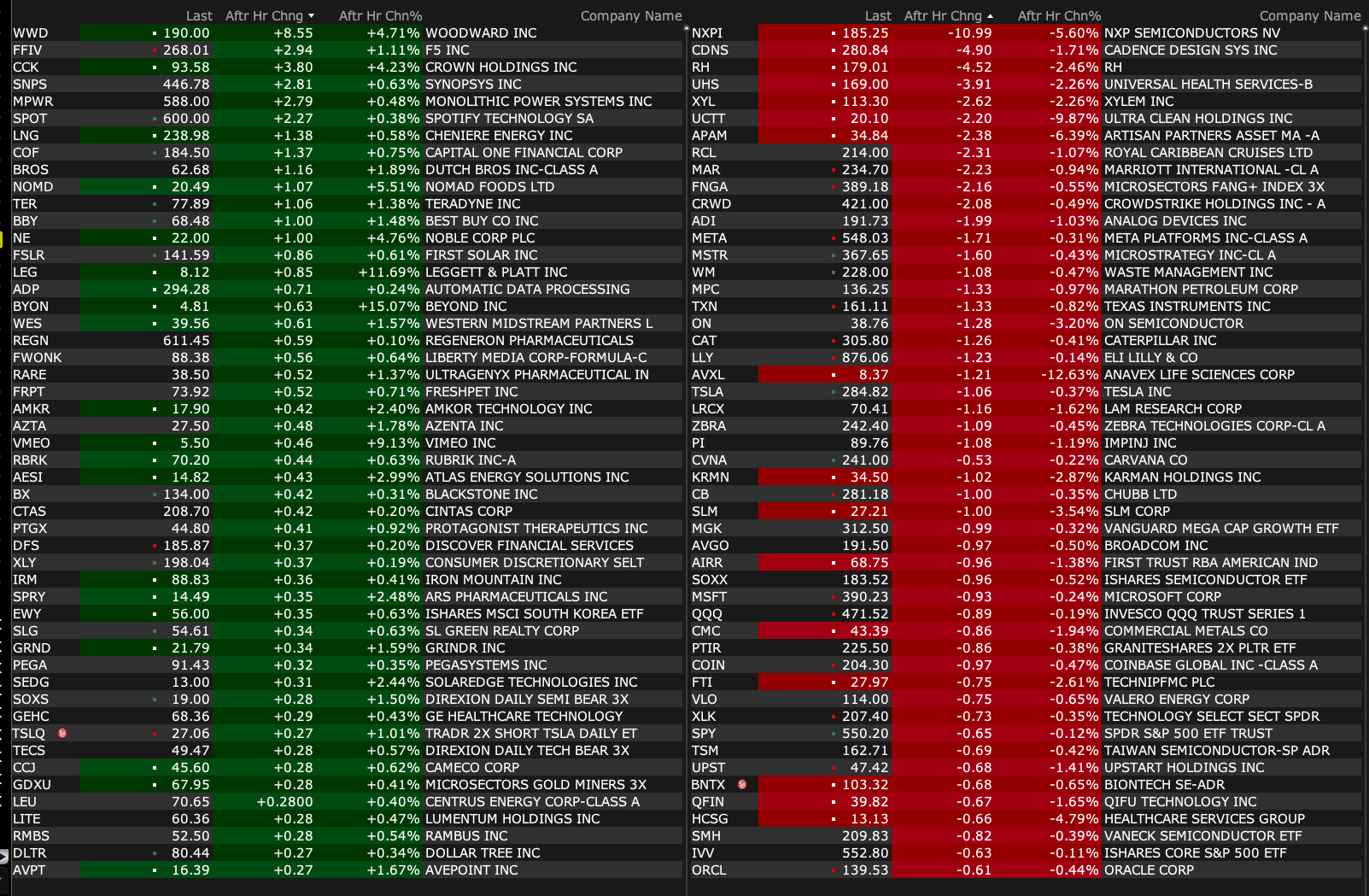

Monday's After-Hours Movers

As of 4:21 p.m.:

BY Doug Kass · Apr 28, 2025, 5:04 PM EDT

As of 4:21 p.m.:

BY Doug Kass · Apr 28, 2025, 5:04 PM EDT

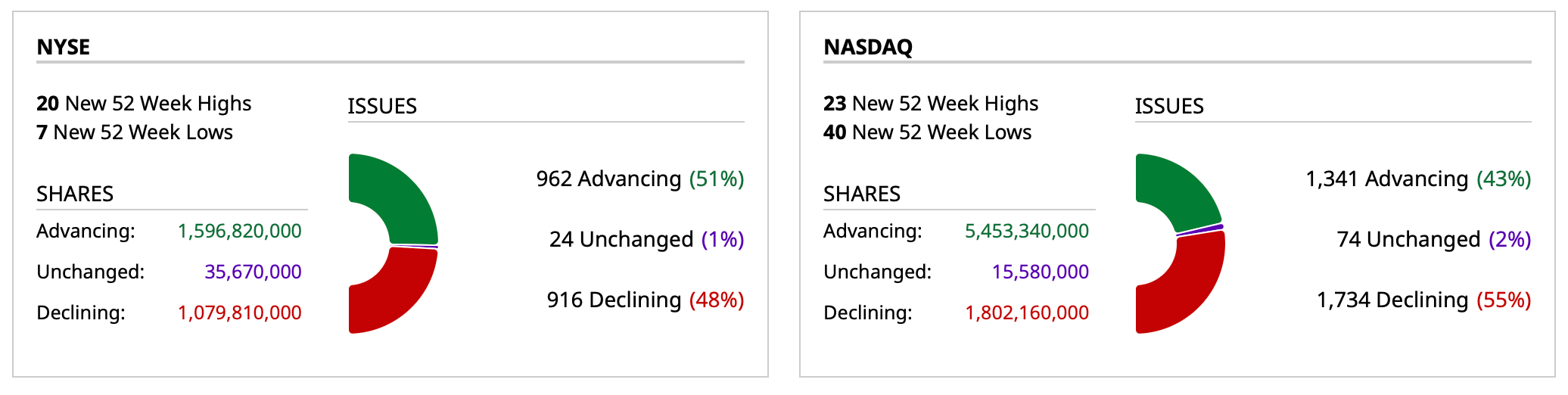

- NYSE volume 36% below its one-month average

- NASDAQ volume 19% above its one-month average

- VIX index: up 1.25% to 25.15

BY Doug Kass · Apr 28, 2025, 4:45 PM EDT

The volatility this afternoon was something to behold — and hard for traders to predict.

I am working on a column about the bonafide threat to American Exceptionalism (and to the U.S. dollar and our capital markets).

Hopefully I will get it done around 5 a.m. tomorrow morning.

Thanks for reading.

Enjoy the evening.

Be safe.

BY Doug Kass · Apr 28, 2025, 4:09 PM EDT

BY Doug Kass · Apr 28, 2025, 3:38 PM EDT

With S&P cash +1 handle (recovering all of the day's losses) I am back shorting index calls.

BY Doug Kass · Apr 28, 2025, 3:26 PM EDT

Shorted more GRNY at $18.72 this afternoon .

