A Quick Gain in the After Market

In the after market, I sold out my TLT at $87.18 for a quick gain.

BY Doug Kass · Apr 22, 2025, 6:35 PM EDT

In the after market, I sold out my TLT at $87.18 for a quick gain.

BY Doug Kass · Apr 22, 2025, 6:35 PM EDT

On the after-hours rip I am selling out of my IWM and RSP in after-hours trading:

* IWM $190.40

* RSP $166

BY Doug Kass · Apr 22, 2025, 6:10 PM EDT

I shorted more SPY at $537.04 and QQQ at $454.02.

BY Doug Kass · Apr 22, 2025, 6:05 PM EDT

In response to a Trump presser, which included that he would not fire Powell and that China tariffs will come down, futures are ripping higher.

I iniitiated a short in the indices:

* SPY $535.10

* QQQ $451.57

BY Doug Kass · Apr 22, 2025, 5:43 PM EDT

At 4:25 p.m.:

BY Doug Kass · Apr 22, 2025, 5:00 PM EDT

BY Doug Kass · Apr 22, 2025, 4:55 PM EDT

Out of TSLA short. Made an oddlot.

BY Doug Kass · Apr 22, 2025, 4:50 PM EDT

BY Doug Kass · Apr 22, 2025, 4:45 PM EDT

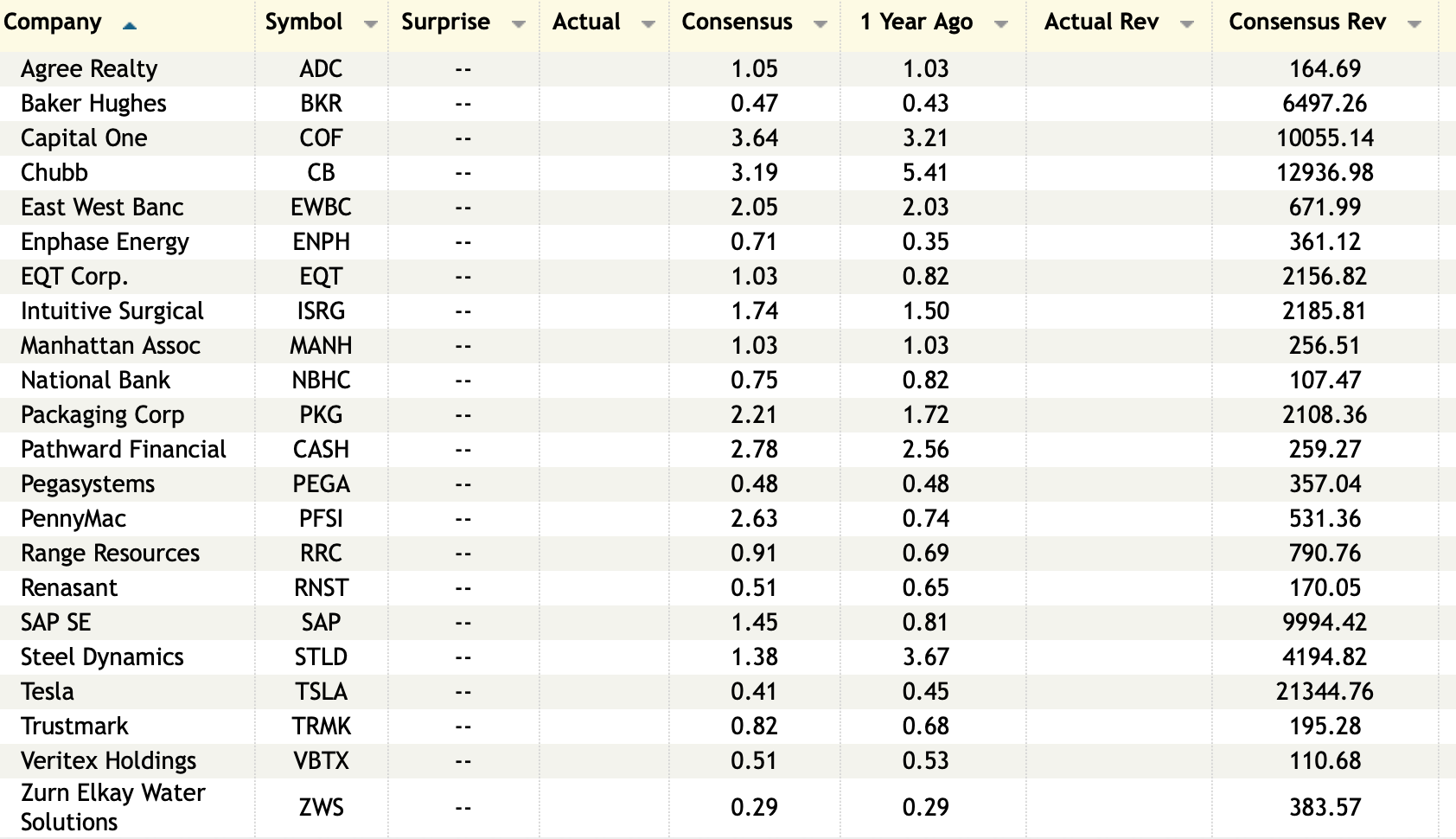

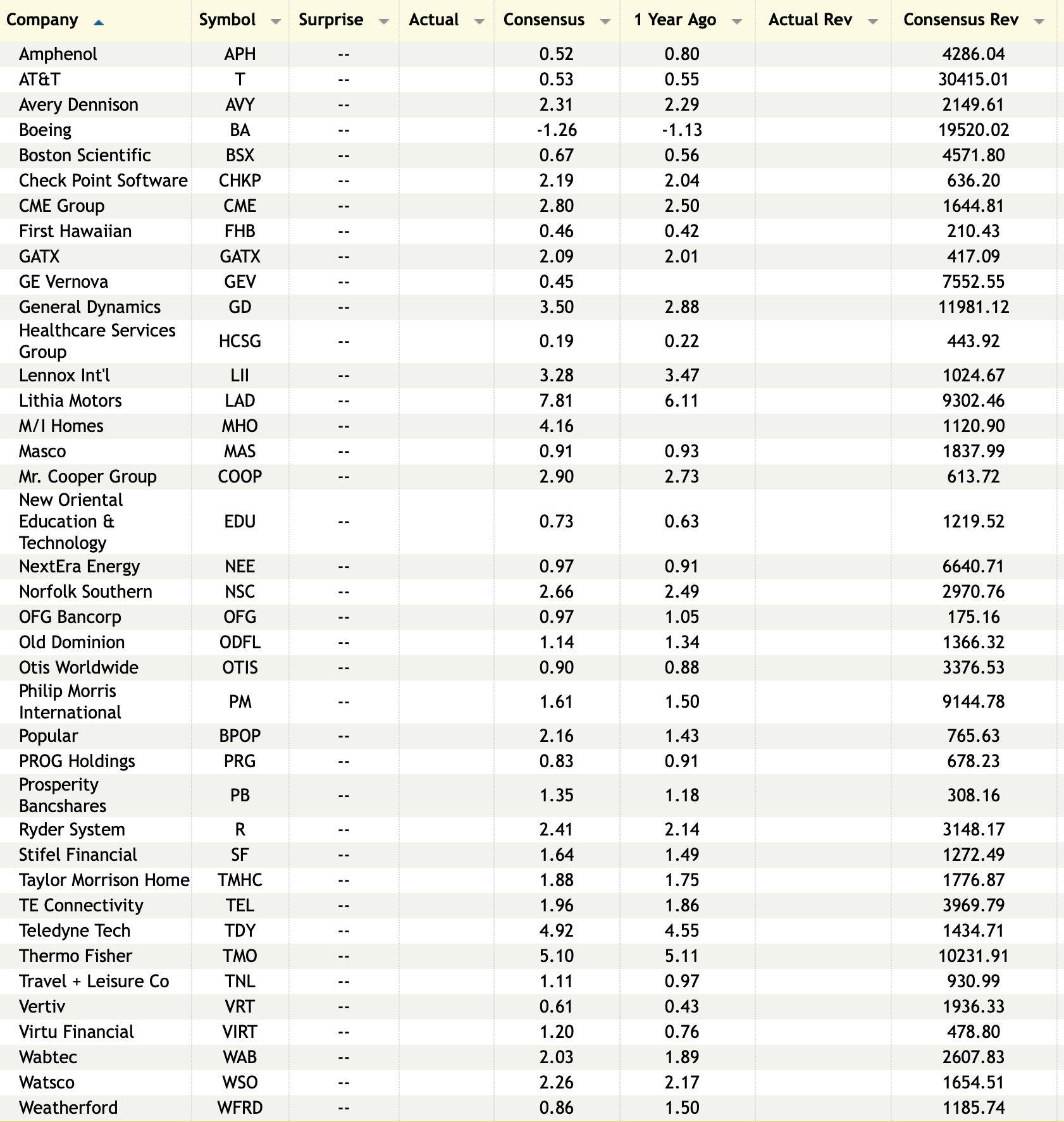

More stats tomorrow...

BY Doug Kass · Apr 22, 2025, 4:40 PM EDT

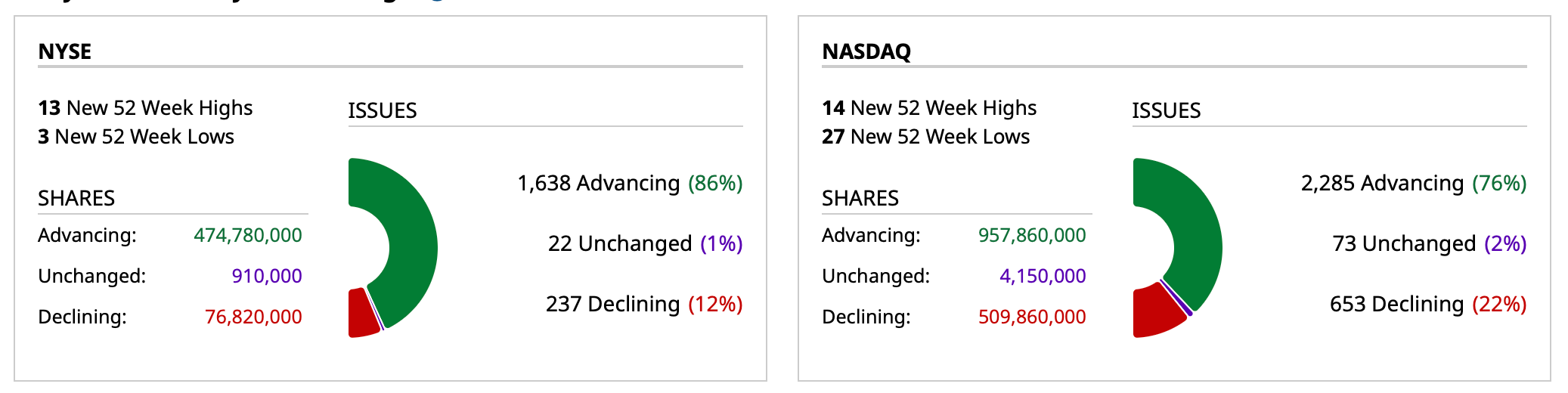

- NYSE volume 23% below its one-month average

- NASDAQ volume 23% below its one-month average

- VIX Index: down 9.31% to 30.67

BY Doug Kass · Apr 22, 2025, 4:25 PM EDT

* Trading rental-kind...

From Comments Section:

Dougie Kass

I took a small short in Tesla at $239.21 into the EPS report.

This is a low confidence trade.

BY Doug Kass · Apr 22, 2025, 4:11 PM EDT

BY Doug Kass · Apr 22, 2025, 3:23 PM EDT

BY Doug Kass · Apr 22, 2025, 3:14 PM EDT

BY Doug Kass · Apr 22, 2025, 2:34 PM EDT

* Let me write what many are thinking...

