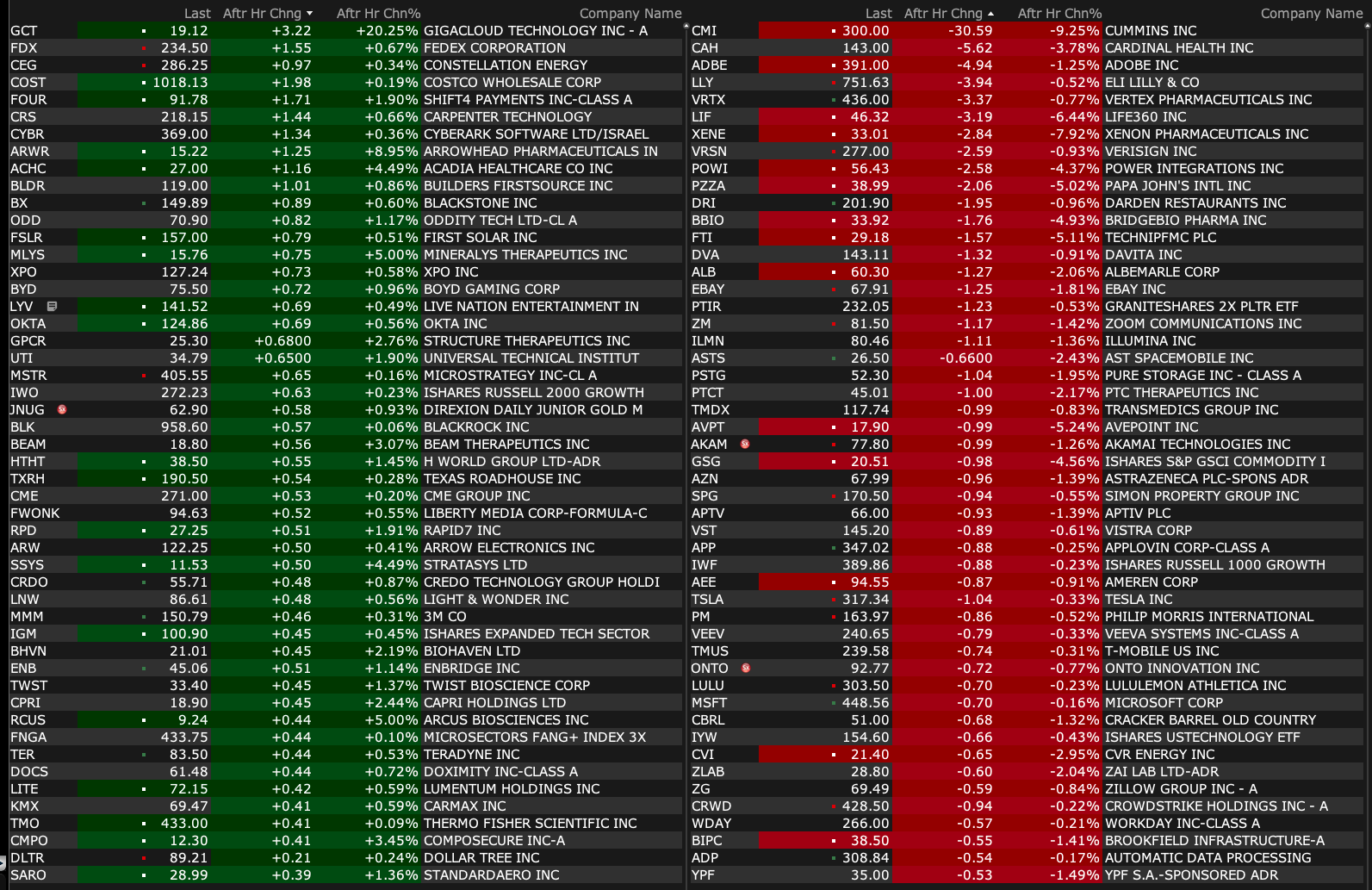

Monday's After-Hours Movers

As of 4:23 p.m.:

BY Doug Kass · May 12, 2025, 4:45 PM EDT

As of 4:23 p.m.:

