Thursday's After-Hours Movers

At 4:24 p.m.:

BY Doug Kass · May 15, 2025, 4:45 PM EDT

At 4:24 p.m.:

BY Doug Kass · May 15, 2025, 4:45 PM EDT

- NYSE volume 1% below its one-month average;

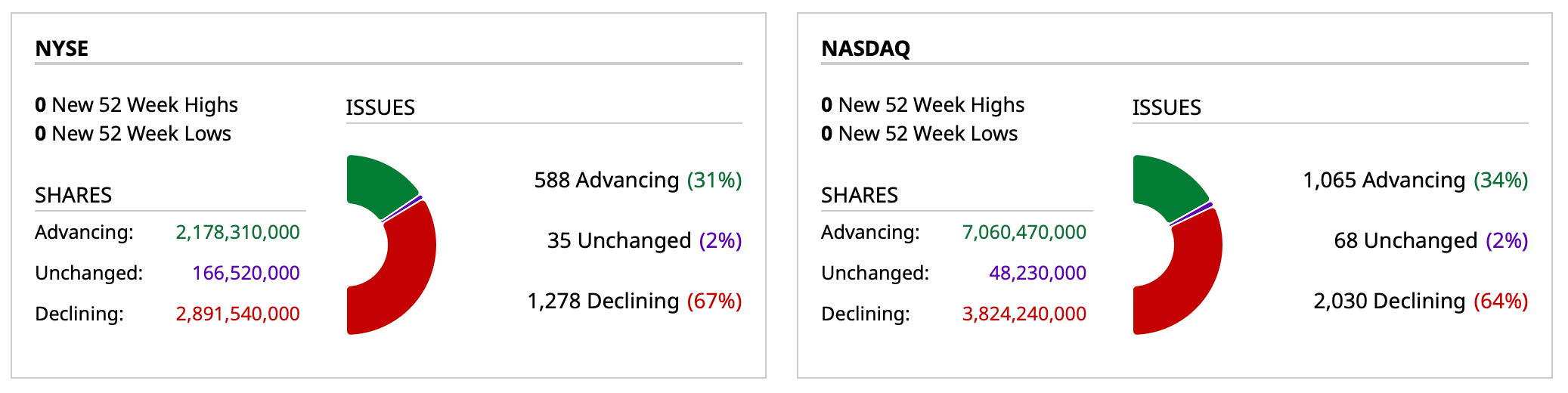

- NASDAQ volume 27% above its one-month average;

- VIX index: down 4.35% to 17.81

BY Doug Kass · May 15, 2025, 4:28 PM EDT

BY Doug Kass · May 15, 2025, 3:55 PM EDT

BY Doug Kass · May 15, 2025, 3:03 PM EDT

Another tranche of shorting the indices (though I still remain small-sized):

* SPY $590.11

* QQQ $521.11

BY Doug Kass · May 15, 2025, 2:07 PM EDT

I added to my GRNY short at $20.95 just now.

BY Doug Kass · May 15, 2025, 1:37 PM EDT

- NYSE volume 2% below its one-month average;

- Nasdaq volume 39% above its one-month average;

- VIX: up 0.43% to 18.70

BY Doug Kass · May 15, 2025, 11:45 AM EDT

From Peter Boockvar:

