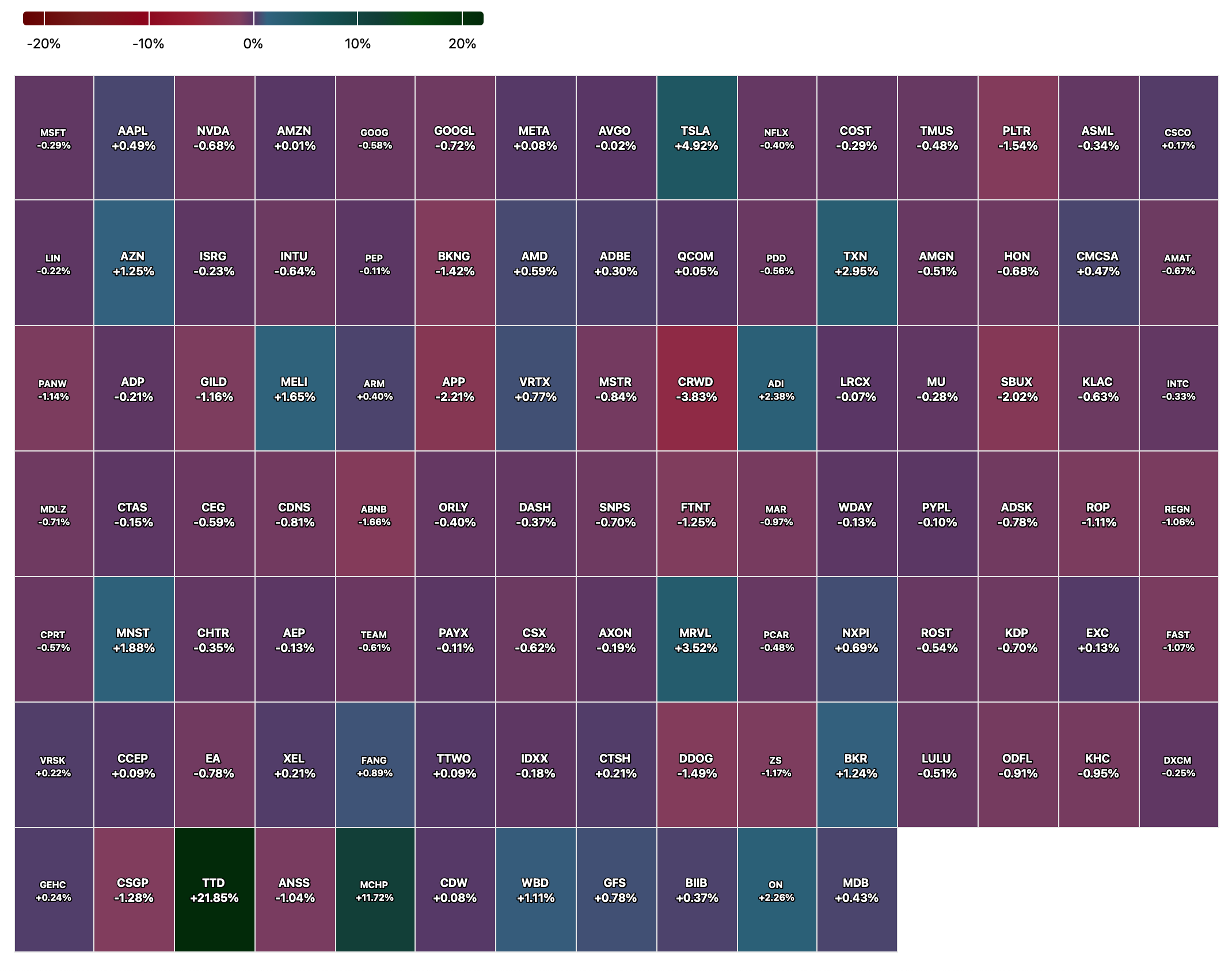

Friday's Closing Market Stats

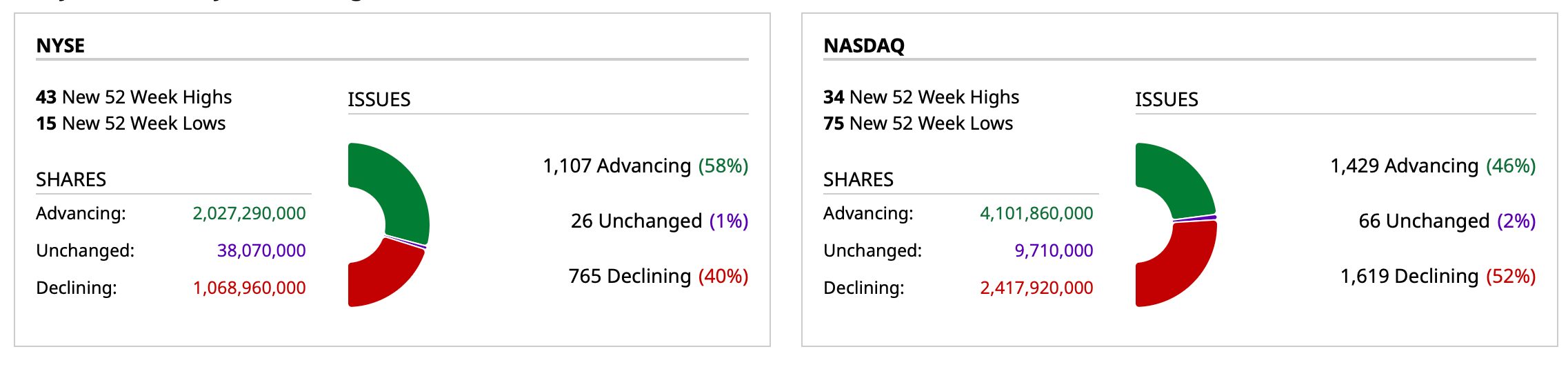

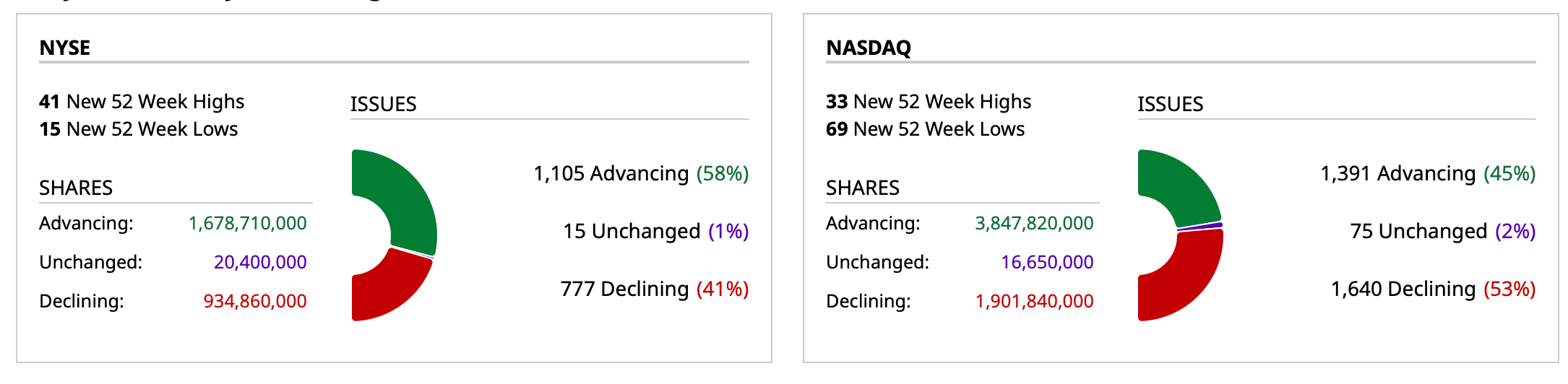

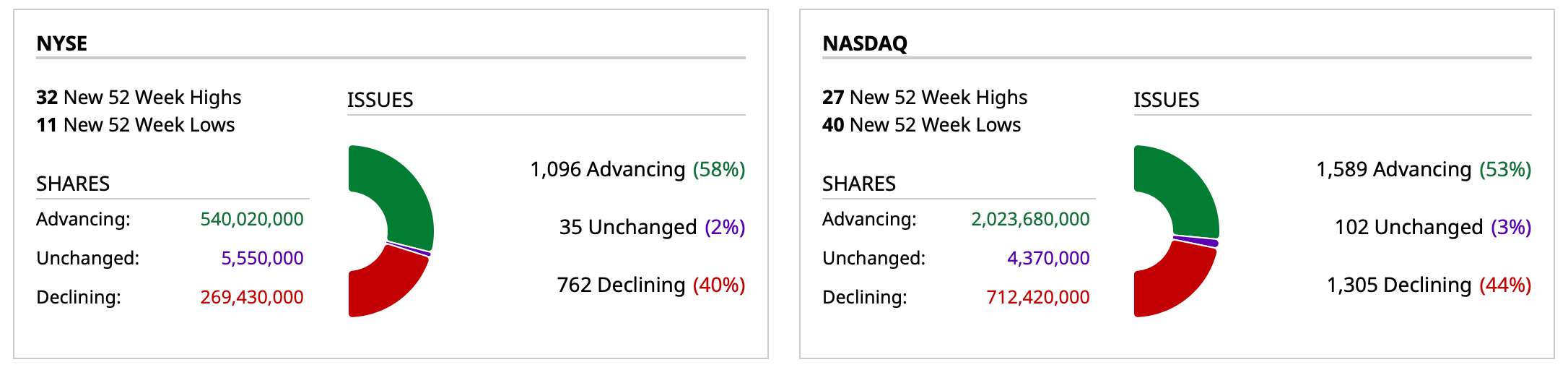

Closing Breadth

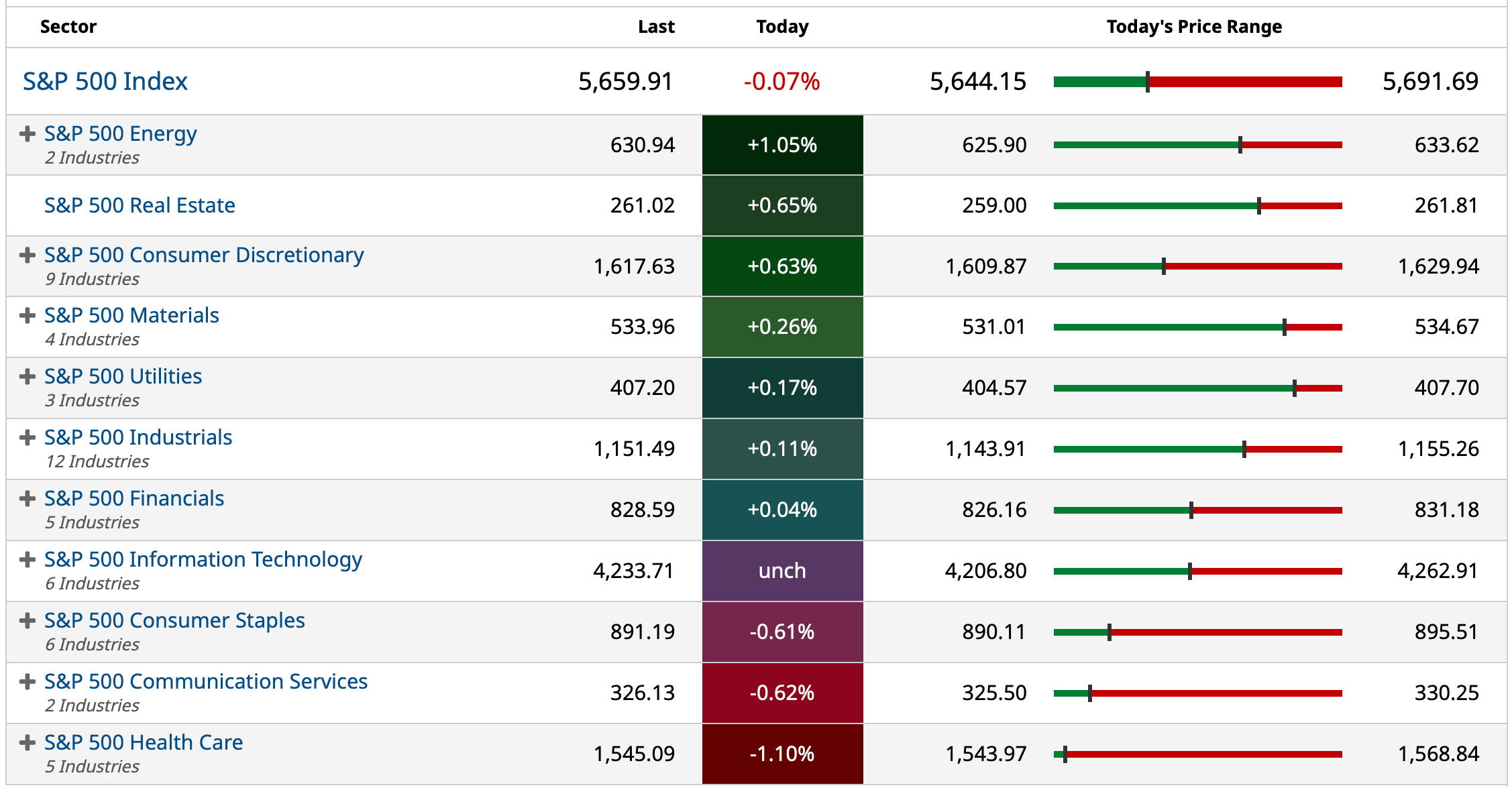

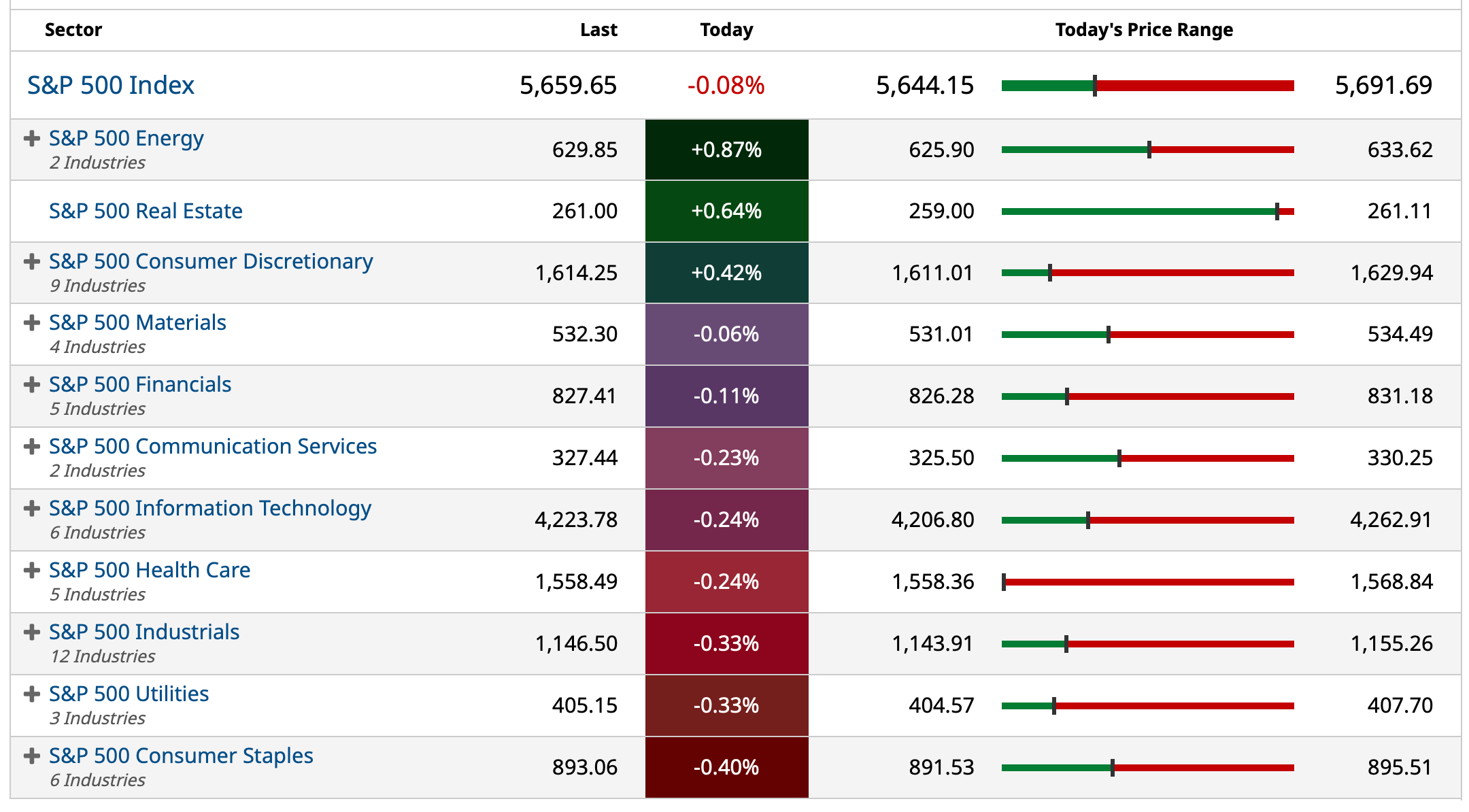

S&P 500 Sectors

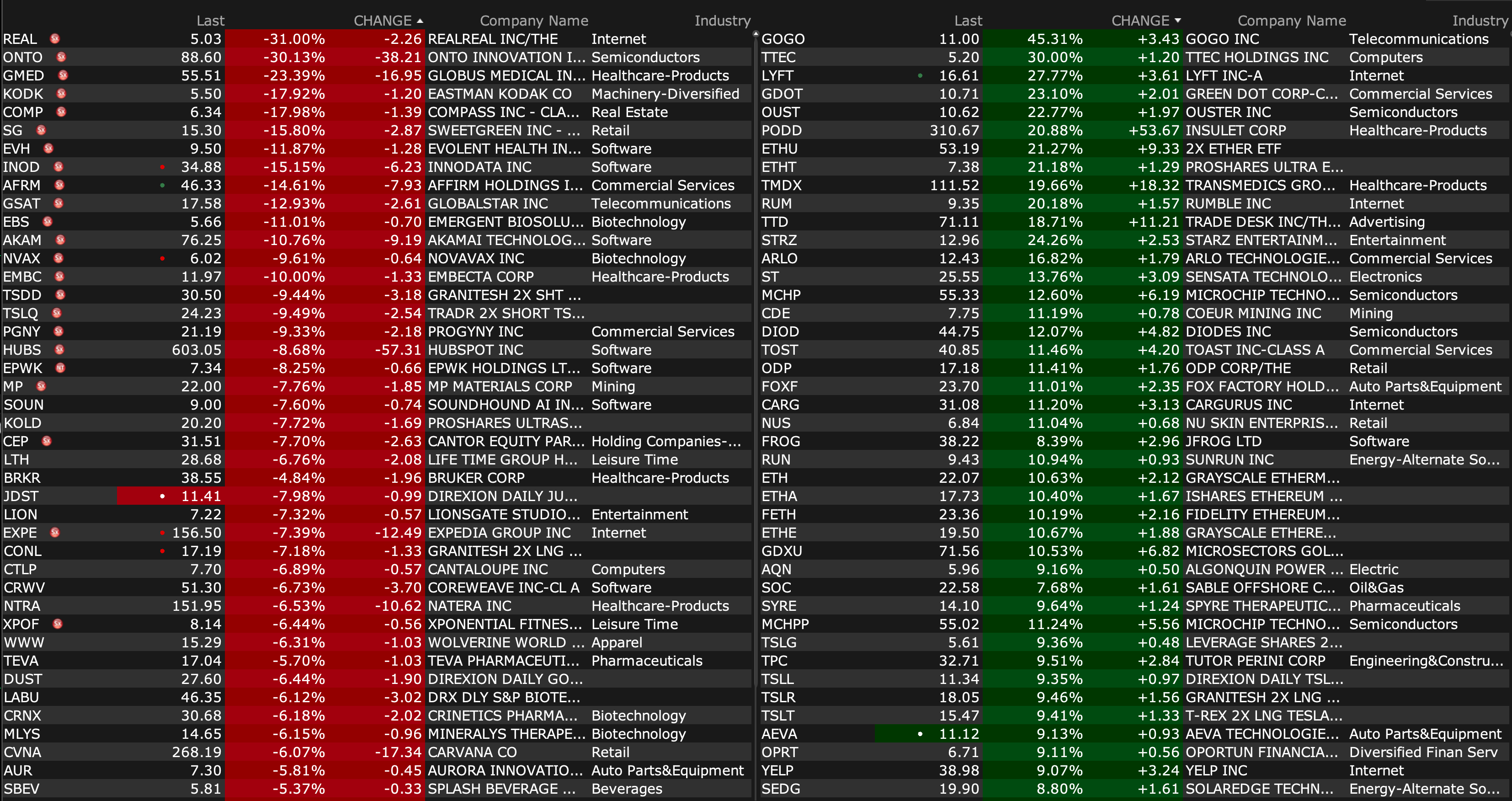

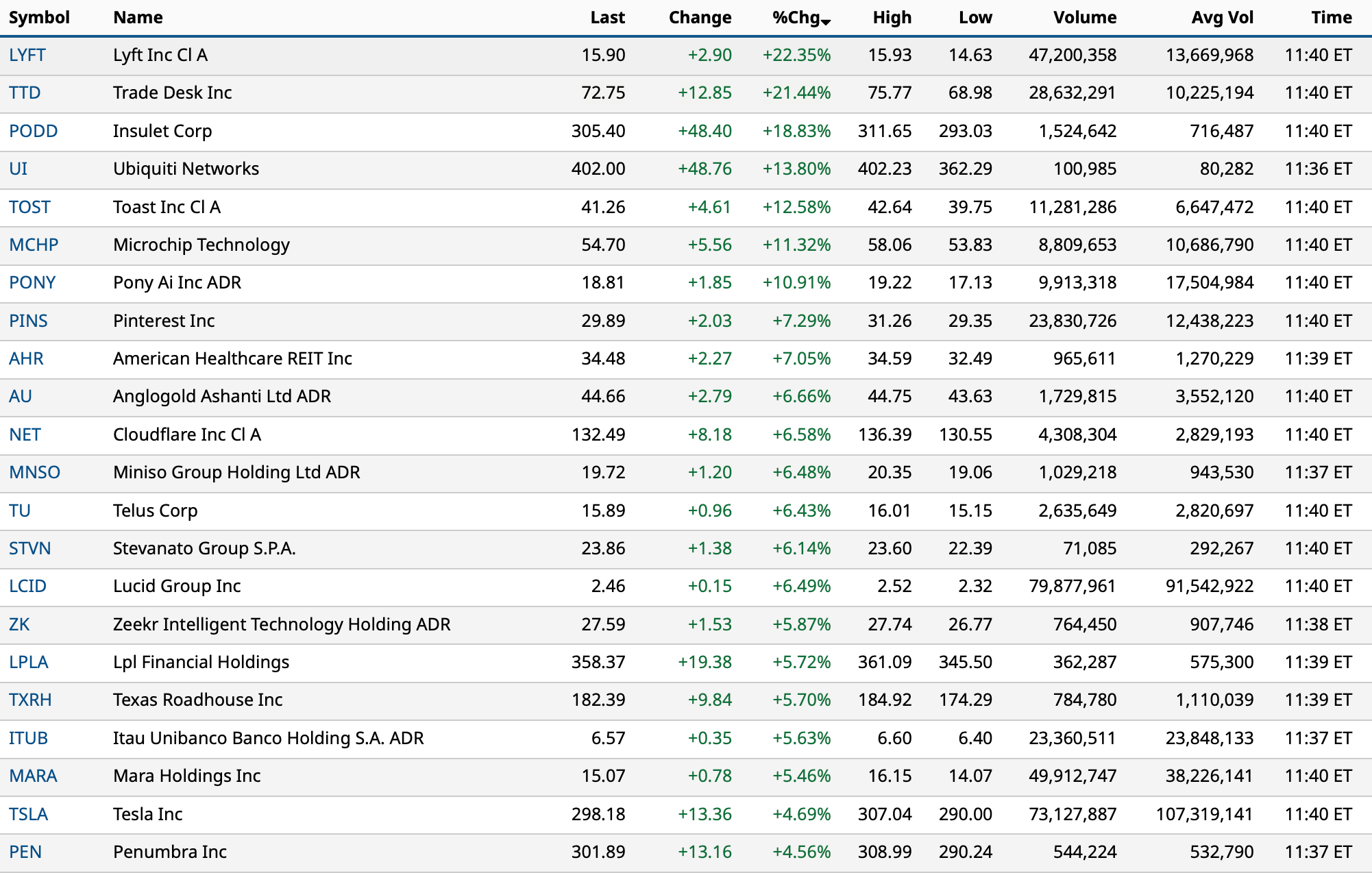

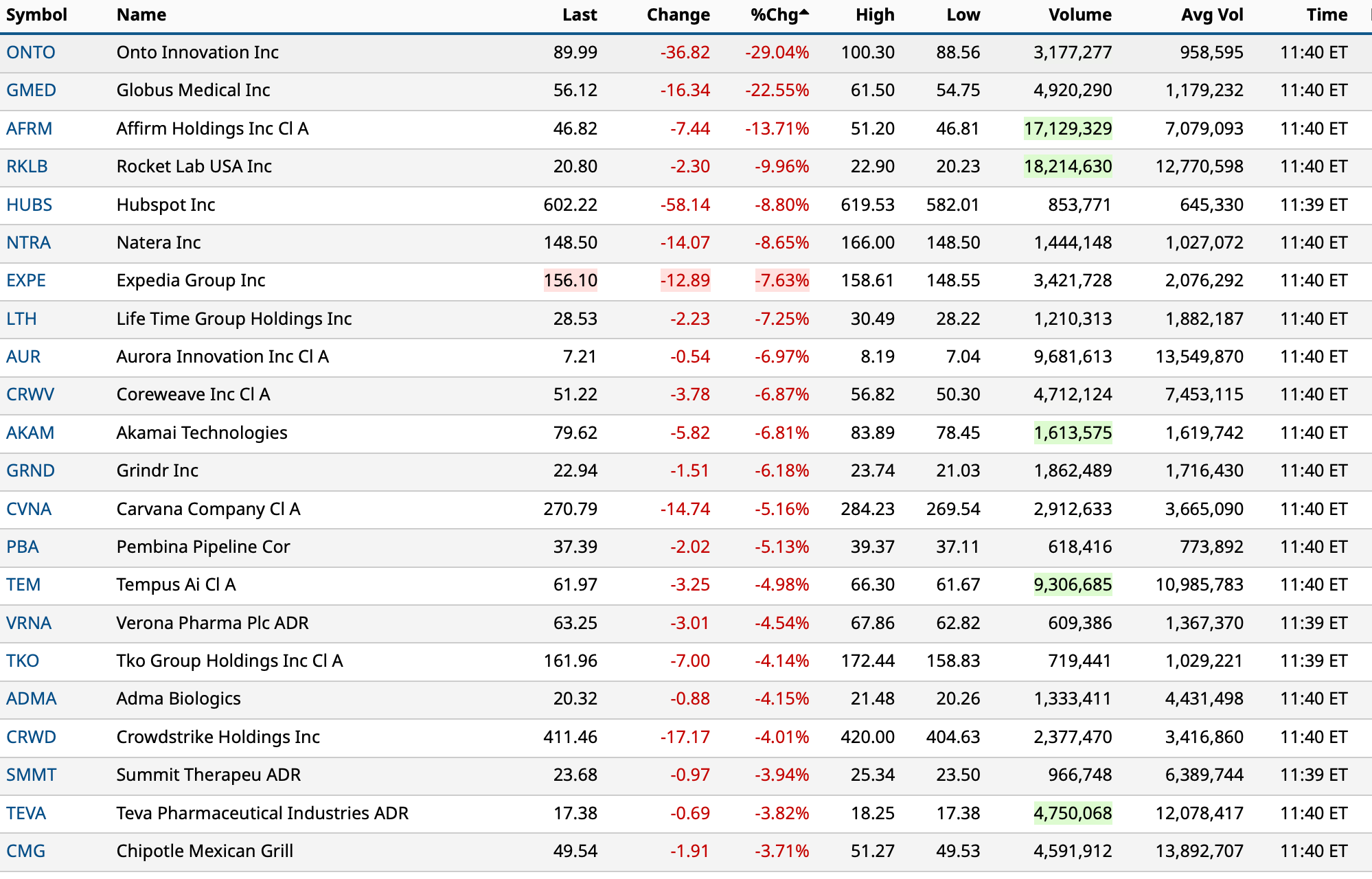

% Movers

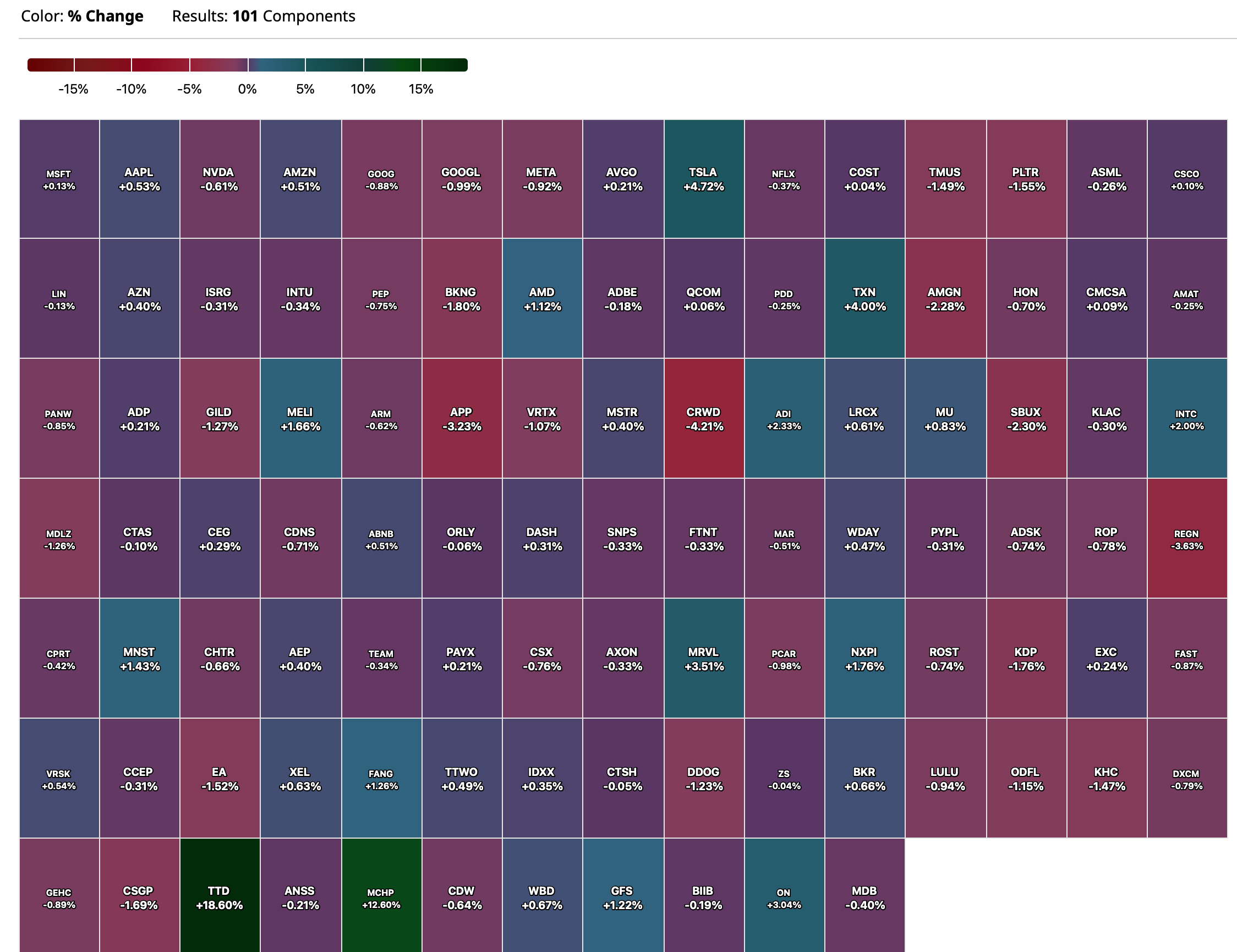

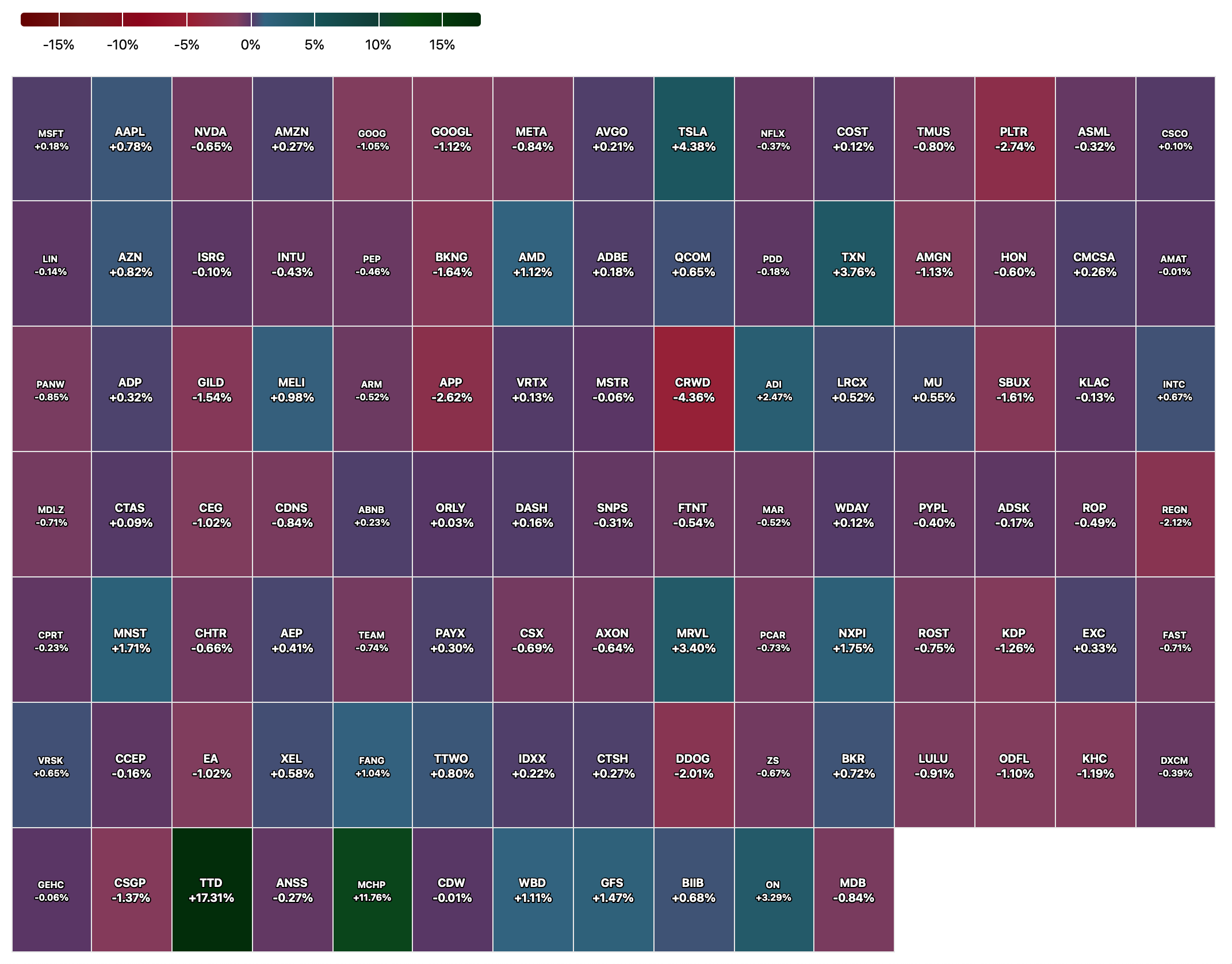

Nasdaq 100 Heat Map

BY Doug Kass · May 9, 2025, 4:38 PM EDT

BY Doug Kass · May 9, 2025, 4:38 PM EDT

Thanks for reading my Diary today and all week.

I hope my output was helpful.

Enjoy the weekend.

Be safe.

And, here is my Tweet of the Month:

BY Doug Kass · May 9, 2025, 4:18 PM EDT

At 3 p.m.:

BY Doug Kass · May 9, 2025, 3:15 PM EDT

From Peter Boockvar:

Positives

1) We now have one trade deal (letter of intent actually) on the board. Hopefully something good comes of the US/China de-escalation talks this weekend.

2) The April ISM services index rose to 51.6 from 50.8 and better than the estimate of a dip to 50.2 and compares with 53.5 in February and 52.8 in January. For perspective, the 6 month average is now 52.5. With regards to overall sector breadth, 11 saw growth vs 10 in March and 14 in February. Six saw their business contract.