From Friday:

New short GRNY ($18.62): GRNY – Fundstrat Granny Shots US Large Cap ETF – ETF Stock Quote | Morningstar

Position: Short GRNY (VS)

By Doug Kass Apr 25, 2025 10:08 AM EDT

BY Doug Kass · Apr 28, 2025, 3:01 PM EDT

BY Doug Kass · Apr 28, 2025, 2:45 PM EDT

Housekeeping item.

I am out of my Microsoft MSFT long at $390.66.

BY Doug Kass · Apr 28, 2025, 2:30 PM EDT

BY Doug Kass · Apr 28, 2025, 2:30 PM EDT

BY Doug Kass · Apr 28, 2025, 2:17 PM EDT

BY Doug Kass · Apr 28, 2025, 1:23 PM EDT

BY Doug Kass · Apr 28, 2025, 1:11 PM EDT

Wolf Street howls about gold imports.

BY Doug Kass · Apr 28, 2025, 12:59 PM EDT

Here is another example of the lack of value (and the "chase" of higher stock prices) on the part of those throwing darts (aka investment strategists).

From earlier this morning, from those wonderful people at JPMorgan (formerly known as Chase Manhattan Bank):

From JPMorgan:

We are updating our view to Tactically Bullish. This differs from our past bullish calls as this one is technical in nature and not fundamental. First, the combination of light positioning, low liquidity, subdued investor participation means that this market is likely to drift higher in the absence of negative news such as tariff headlines or a spike in bond yields. Second, the continuation of MegaCap Tech earnings may give the market a tailwind. Third, the potential for an announced trade deal, or Memorandum of Understanding (“MoU”), skews the risk/reward positively. Combined, we think the pain trade is higher but led by a narrow group of stocks such as the Mag7, similar to 24H1. The SPX closed about 5% below the upper bound of Dubravko’s trading range, 5200 – 5800. Overall, the De-escalation Trade has room to run.

While we think this rally could span multiple weeks, this is not an all clear for markets. Unfortunately, we think we are still 1-2 months away from seeing the negative impact of the trade war on the real economy. The volume of articles pointing to reduced shipments from China continue to increase and the likely impact is a goods shortage sometime this summer. If consumer begin to see empty shelves combined with significantly higher e-commerce prices, then we could see the decline in consumption that precedes a decline into a recession. That said, the hypothesized delayed impact means that immediate macro data is likely to paint a picture of a still resilient economy, starting with NFP on Friday. It remains possible that consumption continues to surprise to the upside and that the US fails to approach a recession. Consensus remains that the hard data “catches down” to the soft data. This phenomenon was noted in a new study by the Fed which finds that consumption has increased despite the significant decline in sentiment. An excerpt from that study, “… what consumers have been saying differs from what they have been doing during the post-pandemic period; consumers say they feel worse, but through the end of 2024, they are buying more – not just spending more – than they did in 2019. This disconnect between what consumers have been saying and doing suggests that consumer sentiment surveys on their own have become weaker indicators of future consumer behavior and of the health of US consumers. While it is important to recognize how consumers feel, we should exercise caution when using consumer sentiment surveys to infer future consumer behavior given this recent disconnect between what consumers say and do.”

Position: None

By Doug Kass Apr 28, 2025 6:15 AM EDT

BY Doug Kass · Apr 28, 2025, 12:35 PM EDT

With S&P futures -33 handles (and -60 from the intraday high) I am taking in my short index calls done today for a profit.

BY Doug Kass · Apr 28, 2025, 11:40 AM EDT

- NYSE volume 32% below its one-month average;

- Nasdaq volume 10% below its one-month average;

- VIX index: up 0.89% to 25.06

BY Doug Kass · Apr 28, 2025, 11:35 AM EDT

A possible reason for the downdraft in the indexes:

APR DALLAS FED MANUFACTURING ACTIVITY: -35.8 V -14.1E Components

- Production 5.1 v +6.0 prior

- Capacity Utilization: -3.8 v -2.3 prior

- New orders: -20 v -0.1 prior

- New order growth rate: -22 v -8.1 prior

- Shipments: -5.5 v 6.1 prior

- Raw materials prices paid: 48.4 v 37.7 prior

- Wages and benefits: 14.3 v 16.0 prior

- Employment: -3.9 v -4.6 prior

BY Doug Kass · Apr 28, 2025, 10:55 AM EDT

I have increased my short Index calls just now.

I have also converted by short common Indices (SPY and QQQ) into more short calls (taking in premium for May).

BY Doug Kass · Apr 28, 2025, 10:47 AM EDT

More Index shorts:

* SPY $551.28

* QQQ $472.31.

BY Doug Kass · Apr 28, 2025, 10:35 AM EDT

The media fanfare following Google's GOOGL "beat" was symptomatic of what is wrong with Fin TV.

Cheerleading, not analysis (never was there a discussion of a sharply lower rate of paid click growth - actually the lowest year over year percentage increase!) - was the prevailing theme of the shows' coverage.

I believe Google is now trading below the price it closed before the "beat."

BY Doug Kass · Apr 28, 2025, 10:31 AM EDT

Adding to individual cannabis names: TCNNF $4.30, TSNDF $0.33 and VRNOF $0.73.

BY Doug Kass · Apr 28, 2025, 10:12 AM EDT

Is the economy now recession proof? What does that mean for Fed policy, and the neutral rate? Is this also now a syntax question as opposed to a practical question? And does this matter to the Fed?

By a syntax question, this is what I mean. Recession is measured by reported GDP and reported employment. GDP is in part a function of reported inflation. If inflation is understated, GDP is overstated, by the same amount. Employment includes jobs going to immigrants, second jobs, jobs created by the birth/death model, and jobs going to government employees that often have negative productivity and whose roles (regulatory and bureaucratic nonsense) end up harming the country and the economy, even though they help GDP over the short term.

It seems the whole country thought we were in recession in the middle part of the Biden term. This includes very prominent financial minds and the average Joe. There is a reason the election went the way it did: “It’s the economy, stupid.” But apparently, as measured by the official stats, not only was there no recession, things were pretty good. Now, we are still not in recession, and as measured by the same stats, it still seems 50% likely we will not be in recession, and if we ever enter one, it feels like it might be mild, at least as measured by those same statistics.

So is the economy now recession proof? If we don’t go into a recession now, with the shaky foundation that was in place, including an overspent consumer, all the debt, global tensions and all the uncertainty, it feels like we will never have a recession.

It seems there are two issues. There are measurement issues which I discussed, and structural issues. I think the biggest structural issue might be we no longer are a manufacturing-based economy, for better or for worse. Therefore, it is harder for the economy to move into a substantial overcapacity position, leading to a recession.

If the economy is now give or take recession proof, as measured, what does this mean for rates over time and what the “neutral” rate really should be?

Probably a fair bit higher than it was the last 20-30 years. In fact, over the last 20-30 years, you could argue the only problems the economy has had have come from interest rates being kept too low for too long. The only crises our economy has had are financial ones, not normal economic recessions driven by corporate over-investment. 2000 tech bubble burst, rates were kept too low, too long going into it. 2008 financial crises, rates were kept too low for too long going into it. Silicon Valley Bank, rates kept too low for too long. The recent inflation problem, rates kept too low for too long and much to much money printing.