BY Doug Kass · May 12, 2025, 4:45 PM EDT

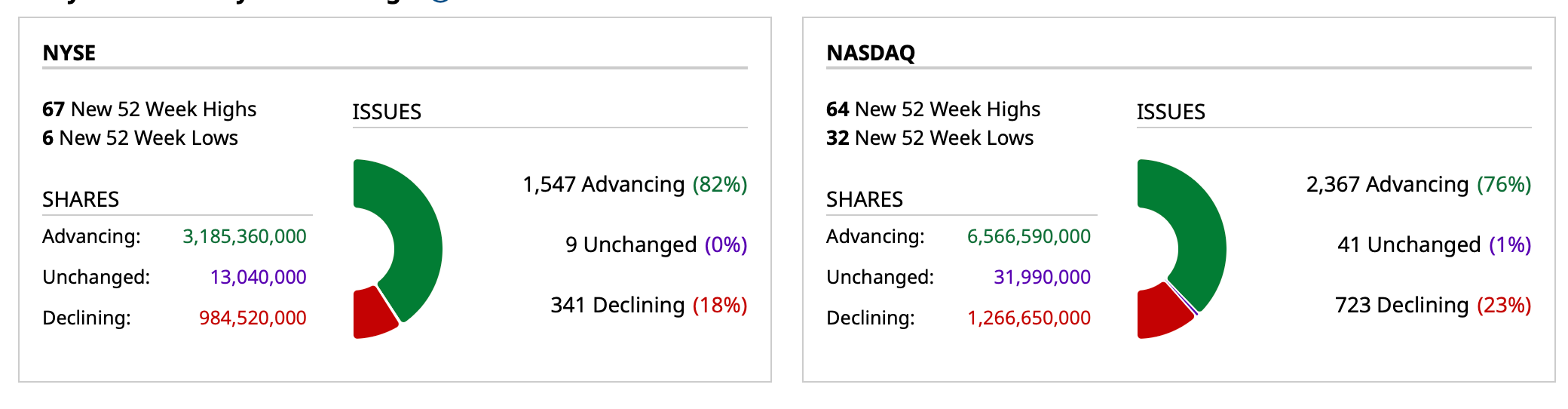

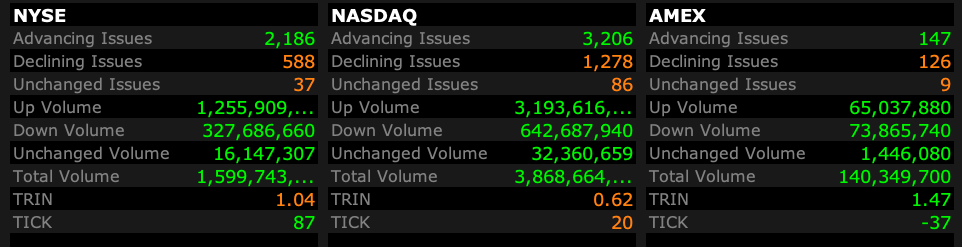

- NYSE volume 25% above its one-month average;

- NASDAQ volume 27% above its one-month average;

- VIX index: down 16.03% to 18.39

BY Doug Kass · May 12, 2025, 4:24 PM EDT

BY Doug Kass · May 12, 2025, 3:15 PM EDT

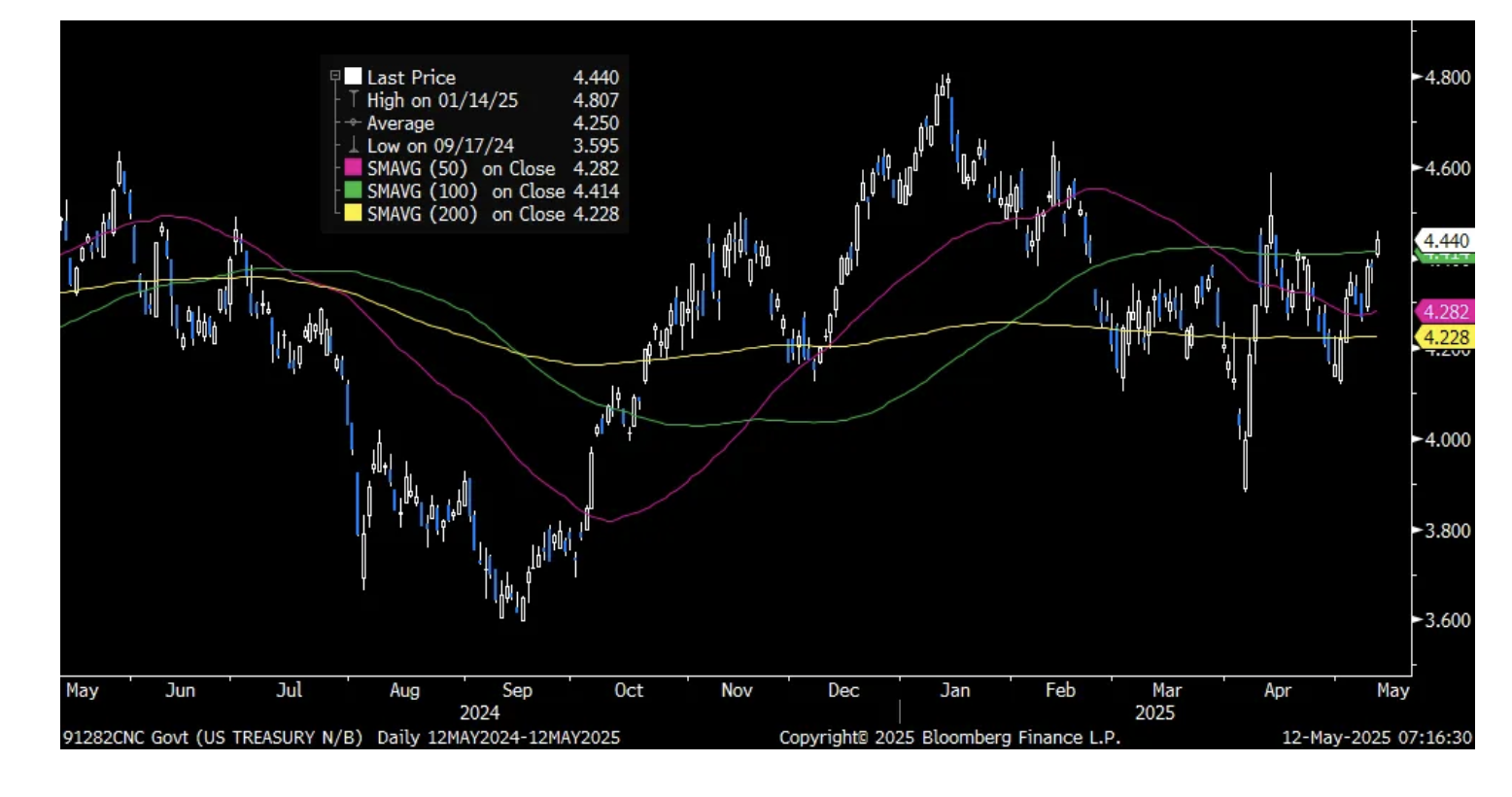

High on the day for bond yields, low on the day for bond prices.

BY Doug Kass · May 12, 2025, 2:57 PM EDT

With S&P cash +177 handles I am adding to my shorts:

* SPY $581.84

* QQQ $507.13

* IWM $207.78

* RSP $177.12

* GRNY $20.41

BY Doug Kass · May 12, 2025, 2:29 PM EDT

I have a research meeting from 2 p.m. to 3 p.m..

BY Doug Kass · May 12, 2025, 1:43 PM EDT

It is unusual to get not one, but two of my favorite commentators for about 45 minutes of pithy and candid market and economic analysis.

