Thanks for Reading Today!

Thanks for reading my Diary today.

I hope my output was useful.

Enjoy the evening.

Be safe.

And congratulations to Randorama for winning the Trivia Quiz!

BY Doug Kass · May 7, 2025, 4:56 PM EDT

Thanks for reading my Diary today.

I hope my output was useful.

Enjoy the evening.

Be safe.

And congratulations to Randorama for winning the Trivia Quiz!

BY Doug Kass · May 7, 2025, 4:56 PM EDT

Likely reason for strength in last few minutes:

BY Doug Kass · May 7, 2025, 3:55 PM EDT

* For a nice profit from our cost basis...

I have moved to very small in my long private equity positions: APO, BX and KKR.

BY Doug Kass · May 7, 2025, 3:51 PM EDT

And the winner is... Randorama!

Randy

I know it was extremely low...so 4.

Dougie Kass

winner, winner chicken dinner randorama!

4x or only 4.5% of the time

amazing accomplishment

BY Doug Kass · May 7, 2025, 3:40 PM EDT

With S&P cash back +22 handles I am adding to my index short call holdings.

BY Doug Kass · May 7, 2025, 3:05 PM EDT

* The winner wins my signed book!

Since Sarge did a baseball trivia question yesterday (see below - I had the correct answer!), I thought I would do one as well today.

Dodger Stadium opened in 1962.

My cousin Los Angeles Dodgers pitcher Sandy Koufax pitched his last five seasons there.

Here were Sandy's seasonal ERAs at Dodger Stadium (all of which consisted of more than 100 innings pitched): 1.75, 1.38, 0.85 (all-time record), 1.39 and 1.52!!!!

Question: In total, cousin Sandy made 88 pitching appearances at Dodger Stadium between 1962-1966. How many times did he allow more than three earned runs in a game at Dodger Stadium during those five years?

Please answer in the Comments Section.

From yesterday:

Q) Since integration, eight MLB hitters have managed to post multiple 50+ home run seasons. Sammy Sosa and Mark McGwire each had four. Alex Rodriguez had three. They are all steroid cheats in my opinion and don't count. The other five, as far as I know, are/were legit. One batter has three and is active. The other four batters all had two such seasons and are no longer active. Name these five ballplayers.

Dougie hit this one out of the park, and got the answer almost right away. Randy did well too and got four of five.

A) The answers are...- Aaron Judge hit 50+ HR in 2017, 2022, and 2024.

- Ken Griffey Jr hit 50+ HR in 1997 and 1998.

- Mickey Mantle hit 50+ HR in 1956 and 1961.

- Willie Mays hit 50+ HR in 1955 and 1965.

- Ralph Kiner hit 50+ HR in 1947 and 1949.

BY Doug Kass · May 7, 2025, 3:00 PM EDT

From Peter Boockvar:

And the Fed says...

In the Fed's statement, they made a point to start that ex the distortions to the Q1 trade data "recent indicators suggest that economic activity has continued to expand at a solid pace." We can all quibble with that optimistic assessment. The commentary on the labor market and inflation remained the same as in the previous statement.

What was added was the obvious acknowledgement of the higher level of unknowns. "Uncertainty about the economic outlook has increased further. The Committee is attentive to the risks to both sides of its dual mandate and judges that the risks of higher unemployment and higher inflation have risen."

Bottom line, that stagflationary risk highlighted by the FOMC is a handcuff type acknowledgement that freezes them for now until they get more details on what the tariff regime globally will look like in coming months/quarters.

The response in the Treasury market was lower yields across the curve I guess on the belief that at the end of the day, that heightened 'uncertainty' will favor a focus more on the unemployment rate than the inflation one. To be clear though, today's statement did NOT lean in any one direction in terms of priorities.

I will though go with what Jay Powell said the last time we heard from him last month that he believed that stable prices were the precursor to a healthy labor market. We look forward to the 2:30pm est presser for more color.

BY Doug Kass · May 7, 2025, 2:27 PM EDT

The Fed is in no rush to cut interest rates.

Prepare for a battle royale between the administration (Trump) and the Fed (Powell).