If we do not go into recession now, or it is just a mild little blip, we have a recession-proof economy. Rates do not need to be near zero in a recession-proof economy, ever! It does more harm than good, and the proof is in the pudding. The neutral rate is now higher.

Post Script: Oops I left out one more important thing. GDP also includes government spend, which goes beyond just government jobs. Wasteful government spend also increases GDP over the short term. Sadly, despite all the noise, it is unclear to me if there is an actual governor on government spend. As best as I can tell, not much has changed in that regard either. Entitlements remain untouched, and the rest of it, who knows, but it feels like the overall budget might be getting worse and not better, which is part of what the price action in gold has been telling you.

BY Doug Kass · Apr 28, 2025, 9:30 AM EDT

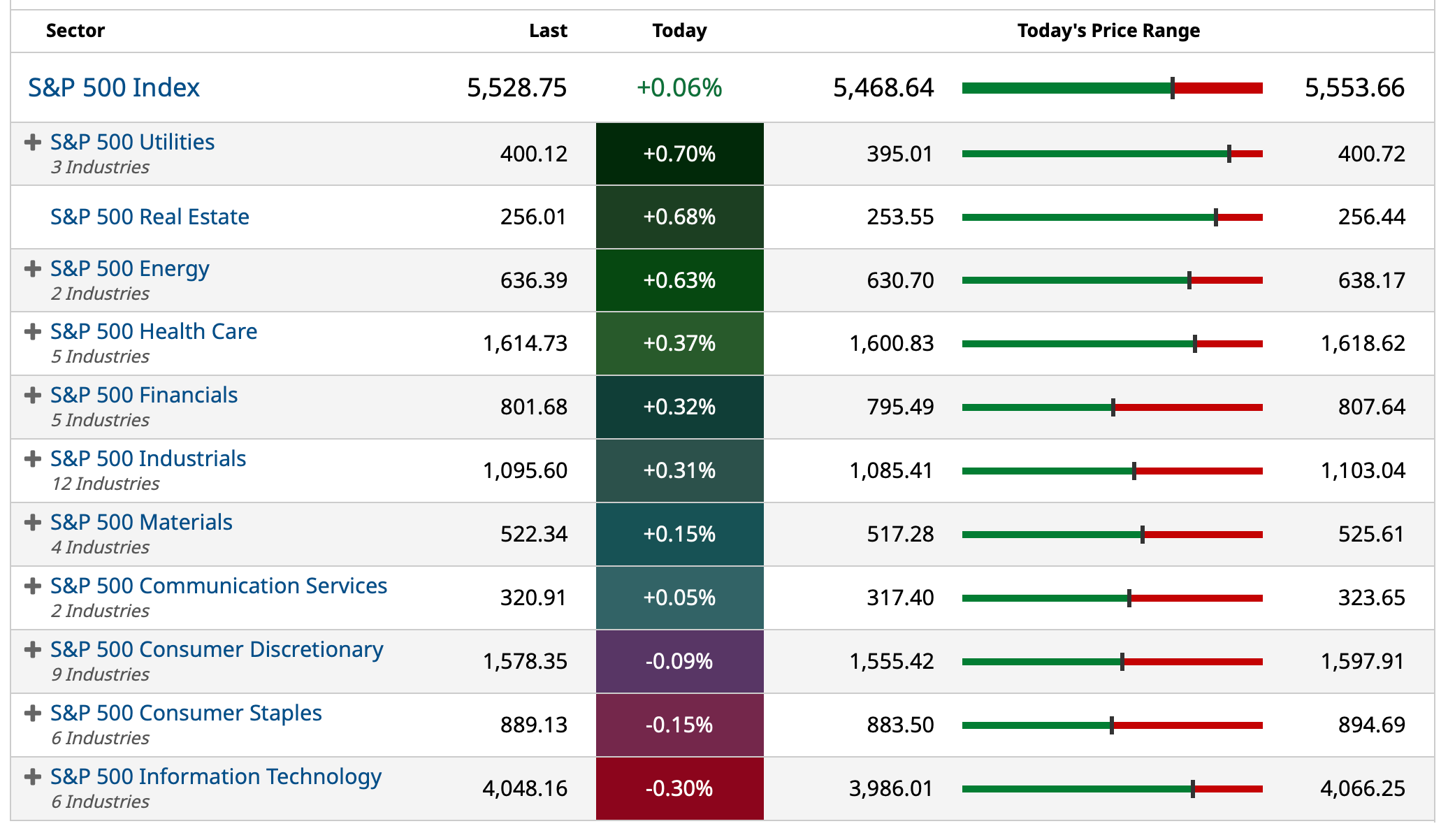

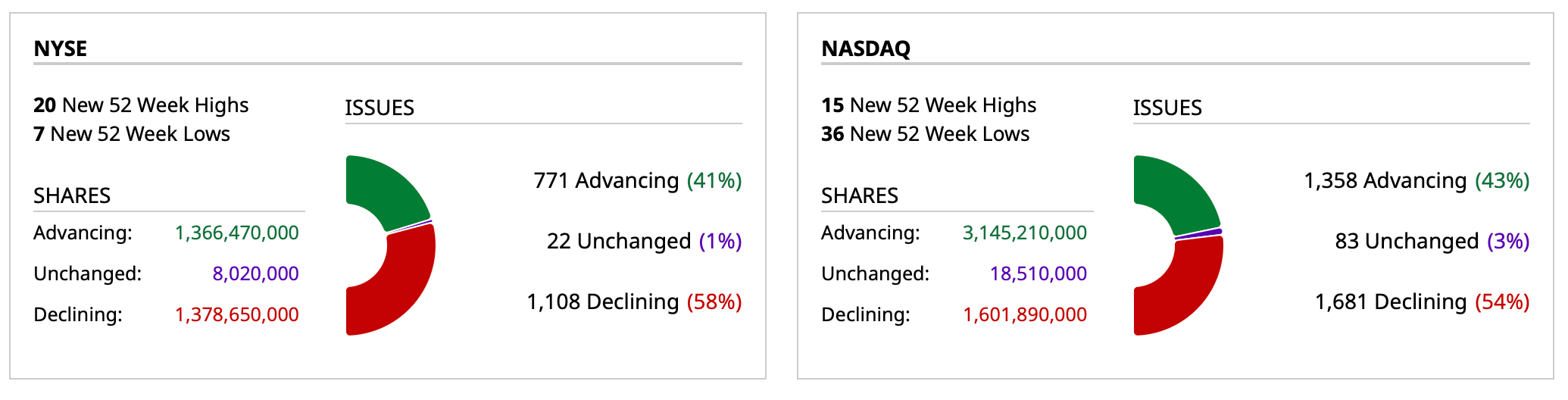

* Friday's strong Index behavior was accompanied by lower volume

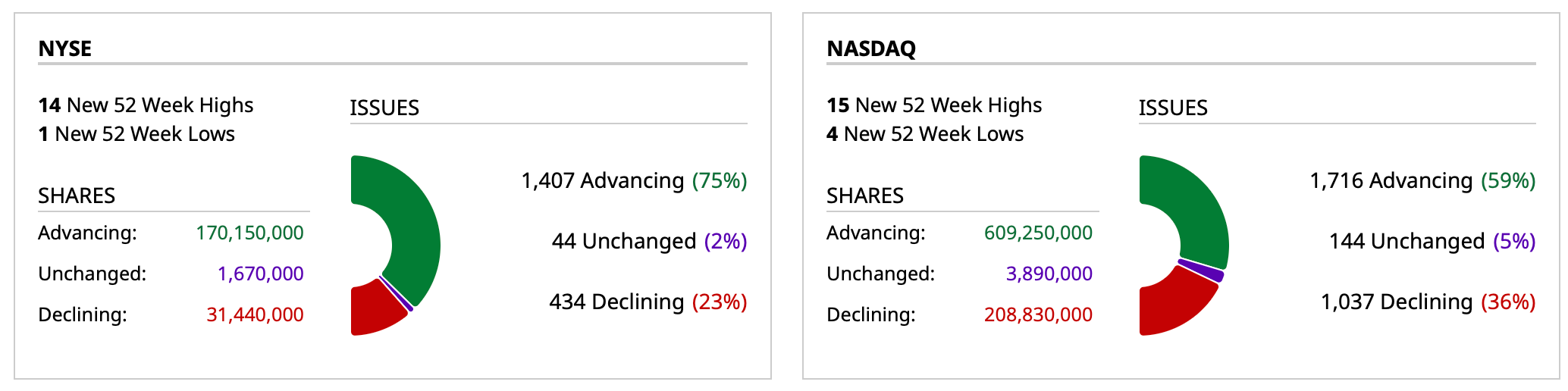

- NYSE volume is 32% below its one-month average

- Nasdaq volume of 18% below its one-month average

* Friday's strong Index action was also accompanied by lower/weak breadth:

* The S&P Short Range Oscillator has moved to a more deeply overbought (5.22% vs. 2.73%).

