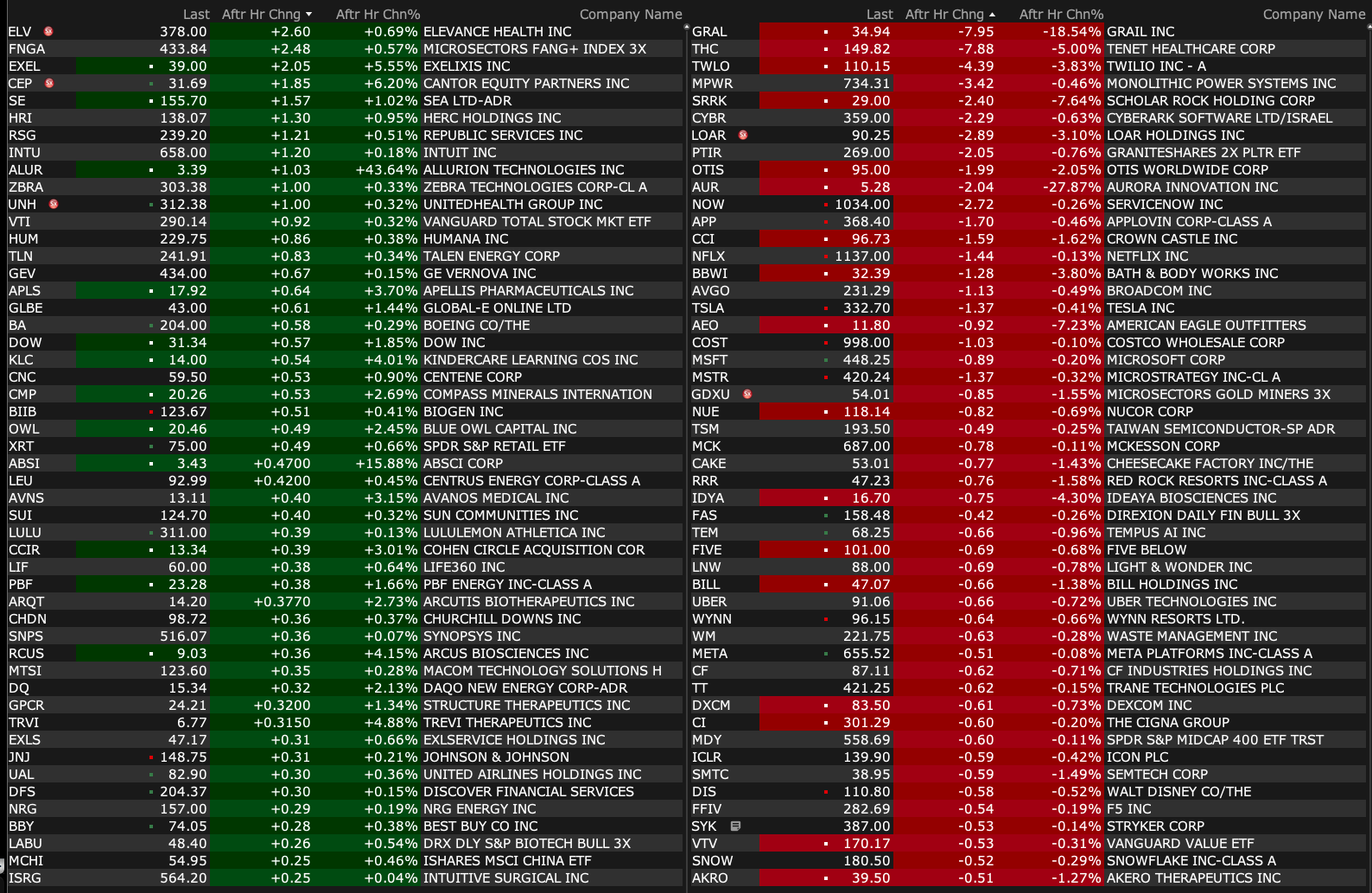

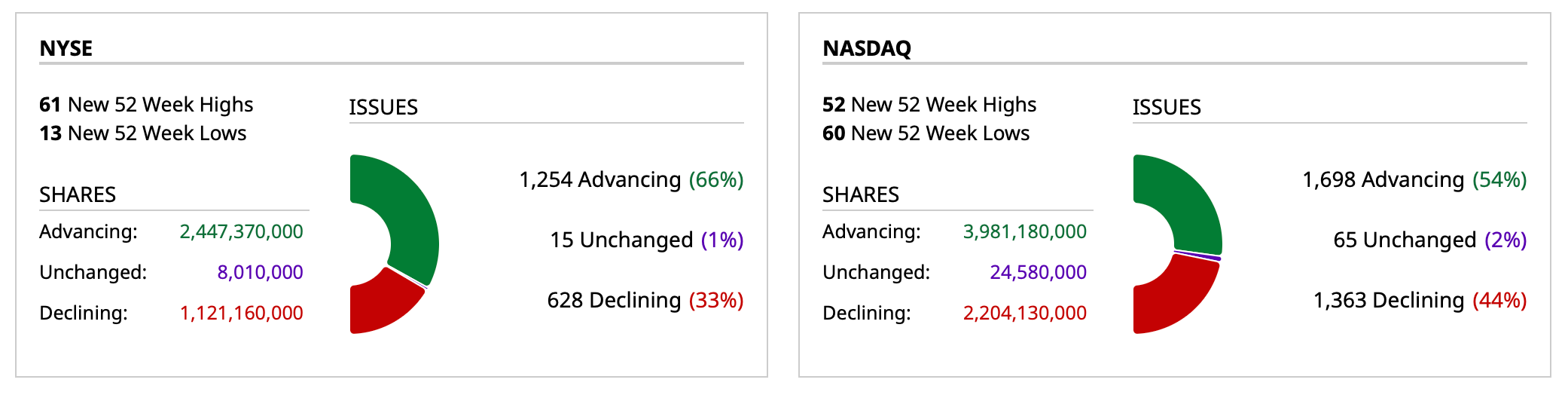

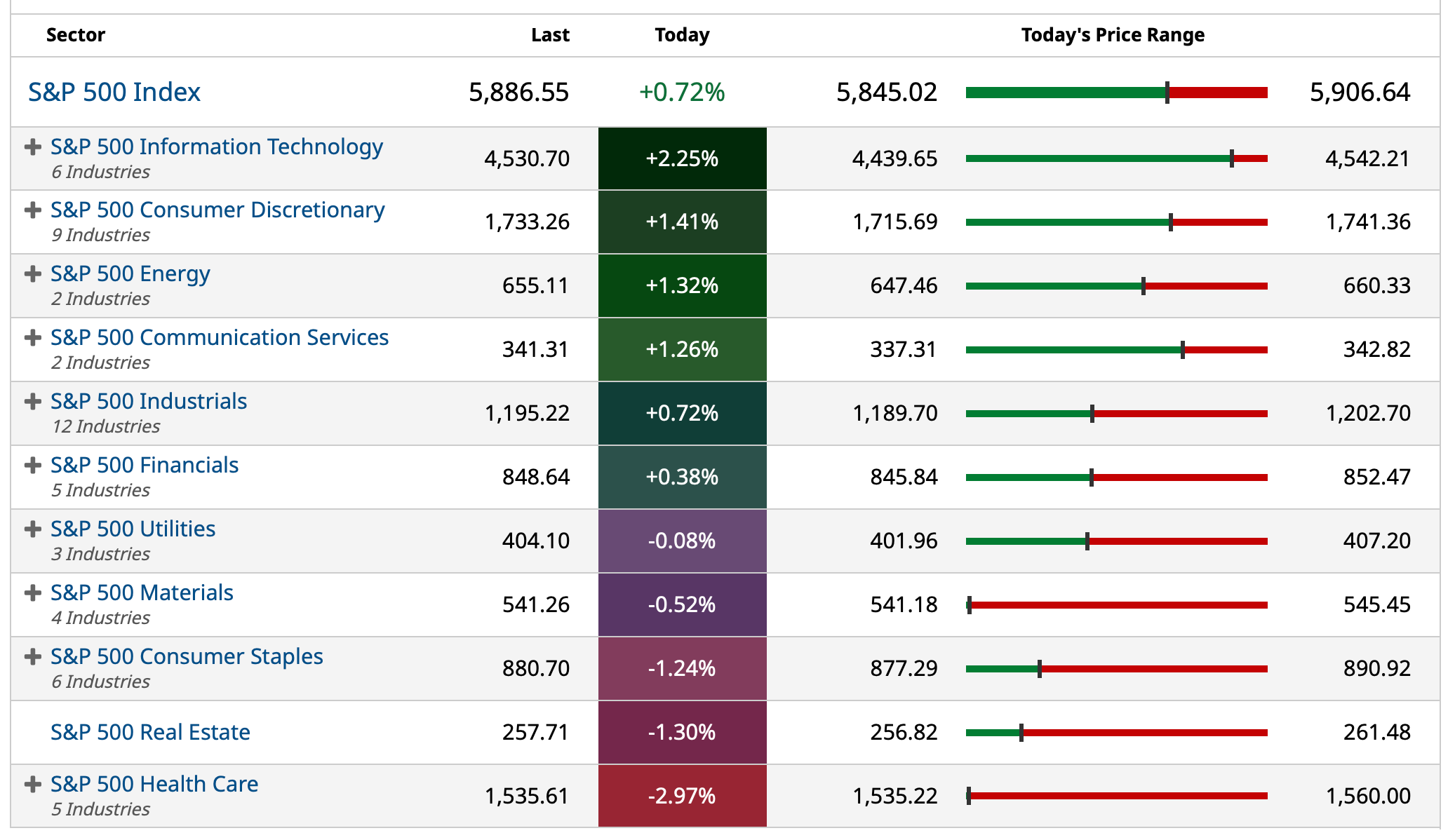

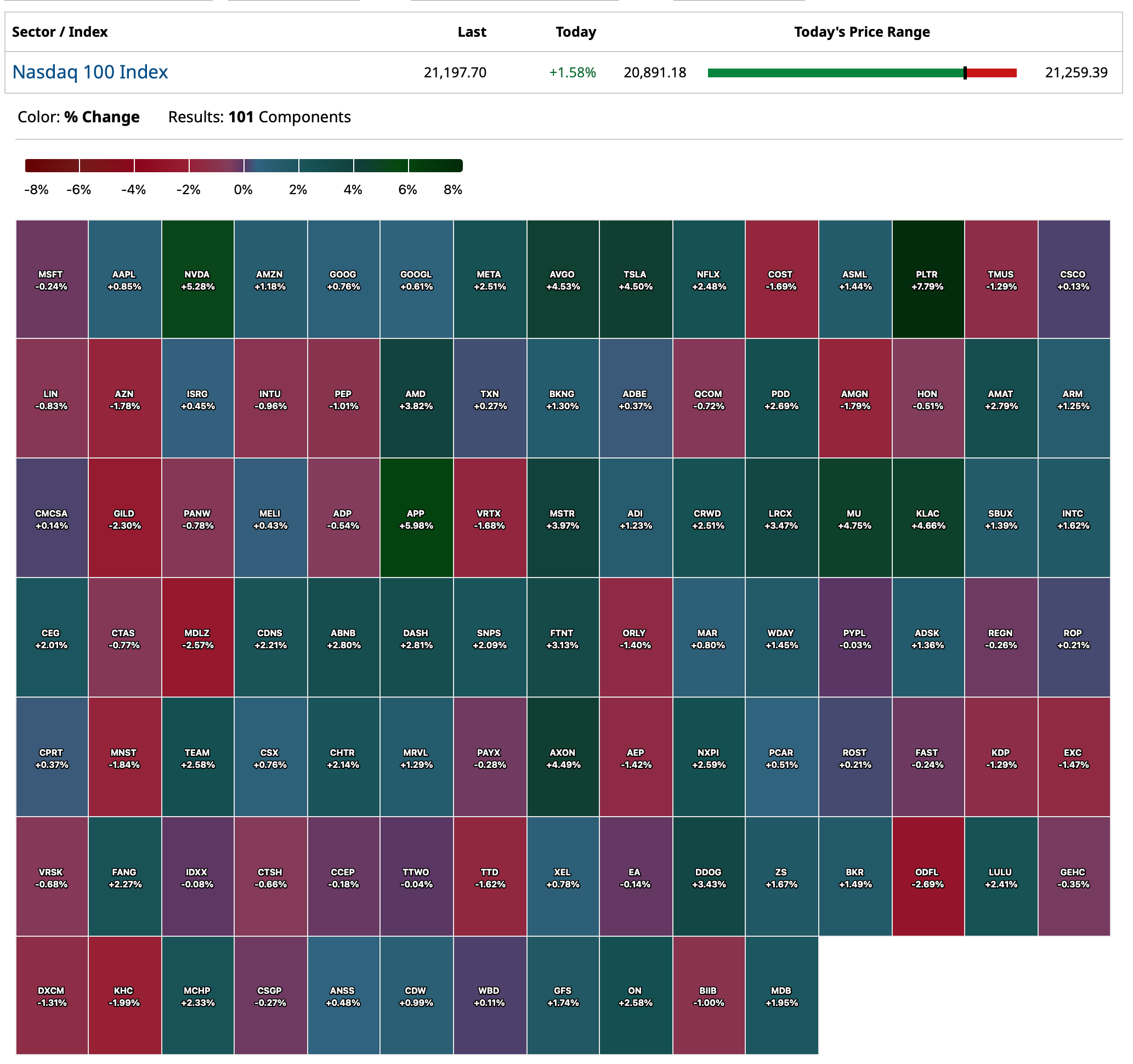

Tuesday's After-Hours Movers

As of 4:17 p.m.:

BY Doug Kass · May 13, 2025, 5:02 PM EDT

As of 4:17 p.m.:

BY Doug Kass · May 13, 2025, 5:02 PM EDT

BY Doug Kass · May 13, 2025, 4:53 PM EDT

Well per below, I think we have our answer. The U.S. economy, as things are measured now (including government spend), is in fact recession proof.

We technically didn’t have a recession in the middle years under the prior administration, when nearly everyone thought there was a going to be a recession, including financial minds that thought we were in one or would have one, and the population that felt like we were in one (and voted thusly).

We seemingly are not going to have a recession now either, even with everything that has gone on, on top of the residue of what had gone on and an overspent and overborrowed consumer.

Therefore, by hook or by crook, we have a recession-proof economy.

That, however, does not mean we do not have a crisis-proof economy.

As the economy has shifted from manufacturing based to service based, it has also become increasingly financialized. We really have not had recessions for a long time, what we really had was financial crisis-induced slowings in the economy, plus Covid (where we left with an inflation problem due to the circular relationship between government excess and monetary policy that was too loose too long).