3) Initial jobless claims fell back to 228k from last week's print of 241k and 2k below expectations. Continuing claims fell to 1.879mm off the highest since November 2021 in the week before at 1.908mm.

4) I understand the growing economic risks, which I completely share, but I just don't see how Jay Powell could have handled the meeting this week any differently.

5) Helped by a dip in mortgage rates, purchase applications lifted by 11.1% w/o/w after 3 weeks of declines. Refi's were up by the same amount and also after 3 weeks down.

6) We'll see in the future if this demand is a sign of consumer budget weakness or not. From Affirm: "Demand for Affirm remains excellent: y/o/y GMV (gross merchandise value) growth accelerated for the third consecutive quarter, including a strong March, which continued into April. Credit outcomes are in line with our predictions, and as always, we are watching attentively for any indicators of macroeconomic stress, and fine-tuning the settings of our models continuously."

7) From Wynn Resorts: Their Vegas business is still doing well as "April RevPAR was up slightly from 2024, slot handle was up, and group activity was as expected. So, the business through April felt pretty good. And the visibility we have into forward demand, which is primarily through our group and convention business, also looks just fine. Of course, the booking window in other channels is much shorter than group, and so we are watching those channels carefully." Macau saw almost 100% hotel occupancy and "the business in Q1 felt very good...But again, the booking window there is short, and we are watching customer activity day-to-day. Long story short, recent results have been good, but we have to acknowledge the uncertainty out there and the impact that uncertainty may have on demand."

8) From Marriott: "RevPAR in the US and Canada region rose over 3% with our luxury and full service hotels meaningfully outperforming select service properties, thanks to solid demand across both group and transient guests. International RevPAR was up nearly 6% led by growth in APAC."

9) From Disney: "Operating results at our domestic parks and experiences increased compared to the prior year quarter primarily due to growth at our domestic parks and resorts and, to a lesser extent, Disney Vacation Club and Disney Cruise Line." Helping too was "an increase in guest spending due to higher spending at our theme parks."

10) From Madison Square Garden Entertainment: They saw gains in revenue and operating income that "reflected our success in attracting a wide variety of special events, family shows, and marquee sports to our venues, robust ongoing demand for our premium hospitality offerings and the conclusion of this year's record setting Christmas Spectacular run in January. And while our business experienced a y/o/y decline in the number of concerts at our venues this quarter, we remain on track to grow the overall number of bookings events this fiscal year...From a demand standpoint, the majority of concerts at our venues continued to sell out during the quarter. In addition, food and beverage per caps at concerts at the Garden were up, while per caps at our theaters were essentially unchanged as compared to the prior year quarter."

11) From Doordash: "we haven't seen any changes in consumer behavior, even if there are changes in consumer sentiment. I've always believed, and I think we saw this - whether it was during things returning back to normal after Covid or peak inflation in '21 or '22, I think what you really saw was that food - or getting convenience delivered really is the most frequent form of spend in consumption, and food really is the most resilient category. We continue to believe that. We continue to see signs of that."

12) From Tapestry: They had a solid quarter with help globally. They said the handbags business has "proven to be durable over time because of the emotional connection that consumers have with our category." And, they are picking up more Gen Z customers.