Desperado, why don't you come to your senses?

You've been out ridin' fences for so long now

Oh, you're a hard one, but I know that you got your reasons

These things that are pleasin' you can hurt you somehow

- The Eagles (Glenn Frey and Don Henley), Desperado

To be blunt, it is pathetic that the bullish cabal is so dependent on positive tariff comments to sustain a rally:

The problems facing a sustained move higher (a condition in which I continue to be doutbtful) are deep and as time goes by, grow deeper.

BY Doug Kass · Apr 22, 2025, 2:10 PM EDT

BY Doug Kass · Apr 22, 2025, 1:55 PM EDT

BY Doug Kass · Apr 22, 2025, 1:30 PM EDT

The only sector that I have not reduced in size is cannabis.

BY Doug Kass · Apr 22, 2025, 1:22 PM EDT

BY Doug Kass · Apr 22, 2025, 1:00 PM EDT

I have moved to small-sized in all of my investment positions.

BY Doug Kass · Apr 22, 2025, 12:52 PM EDT

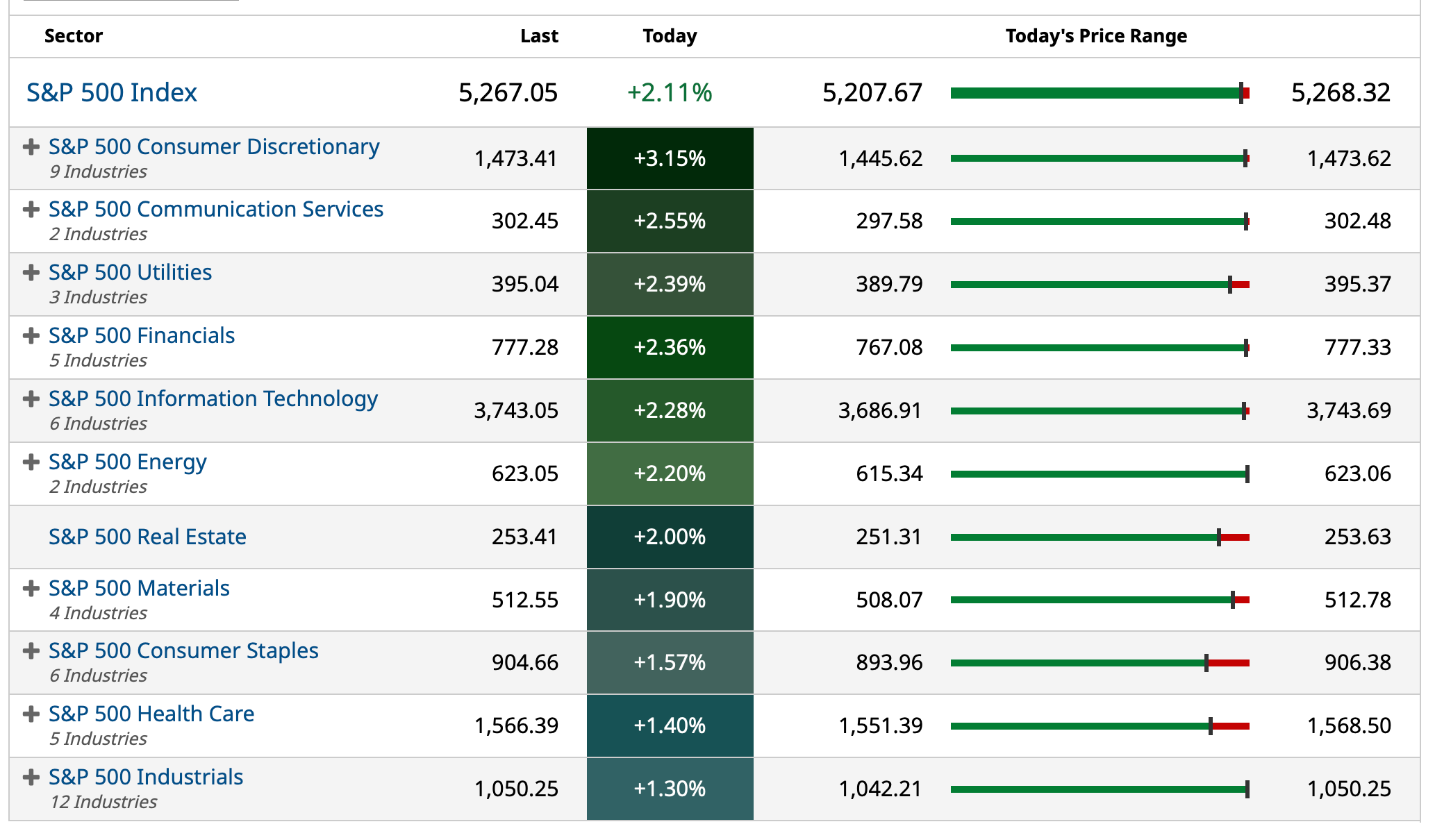

I did not expect today's strength.

With the S&P +147 handles I am going to halve my investment positions across the board.

I just don't trust the rally. It is too "newsy."

BY Doug Kass · Apr 22, 2025, 12:35 PM EDT

- NYSE volume 33% below its one-month average

- NASDAQ volume 26% below its one-month average

- VIX index: down 10.11% to 30.40

BY Doug Kass · Apr 22, 2025, 12:30 PM EDT

With the VIX -3.50 I am collapsing all of my index straddles and strangles for a profit.

I will have no index positions when you get this.

BY Doug Kass · Apr 22, 2025, 12:19 PM EDT

Break in!

Accounting for the rally in last few minutes:

BY Doug Kass · Apr 22, 2025, 12:10 PM EDT

I have a business lunch and I will be out until 1 p.m.

Radio silence.

BY Doug Kass · Apr 22, 2025, 12:00 PM EDT

If you are involved in cannabis, I suggest you tune in to The Dales Report after the close:

BY Doug Kass · Apr 22, 2025, 11:45 AM EDT

US: Futs are higher, following yesterday’s late day buying where the SPX found support ~5,100 level; there is some optimism around a trade deal with either Japan or India and a deal is likely milestone to finally bottom. Pre-mkt, Mag7/Semis are leading with TSLA earnings post-mkt. This week ~25% of the SPX reporting with implied vols among the highest since peak-COVID. The yield curve is twisting flatter and USD seeing a bid following 4 days of losses. The cmdty space is mostly higher led by Energy but gold remains the top story as it sets a new ATH. The macro data focus is on regional Fed activity indicators, but the more impactful data is tmrw’s Flash PMI prints.

and...

Not too much to update overnight as the US stages a rally but the question is whether it can hold or if the market reverses lower, breaking its 5,100 support. At this stage, we feel a completed trade deal is the only catalyst that can break the market out to the upside, and this would still need resilient macro data and solid earnings. So far, earnings season has started weaker than expected but that is with ~12% of the SPX on the tape. Investors should expect volatile moves around the prints.

BY Doug Kass · Apr 22, 2025, 11:25 AM EDT

BofA lowers Boot Barn BOOT price target, sees 'particularly attractive entry point' BofA lowered the firm's price target on Boot Barn to $160 from $195 and keeps a Buy rating on the shares. The company will report Q4 results next month and the firm thinks shares could bounce on FY26 guidance that should include expectations for positive comps in a low to mid-single digit range, mid-teens unit growth, and reduced China sourcing, the analyst tells investors. Shares have been oversold on concerns about a potential sales slowdown and China tariff exposure and the firm thinks the pullback is a "particularly attractive entry point to own one of the only double-digit unit growth stories in retail in a secular growth category," the analyst added.

Figs FIGS price target lowered to $3.75 from $4.25 at Goldman Sachs Goldman Sachs lowered the firm's price target on Figs to $3.75 from $4.25 and keeps a Sell rating on the shares. The firm reduced its outlook for the U.S. apparel and softlines sector to reflect a more cautious macro backdrop. Goldman's economists reduced the firm's U.S. GDP growth outlook to 0.5% in 2025 from 2.5% in 2024 on a Q4-to-Q4 basis and now see a 45% probability of recession, the analyst tells investors in a research note. While Goldman does not incorporate a full recessionary scenario into its estimates, it believes recent market volatility, rising geopolitical uncertainty, and higher tariff rates pose downside risk to earnings.

Nvidia NVDA price target lowered to $150 from $160 at BofA BofA lowered the firm's price target on Nvidia to $150 from $160 and keeps a Buy rating on the shares. Following the H20 effective shipment ban to China on April 15, the firm views China and H20 exposure as "generally de-risked" and believes its revised FY26 and FY27 base case EPS of $3.97 and $5.74, respectively, "fully bakes in the cut." The firm reiterates a Buy on Nvidia as it views the current stock volatility as "an enhanced buying opportunity," the analyst added.

Tesla TSLA price target lowered to $305 from $380 at BofA BofA lowered the firm's price target on Tesla to $305 from $380 and keeps a Neutral rating on the shares. Q1 appears to have shaped up better than previously expected in terms of production volumes and sales, which should partially translate into better-than-expected Q1 results, the analyst tells investors in a preview for the auto group. However, the level of uncertainty related to tariffs is "extremely elevated" and the conversation around tariffs and the potential impact is "far from being settled," adds the analyst, who cut valuation multiples "as much as 1.0x across our coverage" on the belief that the current uncertainty will likely force companies to pull or suspend guidance.

General Motors GM price target lowered to $75 from $85 at BofA BofA analyst John Murphy lowered the firm's price target on General Motors to $75 from $85 and keeps a Buy rating on the shares. Q1 appears to have shaped up better than previously expected in terms of production volumes and sales, which should partially translate into better-than-expected Q1 results, the analyst tells investors in a preview for the auto group. However, the level of uncertainty related to tariffs is "extremely elevated" and the conversation around tariffs and the potential impact is "far from being settled," adds the analyst, who cut valuation multiples "as much as 1.0x across our coverage" on the belief that the current uncertainty will likely force companies to pull or suspend guidance.

Ford FORD price target lowered to $14 from $15.50 at BofA BofA lowered the firm's price target on Ford to $14 from $15.50 and keeps a Buy rating on the shares. Q1 appears to have shaped up better than previously expected in terms of production volumes and sales, which should partially translate into better-than-expected Q1 results, the analyst tells investors in a preview for the auto group. However, the level of uncertainty related to tariffs is "extremely elevated" and the conversation around tariffs and the potential impact is "far from being settled," adds the analyst, who cut valuation multiples "as much as 1.0x across our coverage" on the belief that the current uncertainty will likely force companies to pull or suspend guidance.

Occidental Petroleum OXY price target lowered to $48 from $50 at Piper Sandler Piper Sandler lowered the firm's price target on Occidental Petroleum to $48 from $50 and keeps a Neutral rating on the shares. The firm sees a tricky set up into Q1 prints amid a trade-war and overall macro uncertainty paired with increased OPEC+ supply and a messy seasonal gas tape. While periods of volatility certainly provide entry opportunities in names with deep low-cost inventory and strong balance sheets, for a group where reversion and positioning have also had a big impact on shorter term performance, Piper has a bit of a stronger bias toward oil vs gas heading into Q1.

Eli Lilly LLY selloff on Novo report more than warranted, says Citi Citi analyst Geoff Meacham says Eli Lilly (LLY) shares were weaker yesterday afternoon following a report that Novo Nordisk (NVO) submitted an oral form of semaglutide for obesity to FDA earlier this year. The details are scant, and it remains unknown what dosage or form of semaglutide the submission covers, though Citi suspects it could be a high-dose version of its Rybelsus, the analyst tells investors in a research note. The firm thinks the headline is more negative than warranted, given that Rybelsus has food effect limitations that has stymied its market reception and Lilly's orforglipron demonstrated 14.7% weight loss efficacy at 36 weeks in its Phase 2 obesity study. Citi remains a buyer of Lilly shares.

