AM EDT

BY Doug Kass · May 16, 2025, 10:00 AM EDT

BY Doug Kass · May 16, 2025, 9:45 AM EDT

BY Doug Kass · May 16, 2025, 9:30 AM EDT

-INZY +179% (BMRN acquires Inozyme Pharma for $270M)

-SPCE +14% (earnings, guidance)

-QUBT +12% (earnings)

-RKT +4.9% (ValueAct discloses new RKT stake)

-CHTR +4.4% (confirms merger with privately-held Cox Communications in cash-stock deal valuing it at EV of $34.5B)

-VST +4.4% (to acquire natural gas assets totaling 2,600 MW for $1.9B)

-STZ +3.7% (Berkshire Hathaway doubles stake)

-EL +3.4% (Michael Burry's Scion Management disclosed 200K shares position)

-UNH +3.1% (slight bounce off recent weakness)

-PSFE +2.6% (Tier1 firm Raised PSFE to Neutral from Underperform, price target: $14.30 from $16)

-GLOB -29% (earnings, guidance)

-DOCS -17% (earnings, guidance)

-LAC -6.7% (files up to $1B mixed shelf)

-VVX -6.4% (Holder said to offer shares at $48.88-49.95/share)

-AMAT -4.6% (earnings, guidance)

-NVO -3.9% (CEO to step down; affirms FY25 guidance)

-FLO -2.8% (earnings, guidance)

-BRC -2.4% (earnings, guidance)