BY Doug Kass · Apr 28, 2025, 9:23 AM EDT

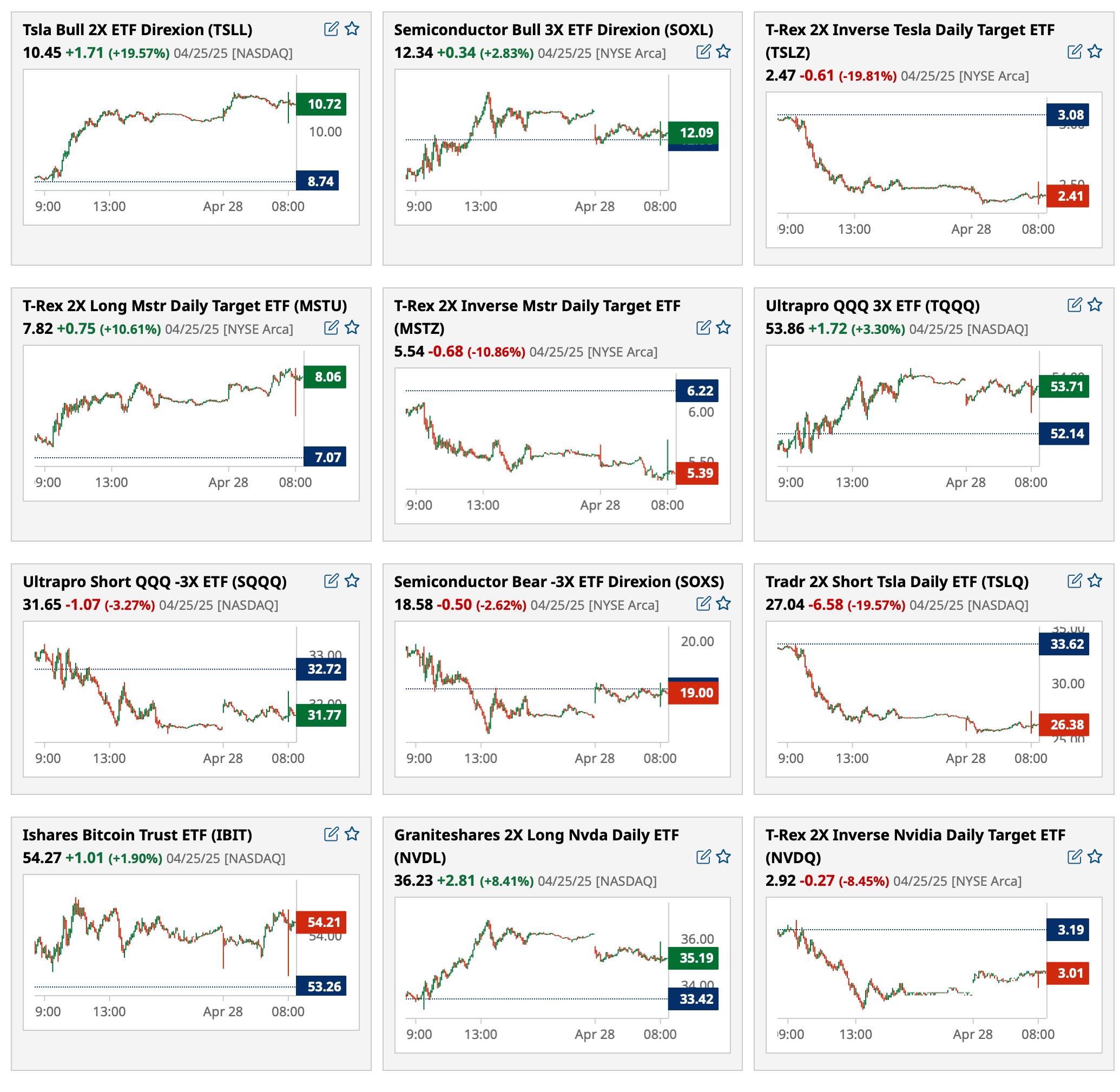

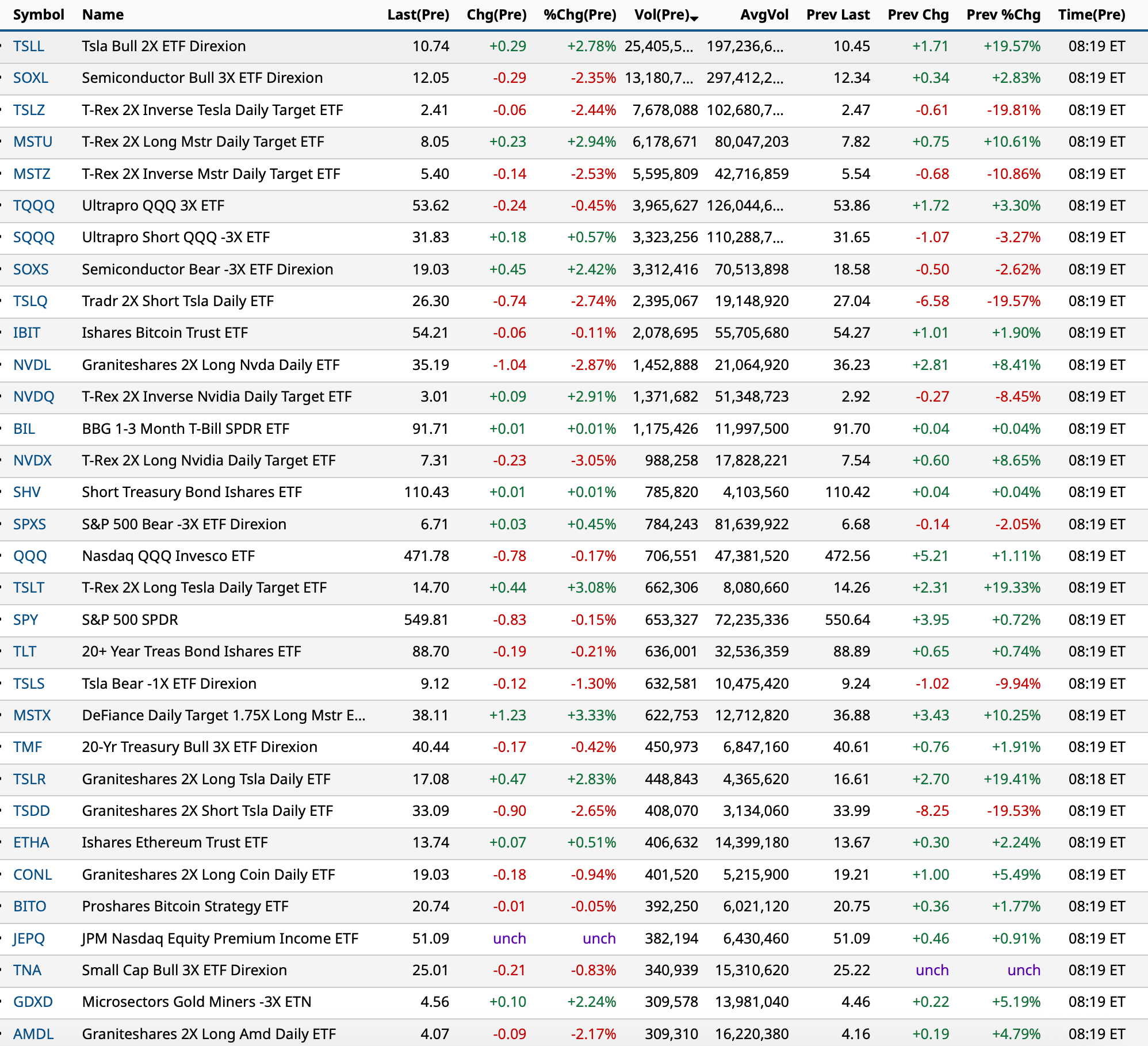

Most active premarket ETFs as of 8:19 a.m. ET:

BY Doug Kass · Apr 28, 2025, 9:15 AM EDT

Premarket percentage movers at 8:37 a.m. ET:

BY Doug Kass · Apr 28, 2025, 9:05 AM EDT

-PRTG +46% (reports Confirmatory Preclinical Results in Mesothelioma Supporting First-In-Human Trial of PORT-7)

-CGON +39% (announces Best-in-Disease Durability Data in BOND-003 Cohort C and Promising Early Signal in Cohort P for Cretostimogene Grenadenorepvec at the American Urological Association Annual Meeting)

-OPRA +13% (earnings, guidance)

-PLUG +12% (prelim earnings, guidance)

-FFAI +6.7% (receives endorsements from California politicians supporting FF’s Global Automotive Bridge Strategy)

-BHVN +6.1% (announces investment up to $600M by Oberland Capital)

-PETZ +5.7% (earnings)

-RVTY +5.5% (earnings, guidance)

-MYNZ +5.4% (provides 1Q25 corporate update and path to FDA Premarket Approval; inclusion of the first patient keeps the Company on schedule to report top-line results by YE25)

-PTON +4.8% (Truist Raised PTON to Buy from Hold, price target: $11)

-SWTX +3.1% (confirms to be acquired by Merck KGaA at $47/shr in cash)

-SPR +2.4% (divests certain assets and sites involved in the production of Airbus aerostructures to Airbus; Airbus also to provide $200M in lines of credit)

-CGNX +2.0% (TD Cowen Raised CGNX to Buy from Hold, price target: $35)

-BA +1.5% (Bernstein SocGen Group Raised BA to Outperform from Market Perform, price target: $218)

-ANTE -4.1% (terminates Deposit Agreement)