13) From Shopify: "While our merchants proudly serve consumers across all income brackets, their buyer base skews towards higher income consumers, with more than half of their buyers in the US having incomes exceeding $100,000. We believe this helps insulate our merchants from some of the potential swings in pricing or other market factors, as higher income consumers tend to be less price sensitive. We acknowledge the uncertainty ahead and are actively monitoring our data to help us support our merchants and adapt to whatever changes may arise...Keeping all this in mind, let's now turn to the outlook. Our GMV data shows continued strength through April and early May, reinforcing our confidence in outperforming the market."

14) From Avis Budget: "Overall, our rental days were in line with TSA activity y/o/y. We did, however, see a pullback in commercial demand as we transition through the quarter. This was mitigated by improved leisure demand and meaningful y/o/y volume growth with our valued partners, a trend that continued in April and will remain an area of emphasis for us moving forward."

15) From CDW: "Broadly speaking, customers remained focused on mission critical projects and must to-do's and their priorities were consistent with 2024, laser focused on operating efficiency and expense elasticity with one addition, client device prioritization, which reflected three factors: need for refresh, the upcoming Windows 10 expiration and the desire to get ahead of tariff related price increases...Federal government market growth was subdued throughout the quarter as agencies digested the impact of new policy priorities, while education growth accelerated towards the end of the quarter, driven by Chromebook demand ahead of potential price increases."

16) From Uber: "We're not seeing trade downs in terms of the kinds of restaurants that our eaters are eating at...And remember, the categories that we operate in, these are restaurants, transportation, grocery, tend to be categories that are quite consistent even during periods of macro uncertainty."

17) From Ferrari: "Please bear in mind that Q1 '25 results were not impacted in any way by the recent introduction of higher tariffs on EU cars imported in the US. Revenues and profitability grew double digits with shipments slightly higher than the previous year and product mix and personalization as the main drivers of growth."

18) From Ford: "Relative to adding manufacturing capacity in the US, for Ford, this is a continuation, not a course correction. Since 2020, we have invested $50 billion in manufacturing capacity and we have a lot of investments in-flight, including manufacturing and battery capacity in Tennessee, batter capacity in Kentucky and Michigan and manufacturing capacity in Ohio."

19) China's exports in April rose 8.1% y/o/y which was 4x the 2% estimate because of increased shipments to everyone but the US. They plunged 21% to the US while rising by 8% to the EU and by 20% to Southeast Asian countries.

20) Reflecting also the large amount of pull forward ordering, Taiwanese exports spiked by 30% y/o/y in April, well higher than the estimate of up 16%.

21) Pull forward here too, German factory orders in March rose 3.6% m/o/m, well above the estimate of up 1.3%. The breadth of orders seemed to be broad.

22) In Vietnam's also as April exports jumped 19.8% y/o/y, well better than the estimate of up 11.9%. Imports were higher by 22.9% vs the forecast of up 17%.

23) The Bank of England cut rates by 25 bps as expected to 4.25% in a 5-4 vote where two wanted a cut of 50 bps and two preferred no change. They said "There has been substantial progress on disinflation over the past two years, as previous external shocks have receded, and as the restrictive stance of monetary policy has curbed second-round effects and stabilized longer-term inflation expectations...Progress on disinflation in domestic price and wage pressures is generally continuing." They are though neutral on what happens next.

24) The Swedish Riksbank and Norges central bank held policy unchanged as expected.

25) The PBOC cut its 7 day reverse repo rate by 10 bps to 1.40%. This is their benchmark rate and also trimmed the reserve requirement ratio by 50 bps to 6.2%. They estimate this RRR cut will result in an extra 1 trillion yuan (about $138b) of fresh liquidity.

26) The Chinese consumer is not laying down as the Golden Week visitation figures out of Macau rose sharply. According to Inside Asian Gaming, "it was Friday that saw a massive surge when 221,968 visitors entered Macau - a new record for the highest single day number of visitors to Macau since the pandemic. It was also the highest single day entry figure since February 2019...Compared to the 604,395 visitor arrivals during last year's May Day Golden Week, this year saw an increase of around 33%."

27) The final April Eurozone services PMI was revised to basically the flat line of 50.1 vs the initial figure of 49.7. Spain and Italy on the services side continue to outperform Germany and France, helped by tourism. The UK services PMI was left little changed at 49 but the first time its below 50 since October 2023.

28) More optimism about the Eurozone economy was apparent in the Sentix Eurozone economic confidence index that rose to -8.1 from -19.5 and above the estimate of -11.5. It's actually back to the average over the past 6 years which captures pre Covid data. The Sentix said "The dust is settling...Investors are acknowledging the calm response to US tariffs so far" and they believe that "the main victims of Trump's tariff policy are the US economy and, to some extent, the economies of China and Switzerland. However, the period of uncertainty is probably not over yet."

Negatives

1) My 6:45am Phoenix to Newark flight today is now scheduled to take off at 12:50pm, assuming it doesn't get delayed for a 6th time. When will enough lessons be learned that crucial services like mail, rail and airlines, among others, in the US should be privatized? This is currently 3rd world type reliability.

2) The modest trade agreement with the UK will still leave a 10% tariff on incoming imports proving that this rate will not just be a base rate for the world but also that tariff use is not all about trade fairness and is rather more about outright protectionism hoping this time will end up prosperously and thus quite differently than what history has proven otherwise.

3) To legitimately save trade between the US and China, the end of the day tariff rate really can't be more than 20% and even that would be tough for many.

4) Within the NY Fed's Consumer Expectations Survey, One yr inflation expectations continue to rise, moving to 3.6%, up 20 bps and to the highest since July 2022 which was around the peak CPI print. The further out 5 yr view slipped by two tenths to 2.7% though. Labor market concerns were evident as unemployment expectations rose to the highest since April 2020 at 44.1% right around the Covid lockdowns. While there was a drop in those believing they will lose their own job, if they do, "The mean perceived probability of finding a job in the next three months" fell by 1.9 percentage points to 49.2%, the lowest reading since March 2021. This decrease was most pronounced for respondents over the age of 60. On one's financial situation compared to a year ago, it "deteriorated sharply in April, with the share of households reporting a worse situation rising and the share reporting a better situation declining. Similarly, year ahead expectations about households' financial situations deteriorated sharply."

5) The Manheim wholesale used vehicle index rose 2.7% m/o/m in April and 4.9% y/o/y on a seasonally adjusted basis. Manheim said "The 'spring bounce' normally ends the 2nd week of April, but this year, wholesale appreciation trends continued for the entire month and were much stronger than we typically observe. We expected to see strong price appreciation in response to the tariffs, and that's exactly what came. Weekly trends showed higher values as we moved through the month, but those increases tapered off each successive week. Used retail sales remain stronger than normal, and wholesale days' supply is a bit tighter, so we will likely see less depreciation than normal over Q2."

6) Along with all the Q1 economic distortions, all beginning in March, productivity fell by .8% q/o/q annualized, though as expected. Unit labor costs were up by 5.7%, above the forecast of up 5.1%.

7) I believe a microcosm of the reality that foreign money is being repatriated out of US markets is the sharp rally seen in the Taiwanese dollar vs the US dollar.

8) From Wynn Resorts: "We had a number of CapEx projects in flight in the US, and while we had sourced for those projects, presuming some tariff impact, the current tariff rates have driven us to delay about $375 million of CapEx projects, including the Encore Tower remodel. Once tariff rates have settled, we will thoroughly re-spec and re-source the most severely affected items. While we're staying nimble, the pace of change at the moment is just too significant to commit to revised timing on that CapEx."

9) From Marriott: "While RevPAR trends internationally were strong throughout the quarter, our US and Canada regions saw softer growth in March, particularly in the select service segment. We operate a cyclical business and there is no doubt that today we are in a period of heightened macroeconomic uncertainty, especially here in the US, with many concerned about slowing economic activity and lower consumer confidence...against this macro backdrop, we are lowering our guidance for full year RevPAR growth by 50 bps due to a more cautious outlook in our US and Canada regions."

10) From Disney: International parks didn't do as well as domestic and was "attributable to Shanghai Disney Resort and Hong Kong Disneyland Resort due to lower theme park attendance and increased costs."

11) From Dine Brands: "In Q1, consumer confidence declined, and that certainly influences the challenges that our guests continue to face. Guests remain cautious with their spending, particularly the lower income guests, and we continue to see check management and trade down to lower priced items."

12) From Bloomin' Brands: "We had a disappointing February, including Valentine's Day week. We continue to operate in a choppy macro environment. In Q2, we have seen some consumer pullback with a softer Easter holiday than anticipated...specifically where we saw the most pressure is the households under $100,000. They seem to be the most pressured. We're seeing apps and desserts hold up well. It's liquor, beer, wine that started to tick down a bit. And we're just seeing a consumer that's just being very cautious, watching their spending."

13) From Wendy's: US comps fell 2.8%. "This was driven by adverse weather in January an February coupled with a weaker than expected consumer environment throughout the month of March." With regards to March, "as the month progressed, consumer confidence deteriorated, leading to a reduction in demand...Due to the high degree of uncertainty in the market, our updated outlook assumes that the current consumer environment persists throughout the remainder of the year."

14) From Cleveland Cliffs: "Underlying these weak results was the lagged impact of very low steel prices that we were exposed to during the 2nd half of 2024 and into the beginning of 2025. The implementation of across-the-board tariffs on foreign steel under Section 232 executed by President Trump on March 12 was the most relevant and necessary action to eliminate unfairly priced competition. The entire domestic industry, Cleveland Cliffs included, continues to suffer and we're starting to see a more consistent business environment and improved pricing in April and May." As they sell into the US automotive market, they welcome the tariffs on imported vehicles. In the meantime, until their business overall picks up, "Between March and May of 2025, Cliffs made the decision to fully or partially idle six facilities."

15) From CDW: They forecast 2025 US IT market growth "to be in the low single digits on a customer spend basis with a CDW growth premium of 200 bps to 300 bps."

16) From On Semiconductor: "Although we began to see early signs of stabilization with favorable booking trends towards the end of the first quarter in certain parts of the industrial end market, inventory digestion persists and customers remain cautious, as I described last quarter."