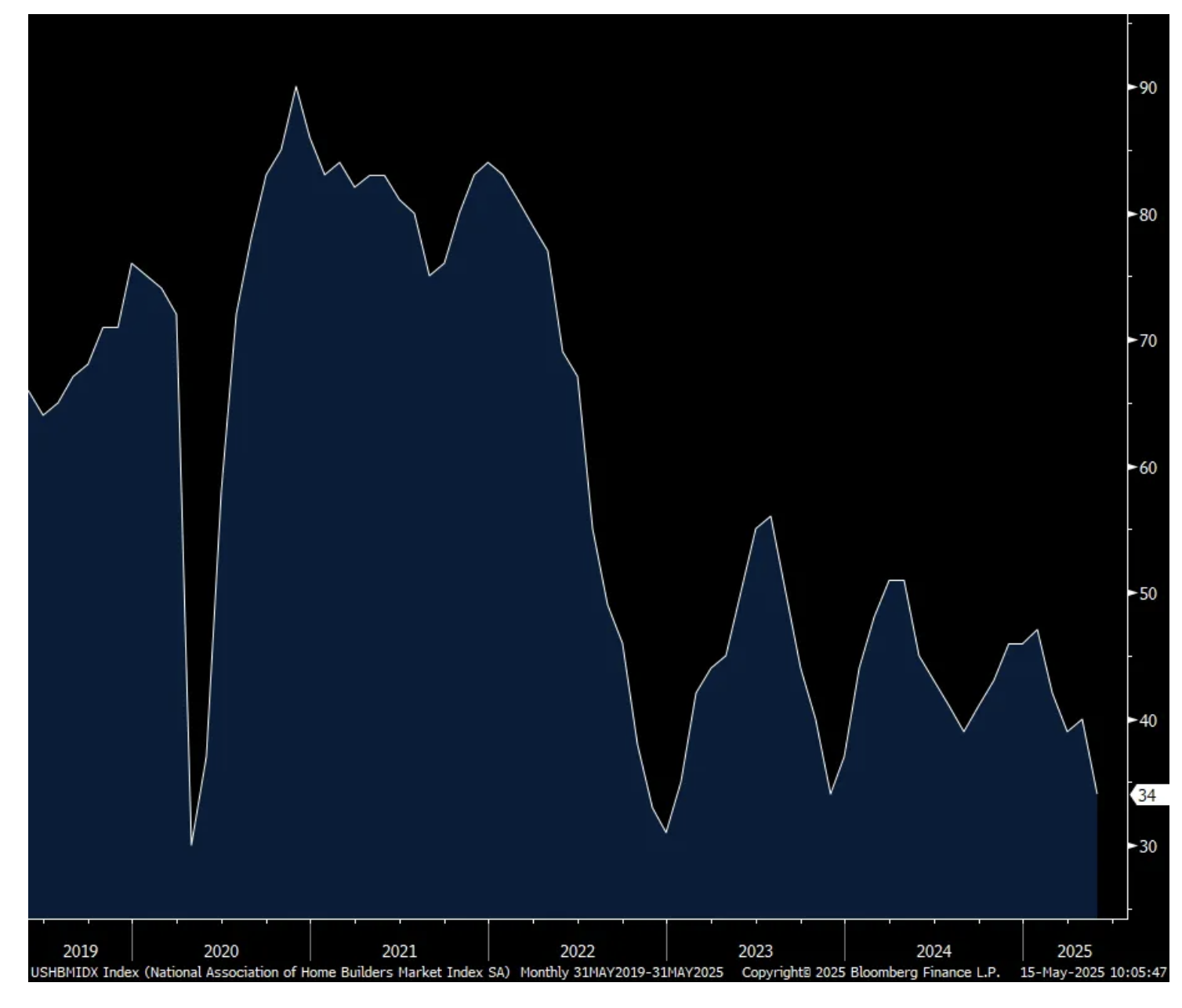

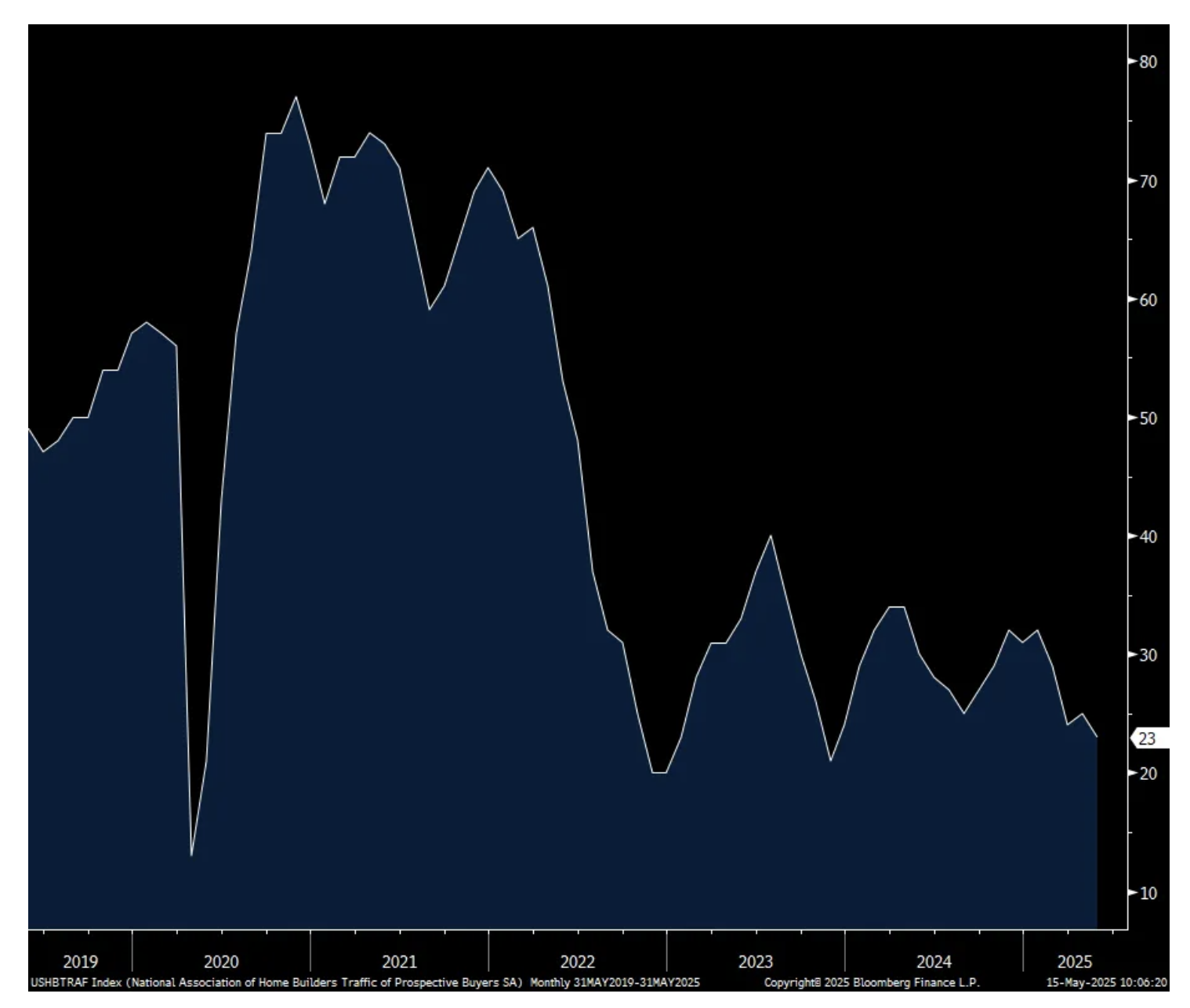

The NAHB May builder sentiment index dropped a sharp 6 pts to 34 from 40, well under the estimate of no change and matches the weakest since December 2022. Most of the decline came in the Present Situation which declined by 8 pts while Expectations were down 1 pt to 42. Prospective Buyers Traffic remains depressed and a bit more so at 23 vs 25, so less than half the breakeven of 50.

The problem in housing remains both a supply and demand issue. The NAHB said “The spring home buying season has gotten off to a slow start as persistent elevated interest rates, policy uncertainty and building material costs factors hurt builder sentiment in May.” Also, “the overall actions on tariffs in recent weeks have had a negative impact on builders, as 78% reported difficulties pricing their homes recently due to uncertainty around material prices.”

This data came before the China tariff pause/deep breath though.

What are builders doing to push sales? “The survey “revealed that 34% of builders cut home prices in May, up from 29% in April and the highest level since December 2023 (36%). Meanwhile, the average price reduction was 5% in May, unchanged from the previous month. The use of sales incentives was 61% in May, the same rate as the previous month.”

Bottom line, the higher cost of delivering a home, in part due to tariffs on the key materials of steel, lumber and aluminum and minimum of 10% on anything else imported that goes into the building of a home doesn’t mesh well when buyers are still challenged by expensive homes and high mortgage rates.

NAHB

Prospective Buyers Traffic

BY Doug Kass · May 15, 2025, 11:30 AM EDT

For the second day in a row the breadth (on both the NYSE and Nasdaq) are 2-1 negative — though the indices have exhibited very little change.

As someone expanding short exposure into this deteriortating breadth backdrop, I have to admit to being very frustrated.

BY Doug Kass · May 15, 2025, 11:22 AM EDT

skeptcl

11 minutes ago

Color on CRWV this morning from TMTB: Key takeaways:

• Demand picture: management is seeing “broad-based acceleration” in inference workloads as enterprises move from experimentation to production, while training demand remains robust. No macro slowdown despite geopolitical noise; tariff-related cost pressure called “marginal.”

• Deal momentum: new $11.2 billion OpenAI contract (accounting keeps it out of RPO for now) and $4 billion expansion with a large AI enterprise signed early 2Q; an additional hyperscaler logo joined the platform. These wins pushed contracted power to 1.6 GW (+300 MW q/q).

• CapEx ramps hard from here: FY-25 spend raised to $20-23 billion (~ +17 % vs Street), with $3-3.5 billion slated for 2Q, as CoreWeave pulls forward Blackwell deployments and data-center build-outs to meet demand…CapEx will materially be financed with debt which will also increase interest expense.

• Margins: interest-expense step-up and IPO-related G&A drove the EPS miss; management flagged further margin dilution near term as opex and interest scale ahead of revenue. • Leverage (including leases) sits near 5× but is expected to climb with the debt-financed CapEx surge.

skeptcl

10 minutes ago

A little something for both the bulls and bears although this print won’t change many minds…Bulls will say CRWV is the pure-play AI hyperscaler—able to stand up large GPU clusters faster than hyperscalers, now layering acquired software on top of best-of-breed infrastructure. They point to unprecedented backlog visibility, accelerating inference demand, first-mover scale in Blackwell, and a path to expanding ROIC as deployed power catches up to spend.

Bears counter that the model is capital-intensive and increasingly leveraged, with margins pressured by skyrocketing interest expense and front-loaded opex (that is: higher interest expense lower than ROA). Customer concentration (OpenAI/Microsoft-linked) and the risk that hyperscalers insource inference, or custom ASICs erode GPU demand, could flatten growth just as debt peaks. RPO nuances and weaker cash conversion raise questions on revenue quality, and the stock already trades at premium.

Morgan Stanley sums up the quarter well: CoreWeave's first quarter out of the gate "gave new talking points to both the bulls and bears," as the company responds to an "acceleration of customer to demand" with a faster pace of build out of their GenAI infrastructure, Keith Weiss wrote. While accelerated build-out enabled a large revenue beat in Q1, it also increases interest expense and capex expectations for FY25, pressuring near-term free cash flow, says the analyst, who calls CoreWeave "a solid [long-term] play on an emerging GPU economy."

BY Doug Kass · May 15, 2025, 11:15 AM EDT

BY Doug Kass · May 15, 2025, 11:00 AM EDT

Doug Kass

STAFF

51 minutes ago

BABA is another example of a stock with great momentum -- that traders bought solely based on the strength of the chart..

Disappointing earnings per share overnight, and now -$11.

A bunch on our site (and on the shows) were moved to buy BABA this week based on the move from the lower left to the upper right.

Will be interested to see if they buy more or punt.

To me, chasing to the upside and to the downside is a fool's errand as I mentioned in my Rethinking American Exceptionalism column yesterday.

BY Doug Kass · May 15, 2025, 10:35 AM EDT

From Peter Boockvar:

Core retail sales in April fell by .2% m/o/m instead of rising by .3% as forecasted and only slightly offset by a one tenth upward revision to March. Not included here were auto sales that after spiking by 5.5% in March due to the pull forward, was flattish m/o/m in April. Building materials rose for a 2nd month after 4 months of declines and by .8% m/o/m.