But that was the case on the just concluded MRKT CALL podcast with my two good pals, Dan Nathan and Peter Boockvar .

(The only person who was missing — that would have made it a Trifecta (!) — was Guy Adami!)

Let's go to the (recorded) tape!

BY Doug Kass · May 12, 2025, 12:25 PM EDT

Adding to TLT at $86.60.

Now large sized.

BY Doug Kass · May 12, 2025, 11:26 AM EDT

* Move over tariffs..

Nice shout out on Bloomberg's Market Surveillance at about the 18 minute mark - in which I highlight the equity market's valuation risks associated with higher interest rates. Bloomberg Surveillance: US-China Trade - Bloomberg

BY Doug Kass · May 12, 2025, 11:20 AM EDT

BY Doug Kass · May 12, 2025, 11:15 AM EDT

HHH HHH, a new purchase last week is trading over $75 now (up from $69) - I have unexpectedly taken the gain just now and I have eliminated this long.

BY Doug Kass · May 12, 2025, 10:55 AM EDT

This week's Trade of the Week was communicated on Friday. (As I suggested, even with today's wonderful tape, look at several of the important components of Fundstrat Granny Shots U.S. Large Cap ETF (GRNY) this morning. (NFLX (Fin TV fave, -$31), MSTR (-$1), PLTR (flat) )

From Friday:

Arguably, equities are overvalued and overbought.

And many of the components of Tom Lee's Granny Shots ETF (e.g. (MSTR) , (PLTR) , (GEV) , (MSFT) , (PGR) , etc.) are among the most overvalued and overbought equities extant. Holdings – Fundstrat Granny Shots ETF

Ergo, GRNY is a conservative way of shorting some of the most exploited areas of the equity market.

For more information, here is the ETF's website. Fundstrat Granny Shots ETF

.

Only four weeks ago (April 7th) GRNY traded at $15. Last sale was $19.78.

Position: Short GRNY (M), MSTR (VS)

By Doug KassMay 9, 2025 12:58 PM EDT

BY Doug Kass · May 12, 2025, 10:20 AM EDT

Long TLT at $86.54.

BY Doug Kass · May 12, 2025, 10:05 AM EDT

From Peter Boockvar:

So, both sides luckily decided to save Christmas. China gave hope to some of its manufacturing base that caters to the US while the US side listened to the existential crisis of many small businesses. Whether still a 30% tariff will be enough to make a difference we'll of course see but for some, you are going to see a rush of ordering over the next 90 days the likes we've never seen before. You are going to see the cost of transportation skyrocket too in the coming weeks/months.

The stock market has of course spoken again that it wants nothing to do with tariffs but we're also seeing US dollar cross rates have become too a daily voting machine on the policies of the US and attractiveness of our markets. With regards to fixed income, bond yields are rising across the world on some economic sanity and excitement over the detente.

Technically speaking we're at key spots. The S&P futures are retesting its 200 day moving average. The 10 yr US yield at 4.44-.45% is now a few bps above all its key moving averages. And the US dollar index is about 30 cents from its 50 day moving average, though well below still the 200 day.

S&P Futures

10 yr Yield

DXY

I do want to put some numbers around the 10% baseline tariff on all US imports of goods that seemingly will be the minimum rate of all these country negotiations. As we import about $3.3 trillion worth of goods, that would be the equivalent of an incremental US corporate tax of $330 billion. The revenue collected from the US corporate income tax is expected to run this year at about $525 billion for comparison. Back of the envelope assuming the 21% corporate tax rate (obviously some pay less and many small business businesses pay pass thru rates), this is off $2.5 Trillion of pre tax income. If I add the $330 billion to the $525 billion, the $855 billion of total corporate taxes that will be paid under this 10% tariff regime would be the equivalent of a 34% corporate income tax rate which happened to be about where it was before Trump rightly cut it in 2017.

Just some perspective. Yes, not all companies will eat the 10% tariff but many don't eat the corporate tax rate either as they pass it on to the rest of us.

Some more perspective that I got from Barron's over the weekend, the importance of the need for lower tariffs. "Some 250,000 small businesses import goods or materials representing a third of the total value of US imports, according to the Chamber of Commerce. And 40% of those...building their products in the US, but requiring raw material or other inputs from abroad."

Regardless of what the end result will be from both where tariff rates will settle out (10% or more) and hopefully lower trade barriers around the world, it is clear that foreigners have had a rethink of their US market exposure. Not that they don't want any, they just seemingly want less off extreme allocation levels. What I'm most interested in seeing soon are the updated 13Fs and 13Ds reflecting the ownership of US stocks.

Below are the top 10 holdings of the investment arm of Norwegian central bank, the Norges Bank, as of December 31st to make my point of how over-exposed at the peak foreigners had to US markets. As the Mag 7 trade is likely over, as you've heard me argue over the past 3 months, and the action reflects this, foreigners are finding other things to buy and of course have gotten shocked by our tariff war.

In case you didn't see the FT Weekend article titled "Dollar asset selling signals start of longer-term shift, warn investors." In it, "Finland's Veritas Pension Insurance Company reduced its US equity exposure in the first quarter. Chief Investment Officer Laura Wickstrom told the Financial Times that valuations on US stocks were high while she also cited 'the uncertainty and the communication around tariffs...the confusion and unpredictability associated with that made us question the idea that you should pay that sort of premium."

Also, "John Pearce, chief investment officer at A$149 Australian pension scheme UniSuper, said on its podcast last month that his fund had quite a large exposure to US assets and would be 'questioning that commitment.' He added: 'Frankly, I think we've seen peak investment in US assets.' "

More, "Danish pension funds embarked in the first quarter on their first sale of US stocks since 2022, making their largest purchase of European listed shares since 2018."

Lastly, Sam Lynton Brown, global head of macro strategy at BNP Paribas had a thought experiment according to the article, "if European pension funds were to reduce their allocation to 2015 levels, that would equate to selling as much as 300b euros in dollar assets."

