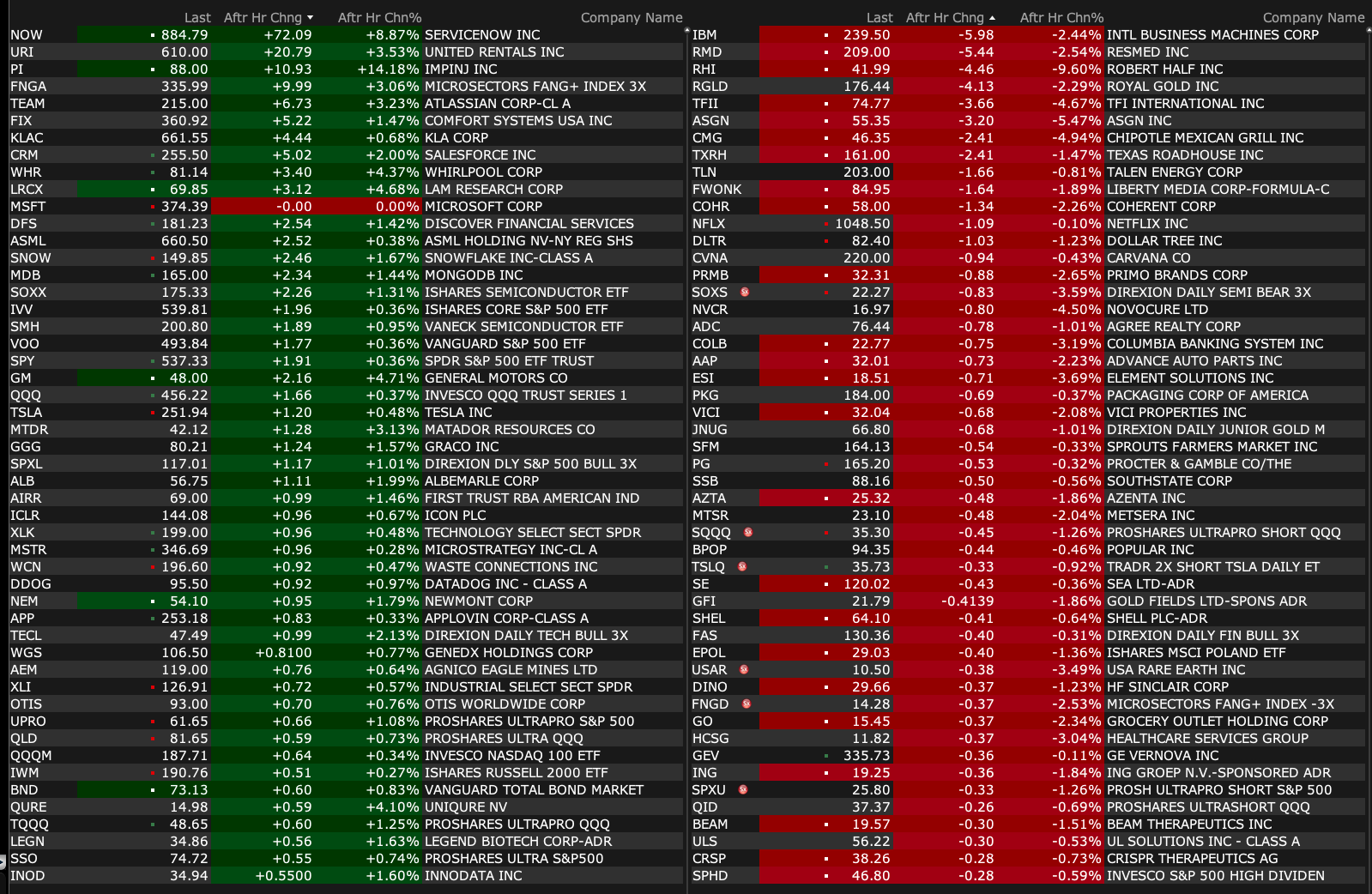

Wednesday's After-Hours Movers

At 4:20 p.m.:

BY Doug Kass · Apr 23, 2025, 4:50 PM EDT

At 4:20 p.m.:

BY Doug Kass · Apr 23, 2025, 4:50 PM EDT

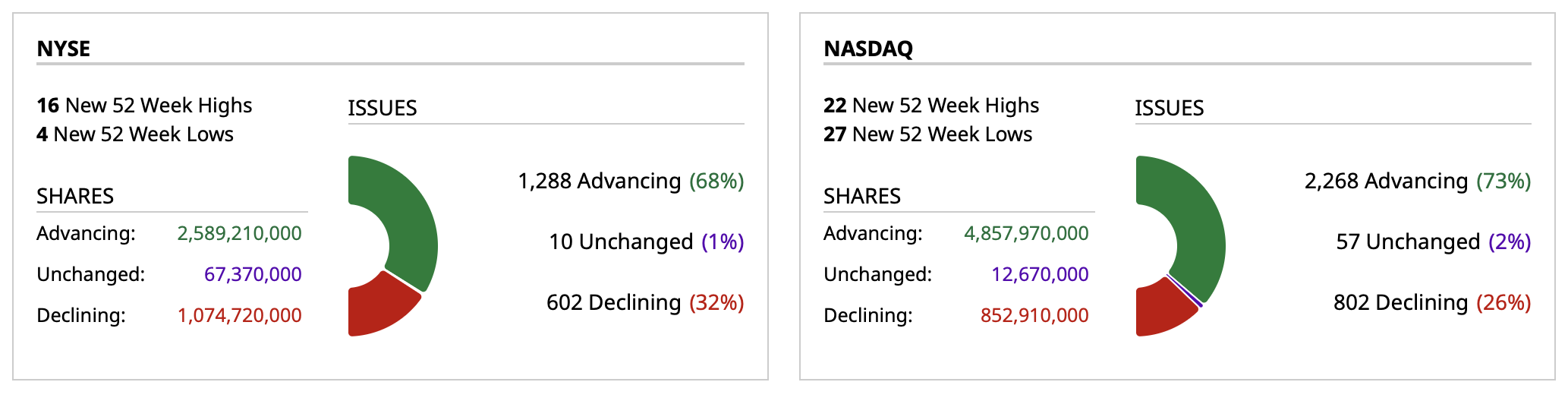

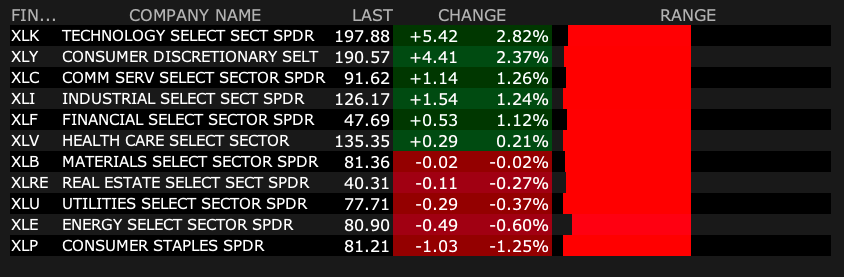

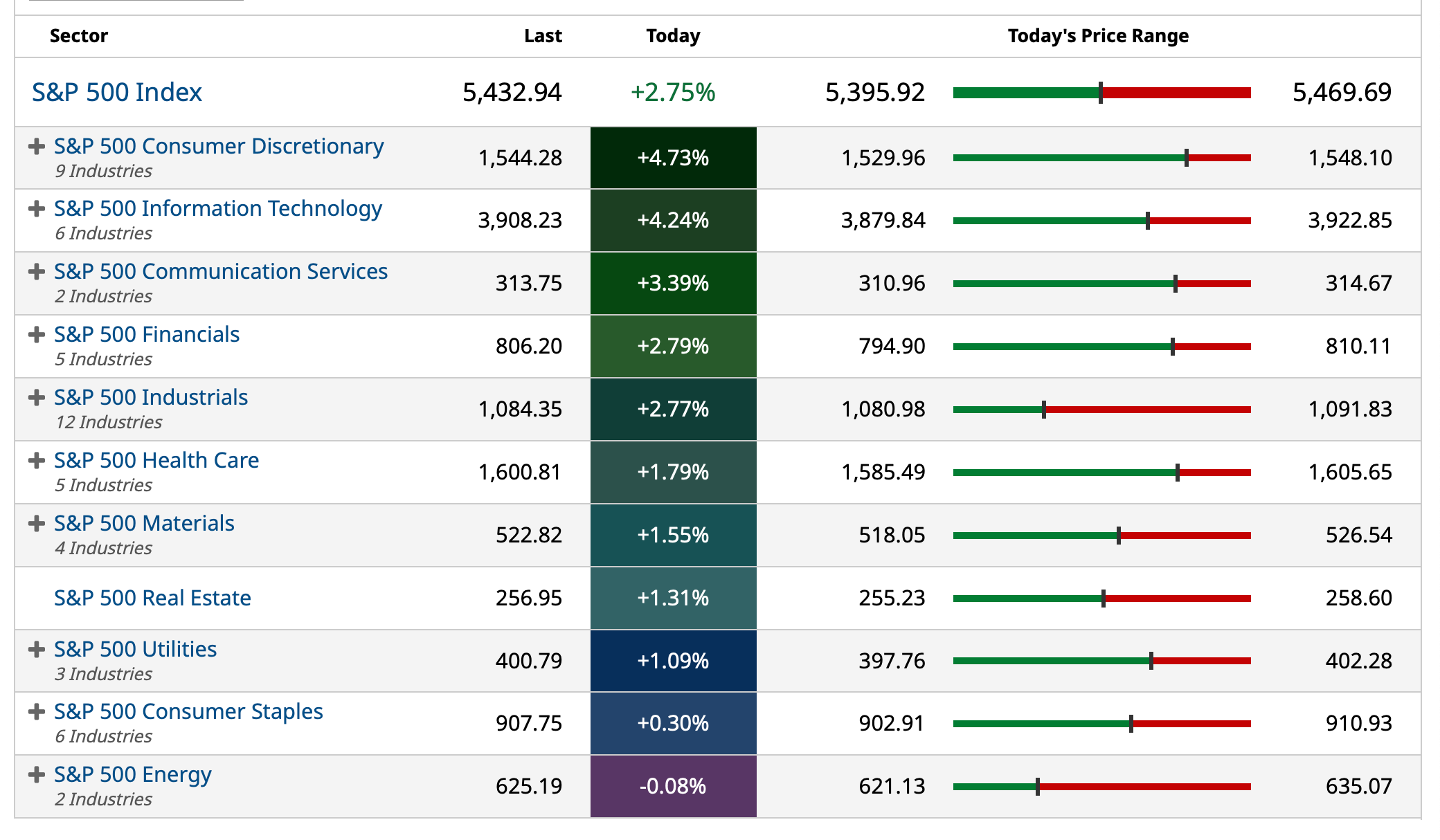

- NYSE volume is 7% below its one-month average

- NASDAQ volume is 3% below its one-month average

- VIX index: down 6.97% to 28.44

BY Doug Kass · Apr 23, 2025, 4:41 PM EDT

After numerous false starts it is not surprising that cannabis investors/traders are in disbelief of any possible legislative initiatives.

However, I am hearing at several levels that there is movement and progress.

Here is one example that just came out:

I plan to buy even more aggressively in the morning...

BY Doug Kass · Apr 23, 2025, 4:30 PM EDT

Here are today's "things":

* I shorted and covered indices for a small lloss.

* I shorted SPY and QQQ calls (unrealized profit).

* Collapsed one of my index straddles for a small loss.

* Sold the balance of my MSFT long at $379.90.

* Added to MSOS at $2.45, TCNNF at $3.90, TSNDF at $0.268, and GTBIF at $5.33.