-DPZ -3.0% (earnings, color)

-LLY -1.6% (hearing HSBC Cuts LLY to Reduce from Buy, price target: $700)

-NVDA -1.6% (weakness off stories of a new China AI chip)

BY Doug Kass · Apr 28, 2025, 8:55 AM EDT

"Dougie, meshugana is trump." (Craziness is three-fold in Yiddish)

- Grandma Koufax

BY Doug Kass · Apr 28, 2025, 8:45 AM EDT

From Peter Boockvar:

A Waymo trip when you don't know about FSD/The tariff challenge of a small business and other impacts/Earnings

We'll start Monday off with some levity after Alphabet/Google finally gave us some detail around Waymo last week in their earnings report and they are doing 250,000 rides now per week. This clip was out 5 months ago but I only saw it for the first time over the weekend of a Waymo trip taken by Jimmy Kimmel's Aunt Chippy.

Not funny is the plight of many small businesses who don't have the resources, flexibility or ability to shift supply chains around and from China on a dime. This interview on This

When it comes to pricing flexibility of small business, I read this over the weekend in the WSJ, "Some 47% of small businesses say they have increased prices since the beginning of the year, and 60% plan to raise prices in the next three months, according to a survey of more than 500 small businesses conducted in April for the WSJ by Vistage Worldwide, a business coaching and peer-advisory firm." The article did not specify though what stage of the supply chain these small businesses are in in terms of whether they have the ability to pass it on to the end consumer or it gets mostly eaten within the supply chain.