Bottom line, we are talking about the pendulum swinging in the other direction from the extreme US asset global love that peaked in January and mean reversion inflection points is what is being discussed here. The US economy and markets will always be the most attractive globally I still believe but it's clear that foreigners got way over their skis in terms of US allocations and valuations, and changing fundamentals and a global tariff war was all that was needed for a global rethink.

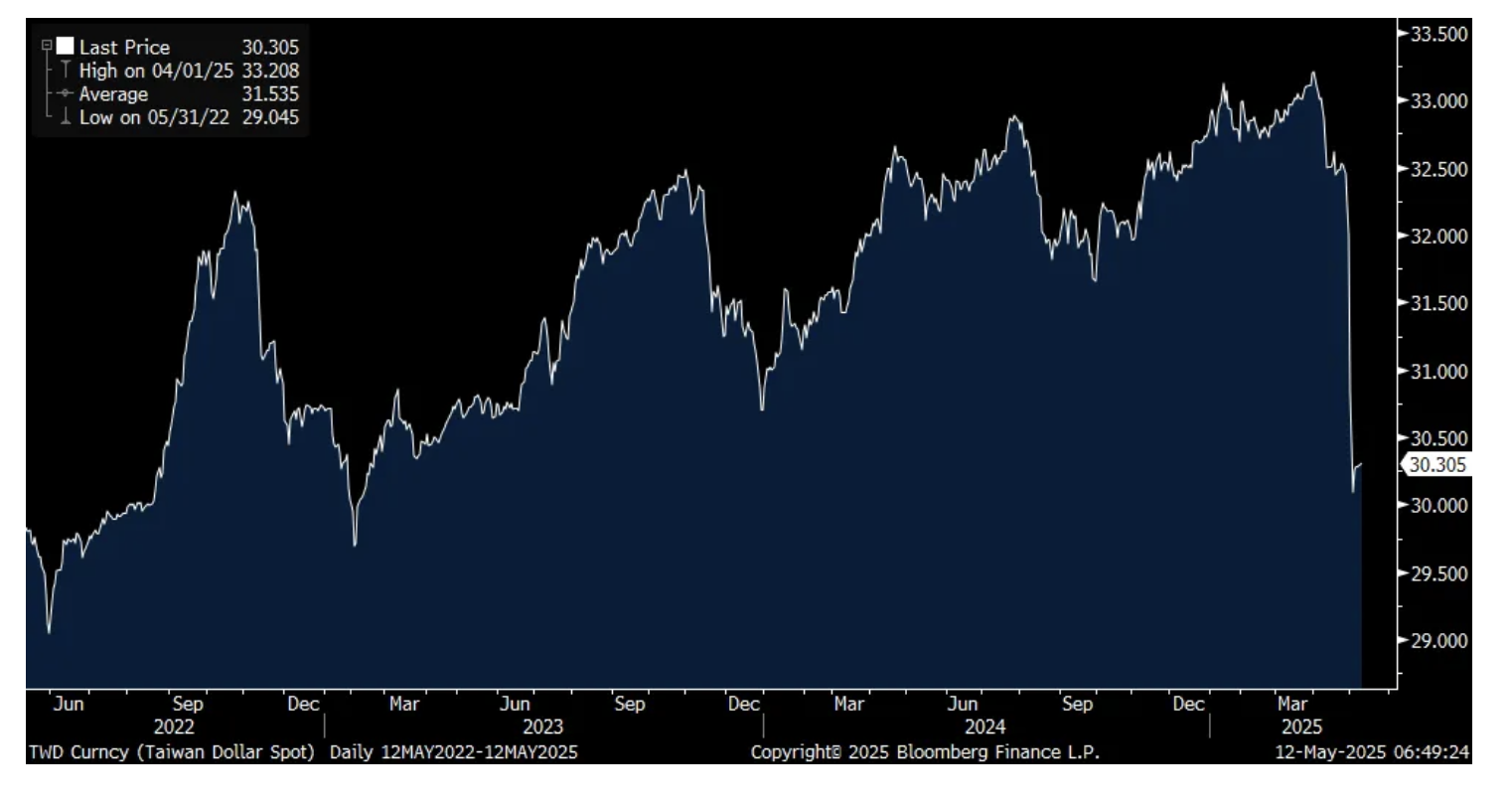

That move in the Taiwanese dollar, the huge rally in just a few days, is not out of the blue as Asian asset managers have massive exposure to US assets too. It is a microcosm of the changing stance and flow of foreign money coming back home. I expect this to be a multi year global allocation shift and why US stock market exceptionalism relative to the rest of the world is going to continue to cool I believe.

Taiwanese Dollar (the lower it goes, the higher its value vs the US dollar)