BY Doug Kass · Apr 23, 2025, 3:56 PM EDT

Here is a partial list of the individual equity long and short positions I have mentioned in my Diary (I have other positions):

Longs: DKNG, TOL, PHM, GRBK, JOE, KBH, BAC, JPM, C, WFC, AXP, GOOGL, KKR, APO, BX, MS, GS, IBKR, GOOGL, META, AMZN, MSFT, CRLBF, FGEN, TCNNF, AYRWF, VRNOF, GTBIF, CURLF, PSIL, TSNDF, VVV

Shorts: BXMT, ROAD, CHGG, MSTR, FIGS, WBD, CRWV, WOOF, RILY, BOOT, KO, PEP, SNBR, WGO, AEG, FXLV, ABR.

BY Doug Kass · Apr 23, 2025, 3:00 PM EDT

BY Doug Kass · Apr 23, 2025, 2:40 PM EDT

BY Doug Kass · Apr 23, 2025, 2:15 PM EDT

IWith the S&P Index +125 handles, I closed the straddle below and I am selling in-the-money index calls (getting shorter) — creating a small delta-adjusted net short in my old straddle:

Putting on some more at the money straddles on the indices for May and June (small sized).

Position: Short SPY common (VS), calls/puts (S), QQQ common (VS), calls/puts (S)

By Doug Kass Apr 23, 2025 11:25 AM EDT

BY Doug Kass · Apr 23, 2025, 1:46 PM EDT

* From the great TechNova:

TechNova

The Donnie Market : As sure as the Sun rises on the East and sets on the West, Donnie caved.

Part 1.

For those who participate in the Comments section this should have been as predictable as the outcome of a Russian Election.

1) Donnie did not have the cards.

The U.S. is a net consumer of goods. We don’t make anything, which is why we have “Trade Imbalances” with countries that only have Penguins for inhabitants. You cannot box out the largest country that actually makes goods that both the US, and the rest of the World needs.

2) You don’t get China to the table by calling them “Peasants”

An even cursory study of Chinese History will tell you that the Chinese would rather eat bricks for lunch for the next 100 years, than accept any terms from a foreigner that disrespects their long heritage. (Google how the Japanese treated the Chinese decades ago, and ask Chinese people today how they feel about Japan).

3) You don’t start a Trade War with the Entire World.

Donnie thought it smart to first attack our most fervent allies: Canada and Mexico, then to move that attack to the entire planet. In all of world history, any time someone attacked the entire world, the entire world won. Even children’s books with many large colorful pictures would tell you that story. So, there was no excuse.

4) Bullies always behave the exact same and predictable way.

Donnie has been a bully his entire life. His behavior at 78, is now entirely predictable. He went after Canada, the 51st State, and got flamed by a blistering NO BS speech by P.M. Carney in no uncertain terms. A punch directly to Donnie’s nose. Donnie backed down, no more 51st State, no more Mr. Governor. He then pretended to exert some kind of 3D Chess move on China, by getting them to “match his Tariffs”. That nonsensical move was parroted by the entire clown car, except that the rest of the world is not on shrooms and reacted appropriately which was to say “China is the reasonable one in this exchange”. This then shifted to “I have asked China to call me to make a Deal”, which then transitioned to the TOTAL and COMPLETE CAPITULATION we saw today.

So, what comes next?

The first part comes by digesting what happened. This will be spun in every possibly way since we now live in Upside Down World rather than reality. This was a TOTAL ABDICATION. A complete admission of DEFEAT, and a recognition that this entire “PLAN” was not a plan, but the ridiculous follies of a disgraced and fake Economist called Peter Navarro. Donnie now destroyed Trillions of dollars of wealth, created one of the worst Trade Deficits in a 60 day period (a Trade surplus in China), froze all investments and hiring, started an exodus of capital and manpower from the US, and started a chain of causality effects we have yet to even imagine. All of this was for NOTHING. Yes, we will hear of small Tariffs here and there, surgically applied to anyone who did not contribute to World Defi, His Campaign, or the Inauguration Ball, but those, like the famous “DOGE SAVINGS” will prove meaningless to revenues and savings. They will amount to nothing compared to what we lost. They will be like the USMCA was to NAFTA. The same exact deal with Donnie’s lipstick applied.

... continued

Part 2.

Given the amount of folks still in the: “He’s maybe a genius, 3D-4D-8D Chess, “Art of the Deal” camp, I can see us getting some pretty strong Bear Market Rallies. Bull Markets die hard, and many folks believe that these “negotiations” are just business as usual. Just the Ups and Downs of every day negotiations between countries. Now that Donnie has folded like a stack of pancakes, we can go back to business as usual.

To me the sheer propensity of folks still in that camp, makes me think SPY could keep chopping in the near term, but I don’t see it breaking below SPY $500 (in the NEAR TERM) as long as Bessent sticks around to keep pumping “good news” into the News Feed. Even if it is only behind closed doors at private events at JP Morgan (because that is completely normal to do for an active Treasury Secretary). If he quits. All bets are off.

As Fake Deal after Fake Deal get “announced”, I could see SPY first make a run at the 20 SMA around $565 then possibly even to the 200 SMA at $572. That would be enough to get people to believe that the Bull is back!

Real Bear Market Rallies feel like Bull Market Rallies. Remember that if we start moving on a large short squeeze and end up making it to the 200 SMA. You will hear “W” bottom, “V” recovery all over the place.

I think IF we happen to see that number, it is a great opportunity to EXIT, not enter. The danger? Well. We are now in a rapidly rising Global M2 environment. Both in the US and in China.

Printer go BRrrrrrrrrr…….

This level of Global M2 has ALWAYS been accretive to Risk ON assets in the past. That is the catch here my friends. Donnie’s complete FLOP is now timed with a very strong rise in Global M2. This is truly a coin flip.

You now have to weigh the destructive force of what just happened to the US Markets against the historical probabilities of rising prices of Risk ON assets during a rise of Global M2.