BY Doug Kass · May 7, 2025, 2:12 PM EDT

With the Nasdaq rallying and S&P cash +25 handles I am back shorting index calls.

BY Doug Kass · May 7, 2025, 1:15 PM EDT

I'm adding to my Apple AAPL short.

BY Doug Kass · May 7, 2025, 12:30 PM EDT

I have sold out of my extremely small Google GOOGL long this morning. (Google is now a value trap, imho).

I have no intention of buying back the shares anywhere near today's prices.

In the Mag 7 universe I am only long Amazon AMZN and Meta META and short Apple AAPL.

BY Doug Kass · May 7, 2025, 12:18 PM EDT

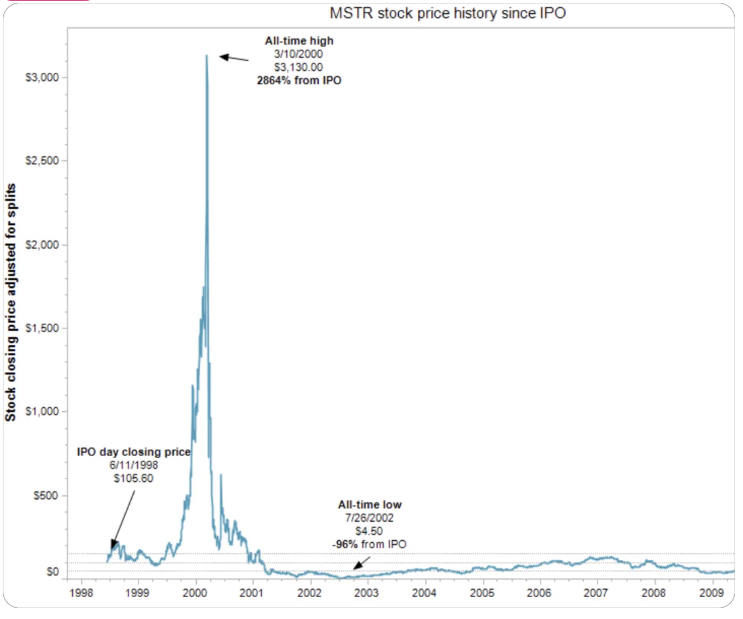

* I remain short MSTR...

TechNova

MSTR and BTC : the odd couple.

Part 1.

I cannot think of a more polarizing stock than MSTR. The former MicroStrategy now simply known as Strategy. Presumably, this implies that they are now big enough to be Macro and not just Micro.

Michael Saylor is touted as a genius by some, and as a huckster snake oil salesman by others. I find myself to be in neither camp as I try to understand, evaluate and formulate an opinion on MSTR, the stock.

When I was 12 years old, living in the South of France, a family moved in next door to us. They were from Israel. My mom baked a “welcome pie” and dragged me to meet them and welcome them to our building. As my mom spoke to the matriarch of the family, I heard that they moved to the South of France because of the world debut of a piano concerto to be performed at the Nice Opera House. I remember thinking what huge fans of classical music they must be to move here, simply to attend a performance, before I was promptly corrected by the clarification that their son, which they affectionately nicknamed “Wolfy”, wrote this concerto. Wolfy turned 5, four months before they moved in next door. Famous pianist Richard Clayderman was flown in to perform this piece, and Wolfy needed to guide him through it, which is why they moved here 3 months before the scheduled World Premiere.

If have not met or seen a “Genius” since I watched Wolfy play while seated on a phonebook with blocks attached to his feet so that he could reach the pedals.

To clarify, I am not saying Saylor is not a smart man. I have listened to him speak for probably more than 100 hours. Via interviews, podcasts, presentations and earnings, I have found him to be infinitely fascinating, and a cornucopia of historical facts and data. I can honestly say that I have always learned something new as a result of listening. Be it about math, physics, history or geography. He seems to know a lot about a lot.

That being said, as an investor in MSTR, Michael Saylor is a CEO. I look at him through that prism to determine his worth in that capacity. As a CEO, he has not shown to be anywhere close to being a genius. Albert Einstein was considered by many to be a genius, but was he a genius businessman? Not by a long shot. So, the distinction needs to be made.