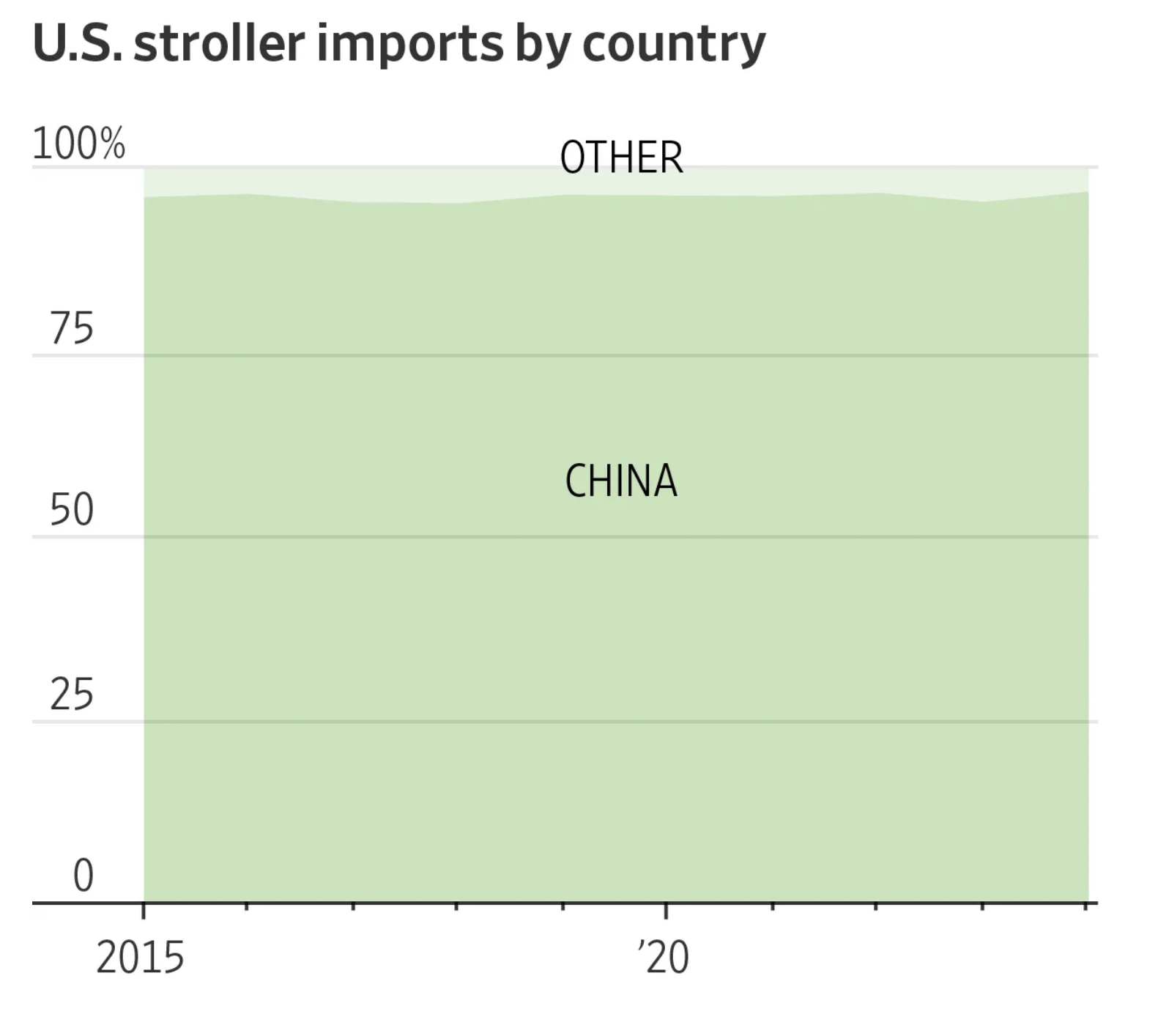

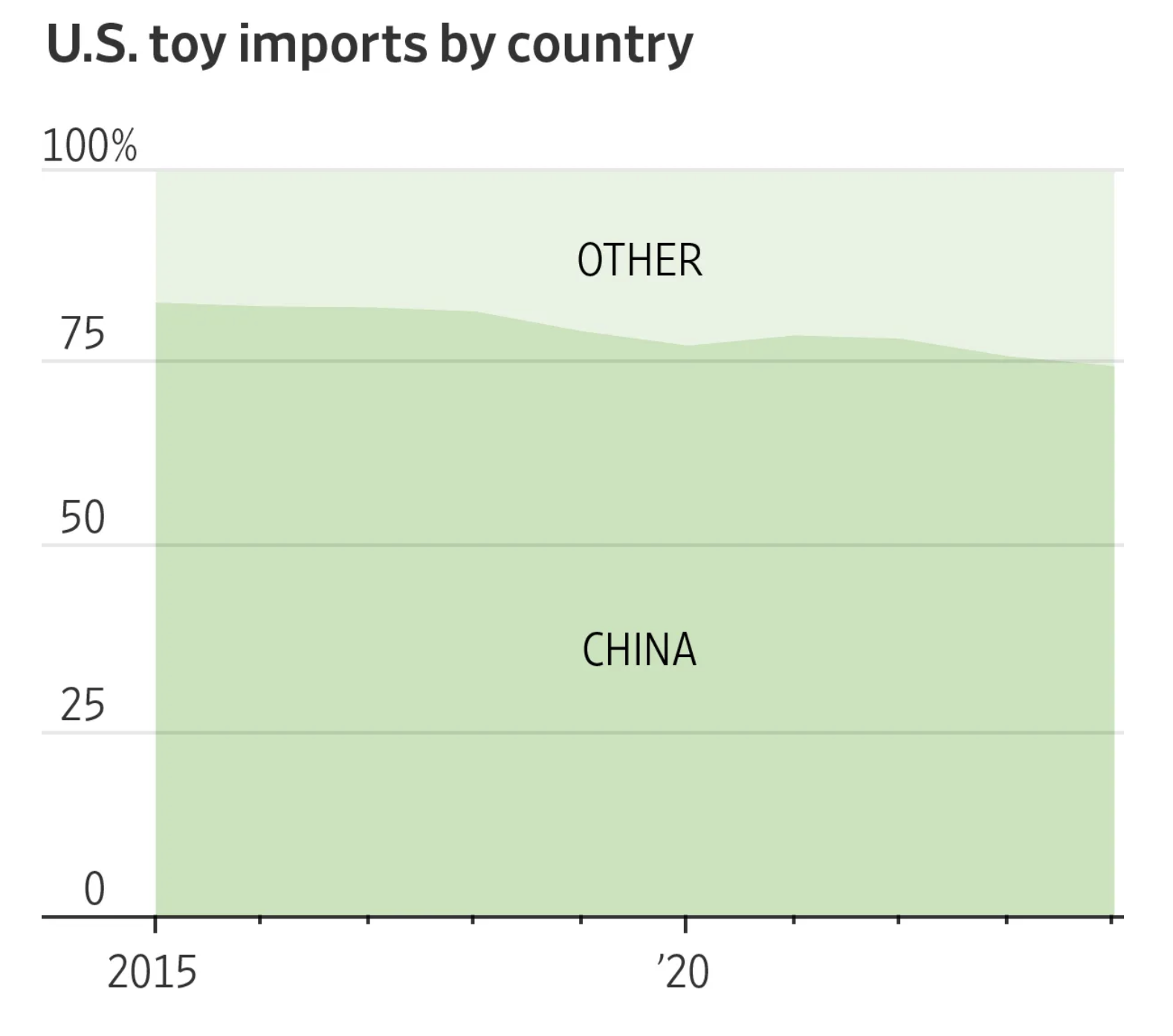

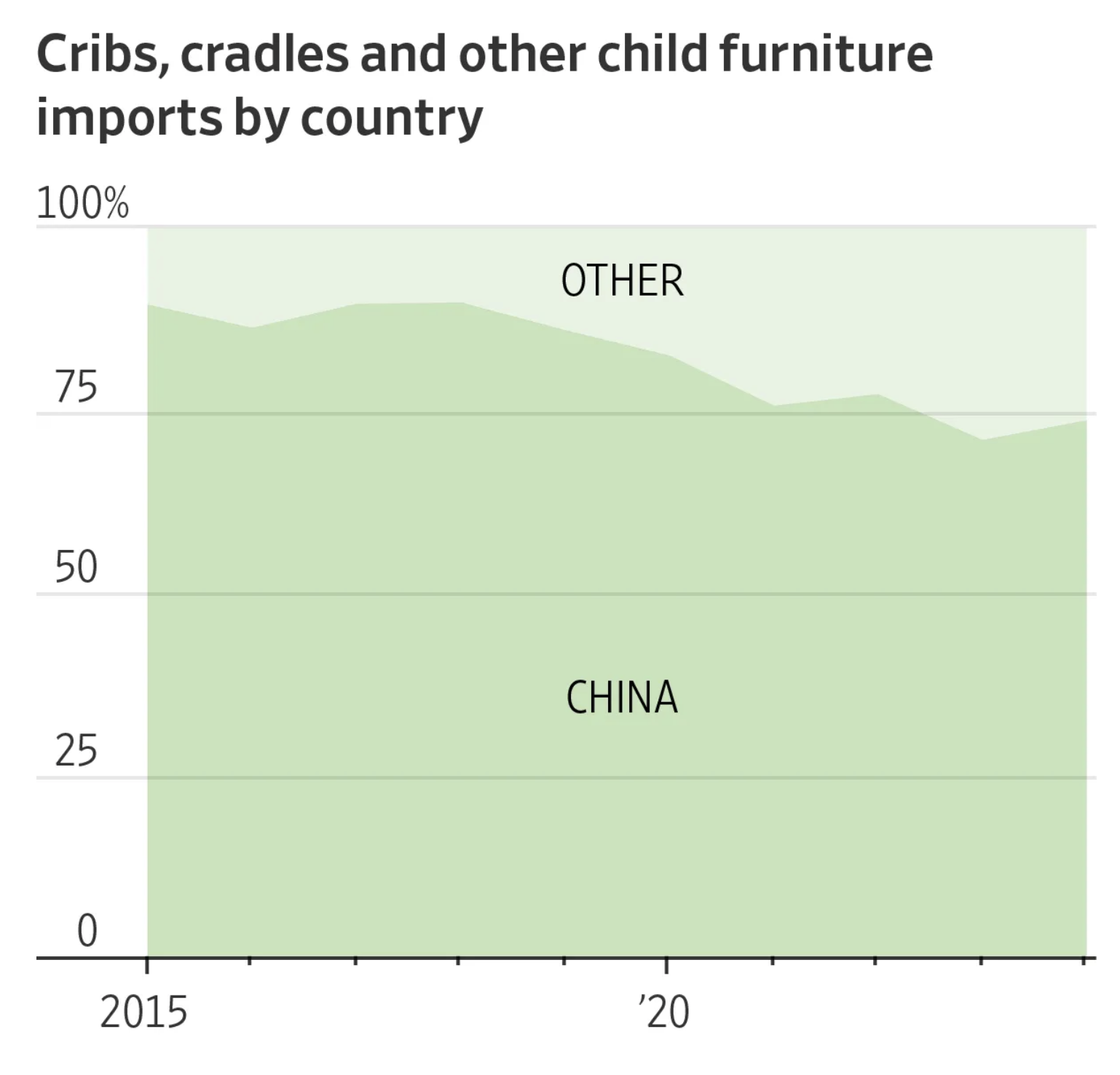

Also in the WSJ, and not news to many of you who have likely heard about our heavy reliance on China when it comes to baby strollers, cribs and toys, prices are jumping in these categories and if tariffs don't fall dramatically, these important store shelves will be bare too.

This as China shipments to the US are down 60% over the past week according to Flexport.

The trucking company Saia said this on Friday and whose stock fell 31%:

Going into 2025, "We expected the macro environment to remain somewhat muted or at least consistent with what we've seen over the last two years. As we approach the end of April, the backdrop is notably different. Historically, we've typically seen seasonal increases in shipments and tonnage of approximately 3% to 4% from February to March. In facilities opened less than three years, we saw the 3% sequential improvement. In legacy facilities, shipments were actually down slightly Feb to March. This year, shipments in total for the company were only modestly improved from March to April, which we attribute primarily to the uncertain macro environment."

"Customers, although satisfied with their service and valuing our network expansion, appear cautious in the current backdrop and are taking a wait-and-see approach."

From LyondellBasell, the chemical company:

The CEO said, "This is the deepest and longest downturn of my career. And while this is likely to be prolonged by volatile trade policies, I remain confident that we will eventually see a recovery."

From Colgate-Palmolive:

"The first challenge is the weaker consumers you've heard throughout the week. While a slowdown in category pricing was always built into our assumptions for 2025, the macroeconomic and consumer uncertainty we saw in Q1, not just in the US, but also in other countries around the world, had a negative impact on volume growth and therefore category growth in the quarter."

"We believe that consumers are still brushing their teeth, taking showers, cleaning their floors, and feeding their pets, where there may have been some pantry de-loading and some modest retailer de-stocking in the quarter. As a result, we have seen some signs of category improvement in April."

"we expect the impact of tariffs that have been announced since our conference call in January and that are currently in effect to have an incremental impact of roughly $200 million in 2025 vs our initial guidance."