Ex Covid, all the economic problems in recent history were really the result of monetary policy that was too loose, and government excess, as opposed to a natural business cycle. Far from traditional recessions. Instead of moving from expansion to contraction at a business level, we move from financial crisis to crisis that are functions of monetary policy and the government.

At any rate, for the time being, all of this is good for the equity markets, which they correctly sniffed out (especially those who got to have dinner and drinks with the right guys in the government). Chaos seemingly smoothed over, and looking at the budget, the government continues to spend like drunken sailors. The one caveat to all of this is the bond market, which for good reason, for the time being is not cooperating like it used to (bonds and equities are decoupling for the third day in a row):

Bond prices continued to decline throughout the day:

* The yield on the 2-year U.S. Treasury note rose by 2 basis points to 4.02%.

* The yield on the 10-year U.S. Treasury note rose by over 4 basis points to 4.50%.

* The yield on the 30-year U.S. Treasury note is 6 basis points higher to 4.95%.

What this all means for the neutral rate, is anyone’s guess, but my view is it is higher than previously thought. We shall see. And the next crisis, we shall see too...

From APR 28, 2025 9:30 AM EDT:

BY Doug Kass · May 13, 2025, 4:31 PM EDT

* Bonds and equities decouple for the third day in a row..

Bond prices continued to decline throughout the day:

* The yield on the 2-year US Treasury note rose by 2 basis points to 4.02%.

* The yield on the 10-year US Treasury note rose by over 4 basis points to 4.50%.

* The yield on the 30-year US Treasury note is 6 basis points higher to 4.95%.