To me the damage inflicted was large enough to offset the rise of equities in Global M2. That is simply a hunch, and not a scientific deduction. This is why I believe that any upside is capped at around SPY $575.

Ironically, it doesn’t matter to me personally. My bet this year is on BTC. I have practically no Equity exposure at the moment. BTC’s sole correlation is to Global M2, and now we have a RISK EVENT on all US Assets – Stocks, Bonds, and Treasuries. I believe this flight out of US Assets will not stop because Donnie caved again. The reality is that he is still the President, and as long as that lasts, more follies will be directed at both our friends, and our ever-growing list of enemies.

We know that, and they know that.

EOM.

BY Doug Kass · Apr 23, 2025, 1:10 PM EDT

BY Doug Kass · Apr 23, 2025, 12:55 PM EDT

At 12:24 p.m.:

BY Doug Kass · Apr 23, 2025, 12:44 PM EDT

BY Doug Kass · Apr 23, 2025, 12:30 PM EDT

I covered SPY at $538.27 and QQQ at $457.19 for a small loss.

BY Doug Kass · Apr 23, 2025, 11:40 AM EDT

BY Doug Kass · Apr 23, 2025, 11:28 AM EDT

Putting on some more at the money straddles on the indices for May and June (small sized).

BY Doug Kass · Apr 23, 2025, 11:25 AM EDT

- NYSE volume 13% above its one-month average

- NASDAQ volume 10% above its one-month average

- VIX index: down 11.32% to 27.11

BY Doug Kass · Apr 23, 2025, 11:20 AM EDT

Housekeeping item.

I am out of MSFT long at $379.97.

BY Doug Kass · Apr 23, 2025, 10:55 AM EDT

From Peter Boockvar:

The state of US mfr'g and services/Home sales lift in March but...

The April US composite PMI fell to 51.2 from 53.5 all due to a 3 point fall in the services component to 51.4. Manufacturing lifted by .5 pt to 50.7 and is now the 4th straight month above 50, though barely above 50. Keep in mind, the services side does not include wholesale and retail trade, nor construction for some reason.

S&P Global summed up it like this, “Manufacturing is broadly stagnating as any beneficial effect of tariffs are offset by heightened economic uncertainty, supply chain concerns and falling exports, while the services economy is slowing amid weakened demand growth, notably in terms of exports such as travel and tourism.” I’m sure some manufacturing took place that was sped up during the 90 day reciprocal tariff pause but confidence lifted for those manufacturers who believe they will be protected by tariffs according to S&P Global. As heard from some airlines, assume the weakness in travel and tourism is mostly from Canada and Europe.

Also of note, “Confidence about business conditions in the year ahead has meanwhile deteriorated sharply, worsening among manufacturers and service providers alike, largely thanks to growing concerns about the impact of recent government policy announcements.”

On inflation, “Tariffs are meanwhile being cited as the key cause of higher prices, though labor costs are also reportedly continuing to rise, causing companies to hike their selling prices at a pace not seen for over a year. In manufacturing, the rate of price increase is the steepest for nearly 2 ½ years.”

With regards to the labor market, “Although a modest net increase in payroll numbers was recorded across the service sector in April, manufacturing jobs were cut for the first time since October. Hiring was often restricted by concerns over the economic outlook and demand environments both at home and in export markets, with rising cost concerns and labor availability also cited as restricting factors.”

I have nothing else to add here.