BY Doug Kass · Apr 22, 2025, 11:10 AM EDT

* In this morning's opening missive I will review my market expectations and the near- and intermediate-term challenges I see

* I will explore my trading/investing tactics and deliver my mind's eye of how to invest successfully in a complex investment mosaic and a very challenging and volatile market backdrop

* I will also examine my "seven lean years" thesis

What follows is a combination of Diary entries and recent communications with my Seabreeze investors. In today's contribution I will spend a bit more time on my tactical strategies in dealing with hostile and volatile markets. I will also try to get you more inside my investing cerebellum, as well as, of course, updating my market view:

During the last 15 months, I have structured my (Seabreeze) Partnership's portfolio conservatively (with mostly pairs trades and modest net short exposure). While failing to expect the emergence of "animal spirits" contributing to large equity fund inflows and a rapid climb in stock prices in the past year, our fund's ability to generate positive investment returns (and not to incur losses) speaks volumes to disciplined risk management (essential in any market environment). Though embracing an admittedly wrong-footed and negative market outlook since early 2024 my fund has recorded profitable returns in 14 of the last 15 months. (My hedge fund's only monthly loss was a meager -0.22%))

"The only certainty is that nothing is certain."

- Pliny The Elder

Looking further out, as I will discuss in today's commentary, my base case is for an extended period of substandard investment returns. As always, I might be proven wrong as I acknowledge the uncertainty of outcomes (see Pliny The Elder!). The factors that influence markets move ever faster these days! So, regardless of my current view, I will remain flexible and opportunistic. Remember, I am not Perma anything. I recognize that shorting stocks preserve capital but buying stocks generate wealth. Despite my intermediate-term market concerns, some sectors and individual securities have already entered value levels (with favorable upside reward vs downside risk) and I have raised our net long exposure to approximately 20%-25%. It seems increasingly probable that, over the next few months, stocks could fall to levels that will encourage me to further and more aggressively expand our net long exposure.

"The trick in investing is just to sit there and watch pitch after pitch go by and wait for the one right in your sweet spot. And if people are yelling, 'Swing, you bum!,' ignore them."

- Warren Buffett

While I will be patient and let stock prices "come to me." It is at that time that it will be time to generate wealth.

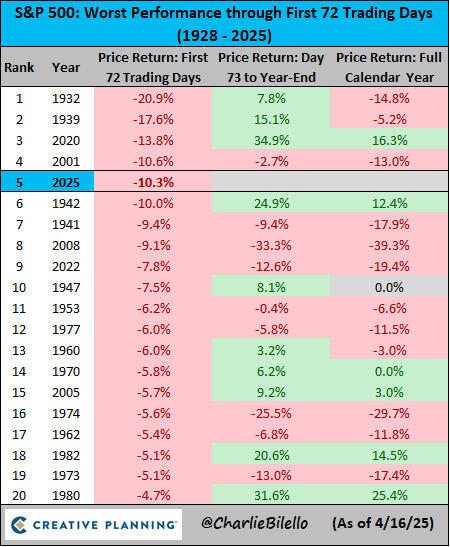

Since early 2024 I have repeatedly expressed a series of concerns regarding corporate profit and economic expectations and sticky inflation. I worried about fiscal and monetary policy mistakes and a paper-thin risk equity premium. I feared that extremely elevated stock market valuations were a poor launching pad for future stock prices. This year the markets have begun to recognize the validity of my concerns and stock prices have fallen. As of Friday the S&P Index is down by -10.3% in the first 72 trading days of 2025:

It got worse yesterday:

Before I restate the market headwinds I see, I will briefly explain why the backdrop of an extended period of non-trending stock prices -- somewhere between slightly higher to slightly lower stock prices (that behave in a volatile manner) -- is the ideal environment for a hedge fund, like Seabreeze, to prosper.

"I don't know how to predict the stock market, I don't know how to predict interest rates, I don't know how to predict business. All I know is if I buy the right kind of business at the right price with the right people I'll do well over time."

- Warren Buffett

Unlike most, I admit to being wrong at times and always in doubt -- that is why we manage your money with a calculator in hand. Having an analytical view of intrinsic values (see Buffett's quote above) and relying on "a margin of safety" keep our uncertainties checked. Let me start by noting that over the course of my investment career I have interviewed thousands of managements. Not surprisingly, not one management team ever expressed concerns about their companies' intermediate-term profit prospects. The same observation applies to money managers. Most asset gatherers state that they can deliver superior investment returns during all sorts of weather.

The reality of investment returns is different, though. Most asset/hedge fund managers only flourish when stocks rise and the tide is in. Few possess the ability to short stocks or to opportunistically capitalize on market volatility by trading unemotionally (and "ringing the cash register") in a period of expanding volatility - when stocks fall and the tides goes out. What makes those opportunities even greater today (than in the past) is the dominance of passive and momentum-based quant trading (like risk parity) that know everything about price and nothing about value. Over history, given my investing style I typically trail rapidly rising markets, but I thrive and differentiate my performance when markets rise slightly, are flat or are down (as I did in 2022, when I delivered positive returns as the major indices dropped by -20%). As I have written in the past, and with a hat tip from Lee Cooperman, here's a quote from the Bible's Genesis 41:27-28, which references the seven years of famine and financial hardship that would follow seven years of prosperity in Egypt (as revealed by Joseph who interprets the Pharaoh's dream): "Behold, seven years of great abundance are coming throughout the land of Egypt, but seven years of famine will follow them. Then all the abundance in the land of Egypt will be forgotten and the famine will devastate the land."

My core view that there is likely to be some lean market years ahead is based on multiple headwinds. Here are a few that concern me:

Besides seeing several years of substandard performance for the major averages, I see a heightened and lengthy regime of greater volatility. This puts a premium on temperament and emotion -- things rarely discussed in evaluating money managers.

"If you can detach yourself temperamentally from the crowd, you will get very rich. You don't have to be very bright, (either), It doesn't take brains. It takes temperament."

- Warren Buffett

These conditions present an ideal setting for the contrarian, for "stock pickers" and for dispassionate and opportunistic traders (that have a sense of "intrinsic value") to produce alpha (or excess returns).

"When things go badly, people become cautious. Then, their caution causes things to go well, and when things go well, they become incautious. I think that’s a forever cycle."

- Howard Marks

Uncertainty in policy and economic/corporate profit outcomes are reagents to continued vaporous market conditions. A regime of heightened volatility is anathema to most buy-and-hold investors who might have problems with it -- having never experienced such volatility in years. By contrast, as I have written, volatility represents opportunity for money managers, as it is satisfying to those with a strong sense of "fair market value" who can capitalize on non-trending markets.

I entered 2025 with the strong belief in several baseline assumptions and expectations:

* The consensus outlook for global economic growth (which serves as the lifeblood for corporate profits and stock prices) was too optimistic. Throughout 2025, growth expectations have been steadily downgraded.

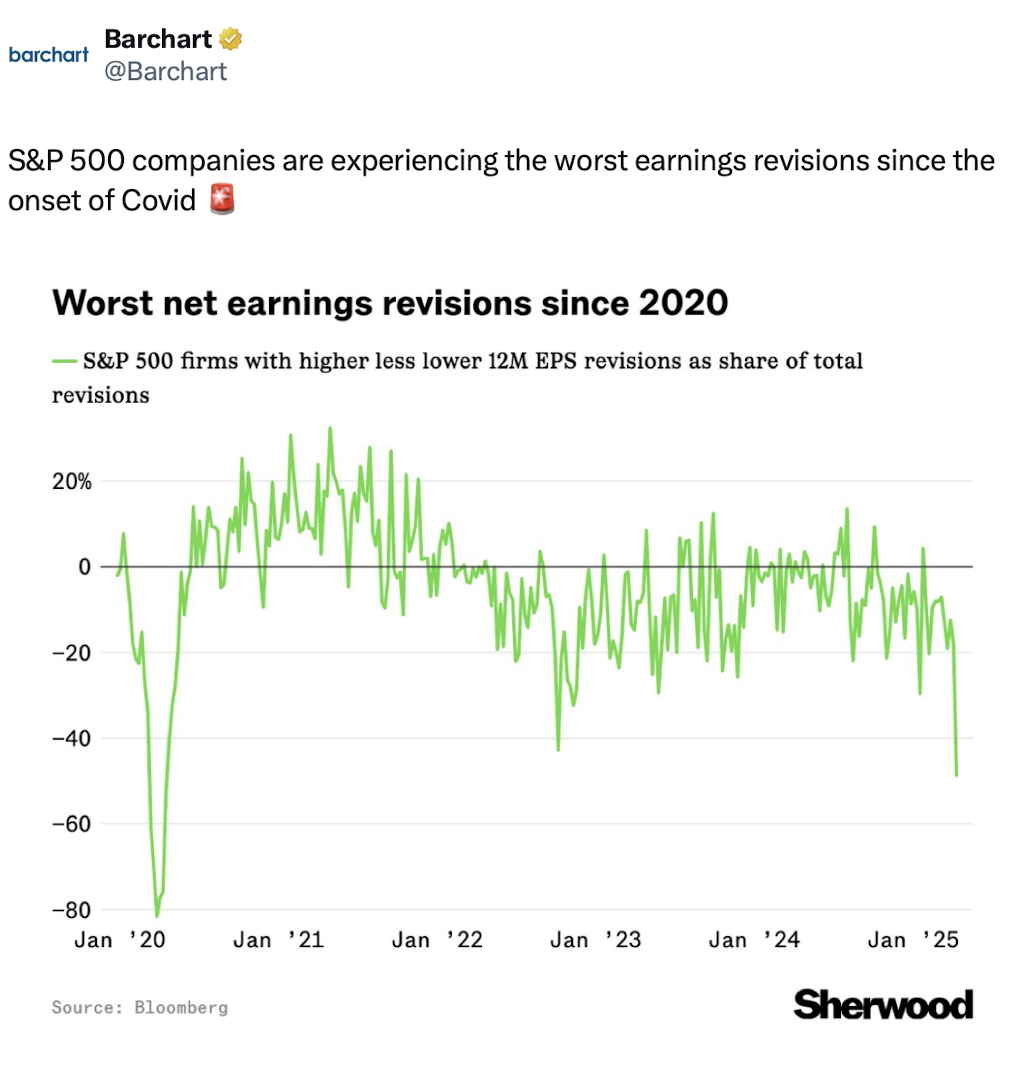

* Consensus 2025-26 S&P profit estimates were unrealistic. Earnings revisions have been marked lower in each of the last seventeen weeks:

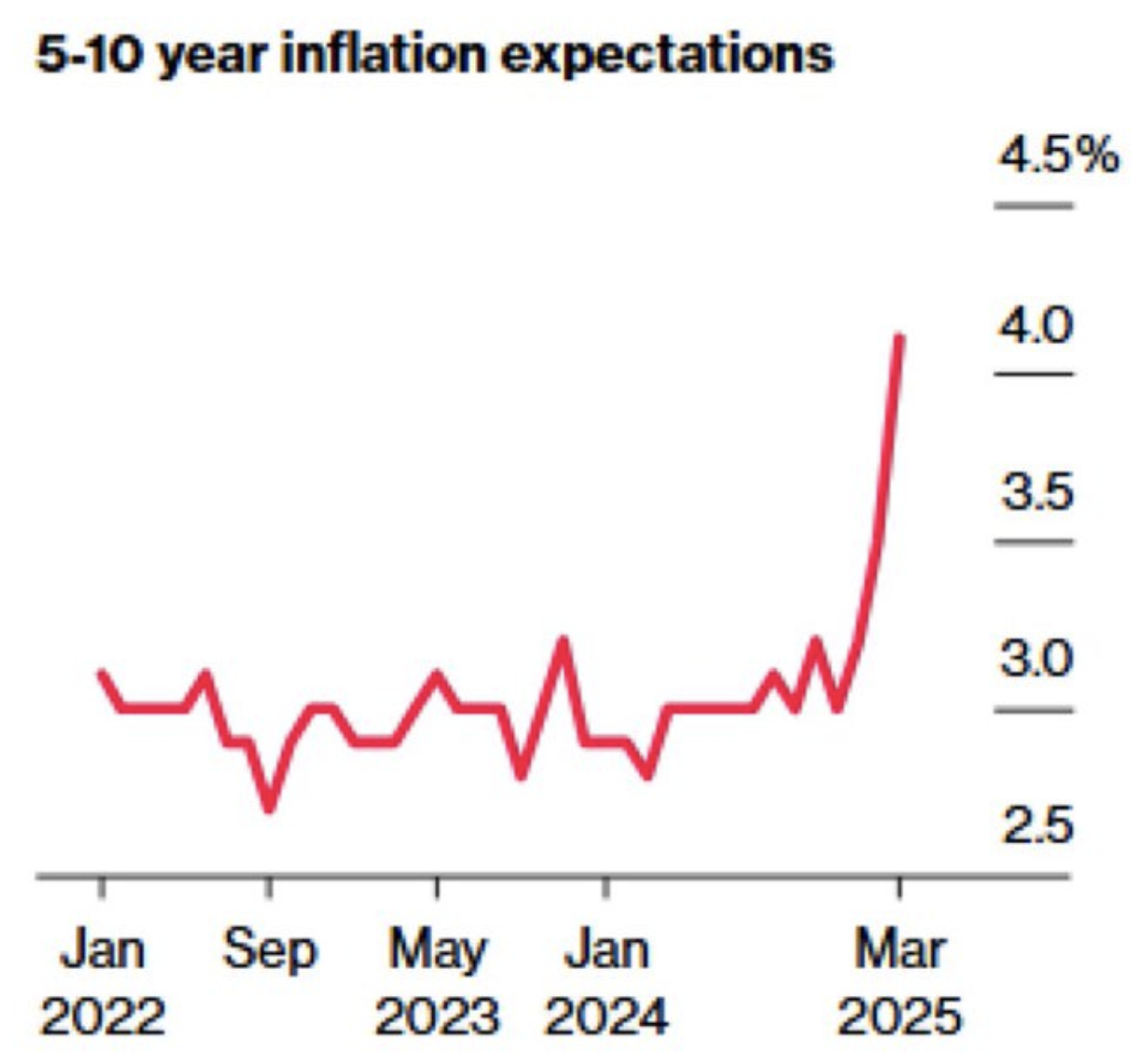

* Inflation would remain uncomfortably high. (Inflation is a price earnings multiple killer) Americans expect inflation to reach +4.1% over the next decade; that's the highest reading since February 1993:

* Fiscal and monetary policies continue to be off the rails and, at times, are dangerously unpredictable and improvisational. Regardless of one's political views, some of these conditions and policies have served to reduce consumer and corporate confidence and have some questioning America as a "safe haven" (with adverse implications for a lower U.S. currency and higher interest rates for longer).

The recent tariff moves, in particular, have the potential to act as a neutron bomb that could wipe out supply chains and small businesses and rekindle inflation - reminiscent of what happened with the spread of Covid.

* Going forward, overseas equities may be viewed as more favorable than U.S. equities. This has already begun to happen. Here is an eighteen-year chart that compares the Vanguard All World Index to the S&P 500 Index.

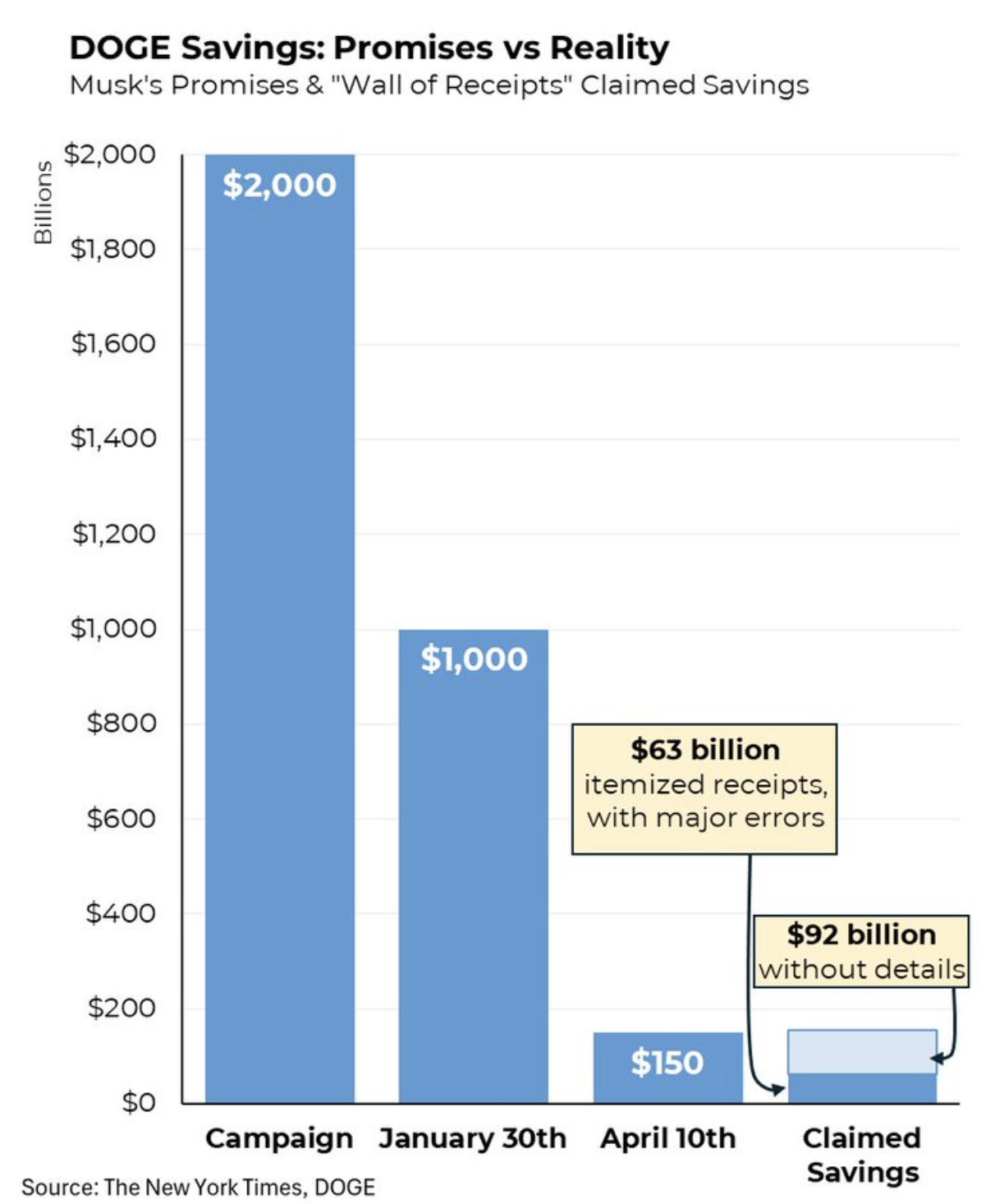

* I expected continued lack of progress in taming the U.S. deficit as Elon Musk's DOGE effort was expected to fall very short of their grandiose expectations. (This, too, has been the case.)

* I forecast that the S&P Index would make the year's top in January 2025. (Thus far this projection has proven correct -- the top was put in place during the last week of January.)

* I expected that the S&P Index had about +5% upside compared to -10% to -15% downside. (Again, correct in forecast thus far; the S&P Index rose by +5% by late January and fell to -16% in early April.) This anticipated range provides us with a general guideline to when we will accumulate equities and when we will disaccumulate (and short) stocks.

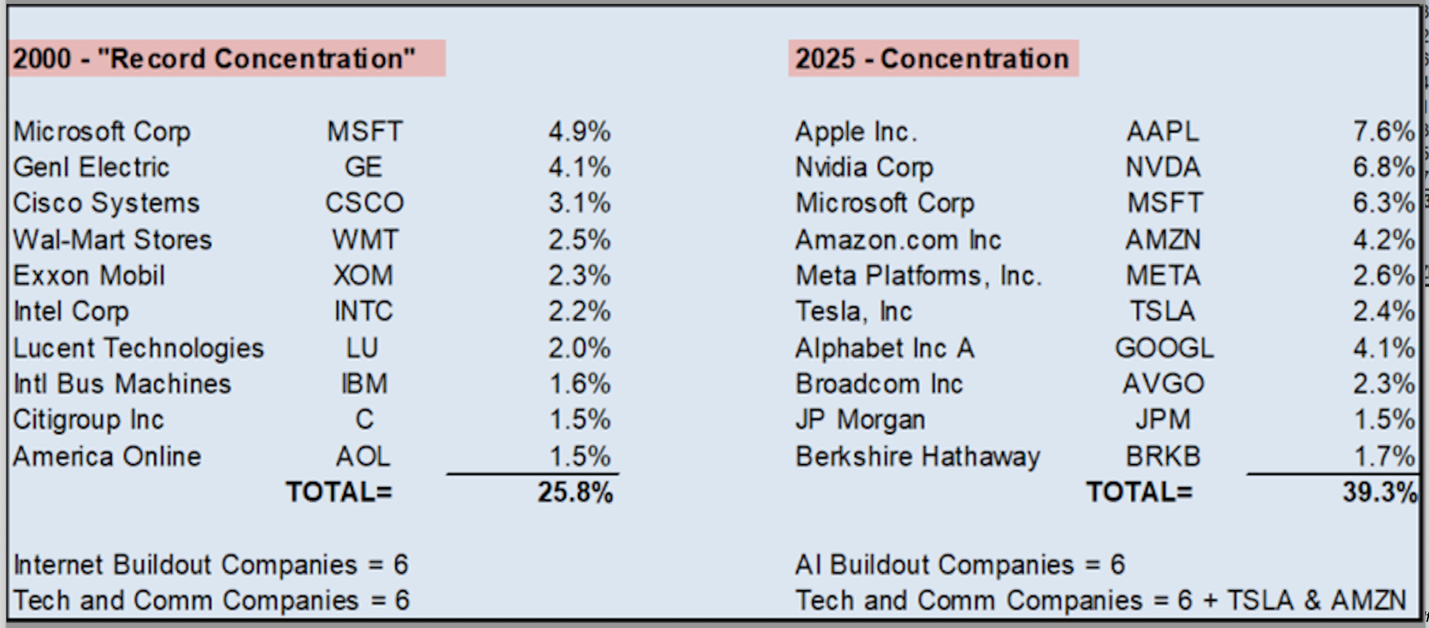

* The long climb of large-cap technology stocks (Mag7) could come to an end early in the year, resembling the end of the popularity of the Nifty Fifty in January, 1973. (This rotation away from Mag7 has been conspicuous this year and is growing ever more glaring in recent weeks.)

I recently wrote:

"The conditions that exist today remind us of an important market top that took place in January 1973. Like 52 years ago, today we face a combative President (Nixon/Trump), market leadership is narrow (it was The Nifty Fifty in the early 1970s and The Magnificent Seven in recent years), interest rates and inflation have turned up (from the prior few decades) and public sector debt has been climbing rapidly. Also, like in 1973, we lack visibility today with regard to any fiscal discipline by our government. In both periods, the forward price-to-earnings was extremely elevated (today, at 23x, in the 96%-tile), the market advance was not broadening out, the "animal spirits" took stock prices higher without a commensurate change in future profit forecasts, and the equity risk premium was paper thin.

An epic market top was completed in January 1973 — leading to a poor year for the S&P Index, which marked the beginning of the end of the Nifty Fifty and several years of weak performance in the Indexes. I expect something similar in January 2025 — an important market top, a down year for the averages and marked by the beginning of the end of the Mag 7, which could extend multiple years. The Unexpected and Leveraged Corners of Speculation* As we have already noted, the entirety of the recent market advance has been based on an expansion in price earnings multiples."