BY Doug Kass · May 13, 2025, 4:23 PM EDT

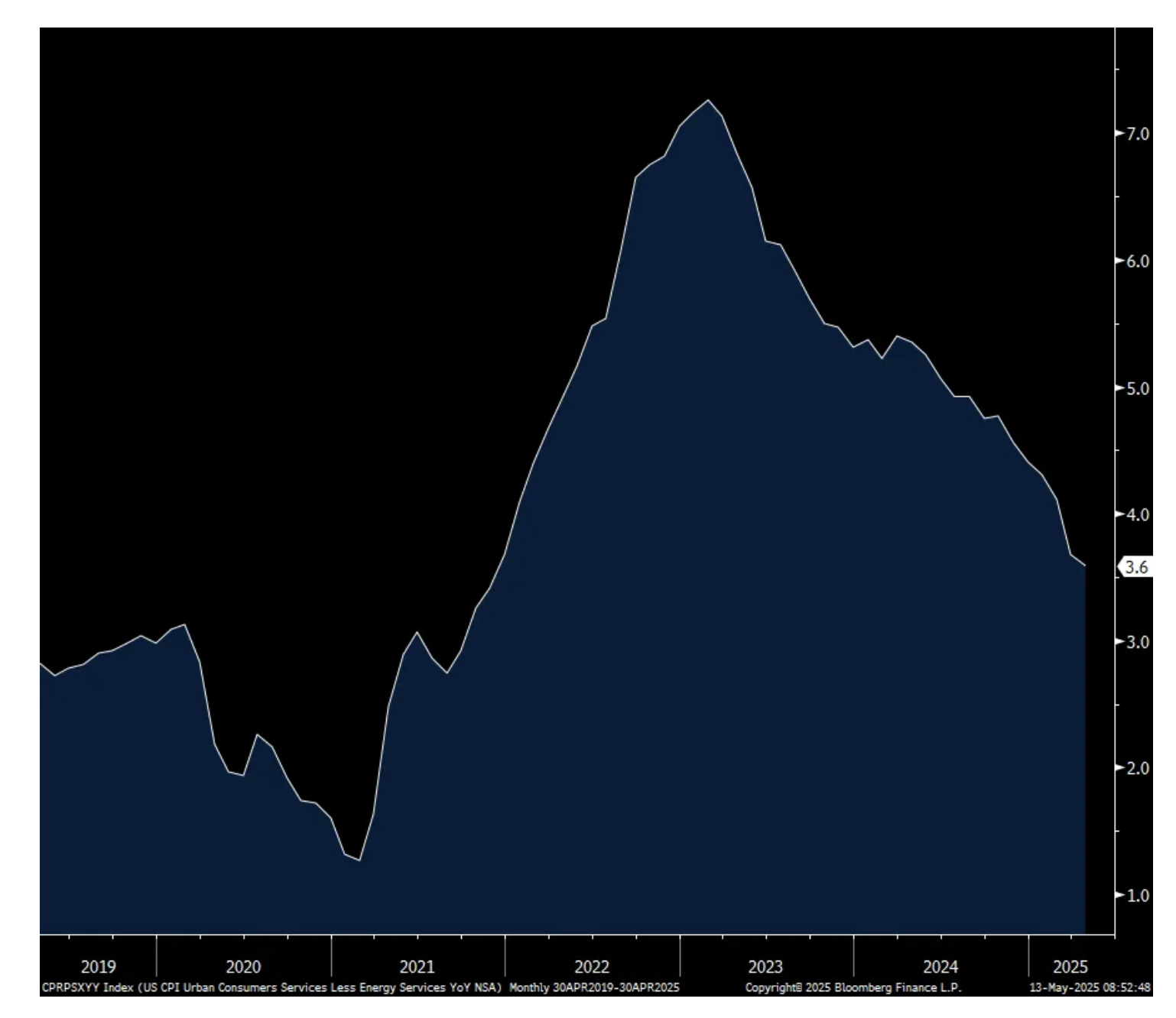

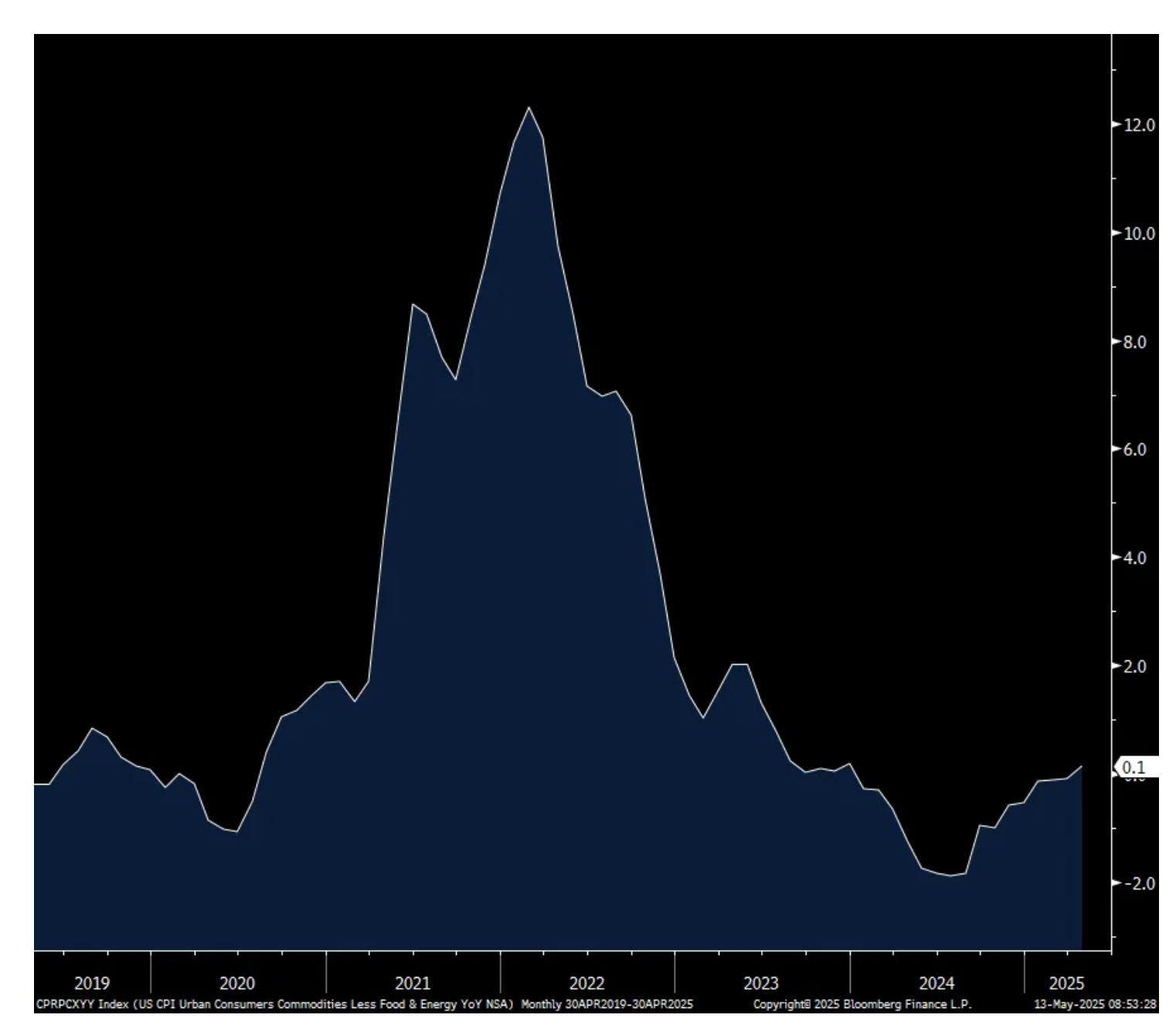

Wolf Street howls about inflation (under the surface)!

BY Doug Kass · May 13, 2025, 3:32 PM EDT

BY Doug Kass · May 13, 2025, 3:26 PM EDT

The yield on the 10-year U.S. Treasury note is +4 basis points to 4.498%.

BY Doug Kass · May 13, 2025, 12:00 PM EDT

BY Doug Kass · May 13, 2025, 11:53 AM EDT

Bond prices continue lower (and yields higher) — with TLT at day's low.

The 10-year Treasury yield is closing in on 4.5% (+2 1/2 basis points).

I have taken a small loss in TLT.

Will revisit.

BY Doug Kass · May 13, 2025, 11:40 AM EDT

Guy and Dan on MRKT CALL!

And it's free.

Let's go to the tape.

Wall Street Strategists Revise S&P 500 Price Targets...Again

BY Doug Kass · May 13, 2025, 11:29 AM EDT

I covered my RSP short for a loss.

BY Doug Kass · May 13, 2025, 10:25 AM EDT

From Peter Boockvar:

The April CPI rose .2% m/o/m both headline and core, one tenth below expectations for each. The y/o/y gains are now 2.3% and 2.8% respectively vs 2.4% and 2.8% in the month before. Energy prices were higher by .7% m/o/m but still down 3.7% y/o/y. Food at home prices dropped by .4% m/o/m helped by lower egg prices, though still up 2% y/o/y while those food prices out of home were higher by .4% and 3.9% y/o/y.