17) From Uber: They saw "a bit more growth internationally than the US, especially in the travel sector that affected overall price/mix." And specifically with the US "that's a bit due to that lower inbound US travel, which comes with lower gross bookings per trip."

18) From Expeditors International: "Subsequent to March 31, 2025, we are seeing early signs that China to US ocean volumes are declining significantly. While some of these volumes are shifting to other lanes, as customers look to mitigate their exposure to China specific tariffs, it is too early to know what the overall decline in volumes might be. Speculation regarding additional tariffs may cause more customers to pause or cancel shipment entirely. While carriers have shown a willingness to manage capacity, the current environment is so unsettled that they simply may not be able to do enough to keep rates from continuing to fall if consumer resilience fades and the capacity/demand imbalance becomes significant in certain lanes...We believe that uncertainty is likely to continue for some time, with possibly significant impacts to our industry."

19) From Celanese: "Most end-markets developed as anticipated, with persistent global demand sluggishness, especially in key segments like automotive, paints, coatings, and construction."

20) From Clorox: "Looking back to the start of the fiscal year, we expected a tougher consumer environment with increased competition and slower category growth. For the first half of the year and the first half of the third quarter, however, US consumer sentiment weakened substantially and macroeconomic and geopolitical uncertainties drove changes in shopping behaviors, resulting in temporary category impact and lower than expected sales...As we look ahead, we anticipate consumers and retailers will remain under pressure, which is reflected in our updated outlook."

21) From Diamondback Energy: US shale oil production is about to roll over. "The shale revolution has evolved from proof concept (outspend cash flow to prove up basins) to manufacturing mode (significant growth) and is now in a more mature stage of development (free cash flow generation and return of capital) . Today, geologic headwinds outweigh the tailwinds provided by improvements in technology and operational efficiency. On an inflation adjusted basis, there have only been two quarters since 2004 where front month oil prices have been as cheap as they are today (excluding 2020 which was impacted by the global pandemic) . Therefore, we believe we are at a tipping point for US oil production at current commodity prices."

22) From Ford: "Based on what we know now, our expectations of how certain details will resolve around tariffs, we've estimated the gross impact of tariffs for full year total company EBIT of $2.5 billion and a net impact of $1.5 billion."

23) China said its private sector weighted Caixin April services PMI fell to 50.7 from 51.9 and vs expectations of 51.8. Caixin said the softer figure "was driven by a slower and only marginal rise in new business, which in turn was impacted by recent tariff announcements. Business sentiment dipped to the lowest level seen since February 2020, while staffing levels continue to fall."

24) Vietnam's April manufacturing PMI fell to 45.6 from 50.5 on the obvious trade worries.

BY Doug Kass · May 9, 2025, 3:03 PM EDT

No trades after my last report!

BY Doug Kass · May 9, 2025, 2:50 PM EDT

Arguably, equities are overvalued and overbought.

And many of the components of Tom Lee's Granny Shots ETF (e.g. MSTR, PLTR, GEV, MSFT, PGR, etc.) are among the most overvalued and overbought equities extant. Holdings – Fundstrat Granny Shots ETF

Ergo, GRNY is a conservative way of shorting some of the most exploited areas of the equity market.

For more information, here is the ETF's website. Fundstrat Granny Shots ETF

Only four weeks ago (April 7th) GRNY traded at $15. Last sale was $19.78.

BY Doug Kass · May 9, 2025, 12:58 PM EDT

Scott Galloway's No Mercy/No Malice... "Brain Drain."

BY Doug Kass · May 9, 2025, 12:45 PM EDT

Speaking of TerrAscend, this morning's The Dales Report had a good interview with the company's Chairman, Jason Wild.

BY Doug Kass · May 9, 2025, 12:25 PM EDT

- NYSE volume 7% below its one-month average;

- NASDAQ volume 14% above its one-month average;

BY Doug Kass · May 9, 2025, 12:15 PM EDT

I added to this cannabis name this morning.

BY Doug Kass · May 9, 2025, 12:03 PM EDT

In terms of getting some near-term sense of direction (on an intraday basis) I would begin to focus on financials.

Some private equity stocks are -$2 from the lows and money centers have had a great run and look overbought (I have small positions in both).

I would not be adding to any financial equity at this point.

BY Doug Kass · May 9, 2025, 11:30 AM EDT

Kdog88

1 hour ago

CAPE near 35x

https://www.multpl.com/shiller-pe

Buffet Indicator at 188%

https://www.gurufocus.com/stock-market-valuations.php?width=400&height=240

BY Doug Kass · May 9, 2025, 10:50 AM EDT

I covered my index short calls for a nearly $5 gain in both SPY calls and QQQ calls - in a matter of minutes.

I plan to reshort on strength.

BY Doug Kass · May 9, 2025, 10:47 AM EDT

I've got a new buy, HHH, getting jiggy.

BY Doug Kass · May 9, 2025, 10:30 AM EDT

* Cash as a percentage of assets...

BY Doug Kass · May 9, 2025, 10:05 AM EDT

The Republican party is considering an increase in the top rate (from 37% to 39.5%) for families with $2.5 million or more of income.

There are 70,000 U.S. household that make over $2.5 million annually.

The proposed increase of 2.5% translates into less than $5 billion of extra tax revenues for the U.S. Treasury (if we assume each family makes $2.5 million - obviously there are much higher earners, but not that many!).

The $5 billion compares to an annual deficit $2 trillion.

Why all the fuss?

What am I missing... or what are the Republicans missing?

From my pal Charlie Gasparino:

BY Doug Kass · May 9, 2025, 9:50 AM EDT

BY Doug Kass · May 9, 2025, 9:50 AM EDT

* With S&P cash +23 handles, I am back shorting Index calls (in the money for May expiration)

*Shorted more: RSP $173.21, Fundstrat Granny Shots US Large Cap ETF (GRNY) $19.90 and IWM $201.74.

* Adding to cannabis Terrascend Corp (TSNDF) $0.39 after a good EPS print.

BY Doug Kass · May 9, 2025, 9:50 AM EDT

From Peter Boockvar:

Time for a stock market sentiment check with us back to the recent highs again and above the April 2nd close. The CNN Fear/Greed index on the day before the 90 day pause on April 8th closed at just 3. Defined as 'Extreme Fear' we could have also called it 'Extreme Panic' as it can't go below zero. Yesterday it was 62 about in the middle of the 'Greed' box. To be clear, this index is measuring what market participants are actually doing by measuring breadth, put/call, credit spreads etc...

Yesterday the AAII individual investor survey which just surveys mood, along with Investors Intelligence, still has Bears well above Bulls but a bit less so. Bears fell by 7.8 pts to 51.5, an 11 week low while Bulls rose by 8.5 pts to 29.4, a 13 week high. In the II survey, Bulls are almost back above Bears at 32.1 vs 28.8 last week while Bears rose a touch to 33.9 from 32.7 with those expecting a Correction down by 4.5 pts to 34.

Bottom line, the extreme bearishness post "Liberation Day" that set the stage for the post April 9th rally since is slowly slipping away but certainly nothing extreme on the bull side. What this means for short term market action, I don't know but expectations it seems are elevated that all the trade worries will be solved by deals and all will be ok. I think the genie is not going back in the bottle.

Yesterday's April NY Consumer Expectations Survey reflected a cautious consumer with higher inflation expectations, a weakened job outlook and worries about their financial situation.

One yr inflation expectations continue to rise, moving to 3.6%, up 20 bps and to the highest since July 2022 which was around the peak CPI print. The further out 5 yr view slipped by two tenths to 2.7% though.

Expectations for higher prices was broad as they rose for homes, rents, gasoline, medical care, and cost of college while falling a touch for food.

Labor market concerns were evident as unemployment expectations rose to the highest since April 2020 at 44.1% right around the Covid lockdowns. While there was a drop in those believing they will lose their own job, if they do, "The mean perceived probability of finding a job in the next three months" fell by 1.9 percentage points to 49.2%, the lowest reading since March 2021. This decrease was most pronounced for respondents over the age of 60.

Earnings growth expectations slipped to the lowest since December 2023 and household income expectations fell to the weakest since April 2021.

Notwithstanding the job market worries and maybe reflecting purchase pull forward, there was a 30 bps rise in nominal spending growth. "This increase was relatively broad-based across age and education groups."

Finally on one's financial situation compared to a year ago, it "deteriorated sharply in April, with the share of households reporting a worse situation rising and the share reporting a better situation declining. Similarly, year ahead expectations about households' financial situations deteriorated sharply."

Speaking of the out of home eating habits of the American consumer and their hesitant mood...

From Dine Brands, the owner of IHOP and Applebee's:

"In Q1, consumer confidence declined, and that certainly influences the challenges that our guests continue to face. Guests remain cautious with their spending, particularly the lower income guests, and we continue to see check management and trade down to lower priced items."

To this, "Across Applebee's and IHOP, the value mix increased vs Q4. At Applebee's, the value mix increased from 28% to 34% and at IHOP, that mix increased from 16% to 19% due to the rollout more broadly of house faves."

The positive, "Despite this challenging backdrop, sales, traffic, and our development pipeline each improved in March, and that positive momentum continued into April." They do though attribute a lot of the improvement in Applebee's to their 'Big Apple promotion.'

Highlighting the huge influence the spike in egg prices have had on their IHOP brand, "Q1 commodity costs rose by 8.4% y/o/y." As Applebee's doesn't really have eggs on their menu, they saw commodity costs higher by just .5% y/o/y.

From Bloomin' Brands, the owner of Outback Steakhouse, Carrabba's, Fleming's Steakhouse, and Bonefish Grill:

"We had a disappointing February, including Valentine's Day week. We continue to operate in a choppy macro environment. In Q2, we have seen some consumer pullback with a softer Easter holiday than anticipated."

"specifically where we saw the most pressure is the households under $100,000. They seem to be the most pressured. We're seeing apps and desserts hold up well. It's liquor, beer, wine that started to tick down a bit. And we're just seeing a consumer that's just being very cautious, watching their spending."