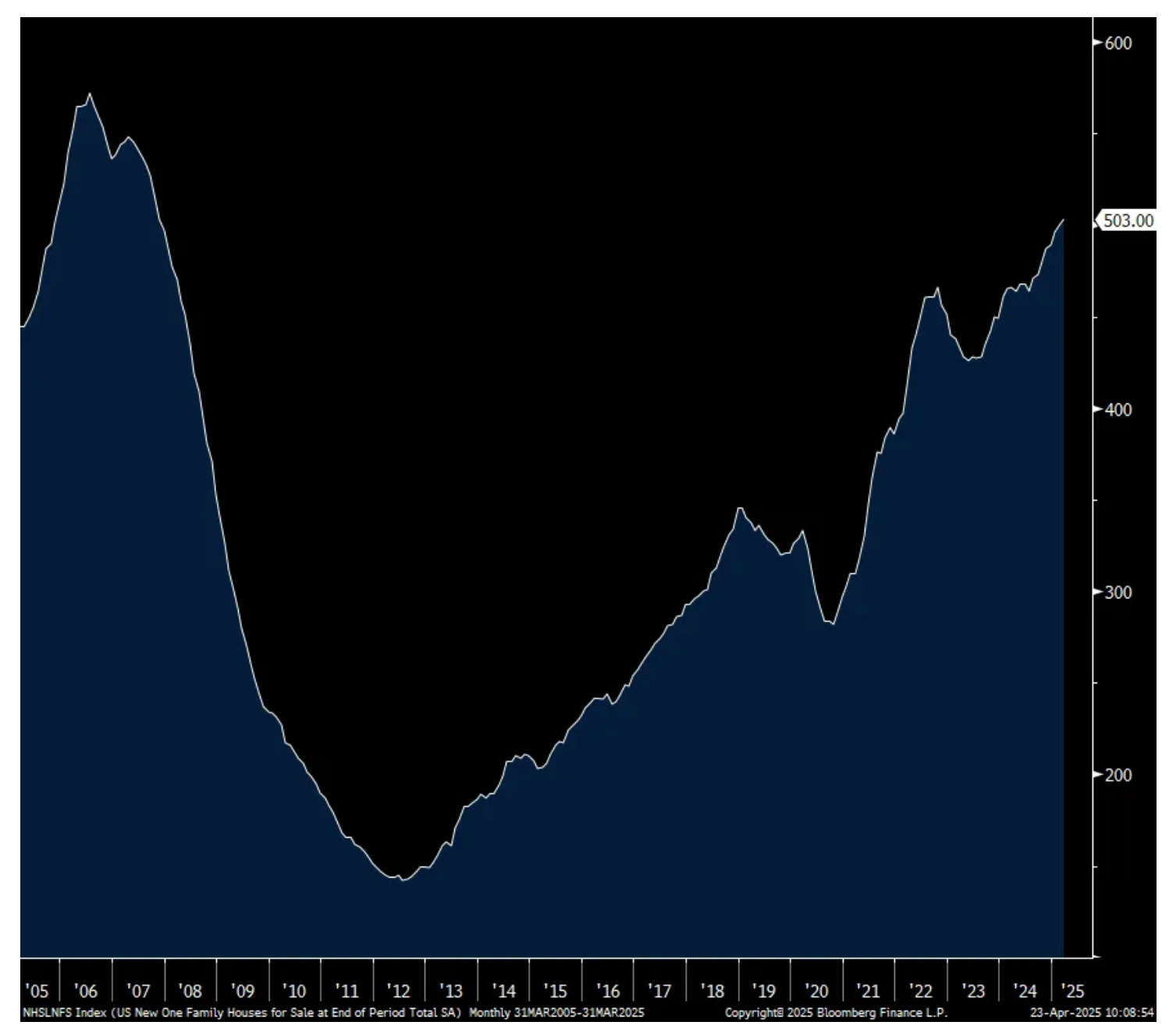

New home sales in March rose to 724k from 674k and that was about 40k more than forecasted. Likely helping was the drop in mortgage rates in March that was proved short lived as they’ve risen since. A jump in sales in the South drove the m/o/m regional gain. Months’ supply fell to 8.3 from 8.9 with the transaction jump but the absolute number of homes for sale rose to 503k, the highest since 2007. Due to mix, the y/o/y home price fell by 7.5% as there was a lift in sales in the number of homes priced below $500k.

I’m going to leave the bottom line to the CEO of Pulte because what was seen in March in terms of activity has faltered so far in April. "In sum, buyer interest and activity in the first quarter were directionally in line with our planning expectations heading into the period. As we've moved from March to April however, we have seen consumers at all price points impacted by changing macro conditions and any resulting decline in overall consumer confidence. Whether it's the volatility in the stock market, concerns about tariff induced inflation, the fluctuation in interest rates, or the growing talk of recession, demand in April has been more volatile and less predictable day-to-day."

Number of New Homes for Sale

BY Doug Kass · Apr 23, 2025, 10:45 AM EDT

* I see limited upside from here...

My view is that the S&P has upside to 5500-5600.

That is all.

I plan to short aggressively into this target.

BY Doug Kass · Apr 23, 2025, 10:20 AM EDT

No trades since premarket.

BY Doug Kass · Apr 23, 2025, 9:59 AM EDT

As of 8:14 a.m.:

BY Doug Kass · Apr 23, 2025, 9:05 AM EDT

-ENSC +165% (receives U.S. Patent for Groundbreaking Treatment of Opioid Use Disorder)

-RZLT +21% (announces Positive Recommendation after Independent Interim Analysis of Phase 3 sunRIZE Study of Ersodetug in Congenital Hyperinsulinism)

-NVAX +12% (believe BLA for Covid Vaccine is approvable based on conversations with U.S. FDA, as of PDUFA date on April 1 and through today)

-SAP +8.7% (earnings, guidance)

-GEV +8.2% (earnings, guidance)

-TSLA +7.0% (earnings, color)

-RRC +6.3% (earnings, guidance)

-TOST +5.3% (hearing Wolfe Research Raised TOST to Outperform from Peer Perform, price target: $44)

-BA +4.9% (earnings; preparing to ask for Federal Aviation Administration approval to ramp up production of its best-selling 737 Max jets to 42 a month this year)

-ISRG +4.9% (earnings, guidance)

-META +4.7% (EU DMA fines announced)

-ZWS +3.8% (earnings, guidance)

-T +3.3% (earnings, guidance)

-ODFL +3.2% (earnings, guidance)

-AAPL +3.1% (EU DMA fines announced)

-COF +3.1% (earnings)

-VIRT +2.4% (earnings)

-NEE +2.3% (earnings, guidance)

-STLD +2.3% (earnings, color)

-CB +1.9% (earnings)

-WSO -5.6% (earnings, color)

-PKG -4.5% (earnings, guidance)

-AVY -3.3% (earnings, guidance)

-OTIS -3.0% (earnings, guidance)

BY Doug Kass · Apr 23, 2025, 8:55 AM EDT

BY Doug Kass · Apr 23, 2025, 8:46 AM EDT

9:00AM: Fed Bank of Chicago President Goolsbee (Voter) gives remarks at the Philadelphia Economic Mobility Summit; (Livestream available. Embargoed text TBD).

9:35AM: Fed Board Governor Waller (Voter) and Fed Bank of St. Louis President Musalem (Voter) give opening remarks before a "Fed Listens" event hosted by the Federal Reserve Bank of St. Louis (Waller text available. No Waller Q&A).

6:30PM: Fed Bank of Cleveland President Hammack (Non-Voter) speaks before the Money Marketeers of New York University (Audience Q&A expected. Text available. Livestream (audio only) available).

BY Doug Kass · Apr 23, 2025, 8:30 AM EDT

From Peter Boockvar:

A bunch here but worth the full read, especially what Elon had to say

It was great to hear the acknowledgement that the current tariff rates that we have on China and they have on us equates to an essential embargo and that it is unsustainable. But, time is of the essence as each day that goes by where there is no dramatic lowering of tariffs, the viability of so many businesses is at risk. And, the reputational damage and loss of trade trust has been done that can't be easily and quickly reversed anytime soon.

The Tesla earnings call was fascinating in many ways. Elon talked about DOGE, the tariffs and the business of Tesla.