Service prices ex energy rose .3% m/o/m and 3.6% y/o/y with again help by higher rents. Owners’ equivalent rent was up by .4% m/o/m and 4.3% y/o/y while Rent of Primary Residence (which really should be the only figure used here in calculating rent instead of OER) was up by .3% m/o/m and 4% y/o/y. Both are still overstating blended rates seen in reality but they never got as high as rents actually got in 2022 either. Medical care costs jumped .5% m/o/m and up by 2.7% y/o/y. Airline fares helped to cap services inflation as they fell by 2.8% m/o/m, lower for a 3rd month and down by 7.9% y/o/y. Hotel prices fell by .2% m/o/m and by 2.3% y/o/y. Higher auto insurance prices remains a problem with rate gains of .6% m/o/m and 6.4% y/o/y. Auto maintenance too with a price jump of .7% m/o/m and 5.6% y/o/y.

On the core goods side, no signs yet of tariff induced inflation as prices were up just .1% m/o/m and by the same amount y/o/y. Lower used vehicle prices were a main reason, down by .5% m/o/m but expect this to reverse higher in the coming months based on what Manheim’s wholesale vehicle data just said. New car prices were unchanged m/o/m and up just .3% y/o/y. Apparel prices were down by .2% m/o/m and lower by .7% y/o/y. Prices for things around the house rose .2% m/o/m and .3% y/o/y.

Bottom line, this was a good inflation report in terms of the lighter figure with still services inflation driving things with not much change in goods but this does not really capture yet the response to tariffs. Yes, some will get passed on to us and not be eaten by the supply chains. To what extent of course we’ll have to see with the tariffs on, tariffs off, and the unknown of what the eventual rate will be, though we likely know it won’t be below 10% globally.

Treasury yields fell a touch in response. The 2 yr was at 3.99% right before the print vs 3.98% as of this writing. The 10 yr yield is actually up by 1 bp post release to 4.46%. I will say this, I remain bearish on the long end of the curve with the short end so much more attractive. I expect a retest of 5% in the 10 yr yield at some point this year as for whatever reason (foreigners selling, weaker US dollar, worries about the US debts and deficits, some still concerned about inflation, etc…) long end Treasuries trade poorly in the face of lower implied inflation rates in TIPS and big economic trade war worries.

As for rate cut odds, through December the fed funds futures market is pricing in a 100% chance of two cuts and just an 18% chance of a 3rd which saw a big reduction yesterday on the heels of the US/China trade coffee talk.

Services inflation ex energy y/o/y

Core Goods Prices y/o/y

BY Doug Kass · May 13, 2025, 10:16 AM EDT

Come down off your throne

And leave your body alone

Somebody must change

You are the reason

I've been waiting so long

Somebody holds the key

Well, I'm near the end and I

Just ain't got the time, oh

And I'm wasted and I

Can't find my way home

- Blind Faith, Can't Find My Way Home

As I go about Rethinking American Exceptionalism and process the rapidly changing upside reward vs. downside risk of the markets, I can't help but think that the economic scars from policy will be deeper than most market participants think and that the expectations for economic and profit growth are too inflated.

Here is a snippet of an upcoming column, Rethinking American Exceptionalism:

"You can ignore reality, but you cannot ignore the consequences of ignoring reality."

- Ayn Rand

In this commentary I want to look longer term and consider the consequences of the economic and profit cycle, the turn away from globalism and towards reshoring (and its deleterious impact on profit margins) and other factors — that could result (much like the Pharaoh's prophecy) in substandard stock market returns over the next few years:"

In the Bible, "lean years" refer to a period of famine that follows a time of abundance, particularly in the story of Joseph in Genesis 41. The prophecy, revealed through dreams to Pharaoh, foretold seven years of great plenty in Egypt, followed by seven years of severe famine. Joseph, interpreting the dream, advised Pharaoh to prepare for the lean years by storing grain during the period of abundance. This preparation allowed Egypt to survive the famine while other surrounding lands suffered greatly."

The post cold war era of endless credit, inexpensive labor, military neglect, product (supply) reliance on our political adversaries, energy dependence, unchecked migration, and the illusion of high margins was never unsustainable — it was always brittle.

The illusion of prosperity was elongated with the $5 trillion Covid stimulus packages and a $20 trillion rise in our country's debt load. Wall Street and our capital markets thrived (with only one or two temporary pauses) even though Main Street suffered from stagnating real wage growth. The disconnect and schism between headline prosperity and lived experience grew ever wider.

But, all the while, reality was catching up as the foundation was cracking.

It was the system that aged and inevitably buckled under its own contradictions.

Change, especially of the political-kind that we are see today, was inevitable (with the benefit of hindsight).

The recalibration or realignment that we are likely to begin witnessing may be violent or gradual — the course is currently uncertain — but is bound to be messy and has only started.

To me, the likely adverse impact of valuations seems more certain.

The subject is broad and spending a couple of thousand words expressing my views doesn't do justice to the topic.

Let's call this...

Rethinking American Exceptionalism

BY Doug Kass · May 13, 2025, 9:30 AM EDT

-TBI +23% (HireQuest offers to acquire company at $7.50/shr)

-ARCT +21% (earnings)

-ITOS +18% (iTeos and GSK terminate Belrestotug development program after GALAXIES Lung-201 results following topline interim results study)

-SE +13% (earnings)

-IHRT +12% (earnings, guidance)

-ADIL +11% (receives Milestone Payment from Adovate Following Initiation of Phase 1 Study)

-GCT +11% (earnings, guidance)

-COIN +10% (to replace DFS in S&P 500 Index, effective May 19th)

-BDTX +9.1% (earnings)

-MVST +8.8% (earnings, guidance)

-ARWR +8.1% (earnings)

-LUNR +7.4% (earnings, guidance)

-JD +4.0% (earnings, color around food delivery business)

-ONON +3.9% (earnings, guidance)

-SATL +3.9% (secures multi-million dollar agreement with Asia Pacific customer)

-GLPG +3.4% (re-evaluates proposed spin-off due to market and regulatory changes; Will explore all strategic alternatives for current businesses including cell therapy)

-ACHC +2.6% (earnings, guidance)

-LSTR +2.1% (earnings, color)

-SGMO -37% (earnings; prices $23.0M offering at $0.50/shr)

-DDD -28% (earnings, withdraws guidance)

-CHRS -18% (earnings)

-NRGV -13% (earnings, guidance)

-RGTI -11% (earnings)

-XENE -11% (earnings)

-UNH -9.2% (CEO Andrew Witty steps down; Suspends 2025 outlook as medical expenditures expected to be higher than anticipated)

-BLNK -8.6% (earnings, guidance)

-ODD -8.5% (announces block trade of 5.5M Class A Ordinary Shares from entity affiliated with Founder, CEO)

-MVIS -7.4% (earnings)

-IGT -7.3% (earnings, guidance)

-GETY -4.5% (earnings, guidance)

-VG -4.1% (earnings, guidance)

-CYBR -3.4% (earnings, guidance)