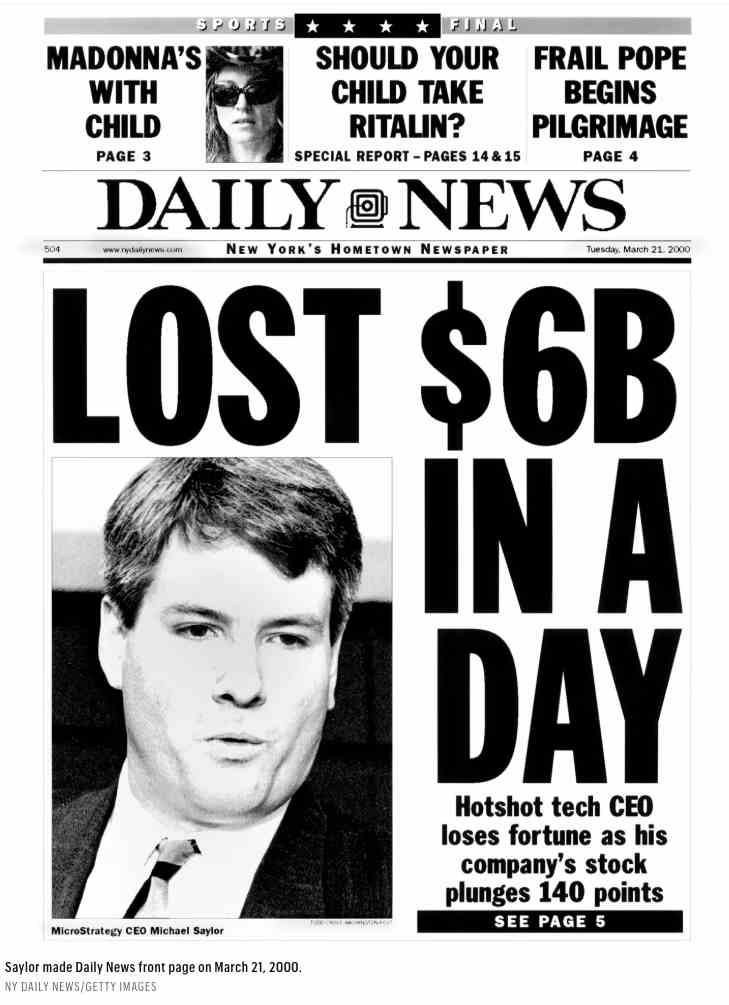

25 Years ago, Michael Saylor lost $6 Billion in a single day.

Part 2.

In 2000, there were serious accounting irregularities found at MSTR, that led to SEC investigations and eventually to filings of fraud charges against MSTR and its executives. The stock absolutely plummeted to the floor.

BY Doug Kass · May 7, 2025, 11:55 AM EDT

On the whoosh lower I took off my long SPY/QQQ common (sold) and short SPY/QQQ calls (covered) for a profit.

BY Doug Kass · May 7, 2025, 11:28 AM EDT

Google GOOGL and Apple AAPL are falling on adverse search news.

BY Doug Kass · May 7, 2025, 11:15 AM EDT

rolf thrane

1 hour ago

Assertions - maybe all obvious

I have sold al my stocks. I have joined Buffet. To me this is one of those very obvious situations where there will be cheap stocks some time this year. Who knows how cheap. It's not easy to time the market. But to me- I am betting we will get a chance to buy significantly cheaper/ IMHO

Bret Jensen

STAFF

34 minutes ago

Good points. We are just starting to see the impacts of the Fed's ZIRP policies. The first casualty was the massive destruction of shareholder value around most companies that came public in the huge SPAC/IPO wave of 2020/2021 in 2022 to 2024. CRE is just beginning to face the reckoning from all the investments that never would have been made (at least not at the valuations purchased) without easy money from the central bank. Everyone knows about the collapse of office property values, but the delinquency rate on Lodging and Retail are quite elevated and have soared around Multi-Family over the past 12 months as well. Residential real estate is getting worse by the month and has years to play out before housing affordability comes down substantially (most likely due to falling values, not rising wages). AKA, we are not getting away from feckless governmental/Federal Reserve actions in recent years unscathed. JMTC