On the necessity side, food/beverage sales were unchanged while health/personal care was down though after jumps in the prior two months and are up 8.8% y/o/y.

On the discretionary side, not knowing to what extent we saw pull forward behavior, furniture and electronic sales each rose .3% m/o/m. As for the latter, I know first hand people that were buying their new iPhones and upgrading computers ahead of possible price increases. Clothing sales along with sporting goods each fell after jumping in the month before. Online sales were little changed for a 2nd month, by .2% and I wonder if reduced sales of Temu and Shein products are one reason due to the end of de-minimus exemptions and the tariffs. Sales at restaurants/bars continued to be good, rising by 1.2% and by 6.9% y/o/y.

Bottom line, outside of the noted auto buying pull forward where we heard that from auto dealerships, it’s hard to know exactly the extent we saw that in April. I will say though after hearing from a slew of company earnings, the US consumer remains circumspect with their spend, even some on the upper end.

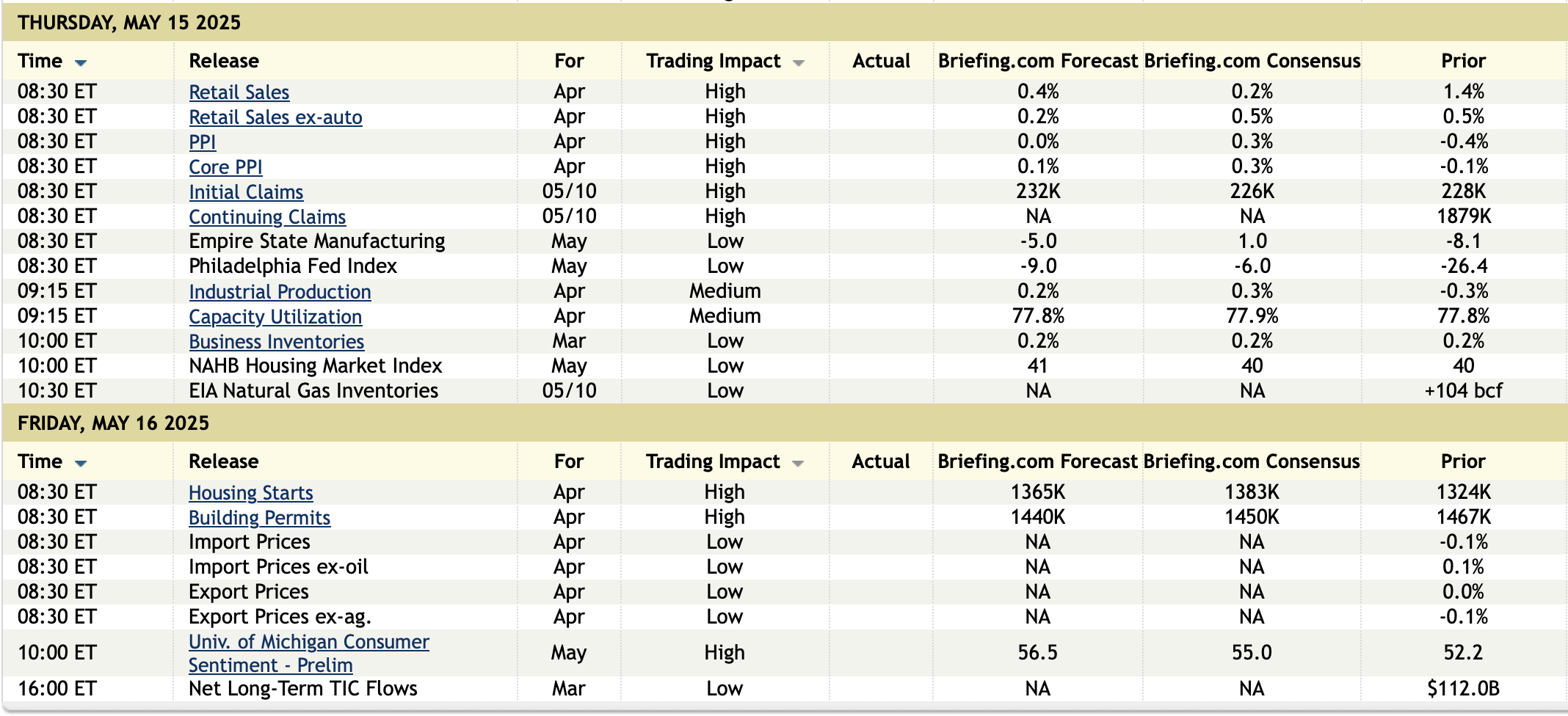

Initial jobless claims were about as expected at 229k, no change from the prior week and staying low. The 4 week average did tick up to 231k from 227k as a print of 216k dropped out. Continuing claims totaled 1.881mm and are staying elevated though. The bottom line here remains the same.

The April PPI unexpectedly fell by .5% m/o/m vs the estimate of up .2% with much offset by an upward revision of 4 tenths to the March read to flat from down .4%. The core rate was lower by 4 tenths vs the forecast of up .3% while March was revised up by 5 tenths.

On the goods side, ex food and energy saw prices up by .4% m/o/m and 2.5% y/o/y and continues to point to signs of bottoming goods prices and the first initial signs of tariff induced inflation, whether one time or not. Leading this was a 1.1% rise in ‘general purpose machinery and equipment.’ On the flip side ‘chicken eggs’ prices plunged by 39%.

Services deflation was the lid on PPI as they fell by .7% m/o/m because of a 1.6% drop in trade prices and .4% decline in transportation/warehousing. The BLS said “Over 40% of the April decline in the index for final demand services is attributable to margins for machinery and vehicle wholesaling, which dropped 6.1%.” Prices fell too for “portfolio management, food and alcohol wholesaling, system software publishing, traveler accommodation services and airline passenger services.”

On the shipping side, and likely not fully reflecting the 90 day April 9th tariff pause and certainly not the China one, air shipment costs jumped by 4.1% m/o/m while falling by .2% for trucking and rising by one tenth for rail. Container shipping prices as seen in my morning note are already spiking.

Bottom line, as stated I point to the core goods price rise of .4% m/o/m and 2.5% as maybe the first sign of tariff induced price inflation.

As seen in the May NY and Philly industrial surveys, the manufacturing recession continued on. The NY index was -9.2 vs -8.1 in the prior month. The Philly index was -4 vs -26.4 in April.

In NY, prices paid rose another 8 pts to 59, the highest since July 2022 but those received gave back the April rise of 6.3 pts. New orders did rebound after the past two months of declines. Employment stayed negative.

As for the 6 month outlook, it remained below zero for a 2nd month and capital spending plans went negative for the first time in a while.

In the Philly index, there was a further rise in both prices paid and received to multi year highs and new orders were positive too. Employment rose in contrast to NY.

Likely in response to the China news, the 6 month outlook skyrocketed to 47.2 from 6.9 and CapEx plans rose too.

Bottom line, these figures are so volatile month to month and everything is swinging around based on the tariff situation. Either way, it seems that the manufacturing challenges continue on.

BY Doug Kass · May 15, 2025, 10:20 AM EDT

From Peter Boockvar:

That Bloomberg News story yesterday saying that the US wants to integrate a lower dollar in the talks with South Korea was informally denied late yesterday. Bloomberg followed its original story by saying "US officials seeking to negotiate trade deals around the world are not working to include currency policy pledges in the agreements, according to a person familiar with the matter."

"After taking part in trade talks with China last weekend, Bessent said 'there was no discussion on currency' with the Beijing delegation. What's happening behind closed doors in various trade negotiations is in line with these positions, according to the person, who spoke on anonymity to discuss sensitive matters. The administration wants partners to abstain from unfairly manipulating their currencies lower, but there's no plan to mention such policy in any upcoming deals that could lower some of Trump's initial tariffs, the person said."