BY Doug Kass · May 13, 2025, 9:20 AM EDT

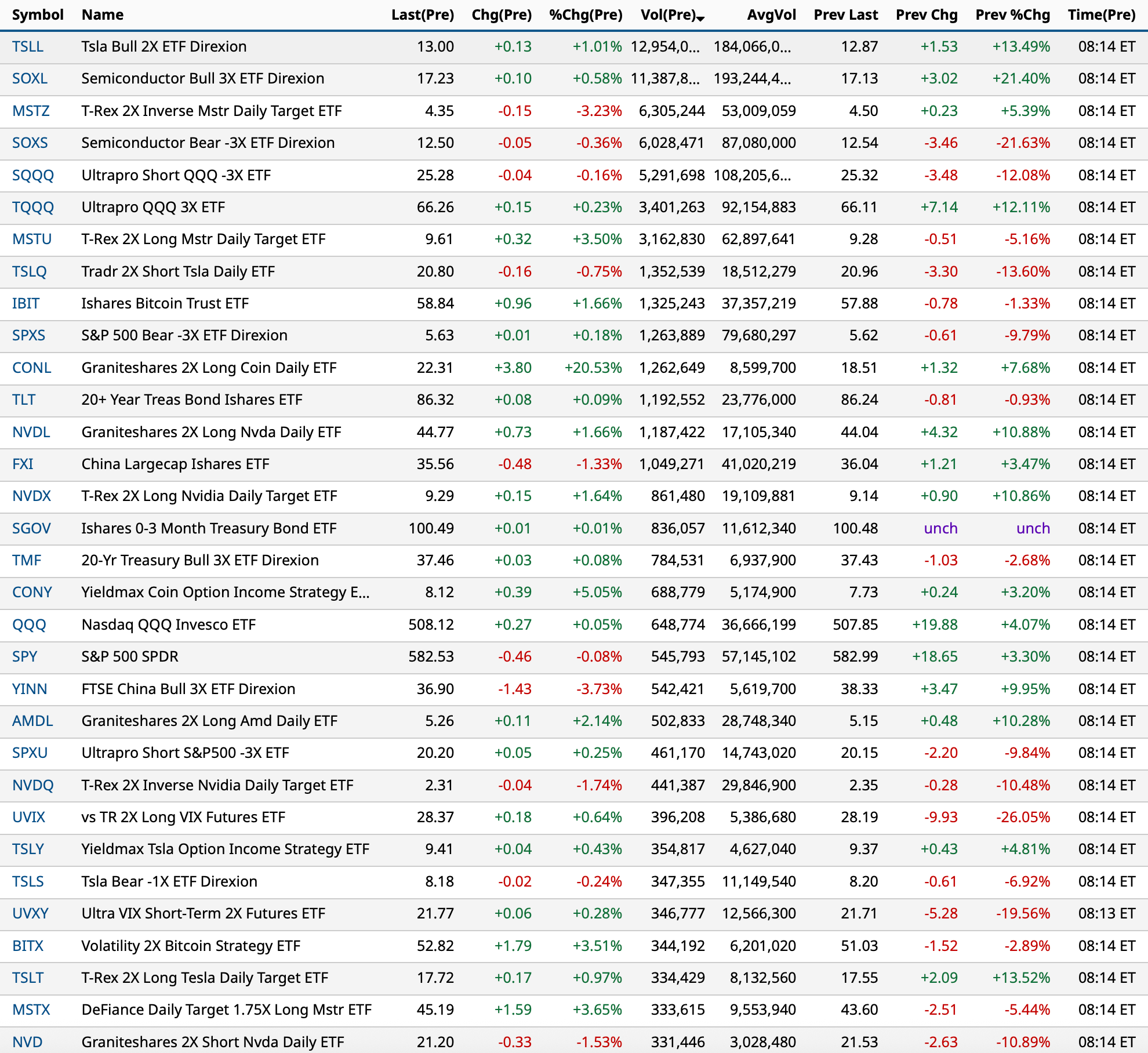

Most active premarket ETFs as of 8:14 a.m. ET:

BY Doug Kass · May 13, 2025, 9:10 AM EDT

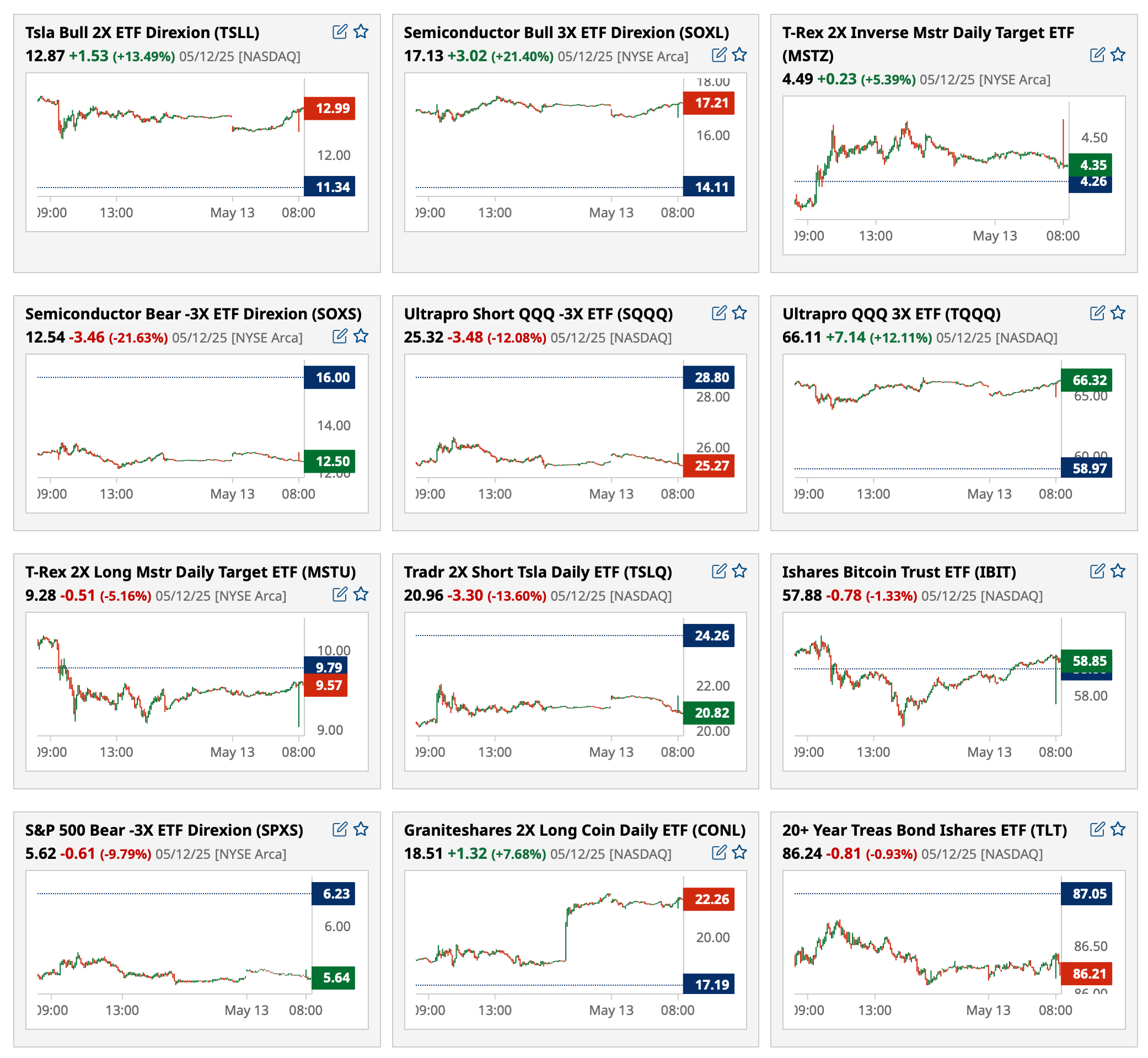

Premarket percentage movers at 8:32 a.m. ET:

BY Doug Kass · May 13, 2025, 9:00 AM EDT

From Peter Boockvar:

A tweet last night from the CEO of Flexport, Ryan Petersen, "Our ocean freight bookings from China to US increased 35% in the first day since the trade deal. A big backlog is looming, soon the ships will be sold out."

I've seen stories that the cost of shipping a 40 ft container from a baseline figure of about $2,000, is now up between $500-$1000. All to be expected however given the opportunity window over the coming months and ahead of back to school and the holidays.

The CEO of the American Apparel & Footwear Association told the South China Morning Post, "Industry conversations immediately shifted from doom and gloom to; how high will the cost of freight rise? And when can I get my goods?"

While tariffs on China are now down to 30%, that is still a very high rate and David Simon, the CEO of Simon Property Group chimed in on it on last night's call:

"Projecting and predicting sales is really difficult because to the extent that there is a retailer that imports goods from China, even with today's kind of reduction in kind of tit for tat, you're still talking about 30% tariff, which is material. And at this point, many retailers are either halting ordering goods from China, which could affect their inventory levels, trying to source it elsewhere, which they may or may not be successful with. And so it's a relatively big unknown to the extent that there is a reliance on China even on today's recent news."

"And given margins, those tariffs in the 30-ish percent, I think are going to give retailers pause whether or not they can afford to have goods shipped to them from China. To the extent that it is in the more flat 10%, I think it's really retailer dependent. I think they're going to probably operate business as usual. They'll I think try to pass a little bit on to the consumer, they'll try to get the manufacturer to take some of it and they may take some of it as well."

Also of note, "traffic is holding up, the malls are actually performing above and the outlets are relatively flat and I would say what we're seeing in the outlet on a traffic point of view is we have assets on the boarder, whether in Mexico or Canada. And obviously, there has been a slowdown in traffic and sales on some of our border great long-term assets, but currently, with all the rhetoric, we're seeing some traffic diminution on some of the border assets with Canada and our Mexican customers. So hopefully as that rhetoric dies down, we'll get back to normal."