The demand for Buy Now, Pay Later remains strong as said by Affirm last night:

"Demand for Affirm remains excellent: y/o/y GMV (gross merchandise value) growth accelerated for the third consecutive quarter, including a strong March, which continued into April. Credit outcomes are in line with our predictions, and as always, we are watching attentively for any indicators of macroeconomic stress, and fine-tuning the settings of our models continuously."

Tapestry, the owner of Coach, Kate Spade and Stuart Weitzman, had a solid quarter with help globally. They said the handbags business has "proven to be durable over time because of the emotional connection that consumers have with our category." And, they are picking up more Gen Z customers.

Shopify had some interesting comments on what they are seeing, which is a very wide lens on businesses of all shapes and sizes. "This diverse merchant base gives us a solid foundation to navigate changing market conditions, providing unique stability to our business. Certain sectors or segments will require more time to address their supply chains in this environment, but many others, also represented by Shopify, can move more quickly, mitigating some of the impact to Shopify from these disruptions."

"Merchants' pivots in response to trade concerns are wide ranging, including decisions on inventory strategies, pricing changes, and sourcing selections. Consider pricing as one example. While some merchants have raised prices, we haven't seen broad based price increases yet."

"However, there remains a mix of strategies at play to navigate tariffs beyond just pricing. Merchants are considering when to change sourcing countries, when to buy inventory, or even adjusting product mix in their catalogs."

"While our merchants proudly serve consumers across all income brackets, their buyer base skews towards higher income consumers, with more than half of their buyers in the US having incomes exceeding $100,000. We believe this helps insulate our merchants from some of the potential swings in pricing or other market factors, as higher income consumers tend to be less price sensitive. We acknowledge the uncertainty ahead and are actively monitoring our data to help us support our merchants and adapt to whatever changes may arise."

Finally, "Keeping all this in mind, let's now turn to the outlook. Our GMV data shows continued strength through April and early May, reinforcing our confidence in outperforming the market."

From Avis Budget Group:

"Overall, our rental days were in line with TSA activity y/o/y. We did, however, see a pullback in commercial demand as we transition through the quarter. This was mitigated by improved leisure demand and meaningful y/o/y volume growth with our valued partners, a trend that continued in April and will remain an area of emphasis for us moving forward."

Following what Manheim said about rising wholesale used car prices, Avis said "Residual values improved throughout the quarter and this is still continuing today" due to lower inventories on the pull forward of purchases.

Cleveland Cliffs begged for steel tariffs believing that was going to be great for their business but after reporting results yesterday the stock fell 16%.

They hope the tariffs will help their business though from here on out. "Underlying these weak results was the lagged impact of very low steel prices that we were exposed to during the 2nd half of 2024 and into the beginning of 2025. The implementation of across-the-board tariffs on foreign steel under Section 232 executed by President Trump on March 12 was the most relevant and necessary action to eliminate unfairly priced competition. The entire domestic industry, Cleveland Cliffs included, continues to suffer and we're starting to see a more consistent business environment and improved pricing in April and May."

As they sell into the US automotive market, they welcome the tariffs on imported vehicles. In the meantime, until their business overall picks up, "Between March and May of 2025, Cliffs made the decision to fully or partially idle six facilities."

Wrapping up with some international figures, China's exports in April rose 8.1% y/o/y which was 4x the 2% estimate because of increased shipments to everyone but the US. They plunged 21% to the US while rising by 8% to the EU and by 20% to Southeast Asian countries. I assume the lift to ASEAN countries was China re-routing exports for still possible a US destination. Imports were little changed, better than the estimate of down 6%.

BY Doug Kass · May 9, 2025, 9:35 AM EDT

-CRVS +27% (earnings; data from Cohorts 1-3 of Placebo-Controlled Phase 1 Clinical Trial of Soquelitinib for Atopic Dermatitis continue to demonstrate favorable safety and efficacy profile)

-GOGO +25% (earnings, guidance)

-PHX +21% (earnings; to be acquired by WhiteHawk for $4.35/shr in $187M all-cash deal)

-TTD +15% (earnings, guidance)

-PINS +13% (earnings, guidance)

-LYFT +10% (earnings, guidance)

-MCHP +9.7% (earnings, guidance)

-ANIP +8.7% (earnings, guidance)

-TOST +8.1% (earnings, guidance)

-NMAX +6.7% (signs with Hulu+ Live TV for Carriage)

-AUR +4.3% (earnings)

-DKNG +3.7% (earnings, guidance)

-BP +2.8% (reportedly rivals considering potential takeover)

-IOVA -36% (earnings, guidance)

-WOLF -21% (earnings, guidance)

-GMED -14% (earnings, guidance)

-ONTO -14% (earnings, guidance)

-EXPE -9.8% (earnings, guidance)

-GRND -8.1% (earnings, guidance)

-AFRM -6.4% (earnings, guidance)

-ZIP -4.6% (earnings, guidance)

-NSPR -3.9% (earnings)

-MNST -3.7% (earnings, color)

-HIMS -3.0% (prices upsized $870M (prior $450M) Convertible Senior Notes Offering)

-AKAM -2.6% (earnings, guidance)