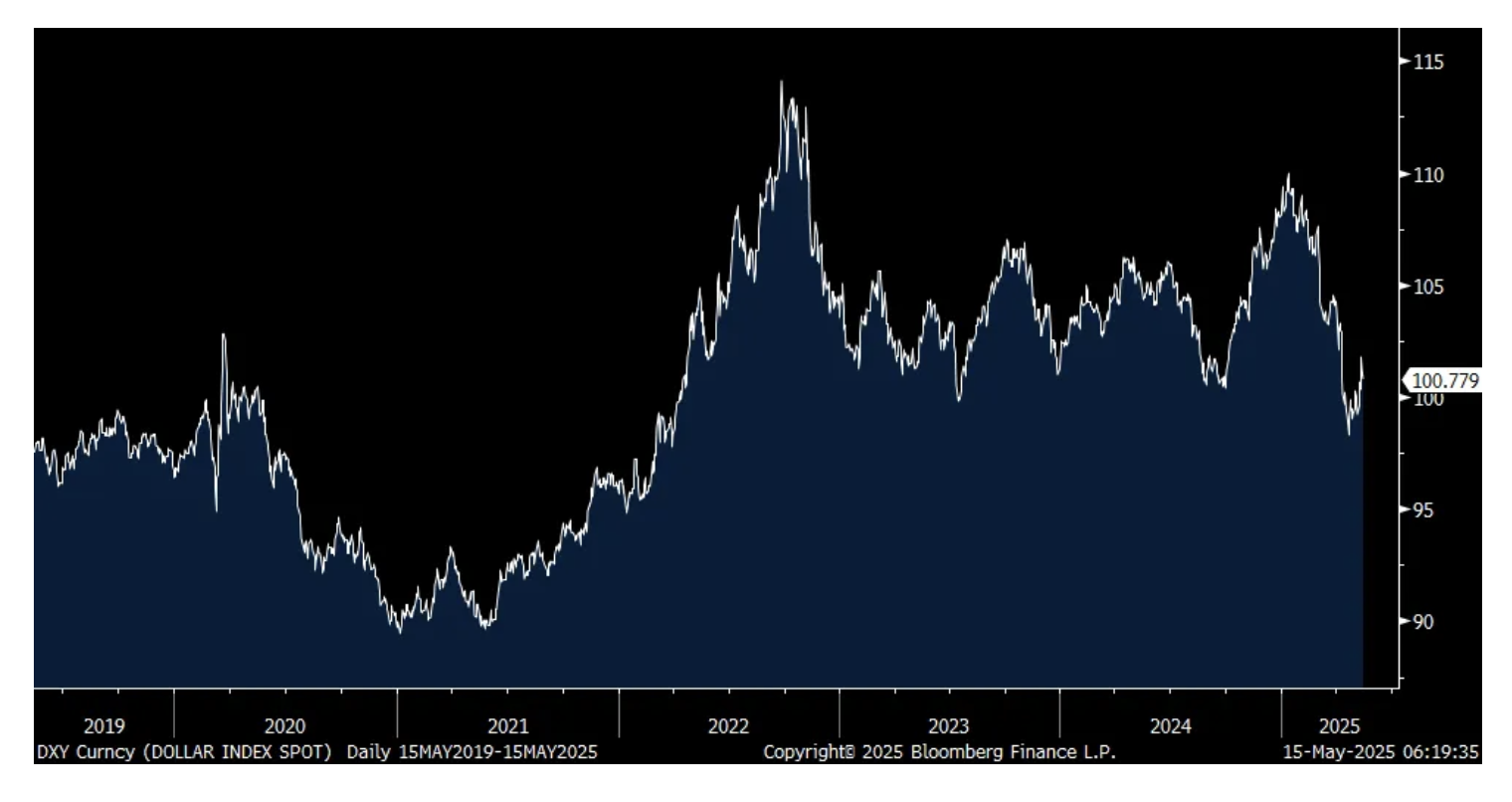

I wonder who this 'person' is but the direction of the US dollar is going to be more driven by foreign flows and they are seemingly exiting stage left to some degree and why I believe the dollar has been weaker and is again today notwithstanding the denial. And by the way, the Federal Reserve over the past few decades via QE, zero rates, etc... Is a grand manipulator too of the US dollar.

DXY

I'm sure it's clear that from my writings I'm not a fan of tariffs so I'm going to continue to point out the unintended consequences of them. In case you didn't see this article in yesterday's FT, "Scrapping of Texas power plant projects places $5bn scheme at risk." It said, "Companies have abandoned almost half the projects in a $5bn Texas program to fund gas power plant construction and prevent more electricity blackouts, as they struggle with ballooning expenses and supply chain delays."

To quantify, "Eight projects, including those backed by Constellation Energy and France's Engie, have been canceled or withdrawn from the state backed scheme to beef up energy supplies in Texas, which was hit by a brutal blackout in 2021. The companies blamed rising expenses, delays getting parts and uncertain revenue for their exits."

We can count all the dollars that flow into the US via 'deals' and any reshoring but we're also creating a higher cost structure in doing business in the US and should start counting what doesn't get done because of that, what business is lost because of that, and what businesses are getting hurt because of that. Lower taxes, deregulation, the easing of permitting, etc...would have been a much more effective way of lowering the cost base of US companies to encourage more production domestically and better position US companies for exporting rather than raising the cost of imports. https://ft.pressreader.com/v99e/20250514/281638196101385

Bullish sentiment continues to creep back into the markets with the pretty violent rally over the past month. Investors Intelligence yesterday said Bulls rose back above the level of Bears at 35.8 vs 32.1 last week. Bears fell to 30.2 from 33.9. The CNN Fear/Greed index closed at 70 vs 3 at the bottom. In the very volatile and fickle AAII survey, Bears still dominate but less so. They fell by 7.1 pts to 44.4 which is the least since early February while Bulls rose by 6.5 pts to 35.9, the most since late January.

Bottom line, nothing extreme here but note the typical human nature behavior as AGAIN, people get most afraid at the lows and most excited at the highs.