BY Doug Kass · May 7, 2025, 10:55 AM EDT

May 7, 2025 Jeff Macke

Disney just beat the crap out of estimates and (surprising part here) guided higher for the year. Despite collapsing consumer sentiment, a drop off in US park visits, leaning even deeper into cruises (which might be the only way to vaporize your money faster than going to a theme park) and national disinterest in all things Marvel and Star Wars Disney guided pretty much every higher for just about every segment and hiked the annual estimate by over 30c a share.Just to flex a little more Disney also raised expected cash flow by more than $2 billion. Oh yeah, Disney also added the news of a new park in Abu Dhabi. Which raises a whole bunch of questionsLet's Grade It!

To see the rest go here.

BY Doug Kass · May 7, 2025, 10:40 AM EDT

IWM (Russell Index) first to fall off from intraday highs - despite equities near the top of the regular session's range.

IWM is -$1 lower than day's high. ($198.55 to $197.54)

It has been the object of my disaffection (and shorting).

BY Doug Kass · May 7, 2025, 10:30 AM EDT

Adding to RSP, IWM and Fundstrat Granny Shots US ETF (GRNY) shorts. Also to short Index calls. (With S&P cash +27 handles I am now net short the Indices)

BY Doug Kass · May 7, 2025, 10:17 AM EDT

With S&P cash +16 handles I have shorted more Index calls.

BY Doug Kass · May 7, 2025, 9:50 AM EDT

From Peter Boockvar:

Finally some high level talks with China are about to take place but we of course have little idea of what a deal would look like, the timing of such and where tariff rates eventually settle out at because they are not going back to zero. I continue to talk about the existential impact to many small businesses of this trade war because of the economic threat they are under, the implications for the broader economy and the unnecessary sacrifice they are having to make.We were reminded of this again yesterday when the CEO of Williams K. Walthers appeared on CNBC yesterday talking about the challenges her business faces, one that was founded in 1932 in the depths of the Great Depression, due to their manufacturing sourcing from China because as she claims, they are good at what they do. They make model trains and accessories. Not quite a national security threat.

Ahead of the Fed meeting, the PBOC cut its 7 day reverse repo rate by 10 bps to 1.40%. This is their benchmark rate and also trimmed the reserve requirement ratio by 50 bps to 6.2%. They estimate this RRR cut will result in an extra 1 trillion yuan (about $138b) of fresh liquidity.

With regards to the Federal Reserve and what we'll hear from Jay Powell, he's as clueless as the rest of us on how this all plays out. Yes, I believe we're headed towards some rate cuts but maybe tweaks rather than anything deeper for now and there is no chance he commits to anything today or until he gets more information from the administration on what the global tariff landscape looks like so they can plug in all the numbers into their econometric models.

I continue to find it really helpful to hear directly from companies about what they are seeing on the economic ground and there is no better way than to dig into as many conference calls as I can, both for stocks we own and others in order to merge the macro with the micro.

While tariffs are not directly impacting the operating business of Wynn Resorts, it is causing a pause in capital spending. "We had a number of CapEx projects in flight in the US, and while we had sourced for those projects, presuming some tariff impact, the current tariff rates have driven us to delay about $375 million of CapEx projects, including the Encore Tower remodel. Once tariff rates have settled, we will thoroughly re-spec and re-source the most severely affected items. While we're staying nimble, the pace of change at the moment is just too significant to commit to revised timing on that CapEx."

Their Vegas business is still doing well as "April RevPAR was up slightly from 2024, slot handle was up, and group activity was as expected. So, the business through April felt pretty good. And the visibility we have into forward demand, which is primarily through our group and convention business, also looks just fine. Of course, the booking window in other channels is much shorter than group, and so we are watching those channels carefully."

Macau saw almost 100% hotel occupancy and "the business in Q1 felt very good...But again, the booking window there is short, and we are watching customer activity day-to-day. Long story short, recent results have been good, but we have to acknowledge the uncertainty out there and the impact that uncertainty may have on demand."