"So the consumer, I think is fine. I do think they're being a little more cautious. And I do think tourism is - this may be the wrong word, flattening, waning, what are the different phases of the moon? Waxing, waning, whatever it is? I think tourism to the US is going to be cautious this year, whether it's from Mexican nationals, Canadians, Europeans, we've just seen a little bit on the border. On the other hand, the dollar is weaker, so maybe that offsets it...And so you put it all together, the economy is clearly a little bit uncertain. You put it all together and it makes it really hard to predict sales right now."

Topgolf Callaway said they are not immune from the tariffs:

"As of this call, and assuming current rates of approximately 10% for all countries of origin other than Mexico, Canada and China; this year's unmitigated impact would be approximately $25 million, an increase of $20 million vs our last call. Looking forward, if these are the final rates, we believe we will be able to mitigate some portion by further optimizing operations and accelerating cost reduction and margin programs. We then believe we will have the ability to pass the balance on, with only a minor impact to demand."

"Vietnam is our primary country of origin for both golf clubs and Travis Mathew apparel. However, we also source goods from Taiwan, several other ASEAN countries, Peru, Bangladesh, and others. Fortunately, we source very little from Mainland China for sale into the US. For the North American market, we assemble our custom golf clubs in Mexico, but even at a 25% US tariff, the cost impact is small, since it is a value added tax and the assembly is not a significant expense."

With regards to Topgolf, "using external data, our fun scores remain high and consumer feedback on the experience remains definitively positive, both in absolute terms and relative to our competitive set. But over the last 18 months, as the mid income consumer has become more stretched, Topgolf has begun to be perceived as relatively expensive. And in a slowing consumer environment, this is a significant but."

Topgolf's Q1 same venue sales fell 12% y/o/y. "We continue to see players manage their spend which we are addressing with targeted food and beverage offerings which cater to group social occasions. In addition, our events business is pressured as corporate spending on team outings and entertainment was reduced. It's clear that our corporate events business is going to be challenged in the near term."