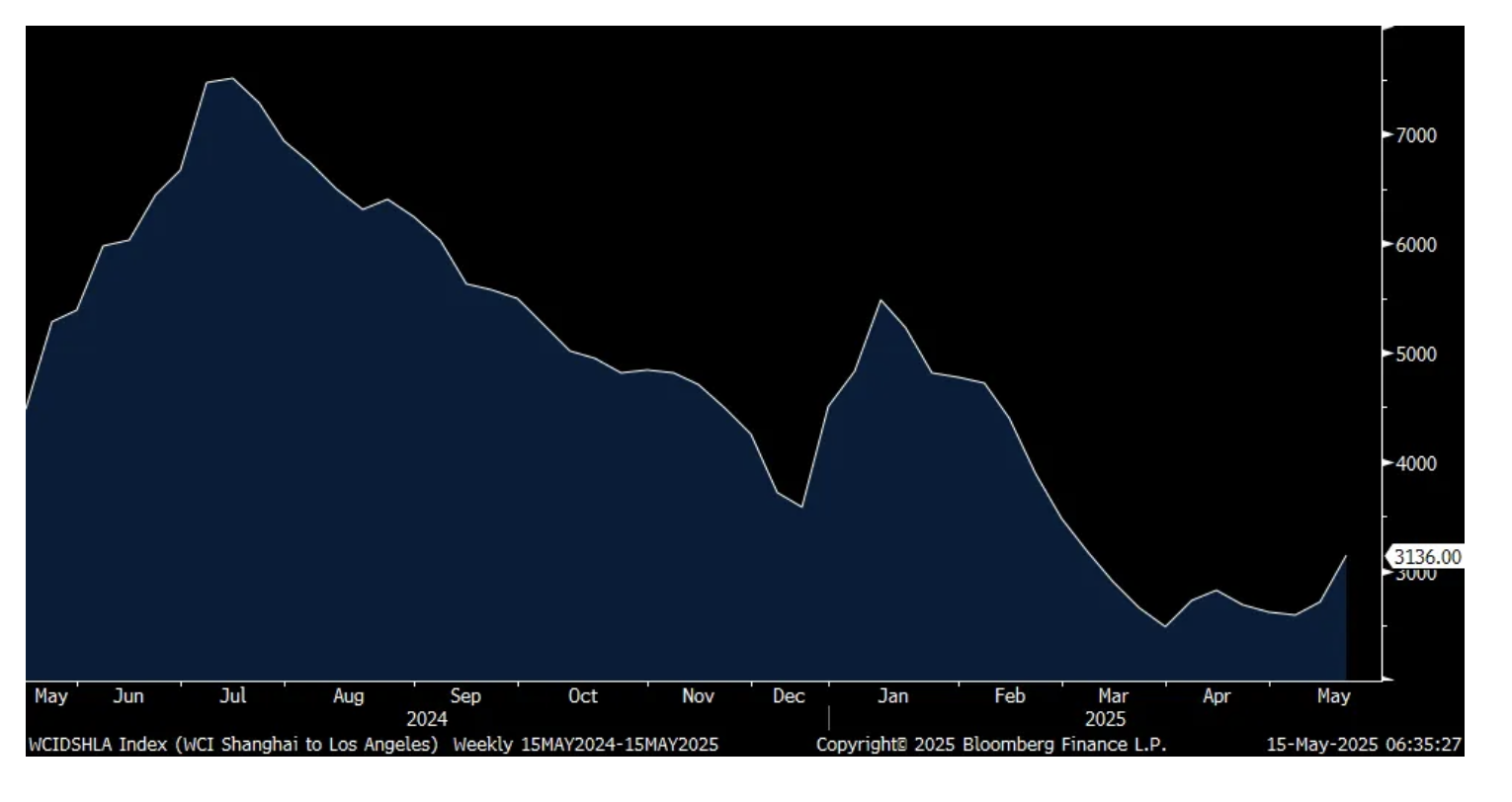

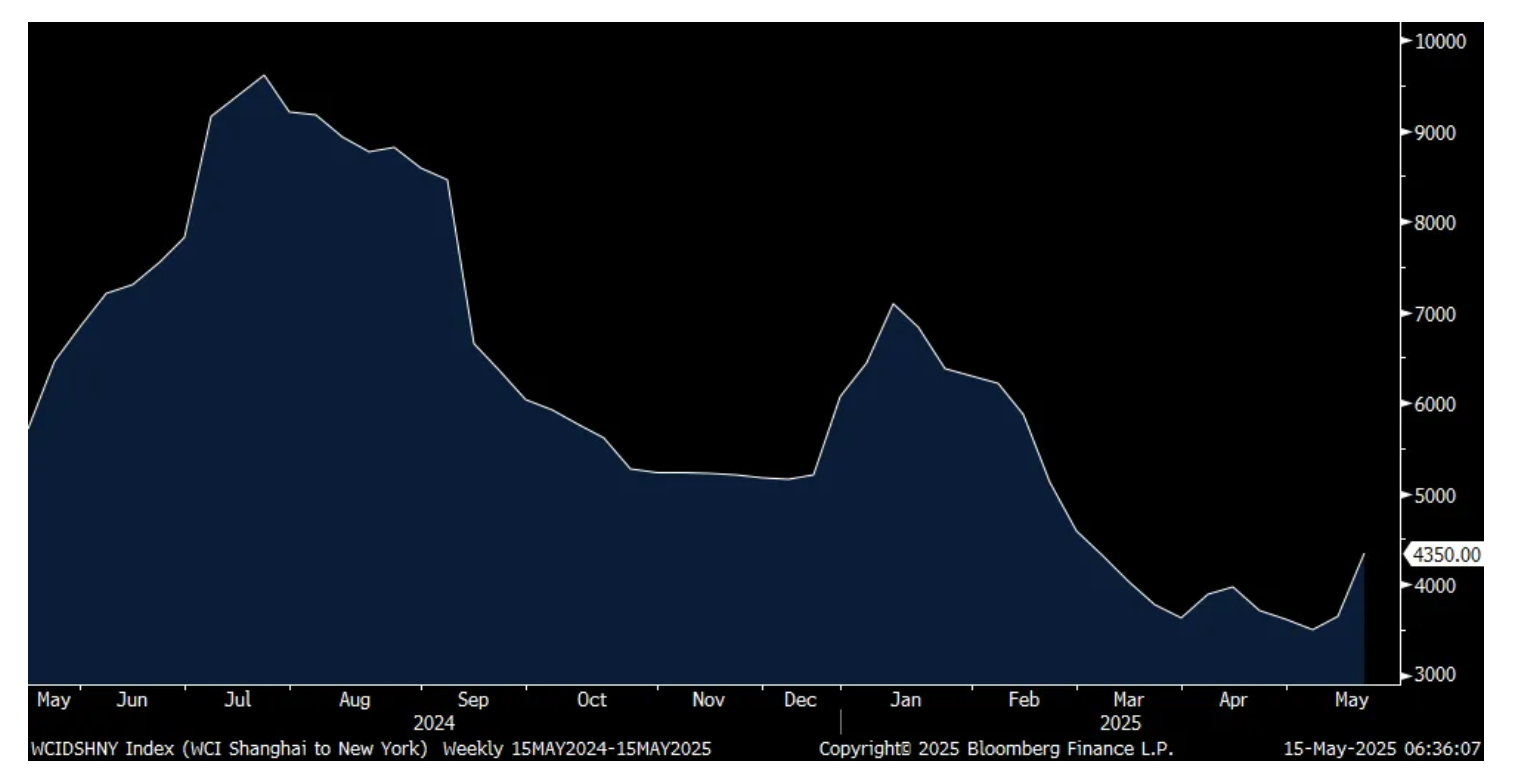

We now have the initial reaction to the US/China trade fight detente in terms of shipping costs and the rush to get stuff. The World Container Index for a 40 ft container saw the Shanghai to LA price rise by 16% w/o/w, by $423 in absolute dollars, to $3,136. That's the highest since early March. The trip from Shanghai to NY jumped 19%, by $704 to $4,350, the highest since late February. Expect further increases in the coming weeks.

WCI Shanghai to LA

WCI Shanghai to NY

Sorry for the delay in going thru this important earnings conference call from ZipRecruiter from a week ago as it's always a good tell on the US labor market.

"While we've yet to see a pronounced pullback in employer hiring, we are also not seeing an acceleration in hiring activity as we enter the 2nd quarter." Revenue fell 10% y/o/y and by 1% q/o/q.

"while the bounds of uncertainty on the macro are increasing, what is true today is that our internal data shows that employers have not yet pulled back. So employer hiring activity is consistent with the trends that we observed coming into 2025. That informs both the quarterly guidance that we provided you as well as the outlook of achieving y/o/y growth in Q4 of 2025. We are watching closely."

To a question of what they are hearing from small and medium sized businesses (SMBs) and other clients, "what we hear from them consistently when it comes to hiring decisions as well as CapEx and other major investment decisions is that certainty is what helps them. So understanding what the rules of the road are and having confidence those will remain the rules of the road for quarters and years to come is what we hear them talking about. We've definitely noticed a change over the past few months in the tenor of some of those conversations as they talk about what they expect in the future. But their behavior has been consistent with what we talked about last quarter."

I'll add, with the experience of Covid and the difficulty bringing back employees and keeping them, I do expect still a muted pace of firings (notwithstanding news that we heard this week from Microsoft laying off 3% of their entire workforce) until the trade deals and ultimate tariff rates are determined but no doubt expect a continued slowdown in hiring's. That said, I've heard about too many small businesses that have cut workers in response to the tariff war particularly with China.

From Jack in the Box:

"It's well known that there is significant pressure on multiple income cohorts, and we've seen the results in our negative traffic. There are definitely more headwinds than tailwinds at the moment for most within our industry." Their comps fell 4.4% y/o/y for the Jack brand and by 3.6% for Del Taco.