From Marriott:

"RevPAR in the US and Canada region rose over 3% with our luxury and full service hotels meaningfully outperforming select service properties, thanks to solid demand across both group and transient guests. International RevPAR was up nearly 6% led by growth in APAC." They saw particular strength in Japan and India.

With China, RevPAR fell 2% "due to the weaker macro environment and tough y/o/y comparisons, though it did come in ahead of our prior expectation primarily as a result of strong domestic demand."

Marriott is another company of many that talked about how Q1 ended weaker than it began. "While RevPAR trends internationally were strong throughout the quarter, our US and Canada regions saw softer growth in March, particularly in the select service segment. We operate a cyclical business and there is no doubt that today we are in a period of heightened macroeconomic uncertainty, especially here in the US, with many concerned about slowing economic activity and lower consumer confidence."

"against this macro backdrop, we are lowering our guidance for full year RevPAR growth by 50 bps due to a more cautious outlook in our US and Canada regions." They did though say that April picked up a bit from March.

They also talked about slower US government related travel spend for obvious reasons.

Going through the Disney earnings release (a stock we own), where my focus was on the parks business, they said "Operating results at our domestic parks and experiences increased compared to the prior year quarter primarily due to growth at our domestic parks and resorts and, to a lesser extent, Disney Vacation Club and Disney Cruise Line." Helping was "an increase in guest spending due to higher spending at our theme parks."

International parks didn't do as well and was "attributable to Shanghai Disney Resort and Hong Kong Disneyland Resort due to lower theme park attendance and increased costs."

From Madison Square Garden Entertainment, the owner of MSG and other venues, benefiting from the robustness of live entertainment and a stock we own:

They saw gains in revenue and operating income that "reflected our success in attracting a wide variety of special events, family shows, and marquee sports to our venues, robust ongoing demand for our premium hospitality offerings and the conclusion of this year's record setting Christmas Spectacular run in January. And while our business experienced a y/o/y decline in the number of concerts at our venues this quarter, we remain on track to grow the overall number of bookings events this fiscal year." Losing the Billy Joel residency is one reason so more supply being the issue than demand for concerts.

"From a demand standpoint, the majority of concerts at our venues continued to sell out during the quarter. In addition, food and beverage per caps at concerts at the Garden were up, while per caps at our theaters were essentially unchanged as compared to the prior year quarter."

From Upstart, the lending platform and whose stock is down sharply pre-market:

"As we look to Q2 and the remainder of 2025, much of the discussion has shifted to potential impacts from the macro environment...we've seen little discernible impact of the macro on credit performance so far. Uncertainty has increased and we see the potential for both upside and downside scenarios that are credible in the near to medium term."

Whether this is a good thing or not we'll find out soon but "I think credit demand continues to be strong."

From Doordash, whose stock fell 7.4% yesterday:

With respect to tariffs and any impact to their business in terms of pricing/demand, "we haven't seen any changes in consumer behavior, even if there are changes in consumer sentiment. I've always believed, and I think we saw this - whether it was during things returning back to normal after Covid or peak inflation in '21 or '22, I think what you really saw was that food - or getting convenience delivered really is the most frequent form of spend in consumption, and food really is the most resilient category. We continue to believe that. We continue to see signs of that."

Expeditors International has a great read of the logistics industry from their brokerage perch:

"Subsequent to March 31, 2025, we are seeing early signs that China to US ocean volumes are declining significantly. While some of these volumes are shifting to other lanes, as customers look to mitigate their exposure to China specific tariffs, it is too early to know what the overall decline in volumes might be. Speculation regarding additional tariffs may cause more customers to pause or cancel shipment entirely. While carriers have shown a willingness to manage capacity, the current environment is so unsettled that they simply may not be able to do enough to keep rates from continuing to fall if consumer resilience fades and the capacity/demand imbalance becomes significant in certain lanes."

"We believe that uncertainty is likely to continue for some time, with possibly significant impacts to our industry."