"As some people know, there's been some blowback for the time that I've been spending in government with the Department of Government Efficiency, or DOGE. I think the work that we're doing there is actually very important for trying to rein in the insane deficit that is hitting our country, the United States and the DOGE team has made a lot of progress in addressing waste and fraud, but a natural blowback from that is those who were receiving the wasteful dollars and the fraudulent dollars will try to attack me and the DOGE team and anything associated with me. So, then I'm really left with two choices. We just let the waste and fraud continue, and it was continuing to grow at a really unsustainable pace that was bankrupting the country, or to fight the waste and fraud and try to get the country back on the right track. And I believe the right thing to do is to fight the waste and fraud and get the country back on the right track, and working together with President Trump and his administration. Because if the ship of America goes down, we all go down with it, including Tesla and everyone else. So I think this is critical work."

"I do think there's the large slug of work necessary to get the DOGE team in place and working in the government to get the national house in order is mostly done. And I think starting probably next month, in May, my time allocation to DOGE will drop significantly...So I think I'll continue to spend a day or two per week on government matters for as long as the President would like me to do so and as long as it is useful, but starting next month I'll be allocating far more of my time to Tesla."

He acknowledges the challenges that Tesla is currently facing but "I remain extremely optimistic about the future of the company. The future of the company is fundamentally based on large scale autonomous cars and large scale, in large volume, vast numbers of autonomous humanoid robots." The autonomous rides will start in Austin in June.

"I continue to believe that Tesla, with excellent execution, will be the most valuable company in the world by far...It may be as valuable as the next five companies combined."

With tariffs, "yeah, tariff on a company when margins are still low. But we do have localized supply chains in both America, Europe and China. So that puts us in a stronger position than any of our competitors."

"And I just want to emphasize that the tariff decision is entirely up to the President of the United States. I will weigh in with my advice with the President, which he will listen to my advice, but then it's up to him, of course, to make his decision. I've been on the record many times saying that I believe lower tariffs are generally a good idea, generally a good idea for prosperity, but this decision is fundamentally up to the elected representative of the people being the President of the United States. So, I'll continue to advocate for lower tariffs rather than higher tariffs, but that's all I can do."

By the way, the CFO did point out the 100% tariff that India places on incoming Tesla's. The actual tariff is 70% and then there is a 30% luxury tax. "It would be a great market to enter because India has a big middle class which we would want to tap in and that is the market which we want to be in. But again, these kinds of things create a little bit of tension which we're trying to work around."

Me here, just imagine if the ONLY focus was to lower tariffs and trade barriers around the world, like in Indian, along with reshoring crucial industries to friendly places and/or at home. And give up the fantasy that we're going to be making everything again in the US, understand that tariffs don't make us rich just as the income taxes we pay to the federal government don't either, and that trade deficits aren't bad to have.

As for their customers, "Tesla is not immune to sort of the macro demand for cars. You know, so when there is economic uncertainty, people generally want to pause on buying, doing a major capital purchase like a car. But absent macro issues, we don't see any reduction in demand."

From Verizon on its customers:

"When it comes to consumer behavior, I mean, in general, we haven't seen any major consumer shifts in behavior even though we read the same articles as everybody else that consumer sentiment is coming down. Of course, we have a product, the mobility and broadband are so essential for our consumers and for our business customers because it's just so relevant. So we haven't seen that."

On customer payments, "they continue very intact, no deterioration on payments."

As for customers upgrading their phones to the new thing, like Apple Intelligence, "In terms of upgrades, look, Q1 was a bit soft and we didn't chase volumes where there was no demand. We didn't think it made sense for us to chase volumes there."

From Kimberly-Clark:

"We currently expect changes in the global tariff environment to result in approximately $300 million of additional costs this year. We also think it's reasonable to expect economic pressure, especially on value-conscious consumers to escalate as we progress throughout the year."

"At a segment level, we experienced a slowdown in overall consumption in North America as a result of the choppy environment," in addition to some divestitures.

From Capital One:

They again released reserves in the quarter on lower credit allowances and "was driven by continued favorable credit performance in the quarter, partially offset by higher consideration to our downside economic scenario and increased qualitative factors to account for heightened uncertainty." Delinquencies have fallen too they said.

In light of everything going on, the CEO was glass half full. "The US consumer remains a source of strength in the economy. That's true for almost any metric that we look at. The unemployment rate is low and stable, job creation remains healthy, real wages are growing. Consumer debt servicing burdens remain stable near pre-pandemic levels. In our card portfolio, we're seeing improving delinquency rates and lower delinquency entries, and payment rates are improving on a y/o/y basis."

"Now of course, the circumstances of individual consumers and households will vary as they always do and what we look at often with national metrics is averages. And as we've discussed before, some pockets of consumers are feeling pressure from the cumulative effects of inflation and higher interest rates. And we're still seeing delayed charge-off effects from the pandemic, although our improving delinquencies suggest that this effect may be moderating. But on the whole, I'd say the US consumer is in good shape."

As for the possibility of a pull forward of purchases, "In recent weeks, we've started to see an uptick in spend - spend growth per customer relative to this time last year across our consumer segments...We've also seen a recent increase in retail spending, particularly electronics in the past few weeks. Maybe that's a pulling forward of purchases in light of the tariffs. We'll have to see over time. At the same time, we've seen some easing in the T&E growth and airfare in particular."

Also, "When we look at industry data, there appears to be a bit of pull-forward in auto purchases, likely as consumers are trying to get ahead of tariff impacts. And we continue to monitor our application and origination volumes. I think also, there is some early indication that auction prices are increasing more than seasonal norms."

From MMM:

"The US was up low single digits despite the challenging macro backdrop with continued high demand for cable accessories and strength in aerospace, partially offset by weakness in auto. And Europe was down low single digits due to the continued weak environment, including a high single digiti decline in auto builds."

The strength in cable accessories was "driven by construction of data centers and renewable energy projects."

Their consumer business was flattish, up .3% organically in Q1. "Growth in investments in new product innovation drove strength for filters, respiratory products, paint protection, and auto care partially offset by soft consumer spending principally in command and packaging."