From Boot Barn, a maker of cowboy boots, work boots (like to the oil & gas industry and ag), etc...and who had a good quarter:

"Turning to current business. We are now six weeks into the first quarter of fiscal '26, and we have continued to see broad based growth as consolidated same store sales increased 9%, driven by increased transactions and full price selling. While we are pleased to see the strong trend of the business continue into fiscal '26, we recognize the ongoing uncertainty with respect to tariffs." They do source from China but much less so over the past 5 yrs and have plans to continue to diversify supply chains.

Tariffs are though going to result in a 5% price increase vs the usual 2% or 3% they said and "We expect to see some elasticity of demand and some softening of demand, and that's what we've embedded in with a flat comp in the third quarter and fourth quarter."

Cisco had a good quarter helped by its AI infrastructure business. "Despite the uncertain macro environment, this demonstrates the valuable outcomes we are delivering for customers in the era of AI."

On what they are seeing in terms of spending behavior from their customers, "we haven't seen any meaningful change in how they're purchasing. And so we haven't seen any customers really fundamentally slowing down. They're still committed to the technology transition. I think the AI transition is just so important that they're going to continue to spin until they just absolutely have to stop. And I think that as of right now, they're still comfortable."

"As it relates to pull-forwards, look, I think I'm sure there was an order here and there from a customer who decided to pull something forward because they were concerned about tariffs, but we looked at a ton of data points to see if we saw any signs of broad based pull ahead business, and we did not." I'll guess we'll now for sure next quarter.

From the Walmart press release where they beat bottom line estimate but missed top line:

Walmart US: "sales strength led by health & wellness and grocery; seasonal events were strong; grocery share gains continued...Comp sales momentum reflects higher transaction counts and unit volumes; strong growth in eCommerce."

As for guidance, "Given the dynamic nature of the backdrop, and the range of near-term outcomes being exceedingly wide and difficult to predict, we felt it best to hold from providing a specific range of guidance for operating income growth and EPS for the 2nd quarter."

Walmart I believe sources about 70% of their goods from China and the CFO told CNBC that tariffs are "still too high" at 30%. And, "We're wired for everyday low prices, but the magnitude of these increases is more than any retailer can absorb. It's more than any supplier can absorb. And so I'm concerned that the consumer is going to start seeing higher prices. You'll begin to see that, likely towards the tail end of this month, and then certainly much more in June." I bolded for emphasis.

Overseas, the UK economy grew by .7% q/o/q which was one tenth above the estimate and by 1.3% y/o/y. The service sector again led the way but there was definitely pull forward type behavior as exports and imports both jumped much more than anticipated. As it's old news, nothing market moving though.

BY Doug Kass · May 15, 2025, 9:50 AM EDT

Added to Index shorts after the opening:

* SPY $586.33

* QQQ $516.95

BY Doug Kass · May 15, 2025, 9:45 AM EDT

BY Doug Kass · May 15, 2025, 9:35 AM EDT

* The equity risk premium is ever more thin - providing a potential headwind to equities after the spectacular stock market run

This morning the bond market tried to rally.

That rally fell flat and TLT is now down on the day as yields reverse higher.

In the last few weeks the yield on the ten year Treasury has risen by +31 basis points and the 30 year yield has increased by +41 basis points.

Result: The equity risk premium has grown even more paper thin (as yields rise and S&P earnings per share forecast decline (see Walmart's WMT effective lowering of next three quarters in this morning's EPS release -- its shares are now -$4 from the premarket high).

For now momentum has favored the bold and the bulls in a market dominated by passive products and strategies that worship at the altar of price momentum.

But FOMO ("fear of missing out") can last so long under these economic, profit and interest rate settings.

Interest rates, in particular, are fundamental to all valuation models for the equity markets. And, as noted, they are climbing.

I am expanding my short exposure in the rally in futures (now down by only -12 handles).