From Celanese, a chemical company:

"Most end-markets developed as anticipated, with persistent global demand sluggishness, especially in key segments like automotive, paints, coatings, and construction."

"The already difficult demand environment has become more uncertain with the developments around tariffs and global trade issues. Our global production network provides us flexibility to manage most of the direct cost impacts of the current tariff conditions. Due to our mitigation preparations, we don't anticipate direct tariff impact in the 2nd quarter."

What a premium brand Ferrari is that can seemingly withstand anything. "Please bear in mind that Q1 '25 results were not impacted in any way by the recent introduction of higher tariffs on EU cars imported in the US. Revenues and profitability grew double digits with shipments slightly higher than the previous year and product mix and personalization as the main drivers of growth."

Likely there was some pull forward but price increases to the consumer have been easily absorbed. Some models won't have a price increase and some will be up to 10%.

"We don't see any specific trend, actually, we don't see any impact on the tariff. But despite this, as we said, we remain vigilant because, let's say, we need to be careful to catch if there is any small signal picking up."

Helped by a dip in mortgage rates, purchase applications lifted by 11.1% w/o/w after 3 weeks of declines. Refi's were up by the same amount and also after 3 weeks down. Affordability though remains a big challenge for many first time buyers.

Reflecting pull forward, German factory orders in March rose 3.6% m/o/m, well above the estimate of up 1.3%. The breadth of orders seemed to be broad but nothing market moving here.

BY Doug Kass · May 7, 2025, 9:39 AM EDT

-AMD +3% earnings

-AVDX +19% earnings

-PRPL+19% earnings

-CURI +20% earnings

-AVDX +18% earnings

-PRCH +19% earnings

-NRDS +20% earnings

-FLYW +12% earnings

-EOSE +12% earnings

-REZI +16% earnings

-KYVO +4% earnings

-ATOM +10% earnings

-LITE +7% earnings

-EA +5% earnings

-CRUS +4% earnings

-KROS +4% earnings

-ELAN +3% earnings

-COR earnings

-CRL +4% Elliott investment

-DIS +7% earnings; guidance

-EMR +4% earnings

-ROK +9% earnings

-CDW +2% earnings

-VSTS -25% earnings

-SRPT -22% earnings

-UPST -15% earnings

-MYGN -20% earnings

-RVLV -11% earnings

-LFVN -10% earnings

-RVLV -5% earnings

-CC -7% earnings

-ANET-5% earnings

-SMCI -6% earnings

-KLIC -5% earnings

-MASI -7% earnings

-MRVL -9% guides Q1 Net Rev $1.875B v $1.88Be

-TDC -6% earnings

-CRWD -3% affirms; announces re-organization

-UBER -4% earnings

BY Doug Kass · May 7, 2025, 9:19 AM EDT

From JPMorgan:

US: Futs are higher with US/China set to meet this weekend to jump start trade relations, though futs are off their highs, having reversed more than 1.5% when the news hit last night. US/UK are said to have a trade deal hit the tape this week. Today’s Fed announcement (2pm EST) is expected to yield no surprises as the CB preaches patience and Powell is likely to reiterate this messaging at the press conference (2.30pm EST). Pre-mkt, Mag7 names and Semis are leading the markets higher while RTY appears to be squeezing into outperformance. Cyclicals are poised for a strong session, too. Bond yields are higher alongside a stronger USD. Cmdtys are bid higher led by Ags and Energy; gold/silver under pressure.

and..