Should I be correct that large cap technology has made a cycle peak, Mag 7’s heavy weighting in the S&P Index and dominance in portfolios will importantly contribute to our lean years thesis:

* Given all of our fundamental and valuation concerns, consensus year-end target price forecasts for the S&P Index for year-end 2025 are still too lofty.

* A number of factors, including market structure and uncertain policy, will likely contribute to unprecedented volatility in our markets this year. (This has proven quite accurate)

BY Doug Kass · Apr 22, 2025, 10:15 AM EDT

With S&P cash +75 handles I am reducing my trading long rentals.

BY Doug Kass · Apr 22, 2025, 10:08 AM EDT

From Peter Boockvar:

I haven't talked about the bullying and belittling of the Fed Chair as it's not the first time we've heard this. I expect Powell to stay in place until he exits stage left next year and he's more focused on his legacy, not someone else's. Regardless of what Powell decides to do though, seen after the Fed cut 100 bps since last September, the long end of the US yield curve is going to go its own way with the likelihood that policy from the administration will have the greater influence, more so than the Federal Reserve.

When you think you're going to truck less stuff on expectations that for now we'll import less goods, you are going to order less trucks. ACT Research yesterday released its final March Class 8 truck order data, totaling 16,500 units, down from February. That figure is down 5.9% y/o/y and "Cancellations rose to their highest point since mid-2023, with a notable uptick in post-Covid pullbacks."

They said "Order activity remains measured, with for-hire carriers maintaining a cautious approach to capital investment. Fleets are responding to ongoing freight market softness, high interest rates, and shifting regulatory signals, including emissions rule reviews and new tariff pressures."

As for smaller trucks, the Class 5-7, orders fell 33% y/o/y to 18.6k units. These medium duty trucks "have slowed through the past four months, as current bloated inventories and a weaker economic outlook weigh on new orders."

From Comerica:

"Muted loan demand, coupled with declines in National Dealer Services (auto dealers) and commercial real estate drove a modest reduction in average loan balances in the quarter."

"Our credit portfolio remained resilient, and despite inflationary pressures continuing to impact customers, our credit metrics remained historically low. Although net charge-offs increased over the very low level seen post Covid, they remained at the low end of the normal 20 bps to 40 bps range."

"Although pipelines and activity levels remain strong, we expect customers to await better visibility before seeing a stronger uptick in loan demand. Recognizing that may not be immediate, we think the 2nd quarter average loans will continue to move down slightly relative to the 1st quarter. From there, we expect to see loan growth resume in the 2nd half of the year."

And what is Comerica hearing from their customers?

"I would say that what you're hearing from customers is that they're not putting the brakes on, but they're taking their foot off the accelerator and you're seeing that around the country and around our businesses, maybe different speeds, if you will, to that approach. I think in markets like Michigan, we've probably seen more concern there than we have per se in Texas, just quite candidly when you talk about middle market."

From Zion Bancorp, who used GenAI to help tell them what is going on:

The CEO "asked ChatGPT for help in explaining the world we're now living in. I got this. 'Trump's tariffs have caused quite a fuss, with markets unsure who to trust. Will prices ascend? Will trade wars extend? Or will growth just stall in the dust?' That actually seemed to explain the time we're in pretty well, I thought." I bolded for emphasis.

He went on to say, "While the outlook guidance always comes with disclaimers about the limitations of forward looking statements, it's worth emphasizing the particular difficulty right now for us and everybody else in this industry in forecasting results a year from now."

As for what they are hearing from business clients on the tariff/trade war:

"I think we've got a lot of businesses in this country that are trying to grapple with really what this is going to mean, whether it's a grand kind of negotiation, I think, that the administration is trying to conduct, and a question as to how far they'll actually allow the economy to get into the ditch before they start to perhaps pull back. I was talking to the owner of a business recently, and he noted that most all of their manufacturing is done in China and Vietnam. He said the only silver lining is all of my competitors are in the same boat. And so, I think it's really hard to gauge how long, how deep the impact could be, but if this goes on for a prolonged period, I personally think it has the potential to be reasonably impactful and really tough for a lot of businesses, small business, large businesses. I don't think it's going to distinguish between the size of the business. It's really all about where their inputs are coming from. And we've moved so much of our manufacturing base to other places, and particularly Asia, in the last 20 or 30 years, that the idea that you can bring that back quickly is kind of far-fetched in my mind."

"So, I think it's still early to know. I think the equity markets are certainly reflecting a lot of concern about it, and that would extend to small businesses as well. It think it's going to have an impact of their willingness to build inventories, to not knowing kind of what price point is that consumers are going to be willing to buy a product where their costs are increasing pretty significantly, and where you could see increased unemployment as a byproduct of all of this."

"Some people liken this to the Smoot-Hawley tariffs, 1930. My belief is it's a really poor analogy because the world was much less interconnected in 1930 than it is today. And so I don't think we have any history that gives us much of a guide personally."