BY Doug Kass · May 15, 2025, 9:30 AM EDT

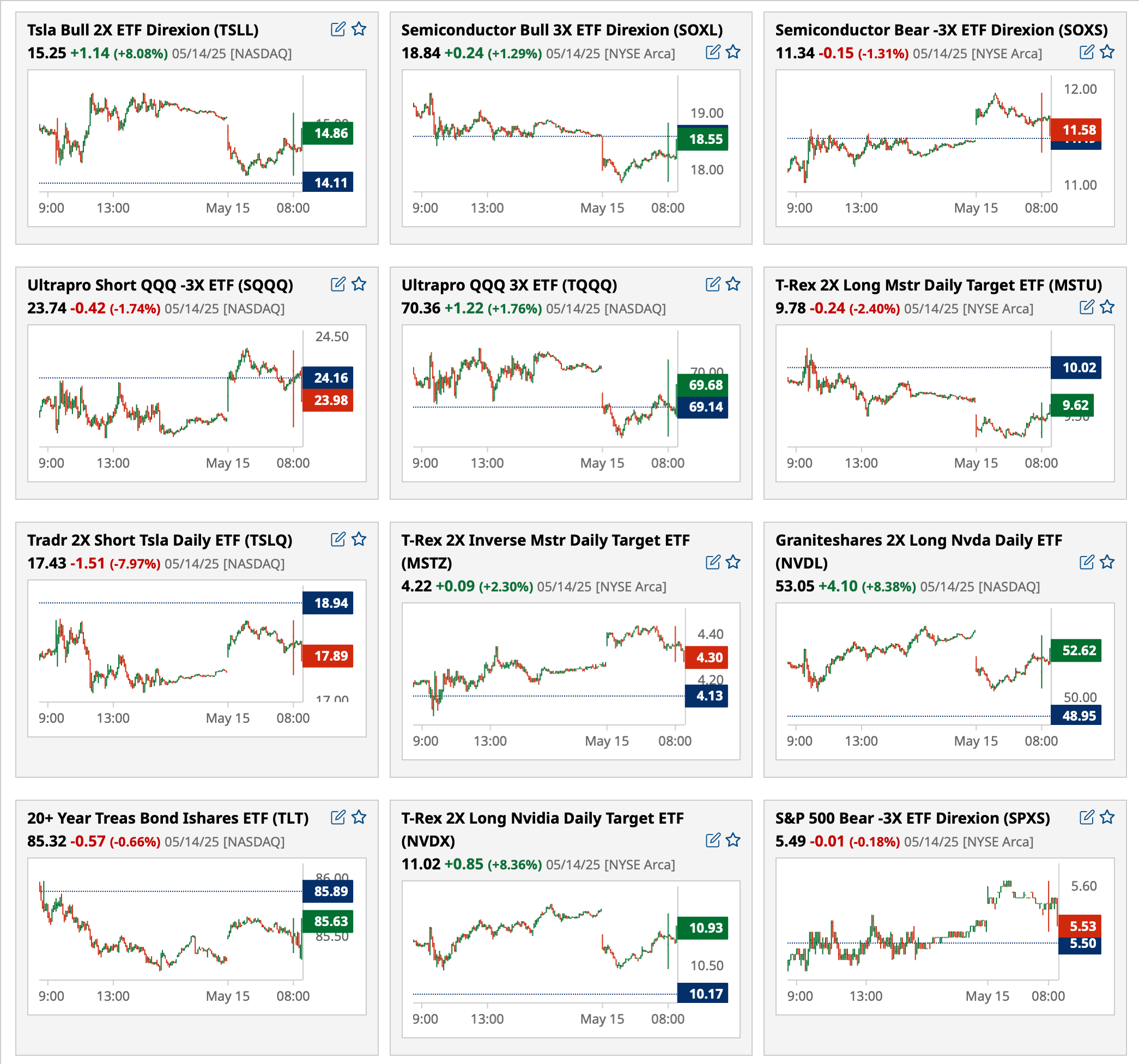

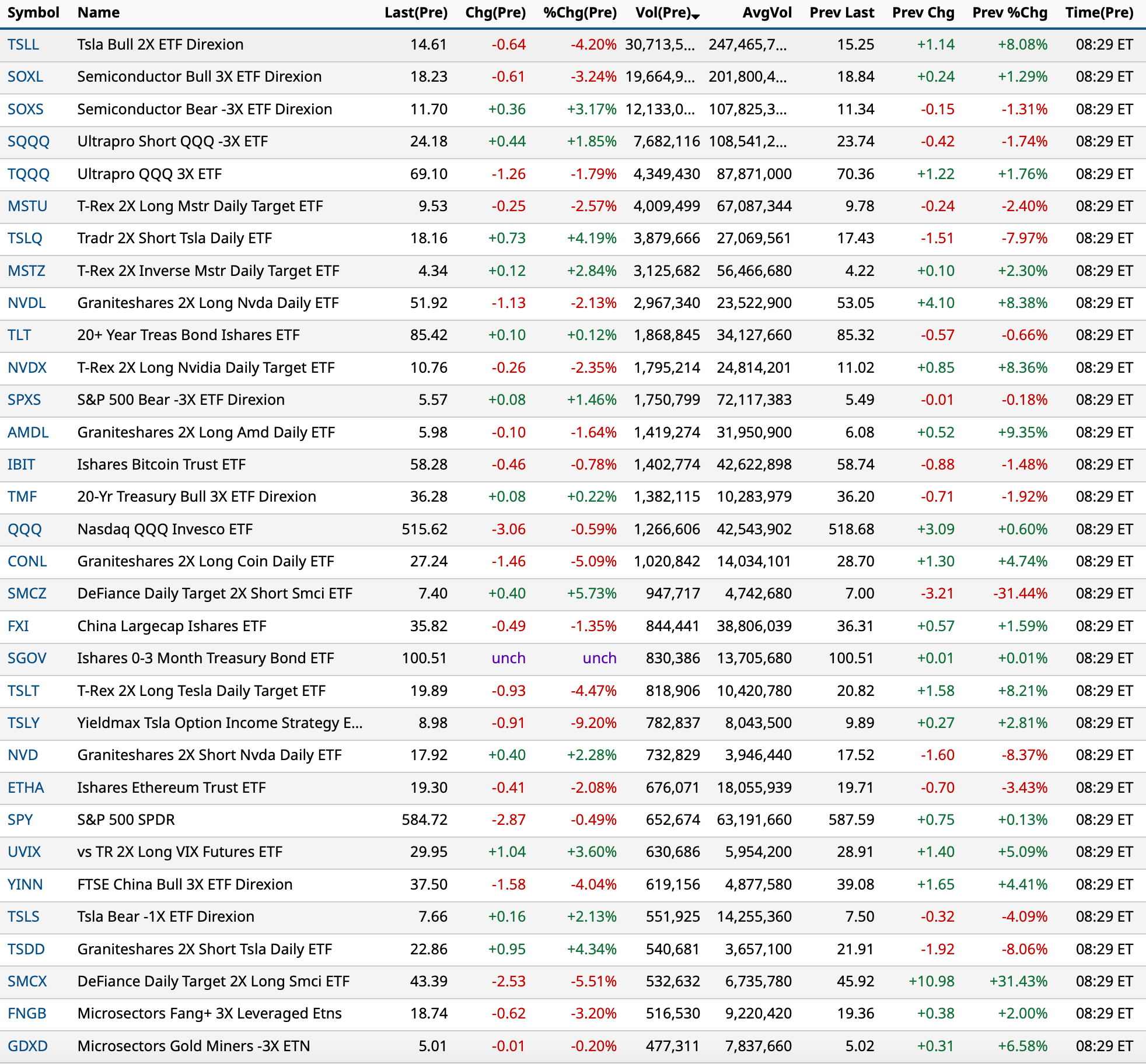

Most active premarket ETFs as of 8:29 a.m. ET:

BY Doug Kass · May 15, 2025, 9:20 AM EDT

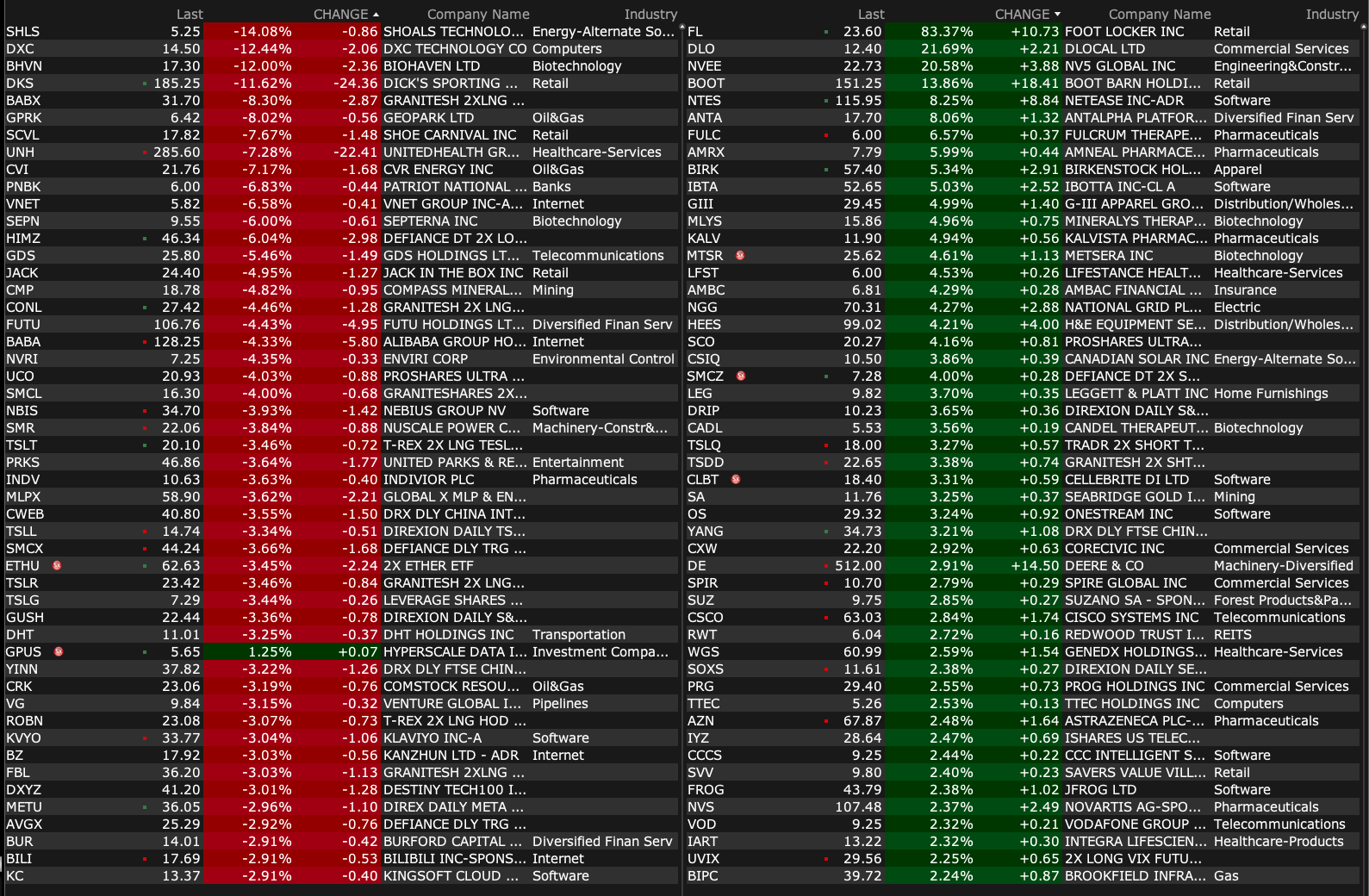

Premarket percentage movers at 8:48 a.m. ET:

BY Doug Kass · May 15, 2025, 9:10 AM EDT

-FL +83% (confirms to be acquired by DICK'S Sporting Goods in ~$2.4B deal; reports prelim Q1)

-AYTU +40% (earnings)

-ISSC +26% (earnings)

-CREV +25% (earnings)

-DLO +23% (earnings)

-TOI +20% (earnings, guidance)

-BNGO +14% (earnings, guidance)

-BOOT +13% (earnings, guidance)

-ICU +8.1% (earnings)