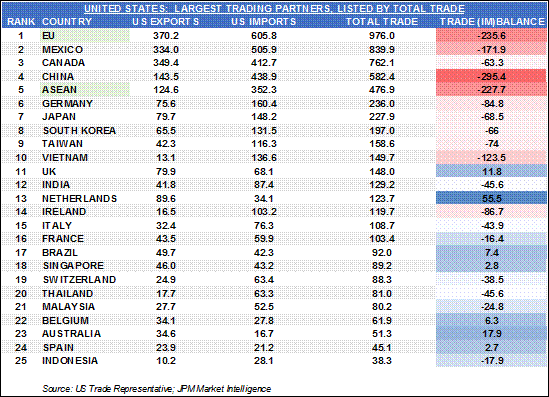

EQUITY & MACRO NARRATIVEYesterday, positive trade war headlines from Bessent helped markets stage an intra-day rally. Bessent said, “There are 18 very important trading relationships. We are currently negotiating with 17 of those trading partners. I expect that we can see a substantial reduction in the tariffs that we are being charged — as well as non-tariff barriers.” The 18th is China. A table of the US’s largest trade partners is below. Further, Bessent said that we may see the first deal hit this week which was later reported to be US/UK, with only treatment of Pharma the sticking point. US: LARGEST TRADING PARTNERS (SORTED BY TOTAL TRADE)

BY Doug Kass · May 7, 2025, 9:02 AM EDT

Sold more IWM short at $198.79.

BY Doug Kass · May 7, 2025, 8:21 AM EDT

Earlier this week I updated my view on the cannabis space, "Cannabis' Weak Foundation, Uncertain Future and Continuing Challenges."

There were two notable headwinds thrown, again, into the face of cannabis investors since my update was delivered:

* Yesterday the Pennsylvania state house proposed a bill to legalize adult use of cannibas but only in stores run by Pennsylvania's Liquor Control Board. While it is very unlikely that the state will ultimately control the sale of cannabis, this can be viewed short term as another negative to MSOSs.

* Florida Governor DeSantis proposed rules that will make it more difficult for citizen organized bills (such as the legalization of adult recreational use of cannabis in Florida).

Meanwhile, there are heavy earnings releases this week for MSOSs:

BY Doug Kass · May 7, 2025, 8:15 AM EDT

BY Doug Kass · May 7, 2025, 8:04 AM EDT

* Several 'tape bombs' upended the markets on Tuesday...

As previously mentioned, the markets are increasingly unpredictable and volatile (VIX remains elevated). It's a good time to have below-average invested positions, given value at risk (VAR) and the potential for more "tape bombs." It is also a great backdrop for opportunistic traders — but no so great for the buy-and-hold crowd.

Yesterday's regular session and action after the close is indicative of these conditions.

The day started with Paul Tudor Jones appearing on Squawk Box at around 8:30 a.m., proclaiming his confident view that equities will undercut the recent lows and that AI is a threat to humanity. Here and here.

Note: My baseline case is similar to Paul Tudor Jones — I see market moving irregularly lower all aummer, with a bonafide threat of new lows (estimated S&P range 4800-5800).

Equities moved irregularly lower during the trading day, closing at their lows at 4 p.m. — but not without drama.

After falling by about 50 S&P handles, a violent and brief rally occurred when President Trump said an important "announcement" would be forthcoming in the next few days. S&P cash rallied to only -5 handles lower at which time I posted in The Comments Section that I had increased my short exposure by selling Index call options (short) and adding to shorts in RSP, IWM and GRNY.

As I mentioned, stocks then faltered and undercut the previous day's lows at the close, falling another -15 handles right after the close.

An "announcement" at around 4:10 p.m. that the Treasury Secretary plans to meet with Chinese trade representatives then lifted to as high as +65 handles. I went to work further on the short side:

Dougie Kass

Sold long SPY and QQQ (held against short calls) at $564.08 and $486.69

Here were yesterday's complete things:

* Shorts: RSP $170.62, IWM $198.24 and GRNY $19.43.

* Added to speculative FGEN at $0.295.

* Sold index longs (against index short calls), added to index calls short and bought back some index common on last night's pullback — now delta neutral in indices.

BY Doug Kass · May 7, 2025, 7:38 AM EDT

Bonus — Here are some great links:

The One Streak That Is Still Alive

Paul Tudor Jones Is Negative - Sees New Lows

BY Doug Kass · May 7, 2025, 7:17 AM EDT

There is a lot to talk about today, especially after the tariff announcement lifted futures so dramatically.

But let's start with the S&P Short Range Oscillator, which fell from a deeply overbought reading of 8.02% (which set the stage for the regular session's sharp fall in the S&P index) to a still healthy overbought of 5.71%.

BY Doug Kass · May 7, 2025, 6:55 AM EDT