BY Doug Kass · May 16, 2025, 9:16 AM EDT

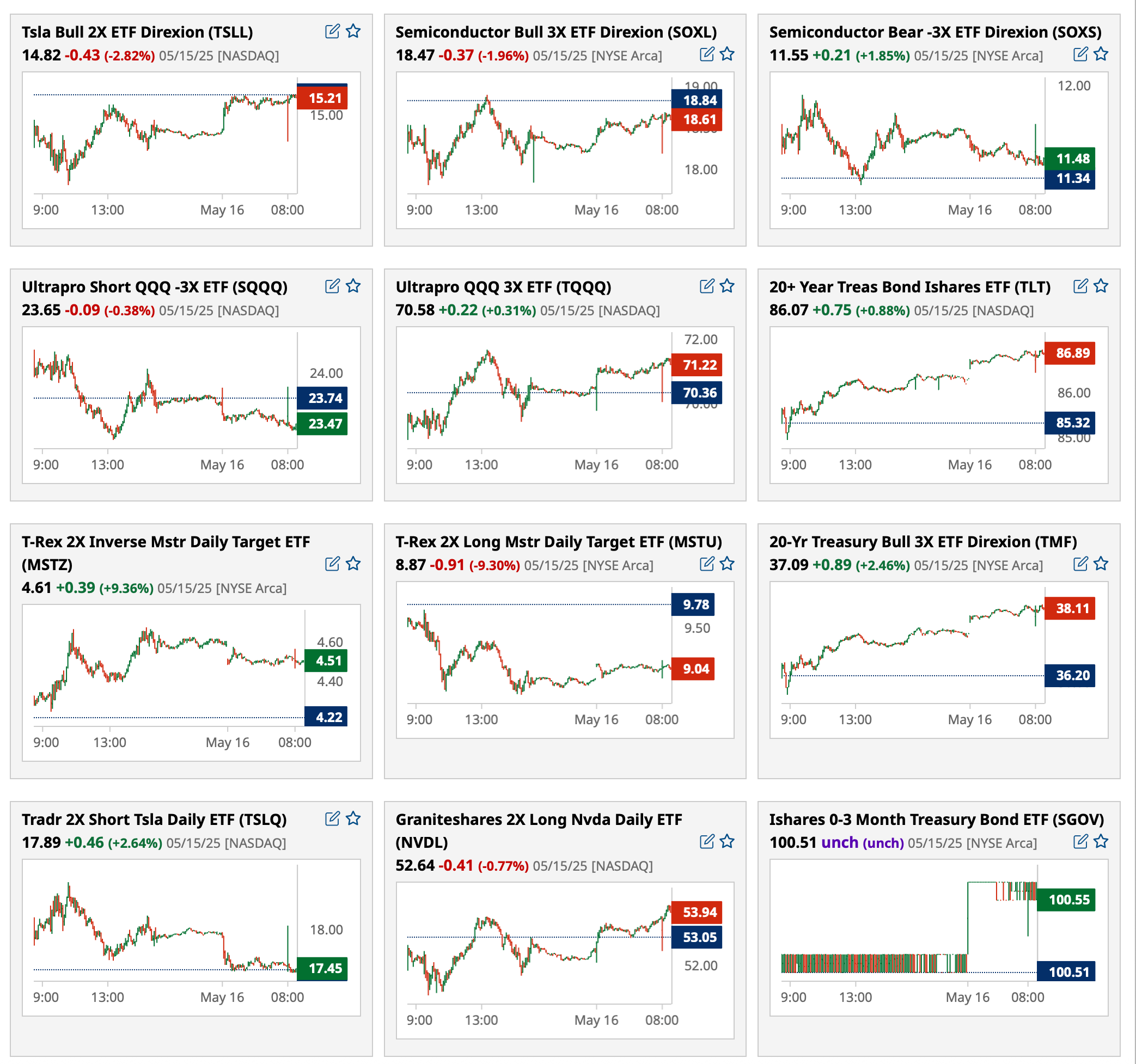

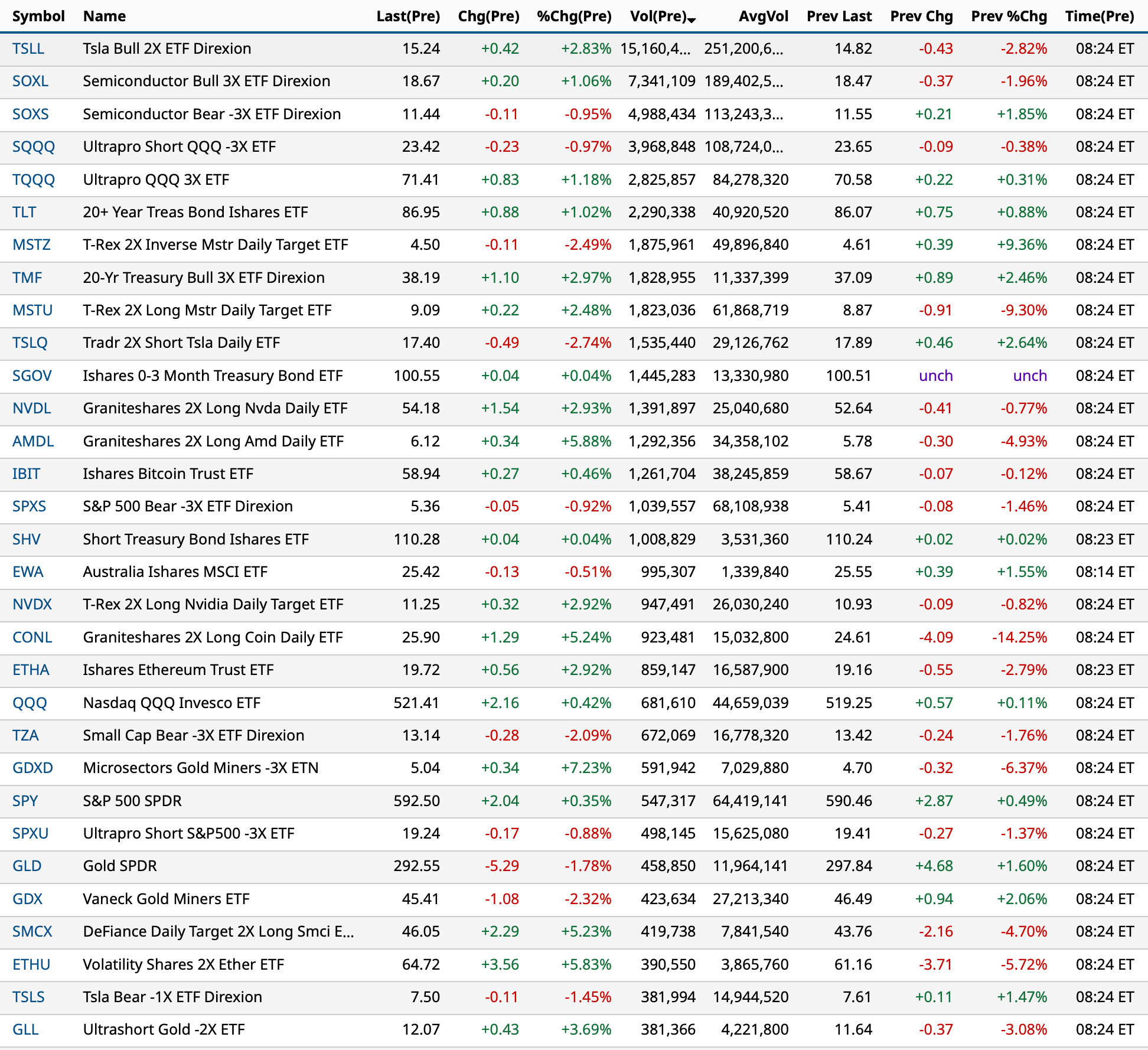

Most active premarket ETFs as of 8:24 a.m. ET:

BY Doug Kass · May 16, 2025, 9:05 AM EDT

BY Doug Kass · May 16, 2025, 8:56 AM EDT

Premarket percentage movers at 8:18 a.m. ET:

BY Doug Kass · May 16, 2025, 8:27 AM EDT

Well here is another big AI fail over at Meta META.