-ATRA +6.1% (earnings; prices 834K common stock shares at $6.61/shr and 1.59M pre-funded warrants at $6.6099/shr)

-CSIQ +5.2% (earnings, guidance)

-IBTA +5.0% (earnings, guidance)

-VXRT +5.0% (earnings; receives BARDA Approval to Initiate Dosing in 10,000-Participant Portion of Phase 2b COVID-19 Trial)

-BIRK +4.7% (earnings, guidance)

-CSCO +2.4% (earnings, guidance)

-NFE -38% (earnings)

-DXC -13% (earnings, guidance)

-DKS -11% (to acquire FL in ~$2.4B deal; reports prelim Q1)

-RCAT -11% (earnings)

-CDXS -9.3% (earnings, guidance)

-REKR -7.9% (earnings)

-JACK -6.0% (earnings, guidance)

-CTXR -5.1% (earnings)

-CRWV -4.8% (earnings, guidance)

-IREN -2.4% (earnings)

BY Doug Kass · May 15, 2025, 9:00 AM EDT

8:40 a.m.: Fed Board President Powell speaks on "Framework Review" before the Thomas Laubach Research Conference, Washington, DC (Text available. No Q&A. Webcast;

2:05 p.m.: Fed Board Governor Barr (Voter) gives opening remarks before virtual 2025 Northeast/Mid-Atlantic Small Business Credit Symposium hosted by the Federal Reserve Banks of New York, Cleveland, Philadelphia, Boston and Richmond (Text available. No Q&A. Livestream.

BY Doug Kass · May 15, 2025, 8:51 AM EDT

I just covered my WMT trading short rental at $96.95 (shorted earlier this morning at $100.01) for a nice and quick profit.

BY Doug Kass · May 15, 2025, 8:24 AM EDT

From JPMorgan:

US: Futs are lower as investors take some profits. Pre-mkt, Mag7/Semis/Cyclicals are weaker; bond yields and USD are lower. Cmdtys are weaker, dragged by energy as US/Iran are said to be close to a deal. SPX failed at 5,900 for the second consecutive day. The silver lining is that, yesterday, NVDA turned positive on the year, joining META and MSFT; if the remaining members follow suit, there is another ~10% upside to the index assuming positive members are flat. YTD, AMZN is -4.2%, GOOG -12.6%, TSLA -13.9%, and AAPL -15.2%. China is removing curbs on rare earth exports to the US. Trump says India is willing to drop is tariffs on US goods. Today’s macro data focus is on Retail Sales where the risk/reward is skewed to the upside given recent credit card data (inflecting higher) and thawing of the trade war. Also, Powell speaks at 8.40am with Barr at 2.05p.

and...

EQUITY & MACRO NARRATIVE

The most popular question/discussion topic: Given the recent run, with NDX already back in a bull market SPX +18% from its April lows but now failing to break through 5,900 have we met the end of the recent run-up? Not yet. We think the core elements of the bull case remain intact (macro data resilience, positive earnings, and thawing trade war) but the speed of the recovery has made this one of the most hated rallies with the incremental buying coming primarily from the Retail investors and corporations. From here, we think a few things and happy to discuss in more detail:

· The May NFP print showed us that any tariff hit is unlikely to be seen in May prints. We may only see a partial impact in the June data, allowing for upside surprises.

· Retail Sales could miss tomorrow and still push markets higher as our credit card data and comments from Mastercard/Visa point to a strong consumer that may be inflecting higher as confidence is restored post-Trump’s trade war pullback.

· NVDA looms large and given the deals being signed in the Middle East this week, could we see a return to the earnings prints (really guidance) that generated a double-digit move?

· Seasonality, on a 10-year basis, is positive for June – July. Over the last 10 years, July has been the second strongest month, averaging 3.35% for the SPX with a 100% hit rate. June has been the fourth strongest month, averaging 1.15% with an 80% hit rate.

· We think more trade deals are coming with the biggest remaining, for those without a preliminary agreement, being Canada, EU, and Mexico. At this stage, it appears unlikely that the 90-day delay expires (July 8) without either another delay or some additional concession.

· We do think there is increasing risk of a pullback but think another correction is unlikely. Concentration risk will magnify fears of this pullback risk as this may be a market similar to 24H1, concentrated within MegaCap Tech. Ultimately, the SPX should make a run at ATHs (6,144) this quarter.

Another popular question/discussion topic: 10Y yield is back above 4.5%, does this create a headwind for stocks? Not exactly. My colleague John Schlegel has found that, in this post-COVID cycle, when the 10Y makes a new high, that it can take 1-2 months for stocks to digest and adjust. The cycle high is 5%, so we have some room. That said, the increase in yields should push investors into the highest quality names, most likely MegaCap Tech, while putting pressure on Staples and Utilities. Separately, Jay Barry increased his YE25 forecast for the 10Y to 4.35% up from 4.00% and he sees the 2Y yield at 3.50% up from 3.10% (full note is here). This increase in his yield forecast results from higher estimated real GDP growth and lower expected inflation; resulting in a delayed easing cycle that is shallower.

BY Doug Kass · May 15, 2025, 7:55 AM EDT

Adding to index shorts:

* SPY $585.39

* QQQ $516.25

Shorted WMT $100.01 (See Comments Section)

BY Doug Kass · May 15, 2025, 7:40 AM EDT

BY Doug Kass · May 15, 2025, 7:25 AM EDT

Bonus - Here are some great links:

Bullish Breadth Thrust Implies More Gains

BY Doug Kass · May 15, 2025, 6:55 AM EDT

With S&P futures -31 handles, this observation by myself and Helene from yesterday may have proven prescient:

* The junior averages are underperforming the senior averages...

This morning I touched on my view (and The Divine Ms M's (see below) that the underperformance of (RSP) (equal weighted S&P) and (IWM) (Russell index) could presage broader market weakness.

So far it hasn't but the underperformance of the later two indices is conspicuous, again, today:

* (SPY) +0.07%

* (QQQ) +0.45%

* (IWM) -0.71%

* (RSP) -0.64%

From this morning:

I thought Helene's comments this morning were spot on (and we saw this in a lagging (RSP) and (IWM) yesterday):

Tuesday was the first day in quite some time that the market felt very index-driven. By that, I mean breadth lagged. Now, before you get hysterical, breadth is still fine, it’s just that on Tuesday, it did not lead as we had only about 65 percent of the volume on the upside. That number has been chiming in well over 70 percent most days.

With breadth lagging, the number of stocks making new highs on the NYSE did not increase. Nasdaq did see a minor increase, but I continue to monitor the Nasdaq Hi-Lo Indicator, and you can see it did not budge on Tuesday. The math says it should try again to push upward, but Tuesday was not it. As a reminder, if it is at a lower high (than last week) when we get intermediate term overbought (late next week), it will be a negative for the market.

Let's see if the dichotomous performance continues today...

Position: Short RSP (S), IWM (S)

By Doug Kass May 14, 2025 6:55 AM EDT

Position: Short SPY common (S), QQQ common (S), RSP (S), IWM (M)

By Doug Kass May 14, 2025 2:40 PM EDT

BY Doug Kass · May 15, 2025, 6:45 AM EDT

BY Doug Kass · May 15, 2025, 6:40 AM EDT

Steve Cohen expects a retest of the market lows and a 45% chance of recession.

Point72's Steve Cohen at Sohn conference: We're not in a recession yet

BY Doug Kass · May 15, 2025, 6:30 AM EDT

Yesterday I initiated a short in ARKK at around $57.80:

Added to (ARKK) short over $58 as reported in Comments Section.

Position: Short ARKK VS

By Doug Kass May 14, 2025 10:17 AM EDT

I am shorting more in the premarket.

BY Doug Kass · May 15, 2025, 6:22 AM EDT

BY Doug Kass · May 15, 2025, 6:17 AM EDT

The S&P Short Range Oscillator dropped (modestly) to 5.16% vs. 5.61% a day earlier.

BY Doug Kass · May 15, 2025, 6:07 AM EDT