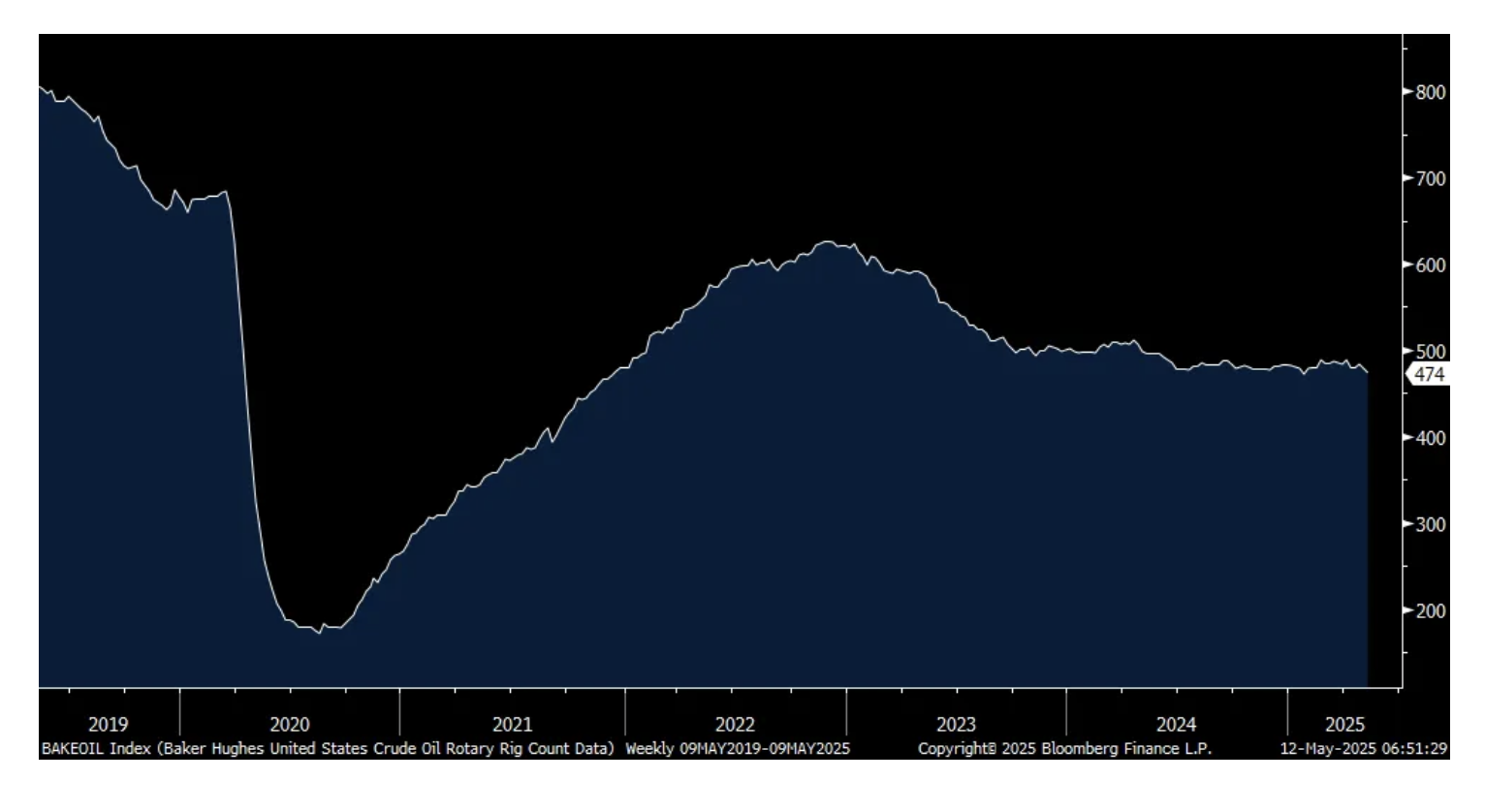

On the heels of the OPEC production news and the anecdote we heard from Diamondback Energy last week that cuts in capital spending on drilling were taking place, the Baker Hughes oil rig count fell for a 2nd week, by 5 rigs and 9 over the past two weeks. At 474, it is just 3 rigs from falling to the lowest level since December 2021.

Oil Rig Count

Barry Sternlicht in Friday's earnings call for Starwood Property Trust, a stock we own, gave us his economic lay of the land:

"The economy is going to weaken. I just was talking to CEOs of Fortune 100 companies in the past few days, returning from the West Coast and there will be issues on shelves and there will be prices for consumers to absorb. And you kind of already were in a recession, you kind of saw it at the lower half of the country and the top 10%, 15% of the country was carrying spending in consumption. And now, we'll see how the wealth effect actually plays through. Actually, the markets have recovered shockingly to pre-Liberation Day highs, but that doesn't really feel right. And things like travel are clearly off. I guess it was Expedia that reported and then Airbnb, and we've seen the travel numbers, the airlines have talked about their stress as international travel in the United States dissipates. But it will go somewhere. So, Canadians will go to Europe or they'll go to the Caribbean. They may not come here."

And on this belief, "that means Powell, sooner or later, will lower rates. And for sure, when he's out in May of '26, there's no chance rates will be higher because the selection will depend on somebody who accommodates a lower rate environment, that is all good for the property segment. And so, I feel like we're through the worst of it and it's going to get better from here."

From Sphere Entertainment, benefiting still from the incredible live experience it provides:

Answering a question on Vegas visitation from overseas, "Las Vegas has over 40 million visitors every year so far. We've seen that the international accounts for a little over 20% of the guests to Sphere and 10% for concerts. We really haven't seen any change. So I think, there's a little going on in our economy with that right? Maybe later on we'll see some substantive reaction from the marketplace, but right now we're really not seeing it. So, and even if we did, it doesn't account for that big of a difference, right? And, I think in general, when it comes to concerts, demand exceeds capacity."

BY Doug Kass · May 12, 2025, 9:35 AM EDT

From JPMorgan:

US: Futs are higher as US/China slash tariffs, with China tariffs falling from 145% to 30% and US tariffs from 125% to 10%, for 90 days. With the countries agreeing that they do not want to de-couple, there is optimism that a longer-term deal can be reached. Trade War 1.0 tariffs remain, as do sectoral tariffs but this is an unambiguous positive for all global risk assets. This will allow markets to look through any near-term weakness in macro data but if CPI, PPI, and Retail Sales surprise to the upside, then that will provide another tailwind to risk assets. Pre-mkt, Mag7 names are higher with many up more than 3%, Semis/Cyclicals are also higher as the market will need to reset its growth expectations higher. Cmdtys are higher, led by Energy, despite a spike in bond yields/USD.

and..

EQUITY & MACRO NARRATIVE

We reiterate the tactical bullish view. In this section, we review the bull case, the call for a potential run to 6k, and additional thoughts for this week.

The tactical bull case is based on (i) positive EPS growth; (ii) stable macro data; and (iii) improving trade rhetoric. So far, the hypothesis has been supported.

· EARNINGS (Mislav) – With 85% of the SPX reporting, we are seeing 4% revenue growth (50% of co’s beating by 1%) and 12% EPS growth YoY (77% of co’s beating by 9%). Energy, Materials, Real Estate, and Staples are seeing negative EPS growth. US Exceptionalism may be coming to an end, but that is not yet reflected in earnings; though Mislav highlights that median EPS growth is 6% for both the US and EU.