On guidance, "Starting with the macro environment, we see a softer outlook than the start of the year. Market forecasts have been lowered reflecting weaker consumer spending and lower demand in industries such as auto and electronics."

From PulteGroup:

"From the high absolute selling prices of today's homes to the resulting high monthly mortgage payments, consumers are struggling with the affordability challenges when it comes to purchasing a home. These headwinds have only been exacerbated recently by growing concerns about the potential for a slowing economy."

How did they mitigate this?, "we have developed and deployed a variety of tools to help consumers overcome their personal home ownership hurdles. This includes offering new produce designs and more efficient floor plans, as well as offering meaningful incentives, including programs that can offer consumers a below market rate on a full 30 year fixed rate mortgage. We leaned into incentives a little more heavily in the first quarter as we executed on our plan to reduce excess spec inventory by actively selling our in-process and finished stock inventory while also adjusting our start pace to better match current demand."

"In sum, buyer interest and activity in the first quarter were directionally in line with our planning expectations heading into the period. As we've moved from March to April however, we have seen consumers at all price points impacted by changing macro conditions and any resulting decline in overall consumer confidence. Whether it's the volatility in the stock market, concerns about tariff induced inflation, the fluctuation in interest rates, or the growing talk of recession, demand in April has been more volatile and less predictable day-to-day."

Speaking of mortgage applications, another rise in the average 30 yr mortgage rate to 6.90% drove a 6.6% w/o/w drop in purchase applications and a 20% fall in refi's.

Yesterday we saw the Philly non manufacturing index for April plunge further to -42.7 from -32.5. In December it was at -3.4 and in October +1.5. The April Richmond manufacturing index dropped 9 pts to -13 with negative signs throughout the internals but big spikes in prices paid and received. Capital spending plans fell too.

Ahead of the US PMI from S&P Global, Japan's composite index rose to 51.1 from 48.9 all due to a 2.2 rise in services to 52.2 while manufacturing remained below 50 at 48.5. Australia's fell at touch to 51.4 from 51.6 with both components lower but still above 50. India's PMI held strong at 60, up .5 pts from strength in both manufacturing and services.

The April Eurozone PMI fell to 50.1 from 50.9 as services fell back under 50 at 49.7 from 51. Manufacturing remained under pressure at 48.7 vs 48.6 in March. S&P Global said, "Manufacturing seems to be holding up better than expected. Despite the US introducing general tariffs of 10% and car tariffs of 25% at the start of April, most manufacturers in the Eurozone are not too fazed. Instead of falling off a cliff, they've actually increased production for the 2nd month in a row, and even more robustly than in March." This could very well be getting stuff done ahead of any trade deal, or not. "The service sector has turned into a bit of a party pooper. Activity has shrunk instead of growing, which it had been doing almost continuously since February 2024. This has pushed the whole economy into stagnation territory."

The UK PMI dropped to 48.2 from 51.5 with manufacturing at just 44 while services fell to 48.9 from 52.5. S&P Global said "The disappointing survey reflects the impact of headwinds from both home and abroad. The biggest concern lies in a slump in exports amid weakened global demand and rising global trade worries, but higher staffing costs have also piled pressure on companies - linked to the National Insurance and minimum wage changes that came into effect at the start of the month. Just as export orders are falling at the sharpest rate since May 2020, during the pandemic lockdowns, firms' costs spiked higher to a degree not seen for over two years."

BY Doug Kass · Apr 23, 2025, 8:20 AM EDT

rolf thrane

Today, Fin Tech TV (CNBC) will be full of cheerleaders if the rally lasts until lunchtime. My problems with the market are

The obvious

1) Fed Put that is a mirage - lowering short duration rates will not change inflation expectations - It will do the opposite and keep current long yields in tact until the economy goes into a tailspin or at least into a significant slowdown

2) Tariff accords may be in play, but that does not mean no tariffs - and China - will be slog to normalize -

3) Less government stimulus. immigration, and more conservative cap-ex will subdue demand

4) Valuations - of course are still high. Maybe not so much on an equal weighted basis, but when has equal weighted been the key metric . If large rich valuation stocks tank, so do other stocks, as we have seen recently.

5) There is pull forward spend which will reduce the need for spending post factum

The less obvious or unknowns

1) Few talk about credit distress - spreads are widening, low end of the market debt repayments are deteriorating, and Credit default Swaps are becoming expensive. Christine Lagarde is not just worried about an economic slowdown, but credit distress around Europe. It is hard to see where a real credit problem will arise - European MBSs are not in good shape. How can subprime lenders in the US not get hit, if the low end consumer is struggling? There has to be some Michael Saylor or other tinderbox - looming - just not sure where the shoe drops

2) There are other triggers hiding in the bushes. Taiwan, the Middle East, who knows

BY Doug Kass · Apr 23, 2025, 7:40 AM EDT

From JP Morgan:

US: Futs are up more 2% this morning led by Tech. There were a few positive developments on the policy front: (i) Trump said that he has no intention of firing Powell, easing some fears on the Fed’s independence (Bloomberg); (ii) Trump’s remarks on China tariff coming down substantially hinted a potential pivot in trade policy (CNN). Pre-market, Mag 7 names are all higher led by TSLA (+6.4%; Musk said that his time on DOGE will significantly drop next month), NVDA (+4.9%), AMZN (+4.1%) and META (+3.7%). 10y yield is down 9bp; USD is higher. Commodities are mostly higher led by oil (+1.6%) and base metals; gold is 1.3% lower.

and...

Overnight, there were a few positive developments on the policy front: (i) Trump said that he has no intention of firing Powell, easing some fears on the Fed’s independence (Bloomberg); (ii) Trump’s remarks on China tariff coming down substantially hinted a potential pivot in trade policy (CNN). This adds to yesterday’s positive progress: (i) news article saying that the White House is “closing in” general agreements with Japan and India (POLITICO); (ii) Bloomberg article saying that Bessent expects tariff standoff with China to De-Escalate; (iii) Leavitt said that Trump is “setting the stage for a deal with China” (THE HILL). Overall, we seem to see a potential pivot from Trump in tariff policy, but uncertainties remain given that we have not yet seen a trade deal being made, particularly within G8 countries. Today, keep an eye on PMIs release: Feroli’s preview is further down below.