BY Doug Kass · Apr 22, 2025, 9:45 AM EDT

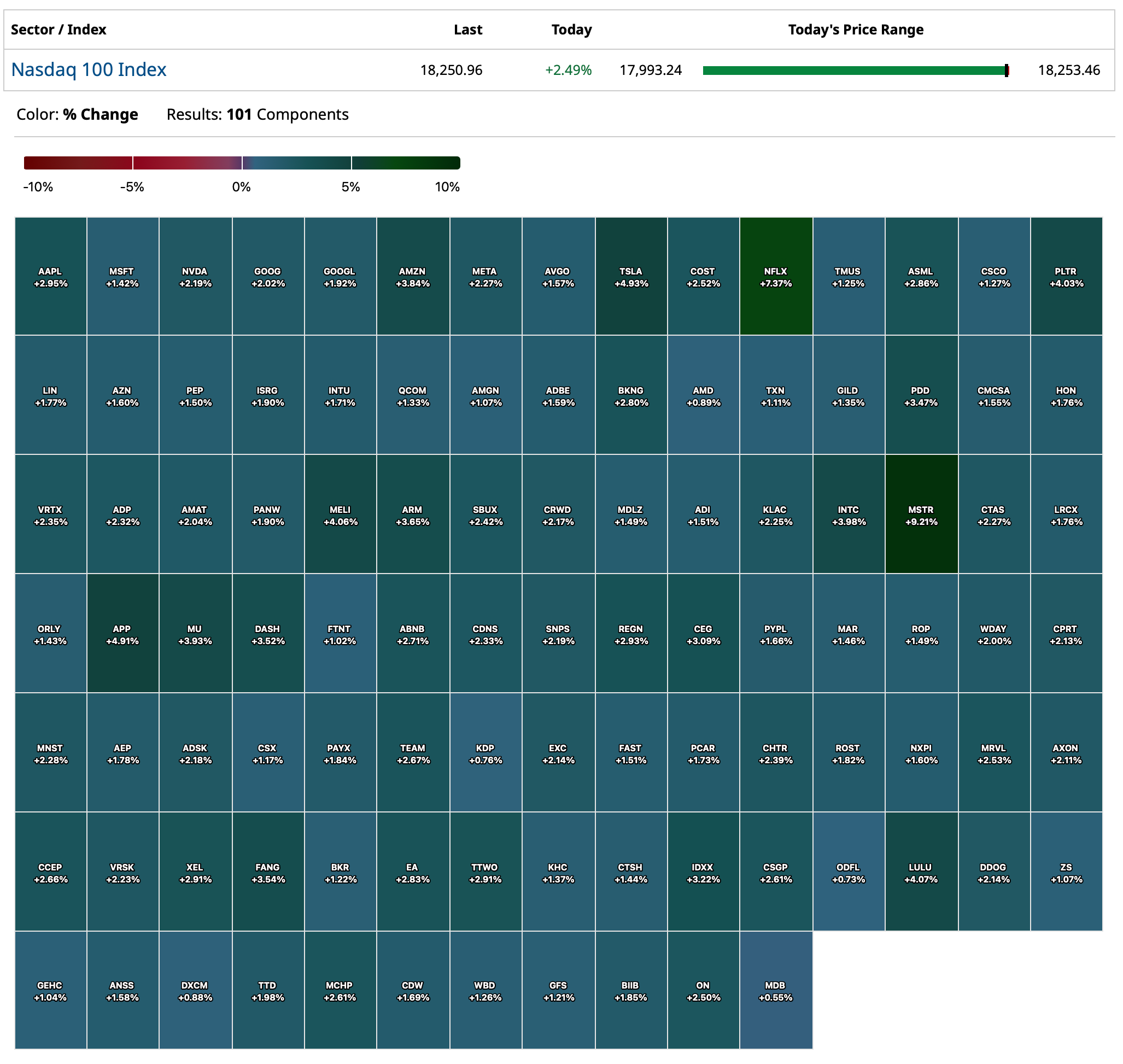

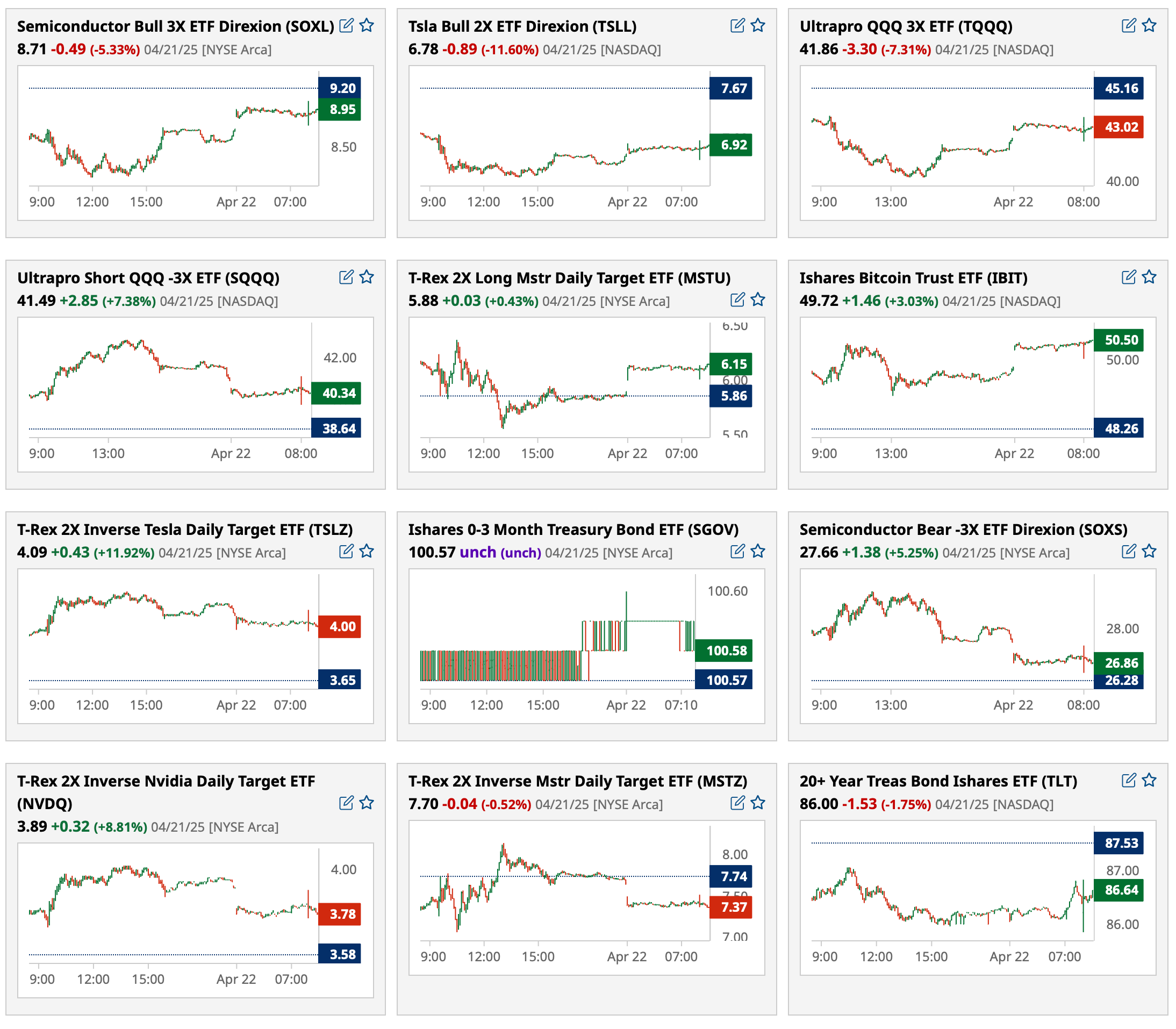

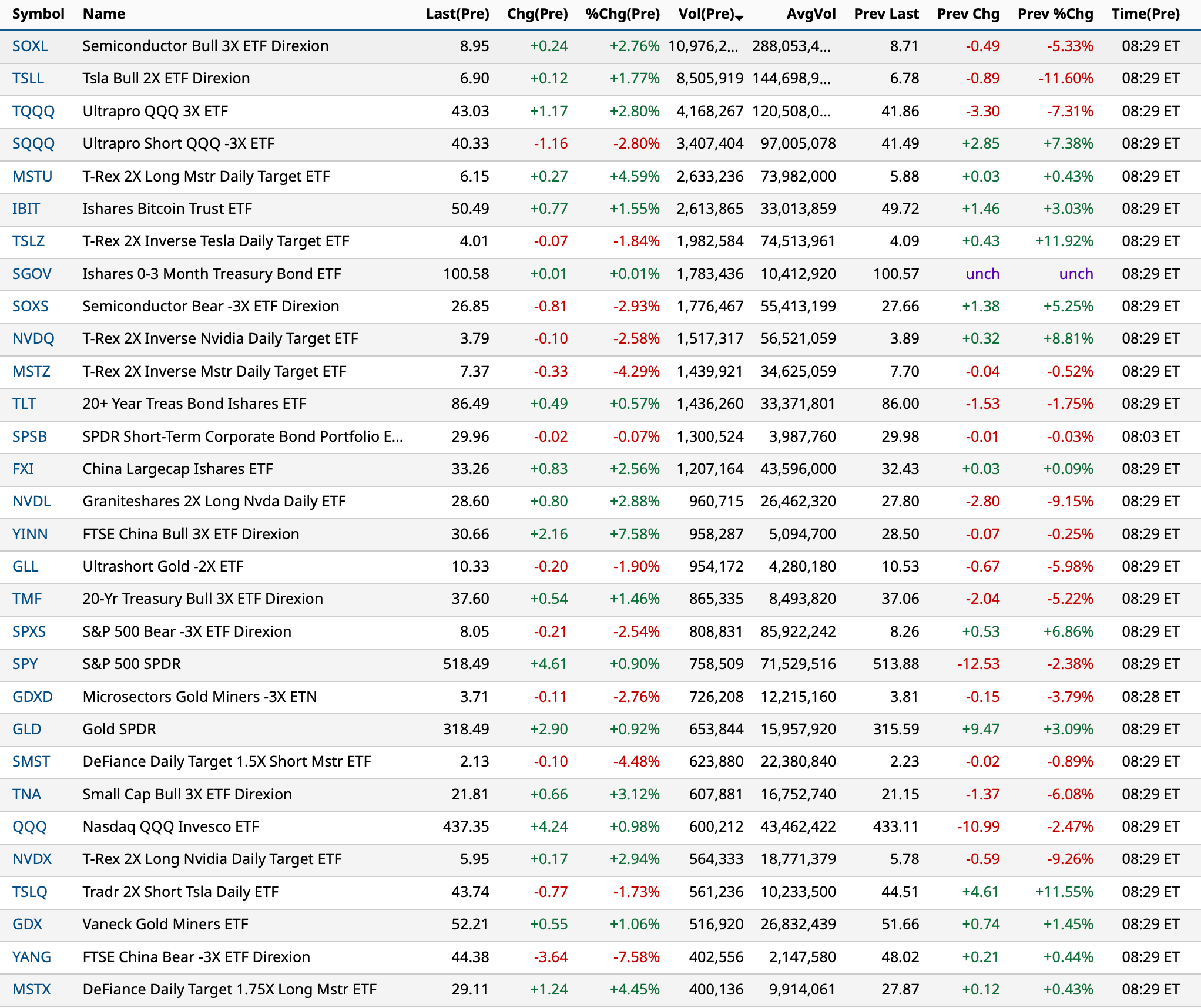

Most active premarket ETFs as of 8:29 a.m. ET:

BY Doug Kass · Apr 22, 2025, 9:23 AM EDT

-ACRS +9.7% (secures U.S. FDA IND clearance for ATI-052, enabling advancement of Novel Bispecific Anti-TSLP/IL-4R Investigational Antibody)

-PNR +7.0% (earnings, guidance)

-MMM +6.3% (earnings, guidance; raises share buyback authorization)

-DHR +6.0% (earnings, guidance)

-DGX +5.0% (earnings, guidance)

-OSTX +4.7% (US FDA Meeting Request Granted; on track for early Q3 submission and anticipate receipt of approval by YE25 with plans to bring OST-HER2 to market in early 2026)

-GE +4.3% (earnings, guidance)

-LMT +3.4% (earnings, guidance)

-EFX +3.1% (earnings, guidance)

-GPC +2.9% (earnings, guidance)

-PHM +2.5% (earnings, color)

-NOC -8.6% (earnings, guidance)

-CURV -6.4% (Goldman Sachs Cuts CURV to Sell from Neutral, price target: $4 from $5.50)

-VZ -5.8% (earnings, guidance)

-HRI -4.9% (earnings, guidance)

-KMB -4.6% (earnings, guidance)

-RTX -3.9% (earnings, guidance)

-SYF -2.6% (earnings, guidance)

-MSCI -2.5% (earnings, guidance)