BY Doug Kass · May 9, 2025, 9:26 AM EDT

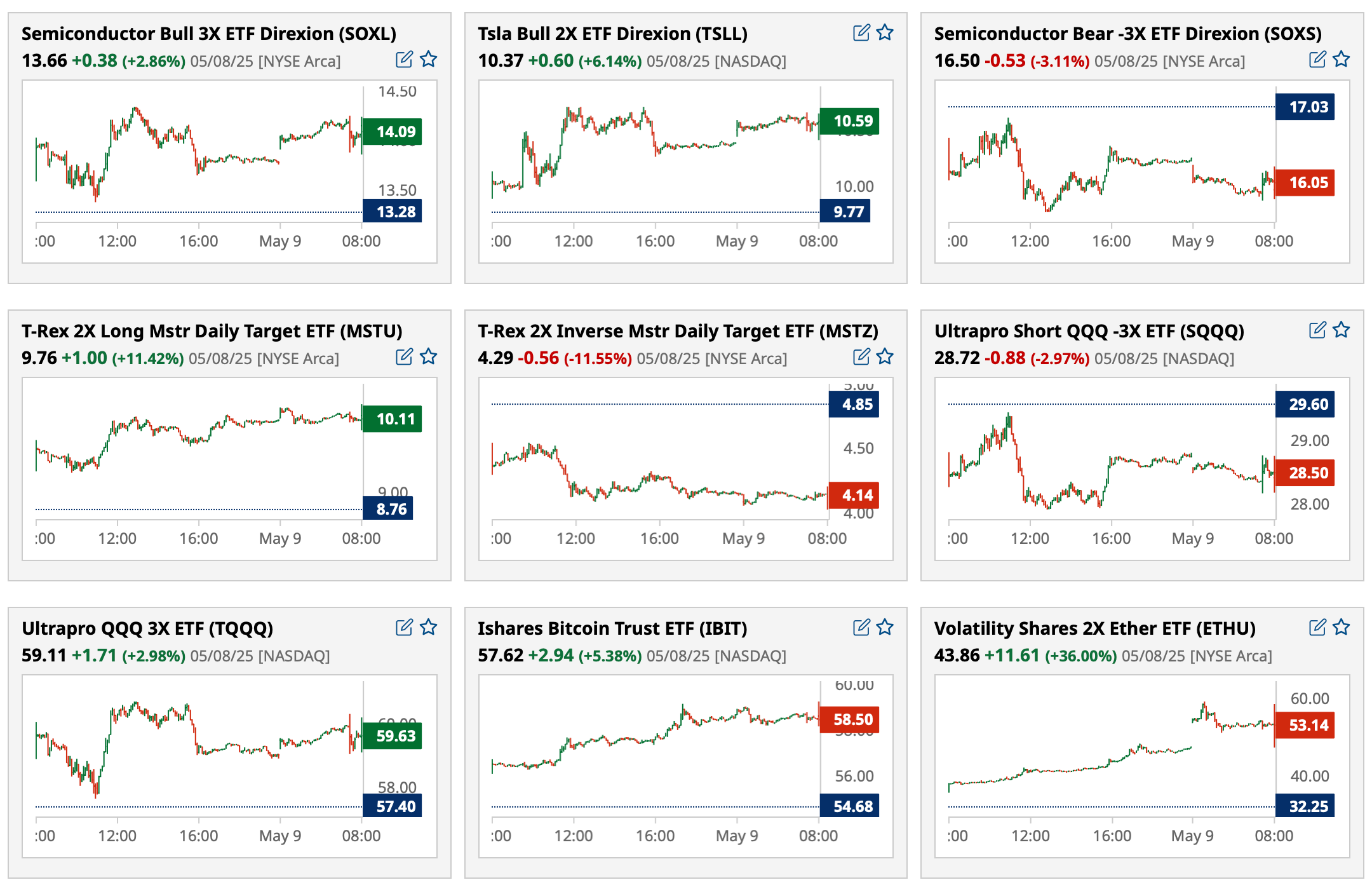

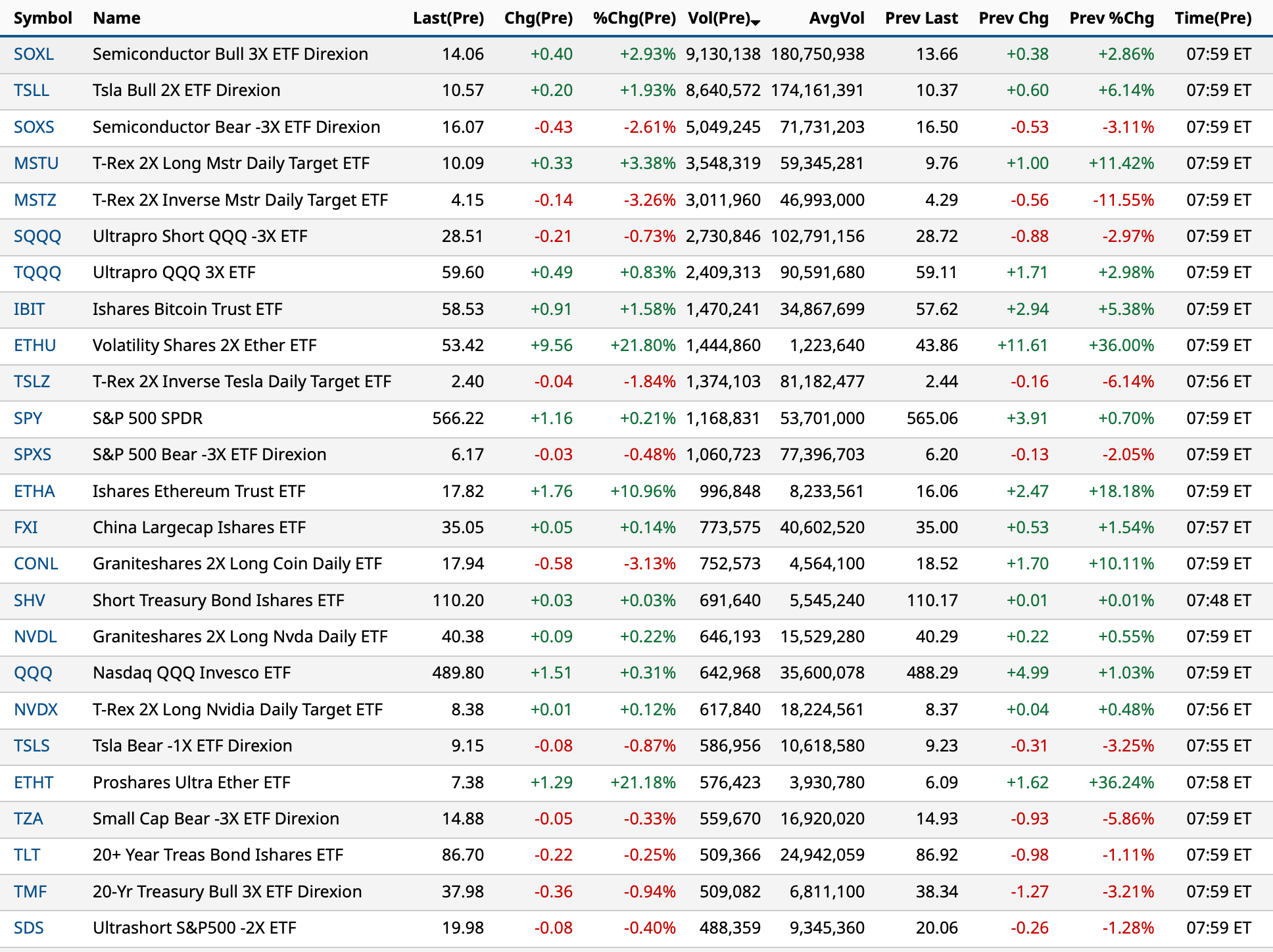

Most active premarket ETFs as of 7:59 a.m. ET:

BY Doug Kass · May 9, 2025, 9:00 AM EDT

Premarket percentage movers as of 8:16 a.m. ET:

BY Doug Kass · May 9, 2025, 8:50 AM EDT

5:55 a.m. ET: Fed Board Governor Barr (Voter) speaks on "Artificial Intelligence and the Labor Market" before the Reykjavik Economic Conference organized by the Central Bank of Iceland and the Center for International Macroeconomics at Northwestern University (Text available. Q&A from moderator. Webcast: );

6:45 a.m.: Fed Board Governor Kugler (Voter) speaks on "Maximum Employment" before the Reykjavik Economic Conference organized by the Central Bank of Iceland and the Center for International Macroeconomics at Northwestern University (Text available. Q&A from moderator.);

8:30 a.m.: Fed Bank of New York President Williams (Voter) speaks before the Reykjavik Economic Conference organized by the Central Bank of Iceland and the Center for International Macroeconomics at Northwestern University, Reykjavik, Iceland (Text and moderated Q&A expected.);

8:30 a.m.: Fed Bank of Richmond President Barkin (Non-Voter) participates in a fireside chat before the Loudon County Chamber of Commerce, Ashburn, VA (No livestream. No text. Media Q&A follows event);

10 a.m.: Fed Bank of Chicago President Goolsbee (Voter) gives welcome and opening remarks before the "Fed Listens: Perspectives from the Midwest" event, Chicago, IL (Livestream available. Embargoed text TBD); 10:00AM: New York Fed Bank Director of Research and Head of the Statistics Group Athreya speaks on NY State Large Credit Unions CEO Roundtable;

11:30a.m.: (VIA PRE-RECORDED VIDEO) Fed Bank of New York President Williams (Voter); Board of Governors of the Federal Reserve System Waller (Voter) speak on "Taylor Rules in Policy" before the Hoover Monetary Policy Conference, Stanford, CA (No text);

7:45 p.m.: Fed Bank of Cleveland President Hammack (Non-Voter); Fed Bank of St. Louis President Musalem (Voter) and Board of Governors of the Federal Reserve System Cook (Voter) speaks on monetary policy before the Hoover Monetary Policy Conference, Stanford, CA (Text TBD. Audience Q&A expected. Livestream available);

BY Doug Kass · May 9, 2025, 8:40 AM EDT

BY Doug Kass · May 9, 2025, 8:35 AM EDT

BY Doug Kass · May 9, 2025, 8:20 AM EDT

BY Doug Kass · May 9, 2025, 8:15 AM EDT

As I recently mentioned in my Diary, during my five decades investing I have NEVER interviewed a company management nor watched a Fin TV interview in which the mgt was negative on their outlook.

Case in point Affirm Holding's AFRM interview on The Death Star now

As Warren Buffett wisely said (I am paraphrasing)..."Company managements often lie like ministers of finance on the eve of devaluation."

BY Doug Kass · May 9, 2025, 7:56 AM EDT

This tweet by the president took the S&P futures down 20 handles:

BY Doug Kass · May 9, 2025, 7:50 AM EDT

I added to my IWM short at $201.52

BY Doug Kass · May 9, 2025, 7:45 AM EDT

"The key is not knowing for sure what a stock is going to do next but knowing what it should do. Then it's a matter of determining whether the proverbial train is on schedule."

- Mark Minervini

Bonus - Here are some great charts:

About Last Month About Last Month - Carson Group

Three Charts for an "All Clear" Three Charts to Watch for an "All Clear" Signal | The Mindful Investor | StockCharts.com

The Morning Show The Morning Show for May 8 - Featuring John Kolovos

All Eyes on the Euro All Eyes on the Euro

BY Doug Kass · May 9, 2025, 7:34 AM EDT

From JPMorgan:

US: Futs are seeing a muted response after yesterday’s trade deal and Trump’s comments to buy the market. The focus is on China this weekend, but if we use the US/UK deal as a template, it is light on details with a seemingly minimal economic impact. Pre-mkt, Mag7 names are higher with Cyclicals mixed but with a bias to Quality names. Bond yields are flat to lower as the yield curve bull steepens and the USD sells off after its strongest day since Nov 6 (day after the US Pres. Election). In cmdtys, Energy continues to see a bid with WTI now above $60/bbl, Ags higher, and precious over base. Macro data and earnings are light today so today’s session will likely be investors trying to position for outcomes after this weekend’s US/China summit.

and..

EQUITY & MACRO NARRATIVE

Yesterday, we had posted: Some questions [on potential trade deals] remain: (i) are these expected to be full trade deal, which typically take 2-3 years to negotiate; (ii) if these are more MoU than full trade deal, then how are tariffs treated while a full deal is negotiated; (iii) if the US still pursuing a strategy of trying to isolate China. Of these questions, the status of tariffs is the most important with the most bullish outcome being a suspension of tariffs, or rollback to 2024 levels, and the most bearish being a reversion to Liberation Day levels.

The US/UK answers those questions and until we see a second deal hit the tape will be the template for evaluating other deals, per Lutnick. Yes, this can be considered a full trade deal with addendums expected. No, tariffs will not be suspended during the negotiation of other ancillary trade deals. Unclear if the US is still trying to force other countries to isolate China. The outcome with US/UK is de minimis though the risk/reward of having taken the UK through Liberation Day remains uncertain. Now, as we turn our attention to this weekend’s US/China summit, my colleague Ilan Benhamou, from our Equity Derivatives team, gives us the following scenario analysis:

· [10%] - DERAILMENT , "more tariffs coming" - (SPX loses 2.5%)·

[40%] - STATUS QUO , "politely agree to continue talking" - (SPX loses 1.5%)·

[35%] - BETTERMENT , "some elusive/prospective numbers are floated around but not agreed , not even in principle" - (SPX gains 1%)·

[15%] - FAIRWAY , they secretly came prepared , "tariff pause or taken down substantially to <50" - (SPX gains 3%)

This aligns with my thinking, though I may be a touch more bullish on a tariff pause outcome. That said, with Trump urging people to go out and buy stocks now, we may see continued covering into the weekend. Yesterday, our High Short Interest basket (JPTASHTE Index) closed +3.4%. Some trade war related headlines:

· Trump Hails UK Trade Framework as First of Many Tariff Deals (BBG)· Trump's UK Trade Deal Leaves Key Issues Unresolved (BBG)

· Trump says 10% is floor for tariffs; ‘Some will be much higher’ (CNBC)

· EU to launch dispute against U.S. tariffs as it sets out 95 billion euros in countermeasures (CNBC)

· Why the Bank of England governor thinks uncertainty is here to stay despite a trade deal (CNBC)

· EU Targets American Aircraft, Car Parts for Possible Tariffs if Talks Fail (WSJ)

· The Bubble Blasters and Other Chinese Goods That Are Paralyzed by Trade Chaos (WSJ)

BY Doug Kass · May 9, 2025, 7:10 AM EDT

BY Doug Kass · May 9, 2025, 6:57 AM EDT

There was nothing in the cannabis EPS reports over the last 48 hours that ameliorates the concerns of maturing state markets, burdensome debt loads and continued cannabis product price compression (and its effect on revenues, cash flow, operating profits and ability to service/refinance liabilities).

BY Doug Kass · May 9, 2025, 6:52 AM EDT

BY Doug Kass · May 9, 2025, 6:35 AM EDT

The S&P Short Range Oscillator slipped from 5.18% to 4.49%, still in the middle of the overbought.

I closed out my index shorts for a small profit on the late afternoon selloff.

I plan to reload my shorts on strength.

BY Doug Kass · May 9, 2025, 6:19 AM EDT