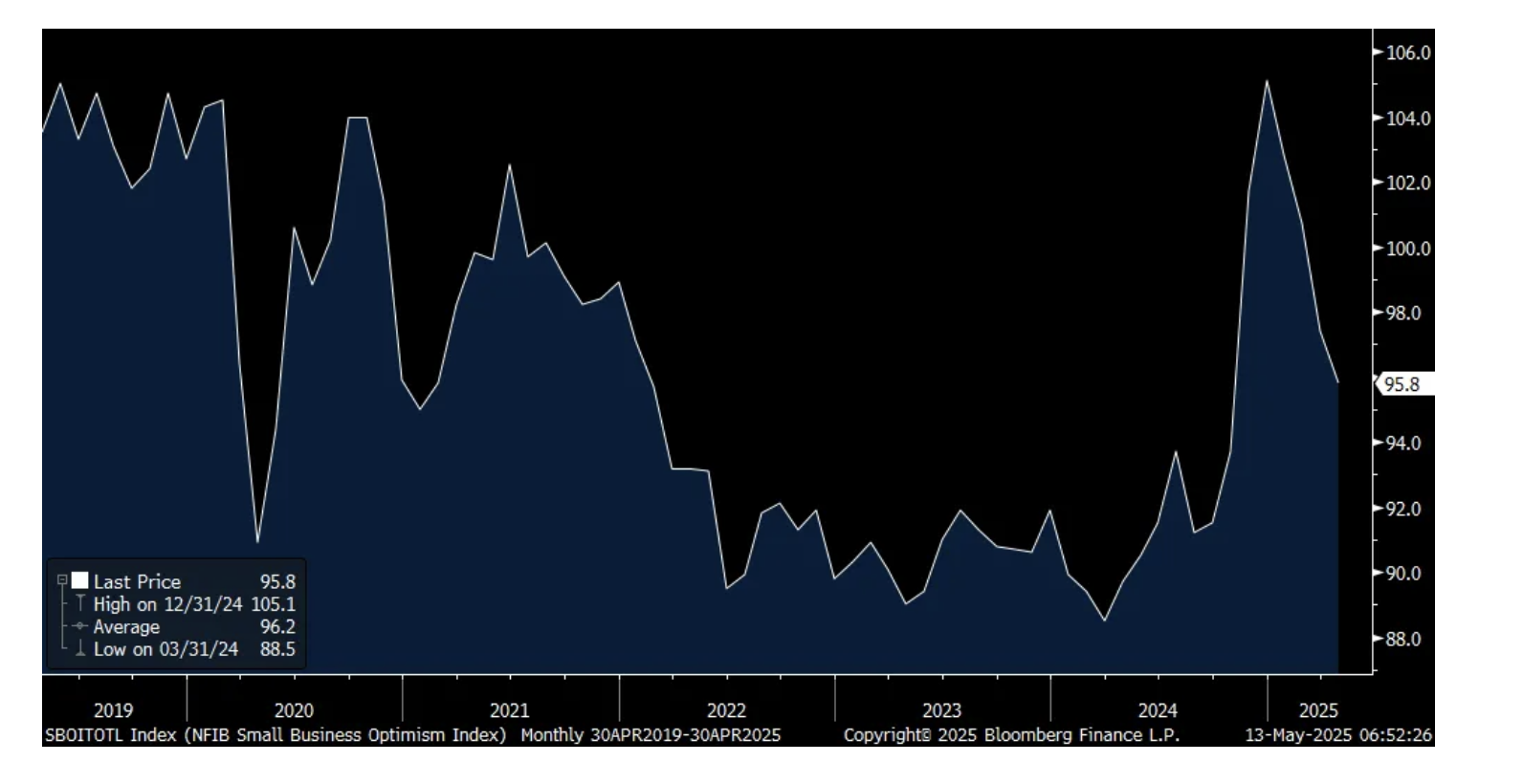

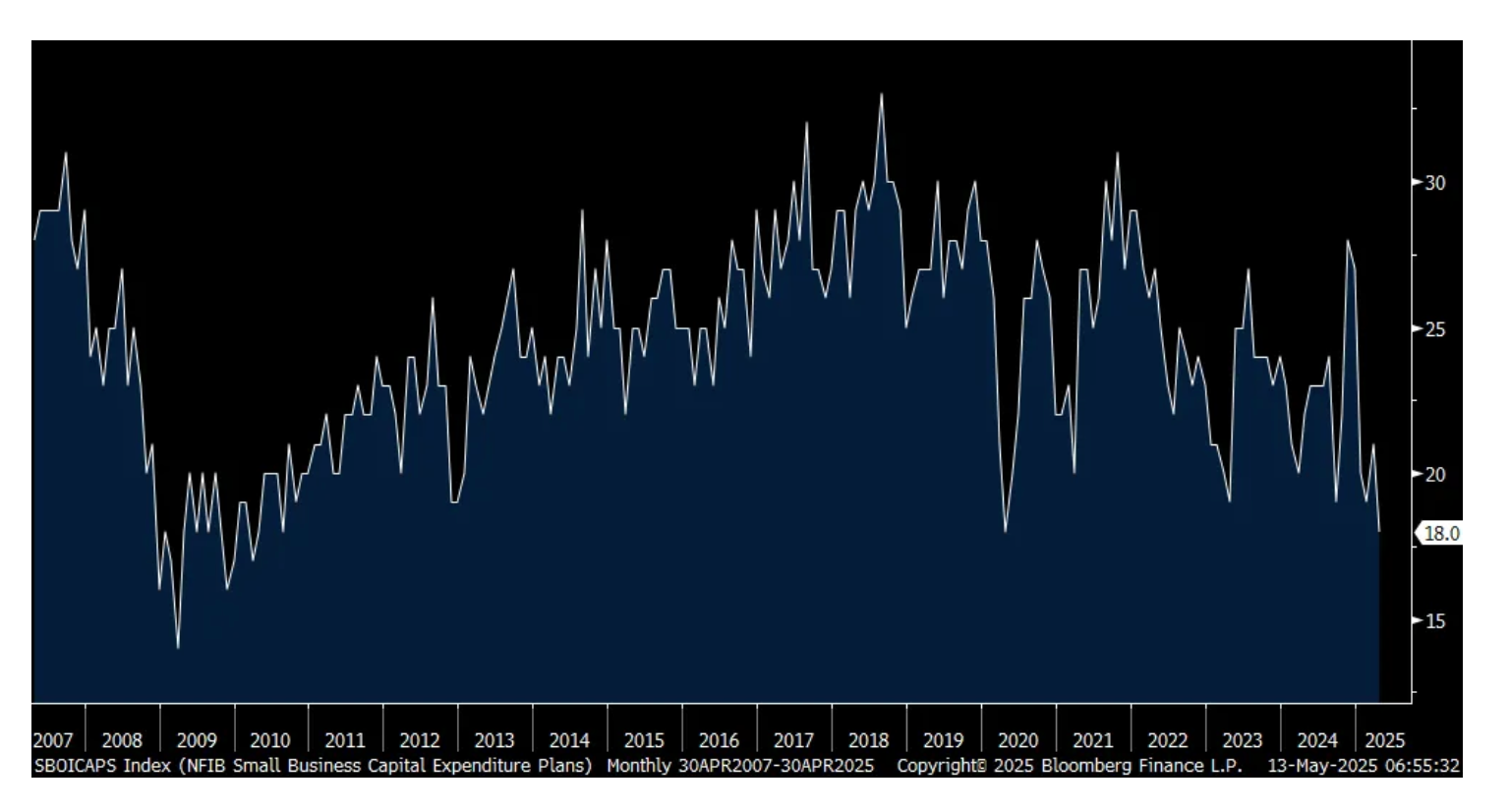

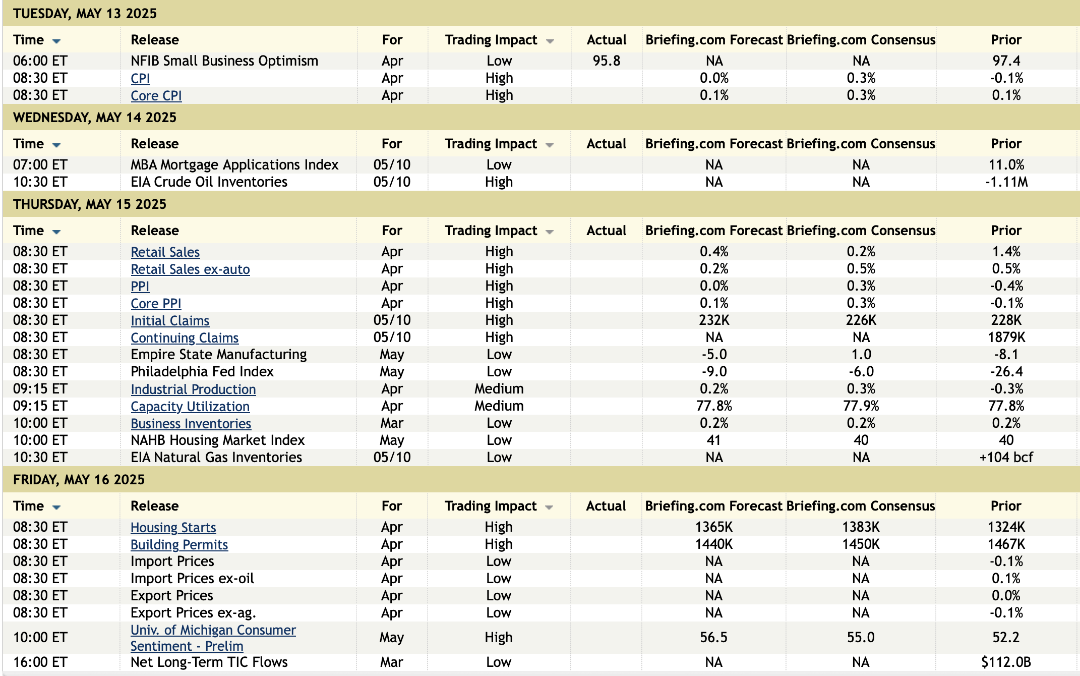

The April NFIB small business optimism index fell to 95.8 from 97.4. It's lower for a 4th straight month and is back to approaching the 93.7 level it was at in October 2024 right before the election. It also comes right before the China de-escalation announcement, and we know small business has been most negatively affected by the tariff/trade war and that was reflected here.

Plans to Hire rose 1 pt to 13% after falling by 2 pts last month. The 6 month average is 16% for perspective. Of note too, job openings fell by 6 pts and compensation, both current and planned, fell m/o/m also.

Capital spending plans dropped by 3 pts to match the weakest since 2010. The match was with the April 2020 Covid print by the way. Plans to Increase Inventory fell 3 pts to the lowest since May 2024. Higher Selling Prices were down by 1 pt.

Those that Expect a Better Economy dropped another 6 pts to 15%. It was at -5 in October and jumped to 52 in December. Those that Expect Higher Sales declined by 4 pts to -1 and compares with the 6 month average of +12. There was no change to the 9% read on Good Time to Expand vs 6% in October and 20% in December.

Also of note, credit conditions tightened by 3 pts to the worst since last September. The average rate paid on a loan stayed at 8.9%, still high and compares with 6% seen in early 2020.

A positive was the earnings trend which while still negative, improved by 7 pts to -21%.

The bottom line, "Uncertainty continues to be a major impediment for small business owners in operating their business in April, affecting everything from hiring plans to investment decisions. While owners are still trying to fill a high number of current job openings, their outlook on business conditions is less supportive of future business investments."

Also, "The percent of small business owners reporting labor quality as the single most important problem for business was unchanged from March at 19%, remaining the top issue for the 3rd consecutive month." The figure was 14% for inflation as their most important problem, down two points and the lowest since September 2021. We'll of course see how this changes in coming months depending on where tariff rates settle out at.

NFIB

Capital Spending plans

Expect a Better Economy

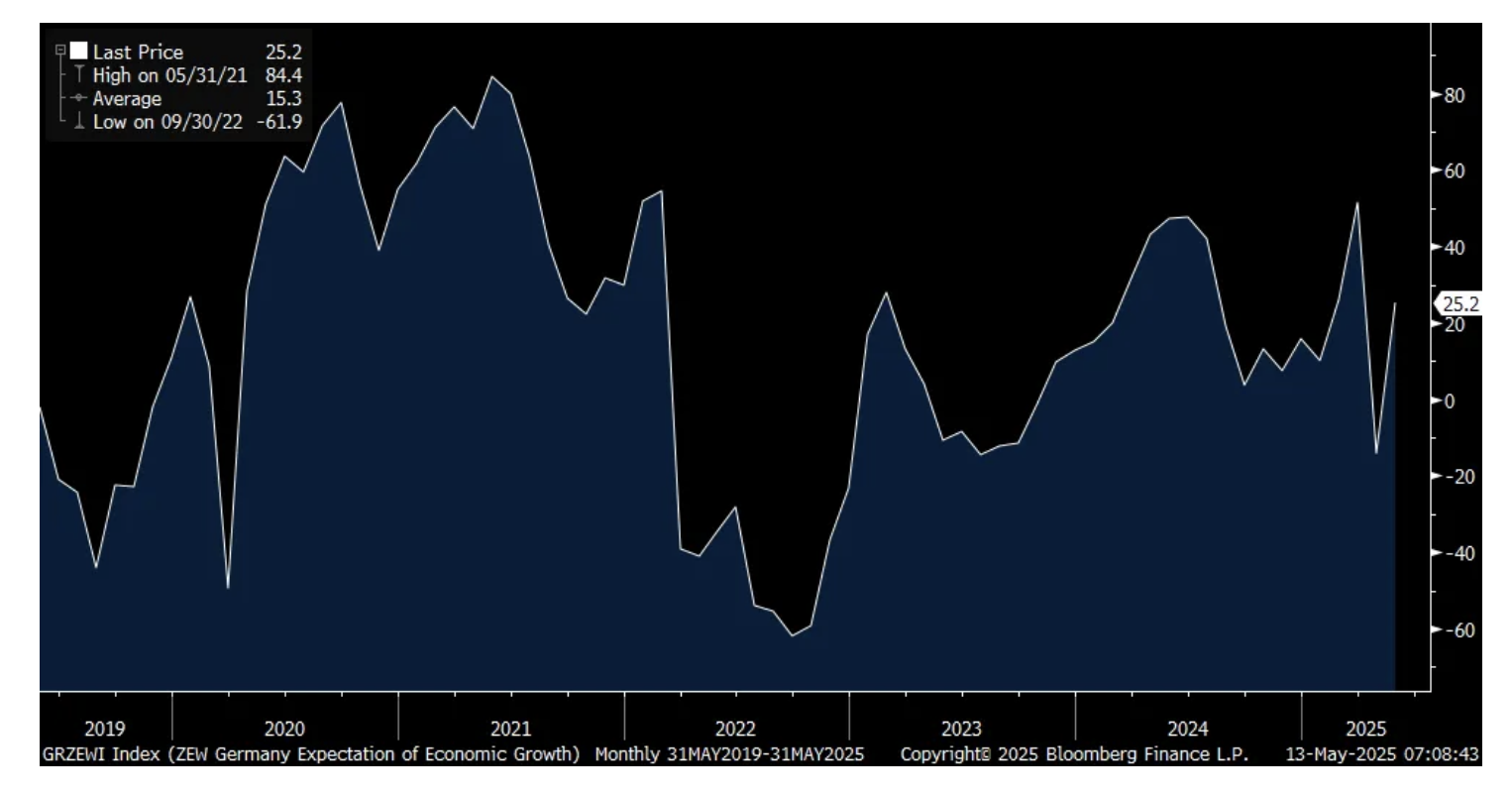

Expectations for an improving German economy jumped in May as measured by the ZEW which rose to +25.2 from -14. The estimate was +11.3. The current situation remains tough though as it came in at -82 vs -81.2 in the month before. This is not a market moving figure but the euro is rebounding and the DAX is higher by 18% ytd trading near record highs. International stock markets are having a day in the sun relative to the US and I expect that to continue.