Who woulda thunk it's not working and not scaling? In fact, it almost seems to be going backwards with more complexity and more processing power.

These guys, Apple AAPL, heck all of em. Open AI’s new models just all seem more expensive and no better, if not worse at certain things:

Meta Stumbles: Delays Release Of Flagship "Behemoth" AI Model Over Performance Concerns

The funny thing about Meta is their head of AI, Yann LeCun, is on record as not even believing Gen AI will work, but it seems like Zuck keeps making them spend on it anyway (and it seems to be going about as well as the Metaverse). Then every time Meta reports their quarters, they keep raising their theoretical CAPEX guidance, but then substantially underspending the numbers, which tells you something.

Then on a more practical note, second link is on Klarna, going back to humans from AI bots for customer service, because the AI sucks and makes things worse and not better.

The article makes an important point that: Companies are using AI NOT because it increases productivity or is better for their customers, they are using AI because they think they have to because they think everyone else is doing it too. Slowly but surely, they are all figuring out it is not working, and business necessity causes them to eventually go back to doing it the old-fashioned way, with real people. So much for the AI productivity miracle! The illusion only lasts so long, and executives only chase for so long. Heck, even Microsoft MSFT seems to be somewhat giving up and prefers to just host the back end for customers that want to burn money on this stuff!

If Klarna was smart, they would have done buy now, pay later, for their AI investment, and then not paid, because it didn’t work! But the way the world is now, maybe Nvidia will start using Klarna so Nvidia’s customers can do buy now pay later for their chips, instead of Nvidia having to fund their customers directly? It really is never ending with this stuff.

I hate to tell the guys in Saudi Arabia, who are the latecomers to the party, this ain’t gonna be the miracle that solves their problems. They would be better off using the money to drill for more oil if you ask me. At least oil does what it is supposed to do, and it is a super high ROI investment for them as well.

"After years of depicting Klarna as an AI-first company, the fintech’s CEO reversed himself, telling Bloomberg the company was once again recruiting humans after the AI approach led to “lower quality.” An IBM survey reveals this is a common occurrence for AI use in business, where just 1 in 4 projects delivers the return it promised and even fewer are scaled up. The apparent turnaround comes after years in which Klarna touted its all-in-on-AI strategy. A year ago, Klarna said that its chatbot, powered by OpenAI, does the work of 700 human agents and does it much faster. In December, the company revealed that it had hired no human workers for the previous year, with the CEO boasting that “people internally at Klarna are just rallying to deploy as much efficiency AI as they can.” “I am of the opinion that AI can already do all of the jobs that we, as humans, do,” the CEO told Bloomberg in February. It now seems that, while chatbots are cheaper, they’re just not as good as humans for some jobs, according to Siemiatkowski.

As cost unfortunately seems to have been a too predominant evaluation factor when organizing this, what you end up having is lower quality,” he told Bloomberg this week. “Really investing in the quality of the human support is the way of the future for us.”

Despite this dismal success rate, companies are going all-in on AI, driven largely by the belief that everyone else is doing it. Nearly two-thirds of CEOs (64%) say “the risk of falling behind drives them to invest in some technologies before they have a clear understanding of the value they bring to the organization,” according to the study."

BY Doug Kass · May 16, 2025, 7:45 AM EDT

BY Doug Kass · May 16, 2025, 6:40 AM EDT

This chart has been the basis for my housing concerns over the last few months:

BY Doug Kass · May 16, 2025, 6:15 AM EDT

BY Doug Kass · May 16, 2025, 6:05 AM EDT

First time, long time:

I shorted Nvidia NVDA at $135.75.

More Tales From Nvidia coming shorrly.

BY Doug Kass · May 16, 2025, 5:54 AM EDT

The S&P Short Range Oscillator remains overbought at 5.77% vs. 5.16%.

BY Doug Kass · May 16, 2025, 5:34 AM EDT