· MACRO DATA – The data over the last month has generally been better than expected (NFP, Retail Sales, CPI, PPI, ISM-Mfg, ISM-Srvc, etc). That trend seems likely to continue this week. Ultimately, this buys the Trump Administration, and the Market, time to get more deals to the tape. The quicker deals occur, the higher we will see economic expectations move.

Source: Bloomberg

· TRADE WAR RHETORIC – Trump has shown a willingness to pull back from his initial demands (90-day pause, removal/reduction of sectoral tariffs, quicker than expected trade negotiations) such that the direction of travel seems clear to the market. The focus is on deals with Canada, China, EU, and Mexico as the most important trading partners.

When we made the call we felt that the market could overshoot to the upside, reaching the 5,800 – 6,000 level. The below is from the May 5 Morning Briefing and then some thoughts on how the hypothesis is playing out.

· WHAT GETS US TO 6K? The pathway there may look something like this, (i) the aforementioned bull hypothesis continues followed by (ii) short squeeze where things like RTY, Retailers, high beta Cyclicals outperform; (iii) USD continues higher leaving things like (iv) EM and Int’l DM to underperform as assets move back to the US (v) pushing TMT higher. If this occurs as CTAs activate and buyback accelerate the SPX may be above 5,800 as HFs are bought into the market.

· US MKT INTEL VIEW (May 5 view) – We think 6k is more likely as markets overshoot with earnings season stronger than expected and Friday’s NFP pushing out the next major, scheduled, catalyst being the June 6 NFP print. Trade war headlines are likely to continue to come out positively. While there is a critical mass of clients unlikely to chase this rally, we may see buybacks, CTAs, and retail investors push the market higher. Some investors were waiting for retail investors to capitulate as a signal the market formed a bottom, but the retail behavior was a continuation of the recent buying trend with April being a record month of net inflows. Should markets make a run at 6,000, with think that represents another near-term peak.

· ASSESSING THE 6K BULL CASE: (i) the tactical bullish framework remains intact, as described above; (ii) over the last two weeks we have seen a bit of a squeeze in these higher beta, highly shorted areas of the market and Positioning Intel say that there is risk of a further squeeze; (iii) the DXY has appreciated about 2% from its YTD lows set on Apr 21 and the index closed above 100 for consecutive session, potentially portending a move higher; (iv) US performance has improved but it has yet to overtake International or EM Equities, which may require more trade deals, stronger USD, and an acceleration of the Tech/AI trade. Further we saw positive fund flows into EM, with $1.4bn into EM Equity funds and $1.7bn into EM ETFs; (v) NDX has outperformed the SPX by 80bp over the last two weeks but the equal-weighted NDX has outperformed the market cap-weighted version, by 49bps, with Mag7 lagging the Tech indices, we have seen Semis (SOX) outperform the NDX by 181bp.

· UPDATED US MKT INTEL VIEW – Tactically bullish. We remain on-track to see the SPX to make a run at 6k, though this will require help from a positioning perspective (buybacks, CTAs, or HFs) despite the continued buy-the-dip behavior from retail investors. April’s buybacks tallied $233.8bn, the second highest monthly total on record. While the headlines of the US/China summit may not have hit expectations (China headline tariffs reduced to 60% or less), we would be a buyer of any near-term weakness as we feel an announcement that includes tariff relief is imminent but potential upside would be anything that addresses rare earth/semiconductor trade, a reduction on shipping fees, or a lower than 60% tariff level while a longer-term deal is negotiated. The downside risk would be both parties walking away and/or a re-escalation, both are tail risks, though.

· MONETIZATION MENU – We still like longs in MegaCap Tech and Cyclicals vs. short in Defensives. At the country/region-level, we like Australia, EU, Japan, Latam, and the UK. We also like China Tech. The potential for US near-term outperformance does not turn RoW into a short.