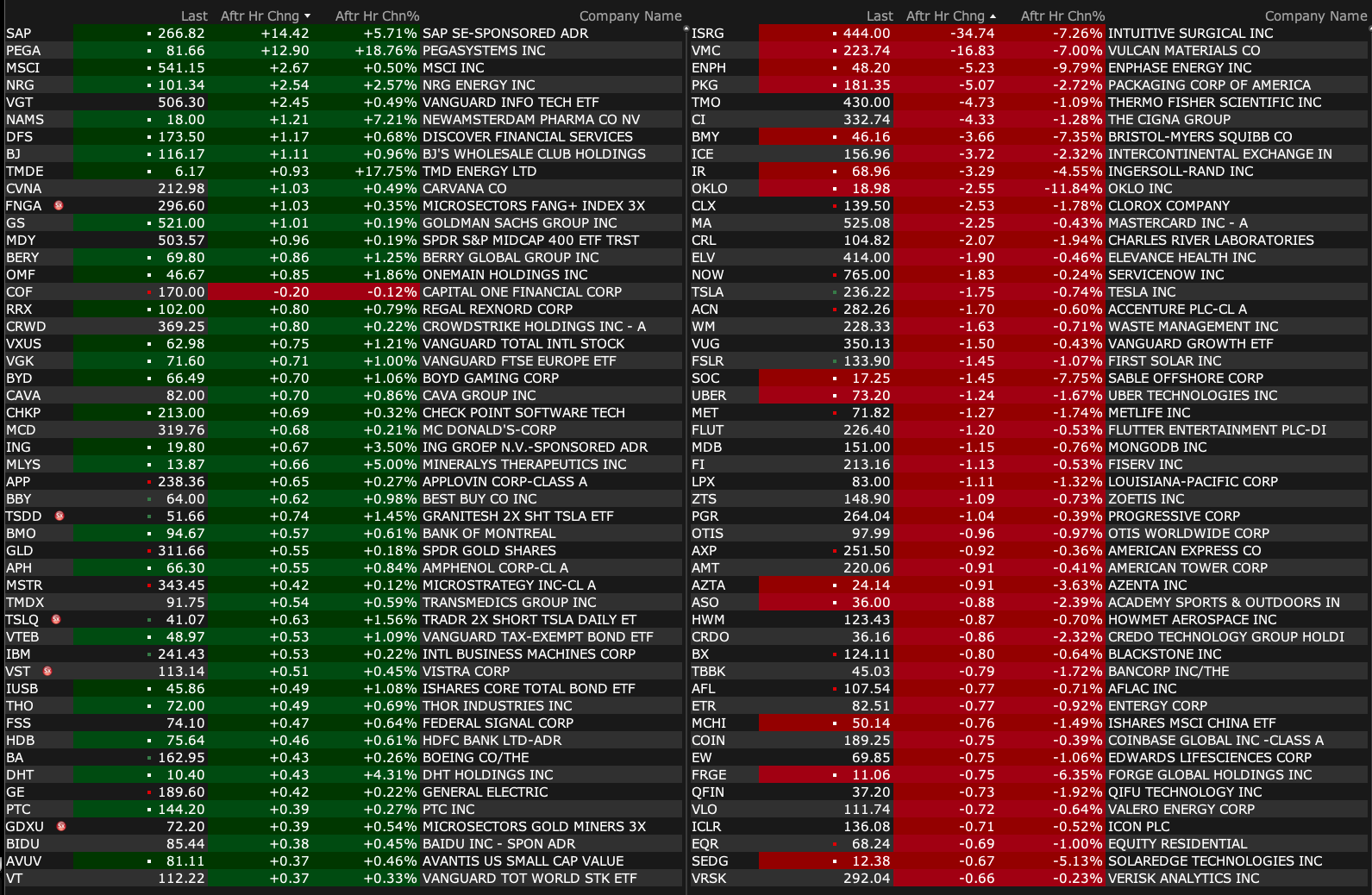

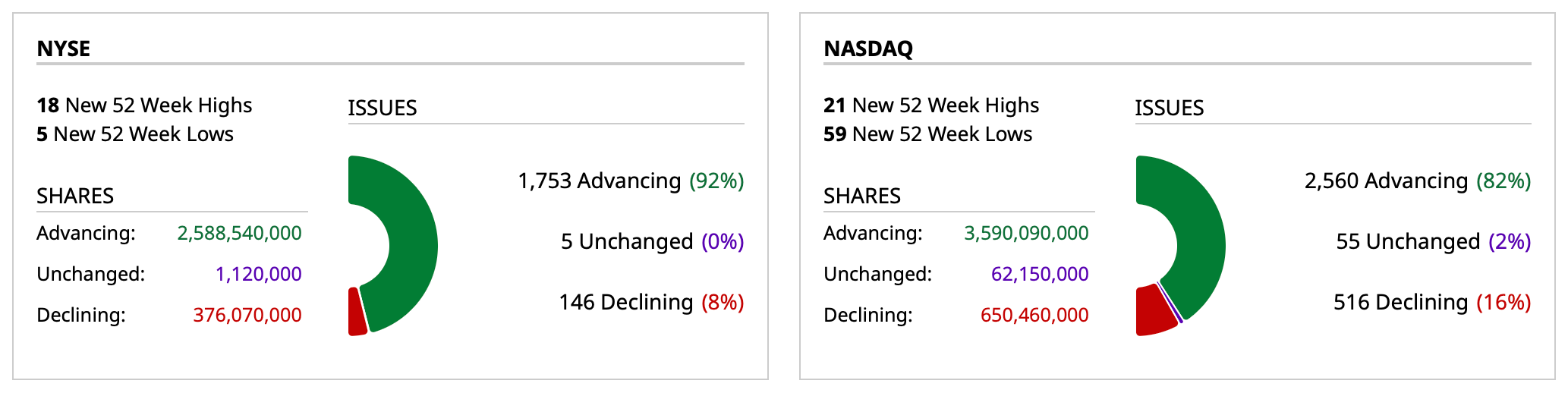

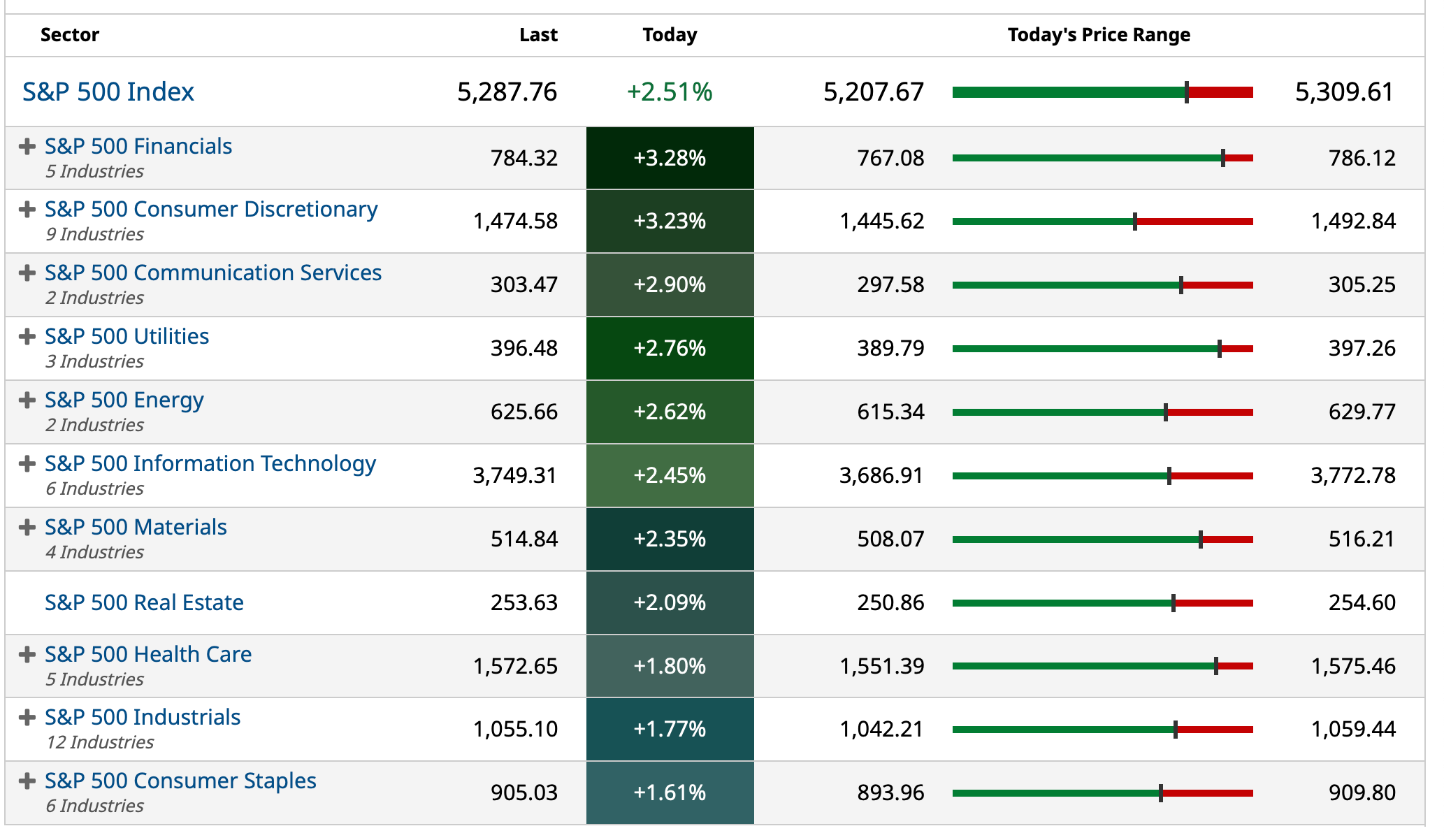

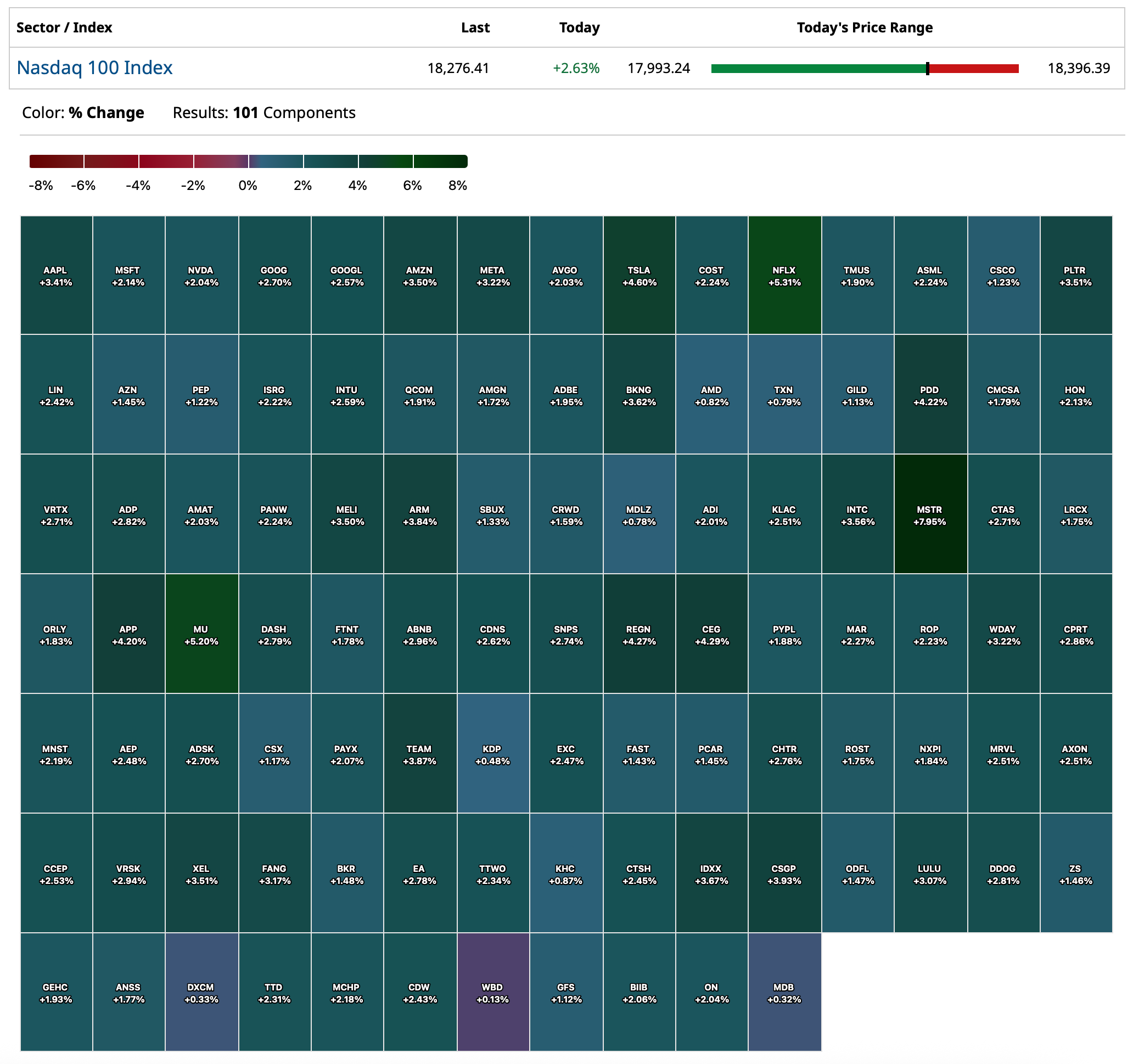

BY Doug Kass · Apr 22, 2025, 9:15 AM EDT

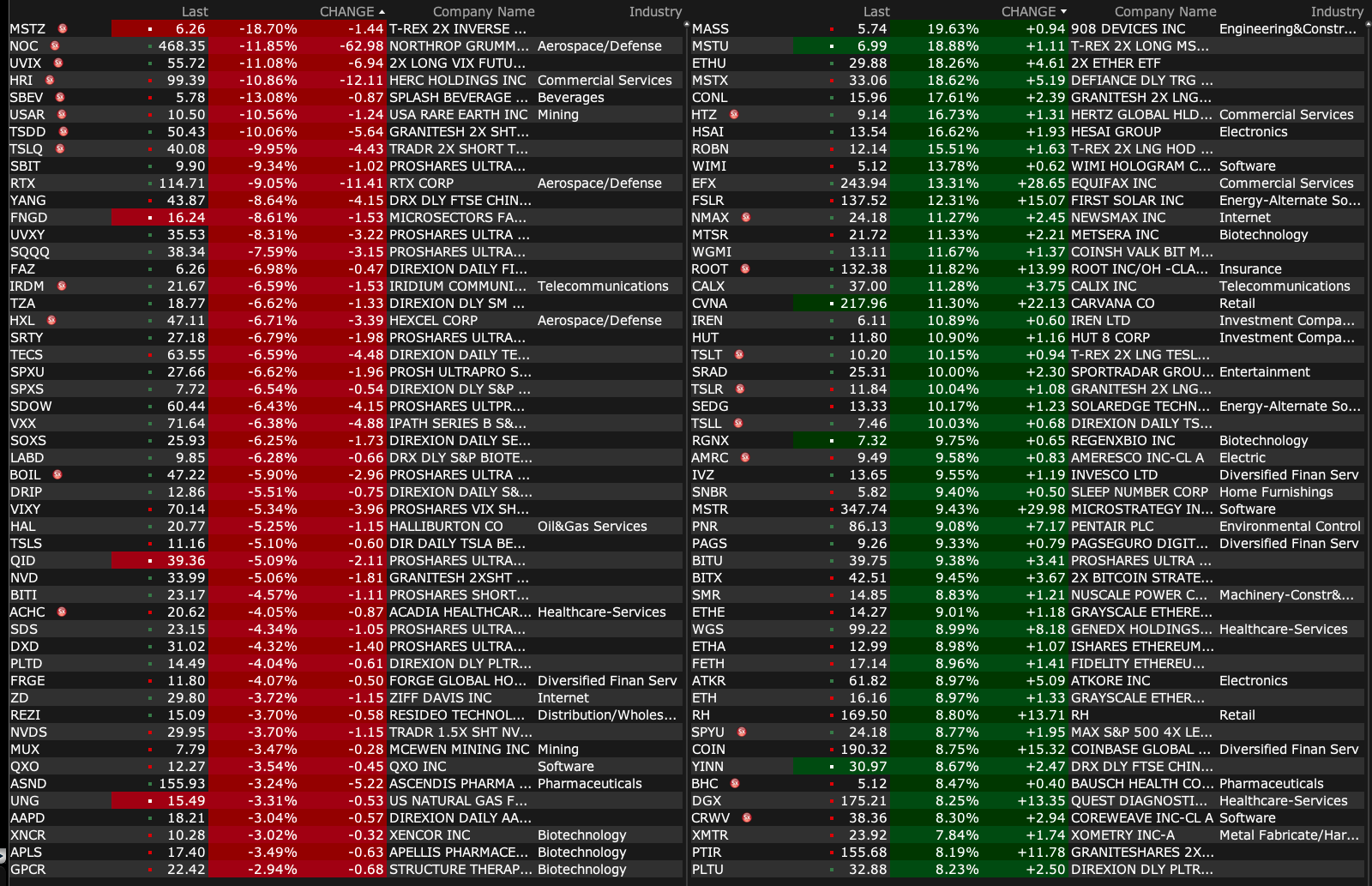

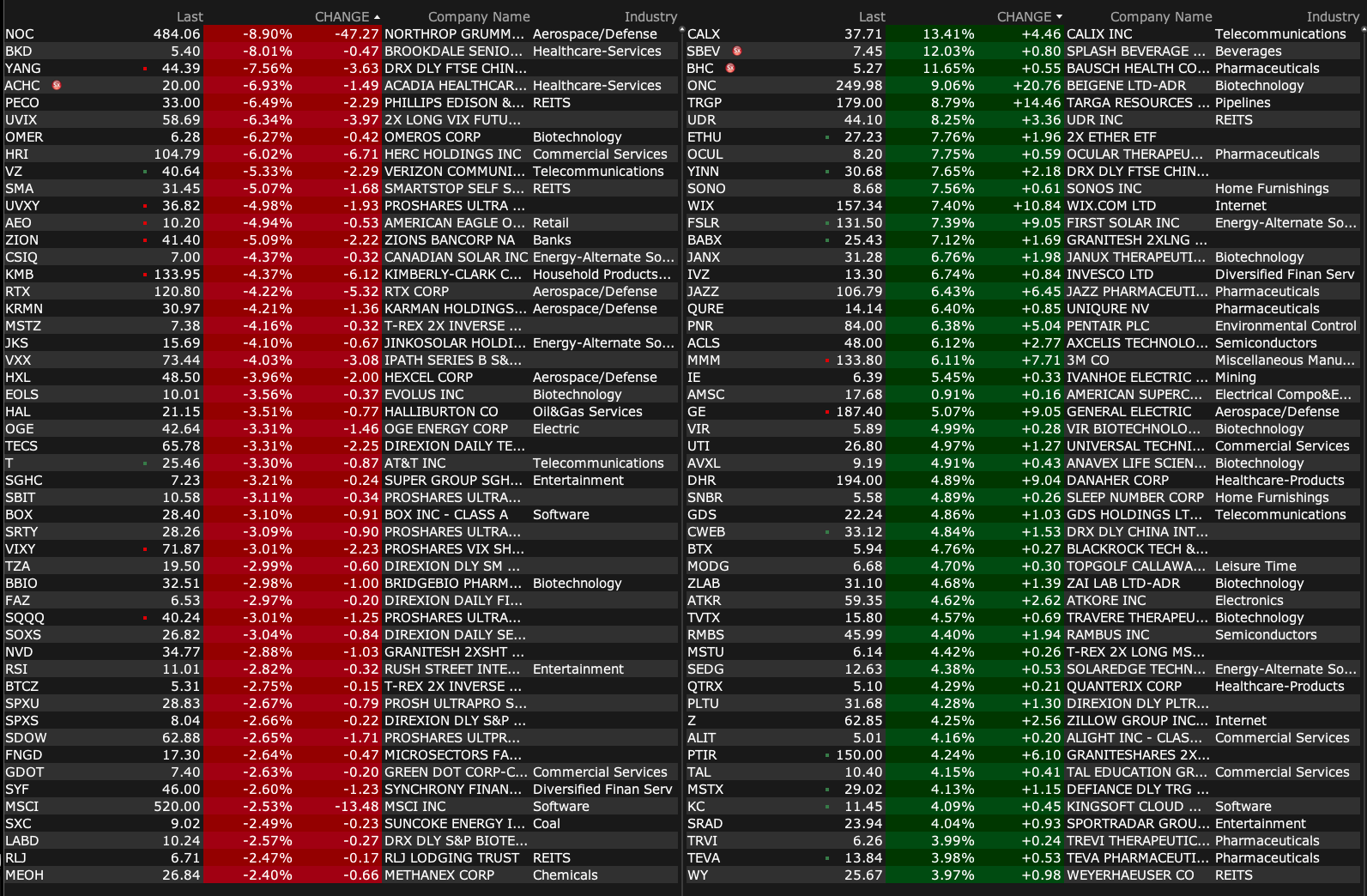

Premarket percentage movers as of 8:49 a.m. ET:

BY Doug Kass · Apr 22, 2025, 9:07 AM EDT

9 a.m.: Fed Vice Chair Jefferson (Voter) speaks on "Economic Mobility and the Dual Mandate" before the Economic Mobility Summit sponsored by the Federal Reserve Bank of Philadelphia (Text available. No Q&A);

9:30 a.m.: Fed Bank of Philadelphia President Harker (Non-Voter) participates in fireside chat on how economic mobility impacts regional economies and can promote local growth before the Economic Mobility Summit sponsored by the Federal Reserve Bank of Philadelphia (No text. No Q&A);

1:40 p.m.: Fed Bank of Minneapolis President Kashkari (Non-Voter) participates in a moderated question-and-answer session before the U.S. Chamber of Commerce Global Summit, in Washington (Audience Q&A expected. No text. No media Q&A. Livestream at minneapolisfed.org);

2:30 p.m.: Fed Bank of Richmond President Barkin (Non-Voter) participates in fireside chat, "Macro and Micro Economic Forces Shaping our Future" before the RVA Big Dipper Innovation Summit, Richmond, VA (No text. No livestream. No media Q&A);

6 p.m. : Fed Board Governor Kugler (Voter) speaks on "Transmission of Monetary Policy" before the University of Minnesota HellerHurwicz Economics Institute (HHEI) Spring 2025 Roundtable, Minneapolis, MN (Text available. Q&A from moderator and audience)

BY Doug Kass · Apr 22, 2025, 8:45 AM EDT

BY Doug Kass · Apr 22, 2025, 8:37 AM EDT

BY Doug Kass · Apr 22, 2025, 8:25 AM EDT

BY Doug Kass · Apr 22, 2025, 8:15 AM EDT

BY Doug Kass · Apr 22, 2025, 8:05 AM EDT

douglas cassel

From an article in the New Yorker about the Chinese side of the trade war.

I do believe this is a moment of reckoning. The relationship between exports and the domestic markets is that the export market, especially in developed countries, is a substitute for domestic consumption. Basically, it’s foreign consumption. When you don’t have a very high level of domestic consumption, but you have a very powerful production capacity, foreign consumption comes to the rescue. Now, we know for sure that foreign consumption is not going to be at the same level as before, to say the least. Even if you resolve the trade war with the Trump Administration, I don’t think it can go back to the previous low level of tariffs. So, essentially, that option of foreign consumption is becoming less viable. It forces the leadership, on economic grounds, to really look at the domestic-market potential and then hopefully focus their attention on that.