German ZEW

The March and April jobs data out of the UK was about as expected, though April saw a drop of 32k jobs. Higher employment costs (national insurance and minimum wages) implemented by the Starmer government isn't helping.

Wage growth in the 3 months ended March rose 5.6% ex bonuses and continues to run well above the rate of inflation. Their unemployment rate rose one tenth to 4.5% which happens to be the highest since July 2021.

As the data was about in line, gilt yields are little changed but higher now by 20 bps over the past 4 trading days, along with the global rise in rates (it wasn't just in the US). The pound is up after yesterday's drop while the FTSE 100 is flat, though still up 5% ytd. There many attractively priced stocks in the UK.

UK Unemployment Rate

BY Doug Kass · May 13, 2025, 8:41 AM EDT

BY Doug Kass · May 13, 2025, 8:26 AM EDT

BY Doug Kass · May 13, 2025, 7:47 AM EDT

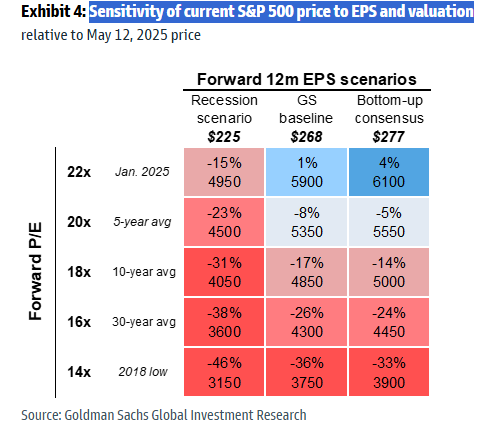

* Strategists, increasingly, chase price...

Apparently Gldman Sachs GS doesnt look at their own analysis:

I would be embarrassed.

BY Doug Kass · May 13, 2025, 7:10 AM EDT

BY Doug Kass · May 13, 2025, 6:47 AM EDT

BY Doug Kass · May 13, 2025, 6:37 AM EDT

Sticking with this view (from yesterday):

With the large ramp in futures, S&P cash will exceed my upside price target of about 5750-5800.

That said I don't see much upside from the expected opening:

* The Fed remains hostile and non-accommodating (see the rise in interest rates this morning). Chasing headlines (both up and down) has been a fool's game.

There is a strong possibility that this morning's "Peak Headlines" are similar to the opposite headlines that produced a market low in April.

Positioning (bearish) is a bit concerning to my skeptical view so I will only average into short exposure (taking "baby steps") - rather than establishing an aggressive attack on the short side.

Position: None.

By Doug Kass May 12, 2025 8:24 AM EDT

BY Doug Kass · May 13, 2025, 6:27 AM EDT

BY Doug Kass · May 13, 2025, 6:17 AM EDT

From JPMorgan:

US: Futs are weaker as markets may take a slight pause following yesterday’s surge. US reduces the tariff on ‘de minimis’ shipments from China, per Reuters , from 120% to 54%. Mag7/Semis names are weaker pre-mkt, pulling the index lower as the yield curve bull steepens. USD is lower after gaining more than 1.4% yesterday, its strongest day since Nov 6, 2024, the day after the election. Today’s macro data focus is on CPI where the YoY numbers are expected to remain flat MoM despite an acceleration in the MoM prints. Earnings prints are not expected to be market moving today.

and...

EQUITY & MACRO NARRATIVE

Yesterday, we saw a strong move in risk assets, but the trading session lacked the flow follow-through one would expect if we saw a shift in the consensus. Thought differently, many investors remain wary of the economic fallout with the average effective rate likely to be the highest since the 1930s. Some clients have expressed the view that they would rather wait to see if we get any more details on a framework for a trade deal with China and others have said that they want to see how the Administration negotiates with Canada, EU, and Mexico before determining next steps. Our view is that the direction of travel is clear and there is another potential positive catalyst before a full US/China deal hits the tape and that would be an agreement on fentanyl, which could remove the emergency tariffs on Canada/Mexico (25%) and further reduce the tariffs on China (20%).

Separately, details on the House budget bill were released and summarized by the WSJ here. Look for the bill to cost approximately $4T - $5T over 10 years. It seems likely that while there is a fiscal tailwind (maybe ~$300bn?) the growth impact may not be enough to remove the risk of a credit downgrade. In any case, this budget may push bond yields higher.

Where does this leave us? It appears that we are going to make a run at all-time highs (6144 in SPX). First, the macro data. We think we are in a “good news is good news and bad news is ignore” regime. The NFP print did not reflect any negative impact from the trade war which may be the case with this week’s data. So, anything that is better than consensus is rewarded and anything worse is ignored since it occurred before the US/China détente. Second, while there was some squeeziness (or queasiness?) to yesterday’s moves, the elevated bond yields will likely put investors back into large-cap, quality names rather than chasing SMID-caps. Third, the JPM TMT Conference may pull additional flows into MegaCap Tech. Fourth, if the move higher in yields and USD continues on a short-term basis (1-2 months), then we are likely to see Equity flows come back to the US, where the easiest place to go being Tech. Fifth, we may see a broader rally if the narrative sits between ‘Reflation’ and ‘Goldilocks’ then Cyclicals (Financials, Industrials, and Semis) add an additional source of support for the rally. Combined, we see more upside.

· My colleague Mike Gormley would add the following to the argument:

o A 90 day window with China will likely bring a rush of pull-forward demand once again before the tariffs could return to 145% after the 90 day window, especially after the focus on shortages and impact to small businesses from the China tariffs which there was little time to prepare for; we are potentially looking at another quarter of front-loading demand;

o while there is the obvious question of, “what is the point of all this?” when tariffs are brought down, they are also coming with purchase agreements, and each purchase agreement is GDP positive, driving investment in US. So, while incremental to broader trade, successive agreements with other countries are still good for US GDP as long as the tariff rates also come lower;

o it’s not just US-China where we are seeing de-escalation: over the weekend, Ukraine’s Zelenskiy agreed to meet Putin to start negotiating a ceasefire this Thursday in Türkiye which Trump may attend, and Pakistan-India have also agreed to a cease fire. We are seeing global conflict also coming down;

o if you were to whisk away all tariffs and we were looking ahead, we’d say the economy and earnings were in a good place in 1Q. On earnings, Mislav Matejka notes that with 85% of the SPX reporting, we are seeing 4% revenue growth (50% of co’s beating by 1%) and 12% EPS growth YoY (77% of co’s beating by 9%). US exceptionalism may be fading, but it hasn’t yet in equities. Removal of these trade overhangs lets us focus on what are solid equity fundamentals

· GORMLEY’S CONCLUSION – The case for SPX through 6,000 to ATHs is realistic given combination of de-escalation, pull-forward demand to be seen again in 2Q, already strong hard data leaving room for soft data to catch up, solid 1Q earnings, and positioning. The month of May is potentially the month where this comes together for SPX to break ATHs before what will be a complicated summer from debt ceiling concerns, tax debate, and the ending of the 90 day tariff windows

BY Doug Kass · May 13, 2025, 6:05 AM EDT

Wolf Street provides another vantage point on an imminent drop in housing activity and prices.

BY Doug Kass · May 13, 2025, 5:55 AM EDT

The S&P Short Range Oscillator rose from 4.67% to 5.60% — into further overbought territory.

The way the Oscillator is calculated (as a moving average) it should become much more overbought in the day(s) ahead.

BY Doug Kass · May 13, 2025, 5:45 AM EDT