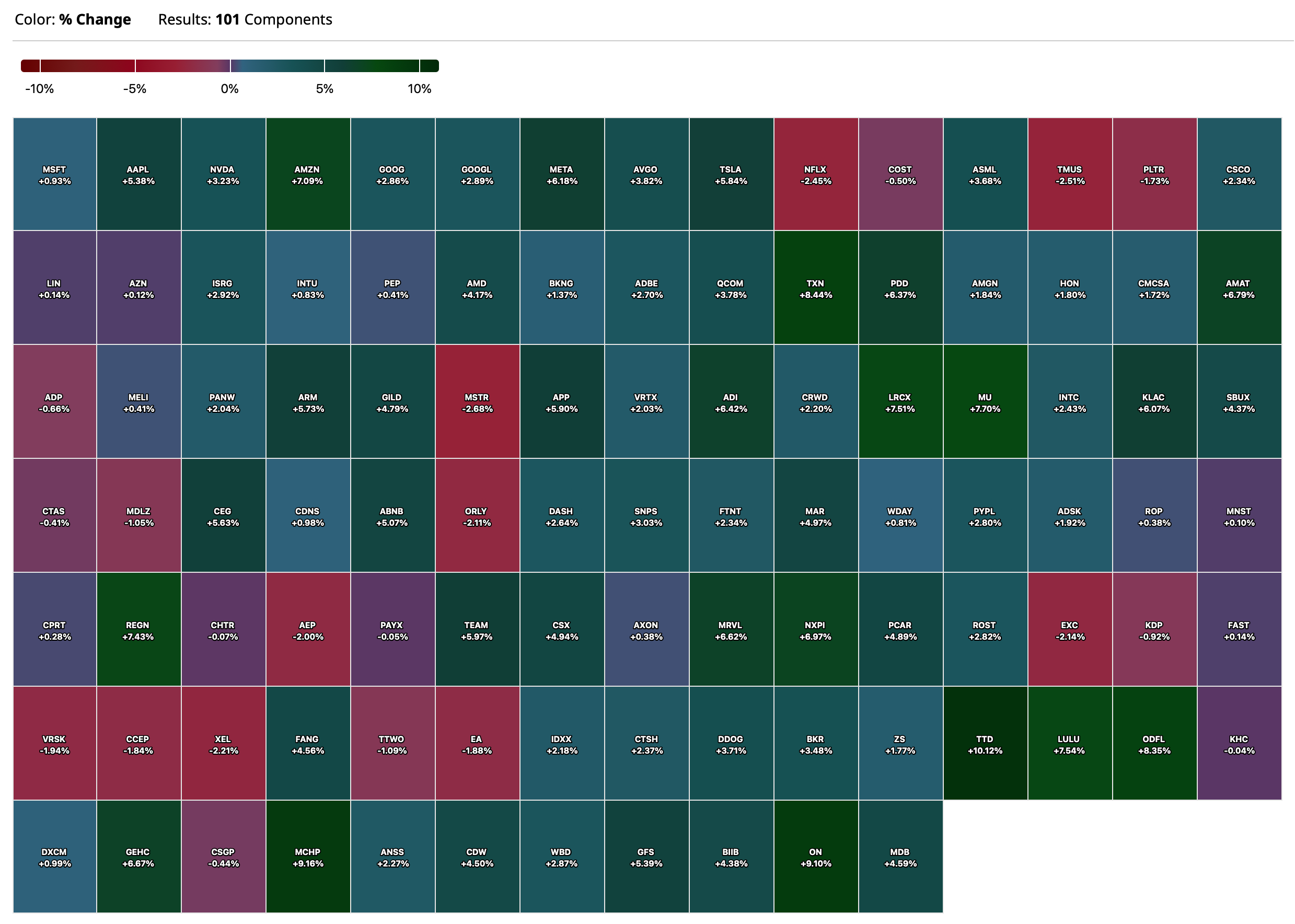

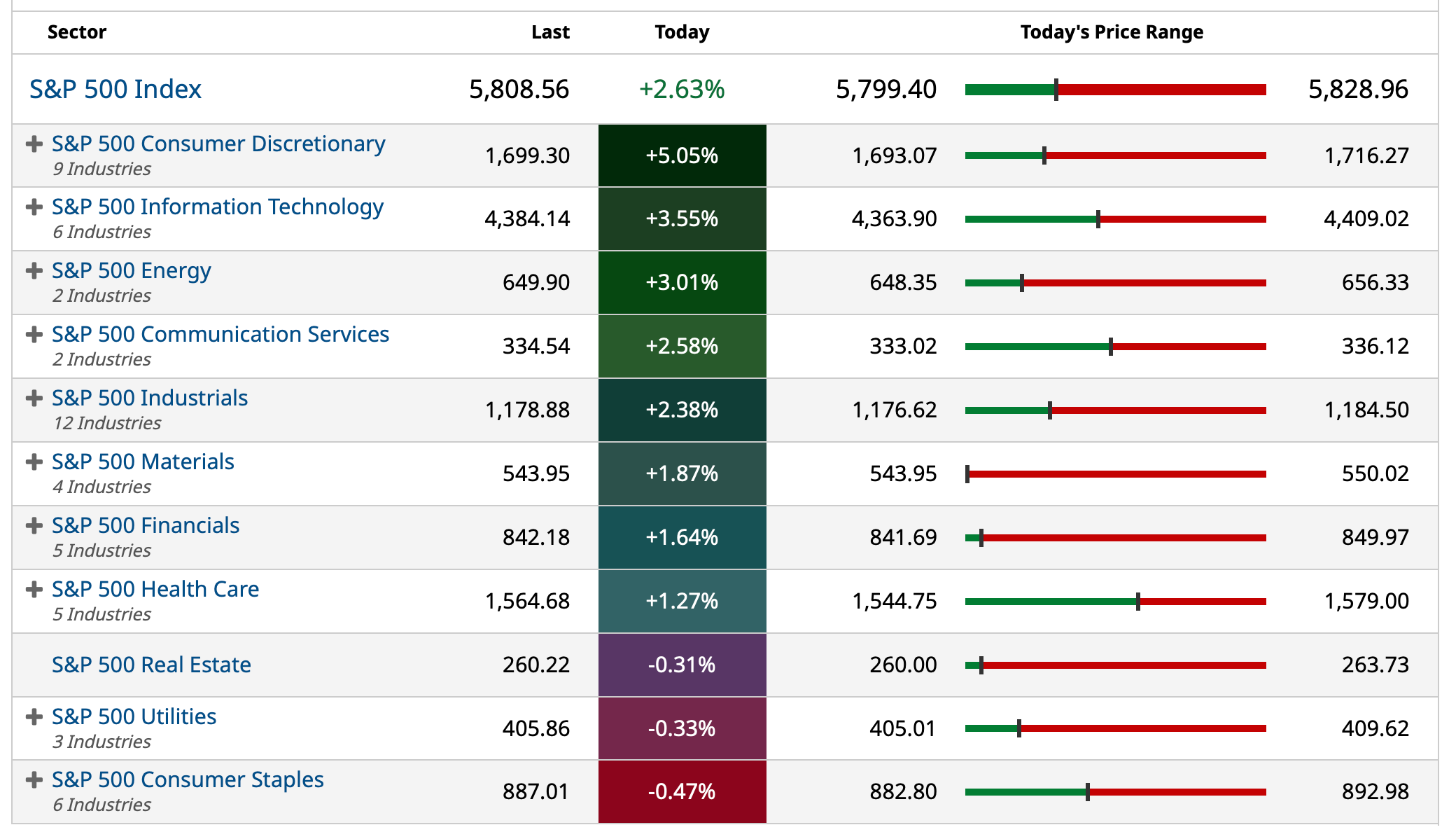

BY Doug Kass · May 12, 2025, 9:25 AM EDT

* I raised my AAPL short from very small to small - in premarket trading at $211.20.