But here’s the problem: to really increase the domestic-market potential would require them to give up some of their power, rather than increase it. Their current model is compatible with the power of the government: industrial policy, industrial parks, urban planning, massive infrastructure building—all of these require the power of the government. But domestic-market consumption requires something different, which is social protection and social welfare. But it also requires them to give up some of their power. So that’s the dilemma they are facing. And I believe that the Trump trade war is forcing that issue on them in a way that was not there before. (Sources: newyorker.com, mitsloan.mit.edu)

BY Doug Kass · Apr 22, 2025, 7:55 AM EDT

BY Doug Kass · Apr 22, 2025, 7:45 AM EDT

PulteGroup PHM repurchased $300 million of its own shares at about $108/share in the first quarter. (Last sale $93)

Presentation: PulteGroup, Inc. - PulteGroup, Inc. Reports First Quarter 2025 Financial Results

More on Pulte after the company's conference call.

BY Doug Kass · Apr 22, 2025, 7:35 AM EDT

I wouldn't want to be a non-U.S. investor in U.S. equities or debt these days:

BY Doug Kass · Apr 22, 2025, 7:25 AM EDT

I am back buying TLT at $86.30.

BY Doug Kass · Apr 22, 2025, 7:15 AM EDT

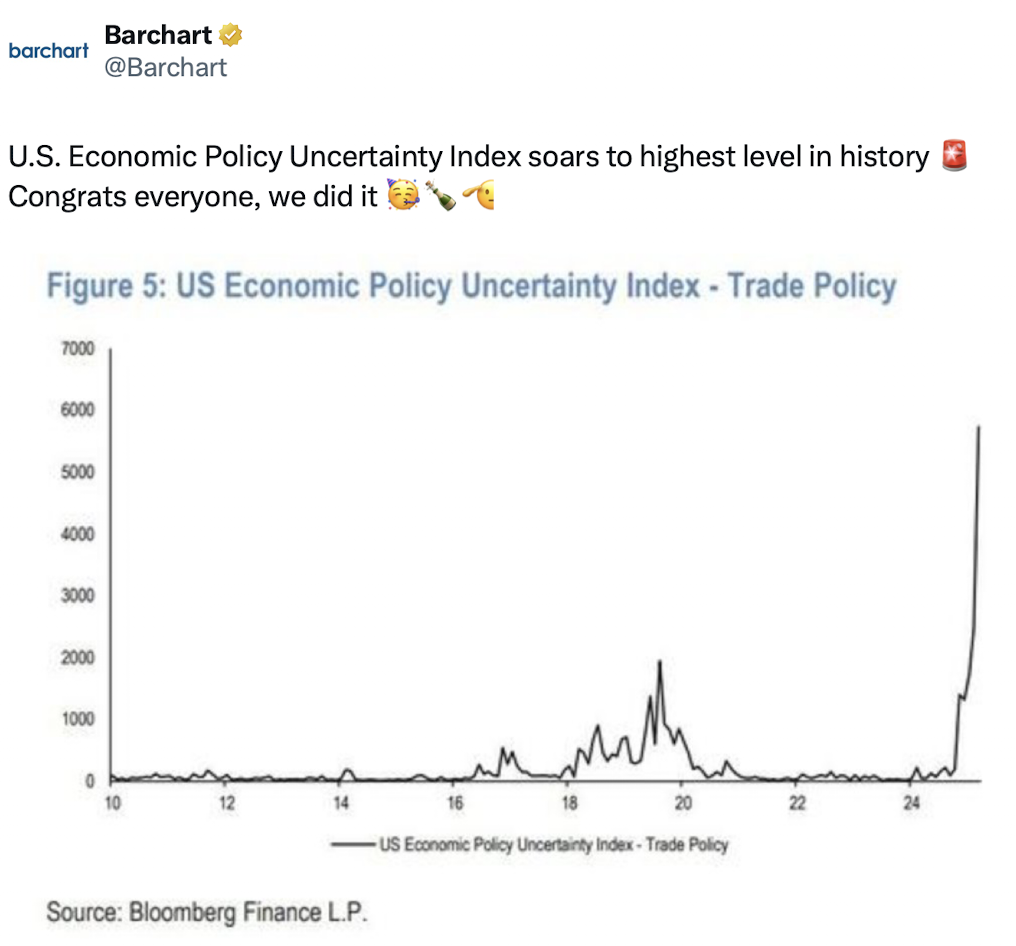

You know some money managers are desperate when they are on pins and needles and feel a need to tweet out apparent or progess on trade deals:

BY Doug Kass · Apr 22, 2025, 7:05 AM EDT

BY Doug Kass · Apr 22, 2025, 6:50 AM EDT

* From Peter Lynch

BY Doug Kass · Apr 22, 2025, 6:40 AM EDT

BY Doug Kass · Apr 22, 2025, 6:20 AM EDT

The S&P Short Range Oscillator stands at -2.56% vs. -2.43%.

Given the S&Ps methodology of using moving averages, the number will get more oversold tomorrow!

BY Doug Kass · Apr 22, 2025, 6:10 AM EDT

S&P futures are +53 handles. I am taking off my trading long rentals in the indices put on yesterday afternoon (I made over +$1 on the QQQ trade and twenty cents on the SPY trade (whopee!):

Sales:

* SPY $519.29

* QQQ $437.98

I still have my straddles and strangles on.

BY Doug Kass · Apr 22, 2025, 5:55 AM EDT