"I expect the 2nd quarter to continue to be soft, given the uncertainty that continues to exist, but the early signs that we're seeing in April at least gives us some confidence that categories will slowly come back as the consumers settle down and the economic uncertainty that surrounds the markets around the world improves."

From Boston Beer:

"While we are encouraged by our first quarter performance, we are operating in a challenging and unpredictable macroeconomic environment."

"There are some factors, such as health and wellness and cannabis that seem to be having an impact on the beer category as a whole. However, our current view is that inflation and economic uncertainty are also significant drivers of the recent weakness, as well as some impact from the timing of Easter this year."

From Autonation:

"Prior to the formal announcement of tariffs, new vehicle sales were performing well, tracking approximately 5% up y/o/y, and the strong pace accelerated following the tariff announcements in late March, adding to our pace, resulting in same store new vehicle unit sales increase of 7% for the quarter from prior year."

"Clearly in the quarter, we benefited in March from a pull-in effect as buyers accelerated their planned vehicle purchases to avoid the coming tariffs. This trend continued into April, albeit at an increasingly moderating pace. And as you can see from our current data supply, we have a level of ground inventory of pre-tariff rates that will, for certain models, sustain this momentum into May."

Premium luxury did the best, up 14%.

On their used car business and something I've talked about many times over the past few years, "Supply availability remains a challenge, particularly for the mid and higher priced tiers, consistent with the past few quarters, driven by lower new vehicle production during Covid."

With regards to their financing business, "The quality of the portfolio continues to improve. Our credit and performance metrics are improving with average FICO scores on origination of 695 for the first quarter, compared to 659 in the first quarter of 2024 and 684 in the fourth quarter of 2024. Delinquency rates at 2% are solid." Helping on the delinquency side is their lower reliance on 3rd party originators.

Reflecting pull forward of trade was the 11.4% y/o/y gain in Hong Kong exports to the USin March. In total, they jumped 18.5% y/o/y vs the estimate of up 12.4%.

BY Doug Kass · Apr 28, 2025, 8:35 AM EDT

BY Doug Kass · Apr 28, 2025, 8:04 AM EDT

I especially liked Helene's column on breadth and sentiment this morning!

Let's go to the tape!!