* I sold some more AMZN at $210.30

BY Doug Kass · May 12, 2025, 9:19 AM EDT

-KDLY +560% (announced merger with BTC specialist Nakamoto)

-CTMX +133% (announces Positive Interim Data from Phase 1 Dose Escalation Study of EpCAM Antibody Drug Conjugate (CX-2051) Candidate in Patients with Advanced Colorectal Cancer (CRC); earnings)

-RGC +22% (short squeeze/momentum)

-RH +16% (tariff pause between US/China amid prospect of potential longer-term trade agreement)

-SOC +16% (Santa Barbara suit filed for allegedly withholding permits to restart ops on dormant offshore platforms)

-W +16% (tariff pause between US/China amid prospect of potential longer-term trade agreement; Argus Raised W to Buy from Hold, price target: $40)

-ALAB +13% (Morgan Stanley Raised ALAB to Overweight from Equal Weight, price target: $99)

-RDW +12% (earnings, guidance)

-BBY +11% (tariff pause between US/China amid prospect of potential longer-term trade agreement)

-NRG +9.8% (acquires a portfolio of natural gas generation facilities and a commercial and industrial virtual power plant (C&I VPP) platform from LS Power in a cash and common stock transaction valued at ~$12.0B EV; earnings)

-MRVL +8.4% (tariff pause between US/China amid prospect of potential longer-term trade agreement)

-AMZN +8.3% (tariff pause between US/China amid prospect of potential longer-term trade agreement)

-TSLA +8.1% (tariff pause between US/China amid prospect of potential longer-term trade agreement)

-WSM +7.7% (tariff pause between US/China amid prospect of potential longer-term trade agreement)

-MAT +7.3% (tariff pause between US/China amid prospect of potential longer-term trade agreement)

-AAPL +6.3% (tariff pause between US/China amid prospect of potential longer-term trade agreement; considering price hikes for Fall iPhone lineup as India is not yet ready to produce high-end iPhones at same scale as China can deliver)

-FDX +6.2% (tariff pause between US/China amid prospect of potential longer-term trade agreement)

-UPS +5.4% (tariff pause between US/China amid prospect of potential longer-term trade agreement)

-IBRX +5.3% (earnings)

-NVDA +4.5% (tariff pause between US/China amid prospect of potential longer-term trade agreement; said to have raised the official prices for almost all of its GPUs, as well as H200 and B200 chips and modules)

-CHRW +4.3% (tariff pause between US/China amid prospect of potential longer-term trade agreement)

-HAS +4.0% (tariff pause between US/China amid prospect of potential longer-term trade agreement)

-INTC +3.8% (tariff pause between US/China amid prospect of potential longer-term trade agreement)

-XOM +2.7% (Santa Barbara suit filed for allegedly withholding permits to restart ops on dormant offshore platforms)

-DXCM +2.6% (tariff pause between US/China amid prospect of potential longer-term trade agreement)

-SUP -60% (earnings, withdraws guidance citing liquidity concerns)

-LLY -3.1% (President Trump to sign order to slash some US drug prices to match those abroad)

-CHCI -2.6% (earnings)

-NVO -2.1% (President Trump to sign order to slash some US drug prices to match those abroad)

-PFE -1.9% (President Trump to sign order to slash some US drug prices to match those abroad)

BY Doug Kass · May 12, 2025, 9:19 AM EDT

Most active premarket ETFs as of 8:24 a.m. ET:

BY Doug Kass · May 12, 2025, 9:12 AM EDT

Premarket percentage movers as of 8:41 a.m.:

BY Doug Kass · May 12, 2025, 9:00 AM EDT

Along the lines of my discussion this morning:

BY Doug Kass · May 12, 2025, 8:50 AM EDT

pops4

31 minutes ago

Dougie, with the new surgeon general it appears pot will never get across the finish line for legalization.

Reply

DK

Dougie Kass

STAFF

20 seconds ago

I dont hold out for any short term legislative relief on the cannabis front - for a number of reasons previously mentioned in my Diiary. Canabis stocks probably stuck in the "weeds" for now...

BY Doug Kass · May 12, 2025, 8:38 AM EDT

With the large ramp in futures, S&P cash will exceed my upside price target of about 5750-5800.

That said I don't see much upside from the expected opening:

* The Fed remains hostile and non-accommodating (see the rise in interest rates this morning). Chasing headlines (both up and down) has been a fool's game.

There is a strong possibility that this morning's "Peak Headlines" are similar to the opposite headlines that produced a market low in April.

Positioning (bearish) is a bit concerning to my skeptical view so I will only average into short exposure (taking "baby steps") - rather than establishing an aggressive attack on the short side.

BY Doug Kass · May 12, 2025, 8:24 AM EDT

BY Doug Kass · May 12, 2025, 7:05 AM EDT

Added shorts:

* IWM $210.36

*SPY $581.72

* QQQ $507.71

BY Doug Kass · May 12, 2025, 6:55 AM EDT

Wolf Street on liquidity.

BY Doug Kass · May 12, 2025, 6:45 AM EDT

BY Doug Kass · May 12, 2025, 6:30 AM EDT

* For now the equity markets are ignoring a continuation of rising interest rates.

* The yield on the 2-year U.S. Treasury note is +11 basis points to 4.00%.

* The yield on the 10 year U.S. Treasury note is +7 basis points to 4.44%.

* The yield on the 30 year U.S. Treasury bond is +2 basis points to 4.856%.

BY Doug Kass · May 12, 2025, 6:20 AM EDT

The S&P Short Range Oscillator is still in overbought (and will obviously move to more overbought over the next few days) — at 4.67% vs. 4.49%.

BY Doug Kass · May 12, 2025, 6:11 AM EDT

BY Doug Kass · May 12, 2025, 6:02 AM EDT

* At 5:15 a.m...

Small shorts in:

* IWM $207.79

* SPY $579.90

* QQQ $506.48

BY Doug Kass · May 12, 2025, 5:52 AM EDT

BY Doug Kass · May 12, 2025, 5:41 AM EDT