BY Doug Kass · Apr 23, 2025, 7:30 AM EDT

* Here is my shocked face...

BY Doug Kass · Apr 23, 2025, 7:20 AM EDT

BY Doug Kass · Apr 23, 2025, 7:10 AM EDT

BY Doug Kass · Apr 23, 2025, 7:00 AM EDT

* Technicians excited about bitcoin this morning...

Bonus — Here are some great links:

BY Doug Kass · Apr 23, 2025, 6:45 AM EDT

BY Doug Kass · Apr 23, 2025, 6:35 AM EDT

BY Doug Kass · Apr 23, 2025, 6:25 AM EDT

From Keith:

BY Doug Kass · Apr 23, 2025, 6:15 AM EDT

With S&P futures +115 handles I am fading the strength.

Shorted more:

* SPY $538

* QQQ $455.32

BY Doug Kass · Apr 23, 2025, 6:05 AM EDT

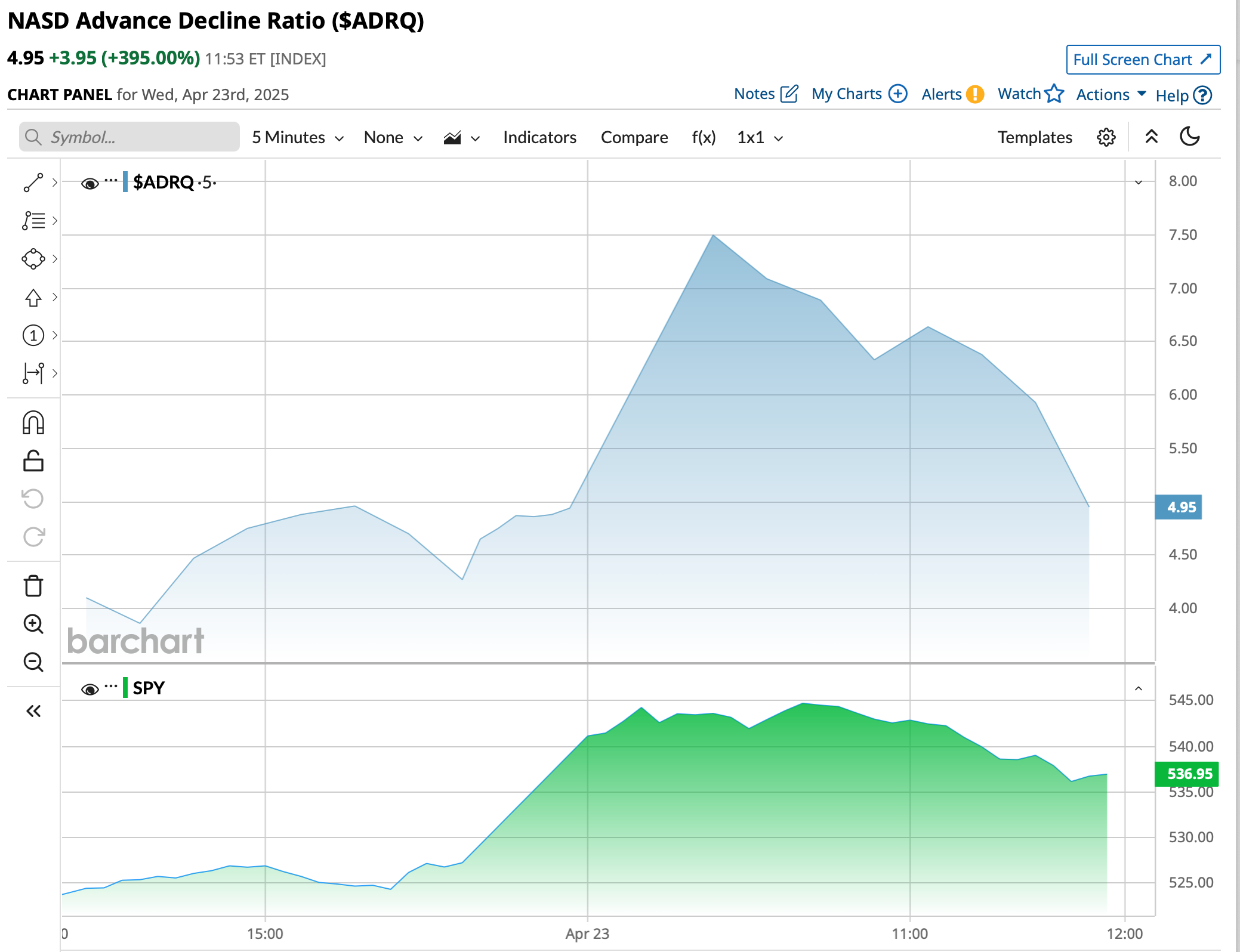

The S&P Short Range Oscillator has moved into overbought at 0.67% vs. -2.43%.

BY Doug Kass · Apr 23, 2025, 5:55 AM EDT

Kass Out:

Dougie Kass

The Pavlovian response to President Trump' s comments on Powell (he wont fire him) and China (we are making progess, which contradicts Bessent comments a few hours ago)- has been to take S and P futures +88 handles and Nasdaq futures +375 handles.

I am taking my entire portfolio of individual equities (except cannabis) to very small size. That includes all technology and financial positions which are ripping after the close. I have eliminated IWM and RSP (on the after hours climb) and I have taken a very small Index short.

Equities have basically rallied to where I thought they would - it has been a tradeable rally.

But Kass is out.

BY Doug Kass · Apr 23, 2025, 5:45 AM EDT