The Bears Will Migrate to the Fence Before They Become Bulls - TheStreet Pro

BY Doug Kass · Apr 28, 2025, 7:05 AM EDT

BY Doug Kass · Apr 28, 2025, 6:50 AM EDT

Bonus —Here are some great links:

BY Doug Kass · Apr 28, 2025, 6:35 AM EDT

BY Doug Kass · Apr 28, 2025, 6:25 AM EDT

From JPMorgan:

US: Futs are weaker but are up off their overnight lows as the US tries to build off of last week’s performance where the SPX added 4.6%, NDX 6.4%, and RTY 4.1%. In constat FX terms, the US outperformed most major int’l mkts. Pre-mkt, Mag7 names are mixed with Cyclicals/Semis under pressure and Defensives catching a bid. Bond yields are higher as the curve bear steepens and USD start the session stronger. This is a data-heavy week but today’s focus is on regional Fed activity but the key’s this week are NFP, JOLTS, ISM-Mfg, and 25Q1 metrics.

and...

We are updating our view to Tactically Bullish. This differs from our past bullish calls as this one is technical in nature and not fundamental. First, the combination of light positioning, low liquidity, subdued investor participation means that this market is likely to drift higher in the absence of negative news such as tariff headlines or a spike in bond yields. Second, the continuation of MegaCap Tech earnings may give the market a tailwind. Third, the potential for an announced trade deal, or Memorandum of Understanding (“MoU”), skews the risk/reward positively. Combined, we think the pain trade is higher but led by a narrow group of stocks such as the Mag7, similar to 24H1. The SPX closed about 5% below the upper bound of Dubravko’s trading range, 5200 – 5800. Overall, the De-escalation Trade has room to run.

While we think this rally could span multiple weeks, this is not an all clear for markets. Unfortunately, we think we are still 1-2 months away from seeing the negative impact of the trade war on the real economy. The volume of articles pointing to reduced shipments from China continue to increase and the likely impact is a goods shortage sometime this summer. If consumer begin to see empty shelves combined with significantly higher e-commerce prices, then we could see the decline in consumption that precedes a decline into a recession. That said, the hypothesized delayed impact means that immediate macro data is likely to paint a picture of a still resilient economy, starting with NFP on Friday. It remains possible that consumption continues to surprise to the upside and that the US fails to approach a recession. Consensus remains that the hard data “catches down” to the soft data. This phenomenon was noted in a new study by the Fed which finds that consumption has increased despite the significant decline in sentiment. An excerpt from that study, “… what consumers have been saying differs from what they have been doing during the post-pandemic period; consumers say they feel worse, but through the end of 2024, they are buying more – not just spending more – than they did in 2019. This disconnect between what consumers have been saying and doing suggests that consumer sentiment surveys on their own have become weaker indicators of future consumer behavior and of the health of US consumers. While it is important to recognize how consumers feel, we should exercise caution when using consumer sentiment surveys to infer future consumer behavior given this recent disconnect between what consumers say and do.”

BY Doug Kass · Apr 28, 2025, 6:15 AM EDT

BY Doug Kass · Apr 28, 2025, 6:05 AM EDT

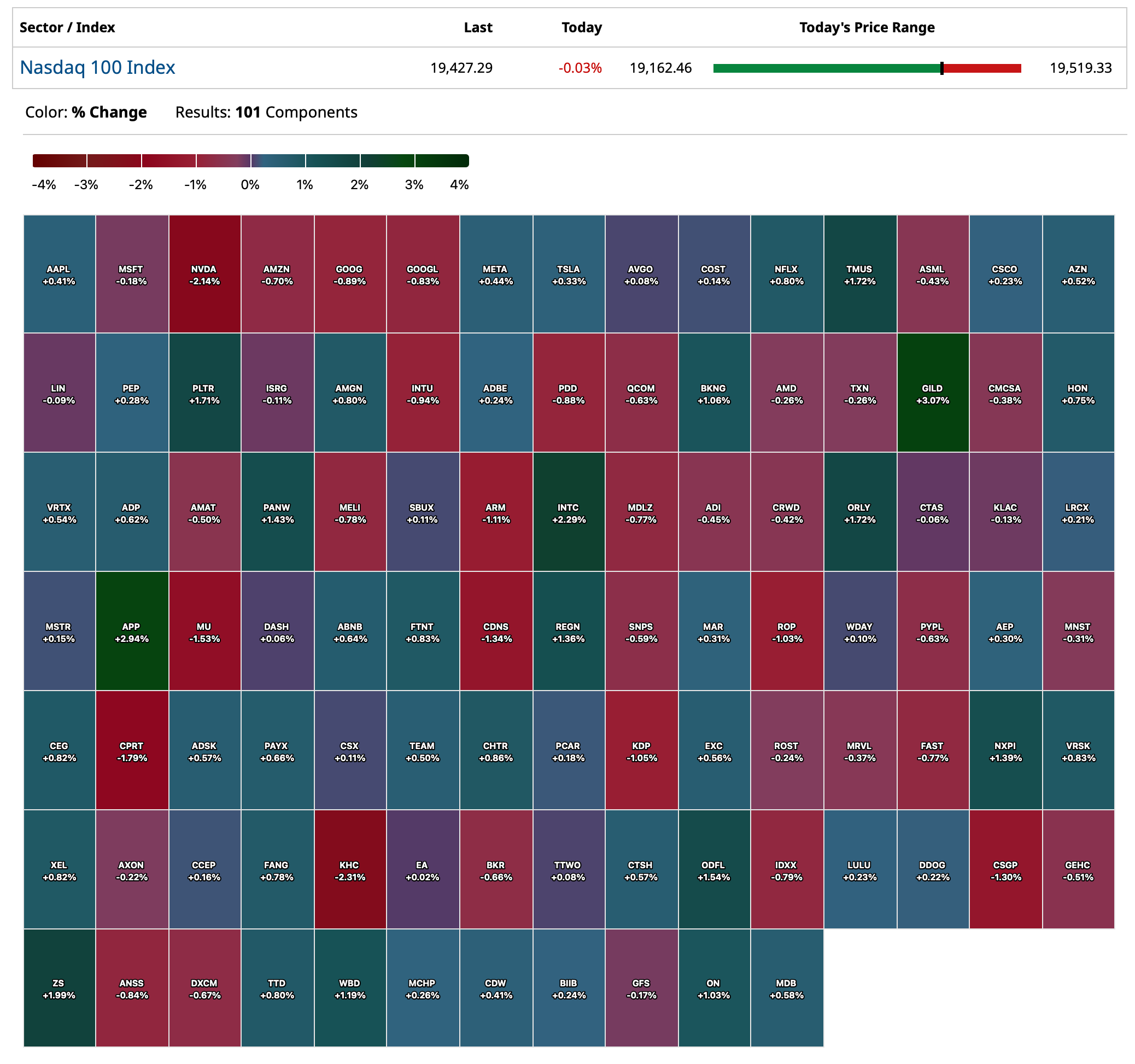

The S&P Short Range Oscillator hit a deeper 5.22% overbought at Friday's close vs. only 2.73% at Thursday's close.

The S&P is now right smack in the middle of my 5500-5600 objective (precision not intended!) and I plan to accelerate shorting on any strength.

BY Doug Kass · Apr 28, 2025, 5:55 AM EDT

Shorted more indices:

* SPY $550.28

* QQQ $472.51

BY Doug Kass · Apr 28, 2025, 5:45 AM EDT

Small business owner explains how Pres. Trump’s high tariffs are raising the cost of his products made overseas. “I’m actually better off just lighting that on fire and taking the loss than I am trying to bring it into the country.” abcnews.link/neOXoQs